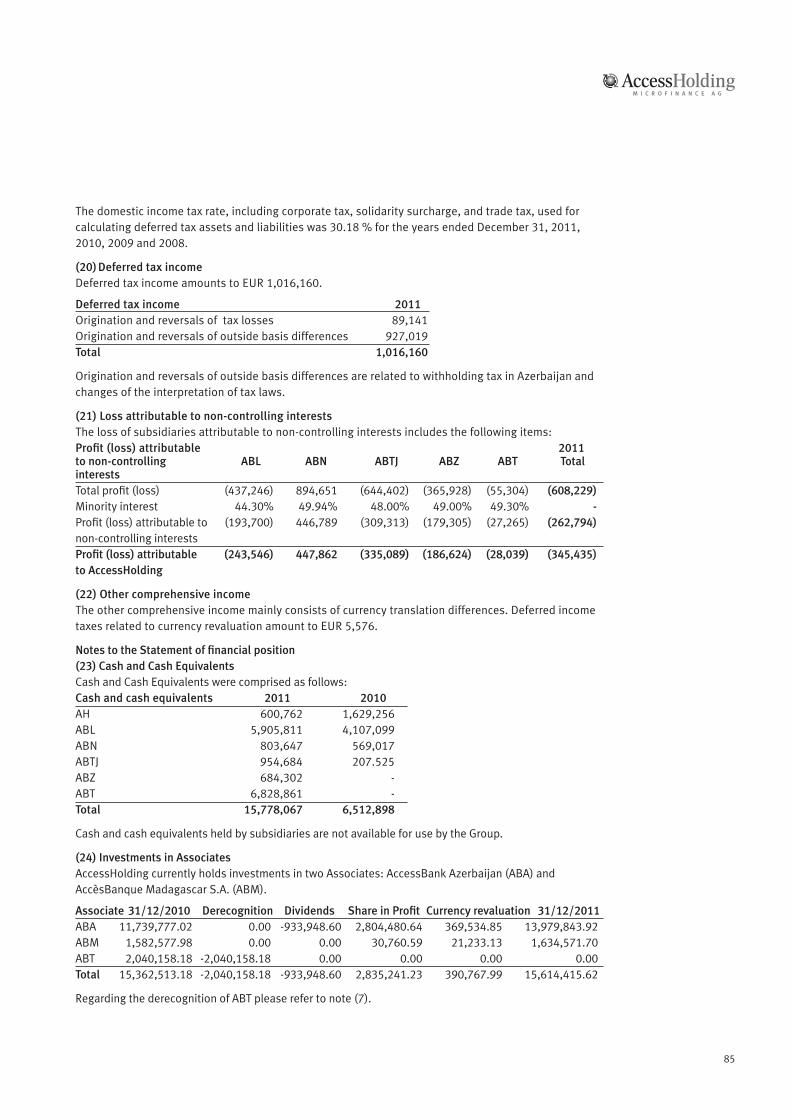

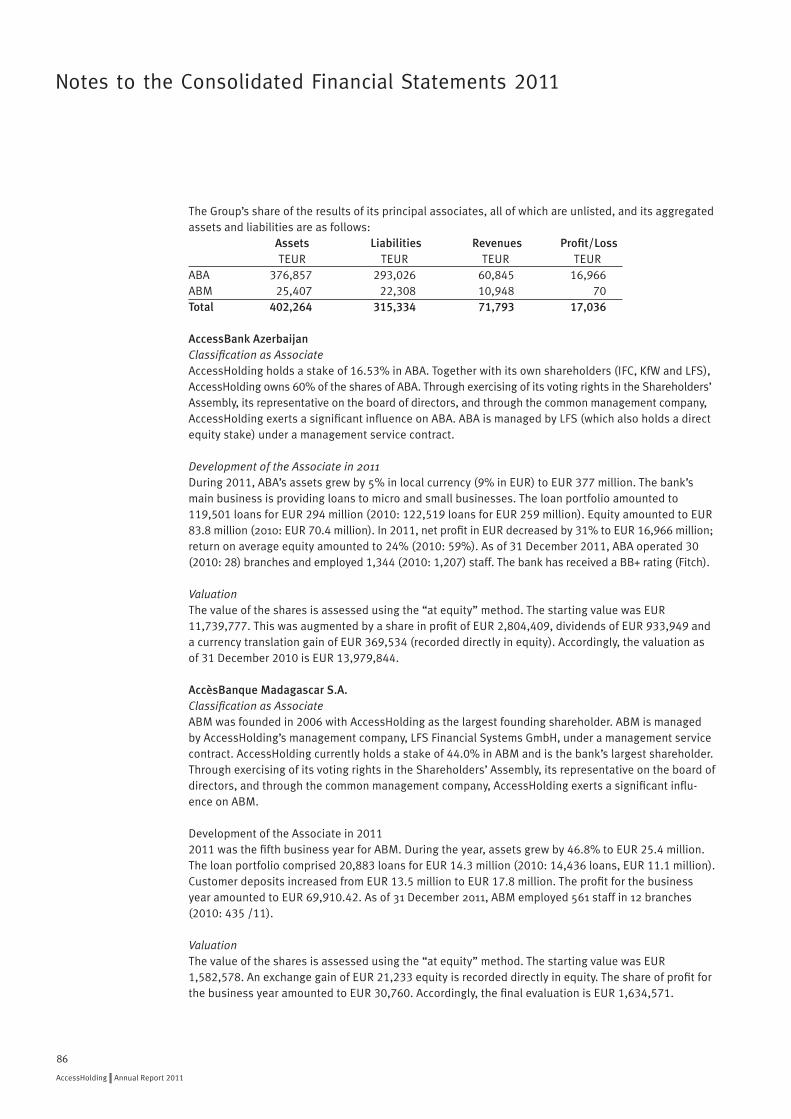

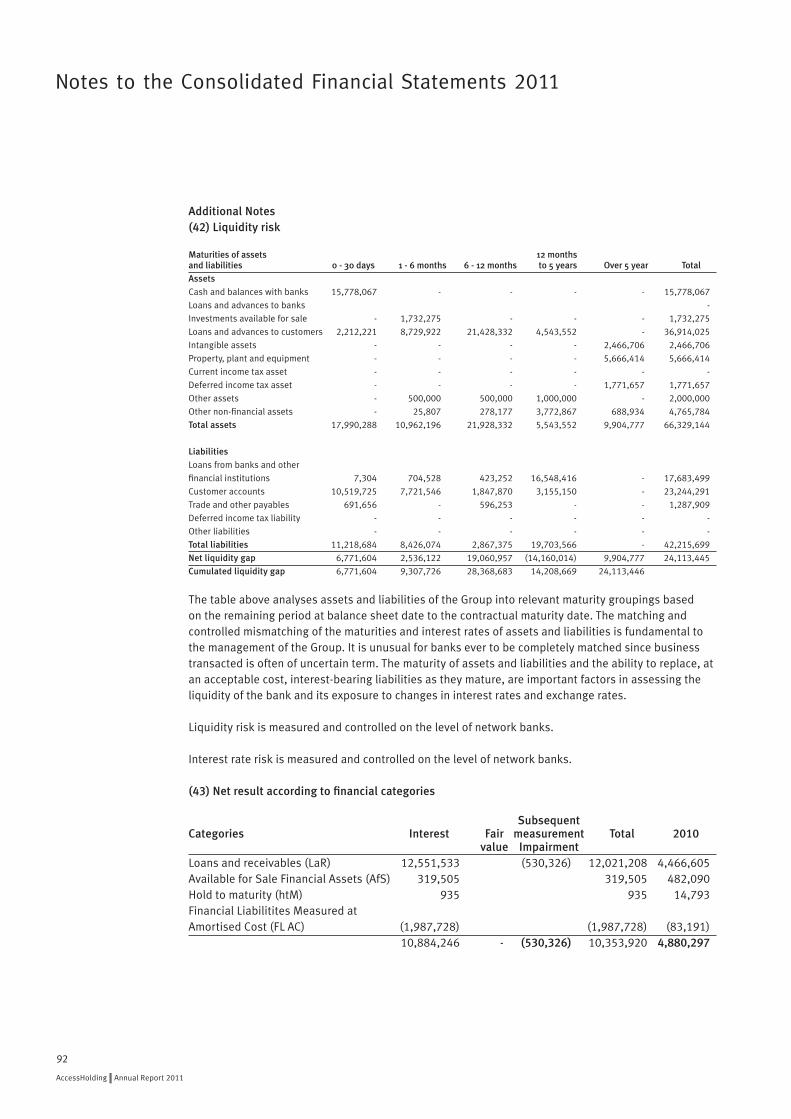

Annual Report 2011

Fruit Sellerfrom Tanzania

www.accessholding.com

Table of Contents

The Access Network . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Key Results of the Year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Letter from the Chairman of the Supervisory Board . . . . . . . . . . . . . . . . . . . . . . . . 6

Letter from the Management Board. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Summary of Business Development in 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Business Purpose . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Our Shareholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12 Corporate Governance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14 General Meeting of Shareholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14 Management Team . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14 Supervisory Board . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

History of AccessHolding . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Presentation of the AccessGroup . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20 AccessBankAzerbaijan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20 AccèsBanqueMadagascar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24 AccessBankTanzania . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26 ABMicrofinanceBankNigeria . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28 AccessBankLiberia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30 AccessBankTajikistan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32 ABBankZambia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

Corporate Social Responsibility in the Holding . . . . . . . . . . . . . . . . . . . . . . . . . 38

AccessBank’s Clients . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

AccessHolding Management Report 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

Auditor’s Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

Consolidated Financial Statements for the Year Ended 31 December 2011 . . 63

Notes to the Consolidated Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . 68

Contact Addresses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100

3

AccessHolding|AnnualReport2011

4

AccèsBanqueMadagascar

ABBankZambia

AccessBankLiberia

ABMicrofinanceBankNigeria

AccessBankTanzania

AccessBankAzerbaijan

The Access Network

AccessHolding|AnnualReport2011

5

AccessHoldingoperatesanetworkofcommer-cialbanksindevelopingandtransitioncountrieswithatargetgroupfocusonmicro,smallandmedium-sizedenterprises.TheAccessBanknetworkcomprisessevenmemberbankswithatotalofabout3,500staffandover500,000clients,growingbyseveralthousandeverymonth.

AccessHolding in Brief

AccessBankTajikistan

Key Results of the Year(asof31December2011)

2011 2010

Totalassets(EUR) 480m 408mGrossloanportfolio(EUR) 351.6m 289.4mNo.ofloansoutstanding 181,902 158,707Portfolio-at-Risk 30daysin% 1.0 % 1.0%Totalcustomerdeposits(EUR) 188m 146mNo.ofdepositaccounts 482,846 332,641No.ofstaff 3,318 2,502No.ofbranches 68 57

6

AccessHolding|AnnualReport2011

Letter from the Chairman of the Supervisory Board

DespitetherecentfinancialmarketturmoilexperiencedinEuropeandNorthAmericatheemergingmarketshaveprovedtoberesili-entunderpinnedbyprudentbanking,growingpopulationsandrisingrealincomes.

AccessHoldingcontinuedtoenjoystronggrowthin2011.Totalassetsofnetworkbanksgrewby18%,loansby21%,depositsby28%andclientsby45%.ThishasbeenachievedboththroughorganicgrowthandbythecontinuedcreationofnewAccessfinancialinstitutions.The7thnetworkbankwasopenedinOctoberwiththelaunchofABBankZambia.ThemostmaturebankinthenetworkisAccessBankAzerbaijanwhichonceagainwonanumberofawardsin2011.Itnowhas30branchesspreadthroughoutthecountry.Over3,300peoplearenowemployedacrossthe7banksandcollec-tivelytheyserveaclientbasethatisexpectedtoexceed500,000inthefirsthalfof2012.

In2011,theGroupposteditsfourthconsolidatedprofitinarow,asignifi-cantprerequisiteforbuildingasustainablebankingnetworkfocusedontheneedsofmicro-entrepreneursandSMEbusinesses.ProfitabilityhasbeenachievedwithoutcompromisingthecommitmentofAccesstooperateinaccordancewiththeSMARTPrinciplesofclientprotectionandtheUNPrin-ciplesforResponsibleInvestment.ProfitabilityisanessentialingredientinenablingAccesstocontinuetoexpandbydrawingcapitalfromitscurrentshareholderbaseandinduecoursefromnewprivatesourcesofcapital.InorderforAccesstomaximiseitsimpactitmustbeprofitableandhencesus-tainableoverthelong-term.

Iwouldliketorecordmythankstoallstaffmembers.Theircontinueddedica-tionandgrowingexpertiseliesbehindthecompany’simpressiveperformance.

HywelRees-Jones

Letter from the Management Board

Fromitsfoundationin2006,AccessHoldinghasgrowntobecomeasuccessfullyoperatinginternationalbanknetwork.Networkbankshaveevolvedintosignificantplayersinthebankingsectorsoftheirrespectivecountriesofoperations.Attheendof2011,weservedmorethan180thousandcreditcustomerswithatotalloanportfolioofmorethanEUR350millionthrough68branchesinsevencountries,andoperatedmorethan480thousandcustomerdepositaccountswithanaggregatebalanceofEUR188million.

Thisprosperous‘takeoff’phaseofAccessBanksisreflectedinanover-achievementofgoalsbyAccessHolding,whichhasshownprofitability(basedonIFRS)ineachyearsince2008.Itcanbeexplainedbytheeffectiveinterplaybetweenshareholders,supervisoryboard,managementandstaffofAccessBanksthatsharestrongcorporatevalues;inparticulartransparency,non-discrimination,opencommunication,performanceorientationandsocialresponsibility.

Theyear2011hasbeenanothersuccessfulbusinessyearforAccessHolding.Allnetworkbankshavebeenperforminginlinewith(orabove)expectations.ThelaunchofABBankZambia,theagreementonthestrategictakeoverofAccessBankinAzerbaijanandthemoveintonewheadquarterpremisesinBerlintosupportfurtherexpansionarejustsomeof2011keymilestones.Thebuildingofheadofficestructuresisespeciallyimportantatthisstageinordertoprovidequalityassuranceandreapthesynergiesrequiredforfurthergrowth.

TheHoldingperformsmanyfunctionsthatcannormallybefoundintheheadofficeofaglobalbank.ApartfromManagement,mainfunctionsare:HRdevelopmentofAccessBanks,productdevelopmentandsupportofthebusinessofthesebanks(loans,deposits,andpaymentservices),accounting,internalaudit,andlegaladvice.Furthermore,theheadofficeplaysanimportantrolewithregardtothedevelopmentofsoftwaresystemsandongoingITsup-portofAccessBanks,andthetrainingofthebanks’managementandstaff.

ThishealthystructuralbackgroundgivesAccessHoldingtheconfidencetoachieveitsmissionofbeingaleadingstrategicinvestorinthemicrofinanceindustryandtofurtherexpanditsglobalnetworkofsubsidiaries.WithjointeffortsAccessHoldingwillrealizeaninterestingpipelinewithfurtherinvest-mentsinthethreefocusregionsSub-SaharanAfrica,CentralAsia/EasternEuropeandLatinAmerica.Inadditiontothisplannedmarketdevelopment,mostAccessBankswillincreasinglyofferservicestomiddleincomecustomersandlarger,moreformalSMEs.Theywillnotonlybemicroandsmallbusinessbanksbut“goodbanks”thatofferrelevantfinancialservicesinacustomerfriendlywayatattractiveconditions.AccessBankswillplaypioneeringroleswithregardstoemploymentstandards,environmentalprotection,customerprotectionandresponsiblelending.

ChristophDiehlandThomasEngelhardt

7

Summary of Business Development in 2011

In2011,AccessHoldinganditsbankingnet-workcontinuedtogrowatarobustpace.Totalassetsofnetworkbanksgrewby18%toEUR480million,fuelledbyanincreaseofthetotalgrossoutstandingloanportfolioby21%toEUR352million.Thenumberofoutstandingloansroseby15%to181,902,whereasthenum-berofcustomerdepositaccountssoaredby45%to482,846(propelledbyastrongclientbaseexpansioninSub-SaharanAfrica).Totalbalancesoncustomerdepositaccountsheldbynetworkbanksincreasedby29%toEUR188million.Morethan3,300staffwereemployedbythesevennetworkbanksasatyear-end,anincreaseof32%comparedto2010.

Mostimportantly,thisgrowthdidnotcomeatthecostofquality.Arrearsandloanlossratesremainatequallylow(i.e.strong)levelsasin2010,withagroup-widePAR 30of1%andcumulativeannualwrite-offsbelow1%attheendof2011.

Profitability-wise,2011wasnotasstrongasthepreviousyear,mainlybecausetheexcep-tionallyhigh2010netprofitofAccessBankAzerbaijanreturnedtomorecustomary(albeitstillstrong)levels.Thetotalafter-taxprofitofallnetworkbankscombinedwasEUR16.7million.

Butevenbeyondtherealmoffinancials,2011hasseennumerousexcitingdevelopmentsandmilestonesacrosstheAccessBanknetwork.Thetimelinebelowvisualizessomeoftheseeventsalongthecourseoftheyear.

8

AccessHolding|AnnualReport2011

ABMicrofinanceBankNigeriawitnessesacapitalincreasefromNGN1bntoNGN1.5 bn(EUR4.7milliontoEUR7.1million).

AccessBankTajikistanreachesaloanportfolioofmorethanEUR5million,afterjustoveroneyearofoperations.

ABMicrofinanceBankNigeriasuccess-fullyimplementsSMElending.

FitchRatingsrecon-firmsAccessBank’sBB+rating–thehighestamongAzerbaijan’sprivatebanks;GlobalFinancemagazinerecognizesAccessBankasthebestbankinAzerbaijaninits2011Awards.

AccessBankTanzaniaintroduces“M-Pesa”mobilephonetransferandpaymentservicesasanagentforVodacomTanzania.

2011 February March April June

9

TheBankerMagazinenamesAccessBankasthe‘BankoftheYearinAzerbaijan’initsannualawards.

AccessBankinAzerbaijandisbursesits500,000thloan.

ABBankZambiaisgivenaprestigiousmicrofinanceawardbytheBankersAssociationofZambia.

AccessBankTanzaniareceivesacapitalincreaseofTZS2bn(EUR975thousand)tosupportnewbranchopenings.AccessHoldingbecomesmajorityshareholder.

AccessBankTanzaniareachesthemilestoneof75,000customerdepositaccounts.

TheCentralBankofLiberiaconfirmsthatAccessBankLiberiahasbyfarthebestportfolioqualityintermsofPARintheLiberianbankingsector.

ABBankZambiaopensitsdoorstothepublic.

August 2011BothLFSand

AccessHoldingmoveintonew,significantlylargerofficepremises,thuscreatingsufficientphysicalcapacityforfurthergrowth.

AccèsBanqueMadagascaropensitsfirstruralbranchwithfocusonagriculturalbusiness.

AccessBankwinstheawardfor“BestBankofAzerbaijan”attheannualEuro-money“AwardsforExcellence”inLondon.

July August October November December

Business Purpose

Our vision is a financial sector that offers re-sponsible financial services to all people with equal ambition for excellence and quality.

AccessHolding’smissiontherebyistooperateagrowingglobalnetworkofresponsiblecom-mercialbanksindevelopingandtransitioncountriesthatprovideresponsiblefinancialservicestolowandmiddleincomehouseholdsandinparticulartomicroandsmallbusinesses.

Intheircountriesofoperations,AccessBanksstrivetobethe‘housebank’(bankofchoice)formicroandsmallenterprises,byofferingallthefinancialservicesthattheyusuallyneed.

WebelievethattheMSEsectorisvitalforthedevelopmentanddiversificationofacountry’seconomy,thecreationofjobsandthereductionofpoverty.

Manypeopleinourcountriesofoperationdonothaveaformalandregularsourceofincomebutlivefromtheproceedsofmicroandsmallenterprises,themajorityofwhichareinformal(orsemi-formal)Mostclientsdonotpossessofficialfinancialdocumentation.Furthermore,mostofthepopulationispoorinthesensethattheyarenotabletoaccumulatelargesavingsandassets.

Traditionalcommercialbanksdonotservethisimportantpartofthepopulationadequatelybecausetheirloanbusinessfocusesonlargecompaniesandconsumerloansforsalaryear-ners.Inaddition,theyusuallydiscouragesmalldepositsthroughavarietyofinstruments,e.g.byaskingforhighminimumbalancesontheaccountsorbyrequiringextensiveaccountopeningdocumentation.

Ontheothersideofthefinancialsector,non-bankfinancialinstitutions(e.g.non-governmentalorganizationsandcooperatives)thatofferservicestomicroenterprisesareoftennotef-ficient,mainlyduetotheincentivesgeneratedbytheirownershipstructure.Furthermore,theyarenotauthorizedtooffermanyoftheservicesthatsmallentrepreneursandtheirfamiliesrequire,inparticulardepositaccountsandsimplepaymentservices.Theyoftenremainsmallandasaconsequencearenotabletoreapeconomiesofscalethatwouldallowthemtoreducetheirmarginsovertime.

SmallentrepreneursandtheirfamiliesarethemaintargetgroupofAccessBanks.Ournetworkbankshaveafullbankinglicense(currentlywiththeexceptionofouraffiliateinNigeria).Thisallowsthemtoofferasufficientlybroadproductrangetoevolveintothebankofchoiceofsmallentrepreneurs.Furthermore,allofourproductshavebeenmindfullydesignedinawaytomeettheneedsofthelatter.

Thebank’sloansareprimarilybasedonanassessmentoftheborrower’srepaymentcapacity.Asaconsequence,providingfinancialservicestoourcustomersispersonnel-inten-siveduetothesmallsizeoftransactionsandbecausesmallentrepreneursinourcountriesofoperationsareusuallynotabletoprovidedocumentationofreliablefinancialdata.Thisrequirescollectinginformationthroughcompa-nyandhouseholdvisits.AccessBanks’dedica-tedproductsandriskmanagementtechnology,specificallydevelopedtoservemicro-,small-,andmedium-sizedenterprises,allowthebankstodothisefficientlyandprofitably.

AccessBanksbuild-uplongtermbusinessrela-tionshipswithcustomersbasedonresponsibil-ityandmutualrespect.Bydoingsotheypromoteasavingscultureandsupportborrowerstobuild-upacredithistory.

10

Core CorporateValues andBusiness Model

Mission Statement

AccessHolding|AnnualReport2011

Shareholders,managementandstaffofAccessBankssharestrongcorporatevalues,inparticular:

Transparency Non-discrimination Opencommunication Performanceorientation Socialresponsibility Environmentalprotection

AccessHolding’s business modelrestsonthecreationoracquisitionofnewlyestablishedorexistingcommercialbankswithatargetgroupfocusonmicro,smallandmedium-sizedenter-prises(MSMEs).Thesebanksarethenintegra-tedintoagroupwithacommonbrandidentity-the“AccessGroup”.Banksinthegroupshareacorerangeofstandardisedproducts(withlocaladaptationsasrequired)andajointcommit-menttothesameprinciples:

1.Ease and speed of access–providingfinancialservicestopreviouslyun-orunderservedpartsofthepopulation,withtheaimtobefasterandmoreefficientthananycomparableoperatorinthecountry;

2.Transparency and clarityofproducts,servi-cesandeligibilitycriteria–withaslittleroomfordiscretionorsubjectiveinterpretationaspossible;

3.Quality leadership–inallourcountriesofoperations,westrivetosetindustrystandardswithrespecttocustomerorientationandservicequality.Atthesametime,allmemberbanksarecommittedtoensuringthehighestpossiblequalityoftheirloanportfoliosthroughadherencetointernationalbestpracticeswithrespecttotheirunderwritingstandardsandcreditriskmanagement.

4.Training and staff development–oneofthevitalelementsofthebuild-upstrategyforeachmemberbankistherecruitmentandtrainingoffreshstaffonalargescale.Ourrecruitmentconceptplacesstrongemphasisonidentifyingtalentedandmotivatedstaffthatnotnecessarilyhaspriorrelevantworkexperience.Qualifyingthemtoassumemoreresponsiblerolesovertimeisachievedthroughregulartrainingandcoachingaswellasfrequentstaffexchangebetweennetworkbanks.

5.Strong business ethics–AllmembersoftheAccessGroupadheretoajointsetofprinciplesofgoodcorporatebehaviour,coveringamongothersareassuchasresponsiblelendingpractices,adherencetointernationalandlocalsocialandenvironmentalstandards,aswellasastringentcodeofconductforallmemberbankemployees.

Hence,AccessHolding’srolegoesbeyondthatofaprojectincubatororconventionalstrategicinvestor.

11

Our Shareholders

AccessHoldingiscurrentlyownedbyeightshare-holders,hereafterpresentedinalphabeticalorder:

CDCistheUK’sdevelopmentfinanceinsti-tutionthatsupportsthebuildingofbusinessesandinfrastructureinthepoorestpartsofAfricaandSouthAsia,creatingjobsandmakingalastingdifferencetopeople’slives.

Workinginsomeoftheworld’smostdeman-dingbusinessenvironmentsCDC’sthreecoreareasofbusinessare:

Private equity funds investing; Direct equity investing in companies,

banks and infrastructure; and Direct lending to companies, financial

institutions and infrastructure projects.Investingfromitsownbalancesheet,CDChasreturnedaprofitof£1.7bnsince2004.

TheEuropean Investment Bank (EIB)istheEuropeanUnion‘sfinancinginstitution.Itsshareholdersarethe27MemberStatesoftheUnion,whichhavejointlysubscribeditscapital.

12

OwnershipStructure ofAccessHolding

ThecurrentownershipstructureofAccessHoldingisshowninthetablebelow.

14,12 %

3,26 %

14,12 %16,12 %

14,12 %

14,12 %

10,03 %

14,12 %

AccessHolding|AnnualReport2011

CDCGroupplc(CDC)

NetherlandsDevelopmentFinanceCompany(FMO)

LFSFinancialSystemsGmbH(LFS)

TheEuropeanInvestmentBank(EIB)

TheOmidyar-TuftsMicrofinanceFund(OTMF)

InternationalFinanceCorporation(IFC)

KfWEntwicklungsbank

MicroAssets

TheEIB‘sBoardofGovernorsiscomposedoftheFinanceMinistersoftheseStates.TheEIB‘sroleistoprovidelong-termfinanceinsupportofinvestmentprojects.OutsidetheEU,theEIBisactiveinover150countries(thepre-accessioncountriesofSouth-EastEurope,theMediterra-neanpartnercountries,theAfrican,CaribbeanandPacificcountries,AsiaandLatinAmerica,CentralAsia,RussiaandotherneighbourstotheEast),workingtoimplementthefinancialpillarofEUexternalcooperationanddevelopmentpolicies(privatesectordevelopment,infrastruc-turedevelopment,securityofenergysupply,andenvironmentalsustainability).

FMOistheDutchdevelopmentbank.Itfi-nancescompanies,projectsandfinancialinsti-tutionsfromdevelopingandemergingmarkets.AttheheartofFMO’sstrategystandsthebeliefthatentrepreneurshipiskeyincreatingsustai-nableeconomicgrowthandimprovingpeople’squalityoflife.FMOisspecializedinsectorswhereitscontributioncanhavethehighest

TheOmidyar-Tufts Microfinance Fund,in-vestsinthefinancialservicessectorinemergingmarketsanddevelopingcountries.Thefundseekstodemonstratetheviabilityofcommercialinvestmentinmicrofinancetoinstitutionalinvestors.ThefundishousedwithintheTuftsUniversityendowment.Thefundwasestablis-hedinNovember2005throughagifttoTuftsUniversitybyPierreOmidyar,founderofeBay,andhiswife,Pam,co-founderofOmidyarNetworkwithherhusband.TuftsUniversity(www.tufts.edu),locatedonthreeMassachusettscampusesinBoston,Medford/Somerville,andGrafton,andinTalloires,France,isrecognizedamongthepremierresearchuniversitiesintheUnitedStates.Tuftsenjoysaglobalreputationforacademicexcellenceandforthepreparationofstudentsasleadersinawiderangeofpro-fessions.

TheownersofAccessHoldingandtheAccess-BankssharetheobjectivesandcorporatevaluesoftheGroupaswellasthefundamentalsofourbusiness model(seepage10–11).Inparticular,theyareconvincedthatprovidingresponsiblefinancialservicestosmallenterprisesandlowerincomestratacanbedoneonaprofitableandsustainablebasis.Theyprovidepatientcapitalthatallowsustopursuealong-termapproachininvestingintrainingandbuildingupasignificantcustomerbasis.

Furthermore,allofourShareholdersplacehighemphasisontheGroup’scorporate social respon-sibility.Tothiseffect,theyhaveformulatedacomprehensivesetofpoliciesforournetworkbanksthatincludesresponsiblelendingpracti-ces,goodemploymentstandards,acodeofconductforallstaffatbankandholdinglevel,andastringentsocialandenvironmentalman-agementsystem.AllmemberbanksoftheAccessGroupstrivetoberecognisednotonlyasexcel-lentfinancialserviceproviders,butmoregenerallyasemployersandstakeholdersofthehighestintegrityintheirlocalcommunities.

ThemixofpublicandprivateinvestorsofAccessHoldingsupportsthemissionofthecompany.WhilepublicinvestorsaddtothereputationandsolvencyofAccessHoldingandstrengthenlongtermcommitmenttodevelop-mentgoals,privateinvestorsareexpectedtoensurecommercialsuccess.

13

long-termimpact-financialinstitutions;energy&housing;andagribusiness,food&water.Theyalsofostercapacitydevelopment,suchasfinancialadministration&planningskills,andsustainablebusinesspractices.

The International Finance Corporation(IFC),amemberofWorldBankGroup,createsopportunityforpeopletoescapepovertyandimprovetheirlives.IFCfosterssustainableeco-nomicgrowthindevelopingcountriesbysup-portingprivatesectordevelopment,mobilizingprivatecapitalandprovidingadvisoryandriskmitigationservicestobusinessesandgovern-ments.Thecorporation’snewinvestmentstotaledUSD12.2billioninfiscalyear2011.Thiswasspreadover518projects;USD4.9billionwenttothepoorestcountrieseligibletoborrowfromtheWorldBank’sInternationalDevelopmentAssociation.IFCalsomobilizedanadditional$6.5billiontosupporttheprivatesectorindevelopingcountries.

KfW Entwicklungsbankfinancesinvest-mentsandaccompanyingadvisoryservicesindevelopingandtransitioncountriesonbehalfoftheGermangovernment.Itsaimistobuildupandexpandthesocialandeconomicinfra-structureoftherespectivecountries,andtoad-vancesoundfinancialsystemswhileprotectingresourcesandensuringahealthyenvironment.KfWEntwicklungsbankisaleaderinsupportingresponsibleandsustainablemicrofinanceandisinvolvedintargetgroup-orientedfinancialinstitutionsaroundtheworld.ItisanintegralpartofKfWBankengruppe,whichistheleadingpromotionalbankinGermany.

LFS Financial Systems GmbH (LFS),whichhasfoundedAccessHoldinginAugust2006andwhichisalsothetechnicalpartnerandma-nagerofthecompanyaswellasitsinvestees.LFSisanadvisoryandmanagementfirmbasedinBerlin,specializinginbankingandfinancialsectorprojectsindevelopingandtransitioncountrieswithfocusonmicro,smallandmedi-umenterprise(MSME)finance

MicroAssets,aBerlin-basedinvestmentcompanythathasbeenestablishedtoenableLFSandstaffoftheAccessnetworktoinvestinAccessHolding.

Common

Objectives and

Values

Corporate Governance

AccessHoldinghasestablishedagovernancestructurethatallowswellinformedandstrongdecisionmaking.Inparticular,theSupervisoryBoardoftheHoldingisactivelysteeringthebusinesswhilemanagementhasfullrespon-sibilityforday-to-daydecisions.Withthesuc-cessivedevelopmentofgloballystandardisedpolicies,productsandsystems(solutions)acrosstheAccessBanknetwork,theManage-mentofAccessHoldingisalsoresponsibletoensurethatmemberbanksareoperatinginconsistencywiththesestandards,soasfortheGrouptoreapnetworksynergiesandfacilitatetheexchangeofpersonnelandotherresourcesbetweenbanks.

AccessHoldingisaJointStockCompany(Aktiengesellschaft)inaccordancewiththeGermanJointStockCompanyLaw(Aktienge-setz)andotherapplicablelaws,furtherrefer-redtoasGermanCorporateLaw.TheCompanyisregisteredinBerlinandsharesofficeswithitstechnicalpartnerLFS.

ThesharesofAccessHoldingareordinaryre-gisterednon-bearershares,whichcanonlybesoldwithpriorapprovaloftheothersharehol-ders.

AccessHoldinghasthethreemaincorporatebodiesofaJointStockCorporationunderGermanCorporateLaw:theGeneralMeetingofShareholders,theSupervisoryBoardandtheManagementBoard.Thefollowingenumera-tionsprovideanoverviewofthetasks,rightsandresponsibilitiesofeachbody.AlloftheseprovisionsaredefinedmorecomprehensivelyintheCompany’sArticlesofAssociationandShareholderAgreement.

1. General Meeting of Shareholders

IntheGeneralMeetingofShareholders(GMSH),allinvestorshavevotingrightsinproportiontotheirrespectiveshareholdings.Thebody’smaintasksandrightsare:

Toapproveoramendthecompany’s ArticlesofAssociation;

ToappointmembersoftheSupervisory Board;

Toappointtheexternalauditorof AccessHolding’sfinancialstatements;

TodeterminetheuseofAccessHolding’s profit.

2. Management Board

Withthesuccessivedevelopmentofgloballystan-dardisedpolicies,productsandsystems(solutions)acrosstheAccessBanknetwork,themanage-mentofAccessHoldingisalsoresponsibletoen-surethatmemberbanksareoperatinginconsis-tencywiththesestandards,soasfortheGrouptoreapnetworksynergiesandfacilitatetheexchangeofpersonnelandotherresourcesbetweenbanks.

WithinthegovernancestructureofAccessHolding,theManagementBoardisresponsiblefortheday-to-dayoperations(includingtheformulationofinvestmentproposals)andsupportstheSupervisoryBoardinitscontrolanddecisionmakingfunctions.

TheManagementBoardofAccessHoldingiscurrentlycomposedoftwomembers,bothofwhichhaveservedatAccessHoldingsinceitsinception:

Thomas Engelhardt (Chairman) Bornin1971,Mr.EngelhardtisoneofthethreepartnersinLFS,andhasbeenwiththecompanysinceitsfoundationin1997.Hehas15

yearsofworkingexperienceintheareaofMSMEfinance,includingvariousseniormanagementpositionsinconsultancyprojectsinCentralAsiaandSouthEasternEurope.Between2002and2006,Mr.EngelhardtservedasthefirstGeneralManagerofAccessBankAzerbaijan(thennamed‘MicroFinanceBankofAzerbaijan’),thusplayingtheleadingroleinbuildingupAccessHolding’sflagshipbankfromscratch.HeistheChairmanoftheSupervisoryBoardsofAccessBanksinTajikis-tanandLiberiarespectively,andisaSupervisoryBoardmemberofAccessBankAzerbaijan.Mr.EngelhardtholdsanM.ScinEconomics,andspeaksGerman,English,RussianandSerbo-Croat.

14

GovernanceStructure

Legal Form/Formof Shares

Bodies

AccessHolding|AnnualReport2011

15

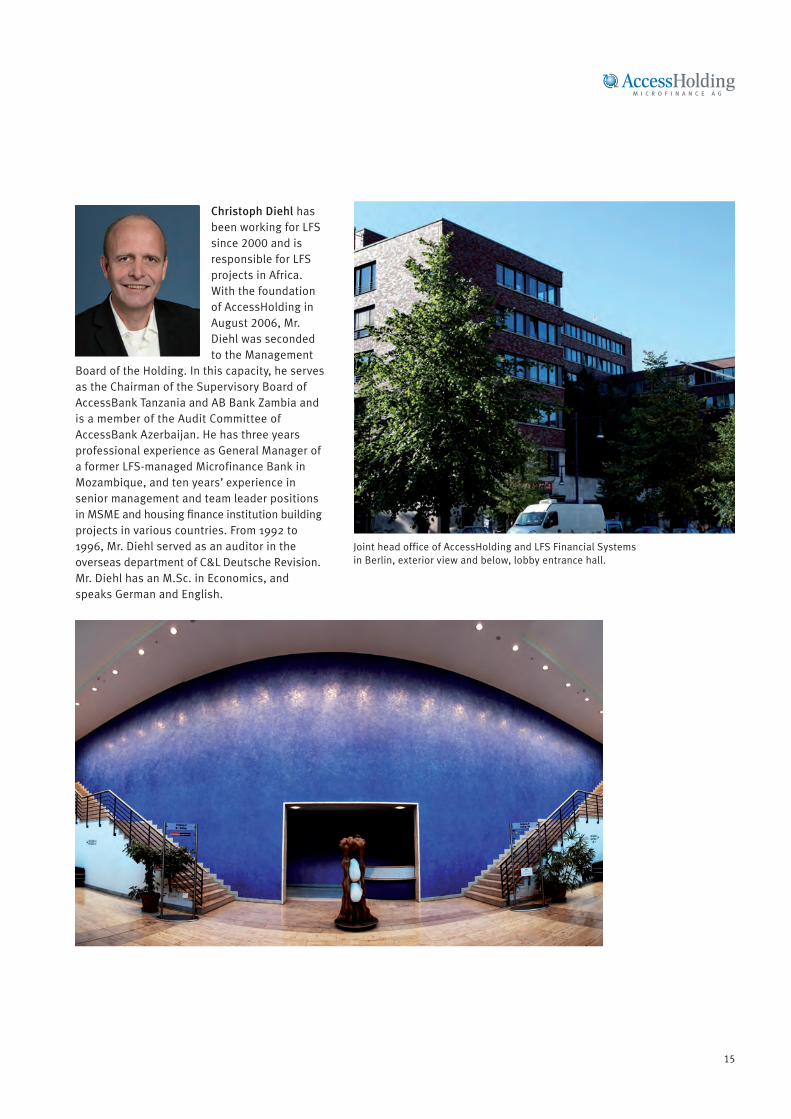

Christoph DiehlhasbeenworkingforLFSsince2000andisresponsibleforLFSprojectsinAfrica.WiththefoundationofAccessHoldinginAugust2006,Mr.DiehlwassecondedtotheManagement

BoardoftheHolding.Inthiscapacity,heservesastheChairmanoftheSupervisoryBoardofAccessBankTanzaniaandABBankZambiaandisamemberoftheAuditCommitteeofAccessBankAzerbaijan.HehasthreeyearsprofessionalexperienceasGeneralManagerofaformerLFS-managedMicrofinanceBankinMozambique,andtenyears’experienceinseniormanagementandteamleaderpositionsinMSMEandhousingfinanceinstitutionbuildingprojectsinvariouscountries.From1992to1996,Mr.DiehlservedasanauditorintheoverseasdepartmentofC&LDeutscheRevision.Mr.DiehlhasanM.Sc.inEconomics,andspeaksGermanandEnglish.

JointheadofficeofAccessHoldingandLFSFinancialSystemsinBerlin,exteriorviewandbelow,lobbyentrancehall.

16

AccessHolding|AnnualReport2011

Corporate Governance/Organization

3. Supervisory Board

WithinthegovernancestructureofAccess-Holding,theSupervisoryBoardisresponsibleforthedeterminationofthegeneralbusinessstrategy,theappointmentoftheManagementBoardmembers,themonitoringofoperationalactivitiesandthedecisiononallinvestmentsordivestments.TheSupervisoryBoardisnotinvolvedintheday-to-dayoperativebusinessoftheHolding.Itcurrentlyconsistsofthefol-lowingsevenmembersnominatedbythesevenmajorshareholdersofAccessHolding.

Edvardas BumsteinasisaSeniorInvestmentOfficerattheEuropeanInvestmentBank(EIB),beingresponsibleformicrofinanceoperationsintheAfrica,CaribbeanandPacific(ACP)region.Heisamemberofgovernancebodiesandinvest-mentcommitteesofvariousmicrofinancein-vestmentcompanies.PriortojoiningEIBin2005,heworkedasconsultantandteamleaderinoperativemicrolendingprojects.Mr.BumsteinasholdsaM.Sc.inTransitionEconomicsfromtheLondonSchoolofEconomicsandPoliticalScience.

Frank BellonisaPrincipalSectorEconomistatKfW.Heisresponsibleformicrofinanceanden-vironmentalfinancewithinKfW’sCompetencyCenterforSustainableEconomicDevelopmentandGlobalFunds.HeservedalsoasDirectorofKfW‘sCountryOfficesforBoliviaandChileaswellasforBosnia-Herzegovina.FrankBellonhasmorethan20yearsofexperienceindevelop-mentbankingandprojectfinanceandisamem-berofseveralgovernancebodiesoffinancinginstitutions.FrankBellonholdsaMasterDegreeinEconomicsfromtheUniversityofTübingen.

Bernd ZattlerisChairmanoftheSupervisoryBoardsofAccèsBanqueinMadagascarandABMicrofinanceBankNigeria,andDirectorontheSupervisoryBoardofAccessHolding.BeforethefoundationofLFS,heworkedforamultinationalfirmandininstitutionsengagedindevelopmentfinance.HefoundedLFS,AccessHolding’stechni-calpartnerin1997,andhassincethenbeenManagingDirectorandmajorityownerofthefirm.

17

MembersoftheSupervisoryBoard:(lefttoright)EdvardasBumsteinas,FrankBellon,BerndZattler,HywelRees-Jones,EltjoKok,SyedAftabAhmed,TryfanEvans

Hywel Rees-JonesisaManagingDirectoratCDCwithprimaryresponsibilityforglobalsectorprivateequityfunds,microfinanceanddebt.Hisentirecareerhasbeenfocusedontheemergingmarketswherehehasworkedasadevelopmenteconomist,lender,privateequityinvestorandfundoffundsinvestor.Hehaslivedformorethan20yearsinemergingmarketsbothinAfricaandAsia.Hehasbeenadirectorofbusinessesintheagribusiness,financial,FMCG,andpropertysectors.

Eltjo Kokisacorporatefinancialadvisor.HefunctionsasBoardroomAdvisorandisspecia-lisedinimprovingpersonal,teamandcorpo-rateperformanceandeffectiveness.HeworkscurrentlywithDirectorsandBoardsofmulti-nationalandfamilyownedcompanies.HehasbeeninvariouspositionsinhiscorporatelifesuchasFinanceDirector,DivisionalRegionalDirectorandGlobalHRDirector.

Syed Aftab Ahmed workedwiththeInternatio-nalFinanceCorporation(IFC)invariouscapa-citiesfromAugust1989untilhisretirementinDecember2006.ThelastpositionheldatIFCwasasSeniorManagerinchargeoftheGlobalMicroandSmallBusinessFinanceGroup.Inthiscapacity,Mr.AhmedledthedevelopmentofIFC‘sglobalmicrofinancebusinesspracticeandrelatedinvestmentportfolio.Sincehisre-tirement,IFChasnominatedhimontheBoardofDirectorsandtheinvestmentcommitteesofvariousportfoliobanksandfinancialinstitutions.Mr.AhmedholdsaMaster‘sdegreeinEconomics.

Tryfan EvansisDirectoroftheOmidyar-TuftsMicrofinanceFundandresponsibleforinvest-mentstrategy,andportfolioconstructionandmanagement.Mr.EvansalsoservesasDirectorofInvestmentsintheTuftsUniversityInvest-mentOfficewhereheisresponsiblefortheendowment‘sinternationalprivateequitypro-gram.Hehasinvestmentexperienceinover20developingcountriesinAfrica,LatinAmerica,EasternEurope,andSouthandSoutheastAsia.

History of AccessHolding – Main Events and Milestones

Sinceitsestablishmentin2006,AccessHoldinghasinvestedineightcommercialmicrofinancebanks.Twohadalreadybeenco-foundedbyLFSpriortotheestablishmentoftheHolding:MicroFinanceBankofAzerbaijan(whichwaslaterrenamedintoAccessBank,‘ABA’)andSocremoBancodeMicrofinançasinMozam-bique.TheinvestmentinSocremowashoweversoldin2008astheshareholdersoftheBankcouldnotreachagreementonitsintegrationintotheAccessBanknetwork.

ThebanksfoundedaftertheestablishmentofAccessHoldingareAccèsBanqueMadagascar(February20071),AccessBankTanzania(Nov-ember2007),ABMicrofinanceBankNigeria(November2008),AccessBankLiberia(January2009),AccessBankTajikistan(April2010)andABBankZambia(October2011).Thefoundationofthesebankswasspearheadedandcoordi-natedbyAccessHoldingastheleadinvestor,incollaborationwithotherinternationalandlocalinvestors.

AllsevenmemberbanksoftheAccessBanknetworkhavebeendevelopinginlinewith(oraheadof )investorexpectations.Thissuccess-fulperformancehasenabledAccessHoldingtobecomeprofitable(basedonIFRS)alreadyin2008,onlytwoyearsafteritsfoundation.Whilethetotalnetwork’sgrossoutstandingloanportfoliogrewtoEUR351.6millionattheendof2011,97%ofoutstandingloansamountedtolessthanEUR10,000,indicatingaclearfocusonthemicroenterpriseclientele.

LFShasalsobeensignificantlyexpandedsinceAccessHolding’screationin2006,enablingeachnetworkbanktodrawonprofessionalsupportofitsIToperationsatanytime.

Moreover,theAccessBanknetworkhasalsomaintainedanexcellentloanportfolioquality,withaconsolidatedPortfolio-at-Riskgreater30days(PAR 30)ratioaround1%andannualwrite-offratiosofbelow1%ineveryyearsinceinception.Thesequalityindicatorsarecurrentlyunrivalledamonggloballyoperatingmicro-financebanknetworkswithsimilarlendingmethodologies.

However,theimpactofAccessBanksisbyfarnotlimitedtotheirlendingactivities.Overthelastyears,thenetworkbankshaveevolvedintosignificantretailbanksintheirrespectivecoun-triesofoperations,withatotalofmorethan3,300staffspreadover68branchesinsevencountries,theyhavebuiltupatotalof482,846customerdepositaccountswithaggregatebalancesofEUR187.8million.Thetotalclientbasewillexceed500,000inthefirsthalfof2012,andisprojectedtoreachonemillionclientsbytheyear2016.

Inparalleltothedevelopmentofitsbankingnetwork,AccessHolding(incollaborationwithLFS)hasbuiltupitsheadofficestructuresinBerlin.Since2010,networkbanksarecom-prehensivelysupportedbycentralpersonnelworkinginareassuchascredit,retail,productdevelopment,internalaudit,humanresources,learning&development,oraccounting&finance.TheinformationtechnologyarmofLFShasalsobeensignificantlyexpandedsinceAccessHolding’screationin2006,enablingeachnetworkbanktodrawonprofessionalsupportofitsIToperationsatanytime.

1Thedatesinbracketsrefertothemonthsinwhichtherespective

banksopenedtheirdoorstothepublic,notwhentherespectivelegal

entitieswerecreated.

18

Summary

AccessHolding|AnnualReport2011

AccessHoldingisfoundedPreparationoffirstroundofinvestments

InvestmentsinexistingbanksinAzerbaijan andMozambique

Foundationandlaunchofnetworkbanksin MadagascarandTanzania

CDCjoinstheshareholdergroup

AHbecomesprofitableDivestmentfromSocremoBank(Mozambique)

LaunchofABMicrofinanceBankNigeria

LaunchofAccessBankLiberiaFMOjoinstheshareholdergroup

LaunchofAccessBankTajikistanSignificantexpansionof

headofficestructures

LaunchofABBankZambiaMoveintonewpremisestosupportfurther

expansionAgreementonstrategictakeoverof

AccessBankinAzerbaijan

19

2006

2007

2008

2009

2010

2011

Watchmakerfrom Azerbaijan

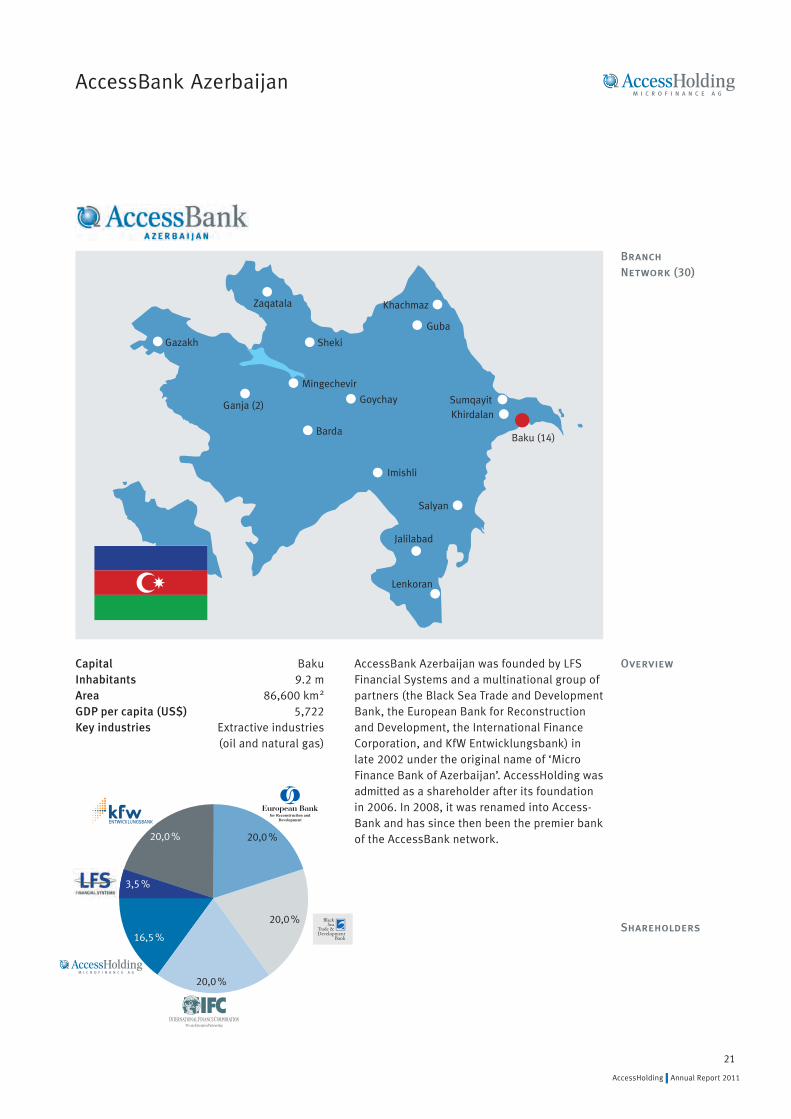

AccessBank Azerbaijan

AccessBankAzerbaijanwasfoundedbyLFSFinancialSystemsandamultinationalgroupofpartners(theBlackSeaTradeandDevelopmentBank,theEuropeanBankforReconstructionandDevelopment,theInternationalFinanceCorporation,andKfWEntwicklungsbank)inlate2002undertheoriginalnameof‘MicroFinanceBankofAzerbaijan’.AccessHoldingwasadmittedasashareholderafteritsfoundationin2006.In2008,itwasrenamedintoAccess-BankandhassincethenbeenthepremierbankoftheAccessBanknetwork.

21

AccessHolding|AnnualReport2011

Overview

BranchNetwork (30)

Shareholders

Capital BakuInhabitants 9.2mArea 86,600km2

GDP per capita (US$) 5,722Key industries Extractiveindustries (oilandnaturalgas)

Baku(14)

KhirdalanSumqayit

Guba

Khachmaz

Mingechevir

Ganja(2)

Gazakh

Zaqatala

Sheki

Goychay

Barda

Imishli

Jalilabad

Lenkoran

Salyan

20,0 %

16,5 %

20,0 %

20,0 %

20,0 %

3,5 %

loans,housingandagriculturalloans,differenttypesofcustomerdeposits,avarietyofmoneytransferservicesaswellaspaymentcards.AgrowingnumberoflargerSMEsarealsousingadvancedbankingservices,suchassalarypaymentfacilitiesandup-to-datetradefinan-cingproducts,suchaslettersofcredit(L/C)andlettersofguaranteewithintheframeworkoftheEuropeanBankforReconstructionandDevelopment’s“TradeFacilitationProgram”.

AccessBank Azerbaijan

Products

AccessBankhasdemonstratedstronggrowthfromthebeginningandhasrecentlyopenedits30thbranch.Ithasquicklyevolvedintotheleadingprovideroffinancialservicestomicro,smallandmedium-sizedenterprises(MSMEs)inAzerbaijan.AsofJanuary2012,AccesBankhasdisbursed528,882loansforUSD1,853,365,972sinceitsinception.ButevenbeyondtherealmofMSMEfinance,AccessBankisarecognizedqualityleaderinthecountry’sbankingsector,holdingthehighestratinginthebankingsector(LongTermIDRBB+/viabilityratingb+,Fitch).

Intermsoftotalbankingassets,AccessBank‘smarketsharewas2.81%attheendof2011withUSD373,086.47.Itisranked7thoutofallbanksinthecountry.Inaddition,intermsoftotalloanportfolio,AccessBank‘smarketshareis3.12%attheendof2011withUSD289,381.71.

Thebankhaswonvariousprestigiousawards(bydifferentinternationalinstitutes)asthebestbankinAzerbaijaninthepastyears.

Initspursuittobea“housebank”foritstargetclienteleofMSMEsandgenerallower/middleincomegroupsinAzerbaijan,ABAhassucces-sivelybroadeneditsrangeofproducts.Itnowoffersvarioustypesofbusinessandpersonal

BusinessDevelopment

AccessHolding|AnnualReport2011

22

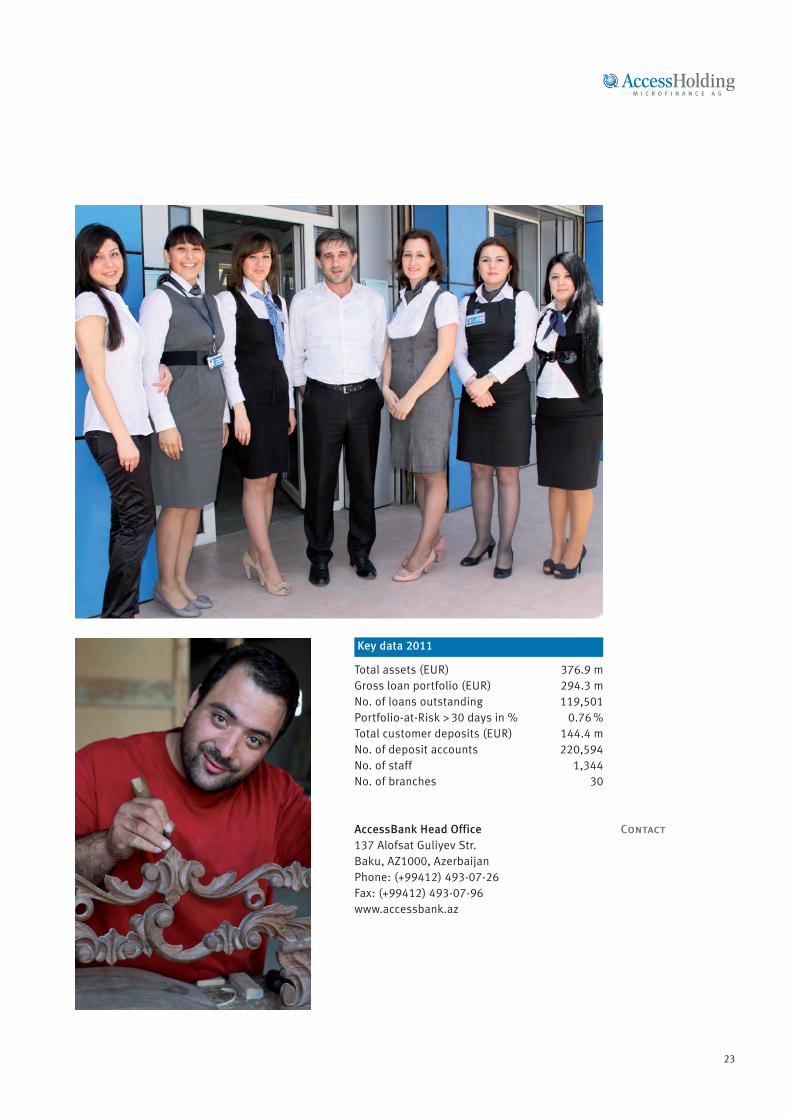

Key data 2011

Totalassets(EUR) 376.9mGrossloanportfolio(EUR) 294.3mNo.ofloansoutstanding 119,501Portfolio-at-Risk 30daysin% 0.76 %Totalcustomerdeposits(EUR) 144.4mNo.ofdepositaccounts 220,594No.ofstaff 1,344No.ofbranches 30

AccessBank Head Office137AlofsatGuliyevStr.Baku,AZ1000,AzerbaijanPhone:(+99412)493-07-26Fax:(+99412)493-07-96www.accessbank.az

23

Contact

Key data 2011

Totalassets(EUR) 25.4mGrossloanportfolio(EUR) 14.3mNo.ofloansoutstanding 20,883Portfolio-at-Risk 30daysin% 4.43%Totalcustomerdeposits(EUR) 17.8mNo.ofdepositaccounts 71,183No.ofstaff 561No.ofbranches 14

AccésBanque MadagascarImmeubleBirHackeimLotIBG21Ter,AntsahavolaAntananarivo101MadagascarPhone:(+261)202232234Email:[email protected]

AccèsBanque Madagascar

Businessdevelopment

Contact

AccèsBanqueMadagascar(ABM)wasestab-lishedinOctober2006byAccessHoldinginpartnershipwithagroupofinternationalandlocalco-investors.Thebankopeneditsfirstbranchinthecountry’scapitalAntananarivoinFebruary2007andhassincethenbuiltupanetworkof14branchesinthecapitalandothertownsofthecountry.

Withmorethan560employeesandover70,000clients,ABMhasevolvedintoasigni-ficantplayerandaleadingemployerintheMalagasybankingsector.Despiteaclearfocusonthecoretargetgroupofmicro,smallandmedium-sizedenterprises(MSMEs),thebankcatersforabroadvarietyofclientsandaspirestobecomea“housebank”forthelower/middleincomestrataoftheMalagasypopulation.

ABM’sproductrangecomprisesloanstomicroandsmallenterprisesbutincreasinglyalsotomediumentrepreneurs.Bankingservicescom-prisecurrentandsavingsaccountsaswellastermdepositfacilitiesandavarietyofpaymentservices(checksandnationalwiretransferservices).

Overview

Products

AccessHolding|AnnualReport2011

24

Capital AntananarivoInhabitants 21.9mArea 587,041km2

GDP per capita (US$) 421Key industries Agriculture andtourism

Antananarivo(11)

AntsirabeBetafoAmbatolampy

Shareholders

16,8%12,0%

13,6%

44,0 %

13,6%

AccèsBanqueMadagascar

Seamstressfrom Tanzania

Key data 2011

Totalassets(EUR) 25.1mGrossloanportfolio(EUR) 15.0mNo.ofloansoutstanding 12,305Portfolio-at-Risk 30daysin% 1.20%Totalcustomerdeposits(EUR) 18.2mNo.ofdepositaccounts 77,356No.ofstaff 342No.ofbranches 6

AccessBank Tanzania LtdP.O.Box95068,Dar-es-Salaam,TanzaniaTel:+255-22-2774355Fax:+255-22-2774340Email:[email protected]://www.accessbank.co.tz

AccessBank Tanzania

27

Businessdevelopment

Contact

AccessBankTanzania(ABT)wasestablishedbyAccessHoldingandfourinternationalco-inves-torsasthethirdmemberoftheAccessBanknetworkon21stNovember2007.Thebankoper-atesunderafullcommercialbanklicenseandhasbynowopenedsevenbranchesinthecom-mercialcapitalDaresSalaamanditswiderperimeter.

Sinceopeningitsdoorsinlate2007,ABThasevolvedintooneofthesignificantprovidersofloansandotherfinancialservicestoMSMEsandthelower/middleincomesegmentsinDaresSalaam.ABThasalsoemergedasoneofthequalityleadersintheTanzanianmicrofi-nancesector,witharrearsratesconsistentlybelowmostofitscompetitors.Thebankhasmorethan80,000clientsandisamongthetenlargestemployersintheTanzanianbankingsector.ABTnowplanstoexpanditsgeographi-calfootprinttootherregionsofTanzaniainitslong-termpursuittobecomeoneoftheleadingretailbanksinthecountry.

ABT’sproductportfoliocomprisesmicroandSMEloansonthecreditside.Bankingservicesincludedepositproducts,butalsoaccountproductsincludingcurrentaccounts,savingsaccounts,savingsplanaccountsandstudentaccounts.Avarietyofmoneytransfersystemsarealsooffered.

Overview

Capital DodomaInhabitants 43.2mArea 945,203km2

GDP per capita (US$) 527Key industries Agriculture tourismand mineralexploitation(gold)

DaresSalaam(7)

Dodoma

Shareholders

AccessHolding|AnnualReport2011

Products

8,3%10,7%

15,8%

50,7%

14,4%

Key data 2011

Totalassets(EUR) 20.2mGrossloanportfolio(EUR) 17.1mNo.ofloansoutstanding 16,930Portfolio-at-Risk 30daysin% 0.95%Totalcustomerdeposits(EUR) 2.2mNo.ofdepositaccounts 44,460No.ofstaff 467No.ofbranches 8

AB Microfinance Bank Nigeria

Businessdevelopment

Contact

ComparedtomanyothercountriesinSub-Sa-haranAfrica,Nigeria’sfinancialservicessectorismoredevelopedanddiversified,offeringagoodvarietyofproductsandservicesforcor-porateandhighnetworthclients.Howeveritsmicrofinancesectorisstillataninfantstage,withveryfewoperatorsofsignificantscale.Thisimpedesthedevelopmentofthecountry’smicroandsmallbusinesssectoranditsabilitytogenerateemploymentandincome.ABMicrofinanceBankNigeria(ABN)wasesta-blishedbyAccessHoldingandImpulseMicro-financeFundinMay2008,withthreeothershareholders(aslistedbelow)joiningshortlyafteritsfoundation.Thebankopeneditsdoorstothepublicon10thNovember2008afterseveralmonthsofpreparation.

Injustoverthreeyearsofoperations,ABNhasbuiltupasolidbranchpresenceacrossthegreatermetropolitanareaofLagos,coveringalldistrictsofsignificantmicroenterpriseactivity.ABN’svisionistobecometheleadingmicrofi-nancebankinNigeriaandtosetnewstandardsfortheNigerianmicrofinancesectorintermsofprofessionalism,transparencyandefficiency.Bydeliveringappropriatefinancialservicestothetargetgroup,ABMicrofinanceBankNigeriaseekstocontributetoprivatesectorgrowthandinvestment,thushelpingtocreatenewbusinessandemploymentopportunitiesfortheNigerianpopulation.

Asidefromprovidingbusinessloanstomicroandsmallenterprises,ABNalsocollectsdepositsfromthepublicandprovidescurrentaccountsandabasicrangeofpaymentservices.

AB Microfinance Bank NigeriaIkeja(HeadOffice)0,ObaAkranAvenue,Ikeja,LagosNigeriaTel:[email protected]://www.ab-mfbnigeria.com/

Overview

Products

AccessHolding|AnnualReport2011

28

Capital AbujaInhabitants 152.2mArea 923,768km2

GDP per capita (US$) 1,222Key industries Extractiveindustries (oilandnaturalgas)

Lagos(8)

Abuja

Shareholders

12,5%12,5%

15,0%

50,1%

10,0%

AB Microfinance BankNigeria

ClientAccessBank, Liberia

Key data 2011

Totalassets(EUR) 13.5mGrossloanportfolio(EUR) 4.2mNo.ofloansoutstanding 7,078Portfolio-at-Risk 30daysin% 5.15%Totalcustomerdeposits(EUR) 5.2mNo.ofdepositaccounts 67,418No.ofstaff 290No.ofbranches 5

Monrovia Head Office20thStreet,Sinkor,TubmanBoulevard,Monrovia,LiberiaTel:+231(0)77852135+231(0)76358499www.accessbank.com.lr

AccessBank Liberia

31

Businessdevelopment

Contact

AccessBankLiberia-theMicrofinanceBank(ABL)startedoperationsinJanuary2009withitsheadquartersinthecapitalMonrovia,whichaccountsforaboutathirdofLiberia’stotalpopulationof3.5million.ABLisalicensedandregulatedfully-fledgedcommercialbank,whilstbeingthefirstLiberiabanktofocusspecificallyonthemicroandsmallbusinessclientele.Accesstobankingserviceswasuntilrecently(withthemarketentryofABL)limitedtoasmallnumberofmostlyhigh-value,well-connectedcustomers.AccessBankLiberia,TheMicrofinanceBankwasfoundedbyfourrepu-tableinternationalshareholdersinajointefforttosupporttheLiberianbankingsectoringeneralandthecountry’smicrofinanceindustryinparticular.

ABL’smissionistobecomethebankofchoiceforthelowandmiddleincomestrataoftheLiberianpopulation,andthecountry’sleadingprovideroffinancialservicestomicro,smallandmediumenterprises.Withinjustoverthreeyearsofopera-tions,theBankhassignedupmorethan80,000clients,demonstratingthatitsproductofferingofloansanddepositserviceshashittherightspotinthisstillunderservedmarket.

ABLprovidesmicroandSMEloanstoeligiblebusinessowners.Regardingbankingservicescurrentandsavingsaccountaswellasatermdepositoptionareoffered.AllaccountscanbeheldinLiberianDollarandUSDollar.

Overview

Products

Capital MonroviaInhabitants 3.5mArea 111,369km2

GDP per capita (US$) 247Key industries Agriculture

Shareholders

Monrovia(5)

AccessHolding|AnnualReport2011

13,3%17,7%

13,3%

55,7%

Key data 2011

Totalassets(EUR) 15.4mGrossloanportfolio(EUR) 9.6mNo.ofloansoutstanding 4,798Portfolio-at-Risk 30daysin% 1.32%Totalcustomerdeposits(EUR) 450,639No.ofdepositaccounts 402No.ofstaff 237No.ofbranches 4

AccessBank Tajikistan

Businessdevelopment

Contact

Tajikistan’sfinancialsectorisnotyethighlydevelopedbutsincetheendoftheCivilWarin1997,politicalstabilityandforeignaidhaveallowedthecountry‘seconomytogrow.Never-theless,Tajikistan’spercapitaGDPisbyfarthelowestintheCISregion.AccessBankTajikistanisajointventureofAccessHoldingandthreeofitspartnerswithlong-standingexperienceinthesector:theEuropeanBankforReconstructionandDe-velopment(EBRD),theInternationalFinanceCorporation(IFC)andKfWEntwicklungsbank.Thebankwasinauguratedon29March2010andhasitsheadofficeaswellasfourbranchesinthecapitalDushanbe.

AccessBankTajikistan’svisionistobecometheleadingmicrofinancebankinTajikistanandtosetnewstandardsfortheTajikbankingindustryintermsofprofessionalism,transpa-rencyandefficiency.Bydeliveringappropriatefinancialservicestoitstargetgroup,thebankseekstocontributetoprivatesectorgrowthandinvestment,thushelpingtocreatenewbusinessandemploymentopportunitiesfortheTajikpopulation.Inordertofacilitateaccesstofinancealsoinotherpartsofthecountry,AccessBankTajikis-tanaimstodevelopastrongregionalpresenceinthecomingyears.

Operatingunderafullbankinglicense,Access-Bankoffersabroadrangeoffinancialservicestomicro,smallandmedium-sizedenterprises(MSMEs)inTajikistanaswellasthegenerallowerandmiddleincomestrataoftheTajikpopulation.DespiteitscurrentfocusonMSMElending,thebankwillsuccessivelyintroducearangeofotherfinancialproductsincludingagricultural,housingandconsumerloans,aswellasforeignexchangeandotherbankingservicesinthecomingyears.

AccessBank Tajikistan61/1Firdavsistr.Dushanbe,734061RepublicofTajikistanPhone:+992372319824

Overview

Products

AccessHolding|AnnualReport2011

32

Capital DushanbeInhabitants 7.6mArea 143,100km2

GDP per capita (US$) 820Key industries Productionofaluminum growingofcotton

Dushanbe(4)

Shareholders

12,0 %

52,0 %

18,0%18,0%

AccessBankTajikistan

AB Bank Zambia’sFirst Customer

Key data 2011

Totalassets(EUR) 3.9mGrossloanportfolio(EUR) 380,123No.ofloansoutstanding 407Portfolio-at-Risk 30daysin% N/ATotalcustomerdeposits(EUR) 83,821No.ofdepositaccounts 1,433No.ofstaff 84No.ofbranches 1

Stand No. 7393, Ground Floor, ChaindaplaceoffCairoRoad,Lusaka.Monday-Friday08:00-16:00Tel:(+260)211220835/36/38/40Email:[email protected]

AB Bank Zambia

Businessdevelopment

Contact

ABBankZambia(ABZ)openeditsdoorsinOctober2011andistheseventhandcurrentlyyoungestmemberoftheAccessBanknetwork.ItwasfoundedbyAccessHoldingincollabora-tionwithfourofitslongstandingpartners:KfWEntwicklungsbank,theInternationalFinanceCorporation,theDutchdevelopmentfinancein-stitutionFMO,andtheBelgium-basedImpulseMicrofinanceFund.

ABZaimstoevolveintooneoftheleadingpro-vidersoffinancialservicestothistargetgroupinZambiaandtosetindustrystandardsintermsofthespeed,easeandqualityofMSMEbanking.ABZ’sbranchnetworkiscurrentlylimitedtoLusakabutthebankplanstoexpandtootherregionsinthecomingyears.Ithashadagoodstartofoperations.

ABZoffersarangeofloananddepositproductsfocusingonthecoreclienteleofmicro,smallandmedium-sizedenterprisesaswellasthegenerallower-/middleincomegroupsofthecountry.Bankingservicesincludetermdeposit,savingandcurrentaccountsaswellasasavingplanandpaymentservicessuchasasalaryproject,mobilepaymentandmoneytransfersystems.

Overview

Products

Capital LusakaInhabitants 13.5mArea 752,618km2

GDP per capita (US$) 1,253Key industries Agricultureand copperindustry

Lusaka

Shareholders

35

AccessHolding|AnnualReport2011

12,5%12,5%

12,5%

51,0%

12,5%

Corporate Social Responsibility in the Holding

Asaninternationallyoperatingbanknetwork,wefeelthatourresponsibilityismanifold.Asaconsequencewehaveovertheyearselaboratedanindividualandcomprehensiveprofileofthisresponsibility.ThisprofilecomprisesallactivitiesandguidelinesinareasinwhichAccessHoldingisdeterminedtotakeonarolethatgoesbeyondcompliancewithlegalobligationsandbasicethicalstandards.

AccessHoldingattributeshighimportancetoconsideringandactingintheinterestofourdifferentstakeholders(suchasclients,commu-nities,shareholders,theenvironment)inordertodobusinessinasustainableandresponsibleway.Weareawarethatweoperateincountrieswhereitcanseemespeciallyimportantthattheprivatesectortakesonitsresponsibilitytocontributetosustainabledevelopment.Ournetworkbanksthereforenotonlyconsidertheirprofitabilityandgrowthbutarecommittedtotheinterestsofthesocietiesandenvironmentstheyareoperatingin.Assuch,ourbanksnotonlystandoutbecauseoftheirmicrofinance-bankingexpertisebutalsobecausetheirbusi-ness modelisbackedbyacorporateculturethathasastrongethicalandmoralbasis.

OperatinginthemicrofinancesectormakesitespeciallyimportantforAccessHoldingtograntthesustainableincorporationofresponsiblepracticesintobusiness.Wearedoingbusinessindevelopingcountriesandtargetsocialgroupsusuallyexcludedfromthetraditionalbankingsystem.Thereforeourengagementisfocusedon:

Our internal guidelinesThecommercializationofmicrofinanceisincreas-inglyaccompaniedbytheriskthatsomeplayersinthemarketareseekingshort-termprofitondispenseofthecustomer.Thelatterismoreandmorethreatenedbyover-indebtednessandotherimmoral/unethicalpractices.ThereforeAccessHoldingisstressingitsdedicationtoresponsiblefinance.

ItisatthecoreofAccessHolding’sCSRphilosophytomakeacontributiontowardsasustainabledevelopmentofthemicrofinance

industryworldwide.Consequentlyprotectingtheclientbylendinginaresponsiblefashionisoneofourkeyprinciples.

Inaddition,itisanintegralpartofAccessHolding’sCSRphilosophytomakeacontributiontowardsasustainabledevelopmentofthemicrofinanceindustryworldwide.Consequentlyprotectingtheclientbylendinginaresponsiblefashionisoneofourkeyprinciples.

Thefollowingguidelineshavebeenformulatedonthisbehalfandareofforemostimportancenotonlyontheholdinglevelbutforeachindividualbank.Inordertoavoidover-indeb-tednessandprotectourclientsweare:

buildinglong-termrelationshipswithour clients;

conductingathoroughandintegral analysisofpaymentcapacitywhichalso includesforexampletherespectoffamily relatedpaymentobligations;

makingsureinstallmentsrepresentonlya limitedcomponentoftheborrower’s monthly‘freecashflow’,

guaranteeingthatreceivingloansisnot conditionalontheclientdepositingmoney inthebank

Responsiblecollectionofoverdue installments

Endorsing the SMART CampaignAccessHoldingisstrivingevernewwaystoemphasizetheimportanceofavoidingover-indebtedness.Assuch,weareaconvincedfollowerandendorseroftheSMARTcampaignwhichissupportedbyallbanksinthenetwork.TheSmartCampaignisaglobalefforttounitemicrofinanceleadersaroundacommongoal:tokeepclientsasthedrivingforceoftheindustry.Acertificationprogramisinprogress.

SmartMicrofinanceencompassesthefollowingcoreClientProtectionPrinciplestohelpmicro-financeinstitutionspracticegoodethicsandsmartbusiness:

Appropriateproductdesignanddelivery Preventionofover-indebtedness Transparency Responsiblepricing

36

Our Philosophy

Responsible Lending/Client Protection

AccessHolding|AnnualReport2011

“All clients of AccessBank should bebetter off using the bank’s products than not.”

Fairandrespectfultreatmentofclients Privacyofclientdata Mechanismsforcomplaintresolution

Inordertodemonstratethe(long-term)impor-tanceattributedtoresponsiblelendingandclientprotection,AccessBankinAzerbaijanhasalreadybeenauditedbytheSMARTcommitteewiththereassuringresultofbeingextraordinarilygoodatavoidingover-indebtednesscomparedtoindustrystandards.

AccessHoldingisconvincedthatthekeytoanysuccessfulorganizationismotivatedandsatisfiedemployeesthatstriveforexcellence.Thereforeandtosetstandardsinourcountriesofoperationswithofteninsufficientlegalsafetyfortheemployee,weapplythefollowingHRpoliciesacrossthenetworktosafeguardthewellbeingandsatisfactionofourstaff:

Clearjobdescriptionsandopencommuni- cationchannels

Employee-friendlyworkingconditionsand avarietyofmotivationalschemessuch additionalinsurancepackages,team buildingdays,sportsevents,andothers. Employmentopportunitiesforrecent graduates–givingyoung,inexperienced talentstheopportunitytohaveafull- scalejobentryanddeveloptheirpotential

Highlytransparent,meritandperformance basedinternalpromotionpolicies,with manyverticalandlateraldevelopment opportunitiesinalldepartments,anda relativelyfasttransferofresponsibilities.

Employmentoflong-termstaffwith tailoredcareerdevelopmentthrough classroomtraining,trainingonthejob, andsupportfromcolleagues

Performance-orientedpaypackages Promotionofequalopportunities

LivinguptosocialandenvironmentalstandardsisofhighmoralimportancetoAH.WehavedevelopedourownSocialandEnvironmentalManagementSystem(SEMS)toensuresocialandenvironmentalresponsibilitythroughoutthenetwork.TheSMESisbasedonacoresocialandenvironmentalpolicyandprovidesindividualAccessBankswithasetofcoreproceduresandguidelines.TheseSocialandEnvironmentalPerformanceStandards(SEPS)thatAccessHoldingseekstoimplementinallAccessBanksfollowtheInternationalFinanceCorporation(IFC)’sMicrofinanceExclusionListthatforbidsinvestmentsinpotentiallyhazar-dousprojects.Inaddition,AHfollowstheCDCInvestmentCodethatsetsoutgeneralguidelinesforethicalinvestmentpractices.Itrequiresre-sponsiblebusinessmanagementofenvironmen-tal,socialandgovernance(“ESG”)mattersandalsofeaturesanExclusionList,whichspecifiesbusinessesandactivitiesinwhichCDC(andtherebyAH)willnotinvest.

Indaytodaybusinessoperations,AHiscom-mittedtoaresponsibleuseofofficesuppliesandotherscarceresourcessuchaswaterandenergy.

37

Human Resources

Corporate Social Responsibility in the Holding

EachAccessBankhasitsindividualwayoftranslatingthecorporateprinciples.Allofournetworkbanksstrivetobegoodcorporateciti-zensbygivingbacktothecommunitiestheyareoperatingin.Besidesworkinghardontheirprofitability,thefollowingtwoexamplesfrompracticeshowAB’scommitmenttobeingagoodcorporatecitizen.

ABA: Building inclusive communitiesAccessBankinAzerbaijanplaysanimportantrolenotonlyintheeconomicdevelopmentoflocalcommunitiesacrossthecountry.Italsosupports,sponsorsandencouragesstafftobecomeinvolvedincharitableandcommunityprojectsthatbothbenefitandpromotetheevo-lutionofinclusivelocalcommunities.Examplesofsuchprojectsin2010included:sponsoringtheGirlsLeadingOurWorld(GLOW)summercampforschoolgirlsfromtheregionsofAzer-baijan,withparticipationofanAccessBankfemalemanager;distributionoffoodtoneedyfamiliesfortheholidaysbyBankstaff;regularvisitsbystafftovarioushomesfororphans,disabled,pensionersandveteranstodistributegoods,andprovideentertainmentandcompany;sponsorshipandjudgingoftheAzerbaijaniportionofthe‘WritingOlympics’,aninternatio-nalEnglishlanguagewritingcompetition;sponsorshipofthe‘SeeinginColor’artexhibi-tionandworkshopforyoungAzeriartistsorganizedbytheBritishCouncil;financingandprintingofahandbookfordoctors,caregiversandrelativesofpeoplewithDown’ssyndrome;aswellasmanymore.Besidesfromhavingastrongfocusoncommunitydevelopment,ABAisalsotheonlybankinAzerbaijantosubscribetotheUnitedNationsGlobalCompact.

ABT: Children dental care campaignAccessBankTanzaniasponsoredthelaunchofacampaignfocusingonChildrendentalcare.ItwasheldincapitalDaresSalaamonthegroundsofalocalschool.TheeventwhichwassponsoredbyABTwasattendedbyfiveschools.Itreachedasignificantaudienceof500studentsandtheirteachers.Thecampaignfocusedonconvincingchildrentobrushtheirteethonaregularbasistoavoidallkindsofdentaldiseases.InherspeechMissJaneth,managerforMarketingandPublicRelationsat

ABT,advisedthechildrentotakegoodcareoftheirteethiftheywanttopursueasuccessfulcareerinmarketingorteaching.Mr.Kalabu,thechairmanoftheforumthankedtheABTforitssponsorship.ThecampaignistobecontinuedandABTwillsponsormoresimilarcampaignsacrossdifferentschoolsinTanzania.

ABM: Towards a cleaner environmentAccèsBanqueisveryconsciousaboutitssocialresponsibilityandhasdefinedacorefocusareaforitsengagement.ABMwantstomakeacontributiontoprovidingahealthyandcleanenvironmenttothepopulationoftheislandandthereforeparticipatesinthecleanupoftheareastheyareactivein.AssuchABMhasrecentlydonatedcleansingkitstoapproxi-mately40fokontany(traditionalMalagasyvillages).Eachkitcontainedacombinationofboots,wheelbarrows,bladesandgrates.InthefirstphaseofthisenvironmentaloffenseonlyfokontanyssituatedclosetoanAccèsBanquebranchhavereceivedcleansingkitswhereasanestimatedpopulationof80,000peoplecouldbenefitfromtheproject.From2012on,ABMisgoingtoenlargeitsfocusandwillreachouttoevenmorevillages.Inadditiontothisenviron-mentalinitiativeABMalsoinvestsintheareaofeducation.Assuch,atthebeginningofthelastschoolyear,alargenumberofschoolkitscontainingexercisebookshavebeendistribu-tedtoover40publicprimaryschools.30,000pupilswerereachedbythisinitiative.

38

Communitydevelopment/ CSR on site

AccessHolding|AnnualReport2011

ABL: Empowering children in the communityThroughanumberofmeasuresABLstrivestoemphasizethespecialimportanceofchildrentotheircommunities.Onthisbehalf,ABLor-ganizesandsponsorsanumberofeventsthattargetchildrendirectlysuchasthefollowing:

Adrawingcompetitionwasorganizedand carriedoutbyABLstaffatHeadoffice. 15schoolkidscamefrom12different schoolstodrawwhattheythinkabouta bankandexplaintheirdrawings.The winnersgotprizesandwerefeaturedin ABL’S2011Calendar.Allthekidswere givenatouroftheABLfacilitybyourstaff, showingthemhowbankingworks.This wasdonetoeducateLiberiankidsabout theimportanceofbanking.

AFootballTournamentwashostedfor around200schoolkidswhoseschoolsare bankingwithABL.Theeventwascoordi- natedby10ABLstaffthatplayedtheroles ofreferee,linesmenandmatchcommission- ers.Winnersweregivenprizesandwere encouragedtotaketheireducation seriously.ABLaimstodiscouragekidsin thecommunityfromearlyschooldropout.

MotherWleh‘sOrphanageconsistsof46 childrendesperatelyinneedofhelp;it wasvisitedbyABLstaffonChristmas.Kids weregivenChristmaspresentsliketoys andclothes.Theorphanagewasgiven detergentsanddisinfectants,beddings andfoodforthechildren.

39

AccessBank‘s Clients

toaskcustomerstopayinadvancebeforedeliveringthefullorder.Thisinturnlimitedthenumberofpotentialclients.

ThroughafirstloanofUSD800fromAccessBankLiberia,Mr.Wellingtonwasabletopre-financehispurchaseswhichhelpedhimtoincreasehissales.DuetohisincreasingincomeafterthefirstloanandanexcellentrepaymentbehaviorhereceivedarepeatloanofUSD1,400foralongermaturity.Thisenabledhimtobuymoreshovelsandwheelbarrowsforhisworkforcewhichincreasedfrom10to35.HerecentlyopenedathirdproductionpointinSinkor,Mon-rovia,andisabletopurchasehigherquantitiesofcementatalowerprice.Mr.Wellingtonhasalsostartedtoproduceblocksofdifferentdesignstomeettheincreasingcompetitionbyawiderchoiceofproductsandbetterquality.AccessBankLiberia,saysMr.Wellington,hashelpedmetogrowmybusinessandgavemetheconfidencetothinkbigger.

40

1. LiberiaHenry Wellington, Producer of Cement Blocks

AccessHolding|AnnualReport2011

AccessHoldinganditsnetworkbanksaregui-dedbyresponsibleandsustainablebusinesspractices.Bybuildingandmaintainingacloserelationtotheirclientele,AccessBanksareinthepositiontotailortheirproductsandservicestotheneedsofthetargetgroup.Thefollowingselectedclientstoriesprovideagoodimpressionofthepositiveimpactsofourbusinessapproachonthosemicroandsmallentrepreneursthatweserve.

HenryWellington,34yearsold,startedtheproductionofcement12yearsagoafterhisgrandfatherhadpassedontohimtheexperi-enceandpassionforthisprofession.TheincomegeneratedfromthebusinessallowedhimtofinancehisstudiesinAccountingattheUniversityofLiberia.However,Mr.Wellingtoncouldhardlymeetthedemandofhisgrowingcustomersontimebecauseofhisfinancialcon-straintsthatlimitedthepurchaseofrequiredcement.Asaconsequencehewasoftenforced

AgnesJacobMollelisahard-workingbusinesswomangrowingmushroomsandraisingpigsinherpremisesinMbesibeach,aresidentialareawithemergingsmallbusinessactivityaround15kmoutsideDaresSalaam.A56-yearoldwidowofMasaioriginwithtwochildrenlivingabroad,AgneshasjustreceivedhersecondloanfromAccessBank’sKijtonyamabranch,whichhasexcellenttransportlinkstothenort-hernperipheryofDaresSalaam.BothloansamountedtoTZS1.6million(around900€)each;thefirstwasusedtoconstructmoresha-desforherpigs,whereasthesecondservestopurchasealargernumberofpigsandaddmoreshelvesforhermushrooms,whichAgnessellstosupermarketsandanumberofindividualcustomers.

IntheNorthernAzerbaijantownofShabran,IlhalmaAlyevaworkswithsevenotherwomenfromhercommunitytomakecarpetsinthetra-ditional“Shirvan”style.Ittakesthreetofourwomentwomonthstoproducethehighqualitycarpet.Whilethishighleveloflaborensuresanexcellentquality,italsomeansthatanexpen-siveproductisbeingmade.Findingbuyerscantakesometime,leavingMs.Aliyevawithlittleincomesheneedstopurchasethematerialsforhernextcarpet.WithloansofAccessBank,Ms.Aliyevahasbeenabletopurchasetheneededmaterialsandalsorepairherloom.Thishasledtoanincreaseinsalaryforthewomenworkingforher,thesepositionsbeingsomeoftheonlypositionsavailabletowomeninhertown.

41

2. Tanzania Agnes Jacob Mollel, Pig Farmer

3. AzerbaijanIlhalma Aliyeva,Carpet Maker

AccessBank Customers

43

Design:MarthaWilleyPhoto archive:StephanieZickertEditorial content:LauraSymma

TheManagementBoardofAccessMicrofinanceHoldingAGisresponsibleforthecontentspresentedinthisdocument.

AccessHolding Management Report 2011

AccessMicrofinanceHoldingAG(AccessHolding),aJointStockCompanyinaccordancewiththeGermanJointStockCompanyAct,basedinBerlin,Germany,isacommercialmicrofinanceholdingcompany.Itsobjectiveistobuildupanetworkofmicrofinance-orientedbanksandtodevelopthesethroughacombinationofequityfinance,holdingservices,andmanagementassistancerenderedbyoneofitsshareholdersandtechnicalpartnerLFSFinancialSystemsGmbH(LFS),Berlin,Germany.AccessHoldingholdsacontrollingstakeinfivefinancialinstitutions,AccessBankTanzania(ABT),AccessBankLiberia(ABL),ABMicrofinanceBankNigeria(ABN),AccessBankTajikistan(ABTJ)andABBankZambia(ABZ).TogetherwithAccessHolding,theseentitiesformagroup,forwhichconsolidatedfinancialstatementsareprepared.TheinvesteecompanyABTisconsolidatedasof31.October2011,whichisthedateonwhichAccessHolding’sownershipstakeinthecompanyincreasedtoabove50percent.

Inaddition,AccessHoldingholdsminoritystakesintwobanks–AccessBankAzerbaijan(ABA)andAccèsBanqueMadagascar(ABM).Theseinstitutionsareclassifiedasassociates,i.e.entitiesoverwhichAccessHoldinghassignificantinfluencebutnocontrol.Accordinglytheseentitiesarenotfullyconsolidatedinthefinancialstatementsbutvaluedatequity(section5ofthisreport).ItisexpectedthatAccessHoldingwillacquireamajoritystakeinAzerbaijanandMadagascarduring2012.Allnetworkbanks,regardlessoftheirstatusassubsidiariesorassociates,areincludedinthegeneralbusinessreportingasprovidedinsections2-4,6and7ofthisManagementReport.ThispartofthereportingdoesnotincludetheassetsandliabilitiesofAccessHoldingitself,nordoesitmakead-justmentsforothershareholdersoftherespectivenetworkbanks.ThesesectionsarethereforenottobereadasconsolidatedfinancialstatementsbutastheaggregatedassetsandliabilitiesoftheAccessHoldingnetworkbanks.

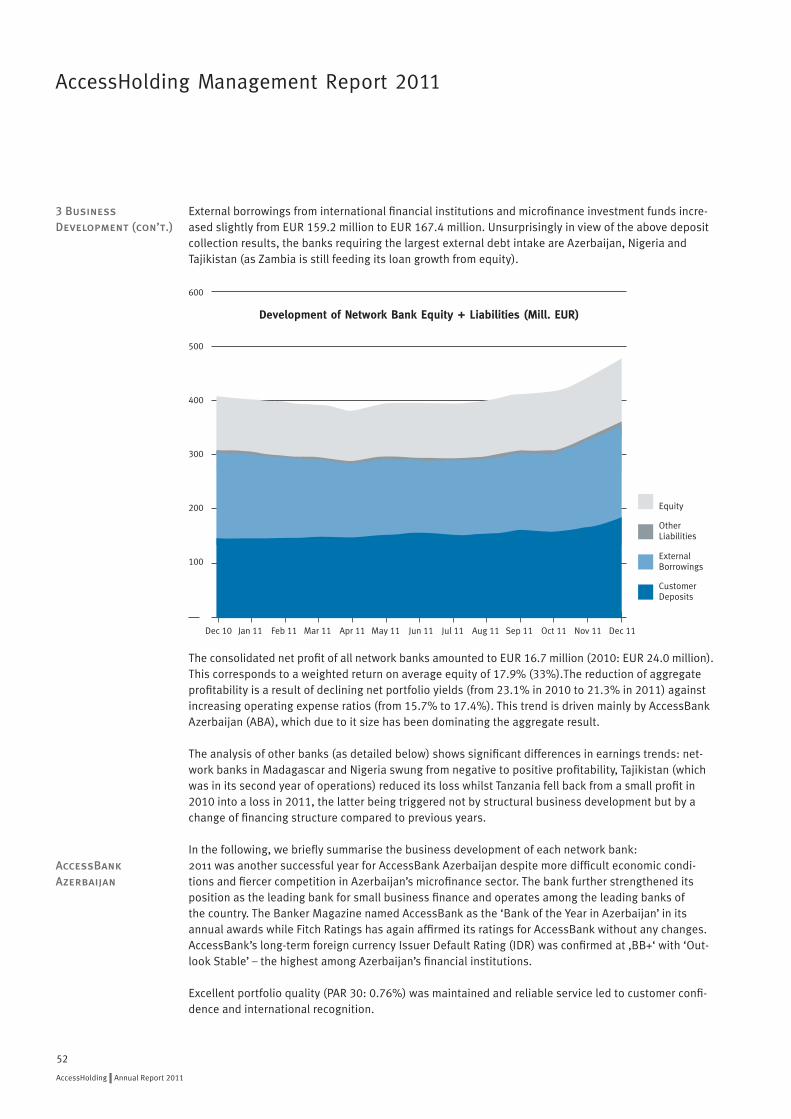

Asinpreviousyears,significantprogresswasmadeinthedevelopmentofthenetworkduring2011.ABZopeneditsdoorstothepublicinOctober,becomingtheseventhAccessBank.By31December2011,totalassetsoftheAccessBanknetworkgrewtoaboutEUR480million(2010:EUR408million);theloanportfolioincreasedtoEUR352million(2010:EUR289million)anddepositstoEUR188million(2010:EUR146million).Creditqualityremainedexcellent,withanetwork-widePortfolio-at-Riskgreater30days(PAR 30)of1%andtotalwrite-offsbelow1%ofthenetwork’syear-endgrossloanportfolio.

Threeofthesevenbanks(ABA,ABN,andABM)closedtheyearwithaprofit.Fuelledmainlybyconti-nuedexcellentperformancesofABAandABN,theaverageweightedreturnonequityforthenetworkbankswas17.9%(2010:33.1%).AccessHoldingposteditsfourthprofitableyearinarow.

Groupintegrationwasstrengthenedthroughstaffexchangeprogrammesbetweennetworkbanksandintensiveknowledgeexchangebetweennetworkbankmanagers(mainlyviacentralworkshopsinareassuchasCredit,Retail,Accounting,InternalAudit,ITorHumanResources).Thebuild-upofheadquarterfunctionscontinuedincooperationwithAccessHolding’stechnicalpartner,LFSFinancialSystems.BothLFSandAccessHoldingmovedintonew,significantlylargerofficepremises,thuscreatingsufficientphysicalcapacityforfurthergrowth.

Morethanthreeyearshavepassedsincetheonsetofthe2008financialcrisisandhopeswerehighthat2011wouldbringaneconomicupswing.However,2011wascharacterizedbytheEurozonedebtcrisis,increasingfoodandoilpricesanddevastatingnaturaldisasterssuchastheTsunamithathitJapan.

However,forAccessHoldinganditsnetworkbanksthesituationoftheworldeconomyhadonlylimitedimplication,asmostoperatingcountriesarelessintegratedintotheglobalfinancialmarkets.Secondaryeffectsfromglobalcrises(e.g.viareducedfundingsupplyfrominternationalfinancialinstitutions)cannotberuledout,butofgreaterimportanceisthespecificeconomicandpoliticalsituationinthecountriesofoperation,whichwillbedescribedbelow.

44

1 Introduction and summary

2 Political andeconomic environ-ment

AccessHolding|AnnualReport2011

Whilemicrofinancemarketsinsomecountriesorsub-regions(e.g.inIndia)havereachedorapproachedsaturationafteryearsofstronggrowth,globalmarketcoveragelevelsremainstilllowgiventhenumberofcountrieswhichareyetlackinganadequatesupplyofsimpleandaffordableaccesstofinancialproducts.

Comparedtoconventionalcommercialbanks,thebusinessofAccessHolding’snetworkbanksisconsideredtobelessvulnerabletoexogenousshocks.Thispremiseisbasedonthewidelyacceptednotionthatmicrofinancelendersarecomparativelyresilienttomacroeconomiceffects,duetotheirhighlyatomisedloanportfoliosandthemicroenterpriseclientele’spredominantfocusonsellingbasicneedsitemsonthedomesticmarket.1AccessHolding’snetworkbanksareusingarigorouson-siteduediligencemethodologytoassesseachborrowerindividually,andtailortheirloansizesandmaturitiesbasedonthisassessment.Inthisway,theyhavebeenabletosustainexcellentassetquality.Moreover,continuedsupportisensuredthroughverystrongshareholdersofAccessHoldingandthenetwork,whocontributetoaconductiveenvironmentforgrowthandanoverallfavourabledevelopment.

Nevertheless,nationaleconomicorpoliticaleventsintherespectivecountriesdohaveacertainimpactonournetworkbanks,especiallythosewithalargershareofSME(SmallandMedium-sizedEnterprises)clients,whichtendtohaveahigherexposuretoexternalshocks.Economicrecessionorpoliticaluncertaintymaydampenloandemand,reducethesupplyof(and/orincreasethecostof )refinancingfunds,andincreasecompetitionasupmarketbanksaremovingdownmarkettoseeknewbusiness.Theextentofsuchimpactsvariesobviouslyfromcountrytocountry,andcanthushardlybegeneralisedwithoutover-simplification.Wewillthusdescribetheminmoredetailintheindividualcountrysectionsbelow.

Theexistingpoliticalorderremainedstablethrough2011,withnonationalelectionsorchallenges.Thesameisanticipatedfor2012andbeyond,withthenextpresidentialelectionsetfor2013whichPresidentIlhamAliyevisgenerallyexpectedtocontestandwin.InDecember,TurkeyandAzerbaijansignedanagreementforconstructionofa2,000kmgaspipelinetotransportAzerbaijan’snaturalgastoEuropeanmarkets.Thefirstdeliveryofgasisnotexpecteduntil2017,butthisagreementsupportsthegeopoliticalimportanceandeconomicstabilityofAzerbaijanforatleastthenextdecadewhileoilproductionbeginstotaperoff.Thiscontractionwasalreadyfeltin2011,withan11%declineinoilproduction,dampeningGDPgrowthto0.1%for2011accordingtotheStateStatisticsCommittee,comparedto5%in2010.Non-oilGDPpostedahealthygrowthof9.4%in2011,with5.8%growthpostedintheagriculturalsectorthankstogoodharvestsin2011,followingweakharvestsin2010–thisimpactedpositivelyonmostruralbusinesses.However,nominalGDPgrewbyamuchstronger20.4%,increasingtoAZN50.1billion(USD63.7billion)fromAZN41.6billion(USD52.9billion)in2010,boostedbyrisingglobaloilprices,thatmorethancompensatedforthereductioninoilproduction.Thishelpedresultinanincreaseinstatebudgetrevenuesof37.7%toAZN15.7billion(USD20.0billion),comparedtoAZN11.4billion(USD14.5billion)in2010,and30.8%inexpenditurestoAZN15.4billion(USD19.6billion)in2011,comparedtoAZN11.8billion(USD15.0billion)in2010.InflationedgedupslightlywithCPIofficiallyreportedat7.9%,comparedwith5.7%in2010and1.5%in2009.

ThehigheroilpricesfedthroughtoanincreaseinthetradesurplustoUSD16.8billion(USD14.8billionin2010)onexportsofUSD26.6billionandimportsofUSD9.8billion.ThissupportedthestabilityofthecurrencyandtheAZNremainedvirtuallyunchangedagainstthelocalreferencecurrency,theUSD,atAZN0.7865versusAZN0.7979at2010-end.Energyexportsshouldensurecontinuedeconomicstabilityinthemedium-term,buttheinherentvolatilityofenergypricesandslowingoilproductionbothreinforcetheneedforeconomicdiversification.Otherconcernsremaincontrolofinflationarypressures,improvingbusinessenvironmentandspreadingthebenefitsofoilincome.

Azerbaijan

45

1Seeexplanationsinchapter8(Risk).ForempiricalunderpinningseeGonzales(2007),‘ResilienceofMicrofinanceInstitutionstoNationalMacroeco-nomicEvents:AnEconometricAnalysisofMFIassetquality’,MixDiscussionPaperNo.1,availableviawww.themix.org

AccessHolding Management Report 2011

Thedevelopmentofthebankingsectorreflectedthatoftheeconomy,withsomebanksfaringbetterthanothers.Totalbankingassetsincreasedby7.3%(toAZN14.3billionfromAZN13.3billion)in2011–whilethetotalloanportfolioincreasedby5%(toAZN9.0billionfromAZN8.6billion)–laggingbehindthe2010growthfigureof14%.Depositsincreasedbyafasterrateof29%toAZN6.7billion.AsaproportionofGDP,totalbankingassetsdecreasedto28%(32%in2010),thetotalloanportfolioto18%(21%in2010),anddepositsincreasedto13%(12%in2010),representingrelativelylowlevelsofbankingpenetration.Themajoritystate-ownedInternationalBankofAzerbaijan,continuestodominate,butsawa9.3%decreaseinitstotalassetsanda15%dropinitscreditport-folioin2011,reducingitsmarket-shareoftotalBankingAssetsto35%andofLoanPortfolioto35%(42%and43%respectivelyat2010-end)

In2011thebankingsectorcontinuedtobenefitfromthethree-yeartaxexemptiononcapitalisedprofit,introducedfrom1January2009tohelpstrengthenthesector.WhiletheCentralBankhasbeenadvo-catingconsolidationinthebankingsectorformanyyears,littleconsolidationhasoccurredandthenumberofbanksat2011-endstoodat44(comparedwith45at2010-end).

AccessBankcontinuedtooutperformthesector,butlesssoin2011thaninyearspastastheeconomicslowdownimpactedonthelowerrungsoftheeconomy.Intermsoftotalbankingassets,AccessBank’smarketsharedecreasedto2.7%from2.8%at2010-endwhiledroppingtoeighthpositionfromseventhoutof44banksinthemarket.Atthesametime,theBank’smarketshareintermsoftotalloanportfolioincreasedfrom3.0%to3.3%whiledroppingtoseventhpositionfromsixth.InagriculturallendingAccessBankremainedthemarketleaderwith30,000clientsand7%shareofthetotalagriculturalport-folioofAzerbaijan’sbankingsector.Apartfromthebanks,approximately27non-bankcreditorganiza-tionsareengagedinmicrofinance.TheAzerbaijanMicrofinanceAssociation(AMFA)collectsdatafor30institutionsinvolvedinmicrofinance(consistingof18ofthesenon-bankfinancialinstitutionsand12banks,includingAccessBank).ThemicroloanportfoliooftheseinstitutionsstoodatUSD646millionat2011-end,givingAccessBank28%marketshare(36%at2010-end),makingAccessBankbyfartheleadingmicrofinanceinstitutioninAzerbaijan,especiallywithsmallfarmerhouseholds.

Somechangesinpoliticalcircumstancescanbereported.Attheendof2011,anewprimeministerwaschosenaspartoftheroadmaptowardspoliticalstabilization.ThisroadmapalsoforeseesthereturnoftheformerPresidentMarcRavalomanana.AnattempttoreturnfromhisexileinSouthAfricawasre-centlystoppedinthelastminutebytheauthorities.InthisrespecttheSADC(SouthernArfricanDeve-lopmentCommunity)isnowdemandingtherevisionofamnestyrights.Ravalomanawassentencedtoprisonandforcedlabourinabsence.Signsofrisingdissatisfactionofthepopulationwiththepoliticalandeconomicsituationmanifestthemselvesindemonstrations,strikesofcourtsandstudents,andariseincriminality.

OfficialnumberssuggestanincreaseofMadagascar’sGDPby0.6%in2011.Theincreaseismainlydrivenbytheminingsectorwhilekeyindustriessuchastextileandagriculturestagnateordeteriorate.Theperceptionbythepopulationisthattheeconomycontractedin2011.Officialinflationin2011waspublishedat7%,whileactualinflationisestimatedcloserto10%.Theriskofafurtherriseininflationisdrivenbyenergyandfoodprices.Energypricesforindustrialclientswillrisein2012,whilethedis-cussiononthestate-subsidyoffuelpricescontinues.Therealpriceisestimated10%abovethepricelimitset,andtheenergysectorcomplainsofnon-ordelayedpaymentsofagreedsubsidies.

Despitethedifficultpoliticalandeconomicsituation,Madagascarisimprovingitsbusinessenvironment.The2012IndexofeconomicfreedomscoresMadagascarasthe75thfreestcountryinthe2012Indexemphasisingimprovementsinbusinessfreedomandthemanagementofgovernmentspending.Madagas-carisranked6thoutof46countriesintheSub-SaharanAfricaregion,anditsoverallscoreisabovetheworldaverage.2

46

Azerbaijan (con’t.)

Madagascar

AccessHolding|AnnualReport2011

2http://www.heritage.org/index/country/madagascar

Thebankingsector’stotalportfoliooutstandingincreasedbyonly3.3%(Jan-Nov2011)toMGA2.0trillion(EUR687million),whiledelinquenciesincreasedfrom12.7%to13.6%inthesameperiod.Theoveralldepositandliquiditypositionofthebankingsectorincreased,causingtreasuryshort-termsratestodecrease,whilelong-termratesremainstableorincreaseslightly.Totalassetsofthemicrofi-nancesectorhaveincreasedbyMGA52.9billion(EUR18.0million),anincreaseof28.8%throughouttheyeartostandatMGA236.2billion(EUR80.2million)attheendofSeptember2011.ThegrossloanportfolioincreasedtoMGA146.4billion(EUR48.7million)inSeptember,a31.3%increaseascompa-redto2010.Portfolioqualityhasslightlyrecoveredduetointenserecoverymeasures.3

Inthefourthquarterof2011,theBankofTanzania(BoT)projecteda6%GDPgrowthfor2011.InthemostrecentMonetaryPolicyStatement(June2011)oftheBoT,theforecastfor2012hasbeenraisedto7.2%.AnalystshoweverpredictthatmonetarypolicytighteningalongwithweakexternaldemandwillslowdowntherealgrowthoftheeconomywithaforecastedrealGDPgrowthdownto2-3%YoYbytheendof20124.

Inflationhasreachedunusuallyhighlevelsin2011,afterseveralyearsofrelativepricestability.Thecontinuousincreasesincethebeginningoftheyearendedupat19.8%inDecembermainlyduetosignificantincreasesinfoodpricesandenergy.AnalystsexpectTanzania‘sinflationratetostabilizeorincreaseslightlyfollowinganelectricitytariffincreaseinthefirstquarterof2012beforeitstartsgoingdown.

Followingtheinflationtrend,theTanzanianShilling(TZS)depreciatedagainsttheUSDollar(USD)andagainsttheEuro(EUR)untilmid-November.TheTZS/USDrate,whichwas1,643asattheendofSep-tember,exceeded1,850inOctoberbeforereturningtoalevelof1,550-1,600.TheTZS/EURrate,whichwas2,215asattheendofSeptember,camecloseto2,500inOctoberbeforereturningtopreviouslevels(around2,000-2,050)attheendoftheyear.

Thebankingsectorcontinuedtogrowduringtheyear2011.Thetotalnumberofbanksincreasedto45from42in2011,whilethenumberofbranchesincreasedto498from464.Threenewbanks,namelyAdvansBank(T)Ltd,EFCTanzaniaM.F.CLtdandFirstNationalBank(T)Ltd,startedoperations.EquityBank(T)Ltd,CovenantBankforwomenandAmanaBankLtdweregrantedprovisionalbankinglicenses.GeneralcompetitionespeciallywithintheSMEsectorisgettingstiffer,althoughonlyoneofthemarketentrants(Advans)hasabusinessmodelthatisbroadlycomparabletoAccessBank’s.

AccordingtotheTanzaniaBankingSurvey2011,AccessBankwaslisted12thintermsofmarketshare(1.9%).

TheaforementionedBoTinterventioninmid-OctobertostopthedepreciationoftheShillingandreduceliquidityinthemarketprovokedadramaticincreaseininter-bankovernightinterestratesfrom8%on30Septemberupto36%inthemiddleofDecember 5.Thefinaldaysoftheyearhaveseenaslightcoolingdownoftheinterbankmoneymarket,withratesfallingto33%,atrendwhichcontinuedinearly2012.Attheendoftheyear,devastatingfloodshitthepopulationofDaresSalaam.AccordingtoTMA(Tanza-niaMeteorologicalAgency),theseweretheheaviestrainsTanzaniahasexperiencedsinceindependencein1961.Hundredsofpeoplelivinginthecity‘svalleyshavebeenlefthomeless.ThishasalsoadverselyeffectedloandisbursementsandlendingarrearsinDecember(seeparagraphonbusinessdevelopmentbelow).

ThepoliticalsituationwithinTanzaniaremainsratherstable.Despitesomesignsofpublicdissatisfactionoverthedisputedoutcomeofthe2010elections,therehavebeennosignificantprotests(letalonegene-ralstrikes)thatwouldhaveunderminedthere-electedgovernment.

FreedomhouseratesTanzaniaaspartlyfreein2011whereasthedemocracyindexonlyplacesit90thoutof163countries,classifyingitasahybridregime.

Tanzania

47

3Allinformationoneconomicdevelopment,bankingandmicrofinancesectortakenfromCentralBank4EconomicinformationusedinthissectionistakenfromBankofTanzania(BoT)5Seedailymoneymarketratesatwww.bot-tz.org

AccessHolding Management Report 2011

Nigeriahaswitnessedatumultuousyear2011.Thepresidentialelectionfinallytookplaceon16April,2011havingbeenpostponedfrom9April.TheelectionfollowedacontroversyastowhetheraMuslimorChristiancandidateshouldbeallowedtobecomepresidentgiventhetraditioninNigeriatorotatethetopofficebetweenthetworeligions.GoodluckJonathan(aChristian)wasdeclarednewpresidenton19April.FollowingtheelectionwidespreadviolencetookplaceintheNorthern,Muslim-dominatedpartofthecountry.

Inthecourseoftheyear,Nigeriawasshakenbyterroristmotivatedviolence.AmongothersasuicidebombingattackonUNheadquartersinAbujakilled23people.RadicalIslamistgroupBokoHaramclaimedresponsibility.Followingthebombing,atleast63peoplearekilledinbombandgunattacksinthenorth-easterntownofDamaturu.Nearly70peoplearekilledindaysoffightingbetweensecurityforcesandBokoHarammilitantsinnorth-easternstatesofYobeandBorno.ViolencereacheditspeakonChristmasDaywhenabombattackkilledabout40people.PresidentJonathanhadtodeclarethestateofemergencytocontainviolencebyBokoHaram.

Nigeria’sNationalBureauofStatistics(NBS)6hasannouncedthatinflationhasdeclinedto10.3%y/yinDecember,from10.5%y/yinNovember-October.Thistranslatesintoanannualinflationrateof10.9%y/yin2011,havingdeclinedfrom13.8%y/yin2010.OnanaggregatebasistheeconomywhenmeasuredbytheRealGrossDomesticProduct(GDP),grewby7.68percentinthefourthquarterof2011asagainst8.60percentinthecorrespondingquarterof2010.Ontheexchangeratemarket,theNairaappreciatedagainsttheEuro,afterapeakattheendofOctoberof223NGN/EUR.Itclosedatarateof206.5NGN/EURattheendofDecember.TheexchangeratetowardstheUSDwasoscillatingaround157.5butdepreciatedinDecemberandwasquotedat159.7NGN/EURattheendofthemonth.Attheendofthefourthquarter2011theNIBORratesstoodataround17%andwerethereby30%higherthanattheendofthethirdquarter2011.ItwasthehighestNIBOR(NigeriaInterbankOfferedRate)ratesintheyears2010and2011.Asforthegeneralbusinessclimate,thingsarerelativelystable.WorldBankranksNigeria133thcountryoutof183foreaseofdoingbusiness,samerankasin2010.7