doing business in kentucky - lex mundi

TRANSCRIPT

www.lexmundi.com

KentuckyPrepared by Lex Mundi member firm, Wyatt, Tarrant & Combs, LLP

Guide to Doing Business

Lex Mundi is the world’s leading network of independent law firms with in-depth experience in 100+ countries. Through close collaboration, our member firms are able to offer their clients preferred access to more than 21,000 lawyers worldwide – a global resource of unmatched breadth and depth.

Lex Mundi – the law firms that know your markets.

This guide is part of the Lex Mundi Guides to Doing Business series which provides general information about legal and business infrastructures in jurisdictions around the world. View the complete series at: www.lexmundi.com/GuidestoDoingBusiness.

2 0 1 3 D O I N G B U S I N E S S I N K E N T U C K Y

A N I N T R O D U C T O R Y G U I D E

W YAT T TA R R A N T & C O M B S L L P

©2013 WYATT TARRANT & COMBS LLP

Wyatt, Tarrant & Combs, LLP is a regional law

firm that is both venerable and progressive.

From our six offices in Kentucky, Tennessee,

Indiana, and Mississippi with approximately 200

lawyers, we serve several thousand clients, large

and small, who reflect a wide array of business

pursuits. Our professionals offer broad experi-

ence in sophisticated litigation and transactional

matters appropriate to our clients’ needs.

FOREWORD

This Guide addresses many of the questions that concern

decision makers and advisors who are evaluating

Kentucky as a business location or who are involved in

a dispute or planning a transaction here. It does not deal

with federal laws or the laws of other states. We assume

that most readers will have some knowledge of the

subject areas and are primarily interested in how Kentucky

law may be similar to, or different from, laws elsewhere.

Finally, we assume that a general reference such as this

serves best as an introduction, not an encyclopedia.

CAUTIONARY STATEMENT

Please do not consider this Guide to constitute, or to be

a substitute for, specific legal advice. We do not intend it

to create, nor does it create, any sort of attorney-client

relationship with the reader. Because these articles are

general, they may not apply to particular legal or factual

circumstances. You should not take (or refrain from taking)

any action based on the information in this Guide without

first obtaining professional advice for your particular

situation. Also, you should not send us confidential infor-

mation without first contacting one of our attorneys and

receiving an explicit authorization to do so.

We invite you to visit our website for detailed informa-

tion about our history, practice, lawyers, capabilities,

and resources.

www.wyattfirm.com

LOUISVILLE.KY 500 West Jefferson StreetSuite 2800 Louisville, KY 40202502.589.5235

LEXINGTON.KY 250 West Main StreetSuite 1600 Lexington, KY 40507859.233.2012 NEW ALBANY.IN 120 West Spring StreetSuite 300New Albany, IN 47150812.945.3561

NASHVILLE.TN 2525 West End AvenueSuite 1500 Nashville, TN 37203615.244.0020 MEMPHIS.TN 1715 Aaron Brenner DriveSuite 800 Memphis, TN 38120901.537.1000

JACKSON.MS4450 Old Canton RoadSuite 210 Jackson, MS 39211 601.987.5300

THIS IS AN ADVERTISEMENT

CONTENTS

About Kentucky .................................................................................................................................... 1

An introduction to Kentucky and a link to current comprehensive information

Civil Dispute Resolution ....................................................................................................................... 3

by Rania M. Basha

An introduction to Kentucky law and practice across the spectrum of resolution alternatives -- informal settlement, mediation, arbitration, and trials and appeals in the state and federal court systems

Business and Personal Taxes .............................................................................................................. 15

by James A. Nitsche

A description of Kentucky income taxation of business and individuals, property taxes, sales and use taxes, local occupational license and utility taxes, inheritance taxes, and some other taxes

Tax Incentives for Business Location and Expansion ....................................................................... 30

by Stephen D. Berger

A summary of the Kentucky Business Investment Program, the comprehensive economic development tax credit incentive program for business location and expansion in Kentucky, and guide to property tax abatement in Kentucky via industrial revenue bond financing

Business Organizations ...................................................................................................................... 42

by Peter G. Diakov and Mark J. Farmer

Summaries of the law concerning the formation and operation of corporations (for profit, nonprofit, professional service, and cooperatives), partnerships (general, limited, and limited liability limited), limited liability companies, sole proprietorships, business trusts, and joint ventures

Labor and Employment ..................................................................................................................... 69

by Leila G. O’Carra

Key principles of Kentucky law affecting employment relationships, from the employment-at-will doctrine to whistle-blower protection for public employees

Intellectual Property ........................................................................................................................... 76

by William H. Hollander

A brief review of Kentucky’s statutory and common law regarding various aspects of intellectual property protection, including trade secrets, trademarks, employee confidentiality, noncompetition agreements, rights of publicity, and franchises and business opportunities

Antitrust and Trade Regulation ......................................................................................................... 79

by Michelle D. Wyrick

A survey of Kentucky’s analogs to the federal Sherman Act and Federal Trade Commission Act, numerous statutes regulating particular industries and practices, and statutes and case law regarding price discrimination

Products Liability ............................................................................................................................... 88

by Ben T. Keller

An introduction to the judicial precedents and statutes that define the environment for resolving claims of liability against manufacturers and others in the production and distribution channels for goods

Environmental Protection .................................................................................................................. 96

by George L. Seay, Jr., Lesly A.R. Davis and H. Carl Horneman

A review of Kentucky’s statutory and administrative framework for protecting air and water quality, handling and disposing of solid and hazardous wastes, cleaning up Superfund sites, and mining and reclamation

Real Property .................................................................................................................................... 107

by James T. Hodge and Jonathon Melton

A survey of Kentucky law governing estates in land, conveying, mortgaging, and leasing property, easements, mechanics liens, eminent domain, and other topics

Unauthorized Transaction of Business ............................................................................................. 128

by Francis J. Mellen, Jr. and Aaron D. Zibart

Guidance to business entities organized in other states and abroad on how to comply with Kentucky’s laws requiring authority to conduct business here and the consequences of non-compliance

Unauthorized Practice of Law .......................................................................................................... 138

by Francis J. Mellen, Jr. and Aaron D. Zibart

Guidance to attorneys not licensed in Kentucky on what constitutes the practice of law here and how to satisfy applicable Supreme Court rules

ABOUT KENTUCKY

1

The name “Kentucky” is of Native American

origin and has received various translations,

among which we favor "the land of tomorrow."

Home to more than 4,300,000 people, Kentucky

is located in the central United States, within

600 miles of two-thirds of the U.S. population,

personal income, and manufacturing. This

advantage is enhanced by a moderate climate,

low cost of living, affordable housing, abundant

educational, cultural and recreational

opportunities, and friendly people. These

factors contribute to a uniquely appealing

quality of life and have made the state

increasingly attractive to business decision

makers.

Among our unique attractions are the rich

tradition of Bluegrass music and the romance

and excitement of the horse breeding and racing

industry -- epitomized by the annual running of

the Kentucky Derby on the first Saturday in

May.

In the last half century, Kentucky’s economy has

evolved from its primary dependence on

agriculture and natural resource development to

include a broad spectrum of manufacturing and

service industries. Among the most prominent

U.S. public companies that have their

headquarters here are Humana, Churchill

Downs, YUM! Brands, Brown-Forman,

Lexmark, Papa John’s, and Fruit of the Loom;

many other well-known U.S. companies have

major operations here, including UPS, Ford,

Fidelity Investments, GE, and Citicorp. In

addition, global companies like Toyota, Nestlé,

Hitachi, Mitsubishi, Itochu, and Sumitomo have

made sizeable investments in Kentucky.

Information Resources

The Kentucky Cabinet for Economic

Development (“KCED”) is an excellent

resource for existing and prospective Kentucky

businesses. Among other services, it maintains

a website with a wealth of reliable data on many

pertinent topics, including Kentucky’s

geography, climate, population, economy,

educational resources, government, and

numerous other topics. The website may be

accessed through this link:

http://www.thinkkentucky.com

Among other resources, this site contains the

Kentucky Business & Industry Information

System (“KBIIS”), a highly detailed, searchable

data base about Kentucky businesses and the

opportunities here.

The following are among the KCED’s recent

points of emphasis in presenting the

opportunities Kentucky offers:

2

Kentucky has one of the lowest overall

costs of doing business.

Kentucky workers continually outperform

the national average for productivity.

Kentucky's workforce training programs

are in the very top tier of state programs

in facilitating customized business and

industry training services for new,

expanding, and existing companies.

Kentucky has one of the lowest industrial

electric power costs in the nation.

Complementing its strategic location,

Kentucky's inter-modal freight and

passenger transportation systems provide

efficient and cost-effective access to all

points on the globe, including worldwide

hubs for UPS and DHL.

As detailed elsewhere in this Guide,

Kentucky offers an array of state

incentives including tax credits, loan

financing, training grants, and

opportunities for foreign trade zone

operations.

CIVIL DISPUTE RESOLUTION

3

Rania M. Basha Louisville, Kentucky www.wyattfirm.com

While the avenues for resolving civil disputes

are generally the same in Kentucky as they are

in other states, the available options may involve

turns and bumps particularly applicable here. In

Kentucky, as elsewhere, parties can attempt to

resolve their differences informally through set-

tlement discussions or by agreement through

mediation or arbitration. When these efforts are

unsuccessful, the state and federal court systems

are available if the parties can satisfy certain

jurisdictional and procedural requirements. If

the dispute is one involving a governmental enti-

ty, specific Kentucky statutes and/or regulations

will govern the proceeding. This section high-

lights aspects of civil dispute resolution in Ken-

tucky.

INFORMAL SETTLEMENT DISCUSSIONS

In Kentucky, the parties retain the same flexibil-

ity they enjoy in other states when trying to re-

solve a disagreement short of commencing for-

mal litigation or incurring the expense of media-

tors or arbitrators. The primary consideration,

when attorneys become involved in settlement

discussions on behalf of Kentucky residents or

businesses, lies in any differences in the ethical

rules applicable to the practice of law in Ken-

tucky versus the rules applicable in other states.

Kentucky Supreme Court Rule (“SCR”)

3.130(4.1(a)) provides that “[i]n the course of

representing a client a lawyer[] shall not know-

ingly make a false statement of material fact or

law to a third person[.]” Comment (1) to SCR

4.1 clarifies that a lawyer has no duty to inform

an opposing party of relevant facts, but “[a] mis-

representation can occur if the lawyer incorpo-

rates or affirms a statement of another person

that the lawyer knows is false.” Comment (2)

also recognizes that whether a statement is one

of fact depends on the circumstances: “Under

generally accepted conventions in negotiation,

certain types of statements ordinarily are not

taken as statements of material fact. Estimates

of price or value placed on the subject of a

transaction and a party’s intentions as to an ac-

ceptable settlement of a claim are ordinarily in

this category, and so is the existence of an un-

disclosed principal except where nondisclosure

of the principal would constitute fraud.”

Under Kentucky Rule of Evidence (“KRE”)

408, offering or accepting a compromise of a

disputed claim is not admissible to prove either

liability for, or invalidity of, the claim. Like-

wise, KRE 408 excludes evidence of conduct or

statements made during negotiations that are not

otherwise discoverable. But it does not require

exclusion when the evidence is offered for an-

other purpose, such as bias or prejudice of a wit-

ness.

4

MEDIATION

As elsewhere in the United States, mediation is a

popular choice in Kentucky for resolving dis-

putes.

Pre-litigation Mediation

A number of organizations here provide media-

tion services, either before or after litigation be-

gins. Many of these provide retired judges who

are able to give clients a meaningful idea of

what may result from a trial or an appeal from a

jury verdict. Other mediators are experienced

practitioners in specific areas of the law, such as

medical malpractice, workers’ compensation,

securities law, employment law, or construction

litigation.

A mediator in Kentucky typically charges by the

hour. A party can expect to pay between $200

and $350 an hour. A qualified mediator in Ken-

tucky will always require the parties to sign a

confidentiality agreement. All nondiscoverable

statements and offers made or rejected during

mediation must be kept confidential. See KRE

408. Before retaining the services of any media-

tor, a party should obtain recommendations as to

who would be the most appropriate choice given

the facts and legal issues in a particular case.

Experienced civil litigators in Kentucky will

know who among available mediators would be

the most effective in a specific case and, absent

a conflict of interest, will assist out-of-state at-

torneys in identifying the best alternatives.

Mediation in State Court Cases

Kentucky lower courts can, and often do, order

mediation. Some circuits have adopted local

rules that specifically provide for alternative

dispute resolution. For example, the Rules of

Practice of the Jefferson Circuit Court (“JRP”)

in Louisville allow the Court to refer a case to

mediation or another alternative dispute resolu-

tion method as agreed by the parties, “[a]t any

time on its own motion or on motion of any par-

ty[.]” JRP 1303. If the parties cannot agree up-

on a mediator, the Court will appoint one. The

judge presiding over a case will not serve as a

mediator unless the parties agree. If the parties

consent, the mediator can advise the Court of

“those matters which, if resolved or completed,

would facilitate the possibility of a settlement.”

JRP 1310. Kentucky state courts favor media-

tion and view it as an effective way to resolve

cases short of trial.

Once a case reaches the Kentucky Court of Ap-

peals, mediation may become part of the formal

proceedings. Under Kentucky Civil Rule of

Procedure (“CR”) 76.03(4), twenty days after a

notice of appeal is filed, the appellant must file a

prehearing statement, which addresses a number

of questions, including whether the appellants

want a “prehearing conference,” the primary

purpose of which is to try to settle the case. The

appellee also has the opportunity to file a pre-

hearing statement within ten days thereafter to

respond to the same questions, including wheth-

5

er the appellee wants a prehearing conference.

Even if all parties to the appeal check “no” to

whether a prehearing conference is desired, the

Court of Appeals may order a prehearing con-

ference, which is conducted by one of the

Court’s two staff attorneys, who are responsible

for holding prehearing conferences and serving

as mediators to settle cases on appeal.

Like informal mediation, the prehearing confer-

ence is confidential when it involves settlement

discussions. The staff attorneys are effective

mediators when the parties are amenable to set-

tlement discussions, particularly if the appeal is

one from a jury verdict. Clients are required

either to be present at the prehearing conference

or to be available throughout the conference by

telephone. If the client is not able to be present,

counsel should advise the conference attorney

that the client will be available by telephone.

Counsel should demonstrate courtesy and coop-

eration before the conference attorney. Out-of-

state counsel representing a client must be ac-

companied by an attorney with a valid Kentucky

license at any proceeding before the Court of

Appeals, including the prehearing conference.

See SCR 3.030(2).

Mediation in Federal Court Cases

The Joint Local Rules of Civil Practice for the

United States District Courts in Kentucky

(“LR”) expressly provide, in LR 16.2, for Alter-

native Dispute Resolution:

Upon motion of any party, or sua sponte, any judicial officer may require parties in civil cas-es to consider some form of al-ternative dispute resolution pro-cess, including but not limited to, mediation, early neutral evaluation, minitrial, or arbitra-tion. Mediation may be con-ducted under the auspices of a private professional mediator or judicial officer.

The process, as always, is confidential, and typi-

cally is conducted by one of the United States

magistrate judges. The process is somewhat

informal, usually occurring in the chambers of a

magistrate. The federal magistrates in Kentucky

enjoy a successful settlement record.

In the United States Court of Appeals for the

Sixth Circuit, to which Kentucky is assigned, the

mediation process is similar to what occurs at a

prehearing conference before the Kentucky

Court of Appeals staff attorney. The Sixth Cir-

cuit requires a conference, which is usually con-

ducted by telephone in Kentucky. The staff at-

torney assigned to the appeal will discuss the

issues with the lawyers and make an effort to

resolve the case. As in the Kentucky Court of

Appeals, the process has an informal feel with

no pressure to settle.

ARBITRATION

Arbitration agreements are enforceable in Ken-

tucky. Under Section 250 of the Kentucky Con-

stitution, the General Assembly has the duty of

enacting laws “as shall be necessary and proper

6

to decide differences by arbitrators, the arbitra-

tors to be appointed by the parties who may

choose that summary mode of adjustment.”

Kentucky Revised Statutes (“KRS”) Chapter

417 governs state arbitration proceedings, except

within the context of disputes between employ-

ers and employees or those involving insurance

contracts. KRS 336.700 prohibits an employer

from conditioning employment on the employ-

ee’s waiver of potential future claims and requir-

ing arbitration. KRS 304.20-050 provides that

an arbitration clause in an automobile liability or

motor vehicle liability insurance policy is unen-

forceable.

Similar to the Federal Arbitration Act, 9 U.S.C.

§2, KRS 417.050 provides that an arbitration

agreement is “valid, enforceable and irrevocable,

save upon such grounds as exist at law for the

revocation of any contract.” KRS 417.060 gov-

erns proceedings to compel or stay arbitration

and requires a court to “proceed summarily” to

determine whether an arbitration agreement ex-

ists if a party denies its existence. The court

cannot deny arbitration on the basis that a claim

lacks merit.

The parties’ agreed upon method of appointing

arbitrators controls, but if they do not agree, the

court has the power to appoint arbitrators under

KRS 417.070. The parties’ agreement also con-

trols the conduct of the hearing. Thus, if the

parties agree to arbitrate under FINRA or AAA

rules, that agreement will control.

If the parties’ agreement is silent, KRS 417.090

governs the hearing and dictates, for example,

that the parties are entitled “to be heard, to pre-

sent evidence material to the controversy and to

cross-examine witnesses[.]” KRS 417.110 gives

the arbitrators the power to issue subpoenas “for

the attendance of witnesses and for the produc-

tion of books, records, documents, and other

evidence[.]” Depositions may also be taken if a

witness is unable to attend the hearing.

A party may move the court to vacate an adverse

arbitration award within ninety days of receiving

it. Like 9 U.S.C. §10, KRS 417.160 provides

narrow grounds for vacating an arbitration

award. The court can vacate the award if (i) it

was procured by corruption, fraud or other un-

due means, (ii) there was evident partiality, cor-

ruption or misconduct by an arbitrator, which

prejudiced the party’s rights, and (iii) the arbitra-

tors exceeded their powers or conducted the

hearing contrary to KRS 417.090 to the party’s

prejudice. Like the federal act, KRS 417.160

does not allow the court to vacate an award

simply because the arbitrators were wrong.

KRS 417.220 allows a party to appeal an order

denying an application to compel arbitration, an

order staying arbitration, an order confirming or

denying an award, an order modifying or cor-

recting an award, and an order vacating an

7

award without directing a rehearing. An appeal

from any of these orders is subject to the same

rules governing appeals from judgments in any

civil case.

Because the grounds for vacating an arbitration

award are narrow under Kentucky law, arbitra-

tion may not represent the most desirable option

for resolving a dispute. Whether it is the best

option depends on the nature of the controversy.

If the potential issues in a business transaction

are likely to be more legal than factual, for ex-

ample, judicial proceedings may be more prefer-

able than arbitration in Kentucky. A business

should consider the procedural restrictions on

arbitration before entering into an arbitration

agreement that would be subject to Kentucky

law.

STATE COURT LITIGATION

One feature of Kentucky courts sets them apart

from some other state court systems. Judges in

Kentucky are elected. At every level of the

Kentucky judicial system, the judges run for

election as nonpartisan candidates for specific

terms of office.

District Courts

Kentucky’s lowest courts are the District Courts.

District Court judges are elected on a non-

partisan basis for terms of four years. Some dis-

tricts encompass multiple counties, while other

districts are composed of only one. A densely

populated district with a concomitant heavy

caseload may consist of one county and have

several district court judges. In more rural areas,

a district may have more than one county and

one judge who travels between counties to hear

cases.

The District Courts have limited jurisdiction,

restricted to juvenile matters, city and county

ordinance enforcement, misdemeanors, traffic

offenses, probate of wills, felony preliminary

hearings, and civil cases where the amount in

controversy is $5,000 or less. Guardianship,

conservatorship, voluntary and involuntary med-

ical commitments, and domestic violence and

abuse cases are also heard in District Court.

Circuit Courts

Significant civil disputes are likely to commence

in Circuit Courts, which are the primary courts

of general jurisdiction and hear civil matters

when more than $5,000 is at stake. There are 57

judicial circuits in Kentucky. And, like Ken-

tucky’s other state courts, judges are elected on a

non-partisan basis for eight-year terms. Circuit

Courts have jurisdiction over capital offenses

and felonies, divorces, adoptions, terminations

of parental rights, land disputes, property title

issues and contested probates of wills. Circuit

Court judges have the power to issue injunc-

tions, writs of prohibition and writs of manda-

mus. They also hear appeals from the District

Courts and administrative agencies.

8

The Kentucky Rules of Civil Procedure govern

the practice of civil cases in Kentucky state

court. While the Civil Rules generally track the

Federal Rules of Civil Procedure, there can be

significant differences in interpretation, as the

discussion of CR 56 below explains, and in the

specific requirements of the rules, such as those

applicable to appeals in state court.

Many Circuit Courts also have adopted their

own local rules applicable to civil cases, and of

them have established “motion hours,” namely

regularly occurring dates for hearing discovery

and other routine motions in civil cases. Coun-

sel for the parties must determine whether local

rules exist and, if so, become familiar with them

before a case is filed if representing the plaintiff,

or promptly thereafter if representing the de-

fendant. Even if there are no official local rules,

a Circuit Court will have its own practices re-

garding motion hour and the deadline for filing

motions to be heard at a particular motion hour.

Some Circuit Courts impose page limits on legal

memoranda and have their own special rules

regarding leave to appear pro hac vice.

Circuit Courts are bound to follow the Kentucky

Constitution, which has a number of provisions

that are particular to Kentucky. Under the Ken-

tucky Supreme Court’s current interpretation,

for instance, the Constitution limits the Legisla-

ture’s ability to diminish the civil remedies

available when the Constitution was adopted.

See Williams v. Wilson, 972 S.W.2d 260, 267-69

(Ky. 1998). This limitation, for example, pre-

vents the General Assembly from enacting stat-

utes to make the recovery of punitive damages

more difficult and from placing a ceiling on

damages recoverable in civil cases.

Circuit Courts also are bound to follow opinions

issued by the Kentucky Court of Appeals and

Kentucky Supreme Court. The latter has made

clear, for example, that Kentucky does not apply

the summary judgment standard that is applica-

ble in federal courts. Steelvest, Inc. v. Scansteel

Service Ctr., Inc., 807 S.W.2d 476, 482-83 (Ky.

1991) (refusing to follow the “more relaxed”

summary judgment standard enumerated by the

United States Supreme Court). A party can ob-

tain summary judgment in state court under CR

56, “[o]nly when it appears impossible for the

nonmoving party to produce evidence at trial

warranting a judgment in his favor should the

motion for summary judgment be granted.” Id.

at 482. This test is more difficult for a defendant

to meet than the one used in federal court.

By contrast, the Kentucky Supreme Court has

held that Kentucky trial courts will apply the

United States Supreme Court’s Daubert test for

expert witnesses. See Goodyear Tire and Rub-

ber Co. v. Thompson, 11 S.W.3d 575 (Ky.

2000). In reviewing the trial court’s ruling on

appeal, however, the appellate court will apply

an abuse of discretion standard, namely whether

9

the trial court’s decision was “arbitrary, unrea-

sonable, unfair, or unsupported by sound legal

principles.” Id. at 581. On the question of an

expert’s “reliability,” the test is “clear error,” a

standard that is even more deferential to the trial

court on appeal than abuse of discretion. See

Miller, M.D. v. Eldridge, 146 S.W.3d 909 (Ky.

2004).

The Kentucky Supreme Court also applies the

test for assessing punitive damage awards that

the Supreme Court announced in BMW of North

America, Inc. v. Gore, 517 U.S. 559, 574-75

(1996) and Cooper Industries, Inc. v. Leather-

man Tool Group, Inc., 532 U.S. 424, 121 S. Ct.

1678 (2001). While the trial court considers a

punitive award under the “first blush” rule,

which focuses on whether the amount was influ-

enced by passion or prejudice, the court on ap-

peal conducts a de novo review and will reverse

or remit an excessive punitive verdict. See Sand

Hill Energy, Inc. v. Ford Motor Co., 83 S.W.3d

483, 496 (Ky. 2002) (vacated on other grounds).

The Supreme Court has articulated a punitive

damage instruction for trial courts to use that

includes a prohibition against using out-of-state

evidence to award punitive damages for conduct

occurring outside Kentucky. Sand Hill Energy,

Inc. v. Ford Motor Co., 142 S.W.3d 153, 167

(Ky. 2004).

In addition to general jurisdiction over civil cas-

es, the Circuit Courts also have a Family Court

system, which was established as a separate di-

vision upon adoption of amendments to the Ken-

tucky Constitution in 2002. These Courts pro-

vide a dedicated forum for resolution of familial

disputes, including dissolution of marriage,

spousal support and equitable distribution, child

custody, support, and visitation, paternity, adop-

tion, domestic violence, dependency, neglect

and abuse, termination of parental rights, runa-

ways, and truancy issues.

Similarly, there is a separate Drug Court divi-

sion, which is a treatment and rehabilitation pro-

gram administered directly by the Circuit

Courts, in which most counties participate. The

program requires at least a one-year commit-

ment on the part of the offender, if eligible, in

exchange for possible avoidance of incarcera-

tion. The program involves weekly status ses-

sions in court, ongoing drug screening, and regu-

lar clinical treatment and support-group meet-

ings. The costs of administering the Drug Court

program are substantially less than the costs of

jail or prison, and the success of program partic-

ipants, after leaving treatment, is greater than

those who are sentenced in a traditional manner.

Court of Appeals

The Kentucky Court of Appeals has jurisdiction

over appeals from Circuit Court. Two judges

are elected from each of seven appellate court

districts for a total of fourteen judges, who serve

eight-year terms. The judges are divided into

10

panels of three to review and decide cases, with

the majority determining the decision.

Although based in the state capital, Frankfort,

the Court of Appeals does not sit permanently in

one location, but travels to different sites around

the state to hear cases. Cases are assigned to

panels, not based on where they are pending, but

on the availability of judges, depending on their

caseload. Therefore, a case out of Jefferson Cir-

cuit Court, for example, will not necessarily be

decided by a panel with a judge from Jefferson

County or its district.

The Kentucky Constitution gives every party the

right to one appeal. Accordingly, a case that

begins in Circuit Court can be appealed to the

Court of Appeals as a matter of right. CR 74.02

allows a party to move to transfer a civil case

directly to the Kentucky Supreme Court if the

case “is of great and immediate public im-

portance[.]” As may be expected, the Supreme

Court rarely grants such motions.

An appeal commences with the filing of a notice

of appeal in Circuit Court. In Kentucky, a notice

of appeal is jurisdictional; if the notice is un-

timely, filed more than thirty days from final

judgment, or from an order denying post-trial

motions, the Court of Appeals will dismiss the

appeal for lack of jurisdiction. The Court of

Appeals also has held that the filing fee for an

appeal, currently $160, is jurisdictional. Some

Circuit Court clerks in Kentucky impose an ad-

ditional charge, which can vary from county to

county. When appealing, counsel should be

aware of the total filing fee in the relevant Cir-

cuit Court. If the notice of appeal is filed within

the deadline, but the check for the filing fee is

late, the Court of Appeals will dismiss the ap-

peal.

The Kentucky Civil Rules set forth many specif-

ic, technical requirements for perfecting an ap-

peal. Except for the notice and the filing fee, the

requirements are not jurisdictional, but good

cause must be shown if a party fails to comply

with the Rules. As a result, counsel should pay

particular attention to the appellate rules and

consult with an attorney specializing in appellate

practice to avoid potential pitfalls for the un-

wary.

For example, parties to an appeal must request

oral argument if desired. Otherwise, the Court

of Appeals may order that no oral argument will

occur. Even if the parties request it, the Court of

Appeals has the discretion to decide the case

without oral argument. Absent circumstances

like the complexity of a case or disagreement

among the judges on its disposition, the Court of

Appeals tries to issue opinions within one month

of oral argument. Generally, the average time

for a civil appeal is eighteen months from the

notice of appeal to the issuance of an opinion.

With few exceptions, a party can only appeal

from a temporary injunction or a final judgment

11

resolving all claims or a judgment that resolves

one or more but less than all of the claims or

parties, if the court recites that the judgment is

final and appealable as to one of the parties

and/or a separable claim and there is “no just

reason for delay.” CR 54.02. While there is

scant authority holding otherwise, an order

denying a motion to dismiss or motion for sum-

mary judgment is ordinarily not appealable.

Likewise, discovery and other pretrial orders are

not appealable. An order denying or granting a

restraining order is not appealable. An order

granting or denying class certification in Ken-

tucky is not appealable.

The principal appellate avenue of relief from

these pretrial rulings are the extraordinary writs

of mandamus and prohibition, which are rarely

granted and should not be attempted if the

judgment is simply wrong. “[W]e have always

been cautious and conservative both in entertain-

ing petitions for and in granting such relief.”

Bender v. Eaton, 343 S.W.2d 799, 800 (Ky.,

1961). A writ is appropriate only when the infe-

rior court is acting without jurisdiction or acting

erroneously within its jurisdiction. If the latter,

the petitioner also must show that he or she has

no adequate remedy by appeal or otherwise and

that he or she would suffer great and irreparable

injury. Id.

Kentucky Supreme Court

As the court of last resort in Kentucky, the Su-

preme Court is the final interpreter of state law.

One Supreme Court justice is elected on a non-

partisan basis from each of the seven appellate

judicial districts. The Justices serve eight-year

terms. The Chief Justice is chosen for a four-

year term by his or her colleagues and serves as

the administrative head of the Kentucky state

court system.

The Court considers appeals in civil cases upon

motion for discretionary review or, in rare in-

stances, on motion to transfer from the Court of

Appeals. Whether the Kentucky Supreme Court

accepts a case for discretionary review lies en-

tirely within the Court’s discretion and “will be

granted only when there are special reasons for

it.” See CR 76.20. A “special reason” may ex-

ist, for example, if the case presents a legitimate

constitutional question or a significant matter of

first impression, or if it has ramifications of pub-

lic policy beyond the parties and matter at issue

in a particular case. The Supreme Court is pri-

marily responsible for the development and pro-

gress of the common law in Kentucky. It has the

power to change the common law.

The fact that the Supreme Court accepts discre-

tionary review does not, ipso facto, signify that

it will reverse the Court of Appeals. While it is

difficult to pinpoint the reversal rate with any

certainty, an examination of discretionary re-

12

view in civil cases involving only private liti-

gants indicates that the reversal rate is around

50% after review is granted.

The Supreme Court does not hear testimony or

any evidence outside the record developed at the

lower court. Counsel for the parties submit

briefs. The Court has oral arguments in the civil

cases accepted for review and usually gives each

side fifteen minutes, allowing the appellant to

divide the time and save some for rebuttal. In

civil cases, the Court issues a written opinion,

which is ordinarily for publication because the

Court decides important questions. A decision

by the Kentucky Supreme Court may only be

reviewed by the United States Supreme Court

upon writ of certiorari.

Attorneys Not Licensed in Kentucky

If an attorney is admitted to practice in another

state, but not in Kentucky, he or she must com-

ply with SCR 3.030(2) which provides:

A person admitted to practice in another state, but not in this state, shall be permitted to prac-tice a case in this state only if that attorney subjects himself or herself to the jurisdiction and rules of the Supreme Court of Kentucky, governing profes-sional conduct, pays a one time per case fee of two hundred seventy dollars ($270.00) to the Kentucky Bar Association and engages a member of the asso-ciation as co-counsel, whose presence shall be necessary at all trials and at other times when

required by the court. No mo-tion for permission to practice in any state court in this jurisdic-tion shall be granted without submission to the admitting court of a certification from the Kentucky Bar Association of receipt of this fee.

Once the attorney obtains the certification form

from the KBA, local counsel files a motion for

leave to appear pro hac vice, with the certifica-

tion attached. Thereafter, leave to appear is rou-

tinely granted. Out-of-state counsel must com-

ply with rules at each level of a proceeding,

namely at the trial court and on appeal at the

Court of Appeals and, again, at the Kentucky

Supreme Court.

FEDERAL COURT LITIGATION

Kentucky has two federal court districts, the

United States District Courts for the Western

District of Kentucky and for the Eastern District

of Kentucky. The Western District has four di-

visions: Bowling Green, Louisville, Owensboro

and Paducah. Currently, there are four active

judges and two judges on senior status. There

are four United States magistrate judges in the

Western District. The Eastern District has six

active judges, four senior judges, and five Unit-

ed States magistrate judges. It is divided into six

divisions: Ashland, Covington, Frankfort, Lex-

ington, London and Pikeville.

The Eastern and Western Districts cooperate in

promulgating local rules that provide uniformity

13

in the local federal court practice between the

Districts in Kentucky. This consistency is not

required by any federal statute and, therefore, is

especially appreciated by practitioners in the

state. As the introduction to the Joint Local

Rules states, “[i]t has long been the intent of the

federal judges in Kentucky to make the practice

of law in the federal courts as simple and under-

standable as possible for the Kentucky federal

practitioner.”

Counsel for parties to any case pending in the

Eastern or Western Districts of Kentucky must

be familiar with the Joint Local Rules. For civil

cases, the Rules contain, for example, page limi-

tations and other requirements for legal memo-

randa (LR 7.1), certain standards for discovery

disputes (LR 37.1) and bond and surety re-

quirements (LR 65.1.1).

Electronic filing is mandatory for virtually all

cases in the Eastern and Western Districts. To

file electronically, an attorney must register in

the district in which the attorney intends to file.

To register, the attorney must be admitted in that

district (pro hac vice admission is acceptable)

and the attorney must certify that the attorney

has been trained on the use of the Court’s elec-

tronic filing system. To register and learn more

about electronic filing, visit the Eastern District

website www.kyed.uscourts.gov or the Western

District website www.kywd.uscourts.gov.

Parties appeal from the Eastern and Western

Districts to the United States Court of Appeals

for the Sixth Circuit, which encompasses Ken-

tucky, Michigan, Ohio and Tennessee. The

Court sits in Cincinnati, Ohio. Currently, the

Sixth Circuit has sixteen active judges and nine

senior judges. It is not unusual for United States

District Court judges in the Sixth Circuit and

elsewhere to serve on panels. In addition to fol-

lowing the Federal Rules of Appellate Proce-

dure, the Sixth Circuit also has adopted Sixth

Circuit Rules, pursuant to FRAP 47, and internal

operating procedures. It is imperative for coun-

sel to become familiar with the local rules and

internal procedures at the outset of an appeal to

the Sixth Circuit.

ADMINISTRATIVE PROCEEDINGS

A party involved in a dispute with a Kentucky

governmental agency will need to consult the

particular statutes or regulations governing pro-

ceedings before that agency. For example, KRS

Chapter 131 governs proceedings between the

Revenue Cabinet and taxpayers and KRS

131.340 gives the Kentucky Board of Tax Ap-

peals exclusive jurisdiction over appeals from

any order of a state or county agency affecting

revenue and taxation.

In addition to any procedures and requirements

tailored to a particular agency, KRS 13B.020

applies to all administrative hearings conducted

by an agency, except those listed as exempted in

14

the statute. The process in KRS Chapter 13B

contemplates meaningful notice of a hearing and

allows interested parties to intervene. See KRS

13B.060. Under KRS 13B.090, the parties have

the right to discover the identity of witnesses in

advance of the hearing. A hearing officer pre-

sides over the hearing and must give the parties

the opportunity to file pleadings, motions, and

objections and may allow the filing of briefs and

proposed findings. KRS 13B.080 also gives the

hearing officer subpoena power and the parties

the right to present evidence and argument and

conduct cross-examination.

KRS 13B.090 provides that hearsay is admissi-

ble but cannot be sufficient in itself to support a

finding unless the hearsay would be admissible

in court over a party’s objection. Any party ag-

grieved by a final order of an agency has the

right to appeal, under KRS 13B.140, by petition-

ing to the Circuit Court in the venue provided in

the agency’s enabling statutes. The appealing

party must satisfy the requirements of KRS

13B.140 to perfect the appeal, including the thir-

ty-day deadline for an appeal.

BUSINESS AND PERSONAL TAXES

15

James A. Nitsche Louisville, Kentucky www.wyattfirm.com

INCOME TAX

Businesses

Kentucky generally follows the Internal

Revenue Code of 1986, as amended through

December 31, 2006 (the “IRC”), except when a

specific provision conflicts. For purposes of the

corporate income tax, the term “corporation” for

Kentucky tax purposes has the same meaning as

that under Section 7701(a)(3) of the IRC. KRS

141.010(24)(a). In order for Kentucky to tax a

corporation’s income, the corporation must be

“doing business in this state,” which includes:

(1) being organized under the laws of Kentucky;

(2) having a commercial domicile in Kentucky;

(3) owning or leasing property in Kentucky; (4)

having one or more individuals performing

services in Kentucky; (5) maintaining an interest

in a pass-through entity (see infra) doing

business in Kentucky; (6) deriving income from

or attributable to sources within Kentucky,

including trusts; or (7) directing activities at

Kentucky customers for the purpose of selling

them goods or services. KRS 141.010(25). This

“commercial presence” standard is a shift from

the former “physical presence” standard, but is

not intended to go beyond the limitations

imposed and protections provided by P.L. 86-

272 or the United States Constitution. Id.

Excluded from the corporate income tax are S

corporations, most banks and trust companies,

savings and loan associations, production credit

associations, insurance companies, certain

printing corporations, entities exempt under

Section 501 of the IRC, and other nonprofit

religious, charitable, and educational

corporations. KRS 141.040(1).

The corporate income tax rate is four percent

(4%) on the first $50,000; five percent (5%) on

the next $50,000; and six percent (6%) on any

income over $100,000. KRS 141.040(6).

All corporations doing business in Kentucky

must apportion their income if the entity is

required to file returns for or pay net income tax,

a franchise tax, or a corporate stock tax in

another state. KRS 141.010(14)(b). A

corporation that owns an interest in a limited

liability pass-through entity (see infra) or a

general partnership organized or formed as a

general partnership after January 1, 2006 must

include its proportionate share of the sales,

property and payroll of the limited liability pass-

through entity or general partnership in

computing its apportionment factors (as

described below). KRS 141.206(10)(b) and

141.120(11). For general partnerships organized

or formed on or before January 1, 2006, the

general partnership must apportion its income

using the standard three-factor formula and the

16

corporate partner must include its distributive

share of the apportioned partnership income

when calculating its corporation income tax.

KRS 141.206(10)(b).

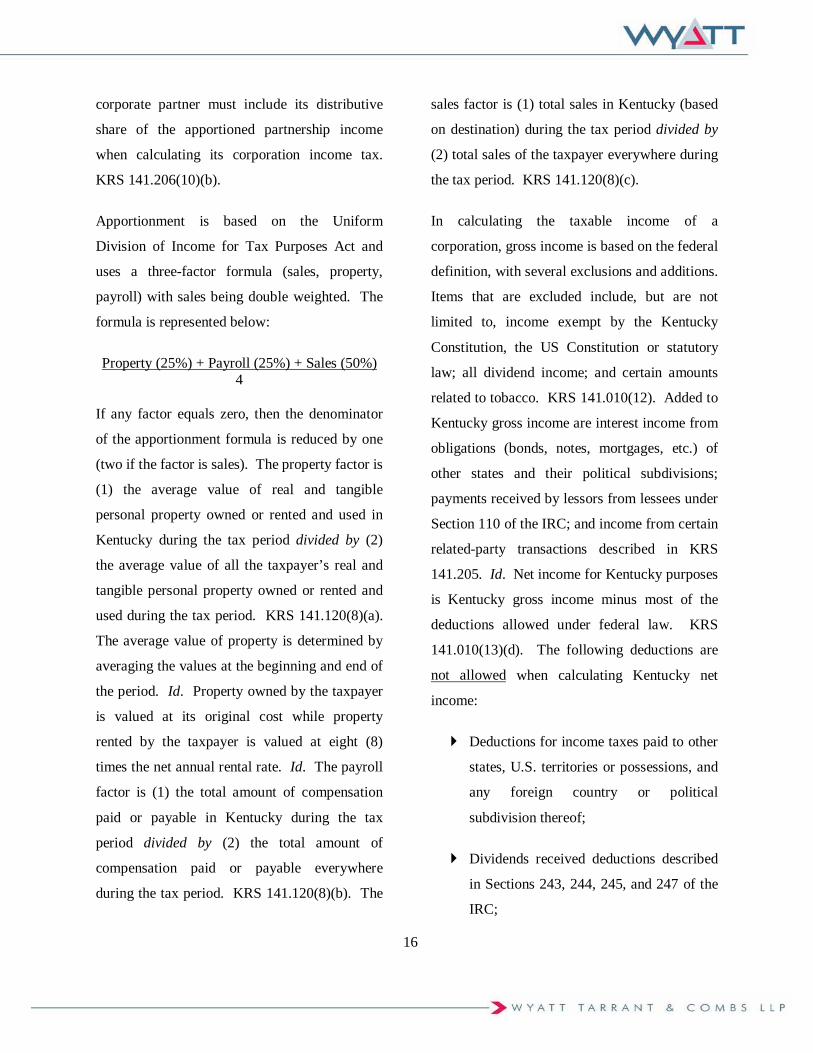

Apportionment is based on the Uniform

Division of Income for Tax Purposes Act and

uses a three-factor formula (sales, property,

payroll) with sales being double weighted. The

formula is represented below:

Property (25%) + Payroll (25%) + Sales (50%) 4

If any factor equals zero, then the denominator

of the apportionment formula is reduced by one

(two if the factor is sales). The property factor is

(1) the average value of real and tangible

personal property owned or rented and used in

Kentucky during the tax period divided by (2)

the average value of all the taxpayer’s real and

tangible personal property owned or rented and

used during the tax period. KRS 141.120(8)(a).

The average value of property is determined by

averaging the values at the beginning and end of

the period. Id. Property owned by the taxpayer

is valued at its original cost while property

rented by the taxpayer is valued at eight (8)

times the net annual rental rate. Id. The payroll

factor is (1) the total amount of compensation

paid or payable in Kentucky during the tax

period divided by (2) the total amount of

compensation paid or payable everywhere

during the tax period. KRS 141.120(8)(b). The

sales factor is (1) total sales in Kentucky (based

on destination) during the tax period divided by

(2) total sales of the taxpayer everywhere during

the tax period. KRS 141.120(8)(c).

In calculating the taxable income of a

corporation, gross income is based on the federal

definition, with several exclusions and additions.

Items that are excluded include, but are not

limited to, income exempt by the Kentucky

Constitution, the US Constitution or statutory

law; all dividend income; and certain amounts

related to tobacco. KRS 141.010(12). Added to

Kentucky gross income are interest income from

obligations (bonds, notes, mortgages, etc.) of

other states and their political subdivisions;

payments received by lessors from lessees under

Section 110 of the IRC; and income from certain

related-party transactions described in KRS

141.205. Id. Net income for Kentucky purposes

is Kentucky gross income minus most of the

deductions allowed under federal law. KRS

141.010(13)(d). The following deductions are

not allowed when calculating Kentucky net

income:

Deductions for income taxes paid to other

states, U.S. territories or possessions, and

any foreign country or political

subdivision thereof;

Dividends received deductions described

in Sections 243, 244, 245, and 247 of the

IRC;

17

Any deduction directly or indirectly

allocable to income that is either exempt

from taxation or otherwise not taxed by

Kentucky (and no item can be deducted

more than once); and

Any deduction for amounts paid to any

club, organization or establishment that

has been determined by a court or

government agency to discriminate in its

membership, services, facilities, or

privileges with regard to race, color,

religion, national origin, or sex (with an

allowance for amounts paid to charitable

organizations that limit membership to

persons of the same religion to promote

the religious principles for which it was

established).

KRS 141.010(13)(d).

In addition to the above, Kentucky does not

allow the bonus depreciation enacted by the Job

Creation and Worker Assistance Act of 2002,

the Jobs and Growth Tax Relief Reconciliation

Act of 2003, and the Gulf Opportunity Zone Act

of 2005. KRS 141.010(3). Furthermore,

Kentucky does not allow net operating losses

(“NOLs”) to be carried back. KRS 141.011(2).

NOLs can be carried forward for up to twenty

years. KRS 141.011(1). In addition, income tax

credits are available for a range of activities

including, but not limited to, new and expanded

manufacturing operations in certain areas,

revitalizing certain industrial areas, certain

recycling operations, rehabilitation of certain

historic structures, and certain coal or biodiesel

operations. See generally KRS 141.0205.

In general, any corporation doing business in

Kentucky must file a separate corporation

income tax return. Entities that have nexus with

Kentucky that are not permitted to file a separate

return include (1) an includible corporation in an

affiliated group, (2) a common parent

corporation, (3) a qualified Subchapter S

subsidiary included in its parent’s return, (4) a

qualified REIT subsidiary included in its

parent’s return, and (5) a disregarded entity

(including a single-member LLC) that is

included in its parent’s (i.e., single owner)

return. KRS 141.200(10).

Consolidated return standards adopted in 2005

apply to affiliated groups on or after January 1,

2005. Such groups are required to file nexus

consolidated returns. See KRS 141.200(1), (8).

For these periods, an “affiliated group” is the

same as the federal definition under Section

1504(a) of the IRC. KRS 141.200(2)(a).

“Affiliated group” includes one or more chains

of includible corporations connected through

stock ownership with a common parent

corporation that is an includible corporation, if:

(1) the common parent directly owns at least

80% of the vote and value of at least one other

includible corporation, and (2) at least 80% of

18

the vote and value of each of the other includible

corporations is directly owned by one or more of

the other corporations in the affiliated group.

KRS 141.200(9)(b). “Includible corporation”

means any corporation doing business in

Kentucky (hence, they have “nexus”) except (1)

corporations exempt from the corporate income

tax under KRS 141.040(1)(a) to (i), (2) foreign

corporations, (3) REITs and RICs, (4) domestic

international sales companies, (5) corporations

with a net operating loss and de minimus

Kentucky apportionment factors, (6)

corporations with no Kentucky apportionment

factors, and (7) S corporations. KRS

141.200(9)(e).

An affiliated group that meets the above

requirements must file a consolidated return for

Kentucky regardless of whether or not they file a

federal consolidated return. KRS

141.200(11)(a). As a result, all transactions

between members of the affiliated group must be

eliminated when determining net income, gross

receipts, and the three Kentucky apportionment

factors. KRS 141.200(11)(b). However, prior to

this step, the net operating losses of the group

must be limited in the following manner:

members are separated into two groups:

members with losses and members with

income;

the aggregate losses of the loss members

cannot be used to offset more than 50% of

the aggregate income of the income

members; and

any remaining losses may be carried

forward in accordance with KRS 141.011.

KRS 141.200(11)(b).

While pass-through entities are exempt from the

corporate income tax, their owners pay income

tax on their distributive share of earnings of the

entity. KRS 141.206(4). Corporate owners of a

pass-through entity doing business in Kentucky

are taxable on their distributive share of the

entity’s income. KRS 141.206(10). If the

corporate owner’s only business activity in

Kentucky is being an owner of a pass-through

entity, then the corporate owner is subject to the

corporate income tax on its distributive share

determined by using the above mentioned

apportionment formula. KRS 141.206(10).

A Limited Liability Entity Tax (“LLET”)

applies for tax years beginning on or after

January 1, 2007. Under KRS 141.010(26), a

“pass-through entity” (or “PTE”) includes any

partnership, S corporation, limited liability

company, limited liability partnership, limited

partnership, or similar entity recognized by the

laws of Kentucky that is not taxed for federal

purposes at the entity level, but instead passes to

each partner, member, shareholder, or owner

their proportionate share of income, deductions,

19

gains, losses, credits, and any other similar

attributes.

In addition, a “limited liability pass-through

entity” (“LLPTE”) includes any PTE that

affords any of its partners, members,

shareholders, or other owners “protection from

general liability for actions of the entity.” KRS

141.010(28).

The LLET applies to both C corporations and

LLPTEs and is not an alternative to another tax.

The LLET is the lesser of $0.095 per $100.00 of

Kentucky gross receipts (defined below) or

$0.75 per $100.00 of Kentucky gross profits

(defined as Kentucky gross receipts less

Kentucky returns and allowances and Kentucky

cost of goods sold). KRS 141.0401(2). A

minimum tax of $175 applies regardless of the

method used. Id. Kentucky gross receipts is

generally defined as including the total amount

of consideration paid for the sale, lease, rental or

use of property. 103 KAR Section 16:270.

However, for certain entities, such as law firms

and accounting firms, the entity must calculate

gross receipts on its business income. See KRS

141.120(8)(c); 103 KAR Section 16:270.

The LLET contains relief for certain small

businesses. Taxable entities with gross receipts

or gross profits equal to or less than $3 Million

are exempt from the LLET. Taxable entities

with gross receipts or gross profits between $3

Million and $6 Million are subject to a phased

out exemption but the LLET cannot be less than

zero. KRS 141.0401(2). The exemption phase-

out is calculated as follows:

$2,850 * $6 Million-Kentucky Gross Receipts $3 Million

OR

$22,500 * $6 Million-Kentucky Gross Profits

$3 Million

No LLET relief exists for entities with gross

receipts or gross profits equal to or greater than

$6 Million. Id. In determining eligibility for the

exemption, a member of a combined group

(defined as the members of an affiliated group

and the LLPTEs that would be included if

organized as corporations) must consider the

combined gross receipts and the combined gross

profits of the entire group, including eliminating

entries from transactions within the group. KRS

141.0401(2)(b)(2).

Entities exempt from the LLET include financial

institutions, insurance companies, non-profit

organizations, public service corporations,

REITs, RICs, REMICs, certain personal service

corporations, certain cooperatives, and publicly-

traded partnerships. KRS 141.0401(6). These

entities are called “qualified exempt

organizations.” KRS 141.0401(7)(a). General

partnerships are also exempt because they do not

fit within the definition of a LLPTE due to the

lack of limited liability. See supra. In addition,

LLPTEs owned in whole or in part by a

20

qualified exempt organization must exclude the

proportionate share of gross receipts or gross

profits attributable to that ownership interest

when calculating the LLET. KRS

141.0401(7)(b). Thus, if a REIT is the single

owner of an LLPTE, the LLPTE is exempt from

the LLET as well.

Regular C corporations are subject to the LLET.

KRS 141.0401(2). However, such corporations

paying the LLET get to apply that amount as a

nonrefundable credit towards their regular

corporate income tax. KRS 141.0401(3). This

credit may not be applied against other income

and cannot be carried over to other tax years. Id.

As a result of the LLET, Kentucky added to its

list of activities that constitute “doing business.”

In addition to the items mentioned above for

corporations, “doing business in this state”

includes (1) maintaining an interest in a PTE

doing business in Kentucky, and (2) deriving

income directly or indirectly from a single-

member LLC that is doing business in Kentucky

and is a disregarded entity for federal tax

purposes. KRS 141.010(25).

Every PTE doing business in Kentucky, other

than publicly-traded partnerships, must withhold

Kentucky income tax on the distributive share,

whether distributed or not, of each nonresident

partner, member or shareholder, or each

corporate partner or member that is doing

business in Kentucky only through its

ownership interest in the PTE. KRS

141.206(5)(a). Withholding is at the maximum

tax rate. KRS 141.206(5)(b). An exemption to

the withholding requirement exists if the PTE

“demonstrates” to the Department of Revenue

that an owner has filed the appropriate return for

the prior year. If so, the PTE is not required to

so withhold until the exemption is revoked by

Kentucky. KRS 141.206(7). However, if the

owner fails to file or pay the tax due, Kentucky

may require the PTE to pay the owner’s share.

Id.

Individuals

Kentucky residents are taxed on all of their

income by Kentucky while non-residents are

taxed by Kentucky only on income received

from labor performed, business done, or other

activities in Kentucky; from tangible property

located in Kentucky; and from intangible

property that has acquired a business situs in

Kentucky. KRS 141.020(4). Neighboring

states, such as Illinois, Indiana, Ohio, Virginia,

Michigan, Wisconsin, and West Virginia, have

reciprocity agreements with Kentucky under

which their residents are not required to pay

Kentucky income taxes on salaries or wages

earned in Kentucky as long as the taxpayer does

not live in Kentucky for more than 183 days

during the tax year. 103 KAR Section 17:010.

However, because Tennessee has no income tax,

residents of that state receive no such special

treatment. The tax rate brackets are as follows:

21

Net Income Rate 0 - $3,000 2.0% $3,001 - $4,000 3.0% $4,001 - $5,000 4.0% $5,001 - $8,000 5.0% $8,001 - $75,000 5.8% $75,001 and above 6.0% KRS 141.020(2)(b).

The Kentucky personal income tax is based on

the federal income tax law in effect on

December 31, 2006, and the regulations and

rulings issued by the IRS are generally followed

where no contrary Kentucky law exists. KRS

141.050. Exempted from Kentucky income

taxes are certain employee pension

contributions; social security and railroad

retirement benefits; income exempt from

taxation pursuant to the Kentucky Constitution,

the US Constitution or statutory law; amounts

paid for health insurance of the taxpayer and his

or her family; amounts paid for long-term care

insurance; capital gains attributable to property

taken by eminent domain; and certain tobacco

payments. KRS 141.010(10). In addition, an

exclusion for pension distributions is allowed up

to $41,110 of total distributions from pension

plans, annuity contracts, profit-sharing plans,

retirement plans, or employee savings plans.

KRS 141.010(10)(i)2. Added to the federal

definition of adjusted gross income is interest

income of the obligations of other states and

their political subdivisions. KRS 141.010(10)(c).

In determining Kentucky net income from

adjusted gross income, four key deductions are

disallowed: (1) any deduction for any state

income taxes, or sales taxes used in lieu of

income taxes as provided by Section 164(b)(5)

of the IRC; (2) any deduction for estate

administration fees; (3) the federal personal

exemption; and (4) any deduction for amounts

paid to any club, organization, or establishment

that has been determined by a court or

government agency to discriminate in its

membership, services, facilities, or privileges

with regard to race, color, religion, national

origin, or sex (with an allowance for amounts

paid to charitable organizations that limit

membership to persons of the same religion to

promote the religious principles for which it was

established). KRS 141.010(11).

A variety of credits are available to taxpayers.

A credit of $20 per taxpayer and per dependent

is allowed, KRS 141.020(3), as well as a credit

up to 25% of the allowable federal credit for

qualified tuition and related expenses, as defined

in Section 25A of the IRC, paid to “eligible

Kentucky education institutions.” KRS 141.069.

Unused portions of this credit can be carried

forward for five years. Id. In addition, a credit

for rehabilitating certified historic structures is

allowed up to 20% of the cost of the

rehabilitation (30% for owner-occupied property

up to $60,000). KRS 171.397. However, a

state-wide limit of $3,000,000 in the aggregate

22

exists for the amount of credit available to all

taxpayers. Id. In addition, a nonrefundable

family size tax credit is available for residents

with a modified gross income of 133% or less of

the national poverty level. KRS 141.066(3)(a).

The amount of the credit allowed decreases as

the modified gross income approaches the 133%

threshold amount. KRS 141.066(3)(c).

Also, individual owners of LLPTEs subject to

the LLET receive a nonrefundable credit against

their individual income tax reduced by the

minimum tax of $175. KRS 141.0401(3)(b).

This credit cannot be used against other income

and cannot be carried over to other tax years. Id.

PROPERTY TAX

The Kentucky property tax is levied on the fair

cash value of all real and tangible personal

property unless exempted by the Kentucky

Constitution or, in the case of tangible property,

by statute. KRS 132.190. In general, property is

assessed as of January 1st of each year. KRS

132.220(1). Real property must be listed for

assessment with the county in which it is located

between January 1st and March 1st. Id. Tangible

property may be listed either with the county or

the Department of Revenue by May 15th. Id.

Section 170 of the Kentucky Constitution

prohibits the taxation of public property used for

public purposes; places of burial not held for

profit; property owned by religious institutions,

purely public charities, and educational

institutions; household goods used in the home;

and crops in the hands of the producer. In

addition, a “homestead exemption” is provided

for the personal residence of a person who is 65

years or older or totally disabled. The

exemption, which is adjusted every two years

based on the federal cost-of-living index, is

$34,000 for 2011 and 2012. See KRS 132.810.

Furthermore, since January 1, 2006, most

intangible property is exempt, with exceptions

for financial institutions and life insurance

companies. KRS 132.208.

State tax is imposed on taxable real estate at a

rate of 12.2 cents per $100 of assessed value.

KRS 132.020(1)(a), (2). Tangible personal

property is taxed for state purposes at various

rates under KRS 132.020(1)(b)-(r). Motor

homes are taxed as real estate unless owned by a

dealer and held for sale. KRS 132.751.

Property taxes generally are levied at the state,

county, city, and school district levels. Local

governments, such as counties, cities, school

districts, and other special taxing districts, are,

however, prohibited from taxing many types of

property -- for example, manufacturing

machinery, raw materials, and goods in process.

See KRS 132.200.

Generally, a county property valuation

administrator (“PVA”), an elected official,

assesses most classes of property for the state,

the county, most cities and all other special

23

taxing districts. KRS 132.220. The Department

of Revenue is charged with administering a

centralized assessment system for tangible

personal property. See KRS 132.486.

Depreciable tangible property is assessed using

replacement cost less accrued depreciation. A

20% salvage value is generally assigned to

property still in use past its economic life.

Business inventories are generally valued at

original value on a FIFO basis.

Personal property stored for subsequent

distribution out-of-state within six months after

the assessment date is exempt from all state and

local property taxes except for fire and special

taxing districts. KRS 132.097, 132.099. State

law allows lower rates for finished goods

inventories while local governments have the

option of exempting this type of property or

taxing it at reduced rates. In addition, private

leasehold interests in certain governmental

property financed through industrial revenue

bonds are taxed at a lower rate if approval is

obtained from the Kentucky Economic

Development Finance Authority (“KEDFA”).

KRS 132.020(1)(b), 132.195. KEDFA approval

also exempts a leasehold from local taxation.

However, if the private leasehold is for property

owned by a non-governmental, tax-exempt

owner and not financed by industrial revenue

bonds, then the leasehold is not exempt from

property taxes. KRS 132.195.

SALES AND USE TAXES

The sales and use tax is imposed at a 6% rate

and generally must be reported and paid monthly

to the Department of Revenue. The sales tax is

imposed on retailers for the privilege of making

retail sales, which include the sale, rental, or

lease of tangible personal property and the sale

of certain services. KRS 139.010(28) and

139.200. The use tax is imposed on tangible

personal property purchased outside Kentucky

for use within the state. KRS 139.310. The use

tax is also imposed on tangible personal property

that is purchased for resale (an exemption from

sales tax discussed below) but is used instead of

resold. KRS 139.290. County clerks are

authorized to collect use tax when certain

tangible personal property purchased outside

Kentucky is presented for registration in

Kentucky. Sales and use taxes are only imposed

by the state and not by local governmental

entities.

Kentucky is a party to the Streamlined Sales and

Use Tax Agreement, which provides uniform

definitions, sourcing rules, and audit procedures.

KRS 139.785 et seq. Under the agreement,

transactions are sourced to where the buyer (or

the buyer’s designee) takes possession of the

property. KRS 139.105. The use tax must be

collected by out-of-state retailers who qualify as

retailers engaged in business in Kentucky. KRS

139.340. If a representative conducts any

activities that help establish or maintain a

24

Kentucky market for the out-of-state retailer, the

retailer must collect tax on the representative’s

sales. KRS 139.340(2)(f). For 2006 and

beyond, any “remote” seller who allows

merchandise to be received and exchanged at an

affiliate or any other location in Kentucky is

treated as a retailer engaged in business in

Kentucky. KRS 139.340(2)(b).

Kentucky offers a variety of exemptions from

sales and use tax, especially to businesses. See

KRS 139.470 et seq. As previously mentioned,

items purchased for resale are not subject to the

tax. See KRS 139.260 and 139.010(25).

However, service businesses, including lawyers,

accountants, and other professional service

providers, are considered the consumers of

personal property they use in rendering services,

and generally must pay the tax at the time of

purchase. 103 KAR Section 26:010(2).

Construction contractors are also considered the

ultimate consumers of building materials,

fixtures, and other personal property

incorporated into buildings and other real estate

improvements -- for example, roads, sewers, and

sidewalks -- and must pay sales tax on their

purchases. 103 KAR Section 26:070(1).

Another major exemption applies to “machinery

for new and expanded industry.” KRS

139.480(10). To qualify, the machinery must be

used directly in a manufacturing process and

incorporated into plant facilities for the first time

in Kentucky. KRS 139.010(13). Machinery

does not qualify if it replaces other machinery

unless it increases consumption of recycled

materials by at least 10%, performs a different

function, manufactures a different product, or

has a greater productive capacity. To meet the

manufacturing requirement, the process must

take property with little or no commercial value

for its intended use and result in property with

appreciable commercial value for its intended

use. Id. A “plant facility” is a single location

dedicated exclusively to manufacturing activities

with only incidental retail activities present. Id.

Additional sales and use tax exemptions are

provided for:

raw materials, industrial supplies, and

industrial tools (KRS 139.470(11));

certified pollution control equipment

(KRS 139.480(12));

industrial machinery sold, delivered, and

used out-of-state (KRS 139.486));

containers, packaging, and wrapping

materials (KRS 139.470(2));

sales to nonprofit charitable, religious, or

educational entities (KRS 139.495(1));

sales made directly to the federal

government or its agencies,

25

instrumentalities, or corporations (103

KAR 30:235));

sales made directly to the Commonwealth

of Kentucky or local governmental

entitles located therein (KRS 139.470(7));

and

occasional sales as defined by KRS

139.010(17) (KRS 139.470(4)).

Exemptions from sales and use taxes for

individuals include, but are not limited to,

unprepared foods, prescription drugs, certain

medical supplies, residential utilities other than

telephone, and residential fuels. KRS 139.470 et

seq.

Communications services are subject to the

Kentucky sales tax. KRS 139.200(2)(e).

“Communications services” include

“telecommunication services” as defined by

KRS 139.195(28) and “ancillary services” as

defined by KRS 139.195(1). KRS

139.195(5)(a). Such services include, but are

not limited to, local and long distance telephone

services, prepaid and postpaid calling services,

data transport services, caller ID services, cell

phone services, and voice over internet protocol

(VoIP). A refundable credit is available to any

business whose interstate communications

service exceeds 5% of that business’s Kentucky

gross receipts for the prior calendar year as long

as that business’s annual Kentucky receipts are