Alternatives Exposure

for DC Participants

John CorcoranSenior Client Portfolio Manager,

Global Multi-Asset Group

2 For Institutional Use Only

Defined Contribution Dilemma

Balancing simplicity versus diversity

Adding flexibility to the line-up

Allowing for some participant

customization

Solutions focused on objectives

Alternative exposure can

improve client outcomes

3 For Institutional Use Only

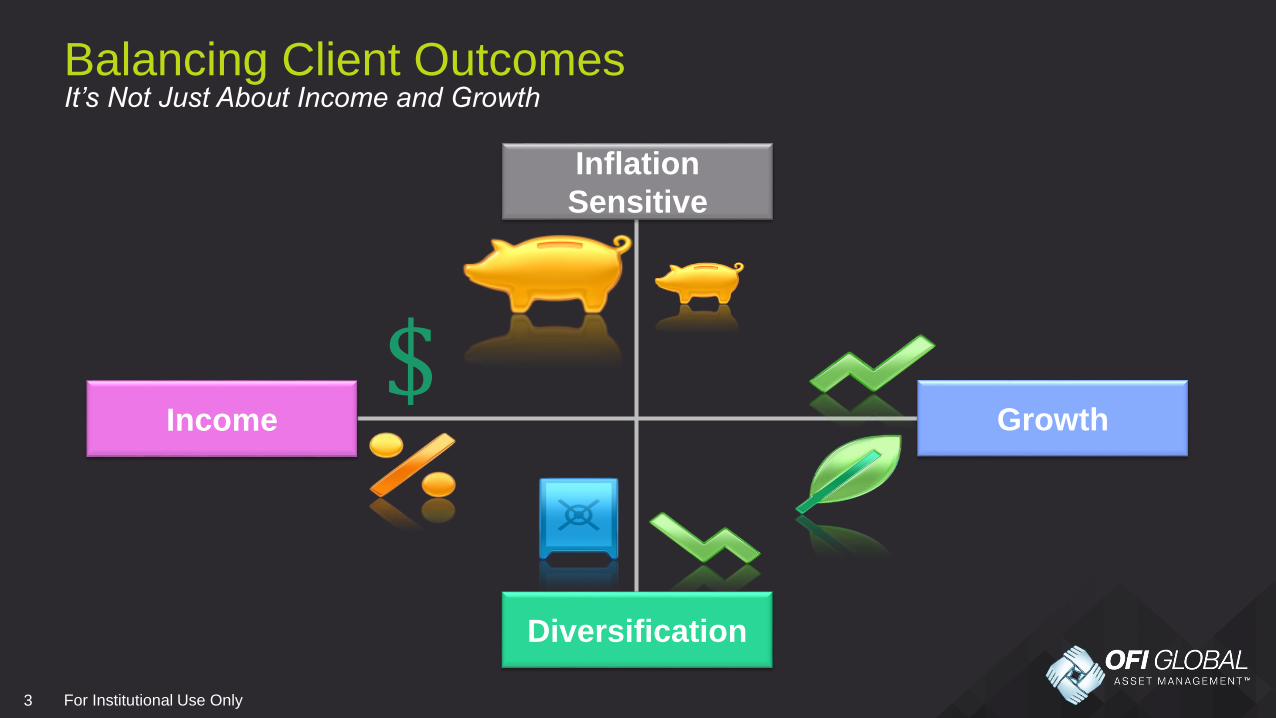

It’s Not Just About Income and GrowthBalancing Client Outcomes

Inflation

Sensitive

$Income Growth

Diversification

4 For Institutional Use Only

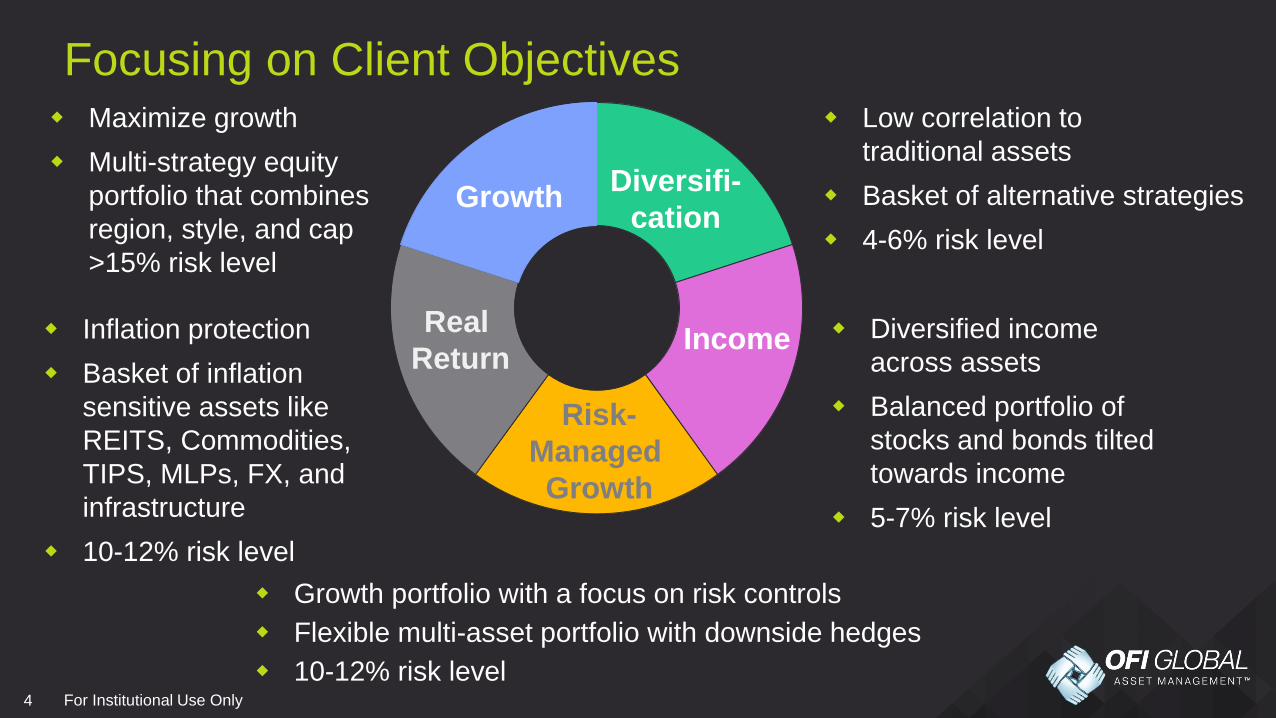

Focusing on Client Objectives

Real

Return

Diversifi-

cation

Income

Risk-

Managed

Growth

Growth

Maximize growth

Multi-strategy equity

portfolio that combines

region, style, and cap

>15% risk level

Inflation protection

Basket of inflation

sensitive assets like

REITS, Commodities,

TIPS, MLPs, FX, and

infrastructure

10-12% risk level

Low correlation to

traditional assets

Basket of alternative strategies

4-6% risk level

Growth portfolio with a focus on risk controls

Flexible multi-asset portfolio with downside hedges

10-12% risk level

Diversified income

across assets

Balanced portfolio of

stocks and bonds tilted

towards income

5-7% risk level

5 For Institutional Use Only

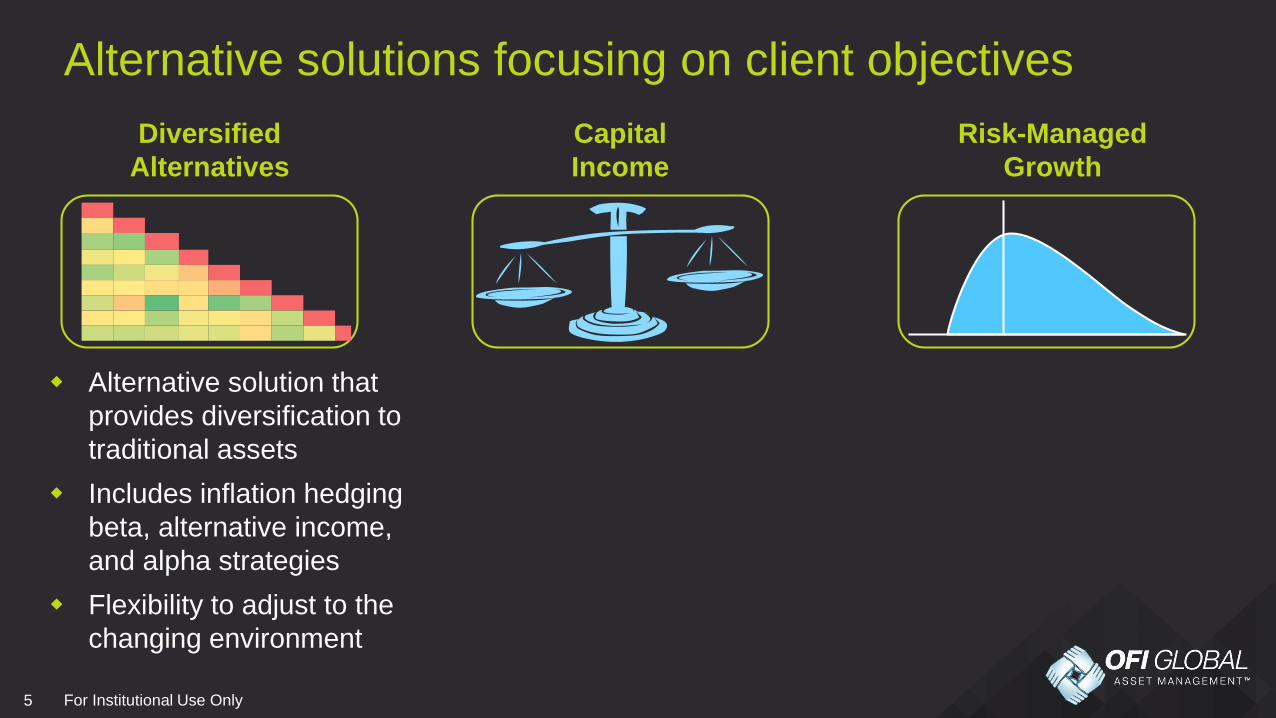

Alternative solutions focusing on client objectives

Alternative solution that

provides diversification to

traditional assets

Includes inflation hedging

beta, alternative income,

and alpha strategies

Flexibility to adjust to the

changing environment

Risk-Managed

Growth

Capital

Income

Diversified

Alternatives

6 For Institutional Use Only

Source of chart data: Bloomberg, Factset, 12/31/13. MLPs are represented by the Alerian MLP Index. Gold is represented by the spot price of one

troy ounce. REITs are represented by the FTSE NAREIT Equity REITs Index. Commodities are represented by the S&P GSCI Commodity Index.

Foreign Currencies are represented by a trade-weighted basket of currencies of the 16 largest trading partners of the U.S., determined by 2000 trade

data. Multi Strategy is represented by the HFRI RV Multi Strategy Index. U.S. Equity is represented by the S&P 500 Index. U.S. Bonds are

represented by the Barclays Capital U.S. Aggregate Bond Index. Leveraged loans are represented by the CS Leveraged Loan Index. Cat bonds are

represented by the Swiss RE Global Catastrophe Bond Index. See page 27 for Index definitions. The indices shown are unmanaged and cannot be

purchased directly by investors. Index performance is shown for illustrative purposes only and does not predict or depict the performance of any

Oppenheimer fund. Diversification does not guarantee profit or protect against loss. Past performance does not guarantee future results.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013Cum. Total

Return

Avg. Annual

Return

REITs

31.58

Commodities

25.55

REITs

35.06

Commodities

32.67

Gold

5.77

MLPs

76.41

MLPs

35.85

MLPs

13.88

REITs

18.06

U.S. Equity

32.39

MLPs

301.30

MLPs

14.89

Commodities

17.28

Gold

17.92

MLPs

26.07

Gold

30.98

U.S. Bonds

5.24

Leveraged Loans

44.87

Gold

29.52

Gold

10.06

U.S. Equity

16.00

MLPs

27.59

Gold

190.20

Gold

11.24

MLPs

16.67

REITs

12.16

Gold

23.15

Cat Bonds

15.44

Cat Bonds

2.45

REITs

27.99

REITs

27.96

REITs

8.29

Cat Bonds

10.28

Cat Bonds

10.91

Cat Bonds

129.19

Cat Bonds

8.64

U.S. Equity

10.88

MLPs

6.32

U.S. Equity

15.79

MLPs

12.72

Multi Strategy

-2.92

U.S. Equity

26.46

U.S. Equity

15.06

U.S. Bonds

7.84

Leveraged Loans

9.43

Multi Strategy

7.77

REITs

124.53

REITs

8.42

Multi Strategy

8.20

Leveraged Loans

5.69

Multi Strategy

12.90

Multi Strategy

11.05

Foreign Currencies

-7.03

Gold

24.36

Cat Bonds

11.13

Cat Bonds

3.73

Multi Strategy

8.18

Leveraged Loans

6.15

U.S. Equity

104.21

U.S. Equity

7.39

Cat Bonds

6.56

Multi Strategy

5.47

Cat Bonds

12.02

Foreign Currencies

7.73

Leveraged Loans

-28.75

Multi Strategy

16.17

Leveraged Loans

9.98

U.S. Equity

2.11

Gold

7.19

REITs

2.54

Leveraged Loans

63.86

Leveraged Loans

5.06

Leveraged Loans

5.60

U.S. Equity

4.91

Leveraged Loans

7.33

U.S. Bonds

6.97

MLPs

-36.91

Commodities

13.48

Commodities

9.03

Leveraged Loans

1.82

MLPs

4.80

Commodities

-1.22

Multi

Strategy

62.59

Multi

Strategy

4.98

Foreign Currencies

5.60

U.S. Bonds

2.43

U.S. Bonds

4.33

U.S. Equity

5.49

U.S. Equity

-37.00

Cat Bonds

13.39

U.S. Bonds

6.54

Multi Strategy

-0.33

U.S. Bonds

4.21

U.S. Bonds

-2.02

U.S. Bonds

55.99

U.S. Bonds

4.54

Gold

5.54

Cat Bonds

1.62

Foreign Currencies

3.92

Leveraged Loans

1.88

REITs

-37.73

U.S. Bonds

5.93

Multi Strategy

4.15

Commodities

-1.18

Foreign Currencies

1.14

Foreign Currencies

-3.58

Foreign Currencies

9.30

Foreign Currencies

0.89

U.S. Bonds

4.34

Foreign Currencies

-4.74

Commodities

-15.09

REITs

-15.69

Commodities

-46.49

Foreign Currencies

5.04

Foreign Currencies

3.87

Foreign Currencies

-1.7

Commodities

0.08

Gold

-28.83

Commodities

7.29

Commodities

0.71

Diversified Alternatives:

Expanding Sources of Return

7 For Institutional Use Only

Real Estate

Gold

Commodities

MLP's

Event-LinkedBonds

ShortDuration

Currencies

Leveraged Loans

Global Macro

Volatility

Relative Value

Long/Short Credit

Equity Hedge

Equity MarketNeutral

Combining Alpha and Beta Alternatives

Alpha Alternatives

Real Assets

Income Alternatives

8 For Institutional Use Only

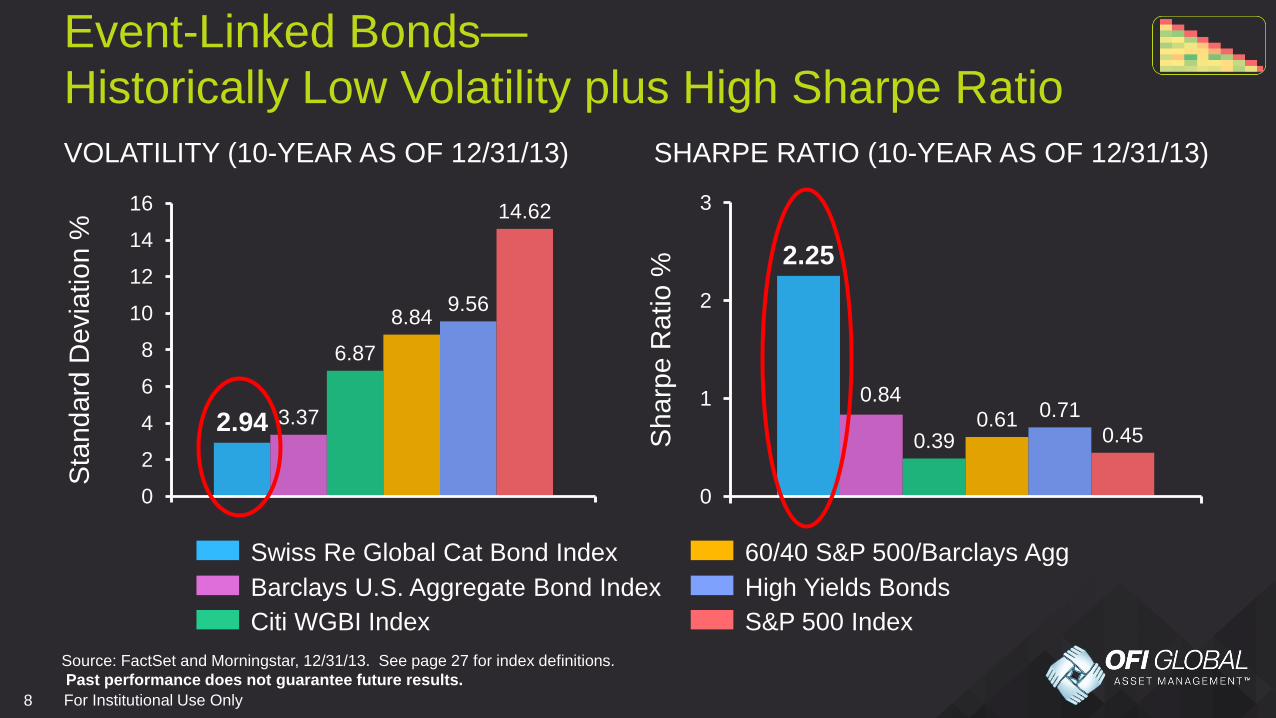

2.94 3.37

6.87

8.849.56

14.62

0

2

4

6

8

10

12

14

16

Source: FactSet and Morningstar, 12/31/13. See page 27 for index definitions.

Past performance does not guarantee future results.

Event-Linked Bonds—

Historically Low Volatility plus High Sharpe RatioS

tandard

Devia

tion %

2.25

0.84

0.390.61 0.71

0.45

0

1

2

3

Sharp

e R

atio %

SHARPE RATIO (10-YEAR AS OF 12/31/13)VOLATILITY (10-YEAR AS OF 12/31/13)

Swiss Re Global Cat Bond Index

Barclays U.S. Aggregate Bond Index

Citi WGBI Index

60/40 S&P 500/Barclays Agg

High Yields Bonds

S&P 500 Index

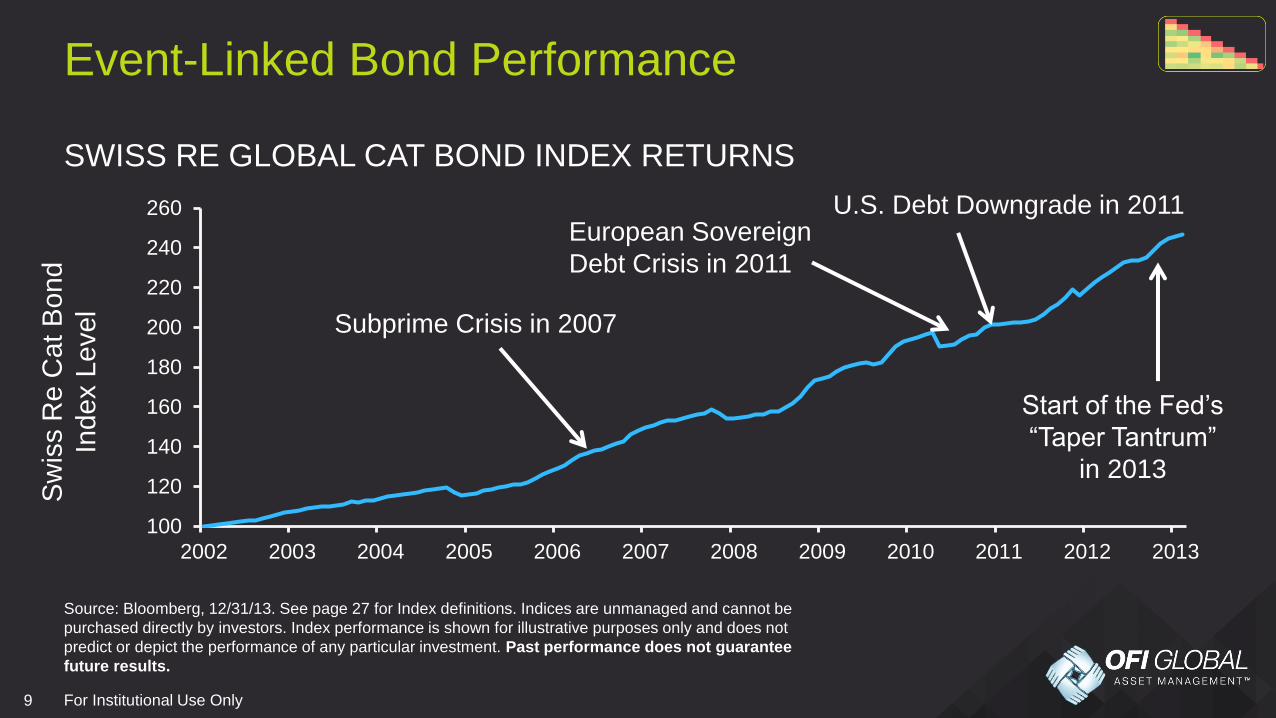

9 For Institutional Use Only

SWISS RE GLOBAL CAT BOND INDEX RETURNS

Event-Linked Bond Performance

Source: Bloomberg, 12/31/13. See page 27 for Index definitions. Indices are unmanaged and cannot be

purchased directly by investors. Index performance is shown for illustrative purposes only and does not

predict or depict the performance of any particular investment. Past performance does not guarantee

future results.

100

120

140

160

180

200

220

240

260

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Sw

iss R

e C

at

Bond

Index L

evel

European Sovereign

Debt Crisis in 2011

Start of the Fed’s

“Taper Tantrum”

in 2013

Subprime Crisis in 2007

U.S. Debt Downgrade in 2011

10 For Institutional Use Only

Alerian MLP Index Total Return (AMZX)

Performance in Periods of Rising Interest Rates

*Indicates the increase in interest rates in terms of basis points for each time period.

An investor cannot invest directly in an index. They are unmanaged and shown for illustrative purposes only. Please see

page 27 for index definitions. Past performance does not guarantee future results.

Source: Bloomberg, Alerian Capital Management, Barclays Research estimates. As of 6/30/2013.

1,600

1,400

1,200

1,000

800

600

400

200

0

Jan

-96

Jan

-97

Jan

-98

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Ja

n-0

8

Jan

-09

Jan

-10

Ja

n-1

1

Jan

-12

Jan

-13

Jan

-99

AMZX

+5%

AMZX

-3%AMZX

-4%

AMZX

+54%

AMZX

+30%

AMZX

+11%

AMZX

+23%

+145 bps*

+249 bps*

+112 bps*

+213 bps*

+175 bps*

+134 bps*

+108 bps*

11 For Institutional Use Only

Diversified Alternatives

Inflation Sensitive

Growth

Diversification

Income

Diversified Alternatives

60/40 Balanced Portfolio

Chart is for illustrative purposes only and is not meant to predict or depict the performance of

any asset category or any investment. Past performance does not guarantee future results.

12 For Institutional Use Only

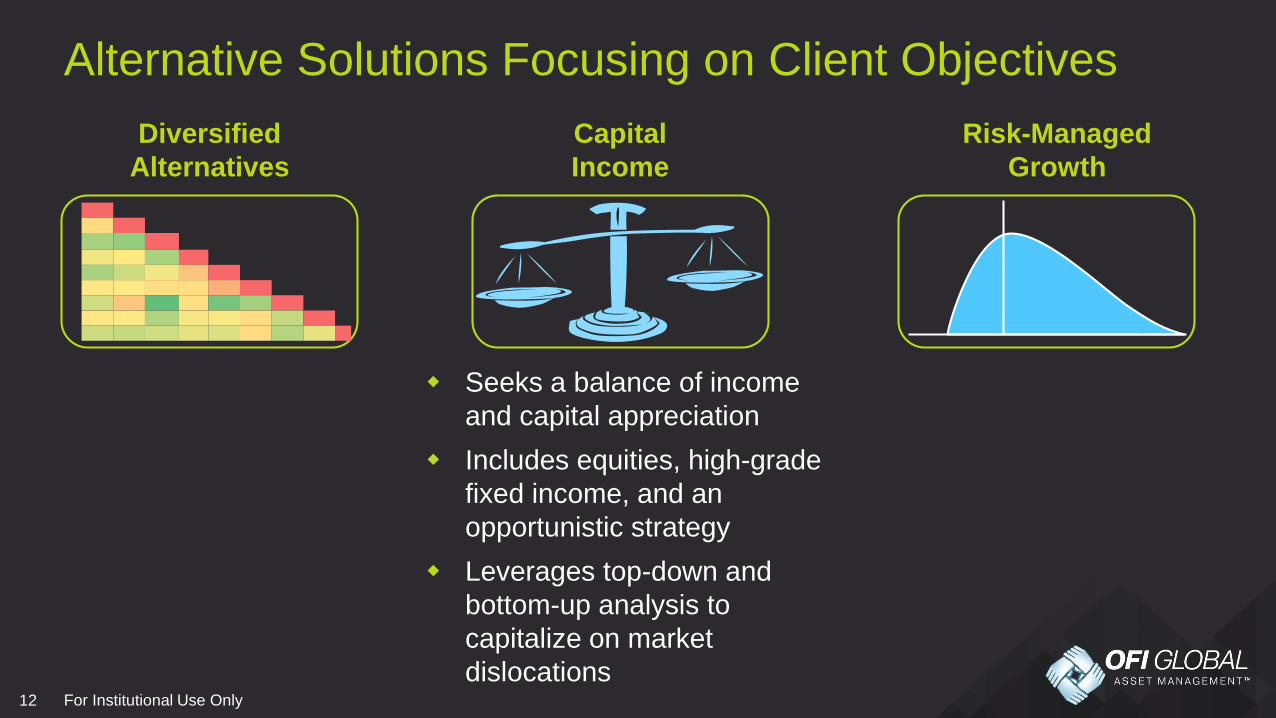

Alternative Solutions Focusing on Client Objectives

Risk-Managed

Growth

Capital

Income

Diversified

Alternatives

Seeks a balance of income

and capital appreciation

Includes equities, high-grade

fixed income, and an

opportunistic strategy

Leverages top-down and

bottom-up analysis to

capitalize on market

dislocations

13 For Institutional Use Only

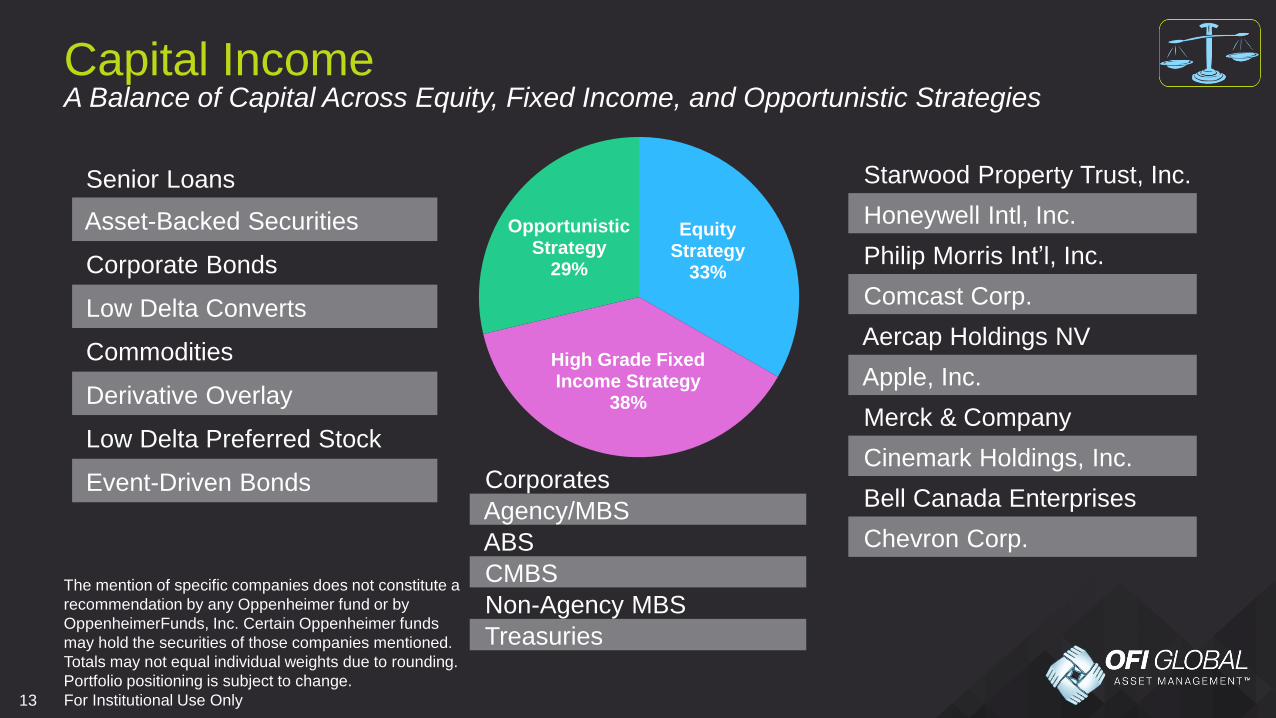

A Balance of Capital Across Equity, Fixed Income, and Opportunistic StrategiesCapital Income

The mention of specific companies does not constitute a

recommendation by any Oppenheimer fund or by

OppenheimerFunds, Inc. Certain Oppenheimer funds

may hold the securities of those companies mentioned.

Totals may not equal individual weights due to rounding.

Portfolio positioning is subject to change.

Equity Strategy

33%

High Grade Fixed Income Strategy

38%

OpportunisticStrategy

29%

Senior Loans

Asset-Backed Securities

Corporate Bonds

Low Delta Converts

Commodities

Derivative Overlay

Low Delta Preferred Stock

Event-Driven Bonds

Starwood Property Trust, Inc.

Honeywell Intl, Inc.

Philip Morris Int’l, Inc.

Comcast Corp.

Aercap Holdings NV

Apple, Inc.

Merck & Company

Cinemark Holdings, Inc.

Bell Canada Enterprises

Chevron Corp.

Corporates

Agency/MBS

ABS

CMBS

Non-Agency MBS

Treasuries

14 For Institutional Use Only

3-YEAR RISK/RETURN (AS OF 12/31/13)

Capital Income: Risk/Return Profile

Source of chart data: Morningstar, 12/31/13.

Past performance does not guarantee future results.

Funds listed above include Oppenheimer Capital Income Fund: OPPEX; Federated Capital Income: CAPAX; Franklin Income:

FKINX; Goldman Sachs Income Builder: GSBFX; Hartford Balanced Income: HBLAX; James Balanced:

Golden Rainbow: GLRBX; JP Morgan Income Builder: JNBAX; MFS Diversified Income: DIFAX;

Principal Diversified Real Asset: PRDAX; Principal Global Diversified: PGBAX. See slide 27

for index definitions.

Annualized Standard Deviation %

-1

1

3

5

7

9

11

13

15

17

0 2 4 6 8 10 12

Annua

lized R

etu

rn

%

Capital

Income

Morningstar Conservative

Allocation Category Avg.

High Risk /Low Reward

Low Risk /High

Reward

S&P 500 Index

Barclays U.S. Aggregate Bond Index

Competitors

15 For Institutional Use Only

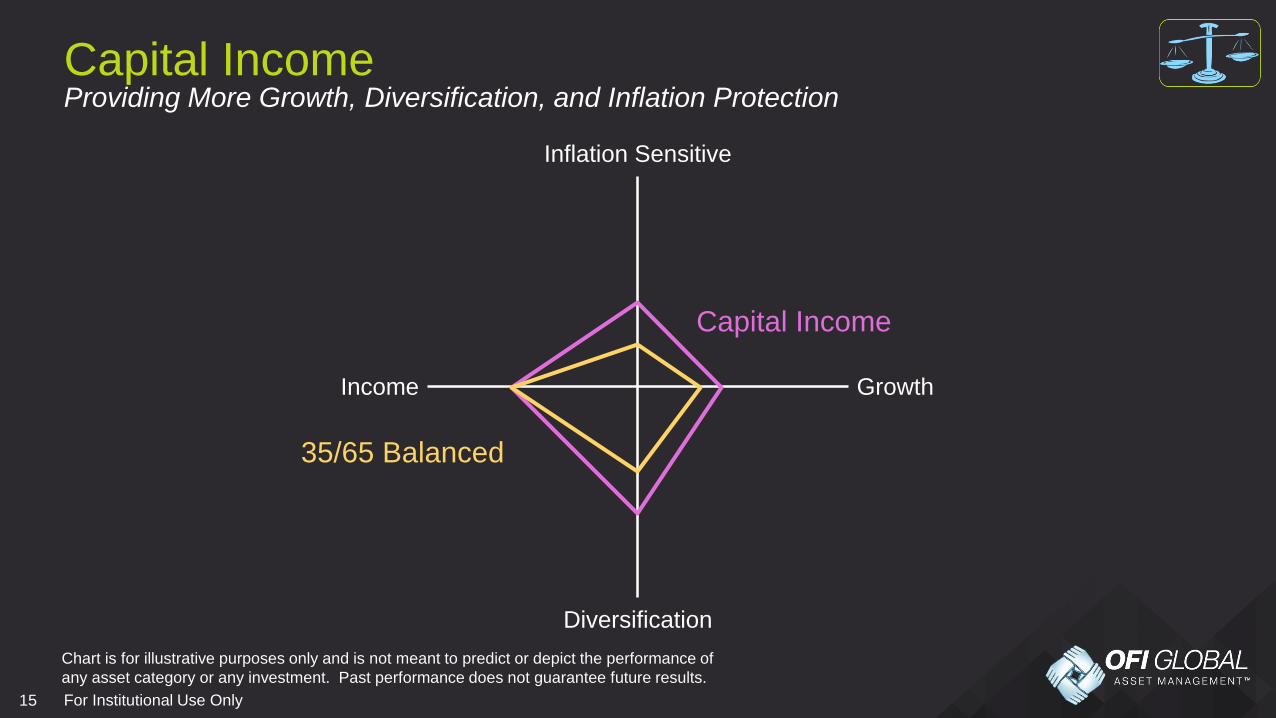

Providing More Growth, Diversification, and Inflation ProtectionCapital Income

Inflation Sensitive

Growth

Diversification

Income

Capital Income

35/65 Balanced

Chart is for illustrative purposes only and is not meant to predict or depict the performance of

any asset category or any investment. Past performance does not guarantee future results.

16 For Institutional Use Only

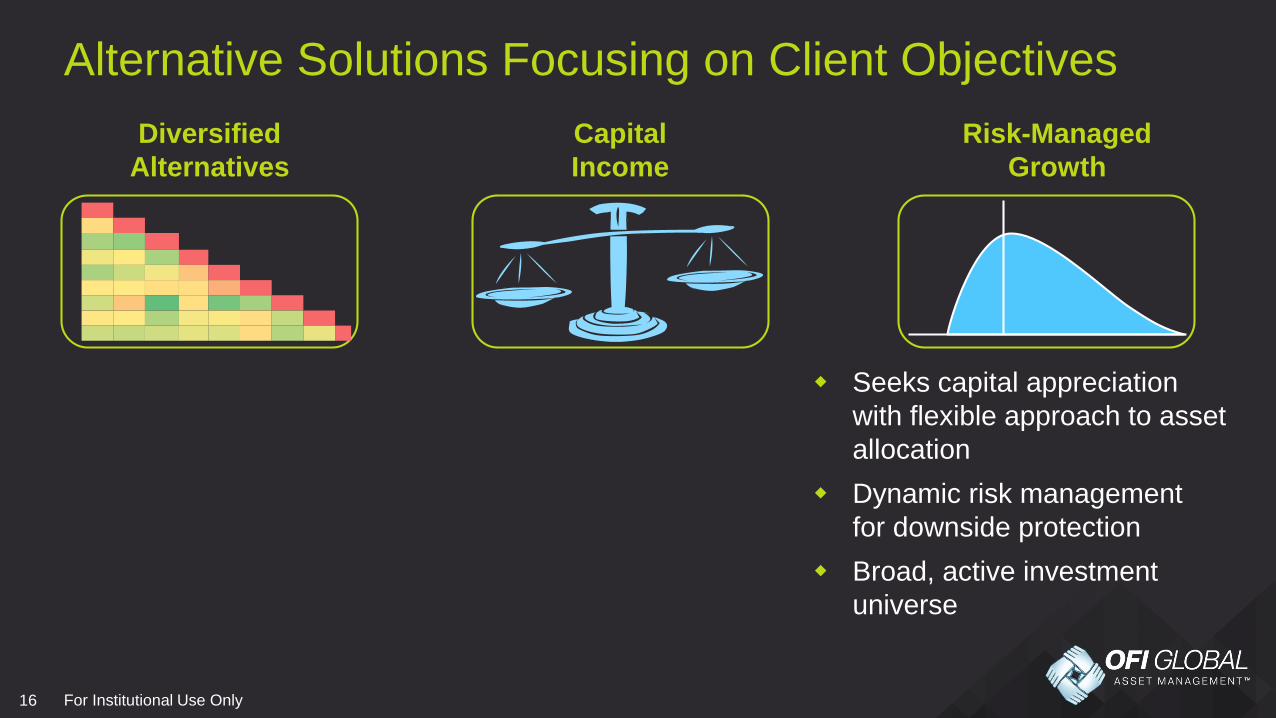

Alternative Solutions Focusing on Client Objectives

Risk-Managed

Growth

Capital

Income

Diversified

Alternatives

Seeks capital appreciation

with flexible approach to asset

allocation

Dynamic risk management

for downside protection

Broad, active investment

universe

17 For Institutional Use Only

Global Equity

Dividend Equity

International Growth Equity

U.S. Large Cap Growth

Small Cap Growth

Emerging Market Equity

High Yield

Leveraged Loans

Mortgages

Event Linked Bonds

Hedges

Cash

Flexible Portfolio Focused on Capital Appreciation

Holdings are subject to change, and are dollar weighted based on total net assets. Negative weightings

may result from the use of leverage. Leverage involves the use of various financial instruments or

borrowed capital in an attempt to increase investment return. Leverage risks include potential for higher

volatility, greater decline of the fund’s net asset value and fluctuations of dividends and distributions paid

by the fund.

Risk-Managed Growth

ASSET WEIGHT

Equity 62.8

Credit 18.0

MBS 6.9

Event Linked 7.0

Hedges 1.9

Cash 3.4

18 For Institutional Use Only

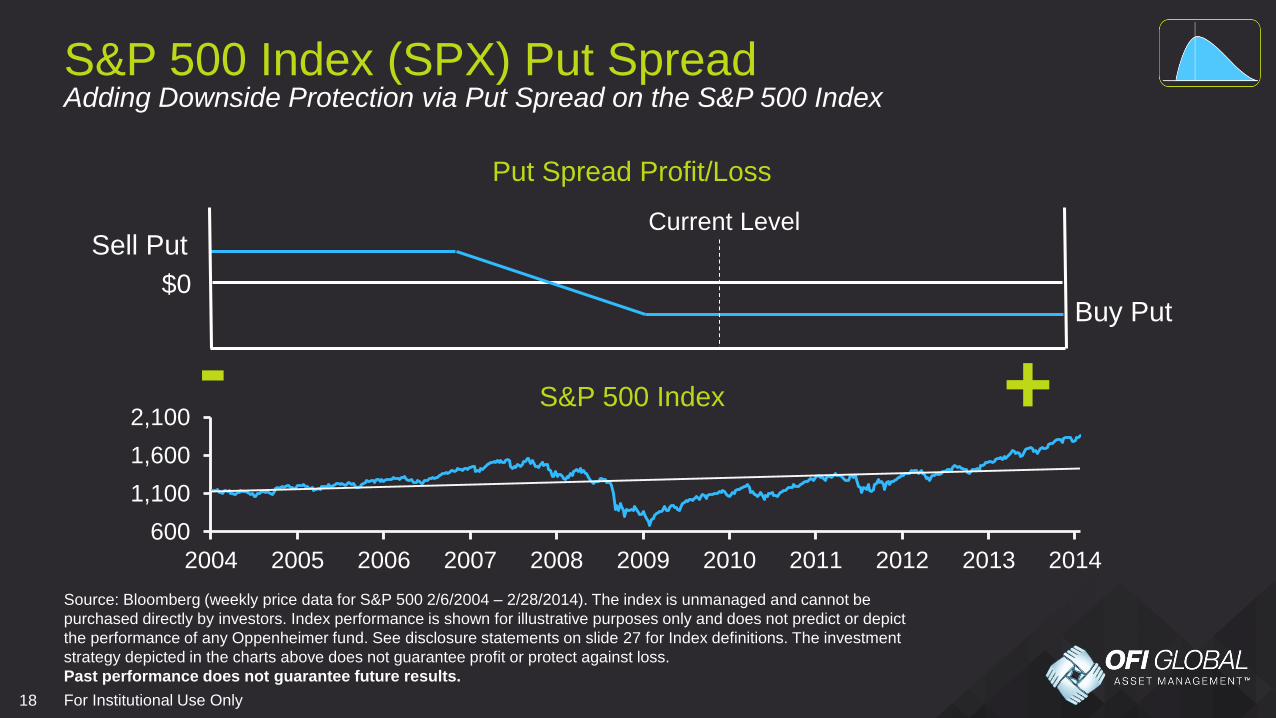

Adding Downside Protection via Put Spread on the S&P 500 IndexS&P 500 Index (SPX) Put Spread

Sell Put

Buy Put$0

Current Level

+-

600

1,100

1,600

2,100

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Source: Bloomberg (weekly price data for S&P 500 2/6/2004 – 2/28/2014). The index is unmanaged and cannot be

purchased directly by investors. Index performance is shown for illustrative purposes only and does not predict or depict

the performance of any Oppenheimer fund. See disclosure statements on slide 27 for Index definitions. The investment

strategy depicted in the charts above does not guarantee profit or protect against loss.

Past performance does not guarantee future results.

Put Spread Profit/Loss

S&P 500 Index

19 For Institutional Use Only

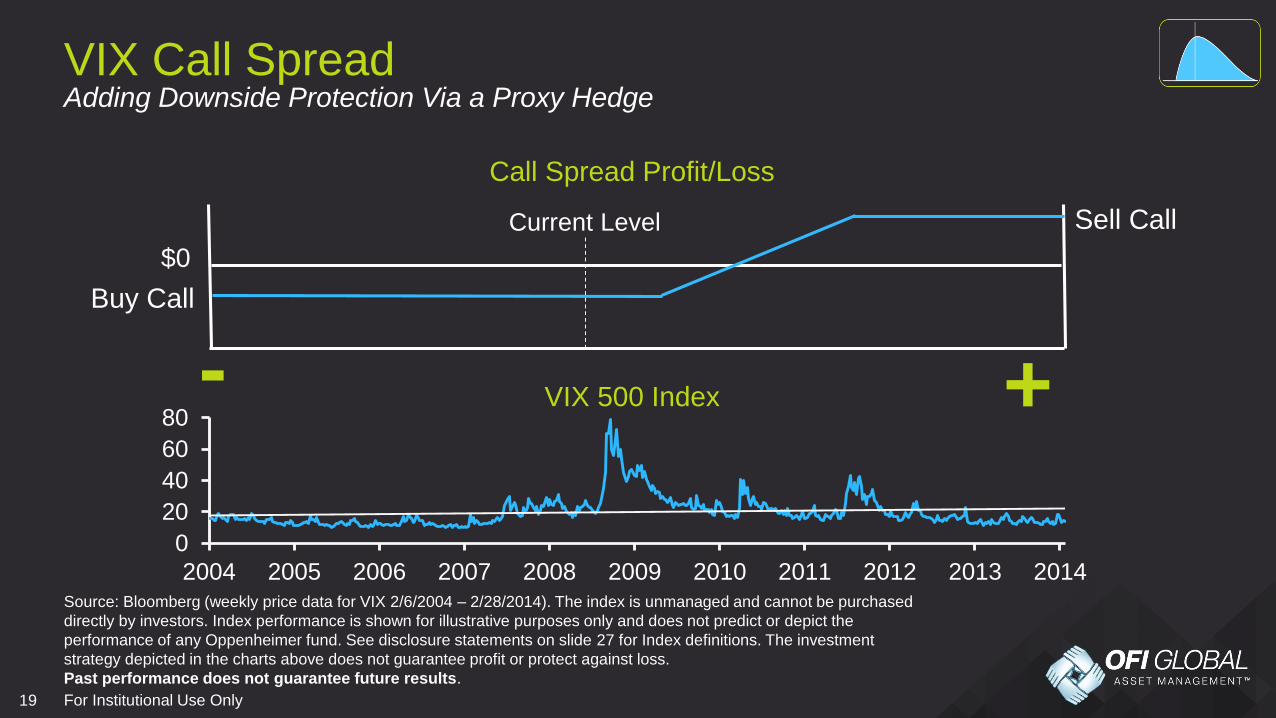

Adding Downside Protection Via a Proxy Hedge VIX Call Spread

Source: Bloomberg (weekly price data for VIX 2/6/2004 – 2/28/2014). The index is unmanaged and cannot be purchased

directly by investors. Index performance is shown for illustrative purposes only and does not predict or depict the

performance of any Oppenheimer fund. See disclosure statements on slide 27 for Index definitions. The investment

strategy depicted in the charts above does not guarantee profit or protect against loss.

Past performance does not guarantee future results.

Buy Call

Sell Call

$0

Current Level

+-

Call Spread Profit/Loss

VIX 500 Index

0

20

40

60

80

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

20 For Institutional Use Only

Scenario Stress Tests are Used to Identify Unwanted Risks

RISK-MANAGED GROWTH PORTFOLIO BEFORE AND AFTER HEDGE

Source: RiskMetrics and OFI analysis. The chart above is shown for illustrative purposes only and does not predict

or depict the performance of any Oppenheimer fund. See disclosure statements on slide 27 for Index definitions.

The investment strategy depicted in the chart above does not guarantee profit or protect against loss. Past

performance does not guarantee future results.

Adding Convexity Through Hedges

-30%

-20%

-10%

0%

10%

20%

30%

40%

-30% -20% -10% 0% 10% 20% 30%

Tota

l R

etu

rn

S&P 500 Shocks

Before Hedge After Hedge

21 For Institutional Use Only

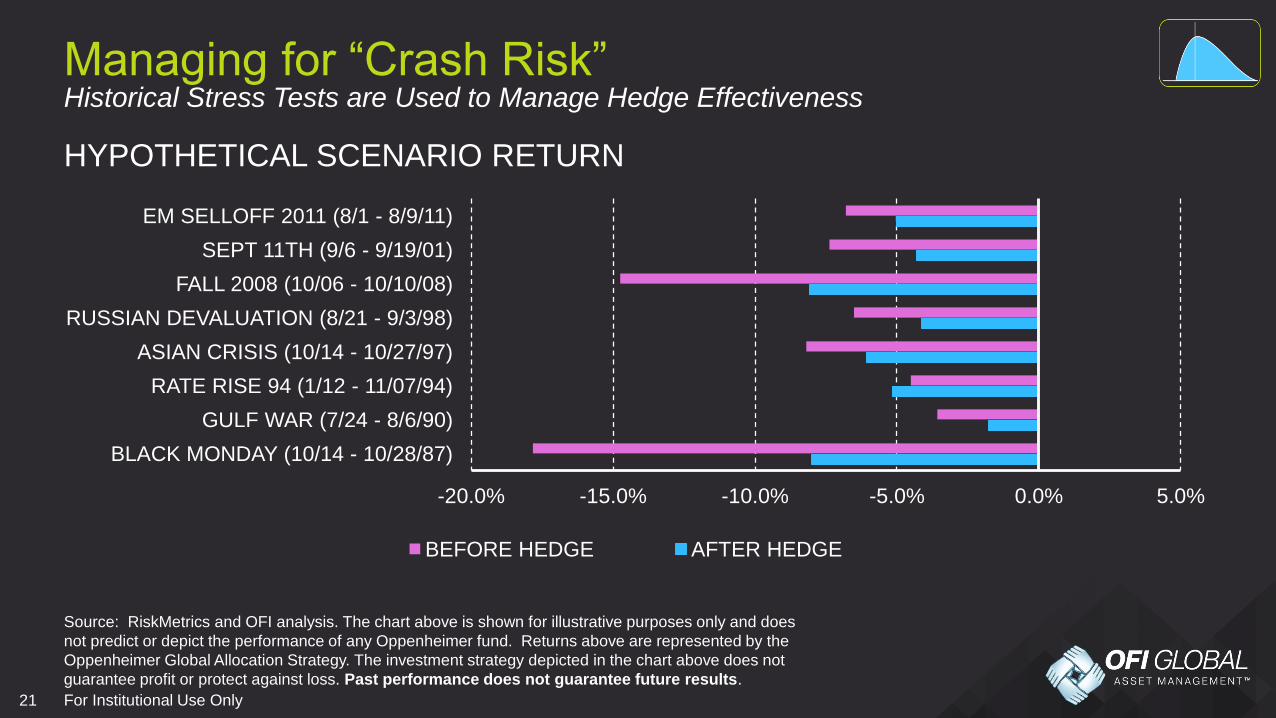

Historical Stress Tests are Used to Manage Hedge Effectiveness

HYPOTHETICAL SCENARIO RETURN

Managing for “Crash Risk”

-20.0% -15.0% -10.0% -5.0% 0.0% 5.0%

BLACK MONDAY (10/14 - 10/28/87)

GULF WAR (7/24 - 8/6/90)

RATE RISE 94 (1/12 - 11/07/94)

ASIAN CRISIS (10/14 - 10/27/97)

RUSSIAN DEVALUATION (8/21 - 9/3/98)

FALL 2008 (10/06 - 10/10/08)

SEPT 11TH (9/6 - 9/19/01)

EM SELLOFF 2011 (8/1 - 8/9/11)

BEFORE HEDGE AFTER HEDGE

Source: RiskMetrics and OFI analysis. The chart above is shown for illustrative purposes only and does

not predict or depict the performance of any Oppenheimer fund. Returns above are represented by the

Oppenheimer Global Allocation Strategy. The investment strategy depicted in the chart above does not

guarantee profit or protect against loss. Past performance does not guarantee future results.

22 For Institutional Use Only

Return Shaping Used to Reduce “Crash Risk”Dynamic risk management

Low Cost Hedges to

Reduce Downside Risk Typical Distribution

of Portfolio Returns

Return

Shaping

Chart is for illustrative purposes only and is not meant to predict or depict the performance of any asset

category or any investment. Past performance does not guarantee future results.

23 For Institutional Use Only

Adding Diversification Through Downside HedgesRisk-Managed Growth

60/40 Balanced

Inflation Sensitive

Growth

Diversification

Income

Risk-Managed Growth

Chart is for illustrative purposes only and is not meant to predict or depict the performance of

any asset category or any investment. Past performance does not guarantee future results.

24 For Institutional Use Only

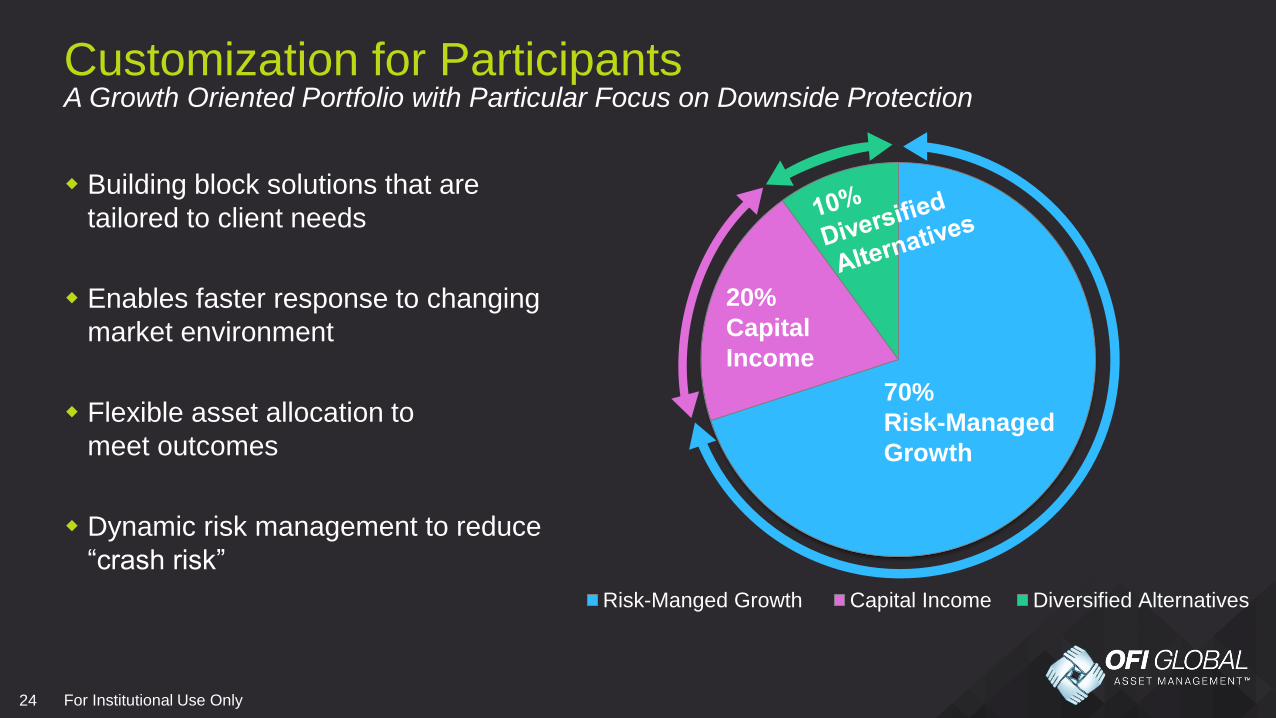

Customization for Participants

Risk-Manged Growth Capital Income Diversified Alternatives

A Growth Oriented Portfolio with Particular Focus on Downside Protection

Building block solutions that are

tailored to client needs

Enables faster response to changing

market environment

Flexible asset allocation to

meet outcomes

Dynamic risk management to reduce

“crash risk”

70%

Risk-Managed

Growth

20%

Capital

Income

25 For Institutional Use Only

Objective Portfolios Keeping Pace with Target Dates

Diversification

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

3/6/201410/17/20135/30/20131/10/2013

Similar Risk Profile as a Target Date 2015 Index

12/31/12 – 3/6/14 CUMULATIVE PERFORMANCE

Flexible Objective Target Date 2015

Chart is for illustrative purposes only and is not meant to predict or depict the performance of any asset category or any

investment. “Flexible Objective” is represented by 70% Risk Managed Growth, 20% Capital Income and 10% Diversified

Alternatives. “Target Date 2015” is represented by the Vanguard Target Date 2015 Fund. Past performance does not

guarantee future results.

26 For Institutional Use Only

Key Takeaways

Adding alternative exposure increases breadth to manage additional

client dimensions

Bundled solutions focused on income, growth or diversification can

be a simple way to add diversity to a line-up

Alternatives include both alpha and beta exposures, and the

management of risk is as important as security selection

Objective approach can enhance flexibility and provide participants

with some customization

27 For Institutional Use Only

Definitions The S&P 500 Index is a free-float capitalization-weighted index of the prices of 500 large-cap common stocks actively traded in the United States.

The MSCI AC World ex-U.S. Index is designed to measure the equity market performance of developed and emerging markets and excludes the U.S. The index is unmanaged and cannot be purchased directly by investors.

The MSCI Emerging Markets Index is designed to measure the equity market performance of emerging markets. The index is unmanaged, includes the reinvestment of dividends and cannot be purchased directly by investors.

The Barclays U.S. Aggregate Bond Index is an investment-grade domestic bond index. The index is unmanaged and cannot be purchased directly by investors.

The EMBI+ tracks returns for actively traded external debt instruments in emerging market, and is also J.P. Morgan's most liquid U.S-dollar emerging markets debt benchmark. The index segments further the universe of emerging markets as defined by the broader EMBI Global and EMBI Global Diversified, by placing a strict liquidity requirement rule for inclusion. Included in the EMBI+ are US-dollar denominated Brady bonds, Eurobonds, and traded loans issued by sovereign entities.

JPM GABI consists of the JPM GABI US, a U.S. dollar denominated, investment-grade index spanning asset classes from developed to emerging markets, and the JPM GABI extends the U.S. index to also include multi-currency, investment-grade instruments.

The FTSE National Association of Real Estate Investment Trusts (NAREIT) Equity Index consists of certain companies that own and operate income-producing real estate that have 75% or more of their respective gross invested assets in the equity or mortgage debt of commercial properties. The index is unmanaged, includes the reinvestment of dividends and cannot be purchased directly by investors.

The Alerian MLP Index is a market-cap weighted, float-adjusted index created to provide a comprehensive benchmark for investors to track the performance of the energy MLP sector.

The Credit Suisse Leveraged Loan Index is a composite index of senior loan returns representing an unleveraged investment in senior loans that is broadly based across the spectrum of senior bank loans and includes reinvestment of income.

The S&P GSCI™ Total Return index measures a fully collateralized commodity futures investment that is rolled forward from the fifth to the ninth business day of each month. Currently the S&P GSCI™ includes 242 commodity nearby futures contracts. The S&P GSCI™ Total Return is significantly different than the return from buying physical commodities.

The Barclays Capital U.S. Government Bond Index is the U.S. Government component of the Barclays Capital U.S. Aggregate Index. It includes public obligations of the U.S. Treasury with a remaining maturity of one year or more. It also includes publicly issued debt of U.S. Government agencies, quasi-federal corporations, and corporate debt guaranteed by the U.S. Government.

The Philadelphia Gold & Silver Index is a market capitalization-weighted index of 30 leading companies focused on the mining of gold and silver.

The Citigroup Non-U.S. World Government Bond Index is comprised of developed market foreign government bonds with maturities over one year.

The Citigroup U.S. Government Index is composed of all U.S. Treasury notes and bonds with remaining maturities of at least one year and outstanding principal of at least $25 million that are included in the Citigroup Broad Investment-Grade Bond Index.

The JPMorgan Domestic High Yield Index is designed to mirror the investment universe for the U.S. dollar domestic high yield corporate debt market.

HFRX RV Multi Strategy Index: Relative Value: Multi-Strategies employ an investment thesis is predicated on realization of a spread between related yield instruments in which one or multiple components of the spread contains a fixed income, derivative, equity, real estate, MLP or combination of these or other instruments. Strategies are typically quantitatively driven to measure the existing relationship between instruments and, in some cases, identify attractive positions in which the risk adjusted spread between these instruments represents an attractive opportunity for the investment manager. In many cases these strategies may exist as distinct strategies across which a vehicle which allocates directly, or may exist as related strategies over which a single individual or decision making process manages. Multi-strategy is not intended to provide broadest-based mass market investors appeal, but are most frequently distinguished from others arbitrage strategies in that they expect to maintain >30% of portfolio exposure in 2 or more strategies meaningfully distinct from each other that are expected to respond to diverse market influences.Gold is represented by the dollar spot price of one troy ounce.

Swiss Re Cat Bond Indices are a series of performance indices constructed to track the price return and the total rate of return for USD denominated cat bonds. Swiss Re Cat Bond Indices track the performance of the main basket, all outstanding USD denominated catastrophe bonds.

The Chicago Board Options Exchange Market Volatility Index (“VIX”) is a measure of the implied volatility of S&P 500 index options and represents the market's expectation of stock market volatility over the next 30-day period.

Past performance does not guarantee future results.

Indices are unmanaged and cannot be purchased directly by investors. Index performance is shown for illustrative purposes only and does not predict or depict the

performance of the fund.

28 For Institutional Use Only

DisclosuresSpecial Risks: Fixed income investing entails credit and interest rate risks. When interest rates rise, bond prices generally fall, and the Fund’s share prices can fall. May invest up to 40% in below-investment-grade (“high yield” or "junk") bonds, which are more at risk of default and are subject to liquidity risk. Value investing involves the risk that undervalued securities may not appreciate as anticipated. Mortgage-backed securities are subject to prepayment risk. Derivative instruments whose values depend on the performance of an underlying security, asset, interest rate, index or currency, entail potentially higher volatility and risk of loss compared to traditional stock or bond investments. Convertible bonds are subject to the additional risk that the market value of the equity or other securities into which they are convertible will never be sufficient to justify conversion, rendering the conversion value of the bonds worthless. Asset-backed securities are subject to prepayment risk. Foreign investments may be volatile and involve additional expenses and special risks, including currency fluctuations, foreign taxes and geopolitical risks. Emerging and developing market investments may be especially volatile. The Fund may also invest through a wholly-owned Cayman Islands subsidiary, which is subject to the laws of the Cayman Islands and involves the risk that changes to those laws could negatively affect the Fund. Diversification does not guarantee profit or protect against loss. These views represent the opinions of OppenheimerFunds, Inc. and are not intended as investment advice or to predict or depict performance of any investment. These views are as of the open of business on March 28, 2014, and are subject to change based on subsequent developments.

Investing in MLPs involves additional risks as compared to the risks of investing in common stock, including risks related to cash flow, dilution and voting rights. Each Fund’s investments are concentrated in the energy infrastructure industry with an emphasis on securities issued by MLPs, which may increase volatility. Energy infrastructure companies are subject to risks specific to the industry such as fluctuations in commodity prices, reduced volumes of natural gas or other energy commodities, environmental hazards, changes in the macroeconomic or the regulatory environment or extreme weather. MLPs may trade less frequently than larger companies due to their smaller capitalizations which may result in erratic price movement or difficulty in buying or selling. Additional management fees and other expenses are associated with investing in MLP funds. The Oppenheimer SteelPath MLP Funds are subject to certain MLP tax risks. An investment in an Oppenheimer SteelPath MLP Fund does not offer the same tax benefits of a direct investment in an MLP. The Funds are organized as Subchapter “C” Corporations and are subject to U.S. federal income tax on taxable income at the corporate tax rate (currently as high as 35%) as well as state and local income taxes. The potential tax benefit of investing in MLPs depend on them being treated as partnerships for federal income tax purposes. If the MLP is deemed to be a corporation, its income would be subject to federal taxation at the entity level, reducing the amount of cash available for distribution which could result in a reduction of the fund’s value. MLP funds accrue deferred income taxes for future tax liabilities associated with the portion of MLP distributions considered to be a tax-deferred return of capital and for any net operating gains as well as capital appreciation of its investments. This deferred tax liability is reflected in the daily NAV and as a result a MLP fund's after-tax performance could differ significantly from the underlying assets even if the pre-tax performance is closely tracked.

These views represent the opinions of OppenheimerFunds, Inc. and are not intended as investment advice or to predict or depict performance of any

investment. These views are as of the open of business on March 16, 2014, and are subject to change based on subsequent developments.

The S&P 500 Index is a free-float capitalization-weighted index of the prices of 500 large-cap common stocks actively traded in the United States.

Shares of Oppenheimer funds are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other

agency, and involve investment risks, including the possible loss of the principal amount invested.

Before investing in any of the Oppenheimer funds, investors should carefully consider a fund’s investment objectives, risks, charges and

expenses. Fund prospectuses and summary prospectuses contain this and other information about the funds, and may be obtained by asking

your financial advisor, visiting oppenheimerfunds.com or calling 1.800.CALL OPP (225.5677). Investors should read prospectuses and

summary prospectuses carefully before investing.

For Institutional Use Only. This material has been prepared by OppenheimerFunds Distributor, Inc. for institutional investors only. It has not been filed with

FINRA, may not be reproduced and may not be shown to, quoted to or used with retail investors.

Oppenheimer funds are distributed by OppenheimerFunds Distributor, Inc.

225 Liberty Street, New York, NY 10281-1008

© 2014 OppenheimerFunds Distributor, Inc. All rights reserved.