1

2005 guidance update & 2006 targets

December 16, 2005

Robert McFarlaneEVP & Chief Financial Officer

2 all dollars in C$ unless otherwise specified

forward-looking statementsThis presentation and answers to questions contain forward-looking statements that require assumptions about expected future events including competition, financing, financial and operating results and targets that are subject to inherent risks and uncertainties. There is significant risk that predictions and other forward looking statements will not prove to be accurate.

Factors that could cause actual results to differ materially include but are not limited to: economic growth; competition; financing and debt requirements (including share repurchases); tax matters; human resources (including the ongoing impact of introducing the new collective agreement and return to work on operating expenses, customer service and revenue); business integrations; pension performance, funding and expenses; technology (including reliance on systems and information technology); regulatory developments; process risks (including conversion of legacy systems); health and safety; litigation; business continuity events (including man-made and natural threats); and other risk factors discussed herein and listed from time to time in TELUS’ reports.

For additional information on potential risk factors and assumptions, see TELUS’ 2004 Annual Report, updates in 2005 quarterly interim reports and other filings with securities commissions in Canada and the United States.

3

2005 guidance update

Recent developments

2006 targets

2006 priorities

Summary

Questions and answers

Agenda

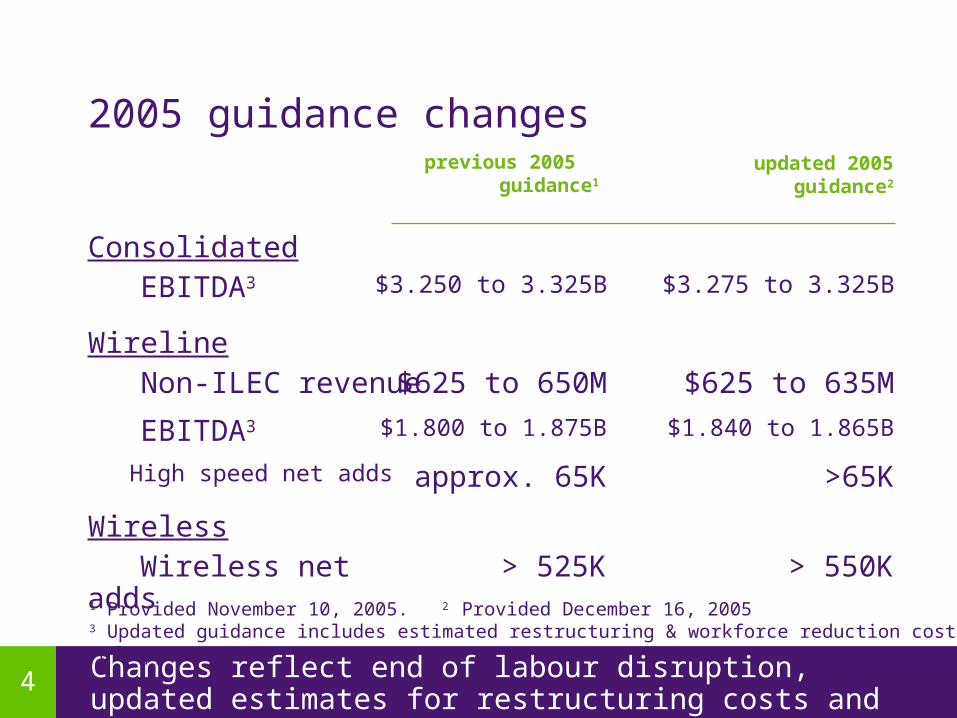

4Changes reflect end of labour disruption, updated estimates for restructuring costs and continued strong wireless growth

2005 guidance changes

1 Provided November 10, 2005. 2 Provided December 16, 20053 Updated guidance includes estimated restructuring & workforce reduction costs of approx. $50M

Wireless

$625 to 650M Non-ILEC revenue

updated 2005 guidance2

Wireline

EBITDA3

previous 2005 guidance1

$3.250 to 3.325B

$625 to 635M

$3.275 to 3.325BConsolidated

> 525K Wireless net adds > 550K

approx. 65K High speed net adds >65K

$1.800 to 1.875B EBITDA3 $1.840 to 1.865B

5 2005 wireless performance well ahead of original targets

2005 wireless guidance summary

1 Provided December 17, 20042 Provided December 16, 2005

425 to 475KWireless Net Adds

$350 to 400MCapex

updated 2005 guidance2

EBITDA

Revenue

original 2005 targets1

$1.35 to $1.40B

$3.2 to $3.25B

>550K

approx. $400M

$1.425 to $1.450B

$3.275 to 3.3B

On track

6Strong execution against original 2005 targets shows resilience of TELUS wireline business

2005 wireline guidance summary

1 Provided December 17, 20042 Provided December 16, 20053 Original target Included restructuring & workforce reduction costs of approx. $100M, vs. approx. $50M for updated guidance

$0 to $10MNon-ILEC EBITDA

$1.85 to $1.90BEBITDA3

updated 2005 guidance2

Non-ILEC Revenue

Revenue

original 2005 targets1

$600 to $650M

$4.7 to $4.75B

Capex

High-Speed Net Adds

$950M to $1.0B

approx. 100K

$15 to 20M

$1.84 to $1.865B

$625 to 635M

$4.825 to $4.85B

approx. $900M

>65K

~

On track

72005 outlook ahead of original targets reflecting continued operating strength in spite of 4 month labour disruption

2005 consolidated guidance summary

1 Provided on December 17, 20042 Updated or reaffirmed December 16, 20053 Original target included restructuring & workforce reduction costs of approx. $100M, vs. approx. $50M for updated guidance

$1.2 to 1.3BFree Cash Flow

$1.3 to 1.4BCapex

$1.65 to 1.85EPS

updated 2005 guidance2

EBITDA3

Revenue

original 2005 targets1

$3.2 to 3.3B

$7.9 to 8.0B

$1.4 to 1.5B

approx. $1.3B

$1.90 to 2.00

$3.275 to 3.325B

$8.1 to 8.15B

On track

8

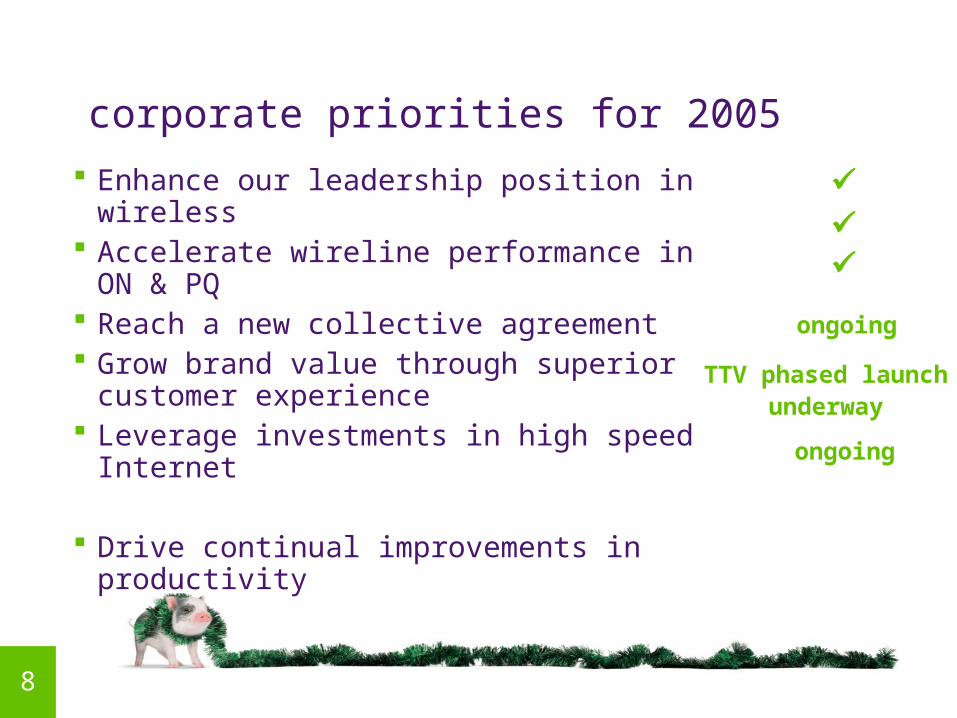

corporate priorities for 2005

Enhance our leadership position in wireless Accelerate wireline performance in ON & PQ Reach a new collective agreement Grow brand value through superior customer

experience Leverage investments in high speed Internet

Drive continual improvements in productivity

TTV phased launch underway

ongoing

ongoing

9

Wireless-wireline merger rationale

Separate wireless and wireline reporting to continue

Advance our industry leading strategy Achieve meaningful commercial differentiation in the market Capitalize technology convergence of wireless and wireline Drive continued operating efficiency and effectiveness

One team, united behind one strategy, defined by one brand

recent developments

10

TELUS executive leadership team structure

DARREN ENTWISTLE

President & CEO

KAREN RADFORD

EVP & President Partner

Solutions & TELUS Quebec

JOE NATALEEVP &

President Business Solutions

JOHN WATSON

EVP & President

Consumer Solutions

EROSSPADOTTO

EVP Technology

Strategy

JANETYALEEVP

Corporate Affairs

KEVIN SALVADORI

EVPBusiness

Transformation & CIO

JOE GRECH

EVP Network

Planning & Operations

ROBERT MCFARLANE

EVP & Chief

Financial Officer

JUDY SHUTTLEWORTH

EVP Human

Resources

TELUS Mobility merged into customer facing structure

2006 targets

12

3.1% GDP growth consistent with Conference Board of Cda

Increased competitive activity from cable-TV, VoIP players

Wireless industry penetration growth similar to 2005

Assume price cap regulatory regime extended for all of 2006

$100M of restr. & workforce reduction costs (~$50M in 2005)

Pension expense increase of ~$40M in 2006 (Discount rate 5.25% vs. 6.0% in 2005)

2006 target considerations (1 of 2)

13

Effective tax rate of approximately 35%

Avg. shares outstanding of 340 to 350M shares depending on NCIB and option exercises

new Normal Course Issuer Bid (NCIB) announced today

Review of tax position indicates cash tax payments expected to be deferred to 2008, from 2007

2006 target considerations (2 of 2)

14

2006 wireless revenue target ($B)

Wireless revenue growth of 15 to 16% driven by continued subscriber & ARPU growth

2005E1 2006E

~3.288

3.775 to 3.825

1 Midpoint of 2005 guidance

15

2006 wireless subscriber net additions target

Wireless net adds expected to remain strong at >550K

2005E 2006E

>4.49M

>5.04M

>550K net adds>550K net

adds

16

2006 wireless EBITDA target ($B)

EBITDA growth of 18 to 22% driven by strong revenue growth and disciplined cost containment

2005E1 2006E

~1.438

1.70 to 1.75

1 Midpoint of 2005 guidance

17

2006 wireless capex target

Wireless capex intensity at best in class 12% level leading to continued strong growth in simple cash flow

approx. $450Mapprox. $400MCapex

$3.775 to 3.825BRevenue $3.275 to 3.30B

approx. 12%Capex intensity approx. 12%

2006E2005E

18

wireless cash flow yield trend

~12%~12%Capex intensity

45 to 46%EBITDA margin1 ~44%

33 to 34%Cash flow yield ~32%

2006E2004 2005E

Strong margins and low capex intensity driving continued premium cash flow yield in 2006

12.5%

40.3%

27.8%

1 based on total revenue

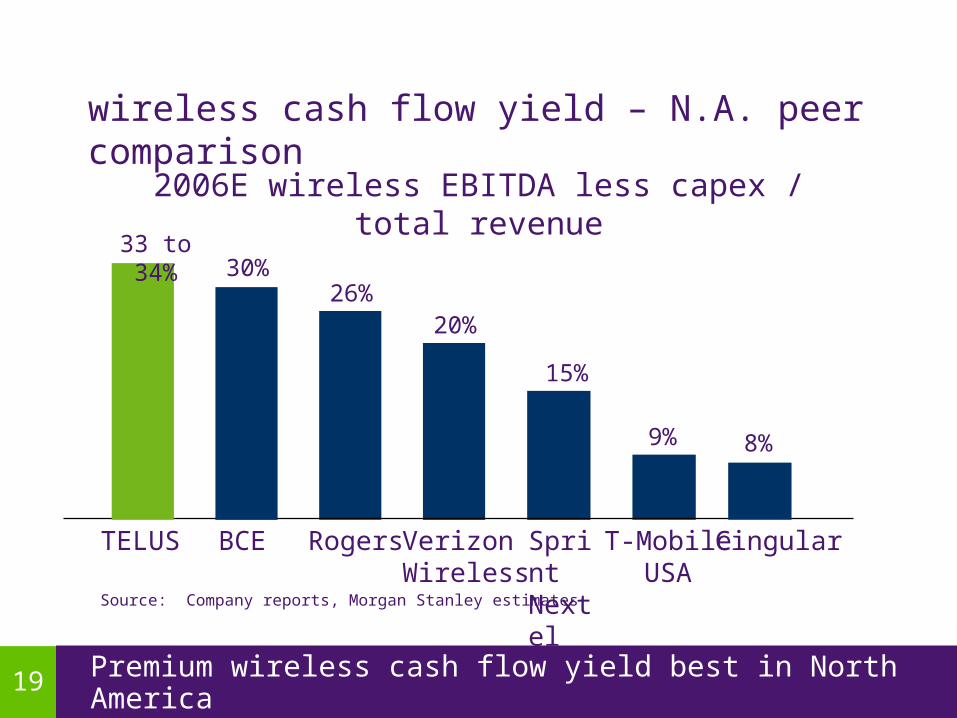

19

Source: Company reports, Morgan Stanley estimates

TELUS Verizon Wireless

T-MobileUSA

wireless cash flow yield – N.A. peer comparison

2006E wireless EBITDA less capex / total revenue

CingularBCE Rogers Sprint Nextel

33 to 34%30%

26%20%

15%

9% 8%

Premium wireless cash flow yield best in North America

20 Wireless expected to represent 49% and 63% of consolidated EBITDA and cash flow

profitability profile - wireless as % of consolidated

EBITDA less capex 2006E

$2.0 to $2.05B

wireline37%

wireless63%

EBITDA 2006E

$3.5 to 3.6B

wireline51%

wireless49%

21

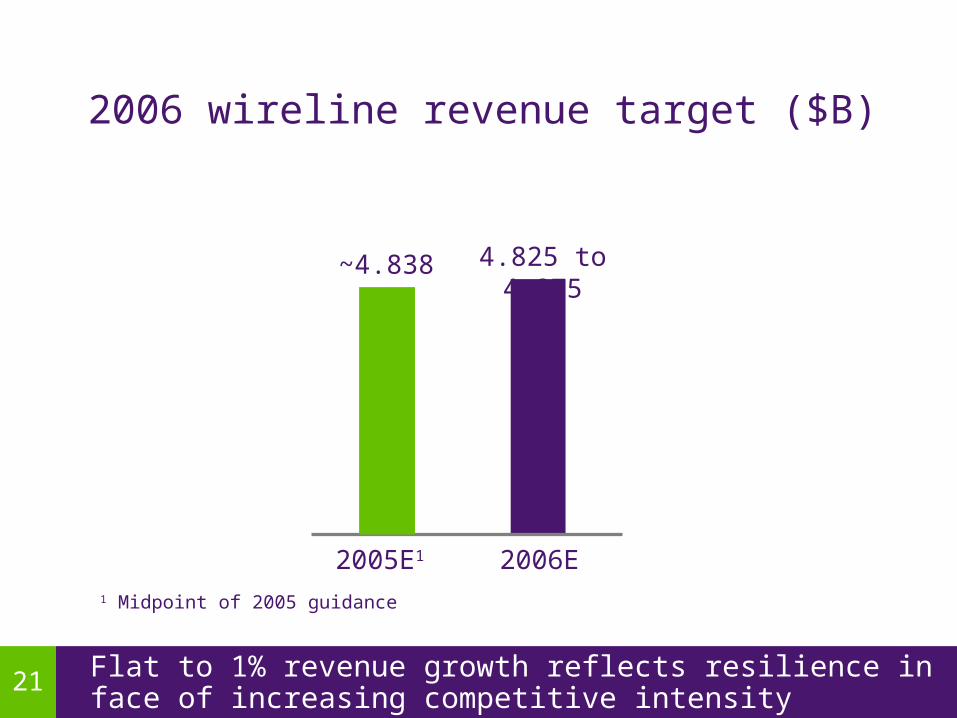

2006 wireline revenue target ($B)

Flat to 1% revenue growth reflects resilience in face of increasing competitive intensity

2005E1 2006E

~4.838 4.825 to 4.875

1 Midpoint of 2005 guidance

22

2006 wireline EBITDA target ($B)

Wireline EBITDA (before restructuring) flat to up $50M

2005E1 2006E2

~1.9031.9 to 1.95

2005E1 2006E2

~1.853 1.8 to 1.85

wireline EBITDA after restructuring

wireline EBITDA before restructuring

1 Midpoint of 2005 guidance. Restructuring & workforce reduction costs of approx. $50M in 20052 Restructuring & workforce reduction costs of approx. $100M in 2006

23

2006 non-ILEC wireline revenue & EBITDA target

Continued focus on profitable, long term growth in C. Canada

2005E1 2006E

~630

650 to 700

2005E1 2006E

~1825 to 40

EBITDA ($M)Revenue ($M)

1 Midpoint of 2005 guidance

24

2006 high-speed Internet subscriber target

>100K target reflects regaining fair share of net adds in maturing market

2005E 2006E

>755K

>855K

>100K net adds>65K net adds

25

2006 wireline capex target ($B)

2006 capex reflects catch-up on deferred capex from 2005

2005E 2006E

1.05 to 1.1~0.9

26

2006 revenue & EBITDA targets

6 to 7% revenue & 6 to 9% EBITDA growth driven by wireless

2005E1 2006E

~8.18.6 to 8.7

TELUS Consolidated

EBITDA ($B)Revenue ($B)

2004

7.6

2005E1 2006E

~3.33.5 to 3.6

2004

3.1

1 Midpoint of 2005 guidance

2003

7.1

2003

2.8

27

EPS target ($)

Earnings growth of 23 to 33% driven by operating profitability growth & lower financing costs

2005E1 2006E

~1.95

2.40 to 2.60

TELUS Consolidated

2004

1.58

1 Midpoint of 2005 guidance

2003

0.92

28

2006 EPS continuity

Normalized EPS growth of 17 to 27%

2005E1 2006E

32 to 50¢

$2.40 to 2.60

TELUS Consolidated

~$2.05~$1.95

17¢

non-recurring

9¢

21¢

9¢7¢

0 to 7¢

2005E normal.

redemption & litigation

tax

1 Midpoint of 2005 guidance.

~22¢

labourdisrup.

EBITDA Growth

interest expense

restruct.costs

otherpensionexpense

29

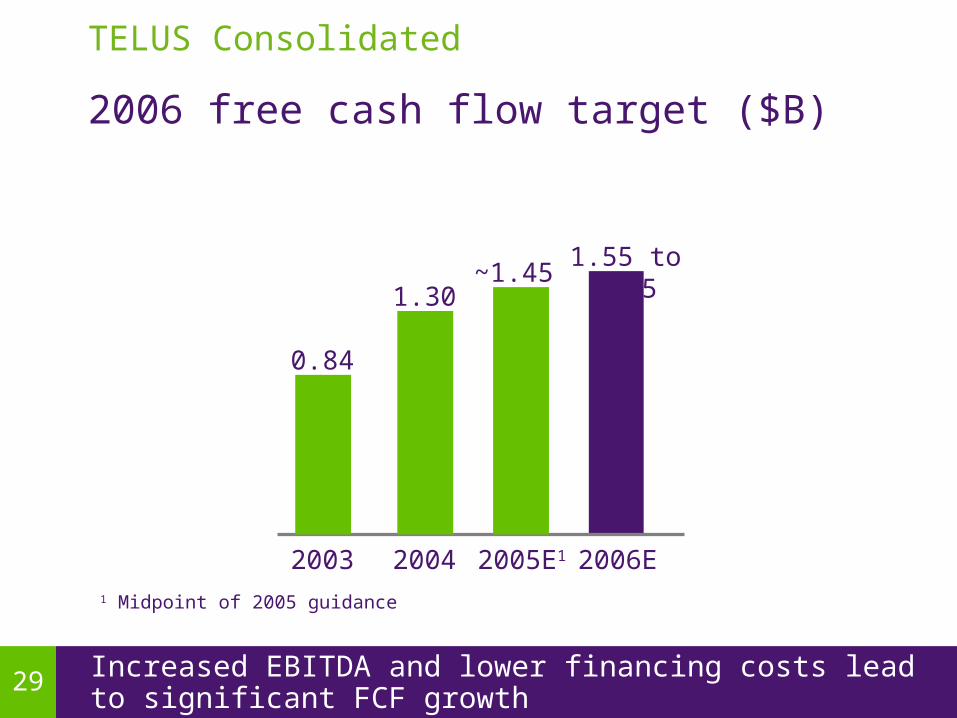

2006 free cash flow target ($B)

Increased EBITDA and lower financing costs lead to significant FCF growth

TELUS Consolidated

2005E1 2006E

~1.451.55 to 1.65

2004

1.30

1 Midpoint of 2005 guidance

2003

0.84

30 2006 targets build upon track record of outstanding growth

2006 consolidated targets summary

1Including restructuring & workforce reduction costs of approx. $50M in 2005 and $100M in 2006

$1.55 to 1.65BFree Cash Flow

$1.50 to 1.55BCapex

$2.40 to 2.60EPS

change

EBITDA1

Revenue

2006 targets

$3.5 to 3.6B

$8.6 to 8.7B

TELUS consolidated

7 to 14%

15 to 19%

23 to 33%

6 to 9%

6 to 7%

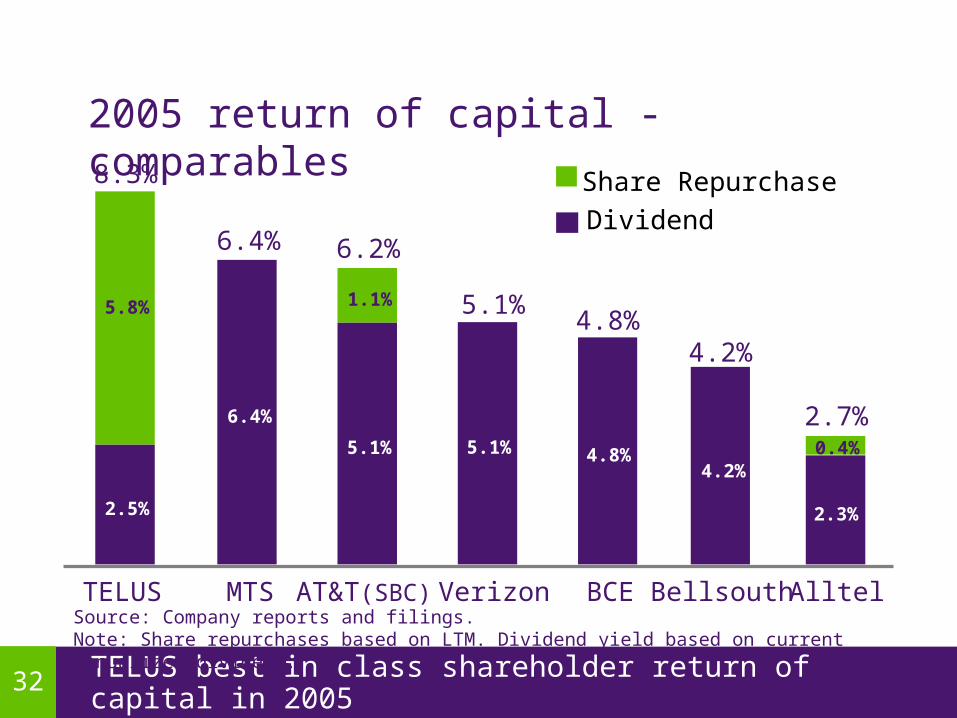

31 Repurchased 84% of shares permitted under current NCIB

return of capital - share buy back update

No. of Shares

Repurchased

No. of Shares

Repurchased

Total

Authorized

%

Repurchased

vs. Auth. Since

Inception

Common 1.8M 10.2M 14.0M 73%

Non-Voting 1.8M 11.3M 11.5M 98%

Total 3.6M 21.5M 25.5M 84%

Total cost $159M $901M

TELUS consolidated

Q4-051 Since inception

1 Repurchases up to and including December 15, 2005

32

2.5%

6.4%

5.1% 5.1% 4.8%

2.3%

5.8% 1.1%

0.4%

TELUS MTS AT&T(SBC) Verizon BCE Alltel

2005 return of capital - comparables

TELUS best in class shareholder return of capital in 2005

Dividend

Share Repurchase

Source: Company reports and filings. Note: Share repurchases based on LTM. Dividend yield based on current annualized dividend.

8.3%

6.4% 6.2%

5.1%4.8%

2.7%

Bellsouth

4.2%

4.2%

33

Completed $1.6B early debt redemption on Dec. 1, 2005

Announced in November 38% quarterly dividend increase to 27.5 cents per share, for Jan. 1, 2006 payment

Consistent with dividend payout ratio guideline of 45 to 55% of sustainable net earnings

New 24 million share NCIB effective Dec. 20, 2005

Authorized to repurchase up to 12M common and 12M non-voting (up to 7.1% of total shares outstanding)

return of capital summary

TELUS has strong track record for returning capital to investors

TELUS Consolidated

34

Advance TELUS’ leadership position in the Consumer, Business and Wholesale markets

Drive improvements in productivity and service excellence

Strengthen the spirit of the TELUS team and the brand

Develop the best talent in global communications industry

Key priorities for 2006

Focused on executing our growth strategy

35

Summary 2005 outlook revised for non-ILEC revenue, wireline and

Consolidated EBITDA, and increased high speed Internet and wireless net additions

2006 targets consistent with TELUS growth model

2006 targets reflect: Strong revenue growth EBITDA growth driven by Mobility Significant EPS growth driven by strong EBITDA growth,

and lower financing and tax costs Significant FCF generation Continued subscriber growth

37

appendix

38

EBITDA: Earnings, after restructuring and workforce reduction costs, before interest, taxes, depreciation and amortization

Capital intensity: capex divided by total revenue

Cash flow: EBITDA less capex

Free Cash Flow: EBITDA, adding Restructuring and workforce reduction costs, cash interest received and excess of share compensation expense over share compensation payments, subtracting cash interest paid, cash taxes, capital expenditures, and cash restructuring payments

definitions

appendix

TELUS definitions for non-GAAP measures

39

$1,550 to 1,650

~(500)

(1,500 to 1,550)

$3,500 to 3,600

2006E

Free Cash Flow

Net Cash Interest

Capex

EBITDA

($M)

50 to 100Other1:

free cash flow

TELUS consolidated

Continued strong free cash flow generation

1 Restructuring expense (net of cash payments), non-cash share based compensation, & net cash tax recoveries