Embracing the New Era:A new chapter of Opening-up in China’s Financial Sector(Updated in May 2018 based on new policies and data)

www.pwccn.com

Management consulting

This report has been updated based on China’s new policies

and data compares to the March 2018 edition.

In his keynote speech at the opening ceremony of the Boao

Forum for Asia 2018 (BFA) on April 10, President Xi Jinping

described economic globalization as an irreversible trend, and

noted that China would continue on its course of opening-up.

On the following day, the People’s Bank of China unveiled

policy details as well as a timeline, that focus on expending

market access and lifting ownership restrictions.

The precise timing for the further opening-up of financial

sector reflects that decision-makers have adequately grasped

the risk of the domestic financial system. After experiencing

strong supervision in 2017, the systematic risk in financial

sector has been reduced to some extent and China’s financial

industry is maturing.

This series of deeper financial measures to open-up are

beneficial to both China and the global financial industry, as

they will create new opportunities for domestic and foreign

players, adding market competition, and leading to new

channels, products and services, with improved customer

experience, and operations.

2018 marks the beginning of a new era that China further opens up its financial service sector

Expanding market access Expected

timeline

Lifting ownership restrictions Expected

timeline

To allow foreign banks to set up

branches and subsidiaries

End of June

2018

To remove the foreign ownership cap for

banks and asset management

companies, treating domestic and foreign

players equally

End of June

2018

To further improve the stock market

connectivity between the mainland and

Hong Kong by increasing the daily quota

threefold

1 May 2018 No longer require jointly funded securities

companies to have at least one local

securities company as a shareholder

End of June

2018

To allow eligible foreign investors to

provide insurance agent and loss

adjuster services

End of June

2018

To raise the foreign ownership cap to

51% for securities companies, fund

managers, futures companies, and life

insurers, and remove the cap in three

years

End of June

2018

To lift restrictions on business scope of

foreign-invested insurance brokerage

companies, treating foreign and domestic

companies equally

End of June

2018

To encourage foreign ownership in trust,

financial leasing, auto finance, currency

brokerage and consumer finance

End of

December 2018

To substantially expand the business

scope of foreign banks

End of

December 2018

Apply no cap on foreign ownership in

financial asset investment companies and

wealth management companies newly

established by commercial banks

End of

December 2018

To remove restrictions on the business

scope of jointly funded securities

companies, treating domestic and foreign

institutions equally

End of

December 2018

Foreign insurance companies will no

longer need to have a representative

office in China for two consecutive years

prior to establishing a subsidiary

End of

December 2018

To launch the Shanghai-London Stock

Connect

End of

December 2018

2

4,5454,038

2,655

2,114 2,295

1,785 1,708

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Bank WealthManagement

Products

Trust AssetManagement

Sercuties AssetManagement

Fund AssetManagement

Insurance AssetManamgement

Mutual Funds Private Funds

Billion USD

It is another good time for foreign financial institutions to seize the country’s growth opportunity

3

Total AUM of China’s asset management service provider, as of 2017

The legendary Chinese strategist SunZi said, “fully

understand the competitive landscape and you will never be

defeated.” With the aim of bringing you the receipt of the

winning formula, we prepared this overview of China’s

financial service sector. Key messages of the overview include:

1) The regulatory policy changes by the authorities are swift

and firm, with full support of Chinese top leadership.

2) While Chinese FIs enjoyed significant growth over last

decade, they are experiencing significant headwind in

recent years. There are little differentiation in product &

service offerings among Chinese FIs. Yet leading Chinese

FIs have made good progress in developing nationwide

channels and branch network. Regional banks have

stronger customer loyalty. Most leading Chinese FIs have

strong digital capabilities, especially in digital payment.

3) Most foreign FIs selected trusted and capable partner(s) to

develop their business in China.

We hope you find this overview insightful. Should you have

any questions regarding China’s financial service sector,

please do feel free to contact us.

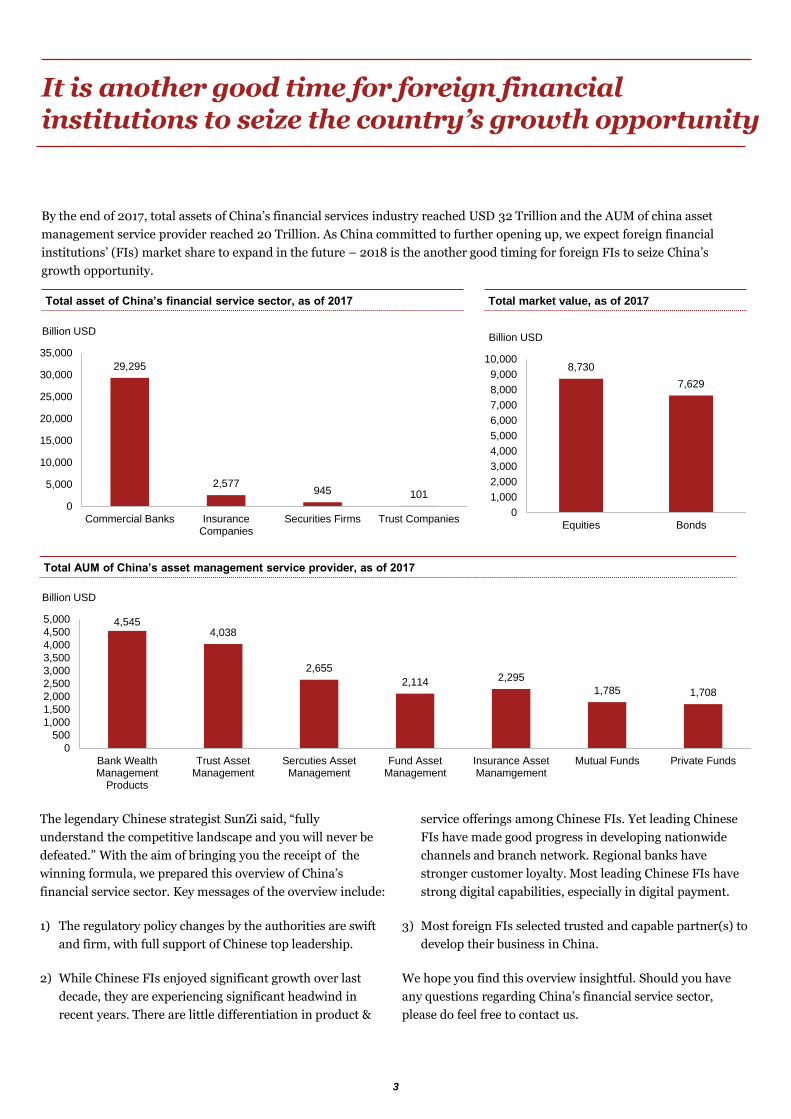

By the end of 2017, total assets of China’s financial services industry reached USD 32 Trillion and the AUM of china asset

management service provider reached 20 Trillion. As China committed to further opening up, we expect foreign financial

institutions’ (FIs) market share to expand in the future – 2018 is the another good timing for foreign FIs to seize China’s

growth opportunity.

Total asset of China’s financial service sector, as of 2017

29,295

2,577945 101

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Commercial Banks InsuranceCompanies

Securities Firms Trust Companies

Billion USD

Total market value, as of 2017

8,730

7,629

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Equities Bonds

Billion USD

4

01 The Financial Regulatory Landscape 05

02 Competitive Landscape: Banking 07

03 Competitive Landscape: Insurance 11

04 Competitive Landscape: Fund Management 17

05

Global FIs Anticipated Challenges in Developing China Market 27

Table of Contents

06

Competitive Landscape: Securities 23

The Financial Regulatory Landscape 1

Re-insurance

Insurance

Insurance broker/agent

Insurance asset management

Shanghai Insurance

Exchange

The Financial Regulatory Landscape

The People’s Bank of China (PBoC, China’s Central Bank)

Financial Stability and Development Commission of the State Council

The separation of supervision of China’s financial services industry has created significant risks in certain subsectors,

including insurance asset management, banking wealth management, shadow banking, etc.

With the People’s Banks of China introducing macro-prudential supervision and the recent establishment of the cross-sector

Financial Stability and Development Commission proposed in National Financial Work Conference (NFWC), as well as other

policy making meetings, such as the 19th CPC Party Congress, Central Economic Work Conference, China’s regulatory

framework is moving to an coordinated and collaborative approach.

Some recent policies with significant implications include:

• The merge of banking and insurance regulatory committee, and restriction on the shadow banking business of asset

management institutions;

• Crack down on Internet micro loans;

• Restriction on Unit-Linked products by insurance company;

• Restriction on program trading;

Trust

Financial Leasing

Banking

Consumer Finance

Auto Finance

Interbank

bond market

Interbank

Loan Asset

Exchange

China Banking & Insurance

Regulatory Commission

Mutual funds and subsidiaries

QD(F)IE/II/LP

Securities

Futures

PE Funds

Main Board/ GEM / NEEQ

China Securities

Regulatory Commission

China’s segmented supervision model of financial service industry is moving towards an coordinated and collaborative approach, enabled by several policy changes in 2017

6

Competitive Landscape:

Banking2

Competitive Landscape: Banking

• As one of the world’s largest credit

market, China’s banking financial

institutions’ RMB loan balance

exceeded USD 18.5 Trillion, and

RMB deposit balance reached USD

25.2 Trillion by the end of 2017.

The Compounded Annual Growth

Rates (CAGR) from 2012 to 2017

are 13.8% and 12.3% respectively.

0

5,000

10,000

15,000

20,000

25,000

30,000

2012 2013 2014 2015 2016 2017

Loan Balance Deposit Balance

• The slow down in net profit growth

stabilized since 2016, mainly due to

improved risk management,

increased fee-based income, and

more diversified business models.

• The growth of fee-based income

could not offset shrinking net

interest margin (NIM) following

the liberation of interest rates.

Interest income still consists of

77.3% of banking sector’s total

income.

0%

5%

10%

15%

20%

25%

0

50

100

150

200

250

300

2012 2013 2014 2015 2016 2017

Net Profit Year-on-Year Growth ROE

2.75%2.68% 2.70%

2.54%

2.22%

2.10%

19.83%21.15% 21.47%

23.73% 23.80% 22.65%

0%

5%

10%

15%

20%

25%

1.5%

1.7%

1.9%

2.1%

2.3%

2.5%

2.7%

2.9%

2012 2013 2014 2015 2016 2017

Net Interest Margin

Non-Interest Income as %

RMB deposit and loan balance of banking financial institutions

Net profit of commercial banks and its year-on-year growth

Net interest margin and non-interest income as %

Billion USD

Billion USD

China’s banking sector, the main pillar of the country’s financial services industry, is facing tremendous profit growth pressure in recent years

Source: CBRC, Wind

8

0.95% 1.00%1.25%

1.67% 1.74% 1.74%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

2012 2013 2014 2015 2016 2017

Commercial Bank

State-owned Commercial Bank

Joint-stock Commercial Bank

City Commercial Bank

Rural Comercial Bank

Competitive Landscape: Banking

Source: CBRC, Wind

Total assets by bank types

Non-performing loan (NPL) ratio by bank types

Loan Structure of Listed Banks

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2014 2015 2016 2017

Rural Banking InstitutionsCity Commercial BankJoint-stock Commercial BankState-owned Commercial Bank

61.41% 59.34%70.44% 66.92%

36.10% 38.14%25.47% 28.09%

State-owned Bank Joint-stock Bank City Commercial Bank Rural Commercial Bank

Corporate Loan Retail Loan Discounted Bill

Larger banks are focusing on optimization of credit portfolio, while regional banks are still actively looking for ways to expand their balance sheets

• City commercial banks and rural

banking institutions (collectively

referred to as “regional banks” in

this context) enjoyed CAGR of

20.6% and 14.1% respectively in

total assets between 2014 and

2017.

• These is a continuous rise in non-

performing loan (NPL) ratios

among regional banks while larger

banks stabilized.

• Regional banks are still heavily

relying on corporate customers.

They have to bear higher costs,

and are more effected by the

“supply side” structural reform.

Billion USD

9

Competitive Landscape: Banking

Bank’s WMPs balance and expected return rates

Wealth management products (WMPs) have been playing important roles in Chinese banks’ transformation. With tighter supervision, banks are under pressure to right size such business

1,570.77

2,310.77

3,615.38

4,469.23 4,544.62

4.88%

4.00% 3.95%

4.83%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2013 2014 2015 2016 2017

Bank Wealth Management Product Balance Expected Annual Return Rate

• Bank’s wealth management

products (WMPs) balance reached

USD 4.54 Trillion in 2017,

representing an CAGR of over 30%

from 2013 to 2017.

• The balance in 2017 almost

stabilized due to tighter regulation.

• The new regulations prohibited

banks from providing “implicit

guarantee” in principal and returns

for most WMPs.

Underlying assets of bank’s WMPs

66.13% 70.31% 73.37% 73.52% 69.19%

25.62% 20.91% 15.73% 17.49%16.22%

8.25% 8.78% 10.90% 8.99%14.67%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2013 2014 2015 2016 2017

Bonds, Money Market Instruments and Bank Deposits Non-standard debt Instruments Others

• Since the CBRC announced

tightened up the non-

standardized investment policy in

2014, bank WMPs investing in

non-standard debt instruments

have decreased.

• We expect the increased needs for

investment grade products to be

fulfilled by all FS sectors.

Data Source: CBRC, Wind

Unit: Billion USD

10

Competitive Landscape:

Insurance3

• Till the end of 2016, by insurance

premium, China has become one

of the largest insurance market in

the world. That said, the

insurance density and penetration

in China were just USD 345 and

4.2% in 2016, much lower than its

counterparts (4,000 USD and 8%)

in developed markets. There is

still huge opportunity in China for

domestic and foreign insurer,

especially when the country is

ageing now.

Insurance density and penetration in China

Insurance premium by product types

Unit: Billion USD

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

150

200

250

300

350

400

2012 2013 2014 2015 2016

Insurance Density Insurance Penetration

330.09

67.53

13.87

151.30

0

50

100

150

200

250

300

350

Life Insurance Health Insurance Personal Accident Insurance Property Insurance

2013 2014 2015 2016 2017

22.83%

40.59%

18.23%

12.17%

CAGR

The insurance sector in China is huge yet the market is far from developed, with the growth momentum expecting to continue

Source: CIRC, Wind

Life Insurance:

• largest volume

• high growth rate

(21.65% from 2013 to 2017)

Health Insurance:

• market with high potential

• highest growth rate, but

greatly slowed down in

2017

Property Insurance:

• 2nd largest volume

• lowest growth rate

Competitive Landscape: Insurance

(Unit: USD)

12

Competitive Landscape: Insurance

• The “universal life insurance” and

“unit-linked insurance plan”

products still focus on providing

insurance coverage to policy

holders in overseas market. But in

China, these products mainly

serve investment purpose.

• Many life insurance companies

have expanded business scale by

selling universal life insurance

and unit-linked products before

2016. The compound growth rate

of non-premium investment

funds from 2013 to 2016 is 57.2%.

• The business model was

considered to bring very high risk,

and was strictly regulated by CIRC

since 2017. As a result, the non-

premium investment funds were

substantially reduced.

• The premium mix of property

insurance companies are stable in

recent years.

• The proportion of vehicle

insurance premium remains the

largest, around 70%.

• As vehicle sales growth began to

slow down, there is a downward

trend of premium growth for

vehicle insurance.

Non-premium investments in separate account and premiums

Premium mix of property insurance companies

Current business models of both life insurance and property insurance companies are not sustainable, there’s urgent business transformational pressure

Unit: Billion USD

Unit: Billion USD

50.70

64.71

128.07

196.91

97.89

0

50

100

150

200

250

300

350

2013 2014 2015 2016 2017

Non-premium investment Premium

0

20

40

60

80

100

120

140

160

2013 2014 2015 2016

Others Health Insurance

Liability Insurance Enterprise Property Insurance

Agricultural Insurance Vehicle Insurance

Source: CIRC, Wind

13

Competitive Landscape: Insurance

For life insurance premium,

• the top 10 companies accounted

for 71.7% market share;

• the top 20 companies accounted

for 86.6% market share;

• foreign companies only account

for 6.9% market share

For property insurance premium,

• the top 10 companies accounted

for 85.1% market share;

• the top 20 accounted for 92.3%

market share;

• foreign companies only accounted

for 1.96% market share

Market share of life insurance premium by companies

Market share of property insurance premium by companies

Insurance market is highly concentrated in China, with top 10 life insurance and top 10 property insurance players’ premium accounting for over 70% and 85% of market share respectively

Source: CIRC, Wind

33%33% 20%

15%

10%

6%

4%

4%

3%

2%

2%

1%

PICC Pingan Ins.

CPIC

China Life

China Ins.

Sunshine Ins.

China Taiping

Sinosure

Tian Ins.

Others

China Continent Ins.

20%20%

13%

9%

7%

5%4%

4%

4%

3%

3%

28%

ChinaLife

Pingan Ins.

Anbang

CPIC

TaiKang LifePICC

China Taiping

NCI

Hua Ins.

Funde Sino Life

Others

14

Competitive Landscape: Insurance

• With the rapid growth of insurance

premium, funds investable by

insurance companies increased at a

compound growth rate of 20%,

reaching over USD 2.3 Trillion in

2017.

• In terms of the asset allocation of

investment portfolio, it used to be

mainly in bonds and bank deposits.

In recent years, high-yield assets

such as unlisted equity and debt

instruments are growing in

demand.

• As insurance companies

investment scope were expanded,

as well as a buyout capital market,

the return on investment (ROI)

continued to grow in 2014 and

2015.

• But as macro economic slowdown

and a lack of quality assets, ROI of

insurance funds felt since 2016.

• If the market remains sluggish, the

ROI of insurance funds will

continue to face pressure.

Asset allocation of insurance companies’ investment portfolio

ROI of insurance companies investment portfolio

5.04%

6.30%

7.56%

5.66%5.77%

3.00%

3.50%

4.00%

4.50%

5.00%

5.50%

6.00%

6.50%

7.00%

7.50%

8.00%

2013 2014 2015 2016 2017

While insurance companies have invested more and more in high-yield assets such as unlisted equity and debt instruments, the return is trending downward in recent two years

29.45% 20.12% 21.78% 18.55% 13.11%

43.42%38.15% 34.39% 32.15% 35.11%

10.23%11.06%

15.18%13.28% 12.80%

16.90%

23.67%

28.65%

36.02%

40.79%

0

500

1,000

1,500

2,000

2,500

2013 2014 2015 2016 2017

Bank Deposit Bond Stock and Funds Alternative2295.48

2060.16

1719.93

1435.60

1182.66

Unit: Billion USD

Source: CIRC, Wind

15

Competitive Landscape:

Fund Management

4

Competitive Landscape: Fund Management

• AuM of mutual funds reached USD

1.7 Trillion, representing a CAGR of

36.9% from 2014 to 2017.

• The CAGR of AuM by stock fund is

-16.68% from 2014 to 2017.

• The significant growth in MMF is

driven by proliferation of FinTech

and restriction of Banks’ wealth

management products .

• Investors are increasingly drawn to

lower risk allocation funds.

• There are 113 fund management

companies, 45 of which are Sino-

foreign joint ventures, 68 of which

are domestic companies.

• Of these 113 companies, 12 are

owned by securities companies & 2

by insurance companies.

• Top 10 players are managing nearly

50% of the total assets.

• Top 20 players are managing 68%

of the total assets.

Total AuM by mutual Funds

Market share (by AuM as of 2017) of Top 10 fund managers, and the rest

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2014 2015 2016 2017

Open-end QDII Fund Open-end Bond Fund

Money Market Fund Open-end Allocation Fund

Open-end Stock Fund Close-end Fund

Total asset under management (AuM) by mutual funds reached USD 1.7 Trillion in 2017, with most noticeable growth in money market funds

Unit: Billion USD

Source: Asset Management Association of China, Wind

50.10%

Others

18

Competitive Landscape: Fund Management

• AuM of private funds remained

high growth since 2014. The

CAGR from 2014 to 2017 is 95.1%,

with total size reaching USD 1.7

Trillion.

• AuM of private securities funds

declined significantly after

regulatory restriction in 2016, and

is around USD 265 billion by the

end of 2017.

• AuM of private equity (PE) funds

continued to increase rapidly and

reached USD 910 billion.

• The PE fund is a popular

investment vehicle in China’s

financial market. Many

institutions are developing related

business to gain higher returns.

• Private fund sector is dominated by funds with asset size under RMB 2 billion in China, with the majority relying on

banks, trusts & securities companies to market the products.

• As oppose to developed markets such as the US, there are no clear dominated players in China.

Private funds AuM

0

200

400

600

800

1000

1200

1400

1600

1800

2014 2015 2016 2017

Private securities funds Private equity funds Others

Although private fund sector is relatively small, with 95% of funds managing RMB 2 billion or less, it is the fastest growing FS subsector

Unit: Billion USD

Number of Private Funds by AUM in China (2017) AuM of Hedge Funds in the US

Source: Asset Management Association of China, Wind

Private securities Funds: private funds invested in public traded investment instruments

Private equity funds: private funds invested in nonpublic traded investment instruments

5% Bridgewater

2.3% AQR Capital

1.5% Two Sigma

RenaissanceTechnologies

1.3% DE Shaw & CO.

1% Millennium

1%Elliot

1% Och-Ziff Capital

0.9% The Baupost

0.8% Winton

1.3%

19

95%Below CNY 2B

84%Others

Competitive Landscape: Fund Management

• Private equity (PE) and venture capital (VC) funds are fueling the rapid growth of China’s emerging sectors such as internet,

other IT, automobile, etc., while investment in financial services, such as crowdfunding has cooled down.

Source: Asset Management Association of China, Wind

Top 10 Industries Invested by PE and VC in 2017

Private equity (PE) and venture capital (VC) funds are fueling the rapid growth of China’s emerging industries

20

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

2013 2014 2015 2016 2017

Chemical

Electronic & Photoelectric Equipment

Entertainment & Media

Biotechnology/Health Care

Manufactory

Financial services

Telecom & Value-added Service

Automobile

Other IT

Internet

Million USD

• Institutional investors such as insurance companies, are

becoming more and more important LPs of PE funds. They

will expect PE funds to provide more professional and

comprehensive services to meet internal management

responsibilities or regulatory requirements.

• Despite a lack of derivatives in China, fund managers still

need to develop quantitative investment capability.

• Fund managers need to actively explore and apply

innovative investment approach to gain alpha returns.

• Fund managers need to provide customized investment

management services to accommodate the diversified

risk appetite of high net worth individual and

institutional clients.

• The number of private fund managers has increased

substantially. Many traditional FIs such as securities firms,

trust companies are entering this market as fund

managers. Institutions with strong investment

management capability will dominate the market in

coming years, which may lead to market concentration.

• Asset Management Association of China (AMAC) has

adopted stricter requirements on information disclosure

of private fund managers and their products, and began

to impose penalty on inappropriate practice.

• With new investor suitability standards issued, many

existing business models are deemed as unacceptable.

Improving

investment

capability

Intensive

market

competition

Changing

investors

behavior

Tightening

regulatory

supervision

Private funds are growing rapidly in recent years, but with tightened supervision and fierce competition, the sector is under the limelight

21

Competitive Landscape: Fund Management

22

Competitive Landscape:

Securities5

Competitive Landscape: Securities

• Due to the fluctuation of stock markets, securities firms’ income experienced significant ups and downs in recent years.

• From the perspective of income mix, the income heavily relies on brokerage, investment and securities underwriting

activities.

• Although all leading securities firms have been actively building their asset management business, income contribution from

such business is still not significant.

• The income proportion of investment banking businesses, such as financial advisory and investment advisory business are

still small.

Income Mix of Securities Firms

Unit: Billion USD

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

100.00

2012 2013 2014 2015 2016 2017

Investment Advisory Income

Financial Advisory Income

Asset Management Income

Income from Underwriting of Securities

Interest Income

Income from IPO service

Investment Returns

Commission Income

Chinese securities firms still heavily rely on brokerage & investment incomes, accordingly their financial results are highly correlated and fluctuated with the performance of stock market

57.21

93.51

45.71

26.03

20.17

52,21

Source: CSRC, Wind

24

Asset Management

Brokerage

Investment Banking

Financial Advisory

Others

2%

17%

8%

50%

Competitive Landscape: Securities

Source: CSRC, Wind

While leading players dominate certain business segments, differentiation in product & service offerings is limited

25

Income Mix of Guangfa Securities

Asset Management

Brokerage

Investment Banking

Financial Advisory

Others

47% 25%

5%

9%

Income Mix of GUOTAI JUAN

13%

23%

• Many leading Chinese securities firms’

income mix looks very similar, with

around 50% from brokerage business

and the rest attributed to asset

management, investment banking and

advisory services;

• On the contrary, their global

counterparts are often known for

specialty in specific service line(s) such

as investment banks, asset management,

financial advisory or even securities

services

Asset Management Income of Leading Broker — Dealers

GUOTAI JUAN

GF Securities

CITIC Securities

Shenwan Hongyuan

Huatai Securities

Zhongtai Securities

Orient Securities

CMS

Everbright Securities

Huarong Securities

Others

44.39%

7.76%

3.77%

8.42%

6.69%

4.08%

3.98%

3.79%

26

Global FIs’ Anticipated Challenges

in Developing China Market

6

Top challenges for foreign financial institutions to succeed in China market

Obtaining license

• Financial licenses are still relatively scarce resources in China because of

the long permission process and large number of candidate institutions in

waiting list. Foreign FIs shall first evaluate whether to apply for a license

or to acquire a local licensed FI.

• During the license application process, Foreign FIs will need to maintain

an effective communication with regulators.

Compliance to local regulations

• The regulations have been evolving rapidly as China market develops.

When entering China market, foreign FIs need to consider how to quickly

adapt to the local regulatory environment.

• Foreign FIs may consider bringing in innovative financial services from

global market, which requires additional communications with regulatory

authorities to review and approve.

Business operation optimization

• Once established China business, Foreign FIs need to build up local

operation team or outsource to such function to local service providers.

The real challenge is how to integrate local operation with global

management framework and process in order to better leverage global

leading practices.

• For some specific operational areas, such as human resource, risk

management, product management, customer and channel management,

financial budgeting, IT system etc, it takes efforts to tailor global

methodologies into the unique settings of China market.

Products & services differentiation

• After rapid development in the recent decade, some major local FIs have

established certain competitive advantages, accumulated a large number

of customers, and extended branch network to wide geographic areas. It is

essential for Foreign FIs to make strategic plans and road maps to

leverage global capabilities to develop differentiated products and services

so as to boost make share and revenue growth.

Global FIs Anticipated Challenges in Developing China Market

28

Most leading FIs in China are PwC clients. This enables us with deep insights on

market trends and dynamics. By providing end-to-end professional services from

strategy to operation, PwC can help foreign FIs address challenges in China.

PwC has wide range of capabilities which can be leveraged to provide various end-to-end support to foreign FIs covering everything from license application to business development

PwC has been providing professional support to various regulatory authorities in China for

decades, including advising on the development of regulations. We can help foreign FIs to evaluate

latest regulations, and facilitate your communications with regulators.

Strategy

Cost

Control

IT

Forensic

Business

Valuation

M&A

Financing

Innovation &

Development

Organization

setup

Reshaping

Execution of

Transaction

Risk Monitoring

Use of Talent

IT application

Risk Management

Talent

Management

Reorganization

Promoting

Transaction ValueFinancial

Management

Operation

Clients

Demands

Compliance to regulatory requirement

and communication with regulators

Target market analysis and strategic

planning

Design and optimization of operation

processes

Design and implementation of risk

management mechanism and system

Finance, accounting and assurance

Financial advisory service and

transaction support during M&A

activities

Tax planning

Long term incentive mechanism design

29

Global FIs Anticipated Challenges in Developing China Market

30

James Chang

China Financial Services Consulting Leader

+86 (10) 6533 2755

Harry Qin

China Asset & Wealth Management Consulting Lead Partner

+86 (10) 6533 5356

Jason B Li

China Financial Service Consulting Director

+86 (10) 6533 7676

Contact us

This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

© 2018 PricewaterhouseCoopers Management Consulting (Shanghai) Limited. All rights reserved. PwC refers to the China member firm, and may sometimes refer to the

PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. CN-20180130-3-C1

www.pwccn.com