PAKISTAN MICROFINANCE REVIEWAnnual Assessment of the Microfinance Industry

FINANCIAL SERVICES FOR ALL

2012

2

Produced by: Pakistan Microfinance NetworkArt Direction: Sumaira SagheerDesign & Layout: Uzma ToorPhotocredits: Retroactive Studios LibraryPrinted at: Pangraphics

© 2013 Pakistan Microfinance Network

PAKISTAN MICROFINANCE REVIEWAnnual Assessment of the Microfinance Industry

FINANCIAL SERVICES FOR ALL

EDITORIAL BOARD

Mr. Ghalib Nishtar Chairperson Editorial Board President, Khushali Bank

Dr. Saeed Ahmed Head of Department, Agriculture Credit and Microfinance Department State Bank of Pakistan

Mr. Blain Stephens COO and Director of Analysis Microfinance Information eXchange, Inc. (MIX)

Mr. Raza Khan Statistics & Results Adviser, Results & Evaluation Team- Economic Growth Group Department for International Development (UK)

Mr. Yasir Ashfaq Group Head, Financial Services Group Pakistan Poverty Alleviation Fund

Mr. Abrar Mir EVP and Group Head, Digital Money & Mobile Payments, United Bank Limited (UBL)

Mr. Masood Safdar Gill Director Program, Urban Poverty Alleviation Program National Rural Support Programme

PMN TEAMMs. Aban Haq Advisor

Mr. Ali Basharat Author and Managing Editor

Mr. Ammar Arshad Co-Author

ACRONYMS and ABBREVIATIONS

AC and MFD Agriculture and Microfinance Division

ADB Asian Development Bank

BPS Basis Points

CAR Capital Adequacy Ratio

CIB Credit Information Bureau

CGAP Consultative Group to Assist the Poor

CNIC Computerized National Identity Card

CPP Client Protection Principles

CPI Consumer Price Index

CPC Consumer Protection Code

DFID Department for International Development, UK

DPF Depositor’s Protection Fund

ECA Eastern and Central Europe

EUR Euro

FIP Financial Inclusion Program

FMFB First Microfinance Bank Ltd.

FSS Financial Self Sufficiency

FY Financial Year

GBP Great Britain Pound

GDP Gross Domestic Product

GLP Gross Loan Portfolio

GNI Gross National Income

GoP Government of Pakistan

IAFSF Improving Access to Financial Services Fund

IFAD International Fund for Agricultural Development

IFC International Finance Corporation

JIWS Jinnah Welfare Society

KBL Khushhali Bank Ltd.

KF Kashf Foundation

KIBOR Karachi Inter-Bank Offering Rate

KMFBL Kashf Microfinance Bank Ltd.

KP Khyber Pakhtunkhwa

MCGF Microfinance Credit Guarantee Facility

MCR Minimum Capital Requirement

MENA Middle East and North Africa

MFB Microfinance Bank

MFCG Microfinance Consultative Group

MF-CIB Microfinance Credit Information Bureau

MFP Microfinance Provider

MFI Microfinance Institution

MIS Management Information System

NADRA National Database and Registration Authority

NGO Non-Governmental Organization

NFLP National Financial Literacy Program

NMFB Network Microfinance Bank Limited

NPLs Non Performing Loans

NRSP National Rural Support Programme

OSS Operational Self Sufficiency

PAR Portfolio at Risk

PBA Pakistan Banks’ Association

PKR Pakistan Rupee

PMN Pakistan Microfinance Network

PPAF Pakistan Poverty Alleviation Fund

PRISM Programme for Increasing Sustainable Microfinance

PRSP Punjab Rural Support Program

PTA Pakistan Telecommunication Authority

ROA Return on Assets

ROE Return on Equity

RSP Rural Support Programme

SBI Shore Bank International

SBP State Bank of Pakistan

SC Smart Campaign

SECP Securities and Exchange Commission of Pakistan

SPTF Social Performance Task Force

SME Small and Medium Enterprise

SRSO Sindh Rural Support Organization

SVDP Soon Valley Development Program

TMFB Tameer Microfinance Bank Ltd

UBL United Bank Limited

USD United States Dollar

HIGHLIGHTS

Year 2009 2010 2011 2012

Active Borrowers (in Million) 1.4 1.6 1.7 2.0

Gross Loan Portfolio (in PKR Billion) 16.8 20.2 24.8 33.1

Active Women Borrowers (in Million) 0.6 0.8 0.9 1.3

Branches 1,221 1,405 1,550 1,460

Total Staff 11,557 12,005 14,202 14648

Total Assets (in PKR Billion) 30.4 35.8 48.6 60

Deposits (in PKR Billion) 7.2 10.1 13.9 20.8

Total Debt (in PKR Billion) 23.2 27.5 38.3 24.9

Total Revenue (in PKR Billion) 6.4 7.5 10.1 12.5

OSS (in Percent) 104.6 99.7 108.4 109.5

FSS (in Percent) 86.8 81.7 100.5 107.5

PAR > 30 (in Percent) 3.4 4.1 3.2 3.7

6

CONTENTS

SECTION 1: THE YEAR IN REVIEW

1.1. Macro-economy and the Microfinance Industry . . . . . . . . . . . . . . 101.2. Policy and Regulatory Environment . . . . . . . . . . . . . . . . . . . . . 121.3. Microfinance Industry Initiatives . . . . . . . . . . . . . . . . . . . . . . . 141.4. Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

SECTION 2: INDUSTRY PERFORMANCE

2.1. Industry Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 252.2. Scale and Outreach . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 262.3. Financial Structure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 342.4. Funding Profile . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 362.5. Profitability and Sustainability . . . . . . . . . . . . . . . . . . . . . . . . 372.6. Efficiency and Productivity . . . . . . . . . . . . . . . . . . . . . . . . . . . 402.7. Risk Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 422.8. Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

SECTION 3: THE WAY FORWARD

3.1. Challenges . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 463.2. Opportunities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

ANNEXURES

Annexure A-1: Performance Indicators-Industry Aggregate (2007-2011) . 56Annexure A-2: Performance Indicators-Individual Institutions and Peer Groups (2012) . . . . . . . . . . . . . . . . . . . . . . . 64Annexure B: Regional Benchmarks 2010 . . . . . . . . . . . . . . . . . . . . . . 94Annexure C: Sources of Data 2012 . . . . . . . . . . . . . . . . . . . . . . . . . 96Annexure D: Adjustments to Financial Data . . . . . . . . . . . . . . . . . . 106Annexure E: Terms and Definitions . . . . . . . . . . . . . . . . . . . . . . . . 108

SECTION ONE

THE YEAR IN REVIEW

CONTENTS

1 Macro-economy and the Microfinance Industry

2 Policy and Regulatory Environment

3 Microfinance Industry Initiatives

4 Conclusion

“The key to ending extreme poverty is to enable the poorest of the poor to get their foot on the ladder of development.”

Jeffrey d. Sachs

The year 2012 saw the industry aiming for growth and profitability although the external environment remained challenging with the adverse security situation and continuing energy shortages in Pakistan. Despite these challenges the industry experienced higher growth in outreach as compared to the last five years1, continued entry of new players and ongoing regulatory and policy reforms. Within the microfinance industry, the total Gross Loan Portfolio (GLP) continued to grow at a fast pace backed by higher loan sizes. Moreover, the Microfinance Banks (MFBs) experienced tremendous growth in deposits.

Pakistan’s economy remained sluggish in 2012. Inflation witnessed a slight decline leading to gradual easing of monetary policy by the State Bank Pakistan. However, the decrease in policy rate did not result in increased private sector borrowing due to heavy borrowing by the government to finance an expanding fiscal deficit.

Within the microfinance sector, there was a major undertaking on the policy and regulatory front as efforts to bring non-bank MFPs under a regulatory umbrella were initiated and regulations for micro-insurance moved forward. Also, the Small and Medium Enterprise (SME) Guarantee facility offered by the State Bank of Pakistan (SBP) was extended to MFBs allowing them to upscale loans while the Microfinance Credit Guarantee Facility (MCGF) coverage was also extended to debt capital markets. In addition, the Pakistan Poverty Alleviation Fund (PPAF), the national apex, aligned the pricing of its loans with market-based floating interest rates.

1: MicroWatch, A quarterly update on microfinance outreach in Pakistan.

SECTION ONE

The year also saw a number of new initiatives being launched and earlier ones being built upon. Branchless banking saw the entry of two new players and witnessed continued growth. The national roll out of the Microfinance – Credit Information Bureau (MF-CIB) took place in June. A Corporate Governance Initiative is underway to strengthen governance practices in the industry while a number of social performance initiatives have also been launched to improve client protection and promote pricing transparency.

MACRO-ECONOMY AND THE MICROFINANCE INDUSTRY

Pakistan’s economy witnessed modest growth of 3.7 percent in the financial year 2012 against a target of 4.2 percent2. The under-performance was mainly due to security challenges, energy shortages and catastrophic flooding in the last two consecutive years. The growth was broad based and evenly distributed across agriculture, industry and services sectors. In comparison, the microfinance industry outperformed overall economic growth as outreach increased by 10 percent and GLP grew by 23 percent in the same time period3.

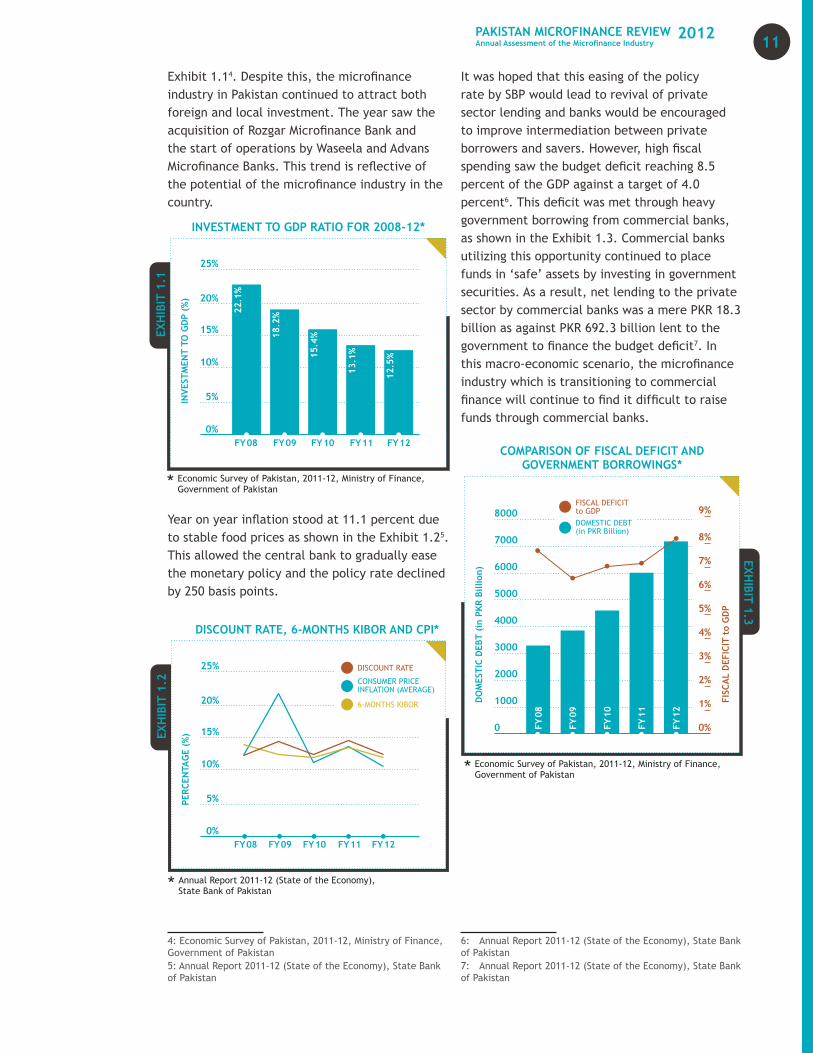

Robust private consumption, the vibrant informal economy, strong worker remittances and high fiscal spending were identified as the main drivers of growth. Investment continued to remain sluggish for the fifth consecutive year with the Investment to GDP ratio further declining to 12.5 percent as shown in the 2: Economic Survey of Pakistan, 2011-12, Ministry of Finance, Government of Pakistan3: MicroWatch, A quarterly update on microfinance outreach in Pakistan.

THE YEAR IN REVIEW

10

Exhibit 1.14. Despite this, the microfinance industry in Pakistan continued to attract both foreign and local investment. The year saw the acquisition of Rozgar Microfinance Bank and the start of operations by Waseela and Advans Microfinance Banks. This trend is reflective of the potential of the microfinance industry in the country.

Year on year inflation stood at 11.1 percent due to stable food prices as shown in the Exhibit 1.25. This allowed the central bank to gradually ease the monetary policy and the policy rate declined by 250 basis points.

4: Economic Survey of Pakistan, 2011-12, Ministry of Finance, Government of Pakistan5: Annual Report 2011-12 (State of the Economy), State Bank of Pakistan

It was hoped that this easing of the policy rate by SBP would lead to revival of private sector lending and banks would be encouraged to improve intermediation between private borrowers and savers. However, high fiscal spending saw the budget deficit reaching 8.5 percent of the GDP against a target of 4.0 percent6. This deficit was met through heavy government borrowing from commercial banks, as shown in the Exhibit 1.3. Commercial banks utilizing this opportunity continued to place funds in ‘safe’ assets by investing in government securities. As a result, net lending to the private sector by commercial banks was a mere PKR 18.3 billion as against PKR 692.3 billion lent to the government to finance the budget deficit7. In this macro-economic scenario, the microfinance industry which is transitioning to commercial finance will continue to find it difficult to raise funds through commercial banks.

6: Annual Report 2011-12 (State of the Economy), State Bank of Pakistan7: Annual Report 2011-12 (State of the Economy), State Bank of Pakistan

11PAKISTAN MICROFINANCE REVIEWAnnual Assessment of the Microfinance Industry

2012

POLICY AND REGULATORY ENVIRONMENT

Pakistan’s regulatory environment and regulatory framework for microfinance industry, continues to be recognized as one of the best globally. The Economist’s Global Microscope on Microfinance Business Environment continues to rank Pakistan’s legal and regulatory framework among the top 3 in the world and considers Pakistan as having one of the most enabling business environment for microfinance regionally and globally.

Regulatory Framework for Non-Bank MFPs

At present, Microfinance Providers (MFPs) can be categorized into three peer groups namely Microfinance Banks (MFBs), Microfinance Institutions (MFIs) and Rural Support Programs (RSPs). However, only MFBs are regulated and supervised by the State Bank of Pakistan (SBP). Currently, the MFIs and RSPs fall under four regulatory frameworks and the respective regulatory authorities are as shown in the Table 1.1.

Presently, the industry has grown to a size where it is felt that regulation is needed for further growth. The regulatory framework would provide institutional and legal cover for the sector and create access to recourse mechanisms for institutions and clients, protecting the industry against willful organized defaults as witnessed in Punjab in 2008-9. It will also help attract investment for the sector to meet its funding needs through greater standardization in disclosures, clarity in legal status and improved governance practices that will boost investor confidence. Moreover, it would lead to a level playing field for all MFPs as currently only MFBs face regulatory and statutory restrictions. Realizing this need, the Pakistan Microfinance Network (PMN) recently established contact with Securities and Exchange Commission of Pakistan (SECP), the regulator of non-bank financial institutions in the country with the objective of developing a regulatory framework for the non-bank MFPs. Subsequent to the meeting a standing committee had been formed on the issue which is chaired by the Chairman SECP and includes all

the pivotal players of the industry namely the SBP, Ministry of Finance (MOF), PMN, PPAF, and leading MFPs. It is hoped that the regulatory framework shall be finalized in the current year.

Extending of SME Guarantee Facility to MFBs

Following the permission to start enterprise lending by MFBs, SBP also extended the SME credit guarantee facility to these institutions8.

SME growth is imperative for any developing country and access to formal finance for this sector is a major problem hindering the growth of small and micro enterprises, particularly in the rural areas. Given the impediments in the way of small and rural enterprises in Pakistan to raise capital from formal financial channels, the Credit Guarantee Scheme is designed to overcome this credit bottleneck. The scheme targets small enterprises and farmers with economic landholding i.e. 12 acres, without any specific regional or cluster restrictions, across

8: IHandSMEFD Circular Letter No.14 of 2012 dated December 4, 2012

TABLE 1.1: LEGAL FRAMEWORK AND REGULATOR*

LEGAL FRAMEWORK

NUMBER OF MFPs REGISTERED UNDER LEGAL FRAMEWORK

REGULATOR SCOPE

The Societies Registration Act, 1860

6 Provincial Government

Deliver Charity Oriented Welfare Services while being fully dependent upon Grant Funding

Voluntary Social Welfare Agencies Ordinance, 1961

2 Provincial Government

To provide legal cover to societies established for promotion of science, literature and fine arts or for charitable purposes

Trust Act, 1882

1 Provincial Government

Can be created for any lawful purpose including microfinance

Companies Ordinance, 1984

9 Securities and Exchange Commission of Pakistan (SECP)

Allows for Microfinance Activities but limits the range of financial services that can be provided. Does not allow for equity investments and prohibits issuing dividends.

* Regulating Pakistan’s Non-Bank Microfinance Institutions by Mehr Shah, MicroNOTE No: 14, Dec 2011

12

the country. Preference for use of the Guarantee Fund is given to fresh and collateral-deficient borrowers.

The SME Credit Guarantee Facility is also part of the Financial Inclusion Program (FIP) but unlike Microfinance Credit Guarantee Fund (MCGF) is not a wholesale guarantee but an enterprise guarantee. The scheme guarantees up to 40 percent of fresh portfolio of financing to small enterprises and farmers. Instead of evaluating each and every loan being extended by banks, the portfolio (principal amount only) of loans (extended after allocation of Credit Guarantee Limit) of a financial institution is guaranteed under the Scheme to the extent of its allocated Credit Guarantee Limit. Banks may apply a market-based mark-up rate under the scheme, as there is be no cap on pricing of loans. The loans for short term and medium term working capital for a period up to 3 years, with maximum amount of PKR 15 million for small enterprises and PKR 2 million for farmers with economic landholdings are guaranteed.

As of now, only one MFB has sought and been allocated a line from the guarantee fund. The remaining MFBs are still in the process of planning to tap the facility and have yet to utilize the opportunity.

Micro-Insurance Regulations

Microfinance does not only meet the borrowing needs of the clients but also provides them with avenues of saving and protection against risks through micro-insurance (MI) products.

At present, micro-insurance in Pakistan is being provided by 19 MFPs. The number of policy holders stood at 2.9 million and sum insured at PKR 36.5 billion. Micro-insurance growth, however, has exhibited a volatile trend over the years as institutions struggle to get the models, products and pricing right. Currently, only two products are being offered i.e. health and credit-life insurance, with the latter accounting for 57 percent of the sum insured. In addition, pilot projects have been launched by the national apex to extend insurance coverage to agriculture sector.

Keeping in view the fragmented nature of the market, the Securities and Exchange Commission Pakistan (SECP) as the regulator of the insurance industry in the country stepped in and is taking a number of steps to regulate and develop micro-insurance in Pakistan. Initially, it commissioned a diagnostic study in collaboration with World Bank that maps the supply and demand for micro-insurance. In addition, a working group9 has been formed under the auspices of to facilitate the development of a regulatory framework for micro-insurance and a development strategy for this segment. The working group has completed its work in this context and the documents will soon be made available for public comment. The group and SECP is also looking into the idea of setting up specialized micro-insurance companies, which will provide micro-insurance products only and have limited capital requirements – a model parallel to the MFBs in the banking sector.

Extending MCGF Coverage to Capital Markets

The State Bank of Pakistan (SBP) through a circular in June 201210, allowed MFPs to raise funds from non-bank sources / capital markets under the Microfinance Credit Guarantee Facility (MCGF). This step effectively extends coverage of the MFCG to debt capital markets.

SBP has taken a number of steps to promote lending to the MFPs through the commercial banking sector. MCGF is big part of this effort. Launched in 2008 with a GBP 10 million grant from UKAID as part of the overall Financial Inclusion Program (FIP), the facility is one of two guarantee funds available to MFPs in the country. The facility aims to allow MFPs to mobilize funds from banks for onward lending to microfinance clients. In order to meet the increasing need of funds by the sector to expand microfinance outreach, the guarantee’s coverage has been extended to non-bank sources. This will allow the MFPs to not only fund their growth but also allow them to diversify their sources of funds by tapping debt markets.

9: The group comprises of a cross section of stakeholders including MFPs, PMN, PPAF, DFID, Insurance Association of Pakistan (IAP), insurance companies and insurance brokers.10: AC and MFD Circular No. 03 of 2012 dated June 21, 2012

13PAKISTAN MICROFINANCE REVIEWAnnual Assessment of the Microfinance Industry

2012

BOX

1.1

In the current scenario where there is heavy public sector borrowing, practitioners can use debt markets to meet their financing needs. Moreover, this will allow capital markets to reduce their risk perception of the industry and lead to enhanced recognition in the investor community. MFPs have been quick to recognize this opportunity and subsequent to the revision of the MFCG guidelines, TMFB issued retail bonds. (See Box 1.1 for details)

Revision of PPAF Pricing Policy

In continuation of its policy to transition from subsidized lending to commercial based lending, PPAF revised its pricing policy of loans being extended to microfinance industry in the year 2012. Interest rates moved towards market based prices with the aim of transforming the industry into a sustainable and viable part of the financial landscape. Earlier, loan sizes below PKR 500 million were charged flat 8 percent.

In the early days of microfinance, PPAF focused on developing and strengthening institutions thus charges were subsided substantially to allow for new players to enter the market and get access to funds for on-lending. Now as institutions have become more robust and sustainable, PPAF has moved towards market based floating interest rates for all loan sizes. Another reason was to correct the pricing anomaly which resulted in growing firms being charged at commercial rates when funds borrowed by them from PPAF increased above PKR 500 million.

Interest rates are now benchmarked with KIBOR. Non-for-profit organizations are extended funding facilities at 6-month KIBOR whereas for profit entities the rate is 6-months KIBOR + 1. Keeping in view large swathes in the country that are yet to be tapped, PPAF continues to subsidize loans for MFPs working in deprived areas where the cost of delivery remains significantly higher as compared to the more developed areas.

MICROFINANCE INDUSTRY INITIATIVES

BRANCHLESS BANKING

The previous year witnessed branchless banking continuing to prosper in terms of entrance of new players and products as well as usage. Pakistan has been described as one of the most innovative places in the world for mobile banking services, with the SBP playing a leading role in its development.”

Recently, the branchless banking sector of Pakistan saw the entrance of two new players - Mobicash and Timepey, bringing the total number of branchless banking deployments to four in the country. Mobicash is an example of a Mobile Network Operator (MNO) entering the market through launching a green field MFB while Timepey is a unique model with a commercial bank and MNO partnering to launch branchless banking services.

Waseela Microfinance Bank in partnership with Mobilink introduced Mobicash as their branchless banking solution. The Mobicash suite of financial services currently includes only domestic remittances and bill payments. However, in the near future, Mobicash expects to introduce a variety of offerings such as ‘Mobile Wallets’, making it possible for customers to transact money directly through their Mobilink mobile connections.

Askari Bank Limited in partnership with Zong launched its branchless banking service under the brand name ‘Timepey’. Unlike the

LAUNCH OF RETAIL BONDS BY TMFB

TMFB successfully listed its Term Finance Certificates (TFCs) & Tameer Sarmaya Certificates (TSC) on the Karachi Stock Exchanges in early 2013. This is the second time a MFP has issued TFCs to raise financing but a first for MFBs. The TFCs have been issued for one year (13 months) and two year (24 months) time periods at a rate of 12 percent and 12.5 percent respectively, with a monthly profit payment mechanism. The total amount of TFCs is PKR 1 billion and the issue is partially secured against the MCGF. Standard Chartered was the lead arranger of the issue and have been assigned an “A” rating by JCR-VIS.

14

BOX

1.2

other BB platforms in the market such as Telenor (EasyPaisa) and Mobilink (Mobicash) which involve an MNO’s direct ownership of a microfinance bank, Timepey is an alliance between a commercial bank and an MNO. The three main services offered by Timepey include Utility Bill Payment, Mobile Account and Funds Transfer.

Table 1.2 shows the list of different players in the branchless banking sector and services being offered currently.

Most of the products being offered are geared towards payments. Branchless banking operators need to go beyond payments and transfer and expand into savings, insurance and loan disbursements solutions. Only then can branchless banking provide a path to scale for financial inclusion.

With the entry of new players, branchless banking services in Pakistan are heading towards growth and healthy competition. The current year witnessed impressive growth on all fronts, the most prominent being the remarkable growth in Mobile-wallets (see Box 1.2) which touched 1.8 million by the end of September 201211. Exhibit 1.4 highlights the growth in branchless banking in the year 2012.

More than 35.3 million transactions worth Rs. 151 billion have been conducted through branchless banking channels from January 2012 to December 201212. The average size of the transaction was PKR 4,278 and bill payments and top ups remained the dominating activity among the transactions with a 45 percent share.

11: Branchless Banking Newsletter, Multiple Issues, State Bank of Pakistan12: Branchless Banking Newsletter, Multiple Issues, State Bank of Pakistan

MOBILE WALLETS

M-Wallet or Mobile Wallet refers to a payment service performed on or via a mobile device. M-Wallets are much like Prepaid Cards – they need to be loaded with money prior to use. However, funds held by the M-Wallet are securely accessed directly from the mobile phone. Just like the prepaid card, an M-Wallet can be topped-up via agent or loading partner. As soon as funds are loaded the subscriber can pay for goods and services or transfer funds from their Mobile Wallet through a simple SMS. Similarly, an employer can also pay his workers directly onto their M-Wallets through bank transfer.

TABLE 1.2: SERVICES BEING OFFERED BY VARIOUS OPERATORS

UBL OmniFor walk-in customers � Account opening with available

ATM cards � Free Bills Payment � Free Mobile Top-Up � Instant Domestic Remittance � Online Shopping � Broadband Bills Payment

For account holders � Account Opening � Cash Deposit and Withdrawal � Bill Payments � Domestic Remittance � Internet Banking � SMS services

Telenor EasyPaisaMobile Account Services � Money transfer � Bill Payment � International Home Transfer � Donations � Easy Load

Easy Pay for Companies � Real time payments report � Payment collection � Funds transfer � Easy payment reconciliation

Khushaal Accidental and Death Insurance

Easy Paisa Ticketing Solution

Zong TimePeyConsumer Services � Money Transfer � Bill Payment � Mobile Top-up � Cash withdrawal and deposit

Corporate Services � Salary Disbursement Solution

Mobilink MobicashConsumer Services � Money Transfer � Bill Payment

15PAKISTAN MICROFINANCE REVIEWAnnual Assessment of the Microfinance Industry

2012

Microfinance - Credit Information Bureau (MF-CIB)

Credit Bureaus play a vital role in mitigating the challenges faced by microfinance ranging from information asymmetry, adverse selection, and moral hazard to over-indebtedness due to multiple borrowing. The credit information provided by the bureau helps financial institutions reduce risks, loan process time, costs and default rates. For borrowers, it leads to lower interest rates, making loans more affordable and more widely available. Analyses of the delinquency crises in Andhra Pradesh, India in 2009 and Punjab, Pakistan, in 2008/9 show that improved credit information about the borrowers could have helped in averting these disasters. Consequently, to address the above mentioned issues, a pilot MF-CIB was initiated in Pakistan in 2010.

PMN, with support of SBP, PPAF, UKaid and the International Finance Corporation (IFC), launched the nation-wide rollout of the MF-CIB in June 2012. The objective of the project is to make MFPs “Bureau Ready and institutionalize MF-CIB in the microfinance ecosystem” by ensuring that MFPs are reporting their data on time and making enquiries on every loan application received. Some major developments and milestones were achieved in 2012 as the national roll out moved forward. A major achievement was the collection of 2.2 million records, which currently are being reconciled. Also, National Database and Registration Authority (NADRA) completed verification of approximately 2.23 million records which greatly increases the integrity of the data repository. The consolidation of the NADRA verified data is in process and would go live in 2013. Most organizations who did not participate in the pilot have been signed up for the MF-CIB and their technical capacity vis-à-vis data reporting and inquiries is being built through trainings, workshops, dedicated CIB Coordinators and technical and financial support in MIS up-gradation. Not only are nearly all PMN members now on board but also PPAF partners that are not members of PMN have been signed up. In the first phase, the emphasis has been on the collection and verification of data to improve data integrity as the quality of the credit report

would ultimately depend on the reliability and consistency of the data in the repository. Also, in order to give exposure to its members regarding the functioning of Credit Bureaus, PMN organized two exposure visits to study the working of a mature bureau in Bolivia and South Korea called “InfoCred” and “NICE” respectively.

As data collection becomes institutionalized, the next focus will be on generation and use of the credit report. PMN is working with MFPs to make them bureau ready and ensuring that their staff is able to analyze the report and make effective credit decisions. To ensure effective monitoring of the project, all donors and PMN agreed to form a project steering committee which comprises of individuals from SBP, PPAF, IFC, UKaid and PMN policy committee. This committee is responsible for providing strategic input, oversight and policy level interventions for effective implementation of the national rollout of MF-CIB.

With the implementation of MF-CIB it is certain that there will be significant developments of credit market discipline in the microfinance industry.

Social Performance

Keeping in view that microfinance is a double bottom line industry where social performance is as important as sustainability and profitability; a number of new initiatives were launched in 2012 by PMN and PPAF.

Pricing Transparency Initiative

PMN in partnership with MicroFinance Transparency and in collaboration with the SBP, PPAF and UKaid has launched a Transparent Pricing Initiative for Pakistan. The aim is to provide an opportunity for microfinance service providers in the Pakistan market to exchange information, standardize pricing practices and demonstrate their commitment to transparent and responsible pricing. Non-transparency has not only damaged the public image of the industry, but has encouraged political and regulatory reactions, such as interest rate caps, that have reduced the availability of credit to the poor in other countries. Via the Transparent

16

Pricing Initiative in Pakistan, MicroFinance Transparency will encourage Pakistan’s microfinance industry to publicly demonstrate its commitment to pricing transparency, integrity and responsible finance. Embarking on this initiative at the industry level will help dispel any threats to microfinance providers in terms of first mover disadvantages that exist in implementing transparent pricing. This initiative will also help provide a level playing field for all types of microfinance providers regardless of legal status to ensure their pricing is transparent to the consumers, and create an environment in which transparency leads to a strengthening of the local microfinance industry.

Social Performance Implementation Fund for Advanced Networks

PMN has been selected to be the part of Global Implementation Program of the Universal Standards for Social Performance Management (USSPM). The Global Implementation Program of the USSPM, funded by the Ford Foundation and managed by the Microfinance Centre (MFC), is working with advanced networks from all over the world to pioneer the roll-out of the USSPM in each of the nine selected countries.

As part of the program PMN will work with its member MFPs to implement the following areas within the USSPM:

1) Ensuring Board, management and employee commitment to social goals

2) Design products, services, delivery models and channels that meet client needs and preferences

3) Treating clients responsibly

Meeting the Standards signifies that an MFP has “strong” social performance management (SPM) practices. It is hoped that the implementation of Universal Standards would allows MFP to assess informally their current level of social performance management, guide their strategies and self-regulate their social performance.

Client Protection Monitoring Initiative, in partnership with the Smart Campaign

This initiative is being conducted by the PMN in partnership with the Smart Campaign at the Centre for Financial Inclusion at ACCION International with support from the State Bank of Pakistan (SBP) under the Financial Inclusion Program (FIP).

The major objective of this initiative is to help member MFPs monitor their client protection, and provide a baseline of client protection practices in place, with the aim of improving client protection at all member MFPs in accordance with globally accepted benchmarks (Smart Campaign’s Client Protection Principles). It involves conducting Smart assessments of all member MFPs during 2013 to 2015.

Client protection can only be achieved in a sustained manner if its core values are institutionalized through practice at MFPs. A key step then is to institutionalize a monitoring process within practitioners to look at compliance with principles of client protection. PMN feels that conducting assessments of MFPs on the client protection principles will help to provide a baseline of existing client protection practices at MFPs, help strengthen monitoring and control within the practitioners for future, and ultimately lead to successful institutionalization of client protection measures. Additionally, building capacity of other players in the industry (like technical assistance providers) will help create a supply of CP monitoring services externally.

Truelift (formerly Seal of Excellence)

PPAF and Microcredit Summit Campaign have signed a Memorandum of Understanding (MOU) to launch the global initiative of Truelift for poverty outreach and transformation in Pakistan. Truelift aims to recognize microfinance institutions that are doing the most to help poor households lift themselves out of poverty and improve their lives. The International Fund for Agricultural Development (IFAD) has provided financial

17PAKISTAN MICROFINANCE REVIEWAnnual Assessment of the Microfinance Industry

2012

support for this exercise which is also being replicated in Jordan, Bolivia, India, Senegal, Peru, South Africa and the Philippines. PPAF is participating in a beta test of the Seal of Excellence in Pakistan through a strategic partnership with the Microcredit Summit Campaign. The seal would ensure that the rights of clients are protected, the focus remains on impact and the double bottom line is assured.

The overall goal of Truelift is to accredit microfinance institutions which are responsible, genuinely inclusive and contributing to positive change in the society. The Truelift looks into all aspects of clients’ protection, social performance and several additional indicators. Institutions will be able to get certified once they undergo an assessment carried out by a firm contracted by the Seal of Excellence. An international rating agency is currently engaged in the assessment of two microfinance institutions in Pakistan.

Crop and Livestock Micro-Insurance Products

IFAD and PPAF through a strategic partnership with the SECP designed an index-based crop insurance and livestock insurance product under the Program for Increasing Sustainable Microfinance (PRISM). The purpose of this initiative is to implement action research on a sustainable market based crop and livestock insurance model which best suits the economic needs and social characteristics of the country with particular focus on small and marginal income farmers. In line with IFAD’s key focus on agricultural development, this product is being rolled-out as a market based commercially viable model.

Keeping this in mind, PPAF is piloting two products which are a Weather-Indexed Crop Insurance and a Live-Weight Livestock Insurance. Alfalah and United Insurance are the insurers for the pilots, and the products are being disseminated to communities in Soon Valley and Talagang through partner organizations, Soon Valley Development Program (SVDP) and National Rural Support Program (NRSP).

In addition to these pilots, PPAF is also currently in the process of implementing pilots for livestock insurance in Tharparkar, while also building a product specifically for milk-producing animals in Southern Punjab. Going forward, these are expected to scale up to include the hybrid ‘live-weight’ livestock insurance product in other areas of Pakistan.

Inclusion of MFBs in SBP’s Agriculture Disbursement Monitoring Framework

MFBs have been included in SBP’s Agriculture Disbursement Monitoring Framework since July 2011. Rural borrowers make up 56 percent of the total active borrowers (see Section 2) for the microfinance sector. Inclusion of MFBs in the framework is recognition of the role being played in agri lending by the microfinance industry in the country. MFBs and non-bank MFIs enjoy a healthy penetration in the rural areas as compared to other financial institutions. There are avenues which can be explored by financial institutions routing funds for agriculture lending through MFPs.

Microfinance Impact Assessment

During the last one decade, the sector has grown through government support in the form of an enabling policy framework and public funds (through donor grants, smart subsidies and tax exemption). This inflow of public money and other concessions have generated a demand to demonstrate impact. In context of the recent crises in microfinance in different countries, stakeholders, such as governments, donors and investors are beginning to question the impact microfinance is having on the lives of the poor. Even within the microfinance sector in Pakistan, there is a need to look inwards and evaluate whether the current strategies, methodology, products and services are serving the ultimate goal of creating social impact.

In order to fill the current knowledge gaps with respect to the impact of microfinance services on the lives of microfinance clients, the Pakistan Microfinance Network (PMN) proposes to conduct a comprehensive impact evaluation study to empirically estimate the social benefits accruing to microfinance clients.

18

The proposed impact evaluation study will seek to overcome the limitations of the existing body of knowledge on the impact of microfinance in Pakistan and deliver more sound and robust estimates of benefits accruing to the microfinance clients, in terms of higher income/ lower poverty levels, improved education and health outcomes and greater empowerment of women, amongst others.

ACQUISITIONS AND ENTRY OF NEW PLAYERS

The year 2012 witnessed continued investor interest in the industry. Two new green field MFBs entered the market and one existing MFB was acquired. Acquisitions and entry of new MFBs at one place is positive reflection on the market potential but also shows investor’s confidence in the business models of MFBs. The series of acquisitions and entry of new players over the last few years reflect positively on the industry’s potential in the country and also ensures that these entities are adequately capitalized. These institutions can if required leverage the balance sheets of their sponsors to raise funds.

Waseela Microfinance Bank:

Waseela Microfinance Bank Limited (WMBL) started its operations as a microfinance bank, with its first branch in Islamabad, in April 2012. The State Bank of Pakistan had issued a license to the bank earlier but the bank was unable to commence operations as it had not met SBP’s requirement of maintaining a minimum asset base of PKR 1 billion.

Later in the year, WMBL also announced the commencement of commercial operations for branchless banking on the back of SBP’s approval to launch Mobile Financial Services (MFS) in Pakistan. WMBL is a fully owned subsidiary of Orascom Telecom Holdings, and a sister concern of Mobilink – Pakistan Mobile Communications Limited (PMCL).

WMBL is the 10th licensed microfinance bank in Pakistan under the MFI Ordinance 2001. It is currently operating with four branches: one in the south region, two in the central region and one in the north region. WMBL plans to introduce mass-market financial products for

providing more choices and benefits to the people of Pakistan, which include cash deposit and withdrawal, fund transfer from account-to-account and person-to-person, Mobilink top-ups and utility bill payment amongst other services.

Advans Pakistan Microfinance Bank

Advans Pakistan Microfinance Bank (APMB) was provided with a license to operate in the province of Sindh, and has commenced its operations with one branch in Karachi. The shareholders of APMB, Advans South Africa and FMO (the Netherlands Development Financial Company) have vast international experience in providing financial services to the informal sector. Advans South Africa is currently operating in six countries, in Africa (Cameroon, Ghana, Democratic Republic of Congo, Tanzania and Ivory Coast) and in Asia (Cambodia). The entry of Advans in the local market is an important step for the industry as it shows that not only local but also international investors are keen to invest in the Pakistani microfinance industry.

Advans Pakistan has established APMB with the view of not only providing microcredit but also helping small businesses. APMB plans to offer loans as well as deposit products with the ambition of catering to the financial requirements for micro and small and medium enterprises in Pakistan.

U Microfinance Bank

Another microfinance bank that has recently re-entered the market is U Microfinance Bank Limited (formerly Rozgar Microfinance Bank Limited). Pakistan Telecommunication Company Limited (PTCL) had acquired 100 percent shareholding of Rozgar Microfinance Bank Limited in August 2012 to roll out its branchless banking setup throughout the country.

SBP had allowed PTCL to buy out Rozgar Microfinance Bank Limited on the condition that PTCL would enhance the status of this microfinance bank into a nationwide MFB within one year. Before the acquisition, Rozgar Microfinance Bank Limited was a district-wide microfinance bank operating in Karachi with one branch and six service centers.

19PAKISTAN MICROFINANCE REVIEWAnnual Assessment of the Microfinance Industry

2012

CONCLUSION

On the whole, the external economy remained challenging for the industry. Persistent energy crisis and security challenges affected the growth in outreach of the microfinance industry. Despite the easing of monetary policy, commercial banks showed limited appetite for lending to private sector. In this scenario, MFPs found it difficult to borrow from banks. Overall, growth in the national economy was modest. But the microfinance industry remained bullish and savings continued to be the main driver of growth for the sector.

On the policy side and regulatory side, Pakistan continued to be recognized among the best enabling environments. Keeping in view the need to extend regulatory and legal cover to non-bank MFIs, a steering committee has been established under the SECP. In addition, in order to promote and expand micro-insurance regulations are being developed. Also, in order to facilitate access to commercial finance for the sector, MCGF was topped and its coverage extended to debt capital markets. Continuing with the policy maker’s desire for microfinance to extend financial services to small and micro-enterprises, SME guarantee fund was extended to the sector.

The year saw launch of number of new initiatives in the microfinance industry and entry of new players. Branchless banking continued to witness growth and saw two new branchless banking systems being deployed. A number of milestones were achieved in the nationwide implementation of MF-CIB. On the social performance and responsible finance side a number of new initiatives were launched. The national PPAF successfully ran the pilots for crop and livestock insurance which is now ready to replicated national level.

The industry continues to receive continued interest from local and international investors. The year saw the launch of two green field institutes and acquisition of another by a mobile network operator (MNO).

20

21PAKISTAN MICROFINANCE REVIEWAnnual Assessment of the Microfinance Industry

2012

SECTION TWO

INDUSTRY PERFORMANCE

CONTENTS

1 Industry Overview

2 Scale and Outreach

3 Financial Structure

4 Funding Profile

5 Profitability and Sustainability

6 Efficiency and Productivity

7 Risk Analysis

8 Conclusion

“Our goal is far beyond extending more credit to more poor people. Our goal is to figure out how to work together in partnership to build financial sectors that work for everyone and in particular for those that are trying desperately to climb the economic ladder to get out of poverty.” Dirk Jan Van Den Berg

This section provides a detailed analysis of the financial performance of the microfinance industry in the country. Performance has been assessed on three levels: industry wide, across peer groups and institution wise. The analysis is backed by 88 financial indicators, calculated from the audited financial statements of the reporting organizations. These indicators have been compared across time and regions to develop a reliable and fair assessment of sector.

Detailed financial information is provided in the Annex A-I and A-II of the PMR. Aggregate data has been reproduced for five years, whereas, the peer group and institution specific data has been made available only for the year 2012.

A total of 22 MFPs submitted their audited financial statements for the PMR 2012. Two new respondents – Farmers Friend Organization (FFO) and Ghazi Barotha Taraqiati Idara (GBTI) – are included in this year’s dataset. For a complete list of reporting organizations refer to Annex B.

Industry Players are categorized into three groups for the purposes of benchmarking and comparison: Microfinance Banks (MFBs), Microfinance Institutions (MFIs) and Rural Support Programmes (RSPs). See Box 2.1 for detailed definitions.

The distribution of respondents (number of reporting organizations) by peer group is given in Exhibit 2.1. As per Exhibit 2.1, the MFI peer group is comprised of the largest number of respondents followed by MFBs and then RSPs.

BOX 2.1

PEER GROUPS

MICROFINANCE INSTITUTION: A non-bank non-government organization (NGO) providing microfinance services. Organizations in this group are registered under a variety of regulations, including the Societies Act, Trust Act, and the Companies Ordinance. The MFI peer group includes local as well as multinational NGOs such as BRAC-Pakistan and ASA-Pakistan.

MICROFINANCE BANK: A commercial bank licensed and prudentially regulated by the SBP to exclusively service the microfinance market. The first MFB was established in 2000 under a presidential decree. Since then, 10 MFBs have been licensed under the Microfinance Institutions Ordinance, 2001. MFBs are legally empowered to accept and intermediate deposits from the public.

RURAL SUPPORT PROGRAM: An NGO registered as a non-profit company under the Companies Ordinance. An RSP is differentiated from the MFI peer group based on the purely rural focus of its credit operations. As a group, the RSPs are registered with and supervised by the Securities and Exchange Commission of Pakistan (SECP).

SECTION TWO

INDUSTRY PERFORMANCE

24

INDUSTRY OVERVIEW

As of December 2012, the total asset base of the reporting microfinance providers stood at PKR 60.5 billion (USD 617 million), depicting an increase of 24 percent as compared to the previous year. Out of the total assets, Gross Loan Portfolio (GLP) was PKR 33.1 billion making up 55 percent of the total assets. Outreach has grown to 2.0 million active borrowers and 1.7 active depositors.

The figures presented above vary significantly from outreach estimates as reported in the PMN’s quarterly publication for the same period i.e. MicroWATCH, December 2012. According to the quarterly update, outreach was estimated at 2.4 million borrowers and 4.68 million savers (savers are the sum 1.9 million depositors intermediated by MFB and 2.8 million savers mobilized by RSPs and MFIs as part of social mobilization).

The significant variation is due to the number of reporting organizations – some of the MFPs contributing data to the MicroWATCH are not affiliated with PMN and hence, do not report for the PMR. Also, some members and affiliates have not been able to provide audited financials for this report before it goes into publication.

SCALE AND OUTREACH

This section focuses on outreach indicators to provide performance analysis of the industry in terms of credit growth and composition, deposit mobilization, depth of outreach and gender.

SCALE AND OUTREACH: BREADTH

Outreach witnessed growth in all key indicators in 2012 – active borrowers grew by 19 percent from 1.6 million to touch 2.0 million, whereas, the gross loan portfolio increased significantly by 33 percent from PKR 24.9 billion to PKR 33.1 billion (Exhibit 2.2). It is pertinent to mention here that the inclusion of Kashf Foundation (KF) in 2012 has had a major impact on outreach – KF added 286,000 borrowers and a loan portfolio worth of PKR 2.9 billion in the current years dataset. Among the MFPs, growth in active borrowers was led by National Rural Support Program (NRSP) which added 28,000 borrowers to its portfolio in 2012. NRSP Bank and Tameer Microfinance Bank (TMFB) also witnessed considerable growth with borrowers increasing from 102,000 to 127,000 and 133,000 to 155,000 respectively. In the current year, BRAC-Pakistan saw a significant reduction in borrowers (by 30 percent) from 98,000 in 2011 to 68,000 in 2012.

The industry in terms of outreach is dominated by nine MFPs that account for 85 percent of the outreach as shown in Exhibit 2.3. Khushhali Bank Limited (KBL) maintains its position as the largest provider of microcredit in terms of active borrowers with a client base of 366,000 borrowers followed by NRSP with 345,000 borrowers and KF with 286,000 borrowers.

Among the peer groups, MFBs continue to dominate the sector by holding 39 percent of the total market share followed by MFIs (34 percent) and RSPs (27 percent) as shown in Exhibit 2.4. However, the market share of MFBs has decreased from 44 percent in 2011 to 39 percent in 2012, whereas in the same period, the share of MFIs has increased from 28 percent to 34 percent. The increase in share of MFIs can be attributed to the inclusion of KF in the current year.

In terms of GLP, MFBs account for 57 percent of the total GLP, followed by MFIs with a share of 23 percent and RSPs with a share of 20 percent (Exhibit 2.5 A and Exhibit 2.5 B). The overall GLP of the sector has increased by PKR 8.1 billion to touch PKR 33.1 billion in 2012. MFB’s witnessed the largest increase in GLP (by PKR 4.1 billion) primarily on the back of TMFB and KBL as their

26

loan portfolios increased by PKR 1.6 billion and PKR 1.5 billion respectively. Moreover, the average loan sizes of MFBs remain the highest among peer group, indicating a greater GLP. The share of GLP for MFIs increased from 20 percent to 23 percent in the year under review, again attributable to the inclusion of KF data which added PKR 2.9 billion worth of portfolio to the peer group.

The average loan size of the sector has increased from PKR 21,000 in 2011 to PKR 24,000 in 2012. The greatest increase in the loan size came from the MFB peer group whose loan size has increase by 25 percent from 23,000 to 29,000 (Exhibit 2.6). Among the MFBs, TMFB has an average loan size of PKR 47,000 (highest among the peer group). However, in 2012, KBL saw greatest increase in the average loan size which has increased by approximately 40 percent from 15,000 in 2011 to 21,000 in 2012.

Furthermore, nearly 85 percent of the industry’s GLP is accounted for by eight MFPs (Exhibit 2.7). TMFB continues to dominate the market in terms of portfolio size by having a GLP of PKR 6.7 billion, despite maintaining a market share of only 7 percent in terms of outreach. The high GLP can be attributed to the high average loan size of PKR 43,000 (highest among MFPs), primarily on the back of secured financing. Almost 84 percent of TMFBs loan portfolio is comprised of their Emergency Loan product which is a secured financial product. KBL holds the second largest loan portfolio of PKR 5.8 billion, where the majority of their portfolio

27PAKISTAN MICROFINANCE REVIEWAnnual Assessment of the Microfinance Industry

2012

(54 percent) is comprised of their Agriculture product. KBL is followed by NRSP, which has the third largest portfolio of PKR 4.4 billion. The portfolio of NRSP is dominated by their Enterprise loan product which contributes to 51 percent of the portfolio. Unlike TMFB, both KBL and NRSP, have a significant share in terms of outreach – collectively, KBL and NRSP hold 37 percent of total borrowers. With the entrance of new MFBs into the market, coupled with increasing loan size of MFBs, we are likely to witness further increase in GLP sizes of MFBs, which in turn will also increase the market share of MFBs.

In the year under review, the sector witnessed a substantial increase in the number of depositors and the value of deposits – depositors grew from 1.3 million to 1.7 million, depicting an increase of 30 percent, whereas, the value of deposits grew by 50 percent from PKR 13.9 billion to PKR 20.8 billion (Exhibit 2.8).

It is important to note here that only MFBs regulated by the SBP can accept and intermediate deposits from the general public to finance an organizations loan portfolio. Thus, MFPs not regulated by SBP can neither hold nor intermediate deposits from general public for the purpose of financing their loan portfolio. These organizations do, however, mobilize savings from their clients for purposes other than financing e.g. collateral.

The largest increase in the number of depositors came from TMFB which added 283,000 depositors followed by KBL which added 157,000 depositors. However, the largest percentage increase was seen by NRSP Bank whose number of depositors have increased by over 400 percent from 15,000 in 2011 to 81,000 in 2012. NRSP Bank commenced its operations in 2011 and since its inception the bank has been growing exponentially in terms of both, active savers and borrowers.

TMFB added PKR 3.9 billion worth of deposits during the year to increase its deposits from PKR 4.5 billion to PKR 8.4 billion (Exhibit 2.9). KBL remains second largest contributor to the value of deposits which added PKR 2.4 billion worth of deposits to close its balance sheet at

28

PKR 4.0 billion deposits. In percentage terms, NRSP Bank had the greatest percentage increase (184 percent) in the value of deposits which had increased from PKR 633 million in 2011 to PKR 1.8 billion in 2012.

Over the past few years, MFBs have been successfully mobilizing deposits, as evident from the increasing deposits on a yearly basis. With an increasing deposit base, MFBs can rely on a business model where deposits will emerge as the main source of funding in the medium to long term. In 2012, TMFB surpassed FMFB to become the largest player as far as deposit mobilization in concerned – TMFB holds a market share of 40 percent in the total value of deposits followed by FMFB with a market share of 32 percent.

The average deposit size of MFBs stood at PKR 12,041, an increase of 15 percent from the previous year. However, except for FMFB and NRSP Bank, the average deposit balance of MFBs is below the industry average as depicted in Exhibit 2.10. FMFB holds the highest average deposit balance at PKR 26,260 followed by NRSP Bank with PKR 22,713.

The Deposit-to-GLP ratio has shown considerable improvement for MFBs; the ratio increased from 95 percent in 2011 to 111 percent in 2012 (Exhibit 2.11 A). The increase in the ratio can be attributed to the increase in the value of deposits which had increased by 50 percent in the current year, whereas, the GLP of MFBs has increased by 27 percent. The improvement in the Deposit-to-GLP ratio is proof that MFBs have been successful in tapping deposits and likewise, consumers are also developing an appetite for formal savings.

A comparison across MFBs shows that the high Deposit-to-GLP ratio can be attributed to FMFB which carries a ratio of 215 percent (Exhibit 2.10 B). However, the improvement in the ratio to 111 percent in the current year came on the back of TMFB whose Deposit-to-GLP ratio increased from 89 percent in 2011 to 125 percent in 2012. TMFB is now the second MFB (after FMFB) which has a deposit base larger than its loan portfolio.

29PAKISTAN MICROFINANCE REVIEWAnnual Assessment of the Microfinance Industry

2012

Following two years of consecutive decline, the number of insurance policy holders and total sum insured saw an increase of 9.6 percent and 19.6 percent respectively in 2012 (Exhibit 2.12). The revive in the number of policy holders and sum insured came primarily on the back of RSPs whose policy holders increased by 21.5 percent while the sum insured increased by 25.1 percent. Among the RSPs, NRSP was the largest contributor which added 52,000 insurance policy holders followed by PRSP, which added 40,000 policy holders in 2012. Among the insurance policies, credit life insurance policies constitute almost 57 percent of total insurance policies followed by health insurance policies.

SCALE AND OUTREACH: DEPTH

The depth of outreach in microcredit operations is measured by a proxy indicator: average loan balance per borrower in proportion to per capita Gross National Income (GNI). A value below 20 percent is assumed to mean that the MFP is poverty focused. Except for TMFB, FMFB and NRSP Bank, all of the other MFPs fall below this benchmark (Exhibit 2.13). Comparison across peer groups shows that the ratio of average loan balance to per capita GNI for MFBs has been on the rise since the past two years. MFBs tend to target the upper end of the market through relatively larger loan sizes, and hence have a ratio of 20 percent compared to MFIs and RSPs which have a ratio of 10 percent and 11 percent respectively.

In the current year, average loan balance to per capita GNI ratio has remained constant for both, MFIs and RSPs with an upward movement in the ratio only witnessed by MFBs. This can be interpreted as the sector is continuing to target the poor but also has implications for appropriate loan sizes in the context of Pakistan’s inflationary environment. Erosion in the value of the money means that a loan worth of PKR 20,000 in one year would be considerably lower in value in the following year. Hence, a low average loan balance to per capita GNI ratio can imply that MFPs will not able to cater to the funding needs of borrowers due to the inflationary pressure. However, the ratio for MFIs and RSPs has remained constant in the current

year, indicating that the average loan size has also increased with an increase in the per capita GNI. Over the year, the per capita income had increased from PKR 108,000 to PKR 118,000 to account for inflation. However, over the same period, the average loan sizes for MFIs and RSPs had also increased from 10,600 to 11,300 and 11,400 to 12,700* respectively. As loan sizes grow and adjust for inflation, clients will be able to meet their borrowing needs from a single institution which, in turn, will help bring down the issue of multiple borrowing.

30

Lending Methodology

In the Pakistan microfinance sector, majority of MFPs follow the group lending methodology – in 2012, 82 percent of the active borrowers represented group lending (see Exhibit 2.14). In 2011, Individual borrowing had gained momentum as many MFPs which were following the group lending methodology, also started focusing on Individual lending methodology. However, individual lending did show any growth in 2012, whereas, group lending has increased by 19.4 percent in 2012. The increase in the share of group lending can be attributed to NRSP which, as mentioned earlier, saw the greatest increase in active borrowers in 2012 and completely follows a group lending methodology.

Gender Distribution

The proportion of women borrowers grew from 55 percent in 2011 to 63 percent in 2012. The share of women borrowers has been increasing over the past couple of years and for the first time the share of women borrowers has surpassed 60 percent (Exhibit 2.15). However, the percentage of women depositors has remained constant at 19 percent in the current year. Women borrowers remain an integral part of the Pakistan microfinance sector and lending to women has been encouraged by various donor and regulatory bodies. The national apex – PPAF – provides funding to MFPs based on a commitment that at least 40 percent of the borrowers will be women. Large players such as ASA Pakistan, BRAC Pakistan and NRSP have portfolios that mostly constitute of women borrowers, whereas, Kashf Foundation only lends to women borrowers.

A comparison across peer groups indicates that MFIs saw the greatest increase in the percentage of women borrowers from 82 percent in 2011 to 96 percent in 2012 (Exhibit 2.16). However, this increase can be attributed to the inclusion of KF data. Similarly, GBTI and FFO, organizations reporting for the first time in the PMR, have more than 90 percent of women borrowers in their portfolios. The proportion of women borrowers for MFBs declined slightly by 1 percent to 27 percent in 2012, primarily on the back of KBL whose proportion of women borrowers declined from 32 percent in 2011 to 27 percent in 2012.

31PAKISTAN MICROFINANCE REVIEWAnnual Assessment of the Microfinance Industry

2012

Given NRSP accounts for the bulk of RSPs’ outreach, the institute remained the main driver in increasing the share of women borrowers for RSPs from 72 percent to 75 percent, by adding 33,000 women borrowers in the current year.

Portfolio Distribution by Sector

The credit portfolio distribution witnessed a noteworthy change with the trade sector lending which decreased from 38 percent in 2011 to 35 percent in 2012 (Exhibit 2.17). The trade sector primarily comprises of general stores, karyana shops, stall hawkers, fruit vendors, etc. The decrease in trade sector lending can be attributed to BRAC-P, where, more than 75 percent of the borrowers of BRAC-P belong to the trade sector and in the current year, BRAC-P witnessed an overall decline in the number of borrowers from 98,000 to 68,000.

Regardless of the decrease in the share of trade sector lending, the services and trading sector continue to dominate the sector-wise distribution of microcredit, together accounting for 44 percent of borrowers in 2012. These are followed by borrowers from agriculture and livestock sectors, which collectively make up 38 percent of the borrowers. Borrowing for ‘other’ purposes (which mostly includes consumption related borrowing) made up 9 percent of the total sector lending, depicting an increase of 1 percent from the previous year.

The predominant share of services and trade is reflective of the general trend in the country’s economy where the services sector has continued to account for over 50 percent of the GDP, as shown in Exhibit 2.18. The share of industry in the country’s economy has shown a marginal decrease; due to persistent energy shortfall, manufacturing has been hit hardest, especially at the micro level. With the regulatory change that now allows MFBs to lend to microenterprises any amount up to PKR 500,000, we are likely to see the share of services and trade to further increase going forward.

32

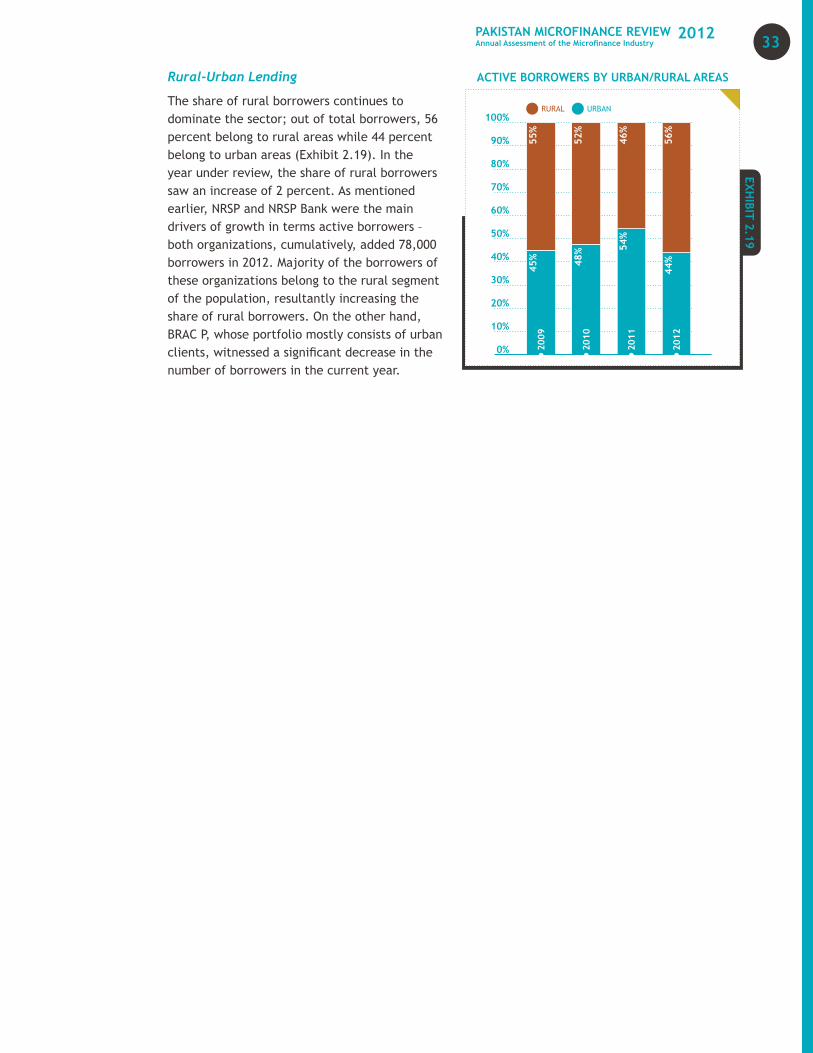

Rural-Urban Lending

The share of rural borrowers continues to dominate the sector; out of total borrowers, 56 percent belong to rural areas while 44 percent belong to urban areas (Exhibit 2.19). In the year under review, the share of rural borrowers saw an increase of 2 percent. As mentioned earlier, NRSP and NRSP Bank were the main drivers of growth in terms active borrowers – both organizations, cumulatively, added 78,000 borrowers in 2012. Majority of the borrowers of these organizations belong to the rural segment of the population, resultantly increasing the share of rural borrowers. On the other hand, BRAC P, whose portfolio mostly consists of urban clients, witnessed a significant decrease in the number of borrowers in the current year.

33PAKISTAN MICROFINANCE REVIEWAnnual Assessment of the Microfinance Industry

2012

FINANCIAL STRUCTURE

This section focuses on the asset base, asset growth and total composition of the left hand side of the balance sheet.

ASSET BASE

The total asset base of the industry stood at PKR 60.5 billion in 2012 as compared to PKR 48.6 billion in 2011 showing a growth of over 24 percent. This is partly due to the inclusion in the data set of KF which has an asset base of PKR 3.8 billion. Among the peer groups MFBs accounted for 64 percent of the asset base with an asset base of 38.6 billion, followed by RSPs which made up 19 percent of the industry assets with total assets of PKR 11.3 billion and MFIs constituted 17 percent of the total assets with an asset base of PKR 10.4 billion as seen in Exhibit 2.20. MFBs continue to expand their share in terms of asset size by growing from PKR 29.8 billion in the previous year to PKR 38.6 billion. The MFI asset base increased from PKR 6.3 billion in the previous year to PKR 10.4 billion in this year (mainly due to the inclusion of KF data). The RSPs asset base witnessed a slight decrease in the same time period from PKR 12.5 billion to PKR 11.4. This fall is due to decrease in the asset size of NRSP from PKR 8.6 billion last year to PKR 7.1 billion this year due to the transfer of assets to NRSP Bank.

Among the individual MFPs, TMBF continued to be the largest player in the industry with a balance sheet of 13.3 billion as compared to PKR 8.2 billion in the previous year as shown in the Exhibit 2.21. TMFB was followed by KBL with an asset base of PKR 9.9 billion. The third largest MFP in terms of asset size was NRSP with an asset base of PKR 7.1 billion.

The industry continues to be concentrated with eight large MFPs accounting for the 87 percent of the market share. Out of these eight, four were MFBs while two each were RSPs and MFIs.

34

ASSET COMPOSITION

The asset utilization ratio increased to 54.8 percent in 2012 from 51.2 percent in the year 2011. The improvement was led by the MFI and RSP peer group. Among the MFIs, inclusion of KF data and improvement in the asset utilization ratio of ASA-P resulted in overall improvement in the industry ratio. Also, among the RSPs, NRSP asset utilization ratio improved from 42.3 percent to 62.3 percent in 2012. For MFBs, the asset utilization ratio remained constant at 48.5 percent largely due to a low ratio contribution by FMFB. As compared to other regions the industry’s utilizations remains low and there is sufficient room for improvement as show in the Exhibit 2.22.

Asset composition continued to vary across the peer groups as shown in Exhibit 2.23. Advances for MFBs rose by 1 percent to end at 53 percent in 2012. Investments rose from 16 percent in 2011 to 20 percent in 2012 as MFBs placed funds in safe assets. Advances make up 71 percent of MFIs asset base declining from 80 percent in the previous year. This was accompanied by an increase in cash which rose from 17 percent in the last year to 24 percent in this year. RSPs witnessed a sharp increase in advances which made up 65 percent of its asset base as compared to 54 percent in the previous year. This increase was primarily due to the increase in the advances of NRSP. Overall, there is a high proportion of liquid cash in the industry which is due to upcoming quarterly repayments to the national apex.

35PAKISTAN MICROFINANCE REVIEWAnnual Assessment of the Microfinance Industry

2012

FUNDING PROFILE

The capital structure of the microfinance industry showed a significant increase in deposits over the last one year, a small decline in equity and a decrease in the proportion of debt in the capital structure as shown in the Exhibit 2.24. MFBs continued success in mobilizing deposits have resulted in deposit base reaching above PKR 20.8 billion from PKR 13.9 billion last year. This has allowed MFBs to lower their reliance on debt for on-lending resulting in overall proportion of debt in the capital structure to change as shown in the Exhibit 2.25 and 2.26.

Overall, banks remain adequately capitalized due to the increase in the Minimum Capital Requirements (MCR). In addition, equity placements done and planned to the tune of USD 8.1 million by PPAF under its PRISM – Equity Fund funded by IFAD, in the mid-sized MFPs has resulted in strengthening of their balance sheet.

However, negative equity in case of certain players has dragged down the proportion of equity in MFI capital structure to 13 percent. The RSPs continue to remain well capitalized.

By the end of 2012, two MFBs, TMFB and First Microfinance Bank, have a deposit base higher than their total GLP (see Exhibit 2.27). In 2012,

TMFB for the first time had a deposit base higher than its GLP. It is apparent with the focus on deposit mobilization by MFBs that they are likely to take a deposit led approach to funding and will have less reliance on debt for on-lending.

The industry continued its transition to commercial financing with the ratio of commercial liabilities to total debt reaching 78 percent in 2012 as compared to 32 percent in the previous year as seen in Exhibit 2.28. This significant increase is largely due to the revision of loan pricing policy by the national apex and re-categorization of inter-company

36

loan of ASA-P from subsidized to commercial. As of 2012, all loans extended by PPAF are priced at market based rates. Though subsidized loans are available but they will be extended only for operations in certain low penetration and underdeveloped areas. PPAF moving towards market based pricing is based on the premise that institutions are now robust and sustainable and therefore do not require subsidized lending.

PROFITABILITY AND SUSTAINABILITY

The total revenue for the industry increased by 24 percent from last year to close at above PKR 12.5 billion and net income increased by 40 percent to end at PKR 1.1 million in the same time period. Unadjusted ROA and ROE continue to remain at 1.9 percent and 9.7 percent for the industry.

The industry continued to remain stable with Operational Self Sufficiency (OSS) continued to remain above 100 percent for the second year running as seen in Exhibit 2.29. The OSS for the industry saw a modest increase of 1 percent as compared to the last year. This modest gain is significant as in the previous years the raise was driven by increasing yield on portfolio. However, this year the yield has decreased as compared to last year. It shows that the players are reducing their expenses and moving towards greater efficiency.

Out of the 22 reporting organizations 18 of them have OSS over 100 percent. In the previous year, 13 organizations showed an OSS over 100 percent. Among the peer groups, MFBs have the highest OSS with 110 percent, closely followed by RSPs with 109 percent and lastly, MFIs with 106 percent.

Financial Self Sufficiency (FSS) for the industry also witnessed a significant rise from 107 percent as compared to the previous year’s 101 percent. FSS also remained the highest for MFB peer groups with 108.8 percent followed by RSP with 108.3 percent and MFIs with 103.6 percent.

37PAKISTAN MICROFINANCE REVIEWAnnual Assessment of the Microfinance Industry

2012

Revenue from loan portfolio stood at PKR 10.1 billion. The yield on portfolio stood at 34.3 percent in 2012 as compared to 35.2 percent in 2011 as seen in Exhibit 2.30. The decrease in yield is first in the last four years which reveals that the pricing of assets plateau-ed last year. Future drivers of profitability will be due to growth in outreach, larger loan sizes and increased efficiency. This is also corroborated by the decrease in the revenue ratio for the industry which fell by 1.6 percent as compared to last year from 23.9 percent and 22.3 percent.

Out of the 22 reporting organizations, 18 of them have OSS over 100 percent. In the previous year, 13 organizations showed an OSS over 100 percent. Among the peer groups, MFBs have the highest OSS with 110 percent, closely followed by RSPs with 109 percent and lastly, MFIs with 106 percent.

Financial Self Sufficiency (FSS) for the industry also witnessed a significant rise from 107 percent as compared to the previous year’s 101 percent. FSS also remained the highest for MFB peer groups with 108.8 percent followed by RSP with 108.3 percent and MFIs with 103.6 percent.

Revenue from loan portfolio stood at PKR 10.1 billion. The yield on portfolio stood at 34.3 percent in 2012 as compared to 35.2 percent in 2011 as seen in Exhibit 2.30. The decrease in yield is first in the last four years which reveals that the pricing of assets plateau-ed last year. Future drivers of profitability will be due to growth in outreach, larger loan sizes and increased efficiency. This is also corroborated by the decrease in the revenue ratio for the industry which fell by 1.6 percent as compared to last year from 23.9 percent and 22.3 percent.

As compared to the region the yield on portfolio in Pakistan continues to remain on the higher end (see Exhibit 2.31). It is hoped that as the industry expands, matures and becomes efficient yield will decrease further.

The bulk of the revenue of the industry continues to come from earnings on the loan portfolio. However, this year saw the proportion of revenue

38

from investments in financial assets increase to 14 percent from 12 percent last year as MFBs placed surplus funds into financial assets to provide them with a financial cushion and meet their liquidity needs (see Exhibit 2.32). Income from branchless banking for TMFB stood at PKR 445 million which more than doubled as compared to the previous year.

The total expense for the industry stood at PKR 12.9 billion put of which PKR 6.8 billion was operating expense, followed by financial expense of PKR 3.9 billion and loan loss expense of PKR 0.6 billion. The expense to assets ratio continued to decline for the last five years as seen in the Exhibit 2.33. The ratio fell to 20.3 percent from 23.9 percent in 2011. The decline is largely due to the decrease in operating expense from 13.7 percent last year to 12.1 percent in the year.

Among the peer groups, RSPs have the lowest expense to assets ratio with 18.3 percent, MFBs with 19.9 percent and the MFIs with highest at 37.0 percent. Expenses are higher for the MFI peer group due to a higher KF due adjusted loan loss provision expense.

Compared to the region, the expense to total assets continues to remain on the higher side despite the consistent decrease over the last few years (see Exhibit 2.34) largely due to a higher operating expense.

The Operating Expense to GLP and Personnel Expense to GLP ratios continued to decline for consecutive years as seen in the Exhibit 2.35. Operating Expense to GLP decreased from 25.5 percent last year to 23.3 percent in this year, whereas the Personnel Expense to GLP decreased from 14.7 percent to 12.7 percent in the same time period.

Among the peer groups MFBs have the highest Operating Expense to GLP ratio at 25.2 percent, closely followed by MFIs with 24.6 percent and RSPs having the lowest ratio with 16.7 percent. However, in the case of Personnel Expense to GLP the MFI peer group has the highest ratio with 15 percent, followed by MFBs with 13.1 percent and RSPs with 8.9 percent.

39PAKISTAN MICROFINANCE REVIEWAnnual Assessment of the Microfinance Industry

2012

Compared globally the operating and personnel expenses to GLP continue to remain on the higher side as seen in Exhibit 2.36.

PRODUCTIVITY

The borrowers per staff ration increased from 117 in the last year to 135 in the year 2012. Overall, the borrowers per staff ratio had exhibited a mixed trend in the last five years as seen in Exhibit 2.37. The ratio varies a little among the three peer groups with the RSPs having highest number for borrowers per staff at 143. It is closely followed by MFIs and MFBs with 139 and 127 respectively. SRSO has the highest number of borrowers per staff at 196 among all the MFPs. Next is TRDP with 185 borrowers per staff.

Depositors per staff ratio continued to raise as deposit mobilization by MFBs gathers pace. Currently, it stands at 118 as compared to 94 in the previous year. Among the MFBs, TMFB has the highest number of depositors per staff with 618. As MFBs further expand their efforts to raise deposits and tap micro savers this number will continue to witness growth.