1

Expanding Borders:

Inclusive Finance at

BancoEstado in

ChileJosé Manuel Mena V.

C.E.O.

Access to Finance: Building an Inclusive Financial

SystemThe Brookings Institution/ World Bank Washington DC, May 30-

31, 2006

BancoEstado

2

I. BancoEstado highlightsHistory and future outlook

• Founded in 1953, with origins going back 150 years• Total assets US$ 20.5 billion

Role / aims

• To improve the quality of people’s lives by expanding access to finance

• To promote economic and social development

• To be a public commercial bank of excellence and to strengthen competition in the banking sector

3

Our Bank’s Vision and Status

To enhance our economic and social roles while continuing to be competitive, efficient and profitable

• No. 1 in client base: ~8 million (1 out of 2 Chileans)

• No. 3 in loans (13% market share)

• Profitability similar to the industry’s. Contributed an annual average of US$ 100 million to the government treasury in taxes and profits over the last 15 years

• Best international risk rating for a commercial bank in Latin America -- together with Banco Santander

• New positioning in the market and in public opinion

Market positioning

4

II. The challenge of expanding our borders

Inclusive Financing – Basic Principles:

• Market solutions to social challenges: competitive, mass-market products and services

• Bank sustained by its customers: profitable, receives no subsidies

BancoEstado

5

Leader in traditional products• Savings accounts (80% of market)

• Mortgages (2 of every 3 bank mortgages)

• Network of branches (only bank in 41% of localities)

Challenge: mass penetration of products• Retail cross-selling of products

• Microfinancing (details later)

Main requirements for success:• Customer orientation (competitiveness, better service)

• Faster and more efficient operations, lower costs• Remote banking (Internet, Contact Center)

• Automated transactions

BancoEstado

6

0.6%

41%37.3%

21.4%

Branch network

No coverage BancoEstado only

Other banks only

BancoEstado and other banks

Percentage of Localities

7

Automated transactions Automated Transactions (Through December of each year)

Source: BancoEstado

69.064.2

60.8

54.352.152.4

0

2

4

6

8

10

12

14

16

18

2000 2001 2002 2003 2004 2005

Millions month

0

10

20

30

40

50

60

70%

N° of transactions % of total transactions

8

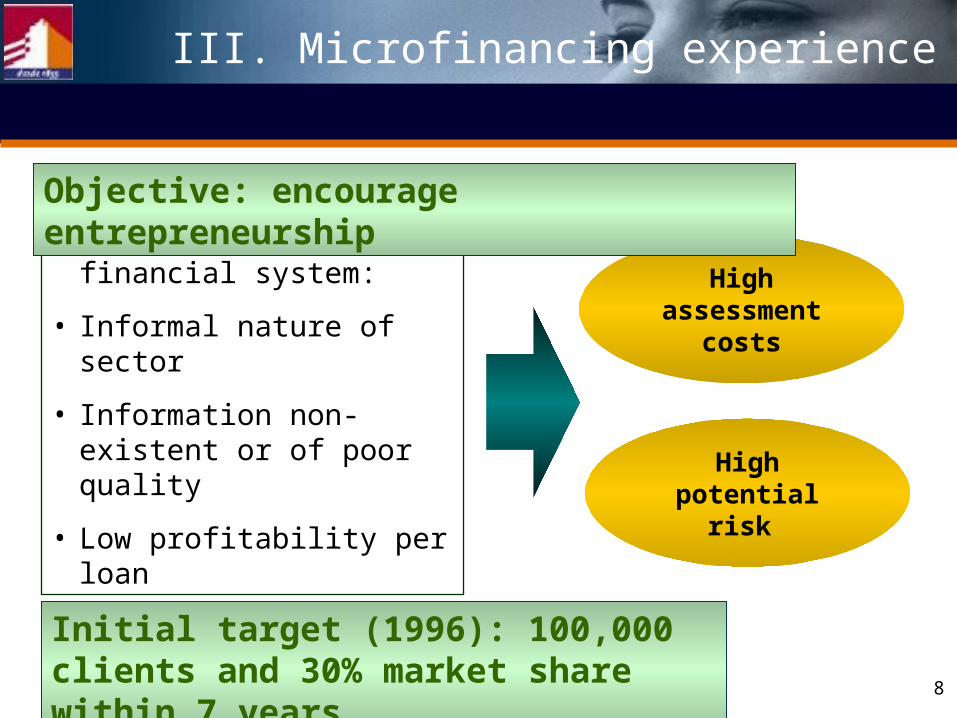

Barriers to accessing financial system:

• Informal nature of sector

• Information non-existent or of poor quality

• Low profitability per loan

High assessment

costs

High potential risk

Initial target (1996): 100,000 clients and 30% market share within 7 years

III. Microfinancing experience

Objective: encourage entrepreneurship

9

• Created a microbusiness subsidiary in 19XX• Commercial design

• Field assessment (credit scoring, no collateral requirements)

• Variety of products / specialized branches• Full service to sector, segmentation of customers

• Technical design• Fully integrated information network• Information management Business intelligence

• Georeferencing system

• Mobile units

Actions / Innovations

11 Internet, red fija,Celular, etc

Optimize field work

12

BancoEstado Micro-Business Loans and Number of Clients

71

124161

272

138

170

90

56

0

50

100

150

200

250

300

2002 2003 2004 2005

US$ millions dec. 2005

0

20

40

60

80

100

120

140

160

180

thousands

Loans No. clients

13

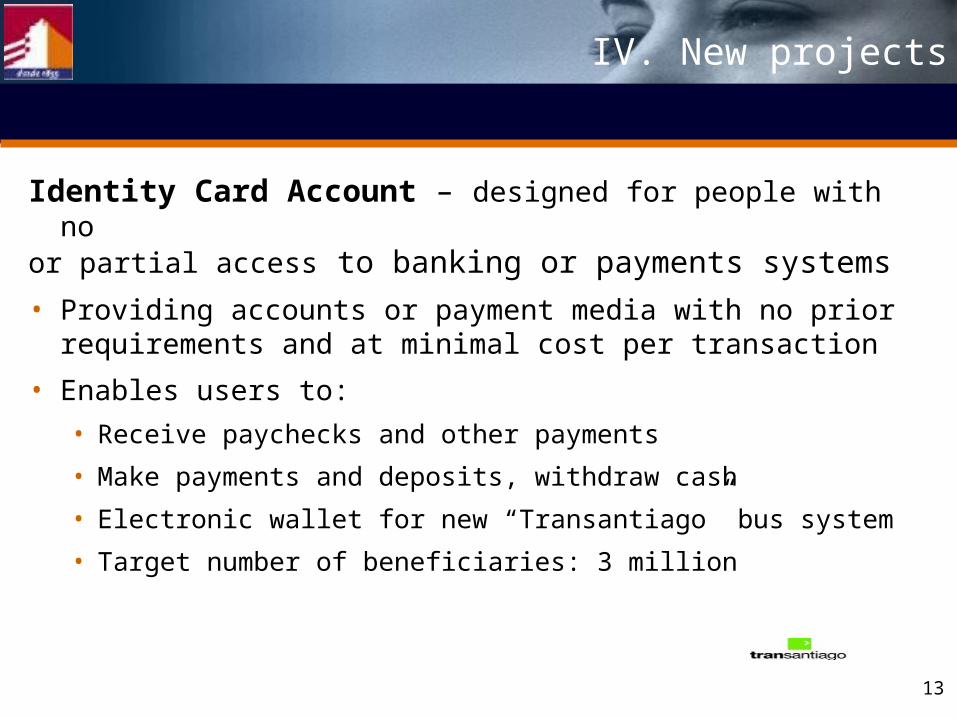

Identity Card Account – designed for people with no

or partial access to banking or payments systems

• Providing accounts or payment media with no prior requirements and at minimal cost per transaction

• Enables users to:

• Receive paychecks and other payments

• Make payments and deposits, withdraw cash

• Electronic wallet for new “Transantiago” bus system

• Target number of beneficiaries: 3 million

IV. New projects

14

Transantiago

Serving people in many daily environments:

A modern, efficient public transport system

15

• Extend distribution network through alternative low cost channels (eg., Lottery Shop / Caixa Economica Federal and Lemmon Bank, both in Brazil)

• Services: transaction and teller facilities at POS terminals (withdrawals, deposits, utility payments)

• 2,500 service points in 270 localities by 2010

• Social benefits

• Beneficiaries: 3 million users

• Transaction cost savings: approx. US$ 400 million

Caja Vecina (Neighborhood teller)

16

Neighborhood teller

Bringing our bank closer to people

17

Expanding Borders:

Inclusive Finance at

BancoEstado in ChileJosé Manuel Mena

V.

C.E.O.

Access to Finance: Building an Inclusive Financial

SystemThe Brookings Institution/World Bank Washington DC, May 30-

31, 2006