1

Chapter 2Chapter 2An Overview of the Financial System

Eco 2154 PPP #1

2

An Overview of the Financial System

Primary Function of the Financial System is Financial Intermediation

The channeling of funds from households, firms and governments who have surplus funds (savers) to those who have a shortage of funds (borrowers).

3

An Overview of the Financial System

Financial Assets/Instruments flow in the opposite direction to funds

4

In Direct Financing, those in needs of funds seek those with surplus funds. In this case, there is no big fee paid to the third party for financial intermediation.

Then, why most of financing needs of the Corporate are met with Indirect Financing?

5

Puzzle 1

• Direct Finance is insignificant compared to Indirect Finance.

• Financial Intermediaries buy most of Marketable Securities

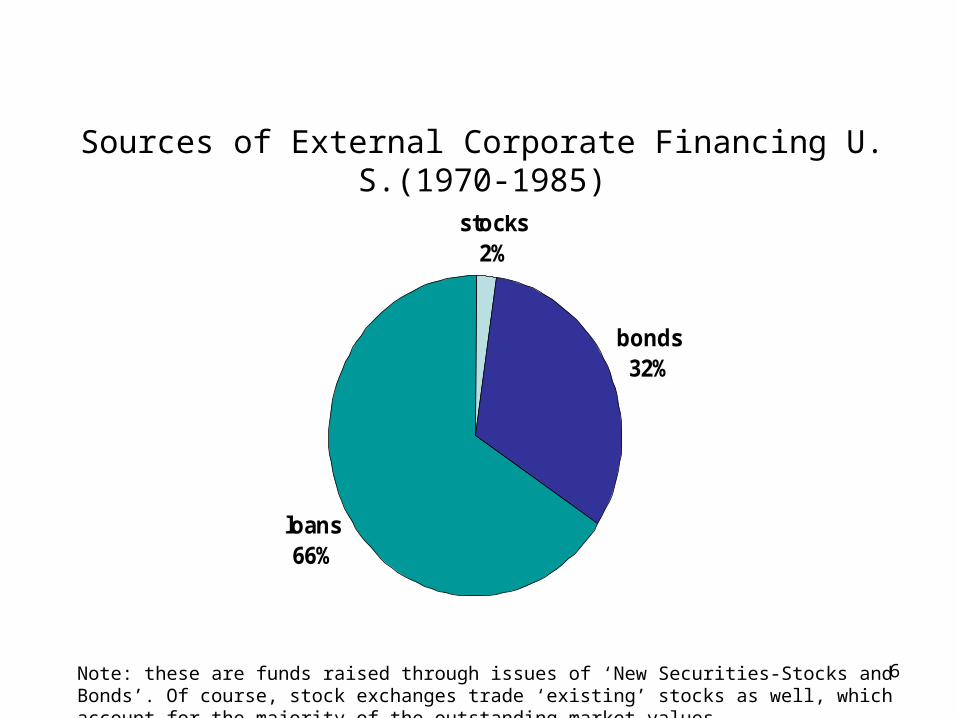

6

Sources of External Corporate Financing U. S.(1970-1985)

stocks2%

bonds32%

loans66%

Note: these are funds raised through issues of ‘New Securities-Stocks and Bonds’. Of course, stock exchanges trade ‘existing’ stocks as well, which account for the majority of the outstanding market values.

7

Puzzle 2:

Stocks or Equities are relatively unimportant

compared with Debt Contracts/Instruments(= Bonds + Loans)

8

Puzzle 3:

Marketable Securities(=Bonds + Stocks) are not so important as Bank Loans

9

Answers to All these Puzzles• Transactions Costs

: Financial Institutions or Intermediaries lower Transactions Cost

• Information Asymmetry

: Some financial instruments have more severe problems of Information Asymmetry than others

- Equities > Bonds > Bank Loans• Capital Structure (Comparative Cost of Funding)

: - interest payment is tax-deductible

- real cost of borrowing is the (actual) real interest rate (=nominal interest rate – inflation rate)

• Issues of Management Control and a Possible Hostile Take Over

10

Function of Financial Intermediaries

Financial Intermediaries• Engage in process of indirect finance

• Are needed i) to reduce transactions costs, ii) to solve asymmetric information problem, and iii) to reduce market risks of portfolio.

11

Function of Financial Intermediaries (Cont’d)

First, Transactions Costs1. Financial intermediaries make profits by

reducing transactions costs.

2. They reduce transactions costs by developing expertise and taking advantage of economies of scale.

12

Second, Asymmetric Information

Adverse Selection• Before transaction occurs• Potential borrowers most likely to produce

adverse outcomes are ones most likely to seek loans and be selected

13

Asymmetric Information (Cont’d)

Moral Hazard• After transaction occurs• Hazard that borrower has incentives to

engage in undesirable activities making it more likely that loan won’t be paid back

14

Third, Further Reduction of Portfolio Risk

• Create and sell assets with low risk characteristics and then use the funds to buy assets with more risk (also called asset transformation)

• Lower risk by helping people to diversify portfolios

15

Financial Intermediaries

16

And their Sizes

17

Issue

In Canada, they used to be called “Four Pillars”.

Now they are moving towards “Full Service”.

18

Classifications of Financial Markets

1) Money Market Short-term Debt Market(maturity < 1 year)

2) Capital Market

Long-term (maturity > 10 year)

• Medium-term (maturity >1 and < 10 years)

19

Classifications of Financial Markets

3) Equity Markets - Common stocks

• Primary Market - New security issues sold to initial buyers

• Secondary Market - Securities previously issued are bought and sold

3) Commodity Markets

4) Derivative Markets

5) FOREX Markets

20

Classifications of Financial Markets (Cont’d)

**Secondary Markets are either Exchanges,• Trades conducted in central locations

(e.g., Toronto Stock Exchange and New York Stock Exchange), or

Over-the-Counter Markets• Dealers at different locations buy and sell

21

Financial Market Instruments

22

Financial Market Instruments (Cont’d)

Other Money Market Instruments• Certificates of deposit• Repurchase agreements• Overnight funds • Derivatives• Commodity Contracts

23

Financial Market Instruments (Cont’d)

24

Financial Market Instruments (Cont’d)

Other Capital Market Instruments• Canada savings bonds• Provincial and municipal bonds

• Government agencies securities

25

Out of Box

There are many ‘New’ financial instruments.

-Some are hybrid. eg) Money Market Mutual Funds

- Some of them are derived from financial assets.

eg) Asset Backed Securities

26

Regulation of Financial Markets

Primary Reasons for Regulation1. Increase information to investors

- Decreases adverse selection and moral hazard problems

- Securities commissions force corporations to disclose information

27

Regulation of Financial Markets (Cont’d)

Primary Reasons for Regulation (continued)

2. Ensuring the soundness of intermediaries- Prevents financial panics- Restrictions on entry/assets/activities, disclosure,

deposit insurance, limits on competition

28

Regulation of Canadian Financial System