Download - 7th International Forum Russian Power 2006

Confidential

The Russian Power 2006

7th International Forum

Alexander Abolmasov

Alternative energy vs Traditional

Zindel Investment Partners

2

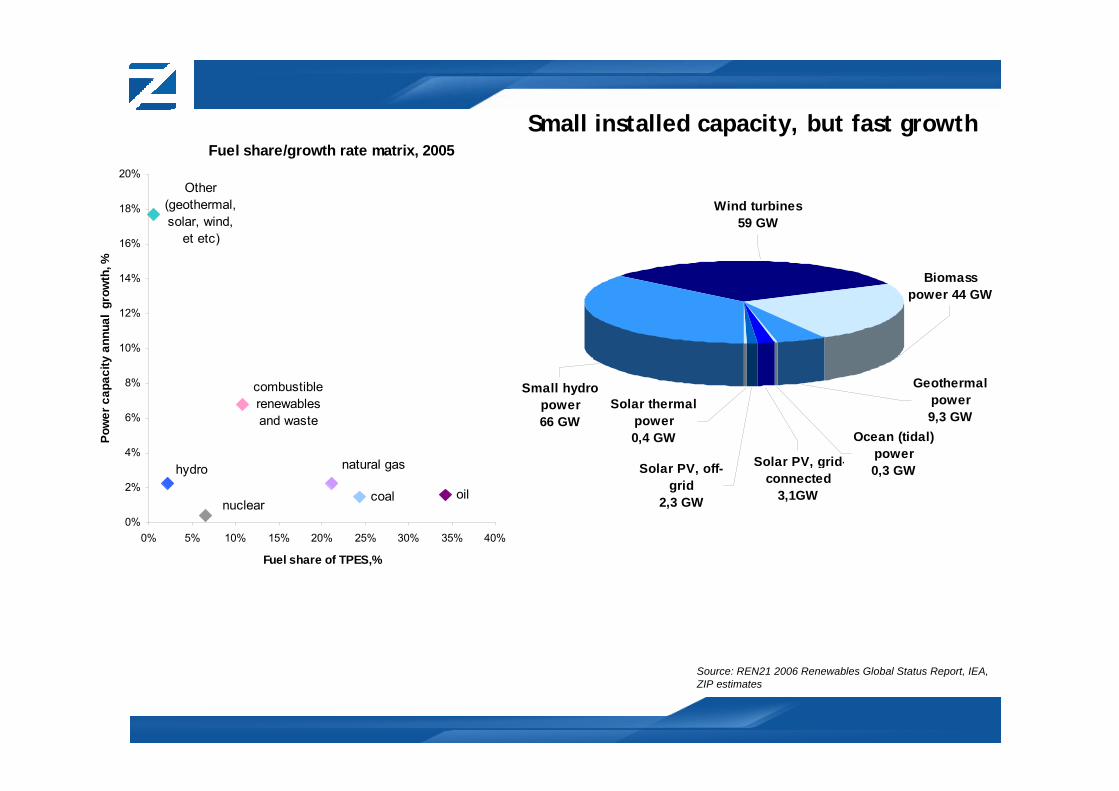

Small installed capacity, but fast growth

Renewable Energy Existing Capacities, 2005

Fuel share/growth rate matrix, 2005

oilcoal

combustible renewables and waste

Other (geothermal,solar, wind,

et etc)

natural gas

nuclear

hydro

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Fuel share of TPES,%

Pow

er c

apac

ity a

nnua

l gr

owth

, %

Ocean (tidal) power0,3 GWSolar PV, grid-

connected3,1GW

Solar PV, off-grid

2,3 GW

Solar thermal power0,4 GW

Geothermal power9,3 GW

Biomass power 44 GW

Small hydro power 66 GW

Wind turbines 59 GW

Source: REN21 2006 Renewables Global Status Report, IEA, ZIP estimates

3

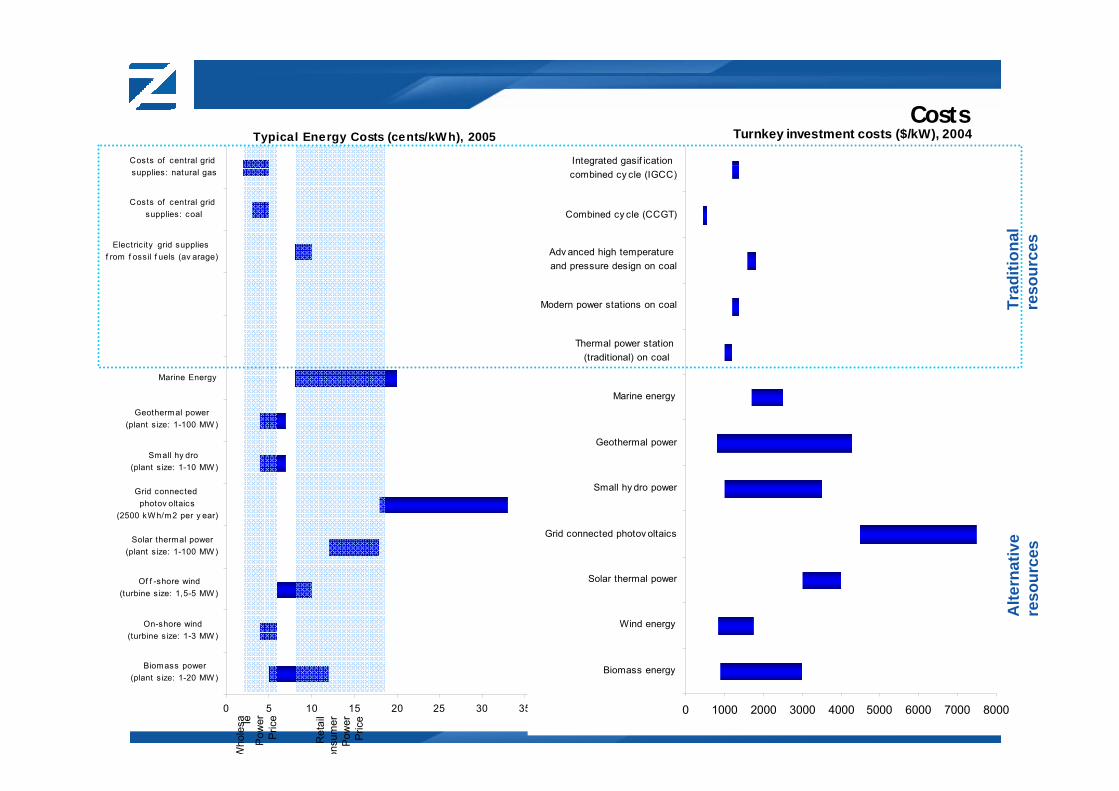

Typical Energy Costs (cents/kWh), 2005

0 5 10 15 20 25 30 35

Biomass power(plant size: 1-20 MW)

On-shore wind(turbine size: 1-3 MW)

Of f -shore wind(turbine size: 1,5-5 MW)

Solar thermal power(plant s ize: 1-100 MW)

Grid connected photov oltaics

(2500 kWh/m2 per y ear)

Small hy dro (plant size: 1-10 MW)

Geothermal power(plant s ize: 1-100 MW)

Marine Energy

Electric ity grid supplies f rom f ossil f uels (av arage)

Costs of central grid supplies: coal

Costs of central grid supplies: natural gas

Turnkey investment costs ($/kW), 2004

0 1000 2000 3000 4000 5000 6000 7000 8000

Biomass energy

Wind energy

Solar thermal power

Grid connected photov oltaics

Small hy dro power

Geothermal power

Marine energy

Thermal power station (traditional) on coal

Modern power stations on coal

Adv anced high temperature and pressure design on coal

Combined cy cle (CCGT)

Integrated gasif ication combined cy cle (IGCC)

Costs

Who

lesa le

Pow

erP

rice

Ret

ail

onsu

mer

Pow

erP

rice

Trad

ition

al

reso

urce

sA

ltern

ativ

e re

sour

ces

4

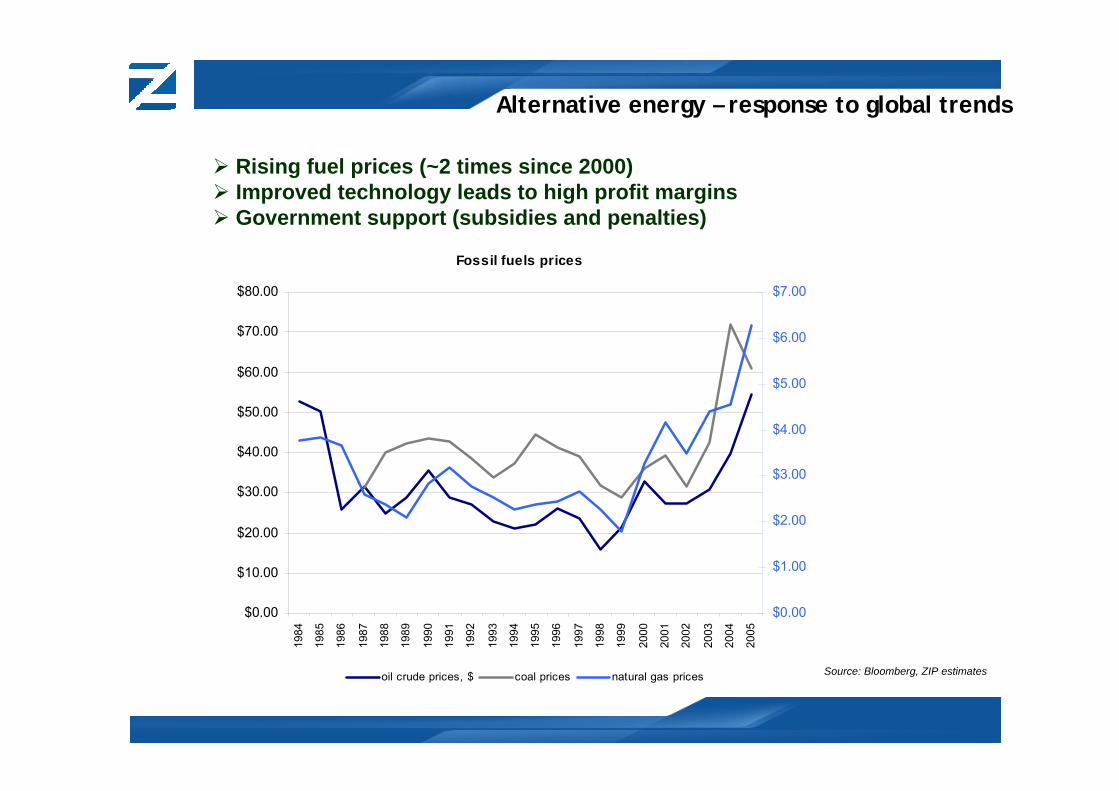

Alternative energy – response to global trends

Fossil fuels prices

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

$80.0019

84

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

oil crude prices, $ coal prices natural gas prices Source: Bloomberg, ZIP estimates

Rising fuel prices (~2 times since 2000)Improved technology leads to high profit marginsGovernment support (subsidies and penalties)

5

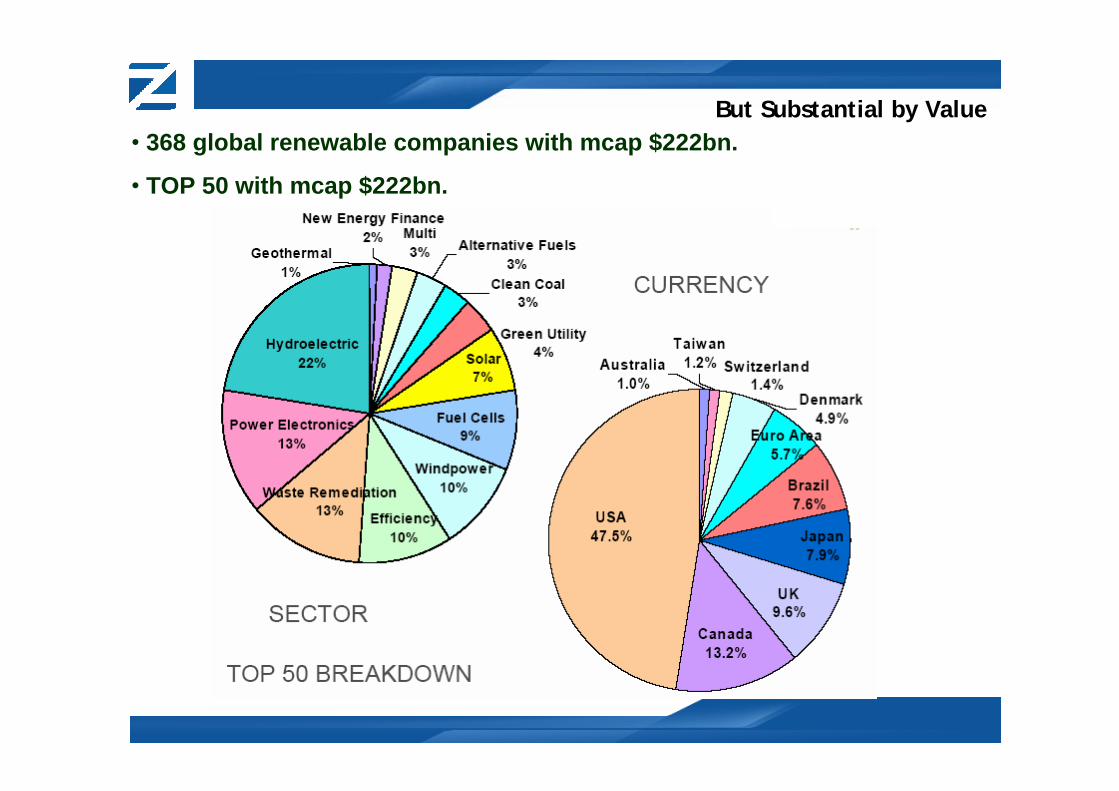

• 368 global renewable companies with mcap $222bn.

• TOP 50 with mcap $222bn.

But Substantial by Value

6

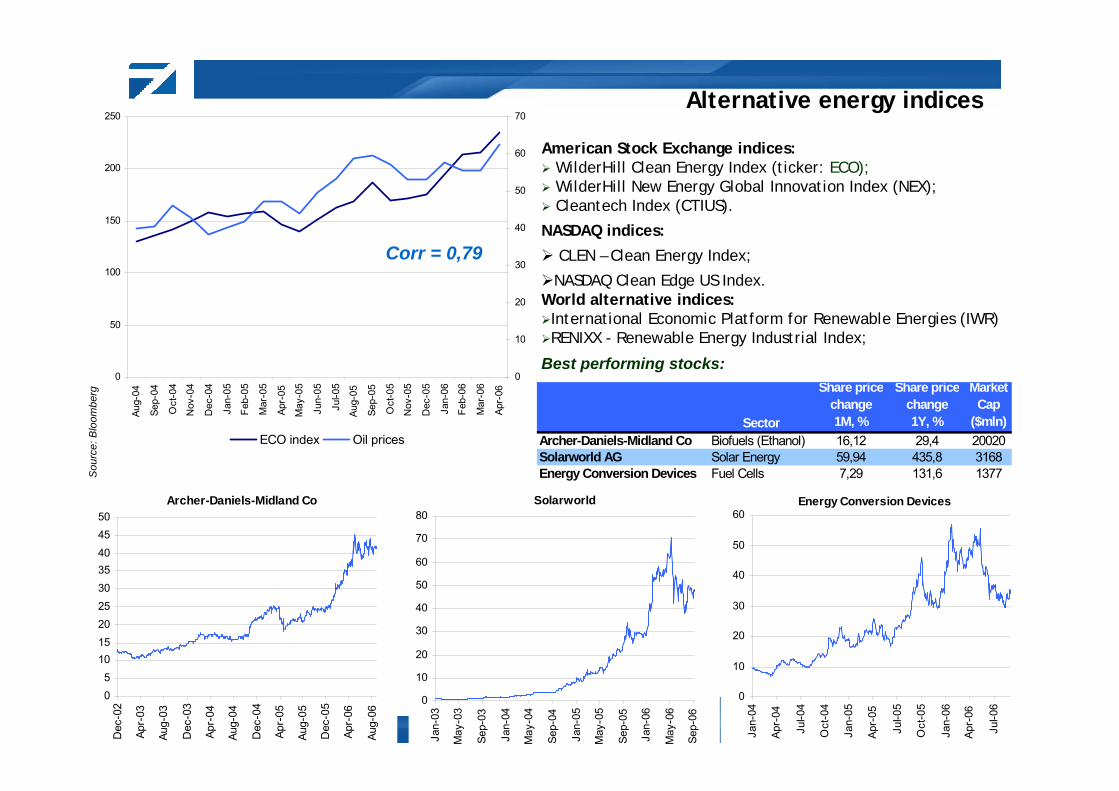

Alternative energy indices

American Stock Exchange indices:WilderHill Clean Energy Index (ticker: ECO);WilderHill New Energy Global Innovation Index (NEX);Cleantech Index (CTIUS).

NASDAQ indices:

CLEN – Clean Energy Index;

NASDAQ Clean Edge US Index.World alternative indices:International Economic Platform for Renewable Energies (IWR)RENIXX - Renewable Energy Industrial Index;

0

50

100

150

200

250

Aug-

04

Sep-

04

Oct

-04

Nov

-04

Dec

-04

Jan-

05

Feb-

05

Mar

-05

Apr-

05

May

-05

Jun-

05

Jul-0

5

Aug-

05

Sep-

05

Oct

-05

Nov

-05

Dec

-05

Jan-

06

Feb-

06

Mar

-06

Apr-

06

0

10

20

30

40

50

60

70

ECO index Oil prices

Corr = 0,79

Archer-Daniels-Midland Co

05

101520253035404550

Dec

-02

Apr-

03

Aug-

03

Dec

-03

Apr-

04

Aug-

04

Dec

-04

Apr-

05

Aug-

05

Dec

-05

Apr-

06

Aug-

06

Solarworld

0

10

20

30

40

50

60

70

80

Jan-

03

May

-03

Sep-

03

Jan-

04

May

-04

Sep-

04

Jan-

05

May

-05

Sep-

05

Jan-

06

May

-06

Sep-

06

Energy Conversion Devices

0

10

20

30

40

50

60

Jan-

04

Apr-

04

Jul-0

4

Oct

-04

Jan-

05

Apr-

05

Jul-0

5

Oct

-05

Jan-

06

Apr-

06

Jul-0

6

Sector

Share pricechange 1M, %

Share pricechange 1Y, %

MarketCap

($mln)Archer-Daniels-Midland Co Biofuels (Ethanol) 16,12 29,4 20020Solarworld AG Solar Energy 59,94 435,8 3168Energy Conversion Devices Fuel Cells 7,29 131,6 1377

Best performing stocks:

Sou

rce:

Blo

ombe

rg

7

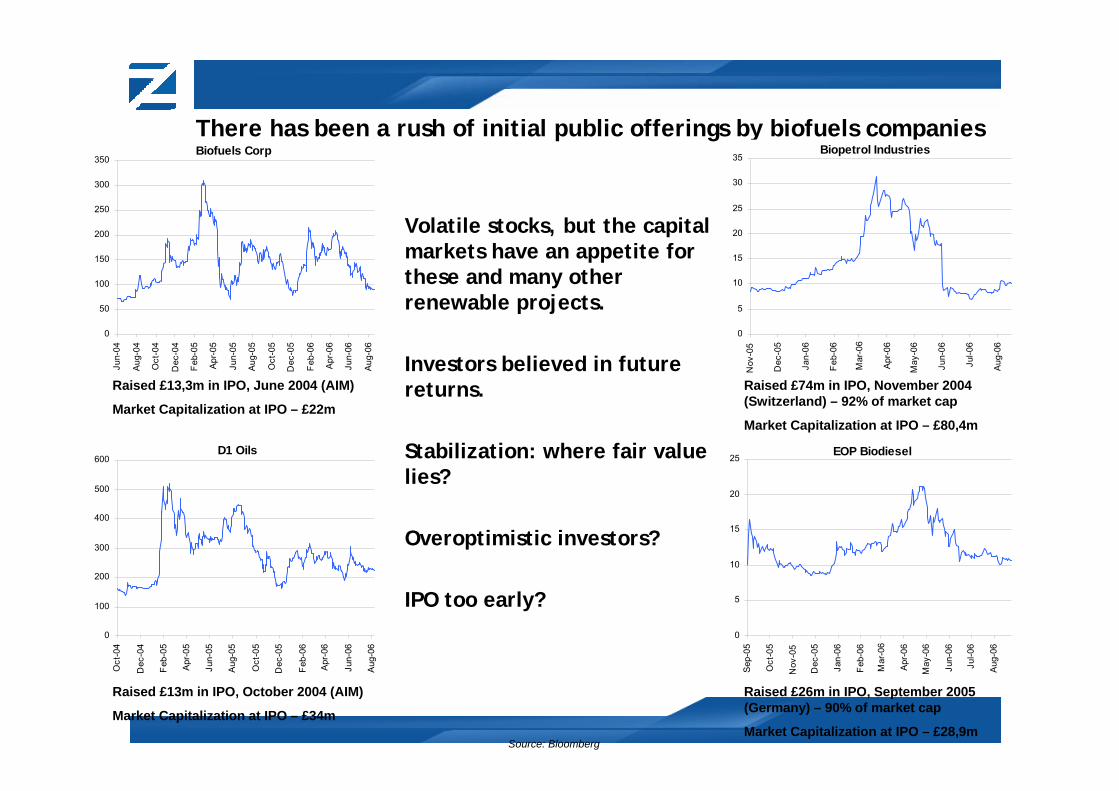

There has been a rush of initial public offerings by biofuels companies

Volatile stocks, but the capital markets have an appetite for these and many other renewable projects.

Investors believed in future returns.

Stabilization: where fair value lies?

Overoptimistic investors?

IPO too early?

Biofuels Corp

0

50

100

150

200

250

300

350

Jun-

04

Aug

-04

Oct

-04

Dec

-04

Feb

-05

Apr

-05

Jun-

05

Aug

-05

Oct

-05

Dec

-05

Feb

-06

Apr

-06

Jun-

06

Aug

-06

D1 Oils

0

100

200

300

400

500

600

Oct

-04

Dec

-04

Feb

-05

Apr

-05

Jun-

05

Aug

-05

Oct

-05

Dec

-05

Feb

-06

Apr

-06

Jun-

06

Aug

-06

Biopetrol Industries

0

5

10

15

20

25

30

35

Nov

-05

Dec

-05

Jan-

06

Feb

-06

Mar

-06

Apr

-06

May

-06

Jun-

06

Jul-0

6

Aug

-06

EOP Biodiesel

0

5

10

15

20

25

Sep

-05

Oct

-05

Nov

-05

Dec

-05

Jan-

06

Feb

-06

Mar

-06

Apr

-06

May

-06

Jun-

06

Jul-0

6

Aug

-06

Raised £13,3m in IPO, June 2004 (AIM)

Market Capitalization at IPO – £22m

Raised £13m in IPO, October 2004 (AIM)

Market Capitalization at IPO – £34m

Raised £74m in IPO, November 2004 (Switzerland) – 92% of market cap

Market Capitalization at IPO – £80,4m

Raised £26m in IPO, September 2005 (Germany) – 90% of market cap

Market Capitalization at IPO – £28,9mSource: Bloomberg

8

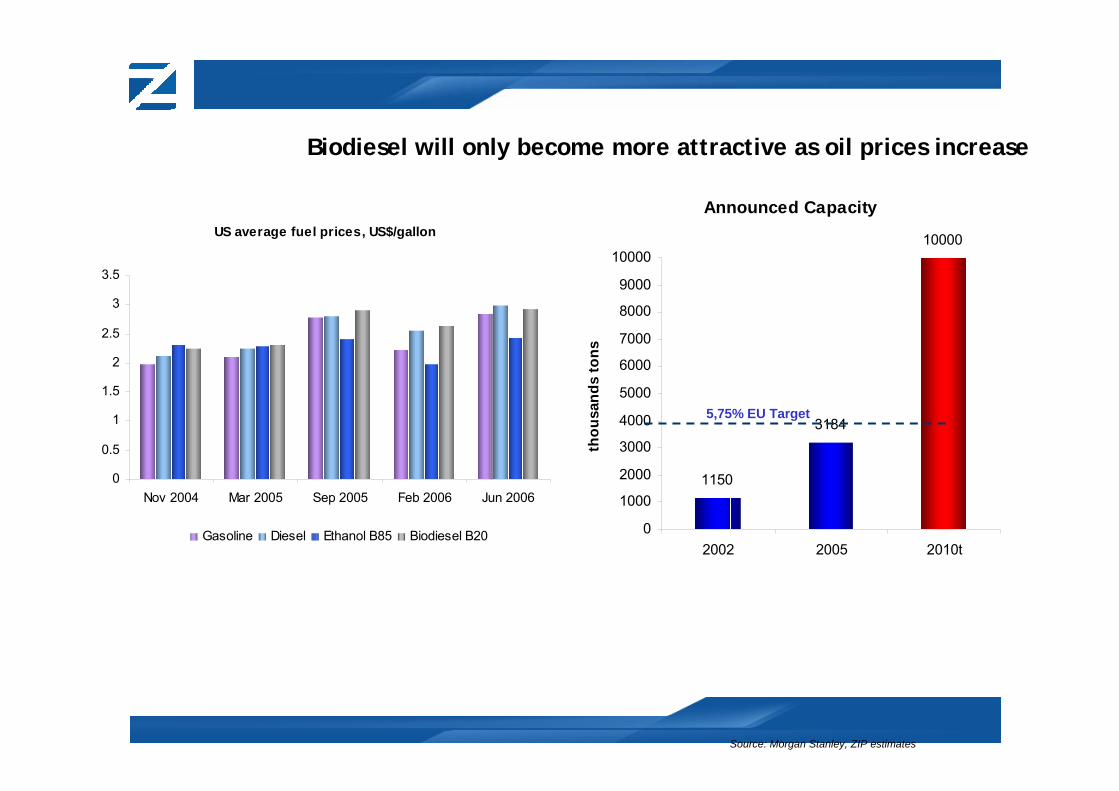

Announced Capacity

1150

3184

10000

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

2002 2005 2010t

thou

sand

s to

ns

Biodiesel will only become more attractive as oil prices increase

5,75% EU Target

Source: Clean Cities Alternative Fuel Report, DOE

Source: Morgan Stanley, ZIP estimates

US average fuel prices, US$/gallon

0

0.5

1

1.5

2

2.5

3

3.5

Nov 2004 Mar 2005 Sep 2005 Feb 2006 Jun 2006

Gasoline Diesel Ethanol B85 Biodiesel B20

9

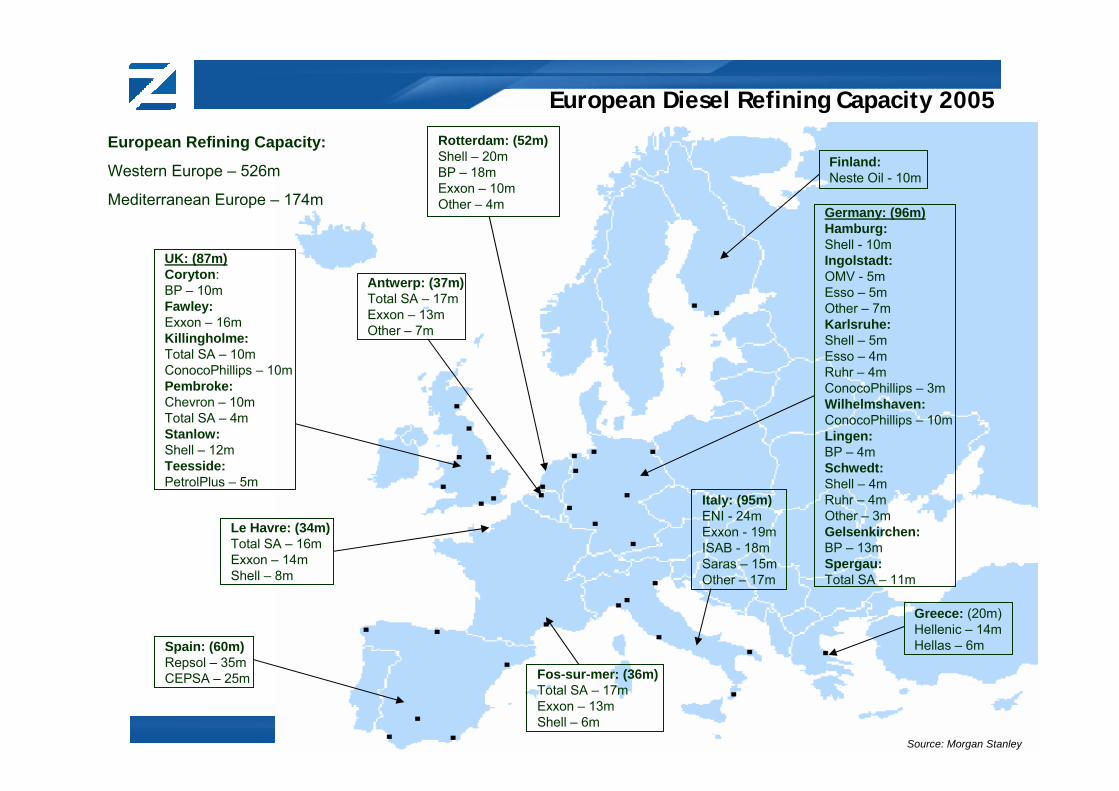

European Diesel Refining Capacity 2005

Finland:Neste Oil - 10m

Germany: (96m)Hamburg:Shell - 10mIngolstadt:OMV - 5mEsso – 5mOther – 7mKarlsruhe:Shell – 5mEsso – 4mRuhr – 4mConocoPhillips – 3mWilhelmshaven:ConocoPhillips – 10mLingen:BP – 4mSchwedt:Shell – 4mRuhr – 4mOther – 3mGelsenkirchen:BP – 13mSpergau:Total SA – 11m

Greece: (20m)Hellenic – 14mHellas – 6m

Fos-sur-mer: (36m)Total SA – 17mExxon – 13mShell – 6m

Italy: (95m)ENI - 24mExxon - 19mISAB - 18mSaras – 15mOther – 17m

Spain: (60m)Repsol – 35mCEPSA – 25m

Le Havre: (34m)Total SA – 16mExxon – 14mShell – 8m

UK: (87m)Coryton:BP – 10mFawley:Exxon – 16mKillingholme:Total SA – 10mConocoPhillips – 10mPembroke:Chevron – 10mTotal SA – 4mStanlow:Shell – 12mTeesside:PetrolPlus – 5m

Rotterdam: (52m)Shell – 20mBP – 18mExxon – 10mOther – 4m

Antwerp: (37m)Total SA – 17mExxon – 13mOther – 7m

European Refining Capacity:

Western Europe – 526m

Mediterranean Europe – 174m

Source: Morgan Stanley

10

Different oil costs, €/ton

334

465

650

365

0

100

200

300

400

500

600

700

Palm oilcosts

Jatropha oilcosts

Soy oil costs Rapeseed oilcosts

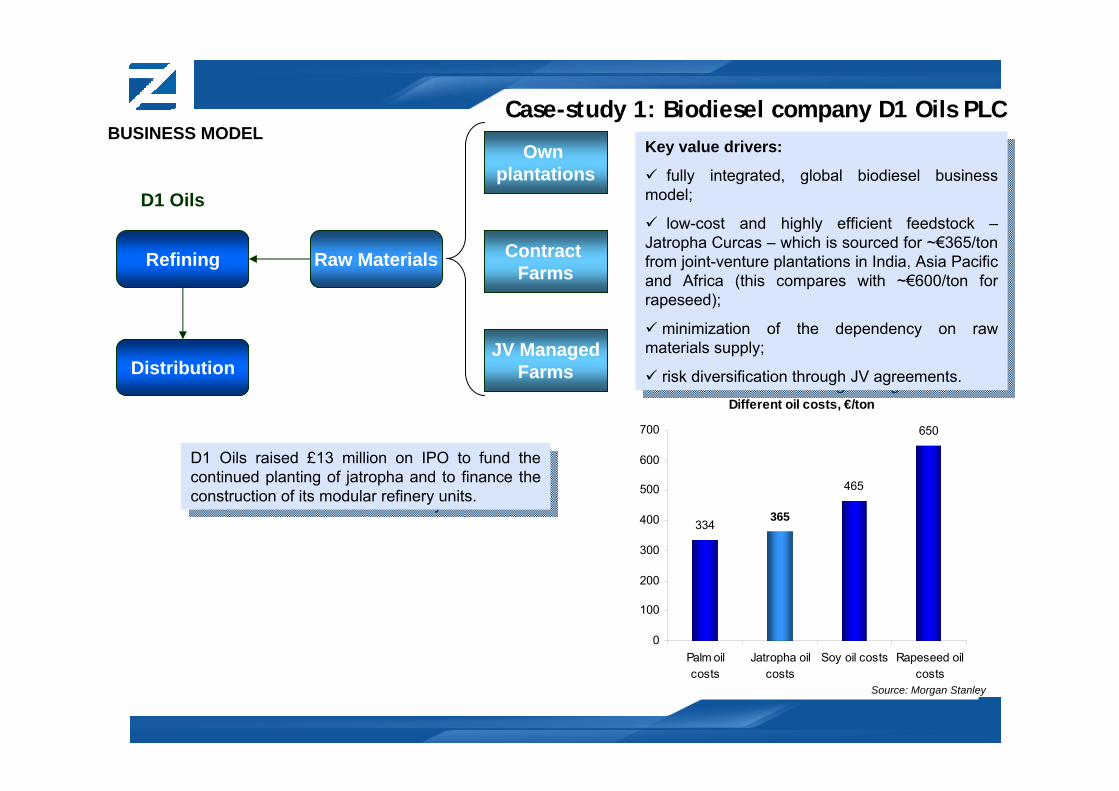

Case-study 1: Biodiesel company D1 Oils PLC

D1 Oils raised £13 million on IPO to fund the continued planting of jatropha and to finance the construction of its modular refinery units.

D1 Oils raised £13 million on IPO to fund the continued planting of jatropha and to finance the construction of its modular refinery units.

BUSINESS MODEL

Refining

Distribution

D1 Oils

Raw Materials

Own plantations

Contract Farms

JV ManagedFarms

Key value drivers:

fully integrated, global biodiesel business model;

low-cost and highly efficient feedstock –Jatropha Curcas – which is sourced for ~€365/ton from joint-venture plantations in India, Asia Pacificand Africa (this compares with ~€600/ton for rapeseed);

minimization of the dependency on raw materials supply;

risk diversification through JV agreements.

Key value drivers:

fully integrated, global biodiesel business model;

low-cost and highly efficient feedstock –Jatropha Curcas – which is sourced for ~€365/ton from joint-venture plantations in India, Asia Pacificand Africa (this compares with ~€600/ton for rapeseed);

minimization of the dependency on raw materials supply;

risk diversification through JV agreements.

Source: Morgan Stanley

11

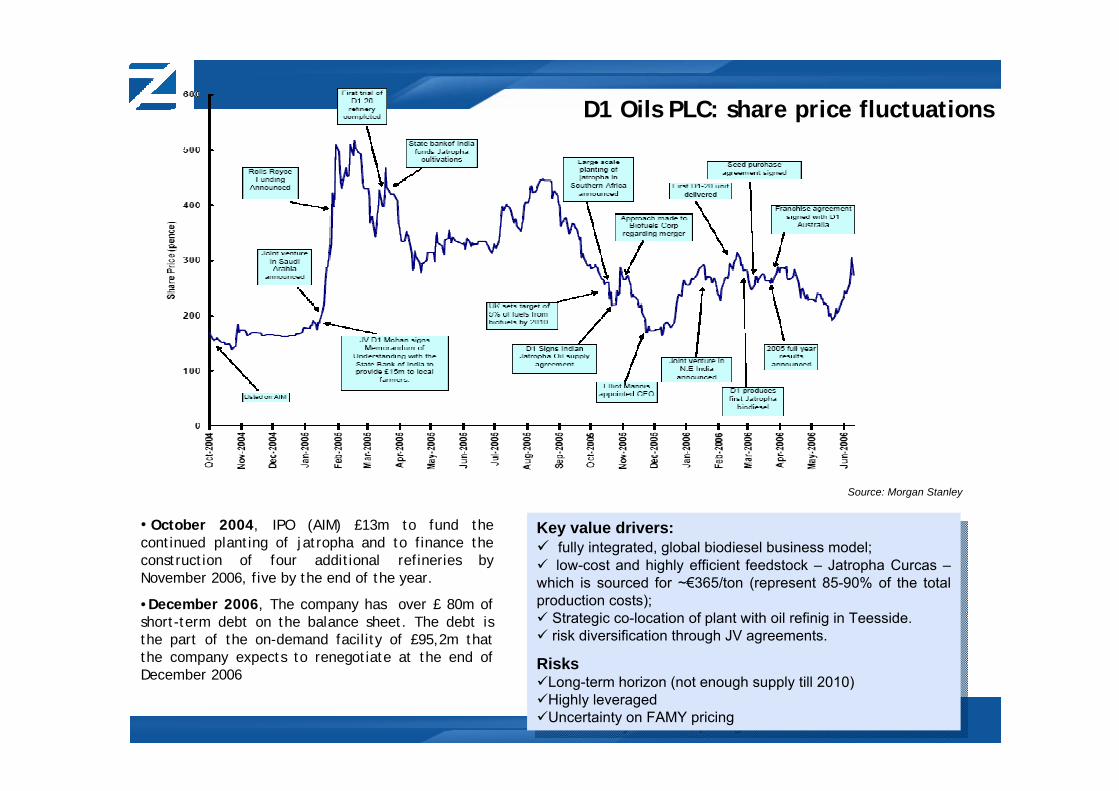

D1 Oils PLC: share price fluctuations

Key value drivers:fully integrated, global biodiesel business model; low-cost and highly efficient feedstock – Jatropha Curcas –

which is sourced for ~€365/ton (represent 85-90% of the total production costs);

Strategic co-location of plant with oil refinig in Teesside.risk diversification through JV agreements.

RisksLong-term horizon (not enough supply till 2010)Highly leveragedUncertainty on FAMY pricing

Key value drivers:fully integrated, global biodiesel business model; low-cost and highly efficient feedstock – Jatropha Curcas –

which is sourced for ~€365/ton (represent 85-90% of the total production costs);

Strategic co-location of plant with oil refinig in Teesside.risk diversification through JV agreements.

RisksLong-term horizon (not enough supply till 2010)Highly leveragedUncertainty on FAMY pricing

• October 2004, IPO (AIM) £13m to fund the continued planting of jatropha and to finance the construction of four additional refineries by November 2006, five by the end of the year.

•December 2006, The company has over £ 80m of short-term debt on the balance sheet. The debt is the part of the on-demand facility of £95,2m that the company expects to renegotiate at the end of December 2006

Source: Morgan Stanley

12

Finland6%Austria

5%

Sweden19%

US8%

Denmark7%

Germany5%

Poland5%

Others (less than 5%)

11%

Canada13%

Baltics11% Russia

10%

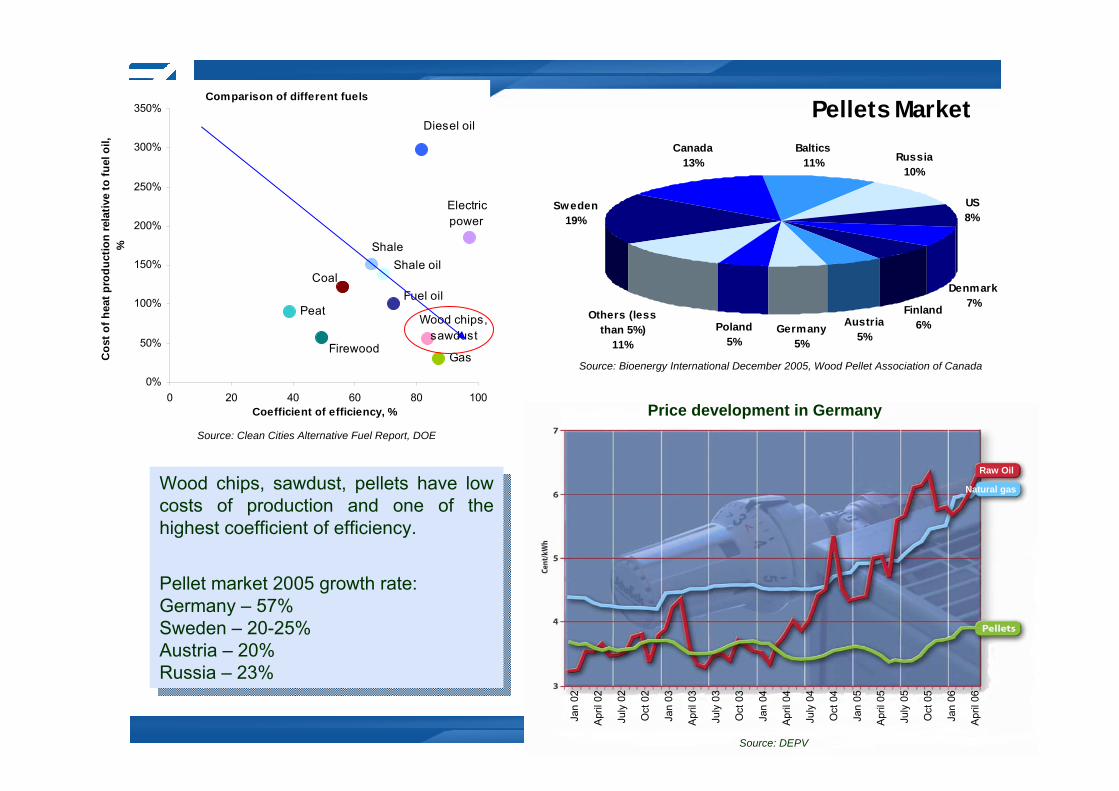

Pellets MarketComparison of different fuels

Gas

PeatWood chips,

sawdust Firewood

Fuel oilCoal

Shale oil Shale

Electric power

Diesel oil

0%

50%

100%

150%

200%

250%

300%

350%

0 20 40 60 80 100Coefficient of efficiency, %

Cos

t of h

eat p

rodu

ctio

n re

lativ

e to

fuel

oil,

%

Wood chips, sawdust, pellets have low costs of production and one of the highest coefficient of efficiency.

Pellet market 2005 growth rate:Germany – 57%Sweden – 20-25%Austria – 20%Russia – 23%

Wood chips, sawdust, pellets have low costs of production and one of the highest coefficient of efficiency.

Pellet market 2005 growth rate:Germany – 57%Sweden – 20-25%Austria – 20%Russia – 23%

Raw Oil

Natural gas

Jan

02

Apr

il 02

July

02

Oct

02

Jan

03

Apr

il 03

July

03

Oct

03

Jan

04

Apr

il 04

July

04

Oct

04

Jan

05

Apr

il 05

July

05

Oct

05

Jan

06

Apr

il 06

Source: DEPV

Source: Clean Cities Alternative Fuel Report, DOE

Price development in Germany

Source: Bioenergy International December 2005, Wood Pellet Association of Canada

13

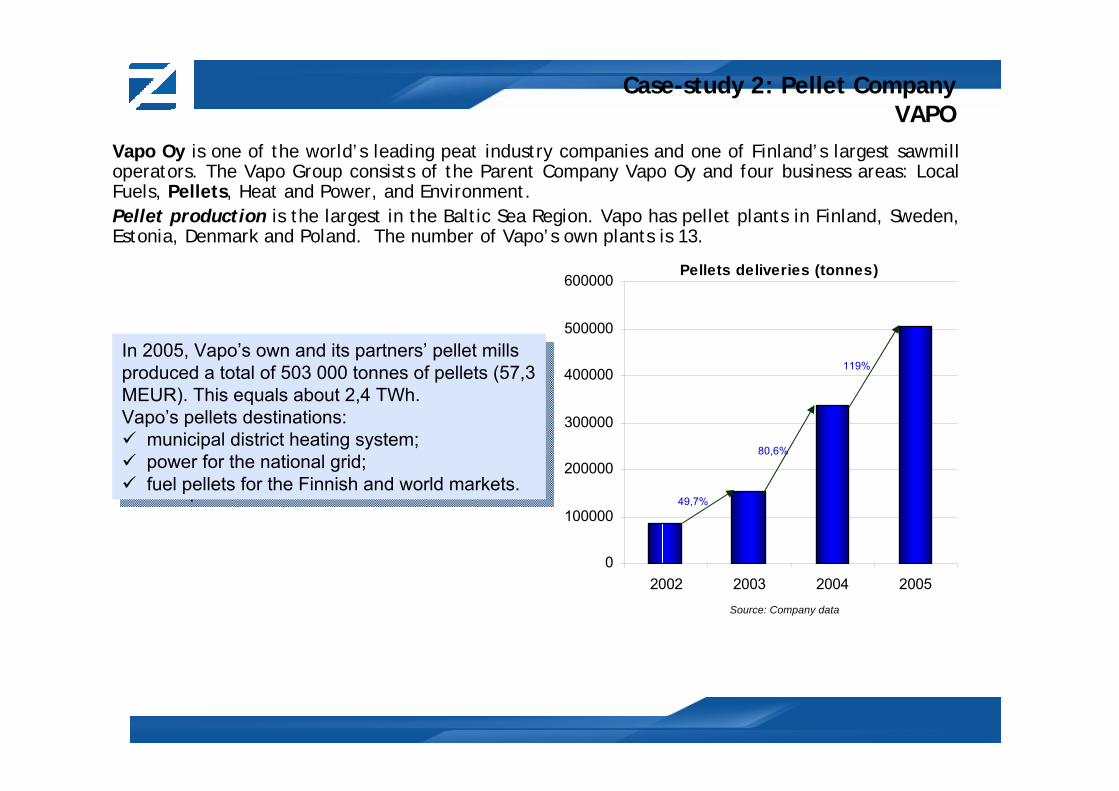

Case-study 2: Pellet CompanyVAPO

Vapo Oy is one of the world’s leading peat industry companies and one of Finland’s largest sawmill operators. The Vapo Group consists of the Parent Company Vapo Oy and four business areas: Local Fuels, Pellets, Heat and Power, and Environment. Pellet production is the largest in the Baltic Sea Region. Vapo has pellet plants in Finland, Sweden, Estonia, Denmark and Poland. The number of Vapo’s own plants is 13.

Pellets deliveries (tonnes)

0

100000

200000

300000

400000

500000

600000

2002 2003 2004 2005

80,6%

49,7%

119%In 2005, Vapo’s own and its partners’ pellet mills produced a total of 503 000 tonnes of pellets (57,3 MEUR). This equals about 2,4 TWh.Vapo’s pellets destinations:

municipal district heating system;power for the national grid;fuel pellets for the Finnish and world markets.

In 2005, Vapo’s own and its partners’ pellet mills produced a total of 503 000 tonnes of pellets (57,3 MEUR). This equals about 2,4 TWh.Vapo’s pellets destinations:

municipal district heating system;power for the national grid;fuel pellets for the Finnish and world markets.

Source: Company data

14

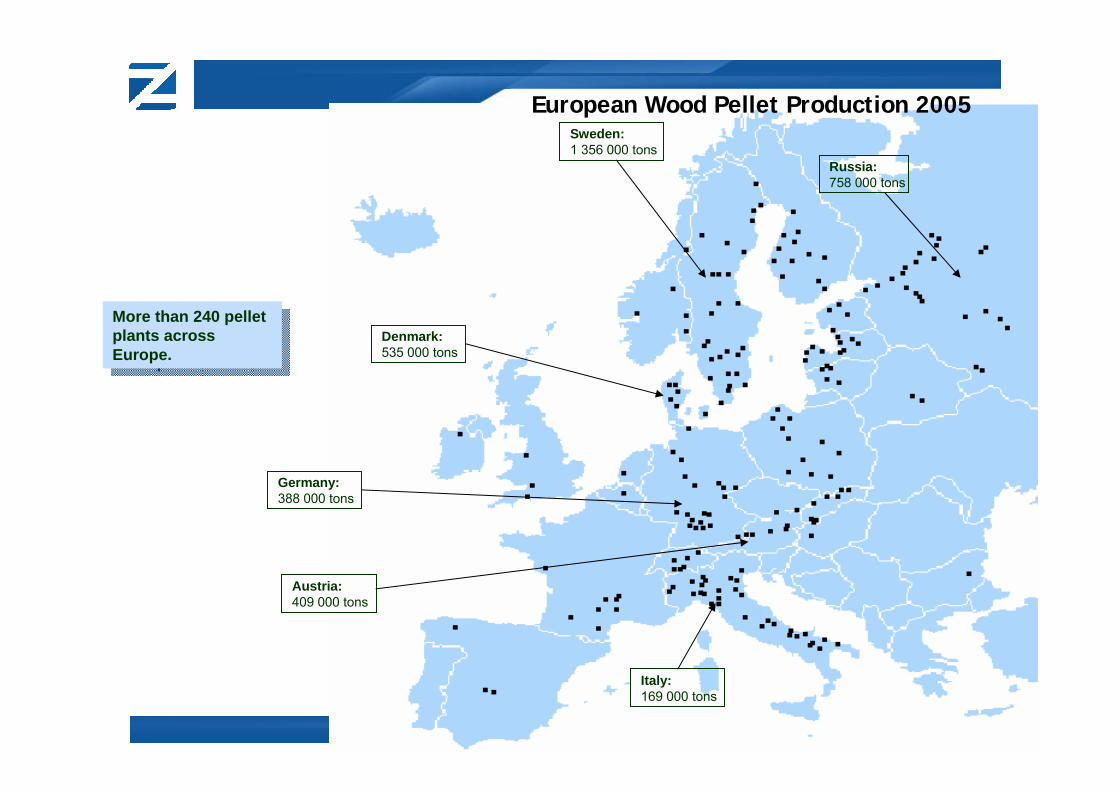

European Wood Pellet Production 2005

More than 240 pellet plants across Europe.

More than 240 pellet plants across Europe.

Sweden:1 356 000 tons

Russia:758 000 tons

Denmark:535 000 tons

Germany:388 000 tons

Austria:409 000 tons

Italy:169 000 tons

15

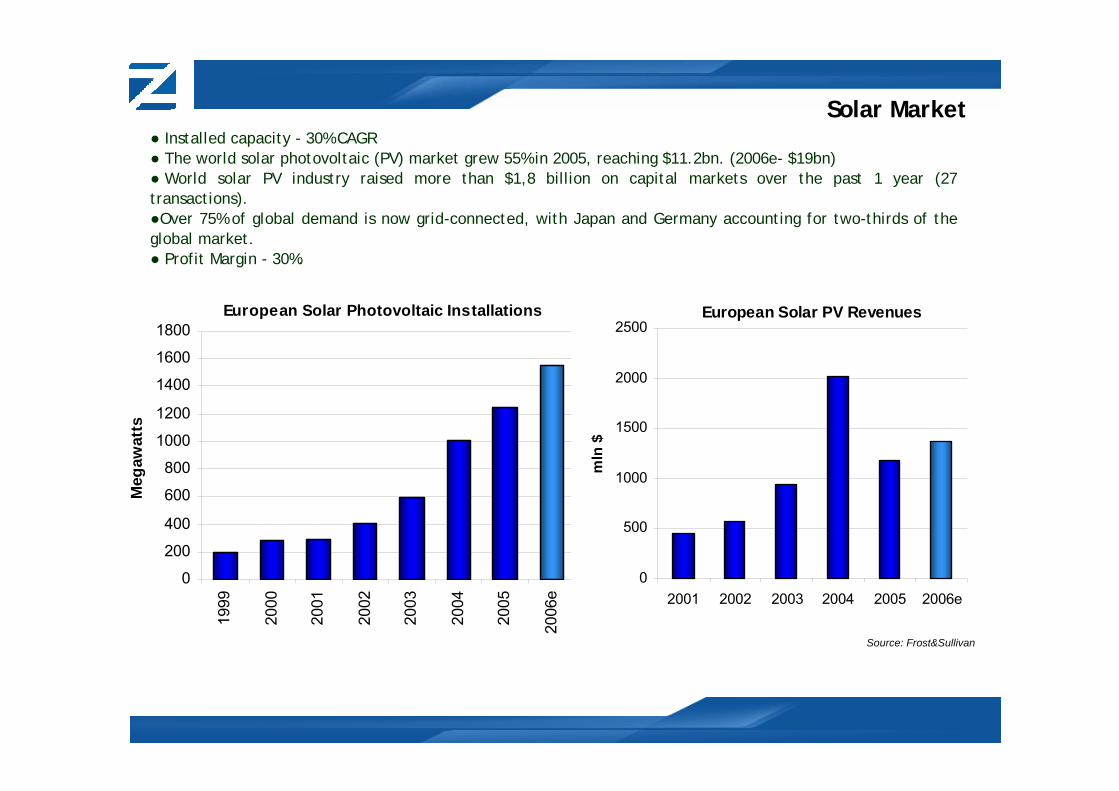

European Solar Photovoltaic Installations

0

200

400

600

800

1000

1200

1400

1600

1800

1999

2000

2001

2002

2003

2004

2005

2006

e

Meg

awat

tsSolar Market

● Installed capacity - 30% CAGR ● The world solar photovoltaic (PV) market grew 55% in 2005, reaching $11.2bn. (2006e- $19bn)● World solar PV industry raised more than $1,8 billion on capital markets over the past 1 year (27 transactions). ●Over 75% of global demand is now grid-connected, with Japan and Germany accounting for two-thirds of theglobal market. ● Profit Margin - 30%.

European Solar PV Revenues

0

500

1000

1500

2000

2500

2001 2002 2003 2004 2005 2006em

ln $

Source: Frost&Sullivan

16

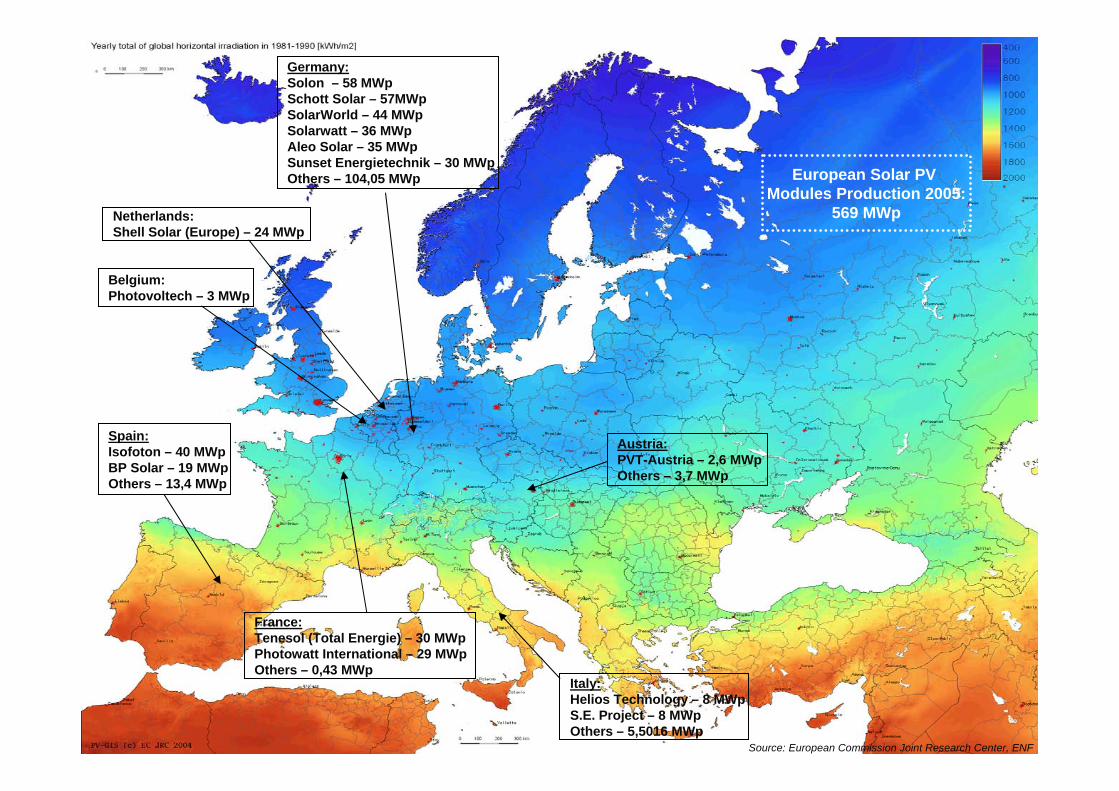

Source: European Commission Joint Research Center, ENF

Germany:Solon – 58 MWpSchott Solar – 57MWpSolarWorld – 44 MWpSolarwatt – 36 MWpAleo Solar – 35 MWpSunset Energietechnik – 30 MWpOthers – 104,05 MWp

Italy:Helios Technology – 8 MWpS.E. Project – 8 MWpOthers – 5,5016 MWp

Spain:Isofoton – 40 MWpBP Solar – 19 MWpOthers – 13,4 MWp

France:Tenesol (Total Energie) – 30 MWpPhotowatt International – 29 MWpOthers – 0,43 MWp

Austria:PVT-Austria – 2,6 MWpOthers – 3,7 MWp

Belgium:Photovoltech – 3 MWp

Netherlands:Shell Solar (Europe) – 24 MWp

European Solar PV Modules Production 2005:

569 MWp

17

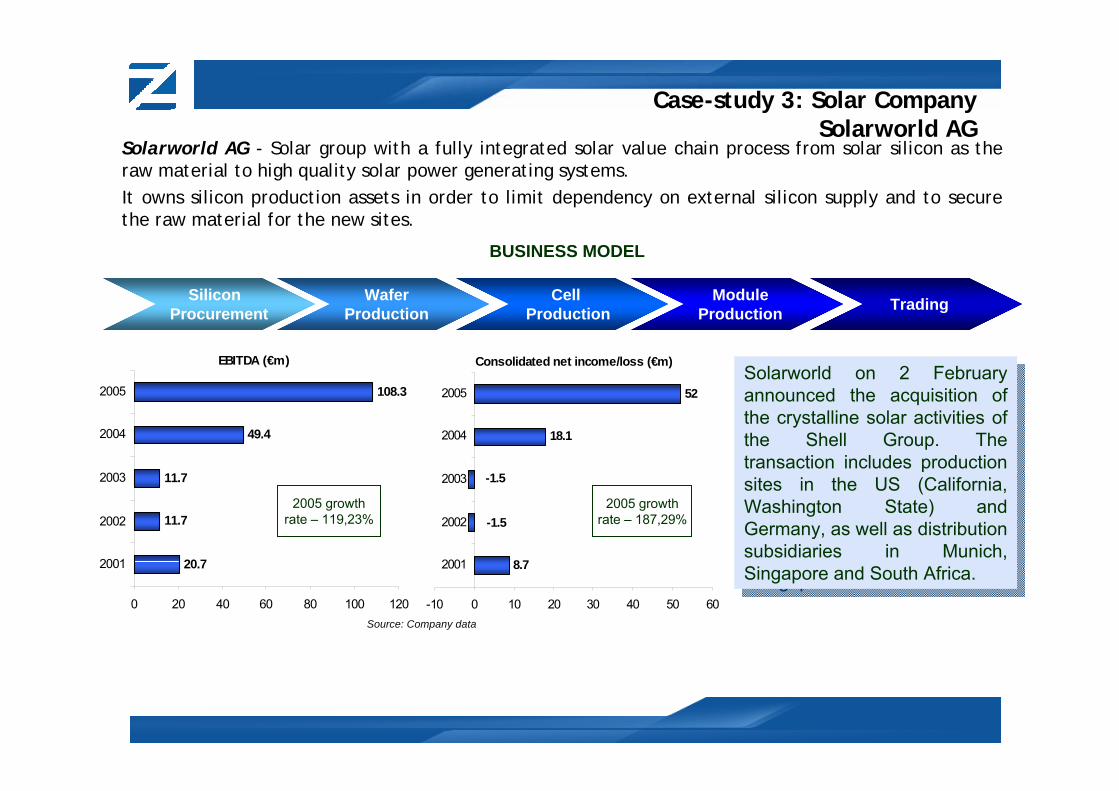

Case-study 3: Solar CompanySolarworld AG

Solarworld AG - Solar group with a fully integrated solar value chain process from solar silicon as the raw material to high quality solar power generating systems. It owns silicon production assets in order to limit dependency on external silicon supply and to secure the raw material for the new sites.

Silicon Procurement

WaferProduction

CellProduction

ModuleProduction Trading

BUSINESS MODEL

EBITDA (€m)

20.7

11.7

11.7

49.4

108.3

0 20 40 60 80 100 120

2001

2002

2003

2004

2005

Consolidated net income/loss (€m)

8.7

18.1

52

-1.5

-1.5

-10 0 10 20 30 40 50 60

2001

2002

2003

2004

2005

2005 growthrate – 119,23%

2005 growthrate – 187,29%

Solarworld on 2 February announced the acquisition of the crystalline solar activities of the Shell Group. Thetransaction includes productionsites in the US (California, Washington State) andGermany, as well as distribution subsidiaries in Munich,Singapore and South Africa.

Solarworld on 2 February announced the acquisition of the crystalline solar activities of the Shell Group. Thetransaction includes productionsites in the US (California, Washington State) andGermany, as well as distribution subsidiaries in Munich,Singapore and South Africa.

Source: Company data

18

www.zindelfund.com

Think about New Energy!!!