Outlook for Key Emerging MarketsGlobal Risk Insights

• The key emerging markets all face individual challenges given the global economic context.

• Recent data indicate that the downturn in the global economy appears to have bottomed out.

• Downside risks include the debt crises in Europe and the US; possible errors by policy-makers; volatility and potential asset bubbles in the financial markets; and the renewed threat of currency wars and protectionism.

• The debt crisis raises the risk of a new global financial crisis.

Global Economic Outlook: Downturn Appears to be Bottoming Out

Although emerging markets have frequently been cited as being the potential ‘saviours’ of the troubledglobal economy (witness recent media coverage about China buying euro-zone assets), each of the key regional emerging markets (Brazil, Russia, India, China and South Africa—the BRICS) has its own individ-ual development trajectory within the global framework. That said, the global outlook provides criticalcontext: recent data indicate that the downturn in the global economy appears to have bottomed out,further reducing the chances of a global recession, but risks remain on the downside. In September, theJPMorgan Global All-Industry Output Index climbed to 52.0, up from the 25-month low of 51.5 recorded inAugust (a score of 50 separates growth from contraction), driven by faster growth in industrial output inthe US (at a six-month high), China and the UK. However, growth slowed in a number of countries (e.g. Germany, Russia, France and India, with faster contractions in output in Brazil, Italy and Spain).

Continued downside risks include the debt crises in Europe and the US; possible policy errors as govern-ments and central banks try to counterbalance dealing with sovereign debt while promoting growth;volatility and potential asset bubbles in the financial markets; and the renewed threat of currency warsand attendant protectionism.

Key Risk: Ongoing Euro-zone Debt Crisis Threatens Financial Stability

Following the agreement to expand the euro-zone rescue fund, euro-zone leaders are working on a planto recapitalise EU banks to protect them from the potential fallout of sovereign defaults in the highly-in-debted euro-area countries (Greece, Ireland, Italy, Portugal and Spain). Many EU banks remain highly ex-posed to sovereign debt. Meanwhile, the ECB has intensified efforts to pump liquidity into the financialsector.

A D&B Special ReportNovember 2011

The recent downturnappears to be

bottoming out…

…but risks remain onthe downside

EU banks will remain vulnerablewithout further recapitalisation

Despite the ECB’s efforts, banks remain reluctant to lend to each other, reflected in a sharp rise in thefunds that euro-zone banks deposit in the ECB’s overnight deposit facility. Weakening credit conditionsundermine economic growth prospects in the euro zone and beyond. Moreover, a vicious cycle of sharpbudget cuts across Euroland (in response to rising debt levels) and weak growth threaten to sustain thedebt crisis, potentially leading to several sovereign defaults and/or the break-up of the euro area, both ofwhich would have dire consequences for global financial stability.

The debt crisis weakens the

economic outlookand threatens global

financial stability

© Dun & Bradstreet Limited 2

Country Risk ServicesA D&B Special ReportNovember 2011

Brazil’s economy issuffering from

global uncertaintyand a slowdown indemand from China

BrazilRisk Insights

• An economic slowdown over Q4 2011 and into Q1 2012 will lead to a rise in short-term credit risk.

• Inflation will increase operating costs and raise the risk premiums on government bonds.

• Short-term currency volatility will increase the risk associated with the Real.

Outlook

The uncertain global economic outlook in the context of the euro-zone debt crisis is undermining Brazil’sshort-term economic outlook. Investor risk appetite has fallen, causing investment flows to stall, whilemore subdued demand from China, the country’s principal export market, is having a negative impact onBrazil’s commodity exports (e.g. iron ore). Industrial output has started to ease markedly across a num-ber of sectors (notably automotive production), while the construction sector is also suffering from a

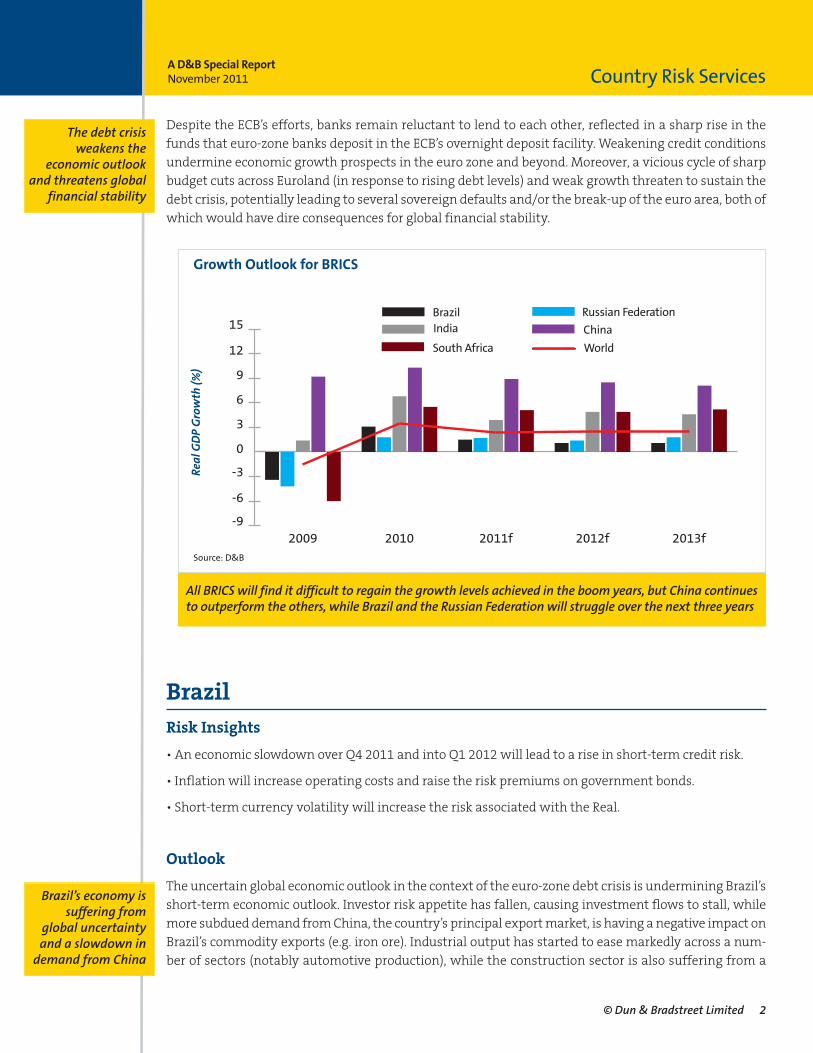

All BRICS will find it difficult to regain the growth levels achieved in the boom years, but China continuesto outperform the others, while Brazil and the Russian Federation will struggle over the next three years

-9

-6

-3

0

3

6

9

12

15

South Africa

ChinaIndiaRussian FederationBrazil

2013f2012f2011f20102009

World

Real

GD

P G

row

th (%

)

Growth Outlook for BRICS

Source: D&B

Loose monetary policy has put

downward pressureon the currency

© Dun & Bradstreet Limited 3

Country Risk ServicesA D&B Special ReportNovember 2011

The economic outlook for 2012 is

more positive

Brazil will remainexposed to a defaultin the euro-zone but

effects will be mitigated by FX

reserves and a strong financial

sector

Be aware of inflation’s impact

on input costs

Hedge against currency volatility

downturn as projects are put on hold. The more subdued economic environment will cause real GDPgrowth to fall to 4.0% in 2011, down from 7.5% in 2010.

The deteriorating economic environment has prompted the authorities to enact measures to stimulatedemand. In August, the central bank started loosening monetary policy, cutting the benchmark Selic in-terest rate by 50 basis points (bp); there was a similar reduction in October, bringing the rate down to11.5%. This ended the period of monetary policy tightening that began in April 2010 in response to Brazil’srapid economic growth and strong upward pressure on the Real. We expect short-term monetary policyto remain loose, with a further interest rate cut likely before end-2011. The combined impact of the newmonetary policy direction and increased investor risk aversion will result in further downward pressureon the Real, which experienced a rapid depreciation against the US dollar in September and continues toexperience volatility in light of the euro-zone crisis. Notably, inflation has remained stubbornly high de-spite the slowdown in the economy; CPI inflation rose to 7.3% in September (although we anticipate thatit will ease slightly by end-2011).

We expect economic growth to pick up in 2012 as investment rebounds amid large-scale investmentprojects such as the development of Brazil’s offshore oil fields and extensive infrastructure enhancement.This will put further upward pressure on inflation, making it likely the central bank will resume tight-ening monetary policy. Improved investment is also likely to support the Real, which we expect to revertto an appreciating trajectory over 2012.

Implications

• An economic downturn in H2 2011 may increase credit risk over the short term, but risks should easein 2012 as a result of a moderate upturn in economic growth.

• A disorderly default in the euro-zone would cause a currency depreciation and contagion to Brazil’sbanking sector. However, the extent of the crisis would be mitigated by Brazil’s robust FX reservesand the fact that Brazil’s banks are relatively well capitalised.

• Resurgent inflation in 2012 will increase operating costs and erode profit margins.

• Higher inflation expectations in 2012 will increase the risk premiums on Real-denominated investments and put downward pressure on Brazilian government bonds, raising yields.

• Capital controls designed to promote a stable currency may dent the appeal of Brazil’s capital markets.

Recommendations

• Businesses operating in Brazil should monitor inflation trends and limit their exposure to higher production costs.

• Companies exposed to Real-denominated liabilities should have adequate hedging strategies inplace to limit the adverse impact of exchange rate volatility.

• Despite a more subdued economic environment, Brazil remains a lucrative market for investors and exporters.

Russian FederationRisk Insights

• The economy’s recovery has been unimpressive compared with those of the other BRICS, and growth will slow in 2012.

• Business conditions will continue to vary across sectors throughout the forecast period.

• Russia remains vulnerable to capital flight triggered by global events.

• Exchange rate and commodity price volatility will remain a concern in 2012.

• Accession to the WTO should improve market access for Russian firms as well as for those exporting to Russia.

Outlook

The Russian economy’s recovery from the deep recession of 2009 has been unimpressive compared withthose registered by other large emerging markets. Indeed, Russia’s economy managed to grow by just4.0% in 2010, far slower than India and China. The sluggish recovery continued in 2011 despite ongoingfiscal stimulus measures and the windfall from oil income. High oil prices have provided the economywith a boost, and the economy did pick up momentum in Q3, accelerating to grow by 5.1% in year-on-year terms. However, even this more rapid pace of growth remains well below the average 7.5% annualgrowth rate registered during the boom years leading up to 2008. Business conditions will continue tovary from sector to sector, with pockets of weakness requiring vigilance throughout the forecast period.

D&B expects the economy to slow in 2012. Russia remains vulnerable to the risk aversion that grippedglobal financial markets during August-October 2011. In Q3 alone the country registered USD18.7bn innet capital outflows, and the rouble fell by 12% against the US dollar. This was the sharpest depreciationof the rouble since the escalation of the global financial crisis in late 2008. Although the central bank isconcerned about the impact of external risks on the Russian economy, it is unlikely to loosen policy. Lowerinterest rates would encourage yet more capital outflows and put the currency under further pressure.For its part, the government will almost certainly retain its still relatively loose fiscal policy into 2012given the upcoming parliamentary (December 2011) and presidential (March 2012) elections.

Implications

• The sharp depreciation of September 2011 will have made it more difficult for Russian borrowers toservice their foreign debt obligations.

• The country’s enormous store of FX reserves mitigates the risk of a balance of payments or financialsector crisis stemming from rapid outflows of capital.

• The country is poised to finally accede to the WTO in 2012, which should improve market access forRussian firms (as well as for those exporting to Russia).

• The almost certain return of Vladimir Putin to the presidency in 2012 will sideline the modernisingagenda of current President Dmitri Medvedev, risking longer-term economic and political stagnation.

• Organised crime, security risks stemming from the Caucasus, endemic corruption, judicial weakness,a cumbersome bureaucracy and harmful government interference will continue to pose considerablerisks to doing business in Russia.

The recovery hasbeen lacklustre

compared with other BRICS

countries…

…and pockets ofweakness require

vigilance

The economy remains vulnerable

to capital flight

The country’s largestore of FX reservesshould prevent any

major financial crisis

There is a risk of government

intrusion into private sector

dealings

© Dun & Bradstreet Limited 4

Country Risk ServicesA D&B Special ReportNovember 2011

Recommendations

• The risk of non-payment/payment delays is likely to remain high during our forecast period. We recommend CiA terms with Russia-based counterparties.

• Exchange rate and commodity price volatility will remain a concern in 2012, with the possibility of renewed capital outflows; active hedging policies should be considered.

• Corruption and opaque links between politicians and local firms can make business dealings difficult for foreigners (requiring extra vigilance and due diligence), while crime and security risksoften warrant security-related expenditures.

• Russia’s oil and gas industry remains in need of significant investment to boost productivity. Given the country’s large reserves, and persistently elevated international prices, this could be profitable for those who are well placed to capitalise.

© Dun & Bradstreet Limited 5

Country Risk ServicesA D&B Special ReportNovember 2011

We recommend CiA terms

Corruption canmake doing

business tricky

IndiaRisk Insights

• After rapid growth in 2010, the economy is now slowing. However, it will continue to grow rapidly by global standards in 2012.

• Business optimism has been eroded by persistent price pressures and rising interest rates.

• Given the global backdrop, exchange rate and commodity price volatility will remain a concern in 2012.

• The government is pressing ahead with long-promised market reforms; just how favourable these will be for the private sector remains uncertain.

Outlook

The economy experienced rapid growth in 2010 as a consequence of the policies implemented in thewake of the global financial crisis, but is beginning to slow noticeably under the weight of easing globalgrowth, financial market volatility, rising interest rates and persistent price pressures. D&B’s CompositeBusiness Optimism Index (BOI) for Q4 2011 fell to 143.7, a year-on-year contraction of 12.1% (the sharpestdrop since Q2 2009). The drop in confidence reflects a broader economic slowdown. Each of the BOI’s sixsub-indices (volume of sales, net profits, selling prices, new orders, inventory levels and employee levels)registered falls. Reflecting the pressures that ongoing inflation is putting on firms’ margins, the net profitindex fell to a nine-quarter low. Of all the sectors surveyed by D&B, the basic goods (e.g. iron and steel,cement) and intermediate goods sectors were the least optimistic.

Even with this slowdown, D&B still expects growth to remain above 7% in 2012, making it robust byglobal standards. Indeed, many sectors continue to function at near-capacity, and thus supply-side con-straints continue to exacerbate price pressures. Inflation has been a problem since 2009, when droughtcaused a food price spike. Ever since, policymakers have been at pains to try to rein-in double-digit (orclose to it) inflation. Between March 2010 and October 2011, the central bank raised interest rates on 13separate occasions, lifting its benchmark lending rate by a total of 375 basis points to 8.5%; however, inflation has remained stubbornly high. With domestic and global growth slowing, we expect the tightening cycle to be close to an end, but inflation will remain a problem into 2012.

Implications

• Political risks remain prominent, having been highlighted over the past two years by a number ofhigh-profile corruption cases exposing the sometimes nefarious and opaque dealings between Indian politicians and businesspeople.

• Amid constant criticism of the government over corruption scandals and rapid inflation, the administration is likely to continue to delay approvals for private sector projects.

• Pressure has forced the government to finally start to progress a number of long-promised marketliberalising reforms; however, just how favourable these will be to the private sector remains uncertain.

© Dun & Bradstreet Limited 6

Country Risk ServicesA D&B Special ReportNovember 2011

After a rapid growthspurt in 2010, the

economy is slowing

Inflation and higherinterest rates willpose problems forbusinesses in 2012

Corruption and political risks remain

prominent

The country’s largestore of FX reservesshould prevent any

major crisis

• Global financial market volatility caused a sharp depreciation of the rupee in August-October 2011.This downward adjustment could undermine the ability (or willingness) of some firms to servicetheir liabilities in a timely manner.

• The country’s large stock of FX reserves mitigates the risk of a balance of payments or financial sector crisis stemming from rapid outflows of capital.

Recommendations

• With firms’ profits under pressure from inflation and higher interest rates, payment risks are likely to rise in 2012. We recommend LC terms with India-based counterparties.

• Exchange rate and commodity price volatility will remain a concern in 2012, with the possibility of further depreciation; active hedging policies should be considered.

• Conducting business in India can be onerous. The situation is complicated by a lack of bankruptcyand payment information, meaning that vigilance is required.

• India’s rapidly growing middle class retains a pent-up demand for basic consumer items, and thegovernment is proposing opening up the retail sector to foreign investment.

© Dun & Bradstreet Limited 7

Country Risk ServicesA D&B Special ReportNovember 2011

We recommend LC terms

Conducting businessin India requires

constant vigilance

ChinaRisk Insights

• The economy is slowing but will continue to expand rapidly, making it the fastest-growing of thelarge emerging markets in 2012.

• Sectors such as property, railway building, shipping, and local government infrastructure projectswill continue to experience a credit squeeze.

• Given the amount of questionable lending encouraged during the authorities’ credit-fuelled stimulus package, bad loans are likely to increase in 2012.

• With profits threatened by cost pressures and tighter credit conditions, payment risks will remain elevated.

Outlook

The Chinese economy, having returned to double-digit growth in 2010 thanks to the massive stimulusmeasures put in place at the height of the global financial crisis, is again slowing. By Q3 2011, the economy was growing at a pace of 9.1% year on year, its slowest rate of expansion in two years. Inflationary pressures and tighter monetary policy, alongside the emerging global slowdown, will prevent any acceleration in the quarters ahead: we expect growth to slow to 8.5% in 2012. Even so, Chinawill remain the fastest-growing of the large emerging markets. The rapid urbanisation and developmentof the inland provinces continues unabated and should help to drive strong growth into the mid-2010s.

With the economy slowing and the property market beginning to deflate, growing concerns stem fromthe credit crunch confronting businesses and local governments, as well as from the stability of the banking sector. The government has announced measures to ease the difficult conditions facing smallbusinesses, making it easier for them to issue bonds and reduce their tax burden. However, with banks’poor loan quality (encouraged by the government’s 2009-10 credit-driven stimulus package) deteriorat-ing into non-performing status, default risks will rise into 2012. Worries about the extent of bad local government debt are troubling both policymakers and ratings agencies. While the central government’sfiscal resources are significant, a large-scale bank bailout would be a huge drain, and GDP growth wouldalso have to slow in line with more conservative credit approval processes.

Implications

• The mild economic slowdown seen so far is due mostly to domestic credit-tightening policies; anyexternal shock from the emerging global slowdown has yet to fully arrive.

• Sectors such as property, railway building, shipping, and local government infrastructure vehicleswill experience a continuing credit squeeze.

• China’s financial system is in a stronger state than in the early 2000s, but contains substantial pockets of weakness that a crisis could turn into serious risks.

• China’s mostly closed capital account means the most significant channel for contagion will still be its exports to the euro zone, other European economies and the US. Worryingly, export orders declined noticeably in Q3 2011.

© Dun & Bradstreet Limited 8

Country Risk ServicesA D&B Special ReportNovember 2011

The economy isslowing, but willcontinue to growrapidly by global

standards

The stability of thebanking sector is agrowing concern

The slowdown so faris due mostly to

domestic tightening

Euro-zone contagionis likely to spread

via weaker exports

• Trade risks would be exacerbated if US politicians impose trade sanctions on China (as they havethreatened) for allegedly manipulating the value of its currency.

Recommendations

• With firms’ profits threatened by cost pressures and tighter credit conditions, payment risks arelikely to rise. We recommend LC terms with China-based counterparties.

• Although the currency should remain broadly stable (and continue to appreciate against the US dol-lar very moderately), commodity price volatility will remain a concern in 2012, and active hedgingpolicies should be considered.

• Vigilance is advised regarding the communications equipment manufacturing sector and the ex-port-oriented manufacturing sector more generally, which are at risk due to high levels of competi-tion as well as rising input prices and wage costs.

• Opportunities could stem from the country’s consumers having developed a rapacious appetite forbranded retail items; China’s luxury goods market is now second largest in the world and growingrapidly.

© Dun & Bradstreet Limited 9

Country Risk ServicesA D&B Special ReportNovember 2011

We recommend LC terms

The export sector isat risk due to rising

input prices andwage costs

South AfricaRisk Insights

• The rand’s increased volatility will undermine long-term corporate planning.

• Weaker external demand and rising input costs will weaken firms’ ability to service their foreign currency-denominated debt.

• The weaker currency will benefit exporters but increase the cost of imported capital equipment, creating a negative impact on fixed investments.

Outlook

Heightened sovereign debt problems in the euro zone (which accounts for around one-fifth of SouthAfrica’s exports) and the resultant fiscal cuts in the EU have weakened prospects for the South Africaneconomy, perpetuating uncertainty in the business climate. Further uncertainty stems from domesticfactors such as growing political tensions over the country’s policy direction (mainly in relation to the private sector’s share of the natural resource and banking sectors), the re-emergence of industrial strikes,and elevated levels of crime and unemployment. While we still expect real GDP to grow in 2011–12, creating opportunities for business expansion (mainly in precious metals), firms doing business in/withthe country will face rising challenges. In particular, growing uncertainty over the euro-zone’s debt crisis has heightened investor risk-aversion in South Africa, prompting many investors to flee from rand-denominated assets. This has in turn led to capital flight, which, together with weaker export receipts, has resulted in a sharp depreciation of the rand: on a trade-weighted basis, the rand has depreciated by around 16.1% against the US dollar since early 2011.

Although the rand’s depreciation will improve export competitiveness, on the downside it will increaseimport costs, somewhat offsetting potential gains. In turn, this will exert pressure on corporate andhousehold finances; the latest official data show that the total number of insolvencies amounted to 254in August 2011 (notably in the finance, insurance, real estate, and wholesale and retail sectors), markinga 9% month-on-month rise; that said, on a cumulative basis (January-August 2011) it fell by 33.8% on thecorresponding period in 2010. Nevertheless, the deteriorating economic outlook is likely to exacerbate therecent trend: indications are that increasing global financial market volatility will put the rand under further pressure, potentially causing inflation to rise beyond the bank’s 6% upper target by end-Q4 2011.This will create a policy dilemma for the monetary authorities, which are under pressure to support aweakening economy by lowering interest rates, while higher interest rates would normally be used tolower inflation.

Implications

• Payments risks will rise as faltering external demand weakens export commodity receipts.

• Capital outflows risk a severe depreciation of the currency, making it difficult for firms to servicetheir foreign debt.

• Elevated living costs may heighten the risk of large-scale social unrest in a country that already faces high youth unemployment and greater income disparity.

• FDI inflows will weaken as uncertainty over the global economic outlook increases, thus weakeningFX liquidity and the currency (although risks will be limited).

© Dun & Bradstreet Limited 10

Country Risk ServicesA D&B Special ReportNovember 2011

Heightened sovereign debt

problems in the eurozone will present

new challenges forbusinesses

Exporters will benefit from a

weaker rand, but rising import costswill offset potential

gains

Rising inflationarypressures willweaken firms’ balance sheets

The rising cost of living could re-ignite

social unrest

• A disorderly default in the euro zone would impact negatively on South Africa’s financial market;however, domestic banks are well-capitalised and profitable.

Recommendations

• Businesses operating in the country should monitor inflation trends and limit their exposure tohigher production costs.

• Export-oriented companies that are susceptible to the volatility of the South African rand shouldconsider hedging strategies to limit the adverse impact.

• Companies are advised to take out adequate security and insurance cover against potential inflation-driven unrest in the country.

• The gold-mining sector will continue to benefit from strong external demand amid growing uncertainty in the global economy.

© Dun & Bradstreet Limited 11

Country Risk ServicesA D&B Special ReportNovember 2011

Companies shouldhedge against exchange rate fluctuations…

…and take out adequate

insurance cover

Feedback

We greatly value your feedback on how relevant you find our analysis and focus. To tell us how effectivelythis special paper addresses the issues facing your business, email us at [email protected] you have any suggestions for future areas of coverage that would be of use to you, we will be happy toconsider them.

Our Team and Products

D&B Country Risk Services has a team of trained economists dedicated to analysing the risks of doing business across the world (we currently cover 132 countries).

We monitor each country on a daily basis and produce both shorter analytical pieces (Country RiskLine Reports), as well as more detailed 50-page Country Reports. For further details please contact Country RiskServices on +44 (0)1628 492595 or email [email protected].

Our Team and Products

The information contained in this publication was correct at the time of going to press. For the most up-to-date information on any country covered here, refer to D&B’s monthly International Risk & Payment Review. For comprehensive, in-depth coverage, refer to the relevant country’s Full Country Report.

Credits: This paper was produced by D&B Country Risk Services, with contributions by Dr. Warwick Knowles,

Gaimin Nonyane, Tom Christie and Dr. Ian Manns.

CONFIDENTIAL & PROPRIETARYThis material is confidential and proprietary to D&B and/or third parties and may not be reproduced,published or disclosed to others without the express authorization of D&B.

© Dun & Bradstreet Limited 12

Country Risk ServicesA D&B Special ReportNovember 2011