Download - ACPI Monthly Viewpoint: March 2017

MONTHLY VIEWPOINT

From the Chief Investment Officer Marco E Pabst

07th

March 2017

ACPI Investments Ltd.

Pegasus House | 37-43 Sackville Street | London W1S 3EH

T +44 (0)20 3697 9580 | F +44 (0)20 3697 9501 | E [email protected]

www.acpi.com

1

Buy everything

“Lenin wanted to destroy the state and that’s my goal too. I want to bring everything crashing down and

destroy all of today’s establishment.” Steve Bannon in 2013

Summary

Controversial and unfounded Trump statements are beginning to threaten his more credible agenda

With markets buying the rumours, they are almost priced to perfection while monetary tightening risks are rising

This is currently balanced by what looks like a new investment cycle across many large economies

Gold is attractive at current levels despite declining physical demand

Investment demand for precious metals is rising and supply will structurally fall over the next three years

It is difficult these days to keep any market commentary a

Trump-free zone. But as equity investors seem to be on bull

market auto pilot it is important not to lose sight of the

robustness of the assumptions they are making, knowingly or

implicitly, and the idiosyncratic risks that come with the

Trump persona.

The risk here is that very positive policy goals such as

smaller government, tax cuts and de-regulation get de-railed

by incompetent statements, ill-chosen personnel and

pointless side shows such as the endless battle with the

press, Hillary Clinton’s campaign or Ivanka’s business

issues.

These serve no real purpose other than making a point but

are responsible for Trump’s quickly declining approval ratings, also amongst his supporters. His statements, for instance,

during Netanyahu’s visit unfortunately only revealed the lack of any coherent idea with regards to the Israeli-Palaestinian

conflict (“I’m looking at a two-state and one-state, and I like the one that both parties like. I’m very happy with the one that

both parties like.”). Sometimes it is just better not to say anything.

Exhibit 1: Performance of different asset classes in 2016

Source(s): ACPI, Bloomberg

-10%

-5%

0%

5%

10%

15%

MS

CI W

orl

d

S&

P 5

00

Eu

rop

e (

Sto

xx 6

00

)

Eu

rozo

ne

(S

tox

x 5

0)

UK

(F

TS

E1

00

)

Ja

pa

n (

Nik

ke

i)

MS

CI E

me

rgin

g M

ark

ets

Bra

sil

Ru

ss

ia

Ind

ia

Ch

ina (

Sh

an

gh

ai)

Ho

ng

Ko

ng

Wo

rld

Fix

ed

In

co

me

Wo

rld

Go

ve

rnm

en

t B

on

ds

US

Tre

as

uri

es

Eu

rozo

ne

go

vt

bo

nd

s

Lo

an

s, to

tal

retu

rn

US

Hig

h y

ield

Glo

ba

l H

igh

yie

ld

EM

ha

rd c

urr

en

cy

de

bt

Eu

rozo

ne

co

rp b

on

ds

Do

lla

r in

de

x

Eu

ro

Po

un

d S

terl

ing

Ja

pa

ne

se

Yen

Ch

ines

e R

MB

Ind

ian

Ru

pe

e

Glo

ba

l c

om

mo

dit

ies

En

erg

y

Pre

cio

us

me

tals

Ag

ric

ult

ura

l c

om

mo

ds

Eq

uit

y R

EIT

S

New

Yo

rk h

om

es

Lo

nd

on

ho

me

s

Ge

rma

n h

om

es

Beij

ing

ho

me

s

Glo

ba

l h

ed

ge

fu

nd

s

MONTHLY VIEWPOINT

From the Chief Investment Officer Marco E Pabst

07th

March 2017

ACPI Investments Ltd.

Pegasus House | 37-43 Sackville Street | London W1S 3EH

T +44 (0)20 3697 9580 | F +44 (0)20 3697 9501 | E [email protected]

www.acpi.com

2

The result of this approach is an aggressive backlash from mainstream media outlets and an increasing alienation of people

who would otherwise agree with most of Trump’s proposals. Appointing people such as Steve Bannon to key roles in

government and letting him drive the more controversial initiatives is something that risks discrediting all other more agreeable

projects.

Exhibit 2: Trump’s approval ratings (lhs) and compared to other Presidents (rhs) at the Mid-February point

Source(s): Gallup

The reason this is important for investors is that markets are almost priced to perfection, implicitly assuming a fairly swift

implementation of the tax reform proposals into law. We should also not forget that even in the best case scenario, none of

these laws will be approved before the end of the year. Trump’s recent change of tack in moving Obamacare reform before

tax reform makes things even more difficult to assess. In addition, should Trump manage further to erode his Republican

support base or even become untenable then we should expect some rather severe disruptions and delays. This could quickly

send markets into a tailspin.

For now, investors are focussing on the positive and this is the prospect of meaningful tax cuts for corporates and individuals

that would imply potentially very large increases in net earnings, especially for more domestically-focused companies in the

US. The crux of the matter is in the border-adjustment tax (BAT) and the fact that tax reform would have to be roughly

revenue neutral.

Exhibit 3: Regulatory roadmap for the US financial sector

Source(s): Morgan Stanley

MONTHLY VIEWPOINT

From the Chief Investment Officer Marco E Pabst

07th

March 2017

ACPI Investments Ltd.

Pegasus House | 37-43 Sackville Street | London W1S 3EH

T +44 (0)20 3697 9580 | F +44 (0)20 3697 9501 | E [email protected]

www.acpi.com

3

As discussed in the annual outlook, the impact on earnings from tax cuts and deregulation could potentially be very

substantial, even if the full impact might not be felt before 2018. Furthermore, there is hope that deregulation in the banking

sector will ease the flow of credit and improve profitability of the industry. It is too early to review this topic as it is not clear at

all how the proposed initiatives will affect the sector, although some assumptions can be made about the range of outcomes.

Exhibit 4: Impact of various measures on earnings per share (EPS) for US financials

Source(s): Morgan Stanley

One can easily see from the chart above, that EPS (earnings per share) upside is quite substantial with possible increases of

between 10% and 30%, which explains why the sector shows such relative strength at the moment even after the gains of last

year. More interestingly, the best performing sector so far this year are NASDAQ stocks, i.e. technology and growth

businesses. This is somewhat counter-intuitive considering Trump’s difficult relationship with the sector and his focus on

domestic and old economy businesses. Even more ironic in this context is that energy stocks are amongst the weakest

relative performers.

Exhibit 5: Relative performance of various sectors versus S&P500 year-to-date (normalised)

Source(s): ACPI, Bloomberg

MONTHLY VIEWPOINT

From the Chief Investment Officer Marco E Pabst

07th

March 2017

ACPI Investments Ltd.

Pegasus House | 37-43 Sackville Street | London W1S 3EH

T +44 (0)20 3697 9580 | F +44 (0)20 3697 9501 | E [email protected]

www.acpi.com

4

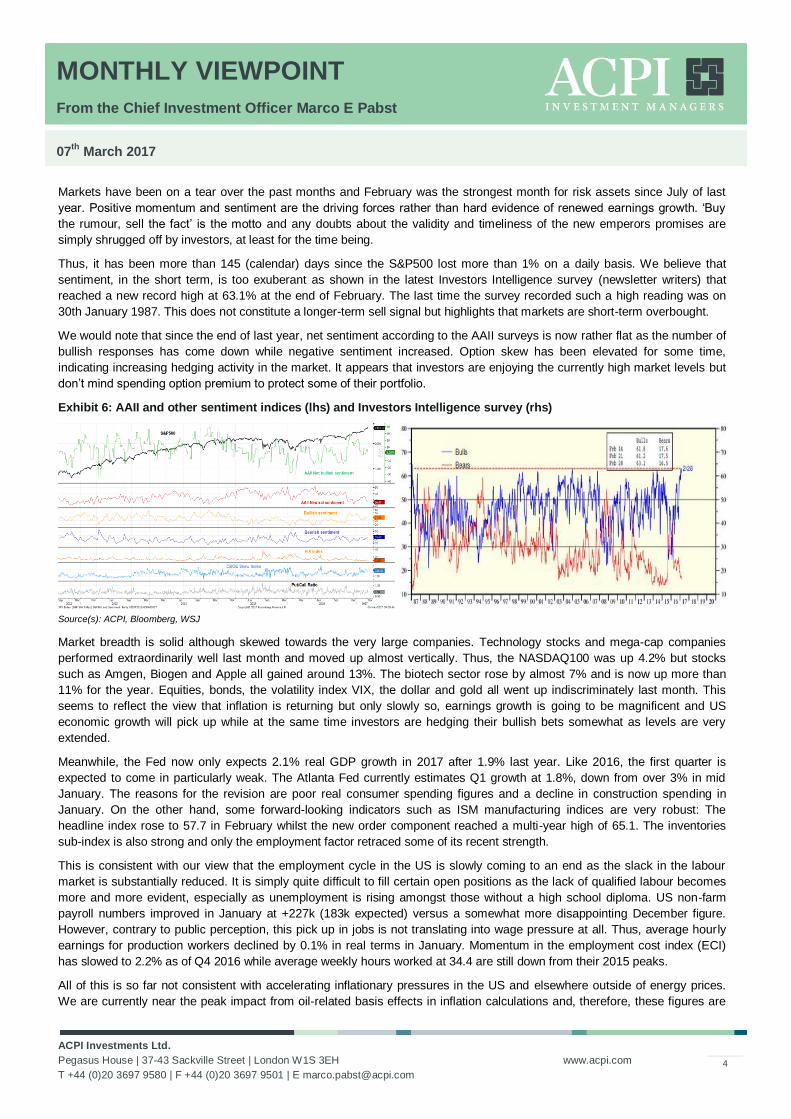

Markets have been on a tear over the past months and February was the strongest month for risk assets since July of last

year. Positive momentum and sentiment are the driving forces rather than hard evidence of renewed earnings growth. ‘Buy

the rumour, sell the fact’ is the motto and any doubts about the validity and timeliness of the new emperors promises are

simply shrugged off by investors, at least for the time being.

Thus, it has been more than 145 (calendar) days since the S&P500 lost more than 1% on a daily basis. We believe that

sentiment, in the short term, is too exuberant as shown in the latest Investors Intelligence survey (newsletter writers) that

reached a new record high at 63.1% at the end of February. The last time the survey recorded such a high reading was on

30th January 1987. This does not constitute a longer-term sell signal but highlights that markets are short-term overbought.

We would note that since the end of last year, net sentiment according to the AAII surveys is now rather flat as the number of

bullish responses has come down while negative sentiment increased. Option skew has been elevated for some time,

indicating increasing hedging activity in the market. It appears that investors are enjoying the currently high market levels but

don’t mind spending option premium to protect some of their portfolio.

Exhibit 6: AAII and other sentiment indices (lhs) and Investors Intelligence survey (rhs)

Source(s): ACPI, Bloomberg, WSJ

Market breadth is solid although skewed towards the very large companies. Technology stocks and mega-cap companies

performed extraordinarily well last month and moved up almost vertically. Thus, the NASDAQ100 was up 4.2% but stocks

such as Amgen, Biogen and Apple all gained around 13%. The biotech sector rose by almost 7% and is now up more than

11% for the year. Equities, bonds, the volatility index VIX, the dollar and gold all went up indiscriminately last month. This

seems to reflect the view that inflation is returning but only slowly so, earnings growth is going to be magnificent and US

economic growth will pick up while at the same time investors are hedging their bullish bets somewhat as levels are very

extended.

Meanwhile, the Fed now only expects 2.1% real GDP growth in 2017 after 1.9% last year. Like 2016, the first quarter is

expected to come in particularly weak. The Atlanta Fed currently estimates Q1 growth at 1.8%, down from over 3% in mid

January. The reasons for the revision are poor real consumer spending figures and a decline in construction spending in

January. On the other hand, some forward-looking indicators such as ISM manufacturing indices are very robust: The

headline index rose to 57.7 in February whilst the new order component reached a multi-year high of 65.1. The inventories

sub-index is also strong and only the employment factor retraced some of its recent strength.

This is consistent with our view that the employment cycle in the US is slowly coming to an end as the slack in the labour

market is substantially reduced. It is simply quite difficult to fill certain open positions as the lack of qualified labour becomes

more and more evident, especially as unemployment is rising amongst those without a high school diploma. US non-farm

payroll numbers improved in January at +227k (183k expected) versus a somewhat more disappointing December figure.

However, contrary to public perception, this pick up in jobs is not translating into wage pressure at all. Thus, average hourly

earnings for production workers declined by 0.1% in real terms in January. Momentum in the employment cost index (ECI)

has slowed to 2.2% as of Q4 2016 while average weekly hours worked at 34.4 are still down from their 2015 peaks.

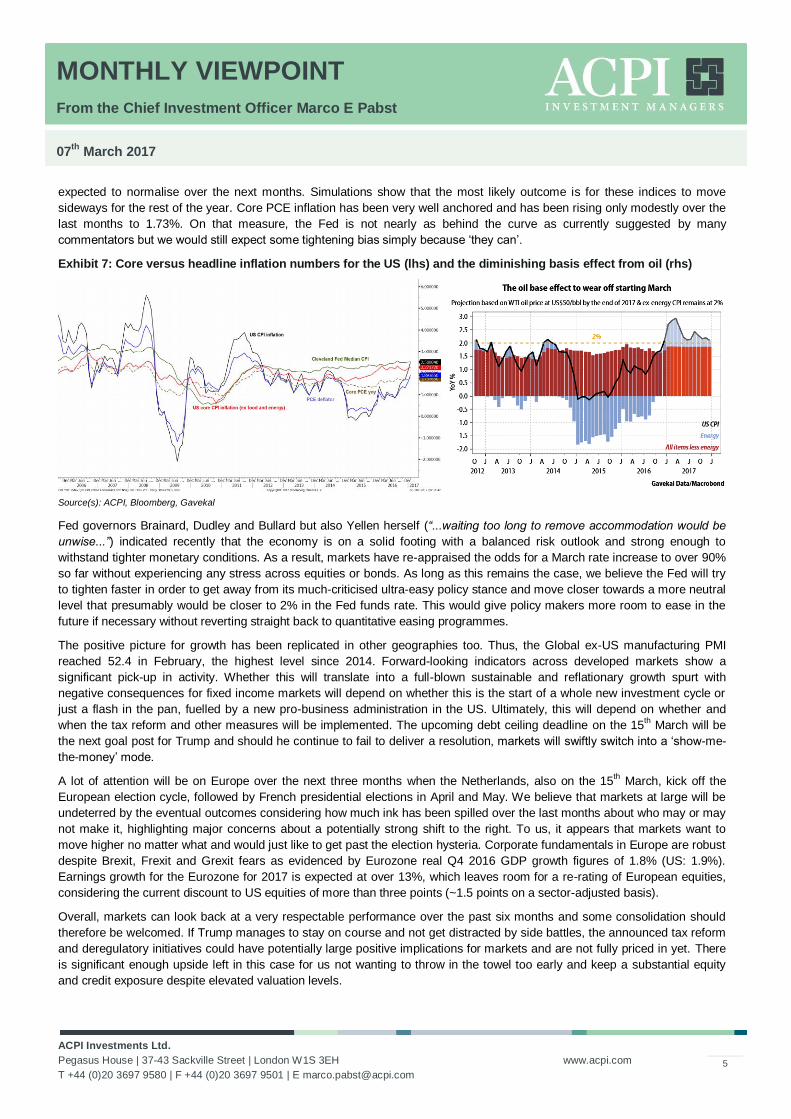

All of this is so far not consistent with accelerating inflationary pressures in the US and elsewhere outside of energy prices.

We are currently near the peak impact from oil-related basis effects in inflation calculations and, therefore, these figures are

MONTHLY VIEWPOINT

From the Chief Investment Officer Marco E Pabst

07th

March 2017

ACPI Investments Ltd.

Pegasus House | 37-43 Sackville Street | London W1S 3EH

T +44 (0)20 3697 9580 | F +44 (0)20 3697 9501 | E [email protected]

www.acpi.com

5

expected to normalise over the next months. Simulations show that the most likely outcome is for these indices to move

sideways for the rest of the year. Core PCE inflation has been very well anchored and has been rising only modestly over the

last months to 1.73%. On that measure, the Fed is not nearly as behind the curve as currently suggested by many

commentators but we would still expect some tightening bias simply because ‘they can’.

Exhibit 7: Core versus headline inflation numbers for the US (lhs) and the diminishing basis effect from oil (rhs)

Source(s): ACPI, Bloomberg, Gavekal

Fed governors Brainard, Dudley and Bullard but also Yellen herself (“...waiting too long to remove accommodation would be

unwise...”) indicated recently that the economy is on a solid footing with a balanced risk outlook and strong enough to

withstand tighter monetary conditions. As a result, markets have re-appraised the odds for a March rate increase to over 90%

so far without experiencing any stress across equities or bonds. As long as this remains the case, we believe the Fed will try

to tighten faster in order to get away from its much-criticised ultra-easy policy stance and move closer towards a more neutral

level that presumably would be closer to 2% in the Fed funds rate. This would give policy makers more room to ease in the

future if necessary without reverting straight back to quantitative easing programmes.

The positive picture for growth has been replicated in other geographies too. Thus, the Global ex-US manufacturing PMI

reached 52.4 in February, the highest level since 2014. Forward-looking indicators across developed markets show a

significant pick-up in activity. Whether this will translate into a full-blown sustainable and reflationary growth spurt with

negative consequences for fixed income markets will depend on whether this is the start of a whole new investment cycle or

just a flash in the pan, fuelled by a new pro-business administration in the US. Ultimately, this will depend on whether and

when the tax reform and other measures will be implemented. The upcoming debt ceiling deadline on the 15th March will be

the next goal post for Trump and should he continue to fail to deliver a resolution, markets will swiftly switch into a ‘show-me-

the-money’ mode.

A lot of attention will be on Europe over the next three months when the Netherlands, also on the 15th March, kick off the

European election cycle, followed by French presidential elections in April and May. We believe that markets at large will be

undeterred by the eventual outcomes considering how much ink has been spilled over the last months about who may or may

not make it, highlighting major concerns about a potentially strong shift to the right. To us, it appears that markets want to

move higher no matter what and would just like to get past the election hysteria. Corporate fundamentals in Europe are robust

despite Brexit, Frexit and Grexit fears as evidenced by Eurozone real Q4 2016 GDP growth figures of 1.8% (US: 1.9%).

Earnings growth for the Eurozone for 2017 is expected at over 13%, which leaves room for a re-rating of European equities,

considering the current discount to US equities of more than three points (~1.5 points on a sector-adjusted basis).

Overall, markets can look back at a very respectable performance over the past six months and some consolidation should

therefore be welcomed. If Trump manages to stay on course and not get distracted by side battles, the announced tax reform

and deregulatory initiatives could have potentially large positive implications for markets and are not fully priced in yet. There

is significant enough upside left in this case for us not wanting to throw in the towel too early and keep a substantial equity

and credit exposure despite elevated valuation levels.

MONTHLY VIEWPOINT

From the Chief Investment Officer Marco E Pabst

07th

March 2017

ACPI Investments Ltd.

Pegasus House | 37-43 Sackville Street | London W1S 3EH

T +44 (0)20 3697 9580 | F +44 (0)20 3697 9501 | E [email protected]

www.acpi.com

6

I have not reflected on gold for quite some time and the recent rise in inflationary pressures and the relatively tumultuous start

of Trump’s term might be a good opportunity to catch up on the topic.

We added some gold exposure back in 2016 on our view that inflation is likely on the rise relative to policy rates, in other

words, real short-term interest rates are not expected to rise and if so, not by much. Real interest rates tend to be gold’s major

adversary and as long as they are in check, precious metals tend to do well. It is therefore no surprise that in an environment

of falling interest rates and an inflating money supply, precious metals perform well as a store of value, which explains the

sector’s performance since 2000 where gold compounded at more than 10% annually.

Exhibit 8: Gold and silver prices since 1992 and non-commercial positioning at futures exchange Comex

Source(s): ACPI, Bloomberg

In contrast to previous decades, however, gold and silver are no longer the hedges of choice against geopolitical turmoil. US

Treasuries and the dollar are more suitable and liquid to accommodate such hedging needs in today’s markets. Nonetheless,

there are several reasons why we re-established some gold exposure last year.

After ten years of a fairly spectacular bull market, precious metals prices began to consolidate in 2011 and 2012. Five years

ago, ‘gold bugs’ were everywhere and industry conferences were standing room only. Central banks had a target on their

backs as arch enemies, whereby, according to gold supporters, endless money printing would make fiat money worthless

and, thus, gold would offer the only safe haven option for investors. Clearly, this was at the peak in prices and precious metals

faded somewhat into the background.

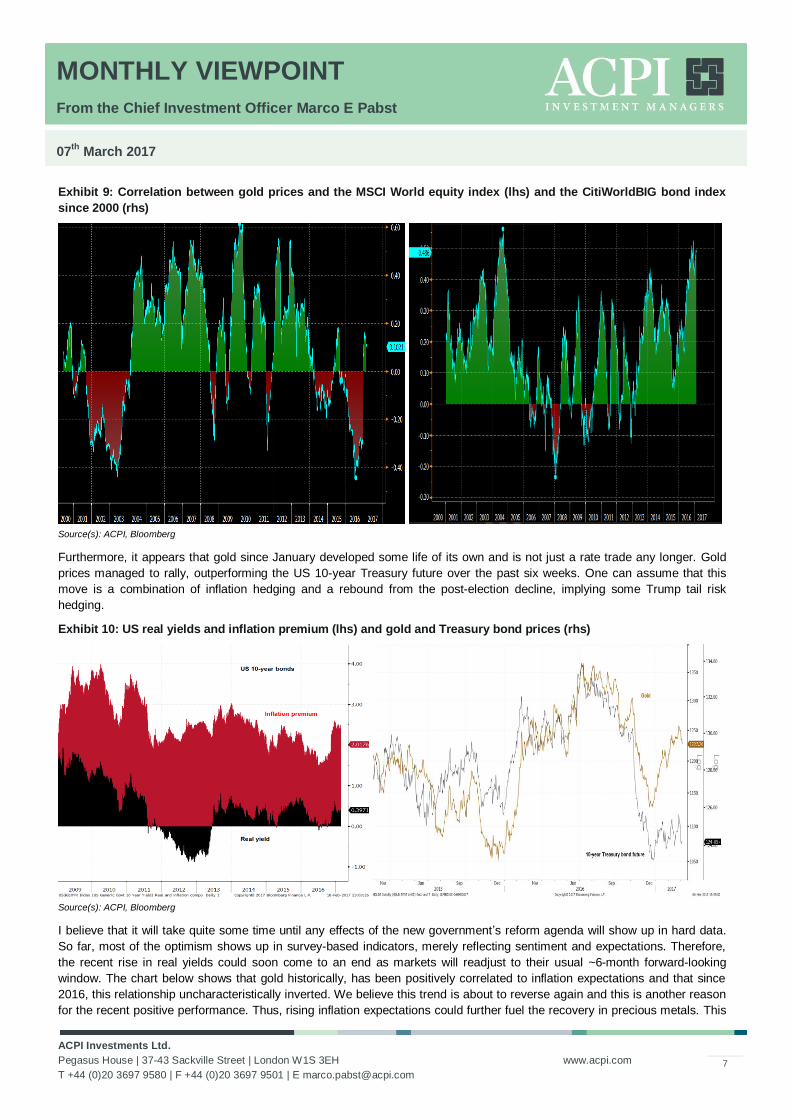

However, after a 50% correction over the past five years, we believe that the time is about right for long-term investors to

reconsider the sector. After all, precious metals also serve as an important diversifier of risk as can be seen in the low

correlations between gold and the MSCI World index where correlations are currently at only around 10%. With regard to

bonds, precious metals tend to be positively correlated most of the time and also more highly so. Currently, this measure is

close to 50% which speaks for the typical risk-off character of precious metals and bonds.

MONTHLY VIEWPOINT

From the Chief Investment Officer Marco E Pabst

07th

March 2017

ACPI Investments Ltd.

Pegasus House | 37-43 Sackville Street | London W1S 3EH

T +44 (0)20 3697 9580 | F +44 (0)20 3697 9501 | E [email protected]

www.acpi.com

7

Exhibit 9: Correlation between gold prices and the MSCI World equity index (lhs) and the CitiWorldBIG bond index

since 2000 (rhs)

Source(s): ACPI, Bloomberg

Furthermore, it appears that gold since January developed some life of its own and is not just a rate trade any longer. Gold

prices managed to rally, outperforming the US 10-year Treasury future over the past six weeks. One can assume that this

move is a combination of inflation hedging and a rebound from the post-election decline, implying some Trump tail risk

hedging.

Exhibit 10: US real yields and inflation premium (lhs) and gold and Treasury bond prices (rhs)

Source(s): ACPI, Bloomberg

I believe that it will take quite some time until any effects of the new government’s reform agenda will show up in hard data.

So far, most of the optimism shows up in survey-based indicators, merely reflecting sentiment and expectations. Therefore,

the recent rise in real yields could soon come to an end as markets will readjust to their usual ~6-month forward-looking

window. The chart below shows that gold historically, has been positively correlated to inflation expectations and that since

2016, this relationship uncharacteristically inverted. We believe this trend is about to reverse again and this is another reason

for the recent positive performance. Thus, rising inflation expectations could further fuel the recovery in precious metals. This

MONTHLY VIEWPOINT

From the Chief Investment Officer Marco E Pabst

07th

March 2017

ACPI Investments Ltd.

Pegasus House | 37-43 Sackville Street | London W1S 3EH

T +44 (0)20 3697 9580 | F +44 (0)20 3697 9501 | E [email protected]

www.acpi.com

8

would be positive for gold which is already one of the best performing assets so far this year, up more than 6% since the end

of a strong 2016.

Exhibit 11: Gold prices (white) and US 5-year inflation expectations (orange) (top panel) and their correlation (bottom)

Source(s): ACPI, Bloomberg

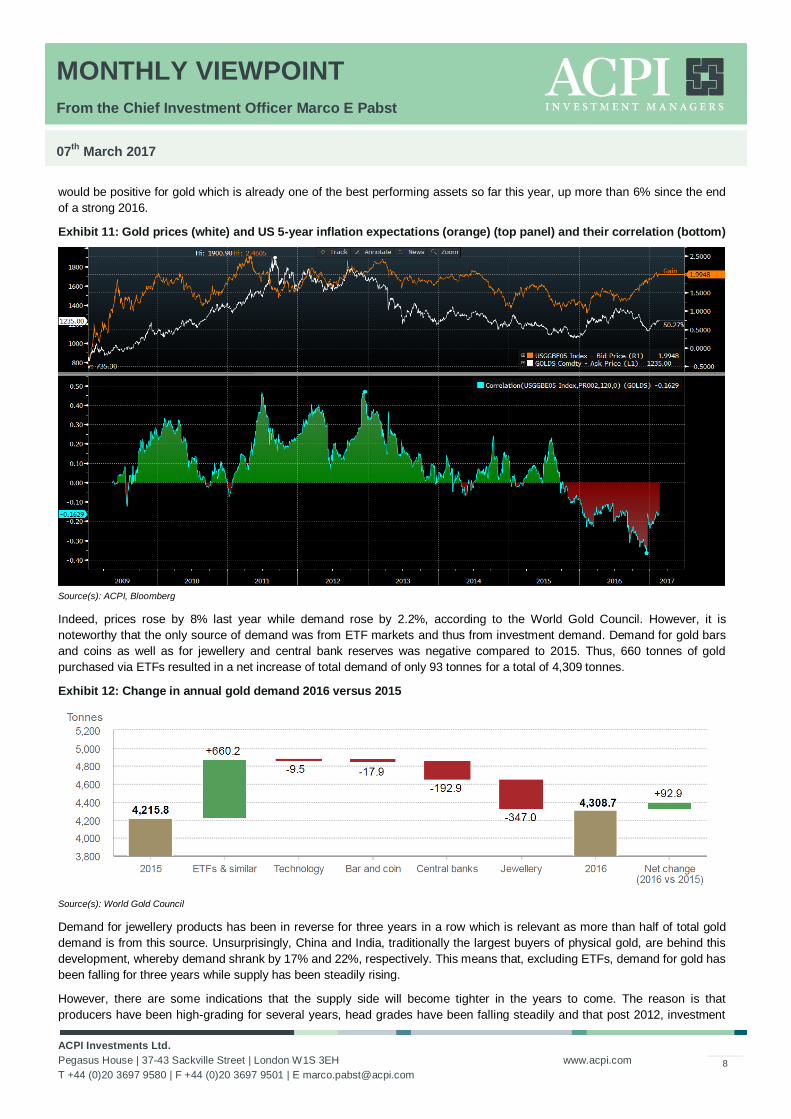

Indeed, prices rose by 8% last year while demand rose by 2.2%, according to the World Gold Council. However, it is

noteworthy that the only source of demand was from ETF markets and thus from investment demand. Demand for gold bars

and coins as well as for jewellery and central bank reserves was negative compared to 2015. Thus, 660 tonnes of gold

purchased via ETFs resulted in a net increase of total demand of only 93 tonnes for a total of 4,309 tonnes.

Exhibit 12: Change in annual gold demand 2016 versus 2015

Source(s): World Gold Council

Demand for jewellery products has been in reverse for three years in a row which is relevant as more than half of total gold

demand is from this source. Unsurprisingly, China and India, traditionally the largest buyers of physical gold, are behind this

development, whereby demand shrank by 17% and 22%, respectively. This means that, excluding ETFs, demand for gold has

been falling for three years while supply has been steadily rising.

However, there are some indications that the supply side will become tighter in the years to come. The reason is that

producers have been high-grading for several years, head grades have been falling steadily and that post 2012, investment

MONTHLY VIEWPOINT

From the Chief Investment Officer Marco E Pabst

07th

March 2017

ACPI Investments Ltd.

Pegasus House | 37-43 Sackville Street | London W1S 3EH

T +44 (0)20 3697 9580 | F +44 (0)20 3697 9501 | E [email protected]

www.acpi.com

9

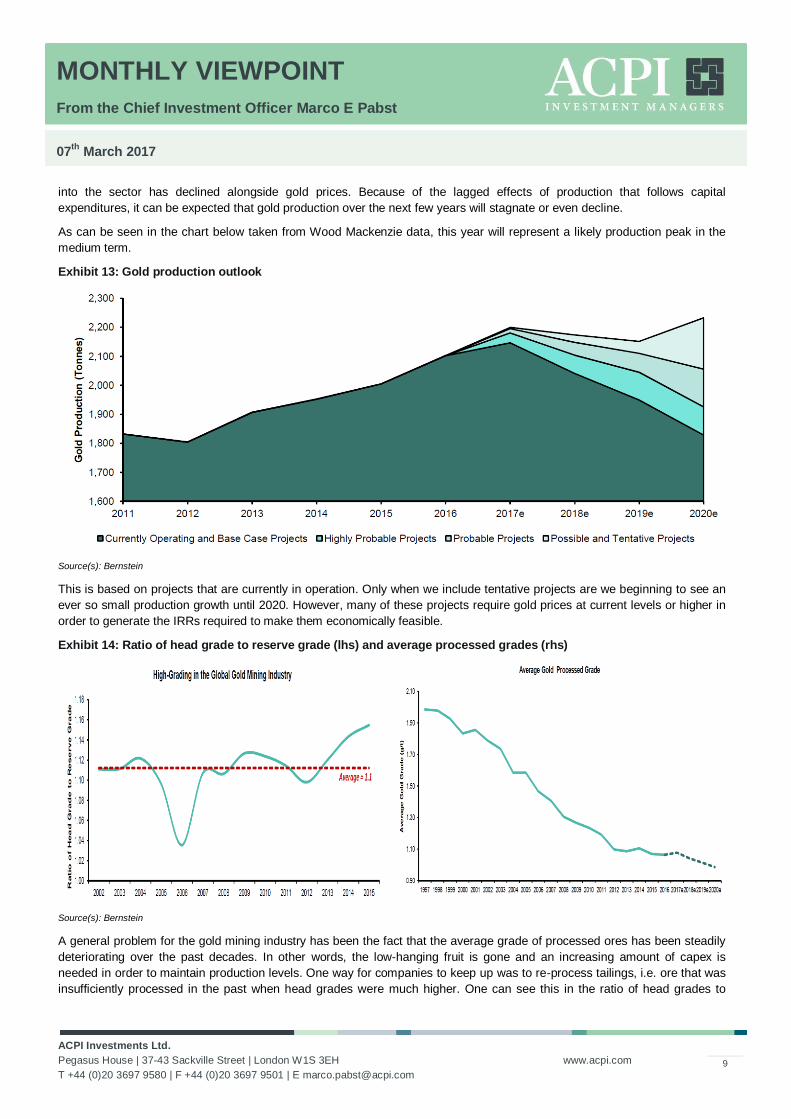

into the sector has declined alongside gold prices. Because of the lagged effects of production that follows capital

expenditures, it can be expected that gold production over the next few years will stagnate or even decline.

As can be seen in the chart below taken from Wood Mackenzie data, this year will represent a likely production peak in the

medium term.

Exhibit 13: Gold production outlook

Source(s): Bernstein

This is based on projects that are currently in operation. Only when we include tentative projects are we beginning to see an

ever so small production growth until 2020. However, many of these projects require gold prices at current levels or higher in

order to generate the IRRs required to make them economically feasible.

Exhibit 14: Ratio of head grade to reserve grade (lhs) and average processed grades (rhs)

Source(s): Bernstein

A general problem for the gold mining industry has been the fact that the average grade of processed ores has been steadily

deteriorating over the past decades. In other words, the low-hanging fruit is gone and an increasing amount of capex is

needed in order to maintain production levels. One way for companies to keep up was to re-process tailings, i.e. ore that was

insufficiently processed in the past when head grades were much higher. One can see this in the ratio of head grades to

MONTHLY VIEWPOINT

From the Chief Investment Officer Marco E Pabst

07th

March 2017

ACPI Investments Ltd.

Pegasus House | 37-43 Sackville Street | London W1S 3EH

T +44 (0)20 3697 9580 | F +44 (0)20 3697 9501 | E [email protected]

www.acpi.com

10

average reserve grades which has been trending higher as gold prices corrected after 2012. It is obviously more economical

for a miner to process old tailings when they still contain more gold per tonne than its current reserves.

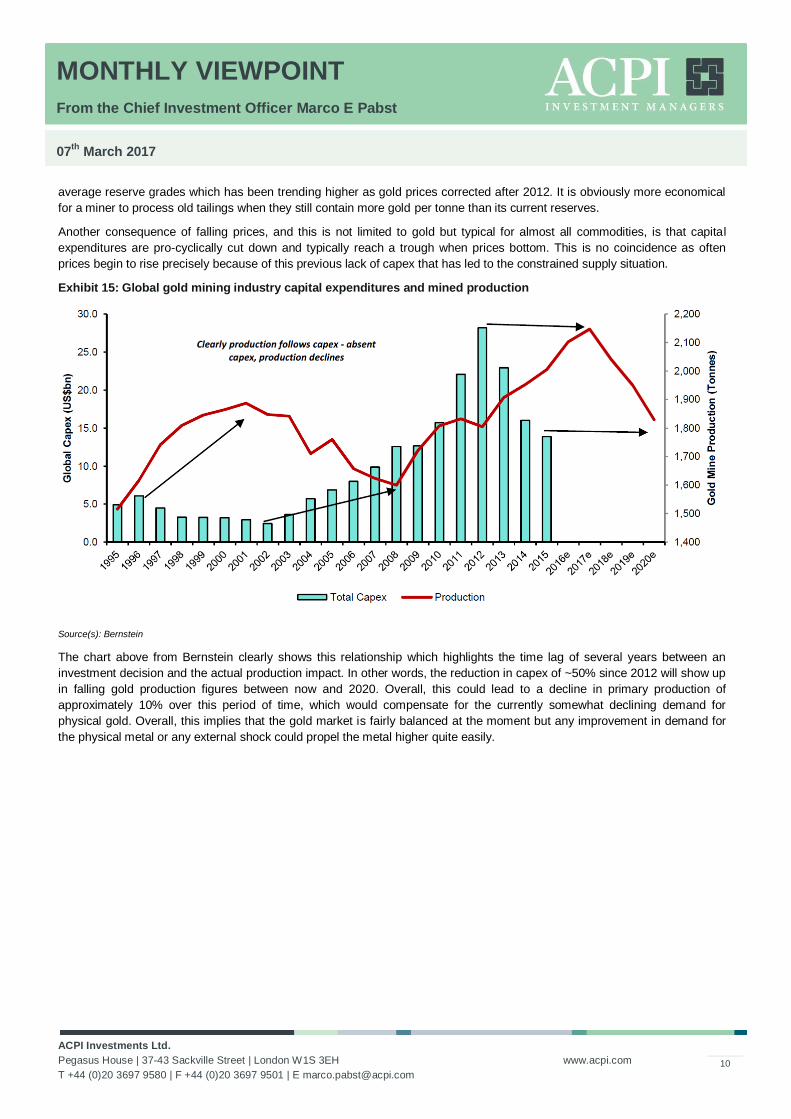

Another consequence of falling prices, and this is not limited to gold but typical for almost all commodities, is that capital

expenditures are pro-cyclically cut down and typically reach a trough when prices bottom. This is no coincidence as often

prices begin to rise precisely because of this previous lack of capex that has led to the constrained supply situation.

Exhibit 15: Global gold mining industry capital expenditures and mined production

Source(s): Bernstein

The chart above from Bernstein clearly shows this relationship which highlights the time lag of several years between an

investment decision and the actual production impact. In other words, the reduction in capex of ~50% since 2012 will show up

in falling gold production figures between now and 2020. Overall, this could lead to a decline in primary production of

approximately 10% over this period of time, which would compensate for the currently somewhat declining demand for

physical gold. Overall, this implies that the gold market is fairly balanced at the moment but any improvement in demand for

the physical metal or any external shock could propel the metal higher quite easily.

MONTHLY VIEWPOINT

From the Chief Investment Officer Marco E Pabst

07th

March 2017

ACPI Investments Ltd.

Pegasus House | 37-43 Sackville Street | London W1S 3EH

T +44 (0)20 3697 9580 | F +44 (0)20 3697 9501 | E [email protected]

www.acpi.com

11

Global economic monitor

Source(s): ACPI, Bloomberg

Sept Oct Nov Dec Jan Feb Trend

Citi Economic Surprise US -5.1 -8.1 17.8 23.3 31.8 34.7

Citi Economic Surprise G10 3.0 14.5 31.4 33.0 36.9 41.9

Citi Economic Surprise Europe 2.6 40.8 56.9 53.1 55.3 71.1

Citi Economic Surprise EM -11.0 -13.9 -4.4 18.1 37.1 46.6

Citi Economic Surprise UK 79.7 75.0 46.3 49.6 69.8 92.3

ISM manufacturing 51.7 52.0 53.5 54.5 56.0 57.7

ISM new orders 57.3 55.9 56.1 60.5 59.5 63.2

Global manufacturing PMI 51.7 53.1 53.2 53.6 53.9 53.5

China manufacturing PMI 50.4 51.2 51.7 51.4 51.3 51.6

Japan manufacturing PMI 50.4 51.4 51.3 52.4 52.7 53.3

US durable goods orders 0.3 5.0 -4.7 -0.8 1.8

US initial jobless claims 246 266 268 237 248 223

US Industrial production -0.3 0.3 -0.2 0.6 -0.3

Euro Industrial production -0.8 0.2 1.5 -1.6

Japan Industrial production 0.6 0.0 1.5 0.7 -0.8

US retail sales 1.0 0.7 0.2 1.0 0.4

Euro retail sales -0.1 1.2 -0.2 -0.5 -0.1

Japan retail sales -1.7 -0.2 1.7 0.7 1.0

China retail sales 10.7 10.0 10.8 10.9

US consumer confidence 103.5 100.8 109.4 113.3 111.6 114.8

Euro consumer confidence -8.2 -8.0 -6.2 -5.1 -4.8 -6.2

ifo German business expectations 104.5 106.0 105.4 105.5 103.2 104.0

China export trade -10.4 -7.9 -1.5 -6.2 7.9

South Korea export trade -5.9 -3.2 2.5 6.4 11.2 20.2

German export trade 0.4 2.0 4.3 3.3

China monthly money supply 11.5 11.6 11.4 11.3 11.3

US personal income 0.4 0.4 0.2 0.3 0.4

MONTHLY VIEWPOINT

From the Chief Investment Officer Marco E Pabst

07th

March 2017

ACPI Investments Ltd.

Pegasus House | 37-43 Sackville Street | London W1S 3EH

T +44 (0)20 3697 9580 | F +44 (0)20 3697 9501 | E [email protected]

www.acpi.com

12

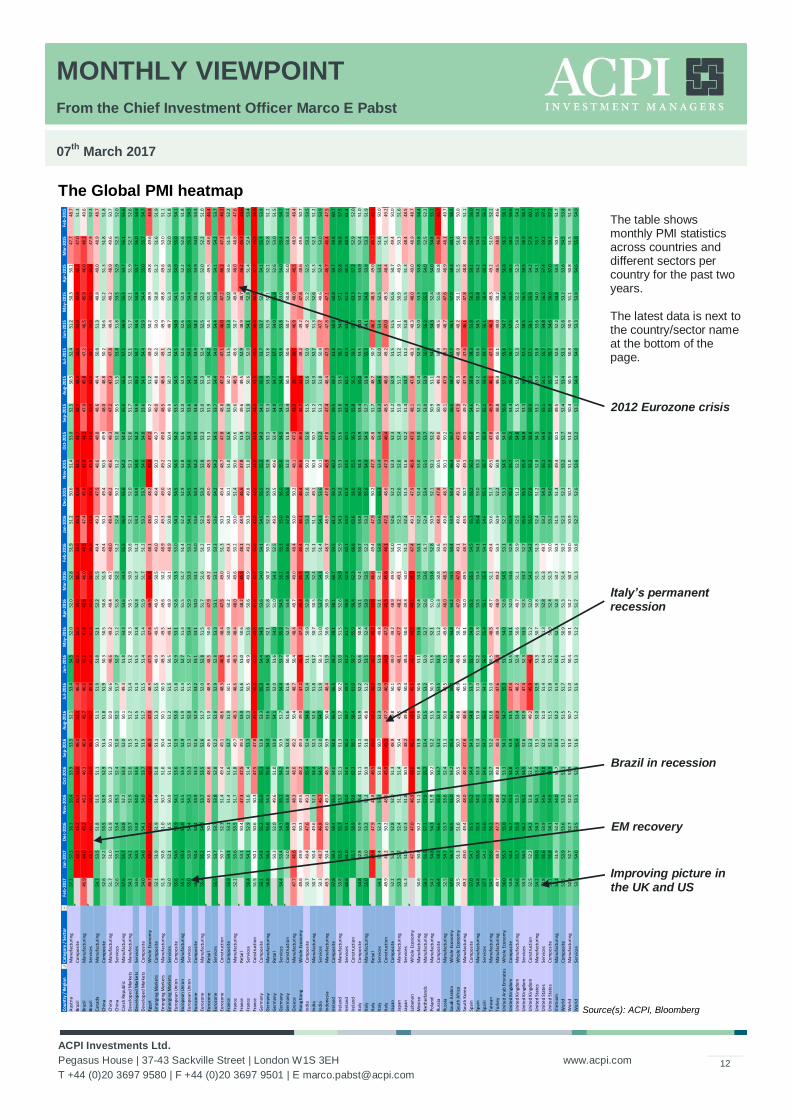

The Global PMI heatmap

Source(s): ACPI, Bloomberg Co

un

try

/ R

egi

on

Cat

ego

ry /

Se

cto

rFe

b-2

017

Jan

-201

7D

ec-

2016

No

v-20

16O

ct-2

016

Sep

-201

6A

ug-

2016

Jul-

2016

Jun

-201

6M

ay-2

016

Ap

r-20

16M

ar-2

016

Feb

-201

6Ja

n-2

016

De

c-20

15N

ov-

2015

Oct

-201

5Se

p-2

015

Au

g-20

15Ju

l-20

15Ju

n-2

015

May

-201

5A

pr-

2015

Mar

-201

5Fe

b-2

015

Au

stri

aM

anu

fact

uri

ng

57.2

57.3

56.3

55.4

53.9

53.5

52.1

53.4

54.5

52.0

52.0

52.8

51.9

51.2

50.6

51.4

53.0

52.5

50.5

52.4

51.2

50.3

50.1

47.7

48.7

Bra

zil

Co

mp

osi

te#N

/A44

.745

.245

.344

.946

.144

.446

.442

.338

.339

.040

.839

.045

.143

.944

.542

.742

.744

.840

.841

.042

.944

.247

.051

.3

Bra

zil

Man

ufa

ctu

rin

g46

.944

.045

.246

.246

.346

.045

.746

.043

.241

.642

.646

.044

.547

.445

.643

.844

.147

.045

.847

.246

.545

.946

.046

.249

.6

Bra

zil

Serv

ice

s#N

/A45

.145

.144

.443

.945

.342

.745

.641

.437

.337

.438

.636

.944

.443

.545

.543

.041

.744

.839

.139

.942

.544

.647

.952

.3

Can

ada

Man

ufa

ctu

rin

g54

.753

.551

.851

.551

.150

.351

.151

.951

.852

.152

.251

.549

.449

.347

.548

.648

.048

.649

.450

.851

.349

.849

.048

.948

.7

Ch

ina

Co

mp

osi

te52

.652

.253

.552

.952

.951

.451

.851

.950

.350

.550

.851

.349

.450

.149

.450

.549

.948

.048

.850

.250

.651

.251

.351

.851

.8

Ch

ina

Man

ufa

ctu

rin

g51

.751

.051

.950

.951

.250

.150

.050

.648

.649

.249

.449

.748

.048

.448

.248

.648

.347

.247

.347

.849

.449

.248

.949

.650

.7

Ch

ina

Serv

ice

s52

.653

.153

.453

.152

.452

.052

.151

.752

.751

.251

.852

.251

.252

.450

.251

.252

.050

.551

.553

.851

.853

.552

.952

.352

.0

Cze

ch R

ep

ub

lic

Man

ufa

ctu

rin

g57

.655

.753

.852

.253

.352

.050

.149

.351

.853

.353

.654

.355

.556

.955

.654

.254

.055

.556

.657

.556

.955

.554

.756

.155

.6

De

velo

pe

d M

arke

tsM

anu

fact

uri

ng

54.1

54.2

53.7

52.9

52.6

51.5

51.2

51.4

51.2

50.3

50.5

50.9

50.8

52.1

52.0

52.3

52.6

51.7

51.9

52.1

51.7

52.1

51.9

52.7

52.6

De

velo

pe

d M

arke

tsSe

rvic

es

53.6

54.5

53.8

54.0

53.6

51.7

51.5

51.3

51.5

51.8

52.3

51.7

51.2

53.3

53.9

54.8

54.2

53.9

55.2

54.7

54.4

54.8

55.7

56.0

54.9

De

velo

pe

d M

arke

tsC

om

po

site

54.0

54.6

54.1

54.0

53.7

51.9

51.7

51.5

51.4

51.4

51.9

51.7

51.2

53.2

53.7

54.6

54.0

53.6

54.6

54.4

53.9

54.4

55.0

55.7

54.7

Egyp

tW

ho

le E

con

om

y46

.743

.342

.841

.842

.046

.347

.048

.947

.547

.646

.944

.548

.148

.048

.245

.047

.250

.251

.249

.250

.249

.949

.849

.646

.8

Eme

rgin

g M

arke

tsC

om

po

site

52.1

51.9

51.9

51.4

51.8

51.1

51.3

51.5

49.9

49.5

49.9

50.5

49.0

50.1

49.4

50.2

49.7

49.0

49.8

50.2

50.0

50.8

51.2

51.6

51.9

Eme

rgin

g M

arke

tsM

anu

fact

uri

ng

51.3

50.8

51.0

50.7

51.0

50.4

50.1

50.3

49.3

49.5

49.6

50.2

48.9

49.3

49.0

49.2

49.0

48.5

48.6

49.1

49.9

49.8

49.6

50.0

51.1

Eme

rgin

g M

arke

tsSe

rvic

es

52.0

52.1

51.5

50.9

51.0

51.0

51.2

51.5

50.5

49.1

49.9

50.1

48.9

50.8

49.5

50.2

50.4

49.9

50.7

51.2

49.7

51.3

51.8

52.0

51.8

Euro

pe

an U

nio

nC

om

po

site

55.6

54.6

54.9

54.1

53.6

52.9

53.0

51.8

52.9

53.1

52.8

53.3

53.0

54.1

54.5

54.5

54.2

53.5

54.5

54.5

54.9

54.1

54.9

55.0

54.1

Euro

pe

an U

nio

nM

anu

fact

uri

ng

55.3

55.3

55.0

53.5

53.4

52.9

51.9

51.4

52.7

51.4

51.5

51.7

51.4

52.4

52.9

52.8

52.6

52.0

52.3

52.6

52.6

52.3

52.2

52.6

51.8

Euro

pe

an U

nio

nSe

rvic

es

55.0

53.9

54.4

54.1

53.3

52.3

52.8

51.5

52.7

53.4

52.9

53.3

53.2

54.1

54.5

54.6

54.3

53.6

54.7

54.8

55.4

54.4

55.4

55.3

54.5

Euro

zon

eC

om

po

site

56.0

54.4

54.4

53.9

53.3

52.6

52.9

53.2

53.1

53.1

53.0

53.1

53.0

53.6

54.3

54.2

53.9

53.6

54.3

53.9

54.2

53.6

53.9

54.0

53.3

Euro

zon

eM

anu

fact

uri

ng

55.4

55.2

54.9

53.7

53.5

52.6

51.7

52.0

52.8

51.5

51.7

51.6

51.2

52.3

53.2

52.8

52.3

52.0

52.3

52.4

52.5

52.2

52.0

52.2

51.0

Euro

zon

eR

eta

il#N

/A50

.150

.448

.648

.649

.651

.048

.948

.550

.647

.949

.250

.148

.949

.048

.551

.351

.951

.454

.250

.451

.449

.548

.646

.4

Euro

zon

eSe

rvic

es

55.5

53.7

53.7

53.8

52.8

52.2

52.8

52.9

52.8

53.3

53.1

53.1

53.3

53.6

54.2

54.2

54.1

53.7

54.4

54.0

54.4

53.8

54.1

54.2

53.7

Euro

zon

eC

on

stru

ctio

n#N

/A50

.752

.351

.449

.449

.148

.648

.346

.548

.447

.549

.051

.350

.349

.448

.747

.848

.847

.247

.146

.047

.246

.247

.146

.2

Fran

ceC

om

po

site

55.9

54.1

53.1

51.4

51.6

52.7

51.9

50.1

49.6

50.9

50.2

50.0

49.3

50.2

50.1

51.0

52.6

51.9

50.2

51.5

53.3

52.0

50.6

51.5

52.2

Fran

ceM

anu

fact

uri

ng

52.2

53.6

53.5

51.7

51.8

49.7

48.3

48.6

48.3

48.4

48.0

49.6

50.2

50.0

51.4

50.6

50.6

50.6

48.3

49.6

50.7

49.4

48.0

48.8

47.6

Fran

ceR

eta

il#N

/A53

.150

.447

.347

.549

.153

.051

.651

.050

.648

.245

.548

.148

.946

.647

.851

.949

.649

.552

.948

.948

.746

.245

.743

.6

Fran

ceSe

rvic

es

56.4

54.1

52.9

51.6

51.4

53.3

52.3

50.5

49.9

51.6

50.6

49.9

49.2

50.3

49.8

51.0

52.7

51.9

50.6

52.0

54.1

52.8

51.4

52.4

53.4

Fran

ceC

on

stru

ctio

n51

.550

.150

.650

.347

.547

.845

.344

.842

.343

.841

.642

.744

.643

.042

.244

.843

.844

.242

.340

.638

.440

.037

.735

.934

.9

Ge

rman

yC

om

po

site

56.1

54.8

55.2

55.0

55.1

52.8

53.3

55.3

54.4

54.5

53.6

54.0

54.1

54.5

55.5

55.2

54.2

54.1

55.0

53.7

53.7

52.6

54.1

55.4

53.8

Ge

rman

yM

anu

fact

uri

ng

56.8

56.4

55.6

54.3

55.0

54.3

53.6

53.8

54.5

52.1

51.8

50.7

50.5

52.3

53.2

52.9

52.1

52.3

53.3

51.8

51.9

51.1

52.1

52.8

51.1

Ge

rman

yR

eta

il#N

/A50

.352

.049

.651

.053

.054

.152

.051

.654

.051

.054

.152

.549

.550

.549

.652

.454

.054

.757

.754

.055

.852

.653

.051

.5

Ge

rman

ySe

rvic

es

54.4

53.4

54.3

55.1

54.2

50.9

51.7

54.4

53.7

55.2

54.5

55.1

55.3

55.0

56.0

55.6

54.5

54.1

54.9

53.8

53.8

53.0

54.0

55.4

54.7

Ge

rman

yC

on

stru

ctio

n#N

/A52

.054

.953

.952

.952

.451

.651

.650

.452

.753

.455

.859

.657

.955

.552

.551

.852

.450

.350

.650

.750

.851

.053

.353

.1

Gre

ece

Man

ufa

ctu

rin

g47

.746

.649

.348

.348

.649

.250

.448

.750

.448

.449

.749

.048

.450

.050

.248

.147

.343

.339

.130

.246

.948

.046

.548

.948

.4

Ho

ng

Ko

ng

Wh

ole

Eco

no

my

49.6

49.9

50.3

49.5

48.2

49.3

49.0

47.2

45.4

47.2

45.3

45.5

46.4

46.1

46.4

46.6

46.6

45.7

44.4

48.2

49.2

47.6

48.6

49.6

50.7

Ind

iaC

om

po

site

50.7

49.4

47.6

49.1

55.4

52.4

54.6

52.4

51.1

50.9

52.8

54.3

51.2

53.3

51.6

50.2

52.6

51.5

52.6

52.0

49.2

51.2

52.5

53.2

53.5

Ind

iaM

anu

fact

uri

ng

50.7

50.4

49.6

52.3

54.4

52.1

52.6

51.8

51.7

50.7

50.5

52.4

51.1

51.1

49.1

50.3

50.7

51.2

52.3

52.7

51.3

52.6

51.3

52.1

51.2

Ind

iaSe

rvic

es

50.3

48.7

46.8

46.7

54.5

52.0

54.7

51.9

50.3

51.0

53.7

54.3

51.4

54.3

53.6

50.1

53.2

51.3

51.8

50.8

47.7

49.6

52.4

53.0

53.9

Ind

on

esi

aM

anu

fact

uri

ng

49.3

50.4

49.0

49.7

48.7

50.9

50.4

48.4

51.9

50.6

50.9

50.6

48.7

48.9

47.8

46.9

47.8

47.4

48.4

47.3

47.8

47.1

46.7

46.4

47.5

Ire

lan

dC

om

po

site

57.8

59.3

58.4

55.5

54.0

54.8

56.9

56.5

59.2

59.1

58.1

60.7

59.5

61.1

59.2

60.2

57.7

59.5

59.7

61.8

60.9

60.8

59.7

59.8

60.7

Ire

lan

dM

anu

fact

uri

ng

53.8

55.5

55.7

53.7

52.1

51.3

51.7

50.2

53.0

51.5

52.6

54.9

52.9

54.3

54.2

53.3

53.6

53.8

53.6

56.7

54.6

57.1

55.8

56.8

57.5

Ire

lan

dSe

rvic

es

60.6

61.0

59.1

56.0

54.6

56.2

59.7

59.5

61.2

61.7

59.8

62.8

62.1

64.0

61.8

63.6

60.1

62.4

62.1

63.4

63.3

61.4

60.6

60.9

61.4

Ire

lan

dC

on

stru

ctio

n#N

/A55

.758

.959

.862

.358

.758

.461

.059

.755

.956

.462

.368

.863

.658

.655

.556

.355

.856

.559

.165

.763

.357

.252

.952

.0

Ital

yC

om

po

site

54.8

52.8

52.9

53.4

51.1

51.1

51.9

52.2

52.6

50.8

53.1

52.4

53.7

53.8

56.0

54.3

53.9

53.4

55.0

53.5

54.0

53.7

53.9

52.4

51.0

Ital

yM

anu

fact

uri

ng

55.0

53.0

53.2

52.2

50.9

51.0

49.8

51.2

53.5

52.4

53.9

53.5

52.2

53.2

55.6

54.9

54.1

52.7

53.8

55.3

54.1

54.8

53.8

53.3

51.9

Ital

yR

eta

il#N

/A45

.647

.948

.846

.545

.043

.240

.340

.245

.242

.646

.649

.447

.950

.247

.748

.851

.748

.750

.746

.748

.349

.045

.742

.3

Ital

ySe

rvic

es

54.1

52.4

52.3

53.3

51.0

50.7

52.3

52.0

51.9

49.8

52.1

51.2

53.8

53.6

55.3

53.4

53.4

53.3

54.6

52.0

53.4

52.5

53.1

51.6

50.0

Ital

yC

on

stru

ctio

n49

.949

.250

.248

.545

.945

.147

.746

.944

.947

.245

.345

.846

.147

.248

.647

.346

.448

.548

.049

.247

.049

.348

.451

.149

.2

Jap

anC

om

po

site

52.2

52.3

52.8

52.0

51.3

48.9

49.8

50.1

49.0

49.2

48.9

49.9

51.0

52.6

52.2

52.3

52.3

51.2

52.9

51.5

51.5

51.6

50.7

49.4

50.0

Jap

anM

anu

fact

uri

ng

53.3

52.7

52.4

51.3

51.4

50.4

49.5

49.3

48.1

47.7

48.2

49.1

50.1

52.3

52.6

52.6

52.4

51.0

51.7

51.2

50.1

50.9

49.9

50.3

51.6

Jap

anSe

rvic

es

51.3

51.9

52.3

51.8

50.5

48.2

49.6

50.4

49.4

50.4

49.3

50.0

51.2

52.4

51.5

51.6

52.2

51.4

53.7

51.2

51.8

51.5

51.3

48.4

48.5

Leb

ano

nW

ho

le E

con

om

y#N

/A47

.747

.046

.943

.845

.145

.045

.544

.444

.844

.145

.047

.449

.147

.946

.947

.148

.147

.849

.349

.348

.049

.048

.948

.7

Me

xico

Man

ufa

ctu

rin

g50

.650

.850

.251

.151

.851

.950

.950

.651

.153

.652

.453

.253

.152

.252

.453

.053

.052

.152

.452

.952

.053

.353

.853

.854

.4

Ne

the

rlan

ds

Man

ufa

ctu

rin

g58

.356

.557

.357

.055

.753

.453

.553

.252

.052

.752

.653

.651

.752

.453

.453

.553

.753

.053

.956

.056

.255

.554

.052

.552

.2

Po

lan

dM

anu

fact

uri

ng

54.2

54.8

54.3

51.9

50.2

52.2

51.5

50.3

51.8

52.1

51.0

53.8

52.8

50.9

52.1

52.1

52.2

50.9

51.1

54.5

54.3

52.4

54.0

54.8

55.1

Ru

ssia

Co

mp

osi

te55

.458

.356

.655

.853

.753

.152

.953

.553

.551

.251

.350

.850

.648

.447

.850

.549

.050

.949

.350

.949

.551

.650

.846

.844

.7

Ru

ssia

Man

ufa

ctu

rin

g52

.554

.753

.753

.652

.451

.150

.849

.551

.549

.648

.048

.349

.349

.848

.750

.150

.249

.147

.948

.348

.747

.648

.948

.149

.7

Sau

di A

rab

iaW

ho

le E

con

om

y57

.056

.755

.555

.053

.255

.356

.656

.054

.454

.854

.254

.554

.453

.954

.456

.355

.756

.558

.757

.756

.157

.058

.360

.158

.5

Sou

th A

fric

aW

ho

le E

con

om

y50

.551

.351

.650

.850

.550

.749

.849

.949

.650

.247

.947

.049

.149

.649

.149

.647

.547

.949

.348

.949

.250

.151

.551

.650

.0

Sou

th K

ore

aM

anu

fact

uri

ng

49.2

49.0

49.4

48.0

48.0

47.6

48.6

50.1

50.5

50.1

50.0

49.5

48.7

49.5

50.7

49.1

49.1

49.2

47.9

47.6

46.1

47.8

48.8

49.2

51.1

Spai

nC

om

po

site

57.0

54.7

55.5

55.2

54.4

54.1

54.8

53.7

55.7

54.8

55.2

55.1

54.5

55.3

55.2

56.2

55.0

54.6

58.8

58.3

55.8

58.3

59.1

56.9

56.0

Spai

nM

anu

fact

uri

ng

54.8

55.6

55.3

54.5

53.3

52.3

51.0

51.0

52.2

51.8

53.5

53.4

54.1

55.4

53.0

53.1

51.3

51.7

53.2

53.6

54.5

55.8

54.2

54.3

54.2

Spai

nSe

rvic

es

57.7

54.2

55.0

55.1

54.6

54.7

56.0

54.1

56.0

55.4

55.1

55.3

54.1

54.6

55.1

56.7

55.9

55.1

59.6

59.7

56.1

58.4

60.3

57.3

56.2

Taiw

anM

anu

fact

uri

ng

54.5

55.6

56.2

54.7

52.7

52.2

51.8

51.0

50.5

48.5

49.7

51.1

49.4

50.6

51.7

49.5

47.8

46.9

46.1

47.1

46.3

49.3

49.2

51.0

52.1

Turk

ey

Man

ufa

ctu

rin

g49

.748

.747

.748

.849

.848

.347

.047

.647

.449

.448

.949

.250

.350

.952

.250

.949

.548

.849

.350

.149

.050

.248

.548

.049

.6

Un

ite

d A

rab

Em

irat

es

Wh

ole

Eco

no

my

56.0

55.3

55.0

54.2

53.3

54.1

54.7

55.3

53.4

54.0

52.8

54.5

53.1

52.7

53.3

54.5

54.0

56.0

57.1

55.8

54.7

56.4

56.8

56.3

58.1

Un

ite

d K

ingd

om

Co

mp

osi

te53

.855

.456

.755

.354

.853

.953

.547

.452

.553

.152

.053

.652

.855

.955

.255

.755

.253

.455

.256

.757

.555

.958

.558

.556

.6

Un

ite

d K

ingd

om

Man

ufa

ctu

rin

g54

.655

.755

.953

.554

.555

.453

.448

.252

.450

.649

.751

.150

.952

.551

.252

.554

.851

.551

.752

.351

.452

.252

.353

.854

.2

Un

ite

d K

ingd

om

Serv

ice

s53

.354

.556

.255

.254

.552

.652

.947

.452

.353

.552

.353

.752

.755

.655

.555

.954

.953

.355

.657

.458

.556

.559

.558

.956

.7

Un

ite

d K

ingd

om

Co

nst

ruct

ion

52.5

52.2

54.2

52.8

52.6

52.3

49.2

45.9

46.0

51.2

52.0

54.2

54.2

55.0

57.8

55.3

58.8

59.9

57.3

57.1

58.1

55.9

54.2

57.8

60.1

Un

ite

d S

tate

sM

anu

fact

uri

ng

54.2

55.0

54.3

54.1

53.4

51.5

52.0

52.9

51.3

50.7

50.8

51.5

51.3

52.4

51.2

52.8

54.1

53.1

53.0

53.8

53.6

54.0

54.1

55.7

55.1

Un

ite

d S

tate

sSe

rvic

es

53.8

55.6

53.9

54.6

54.8

52.3

51.0

51.4

51.4

51.3

52.8

51.3

49.7

53.2

54.3

56.1

54.8

55.1

56.1

55.7

54.8

56.2

57.4

59.2

57.1

Un

ite

d S

tate

sC

om

po

site

54.1

55.8

54.1

54.9

54.9

52.3

51.5

51.8

51.2

50.9

52.4

51.3

50.0

53.2

54.0

55.9

55.0

55.0

55.7

55.7

54.6

56.0

57.0

59.2

57.2

Vie

tnam

Man

ufa

ctu

rin

g54

.251

.952

.454

.051

.752

.952

.251

.952

.652

.752

.350

.750

.351

.551

.349

.450

.149

.551

.352

.652

.254

.853

.550

.751

.7

Wo

rld

Co

mp

osi

te53

.553

.953

.653

.253

.151

.751

.551

.751

.150

.951

.351

.450

.752

.352

.353

.252

.752

.453

.453

.352

.853

.253

.854

.553

.8

Wo

rld

Man

ufa

ctu

rin

g52

.952

.752

.752

.051

.951

.050

.751

.050

.450

.150

.250

.750

.050

.950

.751

.051

.050

.450

.550

.850

.951

.150

.851

.551

.9

Wo

rld

Serv

ice

s53

.354

.053

.553

.152

.951

.651

.251

.651

.351

.251

.751

.350

.852

.752

.653

.653

.253

.154

.454

.053

.353

.854

.655

.054

.0

The table shows monthly PMI statistics across countries and different sectors per country for the past two years. The latest data is next to the country/sector name at the bottom of the page.

2012 Eurozone crisis

Brazil in recession

Italy’s permanent recession

Improving picture in the UK and US

EM recovery

MONTHLY VIEWPOINT

From the Chief Investment Officer Marco E Pabst

07th

March 2017

ACPI Investments Ltd.

Pegasus House | 37-43 Sackville Street | London W1S 3EH

T +44 (0)20 3697 9580 | F +44 (0)20 3697 9501 | E [email protected]

www.acpi.com

13

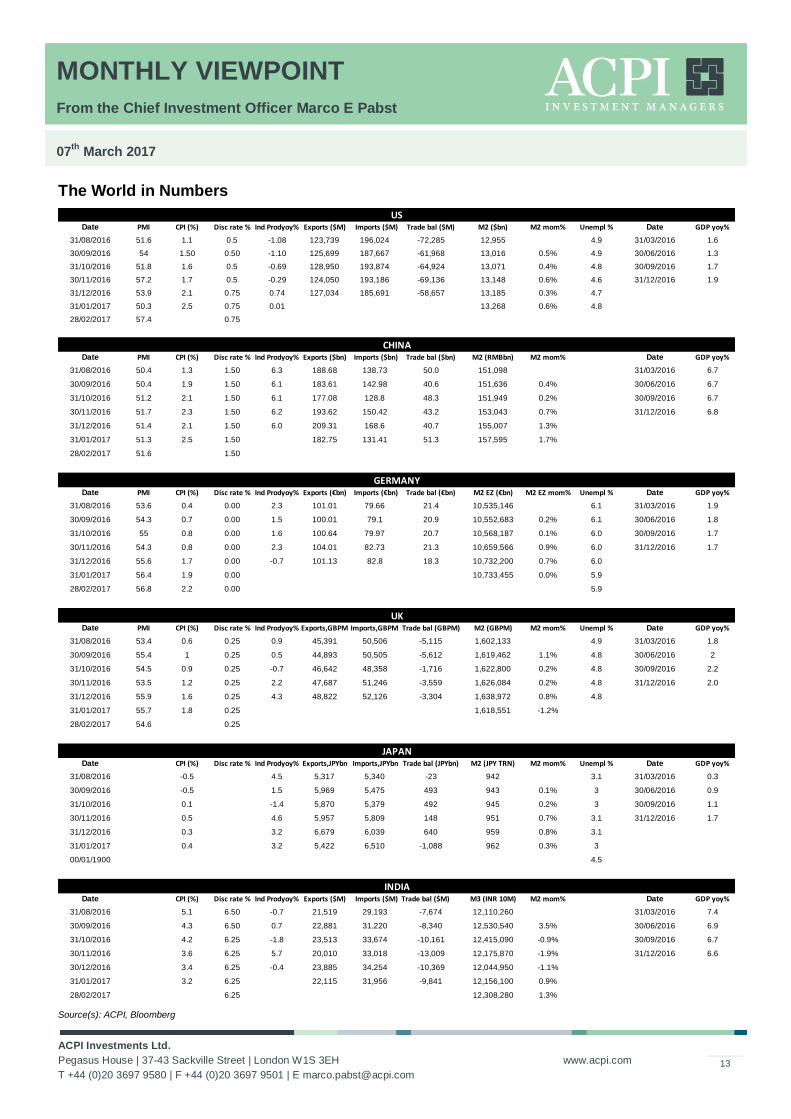

The World in Numbers

Source(s): ACPI, Bloomberg

Date PMI CPI (%) Disc rate % Ind Prodyoy% Exports ($M) Imports ($M) Trade bal ($M) M2 ($bn) M2 mom% Unempl % Date GDP yoy%

31/08/2016 51.6 1.1 0.5 -1.08 123,739 196,024 -72,285 12,955 4.9 31/03/2016 1.6

30/09/2016 54 1.50 0.50 -1.10 125,699 187,667 -61,968 13,016 0.5% 4.9 30/06/2016 1.3

31/10/2016 51.8 1.6 0.5 -0.69 128,950 193,874 -64,924 13,071 0.4% 4.8 30/09/2016 1.7

30/11/2016 57.2 1.7 0.5 -0.29 124,050 193,186 -69,136 13,148 0.6% 4.6 31/12/2016 1.9

31/12/2016 53.9 2.1 0.75 0.74 127,034 185,691 -58,657 13,185 0.3% 4.7

31/01/2017 50.3 2.5 0.75 0.01 13,268 0.6% 4.8

28/02/2017 57.4 0.75

Date PMI CPI (%) Disc rate % Ind Prodyoy% Exports ($bn) Imports ($bn) Trade bal ($bn) M2 (RMBbn) M2 mom% Date GDP yoy%

31/08/2016 50.4 1.3 1.50 6.3 188.68 138.73 50.0 151,098 31/03/2016 6.7

30/09/2016 50.4 1.9 1.50 6.1 183.61 142.98 40.6 151,636 0.4% 30/06/2016 6.7

31/10/2016 51.2 2.1 1.50 6.1 177.08 128.8 48.3 151,949 0.2% 30/09/2016 6.7

30/11/2016 51.7 2.3 1.50 6.2 193.62 150.42 43.2 153,043 0.7% 31/12/2016 6.8

31/12/2016 51.4 2.1 1.50 6.0 209.31 168.6 40.7 155,007 1.3%

31/01/2017 51.3 2.5 1.50 182.75 131.41 51.3 157,595 1.7%

28/02/2017 51.6 1.50

Date PMI CPI (%) Disc rate % Ind Prodyoy% Exports (€bn) Imports (€bn) Trade bal (€bn) M2 EZ (€bn) M2 EZ mom% Unempl % Date GDP yoy%

31/08/2016 53.6 0.4 0.00 2.3 101.01 79.66 21.4 10,535,146 6.1 31/03/2016 1.9

30/09/2016 54.3 0.7 0.00 1.5 100.01 79.1 20.9 10,552,683 0.2% 6.1 30/06/2016 1.8

31/10/2016 55 0.8 0.00 1.6 100.64 79.97 20.7 10,568,187 0.1% 6.0 30/09/2016 1.7

30/11/2016 54.3 0.8 0.00 2.3 104.01 82.73 21.3 10,659,566 0.9% 6.0 31/12/2016 1.7

31/12/2016 55.6 1.7 0.00 -0.7 101.13 82.8 18.3 10,732,200 0.7% 6.0

31/01/2017 56.4 1.9 0.00 10,733,455 0.0% 5.9

28/02/2017 56.8 2.2 0.00 5.9

Date PMI CPI (%) Disc rate % Ind Prodyoy% Exports,GBPM Imports,GBPM Trade bal (GBPM) M2 (GBPM) M2 mom% Unempl % Date GDP yoy%

31/08/2016 53.4 0.6 0.25 0.9 45,391 50,506 -5,115 1,602,133 4.9 31/03/2016 1.8

30/09/2016 55.4 1 0.25 0.5 44,893 50,505 -5,612 1,619,462 1.1% 4.8 30/06/2016 2

31/10/2016 54.5 0.9 0.25 -0.7 46,642 48,358 -1,716 1,622,800 0.2% 4.8 30/09/2016 2.2

30/11/2016 53.5 1.2 0.25 2.2 47,687 51,246 -3,559 1,626,084 0.2% 4.8 31/12/2016 2.0

31/12/2016 55.9 1.6 0.25 4.3 48,822 52,126 -3,304 1,638,972 0.8% 4.8

31/01/2017 55.7 1.8 0.25 1,618,551 -1.2%

28/02/2017 54.6 0.25

Date CPI (%) Disc rate % Ind Prodyoy% Exports,JPYbn Imports,JPYbn Trade bal (JPYbn) M2 (JPY TRN) M2 mom% Unempl % Date GDP yoy%

31/08/2016 -0.5 4.5 5,317 5,340 -23 942 3.1 31/03/2016 0.3

30/09/2016 -0.5 1.5 5,969 5,475 493 943 0.1% 3 30/06/2016 0.9

31/10/2016 0.1 -1.4 5,870 5,379 492 945 0.2% 3 30/09/2016 1.1

30/11/2016 0.5 4.6 5,957 5,809 148 951 0.7% 3.1 31/12/2016 1.7

31/12/2016 0.3 3.2 6,679 6,039 640 959 0.8% 3.1

31/01/2017 0.4 3.2 5,422 6,510 -1,088 962 0.3% 3

00/01/1900 4.5

Date CPI (%) Disc rate % Ind Prodyoy% Exports ($M) Imports ($M) Trade bal ($M) M3 (INR 10M) M2 mom% Date GDP yoy%

31/08/2016 5.1 6.50 -0.7 21,519 29,193 -7,674 12,110,260 31/03/2016 7.4

30/09/2016 4.3 6.50 0.7 22,881 31,220 -8,340 12,530,540 3.5% 30/06/2016 6.9

31/10/2016 4.2 6.25 -1.8 23,513 33,674 -10,161 12,415,090 -0.9% 30/09/2016 6.7

30/11/2016 3.6 6.25 5.7 20,010 33,018 -13,009 12,175,870 -1.9% 31/12/2016 6.6

30/12/2016 3.4 6.25 -0.4 23,885 34,254 -10,369 12,044,950 -1.1%

31/01/2017 3.2 6.25 22,115 31,956 -9,841 12,156,100 0.9%

28/02/2017 6.25 12,308,280 1.3%

INDIA

US

CHINA

GERMANY

UK

JAPAN

MONTHLY VIEWPOINT

From the Chief Investment Officer Marco E Pabst

07th

March 2017

ACPI Investments Ltd.

Pegasus House | 37-43 Sackville Street | London W1S 3EH

T +44 (0)20 3697 9580 | F +44 (0)20 3697 9501 | E [email protected]

www.acpi.com

14

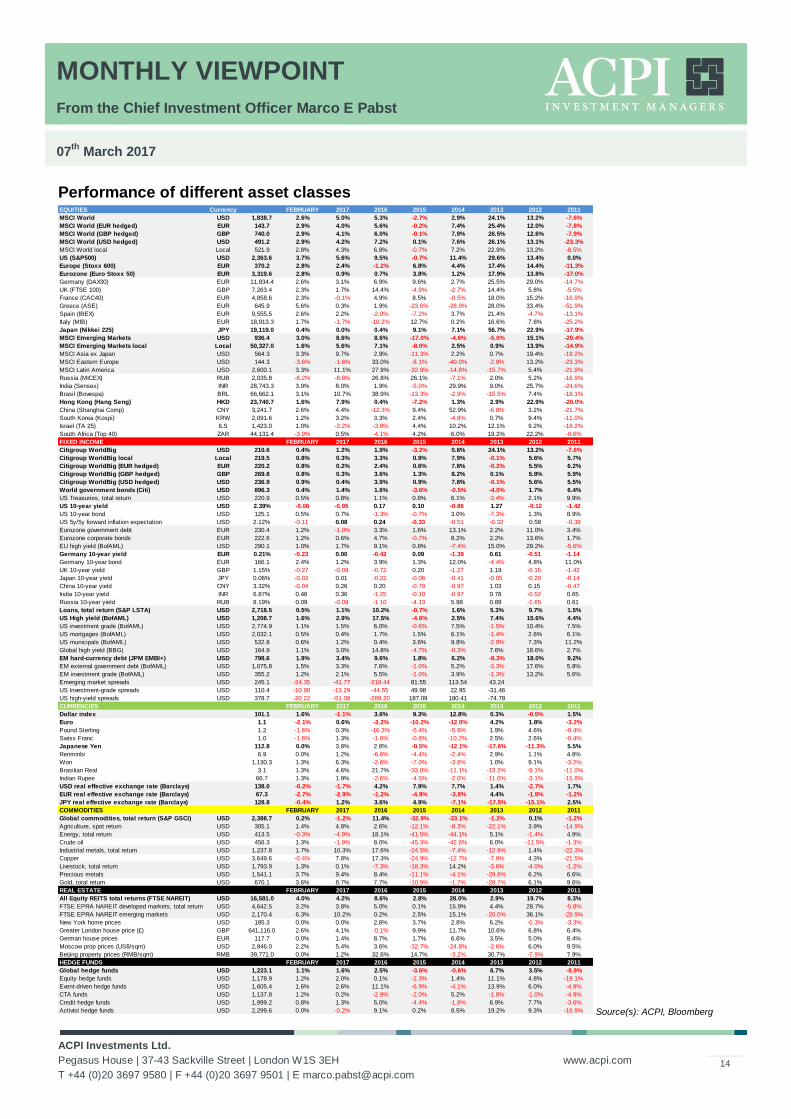

Performance of different asset classes

Source(s): ACPI, Bloomberg

EQUITIES Currency FEBRUARY 2017 2016 2015 2014 2013 2012 2011

MSCI World USD 1,838.7 2.6% 5.0% 5.3% -2.7% 2.9% 24.1% 13.2% -7.6%

MSCI World (EUR hedged) EUR 143.7 2.9% 4.0% 5.6% -0.2% 7.4% 25.4% 12.0% -7.8%

MSCI World (GBP hedged) GBP 740.0 2.9% 4.1% 6.0% -0.1% 7.9% 26.5% 12.6% -7.9%

MSCI World (USD hedged) USD 491.2 2.9% 4.2% 7.2% 0.1% 7.6% 26.1% 13.1% -23.3%

MSCI World local Local 521.9 2.8% 4.3% 6.8% -0.7% 7.2% 22.9% 13.2% -8.5%

US (S&P500) USD 2,363.6 3.7% 5.6% 9.5% -0.7% 11.4% 29.6% 13.4% 0.0%

Europe (Stoxx 600) EUR 370.2 2.8% 2.4% -1.2% 6.8% 4.4% 17.4% 14.4% -11.3%

Eurozone (Euro Stoxx 50) EUR 3,319.6 2.8% 0.9% 0.7% 3.8% 1.2% 17.9% 13.8% -17.0%

Germany (DAX30) EUR 11,834.4 2.6% 3.1% 6.9% 9.6% 2.7% 25.5% 29.0% -14.7%

UK (FTSE 100) GBP 7,263.4 2.3% 1.7% 14.4% -4.9% -2.7% 14.4% 5.8% -5.5%

France (CAC40) EUR 4,858.6 2.3% -0.1% 4.9% 8.5% -0.5% 18.0% 15.2% -16.9%

Greece (ASE) EUR 645.9 5.6% 0.3% 1.9% -23.6% -28.9% 28.0% 33.4% -51.9%

Spain (IBEX) EUR 9,555.5 2.6% 2.2% -2.0% -7.2% 3.7% 21.4% -4.7% -13.1%

Italy (MIB) EUR 18,913.3 1.7% -1.7% -10.2% 12.7% 0.2% 16.6% 7.8% -25.2%

Japan (Nikkei 225) JPY 19,119.0 0.4% 0.0% 0.4% 9.1% 7.1% 56.7% 22.9% -17.9%

MSCI Emerging Markets USD 936.4 3.0% 8.6% 8.6% -17.0% -4.6% -5.0% 15.1% -20.4%

MSCI Emerging Markets local Local 50,327.0 1.6% 5.6% 7.1% -8.0% 2.5% 0.9% 13.9% -14.9%

MSCI Asia ex Japan USD 564.3 3.3% 9.7% 2.9% -11.3% 2.2% 0.7% 19.4% -19.2%

MSCI Eastern Europe USD 144.3 -3.6% -1.6% 33.0% -8.1% -40.0% -2.9% 13.2% -23.3%

MSCI Latin America USD 2,600.1 3.3% 11.1% 27.9% -32.9% -14.8% -15.7% 5.4% -21.9%

Russia (MICEX) RUB 2,035.8 -8.2% -8.8% 26.8% 26.1% -7.1% 2.0% 5.2% -16.9%

India (Sensex) INR 28,743.3 3.9% 8.0% 1.9% -5.0% 29.9% 9.0% 25.7% -24.6%

Brasil (Bovespa) BRL 66,662.1 3.1% 10.7% 38.9% -13.3% -2.9% -15.5% 7.4% -18.1%

Hong Kong (Hang Seng) HKD 23,740.7 1.6% 7.9% 0.4% -7.2% 1.3% 2.9% 22.9% -20.0%

China (Shanghai Comp) CNY 3,241.7 2.6% 4.4% -12.3% 9.4% 52.9% -6.8% 3.2% -21.7%

South Korea (Kospi) KRW 2,091.6 1.2% 3.2% 3.3% 2.4% -4.8% 0.7% 9.4% -11.0%

Israel (TA 25) ILS 1,423.0 1.0% -3.2% -3.8% 4.4% 10.2% 12.1% 9.2% -18.2%

South Africa (Top 40) ZAR 44,131.4 -3.9% 0.5% -4.1% 4.2% 6.0% 19.2% 22.2% -0.6%

FIXED INCOME FEBRUARY 2017 2016 2015 2014 2013 2012 2011

Citigroup WorldBig USD 210.6 0.4% 1.2% 1.9% -3.2% 0.8% 24.1% 13.2% -7.6%

Citigroup WorldBig local Local 219.5 0.8% 0.3% 3.3% 0.9% 7.9% -0.1% 5.6% 5.7%

Citigroup WorldBig (EUR hedged) EUR 220.2 0.8% 0.2% 2.4% 0.6% 7.8% -0.2% 5.5% 6.2%

Citigroup WorldBig (GBP hedged) GBP 269.8 0.8% 0.3% 3.6% 1.3% 8.2% 0.1% 5.8% 5.9%

Citigroup WorldBig (USD hedged) USD 236.9 0.9% 0.4% 3.9% 0.9% 7.8% -0.1% 5.6% 5.5%

World government bonds (Citi) USD 896.3 0.4% 1.4% 1.6% -3.6% -0.5% -4.0% 1.7% 6.4%

US Treasuries, total return USD 220.9 0.5% 0.8% 1.1% 0.8% 6.1% -3.4% 2.1% 9.9%

US 10-year yield USD 2.39% -0.06 -0.05 0.17 0.10 -0.86 1.27 -0.12 -1.42

US 10-year bond USD 125.1 0.5% 0.7% -1.3% -0.7% 3.0% -7.3% 1.3% 8.9%

US 5y/5y forward inflation expectation USD 2.12% -0.11 0.08 0.24 -0.33 -0.51 -0.32 0.58 -0.39

Eurozone government debt EUR 230.4 1.2% -1.0% 3.3% 1.6% 13.1% 2.2% 11.0% 3.4%

Eurozone corporate bonds EUR 222.6 1.2% 0.6% 4.7% -0.7% 8.2% 2.2% 13.6% 1.7%

EU high yield (BofAML) USD 290.1 1.0% 1.7% 9.1% 0.8% -7.4% 15.0% 29.2% -5.6%

Germany 10-year yield EUR 0.21% -0.23 0.00 -0.42 0.09 -1.39 0.61 -0.51 -1.14

Germany 10-year bond EUR 166.1 2.4% 1.2% 3.9% 1.3% 12.0% -4.4% 4.8% 11.0%

UK 10-year yield GBP 1.15% -0.27 -0.09 -0.72 0.20 -1.27 1.19 -0.15 -1.42

Japan 10-year yield JPY 0.06% -0.03 0.01 -0.22 -0.06 -0.41 -0.05 -0.20 -0.14

China 10-year yield CNY 3.32% -0.04 0.26 0.20 -0.79 -0.97 1.03 0.15 -0.47

India 10-year yield INR 6.87% 0.46 0.36 -1.25 -0.10 -0.97 0.78 -0.52 0.65

Russia 10-year yield RUB 8.19% 0.09 -0.09 -1.10 -4.13 5.98 0.89 -1.65 0.61

Loans, total return (S&P LSTA) USD 2,718.5 0.5% 1.1% 10.2% -0.7% 1.6% 5.3% 9.7% 1.5%

US High yield (BofAML) USD 1,208.7 1.6% 2.9% 17.5% -4.6% 2.5% 7.4% 15.6% 4.4%

US investment grade (BofAML) USD 2,774.9 1.1% 1.5% 6.0% -0.6% 7.5% -1.5% 10.4% 7.5%

US mortgages (BofAML) USD 2,032.1 0.5% 0.4% 1.7% 1.5% 6.1% -1.4% 2.6% 6.1%

US municipals (BofAML) USD 532.8 0.6% 1.2% 0.4% 3.6% 9.8% -2.9% 7.3% 11.2%

Global high yield (BBG) USD 164.9 1.1% 3.0% 14.8% -4.7% -0.3% 7.6% 18.6% 2.7%

EM hard-currency debt (JPM EMBI+) USD 798.6 1.9% 3.4% 9.6% 1.8% 6.2% -8.3% 18.0% 9.2%

EM external government debt (BofAML) USD 1,075.8 1.5% 3.3% 7.6% -1.0% 5.2% -3.3% 17.6% 5.8%

EM investment grade (BofAML) USD 355.2 1.2% 2.1% 5.5% -1.0% 3.9% -1.3% 13.2% 5.6%

Emerging market spreads USD 245.1 -24.35 -41.77 -218.44 81.55 113.54 43.24

US Investment-grade spreads USD 110.4 -10.90 -13.29 -44.55 49.98 22.95 -31.46

US high-yield spreads USD 378.7 -20.22 -51.08 -289.20 187.09 180.41 -74.78

CURRENCIES FEBRUARY 2017 2016 2015 2014 2013 2012 2011

Dollar index 101.1 1.6% -1.1% 3.6% 9.3% 12.8% 0.3% -0.5% 1.5%

Euro 1.1 -2.1% 0.6% -3.2% -10.2% -12.0% 4.2% 1.8% -3.2%

Pound Sterling 1.2 -1.6% 0.3% -16.3% -5.4% -5.9% 1.9% 4.6% -0.4%

Swiss Franc 1.0 -1.6% 1.3% -1.6% -0.8% -10.2% 2.5% 2.6% -0.4%

Japanese Yen 112.8 0.0% 3.8% 2.8% -0.5% -12.1% -17.6% -11.3% 5.5%

Renminbi 6.9 0.0% 1.2% -6.6% -4.4% -2.4% 2.9% 1.1% 4.8%

Won 1,130.3 1.3% 6.3% -2.6% -7.0% -3.8% 1.0% 9.1% -3.2%

Brasilian Real 3.1 1.3% 4.6% 21.7% -33.0% -11.1% -13.2% -9.1% -11.0%

Indian Rupee 66.7 1.3% 1.9% -2.6% -4.5% -2.0% -11.0% -3.1% -15.8%

USD real effective exchange rate (Barclays) 138.0 -0.2% -1.7% 4.2% 7.9% 7.7% 1.4% -2.7% 1.7%

EUR real effective exchange rate (Barclays) 67.3 -2.7% -2.9% -1.2% -4.9% -3.8% 4.4% -1.9% -1.2%

JPY real effective exchange rate (Barclays) 128.8 -0.4% 1.2% 3.6% 4.9% -7.1% -17.5% -15.1% 2.5%

COMMODITIES FEBRUARY 2017 2016 2015 2014 2013 2012 2011

Global commodities, total return (S&P GSCI) USD 2,388.7 0.2% -1.2% 11.4% -32.9% -33.1% -1.2% 0.1% -1.2%

Agriculture, spot return USD 305.1 1.4% 4.8% 2.6% -12.1% -8.3% -22.1% 3.9% -14.9%

Energy, total return USD 413.5 -0.3% -4.9% 18.1% -41.5% -44.1% 5.1% -1.4% 4.9%

Crude oil USD 456.3 1.3% -1.9% 8.0% -45.3% -42.6% 6.0% -11.5% -1.3%

Industrial metals, total return USD 1,237.8 1.7% 10.3% 17.6% -24.5% -7.4% -12.9% 1.4% -22.3%

Copper USD 3,649.6 -0.4% 7.8% 17.3% -24.9% -12.7% -7.9% 4.3% -21.5%

Livestock, total return USD 1,793.9 1.3% 0.1% -7.3% -18.3% 14.2% -3.6% -4.0% -1.2%

Precious metals USD 1,541.1 3.7% 9.4% 8.4% -11.1% -4.1% -29.8% 6.2% 6.6%

Gold, total return USD 670.1 3.6% 8.7% 7.7% -10.9% -1.7% -28.7% 6.1% 9.6%

REAL ESTATE FEBRUARY 2017 2016 2015 2014 2013 2012 2011

All Equity REITS total returns (FTSE NAREIT) USD 16,581.0 4.0% 4.2% 8.6% 2.8% 28.0% 2.9% 19.7% 8.3%

FTSE EPRA NAREIT developed markets, total return USD 4,642.5 3.2% 3.8% 5.0% 0.1% 15.9% 4.4% 28.7% -5.8%

FTSE EPRA NAREIT emerging markets USD 2,170.4 6.3% 10.2% 0.2% 2.5% 15.1% -20.0% 36.1% -28.9%

New York home prices USD 185.3 0.0% 0.0% 2.8% 3.7% 2.8% 6.2% -0.3% -3.3%

Greater London house price (£) GBP 641,116.0 2.6% 4.1% -0.1% 9.9% 11.7% 10.6% 6.8% 6.4%

German house prices EUR 117.7 0.0% 1.4% 8.7% 1.7% 6.6% 3.5% 5.0% 8.4%

Moscow prop prices (US$/sqm) USD 2,846.0 2.2% 5.4% 3.6% -32.7% -24.8% -2.6% 6.0% 9.5%

Beijing property prices (RMB/sqm) RMB 39,771.0 0.0% 1.2% 32.6% 14.7% -3.2% 30.7% -7.9% 7.9%

HEDGE FUNDS FEBRUARY 2017 2016 2015 2014 2013 2012 2011

Global hedge funds USD 1,223.1 1.1% 1.6% 2.5% -3.6% -0.6% 6.7% 3.5% -8.9%

Equity hedge funds USD 1,178.9 1.2% 2.0% 0.1% -2.3% 1.4% 11.1% 4.8% -19.1%

Event-driven hedge funds USD 1,605.4 1.6% 2.6% 11.1% -6.9% -4.1% 13.9% 6.0% -4.9%

CTA funds USD 1,137.8 1.2% 0.2% -2.9% -2.0% 5.2% -1.8% -1.0% -4.9%

Credit hedge funds USD 1,999.2 0.8% 1.3% 5.0% -4.4% -1.8% 6.9% 7.7% -3.6%

Activist hedge funds USD 2,299.6 0.0% -0.2% 9.1% 0.2% 8.5% 19.2% 9.3% -16.9%

MONTHLY VIEWPOINT

From the Chief Investment Officer Marco E Pabst

07th

March 2017

ACPI Investments Ltd.

Pegasus House | 37-43 Sackville Street | London W1S 3EH

T +44 (0)20 3697 9580 | F +44 (0)20 3697 9501 | E [email protected]

www.acpi.com

15

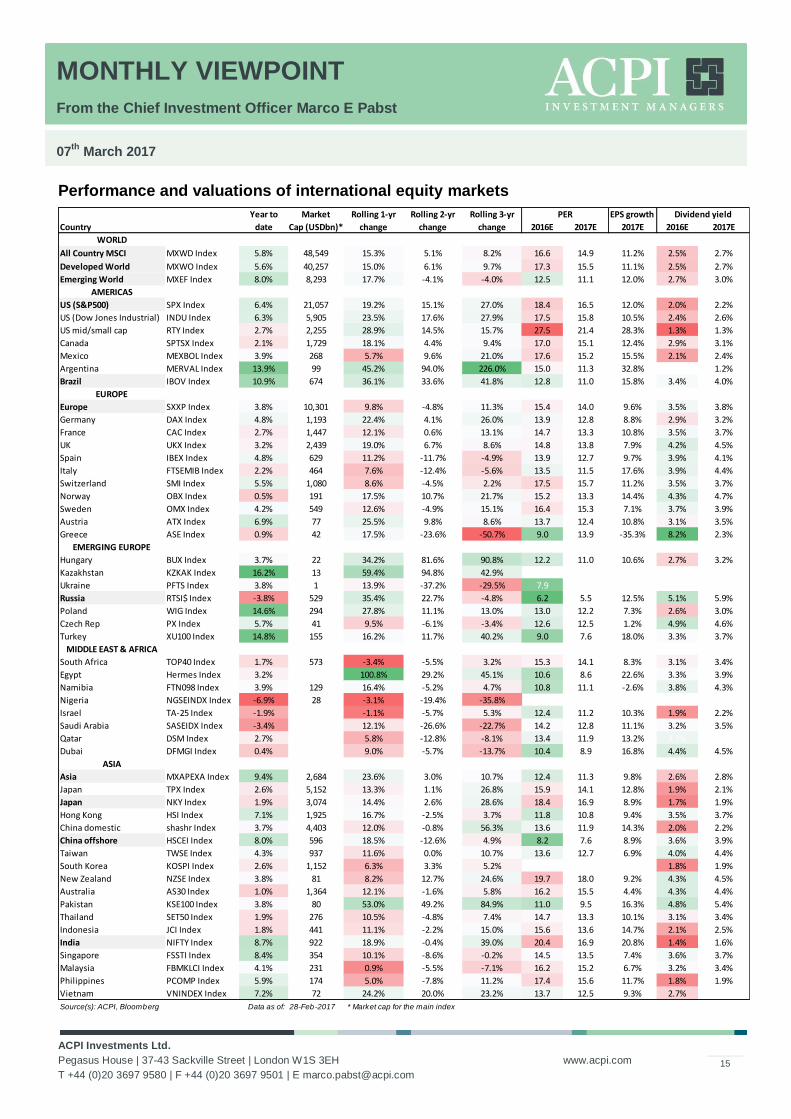

Performance and valuations of international equity markets

Year to Market Rolling 1-yr Rolling 2-yr Rolling 3-yr EPS growth

Country date Cap (USDbn)* change change change 2016E 2017E 2017E 2016E 2017E

WORLD

All Country MSCI MXWD Index 5.8% 48,549 15.3% 5.1% 8.2% 16.6 14.9 11.2% 2.5% 2.7%

Developed World MXWO Index 5.6% 40,257 15.0% 6.1% 9.7% 17.3 15.5 11.1% 2.5% 2.7%

Emerging World MXEF Index 8.0% 8,293 17.7% -4.1% -4.0% 12.5 11.1 12.0% 2.7% 3.0%

AMERICAS

US (S&P500) SPX Index 6.4% 21,057 19.2% 15.1% 27.0% 18.4 16.5 12.0% 2.0% 2.2%

US (Dow Jones Industrial) INDU Index 6.3% 5,905 23.5% 17.6% 27.9% 17.5 15.8 10.5% 2.4% 2.6%

US mid/small cap RTY Index 2.7% 2,255 28.9% 14.5% 15.7% 27.5 21.4 28.3% 1.3% 1.3%

Canada SPTSX Index 2.1% 1,729 18.1% 4.4% 9.4% 17.0 15.1 12.4% 2.9% 3.1%

Mexico MEXBOL Index 3.9% 268 5.7% 9.6% 21.0% 17.6 15.2 15.5% 2.1% 2.4%

Argentina MERVAL Index 13.9% 99 45.2% 94.0% 226.0% 15.0 11.3 32.8% 1.2%

Brazil IBOV Index 10.9% 674 36.1% 33.6% 41.8% 12.8 11.0 15.8% 3.4% 4.0%

EUROPE

Europe SXXP Index 3.8% 10,301 9.8% -4.8% 11.3% 15.4 14.0 9.6% 3.5% 3.8%

Germany DAX Index 4.8% 1,193 22.4% 4.1% 26.0% 13.9 12.8 8.8% 2.9% 3.2%

France CAC Index 2.7% 1,447 12.1% 0.6% 13.1% 14.7 13.3 10.8% 3.5% 3.7%

UK UKX Index 3.2% 2,439 19.0% 6.7% 8.6% 14.8 13.8 7.9% 4.2% 4.5%

Spain IBEX Index 4.8% 629 11.2% -11.7% -4.9% 13.9 12.7 9.7% 3.9% 4.1%

Italy FTSEMIB Index 2.2% 464 7.6% -12.4% -5.6% 13.5 11.5 17.6% 3.9% 4.4%

Switzerland SMI Index 5.5% 1,080 8.6% -4.5% 2.2% 17.5 15.7 11.2% 3.5% 3.7%

Norway OBX Index 0.5% 191 17.5% 10.7% 21.7% 15.2 13.3 14.4% 4.3% 4.7%

Sweden OMX Index 4.2% 549 12.6% -4.9% 15.1% 16.4 15.3 7.1% 3.7% 3.9%

Austria ATX Index 6.9% 77 25.5% 9.8% 8.6% 13.7 12.4 10.8% 3.1% 3.5%

Greece ASE Index 0.9% 42 17.5% -23.6% -50.7% 9.0 13.9 -35.3% 8.2% 2.3%

EMERGING EUROPE

Hungary BUX Index 3.7% 22 34.2% 81.6% 90.8% 12.2 11.0 10.6% 2.7% 3.2%

Kazakhstan KZKAK Index 16.2% 13 59.4% 94.8% 42.9%

Ukraine PFTS Index 3.8% 1 13.9% -37.2% -29.5% 7.9

Russia RTSI$ Index -3.8% 529 35.4% 22.7% -4.8% 6.2 5.5 12.5% 5.1% 5.9%

Poland WIG Index 14.6% 294 27.8% 11.1% 13.0% 13.0 12.2 7.3% 2.6% 3.0%

Czech Rep PX Index 5.7% 41 9.5% -6.1% -3.4% 12.6 12.5 1.2% 4.9% 4.6%

Turkey XU100 Index 14.8% 155 16.2% 11.7% 40.2% 9.0 7.6 18.0% 3.3% 3.7%

MIDDLE EAST & AFRICA

South Africa TOP40 Index 1.7% 573 -3.4% -5.5% 3.2% 15.3 14.1 8.3% 3.1% 3.4%

Egypt Hermes Index 3.2% 100.8% 29.2% 45.1% 10.6 8.6 22.6% 3.3% 3.9%

Namibia FTN098 Index 3.9% 129 16.4% -5.2% 4.7% 10.8 11.1 -2.6% 3.8% 4.3%

Nigeria NGSEINDX Index -6.9% 28 -3.1% -19.4% -35.8% 27.6%

Israel TA-25 Index -1.9% -1.1% -5.7% 5.3% 12.4 11.2 10.3% 1.9% 2.2%

Saudi Arabia SASEIDX Index -3.4% 12.1% -26.6% -22.7% 14.2 12.8 11.1% 3.2% 3.5%

Qatar DSM Index 2.7% 5.8% -12.8% -8.1% 13.4 11.9 13.2% 3.7% 4.0%

Dubai DFMGI Index 0.4% 9.0% -5.7% -13.7% 10.4 8.9 16.8% 4.4% 4.5%

ASIA

Asia MXAPEXA Index 9.4% 2,684 23.6% 3.0% 10.7% 12.4 11.3 9.8% 2.6% 2.8%

Japan TPX Index 2.6% 5,152 13.3% 1.1% 26.8% 15.9 14.1 12.8% 1.9% 2.1%

Japan NKY Index 1.9% 3,074 14.4% 2.6% 28.6% 18.4 16.9 8.9% 1.7% 1.9%

Hong Kong HSI Index 7.1% 1,925 16.7% -2.5% 3.7% 11.8 10.8 9.4% 3.5% 3.7%

China domestic shashr Index 3.7% 4,403 12.0% -0.8% 56.3% 13.6 11.9 14.3% 2.0% 2.2%

China offshore HSCEI Index 8.0% 596 18.5% -12.6% 4.9% 8.2 7.6 8.9% 3.6% 3.9%

Taiwan TWSE Index 4.3% 937 11.6% 0.0% 10.7% 13.6 12.7 6.9% 4.0% 4.4%

South Korea KOSPI Index 2.6% 1,152 6.3% 3.3% 5.2% 1.8% 1.9%

New Zealand NZSE Index 3.8% 81 8.2% 12.7% 24.6% 19.7 18.0 9.2% 4.3% 4.5%

Australia AS30 Index 1.0% 1,364 12.1% -1.6% 5.8% 16.2 15.5 4.4% 4.3% 4.4%

Pakistan KSE100 Index 3.8% 80 53.0% 49.2% 84.9% 11.0 9.5 16.3% 4.8% 5.4%

Thailand SET50 Index 1.9% 276 10.5% -4.8% 7.4% 14.7 13.3 10.1% 3.1% 3.4%

Indonesia JCI Index 1.8% 441 11.1% -2.2% 15.0% 15.6 13.6 14.7% 2.1% 2.5%

India NIFTY Index 8.7% 922 18.9% -0.4% 39.0% 20.4 16.9 20.8% 1.4% 1.6%

Singapore FSSTI Index 8.4% 354 10.1% -8.6% -0.2% 14.5 13.5 7.4% 3.6% 3.7%

Malaysia FBMKLCI Index 4.1% 231 0.9% -5.5% -7.1% 16.2 15.2 6.7% 3.2% 3.4%

Philippines PCOMP Index 5.9% 174 5.0% -7.8% 11.2% 17.4 15.6 11.7% 1.8% 1.9%

Vietnam VNINDEX Index 7.2% 72 24.2% 20.0% 23.2% 13.7 12.5 9.3% 2.7% #VALUE!

Source(s): ACPI, Bloomberg Data as of: 28-Feb-2017 * Market cap for the main index

PER Dividend yield

MONTHLY VIEWPOINT

From the Chief Investment Officer Marco E Pabst

07th

March 2017

ACPI Investments Ltd.

Pegasus House | 37-43 Sackville Street | London W1S 3EH

T +44 (0)20 3697 9580 | F +44 (0)20 3697 9501 | E [email protected]

www.acpi.com

16

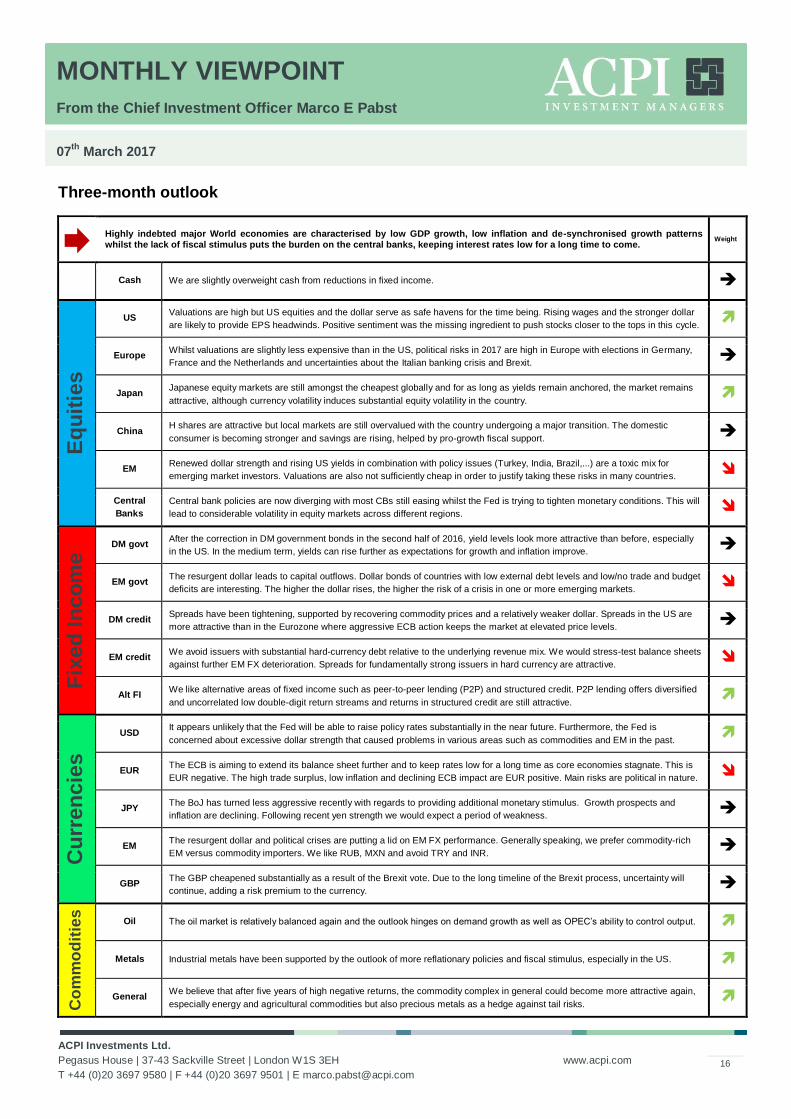

Three-month outlook

Highly indebted major World economies are characterised by low GDP growth, low inflation and de-synchronised growth patterns whilst the lack of fiscal stimulus puts the burden on the central banks, keeping interest rates low for a long time to come.

Weight

Cash We are slightly overweight cash from reductions in fixed income.

Eq

uit

ies

US Valuations are high but US equities and the dollar serve as safe havens for the time being. Rising wages and the stronger dollar

are likely to provide EPS headwinds. Positive sentiment was the missing ingredient to push stocks closer to the tops in this cycle.

Europe Whilst valuations are slightly less expensive than in the US, political risks in 2017 are high in Europe with elections in Germany,

France and the Netherlands and uncertainties about the Italian banking crisis and Brexit.

Japan Japanese equity markets are still amongst the cheapest globally and for as long as yields remain anchored, the market remains

attractive, although currency volatility induces substantial equity volatility in the country.

China H shares are attractive but local markets are still overvalued with the country undergoing a major transition. The domestic

consumer is becoming stronger and savings are rising, helped by pro-growth fiscal support.

EM Renewed dollar strength and rising US yields in combination with policy issues (Turkey, India, Brazil,...) are a toxic mix for

emerging market investors. Valuations are also not sufficiently cheap in order to justify taking these risks in many countries.

Central

Banks

Central bank policies are now diverging with most CBs still easing whilst the Fed is trying to tighten monetary conditions. This will

lead to considerable volatility in equity markets across different regions.

Fix

ed

In

co

me DM govt

After the correction in DM government bonds in the second half of 2016, yield levels look more attractive than before, especially

in the US. In the medium term, yields can rise further as expectations for growth and inflation improve.

EM govt The resurgent dollar leads to capital outflows. Dollar bonds of countries with low external debt levels and low/no trade and budget

deficits are interesting. The higher the dollar rises, the higher the risk of a crisis in one or more emerging markets.

DM credit Spreads have been tightening, supported by recovering commodity prices and a relatively weaker dollar. Spreads in the US are

more attractive than in the Eurozone where aggressive ECB action keeps the market at elevated price levels.