© 2015 Fair Isaac Corporation. Confidential. This presentation is provided for the recipient only and cannot be reproduced or shared without Fair Isaac Corporation’s express consent.

An Overview of Scoring

John HadlowSenior Director - Scores

Agenda

© 2015 Fair Isaac Corporation. Confidential.2

► About FICO

► Types of Scoring

► Consumer Access to Scores

► Innovations

© 2015 Fair Isaac Corporation. Confidential.3

About FICO®

4 © 2015 Fair Isaac Corporation. Confidential.

FICO® Score Solution Set

► Critical in billions of decisions each year

► 90 of top 100 largest US financial institutions use FICO® Scores

► Deployed in 20 countries and counting

► Share the FICO® Scores you use with clients

► Strengthen customer relationships by adding value

► Increase profitability and growth

► Consumer Access to their FICO® Score

► Only single source for identity, credit, and FICO®

Score monitoring

Open Access

5 © 2015 Fair Isaac Corporation. Confidential.

FICO® Scores - Expertise

► FICOTM pioneered credit bureau scoring modeling technology

► FICO has partnered with all five major credit bureaus in the United States and Canada

► 150 billion FICO® scores have been sold to date

► Powers 10 billion+ decisions a year

► 70,000+ businesses rely on FICO® scores

► FICO® scores enhance decision-making► Across lenders of all credit industries

► Across various decision points such as approval/denial, marketing and portfolio management

► Use of FICO® scores has expanded into non-traditional markets such as rating agencies – “the FICO Score is an Index”

6 © 2015 Fair Isaac Corporation. Confidential.

UNITED STATES of AMERICA

CANADA

ALASKA (USA)

MEXICO

COLOMBIA

VENEZUELA

BRAZIL

PERU

BOLIVIA

HONDURAS

NICARAGUA

ECUADOR

GUYANA

SURINAMEFRENCH

GUIANA

COSTA RICA

PANAMA

GUATEMALA

CUBA

PARAGUAY

ARGENTINA

URUGUAY

CHILE

GREENLAND

ICELAND

UNITED

KINGDOM

REPULIC OF

IRELAND

NORWAY

SWEDEN

FINLAND

DENMARK

ESTONIA

LATVIA

LITHUANIA

POLANDBELARUS

GERMANY

CZECH

REPUBLIC

NETHERLANDS

BELGIUM

FRANCE

SPAIN

PO

RT

UG

AL

SWITZ.

AUSTRIA

SLOVAKIA

HUNGARY

ROMANIA

BULGARIA

ITALY

UKRAINE

TURKEYGREECE

SYRIA

IRAQ

SAUDI

ARABIA

YEMEN

OMANUAE

EGYPTLIBYA

ALGERIA

MOROCCOTUNISIA

WESTERN SAHARA

MAURITANIAMALI

NIGER CHAD

SUDAN

ETHIOPIA

SOMALIAUGANDA

SENEGAL

GUINEA

LIBERIA

COTE

D’IVOIRE

BURKINA

GHANA

NIGERIA

CAMEROON

CENTRAL

AFRICAN REPUBLIC

GABON CONGODEMOCRATIC

REPUBLIC OF

CONGO

KENYA

TANZANIA

ANGOLA

ZAMBIA

NAMIBIA

BOTSWANA

ZIMBABWE

REPUBLIC

OF SOUTH

AFRICA

MADAGASCAR

RUSSIAN FEDERATION

KAZAKHSTAN

GEORGIA

IRAN

UZBEKISTAN

TURKMENISTAN

AFGHANISTAN

KYRGYZSTAN

TAHKISTAN

PAKISTAN

INDIA

CHINA

NEPAL

MYANMAR

THAILAND

SRI

LANKA

MONGOLIA

NORTH

KOREA

SOUTH

KOREA JAPAN

TAIWAN

CAMBODIA

LAOS

VIETNAM

PHILIPPINES

MALAYSIA

INDONESIA

PAPUA

NEW GUINEA

AUSTRALIA

NEW

ZEALAND

Global FICO® Scores Footprint

* Source: World Bank. 2013. Doing Business 2014: Understanding Regulations for Small and Medium-Size Enterprises. Washington, DC: World Bank Group. DOI: 10.1596/978-0-8213-9984-

2. License: Creative Commons Attribution CC BY 3.0

Credit Information Legend *

Full Data Sharing

Negative-only Data Sharing

No Data Sharing

FICO Score Deployment Legend

FICO® Score Deployed

FICO® Score Available at Credit Bureau

© 2015 Fair Isaac Corporation. Confidential.7

Types of Scores

8 © 2015 Fair Isaac Corporation. Confidential.

FICO® Scores, Bureau Scores

► The FICO® Score:►Is a credit score that summarizes a consumer’s or business’s credit risk, based

on a snapshot of their credit report, history at a particular point in time

►Helps lenders and others predict how likely consumers or businesses are to make their credit payments on time

►Affects whether consumers or businesses can access credit and how much they pay for credit cards, auto loans, mortgages and other kinds of credit

►Is the most widely used credit score

► Other Bureau Scores►May include or exclude some of the above

► BI Scores►Either driven primarily by consumer data or balance sheet and other

information: SME is primarily consumer data

9 © 2015 Fair Isaac Corporation. Confidential.

FICO® Score – A Family of Scores

Global FICO Score

FICO Score

Propensity Score

Economic Impact Score

Application Fraud Score

Credit Capacity

Score

Alt-Data Score

Collection Score

SME Score

Household Score (Non

US)

Industry Scores

Invitation to Apply Score

Expansion Score

Insurance Score

Medication Adherence

Score

Revenue Score

Bankruptcy Score

10 © 2015 Fair Isaac Corporation. Confidential.

► Developed using FICO’s proprietary modeling platform and segmented scoring technology

► Scores designed as “second chance” model to address unscoreableapplicants

► Includes FCRA compliant alternative data sources & bureau data

► Same look and feel as the FICO® Score► Scaling

► Reason codes

► Attention to regulatory compliance using palatable predictive data

Alternative Credit Data Score

11 © 2015 Fair Isaac Corporation. Confidential.

US Alternative Data Score

► FICO has undertaken extensive research in the use of alternative credit data for assessing consumer credit risk

► We believe that a combination of three data sources provide best benefit in scoring consumers with sparse or no traditional credit data► Traditional credit data (as available)

► Property and public record data (LexisNexis)

► Cellular and utility billing information (NCTUE managed by Equifax)

► Initial models demonstrate good KS ranges for FICO unscoreables

► FICO and our partners will be conducting a pilot in the near term for card issuers interested in evaluating these scores

► We would like to gauge your interest in pilot participation

12 © 2015 Fair Isaac Corporation. Confidential.

Expert and other Scores- Example: Global FICO® Score

► Global standard for consumer credit risk assessment

► Evaluates consumer credit risk on any form of consumer credit bureau data

► Can be deployed in almost any geography with local credit bureau information or local bank information

► Adopted by global financial institutions to ensure consistent portfolio and risk management assessment across global portfolios

► Compliance► Rating Scale Methodology – Risk calibration across portfolios and countries – enables

capital allocation optimization

► Model Governance (OCC 11/12 Compliant)

► Leverages the fact that a primary driver of score performance is the data

► Has been shown to outperform empirically developed scores

13 © 2015 Fair Isaac Corporation. Confidential.

Application Fraud Score

Provides lenders with the probability that a credit application may be high risk (high probability of

fraud)

Delivered through many platforms and can use data from over 23 bureaus globally

Assesses fraud risk of each credit application by scoring at the time of origination

Solution provides a score from 1-999: Low number is low risk of fraud, high number is higher risk of

fraud

Origination fraud scores have been shown to give 5-30% improvement in

detection performance compared to rules based systems

14 © 2015 Fair Isaac Corporation. Confidential.

Types of Application Fraud Detected

First-party fraud in

credit cards worldwide

cost $18.5BN in 2012

and will rise to

$28.6BN by 2016

Fraudulent obtaining of credit (often by

falsifying information) without intending to

pay it back

FIRST

PARTY

Involves identity theft and fraud that is

committed without the knowledge of a person

whose identity is used to commit the fraud

THIRD

PARTY

© 2013 Fair Isaac Corporation. Confidential.14

15 © 2015 Fair Isaac Corporation. Confidential.

Propensity Scores focus on WHEN and not IF

Traditional Scorecards

A cross-sectional data analysis paradigm

Time-to-Event Scorecards

A longitudinal data analysis paradigm

Focus is on if event will happen, not when

Predictive information is summarized at

observation point.

Fixed scorecard building period

Focus is on when event will happen

Predictive information is exploitable right up to

the time period prior to the target event

Moving time windows

Obs Perf

TimeDiscrete

Time Periods

Target event yes/no? Target event at

time period k

Joe

Mary

No target

event until

censoredMax

Snapshot 1 Snapshot 2 Many snapshots

Predictive information

16 © 2015 Fair Isaac Corporation. Confidential.

FICO SME Score - Overview

► Provides credit grantors with an effective tool for rank-ordering the credit risk of small and medium enterprises, the higher the score the lower the risk.

► Applies to different product types, (loans, leases & trade credit) and can be used throughout the credit lifecycle

► Enables faster, more consistent and profitable credit decisions

► Reduces delinquency and charge-off losses

17 © 2015 Fair Isaac Corporation. Confidential.

FICO® SME Score - Blended Model

FICO® SME Score

“165”

Shareholder 1 Data Application

Consumer CreditBureau Report

Business Data Financials

Business CreditReport

Shareholder 2 Data Application

Consumer CreditBureau Report

FICO® SME Score

“190”

18 © 2015 Fair Isaac Corporation. Confidential.

Importance of Compliance with International Regulation

► Global shift from principle based governance to demonstrable governance

► The additional monetary and other exposures (public and political) new regulatory requirements will impose on our international customers

► Compliance with new and ever-increasing global regulations is time consuming, resource intensive and a management distraction

► New regulations are forcing financial institutions into a higher level of proof of global risk standardization in addition to greater governance proof and reporting than ever before

De-regulation

Re-regulation

Market cycles

Dodd-Frank BASEL III

Risk-based Pricing

Udall

Financial Policy Committee

Durbin

© 2015 Fair Isaac Corporation. Confidential.19

Consumer Access to Scores

© 2014 Fair Isaac Corporation. Confidential.20

Industry Pressures to Increase Consumer Education &

Transparency Provide Opportunity

Regulatory focus on consumer business practices

Proposals for “free score” legislation and regulation

FICO helps financial services clients address these pressures and capture the opportunity

Appeals for increased consumer education

Initiatives to build customer trust, loyalty & satisfaction

21 © 2015 Fair Isaac Corporation. Confidential.

► Clients (Lenders) make available for FREE for their customers

► Helps enable clients to provide the actual FICO®

Score purchased to make customer decisions

► Helps address issues in an industry facingregulatory and other pressures

► Helps drive increased online engagement, share of wallet, loyalty and customer satisfaction

Example: FICO® Score Open Access—a Valuable

Program that…

Without additional score fees charged by FICO*

*Consumer Reporting Agency may charge a fee

21

22 © 2015 Fair Isaac Corporation. Confidential.

FICO® Score

How FICO® Score Open Access Works

Provide Consumer Empowerment Tools

FICO® Score Meter

12-month Graphical Trend

Two Score Factors (reason codes)

Credit Educational Content

Frequently Asked Questions

23 © 2015 Fair Isaac Corporation. Confidential. Source: Yahoo Finance News, Image – whitehouse.gov

Strong Support from Key Industry Stakeholders

Source: New York Times

© 2015 Fair Isaac Corporation. Confidential.24

Innovations

25 © 2015 Fair Isaac Corporation. Confidential.

Interesting and Hard Problems to Solve

► Income Estimation

► Big Data and Machine Learning

► Using Unstructured Data

26 © 2015 Fair Isaac Corporation. Confidential.

Income Estimation Score: Development Data Specifics

► FICO undertook a proof of concept to determine whether we could build an empirically derived income estimator based exclusively on credit bureau data

Key Features

Development Data Verified income from mortgage applications

Sample is from loans opened between the years of October 2005

and April 2012

Model Coverage Annual, individual income predicted up to $600,000

Predictive Data Sources Credit Bureau data

Output Point estimate of income

27 © 2015 Fair Isaac Corporation. Confidential.

Model Results

► POC Model results were benchmarked to an existing income estimator

FICO Income EstimatorExisting Income Estimator in

the Market

Output Point estimate of income Range estimate of income

Development data Verified income Aggregated from census data

Model Coverage Up to annual income of $600,000 Up to annual income of $150,000

Predictive Data Sources Credit Bureau Data Demographic Data

R – Squared Value 0.408* 0.160

10% Percent Prediction Error 18.9% 14.1%

* R-Squared value as high as 0.571 depending on data availability – such as using mortgage related variables like “original loan amount”

28 © 2015 Fair Isaac Corporation. Confidential.

Use Case - Reasonability Check at Origination

► Utilize debt to income ratios established by policy to determine initial loan amount.► E.g., $50,000 annual income qualifies for a $10,000 credit card limit.

► Start with a point estimate of income for the applicant.

► Apply an empirically derived confidence interval as a filter to bring the estimate to a specified level of certainty.

► Resulting output for consumer: income is at least $50,000 with 95% confidence.

► Advantage –► Using a confidence level avoids overestimation of income (conservative approach).

► Disadvantage► Confidence level could restrict some borrowers with higher incomes from qualifying for a more

substantial offer of credit.

► However, there is a point where the additional income may make little difference in the amount of credit offered – perhaps, less of a concern for high incomes.

29 © 2015 Fair Isaac Corporation. Confidential.

Practical Scoring Using Big Data

2

9

Big Data creates new opportunities for credit scoring:

Predict consumer behavior more accurately

To harness the value of Big Data for credit decisions requires transparent

analytics: Comprehensible scores, justifiable decisions

Data-

drivenValuable

Decisions

Effective, transparent analytics balances

data with domain expertise

Expert

guided

30 © 2015 Fair Isaac Corporation. Confidential.

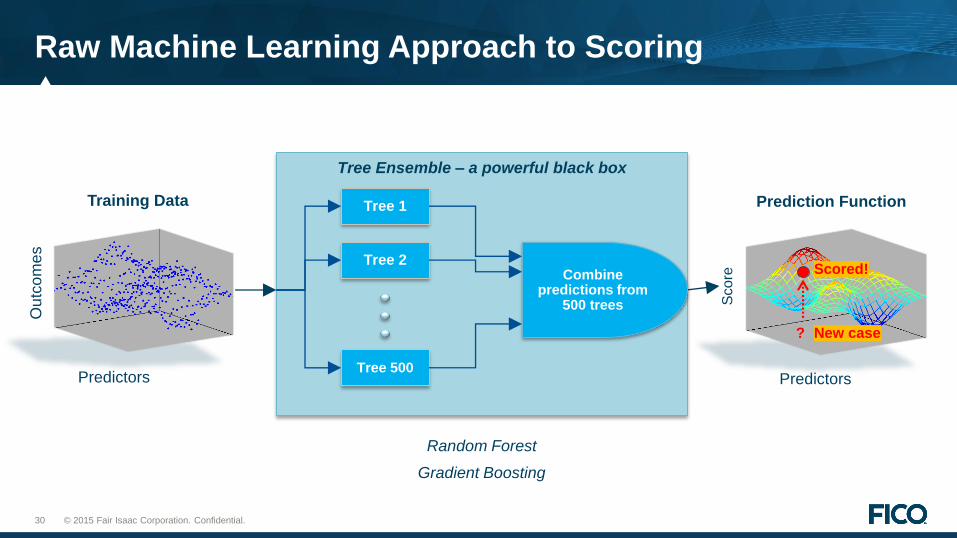

Training Data Prediction Function

Predictors

Ou

tco

me

s

Tree 1

Tree 2

Tree 500

Combine predictions from

500 trees

Tree Ensemble – a powerful black box

Predictors

Random Forest

Gradient Boosting

?

Scored!

New case

Raw Machine Learning Approach to Scoring

Sco

re

31 © 2015 Fair Isaac Corporation. Confidential.

CONS

Difficult to incorporate domain expertise into black box

Decisions based on models can sometimes be hard to justify

But handle with care.

Vulnerable to data limitations. Sometimes non-intuitive associations

PROS

Minimal assumptions on customer behavior

Supports discovery of new, unexpected predictive associations

Highly automated, productive data analysis

PROS and CONS: Raw Machine Learning Tools for Credit Scoring

Embrace!

32 © 2015 Fair Isaac Corporation. Confidential.

0 50 100

100

50

0

% B

ad

sR

eje

cte

d

S/c #1 S/c #2 S/c #3 S/c #4 S/c #5

Segmentation derived by Scorecardizer

% Goods Rejected

5-fold cross-validated AUC

Tree Ensemble (not comprehensible) 0.96

Scorecardizer (comprehensible) 0.94

Traditional Scorecard (comprehensible) 0.91

Age of oldest tradeline (mts.)

Value of current property($)

Results: Tradeoff curves (Test set) Home Equity Loan data

33 © 2015 Fair Isaac Corporation. Confidential.

Scoring with Unstructured Data

► Many additional sources of data►Call centres

►Social media

►Comments in bureaus, other data storage

► It works

► It adds value

► In the absence of traditional data it is valuable

34 © 2015 Fair Isaac Corporation. Confidential. 3

4

Cumulative Fraction Good

Cum

ula

tive F

raction B

ad

Winner: Model using regular and text-based variables

Close 2’nd: Model based on regular data only

For comparison: Model based on text data only

Predictive Lift From Combining Regular and Text Data

35 © 2015 Fair Isaac Corporation. Confidential.

Unstructured Data Scoring: Main Takeaways

► Embrace the power of new data sources, such as unstructured text

► Powerful analytic approaches such as topic modeling and semantic scorecards allow you to comprehend the value and meaning of text data for predicting consumer behavior

► Existing Structured Data is still the most valuable source-unless you don’t have information about a consumer or business

► The tools are already here to build the scores – the challenge is to operationalize them and make them compliant with legislation

3

5

© 2015 Fair Isaac Corporation. Confidential. This presentation is provided for the recipient only and cannot be reproduced or shared without Fair Isaac Corporation’s express consent.

johnhadlow@fico,com