1

Preparation of master budget

2

Budget

A budget is a quantitative statement, for a defined period of time, which may include planned revenue, expenses, assets, liabilities and cash flows

3

Purpose of preparing budget

Planning Coordination Communication Motivation Performance evaluation

4

Steps in the preparation of budget

Consideration of all external factors Preparation of other budgets

Production budget, purchases budget, direct labour budget, overheads budget and selling and administrative budget

Negotiation of budget Coordination of budget

Cash budget, capital expenditure budget, budget balance sheet, budget income statement, budget cash flow statement, budget statement of retained earnings

5

Final acceptance of budget Budget review

6

Cash budget

7

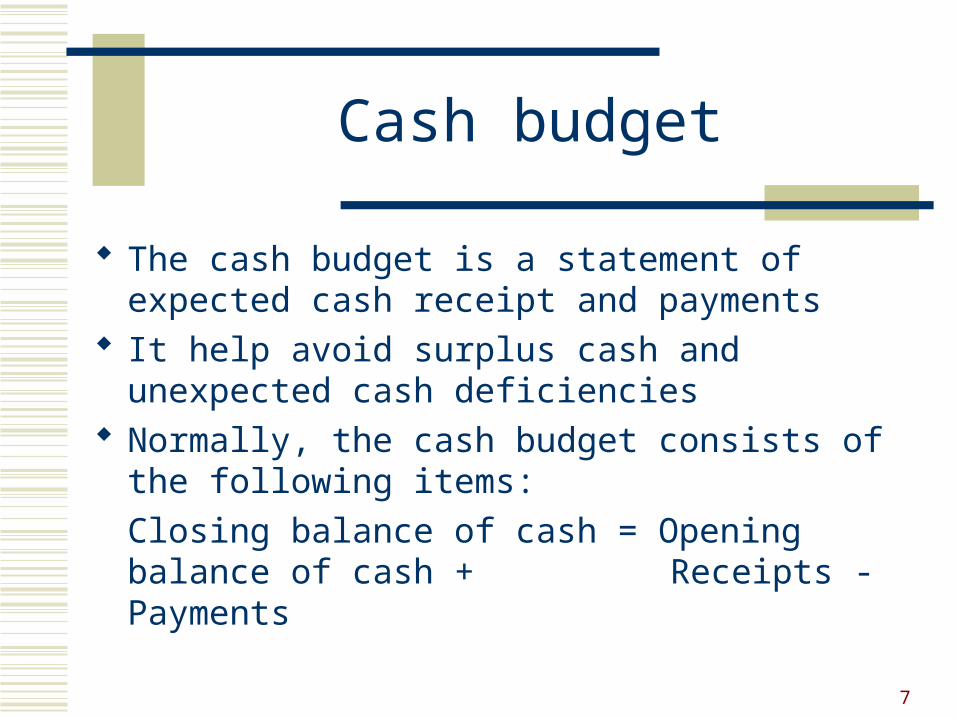

Cash budget

The cash budget is a statement of expected cash receipt and payments

It help avoid surplus cash and unexpected cash deficiencies

Normally, the cash budget consists of the following items:

Closing balance of cash = Opening balance of cash + Receipts - Payments

8

Cash budget Receipts include:

Cash sales Collection from debtors Other incomes such as investment income, rent received

Payments include: Cash purchases Payment to creditors Direct labour Other expenses such as manufacturing overhead, administrative

and selling expenses (depreciation does not involve cash flow) Tax payment

9

Cash budget

In drawing up a cash budget, it can be found that all the payments for units produced would very rarely be at the same as production itself. For instance, the raw materials might be bought in March, goods being produced in April ad paid for in May

Similarly the date of sales and the date of receipt of cash will not usually be at the same time. For instance, the good might be sold in May and the money received in August

10

Example

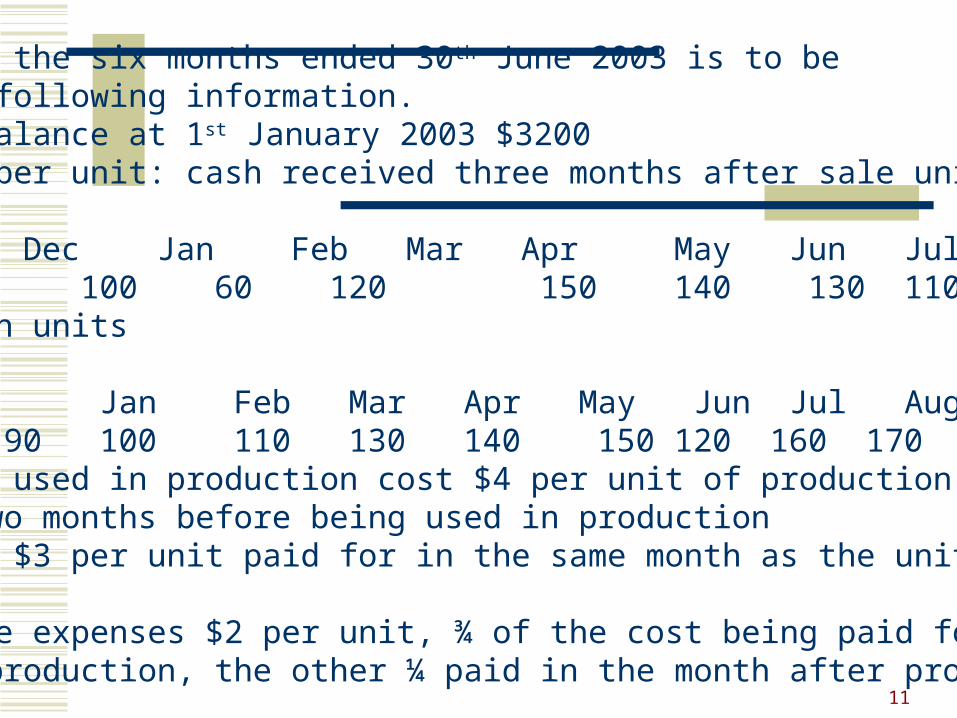

11

A cash budget for the six months ended 30th June 2003 is to be Drafted from the following information.(a) Opening cash balance at 1st January 2003 $3200(b) Sales: at $12 per unit: cash received three months after sale units:

2002 2003Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep 80 90 70 100 60 120 150 140 130 110 100 160

(c) Production: in units2002Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep70 80 90 100 110 130 140 150 120 160 170 180

(d) Raw materials used in production cost $4 per unit of production. They are paid for two months before being used in production

(e) Direct labour: $3 per unit paid for in the same month as the unit is produced.

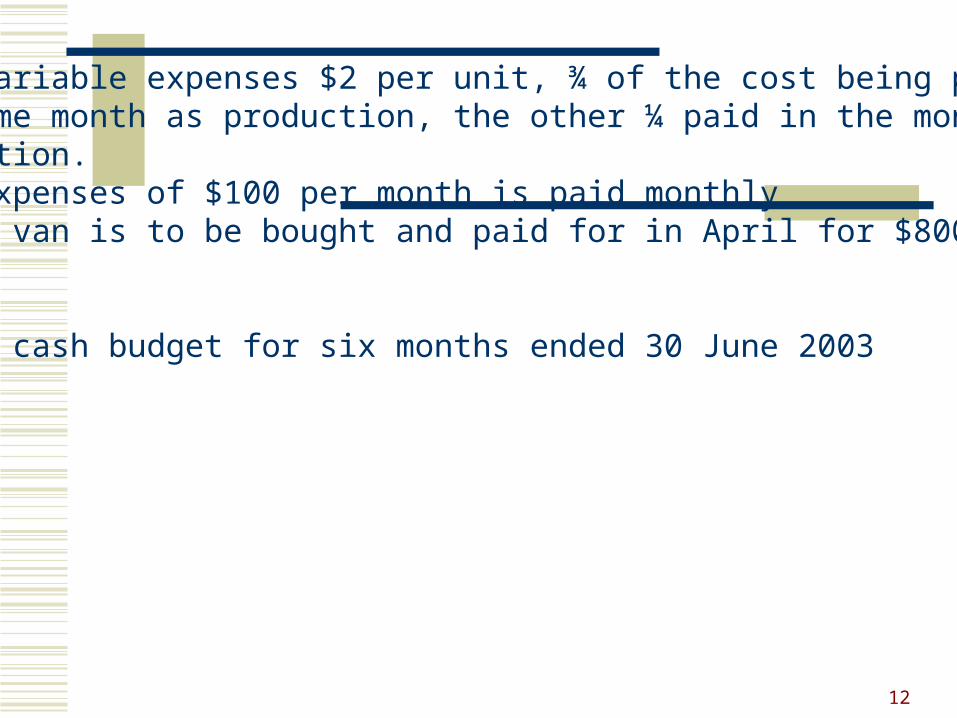

(f) Other variable expenses $2 per unit, ¾ of the cost being paid for in the same month as production, the other ¼ paid in the month after production

12

(f) Other variable expenses $2 per unit, ¾ of the cost being paid for in the same month as production, the other ¼ paid in the month after production.(g) Fixed expenses of $100 per month is paid monthly(h) A motor van is to be bought and paid for in April for $800

Required:Prepare the cash budget for six months ended 30 June 2003

13

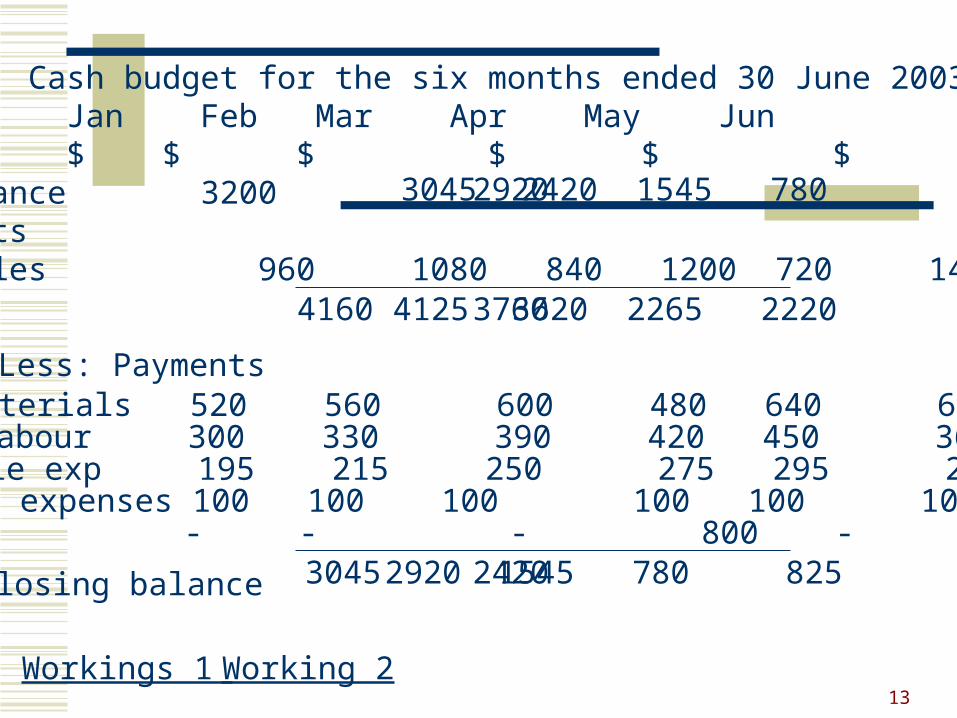

Cash budget for the six months ended 30 June 2003Jan Feb Mar Apr May Jun$ $ $ $ $ $

Opening balance 3200Add: Receipts Sales 960 1080 840 1200 720 1440

4160

Less: PaymentsRaw materials 520 560 600 480 640 680Direct labour 300 330 390 420 450 360 Variable exp 195 215 250 275 295 255Fixed expenses 100 100 100 100 100 100Motor van - - - 800 - -

3045

3045

4125

2920

2920

3760

2420

2420 1545 780

3620 2265 2220

1545 780 825

Workings 1 Working 2

Closing balance

14

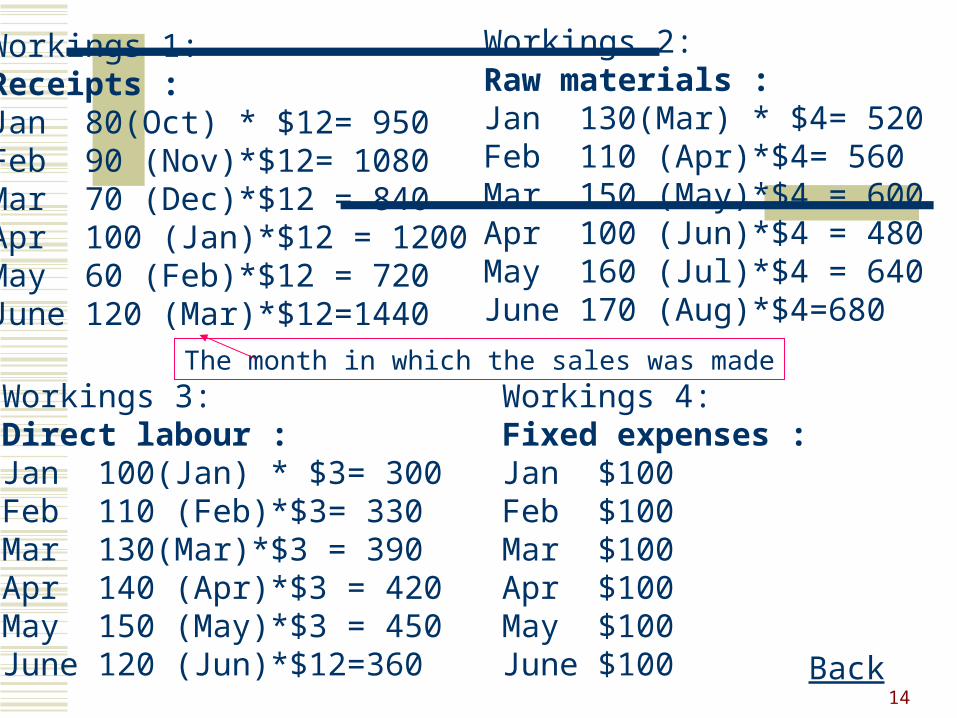

Workings 1:Receipts :Jan 80(Oct) * $12= 950Feb 90 (Nov)*$12= 1080Mar 70 (Dec)*$12 = 840Apr 100 (Jan)*$12 = 1200May 60 (Feb)*$12 = 720June 120 (Mar)*$12=1440

Workings 2:Raw materials :Jan 130(Mar) * $4= 520Feb 110 (Apr)*$4= 560Mar 150 (May)*$4 = 600Apr 100 (Jun)*$4 = 480May 160 (Jul)*$4 = 640June 170 (Aug)*$4=680

Workings 3:Direct labour :Jan 100(Jan) * $3= 300Feb 110 (Feb)*$3= 330Mar 130(Mar)*$3 = 390Apr 140 (Apr)*$3 = 420May 150 (May)*$3 = 450June 120 (Jun)*$12=360

Workings 4:Fixed expenses :Jan $100Feb $100Mar $100Apr $100May $100June $100

The month in which the sales was made

Back

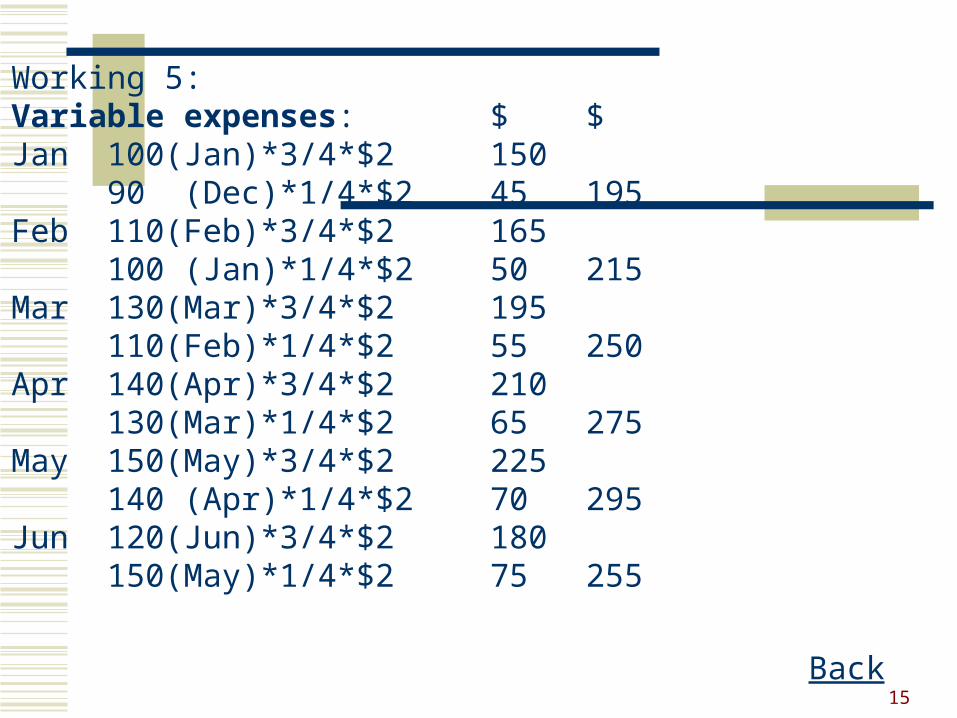

15

Working 5:Variable expenses: $ $Jan 100(Jan)*3/4*$2 150

90 (Dec)*1/4*$2 45 195Feb 110(Feb)*3/4*$2 165

100 (Jan)*1/4*$2 50 215Mar 130(Mar)*3/4*$2 195

110(Feb)*1/4*$2 55 250Apr 140(Apr)*3/4*$2 210

130(Mar)*1/4*$2 65 275May 150(May)*3/4*$2 225

140 (Apr)*1/4*$2 70 295Jun 120(Jun)*3/4*$2 180

150(May)*1/4*$2 75 255

Back

16

Budget income statement and balance sheet

17

Budgeted income statement and balance sheet

These financial statements reflect the predicted results to be achieved.

18

Example

19

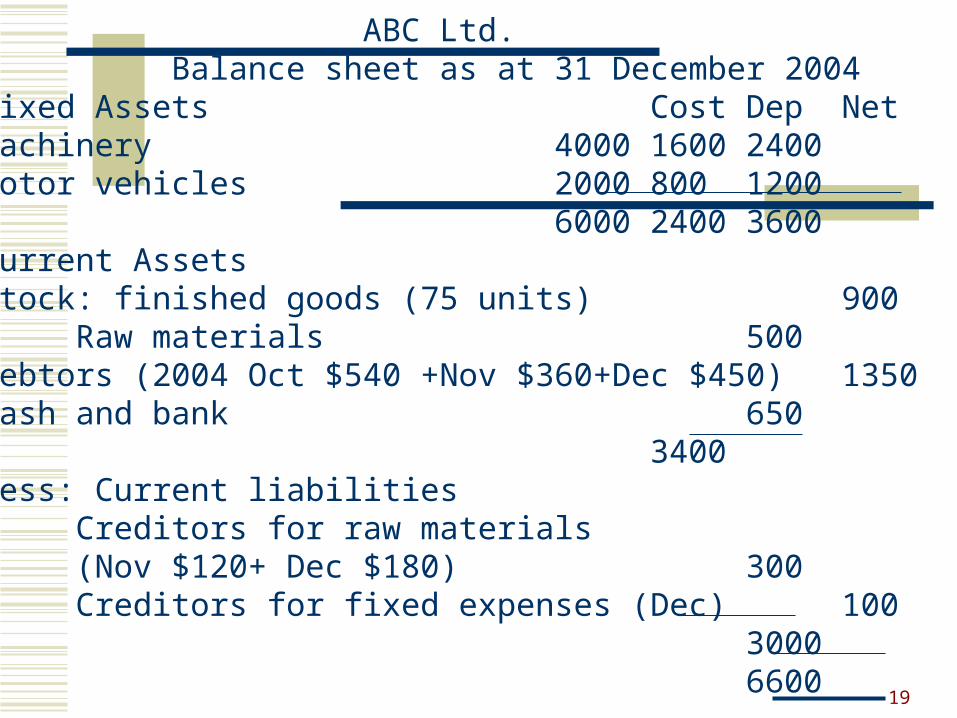

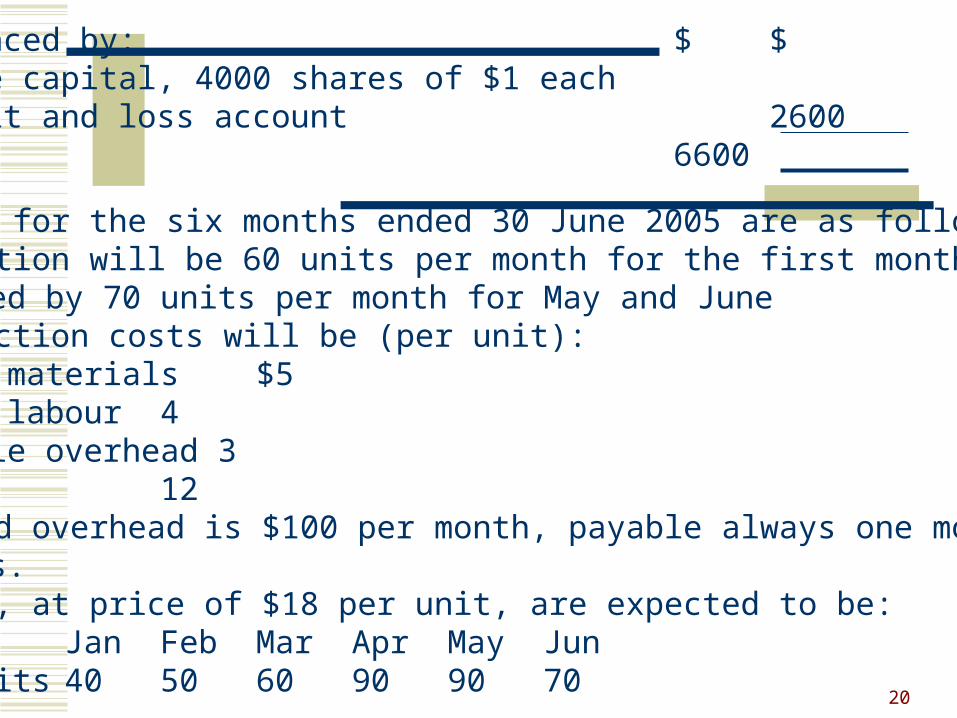

ABC Ltd.Balance sheet as at 31 December 2004

Fixed Assets Cost Dep NetMachinery 4000 1600 2400Motor vehicles 2000 800 1200

6000 2400 3600Current AssetsStock: finished goods (75 units) 900

Raw materials 500Debtors (2004 Oct $540 +Nov $360+Dec $450) 1350Cash and bank 650

3400Less: Current liabilities

Creditors for raw materials (Nov $120+ Dec $180) 300Creditors for fixed expenses (Dec) 100

30006600

20

Financed by: $ $Share capital, 4000 shares of $1 each 4000Profit and loss account 2600

6600

The plans for the six months ended 30 June 2005 are as follows:(i) Production will be 60 units per month for the first months,

followed by 70 units per month for May and June(ii) Production costs will be (per unit):

Direct materials $5Direct labour 4Variable overhead 3

12(iii) Fixed overhead is $100 per month, payable always one month in

arrears.(iv) Sales, at price of $18 per unit, are expected to be:

Jan Feb Mar Apr May Junno. of units40 50 60 90 90 70

21

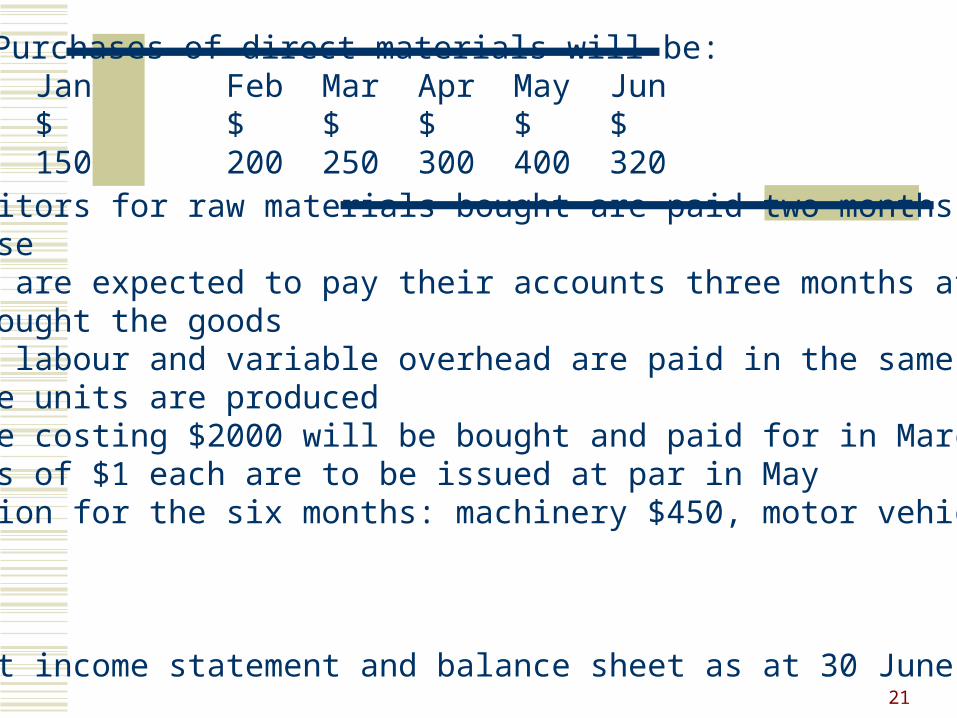

(v) Purchases of direct materials will be:Jan Feb Mar Apr May Jun$ $ $ $ $ $150 200 250 300 400 320

(vi) The creditors for raw materials bought are paid two months after purchase(vii) Debtors are expected to pay their accounts three months after they have bought the goods(viii) Direct labour and variable overhead are paid in the same month as the units are produced(ix) A machine costing $2000 will be bought and paid for in March(x) 3000 shares of $1 each are to be issued at par in May(xi) Depreciation for the six months: machinery $450, motor vehicles

$200

Required:Prepare budget income statement and balance sheet as at 30 June 2005

22

Budget income statement

23

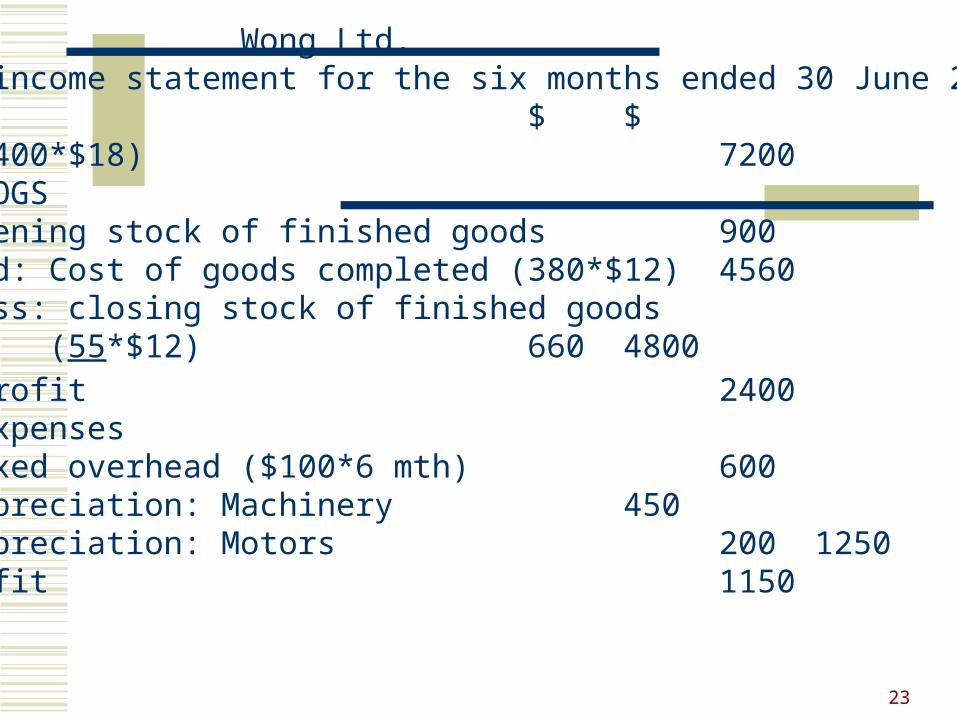

Wong Ltd.Budget income statement for the six months ended 30 June 2005

$ $Sales (400*$18) 7200Less: COGS

Opening stock of finished goods 900Add: Cost of goods completed (380*$12) 4560Less: closing stock of finished goods

(55*$12) 660 4800Gross profit 2400Less: expenses

Fixed overhead ($100*6 mth) 600Depreciation: Machinery 450Depreciation: Motors 200 1250

Net profit 1150

24

Wong Ltd.Budget balance sheet as at 30 June 2005

Fixed asssets Cost Dep Net$ $ $

Machinery 6000 2050 3950Motor vehicles 2000 1000 1000

8000 3050 4950Current assetsStock: finished goods 660

raw materials 220Debtors 4500Cash and bank 1240

6620Less: Current liabilities

Trade creditors 720Creditors for overheads 100 5800

10750

25

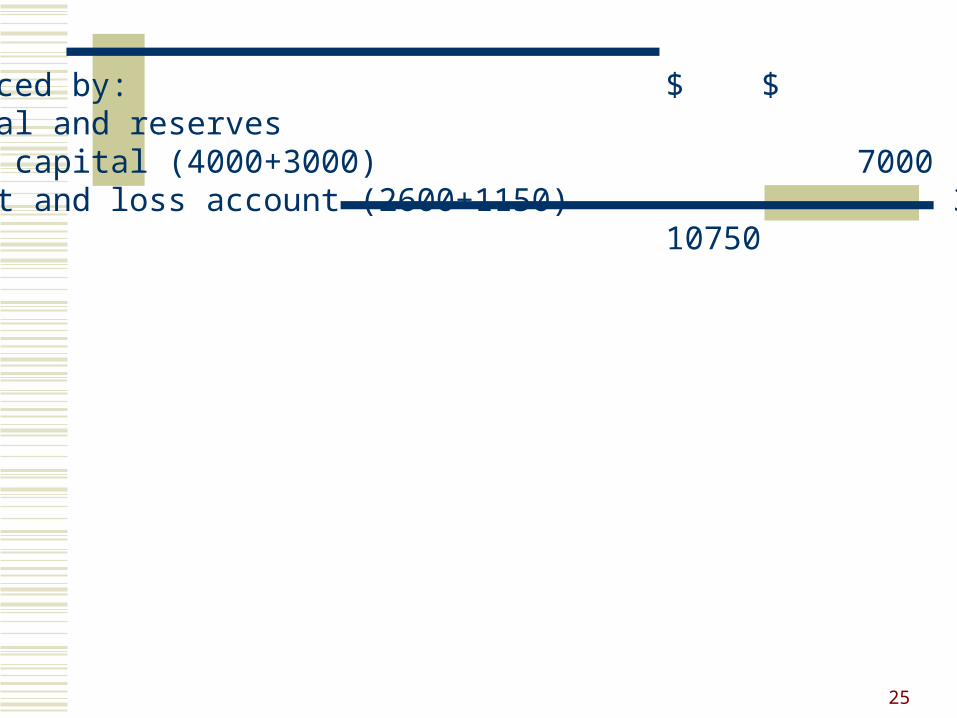

Financed by: $ $Capital and reservesShare capital (4000+3000) 7000Profit and loss account (2600+1150) 3750

10750

26

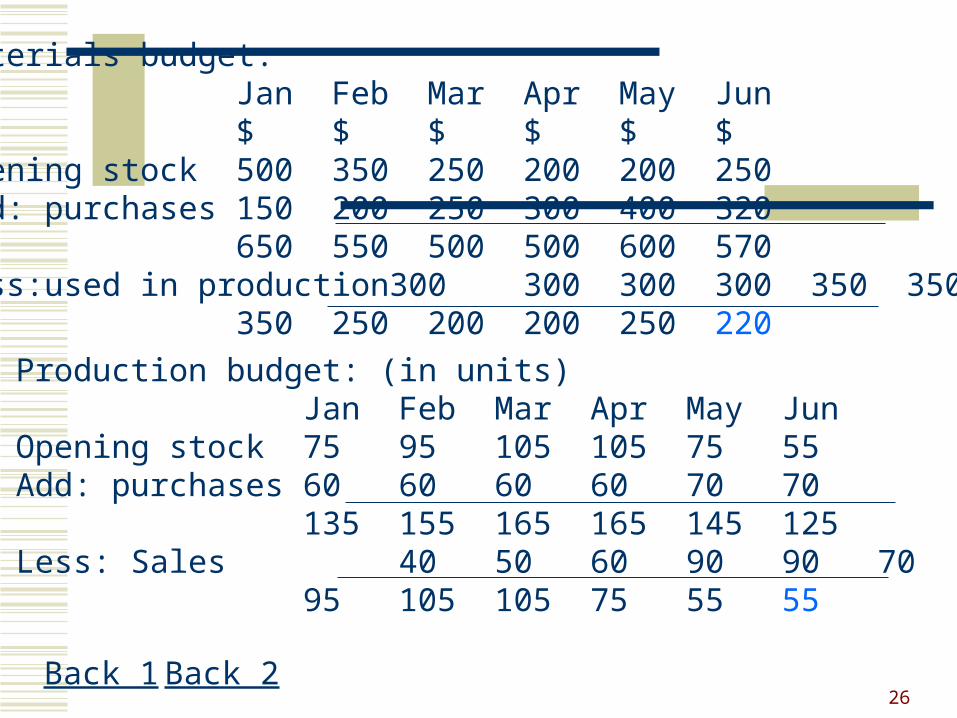

Materials budget:Jan Feb Mar Apr May Jun$ $ $ $ $ $

Opening stock 500 350 250 200 200 250Add: purchases 150 200 250 300 400 320

650 550 500 500 600 570Less:used in production300 300 300 300 350 350

350 250 200 200 250 220

Production budget: (in units)Jan Feb Mar Apr May Jun

Opening stock 75 95 105 105 75 55Add: purchases 60 60 60 60 70 70

135 155 165 165 145 125Less: Sales 40 50 60 90 90 70

95 105 105 75 55 55

Back 1 Back 2

27

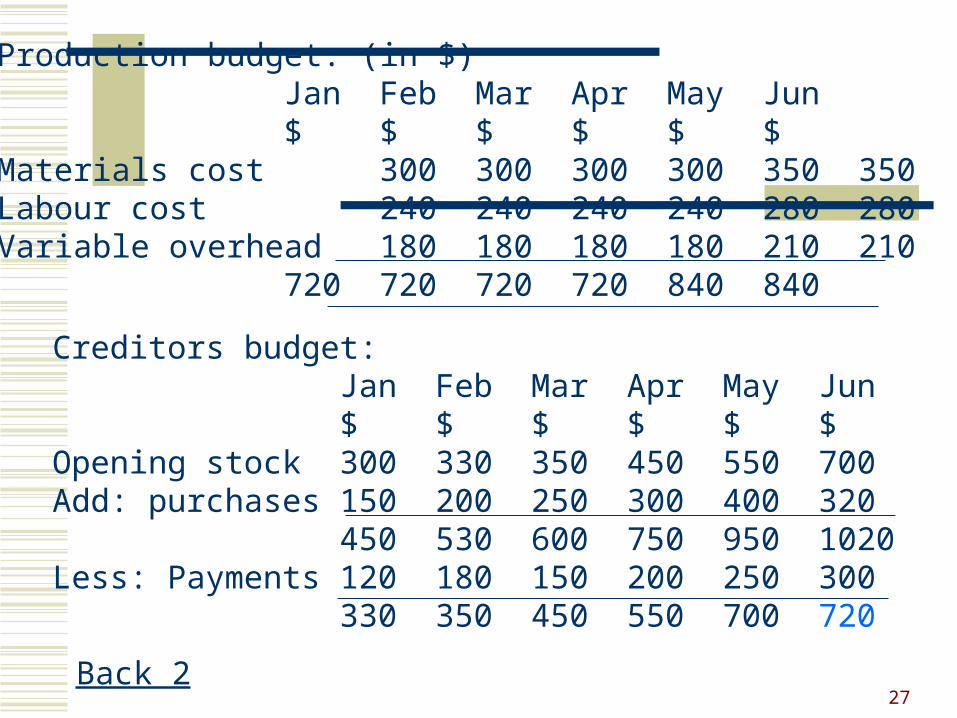

Production budget: (in $)Jan Feb Mar Apr May Jun$ $ $ $ $ $

Materials cost 300 300 300 300 350 350Labour cost 240 240 240 240 280 280Variable overhead 180 180 180 180 210 210

720 720 720 720 840 840

Creditors budget:Jan Feb Mar Apr May Jun$ $ $ $ $ $

Opening stock 300 330 350 450 550 700Add: purchases 150 200 250 300 400 320

450 530 600 750 950 1020Less: Payments 120 180 150 200 250 300

330 350 450 550 700 720

Back 2

28

Debtors budget:Jan Feb Mar Apr May Jun$ $ $ $ $ $

Opening stock 1350 1530 2070 2700 3600 4320Add: Sales 720 900 1080 1620 1620 1260

2070 2430 3150 4320 5220 5580Less: Received 540 360 450 720 900 1080

1530 2070 2700 3600 4320 4500

Back 2

29

Cash budget:Jan Feb Mar Apr May Jun$ $ $ $ $ $

Opening balance 650 550 210 (2010) (2010) 1050Add: Debtors 540 360 450 720 900 1080 Share issue - - - - 3000 -

650 550 500 500 600 570Less: Creditors 120 180 150 200 250 300 Fixed overhead 100 100 100 100 100 100 Direct labour 240 240 240 240 280 280 Variable O/H 180 180 180 180 210 210 Machinery - - 2000 - - -

550 210 (2010) (2010) 1050 1240

Back 2

30

Fixed and flexible budget

31

Fixed budget

Fixed budget is a budget which is designed to adjust the permitted cost levels to suit the level of activity actually attained

32

Fixed budget

A fixed budget is a budget, which is designed to remain unchanged irrespective of the volume of output or turnover attained

33

Example

34

ABC Ltd. Manufactures and sells a single product. Prepare the flexible budgets for 2005 at the activity levels of 80%, 100% and 120%.In accordance with the following information:1. 100% activity represents 60000 units produced2. Variable cost (per unit):

$Materials 40Direct labour 30Royalties 2 Electricity 6Maintenance 5

833. Fixed cost

$Depreciation 20000Rent 120000Indirect labour80000

35

Flexible budgetLevel of activity 48000 60000 720000 units

Variable cost $ $ $Materials 1920000 2400000 2880000Direct labour 1440000 1800000 2160000Royalties 96000 120000 144000Electricity 288000 360000 423000Maintenance 240000 300000 360000

3984000 4980000 5976000Fixed costDepreciation 20000 20000 20000Rent 120000 120000 120000Indirect labour 80000 80000 80000

4024000 5200000 6196000

36

Flexible budgets and budgetary control

By comparing the actual results with the budgeted amounts, the managers can ascertain which costs do not conform to the original plans and therefore deserve their attention

The differences between the actual results and the expected outcomes are called variance

37

If we compare the actual results with the fixed budgets, we do not know whether the variance are caused by the difference in the levels of activity or the change in efficiency

However, by comparing the actual costs with the flexible budget prepared at the actual activity level, we can see how efficient the managers are in controlling the costs

38

Example

39

ABC Ltd. Manufactures and sells a single product. In accordance with the following information:1. 100% activity represents 60000 units produced2. Variable cost (per unit):

$Materials 40Direct labour 30Royalties 2 Electricity 6Maintenance 5

833. Fixed cost

$Depreciation 20000Rent 120000Indirect labour80000

40

The budget and actual results for 2005 are shown as follows:Budgeted Actual Variance60000 units 80000 units$ $

Sales revenue ($100 each) 6000000 8000000 2000000(F)Less: variable cost

Materials 2400000 3201000 801000 (A)Labour 1800000 2500000 700000 (A)Royalties 120000 160000 40000(A)Electricity 360000 485000 125000 (A)Maintenance 300000 404000 104000 (A)Fixed overhead: Depreciation 20000 20500 500 (A)

Rent 120000 160000 40000 (A) Indirect labour 80000 95000 15000 (A)

800000 974500 174500 (F)

* F = favourable, A = Adverse variance

41

Required:(a) Prepare a flexible budget based on the original budgeted

unit costs and selling price(b) With the use of the variances, reconcile the original budget profit

with the actual profit

42

Fixed Flexible Actual Variancebudget Budget results60000 units 80000 units 80000 units(a) (b) ( c) ( c) – (b)$ $ $ $

Sales revenue ($100 each) 6000000 8000000 8000000 -Less: variable cost

Materials 2400000 3200000 3201000 1000 (A)Labour 1800000 2400000 2500000 100000 (A)Royalties 120000 160000 160000 -Electricity 360000 480000 485000 5000 (A)Maintenance 300000 400000 404000 4000(A)Fixed overhead: Depreciation 20000 20000 20500 500 (A)

Rent 120000 120000 160000 40000 (A) Indirect labour 80000 80000 95000 15000 (A)

800000 1140000 974500 165500 (F)

$340000 (F) Volume variance $165500 (A) Expenditure variance

Total variance $174500 (F)

80000*budget units cost

43

(b) The overall reconciliation of profit is shown as follows:$ $

Fixed budget profit 800000VariancesSales volume ($100 - $83)*20000 340000 (F)Materials 1000(A)Labour 100000(A)Electricity 5000 (A)Maintenance 4000 (A)Depreciation 500(A)Rent 40000 (A)Indirect labour 15000 (A) 165000 (A)Actual profit 974500

•According to the above variance analysis statement, the increase in actual profit is caused by the increase in sales volume•However, the adverse cost variance show that there may have been a general price rise of expenditure or inefficient control of expenditure by departmental managers