A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

Odeon & UCI Finco plc

FY 2013 Investor Presentation

20 March 2014

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

Disclaimer

DISCLAIMER

THIS DOCUMENT HAS BEEN PREPARED BY ODEON & UCI FINCO PLC (“ODEON”). BY REVIEWING THIS

DOCUMENT OR PARTICIPATING IN THE CONFERENCE CALL THAT PRESENTS IT, YOU AGREE TO BE BOUND

BY THE FOLLOWING CONDITIONS.

THIS DOCUMENT IS FOR INFORMATION PURPOSES ONLY AND DOES NOT CONSTITUTE AN OFFER TO SELL OR

THE SOLICITATION OF AN OFFER TO BUY SECURITIES IN ODEON. FURTHERMORE, IT DOES NOT CONSTITUTE

A RECOMMENDATION BY ODEON OR ANY OTHER PARTY TO SELL OR BUY SECURITIES IN ODEON OR ANY

OTHER SECURITIES. ALL WRITTEN OR ORAL FORWARD-LOOKING STATEMENTS ATTRIBUTABLE TO ODEON

OR PERSONS ACTING ON THEIR BEHALF ARE QUALIFIED IN THEIR ENTIRETY BY THESE CAUTIONARY

STATEMENTS.

Unaudited Information

This document contains financial information regarding ODEON and its fellow subsidiaries (the “Group”). Such financial

information may not have been audited, reviewed or verified by any independent accounting firm. The inclusion of such

financial information in this document or any related presentation should not be regarded as a representation or warranty

by ODEON, any of its respective affiliates, advisors or representatives or any other person as to the accuracy or

completeness of such information’s portrayal of the financial condition or results of operations by the Group.

Non-GAAP information

We have presented certain non-GAAP information in this document. As used in this document, this information includes

‘‘EBITDA’’, which represents earnings before interest, tax, depreciation, amortisation, exceptional items and strategic

costs. Our management believes that EBITDA is meaningful for investors because it provides an analysis of our

operating results, profitability and ability to service debt and because EBITDA is used by our chief operating decision

makers to track our business evolution, establish operational and strategic targets and make important business

decisions. In addition, we believe that EBITDA is a measure commonly used by investors and other interested parties in

our industry.

2

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

Forward-Looking Statements

Forward-Looking Statements

This document includes forward-looking statements. When used in this document, the words “anticipate”,

“believe”, “estimate”, “forecast”, “expect”, “intend”, “plan” and “project” and similar expressions, as they relate to

ODEON, its management or third parties, identify forward-looking statements. Forward-looking statements

include statements regarding ODEON’s business strategy, financial condition, results of operations, and market

data, as well as any other statements that are not historical facts. These statements reflect beliefs of ODEON’s

management, as well as assumptions made by its management and information currently available to ODEON.

Although ODEON believes that these beliefs and assumptions are reasonable, the statements are subject to

numerous factors, risks and uncertainties that could cause actual outcomes and results to be materially different

from those projected. These factors, risks and uncertainties expressly qualify all subsequent oral and written

forward-looking statements attributable to ODEON or persons acting on its behalf.

3

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

Contents

Highlights

EBITDA

Markets, Films and 3D

KPIs, Margins and Costs

Spain

Cash Flow, Net Debt and Leverage

2013 Activity Highlights

Current Trading and Outlook

4

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

Highlights

5

Q4 EBITDA was £33.2m, our second highest quarter on record.

- Operating costs Like For Like were reduced, particular progress in Spain.

- Gross profit margin improved.

- Group market share for the year has remained broadly stable.

- Good local content in Italy and Germany

- But did not match the exceptional Q4 2012 with Skyfall in the UK and Germany and Impossible

in Spain.

Good progress to position the business for volume recovery.

Strong finish to year did not fully compensate for weaker quarters mid-year.

Markets down 5% for the year overall.

- Very hot summer.

- Weaker slate.

- Spain.

Strong working capital release of £37m in the quarter. Net Debt was reduced by £108m, repaying the

revolver and leaving cash on balance sheet of £40m at year end.

PropCo asset disposals progressed well and expected to be completed by end Q1.

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

0.0

10.0

20.0

30.0

40.0

50.0

60.0

2009 2010 2011 2012 2013

£m

Q1 Q2 Q3 Q4

Quarterly EBITDA

6

Long hot

summer,

depressed

Spain

Avatar

Skyfall & prior year

one off (£9m)

Olympics

& Euros

Q4 2013 EBITDA was our second highest earning quarter on record.

£9m

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

Total Market by Major Territory

7 (1) Average of all our territories’ market attendances, weighted on our 2012 attendances.

Q4 2013 Variance FY 2013 Variance

Odeon UCI

Attendance

FY Growth %

UK Market Attendance (k) 40,350 (19.1%) 165,540 (4.0%)

Germany Market Attendance (k) 40,265 (5.6%) 129,675 (4.0%)

Italy Market Attendance (k) 37,020 10.1% 106,007 5.9%

Spain Market Attendance (k) 22,889 (19.5%) 79,712 (15.3%)

Average Weighted Market(1) incl. Spain (11.2%) (4.8%) (2.9%)

Average Weighted Market(1) excl. Spain (8.8%) (1.6%) (0.4%)

Q4 market attendance(1) was 11% below 2012, largely due to the strength of last year’s

blockbuster Skyfall, especially in UK and Germany, and The Impossible in Spain. The Italian

market was ahead of Q4 2012 as Sole A Catinelle played, the biggest film in Italy since

Titanic in 1998, and F**k Ju Gohte played well in Germany.

Full Year market attendance(1) was down 5% overall. Italy was up, UK and Germany down,

Spain significantly so. Excluding Spain, Full Year market attendance(1) was down 2%.

Group attendance for the year performed better than the market, including and excluding

Spain.

Full Year Attendance Growth Ahead of Market in Spain and Italy

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

Top Films Q4

8

2012 2013 % change

Q4 Actual

(GBO £m)

Q4 Actual

(GBO £m)

Skyfall 100 Hunger Games: Catching Fire 32

Hobbit: An Unexpected Journey

(2D&3D) 37

Hobbit: The Desolation Of Smaug

(2D&3D) 32

Twilight Saga: Breaking Dawn - Part 2 35 Gravity (2D&3D) 27

Taken 2 24 Frozen (2D&3D) 26

Madagascar 3: Europe's Most Wanted

(2D&3D) 22 Thor: The Dark World (2D&3D) 20

Top 5 Total 219 Top 5 Total 137 (37%)

Total Market 357 Total Market 296 (17%)

In UK & Ireland, Skyfall

dominated the market in

Q4 2012, dwarfing this

year’s winner, The

Hunger Games: Catching

Fire. This year’s

instalment of The Hobbit

was weaker than last

year’s.

In Germany, although the

local and top title of Q4

2013, F**k Ju Gohte,

played very strongly, it fell

short of the success of

Skyfall last year.

Q4 Actual

(Adm m)

Q4 Actual

(Adm m)

Skyfall 7.2 F**k Ju Göhte 5.5 Hobbit: An Unexpected Journey

(2D&3D) 4.3

Hobbit: The Desolation Of Smaug

(2D&3D) 4.4

Madagascar 3: Europe's Most Wanted

(2D&3D) 3.8 Hunger Games: Catching Fire 3.4

Twilight Saga: Breaking Dawn - Part 2 3.4 Frozen (2D&3D) 3.3 Hotel Transylvania (2D&3D) 1.1 Thor: The Dark World (2D&3D) 1.4 Top 5 Total 19.9 Top 5 Total 18.1 (9%)

Total Market 42.6 Total Market 40.3 (6%)

UK & Ireland

Germany

Local titles in red

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

Top Films Q4 (cont.)

9

In Italy, the top film

this year in Q4

was the record

breaking local title,

Sole A Catinelle,

which drew the

strongest

audiences since

Titanic in 1998.

In Spain, the Top

2 films of last year,

The Impossible,

and Twilight were

screened in Q4.

There was a lack

of comparable

blockbusters this

year. Local titles in red

Q4 Actual

(Adm m)

Q4 Actual

(Adm m)

The Impossible 5.9 Hobbit: The Desolation Of Smaug

(2D&3D) 1.9

Twilight Saga: Breaking Dawn - Part 2 3.2 Frozen (2D&3D) 1.9

Hobbit: An Unexpected Journey

(2D&3D) 2.2 Hunger Games: Catching Fire 1.6

Hotel Transylvania (2D&3D) 1.7 Gravity (2D&3D) 1.2

Skyfall 1.5 Thor: The Dark World (2D&3D) 1.0

Top 5 Total 14.5 Top 5 Total 7.7 (47%)

Total Market 28.4 Total Market 22.9 (19%)

2012 2013

%

change Q4 Actual

(Adm m)

Q4 Actual

(Adm m)

Twilight Saga: Breaking Dawn - Part 2 3.1 Sole A Catinelle 8.7 Ice Age 4: Continental Drift (2D&3D) 2.6 Despicable me 2 (2D&3) 2.6

Skyfall 2.1 Frozen (2D&3D) 1.9 Ted 1.8

Hobbit: The Desolation Of Smaug

(2D&3D) 1.6

Hobbit: An Unexpected Journey

(2D&3D) 1.8 Colpi Du Fortuna 1.4

Top 5 Total 11.4 Top 5 Total 16.2 +42%

Total Market 33.6 Total Market 37.0 +10%

Spain

Italy

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2 18%

22%

26%

21%

10%

31%

17%

13%

20%

25%

13%

24%

0%

5%

10%

15%

20%

25%

30%

35%

Q1 Q2 Q3 Q42011 2012 2013

3D Quarterly Performance

3D represented 24% of the UK & Ireland market BOR, higher than Q4 last year when 2D product dominated

(Skyfall, Twilight).

There were more 3D titles on release in Q4 this year and four of the Top 5 films were 3D, only two last year.

Gravity played particularly well in 3D.

Avengers

Titanic

Harry

Potter 7.2

UK

& I

rela

nd M

ark

et

3D

BO

R a

s %

of

Tota

l B

OR

2013 included more 3D films than in 2012 10

UK & Ireland Market 3D Box Office Revenue (BOR) as a percentage of Total BOR

Tangled

Skyfall

Twilight

In 2D

Iron man 3,

Man of Steel

Ice Age 4

Spiderman

Tin Tin

Lion King 3D

Life of Pi

The Hobbit

Gravity

Frozen

Thor

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

107.8 110.0101.6 98.4 94.2

79.7

0

20

40

60

80

100

120

2008 2009 2010 2011 2012 2013

129.4146.3

126.6 129.6 135.1 129.7

020406080

100120140160

2008 2009 2010 2011 2012 2013

111.0 109.0120.6

112.1

100.1106.0

0

20

40

60

80

100

120

140

2008 2009 2010 2011 2012 2013

162.5172.9 168.8 172.1 172.5 165.5

0

50

100

150

200

2008 2009 2010 2011 2012 2013

Full Year Market Attendance

2013 was the weakest of four of the previous five years in the UK and Italy.

2013 was weaker than the previous five years in Spain.

11

Territory Market attendances were below their recent averages

UK 2008 – 2013 Market

Germany 2008 – 2013 Market Italy 2008 – 2013 Market

Spain 2008 – 2013 Market

6 year average 6 year average

6 year average 6 year average

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

17.4%

18.0%

18.5%

18.9%

18.2%

18.4%18.5%

18.6%

18.4% 18.4%

16.5%

17.0%

17.5%

18.0%

18.5%

19.0%

Q1 Q2 Q3 Q4 Full Year

2012 2013

Group Average Market Share

12

Full Year market share broadly stable

Market share(1) in Q4 did not compare to the strong performance achieved last year, particularly

on Skyfall. Our estate tends to perform better on blockbusters and with higher levels of market

attendance. Nevertheless, market share(1) increased marginally year on year.

(1) Weighted average of all our territories’ attendance market shares.

Mark

et share

(1)

Group Weighted Average Market Share(1)

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

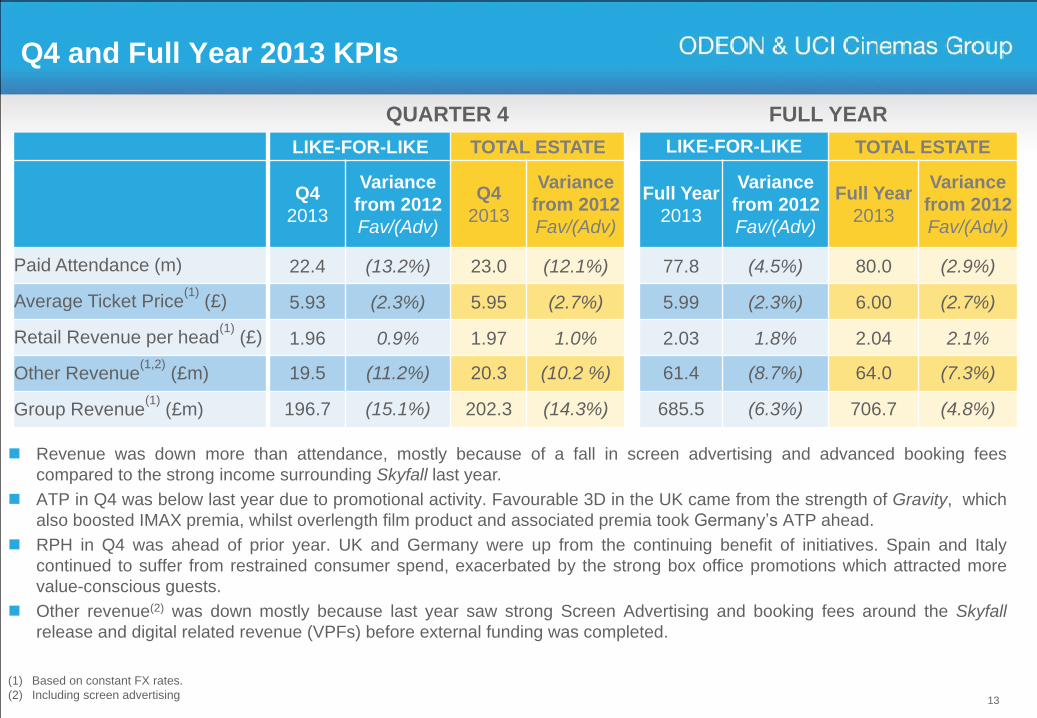

Revenue was down more than attendance, mostly because of a fall in screen advertising and advanced booking fees

compared to the strong income surrounding Skyfall last year.

ATP in Q4 was below last year due to promotional activity. Favourable 3D in the UK came from the strength of Gravity, which

also boosted IMAX premia, whilst overlength film product and associated premia took Germany’s ATP ahead.

RPH in Q4 was ahead of prior year. UK and Germany were up from the continuing benefit of initiatives. Spain and Italy

continued to suffer from restrained consumer spend, exacerbated by the strong box office promotions which attracted more

value-conscious guests.

Other revenue(2) was down mostly because last year saw strong Screen Advertising and booking fees around the Skyfall

release and digital related revenue (VPFs) before external funding was completed.

Q4 and Full Year 2013 KPIs

13

QUARTER 4 FULL YEAR

LIKE-FOR-LIKE TOTAL ESTATE LIKE-FOR-LIKE TOTAL ESTATE

Q4

2013

Variance

from 2012

Fav/(Adv)

Q4

2013

Variance

from 2012

Fav/(Adv)

Full Year

2013

Variance

from 2012

Fav/(Adv)

Full Year

2013

Variance

from 2012

Fav/(Adv)

Paid Attendance (m) 22.4 (13.2%) 23.0 (12.1%) 77.8 (4.5%) 80.0 (2.9%)

Average Ticket Price(1)

(£) 5.93 (2.3%) 5.95 (2.7%) 5.99 (2.3%) 6.00 (2.7%)

Retail Revenue per head(1)

(£) 1.96 0.9% 1.97 1.0% 2.03 1.8% 2.04 2.1%

Other Revenue(1,2)

(£m) 19.5 (11.2%) 20.3 (10.2 %) 61.4 (8.7%) 64.0 (7.3%)

Group Revenue(1)

(£m) 196.7 (15.1%) 202.3 (14.3%) 685.5 (6.3%) 706.7 (4.8%)

(1) Based on constant FX rates.

(2) Including screen advertising

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

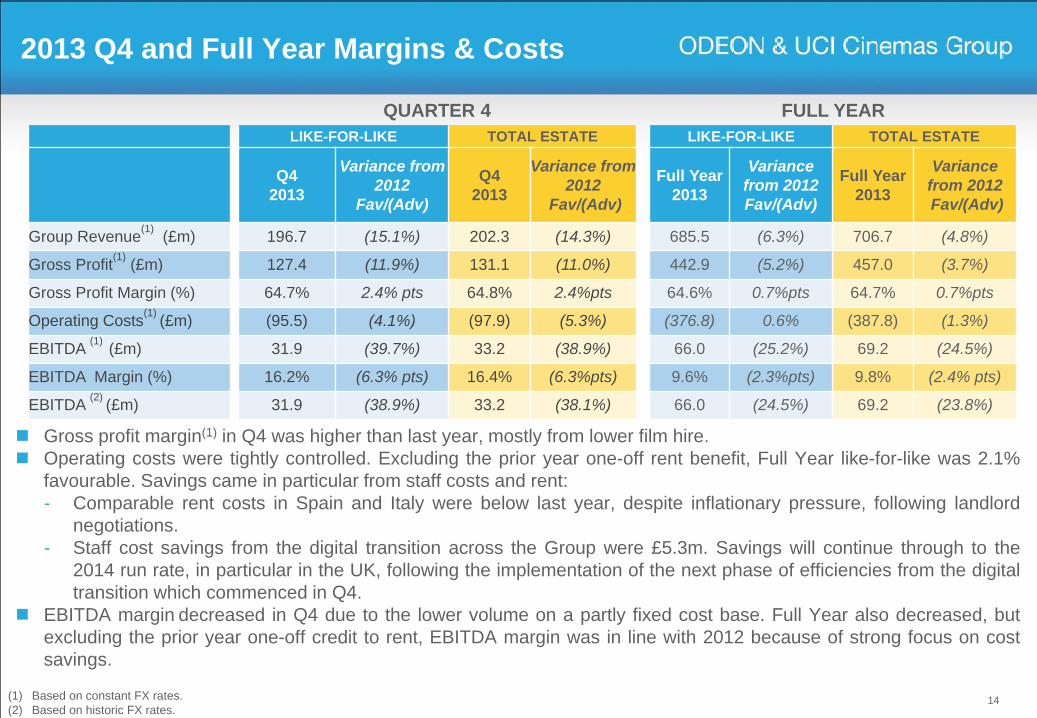

2 Gross profit margin(1) in Q4 was higher than last year, mostly from lower film hire.

Operating costs were tightly controlled. Excluding the prior year one-off rent benefit, Full Year like-for-like was 2.1%

favourable. Savings came in particular from staff costs and rent:

- Comparable rent costs in Spain and Italy were below last year, despite inflationary pressure, following landlord

negotiations.

- Staff cost savings from the digital transition across the Group were £5.3m. Savings will continue through to the

2014 run rate, in particular in the UK, following the implementation of the next phase of efficiencies from the digital

transition which commenced in Q4.

EBITDA margin decreased in Q4 due to the lower volume on a partly fixed cost base. Full Year also decreased, but

excluding the prior year one-off credit to rent, EBITDA margin was in line with 2012 because of strong focus on cost

savings.

2013 Q4 and Full Year Margins & Costs

14 (1) Based on constant FX rates.

(2) Based on historic FX rates.

QUARTER 4 FULL YEAR

LIKE-FOR-LIKE TOTAL ESTATE LIKE-FOR-LIKE TOTAL ESTATE

Q4

2013

Variance from

2012

Fav/(Adv)

Q4

2013

Variance from

2012

Fav/(Adv)

Full Year

2013

Variance

from 2012

Fav/(Adv)

Full Year

2013

Variance

from 2012

Fav/(Adv)

Group Revenue(1)

(£m) 196.7 (15.1%) 202.3 (14.3%) 685.5 (6.3%) 706.7 (4.8%)

Gross Profit(1)

(£m) 127.4 (11.9%) 131.1 (11.0%) 442.9 (5.2%) 457.0 (3.7%)

Gross Profit Margin (%) 64.7% 2.4% pts 64.8% 2.4%pts 64.6% 0.7%pts 64.7% 0.7%pts

Operating Costs(1)

(£m) (95.5) (4.1%) (97.9) (5.3%) (376.8) 0.6% (387.8) (1.3%)

EBITDA (1)

(£m) 31.9 (39.7%) 33.2 (38.9%) 66.0 (25.2%) 69.2 (24.5%)

EBITDA Margin (%) 16.2% (6.3% pts) 16.4% (6.3%pts) 9.6% (2.3%pts) 9.8% (2.4% pts)

EBITDA (2)

(£m) 31.9 (38.9%) 33.2 (38.1%) 66.0 (24.5%) 69.2 (23.8%)

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

Cost Savings

Costs were managed tightly last year, and efficiencies improved, with

significant savings achieved against what would have been incurred if

no action had been taken.

2014 will benefit from the flow through of run rate savings as well as

new savings targeted.

Group Employment costs

- Digital savings resulted in over £5m incremental savings in 2013 with a

further £2m run rate benefit in 2014.

- Staff cost savings in Spain in 2013 of £3m and elsewhere £1m, and a

further £1m run rate savings to come in 2014.

Group Operating Costs and Support Office

- £6m lower than 2012 inflated.

Group Rent

- A mixture of long and short term agreements resulted in savings in 2013 of

over £4m with a further £2m run rate savings to come in 2014.

- Additional reductions are targeted in 2014.

15

Note: The above charts are based on LFL costs, with 2012 rent

adjusted for £9m PY landlord contribution . Inflationary increases

of 2% assumed.

122115

9

2

9095

100105110115120125130

2012 Infl. increase

Saving 2013

£m

Group Employment Costs

136 133

63

90

100

110

120

130

140

150

2012 Infl. increase

Saving 2013

£m

Group Operating/ Support Office Costs

130 129

43

9095

100105110115120125130135

2012 Infl. increase

Saving 2013

£m

Group Rent

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

Excluding Spain, attendance was in line with

2012, from increased share in markets down

2%.

ATP was lower than last year because of a

lower 3D proportion and promotional activity,

but RPH was ahead.

EBITDA was 9% behind last year, due to one

off credits in 2012.

Excluding Spain and also the prior year one-

off benefit to rent (adjustment of landlord

contribution accounting), EBITDA was 2%

down.

EBITDA margin was 11.9%, (1.0%) pts lower

than 2012, or in line with 2012 when the prior

year one-off benefit is also excluded.

Group Highlights Excluding Spain

16

Full Year YoY

% Growth Group

Group

excl.

Spain

Group excl.

Spain and

2012 one-

off

Attendance (3%) - -

ATP(1) (3%) (2%) (2%)

RPH(1) +2% +3% +3%

Other revenue

& screen ads(2) (7%) (5%) (5%)

Revenue(2) (5%) (2%) (2%)

EBITDA(3) (24%) (9%) (2%)

(1) At constant FX rates and constant territory weighting, for major territories.

(2) At constant FX rates.

(3) At historic FX rates.

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

7.3%

14.7% 15.4% 15.4%

20.6% 21.6%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2005 2009 2010 2011 2012 2013

Spain

17

Decline in the number of screens in the

Spanish market

In Spain, market attendance was down on prior year (15% full year,

19% Q4), with the impact of the September 2012 VAT increase on

ticket prices exacerbated by the weak economy and high

unemployment. Market attendance was down in Q4 due to strong

admissions in The Impossible in 2012.

Competitors’ screens have been closing, further correcting the historic

over-screening in the country.

We have been repositioning the business for lower market volumes

and to be able to capitalise on recovery from a position of strength:

– We have closed 3 loss-making cinemas.

– We have been renegotiating costs, staff cost and rent in particular, down

respectively 14% and 5% (excluding Landlord Contribution) versus prior year

for the Like-for-Like estate.

– We have continued to gain attendance market share to over 21% in 2013, the

clear #1 in the market, over 8% pts ahead of our nearest rival.

The underlying demand for cinema is still present.

In 2014, there are some early signs that the economy may be turning

(see next slide).

Attendance Market Share

Q4 Market Attendance

4,401

4,082

3,832

3,500

3,600

3,700

3,800

3,900

4,000

4,100

4,200

4,300

4,400

4,500

2005 2009 2013** Estimated

2326

28

23

0

5

10

15

20

25

30

2010 2011 2012 2013

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

Spain Macroeconomic Conditions

18

2013 2014

GDP (1.4%) 0.9%

Unemployment 26.4% 25.6%

CPI (%) Average 1.4% 0.5%

Source: Historic information from National Statistics Institute, forecasts from BBVA research.

Macro-economic indicators may be turning in Spain: unemployment has started to fall slightly, whilst

Retail Sales grew in Q3 and Q4. Some banks are forecasting a positive 2014.

BBVA Annual Forecast

8.3

11.3

18.0 20.1

21.6

25.0 27.2 26.3 26.0 26.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

2007 2008 2009 2010 2011 2012 Q12013

Q22013

Q32013

Q42013

%

Unemployment rate

(2.1)

(7.5)

(1.2)

(4.5)

(6.5)

(10.8) (10.8)

(6.9)

2.1

0.3

(12.0)

(10.0)

(8.0)

(6.0)

(4.0)

(2.0)

0.0

2.0

4.0

2007 2008 2009 2010 2011 2012 Q12013

Q22013

Q32013

Q42013

%

Annual Retail Sales Movement

0.6

0.3

0.0

(0.6)

(1.2)

(1.6) (1.7)

(2.1) (2.0)

(1.6)

(1.1)

(0.1)

0.9

(2.5)

(2.0)

(1.5)

(1.0)

(0.5)

0.0

0.5

1.0

1.5

%

Quarterly GDP Movement

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

Odeon Property Group

19

In the Q3 investor presentation we described

how Odeon Property Group had sold 16 of its

properties and used the proceeds to repay

bank debt and £13m of loans from

OUCG/OUCH, which was contributed as

equity to the bond group.

By the year end, an additional 6 properties

were sold bringing the total equity contributed

to the bond group to £27m.

The disposals resulted in £29m of finance

leases being reclassified as operating leases,

reducing net debt.

Completion on the remaining 6 properties will

be before quarter end, leading to an

anticipated further contribution to Opco of

over £16m.

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

2013 Q4 and Full Year Cash Flow and Net Debt

Net debt was reduced by £108m in the quarter and £14m for the year leading to the full repayment of the

revolver and cash at year end of £40m.

Working capital was positive £37m in the quarter, reflecting seasonal stronger year end trading, but negative

£7m for the year, principally due to the unwind in Q1 2013 of the strong trading in Q4 2012 from Skyfall.

Capital expenditure was £6m in Q4 and £30m for the year, lower than 2012 with capex reduced in response to

the lower EBITDA.

Finance costs in Q4 were £7m, primarily representing one quarter’s Euro note interest. The half-yearly Sterling

note interest payments are made in February and August. The interest rate swap on floating rate notes will

reduce from 9.1% to 5.3% from May 2014, saving €7m pa.

PropCo proceeds of £27m were received as equity in the year and the disposals led to the removal of £29m of

finance leases. 20

Q4 2012 Q4 2013 FY 2012 FY 2013

£m

EBITDA 53.6 33.2 90.8 69.2

Working capital and other 21.0 37.4 12.7 (6.7)

Net capital expenditure (12.4) (6.2) (41.9) (30.2)

Provisions and one offs (5.4) (5.1) (15.7) (14.6)

Finance costs (8.8) (7.2) (60.0) (55.8)

Tax (0.8) (0.3) (2.6) (1.1)

Acquisitions and disposals (3.3) (0.5) (3.6) (1.1)

PropCo 0.0 56.3 0.0 56.3

Fx and other (3.7) (0.1) 4.6 (1.8)

Change in Net Debt 40.2 107.5 (15.7) 14.2

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

Debt and Leverage

LTM EBITDA decreased, as Q4 2013 EBITDA couldn’t match the record breaking last

quarter from 2012.

Cash flow was particularly strong in Q4, reducing year end net debt to £436m.

Despite the reduction in net debt, leverage increased to 6.1x due to the lower LTM

EBITDA.

21

(1) Proforma adjustments for Q4 2013 relate to Digital cost savings and new sites.

Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013

LTM EBITDA £m 91 97 93 90 69

Proforma adjustments(1)

£m 6 4 3 2 3

Proforma LTM EBITDA £m 97 101 96 92 72

Net Debt £m 450 500 511 544 436

Net Debt to EBITDA 4.6x 4.9x 5.3x 5.9x 6.1x

Fixed Charge Cover 2.6x 2.7x 2.6x 2.5x 1.9x

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

2013 Q4 and Full Year Activity Highlights

New Sites

– In October, Trowbridge with 7 screens.

– In December, Villesse, Italy, with 7 screens.

– Earlier we opened Gualtieri in Italy (3 screens) and West Bromwich (5 screens).

– At the end of December we operated 239 cinemas with 2,191 screens.

Retail Innovation

– Lobby refurbishment at Vienna SCS, adding a coffee bar.

– Our first Coffee Republic opened during December at Glasgow Braehead.

– New Costa Coffee at Trowbridge took our total UK Costa Coffee outlets to 41.

Digital – New digital plasma screens in Germany.

State-of-the-art LED signage across 3 substantial panels onto the front of Odeon

Leicester Square.

22

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

Note: Based on UK slate phasing, top 5 films of each year in red.

2014 Estimated Top 20 Title Phasing

The slate seems to be evenly phased compared to previous years, and has a stronger Q3 than 2013.

2013 Top 20 2014 Top 20

Q1 Life of Pi 3D Lego 3D

Les Miserables IMAX Captain America 2: Winter Soldier 3D

Django Unchained Mr Peabody and Sherman 3D

Wreck-It Ralph 3D Muppets Most Wanted

The Croods 3D The Wolf of Wall Street

The Hobbit: An Unexpected Journey 3D IMAX 12 Years a Slave

Q2 Iron Man 3 3D IMAX The Amazing Spiderman 2 3D IMAX

Star Trek Into Darkness 3D IMAX X-Men: Days of Future Past 3D

Fast and Furious 6 Godzilla 3D IMAX

The Great Gatsby 3D Rio 2 3D

The Hangover Part III

Man of Steel IMAX

Q3 Despicable Me 2 3D How to Train Your Dragon 2 3D IMAX

Monsters University 3D Inbetweeners 2

Dawn of the Planet of the Apes 3D

Transformers 4 3D IMAX

Guardians of the Galaxy 3D IMAX

Q4 Thor: The Dark World 3D IMAX The Hunger Games: Mockingjay Part 1 IMAX

Gravity 3D IMAX The Hobbit: There and Back Again 3D IMAX

Hunger Games: Catching Fire IMAX Interstellar IMAX

Captain Phillips Paddington Bear

Frozen 3D Taken 3

The Hobbit: The Desolation of Smaug 3D IMAX

23

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

Current Trading and Outlook

The year has got off to a good start, with the ‘awards season’ films playing well (e.g. 12

Years A Slave, The Wolf of Wall Street and American Hustle) and, adjusting for Easter,

Q1 markets are expected to be comparable to Q1 2013.

Growth in our portfolio continues, with three sites taken over in Italy, for a small amount

of capex. We are looking at similar opportunities in Spain.

Run-rate benefits of approximately £5m of cost savings made in 2013 will flow into 2014

EBITDA. Finance costs will reduce by €7m pa from May.

A rebound in the Spanish economy would see a recovery in the cinema market, and

economic recovery across Europe is expected to see increases in revenue KPIs and

screen advertising, but we are not building these into our expectations for 2014,

because timing is uncertain. These recovery factors would be upside.

2014 film slate looks to be well balanced across the year with some good IMAX and 3D

titles, as well as local content.

24

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

Q&A & AOB

Any questions?

Further questions can be addressed below: – Email: [email protected]

– PR: [email protected]

– Financial PR: [email protected]

25

A4 FORMAT

Please don’t

change page set

up to A3, print to

A3 paper and fit

to scale

41

170

224

253

208

48

198

96

127

182

143

2

Films to come

26