dollars real spot price in april 2017 price fob (dollars ......apr 28, 2017 · projects wti prices...

TRANSCRIPT

ISSN 1948-2388

The Fuel and Vehicle Trends Report

April 28, 2017

1

This report is a summary of the latest fuel prices and other oil industry key statistics. In addition, this report provides the latest trends in vehicle

registrations and transportation tax collections for the state of Washington. It also summarizes articles appearing in popular, business, and technical

media referring to fuel price, production and supplies as well as vehicle sales and registration trends. At the end of the report is a listing of all articles

summarized, with hyperlinks to internet sources where available. Some hyperlinks may require free registration or paid subscriptions to access. The appearance of articles, products, opinions, and links in this summary does not constitute an endorsement by the Washington State Department of

Transportation. Photos and other artwork included in the report are either included with permission or are in the public domain. The Fuel and Vehicle

Trends Report (ISSN 1948-2388) is compiled by Brian L. Calkins, M.S. Agricultural Economics, Lizbeth Martin-Mahar, Ph. D., and David Ding, Ph. D., Economic Analysis Section, Budget and Financial Analysis Office of the Washington State Department of Transportation. Contact the editors

by email at [email protected] or [email protected] or [email protected] by telephone at (360) 705-7991 or (360) 705-7942 or

(360) 705-7502.

TABLE OF CONTENTS

FUEL PRICE TRENDS: CRUDE, GASOLINE AND DIESEL MARKETS………………...………...…………...1

WASHINGTON RETAIL GAS AND DIESEL PRICES……………..…………………….….…………………......6

BIODIESEL FUTURES AND PRICE TRENDS…………………………………………….….………………..…...8

FUEL PRICE TRENDS COMPARED TO FORECAST……..………………………………………….....…...…...11

MOTOR VEHICLE FUEL TAX COLLECTION TRENDS COMPARED TO FORECAST ………………...…12

VEHICLE TRENDS ……………...………………………………………………………………………......…….…14

SUBSCRIBING TO THE FUEL AND VEHICLE TRENDS REPORT….…...……………………………...……....16

ARTICLES REFERENCED…………...………………………………………………………………………...….…16

FUEL PRICE TRENDS: Crude, Gasoline and Diesel Markets

Analysis by Brian L. Calkins, M.S.

Figure 1: Weekly Cushing, Oklahoma WTI Spot Price FOB (Dollars Per Barrel) January 1990 to April 2017.

Source: Energy Information Administration (EIA), 2017a

July 4, 2008$142.52

Dec 26, 2008$32.98 Feb 12, 2016

$28.14

Apr 21, 2017$53.19

$0

$20

$40

$60

$80

$100

$120

$140

$160

Do

llar

s p

er

Bar

rel

Weekly Cushing, OK WTI Spot

Price FOB (Dollars per Barrel)

Real Spot Price in April 2017

dollars

$19.81

$30.66

$19.81$

The Fuel and Vehicle Trends Report ISSN 1948-2388 April 28, 2017

2

WTI spot prices crude averaged $52.50 per barrel for January 2017. Since then, WTI crude

oil prices increased nearly $1 to $53.47 per barrel in February before falling to $49.33 per barrel in

March 2017. EIA’s daily prices average $52.17 per barrel through April 17. Unplanned supply

cutbacks in Libya and perceptions of a continuance of OPEC/Non-OPEC production cuts led to

higher crude prices in late March and April (EIA, 2017b. EIA’s daily prices rose to an average

$52.17 per barrel through April 17. A year ago in April 2016, WTI spot prices were much lower at

$40.75 per barrel. WTI prices bottomed out at $28.14 per barrel for the week ending February 12,

2016.

EIA’s April 2017 Short-term Energy Outlook (STEO) reported an average WTI price of

$43.33 per barrel for calendar year (CY) 2016 and projects a $52.24 per barrel for CY 2017 and

$55.10 per barrel in CY 2018 (EIA, 2017b), nearly the same as January’s STEO $52.50 per barrel

for CY 2017 and $55.18 per barrel for CY2018. IHS Global Insight’s April 2017 forecasts a WTI

crude oil price of $52.80 per barrel in 2017 and $51.46 per barrel in 2018. Consensus Economics

projects WTI prices of $49.88 a barrel in calendar year 2017 and $56.59 per barrel in 2018

(Consensus Economics Inc., April 2017).

EIA forecasts Brent crude oil price to average $54.23 per barrel for 2017 and $57.10 per

barrel in 2018. The daily WTI-Brent crude oil spot price difference fluctuated from an average of

$2.07 per barrel in January 2017, $1.40 per barrel in February, $2.39 per barrel in March, and $1.32

per barrel in the 1st half of April 2017 (Figure 2). The WTI price discount to the Brent crude oil

price averaged $0.40 per barrel in 2016 and is estimated to increase to $2 per barrel in both calendar

years 2017 and 2018. The WTI-Brent spread of $2 per barrel is due to increasing oil exports from

the US to Asian markets pushing Brent crude prices up because of transportation costs.

EIA reports that U.S. oil production averaged 9.4 million barrels per day (b/d) in 2015 and

declined to an average of 8.9 million b/d in calendar year 2016. Production is forecasted to increase

to an average of 9.2 million b/d in 2017 and 9.9 million b/d in 2018. EIA indicates that oil

companies are increasing capital expenditure activity and increasing active and more efficient oil

rigs. This supports growth projections in calendar years 2017 and 2018.

The Fuel and Vehicle Trends Report ISSN 1948-2388 April 28, 2017

3

Figure 2: WTI - Brent Crude Oil Spot Price Spreads from January 2008 to April 17, 2017.

Source: EIA 2017a Daily WTI and Brent crude oil spot prices

Inventories

January’s Trends Report used newly calculated five-year averages for inventories to

compare to current inventory levels. Weekly inventories for crude oil, gasoline, and distillate are

now updated to the five-year span from 2012 to 2016. EIA’s Weekly Petroleum Status Report

shows U.S. crude oil inventories, excluding Strategic Petroleum Reserve (SPR) stocks, at 532.343

million barrels for the week ending April 14, 2017 (Figure 3). This storage level is 127.8 million

barrels or 31.6 percent higher than the 5-year (2012-2016) historical average of 404.4 million

barrels for this week and even surpasses record inventories from 2016 by 25 million barrels for this

week.

-$35

-$15

$5

$25

$45

$65

$85

$105

$125

$145

Spread

WTI Crude Oil Price

Brent Crude Oil Price

The Fuel and Vehicle Trends Report ISSN 1948-2388 April 28, 2017

4

Figure 3: Comparison of Crude Oil Weekly Inventories from January 2012 to April 2017.

300

350

400

450

500

550

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

5 year average 2012-2016

2017 inventories

2016 inventories

5 year range 2012-2016

Weekly U.S. Ending Inventories of Crude Oil Excluding Strategic Petroleum Reserve

Mil

lio

n B

arr

els

The Fuel and Vehicle Trends Report ISSN 1948-2388 April 28, 2017

5

Figure 4: Comparison of Gasoline Weekly Inventories (West Coast PADD5) from January 2011 to January 2017

22

24

26

28

30

32

34

36

38

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

5 year average 2012-2016

2017 inventories

2016 inventories

5 year range 2012-2016

Figure 4 shows gasoline inventories increasing from 28.6 million b/d in the week ending

March 17, 2017 to 30 million b/d in the week ending April 14, 2017 within the West Coast

Petroleum Administration for Defense District (PADD5). This inventory volume for the week of

April 14th is also 5.5 percent higher than the 5-year average of 28.5 b/d. For comparison, U.S. total

gasoline inventories for the week ending April 14, 2017 are tracking just 2 million b/d below the

inventories for the same week in 2016, the year that had the highest inventories in the last 5 years.

Figure 5 shows weekly distillate inventories for PADD5 (West Coast) in 2017. In the last

five weeks from March 17 to April 14 week-ending inventories deviated from the 5-year average by

a mere positive 0.3 percent. Figure 5 also shows distillate inventories were lower than average for

most of January but peaked beyond the 5-year average for week-ending inventories on February 10.

National distillate inventories, to date, follow a different trajectory in 2017. In January and

February, inventories exceeded the 5-year average maximum boundary, which 2016 established. In

contrast, March and April inventories are falling an average of 1.4 percent per week or a total of 9.7

percent. However, in context, April 14 week-ending inventories range 14.9 percent or 19.3 million

gallons above the 5-year average.

The Fuel and Vehicle Trends Report ISSN 1948-2388 April 28, 2017

6

Figure 5: Comparison of Monthly Distillate Inventories (West Coast PADD5) from January 2011 to April 2017

10

11

12

13

14

15

16

17

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

5 year average 2012-2016

2017 inventories

2016 inventories

5 year range 2012-2016

Mil

lio

n B

arr

els

Washington Retail Gasoline and Diesel Prices

Since the last Trends Report in January, Washington’s monthly average gasoline prices

steadily increased, beginning December 19, 2016, with a price of $2.53 per gallon. (Figure 6). (EIA,

2017d). The seasonal increase in gasoline prices, starting in December or January is typical for

Washington. Monthly per gallon prices in 2017 for January through April averaged $2.68 per gallon

for January, $2.70 per gallon for February, $2.80 per gallon for March, and $2.88 per gallon for

April. The price in the last week in April topped out at $2.90 per gallon. The year-to-year change in

the Washington price for a gallon of regular gasoline averaged $2.73 per gallon in April 2015 and

$2.28 per gallon in April 2016. Recent prices are considerably higher than one year ago.

The nation-wide price of $2.42 per gallon in April 2017 for a gallon of regular gasoline is

much lower than Washington’s price of $2.88 per gallon because of Washington’s higher excise

taxes on motor vehicle fuel and the relative distance and isolation of PADD5 states to other PAAD

district markets in the U.S. The regional price variation again showed the West Coast (PADD 5)

with the highest price in April 2017 at $2.88 per gallon of regular gasoline compared to the lowest

average price in Gulf Coast (PADD 3) at $2.20 per gallon. The West Coast (PADD5) less

California price came in at $2.65 per gallon for April, still 23 cents higher than the national average

of $2.42 per gallon (EIA, 2017d). EIA’s April 2017 STEO forecasts a national average retail regular

The Fuel and Vehicle Trends Report ISSN 1948-2388 April 28, 2017

7

gasoline price of $2.39 per gallon in calendar year 2017 and $2.44 per gallon in calendar year 2018

(EIA, 2017b).

The price for regular gasoline in California averaged $3.00 per gallon in April 2017

compared to April 2016’s price of $2.77 per gallon. California’s regular gasoline price for April

2017 was 12 cents per gallon higher than Washington’s $2.88 per gallon for the same month.

Since the last Trends Report, Washington’s retail diesel prices rose 11 cents from December

2016 to January 2017. From February through April 2017, Washington’s retail diesel prices rose

only an average 2 cents per month. Washington’s retail diesel price average of $2.87 per gallon in

April 2017 was 58 cents higher than April’s 2016 price of $2.29 per gallon (Figure 6). Nationally,

April 2017’s retail diesel price averaged $2.42 per gallon, compared to $2.11 per gallon in April

2016, a 31 cent increase. EIA forecasts a national average retail diesel price of $2.69 per gallon for

calendar year 2017 and $2.85 per gallon for calendar year 2018 (EIA, 2017b).

California’s diesel price increased 48 cents per gallon to $2.94 per gallon in April 2017 from

April 2016’s $2.46 per gallon. Washington’s April 2017 diesel price was only 7 cents lower at

$2.87 per gallon than California’s price for the same month.

Figure 6: Washington Retail Regular Gasoline and Diesel Prices ($ per gallon): January 2, 2006 to April 24, 2017.

Source: AAA Fuel Gauge Report for Washington Retail Diesel Prices and EIA 2017d Weekly

Retail Gasoline Prices

Jul 14, 2008$4.96

Mar 23, 2009$2.27

Apr 09, 2012$4.52

Feb 2, 2015$2.76

Apr 24, 2017

$2.89

Jun 30, 2008$4.37

Dec 15 and Dec 22, 2008, $1.78

May 28, 2012$4.30

Feb 2, 2015$2.11

Feb 29, 2016$2.00

Apr 24, 2017$2.90

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

Regular Gasoline

Diesel

The Fuel and Vehicle Trends Report ISSN 1948-2388 April 28, 2017

8

EIA annually provides a supplementary report Summer Fuels Outlook with the April issue of

the Short-Term Energy Outlook (EIA), 2017e. EIA expands the extent of “summer” in Summer

Fuels Outlook to April through September. I recommend this report to readers who want further

understanding of crude oil, gasoline, and distillates during the months where changes in demand

and supply can greatly affect market prices.

EIA provides a one-page summary, which nicely identifies the key factors for oil prices for

the upcoming 2017 summer season:

Worldly, oil supply and consumption are expected to be relatively balanced in 2017,

Brent crude oil will average $54/barrel in summer 2017, $8 higher than in 2016,

As always, there is price uncertainty calculated from current dollar values of futures and

options contracts. There is a 10 percent probability that WTI prices could exceed $60 per

barrel in July, $5 higher than EIA’s forecast for July 2017. Price uncertainty increases as the

forecast unfolds into further into the forecast,

The U.S. and OPEC are driving the forecasted global liquid petroleum production up by 1.1

million b/d in 2017,

Worldwide, liquid fuels consumption is projected to increase by 1.5 million b/d in 2017, and

Global consumption will outpace supply in 2017, which will reduce inventory builds.

BIODIESEL PRICE PREMIUM TRENDS

Analysis by Lizbeth Martin-Mahar, Ph.D.

Soybean Oil Futures and Biodiesel Prices Soybean Oil Futures

Biodiesel prices are dependent in a large part on the cost of the feedstock used in producing

biodiesel. Since soybean oil is the predominant feedstock for biodiesel, the futures for soybean oil

have been examined in past Fuel and Vehicle Trends Reports. Figure 7 shows the latest futures for

soybean oil for the past 2 years beginning in December 2014 through January 2017. Futures have

ranged from 28 cents per pound in October 2015 to 36 cents per pound recently projected in January

2017 for July 2017. These latest April 2017 soybean futures are lower than four months ago in

January. April 2017 futures start at 31.8 cents per pound for soybean oil instead of 35 cents in

January. Over time, the latest futures are not anticipated to rise much, to 33 cents per pound by

February 2018 and then stay at 33 cents until December 2019.

The Fuel and Vehicle Trends Report ISSN 1948-2388 April 28, 2017

9

Figure 7: Futures Prices for Soybean-oil (December 2014 through April 2017)

Biodiesel Prices: Comparison of Historical and Recent Prices Recent Trends: Washington B99 Biodiesel Prices

Since January 2017, the average monthly B99 biodiesel price has been stable at around

$2.20 per gallon each month. Prior to January 2017, B99 prices had fallen significantly since March

2016. In calendar year 2016 after February, B99 prices averaged $1.62 per gallon. In January 2017,

the B99 average monthly price increased to $2.18 per gallon and in February, the monthly average

price increased to $2.28 per gallon. In March and April 2017, the monthly average B99 price was

$2.29 and $2.21 per gallon respectively. A year ago, in March and April, the monthly average B99

price was even lower at $1.83 and $1.84 per gallon respectively.

As we reported in the prior editions of the Fuel and Vehicle Trends Report, the recent

decline in B99 biodiesel prices has fallen so far that is now below regular retail diesel prices. As a

result, the B99 price premium is no longer a premium but a discount like B5 biodiesel prices. In

February and March, the B99 price discount was $0.14 and $0.13 per gallon or 5.7 percent and 5.3

percent below retail diesel prices. In April, B99 prices dropped a little so the B99 price discount

grew to 8.7 percent.

Recent Trends: Washington B10 Biodiesel Prices

Washington State Ferries (WSF) is now testing using B10 biodiesel in their vessels. We are

going to track the trends in the B10 biodiesel prices. We have B10 biodiesel prices since January

2016. On average during calendar year 2016, B10 biodiesel prices were $1.58 per gallon. Since the

beginning of calendar year 2017, B10 monthly average prices have been higher. In January through

March 2017, B10 biodiesel prices were $1.86 per gallon and by April, the B10 monthly average

The Fuel and Vehicle Trends Report ISSN 1948-2388 April 28, 2017

10

price increased to $1.91 per gallon. A year ago, B10 monthly average prices were significantly

lower. In February 2016, the monthly average price was $1.47 per gallon and in March, the B10

biodiesel price was only $1.14 per gallon. In April 2016, the average B10 price was $1.20 per

gallon, which was $0.71 per gallon lower than this April. The B10 biodiesel price discount was 21.4

percent in April and 23 percent in February and March. The recent months’ B10 price discount is

smaller than a year ago when the discount ranged from 33 percent to 35 percent.

Figure 8: Washington OPIS B99, B10 and B5 Biodiesel Prices in Seattle

B99 Prices B10 Prices B5 Prices

Monthly

Average Price

Price

($/gal)

% Change

from State Avg

Diesel Price

Price

($/gal)

% Change

from State Avg

Diesel Price

Price

($/gal)

% Change from

State Avg Diesel

Price

February 2016 3.37 90.6% 1.47 -17.0% 1.13 -34.8%

February 2017 2.28 -5.7% 1.86 -23.1% 1.76 -27.3%

March 2016 1.85 3.2% 1.14 -36.7% 1.13 -35.5%

March 2017 2.29 -5.3% 1.86 -23.0% 1.66 -31.1%

April 2016 1.86 0.6% 1.20 -35.3% 1.23 -32.8%

April 2017 2.21 -8.7% 1.91 -21.4% 1.80 -25.6%

Source: B99, B10 and B5 biodiesel price data - OPIS Fuel Price Survey for various locations in

Washington State.

The Fuel and Vehicle Trends Report ISSN 1948-2388 April 28, 2017

11

Recent Trends: Washington B5 Biodiesel Prices

B5 biodiesel prices in Seattle averaged $1.75 per gallon between January and April 2017. In

January and February, the B5 biodiesel price averaged $1.79 and $1.76 per gallon, respectively. In

March, the B5 price fell to $1.66 per gallon but in April, it increased up to an average of $1.80 per

gallon. The B5 price discount is still high at -27.3 percent in February, -31 percent in March and -

25.6 percent in April. A year ago, B5 prices were even lower at $1.15, $1.16 and $1.24 per gallon

respectively for February through April. A year ago, the B5 price discount at -35 percent was even

larger than now.

FUEL PRICES AND CRUDE OIL PRICE TRENDS COMPARED TO RECENT

FORECASTS: US crude oil prices, Washington retail prices of gasoline and diesel

Analysis by Lizbeth Martin-Mahar, Ph.D.

In the last edition of the Fuel and Vehicle Trends Report, we discussed that WTI crude oil

prices have remained pretty low and flat and now we have only seen $1 per barrel decline in WTI

crude oil prices since the average price at the beginning of the calendar year. In January 2017, the

average monthly WTI price was $52.49 per barrel and in February, the average monthly crude oil

price was only $53.47 per barrel. In March, the monthly average WTI price was $49.33 per barrel

and in April, the monthly average WTI price was $51.20 per barrel so there has been little

movement in the prices. When comparing to the March 2017 forecast in recent months, in

February, the actual WTI monthly average was 0.9 percent above the first quarter 2017 forecasted

average. In March, the actual WTI price was 6.9 percent below the first quarter 2017 projected

average of $53 per barrel. In April, WTI prices came in a little higher at $51.2 per barrel, which was

below the forecast by 3.4 percent. See Figure 9 for more detail.

Consistent with the recent trend in WTI crude oil prices being below the latest forecast,

Washington retail gasoline prices also came in below the first and second quarter projections of

$2.70 and $2.87 per gallon respectively. In the month of February, retail gas prices averaged $2.70

per gallon, which was 0.1 percent below March’s first quarter of 2017 projection. In March 2017,

retail gas prices came in above the forecast by 3.6 percent at $2.80 per gallon. In April, retail gas

prices came in slightly higher at $2.88 per gallon, which was 0.2 percent above the second quarter

forecast of $2.87 per gallon.

The recent trends for retail diesel repeat crude oil and retail gasoline price trends. During the

last three months, retail diesel prices have been flat at $2.86 per gallon in February and March. In

April, retail diesel prices rose a little to $2.88 per gallon, which was slightly below the latest

projections of $2.97 per gallon in the second quarter. .All recent months of retail diesel prices were

below the March projections.

In the last three months (February through April), we have seen the difference between retail

gas and diesel prices narrow from $0.16 per gallon to being nearly no change between prices by

April 2017. This trend is the result of diesel prices being flat while retail gas prices have risen some

in the last three months.

The Fuel and Vehicle Trends Report ISSN 1948-2388 April 28, 2017

12

Figure 9: Percent Change in February through April 2017 Average Fuel Prices Compared to the March 2017 Price Forecast

Source: Washington Transportation Revenue Forecast Council March 2017 Forecast, EIA and AAA

weekly fuel prices

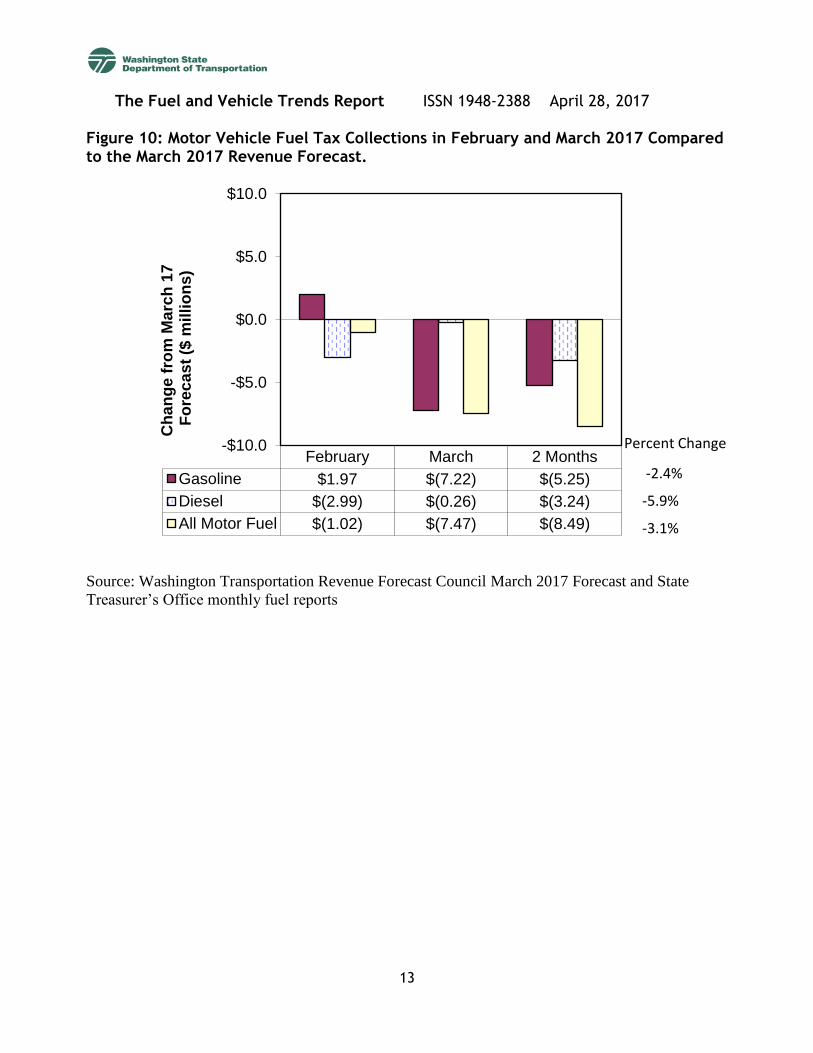

WA MOTOR VEHICLE FUEL TAX COLLECTION TRENDS COMPARED TO RECENT

FORECASTS: Gasoline and Diesel Tax Collections

Analysis by Lizbeth Martin-Mahar, Ph.D.

Since the adoption of the March 2017 forecast, two months of fuel tax collections were

reported. Overall fuel tax collections came in at $140.2 million for February, which was $1 million

down from the March forecast. See Figure 10. In February, gas tax collections came in at $114.74

million, which was slightly above the forecast by $1.97 million or 1.7 percent, the March forecast of

$112.8 million. Diesel tax collections in February came in at $25.45 million and below forecast by

$3.0 million or 10.5 percent.

A month later in March the overall March actuals came in at $126.24 million, which was

$7.5 million below the March forecast. Gas tax collections came in at $100.24 million, which was

below the March forecast by $7.22 million. Diesel tax collections totaled $26 million, which was

below the March forecast by $0.26 million.

For both months, gas tax collections have come in below forecast by $5.25 million while

diesel tax collections have come in below the latest forecast by $3.24 million.

The Fuel and Vehicle Trends Report ISSN 1948-2388 April 28, 2017

13

Figure 10: Motor Vehicle Fuel Tax Collections in February and March 2017 Compared to the March 2017 Revenue Forecast.

Source: Washington Transportation Revenue Forecast Council March 2017 Forecast and State

Treasurer’s Office monthly fuel reports

February March 2 Months

Gasoline $1.97 $(7.22) $(5.25)

Diesel $(2.99) $(0.26) $(3.24)

All Motor Fuel $(1.02) $(7.47) $(8.49)

-$10.0

-$5.0

$0.0

$5.0

$10.0

Ch

an

ge f

rom

Ma

rch

17

Fo

rec

as

t ($

mil

lio

ns)

Percent Change

-2.4%

-5.9%

-3.1%

The Fuel and Vehicle Trends Report ISSN 1948-2388 April 28, 2017

14

VEHICLE TRENDS

Analysis by David Ding, Ph.D.

Vehicle Registrations and Revenue

For the two months of data, we have since the March forecast, vehicle registrations are down

for the month of February and up for the month of March. Passenger car registrations came in at

366,156 for February and 492,214 for March. We forecasted that 431,190 and 465,863 vehicles

would register in February and March respectively. The February actual is lower than we expected,

which was mainly due to several Department of Licensing (DOL) field offices temporarily closing

during that time. It is quite possible that the missed registrations will pick up in later months. Truck

registrations were also lower than forecasted in the two months, with only 258,502 trucks

registering, when 276,604 were expected to register. Like passenger cars, DOL field office closures

accounted for the lower registrations in trucks. Overall, for both months, passenger cars are down

0.31 percent, trucks were down 6.5 percent and total registrations were down 4.8 percent.

Figure 11: Vehicle registrations, February and March 2017, Forecast vs. Actual.

Source: Washington Transportation Revenue Forecast Council March 2017 Forecast and

Department of Licensing Reports 13, February and March 2017.

We have three months of revenue since the March forecast: January, February and March

(Figure 12). Revenue from $30 basic fee vehicles was $12.12 million, just $290,000 shy of the

forecasted $12.41 million in January. February basic license fee revenue forecast also fell short. The

Department of Licensing collected $11.02 million, $1.39 million less than the $12.41 million we

forecasted. The March revenue made up some of the shortfall of the previous months, and the

shortage is $750,000 in total or 1.9 percent. Revenue for trucks was lower than expected for January

and February, however, it came in higher than expected for March. January’s collections of $15.99

million fell behind the expected $23.1 million by $7.11 million. This was because some truck

The Fuel and Vehicle Trends Report ISSN 1948-2388 April 28, 2017

15

revenues were not picked up by DOL’s new vehicle registration and revenue computer system.

February’s collections of $14.22 million fell short by $4.86 million than the forecasted revenue, the

shortage is reflected in the lower than expected registrations discussed earlier. In March, the truck

revenue was $2.63 million higher than forecasted, which picked up some lost revenue in the

previous two months. For all three months, the truck revenue fell short by $9.34 million in total or

15 percent. This lower revenue does align with the lower than expected truck counts. During the

transition to the new reporting system, DOL’s monthly reporting did not pick up all the prorate

truck revenue in January and February. We saw some of the revenue in the March report but we

expect additional truck revenue in April. We will continue to investigate this and other reporting

issues further with DOL as the transition to the new vehicle reporting system is smoothed out.

Finally, total License, Permit, and Fee (LPF) revenue was behind forecast by 6.0% for

January, February and March. We forecasted $59.86 million in January, but received $51.26

million. For February, we forecasted $55.22 million, but received $46.68 million. For March, we

forecasted 64.23 million, while realizing $70.55 million. Overall, total license, permits and fee

revenue is down $10.82 million.

Figure 12: Vehicle revenue for Jan., Feb. and Mar. 2017, Forecast vs. Actual.

Source: Washington Transportation Revenue Forecast Council March 2017 Forecast and

Department of Licensing Balance Forward, Jan., Feb. and Mar. 2017.

New Car and Truck Registrations from Sales

In this report, which covers new car registrations for January, February and March, we can

see year over year increases for two of the three months. New car registrations showed a strong

increase. In January 2017, new car registrations were 2,767 above registrations for January 2016. In

The Fuel and Vehicle Trends Report ISSN 1948-2388 April 28, 2017

16

February, there were 1,230 fewer vehicles than the prior year. March 2017 was 815 vehicles higher

than 2016, which contributed to a total extra vehicle registration of 2,352 for the three months. New

truck registrations were higher as well. January 2017 new truck registrations exceed the previous

January by a mere 119 trucks. February 2017 new truck registrations were 280 trucks above 2016.

March was even higher, exceeding the previous March by 502 trucks. The 3-month result in total is

901 new truck registrations compared to last year during these same months. This indicates steady

growth over the year.

Figure 13: New vehicle registrations Comparisons

Source: Department of Licensing Report 14.

SUBSCRIBING TO THE FUEL AND VEHICLE TRENDS REPORT. The Fuel and Vehicle Trends is available at

this link. From there, you can download the current report in a PDF, look at back issues, or subscribe to a

notification service that lets you know when the next report is available. You may also click this link to

subscribe.

ARTICLES REFERENCED

Transportation Revenue Forecast Council. March 2017 Transportation and Revenue Forecasts.

Fuel Trends:

AAA. http://fuelgaugereport.opisnet.com/WAavg.asp

CME Group. 2017a. Soybean Futures Prices.

The Fuel and Vehicle Trends Report ISSN 1948-2388 April 28, 2017

17

http://www.cmegroup.com/trading/agricultural/grain-and-oilseed/soybean-

oil_quotes_settlements_futures.html

Consensus Economics Inc. April 18, 2017. Energy & Metals Consensus Forecasts.

Energy Information Administration. 2017a. April 2017. Spot Prices for Crude Oil and Petroleum

Products. http://www.eia.gov/dnav/pet/pet_pri_spt_s1_d.htm

Energy Information Administration. 2017b. April 11, 2017. Short-Term Energy Outlook.

http://www.eia.doe.gov/emeu/steo/pub/contents.html

Energy Information Administration. 2017c. April 14, 2017. Weekly Petroleum Status Report.

http://www.eia.gov/petroleum/supply/weekly/

Energy Information Administration. 2017d. April 26, 2017. Weekly Retail Gasoline and Diesel

Prices http://www.eia.gov/dnav/pet/pet_pri_gnd_dcus_nus_w.htm

Energy Information Administration. 2017e. April 2017. Summer Fuels Outlook

https://www.eia.gov/outlooks/steo/special/summer/2017_summer_fuels.pdf

IHS Global Insight. 2017. April, 2017. U.S. Economy – Models and Databanks

Vehicle trends:

Washington State Department of Licensing. September, October and November 2016. State of

Washington Vehicle Registration Reports 7 and 14.

Washington State Department of Licensing. November 2016. Balance Forward Reports.