A better approach to investingin an uncertain world

Montgomery Global Investment Management

Montgomery

Global FundChristopher DemasiPortfolio Manager

The times of “easy money” are behind us

Last 30 years

Interest rates Declining

Profit margins Increasing

Debt levels Increasing

Demographics More favourable

Equity returns ~9% p.a. (~3% p.a. above average)*

Future equity returns are likely to be lower than in the past

*Source: McKinsey Global Institute 2

The times of “easy money” are behind us

Last 30 years Next 30 years

Interest rates Declining Flat/increasing

Profit margins Increasing Flat/declining

Debt levels Increasing Deleveraging?

Demographics More favourable Less favourable

Equity returns ~9% p.a. (~3% p.a. above average)* ?

Future equity returns are likely to be lower than in the past

*Source: McKinsey Global Institute 3

We are living in extremely uncertain times

Global equity markets have rallied 25% from their 2016 lows amid heightened uncertainty

Source: Bloomberg

1,400

1,450

1,500

1,550

1,600

1,650

1,700

1,750

1,800

1,850

1,900

MSCI World Index since 1 January 2016

4

The most important things for investors today

1. Downside protection • Capital preservation primary concern• Market downturns• Currency risks

2. Alpha generation • Relatively larger share of total return• Broad and diverse opportunity set• Flexibility: all-cap, sector, geography, long/short• Active management

3. Low correlation • Independent of markets• Complementary to other managers

Investors require a unique investment approach

5

Montaka’s unique approach

ImplicationsAssets Funding

Long(15-30 stocks)

Short(25-40 stocks)

Cash

Client NAV

• Company-specific, bottom-up approach to value-investing:− High-quality

businesses− Attractive prospects− Acquired at discount

to intrinsic value

• Nature-specific approach to short portfolio management:− Thematics/structural

declines− Divergent expectations− Asymmetries− Misperceptions

• Variable net exposure:− Driven primarily by availability of bottom-

up long and short opportunities− Informed by top-down systematic process− Typically 30-70%

6

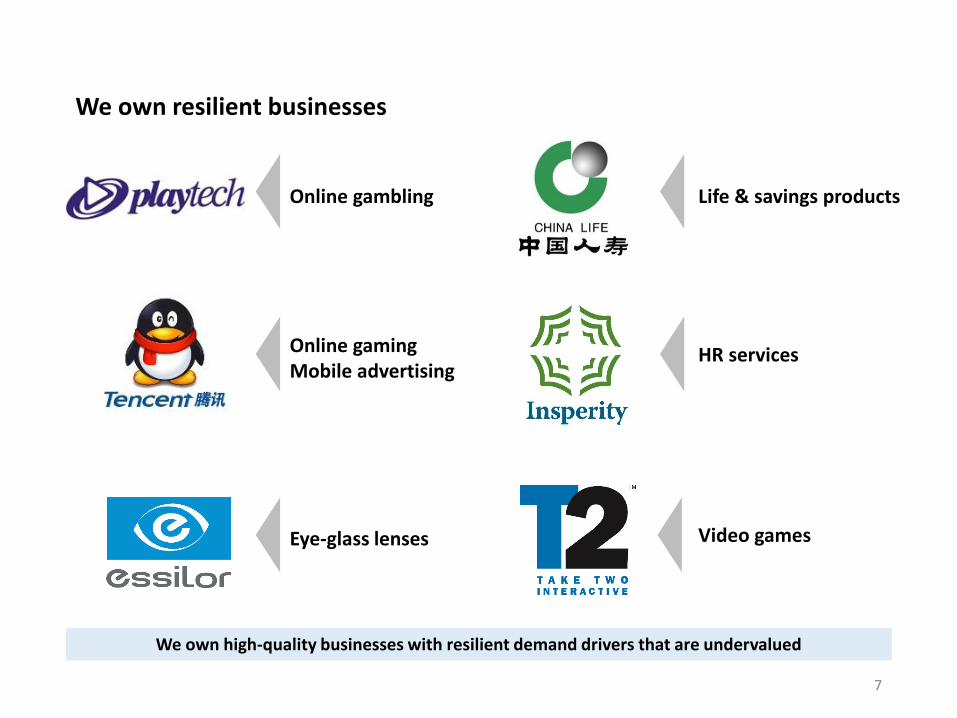

We own resilient businesses

Implications

Online gambling Life & savings products

HR services

Eye-glass lenses

Online gaming Mobile advertising

Video games

We own high-quality businesses with resilient demand drivers that are undervalued

7

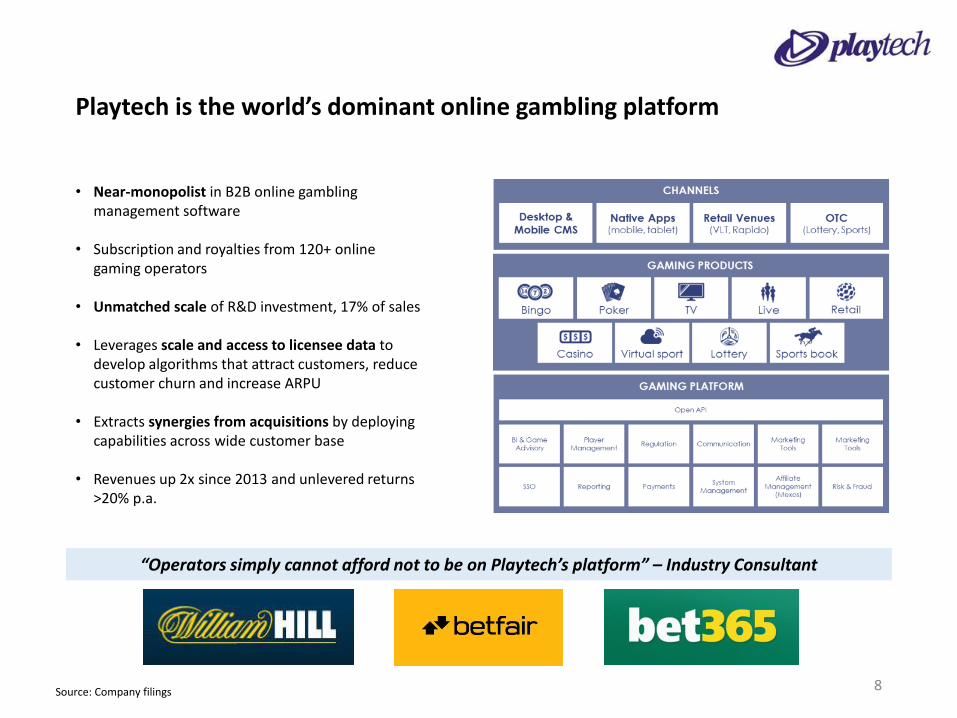

Playtech is the world’s dominant online gambling platform

• Near-monopolist in B2B online gambling management software

• Subscription and royalties from 120+ online gaming operators

• Unmatched scale of R&D investment, 17% of sales

• Leverages scale and access to licensee data to develop algorithms that attract customers, reduce customer churn and increase ARPU

• Extracts synergies from acquisitions by deploying capabilities across wide customer base

• Revenues up 2x since 2013 and unlevered returns >20% p.a.

“Operators simply cannot afford not to be on Playtech’s platform” – Industry Consultant

8Source: Company filings

Resilient fundamentals drive Playtech’s growth

• Global gambling revenues are highly stable and continued to grow during the Great Recession

• Online gambling represents only ~10% of total gambling revenues globally

• Online gambling market growing >10% p.a. as gamblers move online and to mobile

• Playtech’s take rate increasing, up 3x in last decade but still <2%

In the face of global uncertainty online gambling revenues are growing reliably with a long runway

9Source: Company filings; Morgan Stanley; Statista

Playtech’s share price has followed its growth trend upwards

0

100

200

300

400

500

600

700

800

200

300

400

500

600

700

800

900

1,000

Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

Playtech share price and LTM revenues

Share price (GBp) Sales (GBPm)

10Source: Company filings; Bloomberg

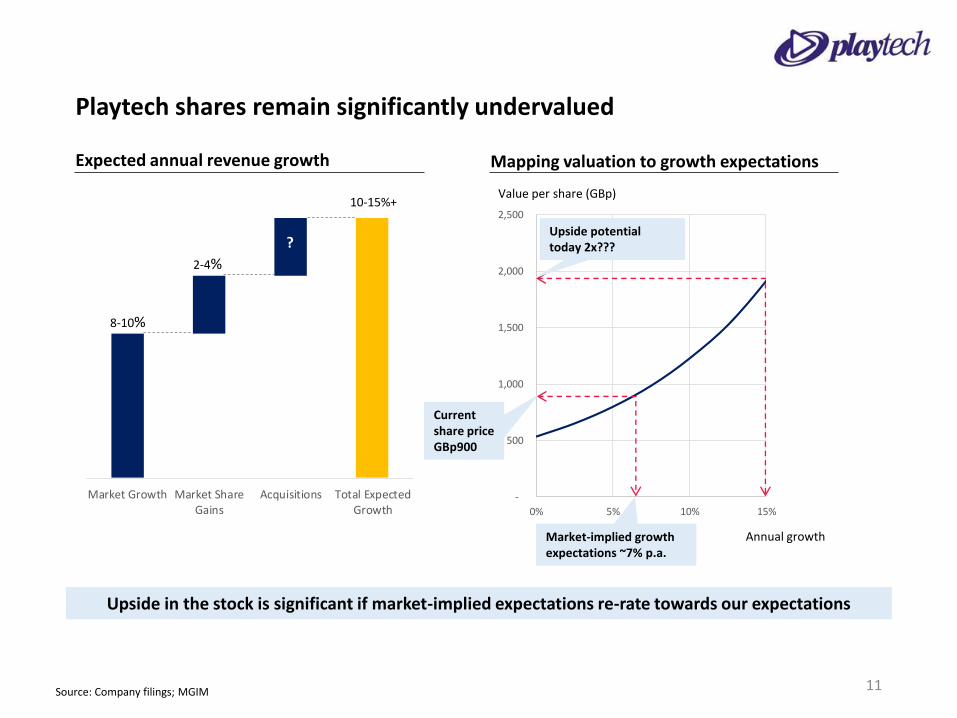

Playtech shares remain significantly undervalued

Expected annual revenue growth

Market Growth Market ShareGains

Acquisitions Total ExpectedGrowth

Mapping valuation to growth expectations

-

500

1,000

1,500

2,000

2,500

0% 5% 10% 15%

Market-implied growth expectations ~7% p.a.

Current share price GBp900

Upside potential today 2x???

8-10%

2-4%

?

10-15%+Value per share (GBp)

Annual growth

Upside in the stock is significant if market-implied expectations re-rate towards our expectations

11Source: Company filings; MGIM

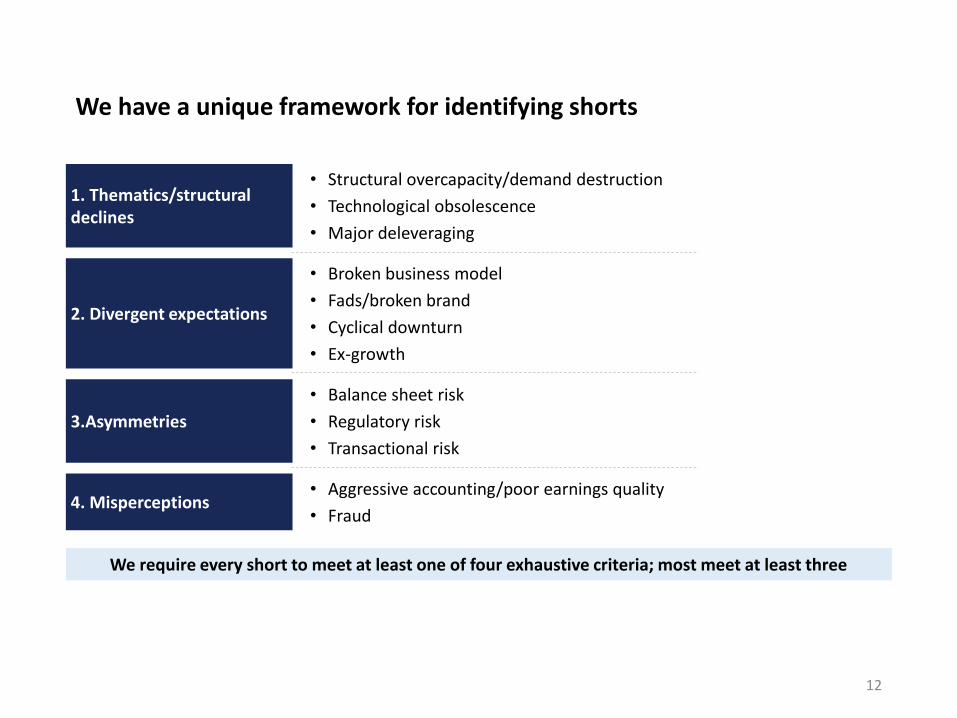

We have a unique framework for identifying shorts

1. Thematics/structural declines

• Structural overcapacity/demand destruction

• Technological obsolescence

• Major deleveraging

2. Divergent expectations

• Broken business model

• Fads/broken brand

• Cyclical downturn

• Ex-growth

3.Asymmetries

• Balance sheet risk

• Regulatory risk

• Transactional risk

4. Misperceptions• Aggressive accounting/poor earnings quality

• Fraud

We require every short to meet at least one of four exhaustive criteria; most meet at least three

12

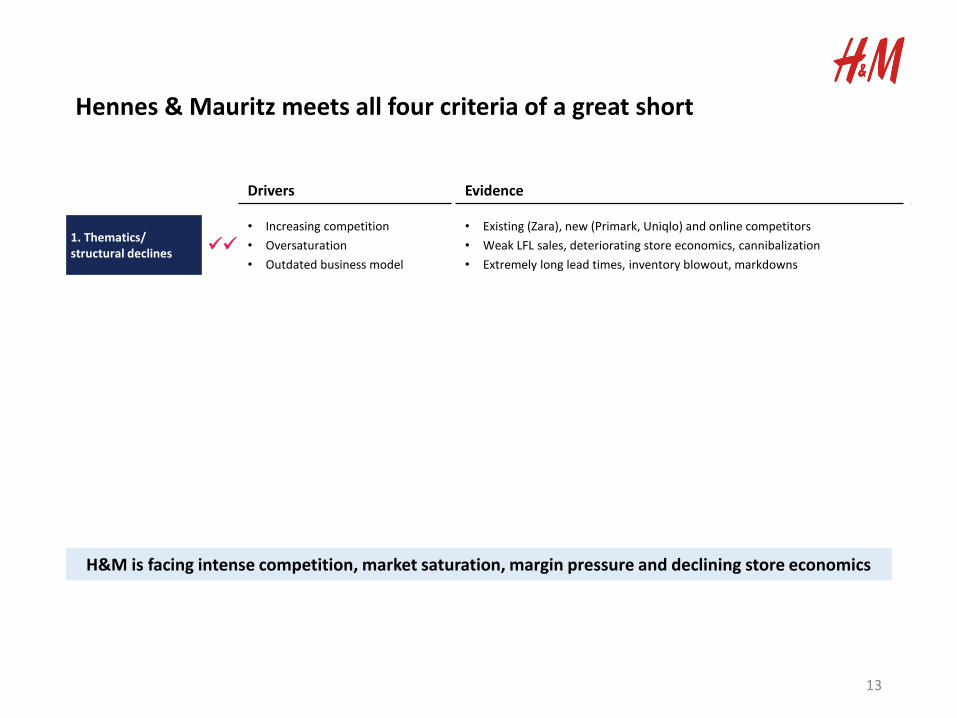

Hennes & Mauritz meets all four criteria of a great short

Drivers Evidence

1. Thematics/ structural declines

• Increasing competition

• Oversaturation

• Outdated business model

• Existing (Zara), new (Primark, Uniqlo) and online competitors

• Weak LFL sales, deteriorating store economics, cannibalization

• Extremely long lead times, inventory blowout, markdowns

H&M is facing intense competition, market saturation, margin pressure and declining store economics

13

Hennes & Mauritz meets all four criteria of a great short

Drivers Evidence

1. Thematics/ structural declines

• Increasing competition

• Oversaturation

• Outdated business model

• Existing (Zara), new (Primark, Uniqlo) and online competitors

• Weak LFL sales, deteriorating store economics, cannibalization

• Extremely long lead times, inventory blowout, markdowns

2. Divergent expectations

• Consensus too optimistic

• Overreaction to new sales target

• Dividend at risk

• Consensus expects LSD LFL sales growth and margin pressure to relent

• Share price jump suggests incorrect market interpretation as an upgrade

• Dividend payout > FCF since 2011

The market is yet to realise the full extent and impact of the deterioration

14

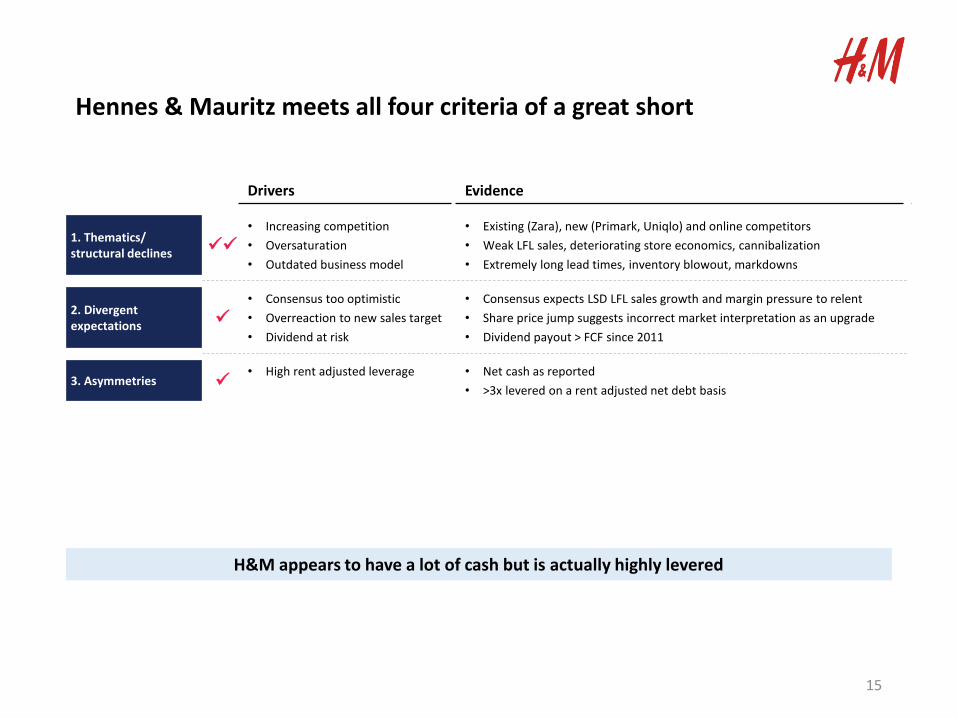

Hennes & Mauritz meets all four criteria of a great short

Drivers Evidence

1. Thematics/ structural declines

• Increasing competition

• Oversaturation

• Outdated business model

• Existing (Zara), new (Primark, Uniqlo) and online competitors

• Weak LFL sales, deteriorating store economics, cannibalization

• Extremely long lead times, inventory blowout, markdowns

2. Divergent expectations

• Consensus too optimistic

• Overreaction to new sales target

• Dividend at risk

• Consensus expects LSD LFL sales growth and margin pressure to relent

• Share price jump suggests incorrect market interpretation as an upgrade

• Dividend payout > FCF since 2011

3. Asymmetries • High rent adjusted leverage • Net cash as reported

• >3x levered on a rent adjusted net debt basis

H&M appears to have a lot of cash but is actually highly levered

15

Hennes & Mauritz meets all four criteria of a great short

Drivers Evidence

1. Thematics/ structural declines

• Increasing competition

• Oversaturation

• Outdated business model

• Existing (Zara), new (Primark, Uniqlo) and online competitors

• Weak LFL sales, deteriorating store economics, cannibalization

• Extremely long lead times, inventory blowout, markdowns

2. Divergent expectations

• Consensus too optimistic

• Overreaction to new sales target

• Dividend at risk

• Consensus expects LSD LFL sales growth and margin pressure to relent

• Share price jump suggests incorrect market interpretation as an upgrade

• Dividend payout > FCF since 2011

3. Asymmetries • High rent adjusted leverage • Net cash as reported

• >3x levered on a rent adjusted net debt basis

4. Misperceptions

• Aggressive store rollout

• Weak LFL sales and declining profit density masked

• Online sales unprofitable

• >90% of sales growth from new selling space vs LFL sales since 2007

• Operating profit gains driven by selling space growth > decline in profit/m2

• Online sales are likely cannibalizing in-store sales while requiring additional expense and investment

H&M’s aggressive store rollout and online expansion is masking the true economics of the business

16

H&M’s misperceived growth is slowly being uncovered

100

150

200

250

300

350

400

Hennes & Mauritz share price (SEK)

We believe there is much more downside to come

17Source: Bloomberg

We manage currency exposure to maximize global purchasing power

(20%) (10%) 0% 10% 20% 30% 40%

LATAM

Australia

Japan

China

EU

UK

US

Short Long

Currency exposure (look-through earnings basis)

% of net asset value

= net exposure

GBP exposure hedged ahead of Brexit

EUR exposure hedged ahead of Italian Referendum

We protected investor capital by actively hedging currencies ahead of extreme macro/political events

1.20

1.25

1.30

1.35

1.40

1.45

1.50

Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16

GBP in USD

1.00

1.02

1.04

1.06

1.08

1.10

1.12

1.14

Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16

EUR in USD

18Source: MGIM; Bloomberg

Note: currency exposure of investments based on month-end February 2017

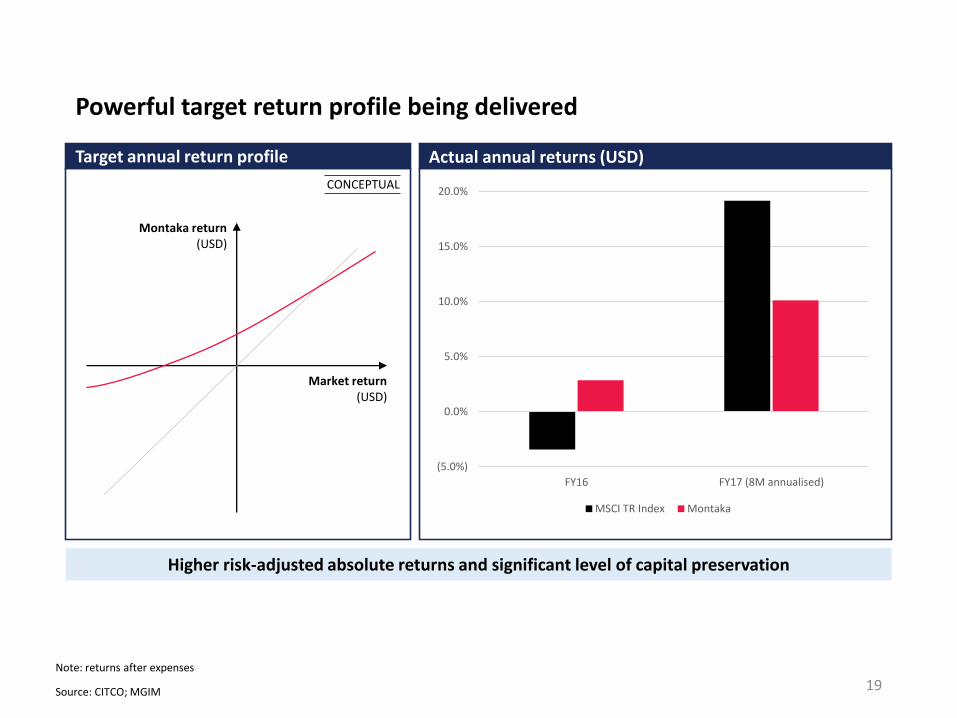

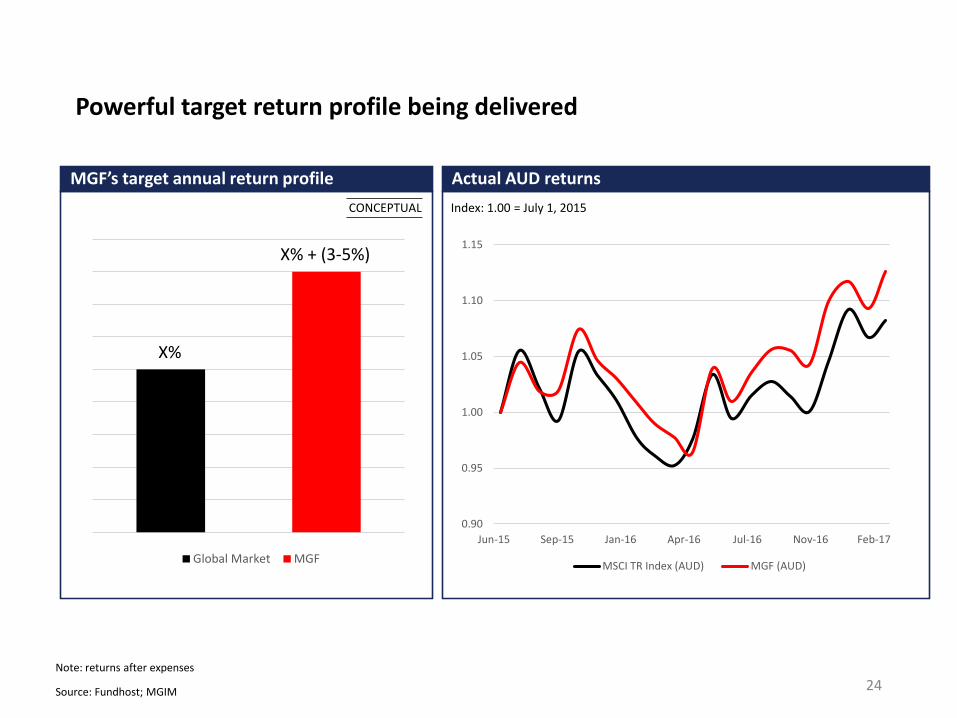

Powerful target return profile being delivered

Higher risk-adjusted absolute returns and significant level of capital preservation

(5.0%)

0.0%

5.0%

10.0%

15.0%

20.0%

FY16 FY17 (8M annualised)

MSCI TR Index Montaka

Target annual return profile Actual annual returns (USD)

Market return(USD)

Montaka return(USD)

CONCEPTUAL

19Source: CITCO; MGIM

Note: returns after expenses

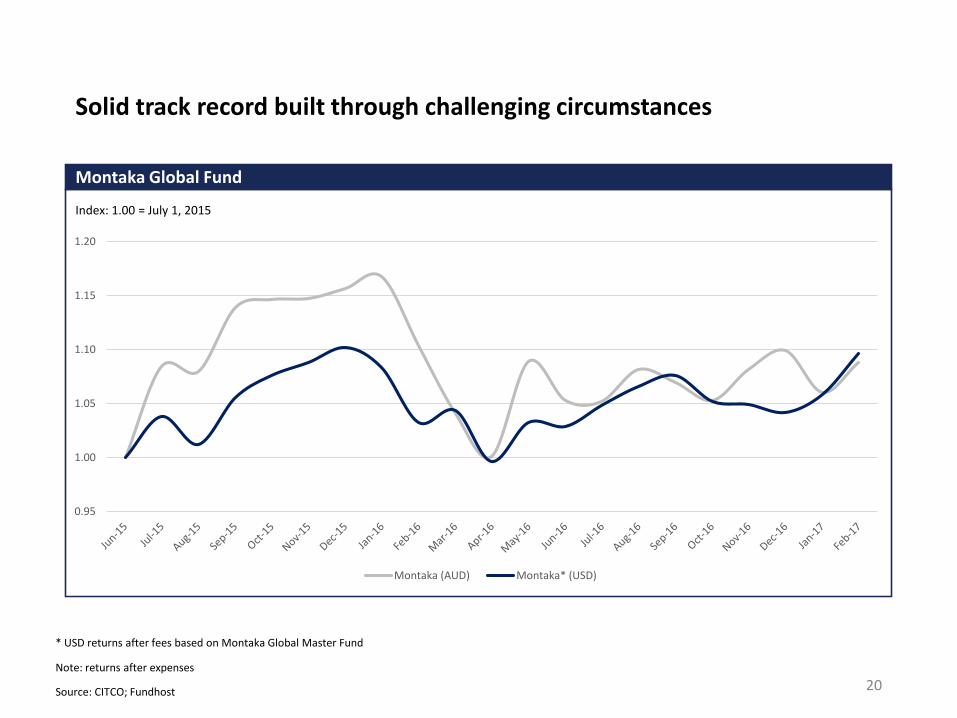

Solid track record built through challenging circumstances

0.95

1.00

1.05

1.10

1.15

1.20

Montaka (AUD) Montaka* (USD)

Montaka Global Fund

Index: 1.00 = July 1, 2015

20Source: CITCO; Fundhost

Note: returns after expenses

* USD returns after fees based on Montaka Global Master Fund

Solid track record built through challenging circumstances

0.95

1.00

1.05

1.10

1.15

1.20

Montaka (AUD) Montaka* (USD)

Montaka Global Fund

Index: 1.00 = July 1, 2015

21Source: CITCO; Fundhost

Note: returns after expenses

* USD returns after fees based on Montaka Global Master Fund

Launched Montaka Global Access Fund

Montaka is a top performer compared to peers

One of the highest performers in the marketplace with an attractive and complementary return profile

22

Performance comparison

Correlation matrix — Montaka clearly stands apart from the peer group

Montaka

Montaka correlation with peers just 28-53%

0% 5% 10% 15% 20%

Peer 5

Peer 4

Peer 3

Peer 2

Montaka Global Fund

Peer 1

Upside-downside capture

Source: Morningstar; MGIM

Note: peer group includes Antipodes, K2, Morphic, Platinum, PM Capital; fund performance in A$ after expenses from 1 July 2015 to 28 February 2017

Introducing the Montgomery Global Fund

Montgomery

Global Fund

Assets Funding

Long(15-30 stocks)

Cash

Client NAV

• Same long portfolio as Montakao All capo All geographieso All sectors

• Flexible cash weighting 0-30% (max 50%)o Driven primarily bottom-up,

informed by top-down processo Protect downsideo “Dry powder”

• Same currency hedging policy as Montaka

• Synergy benefits with short research process underlying Montaka

23

Powerful target return profile being delivered

MGF’s target annual return profile Actual AUD returns

CONCEPTUAL Index: 1.00 = July 1, 2015

Global Market MGF

X%

X% + (3-5%)

0.90

0.95

1.00

1.05

1.10

1.15

Jun-15 Sep-15 Jan-16 Apr-16 Jul-16 Nov-16 Feb-17

MSCI TR Index (AUD) MGF (AUD)

24Source: Fundhost; MGIM

Note: returns after expenses

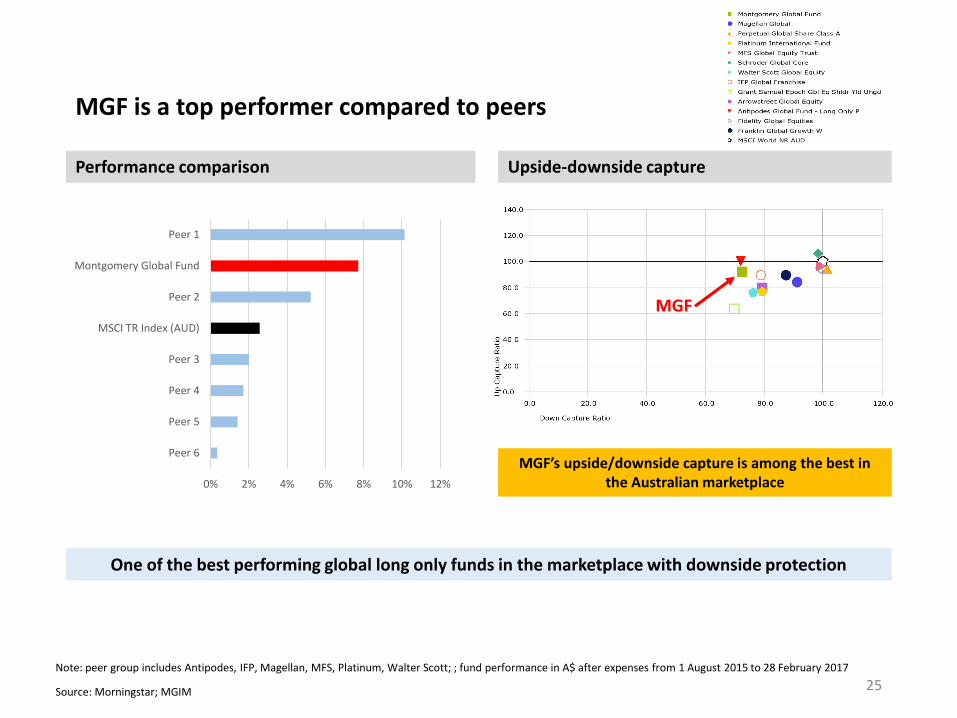

MGF is a top performer compared to peers

Upside-downside capture

MGF

0% 2% 4% 6% 8% 10% 12%

Peer 6

Peer 5

Peer 4

Peer 3

MSCI TR Index (AUD)

Peer 2

Montgomery Global Fund

Peer 1

MGF’s upside/downside capture is among the best in the Australian marketplace

Performance comparison

One of the best performing global long only funds in the marketplace with downside protection

25Source: Morningstar; MGIM

Note: peer group includes Antipodes, IFP, Magellan, MFS, Platinum, Walter Scott; ; fund performance in A$ after expenses from 1 August 2015 to 28 February 2017

Our dedicated global team

• Andrew Macken, Chief Investment Officer• Launched Montaka/MGF July 2015• Formerly at Kynikos Associates, New York, under Jim

Chanos• MBA, Applied Value Investing Program, Columbia

Business School, New York• Master of Commerce, High Distinction, University of New

South Wales (UNSW), Sydney• Bachelor of Engineering, First Class Honours, Academic

Scholarship, UNSW, Sydney

• Christopher Demasi, Portfolio Manager• Launched Montaka/MGF July 2015• Formerly at LFG, the private investment group of

the Lowy family, New York• Formerly One East Partners, New York; and

Goldman Sachs, Sydney• Bachelor of Commerce, Academic Scholarship,

UNSW, Sydney

• Daniel Wu, Research Analyst• Joined Montgomery Global in June 2016• Formerly Analyst at Goldman Sachs and UBS

investment banking divisions, Sydney• Bachelor of Commerce, Distinction, University of

Sydney, Sydney• Bachelor or Laws, University of Sydney, Sydney

• Paul Mason, Chief Financial & Operating Officer• Launched Montaka July 2015 • Formerly COO AMBATA Capital Partners, a global private equity firm, New York• Formerly COO Credit Suisse Standard Securities (JV Credit Suisse / Standard Bank), Johannesburg• Formerly COO Credit Suisse European Prime Services, London

• George Hadjia, Research Analyst• Joined Montgomery Global in August 2015• Formerly Analyst at Private Portfolio Managers, a global

equity fund manager, Sydney• Bachelor of Commerce, Distinction, University of Sydney,

Sydney• Bachelor or Laws, University of Sydney, Sydney

26

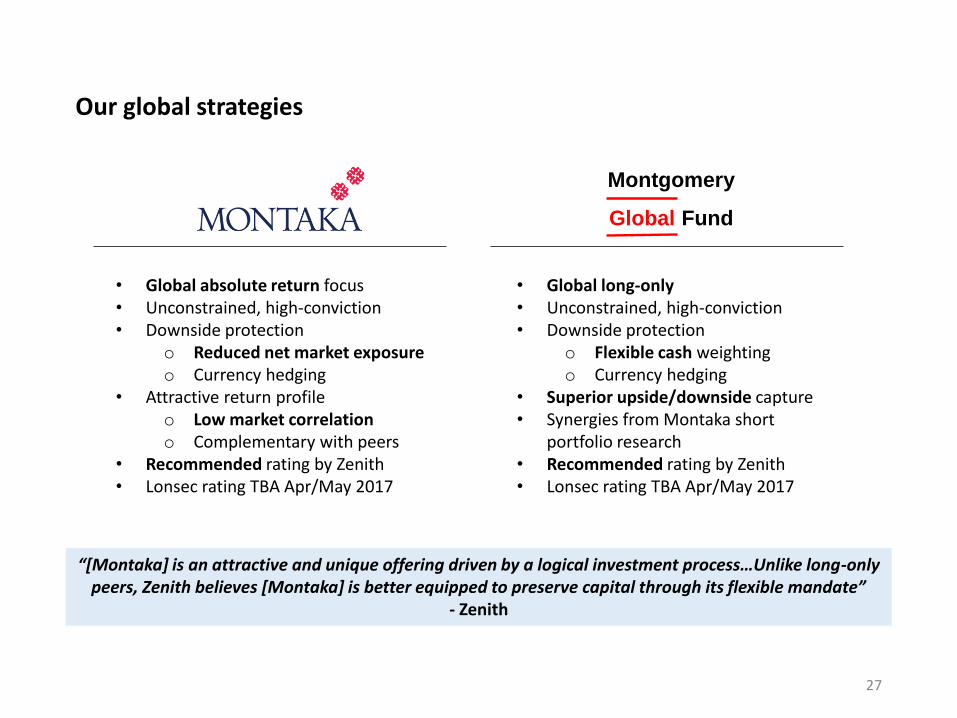

Our global strategies

27

• Global absolute return focus• Unconstrained, high-conviction• Downside protection

o Reduced net market exposureo Currency hedging

• Attractive return profileo Low market correlationo Complementary with peers

• Recommended rating by Zenith• Lonsec rating TBA Apr/May 2017

Montgomery

Global Fund

• Global long-only• Unconstrained, high-conviction• Downside protection

o Flexible cash weightingo Currency hedging

• Superior upside/downside capture• Synergies from Montaka short

portfolio research• Recommended rating by Zenith• Lonsec rating TBA Apr/May 2017

“[Montaka] is an attractive and unique offering driven by a logical investment process…Unlike long-only peers, Zenith believes [Montaka] is better equipped to preserve capital through its flexible mandate”

- Zenith

Thank You

Montgomery Global Investment Management

Montgomery

Global Fund

28