Analysing Startup Valuation and Fundraising Are we entering Dot Com Bubble 2.0?

Aditya Haripurkar

INSEAD Master in Finance 2015

1

TABLE OF CONTENTS

1. OVERVIEW

2. THE PRESENT INTERNET LANDSCAPE

3. STARTUP BUSINESS MODELS AND VALUATION ISSUES

4. TO IPO OR NOT : THE RISE OF LATE STAGE PRIVATE FINANCING

5. GLOBAL STARTUP INVESTMENT TRENDS : THE RISE OF ASIA

6. STARTUP VALUATION TECHNIQUES AND CONSIDERATIONS

7. DOTCOM BUBBLE 2.0 MYTH OR REALITY

8. CONCLUSION

9. REFERENCES

© Aditya Haripurkar

INSEAD Master in Finance 2015

2

OVERVIEW

Recent advancements in technology and the introduction of disruptive and innovative business models have changed the way we lead our day to day lives and the dynamics of major business verticals. The introduction of the smartphone and the app economy has led to the formation of innovative companies and the pivoting of business models towards mobile by traditional and older organisations. The mobile strategy adopted by these companies is further validated by the increasing smartphone and internet penetration observed all over the word especially in emerging markets. Venture capital firms and private investors have sought to capitalise on these trends by injecting massive amounts of funds into businesses that merge problem solving approaches and cutting edge technology. This influx of funds has showed no signs of abating in recent times, which has lead to concerns and fears of a dotcom bubble similar to the one witnessed at the turn of the century. Many of these concerns arise from the fact that funds are being invested in business models which have not demonstrated a sustained ability to generate revenues and that many of these investment decisions appear to be ‘bet’ plays or better known as making decisions based on the ‘FOMO’ (Fear of Missing Out) sentiment. This paper looks at the underlying issues fueling this inflow of funds with a deep dive into common valuation techniques used by investors, startup investment activity observed globally, and a discussion on whether a dotcom bubble 2.0 is imminent given recent irrational investor behaviour.

© Aditya Haripurkar

INSEAD Master in Finance 2015

3

THE PRESENT INTERNET LANDSCAPE

The introduction of the iPhone in 2007 and Android operating system in 2009 was the beginning of the smartphone revolution. While Facebook, Amazon and Google were the big internet giants at the time, the smartphone, it can be argued provided the internet a new lease of life, which led to the creation of truly disruptive business models. Today’s billion dollar valuation companies or ‘Unicorns’ as they are referred to such as Uber, Airbnb, Snapchat, Pinterest and Dropbox are all products of the smartphone revolution. These companies have not only disrupted business verticals such as transportation in the case of Uber or travel in the case of AirBnB, they offer a unique and delightful user experience which was lacking in traditional players in these verticals. These companies have introduced business models vastly different than those observed in traditional internet companies, where no inventory is owned as in the case of Instacart, the grocery delivery company or no media is owned as in the case of Twitter which is increasingly viewed as a media outlet. These businesses have fueled a new ondemand economy characterised by instant gratification and user experience. A classic example of this is Uber which acts as a the platform that matches demand i.e users requesting a ride to supply i.e drivers registered on the Uber platform. The image below best illustrates the impact of businesses such as Uber, Facebook, Alibaba and Airbnb.

©Tom Goodwin

© Aditya Haripurkar

INSEAD Master in Finance 2015

4

Apart from the introduction of disruptive business models, the wide and global penetration of the internet through sales of desktops, laptops, tablets and mobiles is one of the major reasons why internet startups have been gaining a lot of attention from investors. Today, the internet can be accessed by 42% of the world’s population as per statistics shown in the image below and this figure is estimated to grow rapidly as investment in internet infrastructure and networks increases in emerging markets.

©We Are Social

The increasing access to the internet through smartphones in developing markets has led to an explosion in the use of social media and mobile based products & services. Hence the smartphone is the focal point around which products and services are built and internet startups that aim to solve real life and local problems through mobile technology and have sustainable business models will continue to attract significant investor attention.

© Aditya Haripurkar

INSEAD Master in Finance 2015

5

STARTUP BUSINESS MODELS AND VALUATION ISSUES

The primary startup business models today can be categorized into the following :

1) SaaS (Software as a Service) 2) Audience 3) ECommerce 4) Enterprise

The revenue models differ amongst the above business models. For example ECommerce companies such as Uber and Airbnb will charge customers based on the product or service delivered while Audience companies such as Snapchat and Facebook generate revenue through advertising or leads. On the other hand , Enterprise and SaaS business models follow a subscription or a monthly based billing model. A fifth and emerging business model will be the internet of things and one can expect this business model to have an innovative revenue model in the near future. All the above business models feature extensively in the coveted ‘Unicorn’ club and continue to 1

attract hefty valuations. A moot question though is, are these valuations based on strong fundamentals i.e profitability generating potential or based on high investment values due to investors jumping on the FOMO sentiment? Let us have a close look at the profitability of some 2

of these companies:

Business Model Company

Valuation (USD in Billions)

Investment ( USD In Billions )

Approx Revenues (USD in Billions) Profitable

Valuation : Investment

Ratio

SaaS Dropbox 10 1.1 0.2m No 9.09

ECommerce AirBnB 10 0.8 1.4 Yes 12.50

Audience Pinterest 11 0.76 0.2 No 14.47

ECommerce Flipkart 11 2.5 1 No 4.40

Enterprise Palantir 15 1 1 No 15.00

Audience Snapchat 10 0.65 0 No 15.38

ECommerce Uber 41 6 10 No 6.83

Source : blogs.endjin.com

1 The Unicorn club comprises of internet startups with private valuations of over 1 billion dollars

2 Fear of Missing Out

© Aditya Haripurkar

INSEAD Master in Finance 2015

6

The above list of companies belong to all the different models mentioned above and clearly show revenue earning capabilities with the exception of Snapchat which belongs to the Audience business model. While all these companies enjoy high valuations and investment rounds, profitability which is conventionally thought of as the most important investment indicator, is clearly missing from all these companies except for AirBnB. If profitability is not driving valuations, what drives valuation levels? One factor is revenue growth and as can be observed in the below graph, a startup needs to demonstrate that investment funds are being used to increase revenues i.e the ability to execute. In the example below with AirBnB, a clear correlation between revenue growth and investment levels can be clearly established.

Source : blogs.endjin.com

The other factor that drives valuations is the VC’s themselves as they can assign valuation levels to companies based on funding rounds. In the table provided above, investment to valuations ratios of between 7% 15% as observed, will be in line with VC expectations as it is in the VC’s interest to drive valuations of these companies higher as it not only sends the right signals to the investment press, but also sets market expectations in the event of a takeover which is when VC’s make significant returns.

© Aditya Haripurkar

INSEAD Master in Finance 2015

7

The VC’s approach towards building a startup portfolio involves : 1) Identifying a portfolio of companies with diversified business models and verticals. A particular emphasis is placed on the team behind the startup as the ability to execute or the ability of the company to drive revenue growth as mentioned earlier is one of key factors that VC’s pay close attention to. 2) Taking positions in each of the companies that range between 8%20% at investment levels that set the right market expectations with a forward looking view and in line with the capital requirements of the startups. 3) Making an exit either through a takeover or IPO. A typical early stage VC aims for a 10x cash on cash return. The VC firm would factor in expectations that out of every 10 investments, 9 investments will tank and 1 of those investments will be a home run. The size of the returns expected varies depending on the stage at which VC’s have invested in the startup. Early stage investors will typically make the most return due to the risks that investors assume in investing in an early stage startup, while late stage investors have lower return multiples on average. The below table and accompanying graph illustrates this point :

@Unitus Seed Fund © Aditya Haripurkar

INSEAD Master in Finance 2015

8

TO IPO OR NOT : THE RISE OF LATE STAGE PRIVATE FINANCING The emergence of the Unicorn club recently i.e private companies or startups with a valuation of greater than USD 1 billion, has led to a great deal of debate amongst the investment community as to why these companies have chosen to delay raising funding in the public markets. Let us have a close look at the valuations of the top 15 Unicorns as of September 2015 :

@Wall Street Journal

The valuations of some of the above companies are way above the market cap of well known publicly listed companies. For example, Twitter which went public in 2013 has a market cap in the range of $19 billion which is less than the valuation of Uber, Xiaomi, Airbnb and Palantir. Snapchat which launched just 4 years back now has a valuation close to the market cap of Twitter, a 9 year old company that has been listed for 2 years. A similar comparison can be made between Box and Dropbox , two cloud storage companies. Box which went public earlier this year has a market cap of $1.4 billion, while Dropbox has a valuation of $10 billion.

© Aditya Haripurkar

INSEAD Master in Finance 2015

9

The number of companies entering this coveted club is also showing no signs of slowing down as illustrated in the below graph where it is projected that 2015 will have 50 companies entering the unicorn club.

@CB Insights

The increase in late stage private financing i.e Series D and Series E + is the leading cause for these companies having inflated valuations as shown in the below graph.

@CB Insights

© Aditya Haripurkar

INSEAD Master in Finance 2015

10

So what are the reasons behind the surge in late stage financing and the delay in startups going public. Let us examine a few of those reasons below:

1. Private financing provides startups with more flexibility to continue growing their business without subjecting themselves to regulations. Public market investors focus on profitability which shifts the focus for startups and hence leads to ineffective business decision making.

2. The availability of financing from a number of late stage investors such as mutual funds, hedge funds, sovereign funds and other public investors. Late stage investors are also incentivized by the availability of preferred shares (which is discussed in detail in the following sections of this report) which provides downside protection. A low interest regime and positive sentiment in the equity markets has also facilitated this increase in the availability of late stage financing.

3. The FOMO sentiment that exists amongst late stage investors where everyone is keen to get a slice of the winners pie.

4. It is widely believed that late stage financing is the new IPO for startups and this is illustrated in the below graph where returns in tech markets which used to be in public markets, have now moved to the private markets.

@Andreeson Horowitz

5. Tech IPO volumes are at all time lows which does not make it favorable for startups to

raise funding in the public markets as trading liquidity will remain low. From the points above, it can be argued that VC’s continue to raise large amounts of funding and hence may be the reason why startups are able to attract high investment rounds even at a later stage. However is this true?

© Aditya Haripurkar

INSEAD Master in Finance 2015

11

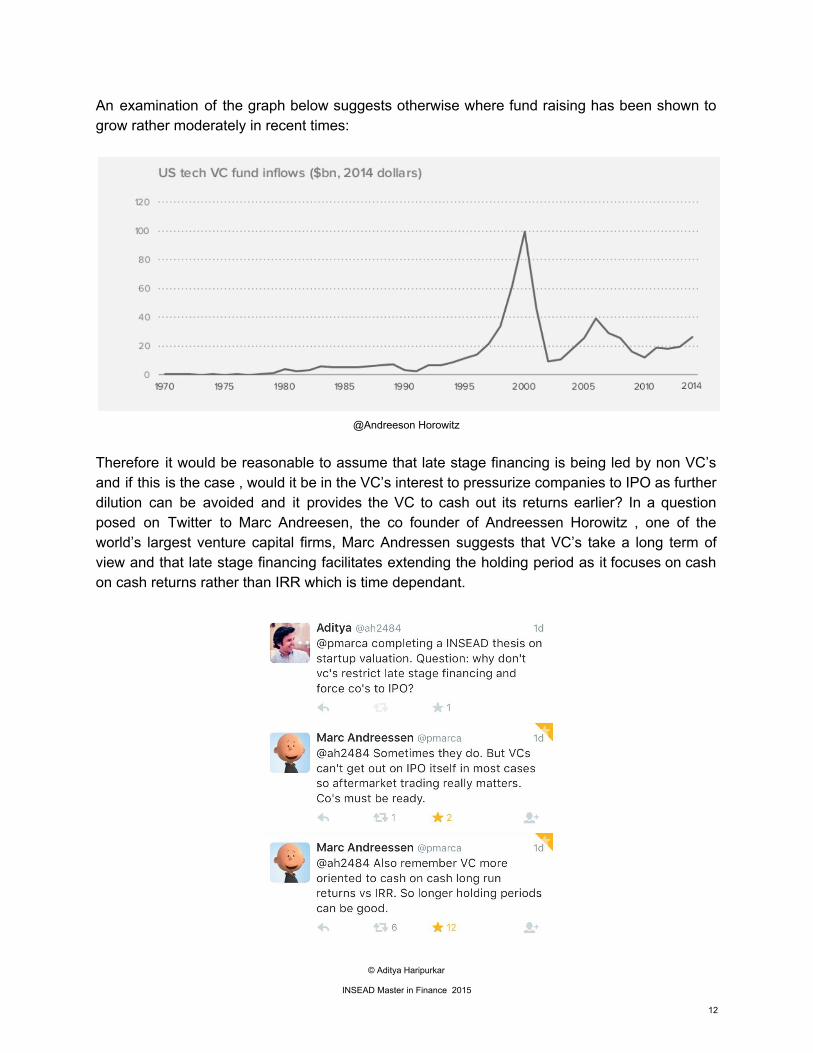

An examination of the graph below suggests otherwise where fund raising has been shown to grow rather moderately in recent times:

@Andreeson Horowitz

Therefore it would be reasonable to assume that late stage financing is being led by non VC’s and if this is the case , would it be in the VC’s interest to pressurize companies to IPO as further dilution can be avoided and it provides the VC to cash out its returns earlier? In a question posed on Twitter to Marc Andreesen, the co founder of Andreessen Horowitz , one of the world’s largest venture capital firms, Marc Andressen suggests that VC’s take a long term of view and that late stage financing facilitates extending the holding period as it focuses on cash on cash returns rather than IRR which is time dependant.

© Aditya Haripurkar

INSEAD Master in Finance 2015

12

GLOBAL STARTUP INVESTMENT TRENDS : THE RISE OF ASIA

While North America continues to have large number of VC deals and funding rounds, the rest of the world especially Europe and Asia is quickly catching up in terms of startup investment activity. With two of the world’s most populous nations based in Asia and a growing mobile and internet subscriber base, it is not a surprise that investment activity in Asia now lags North America in terms of number of deals and the size of the deals. Amongst the top 15 unicorn companies highlighted in the report, 5 are based in Asia (Xiaomi, Flipkart, Didi Kuaidi, Lufax and DJI) and 1 is based in Europe (Spotify) which highlights the growing importance of venture capital investment activity in these regions. Startup investments in Asia especially in China and India has lately hit astronomical values with huge funding sizes and a number of deals taking place especially in the mobile and internet space. This is not surprising given that internet penetration and smartphone sales are on the rise in this region and with a large population base, venture capital firms have been quick to fund startups that have tried to address large scale consumer problems.

@CB Insights

The number of early stage funding rounds in the region mirrors North America as this assumes greater importance in Asia since infrastructure and networks are not as sophisticated as those observed in North America. Similarly late stage financing in the region too is also on the rise and this was highlighted by the recent funding rounds for Flipkart and Coupang.

© Aditya Haripurkar

INSEAD Master in Finance 2015

13

@CB Insights

The business models of many of the startups based in region are considered to be models inspired or copied by US based startups. For example, Baidu is considered to be the Google of China, Ola Cabs is the Uber of India and Flipkart the Amazon of India. At the same time, messaging apps such as WeChat and Line have innovated and evolved into full scale platforms where a number of local services and products are offered. There are other notable startups in the region such as Coupang, GrabTaxi, Lazada, RedMart and Zomato which are offering unique and personalised experiences to local users.

Hence the focus for such startups based in these large markets is to grow and scale quickly. VC’s and other investors have facilitated this process by participating in sizeable and quick funding rounds. In addition to funding rounds, startups have also managed to scale and grow quickly by acquiring companies. For example, the number of tech M&A’s increased in China by 62% in 2014 year on year, while India witnessed the highest number of M&A transactions in 2014 in the 5 years. Another interesting insight into investment activity in the region is that China and India feature in the top 10 markets for tech exits with India recently entering the top 5 club.

@CB Insights

© Aditya Haripurkar

INSEAD Master in Finance 2015

14

STARTUP VALUATION TECHNIQUES AND CONSIDERATIONS

Valuation of startups is not as straightforward and simple as the valuation of companies that have a steady flow of cash and are profitable. These companies can be valued by using techniques such as DCF as revenue and growth can be reliably estimated. Startups especially in the pre seed stage can be difficult to value as these companies are at a pre revenue stage and there is limited availability of information by which a reasonable valuation can be derived. Below are some commonly used pre revenue startup valuation methods : Early stage valuation Method:

● Determine your startup’s capital requirements for the next 18 months.The amount of funding raised should be sufficient to launch the product , build a team and drive growth and revenue.

● Determine the amount of equity you would like to provide to the angel investor. Ensure that the investor is not given too much equity at this stage as providing a large stake may not provide enough motivation for the founder to work towards building the startup. A range of between 5% to 20% for an investment amount in the range of $100k to 500k would be termed as reasonable terms for the angel investor. An equity stake of 20% for an investment of $200k will imply valuing the company at $1m. The final stake will be dependant upon how the investor values other comparable companies and the founder’s growth estimations.

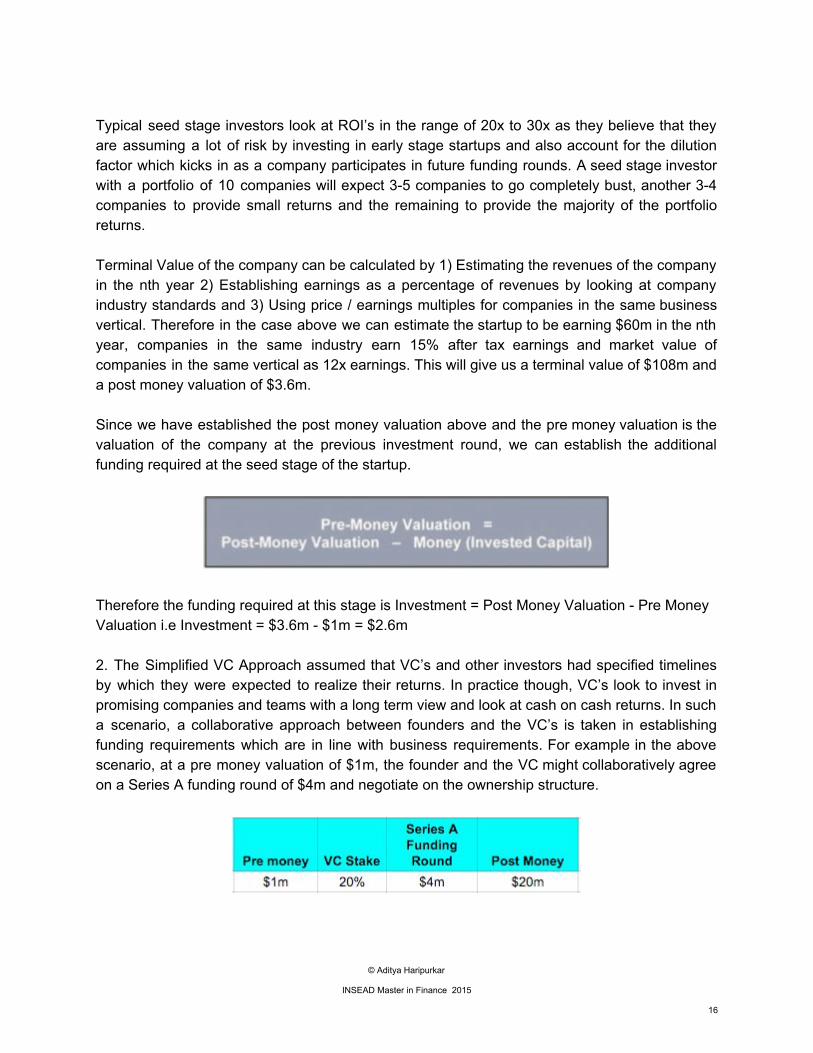

At the subsequent funding stages, a company will look to scale its operations in terms of size, geographies and revenue and hence will look to raise additional rounds of financing to drive the founder’s vision. There are a few ways by which valuation can be approached at this stage. Advanced Investment Rounds (Series A, Series B, Series C) Valuation Methods: 1. The Simplified VC Approach Using the above numbers where the startup was valued at $1m at the pre seed stage, we can establish the post money valuation using the simplified VC approach where :

©William Sahlman, “The Venture Capital Method”, HBS Case # 9288006

© Aditya Haripurkar

INSEAD Master in Finance 2015

15

Typical seed stage investors look at ROI’s in the range of 20x to 30x as they believe that they are assuming a lot of risk by investing in early stage startups and also account for the dilution factor which kicks in as a company participates in future funding rounds. A seed stage investor with a portfolio of 10 companies will expect 35 companies to go completely bust, another 34 companies to provide small returns and the remaining to provide the majority of the portfolio returns. Terminal Value of the company can be calculated by 1) Estimating the revenues of the company in the nth year 2) Establishing earnings as a percentage of revenues by looking at company industry standards and 3) Using price / earnings multiples for companies in the same business vertical. Therefore in the case above we can estimate the startup to be earning $60m in the nth year, companies in the same industry earn 15% after tax earnings and market value of companies in the same vertical as 12x earnings. This will give us a terminal value of $108m and a post money valuation of $3.6m. Since we have established the post money valuation above and the pre money valuation is the valuation of the company at the previous investment round, we can establish the additional funding required at the seed stage of the startup.

Therefore the funding required at this stage is Investment = Post Money Valuation Pre Money Valuation i.e Investment = $3.6m $1m = $2.6m 2. The Simplified VC Approach assumed that VC’s and other investors had specified timelines by which they were expected to realize their returns. In practice though, VC’s look to invest in promising companies and teams with a long term view and look at cash on cash returns. In such a scenario, a collaborative approach between founders and the VC’s is taken in establishing funding requirements which are in line with business requirements. For example in the above scenario, at a pre money valuation of $1m, the founder and the VC might collaboratively agree on a Series A funding round of $4m and negotiate on the ownership structure.

© Aditya Haripurkar

INSEAD Master in Finance 2015

16

Ownership stakes is one of major factors involved in early stage startup investing and hence understanding the mechanics of ownership becomes an important issue for both the founders and the investors. From the example given below, it is clear that as founders raise money at each stage, there is clear evidence of dilution in the ownership of the company. However the value per share has increased which implies that the value of the founders ownership is a lot more than at founding stage.

© Matt Nunogawa

3. Another popular startup valuation method involves projecting the EBITDA at the year of exit and multiplying the EBITDA by a industry standard multiple or by taking the multiple used to value a startup in the same business vertical. This value is then used to determine the IRR and

© Aditya Haripurkar

INSEAD Master in Finance 2015

17

the cash on cash return for the investor. Example of this valuation technique is given below which assumes investment in a single round.

© Macabacus, LLC

4. The Berkus Method: This method makes the assumption that fewer than one in a thousand startups meet or exceed revenue projections and hence valuing a company using this metric is not useful. Therefore , assuming a startup has the potential to reach $20m in revenues over a 4 year timeline, the startup can be valued by assigning values based on progress made by startups in commercialization activities. The method involves assigning the below values based existing startup attributes :

© Aditya Haripurkar

INSEAD Master in Finance 2015

18

5. Scorecard Valuation Method: This method involves determining the median premoney valuation for startups based in a particular region and operating within a business vertical and then adjusting the median premoney valuation based on seven characteristics of the company. An example of factor weights assigned to a startup operating in a region and business vertical which has a premoney median valuation of $1.5m is as below :

There are a number of other methods used to value startups and as such no one method is superior to the other. The best practise would involve using multiple valuations techniques and adjusting valuations based on the people behind the startup, the location and the industry. A feature of the example provided above by Matt Nunogawa is the presence of convertible notes at the preseed / seed stage. A convertible note is an instrument which allows pre seed / seed investors such as angels to convert into shares of preferred stock upon the startup securing series A funding. The issuance of convertible notes is essentially debt taken by founders which allows the founders to keep full ownership of the company. Apart from the lack

© Aditya Haripurkar

INSEAD Master in Finance 2015

19

of dilution, issuance of convertible notes is a quick and simple way of getting access to funds and also does not provide investors any control in the form of voting rights. Convertible notes also provide an added feature that benefits the angel investors in the event that the company raises a significant Series A investment round. This feature is called the conversion valuation cap which essentially imposes a floor on the angel investor's purchase price. Unlike a convertible note, issuance of preferred shares however allows investors the right to sit in board meetings and have veto rights. Preferred shareholders as the name suggests gives preference to preferred shareholders over common shareholders in the event of any sale or liquidation. Sophisticated investors invariably push for preferred shares instead of convertible notes since these shares also provide additional economic rights like prorata rights and liquidation preference. Liquidation preference is one of the most essential components of preferred stock and is the second most important deal term in a VC investment. Liquidation preference rights essentially allows investors to get their full investment back in the event that the value of the sale or liquidation is below the value of their investment. If the value of the sale or liquidation is above the investor’s investment value, the investors get a percentage of the company they own. The three types of liquidation preferences are as follows :

➔ Straight or Non Participating Preferred: This liquidation preference allows investors to get the full value of their investment plus any accrued dividends back in the event of a sale or liquidation and is widely considered to be the most founder friendly option.

➔ Participating Preferred : This liquidation preference is the most investor friendly option as it not only allows investors to recover the full value of their investment , but also allow investors a share of the proceeds based on their ownership of the company. Hence this deal term allows the investors to be paid twice.

➔ Capped Participating Preferred : This option has the same features as the Participating Preferred, however the returns on the proceeds is capped. Therefore this term represents a better option for the founder.

An additional concept in liquidation preferences is that of multiples. A 2X multiple means that preferred stockholders are entitled to twice the value of their original investment in case of a liquidation. Including any of the liquidation preference terms is likely to benefit the investor in terms of increasing upside potential and at the same time protect the investor on the downside. Hence it is important that the founder takes into the account the impact of these terms on dilution of ownership and in valuing the startup as including these provisions at an early stage would imply that future investors will want to include the same provisions.

© Aditya Haripurkar

INSEAD Master in Finance 2015

20

DOT COM BUBBLE 2.0 MYTH OR REALITY The emergence of the unicorn club where startups are being funded with massive late stage rounds in addition to an increase in early stage funding has led to many experts raising concerns about an impending dot com crash similar to the one that took place in 20002001. While some of the concerns expressed by respected voices in the tech and vc community are valid, this issue requires a deeper understanding of the market conditions, company fundamentals and the internet landscape that exists today and during the dot com crash.

Market conditions A good starting point will be to compare the top 5 high profile startups from the dot com era and the current era.

The noticeable feature above is the last valuations of both sets of companies, where publicly listed companies from the dot com era, commanded far lower valuations than today’s top high profile startups. The differentiating factor is the availability of late stage private financing that is available today due to low interest rates, the presence of mutual and sovereign funds and stable public markets. Companies from the dot com era resorted to going public at the first given opportunity to raise further funds due to the lack of large sized private funding options as opposed to the funding rounds that Unicorns receive today.

Source : Capital IQ, a16z

© Aditya Haripurkar

INSEAD Master in Finance 2015

21

Funds that would earlier be available in public markets are now available in the private markets and therefore the tech ipo market is essentially a dead market today. However one of the reasons, startups from the dot com era were quick to go public was the frothiness that existed in the stock markets at the time which made IPO’s a very favourable option. This is illustrated in the below graph.

Source : Bloomberg

A closer look at the chart above suggests that stock market valuations are approaching levels experienced during the dot com era which might encourage unicorns to go public in the near future. The state of the global economy directly impacts the funding raised by venture capital firms and tech stocks. An analysis into the state of the global economy during the dot com era and the present situation suggests some interesting parallels. The late 1990’s witnessed a financial crash in Russia, falling oil prices and a strong dollar, a gold rush in silicon valley and a vibrant US economy, weakness in Japan and Germany, falling emerging market currencies. This certainly has parallels with the current scenario in 2015 , where the US economy is experiencing high growth due to low unemployment figures, strong currency, buoyant capital markets and a low interest regime. Funding in tech startups based in the US and in emerging startup markets such as India and China are at all time high and some of the world’s largest economies such as Germany, Japan and China are experiencing a slowdown in growth. Although the chinese economy was not a major player during the dot com crash, the recent stock market crash in China affected stock markets and tech stocks in particular all over the world. This lends credence to the saying that when China sneezes, the world catches a cold and this can have repercussions for the global startups funding market and tech stocks such as Alibaba and Baidu.

© Aditya Haripurkar

INSEAD Master in Finance 2015

22

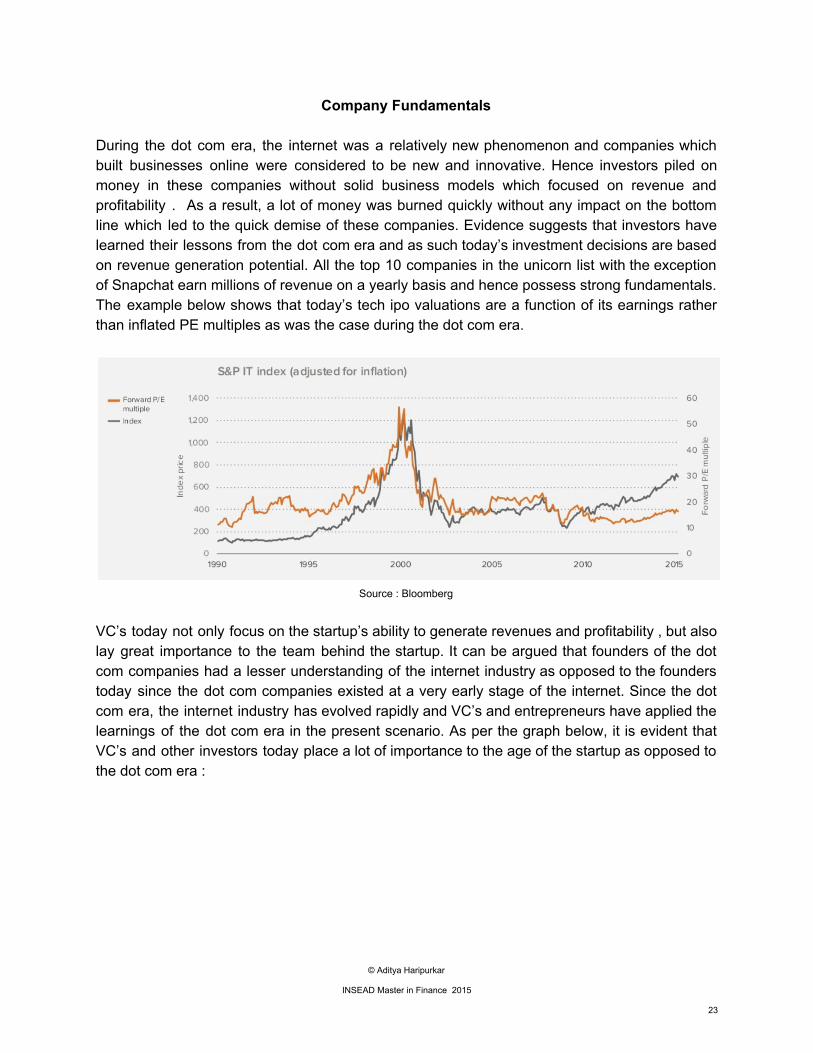

Company Fundamentals

During the dot com era, the internet was a relatively new phenomenon and companies which built businesses online were considered to be new and innovative. Hence investors piled on money in these companies without solid business models which focused on revenue and profitability . As a result, a lot of money was burned quickly without any impact on the bottom line which led to the quick demise of these companies. Evidence suggests that investors have learned their lessons from the dot com era and as such today’s investment decisions are based on revenue generation potential. All the top 10 companies in the unicorn list with the exception of Snapchat earn millions of revenue on a yearly basis and hence possess strong fundamentals. The example below shows that today’s tech ipo valuations are a function of its earnings rather than inflated PE multiples as was the case during the dot com era.

Source : Bloomberg

VC’s today not only focus on the startup’s ability to generate revenues and profitability , but also lay great importance to the team behind the startup. It can be argued that founders of the dot com companies had a lesser understanding of the internet industry as opposed to the founders today since the dot com companies existed at a very early stage of the internet. Since the dot com era, the internet industry has evolved rapidly and VC’s and entrepreneurs have applied the learnings of the dot com era in the present scenario. As per the graph below, it is evident that VC’s and other investors today place a lot of importance to the age of the startup as opposed to the dot com era :

© Aditya Haripurkar

INSEAD Master in Finance 2015

23

Source : Capital IQ, a16z

Startup founders too have understood the importance of demonstrating sustained periods of revenue generating ability and hence hold out going public as opposed to the case in 2000 when companies without any revenues went public.

Source : Google Ventures

© Aditya Haripurkar

INSEAD Master in Finance 2015

24

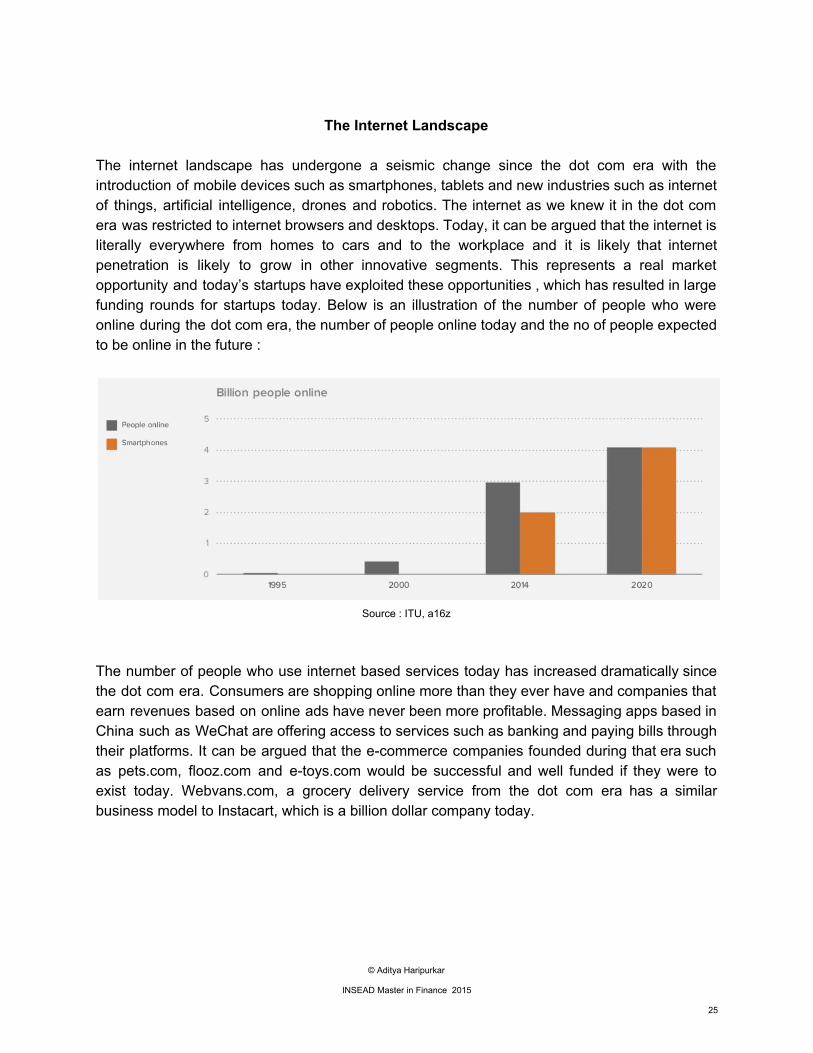

The Internet Landscape

The internet landscape has undergone a seismic change since the dot com era with the introduction of mobile devices such as smartphones, tablets and new industries such as internet of things, artificial intelligence, drones and robotics. The internet as we knew it in the dot com era was restricted to internet browsers and desktops. Today, it can be argued that the internet is literally everywhere from homes to cars and to the workplace and it is likely that internet penetration is likely to grow in other innovative segments. This represents a real market opportunity and today’s startups have exploited these opportunities , which has resulted in large funding rounds for startups today. Below is an illustration of the number of people who were online during the dot com era, the number of people online today and the no of people expected to be online in the future :

Source : ITU, a16z

The number of people who use internet based services today has increased dramatically since the dot com era. Consumers are shopping online more than they ever have and companies that earn revenues based on online ads have never been more profitable. Messaging apps based in China such as WeChat are offering access to services such as banking and paying bills through their platforms. It can be argued that the ecommerce companies founded during that era such as pets.com, flooz.com and etoys.com would be successful and well funded if they were to exist today. Webvans.com, a grocery delivery service from the dot com era has a similar business model to Instacart, which is a billion dollar company today.

© Aditya Haripurkar

INSEAD Master in Finance 2015

25

Final Analysis

From the points analysed above and in the earlier sections of this paper, it is clear that the startup investment activity and the online landscape at present is very different from the one that existed 15 years ago. A tech bubble if it exists today is likely to be very different to the one that occurred at the turn of the century. All economic downturns and shocks in history have had their own unique feature right from the great depression in the 1930’s to the dot com crash in 2000 to the subprime mortgage crisis in 2008. It is however important to take note of learnings of the past and ensure that history does not repeat itself. Although there is evidence that we are currently not in a tech bubble, there are warning signs that are clearly flashing right now which needs to be paid close attention to. A lot of funding is now taking place in the private markets and if companies choose to remain private, the only option for investor exits will occur through acquisitions and this situation hence creates illiquidity. It is true that there is a lot of frothiness in the private markets and that funding rounds and valuations have gone through the roof and much of it is not reflective of actual company requirements and fundamentals. This situation is creating an unhealthy buildup of exposure in the private markets where stakeholders include company founders, employees, investors including venture capital firms, pension funds, institutional investors, mutual funds and sovereign funds. This buildup of exposure has parallels with the subprime mortgage crisis which affected individuals and investors in the entire economic system. This is the tech bubble that is likely to exist in the near future unless preventive action is not taken by all stakeholders. One of the preventive actions requires startups to reduce their burn rate and reserve resources in the event of a downturn. Startups must pursue profitability and revenue growth as their main goal and cut back on excessive spending. An example of this in recent times has been Groupon and Evernote which have recently cut jobs globally. There is also the impending threat of a global slowdown due to the credit crunch in China, weak emerging market currencies and a Fed reserve hike. This can have a contagion effect throughout the startup ecosystem and hence reinforces the importance that startups use their resources wisely. Another preventive action involves investors forcing startups to IPO given the right market conditions. Many unicorns have wasted the opportunity to go public when markets have been at all time highs recently and have instead chosen to sit back and secure private rounds of financing, thereby elevating their valuations. Forcing startups to IPO will also remove the uncertainty that is created around private valuations as public markets will allow everyone to understand the true valuation of the startup. Recent IPO’s such as Shopify, GoPro and Alibaba suggest that going public can not only be good for the startup brand, but also allows everyone to stake a claim in the stock market returns.

© Aditya Haripurkar

INSEAD Master in Finance 2015

26

CONCLUSION

This paper has explored important issues that affect the startup ecosystem such as founding teams, funding rounds, valuation techniques and investor expectations. The potential of the internet to disrupt industries and change the way we lead our lives has never been so great and hence an understanding of these issues is important for both investors and startup entrepreneurs. The industry is undergoing transformation and innovation at a breakneck speed with new categories such as internet of things, robotics, machine learning and artificial intelligence emerging in recent times. We might soon be leading a life where we interact with artificial intelligence assistants to get our work done, ride in self driven cars, rely on battery packs to power our homes and maybe even take holidays to space. Startups all over the world are changing the way we lead our lives and provide solutions to real life problems and need all the encouragement and support from investors. With this in mind, investors have a responsibility to ensure startups with real potential and strong fundamentals get funding support and take preventive action to ensure there are no systemic fallouts that prevent startups from achieving their vision. By taking these steps, we can all look forward to an exciting future envisioned by innovative startups, that make lives easier and convenient for all.

© Aditya Haripurkar

INSEAD Master in Finance 2015

27

References

1. http://www.economist.com/news/leaders/21636742worldeconomy2015willcarrytroublingechoeslate1990spastandfuturetense

2. http://www.forbes.com/sites/quora/2015/06/15/yesthisbubblewillburstbutitsnotexactlylikethedotcombubble/

3. http://berkonomics.com/?p=1214 4. http://www.forbes.com/sites/mariannehudson/2015/03/06/theartofvaluingastartup/ 5. http://avc.com/2011/07/financingoptionspreferredstock/ 6. http://www.startuplawblog.com/2014/02/21/whatisavaluationcap/ 7. http://paulgraham.com/hiresfund.html 8. http://walkercorporatelaw.com/vcissues/whatisaliquidationpreference/ 9. http://techcrunch.com/2012/04/07/convertiblenoteseedfinancings/ 10. http://fundersandfounders.com/howstartupvaluationworks/ 11. https://www.techinasia.com/15mostwellfundedstartupssoutheastasia/ 12. https://www.techinasia.com/indiaovertakeschinaleadasianmarketstechexits/ 13. http://www.nextbigwhat.com/indianstartupmergerreport297/ 14. http://www.nytimes.com/2015/05/23/technology/overvaluedinsiliconvalleybutnotthe

wordthatmustnotbeuttered.html?_r=0 15. http://www.forbes.com/sites/ninaxiang/2014/09/25/warningwatchoutforachinatechbu

bbleburst/ 16. http://www.bloombergview.com/articles/20150706/thereisnotechbubblestillbeworri

ed 17. https://www.macabacus.com/venturecapital/returns 18. http://www.fenwick.com/FenwickDocuments/TheTermsBehindTheUnicornValuations.

pdf 19. http://www.slideshare.net/a16z/stateof49390473 20. http://www.slideshare.net/wearesocialsg/digitalsocialmobilein2015 21. http://www.slideshare.net/KellySchwedland/buildingthebilliondollarsaasunicornceog

uide 22. http://techcrunch.com/2015/07/18/welcometotheunicornclub2015learningfrombillio

ndollarcompanies/#.fgkad6:Lhp0 23. http://tomtunguz.com/privatemarketpublicmarketdisparity/ 24. http://techcrunch.com/2015/03/21/noneedforalarmoverprivatecompanyvaluations/ 25. http://heidiroizen.tumblr.com/post/118473647305/howtobuildaunicornfromscratchan

dwalk 26. http://blogmaverick.com/2015/03/04/whythistechbubbleisworsethanthetechbubble

of2000/ 27. http://techcrunch.com/unicornleaderboard/

© Aditya Haripurkar

INSEAD Master in Finance 2015

28

28. http://fortune.com/2015/09/17/facebookinvestorbreyerbubble/ 29. http://www.angelcapitalassociation.org/data/Documents/Resources/AngelCapitalEducati

on/ACEF__Valuing_Prerevenue_Companies.pdf 30. https://blogs.endjin.com/2015/02/astepbystepguidetotechnologystartupsvaluationa

ndthevcmarket/ 31. http://billpayne.com/2011/02/05/startupvaluationstheventurecapitalmethod.html 32. https://medium.com/gvnotes/techbubblemaybemaybenotb83d6a2dbc9f 33. http://techcrunch.com/2015/03/24/techbubblemaybemaybenot/ 34. http://techcrunch.com/2015/08/28/ourmarketplaceobsessionandbubble/ 35. http://techcrunch.com/2015/08/28/themathbehindsaasstartupvaluation/ 36. http://mobile.nytimes.com/2015/08/27/technology/theupsideofadownturninsiliconvall

ey.html?utm_medium=referral&utm_source=pulsenews&_r=2&referrer= 37. http://techcrunch.com/2015/08/25/afewthoughtsontechstocks/ 38. http://mobile.nytimes.com/blogs/bits/2015/08/25/dailyreportwhatahiccupinstartupla

ndmightlooklike/?smid=linytimes&smtyp=comnews&_r=0&referrer= 39. http://www.wired.com/2015/08/blackmondayunicorns/?mbid=nl_82415 40. http://techcrunch.com/2015/08/24/ripsummer/ 41. http://techcrunch.com/2015/08/23/thereisnosiliconvalleycrashcomingatleastforaw

hile/ 42. http://blog.startupprofessionals.com/2012/11/10rulesofthumbforstartup.html 43. http://aswathdamodaran.blogspot.sg/2015/02/bloodinsharktankpremoneypost.html 44. http://amattn.com/p/venture_capital_math_101_premoney_postmoney_seed_series_a

_b_c_d_up_rounds_and_down_rounds.html 45. http://www.forbes.com/pictures/gfmj45eeli/premoneyvspostmoney/ 46. http://usf.vc/getfunded/avoidingvaluationtrap/ 47. https://home.kpmg.com/xx/en/home/insights/2015/07/venturepulseq2.html?cid=ext_eml

_ent_eml_global_2015_%7bkeyword%7d_venture+pulse+email01_venturepulse&utm_source=ext_eml&utm_medium=eml&utm_term=%7bkeyword%7d&utm_content=venture+pulse+email01&utm_campaign=2015+ent+venturepulse

48. http://techcrunch.com/2015/08/15/navigatingthenewwatersoffundraising/ 49. http://techcrunch.com/gallery/the11bestperformingtechiposofthelastyear/ 50. http://techcrunch.com/2015/08/09/biggerisntalwaysbetterhowabigroundcanhurtyo

urstartup/ 51. http://techcrunch.com/2015/08/07/tenquestionseveryfoundershouldaskbeforeraising

venturedebt/?ncid=rss&utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+Techcrunch+%28TechCrunch%29&sr_share=twitter

52. http://techcrunch.com/2015/07/27/inglobalstartupecosystemrankingsiliconvalleyslipswhilesoutheastasiagainstraction/?ncid=rss&utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+Techcrunch+%28TechCrunch%29#.fgkad6:J5F1

53. http://techcrunch.com/2015/07/18/welcometotheunicornclub2015learningfrombilliondollarcompanies/#.fgkad6:Lhp0

54. http://techcrunch.com/2015/07/16/buyholdsell/

© Aditya Haripurkar

INSEAD Master in Finance 2015

29

55. http://techcrunch.com/2015/06/26/thetechindustryisindenialbutthebubbleisabouttoburst/?ncid=rss&cps=gravity_1730_7218853287940442458

56. http://www.slideshare.net/kleinerperkins/internettrendsv1 57. http://techcrunch.com/2015/05/30/howmuchdoesyourstartupneedtoraise/ 58. http://fundersandfounders.com/howfundingworkssplittingequity/ 59. http://recode.net/2015/05/26/snapchatceothetechbubbleisrealandyesitwillburst/ 60. http://techcrunch.com/2015/05/24/whowillbehurtmostwhenthetechbubbleburstnot

vcs/#.fgkad6:Hs05 61. http://techcrunch.com/2015/05/16/bubble20/ 62. http://recode.net/2015/05/10/heresonethingallthebilliondollarunicornshaveincomm

on/ 63. http://www.theverge.com/2015/4/17/8431989/slacksmassivenewfundingroundisever

ythingamazingandinsane 64. http://techcrunch.com/2015/04/08/securingahugegrowthround/ 65. http://techcrunch.com/2015/04/08/theimplicationsoftheseedfundingboom/?ncid=rss&

utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+Techcrunch+%28TechCrunch%29

66. http://techcrunch.com/gallery/letstalkaboutmoney/ 67. http://www.theguardian.com/money/usmoneyblog/2015/feb/22/snapchattrexventures

dotcombubble 68. http://techcrunch.com/2015/02/15/startupslatestagevaluationsandbull

© Aditya Haripurkar

INSEAD Master in Finance 2015

30