dollarization in latin america a study of argentina - ecuador jeff cotter, delphine pape, james...

Post on 22-Dec-2015

217 views

TRANSCRIPT

Dollarization in Latin America

A study of Argentina - Ecuador

Jeff Cotter, Delphine Pape, James Phillips, Victor Pinto, Gary Sidell, Betsy Townsend

Dollarization

• A country uses the dollar/another currency

alongside or instead of the domestic currency

• Uses include:

– Payment for wages, Consumer purchases, Tax

Payments, Government Payments

• Unofficial vs. Official dollarization

How Unofficial Dollarization Works

• Informal/Unofficial

• Formal/Unofficial Dollarization– Currency Board established

• Authority to issue domestic currency at fixed exchange rate in concordance with the international reserve.

• Maintains full, unlimited convertibility.

– Orthodox/Unorthodox Currency Boards

How Official Dollarization Works

• Dollarized country relinquishes its monetary policy and adopts the policy of the issuing country.

• Inflation and interest rates tend to be the same between the two countries.

• Money Supply is determined by the Balance of Payments.

• Financial integration occurs as foreign and domestic financial institutions compete.

Why Consider Dollarization? • Create Fiscal and Monetary discipline

• Lower and stabilize inflation

• Increase reliability of financial markets

• interest rates & access to long term debt

• Create a more stable business environment

Costs/Benefits of DollarizationCosts

• Loss of flexibility in monetary policy

• What is good for US may not be for others

• Lost revenues of seigniorage

• No central bank as lender of last resort

Benefits

• Fosters budgetary discipline/credibility

• Lower international transaction costs

• Lower inflation today and lower risk of future inflation

• Stable interest rates

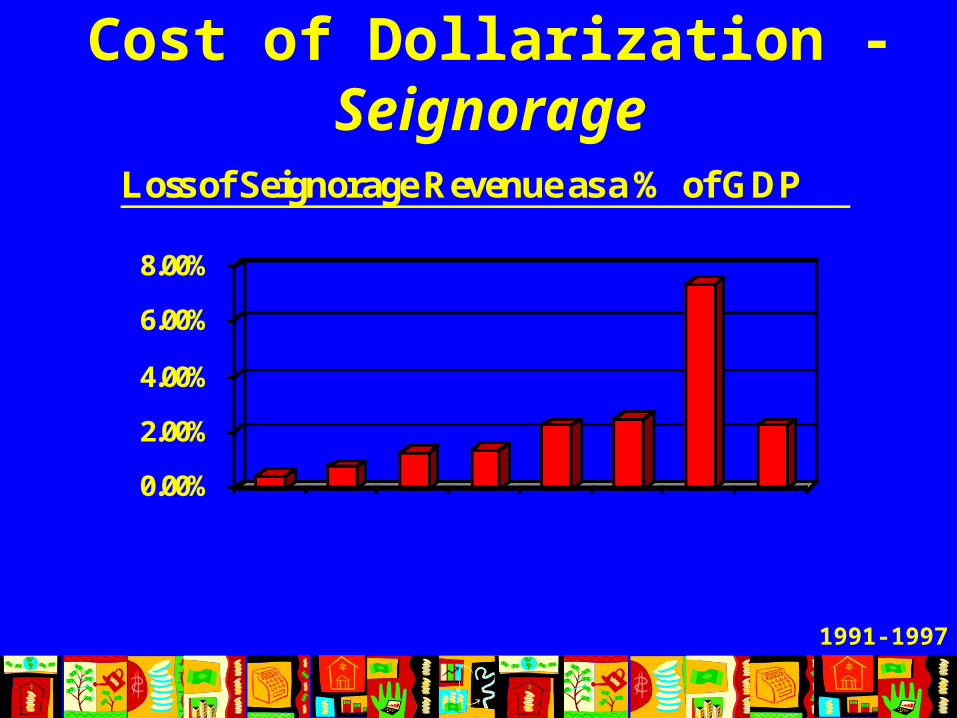

Cost of Dollarization - Seignorage

0.00%

2.00%

4.00%

6.00%

8.00%

ArgentinaMexicoBrazilBolivia

El Salvador

Peru

EcuadorAverage

Loss of Seignorage Revenue as a % of GDP

1991-1997

1991-1997

Argentina: History

• Pre-1991: Hyperinflation (up to 5000%)– unofficial dollarization

• 1991: Convertibility Law passes

• 1994: Foreign financial institutions compete on equal basis with Argentine institutions

• February 1999: Propose official dollarization

Convertibility Law = Unofficial Dollarization

• Central Bank must hold reserves = 100% of monetary base (currently $13.9 bil.)

• 1:1 exchange rate - 10,000 australes per $1, new Peso equal to 10,000 australes

• Law prevents central bank from printing money (limits powers as lender of last resort)

Convertibility Plan Performance

• Relative economic stability since 1991

• Interest rate spikes – during Mexico’s currency crisis in 1994-5– during Asian and Brazil currency crises since 1997

• Speculative pressure against Argentine peso until government threatened to dollarize

Argentine Inflation after Economic Restructuring

0%

1000%

2000%

3000%

4000%

5000%

19891990199119921993199419951996199719981999

Dollarization Goals

• Eliminate speculation about the Peso devaluation.

• Lower/eliminate spread between U.S. and Argentine interest rates.

• Restore confidence in the Argentine monetary system.

Dollarization Concerns: Applicability to Argentina

• The peso, a symbol of Argentina / loss of independence

• Argentines already use $ under Convertibility Law.

• Revenue is minimal because they do not have freedom to print

• Not proven (evidence shows dollarized countries do better).

• Lose ability to cope with external shocks

• Lose revenue derived from seignorage

Argentina Today

• Convertibility Law still in effect.

• No immediate plans to officially dollarize under new President Fernando de la Rua.

• Debate/discussion continues - Argentine and American officials met last month in Washington to discuss dollarization.

Ecuador: All is not Well

• Worst economic crisis in five decades.– Economic and Natural environment

• Social consensus for economic reform needed– President proposes ending the severe recession with

implementing dollarization, in 180 days. – President overthrown, new president implements

• International Reception:– Well internationally, along with a belief of “Dollarization

out of Desperation” -IMF head Stanley Fischer

Dollarization: The Plan• Swap Rate

– 25000:1

• Central Bank 180 days to exchange currency– $936M in reserves

• Financial Institutions – Transact in $US

• Accounting (public/private entities & individual) – Expressed in $US

Dollarization: The Plan• Debt

– Individual & company debt >$50K US restructured to settle in 3-7 years

• No capital controls on foreign currency

• Interest rates with a maturity of 1/10-11 2001 – 16.82% on loans – 9.35% for deposits

• Finance Minister may not present a budget with a deficit exceeding 2.5% of GDP

Goals

• Increased confidence spurs foreign investment and trade– remove currency risk

– curbs hyperinflation

• Privatization of SOE’s– pipeline investment

Dollarization Has Occurred: Now What?

• $900M in loans--IMF

• Stimulate new capital inflows

• Gain full domestic support through additional legislation. – Guarantee of part time wage of $.50 per hour

• May receive 85% of seignorage benefits of dollarization from US.

Dollarization• Brings discipline & stability to financial markets.

• Not a formula.

• Difficult and expensive to implement depending on circumstances.

• Often has proven to achieve objectives.– GDP growth , lower inflation, lower interest rates

Effects on US & other countires

• US has broader responsibility to consider effects of fiscal policies on dollarized nations.

• Caution: IMF funding Programs should not be regarded as surrogate central bank opportunities.

Sources• Central Bank of Argentina (www.bcra.gov.ar)

• Hanke, Steve H. and Schuler, Kurt, A Dollarization Blueprint for Argentina, “Friedberg’s Commodity and Currency Comments Experts’ Report”, February 1, 1999.

• Calvo, Guillermo, Argentina’s Dollarization Project: A Primer, February 18, 1999.

• Argentina Mulls Dollarization, (www.oir.com)Optima Investment Research, 1999

• “Dollars enticing South of the Boarder, US Passive to Trend Despite Benefits” -Washington Times, February 17, 2000

• Calvo, Guillermo A., “Testimony on Full Dollarization” Presentation before Joint Hearing of the Subcommittees on Economic Policy and International Trade & Finance. April 22, 1999.

• Cardosa and Franko texts

More Sources

• Reuters news service, 2/29/00, 3/1/00 and 3/3/00

• Casey, Michael Dow Jones Newswires “Ecuador’s Dollarization Plan Fuels Talk, If Little Else” 3/3/00.

• Casey, Michael Dow Jones Newswires “A Wary Wall Street Welcomes Ecuador Dollarization Bill” 3/1/00

• http://sica.gov.ec/ingles/docs/basics_of_dollarization.htm

• http://www.odci.gov/cia/publications/factbook/ec.html

• ABC-CLIO, Inc., Kaleidoscope

Sources• Dollarization, July 1999, Joint Economic Committee Staff Report

Office of the Chairman, Connie Mack Prepared by Kurt Schuler, Senior Economist to the Chairman*

• U.S. Senate Banking Committee “Citizens Guide to Dollarization” 1999• Should there be five currencies or one dundred and five? Ricardo

Hausmann• U.S. Senate Joint Economic Committee Report “Basics of

Dollarization,” January, 2000 (www.senate.gov/~jec/basics.htm)• Three cheers for Dollarization. Euromoney, London 1999. Steve Hanke• http://users.erols.com/kurrency/ intro.htm *• http://users.erols.com/kurrency/, OFFICIAL OR "FULL"

DOLLARIZATION: CURRENT EXPERIENCES AND ISSUES by Zeljko Bogetic, International Monetary Fund, June 9, 1999.*

*copy included in Word document “doll2”