ACC/JDC/FENWICK & WEST LLP Nonprofit Legal Audit Clinic "March 18, 2016"

Corporate Governance and Board of Directors Issues Affecting Section 501(c)(3) Organizations"

Lynda Twomey"March 18, 2016"

3

Review of Checklist Categories

3 3 3 3

I. Legal Form and Governance As a nonprofit and/or tax-exempt organization, you are subject to review by federal and state regulators. In general, nonprofit and tax-exempt organizations must satisfy certain on-going requirements under federal and state law. Similarly, organizational documents must satisfy certain federal and state requirements, and may contain additional requirements. Under certain circumstances, failure to satisfy these requirements could result in loss of your status under state law, loss of your federal tax-exempt status, and, in egregious circumstances, the imposition of an excise tax or penalties on the organization, its directors, or its officers. Every nonprofit and tax-exempt organization needs to understand these requirements and how to satisfy them.

CO

RPO

RAT

E G

RO

UP

4

Forming a Non-Profit Corporation

! Incorporation & Governance Steps:

• 1. Draft the Articles of Incorporation & Bylaws.

• 2. Incorporator files the Articles with the California Secretary of State.

• 3. Incorporator resigns and appoints the Board of Directors.

• 4. Board of Directors elects the officers and approves the Bylaws and other standard governance matters.

CO

RPO

RAT

E G

RO

UP

5

Articles of Incorporation

! Section 501(c)(3): Organizational Test:

• Articles must contain a provision limiting the Corporation to a “charitable” purpose – i.e.,

– “This corporation is a nonprofit public benefit corporation and is not organized for the private gain of any person. It is organized under the Nonprofit Public Benefit Corporation Law for a charitable purpose.”

• Articles must contain a dissolution clause – i.e., – “Upon the dissolution or winding up of the corporation, its assets remaining after payment, or provision for payment, of all debts and liabilities of this corporation shall be distributed to a nonprofit fund, foundation, or corporation which is organized and operated exclusively for charitable purposes and that has established its tax-exempt status under Section 501(c)(3) of the Code.”

CO

RPO

RAT

E G

RO

UP

6

Bylaws – Conflict of Interest Policy

! It is not required, but recommended by the IRS, that the Corporation adopt a “Conflict of Interest Policy.”

! This policy is typically drafted into the Bylaws.

! Good practice is to have all directors, officers and other principals sign a copy of the policy for inclusion in the Corporation’s records.

! Having a policy in place will help ensure that the Corporation maintains its tax-exempt status.

CO

RPO

RAT

E G

RO

UP

7

Filing the Articles

! An individual or entity acting as the “Incorporator” will file the Articles with the Secretary of State.

! After the filing, the Incorporator should execute a document whereby the Incorporator appoints the initial Board of Directors and resigns as the Incorporator.

CO

RPO

RAT

E G

RO

UP

8

Initial Board Actions

! Following its appointment, the Board should hold an initial meeting, or execute a unanimous written consent, to accomplish the following:

• Ratification of Incorporator actions • Approval of the Bylaws • Election of the officers • Approval of other standard governance matters

9

Management

! Directors are charged with overall management responsibility.

! Day-to-day management duties are delegated to off icers and employees under the Board’s supervision.

! Fiduciary obligations: Duties of

• (1) care

• (2) loyalty

• (3) obedience

10

Duty of Care

! Handle duties with such care as an ordinarily prudent person would exercise in a like position under similar circumstances.

! Directors must be diligent and informed, and should exercise honest and unbiased business judgment.

! Judges will not ordinarily interfere with the business judgments of directors absent a showing of gross negligence, fraud or an ultra vires act.

CO

RPO

RAT

E G

RO

UP

11

Duty of Care (cont.)

! The Business Judgment Rule generally requires that decisions be made:

• In good faith;

• Without a conflict of interest;

• On a reasonably informed basis; and

• With a rational belief that the business judgment is in the best interests of the corporation.

CO

RPO

RAT

E G

RO

UP

12

Duty of Loyalty

! A director should act in good faith and in the best interests of the corporation, not permitting his or her own interests to prevail over those of the corporation.

! Duty of Loyalty concerns primarily relate to:

• conflicts of interest

• corporate opportunities

• confidentiality issues

CO

RPO

RAT

E G

RO

UP

13

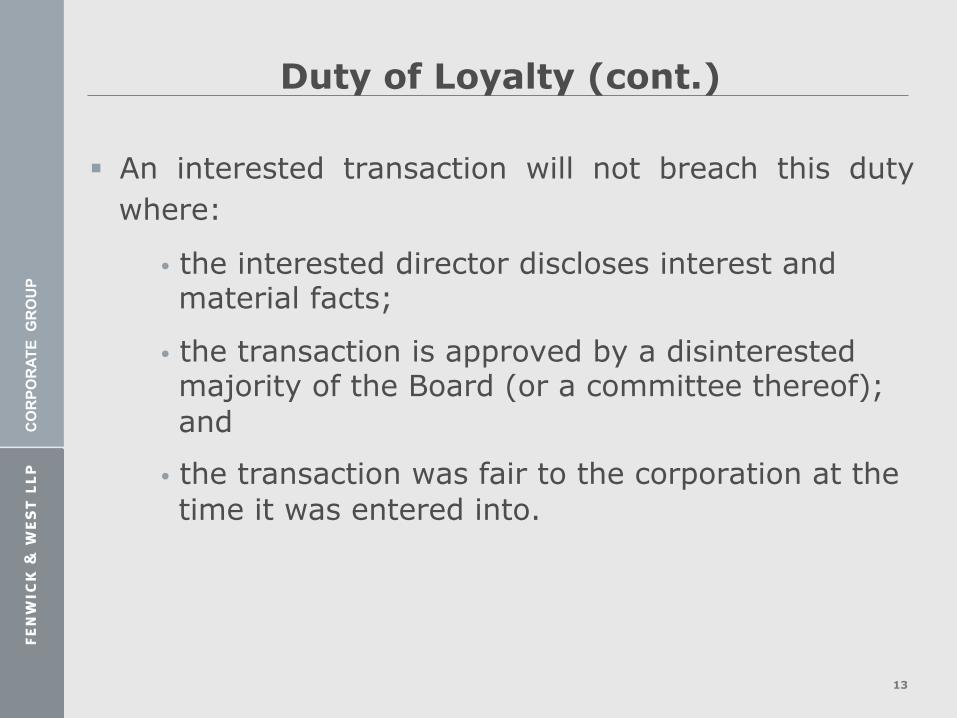

Duty of Loyalty (cont.)

! An interested transaction will not breach this duty where:

• the interested director discloses interest and material facts;

• the transaction is approved by a disinterested majority of the Board (or a committee thereof); and

• the transaction was fair to the corporation at the time it was entered into.

CO

RPO

RAT

E G

RO

UP

14

Duty of Obedience

! A director should act with fidelity, within the bounds of the law, to the organization’s mission and avoid committing acts beyond the scope of the powers of the corporation (ultra vires acts).

! A director is generally held liable only if the act is in violation of public policy or specific statute.

! Directors who deal with investment issues should be particularly aware of state laws affecting investments.

CO

RPO

RAT

E G

RO

UP

15

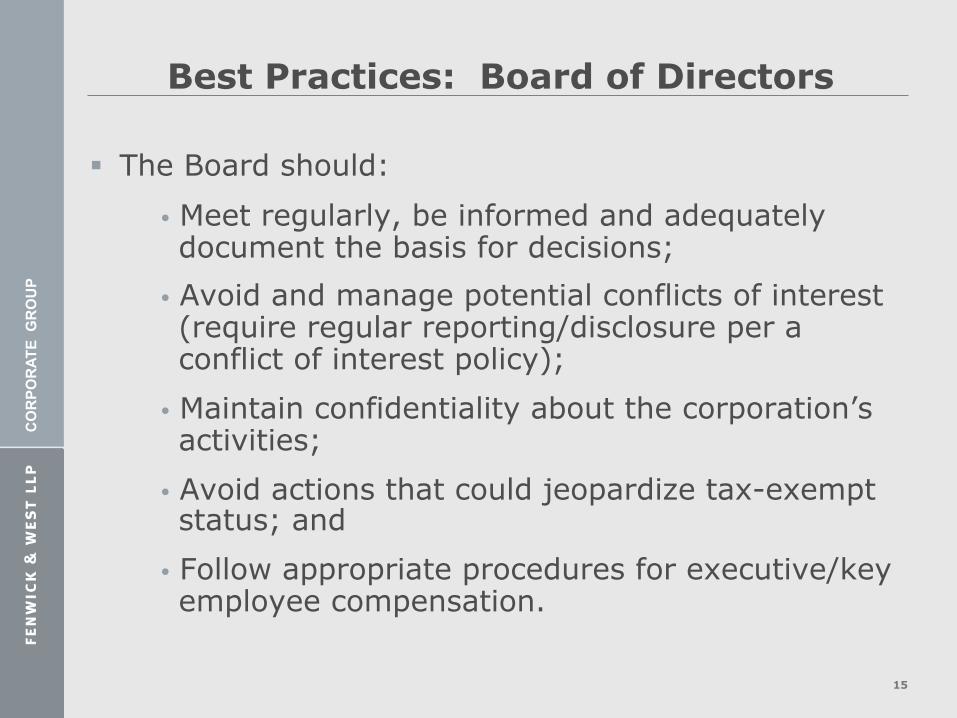

Best Practices: Board of Directors

! The Board should:

• Meet regularly, be informed and adequately document the basis for decisions;

• Avoid and manage potential conflicts of interest (require regular reporting/disclosure per a conflict of interest policy);

• Maintain confidentiality about the corporation’s activities;

• Avoid actions that could jeopardize tax-exempt status; and

• Follow appropriate procedures for executive/key employee compensation.

CO

RPO

RAT

E G

RO

UP

Conclusion

! Q&A

! Thank you!

16

Select Tax Issues Affecting Existing and Potential Section 501(c)(3) Organizations"Larissa Neumann"March 18, 2016"

Tax: Why Should A Lawyer Be Involved?

! Non-profits are closely policed because of favorable tax status and importance to the community.

! Federal/state regulatory review.

! Ongoing federal/state filing requirements.

! Avoiding civil penalties and potential liability.

18

19

Review of Checklist Categories

I. Reporting & Compliance with Federal, State and Local Regulations California nonprofit corporations and § 501(c)(3) organizations generally must satisfy certain annual reporting requirements. If you file annual reports with the IRS or local/state officials, the content of those reports is used to determine whether you still qualify for corporate and tax-exempt status. Information in those reports is also available for public inspection. You must understand what filing requirements apply under state and federal law and ensure that internal controls are in place to verify that reports are complete, accurate, and filed on a timely basis. Failure to satisfy these requirements could result in the imposition of a penalty (e.g., the penalty for failure to timely file IRS Form 990).

20

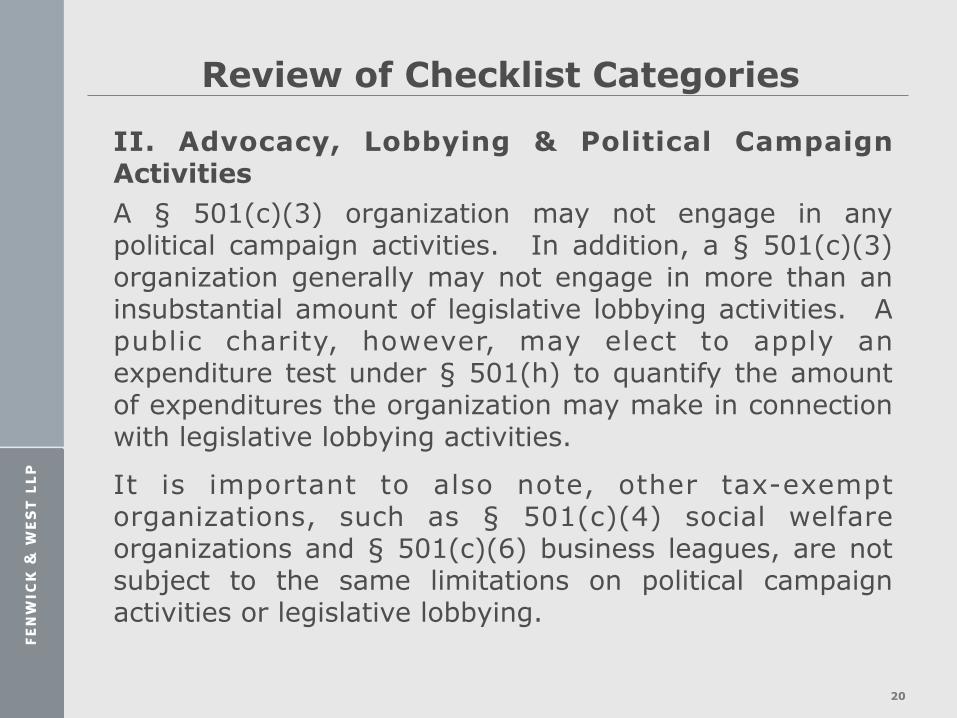

Review of Checklist Categories

II. Advocacy, Lobbying & Political Campaign Activities A § 501(c)(3) organization may not engage in any political campaign activities. In addition, a § 501(c)(3) organization generally may not engage in more than an insubstantial amount of legislative lobbying activities. A public charity, however, may elect to apply an expenditure test under § 501(h) to quantify the amount of expenditures the organization may make in connection with legislative lobbying activities.

It is important to also note, other tax-exempt organizations, such as § 501(c)(4) social welfare organizations and § 501(c)(6) business leagues, are not subject to the same limitations on political campaign activities or legislative lobbying.

21

Review of Checklist Categories

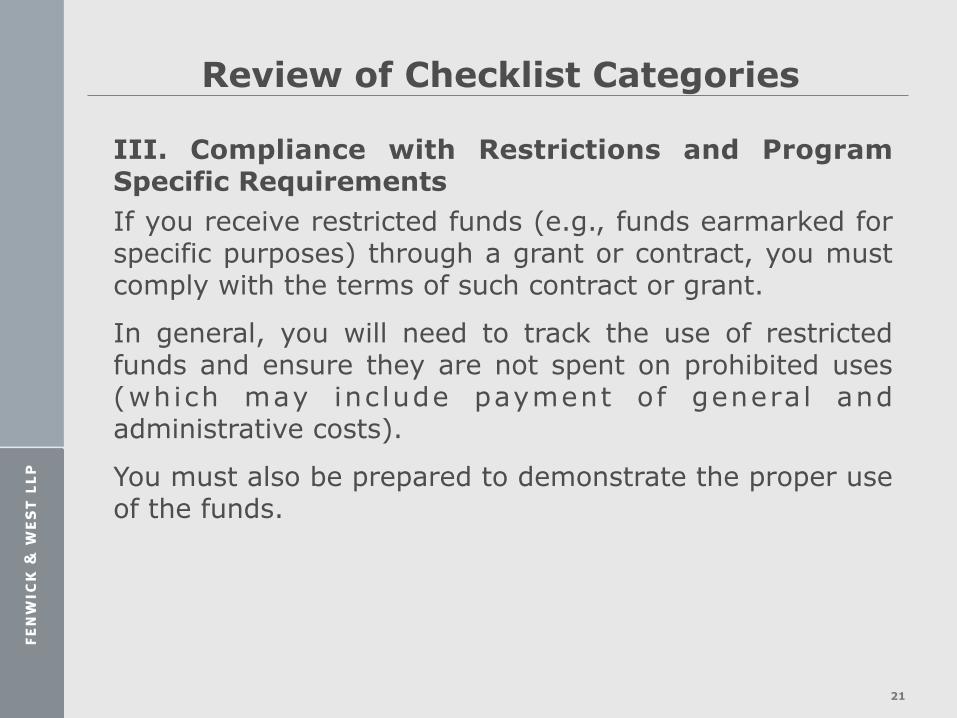

III. Compliance with Restrictions and Program Specific Requirements If you receive restricted funds (e.g., funds earmarked for specific purposes) through a grant or contract, you must comply with the terms of such contract or grant.

In general, you will need to track the use of restricted funds and ensure they are not spent on prohibited uses (which may inc lude payment of general and administrative costs).

You must also be prepared to demonstrate the proper use of the funds.

22

Review of Checklist Categories

IV. Earned Revenue & Unrelated Business Income Tax If you own or operate a business, either within your organization or through a separate entity, or if you charge fees for your services or charge fees for the sale of your products, you must determine whether the rules regarding commercial activities and the unrelated business income tax apply to your organization.

Under these rules, a § 501(c)(3) organization is subject to a tax at the highest corporate income tax rate on income derived from an activity that (a) constitutes a "trade or business," (b) is "regularly carried on," and (c) is not substantially related to the organization's tax exempt purpose. If such unrelated activity is substantial, the activity may jeopardize the organization's tax exempt status.

23

Review of Checklist Categories V. Compliance with Private Inurement, Excess Benefit and Self-Dealing Rules An organization does not qualify under § 501(c)(3) if any part of its "net earnings" inure to the benefit of any private "shareholder or individual" or insider (the "Private Inurement" doctrine).

Similarly, an individual (not just insiders) may not receive a benefit from a § 501(c)(3) organization not accorded the public as a whole (the "Private Benefit" doctrine). Violation of the Private Inurement or Private Benefit doctrines may result in loss of tax exempt status.

24

Review of Checklist Categories

VI. Finances and Fiscal Management Fiscal accountability is one of the most important obligations of any nonprofit organization. Because proper financial management can be very demanding and is subject to objective evaluations, it is also one of the areas that is most likely to get you into trouble.

Government regulators, such as the IRS or your state attorney general, and private and government contributors expect that you will keep accurate records and make efficient use of funds. If you become aware of any misallocation of funds, an attorney can work with your accountants to help you get back into compliance with regulations and grant or contract obligations. If you are in financial trouble, a lawyer also can help you negotiate with creditors and can advise on options, like bankruptcy or merger, which might be appropriate.

Review of Checklist Categories VII. Employment & Human Resources If you have employees or independent consultants, you have to comply with payrol l and withholding requirements and with a host of federal and local laws that regulate employment relationships.

You should know your rights and obligations as an employer and move quickly to strengthen any areas where proper compliance is in question.

25

Tax: Overview and Introduction

! Overview of § 501(c)(3) organizations:

• Public Charities

• Private Foundations

! Maintaining exempt status, including filing and reporting requirements.

! Typical hot button charitable organization management issues.

! Seeking tax deductible donations.

26

Tax: Public Charity/Private Foundation

! Section 501(c)(3) organizations are classified as either: • Public charities (broad public support). • Private foundations (limited sources of support, e.g., single individual, family, or corporation).

! Private foundations face higher degree of regulation with regard to:

• Self dealing • Mandatory distributions • Jeopardy investments • Excess business holdings • Taxable expenditures

27

Tax: Maintaining Exempt Status

Six components to qualifying / maintaining § 501(c)(3) tax-exempt status:

I. The organization must be organized exclusively for charitable purposes (“the Organizational Test”).

II. The organization must be operated exclusively for charitable purposes (“the Operational Test”).

III. No part of the organization’s net earnings may inure to the benefit of any private shareholder or individual.

IV. The organization may not conduct more than an insubstantial amount of lobbying activities.

V. The organization may not interfere in a political campaign. VI. The organization must file necessary documents annually.

28

I. The Organizational Test

! The corporation’s organizational documents must, at a minimum, contain:

• A limitation to “charitable” purposes.

• A proper dissolution clause.

! Satisfaction of the organizational test is basically a drafting issue.

29

II. The Operational Test

! The organization must be operated for one or more of the following charitable purposes: (1) religious, (2) charitable, (3) scientific, (4) testing for public safety, (5) literary, (6) educational, (7) fostering amateur sports competition, or (8) prevention of cruelty to children or animals.

! The organization’s activities or purposes may not be contrary to established or fundamental public policy.

! The organization must act in a manner consistent with its charitable purposes to continue to satisfy the operational test.

! Pressure Points:

• Board and officers must be cognizant of scope of permissible activities, especially when engaging in new activities.

• High profile media exposure can subject the organization to some risk of and IRS audit on this issue.

30

III. Prohibition on Private Benefit / Inurement ! The prohibition against private inurement targets “insiders”

i.e., those in a position to control the organization’s activities.

! Private benefit applies to third parties as well as insiders.

! Pressure Points: • Definition of “benefit” can be broad. • Transactions with Insiders:

– Fair and reasonable compensation – Transfer or license of property – Extension of credit – Provision of services

• Transactions with For-Profit Entities: – Arm’s-length compensation issues – Financial guarantees & other incentives – Lease of real estate or personal property from or to insiders

31

IV. Lobbying Limitations

! “No substantial part of the activities” of a public charity may constitute “carrying on propaganda, or otherwise attempting, to influence legislation.”

! Two tests (organization may elect): • A subjective “no substantial part” test that looks at the

substantiality (size & scope) of the activity. • The “lobbying election” which looks only at the amount of

expenditures the organization may make in connection with such activities.

! Private foundations are prohibited from lobbying.

! Pressure Points: • Notifying the IRS (as required and appropriate). • Monitoring exposure to hot political issues.

32

V. Prohibition on Political Intervention

! There is an absolute prohibition against participating or intervening in any political campaign (including publishing or distributing statements) on behalf of, or in opposition to, any candidate for public office or any public initiative.

! Pressure Points:

• Taking public positions on political candidates.

• Taking public positions on political issues.

33

VI. Federal and State (California) Filing and Reporting Requirements

! In order for a nonprofit corporation to maintain its status as a tax exempt organization it must file the following forms with the IRS annually:

• Form 990 (or 990-EZ if the corporation’s gross receipts for the year were under $200k and its total assets were less than $500k). Must be filed on or before the 15th day of the fifth month after the close of the tax year. Must be accompanied by Schedule A (Public Charity Status and Publ ic Support) and Schedule B (Schedule of Contributors).

• Form 990-T must be filed if the organization has gross income of $1,000 or more from UBIT.

34

Note on Unrelated Business Income Tax (“the dreaded UBIT”)

! Tax-exempt organizations are subject to tax on income derived from an �unrelated trade or business.� Too much UBIT may indicate a substantial non-exempt purpose and jeopardize exemption.

! Must know if have UBIT to know what filings to make.

! Three basic criteria are used to determine if UBIT exists: the activity must be (1) a trade or business; (2) regularly carried on; and (3) not substantially related to the organization�s exempt purpose.

! UBIT issues can be very complex and most organizations try to steer clear of the entire area. Flag for further follow up!

35

Federal and State (California) Filing and Reporting Requirements (Continued)

! In order for a nonprofit corporation to maintain its California tax exempt status under the California Revenue and Taxation Code section 23701(d) it must annually file:

• Form 199 - California Exempt Organization Annual Information Return. Form 199 is due within four and a half months of the close of the organization’s tax year and is filed with the California Franchise Tax Board.

• Form 109 - if the corporation has gross income in excess of $1,000 from UBIT. Must be filed within four and a half months after the end of the tax year.

36

Federal and State (California) Filing and Reporting Requirements (continued)

• Form RRF-1, Annual Report, must be filed with the California Attorney General Registry of Charitable Trust within four months and fifteen days after the end of the organization’s tax year. Must be accompanied by IRS Form 990 (or 990-EZ), if gross receipts or total assets are greater than $25,000.

• Form SI-100, Statement of Information, must be filed with the California Secretary of State biennially during calendar month in which the original articles of incorporation were filed and the immediately preceding five months.

37

Federal and State (California) Filing and Reporting Requirements (continued)

• The organization must provide all directors with an annual report within 120 days after the close of the fiscal year. This report must provide the company’s financial information, including assets, liabilities, receipts and expenditures as well as indemnification or self-dealing transactions.

! Pressure Points:

• Forms 990, 990EZ & 990-PF (and State equivalents) are “public” documents.

• Unique charitable solicitation and fundraising approaches may generate unwanted attention (e.g., selling name rights to college classes will get you in the news and could result in an IRS or State Attorney General examination).

• State Attorney Generals are watching and know how to take draconian action against a specific charity for conduct unbecoming of a charitable organization.

38

Charitable Organization Management: Board Obligations

! Directors are charged with overall management responsibility of a charitable organization’s activities.

! Board members are subject to fiduciary obligations: duties of (1) care, (2) loyalty, and (3) obedience.

! Day-to-day management duties are usually delegated to officers and employees under the board’s supervision.

! Pressure Points:

• Aggressive board members acting outside the scope of their authority.

• Failure to reasonably inquire into the actions of the organization’s officers.

39

Charitable Organization Management: Recommended Written Policies to Adopt

! In 2008 the IRS released governance guidelines for tax-exempt organizations, stating that it will review an organization’s application for exemption and annual information returns to determine whether the organization has implemented the following policies:

• Conflicts of interest, see IRS Forms 990 and 1023

• Executive compensation, see IRS Form 990

• Investments and Fundraising, see IRS Form 990

• Documenting governance decisions, see IRS Form 990

• Document retention and destruction, see IRS Form 990

• Whistleblower claims, see IRS Form 990

40

Recommended Written Policies to Adopt (Continued)

! Conflict of Interest Policy

• Is recommended, though not required. However -

• Form 1023 (Application for Recognition of Exemption) specifically asks the organization to answer the following questions or provide the following comments:

– Will the individuals that approve compensation arrangements follow a conflict of interest policy?

– Has the organization adopted a policy consistent with the sample provided in Appendix A of Form 1023?

– Has the organization provided to the IRS a copy of the policy and explained how the policy has been adopted?

– What procedures will the organization follow to assure that persons who have a conflict of interest will not have influence over the organization for setting their own compensation and regarding business deals with themselves?

41

Charitable Organization Management: Board Finance Issues

! Hire outside professional accountant for preparation of (audited) financial statements if necessary

! Establish Finance Committee and/or Audit Committee

! Establish internal financial controls

! Establish clear signing authority

42

Seeking Tax Deductible Donations

! Common sense goes a long way to heading off trouble in the fundraising area.

! Labeling Issues. Prior to any solicitation, California requires that a donor making a charitable contribution be given printed material containing the following information:

• The name and address of the organization.

• Whether the organization is tax exempt under both federal and state law.

• The percentage of the gift or purchase price that will be used for charitable purposes.

• The amount of the gift or purchase that can be deducted as a charitable contribution.

43

Seeking Tax Deductible Donations (Continued)

! California Business and Professions Code section 17510.25(a)(2) requires that donations solicited in a public venue be preceded by an application with the local authority at least 10 business days beforehand including:

• The date and time of day of the solicitation.

• The location where the solicitation is to occur.

• The manner and conditions under which the solicitation is to occur.

• Proof of a valid liability insurance policy in the amount of at least one million dollars.

44

Seeking Tax Deductible Donations (Continued)

! If an organization receives charitable deduction property and within 3 years disposes of the property, the organization must file IRS Form 8282.

! However, the organization is not required to file if the property (1) is worth less than $500 or (2) is consumed or distributed for charitable purposes.

! Form 8282 must be filed with the IRS within 125 days after the disposition. Additionally, a copy of the form must be given to the donor.

! Auction items are the main source of issues in this area.

45

Seeking Tax Deductible Donations: Raffles For a Prize

! Since 2001, a California nonprofit may legally raffle subject to the administrative requirements outlined by the attorney general. See California Penal Code section 320.5.

! The prize value less the wager (or raffle ticket purchase price) is characterized as UBIT income unless it satisfies an exception, such as when the labor used to conduct the raffle is entirely voluntary, or when the activity is a “public entertainment activity.” See Section 513.

! A prize must be reported using Form W-2G if the prize value less the wager exceeds $600 and the value is more than 300 times the wager. Also, tax must be withheld if the prize value exceeds $5,000.

46

Note on Fiscal Sponsorships

! Sponsor which is already exempt under § 501(c)(3) receives donations on behalf of an individual or group.

! Written agreement highly recommended.

! Usually for start up or short term project.

! Sponsor must retain discretion and control over non-exempt project.

! Flag for follow up!

47

Organization-Specific Issues

! Some organizations may have access to restr icted grants or contracts, e i ther governmental or private.

! Some organizations may need to apply for other licenses for specific activities or be subject to special regulation (i.e. non-profit daycare).

48

Conclusion

! Q&A

! Thank you!

49

Employment Issues for Non-Profit Employers"Sheeva J. Ghassemi-Vanni"March 18, 2016"

Introduction

! Worker Classification

! Employee Handbooks and Policies

! Termination of Employment

51

Worker Classification

! Employee

! Independent contractor/consultant

! Volunteer

! Intern

52

Worker Classification Employee

! Employee

• “Suffer or permit” to work for employer

• Employer exercises control over employee and work performed

• Doing work that is core to the business

53

Worker Classification Employee: Exempt or Non-Exempt

! “Exempt” from what? – Overtime

! Salary Basis Test – Annualized 2x California minimum wage rate (currently $10 = $41,600, except for engineers)

! Duties Test – If not fit exemption (Executive, Professional, Administrative, Outside Sales, Inside Sales, Computer Software), then must be non-exempt

54

Worker Classification Obligations to Non-Exempt Employees

! Minimum Wage • Beware – local ordinances setting rate higher than state or

federal standard: San Francisco ($12.25/increase to $13.00 July 1, 2016); Oakland ($12.55); San Jose ($10.30)

! Overtime Wage (daily or weekly) • More than 8 hours in a day or more than 40 hours in a week

! Meal and Rest Breaks • One unpaid 30 minute meal break

• Two paid 10 minute rest breaks

55

Worker Classification Other Workers

! Independent contractor/consultant – no right of control and not doing work that is core to the business

! Volunteer – person gratuitously performing volunteer service for private nonprofit organization

! Intern – unskilled/junior and performing services, usually through a university, without pay

56

Employee Handbooks and Policies

! Don’t have to have one, but it’s a good idea

! Should be reviewed every few years for compliance

! Key provisions – at-will, equal employment, wage and hour, harassment and complaint procedures, paid time off, leaves, computer/internet usage and social media, right to make changes, and acknowledgment of receipt

57

Termination of Employment

! “At-Will” and Arbitration clauses (check offer letters)

! Termination Documents – providing separation agreements (with or without severance) and ensuring all onboarding documents signed (offer letter, PIIA, handbook acknowledgment, etc.)

! Final Paycheck • Involuntary – immediate

• Resignation – 72 hours

• Accrued, unused vacation or PTO must be included 58

Conclusion

! Q&A

! Thank you!

59

Real Estate (Briefly)"Lynda Twomey"March 18, 2016"

61 61 61

Review of Checklist Categories

IX. Owned or Leased Property If you own or rent real estate, you have certain legal

rights and obligations. These include property taxes, building-code compliance, leasing, insurance, and zoning or other use restrictions. You must understand your legal rights and obligations. Similarly, if you lease significant equipment, such as a copier or telephone system, you must keep abreast of your rights and obligations.

REA

L E

STAT

E

Owned and Leased Property: Why Should A Lawyer Be Involved?

! Lease negotiation and compliance

! Property tax issues

! Building code compliance

! Zoning, licensing restrictions for certain uses

! Insurance

62

REA

L E

STAT

E

Owned and Leased Property

! Owned property (real or personal)

• Ask for proof of title/ownership

• Ask for proof of property tax payments

• Organization may be eligible for real or personal property taxes. Flag for follow up!

! Leased property (real or personal)

• Fully executed lease agreement?

• Subleases?

63

REA

L E

STAT

E

Conclusion

! Q&A

! Thank you!

64

REA

L ES

TATE

Intellectual Property Issues"R.J. Heher"

March 18, 2016"

66 66 66

Review of Checklist Categories

X. Reputation, Branding and Data Collection Your organization's reputation may be its most important asset, so you must protect against confusion between your organization and the activities of others with similar names or missions, or the use of your organization's name by another party. If you publish or distribute materials to the public, you should know the rules of copyright. If you want to have exclusive rights to use your name (or prevent others from using it), you need to know about trademarks. If you collect data online, you need to make those practices clear to your clients.

INTE

LLEC

TUA

L P

RO

PER

TY G

RO

UP

Intellectual Property: Why Should a Lawyer Be Involved?

67

! Most valuable asset for a nonprofit is reputation

! Create exclusivity with respect to name/brand

! Ensure compliance with copyright laws

! Protect proprietary information and technology

! Ensure organization is avoiding infringing on the IP rights of others

INTE

LLEC

TUA

L P

RO

PER

TY G

RO

UP

Types of Intellectual Property

68

! Trademarks – cover words, symbols, colors, and look that serve to identify the source of goods and services.

! Copyrights – cover the expression of ideas, not ideas themselves (software, books, music, artwork).

! Patents – cover an invention (methods, products, designs, etc.).

! Trade Secrets – cover business information that is maintained as confidential.

INTE

LLEC

TUA

L P

RO

PER

TY G

RO

UP

Trademarks

69

! Protection: Lanham Act and State Trademark Laws protect words, names, symbols, or devices used in commerce as an indication of source or affiliation.

! Purpose: Allows the public to distinguish among goods or services of different entities.

! Term: Potentially unlimited, so long as not abandoned.

! Famous Marks: If you can establish a famous mark, then you obtain broader rights of enforcement.

INTE

LLEC

TUA

L P

RO

PER

TY G

RO

UP

Establishing Trademark Rights

70

! Trademark rights in the U.S. arise from:

• Actual use of the mark (common law), or

• Registering a mark with the Patent and Trademark Office (use or intent to use)

! Federal registration is not required to establish rights

! Federal registration provides benefits particularly in enforcement

Copyrights

71

! Protection: Original works of authorship fixed in a tangible medium.

! Purpose: Encourage creation of creative works.

! Term:

• Known author: life of author + 70 years.

• Corporate author/anonymous/pseudonymous: shorter of 95 years from publication or 120 years from creation.

INTE

LLEC

TUA

L P

RO

PER

TY G

RO

UP

Requirements for Copyright Protection

72

! Originality: independently created by author.

! Creativity: modicum of creativity required.

• E.g., a phonebook is not sufficiently creative.

! Expression: protects expression, not the ideas or concepts underlying the expression.

! Fixation: in a medium from which work can be perceived or communicated

• E.g., extemporaneous speech, musical improvisation are not sufficiently fixed.

INTE

LLEC

TUA

L P

RO

PER

TY G

RO

UP

Establishing Copyright Protection

73

! Copyright is secured automatically when the work is created and fixed in a medium for the first time.

! No publication or registration is required

• Registration provides enhanced remedies: statutory damages and attorney fees

! Copyright notice is not required under U.S. law, but notice is useful to inform public that the work is protected

• Notice consists of �Copyright� or �©�, year of first publication, and name of owner

• Example: © 2013 Fenwick & West LLP

INTE

LLEC

TUA

L P

RO

PER

TY G

RO

UP

Patents

74

! Protection: new, useful, and non-obvious inventions.

! Purpose:

• Foster innovation by providing inventors with an incentive to disclose their inventions to the public.

• Inventor gets right to exclude others from making, using, selling, offering to sell, and importing invention in the U.S. for a limited time in exchange for a description of how to make and use the invention.

! Term: 20 years from filing of patent application, provided maintenance fees are paid to keep patent in force.

INTE

LLEC

TUA

L P

RO

PER

TY G

RO

UP

Patenting Process

75

! Obtaining a patent is a rigorous and expensive process, on average requiring 3 years and approximately $20,000-$30,000.

! Weigh the costs versus the benefits

INTE

LLEC

TUA

L P

RO

PER

TY G

RO

UP

Trade Secrets

76

! Protection: Proprietary information that has economic value from not being generally known or readily ascertainable and is the subject of reasonable efforts to keep it secret.

• Examples: certain customer lists, formula for product, software code that is maintained as confidential.

! Purpose: Prevent unfair competition.

! Term: Potentially unlimited, so long as not disclosed.

INTE

LLEC

TUA

L P

RO

PER

TY G

RO

UP

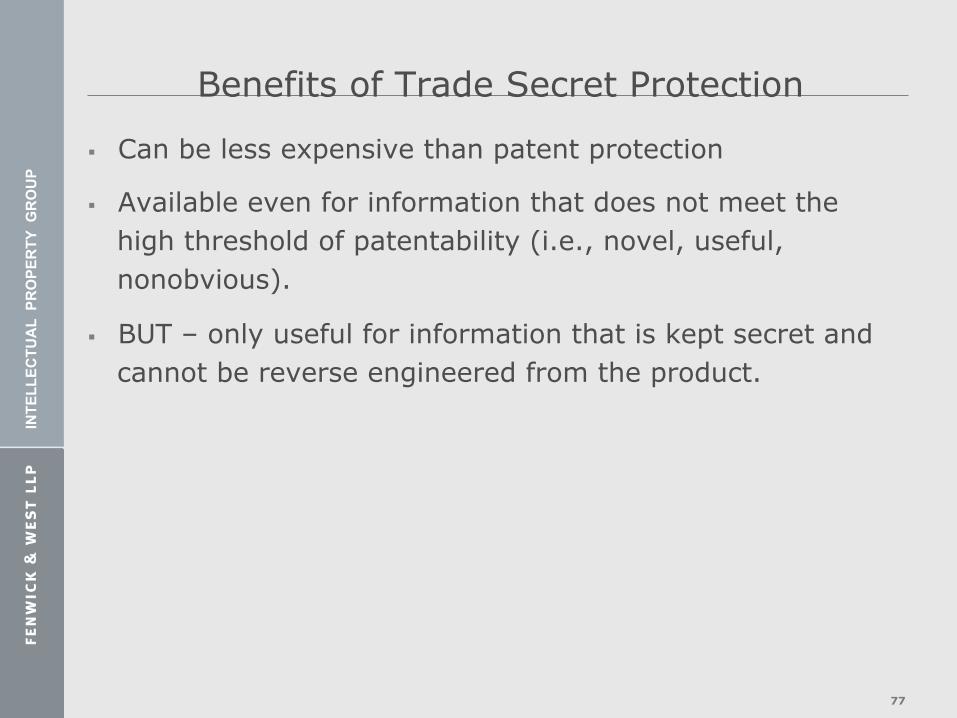

Benefits of Trade Secret Protection

77

! Can be less expensive than patent protection

! Available even for information that does not meet the high threshold of patentability (i.e., novel, useful, nonobvious).

! BUT – only useful for information that is kept secret and cannot be reverse engineered from the product.

INTE

LLEC

TUA

L P

RO

PER

TY G

RO

UP

Data Collection and Privacy

78

! California’s Online Privacy Protection Act of 2003:

• Requires websites operators or online services that collect personally identifiable information from consumers residing in California to:

– Post a privacy policy that sets forth what personally identifiable information is collected, and with whom it is shared.

! Penalties set under Unfair Competition Law (§17200).

! Important to maintain compliance.

INTE

LLEC

TUA

L P

RO

PER

TY G

RO

UP

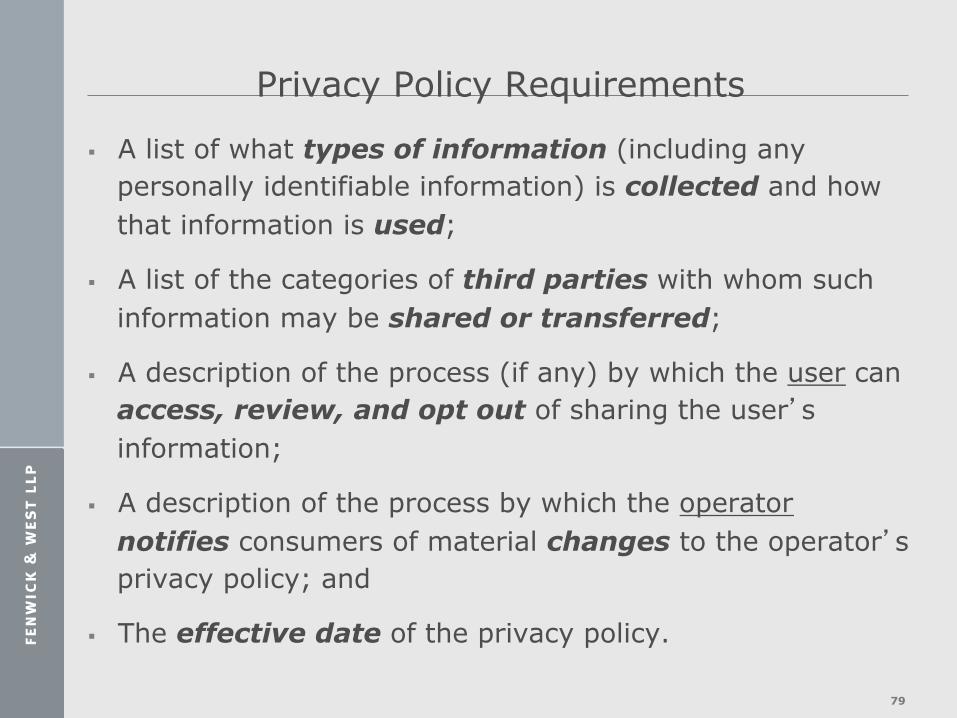

Privacy Policy Requirements

79

! A list of what types of information (including any personally identifiable information) is collected and how that information is used;

! A list of the categories of third parties with whom such information may be shared or transferred;

! A description of the process (if any) by which the user can access, review, and opt out of sharing the user�s information;

! A description of the process by which the operator notifies consumers of material changes to the operator�s privacy policy; and

! The effective date of the privacy policy.

Respecting Intellectual Property of Others

80

! Do not ignore legal threats – Know when to call a subject matter expert.

! Register with the Copyright Office as an Internet provider if online user contributions are anticipated.

! Contests and give-aways require compliance with state law even if a non-profit is involved.

INTE

LLEC

TUA

L P

RO

PER

TY G

RO

UP

Conclusion

! Q&A

! Thank you!

81

INTE

LLEC

TUA

L P

RO

PER

TY G

RO

UP

•j•• •

(:' ... CENTER

OF lHE BAR ASSOCIATION OF SAN FRANCISCO

ACssociation of Corporate Counsel - SAN FRANCISCO BAY AREA -

Ten-Step Legal Checklist for Consultation with Nonprofits

Organization Name: _ _________ _

Organization Representative(s) Participating: _ ___________ _

Address:----------

Phone Number: - -------- E-mail: - -------------

Volunteers Participating:-----------------------

I. Corporate Governance and Reporting Requirements

"Why do./ need a lawyer?"

As a nonprofit entity, you are subject to review by, among others, state regulators and your members, if any. In general, nonprofit organizations must comply with basic state laws concerning governance procedures, records retention, and ongoing reporting requirements. Undet certain circumstances, failure to satisfy these requirements could result in loss of your nonprofit entity status under state law, loss of your federal tax-exempt status, and, in egregious circumstances, the imposition of an excise tax or penalties on the organization or, potentially, personal liability of your directors. Every nonprofit organization needs to understand these requirements and how to satisfy them.

a) Is your organization incorporated as a California nonprofit corporation? If so, may we see copies of your articles of incorporation and bylaws? If not, please provide a copy of your organizational documents (i.e., trust agreement, operating agreement, charter, etc.)

Notes:

1

b) Do you maintain permanent records as required under California law (e.g., copies of . your articles and bylaws, including all amendments, minutes of board meetings, records of actions, resolutions adopted by the board of directors, accounting records, financial statements, a list of members, etc.)?

c) Please describe the operations/functioning of your board of directors (i.e., number of members, how they are selected, length of terms, etc.). Does your bo!ll"d have a compensation committee and/or an audit committee?

d) Do you provide orientation or training to board members, such as with respect to their legal duties?

e) Do you maintain directors' & .. officers' insurance?

f) If you are a California nonprofit corporation, have you filed a Statement of Information (Form Sl-100) with the California Secretary of State (i) within 90 . days after .filing your original articles of incorporation, and (ii) biennially thereafter?

g) Have you completed the initial registration (Form CT-1) with the California Attorney General's Registry of Charitable Trusts? Do you file annual registration renewal fee reports (Form RRF-1)?

h) Does your organization operate outside of .California? If so, has your organization registered to do business under each applicable state's laws? Does your organization file the necessary reports under these laws?

Notes:

2

i) Has your organization registered under each applicable state's charitable solicitation laws? Does your . organization file required reports under these charitable solicitation laws?· For example, California requires the filing of an annual financial solicitation report (Form CT-694).

Notes:

3

IL Obtaining Tax Exemptions and Subsequent Reporting Requirements

"Why do I need a lawyer?"

In addition to with requirements of corporate statutes, California nonprofit corporations that obtain federal and state tax-exempt status are subject to ongoing tax scrutiny and reporting requirements. For example, revisions to your organizational documents may affect your tax-exempt status. The content of annual returns filed with the IRS or state authorities will also be used to determine whether you still qualify for tax-exempt status. Information in those reports is also available for public inspection. You must understand what filing requirements apply under state and federal law and ensure that internal controls are in place to verify that reports are complete, accurate, and filed on a timely basis. Failure to satisfy these requirements could result in the imposition of a penalty (e.g., the penalty for failure to timely file IRS Form 990).

Notes: a) Has your organization obtained federal tax-

. exempt status under l.R.C. § 50l(c)(3)? If SO; please provide a copy of your determination letter from the IRS.

b) Has your organization obtained California tax-exempt status? If so, please provide a copy of your determination letter from the California FTB.

c) Does your organization have any affiliate organizations that control or are controlled by your organization, or share board members or facilities? If so, have these ' organizations obtained and state tax-exempt status?

d) Has your organization made any changes or amendments to your organizational documents or activities? If so, have you notified the IRS?

e) Does your organization have procedures in place to ensure compliance with applicable federal and state tax filing requirements?

f) Does your organization file annual returns with the IRS (e.g., Forms 990, 990-EZ, 990-PF, 990T)? If so, please provide a copy of your latest filing.

g) Do you make your IRS Form 990 returns available for public inspection (by hard copy or posting on the Web)? Do you make your IRS Fonn 1023 available for public

4

Notes: inspection?

b) Does your organization file annual returns with the California FTB (e.g., Fonns 199, 109)? If so, please provide a copy of your latest filing.

' i) Has your organization sought exemption

from sales and use truces? If so, please provide a copy of your exemption letter.

5

ill. Employment & Human Resources

"Why do I need a lawyer?"

If you have employees or independent contractors/consultants, you must comply with payroll and withholding requirements and with a host of federal, state, and local Jaws that regulate employment relationships. You should know your rights and obligations as an employer and move quickly to strengthen any areas where proper compliance is in question.

Notes: a) Do you have employees? If so, how

many?

b) Are your employees salaried exempt or hourly non-exempt?

c) Do you hire independent contractors or consultants? If so, how many are currently providing services to you? How long have they been providing services and in what capacity?

d) Do you have any interns or regular volunteers? If so, how many are currently providing services to you? How long have -they been providing services and in what capacity?

e) Do you have your employees, independent contractors, interns or volunteers sign written agreements? If so, list the types of agreements (e.g., employment contracts, offer letters, confidentiality or non-disclosure agreements, consulting or independent contractor agreements). Have the agreements been reviewed in the past two years for changes in the law? Please provide copies of all fonn agreements.

f) Do you conduct background checks before hiring employees?

g) Do you have a personnel policy or employee handbook? Has it been reviewed within the past two years for changes in the law?

h) Do you comply with federal and state payroll, reporting, and withholding

6

obligations (including IRS Form 941, "Employer's Quarterly Federal Tax Return")? Payments for services performed by an employee of an I.RC. § 501(c)(3) organization may be exempt from FlJTA taxes, but are not exempt from FICA taxes (except for churches and qualified church-controlled organizations).

Notes: ·

7

IV. Intellectual Property and Privacy

"Why do I need a lawyer?"

Your organization's intellectual property may be among its most important assets, so you must protect such intellectual property from Wtauthorized use by others. In addition, your organization can incur significant liability if you use intellectual property of others without authorization, or if you do not follow applicable requirements with respect to the co(lection, storage, and use of personal information. If you want to have exclusive rights to use your name (or prevent others from using it). you need to know about trademarks. If you publish or distribute materials to the public, you should know rules of copyright. If you have proprietary information or new techniques or products, you should understand how to protect them. If you collect data from others, you need to make those practices and policies are clear to the effected. individuals.

a) Do you use any trademarks or logos in connection with your organization and/or its products or services? · Do you have any trademark applications or registrations related to these trademarks? If so, please provide copies. Also, if you have any agreements allowing you to use trademarks from other organizations, please provide copies.

b) Are any trademarks that you use licensed from other organizations or affiliates (or from the national chapter of an organization)? If so, do you have a written agreement authorizing your use of those trademarks?

c) Do you allow any third parties to use your organization's name and/or trademarks (such as through a cause-related marketing campaign by a for-profit)? If so, please describe these arrangements and provide any related written agreements.

d) Does your organization have or intend to have a website · and domain name? If so, please specify the domain name and provide any registration details. Please also describe where the website content comes from (e.g., who created it), including whether your website includes any user-generated content. Finally, please provide copies of any tenns of use, privacy policies, and similar legal terms posted or linked on your website.

Notes:

8

e) Does your organization create any content, documentation, technology (e.g., software), or

·other materials, or have any such materials that are important to your organization created for you by others? What is being done to protect them? Are employees and volunteers subject to confidentiality agreements?

f) Do you receive from third parties or discfose to third parties any information or data you consider confidential or proprietary? If so, please describe these arrangements and provide any related written agreements (e.g., non-disclosure agreements).

g) Do you collect personal information from individuals (your clients and constituents), either electronically or in documents? If so, please describe these practices. For any online data collection, do you have a privacy policy in place? If so, please provide a copy of the policy.

b) Do you permit others to access and use any personal infonnation you collected from individuals? If so, please describe such practices.

Notes:

9

V. Advocacy, Lobbying, and Political Campaign Activities

"Why do I need a lawyer?"

An I.RC. § 50l(c)(3) organization may not engage in any political campaign activities. In addition, an l.R.C. § 501(c)(3) organization generally may not engage in more than an insubstantial amount of legislative lobbying activities. A public charity, however, may elect to apply an expenditure test under l.R.C. § 501(b) to quantify the amount of expenditures the organization may make in connection with legislative lobbying activities. It is important to also note, other tax-exempt organizations, such as I.R.C. § 501 (c)(4) social welfare organizations and I.R.C. § 501(c)(6) business leagues, are not subject to the same limitations on political campaign activities or legislative lobbying.

a) Do you support or oppose legislation, either directly by contacting legislators or indirectly by urging the public to express your view to legislators?

b) If you do support or oppose legislation, please briefly describe your efforts. Do you write letters of support, meet with legislators, or propose measures to legislators? Do you track staff time and expenses for these efforts?

c) Have you made an election under I.R.C. § 501(b) to apply the expenditure test?

d) Have you engaged in· any political campaign activities (defined as an intervention in a political campaign on behalf of or in opposition to any candidate for public office, including publication or distribution of written statements or making oral statements)?

e) If staff members participate in political campaigns, do they do so on their own time, and do they clearly indicate that any endorsement is not meant to represent the organization?

f) Has your organization established a related I.RC. § 50l(c)(4) or 50l(c)(6) organization? If so, do you keep. separate records and bank accounts and properly allocate shared resources (assets, employees, space, etc.) between the orS?:anizations?

Notes:

10

Notes:

g) If your organization engages in any lobbying activity, does your organization comply with other federal and state lobbying laws?

11

VI. Compliance with Restrictions and Program Specific Requirements

"Why do I need a lawyer?"

If you receive restricted funds (e.g., funds earmarked for specific purposes) through a grant or contract, you must comply with the terms of such contract or grant. In general, you will need to track the use of restricted funds and ensure they are not spent on prohibited uses (which may include payment of general and administrative costs). You must also be prepared to demonstrate_ the proper use of the funds. Private foundations are also subject to restrictions regarding the use of :funds (both restricted and unrestricted funds). In addition, specific laws and regulations may govern your activities. For example, certain activities require a license or pennit (e.g., health care, child care, counseling). Alternatively, certain government grants are subject to or contingent on satisfaction of certain criteria. If your activities are regulated by a government agency, or you receive grants subject to government regulation, you need to monitor and confinn compliance.

a) Have you received any restricted funds through grants or contracts? If so, which are from government sources and which are from private sources? Please provide copies of any grant agreements or contracts.

b) How do you account for (i) expenditure of the funds and (ii) fulfillment of the activities and objectives of the grants or contracts?

c) Are you classified as a private foundation under I.R.C. § 501(cX3)? If so, are procedures in place to ensure compliance with the expenditure responsibility rules under J.R.C. § 4942 and the taxable expenditure rules under I.R.C. § 4945? Please explain.

d) Do you employ licensed professionals, such as doctors, lawyers, or clinical social workers?

e) Are there specific licenses, pennits, or inspection requirements that apply to your activities? If so, has your organization applied for them?

f) Is your receipt of funds subject to any special regulation (e.g., compliance with specific federal or state laws)? If so, how does your organization ensure compliance?

Notes:

12

VIl. Fundraising, Earned Revenue, and Unrelated Business Income Tax

"Why do I need a lawyer?''

If you own or operate a business, either within your organization or through a separate entity, or if you charge fees for your services or your products, you must determine whether the rules regarding commercial activities and the unrelated business income tax apply to your organization. Under these rules, an l.R.C. § 50l(c)(3) organization is subject to a tax at the highest corporate income tax rate on income derived from an activity that (a) constitutes a "trade or business,'' (b) is "regularly carried on," and (c) is not substantially related to the organization's tax-exempt purpose. If such unrelated activity is substantial, the activity may jeopardize the organization's tax-exempt status.

a) Please briefly describe your fundraising activities. Do you sell products or charge an admission fee . in connection with any fundraising activities? Do you use a commercial fundraiser? If so, do you have a written contract with the commercial fundraiser?

b) Do you charge a fee for your goods or services? If so, how frequently do you conduct the activities related to these goods or services? How do these activities relate to your tax-exempt purpose?

c) Do you receive any revenue from advertisers on your website, publications, or any other communications? (Note that mere recognition or acknowledgment of a corporate sponsor may not necessarily constitute "advertising.")

d) Do you participate in any joint ventures? If so, please describe the purpose of this joint venture and your activities related to the joint venture. Please provide any related agreements.

e) Do you engage in any charitable gaming activities (e.g., raffles, sweepstakes, 50/50 drawings, games of chance, etc.)? (Consider state and local laws, as well as income tax issues.)

f) Do you receive any income from passive sources (e.g., dividends, interest, annuities, rents, or royalties)? If so, please explain. Is there any outstanding debt related to the

Notes:

13

Notes: assets that produce such passive income?

l

14

VIlI. J.>rivate lnurement, Private Benefit, Excess Benefit, and Self-Dealing Rules

"Why do I need a lawyer?"

An organization does not qualify under l.R.C. § 50l(c)(3) if any part of its "net earnings" inures to the benefit of any private "shareholder or individual" or insider (the "Private Inurement" doctrine). Similarly, an individual (not just insiders) may not receive a benefit from an l.R.C. § 501(cX3) organization not accorded the public as a whole (the "Private Benefit" doctrine). Violation of the Private Inurement or Private Benefit doctrines may result in loss of tax-exempt status. Similarly, an excise tax may be imposed on a public charity and its directors or officers with respect to any "excess benefit transaction» (i.e., a transaction in which an economic benefit is provided by an exempt organization directly or indirectly to or for the use of any disqualified person, and the value of the benefit provided exceeds the value of the consideration (including the perfonnance of services) received for providing the benefit). Alternatively, an excise tax may be imposed on a private foundatiop. with respect to any "self-dealing'' transaction (which may include any transaction between the exempt organization and a disqualified person). A disqualified person generally includes an organization's directors and officers, certain family members of such directors and officers, and certain entities in which such directors and officers (and their family members) own more than a 35% interest. In addition, a disqualified person may include a substantial contributor to the organization.

a) Does your organization have a conflict of interest policy? If so, please provide a copy of the policy. Do your directors and officers periodically review the conflict of interest policy?

b) What procedures do you follow to establish compensation? Do you approve compensation arrangements in advance and record the decision in writing? Does the organization compare compensation paid by similarly-situated organizations?

c) Does your organization have any percentage compensation arrangements (e.g., compensation based on a percentage of income, etc.)? If so, please describe such arrangement. ls there a cap on the amount of compensation?

d) Does your organization engage in any transactions with your officers, directors, thefr family members, or any other disqualified persons? If so, how does your organization ensure that such transactions are at arm's length, reflect fair market value, and are in the best interests of the organization?

Notes:

15

IX. Owned or Leased Property

"Why do I need a lawyer?"

If you own or rent real estate, you have certain legal rights and obligations. These include property taxes, building code leasing, insurance and zoning or other use You need to make sure you understand your legal rights

and obligations. Similarly, if you lease significant equipment, such as a copier or telephone system, you need to keep track of your rights and obligations.

a) . Do you own or lease, as a tenant, any land or buildings? If so, may we see copies of any title documents, leases or subleases?

b) If you own any land or buildings, do you lease any portion of it to another party? If so, may we see copies of any leases?

c) Do you lease any significant equipment items, such as a copier, telephone system, or machinery? If so, may we see copies of any leases?

d) Have you sought or obtained exemption from real or personal property taxes? If so, may we see copies of any property tax exemption letters you may have received granting your organization qualifying status?

e) Do you have any leases with your officers, directors, trustees, employees, or independent contractors? If so, bow does your organization ensure that such leases are negoti!lted at arm's length, reflect fair market value, and are in the best interests of the organization?

Notes:

16

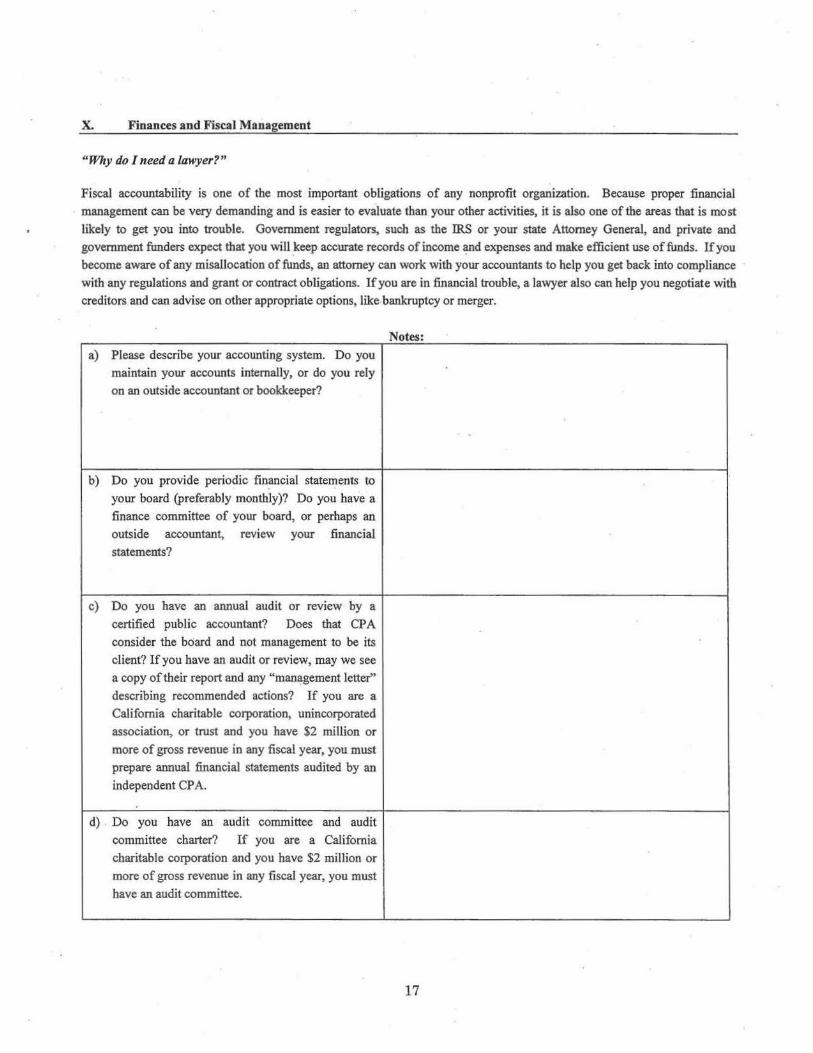

X. Finances and Fiscal Management

"Why do I need a lawyer?"

Fiscal accountability is one of the most important obligations of any nonprofit organization. Because proper financial management can be very demanding and is easier to evaluate than your other activities, it is also one of the areas that is most likely to get you into trouble. Government regulators, such as the IRS or your state Attorney General, and private and government funders expect that you will .keep accurate records of income expenses and make efficient use of funds. If you become aware of any misallocation of funds, an attorney can work with your accountants to help you get back into compliance with any regulations and grant or contract obligations. If you are in financial trouble, a lawyer also can help you negotiate with creditors and can advise on other appropriate options, like-bankruptcy or merger.

a) Please describe your accounting system. Do you maintain your accounts internally, or do you rely on an outside accountant or bookkeeper?

b) Do you provide periodic statements to your board (preferably monthly)? Do you have a finance committee of your board, or perhaps an outside accountant, review your financial statements?

c) Do you have an annual audit or review by a certified public accountant? Does that CPA consider the board and not management to be its client? If you have an audit or review, may we see a copy of their report and any "management letter" describing recommended actions? If you are a California charitable corporation, unincorporated association, or trust and you have $2 million or more of gross revenue in any fiscal year, you must prepare annual financial statements audited by an independent CPA.

d) Do you have an audit committee and audit committee charter? If you are a California charitable corporation and you have $2 million or more of gross revenue in any fiscal year, you must have an audit committee.

Notes:

17

e) Do the same individuals serve on the audit committee and finance committee? California generally requires that these committees be separated and that the audit committee nof perform finance committee functions and vice versa.

f) Please describe any internal financial controls (such as check signature requirements or separating logging receipt of checks from entry of deposits).

g) Do you have a line of credit or any significant loan obligations?

h) Do you make certain that you withhold payroll taxes? Do you make timely payments of your tax withholdings to the government?

i) Do you comply with substantiation requirements? Donors must have written substantiation for contributions of $250 or more, and you must provide a statement to donors who receive goods or services in excbange for contributions in excess of$75.

Notes:

18

CALIFORNIA EXEMPTIONS

Executive Exemption

A person employed in an executive capacity means any employee:

1. Whose duties and responsibilities involve the management of the enterprise in which he or she is

employed or of a customarily recognized department or subdivision thereof; and

2. Who customarily and regularly directs the work of two or more other employees therein; and

3. Who has the authority to hire or fire other employees or whose suggestions and

recommendations as to the hiring or firing and as to the advancement and promotion or any other

change of status of other employees will be given particular weight; and

4. Who customarily and regularly exercises discretion and independent judgment; and

5. Who is primarily engaged in duties, which meet the test of the exemption.

6. An executive employee must also earn a monthly salary equivalent to no less than two times the

state minimum wage for full-time employment. Full-time employment means 40 hours per week

as defined in Labor Code Section 515(c).

With respect to the requirement that management duties must be exercised over the entire

enterprise or a customarily recognized department or subdivision thereof, it is important to note

that the phrase "customarily recognized department or subdivision thereof" has a particular

meaning. The phrase is intended to distinguish between "a mere collection of employees

assigned from time to time to a specific job or series of jobs" and "a unit with permanent status

and function." Thus, in order to meet the criteria of a managerial employee, one must be more

than merely a supervisor of two or more employees. The managerial exempt employee must be

in charge of the unit, not simply participate in the management of the unit.

The IWC Orders require as a basic condition for the executive exemption that the manager must

supervise two or more employees. This may be one full-time and two half-time employees. It has

been the experience of the DLSE that a managerial employee supervising as few as two

employees rarely spends as much as 50% of his or her time primarily engaged in managerial

duties.

Regarding the requirement for the exemption to apply that the employee "customarily and

regularly exercises discretion and independent judgment," this phrase means the comparison and

evaluation of possible courses of conduct and acting or making a decision after the various

possibilities have been considered. The employee must have the authority or power to make an

independent choice, free from immediate direction or supervision and with respect to matters of

significance. With respect to the executive exemption, the most frequent cause of misapplication

of the phrase "discretion and independent judgment" is the failure to distinguish discretion and

independent judgment from the use of independent managerial skills. An employee who merely

applies his or her memory in following prescribed procedures or determining which required

procedure out of the company manual to follow, is not exercising discretion and independent

judgment.

Employee in the Computer Software Field

Except as provided below in paragraph 5, an employee in the computer software field who is

paid on an hourly basis shall be exempt under the professional exemption, if all of the following

apply:

1. The employee is primarily engaged in work that is intellectual or creative and requires the

exercise of discretion and independent judgment.

2. The employee is primarily engaged in duties that consist of one or more of the following:

a. The application of systems analysis techniques and procedures, including consulting with users,

to determine hardware, software, or system functional specifications.

b. The design, development, documentation, analysis, creation, testing, or modification of computer

systems or programs, including prototypes, based on and related to, user or system design

specifications.

c. The documentation, testing, creation, or modification of computer programs related to the design

of software or hardware for computer operating systems.

3. The employee is highly skilled and is proficient in the theoretical and practical application of

highly specialized information to computer systems analysis, programming, and software

engineering. A job title shall not be determinative of the applicability of the exemption.

4. The employee's hourly rate of pay is not less than $41.00 [the rate in effect on September 19,

2000]. The Division of Labor Statistics and Research shall adjust this pay rate on October 1 of

each year to be effective on January 1 of the following year by an amount equal to the percentage

increase in the California Consumer Price Index for Urban Wage Earners and Clerical Workers.

Click here for adjusted rate information (pdf) (doc).

5. The exemption described above does not apply to an employee if any of the following apply:

a. The employee is a trainee or employee in an entry-level position who is learning to become

proficient in the theoretical and practical application of highly specialized information to

computer systems analysis, programming, and software engineering.

b. The employee is in a computer-related occupation but has not attained the level of skill and

expertise necessary to work independently and without close supervision.

c. The employee is engaged in the operation of computers or in the manufacture, repair, or

maintenance of computer hardware and related equipment.

d. The employee is an engineer, drafter, machinist, or other professional whose work is highly

dependent upon or facilitated by the use of computers and computer software programs and who

is skilled in computer-aided design software, including CAD/CAM, but who is not in a computer

systems analysis or programming occupation.

e. The employee is a writer engaged in writing material, including box labels, product descriptions,

documentation, promotional material, setup and installation instructions, and other similar

written information, either for print or for onscreen media or who writes or provides content

material intended to be read by customers, subscribers, or visitors to computer-related media

such as the World Wide Web or CD-ROMS.

f. The employee is engaged in any of the activities set forth in nos. 1 through 4 above for the

purpose of creating imagery for effect used in the motion picture, television, or theatrical

industry.

Administrative Exemption

A person employed in an administrative capacity means any employee:

1. Whose duties and responsibilities involve either:

a. The performance of office or non-manual work directly related to management policies or

general business operations of his or her employer or his or her employer's customers, or

b. The performance of functions in the administration of a school system, or educational

establishment or institution, or of a department or subdivision thereof, in work directly related to

the academic instruction or training carried on therein; and

1. Who customarily and regularly exercised discretion and independent judgment; and

2. Who regularly and directly assists a proprietor, or an employee employed in a bona fide

executive or administrative capacity, or

3. Who performs, under only general supervision, work along specialized or technical lines

requiring special training, experience, or knowledge, or

4. Who executes, under only general supervision, special assignments and tasks, and

5. Who is primarily engaged in duties which meet the test for the exemption.

6. An administrative employee must also earn a monthly salary equivalent to no less than two times

the state minimum wage for full-time employment. Full-time employment means 40 hours per

week as defined in Labor Code Section 515(c).

Following are examples of employees who might qualify for the exemption if, and only if, they

meet the criteria set forth above:

1. Employees who regularly and directly assist a proprietor or exempt executive or administrator.

Included in this category are those executive assistants and administrative assistants to whom

executives or high-level administrators have delegated part of their discretionary powers.

Generally, such assistants are found in large establishments where the official assisted has duties

of such scope and which require so much attention that the work of personal scrutiny,

correspondence and interviews must be delegated.

2. Employees who perform, only under general supervision, work along specialized or technical

lines requiring special training, experience or knowledge. Such employees are often described as

"staff employees," or functional, rather than department heads. They include employees who act

as advisory specialists to management, or to the employer's customers. Typical examples are tax

experts, insurance experts, sales research experts, wage rate analysts, foreign exchange

consultants, and statisticians. Such experts may or may not be exempt, depending on the extent

to which they exercise discretionary powers. Also included in this category would be persons in

charge of a functional department, which may even be a one-person department, such as credit

managers, purchasing agents, buyers, personnel directors, safety directors, and labor relations

directors.

3. Employees who perform special assignments under only general supervision. Often, such

employees perform their work away from the employer's place of business. Typical titles of such

persons are buyers, field representatives, and location managers for motion picture companies.

This category also includes employees whose special assignments are performed entirely or

mostly on the employer's premises, such as customers' brokers in stock exchange firms and so-

called "account executives" in advertising firms.

Regarding the requirement for the exemption to apply that the employee "customarily and

regularly exercises discretion and independent judgment," this phrase means the comparison and

evaluation of possible courses of conduct and acting or making a decision after the various

possibilities have been considered. The employee must have the authority or power to make an

independent choice, free from immediate direction or supervision and with respect to matters of

significance. With respect to the administrative exemption, this phrase has been most frequently

misunderstood and misapplied by employers and employees alike in cases involving the

following:

1. Confusion between the exercise of discretion and independent judgment, and the use of skill in

applying techniques, procedures, or specific standards.

2. Misapplication of the phrase to employees making decisions relating to matters of little

consequence.

3. Perhaps the most common misapplication is the application of the exemption to employees

engaged in production aspects of the employer's business as opposed to administrative functions.

Caveat. As with any of the exemptions, job titles reflecting administrative classifications alone

may not reflect actual job duties and therefore, are of no assistance in determining exempt or

nonexempt status. The fact that an employee may have one of the job titles listed above is, in and

of itself, of no consequence. The actual determination of exempt or nonexempt status must be

based on the nature of the actual work performed by the individual employee.

Professional Exemption

A person employed in a professional capacity means any employee who meets all of the

following requirements:

1. Who is licensed or certified by the State of California and is primarily engaged in the practice of

one of the following recognized professions: law, medicine, dentistry, optometry, architecture,

engineering, teaching, or accounting, or

2. Who is primarily engaged in an occupation commonly recognized as a learned or artistic

profession. "Learned or artistic profession" means an employee who is primarily engaged in the

performance of:

3.

a. Work requiring knowledge of an advance type in a field or science or learning customarily

acquired by a prolonged course of specialized intellectual instruction and study, as distinguished

from a general academic education and from an apprenticeship, and from training in the

performance of routine mental, manual, or physical processes, or work that is an essential part of

or necessarily incident to any of the above work; or

b. Work that is original and creative in character in a recognized field of artistic endeavor (as

opposed to work which can be produced by a person endowed with general manual or

intellectual ability and training), and the result of which depends primarily on the invention,

imagination, or talent of the employee or work that is an essential part of or necessarily incident

to any of the above work; and

c. Whose work is predominantly intellectual and varied in character (as opposed to routine mental,

manual, mechanical, or physical work) and is of such character that the output produced or the

result accomplished cannot be standardized in relation to a given period of time.

4. Who customarily and regularly exercised discretion an independent judgment in the performance

of duties set forth above.

5. Who earns a monthly salary equivalent to no less than two times the state minimum wage for

full-time employment. Full-time employment means 40 hours per week as defined in Labor Code

Section 515(c).

Regarding the requirement for the exemption to apply that the employee "customarily and

regularly exercises discretion and independent judgment," this phrase means the comparison and

evaluation of possible courses of conduct and acting or making a decision after the various

possibilities have been considered. The employee must have the authority or power to make an

independent choice, free from immediate direction or supervision and with respect to matters of

significance.

For the learned professions, an advanced academic degree (above the bachelor level) is a

standard prerequisite.

For the artistic professions, work in a "recognized field of artistic endeavor" includes such fields

as music, writing, the theater, and the plastic and graphic arts.

Outside Salesperson

Any person, 18 years of age or older, who customarily and regularly works more than half the

working time away from the employer's place of business selling tangible or intangible items or

obtaining orders or contracts for products, services, or use of facilities.

Inside Salesperson

Employees (except minors) whose earnings exceed one and one-half times the minimum wage

and more than half their compensation represents commissions.

EMPLOYMENT DETERMINATION GUIDE