Download - 55106500 Beml Project Print OUT

BEML

GENERAL INTRODUCTION

INDUSTRIAL BACKGROUND

Industries are the pointing lights to the growth of an economy and are

the backbone of the country. The development and growth of a country

largely depends on industrialization of its economy.

India is basically an agriculture-based country. It is after the

independence, India has given importance to the growth of Industries

through 5year planning programmes. Government has taken a leading

march to up heave the movement of Industrialization.

For any country, small or big, developed or developing, need good

infraustructural facilities, such as roads, dams, tunnels etc. The

infraustructural facilities are the primary need for the transportation or

movement of goods. Roads play an important role in this aspect.

Tremendous development has taken place in science and technology,

which has mechanized every work in every field. Manually carried out work

is less productive and time consuming. Thus, to increase efficiency and

productivity, mechanical equipments came into existence and almost every

field is mechanized. As such, the demand for such mechanical equipments

has increased tremendously.

Foreigners have ruled India for several years. And as such, after

Independence, India has given priority to strengthen the country’s defence

force. Several Industries producing defence equipments have been started by

the Indian Government there after. India felt the need of having strong

defence, which is capable of defending its borders from neighbours. In this

view, BEML has been established by the Ministry of Defence.

Adarsha College of Maanagement & Science

1

BEML

BEML was mainly established to produce defence equipments and

heavy capital equipments like, Railway coaches, Earthmovers, Machineries

etc.

Two aggressive wars with Pakistan and China have made Defence Ministry

to start one more unit of BEML. It was started in Kolar Gold Fields in the

year 1964. It is one of the biggest units in Asia.

BEML has number of branches all over India. Its various units in

different parts of the country have immensely contributed to the growth of

the economy. It is not only has provided employment, but also has

successfully achieved the advantages of economies of scale. Ancillary and

small scale Industries has been started around its vicinity. It is also earning

foreign exchange to the country. It is contributing to the economy’s growth

both directly and indirectly. It has emerged as a powerful Industrial unit of

Indian economy.

India’s heavy Earth Moving equipment and spare parts manufacturers

manufacture various capacities ranging from mini version to giants.

Overseas manufacturers also manufacture the equipment and spares and

export to our country, hence, providing a stiff competition.

There are four major OEM and around 500 spare parts manufactures in

the country. The four major manufacturers are:

BEML

L&T

TATA-HITACHI

ESCORTS

Among them BEML is dominating.

Adarsha College of Maanagement & Science

2

BEML

MARKET STRUCTURE

The major customers for the above products are the coal mines

ministry, defence ministry, fleet owners in the construction industry, state

government civil engineering and irrigation department and some small

individual operators.

Adarsha College of Maanagement & Science

3

BEML

SUBJECT BACKGROUND

INTRODUCTION TO FINANCE

Finance is lifeblood of the economy. It is one of the major

components, which activates and stimulates the overall growth of the

economy.

Finance is a body of principles and theories, which deals with rising, and

acquiring of funds on reasonable terms, and use of money by the acquirer.

In the modern money oriented economy, finance is one of the basic

foundations of all kinds of economic activities. It is a master key, which

provides access to all the sources for being employed in manufacturing and

merchandising activities. It is rightly said that, “Business needs money to

make more money”. Efficient management of every business enterprise is

closely linked with efficient management of finance. Hence, a well-knit

financial system directly contributes to the growth of the economy.

BUSINESS FINANCE

Business finance is that business activity, which is concerned with the

acquisition and conservation of capital funds to meet financial needs and

overall objectives of a business enterprise.

Financial functions of a business may be stated as the procurement of funds

and their effective utilization.

Adarsha College of Maanagement & Science

4

BEML

FINANCIAL MANAGEMENT

Sound financial management is necessary in every organization.

Collins Brooks has remarked that, “Bad production management and sales

management have stain in hundreds, but, a faulty financial management

have stain in thousands”.

Financial management is a managerial activity, which is concerned

with the anticipation of financial needs, acquiring financial resources,

allocating funds in business, administrating the allocation of funds and

accounting and reporting to the management over the financial matters.

OBJECTIVES

The firm’s investment and financing decisions are unavoidable and

continuous. In order to make them rational, the firm must have certain

goals.

The main objectives of financial management are:

1. Profit maximization as a social obligation.

2. To ensure wealth maximization.

3. To have a balanced asset structure, that is, proper balance between

fixed assets and current assets.

4. To maintain liquidity to meet the upcoming obligations.

5. To ensure fair returns to share holders.

6. To have an efficient and disciplined financial structure.

7. To avail the creation of resources needed by the firm.

Adarsha College of Maanagement & Science

5

BEML

FUNCTIONS OF BUSINESS FINANCE

The functions of a financial manager are to plan cautiously, control

and execute the financial objectives with great care. He should review and

control the financial decisions to commit or recommit the funds to new or

outgoing uses. Thus, in addition to raising funds, financial management is

directly concerned with production, marketing and other functions of an

enterprise.

The main functions of business finance are:

1. Funds requirement decisions

2. Financing or capital-mix decision

3. Investment or long-term asset-mix decision

4. Liquidity or short-term asset-mix decision

5. Dividend or profit allocation decision

FINANCIAL STATEMENTS

A firm communicates financial information to the users through

financial statements and reports. Financial statements are the organized

collection of financial data, undertaken according to logical and consistent

accounting procedures for the purpose of presenting a periodical review or

report on the financial aspects o f a business firm, such as operating results

and financial position of the firm at a particular period of time.

Adarsha College of Maanagement & Science

6

BEML

OBJECTIVES

I. Basic objective is to assist in decision-making.

II. To provide reliable information about economic resources and

obligations of a firm.

III. To provide financial information that assist in estimating the earning

potential of the enterprise

DIVISIONS OF FINANCIAL STATEMENTS

FINANCIAL STATEMENT

I. INCOME STATEMENT OR PROFIT AND LOSS ACCOUNT

It is a statement, which matches the revenues of a concern with the

costs incurred in earning those revenues, and thereby, reveals the net profit

or the net loss of an enterprise for an accounting year. It is the “score-board”

of the firm’s performance during a particular period of time. The income

statement reflects the earning capacity and potential of the firm. It represents

the summary of revenues, expenses and net income/loss of a firm for a

period of time.

II. BALANCE SHEET OR POSITION STATEMENT

It is a statement, which indicates the financial position of the business

as on particular date. It discloses the assets and liabilities of the business

and also the owner’s capital in the business as on the last date of the

Adarsha College of Maanagement & Science

7

Income Statement

Position Statement

Statement of Retained Earnings

Statement of Changes in Financial Position

BEML

accounting year. It contains information about the resources and obligations

of a business entity and about the owner’s interest in the business.

III. STATEMENT OF RETAINED EARNINGS OR CHANGES IN

OWNER’S EQUITY OR PROFIT & LOSS APPROPRIATION

ACCOUNT

It is a connecting link between Profit and loss account and Balance

sheet. Only Joint Stock companies prepare it.

It is a statement, which is prepared to show the distribution of the earnings

or profits of a company during a particular accounting period as retained

earnings and dividends and reserves. The balance shown by the income

statement is transferred to the balance sheet through this statement after

making necessary appropriations.

I. STATEMENT OF CHANGES IN FINANCIAL POSITION

It is a statement, which discloses the changes in assets, liabilities and

owner’s equity between dates of two balance sheets. It also discloses the

way in which the firm used its financial resources during the period.

The most commonly used forms of the statement of changes in financial

position are:

(a) Statement of sources and uses of funds or Fund flow statement

(b)Cash flow statement

(a)STATEMENT OF SOURCES AND USES OF FUNDS OR

WORKING CAPITAL

It is a statement prepared to determine the changes in the sources and

uses of working capital between dates of two balance sheets.

It helps management in planning and proper utilization of funds.

Adarsha College of Maanagement & Science

8

BEML

(b)CASH FLOW STATEMENT

It is a statement, which summarizes the causes for the changes in cash

position of a business between dates of two balance sheets. It indicates

sources and uses of cash. It helps the management in making projections of

cash inflows and outflows for the near future to determine the availability of

cash.

ANALYSIS AND INTERPRETATION OF FINANCIAL

STATEMENTS

Analysis and interpretation of the financial statements is the

methodical classification of the data given in the financial statements into

simple component parts or elements, establishment and study of the

relationship between the classified component parts with a view to provide a

full diagnosis of the profitability and financial strength of an enterprise.

STEPS INVOLVED IN ANALYSIS OF FINANCIAL STATEMENTS

It involves three steps or processes:

1.ANALYSIS

Analysis of financial statements refers to the splitting up or

regrouping of the figures found in the financial statements into the desired

homogenous and comparable component parts.

Eg: The amount of current assets in the balance sheet may be regrouped as

Debtors, Cash, Inventories etc.

Adarsha College of Maanagement & Science

9

BEML

2. COMPARISON

Comparison is the process of ascertainment of the relative magnitudes

of the component parts or the study of the extent of relationship of the

component parts.

3. INTERPRETATION

Interpretation refers to the formation of rational judgment and the

drawing of proper conclusions of the business through careful study of the

relationship of component parts obtained through analysis and interpretation.

Analysis and interpretation go in hand-in-hand. Interpretation cannot

be done without analysis and comparison, and mere analysis without

interpretation is of no value.

OBJECTIVES

The objectives of the analysis and interpretation of financial statements are;

1. To determine the progress of the concern

2. To measure the operational efficiency of the company

3. To judge the financial position, i.e., short-term liquidity and long-term

solvency of the concern.

4. To ascertain the future prospects of the company.

TYPES OF FINANCIAL ANALYSIS

Financial analysis may be classified into different types:

1. On the basis of materials used for the analysis or the persons interested in

the analysis

2. On the basis of the modus operandi or method of operation followed in

the analysis

Adarsha College of Maanagement & Science

10

BEML

1. ON THE BASIS OF PERSONS INTERESTED IN THE ANALYSIS

• EXTERNAL ANALYSIS: is the analysis done by external parties, i.e.,

the parties, who are outsiders to the business. The external parties are

shareholders, investors, lenders, creditors etc. who have no access to the

books of account and the internal records of the concern. The analysis

mainly depends upon the published financial statements.

• INTERNAL ANALYSIS: is the analysis done by the internal parties of

the concern. They include persons who have access to the books of

accounts and the internal records of the concern. They are personnel of

finance and accounting departments of the concern and the executives for

management purpose.

2. ON THE BASIS OF THE METHOD OF OPERATION

FOLLOWED IN THE ANALYSIS

• VERTICAL OR STRUCTURAL ANALYSIS: when a single set of

financial statements relating to just one accounting year is analyzed, it is

said to be vertical analysis.

It is an analysis used to study the quantitative relationship of items in the

financial statements as on a particular date or for one accounting year,

through ratios. The figure from a year’s financial statement is compared

with a base figure selected from the same financial statement.

• HORIZONTAL ANALYSIS OR TREND ANALYSIS: When the

financial statements of a number of years are analyzed, it is said to be

Adarsha College of Maanagement & Science

11

BEML

horizontal analysis. In this, a comparison of the trend of each item in the

financial statements over a number of years is made.

The current year’s figures are compared with the figures of the standard

or base year, and changes in each of the elements from the base year are

shown, usually, in the form of percentages.

TOOLS AND TECHNIQUES OF FINANCIAL ANALYSIS

A number of tools and techniques are available for financial analysis. The

important tools are as follows:

i. Comparative financial statement analysis

ii. Common-size statement analysis

iii. Trend analysis or trend percentages

iv. Ratio analysis

v. Fund flow analysis

vi. Cash flow analysis

i. COMPERATIVE FINANCIAL STATEMENTS

These are the financial statements, which summarizes and present

relative accounting data for a number of years, incorporating therein changes

in individual items.

The current year financial happenings are compared with the previous year’s

events and the direction of growth of the enterprise is found out.

There are two important comparative financial statements:

COMPARATIVE BALACE SHEET: is a balance sheet which is

prepared to facilitate the comparison of assets, liabilities and proprietor’s

Adarsha College of Maanagement & Science

12

BEML

capital of a business as on two different dates and to find out the changes

in the elements.

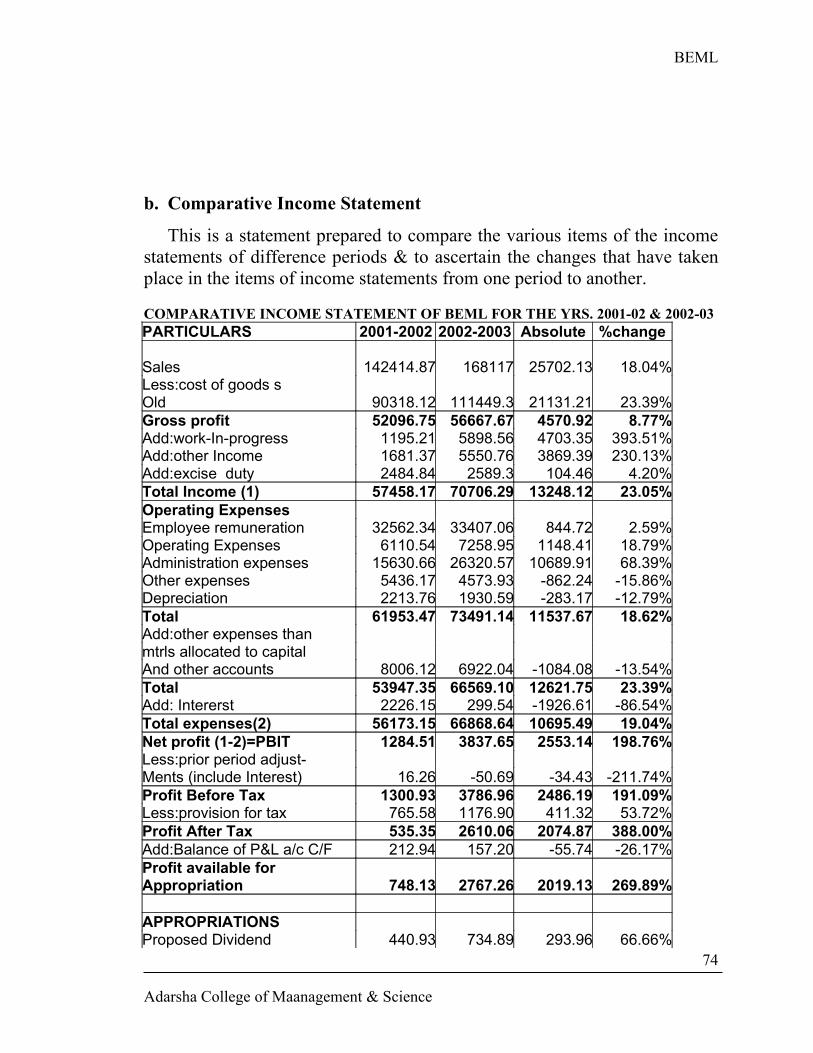

COMPARITIVE INCOME STATEMENT: is a statement prepared to

compare the various items of income statements of the different periods

and to ascertain the changes in the items of income statements from one

period to another.

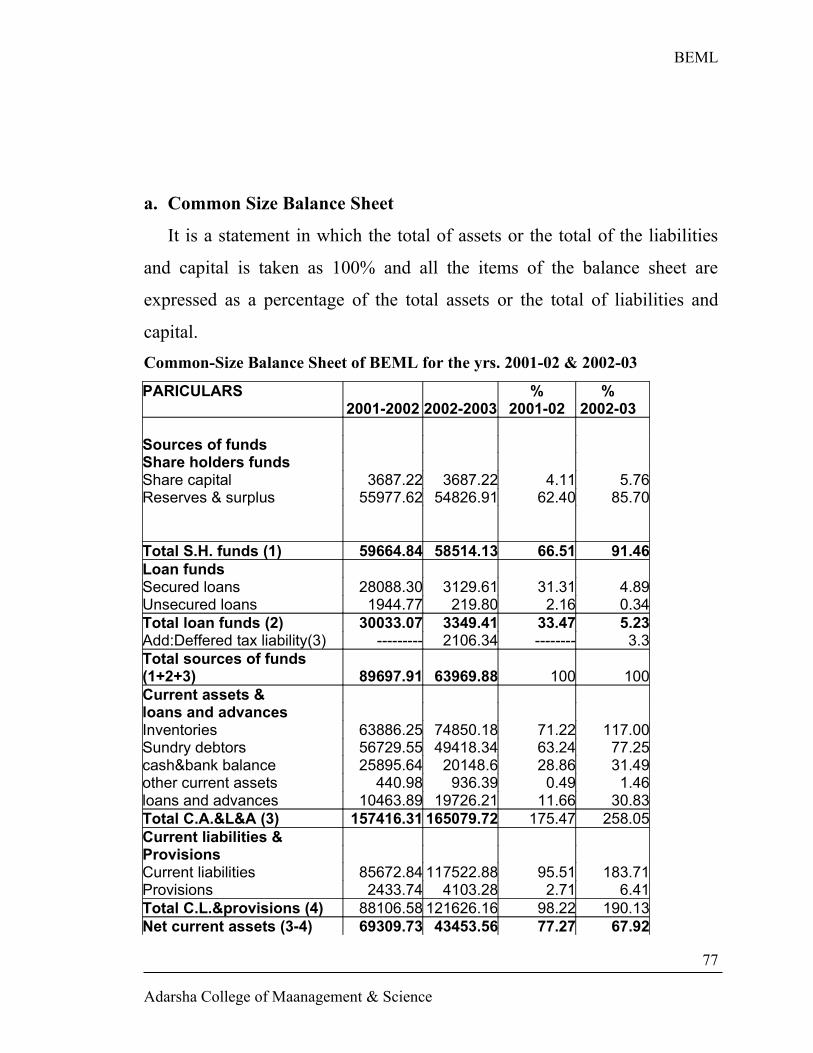

ii. COMMON-SIZE STATEMENT

These are the statements in which the data or figures reported in the

financial statements are converted into percentages, taking some common

base. These statements are also known as component percentage

statements or 100 percent statements, because each statement is reduced

to the total of 100% and each individual item is expressed as percentage

of the total of 100.

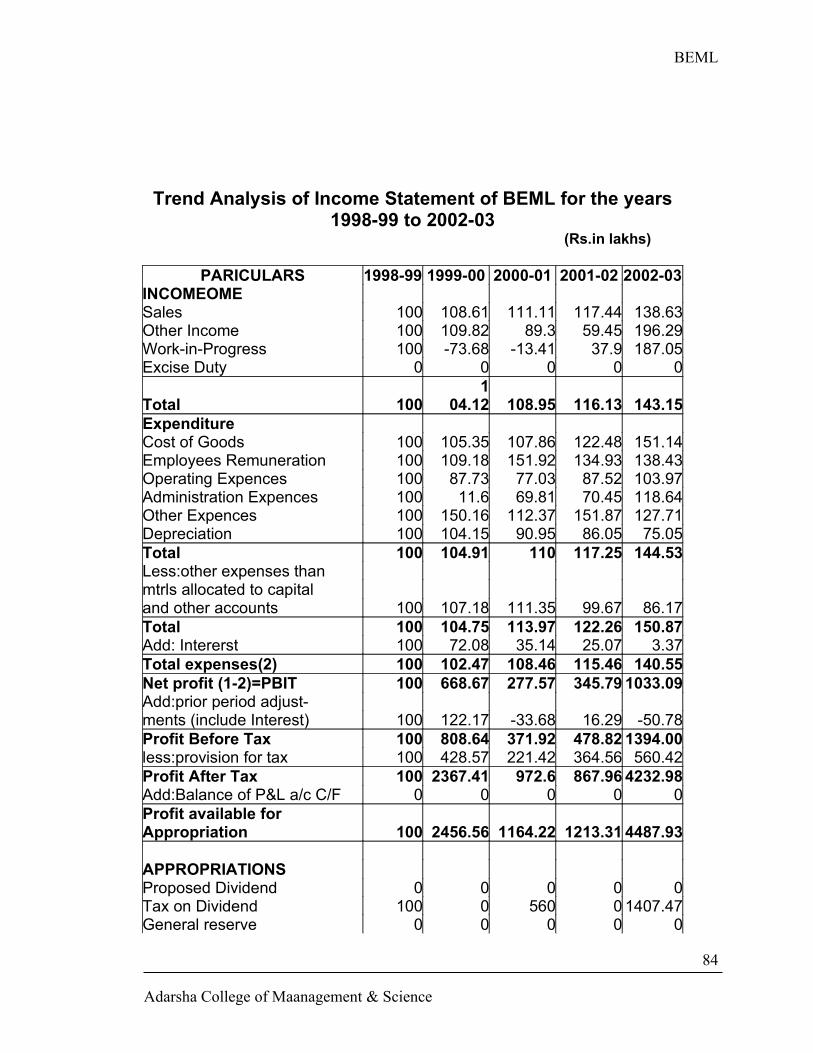

iii. TREND ANALYSIS

Trend analysis is a horizontal analysis of financial statements, as the

financial statements of more than one year is analyzed. Comparison of past

data over a period of time with a base year is known as trend analysis.

It is possible to identify the areas in which the concern has improved over

the years and the areas in which it has not succeeded. It is possible to know

the present position and the trend or direction in which the enterprise is

moving, through trend analysis.

Adarsha College of Maanagement & Science

13

BEML

iv. RATIO ANALYSIS

Financial statements, no doubt, contain the items related to profit and loss

and financial position of a concern, but the items found in financial

statements will not be of much use, if they are considered independently.

They will be very useful only when one item is considered in the light of

another, i.e., compared.

In this regard, ratio analysis is a powerful tool. A ratio is defined as “The

indicated quotient of two mathematical expressions” and “as the relationship

between two or more items”.

It is used as an index or yardstick for evaluating the financial position

and performance of a firm. Ratio analysis is the technique of the calculation

of number of accounting ratios from the data found in the financial

statements, the comparison of the accounting ratios with those of the

previous years or with those of the concerns engaged in similar line of

activities or with those of standard or ideal ratios and interpretation of the

comparison there after.

Ratios can be expressed in two ways:

In the terms of time. Eg.: current assets to current liabilities = 1.36 times

In terms of percentage. Eg.: net profit to net sales = 50%

CLASSIFICATION OF ACCOUNTING RATIOS

Accounting ratios can be classified mainly on 2 bases:

I. On the basis of origin or source of figures placed in relation with

each other:

(a) Balance sheet ratios or financial ratios

(b)Profit and loss account ratios or operating ratios

(c) Mixed or combined or inter-statement ratios

Adarsha College of Maanagement & Science

14

BEML

II. On the basis of nature and functions of the accounting ratios:

(a) Liquidity ratios

(b)Leverage ratios

(c) Turnover ratios

(d)Profitability ratios

LIQUIDITY RATIOS OR SHORT-TERM SOLVENCY

RATIOS

The importance of liquidity in the sense of the ability of a firm to meet

current or short-term obligations when they become due for payment can

hardly be over-stressed. This liquidity ratio measures the ability of a firm to

meet its short-term obligations and reflect short-term financial strength or

solvency of a firm.

The most common ratios which measures the liquidity of a firm are:

1. Current ratio or working capital ratio

2. Quick ratio or Acid test ratio or Liquid ratio or Liquidity ratio

3. Absolute liquid ratio or Cash position ratio or Cash ratio

4. Inventory to Working capital ratio

5. Net working capital ratio

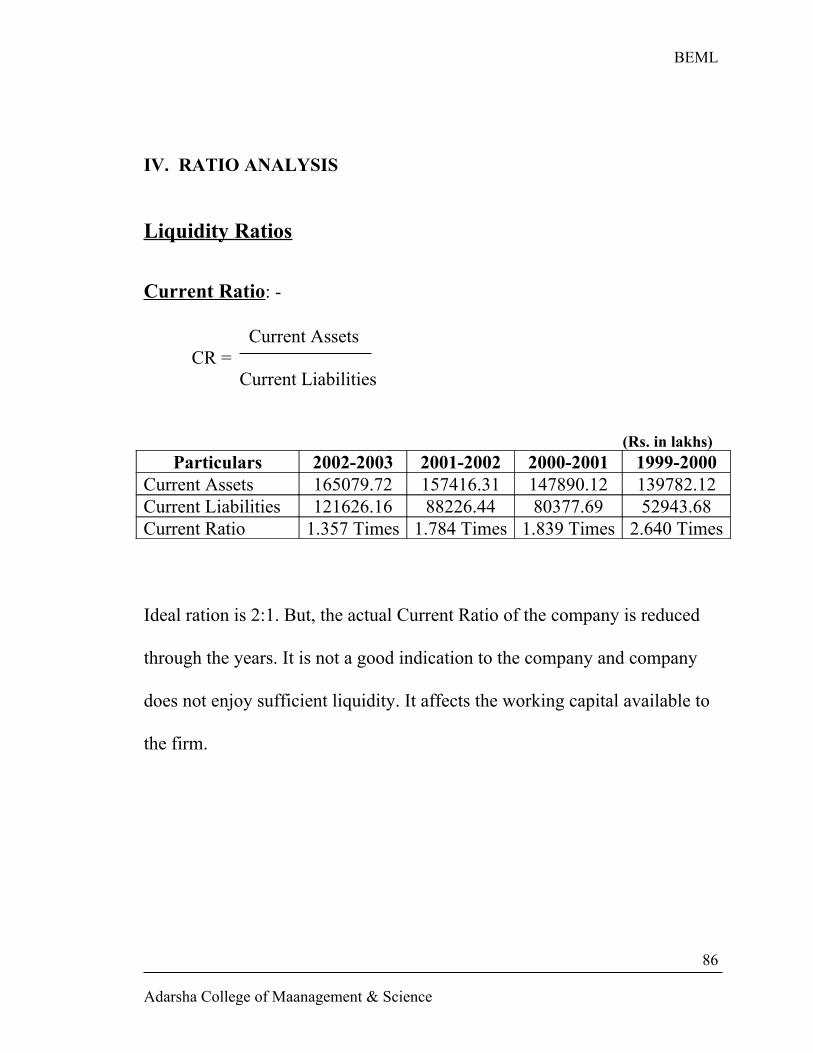

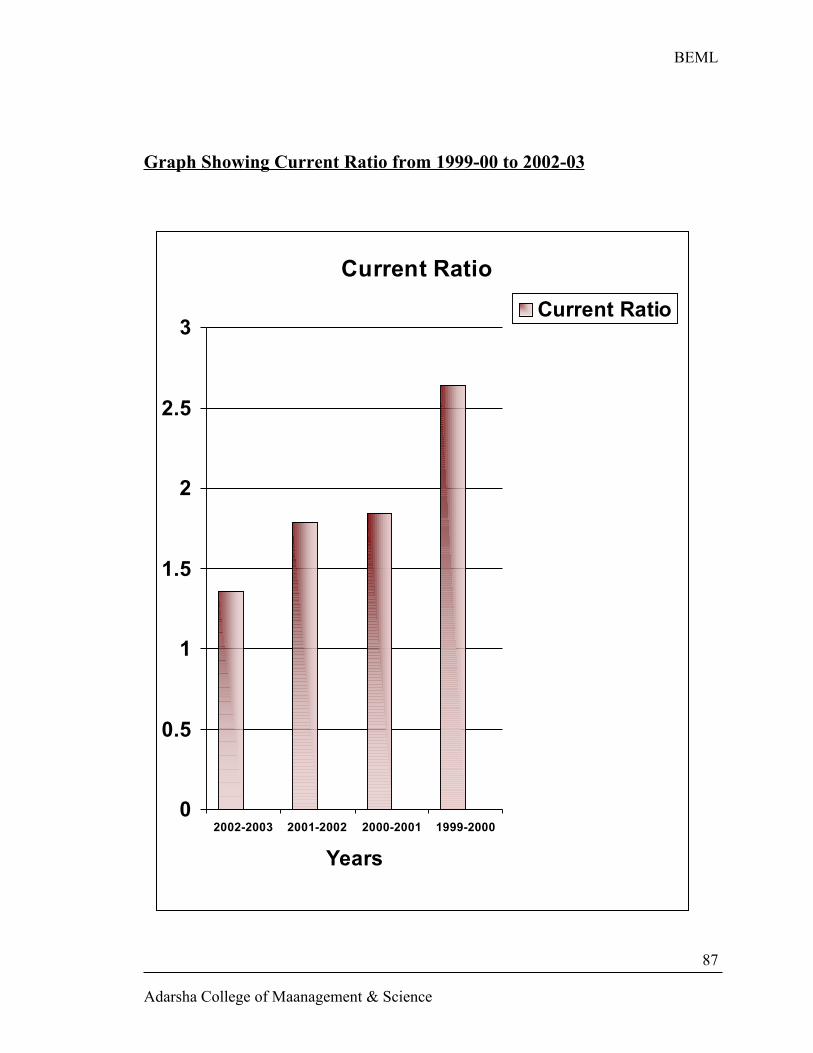

1. Current ratio

It is the ratio, which expresses the relationship between current assets &

current liabilities.

Current Assets: Includes cash & other assets which can be converted into

cash with in an year, such as marketable securities, debtors, inventories,

prepaid expences, o/s or accured incomes, advances to staff & others,

provisions for bad & doubtful debts.

Adarsha College of Maanagement & Science

15

BEML

Current Liabilities: All obligations maturing within a year are included in

current liabilities. They include bills payable, creditors, bank overdrafts,

accrued expenses, short term bank loans, provision for income tax, dividend

payable, incomes received in advance and long term debt maturing in the

current year.

Expression of Current Ratio:

C.R. = Current assetsCurrent liabilities

Interpretation

As a conventional rule, a current ratio of 2:1 or more is considered

satisfactory. If the actual current ratio is less than 2:1, the logical conclusion

is that the concern doesn’t enjoy sufficient liquidity & there is shortage of

working capital.

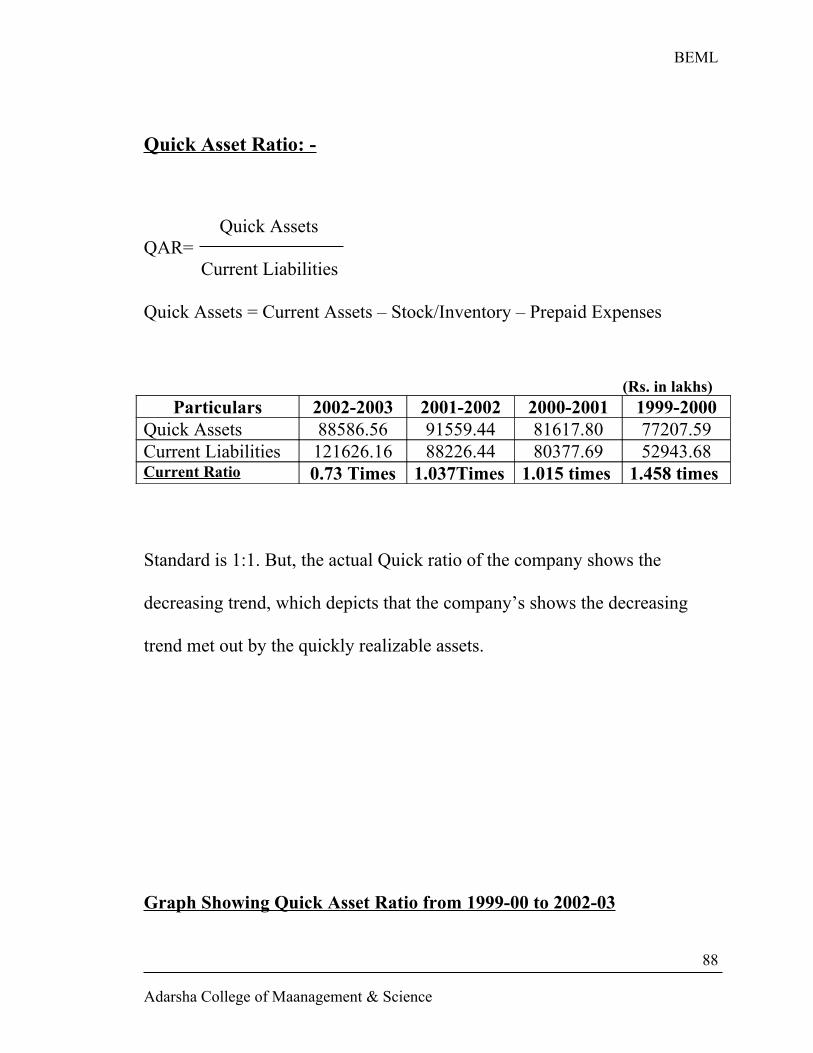

2. Quick/ Acid Test Ratio

Quick ratio is the ratio, which express the relationship between quick or

liquid assets & quick or liquid liabilities.

Quick assets include all the current assets excluding stock or inventory &

prepaid expenses.

Quick liabilities include all the current liabilities excluding bank o/d &

cash credit.

Expression of Quick Ratio: Quick Ratio Quick Liabilities

Interpretation

The ideal quick ratio is 1:1. If the quick ratio is equal or more than the

standard ratio, it is satisfactory.

Adarsha College of Maanagement & Science

16

BEML

3. Cash Ratio/ Absolute Liquid Ratio

Cash Ratio is the ratio, which expresses the relationship between absolute

liquid assets & quick liabilities. Absolute Quick Assets refer to cash & near

cash assets include cash in hand, cash at bank & readily marketable

securities.

Expression: Absolute Liquid Assets Liabilities Current

Interpretation

The ideal Absolute Liquid Ratio is 1:2. If the actual absolute Liquid

Ratio is equal or more than the standard ratio the concern is liquid.

4. Inventory to Working Capital Ratio

It is the ratio of Inventory to Working Capital. Inventory refers to closing

stocks of raw materials, work in progress (semi finished goods) & finished

goods. Working capital is the excess of current assets over current liabilities

Expression: Inventory * 100 Working Capital

Interpretation

As per standard ratio, the inventories should not absorb more than

75% of working capital. A low inventory to working capital ratio indicates

under stocking & company, high liquid position & high ratio indicates over

stocking & company, a low liquid position.

5. Net Working Capital Ratio

It is the relationship between net working capital & net assets or capital

employed. Net Working Capital is the difference between current assets &

current liabilities

Expression: Net Working Capital Net Assets

Adarsha College of Maanagement & Science

17

BEML

Interpretation

The Net Working Capital should be more than the net assets to meet

the short-term obligations of the company easily.

LEVERAGE/ CAPITAL STRUCTURE/ LONG TERM SOLVENCY

RATIO

Leverage Ratios are the financial ratios, which throw light on long-

term solvency of a firm as reflected in its ability to assure the long-term

creditors with, regarded to

i. Periodic payment of interest during the period of loan

ii. Repayment of principal on maturity or in pre determined installments at

due dates

There are thus, two aspects of the long-term solvency of a firm

Ability to repay the principal when due &

Regular payment of interest

Accordingly, there are two different, but, mutually dependant & inter

related, types of leverage ratios

(a) First, ratios are based on the relationship between borrowed funds &

owners capital. Their ratios are computed from the balance sheet & have

many variations, such as

Debt Equity Ratio/ External- Internal Ratio

Property/ Equity/ Net worth Ratio

Solvency Ratio

Fixed Asset to Net worth Ratio

Current Asset to Net worth Ratio

Current Liabilities to Net worth Ratio

Adarsha College of Maanagement & Science

18

BEML

Capital Gearing Ratio

Fixed Assets Ratio

(b) The second type of capital structure ratios, popularly called as Coverage

Ratios are calculated from profit & loss account included in this category

Interest Coverage Ratio

Dividend Coverage Ratio

Total Fixed Charges Ratio

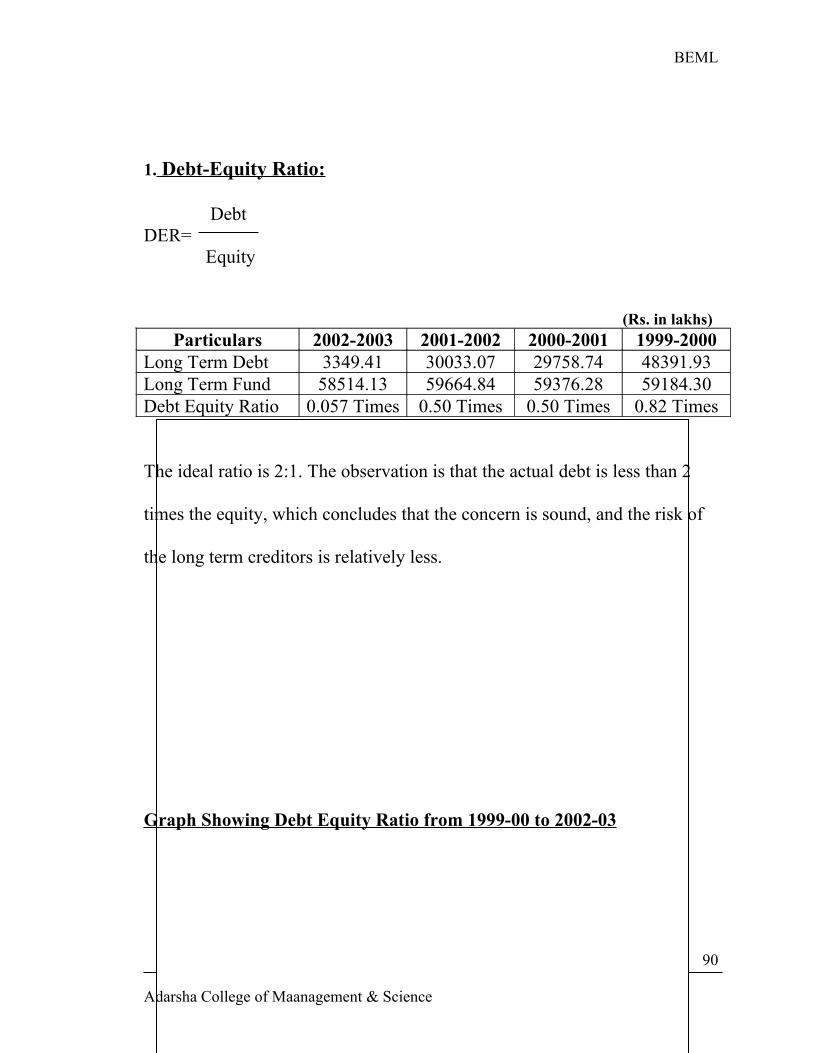

1. Debt Equity Ratio

This is the Ratio of total outside liabilities to total owner’s funds. The

ratio reflects the relative claims of creditors & shareholders against the

assets of the firm.

Equity/Owners fund = capital+ all accumulated results + profits.

Expression: Total Long term Debt Total Long-term funds

Interpretation

The ideal Debt Equity Ratio is 2:1. As such, if the debt is less than two

times of equity, the logical conclusion is that the financial structure of the

firm is sound & the stake of long term creditors is relatively less.

2. Proprietary Ratio

This is the Ratio, which express the relationship between net worth and

equity & total assets. Net worth/ Equity means the excess of total assets over

total liabilities. It means proprietor’s funds. Total Assets refers to all

realizable assets, both tangible & intangible except goodwill.

Expression: Net worth/ Shareholders Fund

Adarsha College of Maanagement & Science

19

BEML

Total AssetsInterpretation

Ideal ratio is 0.50:1. Higher the Proprietary Ratio, the stronger is the

financial position of the concern & vice versa.

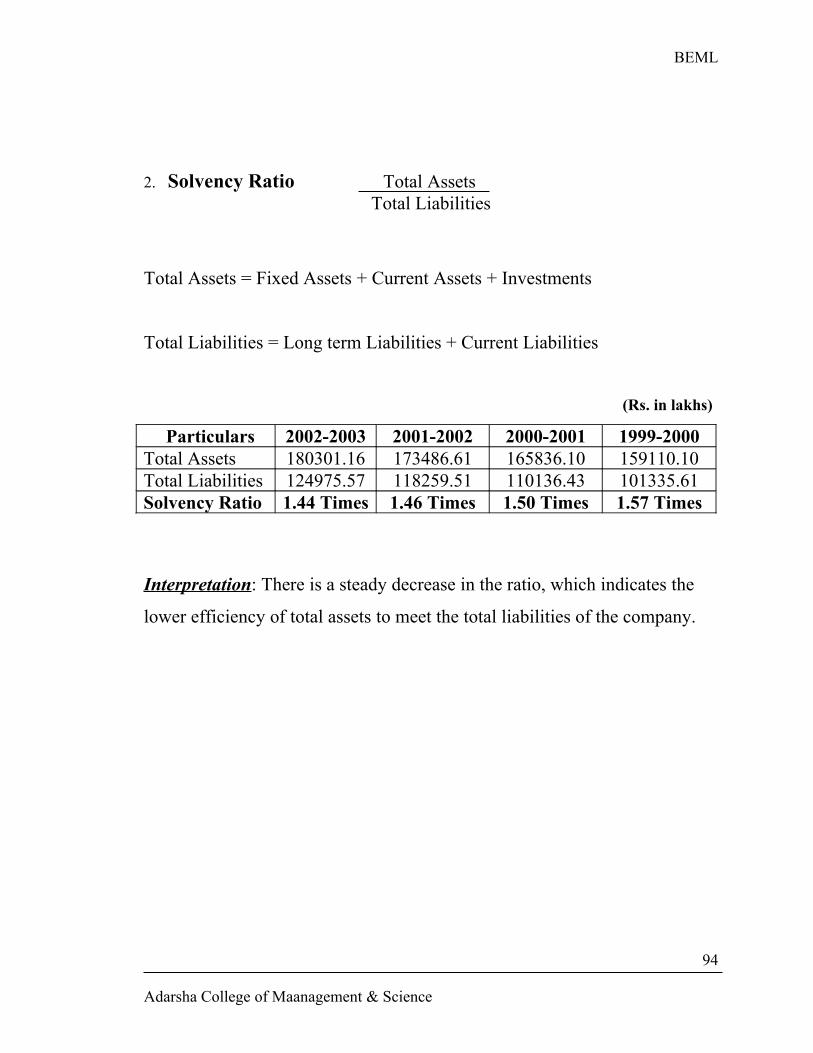

3. Solvency Ratio

This is the ratio between total assets & total liabilities

Expression: Total Assets Total Liabilities

Interpretation

Higher the Solvency Ratio of a concern the stronger is the financial

position.

4. Fixed Assets to Net worth Ratio

It is the Ratio between the fixed assets & net worth

Fixed Assets: (machinery, building, furniture etc) – depreciation

Net worth: owner’s fund

Expression: Net Fixed Assets * 100 Net worth

Interpretation

Ideal ratio is 2/3 or 67% if the fixed assets constitute more than 67%

of the proprietor’s fund, the indication is that the concern is financially weak

& greater risk for creditors & vice versa.

5. Current Assets to Net worth

This is the Ratio between current assets & net worth

Expression: Current Assets Net worth

Interpretation

If the ratio is high, the financial strength of the concern is good.

Adarsha College of Maanagement & Science

20

BEML

6. Current Liabilities to Net worth

It is the ratio between current liabilities & net worth of a concern.

Expression: Current Liabilities Net worth

Interpretation

The desire level set is 1/3 or 33 1/3. If the Actual Ratio is very high, the

liability base of the concern will not provide an adequate cover for long-term

creditors. That means, it would be difficult for the concern to obtain long-

term funds.

7. Capital Gearing Ratio

This is the Ratio, which expresses the relationship between equity capital

& fixed interest bearing securities & fixed dividend bearing shares.

Equity Capital: Equity Share Capital + Accumulated Reserves & profits

Fixed Interest Bearing Securities: Long-term loans carrying fixed rate of

interest. They comprise debentures, long-term loans & long-term fixed

deposits.

Fixed Dividend Bearing Shares: Preference Share Capital, which is entitled

to, fixed rate of interest every year.

Expression:

Fixed Interest Bearing Securities + Fixed Dividend Bearing Securities

Equity Share holders Fund

Interpretation

If the fixed interest bearing securities & fixed dividend bearing securities

are more than equity share holder’s fund, the company is said to be highly

geared & vice versa.

Adarsha College of Maanagement & Science

21

BEML

8. Fixed Assets Ratio

This is the ratio between fixed assets & capital employed.

Capital Employed = owner’s fund + long term loans, deposits & debentures

(or) = Fixed Assets + Trade Investments+ Net Working Capital.

Expression: Fixed Assets Capital Employed

Interpretation

The Ratio should not be more than 1. The ideal ratio is 0.67, this

would means that not only all the fixed assets but also a part of working

capital are financed by long term funds, because part of working capital

known as “ CORE WORKING CAPITAL”, should met out of long term

funds.

Coverage Ratios

It measures the relationship what is normally available from operations of

the firms & claims of the outsiders.

1. Interest Charged Ratio

This measures the debt servicing capacity of a firm in so far as fixed

interest & long term loans is concerned. This shows how many times the

interest charges are covered by the EBIT out of which they will be paid.

Expression: EBIT Fixed Charges

Interpretation

Ideal fixed charges cover 6 to 7 times, as such, higher fixed charges

cover indicates that there is greater margin of safety for the long term

Adarsha College of Maanagement & Science

22

BEML

lenders & it is easy to obtain long term loans & vice versa in low fixed

charges.

2. Dividend Coverage Ratio

This measures the ability of the firm to pay dividend on the preference

shares, which carry a fixed rate of return.

Expression: EAT Preference Dividend

3. Total Coverage Ratio

The over all ability of a firm to service outside liability is truly reflected

in total Coverage Ratio. It takes into account fixed charges like interest on

loan, preference dividend, repayment of principal etc.

Expression: EBIT Fixed Charges

Activity/ Performance/ Turnover Ratios

Activity Ratios refers to Ratios, which measures the level of activities,

the performance or the operating efficiency of an enterprise. They may be

defined as the test of relationship between sales & various assets of the firm.

Several Activity Ratios are calculated to judge the effectiveness of asset

utilization.

The important Activity Ratios are

1. Inventory/ Stock Turnover Ratio

2. Receivable/ debtors Turnover Ratio/ debtors Velocity

3. Creditors Turnover Ratio/ creditors Velocity

4. Cash Turnover Ratio/ Cash Velocity

5. Assets Turnover Ratio/ Investment Turnover Ratio

Adarsha College of Maanagement & Science

23

BEML

6. Sales to net worth Ratio

7. Working Capital Turnover Ratio

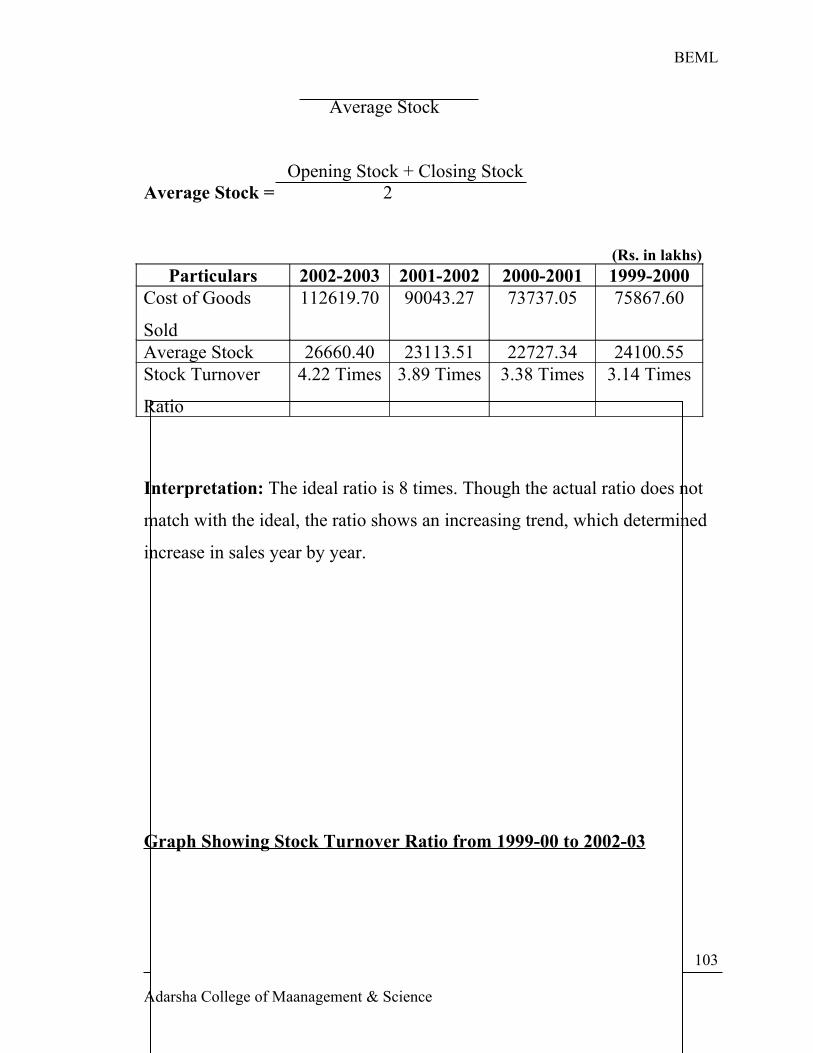

1. Inventory Turnover Ratio

This is the ratio, which indicates the number of times the stock is turned

over during the year. This ratio indicates the efficiency of the firm in selling

its products. It is the ratio between stock & cost of goods sold.

Expression Cost of Goods Sold Average Stock/ Inventory

Average Stock = Opening Stock of Closing Stock of finished goods + finished goods 2

Cost of Goods Sold = Opening stock of goods+ manufacturing cost

(including purchases) - closing stock.

Interpretation

A stock turn over Ratio of 8 times a year is considered ideal. The ratio

higher than the ideal rate indicates the efficient sales of the concern i.e., the

business is expanding & lower ratio indicates the inefficient in sales of the

products i.e., business is not prosperous.

The manufacturing firms inventory consists two more components

viz.

(a) Raw Materials

(b) Work-in-progress

Adarsha College of Maanagement & Science

24

BEML

To know the levels of raw materials involved in inventory & work-in-

progress inventory held by the firm on coverage, the following two ratios are

helpful.

(a) Raw Materials Inventory TOR = Cost of raw materials used Average Raw Material Inventory

(b) Work-in-progress TOR Ratio = Cost of Goods manufactured Average work-in-progress Inventory

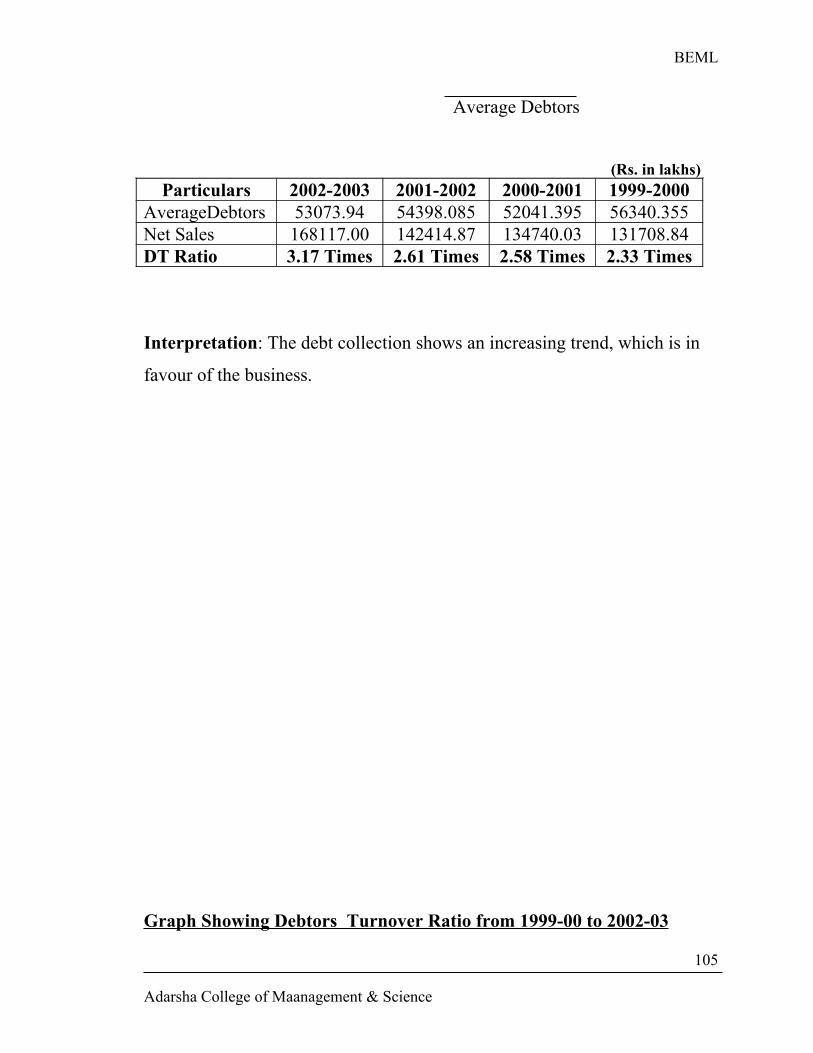

2. Debtors Turnover Ratio

It is the ratio, which indicates the relationship between debtors & sales. It

is the ratio, which indicates the number of times the debts collected in a

year.

Expression: Net Credit Sales Average Debtors

Debtors = Sundry debtors + Bills Receivable

Average Debtors = Opening Debtors + Closing Debtors 2

Debt Collection Period

This indicates the average time taken by the firm to collect debts.

Expression: Months/ Days in a year Debtors TOR Ratio

Interpretation

If the actual period of credit allowed is more than the normal period of

credit or ideal period of credit (30 days) the indication is that credit

collection is not efficient. In the adverse case, it is the indication of efficient

credit collection.

Adarsha College of Maanagement & Science

25

BEML

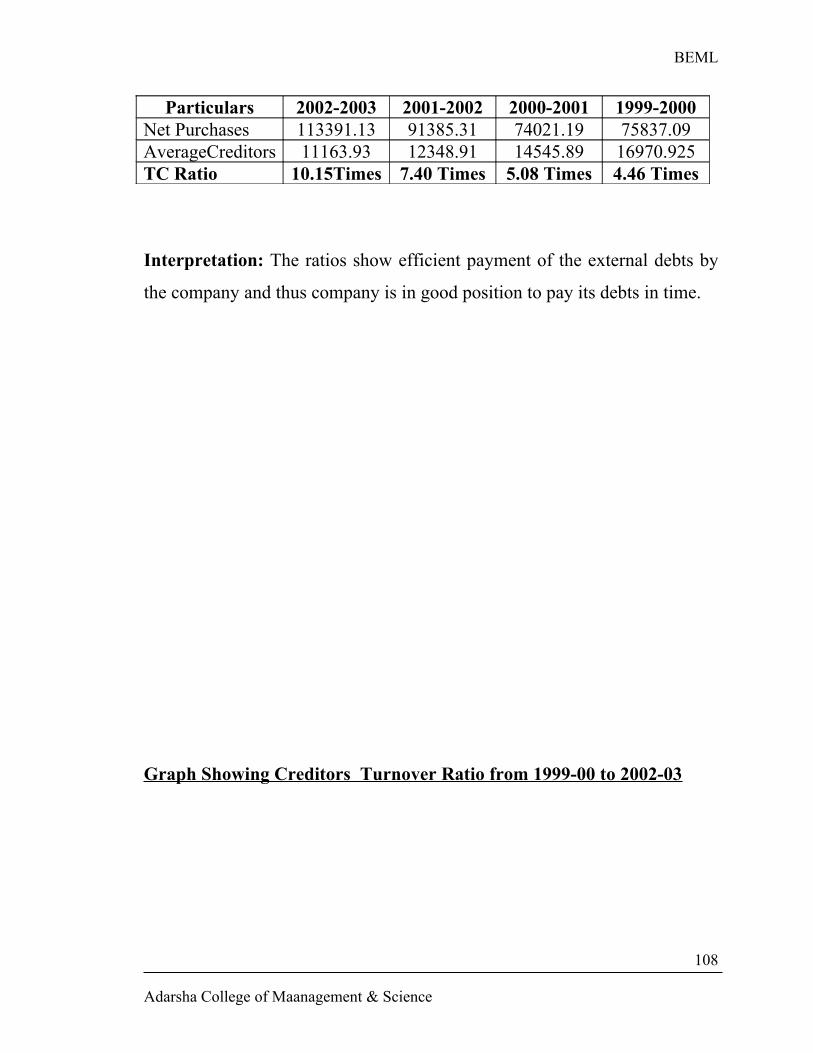

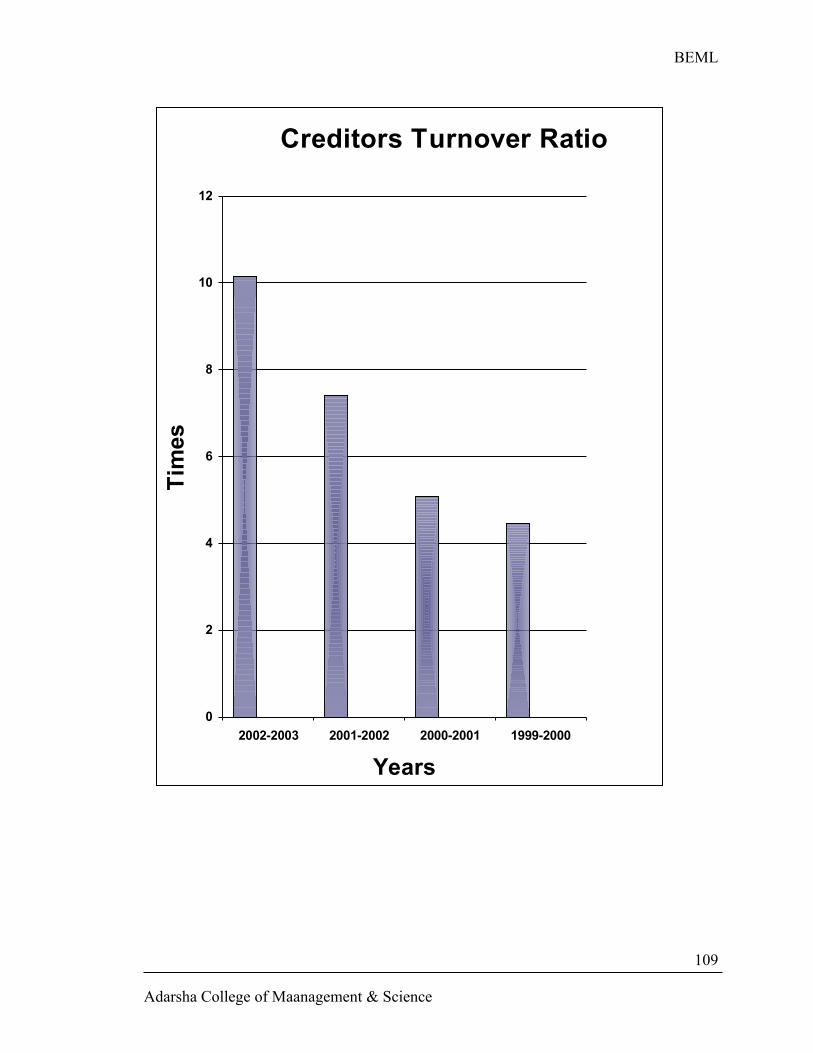

3. Creditors Turnover Ratio

This is the Ratio between creditors & purchasers. It is the Ratio, which

indicates the number of times the creditors are paid in a year.

Expression: Net Credit Purchases Average creditors

Creditors = sundry creditors + bills payable.

Average creditors = Opening creditors + Closing crs 2

Debt Payment Period

This indicates the time with in which the payments are made to

creditors.

Expression: Days/ Months in a Year Creditors TOR Ratio

Interpretation

If the actual period of credit received from creditors is less than 30 days

(ideal time), it indicates that sufficient period of credit has not been received

from creditors. In the adverse case, it indicates that the concern has received

sufficient period of credit from the creditors.

4. Cash TOR Ratio

This is the ratio between cash & turnover or sales

Expression: Net Annual Sales Cash

Cash = cash in hand + cash at bank & readily realizable investments

Or securities

Net Sales = Sales – Sales Returns.

Interpretation

Adarsha College of Maanagement & Science

26

BEML

Ideal Cash TOR Ratio is 10:1. The Actual Ratio equal or more than the

ideal ratio indicates the effective utilization of the cash resources, & vice

versa in adverse case.

5. Assets Turnover Ratio

This represents the relationship between sales & assets. Several assets

TOR Ratio can be calculated as follows

Total Asset TOR Ratio

Fixed Asset TOR Ratio

Current Asset TOR Ratio

Asset TOR Ratio

This is the ratio between total assets or turn over or sales

Expression: Net Sales Total Assets

Interpretation

The ideal Total Asset TOR Ratio is that the sales should be at least two

times the value of the assets (2:1). The actual Ratio more than the ideal

Ratio indicates that the assets of the concern are utilized effectively & vice

versa in adverse case.

Fixed Asset Turnover Ratio

This is ratio between fixed asset & turnover

Expression: Net Sales Fixed Assets (net)

Net Sale = Sales – Returns

Adarsha College of Maanagement & Science

27

BEML

Fixed Assets = Fixed Assets – Depreciation

Interpretation

Ideal ratio is 5:1 the actual ratio equal or more than the ideal ratio

indicates the better utilization of fixed assets & vice versa in adverse case.

Current Assets TOR Ratio

This is the between current assets & turn over

Expression: Net Sales Current Assets

Interpretation

There is no ideal ratio. Yet the interference is that a high Current TOR

Ratio is an indication of better utilization of current assets & vice versa in

adverse cases.

6. Sales Net worth Ratio

This is the ratio between sales & net worth (owner’s fund)

Expression: Net Sales Current Assets

Interpretation

If the volume of sales in relation to net worth is reasonable, it indicates

that the owner’s funds have been effectively utilized.

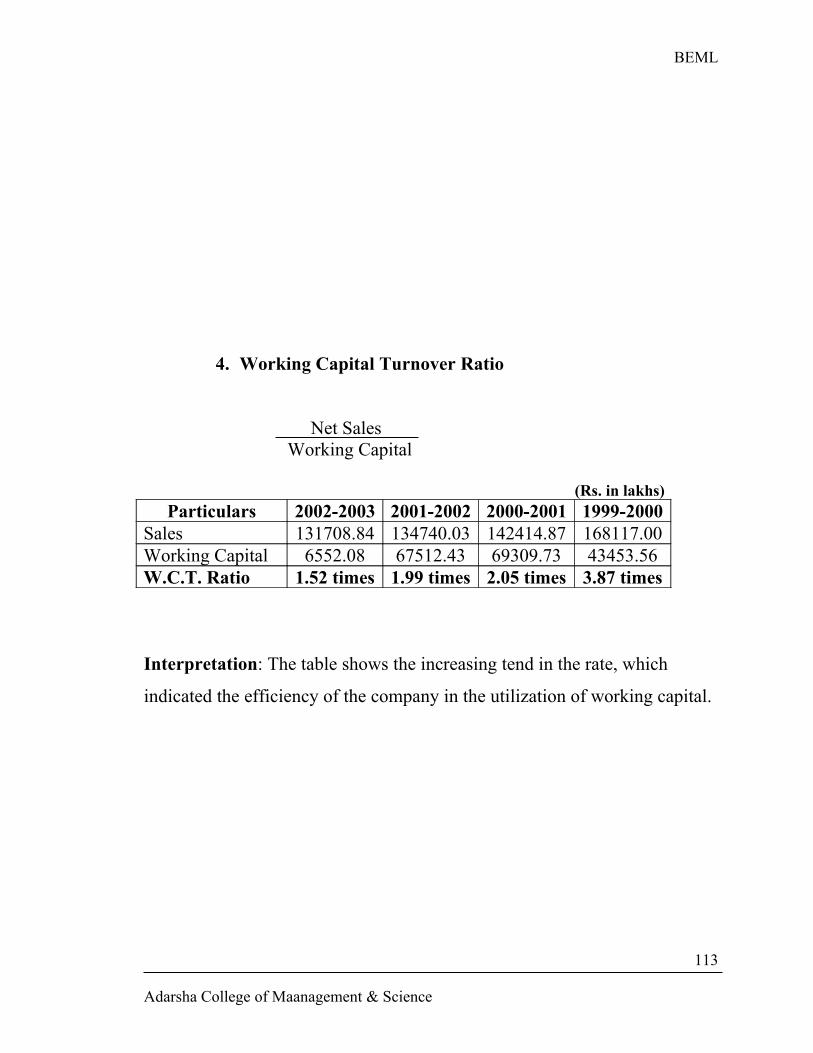

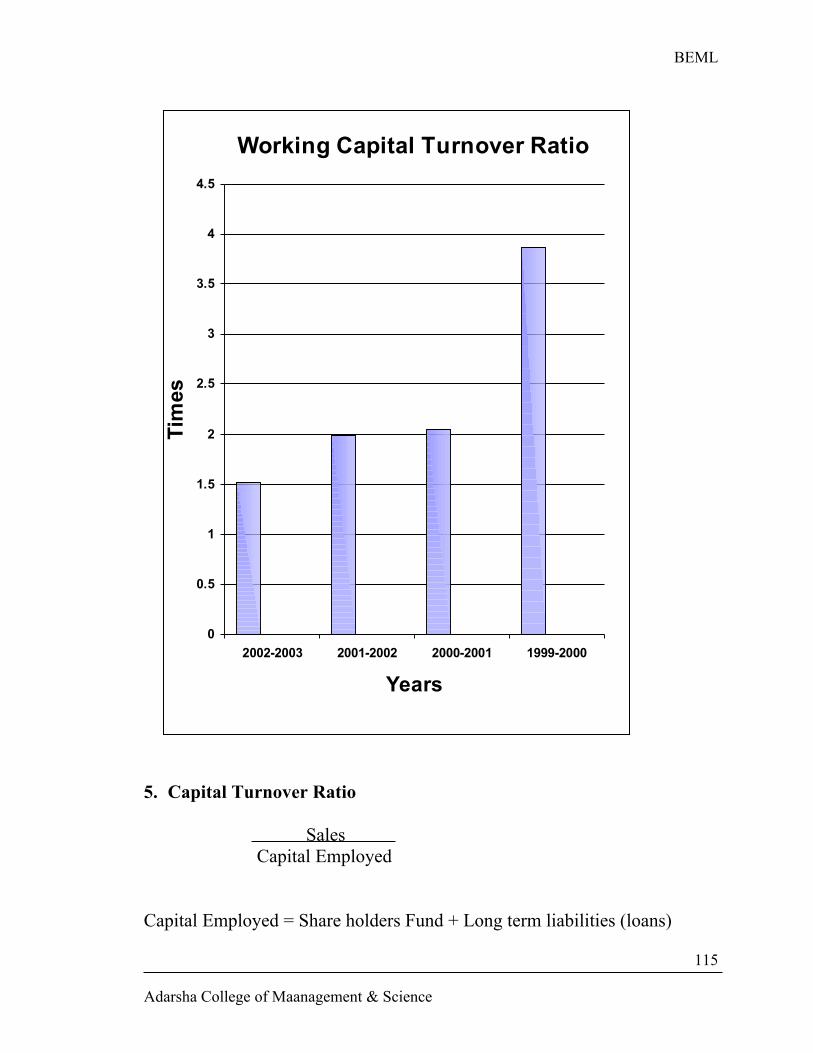

7. Working Capital Turnover Ratio

This is the ratio between working capital & turnover

Expression: Net Sales Working Capital

Interpretation

Adarsha College of Maanagement & Science

28

BEML

Higher Working Capital TOR Ratio indicates the efficiency & low

ratio indicates the inefficiency of the management in the utilization of

working capital.

Profitability Ratios

Profit is the difference between revenues & expenses over a period of

time. Profit is the ultimate output of the company & it will have no future if

it fails to make sufficient profits.

Profitability Ratios reveal the total effect of the business transactions

on the profit position of the enterprise & indicate how far the enterprise has

been successful in its aim.

1) Profit Ratios Related to Sales

2) Profitability in Relation to Investment

1. Profit Ratios Related to Sales

These are the ratios, which are based on the premise that a firm should

earn sufficient profit on each rupee of sales, the difference ratios under this

head are:

i. Profit Margin Ratio

Measures the relationship between profit & sales. The ratios under this

category are:

o Gross Profit Ratio

o Net Profit Ratio

ii. Expenses Ratio

Adarsha College of Maanagement & Science

29

BEML

Expenses refer to operating expenses of a firm exclusive of financial

expenses like interest, taxes & dividends & extra ordinary losses due to theft

of goods, goods loosed by fire etc. Different expense ratios are

o Operating Expenses Ratio

o Cost of Goods Sold Ratio

o Specific Expenses Ratio

2. Profitability Ratios Related to Investments

This is based on the exim that a firm should earn reasonable profits on

the capital invested. The different ratios under this category are

o Return on Assets

o Return on Capital Employed

o Return on Share holder’s Equity Funds

o Return on Equity Capital Ratio

o Earning Per Share

o Dividend Per Share

o Dividend Payout Ratio

o Earnings & Dividend Yield

o Price-Earning Ratio

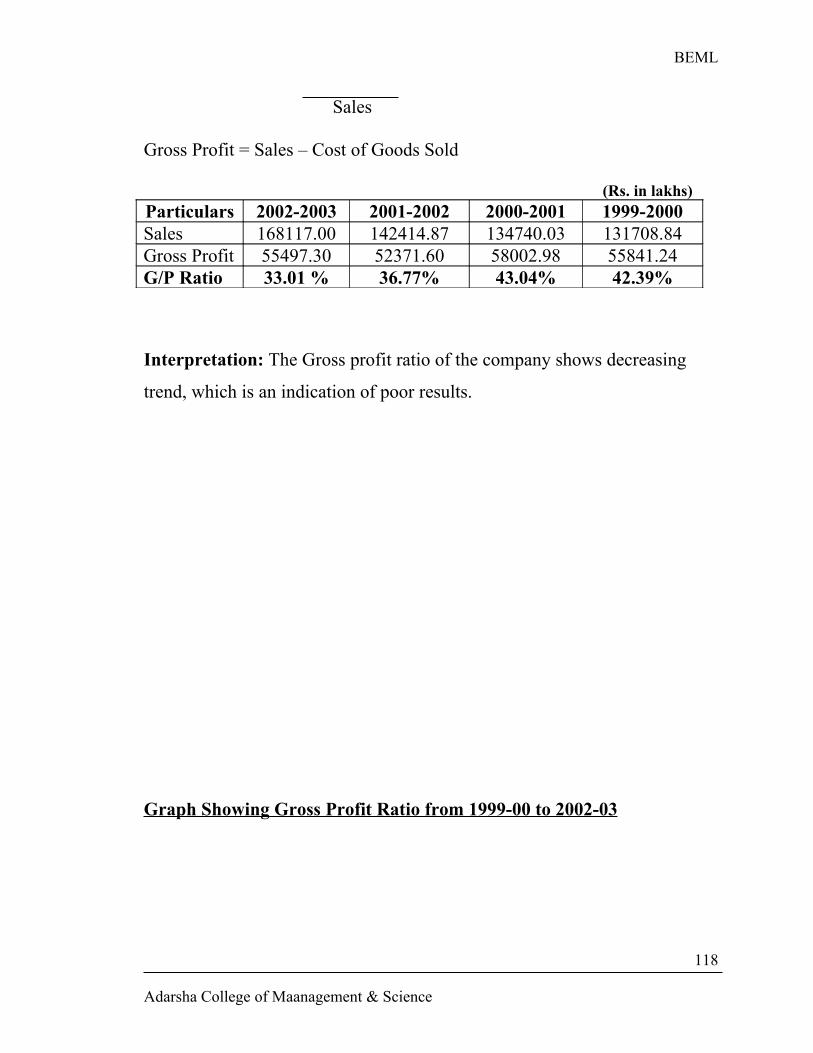

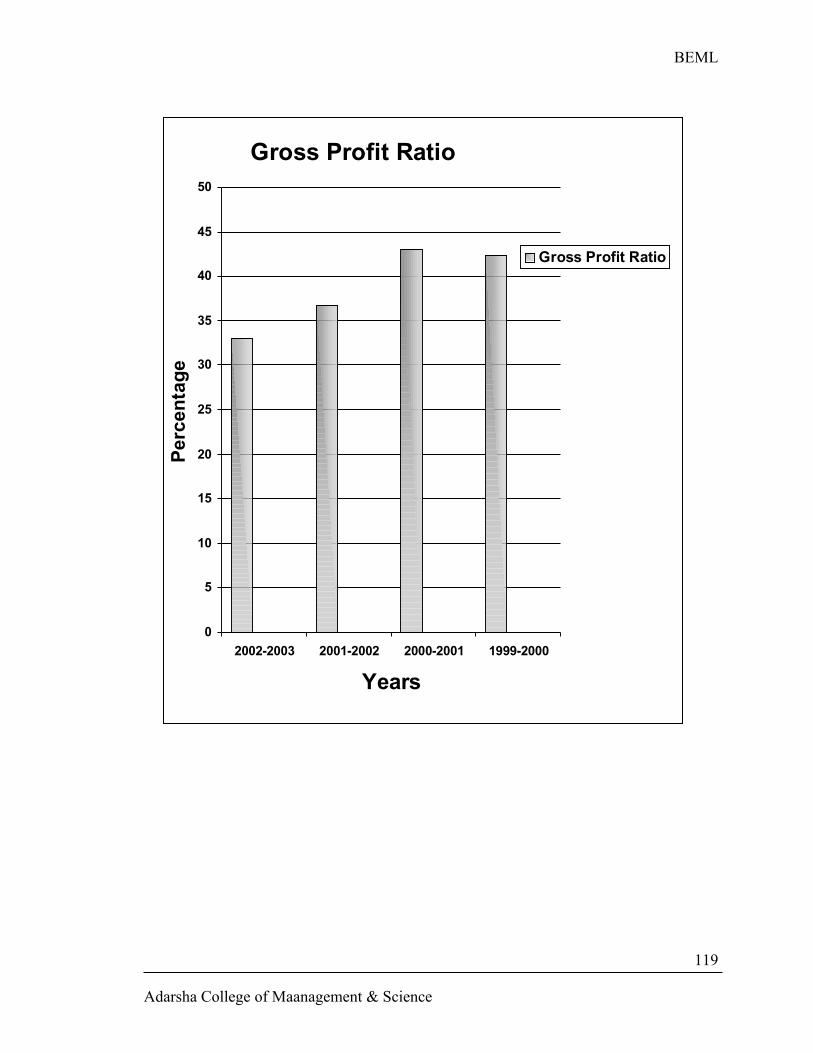

1. Gross Profit Ratio

This is the relationship between gross profit & sales

Expression: Gross Profit * 100 Sales

Interpretation

A high Ratio of G/P to sales is a sign of good management, as it

implies that the cost of production of the firm is relatively low. It may also

Adarsha College of Maanagement & Science

30

BEML

be indicative of higher sales price without a corresponding increase in the

CGS.

2. Net Profit Ratio

This is the ratio between net profit & sales.

Expression: Net Profit * 100 Sales

Interpretation

A high Ratio indicates that profitability of the concern is good & vice

versa in adverse cases.

3. Operating Expenses Ratio

This is the ratio of operating expenses to sales.

Expression: Operating Expenses * 100 Sales

Operating Expenses = CGS + other operating expenses

Interpretation

A low Ratio is an indication of operating efficiency of the business.

4. Cost of Goods Sold Ratio

This is the ratio of CGS to sales

Expression: Cost of Gods Sold Sales

Cost of Goods Sold =Operating Stock+ Purchase – Closing Stock.

5. Specified Expenses Ratio

This is the ratio of specified expenses & sales

i. Factory Expenses Ratio = Factory Expenses * 100 Net Sales

Factory Expenses = Wages, Power etc.

Adarsha College of Maanagement & Science

31

BEML

ii. Administrative Expenses Ratio = Administrative Expenses * 100 Net Sales

Administrative Expenses = Salaries, Office Rent, Printing, Stationary…

iii. Selling & Distribution Expenses Ratio

= Selling & Distribution Expenses * 100 Net Sales

Selling & Distribution Expenses = Advertisement, Cash discounts allowed,

carriage outward etc

Interpretation

A low expense ratio is an indication of the economy & efficiency of

operations. A high ratio is the indication of inefficiency.

6. Return on Assets

This is the ratio of net profit to total assets

Expression: Net Profit after Tax * 100 Total Assets

Interpretation:

A return of 10% is considered as ideal ratio. As such, if the actual

ratio is equal or more than 10%, it indicates the higher productivity of the

total resources/ assets & vice versa in adverse cases.

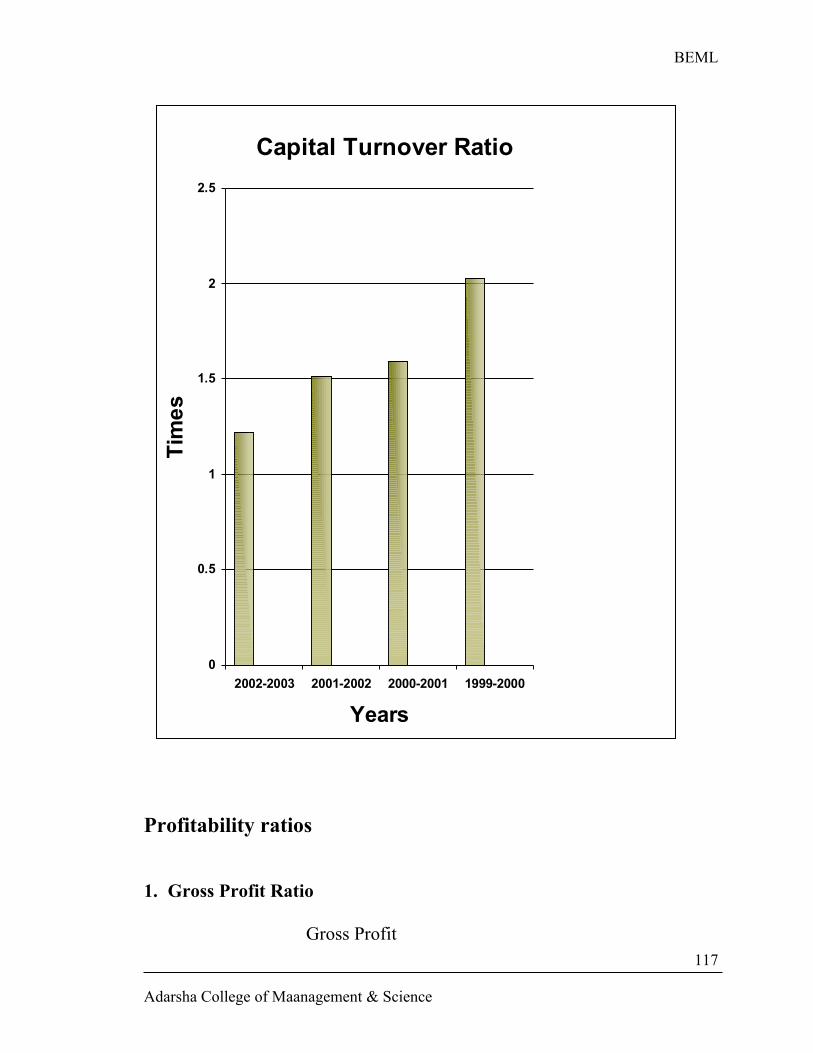

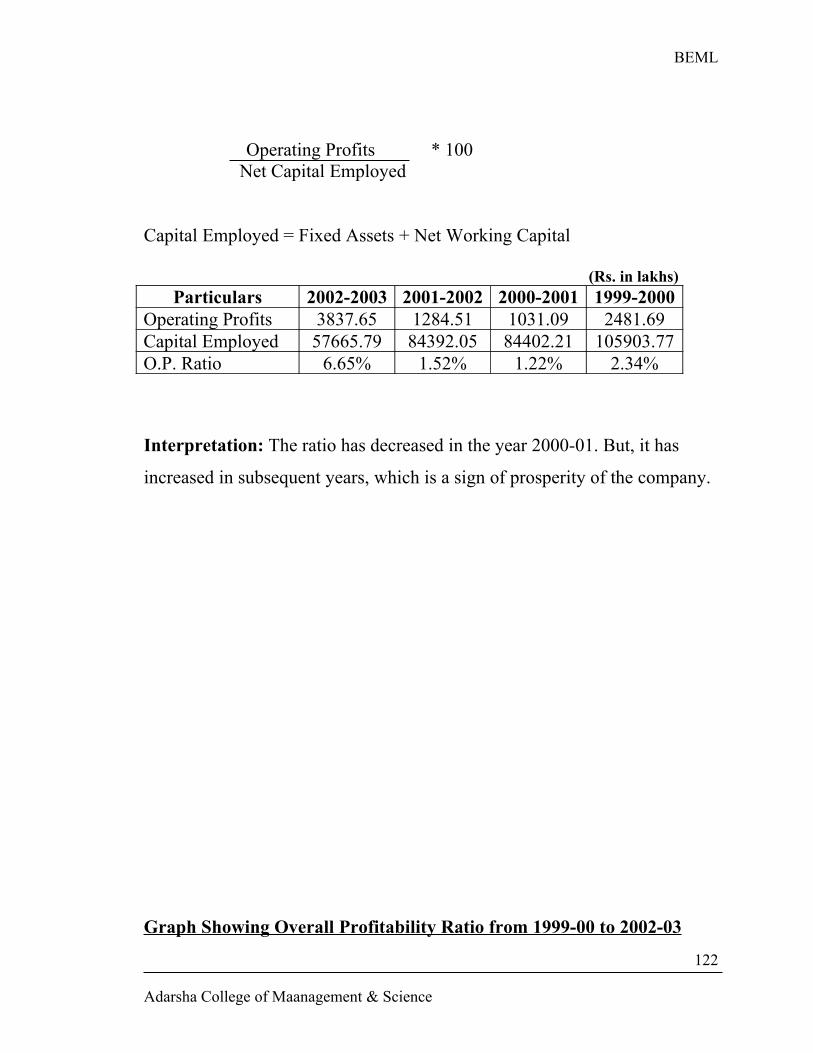

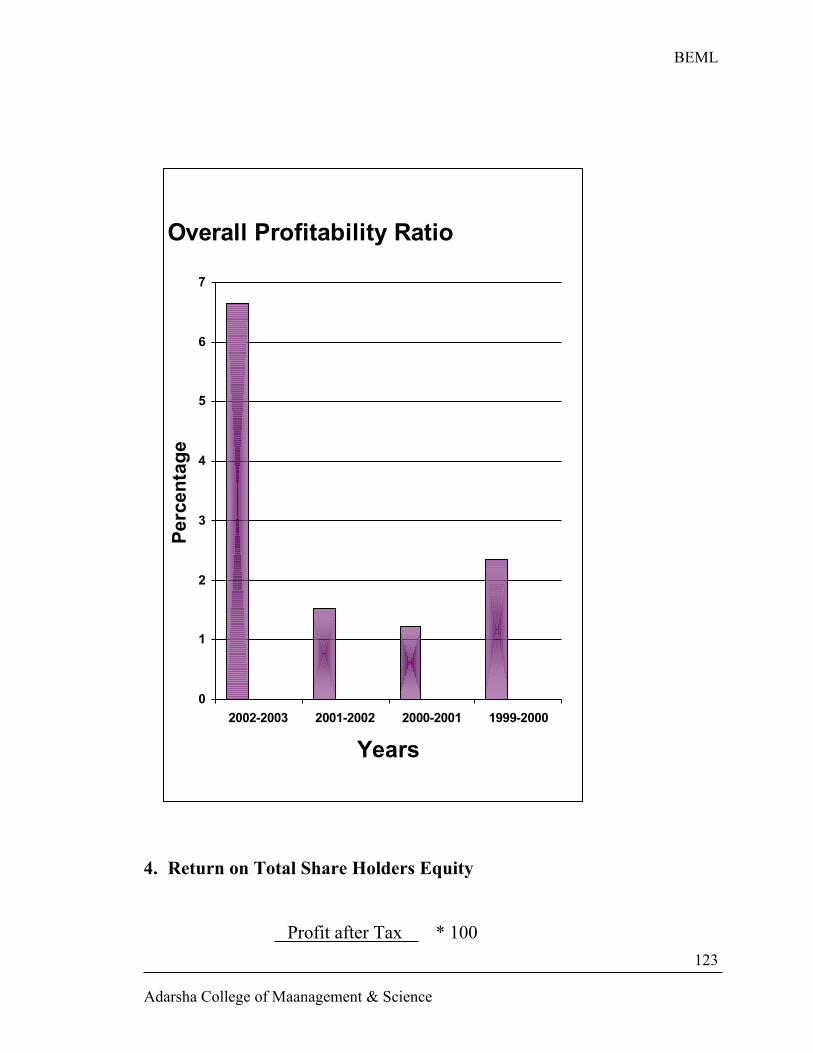

7. Return on Capital Employed

This is the ratio of return on capital employed & capital employed

Return on Capital Employed = EBIT/ Net Profit after Tax

Total Capital Employed =Net Fixed Assets + Trade Investment + W.C.

Expression: Net Profit after Tax * 100 Total Capital Employed

Interpretation

Adarsha College of Maanagement & Science

32

BEML

Ideal ratio is about 15%. Actual Ratio equal or more than 15% is the

indication of higher productivity of capital employed & vice versa.

8. Return on Shareholders Equity

This is the ratio of net profit to net worth.

Expression: Net Profit after Tax (between dividend) * 100 Net worth

Net worth = share capital + share premium + reserves & surplus –

Accumulated loss.

Interpretation:

Ideal ratio is 13%. If actual ratio is equal or more than 13%, it

indicates good return on shareholders fund & vice versa.

9. Return on Equity Capital Ratio

This is the ratio of net profit to equity capital

Expression:

Net Profit available for Equity Share Holder’s * 100Equity Shareholders Fund lonely Equity Capital

Net Profit = Profit after Tax & Dividend

Equity SH Fund = Equity Share Capital + Accumulated Reserves &

Surplus – losses & Fictitious Assets

Interpretation:

There is no ideal ratio. The actual net profit to equity capital ratio is

compared with those of others similar concerns & the productivity of equity

capital is determined.

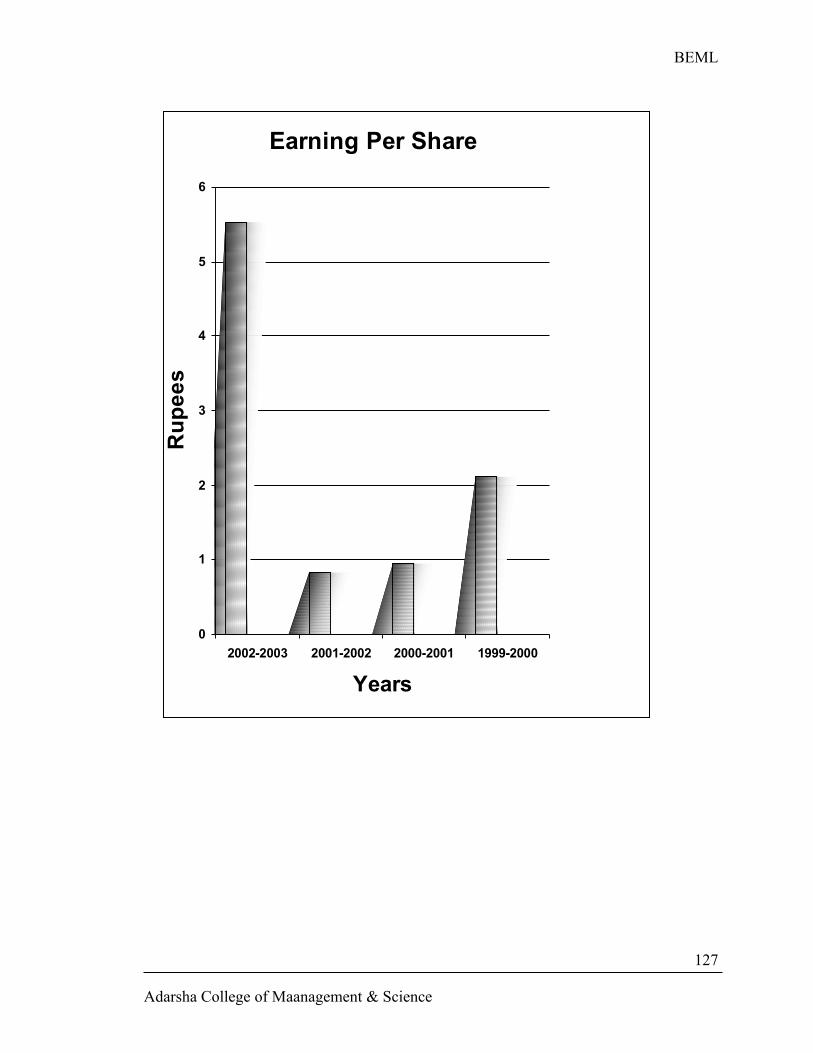

10.Interpreted Earning Per Share

Adarsha College of Maanagement & Science

33

BEML

This is the ratio of Net Profit available for Equity Shareholders i.e.,

Net Profit after tax & dividend to the no of Equity Shares or common shares

outstanding.

Expression: Profit after Tax & Dividend * 100 No of common shares outstanding

Interpretation

The more the EPS, the better is performance & future

prospectus of the company & vice versa.

11.Dividend Per Share

This is the ratio of earnings paid to share holders to number common

shares outstanding.

Expression: Earnings paid to Share Holders Number of Common Shares Outstanding

Interpretation:

A higher ratio attracts investors in shares & vice versa.

12.Dividend Payout Ratio

This is the ratio of Dividend Share to EPS.

Expression: Dividend Per Share EPS

Interpretation :

A high ratio indicates high dividends & low retained profits & vice

versa.

13.Earnings & Dividend Yield

i. Dividend Yield = Dividend Per Share * 100 Market Price of Share

Adarsha College of Maanagement & Science

34

BEML

Interpretation :

If the dividend yield of the company is more than the other company,

it is an indication to the investor that it is worth investing on shares of the

company & vice versa.

ii. Price Earning Ratio

This is the ratio of market price per share to earning per share

Expression: Market Price of Share EPS

Interpretation:

The higher the price, the better are the chances of appreciation in the

market price of shares.

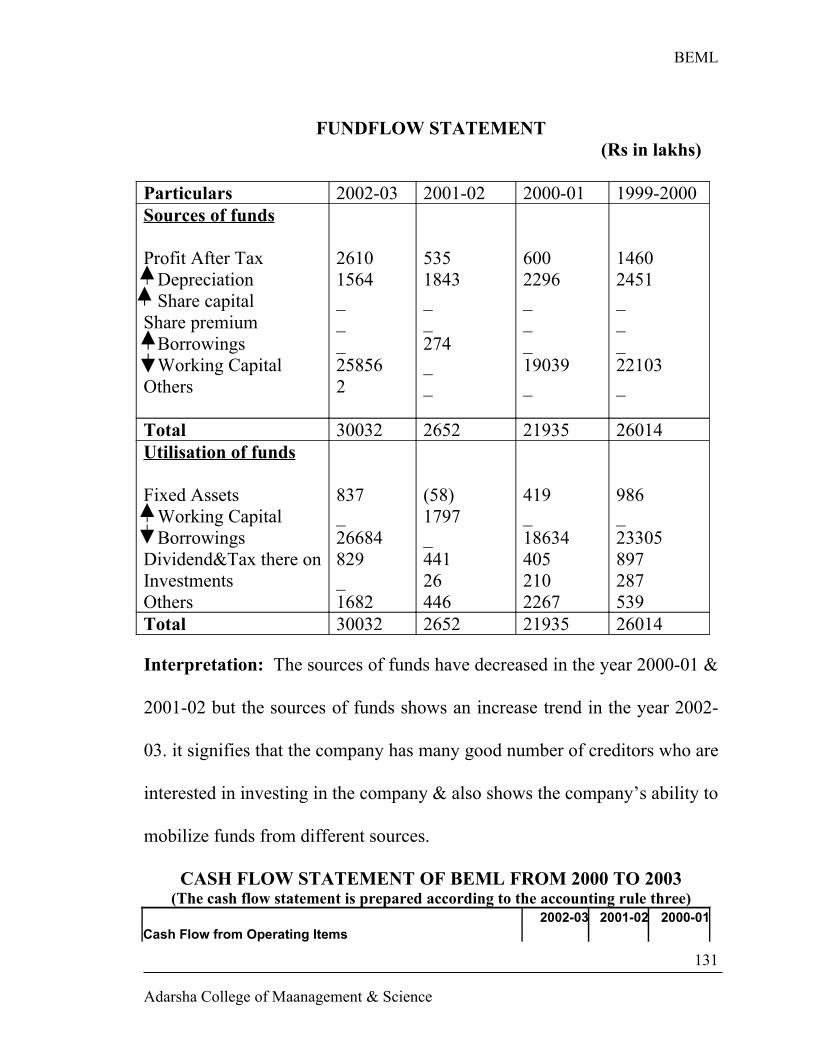

V. FUND FLOW ANAYSIS

FUND

The term fund may be interpreted in various ways, namely as cash, as

total current assets & as net current assets or net w.c.

FUND FLOW

Flow of fund means changes in the amount of fund or net w.c. There

is said to be flow of fund when a business transaction results in change,

either in an increase or in a decrease in the amount of fund or net w.c. If a

transaction results in an increase in the amount of fund, it is considered as

source of fund. If a transaction results in decrease of fund, it is considered as

an application/use of fund.

FUND FLOW STATEMENT

Adarsha College of Maanagement & Science

35

BEML

A fund flow statement is a statement of sources & uses of fund or net

w.c. It is also be defined as a condensed report of how activities of a

business have been financed & how the financial resources have been used

during the period conversed by the statement.

Steps Involved in the Preparation of Fund Flow statement:

i. Preparation of schedule of change in w.c.

ii. Preparation of adjusted profit & loss account to find out funds from

operation.

iii. Preparation of fund flow statement.

Significance

A Fund Flow statement is useful in following ways:

i. It is helpful in knowing sources of fund.

ii. It suggests the way in which w.c. Position can be improved.

iii. It can be used in planning a sound dividend policy.

iv. It is helpful in planning the temporary investment of ideal fund.

v. It is useful in forecasting the fund flow & in projecting the w.c.

requirements.

vi. On a comparison of the fund flow statements of a concern for a numbers

of years, the information about the financial method used in part can be

obtained.

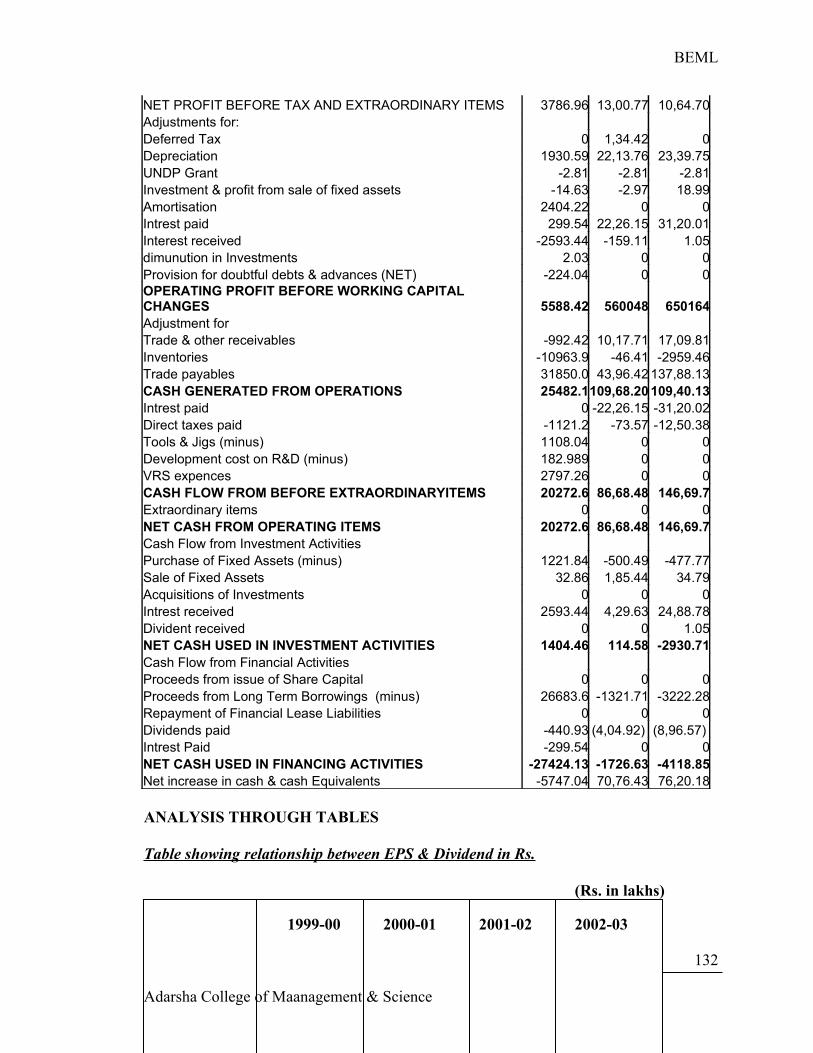

VI. CASH FLOW ANALYSIS

CASH FUND

It includes only cash along with bank balance.

CASH FLOW

Adarsha College of Maanagement & Science

36

BEML

It means actual flow or movement of cash in & out of an

enterprise. The increase in the cash balance implies the inflow of cash,

source of cash or positive cash flow. The decrease in the cash balance

indicates the out flow of cash, application of cash or negative cash flow.

CASH FLOW STATEMENT

It is a statement, which depicts the change in the cash position of a

concern between one balance sheet dates to another. A cash flow statement

is prepared by taking into account the opening & closing cash &bank

balances, various sources of cash & various uses of cash.

STEPS

Ascertainment of operating cash profit.

i) Ascertainment of cash flow from operations.

ii) Preparations of cash flow statement.

Significance

It gives penetration review of cash movements over an operating cycle.

i. It is helpful to a concern to evaluate its current cash position.

ii. It is helpful in determining the policies of financial management like

dividend payments, repayments of long-term loans etc…

iii. It facilitates an affective & efficient cash planning.

iv. It helps the management to analyse the past behavior of the cash cycle,

& to control the uses of cash in future.

Adarsha College of Maanagement & Science

37

BEML

Title of the Project

“A case study on Financial Performance with reference to Bharath Earth

Movers Limited”

Statement of the Problem

The statement of the problem under study is “A case study on

Financial Performance with reference to Bharath Earth Movers Limited”.

This study is made in the light of different tools of financial

management such as, comparative statements, common-size statements,

trend analysis & ratio analysis. The study broadly makes an attempt to

determine the overall financial performance of a company from last few

years. Since finance is an important parameter of every business concern to

determine the growth & profitability, the study of the topics sounds

momentous.

Adarsha College of Maanagement & Science

38

BEML

Purpose of the Study

The study was conducted in BEML for the purpose of fulfillment of

curriculum.

The main purpose is to make the thorough study on the growth &

working of the company from its inception till date.

The purpose is to assess the company’s trend specifically for last four

years with regard to operational performance.

To examine the factors affecting the financial & operational

performance of a company.

To asses the market strength & position of the company.

The main focus is to identify the loopholes of the company & give

suitable solutions to the problem based on analysis.

The study is concerned under this topic, which may help in further

academic education.

Objectives of the Study

To analyse & interpret the financial statements of BEML.

To study validity of tools of financial statements in real life situation.

To know about the soundness of the financial performance of the

company.

To know about the accounting policies & accomplishment of

accounting standards by the company.

To know the capital structure of the company.

To know about the working capital management & dividend policy of

the company.

To gain some practical experience about cash control & cash

management.

Adarsha College of Maanagement & Science

39

BEML

To study history & agenda of the company.

Significance of the Study

An analysis & interpretation of financial statements is very important

in today’s competitive business world. As the study gives a clear picture of

the growth & financial performance of the company, it helps the company to

rectify the errors & it improve in the field of weak performance. It also helps

in framing budgets & in framing dividend policies of the company.

Scope of the Study

The analysis & interpretation of financial statements is made by using

various techniques of analysis, each having their own merits & demerits.

The company to derive meaningful decisions concerning financial matters

can evidently use the report. More over, the study is confined to “Bharat

Earth Movers Limited” only.

Hypothesis

This is an organizational & financial study & hence, there are no

assumptions to be proved or disproved in this report.

Adarsha College of Maanagement & Science

40

BEML

Inception of the Industry

Bharath Earth Movers Limited an acronym for BEML, is a premier

ISO 9000 certified public sector Company, under the administrative control

of ministry defence.

BEML manufacturers the Earth Moving equipments & Defence

products, which build the Nation. It is the largest manufacturer of earth

moving equipments in India & second largest manufacturer in Asia after

Komatsu Industries in Japan.

BEML was incorporated on 11th May 1964 and is one of the few

public sectors earning profits since inception.

BEML commenced operations with the transfer of the Erst while Rail

Coach Manufacturing facilities from then Hindustan Aeronautics Limited

[HAL] at Bangalore on 1st January 1965 [Date of Registration]. Initially

BEML was entrusted with the manufacture of wheeled earth moving

equipments under the collaboration agreement with Government of India &

Westing House Air- Brake Company limited USA [Later renamed as Dress

Adarsha College of Maanagement & Science

41

BEML

Industries]. Subsequently BEML entered into collaboration agreement with

the Komatru Limited, Japan.

Under, the section 43 of the Companies Act, 1956, the provision has

made by treating the private limited company whose turnover exceeds Rs. 1

crore. It was deemed as a public company till 1989. It became a public

limited company by amendment of Articles of Association.

The company status has been changed from wholly Government

Company to partly Government Company. It was incorporated in the year

11-5-1964 with the capital investment of 3198 lakhs in the form of equity

shares capital as a private sector of Rs. 681 lakhs held by the President of

India.

BEML started a unit at KGF complex in the year 1967 for the purpose

of manufacturing Earth Moving Equipments to fulfill the requirements of the

Defence & other sectors of economy.

To maximize the indigenous technology in its products & to support

its production units, BEML has setup a multi crore R&D unit at HP division

in 1979 near KGF complex.

BEML Mysore complex was started in the year 1983 to manufacture

heavy-duty trucks, which were manufactured at KGF complex previously.

Due to lack of space facilities, it shifted its truck unit to Mysore. To develop

its own engines to its products, BEML started Engine division in 1989 at

Mysore, which was imported from M/S Komatsu, Japan.

Type of Organization

Bharat Earth Movers Limited is a public sector company under the

administrative control of Ministry of Defence. BEML is a premier ISO 9000

Adarsha College of Maanagement & Science

42

BEML

Company in India & second largest manufacturer in Asia after Komatsu

Industries in Japan. The total share capital was Rs. 36.87 crores of which

government capital was Rs. 22.50 crores, others Rs. 14.37 crores & revenues

& surplus Rs. 548.27 crores.

Nature of Business

Bart Earth Movers Limited is a multi technology company offering

high-quality products for diverse sectors of economy such as coal, mining,

steel, limestone, power, irrigation, construction, road building, defence &

railways. It has its products range to cover high equity hydraulic aggregates,

heavy-duty diesel engines, welding robots & heavy fabricated structures.

In the last four decades, it has come to the forefront of heavy

Engineering industry & established an undisputed leadership in Earth

Moving industry.

Board of Directors

The board consists of a whole time Chairman & the Managing

Director, Five functional Directors, & Four Promotive Directors holding

responsible positions with vast & varied experience. All of them are

nominated by President of India and also appointed by shareholders.

The Part-time Directors include two from Ministry of Defence, one

from the Ministry of Railways, one from Ministry of Coal & Mines and

another from the Government of Karnataka.

VRS NATARAJAN : Chairman & MD

VENKATANANTHAN : Director (R&D)

RAMESH.C.SUTHAR : Director (Production)

P. MAZUMDAR : Director (Finance)

Adarsha College of Maanagement & Science

43

BEML

K.A. NAGARAJ : Director (Marketing)

B.V. RAMANNA : Director (HRD)

A.P.V.N. SHARMA : Jt. Secretary (coal) [Ministry of Coal &

Mines]

ABHIJIT BARU : Additional Financial Advisor (B) &

Jt.Secretary, [Ministry of Defence]

TAPAN RAY : Jt. Secretary (Export) department of Defence

Production & supplies, [Ministry of Defence]

Market Share

BEML was the first company to enter the earth moving equipment

market & is the market leader holding 70% of market share. It holds 66%

market share in respect of Dozers & Dumpers & 33% in respect of

Excavators. Nearly 40% of its equity has been diverted to Financial

Institutions & public.

Competitors

After the new economic policy of 1991, the economy opened its

floodgates to foreign investment & foreign companies to start their business

in India.

As a result of this, many multi-nationals came into existence to compete

with the domestic industries in all sectors of the economy. As such, BEML

is also facing competition from many MNC’S & domestic industries.

Competitors

Larsen & Turbo -- Komatsu

Hindustan motors

Adarsha College of Maanagement & Science

44

BEML

Tata Engineering & Locomotives Co., Ltd [TELCO]

ESCORTS -- JCB

Godrej

Komatsu -- Japan

Catter Piller -- Russia

Hitachi -- Japan

BE -- USA

Fial

Liebherr Mitobhachi

Volva -- Swiss

Terex -- USA

Dresser Marian -- USA

AUSA -- Australia

O&K

P&H

Collaborations

M/S Komatsu, Industries -- Japan

O mnipol -- Burma

Voest alpine -- Germany

IGM -- Austria

Burma Labedy -- Poland

Letourneau Westing House Co., -- USA

M/S Mit Suimike -- Japan

Indersco

Adarsha College of Maanagement & Science

45

BEML

The flow of state - of the – art technology from global partners has

enabled BEML to achieve high standards in product engineering & gain

international competence.

BANKERS

BEML being a huge organization, should possess better banking

facilitates to meet the timely requirements of capital of the company & also

to fulfill the financial obligations of supplies, customers & other personnel

having relationship with the company.

The Bankers of the company are:

State Bank of India --State Bank of Mysore

Canara Bank --Punjab National Bank

State Bank of Saurarhtra --State Bank of Patiala

Bank of India -- State Bank of Bikaner & Jaipur

Central Bank of India -- Bank of Baroda

Adarsha College of Maanagement & Science

46

BEML

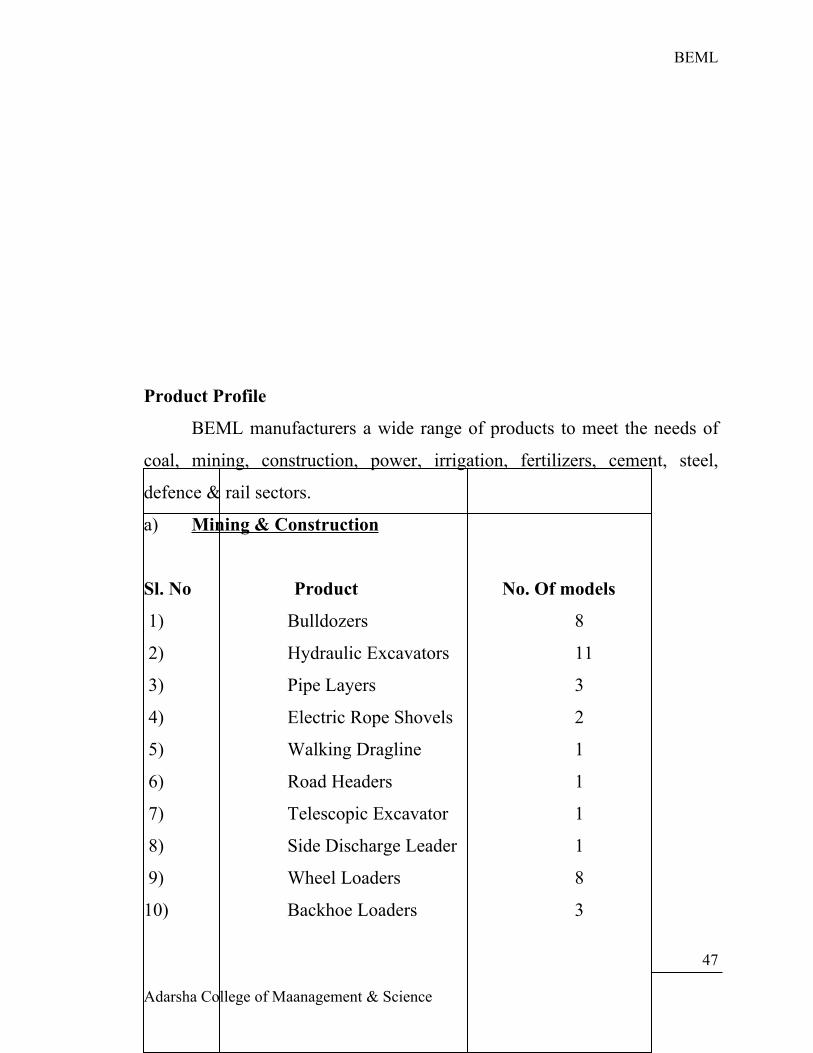

Product Profile

BEML manufacturers a wide range of products to meet the needs of

coal, mining, construction, power, irrigation, fertilizers, cement, steel,

defence & rail sectors.

a) Mining & Construction

Sl. No Product No. Of models

1) Bulldozers 8

2) Hydraulic Excavators 11

3) Pipe Layers 3

4) Electric Rope Shovels 2

5) Walking Dragline 1

6) Road Headers 1

7) Telescopic Excavator 1

8) Side Discharge Leader 1

9) Wheel Loaders 8

10) Backhoe Loaders 3

Adarsha College of Maanagement & Science

47

BEML

11) Motor Graders 3

12) Rear Dumpers 11

13) Bottom Dumpers 2

14) Water Sprinkler 2

15) Wheel Dozers 3

16) Tyre Handler 1

17) Hydraulic Excavator 1

b) Defence

Sl. No. Product No.of models

1) Tatra Heavy Duty Trucles 3

2) Heavy Duty Trailers 2

3) Pontoon Mainstreem Bridge System 1

4) Armovred Recovery Vehicle 1

5) Bridge Layer 1

6) Ammunition Loader 1

7) Radar Carrier Vehicle 1

8) Field Artillery Tractor 1

9) Heavy Recovery Vehicle 1

10) Medium Recovery Vehicle 1

11) Crash Fire Tender 1

12) Aircraft Towing Tractor 1

13) Mine Plough 1

Adarsha College of Maanagement & Science

48

BEML

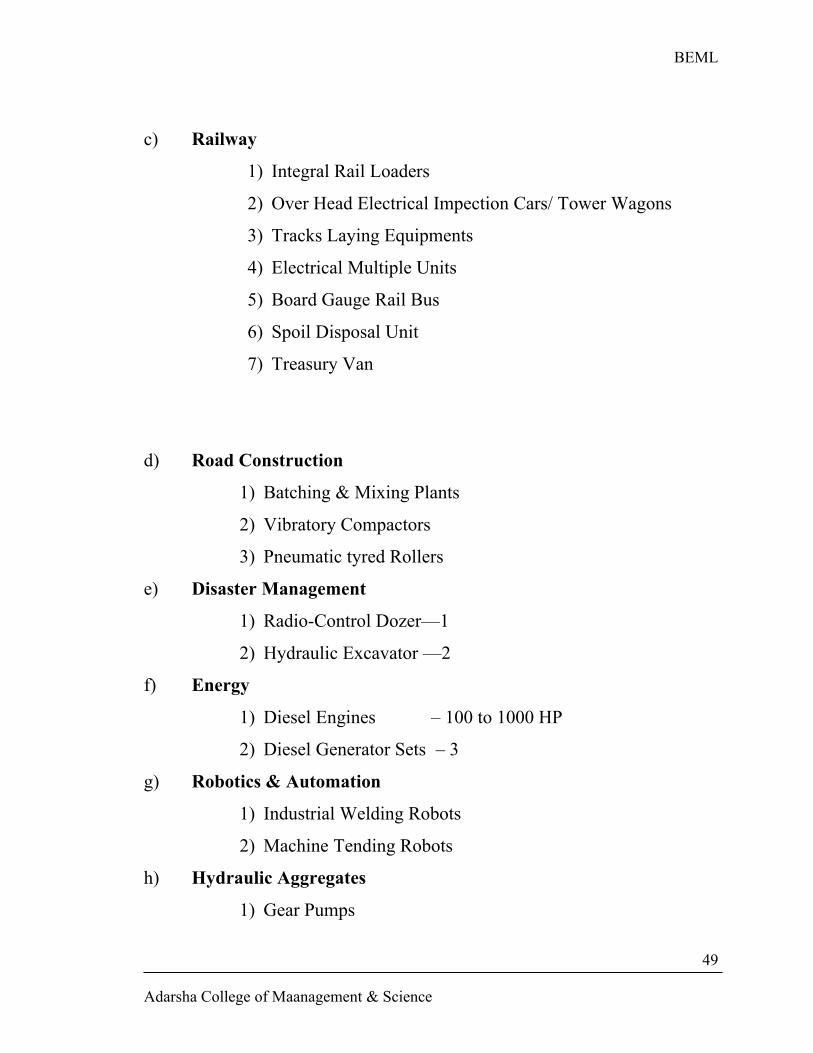

c) Railway

1) Integral Rail Loaders

2) Over Head Electrical Impection Cars/ Tower Wagons

3) Tracks Laying Equipments

4) Electrical Multiple Units

5) Board Gauge Rail Bus

6) Spoil Disposal Unit

7) Treasury Van

d) Road Construction

1) Batching & Mixing Plants

2) Vibratory Compactors

3) Pneumatic tyred Rollers

e) Disaster Management

1) Radio-Control Dozer—1

2) Hydraulic Excavator —2

f) Energy

1) Diesel Engines – 100 to 1000 HP

2) Diesel Generator Sets – 3

g) Robotics & Automation

1) Industrial Welding Robots

2) Machine Tending Robots

h) Hydraulic Aggregates

1) Gear Pumps

Adarsha College of Maanagement & Science

49

BEML

2) Cylinders/ Suspensions

3) Control Values

4) Axels

5) Power Take-offs

Exports

BEML is a recognized export house with star exporter status. Its

strengths in handling large-scale trading & counter-trade have helped it to

push exports of engineering goods & non-military equipments.

The company has established a full-fledged export division for the

purpose of globalising the market. As a top quality supplier of surface

mining equipments, BEML exports machines to over 30 countries

worldwide covering Asia, Africa, Latin America & Middle East.

Export turnover stood Rs. 21.45 crores of which Rs. 12.45 crores

related to physical exports to Abudhabi, Bhutan, South Africa, Tanzania,

Syria & Tunisia. The physical exports were affected by the Middle East

crisis.

BEML plans to further strengthen its global presence by setting up

overseas offices & joint ventures in diverse areas & by executing turnkey

projects in mining & allied fields.

Customers

BEML takes pride in serving its customers who belong to the vital

sectors of the national economy like coal, mining, irrigation, power, steel &

iron ore, defence & railways.

Adarsha College of Maanagement & Science

50

BEML

BEML’S consumers in public sector include Singareni Collieries Co.,

Neyveli Legnite Co., Hindustan Copper Ltd., Hindustan Zinc Ltd., National

Aluminium Co., Ltd., CCL Ltd., SAIL, NHPC, NTPC, etc…

Private Sector: TISCO, Gujarat Ambuja Cements, Modi Cements,

Jayaprakash Associatives etc…

Business Operations

1. Corporate office & Marketing Division

BEML is a vast organization having corporate head office & marketing

division at Bangalore with many regional offices, district offices, spare parts

depots, service centers located in difference parts of country where, BEML

equipments are functioning to ensure efficient after sales services to the

satisfaction of its customers.

The regional offices are at Bangalore, Bilaspur, Kolkota, Hyderabad,

Mumbai, Nagpur, New Delhi, Ranchi, Sambalpur & Singrauli.

The district offices at Asancol, Ahmedabad, Bhilai, Bhuwaneshwar,

Chandrapur, Chennai, Dhanbad, Ghuwahti, Jammu, Kochi/ Ernakulam,

Kothagudam, Neyveli, Panjim, Ramgundam & Udaipur.

2. Manufacturing Units

In order to meet the demands of heavy earthmoving equipments, rail

coaches & heavy-duty trailers, BEML has established units at Bangalore,

KGF, & Mysore. These units are equipped with sophisticated manufacturing

facilities.

Bangalore Complex

BEML started in 1964 with railway equipment division at Bangalore.

This unit is spread over an area of 200 acres. The first rail coach in the

Indian sub continent, this unit has consolidated its status as a major supplier

Adarsha College of Maanagement & Science

51

BEML

of integral rail coaches, meeting about 25% of the country’s demand. It has a

production capacity of over 800 coaches per annum & has work force of

4500 employees. To meet the growing requirements of rail sector, BEML

has diversified into manufacture of overhead equipment, inspection cars &

truck laying equipments. Recently this unit has taken the production of

electric multiple units & rail bus.

The Bangalore unit also manufacturers heavy-duty trucks & trailer, as

also defence aggregates, to meet the needs of the armed forces. Road

headers & side discharge loaders, for use in underground mining are also

produced here.

The factory has comprehensive manufacturing facilities, which are

constantly augmented & modernized to keep pace with the growing

demands of production.

KGF Complex

At Kolar Gold Fields, located 100 kms from Bangalore, spread over an

area of 1850 acres, BEML has established an extensive manufacturing base.

A skilled work force of over 7400 turn out state-of-the-art Bulldozers,

Hydraulic Excavators, Wheel Loaders, Rope Shovels & Walking Draglines

for mining & construction industry. Sophisticated CNC machines & latest

technology welding equipments have been installed.

A multi-million-rupee heavy equipment shop has been setup for major

fabrication work with a capacity of 5000 MT, this shop turns out heavy

structures for industry.

The exclusive Hydraulic and Power [HP] division, manufactures

precision assembles & aggregates, not only for captive consumption but also

Adarsha College of Maanagement & Science

52

BEML

for meeting customer’s requirements. State-of-the-art gear pumps, control

valves, suspensions, cylinders, heavy-duty planetary axels & automatic

transmissions are productionised here.

Mysore Complex

The biggest dumb truck factory in India is located at BEML’s Mysore

Complex. This unit is located about 180 kms from Bangalore & occupies

about 178 acres of land, having a work force of about 2500 employees.

Apart from the popular 35-ton & 50 ton rear dumpers, BEML also

manufactures 85 ton & 120 ton dumpers here. Plans are afoot to take up

manufacture giant 170-ton dumpers on the production line.

The integration of robotized manufacture on the shop floor by installation

of an arc-welding robot for fabrication of giant structures has accelerated the

pace of activity & provides a flexible & powerful facility.

Engine division has been established to manufacture diesel engines of

100-1000 HP rating at Mysore. These are used not only for captive

consumption but also for applications like diesel generators & comrerssors.

The company plans to further expand the division by installing flexible

manufacturing systems.

3. Research & Development

BEML’S growth in Earthmover industry owes a great deal to its strength

in R&D centers located at KGF. Partly founded by the United Nations

Development Programme, the center houses sophisticated laboratories,

powerful computer Aided Design (CAD) facilities, test equipments & a full-

fledged PROTOTYPE manufacturing shop.

Adarsha College of Maanagement & Science

53

BEML

Over 280 qualified Engineers work constantly to improve on product &

develop new equipments to meet market requirements. As many as 30 new

products have been developed in house &have been successfully launched.

Examples include state-of-the-art 35-ton dump truck, aircraft towing tractor,

backhoe loader etc.

Joining hands with several user organizations including defence Research

& Development Organization (DRDO), Department of Science &

Technology (DST) & the Railway Board, BEML has developed several

products successfully.

Subsidiary & Supporting Units

1. Subsidiary Company

BEML has a captive foundry M/S Vignyan Industries limited, at Tarikere

in Karnataka which manufacturers & supplies various types of cartings

required for BEML.

2. Supporting Units

Engine Division (Mysore Complex)

The engine division of BEML situated at Mysore manufactures diesel

engines of 100 to 1000 HP ratings. It also manufactures engines &

generators for their own vehicles like Dozers, Excavators etc.

Hydraulic & Power Line Division (KGF Complex)

BEML started H&P division in the year 1979, in order to meet the area of

hi-tech product range & also to double the share of supplies to vital defence

sector. H&P division manufacturers precession assembles & aggregates not

Adarsha College of Maanagement & Science

54

BEML

only for captive consumption but also for meeting customer’s requirements.

State-of-the-art gear pumps, control valves, suspensions, cylinders, heavy-

duty planetary axles & automatic transmissions are productionised here.

Customer Service

BEML field offices & spare parts depots provide total equipments care &

maintenance support. BEML NET, a dedicated setcom network aims at

streamlining supply of spares across the nation effecting inter-depot transfers

and rationalizing inventories thus, enabling faster response to customers

needs. Service centers located in strategic areas help out users in equipment

rehabilitation as well as overhaul services. In taking service to the doorsteps

of customers, site engineers ensure high availability of machines through

prompt after-sales service. BEML also undertakes to service high-cost

machines throughout their lifetime. BEML also offers credit facility to

prospective buyers of its equipments. Suitable credit packages at competitive

rates are offered duly taking into account, credit rating of customers. All this

activities are aimed at achieving total customers satisfaction.

Perusing Consistent Quality

Quality is the hallmark of excellence in BEML. All manufacturing

facilities are certified under ISO 9000 STD Field trails in actual working

conditions are conducted at BEML’s own testing grounds & tracks.

Future Prospectus and Growth

The growth of the company is directly linked with the development of

core sector and infrastructure in keeping with the importance of road

Adarsha College of Maanagement & Science

55

BEML

infrastructure, the company has planned to introduce several products such

as vibratory compactors, crushing equipments etc with an eye to get a good

share of market for their equipments.

With a view to addressing itself to national interest, BEML has tied up with

Technology Information Forecasting and Assessment Council [TIFAC] for

the manufacture of specialized equipments to be used in disaster

management and is planning to produce them for employment in hazardous

situation.

During the next five years, BEML is planning for diversification activities in

the allied and non-allied areas of business.

Awards & Achievements

♦ Sixth international award to export-Athens

♦ Seventh international award to export-Greece 1984

♦ BEML has won National award for import substitution for its R & D

developed 50 tones tank transportation trailer & crawler mounted shovel

of 2.3 cubic meter capacity.

♦ Corporate Excellence Award for outstanding performance in 1987-88

among all PSU, in the engineering sector in the country instituted by the

department of Public Enterprise, Government of India.

♦ National Safety award won by BEML in the years 1982, 1984, 1985,

1986, 1988 …1999 for longer accident free period.

♦ EEPC’s [Engineering Export Promotion Council] All India Special

Shield for special performance during 88-89, 95-96,96-97 & 1999-2000.

♦ Best productivity award for 1989-90 received from vice-president of

India.

Adarsha College of Maanagement & Science

56

BEML

♦ Special award won by BEML for displaying the most popular working

model at defence & science exhibition in New Delhi.

♦ Company was awarded a standardization commendation award in 1989-

90 & 1990-91 instituted by the Institute of Standards Engineering in

recognition of commandable work done in the field of standardization

improving quality & reducing costs.

♦ BEPC National awards for export excellence in 1995-96 amongst non-

SSI exporters.

♦ Armed forces stage award for employing number of ex-service men for

the yr 1996-97.

♦ National award for 1997 instituted by the Ministry of welfare,

Government of India, for being the outstanding employees of the

physically handicapped.

♦ During the year 2002-03, the Mysore complex equipment division won

the National Safety Award 2000 for achieving the lowest average

frequency rate of accidents. This is the 8th time that the division has

bagged this award.

Adarsha College of Maanagement & Science

57

BEML

Milestones of BEML

1964 - BEML incorporated under Companies Act, 1956 with HQ at

Bangalore. Simultaneously the new company took the

production of rolling stock at rail coach division in Bangalore.

1968 - Heavy Earth Moving division is established at KGF

1979 -Technical Collaboration with Komatsu, Japan finalized.

1985 - Dump Truck division is established at Mysore.

1986 - Received National Import Substitution award from the Ministry of

Science & Technology, Government of India.

1987 - An exclusive Hydraulics & Power line division &a full fledged R&D

center setup at KGF

1988 - Bags National Export award from Ministry of Commerce,

Government of India.

1990 - Asia’s largest 170-ton electric dump truck assembled & launched at

NCL.

1991 - Engine division to manufacture heavy-duty diesel engines comes at

Mysore.

1992 - Gets recognition as export house with Star Exporter Status.

Adarsha College of Maanagement & Science

58

BEML

1994 - Mammoth equipment walking dragline launched.

1994 -BEML goes Public.

1995 - Crosses Rs. 10000 million mark in sales turnover.

1995 - ISO 9000 certification received.

1996 - Major counter-trade agreement with Syria executed against import of

rock Phosphate.

1996 - Dedicated spare parts operation connected to NICNET.

1997 - Recipient of award for best employer of the physically handicapped

from Ministry of Welfare, Government of India.

1998 - Bags orders against World Bank tenders valued at Rs.7000 millions

for equipments supply to CIL projects.

1999 - Integrated hi-tech applications programme implemented in decisions

covering manufacturing, operations and communications.

Adarsha College of Maanagement & Science

59

BEML

ORGANISATIONAL CHART

Director

Marketing

Director Production

Director Finance

DirectorResearch and Development

Director Human

Resources

Adarsha College of Maanagement & Science

Share Holders

Minister of Defence

Chairman and Managing Director

Chief General Manager

General Manager

Deputy General Manager

Asst. General Manager

Manager

Asst. Managers

Engineers

Asst. Engineers

60Supervisors

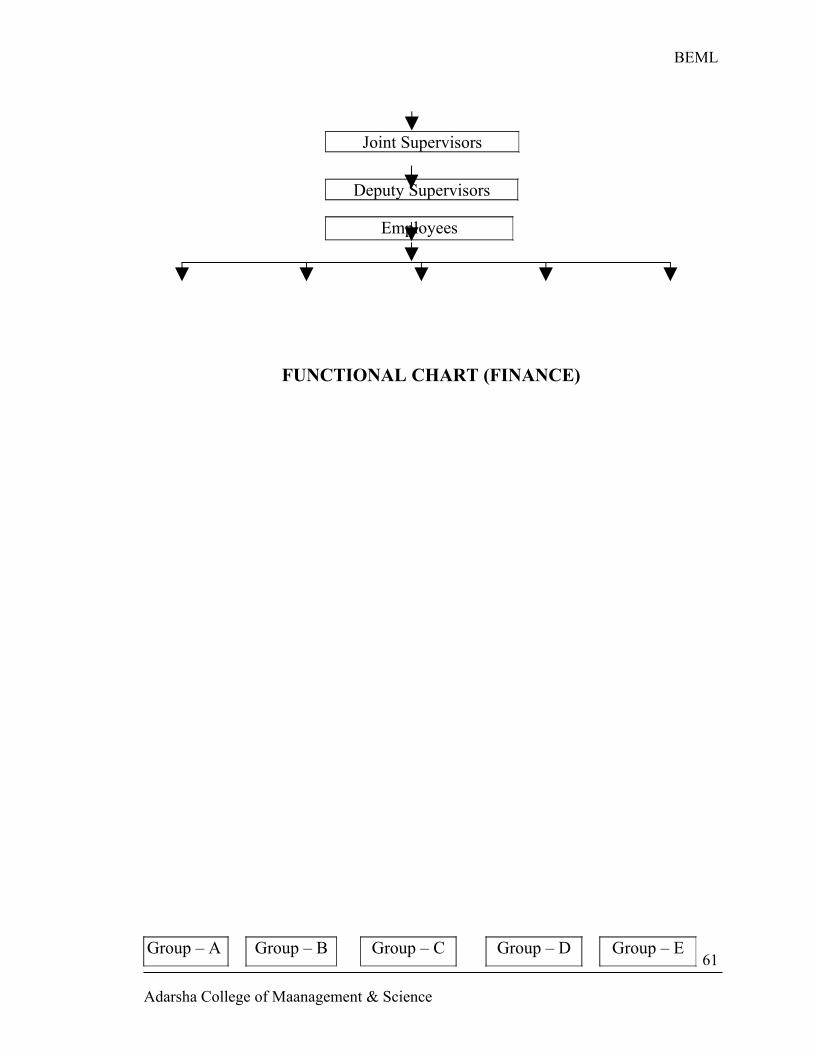

BEML

FUNCTIONAL CHART (FINANCE)

Adarsha College of Maanagement & Science

Joint Supervisors

Deputy Supervisors

Employees

Group – A Group – B Group – C Group – D Group – E61

BEML

Introduction

The quality of the project work depends on the methodology adopted

for the study. Methodology, in turn, depends on the nature of the project

work. The use of proper methodology is an essential part of any research. In

order to conduct the study scientifically, suitable methods & measures are to

be followed.

Research Design

The type of research used for the collection & analysation of the data

is “Historical Research Method”

The main source of data for this study is the past records prepared by

the company. The focus of the study is to determine the performance of the

company since its inception & to identify the ways in which the performance

especially the financial performance of BEML can be improved.

The data regarding company history & profile are collected through

“Explanatory Research Design” particularly through the study of secondary

sources and discussions with individuals.

Data Collection Method

Adarsha College of Maanagement & Science

62

BEML

Data has been collected from both primary & secondary sources.

Primary Data

Having discussions with different department managers & officers of

the company to get general information about the company & its activities.

Having face to face discussions with the company officials

By taking guidance from company guide & departmental guide.

Secondary Data

Collection of data through company annual reports, company manuals

and other relevant documents

By text books & journals

Collection of data through the literature provided by the company.

Research Measuring Tool

The tools used for data collection are:

1. Personal Interview

The authenticity of the study would be more if, the information were

collected through direct interview. In this, discussions are held directly with

the officials & section heads to get the clear-cut information about the topic.

2. Secondary Sources

Annual company reports, Balance Sheets, Profit & Loss account & other

literatures provided by the company, textbooks & journals are also used to

collect the data.

Further, data has been processed using various tools like,

• Comparative Statements

Adarsha College of Maanagement & Science

63

BEML

• Common-size Statements

• Trend Analysis

• Ratio Analysis

Some other vital research measuring tools used for the analysis are

leverages, tables and graphs, various charts etc.

Analysis

The study is concerned with the analysis of the financial statements of

BEML. Analysis of statements and data is done by using some of the

accounting techniques based on the past four-year's balance sheet and

income statements of the company.

Balance sheets, Profit & Loss account, Ratios, Financial Leverages,

Tables & graphs, Charts etc. are used as analysis module, which has made

the study truthful.

Limitations of the Study

1. The study is only on interim reports.

2. It doesn't consider the changes in price level.

3. Changes in accounting procedure by the firm may be misleading.

4. Due to time constraints, all the ratios couldn’t be calculated. Only a few