Int. Journal of Economics and Management 5(1): 179 – 215 (2011) ISSN 1823 - 836X

Are There Prospects for Future Economic Integration Among Muslim Countries? Evidence from Selected OIC Countries

RuzIta Mohd. aMINa*, zaRINah haMIdb aNd NoRMa Md. Saadc

a,b,cInternational Islamic University Malaysia, Malaysia

AbSTrACTSince mid-1980s, trade has been one of the main agenda among the organization of Islamic Conference (oIC) member countries as a means towards achieving higher economic development. January 1st, 2009 has been declared as the target date for the establishment of the trade Preferential System among the oIC countries, by which date intra-trade should be increased to 20%. Malaysia, which is considered to be one of the more successful economies among the oIC countries, is expected to play a pivotal role in enhancing intra-trade and ensuring that the targets are achieved. this paper investigates the degree of intra-trade activities among six oIC members, namely Egypt, Jordan, Malaysia, Saudi arabia, Syria and oman. It analyzes the trade structure of these oIC members utilizing “revealed comparative advantage” indices, “trade concentration”, and “trade competition” profiles. The findings show only small potentials for higher intra-OIC trade, generally in chemicals and materials, food and live animals, manufactured goods, and machinery and transport equipment. this indicates that much greater efforts need to be undertaken by oIC countries to prepare themselves for the establishment of an Islamic Common Market.

Keywords: economic integration, oIC countries, trade concentration, trade divergence, revealed comparative advantage

InTrOduCTIOnthe last decade has seen an increasing emphasis on economic integration among various groups of countries in the world. Integration has the potential to create a

* Corresponding author: E-mail: [email protected] remaining errors or omissions rest solely with the author(s) of this paper.

180

International Journal of Economics and Management

more competitive trade environment from the removal of trade barriers and is also an important impetus for stimulating investment in the member countries from both internal and foreign sources. the larger market as a result of trade integration reduces risk and uncertainty for producers while foreign investors become more inclined to invest in productive capacity in a member country as a way to avoid being excluded by trade restrictions and a high common external tariff (appleyard, 1995). the increased trade and investment through economic integration can, hence, spur economic development among participating countries.

the organization of Islamic Conferences (oIC), as with other groupings, would not be left behind in trying to benefit from economic integration. The OIC is an inter-governmental grouping of fifty-seven countries. Established in Rabat, Kingdom of Morocco, on 25 September 1969, it has the objective of strengthening the solidarity and cooperation among Muslim countries in the political, economic, cultural, scientific and social fields.

Various measures have been undertaken to enhance economic cooperation and, later, integration among members. In May 1976, the idea to establish the Islamic Chamber of Commerce and Industry (ICCI) was proposed in the Seventh Islamic Conference of foreign ministers held in Istanbul, turkey. the idea was subsequently accepted and the constitution of the ICCI adopted by the First and Second Conference of the Chambers of Commerce and Industry in october 1977 and in december 1978, respectively. the ICCI serves as an allied organ of the oIC and represents the private sector of member countries.1 It aims at intensifying greater collaboration in the field of trade, commerce, information technology, insurance/reinsurance, shipping, banking, promotion of investment opportunities and joint ventures in the member countries.

In the late 1990s, the oIC member countries signed an agreement on a trade Preferential System (tPS) and declared the target date for its establishment to be 1 January 2009. the tPS aims at further promoting trade among oIC member states through the exchange of trade preferences to ensure equal and non-discriminatory treatment among participating countries. In the tPS agreement, the exchange preferences are not only limited to tariffs, but will be progressively extended to para-tariff and non-tariff concessions. the tPS agreement also extends trade preferences to all commodities including agricultural and animal products, manufactured or semi-manufactured products.

to date, eleven Islamic Summit conferences and thirty-seven Islamic Conferences of Foreign Ministers (ICFM) have been held. the 10th Islamic Summit Conference held in Putrajaya, Malaysia on 11-18 october 2003, elected Malaysia as the Chairman of the organization until 2008. The Summit reaffirms the desire to intensify trade and economic cooperation and to increase the share of global

1 Its membership consists of the national chambers, unions, federations of chambers of commerce and industry of the member countries.

181

are there Prospects for Future Economic Integration among Muslim Countries?

trade between member countries as well as with other nations. on 17 october 2003, the oIC countries adopted a resolution on the establishment of an Islamic common market.

the declaration of the establishment of the tPS represents a very important step towards increasing the intra-oIC trade to 20% by the target date. In addition, the resolution to establish an Islamic Common market presents a clear indication of the intention to move towards a higher degree of economic integration among member countries. Malaysia, being once the chairman of the oIC and being one of the member countries which is very open to international trade with more than 200% trade to GdP ratio, is expected to play a pivotal role in enhancing trade activities among the oIC countries and ensuring that the targets are achieved.

In view of the above development it is, hence, very pertinent to investigate if the oIC possesses the necessary prerequisites to enable a successful economic integration among its member countries that have different economic and trade characteristics. one of the important questions is whether the oIC countries’ export structures are diverse enough to support higher intra-oIC trade activities. the ability to increase regional exports has been said to depend upon the degree to which countries’ dynamic exports are incorporated in the regional export mix. this means that the extent to which the relative share of intra-oIC trade can be increased depends on the extent to which countries’ dynamic exports are represented in intra-oIC trade. apart from that, the likely success or failure of any regional economic integration is highly dependent on the range of products that members have the capacity to export or import. Members exporting a wide range of diversified goods are considered a positive factor, while concentration of exports is considered a limiting factor to the prospects of increasing regional trade (Pitigala, 2005). Such an argument is based on the product substitution theory where substitutability of products of member countries for those of non-member countries has the effect of increasing the chance of trade creation, representing a positive welfare effect of economic integration (Park, Park & Estrada, 2008).2 Exports of member countries that are highly diversified increase the chances of substitutability of products, hence improving the prospects of a successful regional integration.

this paper investigates the degree of intra-trade activities among six oIC members, namely Egypt, Jordan, Malaysia, Saudi arabia, Syria and oman. Specifically, it examines the extent to which countries’ dynamic exports are represented in intra-OIC trade as well as the extent of trade concentration/ trade diversification by analyzing the “trade divergence”, and “trade concentration” profiles between the years 1990 and 2005. In addition, it checks for trade complementarities and the prospects for higher intra-trade among the selected

2 trade creation arises when higher cost domestic products are replaced with lower cost imports from member countries. The change from an expensive to a cheaper source of supply is beneficial because it is a move toward freer trade.

182

International Journal of Economics and Management

countries and identifies the range of products that members have the capacity to export or import by using the “revealed comparative advantage” indices for the same years. The findings provide an indication as to whether the existing trade structure and trade potentials would facilitate intra-trade among oIC members in their effort towards economic integration. Such information will be useful for member countries to formulate strategies that would foster closer trade relations among themselves.

this paper is organized as follows. the next section provides a survey of literature on regional integration and the use of statistical indices in analyzing intra-trade activities, trade concentration and trade divergence. Section 3 describes the methodology and data used in this study. Section 4 presents the analysis and discussion of the findings while the last section concludes.

LITErATurE rEvIEwthe “natural trading partners” hypothesis introduced by Lipsey (1960) presents one of the early works that deal with the idea of regional integration. the hypothesis suggests that the higher the proportion of intra-trade within the region, the more likely a regional agreement would result in an increase in welfare effects. the natural trading partner hypothesis was later modified by other studies, such as those by Wonnacott and Lutz (1989) and deardoff and Stern (1994) who added location and transportation costs into the analysis in an effort to identify other factors determining regional trade. the “natural trading partners” hypothesis was later popularized as “natural trading blocs” by Krugman (1991) who put emphasis on geographical proximity. these studies found that geographical proximity between countries provides a positive contributing factor to intra-trade activities.

other studies such as Michaely (1996) and Pitigala (2005) have proposed that natural trading partners be defined based on trade complementarity, where the natural trading partner hypothesis is likely to hold if a country imports what its trading partner exports. Michaely (1996), for instance, used the complementarity index and argued that the higher the observed values of the index between partners, the more likely it is that a regional trade agreement will succeed. along similar argument, Pitigala (2005) utilized revealed comparative indices to assess the complementarity of intra-regional trade as a pre-requisite for the potential success of the regional arrangement among the South asian association for Regional Cooperation (SaaRC) countries. he argues that the likely success or failure of any regional economic integration is highly dependent on the range of products that members have the capacity to export or import. Members exporting a wide range of diversified goods are considered a positive factor, while concentration of exports is considered a limiting factor to the prospects of increasing regional trade (Pitigala, 2005).

183

are there Prospects for Future Economic Integration among Muslim Countries?

Trade concentration and diversification of exports have been shown to have impacts on regional trade arrangements. Massell (1964), who performed a cross section analysis of 36 countries and Soutar (1977) who adopted a cross section analysis of 48 less developed countries between 1957 and 1969, found a clear relationship between instability of export earnings and concentration of exports. Massel (1964) further elaborated that trade diversification would be more likely to provide the economy with greater flexibility and stability in export earnings. In a related work, Yeats (1998) reported that studies have shown that countries with highly concentrated exports may experience a relatively high degree of export earning instability that could reduce a country’s ability to maintain the financial commitment required by regional arrangements.

there are many studies that analyzed the relationship between regional trade arrangements and intra-trade, to name a few (Grubel and Llyod: 1975, Greenaway: 1986, 1989, Globerman: 1992, Kim and Lee: 2003 and Chen et al.: 2007). these studies found some evidence that regional trade arrangements stimulate intra-trade among its member countries and vice-versa. Grubel and Llyod (1975) and Greenaway (1986, 1989) for instance, suggest that regional trade arrangements among developed countries stimulate trade by creating a more competitive trade environment as a result of the removal of trade barriers and the possibility of realizing economies of scale. Kim and Lee (2003) highlighted that regional trade arrangements among developing countries such as Mercosur have effects on trade because member countries have significant industrial base in sectors characterized by economies of scale and the existence of preferential treatment in the form of lower tariffs.

The Gini coefficient and the modified version called the Gini-Hirschman coefficient of concentration are commonly used methods for measuring commodity concentration. however, Low, olarreaga and Suarez (1998) used three different concentration indices namely Herfindal-Hirschman concentration index, Theil-entropy coefficient and Mean Logarithm deviation to investigate if globalization has affected the concentration indices. Kali, Mendez and Reyes (2007) highlighted the fact that empirical measures of trade characteristics or trade structures are limited. they used trade dispersion among trading partners as one of the measures of trade structure. as in Low, olarreaga and Suarez (1998), Kali, Mendez and Reyes (2007) constructed a Herfindahl-Hirschman concentration index of trade for all countries to measure trade dispersion among all trading partners. a low value of the index indicates low concentration or high dispersion, and vice versa. the study found trade concentration to be positively correlated with growth for all countries, but the effect is found to be more pronounced for poor countries.

this paper attempts to look at the potential success of economic integration among selected oIC countries by analyzing trade concentration, trade divergence and revealed comparative advantage indices as in Pitigala (2005). In line with

184

International Journal of Economics and Management

Low, olarreaga and Suarez (1998), Pitigala (2005), and Kali, Mendez and Reyes (2007), this study will focus on the export component of trade, except in the case of revealed comparative advantage where both exports and imports are utilized. the advantage of using these measurements is that they allow for a more in-depth analysis at the product level as well as country-level examination which could be used to gauge the prospects for the success of economic integration. Since there has been no such effort to investigate the success of regional trade among the oIC member countries at the disaggregated level, the findings of this paper would serve to provide useful information for the formulation of strategies that would enhance regional economic integration among the members of the grouping. the details of the measurements are described in the next section.

dATA dESCrIPTIOn And METhOdOLOgyThe statistical analysis uses trade data of Malaysia and five other members of the oIC namely Egypt, Jordan, oman, Saudi arabia and Syria for the years 1990 and 2005. the two years are chosen to examine whether the oIC grouping possesses the characteristics that are conducive for the establishment of an Islamic Common Market. Values of the countries’ intra-oIC trade and their trade to the rest of the world (RoW) based on the SItC Revision 2 at 4-digit level were extracted from the uNCoMtRadE data source provided by the World Integrated trade Solution (WItS) database. the SItC 4-digit level is selected since it is the highest level of disaggregation for which comparisons can be carried out. this is due to the fact that consistent reporting of data is unattainable at further disaggregated levels, such as the SItC 6- to 8-digit levels (Pitigala, 2005).

The study confines itself to Malaysia, who is expected to play a pivotal role in enhancing trade activities among the oIC countries being one of the member countries with the most open economy as mentioned earlier, and five other selected OIC countries as listed earlier. The five countries are chosen for the reason that they are mainly located in the Middle-eastern and african region (where most members of the oIC are located geographically) and their economic, trade and preference structures are quite different from those of Malaysia’s. hence, any sign of potentially higher intra-trade activities, particularly among these diverse countries, would provide an indication of the prospects of economic integration among oIC countries as a whole.

In order to compute the share of intra-oIC exports and share of total exports, the disaggregated individual product at 4-digit level is divided by intra-oIC total exports of the individual countries and total exports of individual countries to the rest of the world, respectively. these values are used to calculate the share in the growth of total exports to the oIC and to the rest of the world, between 1990 and

185

are there Prospects for Future Economic Integration among Muslim Countries?

2005. the share in the growth of total exports of each commodity i for country j (Si,j) between 1990 and 2005 can be computed as:

S

X

X X

XX X

,

,

, ,

,

, ,

i j

i j

i

n

i j i j

i

n

i

n

i j

i

n

i j i j

1990

1

2005 1990

11

1990

1

2005 1990

=

-

-

=

=-

-

J

L

KKKK

fN

P

OOOO

p

/

//

/ (1)

which can be simplified to:

SX X

X X,

, ,

, ,

i j

i j i j

i

n

i

n

i j i j

2005 1990

11

2005 1990

=-

-

==

c

^m

h//

(2)

where X ,i j1990 and X ,i j

2005 are export of commodity i of country j for 1990 and 2005,

respectively; X ,i j

i

n1990

1=

/ and X ,i j

i

n2005

1=

/ are total exports of country j for 1990 and 2005,

respectively. the share in equation (1) is derived based on the commutative property of

subtraction where,

X

X X

X

X X

,

, ,

,

, ,

i j

i

n

i j

i

n

i j

i

n

i j

i

n

i j i j

i

n

1990

1

2005

1

1990

1

1990

1

2005 1990

1

-

=

-

=

= =

=

=

c ^m h

/

/ /

/

/

X

X X

X

X X

X

X X

,

, ,

,

, ,

,

, ,

i j

i

n

i j i j

i j

i

n

j j

i j

i

n

n j n j

1990

1

2005 1990

1990

1

22005

21990

1990

1

2005 1990

f f

=-

+-

+ +-

= =

=

^ ^

^

h h

h

/ /

/

(3)

186

International Journal of Economics and Management

dividing equation (3) by the growth of total exports, X

X X

,

, ,

i j

i

n

i j

i

n

i j

i

n

1990

1

2005

1

1990

1

-

=

= =

c m

/

/ / the

equation becomes,

1

X

X X

XX X

X

X X

XX X

X

X X

XX X

,

, ,

,

, ,

,

, ,

,

, ,

,

, ,

,

, ,

i j

i

n

i j

i

n

i j

i

n

i j

i

n

i j i j

i j

i

n

i j

i

n

i j

i

n

i j

i

n

j j

i j

i

n

i j

i

n

i j

i

n

i j

i

n

n j n j

1990

1

2005

1

1990

1

1990

1

2005 1990

1990

1

2005

1

1990

1

1990

1

22005

21990

1990

1

2005

1

1990

1

1990

1

2005 1990

f

=

-

-

+

-

-

+ +

-

-

=

= =

=

=

= =

=

=

= =

=

J

L

KKKK

J

L

KKKK

J

L

KKKK

f f

f

N

P

OOOO

N

P

OOOO

N

P

OOOO

p p

p

/

/ /

/

/

/ /

/

/

/ /

/

(4)

thus,

S S S1 , , ,i j j n j2 f= + + + , or S1 ,i j

i

n

1

==

/ (5)

Collectively, the shares of growth computed are used to identify the dynamic exports of the individual countries, where dynamic exports are defined as products which accounted for a significant amount of total export growth to the region and to the rest of the world between 1990 and 2005. Pitigala (2005) classifies products that account for 75% of total export growth (which exclude marginal products that might not be reported on regular basis) as dynamic exports. For comparison purposes, apart from using the 75% cut-off point as in Pitigala (2005), this study also employs a cut-off point of 95% to identify dynamic exports.

The divergence and concentration of exports are based on the profile of dynamic exports at both the 75% and 95% cut-off points. divergence of exports can be interpreted as the extent to which a country’s dynamic exports to the rest of the world are represented in its regional dynamic exports. Conversely, the divergence of exports can also be defined as the extent of the departure (i.e., differences) of dynamic exports to the region from dynamic exports to the rest of the world. hence, smaller differences (larger similarities) in the dynamic export composition provide an indication for the possibility of higher intra-trade among the selected oIC member countries.

187

are there Prospects for Future Economic Integration among Muslim Countries?

Based on Pitigala (2005), the divergence of exports of country j (Dj) is calculated as:

DC

C

,

,

j

i ROWj

i

k

i OICj

i

k

1

1=

=

=

/

/,

where i = 1, ..., k; k is the number of common dynamic exports to the oIC and RoW, while C ,i OIC

j and C ,i ROWj are common dynamic exports to the oIC and RoW,

respectively. a high value of D j indicates a more similar (or less different) dynamic export composition of a country to the region and to the rest of the world, hence the better the prospects of increasing regional trade. Meanwhile, the concentration of exports at the 75% (or 95%) cut-off point is measured by the number of products accounting for 75% (or 95%) of export growth to the rest of the world between the years 1990 and 2005.

Revealed comparative advantage measures a country’s trade specialization in a commodity group and is defined as a country’s sectoral share divided by the world sectoral share. hence, the IRCAij measures the index of revealed comparative advantage of country i in commodity j as follows:

IRCA X XX X

ijwj w

ij i=

where Xij represents country i’s export of commodity j, Xwj represents world exports of commodity j, Xi represents the total exports of country i, and Xw represents total world exports. the index value ranges between zero and infinity with values greater than unity indicating specialization in that commodity group, while a value between zero and unity indicates no specialization in that commodity group. the top 50 imports of each country are listed and compared to the IRCa of the respective trading partners in order to check for trade complementarities and the prospects for higher intra-trade among the selected countries.

AnALySIS And dISCuSSIOn OF FIndIngS

Overall Trade Patterns of Selected OIC CountriesIn order to evaluate whether the oIC members possess certain fundamental conditions to become a successful grouping, this section first provides a general description of the trade structure of the oIC countries. an analysis of product-level trade data in table 1 suggests that food & live animals, chemicals & materials, and manufactured goods have dominated intra-regional trade in oIC for the past decade. For example, in 2005, the percentage of regional exports that originated in food & live animals was close to 55% for Syria, 36% for oman, 26% for Egypt, and 20%

188

International Journal of Economics and Management

Tabl

e 1

Prod

uct c

ompo

sitio

n of

sele

cted

oIC

cou

ntrie

s’ in

tra-r

egio

nal a

nd e

xtra

-reg

iona

l exp

orts

Food

& li

ve

anim

als

bev

erag

es

& to

bacc

oC

rude

m

ater

ials

Min

eral

s &

fuel

s

Ani

mal

&

vege

tabl

e fa

t

Che

mic

als

& m

ater

ials

Man

ufac

ture

d go

ods

Mac

hine

ry

& tr

ansp

ort

equi

pmen

t

Mis

cella

neou

s m

anuf

actu

res

Oth

er

com

mod

ities

OIC

rO

wO

ICr

Ow

OIC

rO

wO

ICr

Ow

OIC

rO

wO

ICr

Ow

OIC

rO

wO

ICr

Ow

OIC

rO

wO

ICr

Ow

Egyp

t19

9046

.51

7.48

0.14

0.14

2.71

10.3

71.

3230

.35

0.01

0.03

9.95

4.54

22.5

437

.01

2.82

0.58

13.1

99.

500.

820.

0020

0525

.85

12.4

50.

020.

083.

447.

4313

.68

39.3

70.

210.

367.

668.

4542

.78

24.6

23.

321.

782.

735.

150.

310.

29

Jord

an19

9025

.81

7.49

0.57

0.75

10.5

042

.33

0.00

0.00

0.17

0.10

42.3

929

.24

12.6

012

.99

2.05

2.37

5.91

4.74

0.00

0.00

2005

20.2

59.

320.

202.

136.

8614

.81

0.04

0.01

0.61

3.16

37.0

520

.08

15.9

05.

4314

.79

3.48

4.31

41.5

60.

000.

02

Mal

aysi

a19

9015

.53

4.24

0.35

0.12

7.62

14.6

60.

0017

.44

35.1

06.

840.

871.

677.

658.

2529

.66

36.4

63.

0210

.28

0.19

0.04

2005

5.55

2.07

0.05

0.34

2.24

2.82

0.02

11.0

432

.71

4.55

3.03

5.61

28.8

27.

4720

.81

57.0

26.

778.

780.

000.

31

om

an19

9023

.32

1.23

2.28

0.08

0.70

0.20

0.00

92.4

80.

430.

048.

250.

2458

.61

1.05

1.68

3.57

4.72

0.83

0.00

0.27

2005

36.0

01.

411.

560.

090.

970.

280.

0093

.59

11.3

20.

2813

.52

1.35

24.4

41.

822.

180.

618.

260.

511.

750.

07

Saud

i a

rabi

a19

903.

840.

590.

170.

091.

621.

0538

.42

90.7

30.

740.

0130

.72

4.50

13.0

30.

759.

141.

211.

580.

720.

740.

3520

052.

850.

230.

640.

050.

760.

4467

.37

88.8

00.

160.

0117

.87

8.85

7.54

0.81

1.65

0.61

1.16

0.19

0.01

0.00

Syria

1990

67.2

28.

250.

750.

523.

895.

688.

4548

.45

0.00

0.00

0.90

13.8

87.

5914

.52

0.50

0.13

10.6

58.

560.

050.

0020

0554

.58

6.09

1.95

1.02

2.92

5.26

0.00

73.8

60.

741.

965.

533.

0720

.35

4.76

2.87

1.06

11.0

62.

910.

010.

01

Not

e: F

igur

es re

pres

ent t

he p

erce

ntag

e ex

port

shar

e of

eac

h pr

oduc

t cat

egor

y ou

t of i

ntra

-reg

iona

l tra

de (w

ith se

lect

ed o

IC c

ount

ries)

and

ext

ra-r

egio

nal t

rade

(with

Ro

W),

resp

ectiv

ely.

189

are there Prospects for Future Economic Integration among Muslim Countries?

for Jordan. Except for oman, the percentage has, however, shown a declining trend in the intra-regional trade share of this category for all these countries from 1990.

of all the six countries, Egypt and oman are major exporters of manufactured goods within the oIC grouping with a share of 22.54% and 58.61%, respectively, in 1990. however, this sector showed a substantial decline to only 24.44% share in regional exports in 2005 for oman, but Egypt managed to increase its share substantially to about 43% in the same year. Malaysia emerged as one of the important supplier of manufactured goods within the grouping with a considerable export share of 28.82% in 2005 from only 7.65% in 1990. Malaysia also is found to be a major supplier of animal & vegetable fat and machinery & transport equipment to the oIC countries, with the share of 32.71% and 20.81%, respectively, in 2005.

Chemicals & minerals are found to be important for Jordan and Saudi arabia, accounting for 42.39% and 30.72% of intra-regional trade in 1990, and 37.05% and 17.87% in 2005, respectively. For Saudi arabia, the importance of chemicals & materials is closely associated with the production and exports of minerals & fuels, which are found to have dominated intra-regional trade of the country with an export share of 67.37% in 2005.

Minerals & fuels have also been found to be the dominating sector in oIC exports share to the rest of the world for three countries with oman, Saudi and Syria showing significant shares. Oman’s share of exports of minerals & fuels to the rest of the world accounted for 92.48% and 93.59% in 1990 and 2005, respectively; Saudi arabia’s share accounted for 90.73% and 88.80%, while Syria’s share are 48.45% and 73.86% in the same years, respectively.

other sectors that, to a certain extent, are also important exports to the rest of the world include minerals & fuels and manufactured goods for Egypt, crude materials and chemicals & materials for Jordan, and machinery & transport equipment for Malaysia. In summary, the region has established a mutual dependency in basic foods & agricultural products. In general, there appears to be a significant divergence3 between products that are exported to the region and to the rest of the world. Primary products seem to dominate intra-regional trade while minerals & fuels dominate exports to the rest of the world.

Trade divergence and Trade Concentrationthe likely success or failure of any proposed regional trade arrangement depends on the range of products that members have the capacity to export or import. Members exporting a wide range of diversified goods present a positive signal to a successful regional trade arrangement. however, concentration of exports will limit the prospects of increasing regional trade (Pitigala, 2005).

3 As mentioned in the earlier section, divergence is defined as the departure of intra-regional exports from exports to the rest of the world in major product categories (Pitigala, 2005).

190

International Journal of Economics and Management

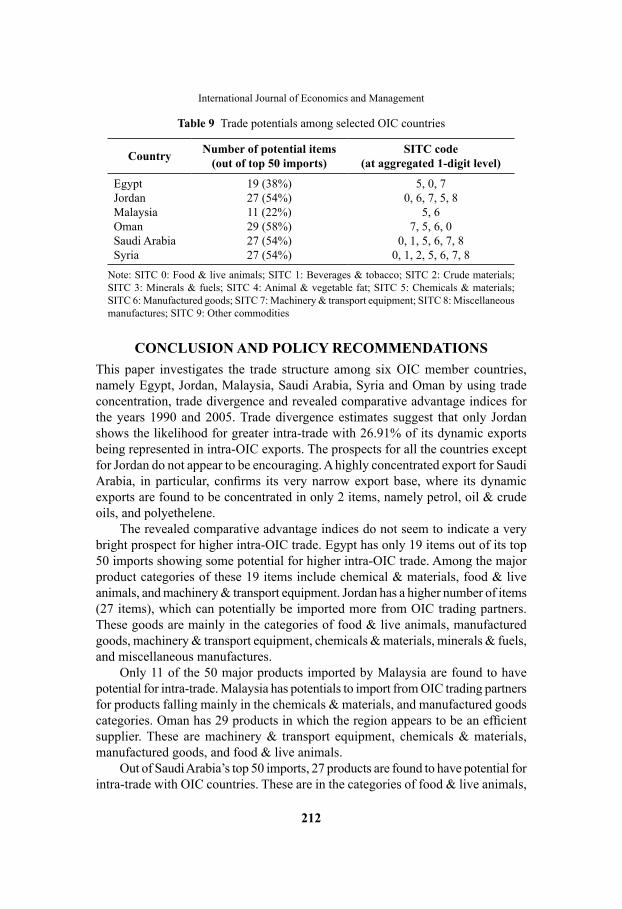

table 2 presents a summary of the divergence and concentration estimates to examine the two propositions above.4 Based on the 75% cut-off point, the figures suggest that only Jordan shows the likelihood for greater intra-trade with 26.91% of its dynamic exports being represented in intra-oIC exports. the disparity is extreme for the other countries, particularly oman, Saudi arabia and Syria, where none of their products that accounted for 75% of the countries’ growth in exports to the rest of the world is represented in the growth of its regional exports. Since the extent to which the relative share of intra-oIC trade can be increased depends on the extent to which countries’ dynamic exports to the rest of the world are represented in the oIC trade, the prospects for all the countries except for Jordan do not appear to be encouraging. a highly concentrated export for these countries, especially Saudi Arabia, also confirms their narrow export base. Saudi Arabia’s dynamic exports are found to be concentrated in only 2 items, namely petrol, oil & crude oils (SItC 3330) and polyethelene (SItC 5831).

Table 2 divergence and concentration summary

Egypt Jordan Malaysia Oman Saudi Arabia Syria

95% cut-off pointdivergence of exports (%) 12.69

(9)26.05(50)

6.13(13)

0 (0)

2.25(2)

0(0)

Concentration of exports 42 50 23 22 35 42

75% cut-off pointdivergence of exports (%) 12.25

(4)26.91(17)

2.60(7)

0(0)

0(0)

0(0)

Concentration of exports 13 17 8 11 2 19

Notes: Figures in parentheses represent the number of product categories in intra-oIC exports that match exports to the RoW that were among its dynamic exports (account for 75% or 95% of total export growth between 1990 and 2005).divergence of exports = intra-oIC exports that match exports to the RoW as a share of the latter.Concentration of exports = Number of products accounting for either 75% or 95% of export growth to the RoW between 1990 and 2005.

Based on the 95% cut-off point for dynamic exports, the number of items of regional exports that match exports to the rest of the world is higher for Jordan, Malaysia and Egypt (50, 13, and 9, respectively). the measurements for export divergence are also higher for Jordan, Egypt and Malaysia. For Jordan and Egypt, the percentage share is not much different from the figures at the 75% cut-off point. In the case of Oman and Syria, the divergence of export figures remain at 0% at the 75% cut-off point which means that there is no match at all between dynamic exports to the region and to the rest of the world. at the 95% cut-off point, table 2 shows a relatively lower degree of trade concentration for all the selected oIC countries compared to the 75% cut-off point.

4 The tables from which the figures are derived are available from the authors upon request.

191

are there Prospects for Future Economic Integration among Muslim Countries?

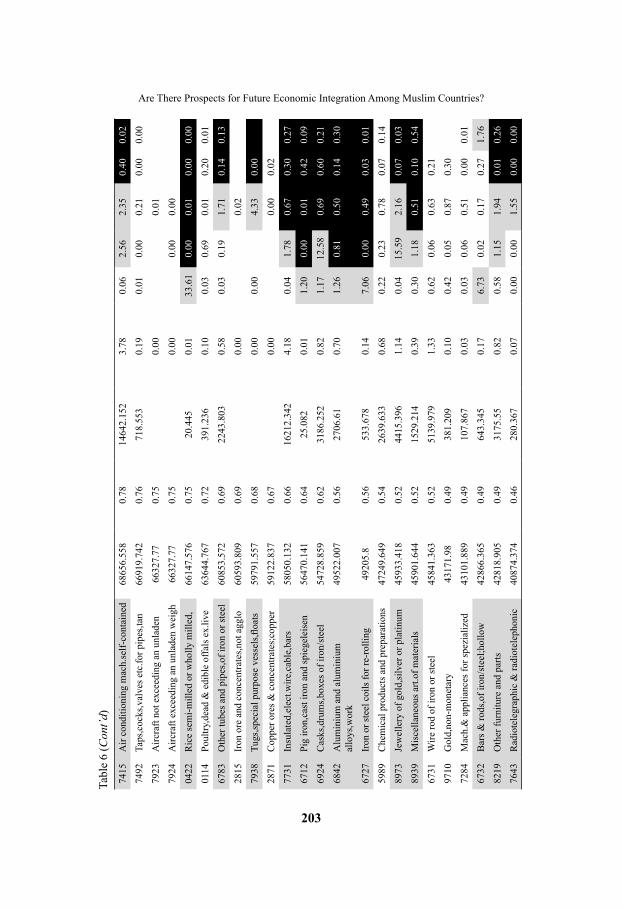

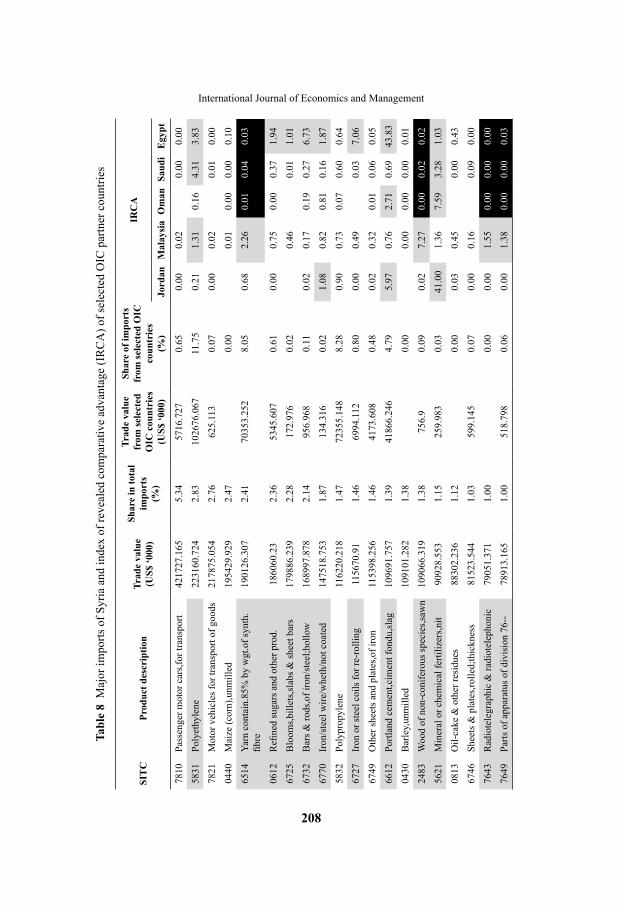

revealed Comparative Advantage and Trade Complementarities

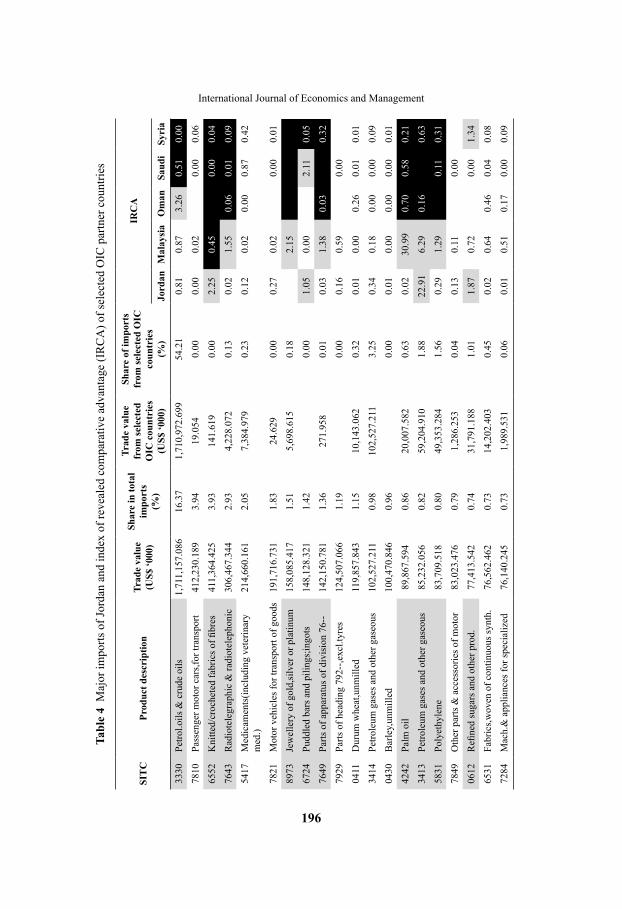

Egypttable 3 shows that Egypt’s top 50 imports comprise mainly of food & live animals (SItC 0) accounting for about 13% share of total imports, machinery & transport equipment (SItC 7) accounting for about 10% share of imports, and minerals & fuels (SItC 3) accounting for 8.8% share of imports. others include chemicals & materials (SItC 5) with 6.3% import share, and manufactured goods (SItC 6) with 7.2% import share.

out of Egypt’s top 50 imports, only 19 items show some potential for higher intra-oIC trade based on the IRCa values of its trading partners in the grouping. In terms of the number of items, among the major product categories include 5 items from chemical & materials (SItC 5), four items from food & live animals (SItC 0), and 4 items from machinery & transport equipment (SItC 7). Malaysia seems to demonstrate the highest number of products (11 products) in which it has trade complementarities with Egypt. this is followed by oman with 7 products, Saudi arabia with 5 products, and Syria and Jordan, each with 3 products. all the oIC trading partners except for Syria have IRCa>1 in minerals or chemical fertilizers (SItC 5621), but the share of imports of this product from oIC trading partners in 2005 is very small, i.e., only 0.77%. Petroleum gases (SItC 3413) and petrol, oils & crude oils (SItC 3330) each show 3 countries having comparative advantage in exporting these products to Egypt. Similarly, the shares of imports of these goods from the selected oIC trading partners are, again, very small with 3.64% and almost 0%, respectively. this shows potentials for Egypt to increase its imports of these products from oIC trading partners.

Palm oil (SItC 4242) shows the highest import share from oIC countries of 14.86% with oman and Malaysia, in particular, having a high comparative advantage in exporting this product to Egypt. this does not come as a surprise since Malaysia is a major world exporter of palm oil, hence having a natural niche on the export of this product. Polyethelene (SItC 5831) represents the second highest import share of Egypt from oIC countries with 4.99%, followed by petroleum gases (SItC 3413) and yarn (SItC 6514) representing 3.64% and 2.41% of intra-oIC imports, respectively.

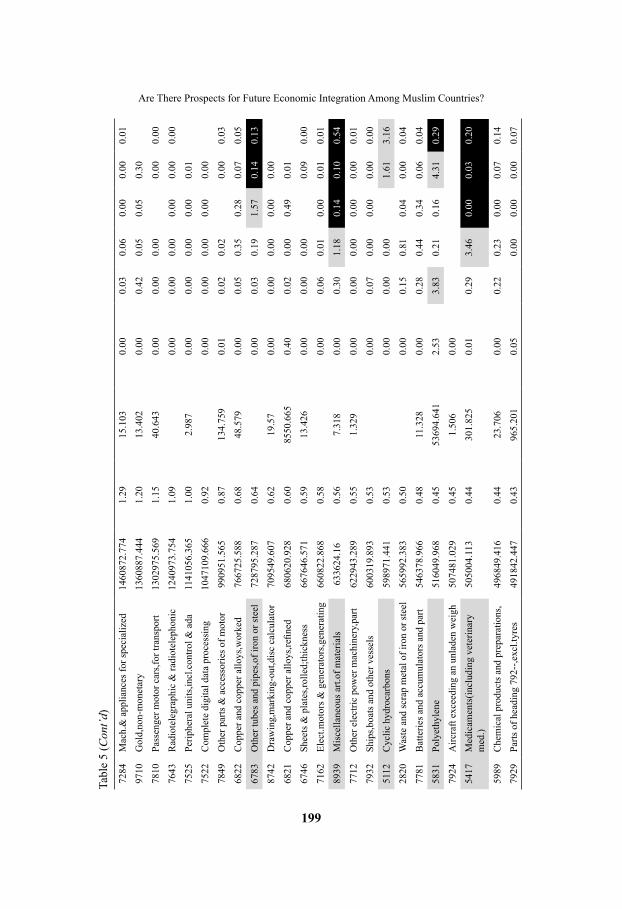

JordanJordan’s top 50 imports are mainly dominated by minerals & fuels (SItC 3), machinery & transport equipment (SItC 7), and manufactured goods (SItC 6) accounting for 18.79%, 14.82% and 9.18%, respectively (see table 4). Petrol, oils & crude oils (SItC 3330) represents the highest import share for Jordan at 16.37%. as with Egypt, the majority of products (38 out of the 50 products) in the list individually represent a very small share of Jordan’s total imports (less than

192

International Journal of Economics and ManagementTa

ble

3 M

ajor

impo

rts o

f Egy

pt a

nd in

dex

of re

veal

ed c

ompa

rativ

e ad

vant

age

(IR

Ca

) of s

elec

ted

oIC

par

tner

cou

ntrie

s

SIT

CPr

oduc

t des

crip

tion

Trad

e va

lue

(uS$

‘000

)

Shar

e in

to

tal i

mpo

rts

(%)

Trad

e va

lue

fr

om se

lect

ed

OIC

cou

ntri

es

(uS$

‘000

)

Shar

e of

impo

rts

from

sele

cted

OIC

co

untr

ies

(%)

IrC

A

Jord

anM

alay

sia

Om

anSa

udi

Syri

a

0411

dur

um w

heat

,unm

illed

9158

39.2

714.

6230

508.

112.

000.

000.

260.

0035

.50

3413

Petro

leum

gas

es a

nd o

ther

gas

eous

80

6903

.271

4.07

5554

5.95

73.

646.

4330

.55

4.78

0.09

3330

Petro

l.oils

& c

rude

oils

79

7563

.925

4.03

0.00

0.93

11.5

512

.73

9.89

6725

Blo

oms,b

illet

s,sla

bs &

shee

t bar

s 77

4417

.048

3.91

145.

128

0.01

0.46

0.01

0440

Mai

ze (c

orn)

,unm

illed

6964

63.7

733.

510.

000.

010.

000.

000.

00

2482

Woo

d of

con

ifero

us sp

ecie

s,saw

n43

5866

.775

2.20

0.20

50.

000.

010.

030.

000.

000.

02

7810

Pass

enge

r mot

or c

ars,f

or tr

ansp

ort

3040

60.1

541.

5355

05.7

770.

360.

000.

020.

000.

00

7849

oth

er p

arts

& a

cces

sorie

s of m

otor

29

3261

.494

1.48

1526

.969

0.10

0.02

0.11

0.00

0.03

0111

Mea

t of b

ovin

e an

imal

s, fr

esh,

chi

lled

2770

85.8

751.

400.

000.

250.

010.

010.

01

5417

Med

icam

ents

(inc

ludi

ng v

eter

inar

y m

ed.)

2688

58.1

981.

3651

34.0

010.

343.

460.

020.

000.

030.

20

4242

Palm

oil

2674

30.0

021.

3522

6918

.763

14.8

60.

1531

.05

1.18

0.00

7649

Parts

of a

ppar

atus

of d

ivis

ion

76--

2336

81.7

61.

1871

5.06

60.

050.

001.

380.

000.

000.

00

7643

Rad

iote

legr

aphi

c &

radi

otel

epho

nic

2300

56.4

061.

1657

.283

0.00

0.00

1.55

0.00

0.00

0.00

2222

Soya

bea

ns19

3980

.953

0.98

0.00

0.02

0.00

0.06

5621

Min

eral

or c

hem

ical

ferti

lizer

s19

2696

.383

0.97

1173

2.02

10.

7741

.00

1.36

7.59

3.28

0.04

2820

Was

te a

nd sc

rap

met

al o

f iro

n

or st

eel

1876

66.7

930.

9530

9.61

30.

020.

810.

030.

040.

000.

04

7284

Mac

h.&

app

lianc

es fo

r spe

cial

ized

18

6422

.487

0.94

927.

902

0.06

0.06

0.51

0.00

0.00

0.01

2873

alu

min

ium

ore

s and

con

cent

rate

s 18

5890

.823

0.94

3391

.855

0.22

0.01

0.00

0.00

193

are there Prospects for Future Economic Integration among Muslim Countries?

6514

Yarn

con

tain

.85%

by

wgt

.of s

ynth

.fib

re17

8751

.022

0.90

3684

8.68

32.

410.

682.

260.

010.

040.

38

5831

Poly

ethy

lene

1737

41.7

390.

8876

196.

145

4.99

0.21

1.31

0.16

4.31

0.29

0542

Bea

ns,p

eas,l

entil

s & o

ther

legu

min

o16

6041

.413

0.84

1221

4.80

50.

800.

000.

070.

000.

0122

.68

1211

toba

cco,

not s

tripp

ed15

4848

.672

0.78

30.9

620.

000.

110.

010.

180.

000.

02

7599

Parts

of a

nd a

cces

sorie

s 15

1115

.281

0.76

1258

.312

0.08

0.00

3.64

0.00

0.00

0813

oil-

cake

& o

ther

resi

dues

15

0333

.949

0.76

0.00

0.03

0.45

0.00

0.89

7499

oth

er n

on-e

lect

ric p

arts

& a

cces

sorie

s14

7648

.762

0.75

148.

543

0.01

0.10

0.49

0.00

0.01

0.07

6821

Cop

per a

nd c

oppe

r allo

ys,re

fined

13

6174

.307

0.69

4192

.441

0.27

0.00

0.01

0.49

0.01

3222

Oth

er c

oal,w

heth

er/n

ot p

ulve

rized

1327

44.0

080.

670.

000.

000.

010.

000.

15

7721

Elec

t.app

.such

as s

witc

hes,r

elay

s13

0192

.018

0.66

945.

214

0.06

0.07

2.98

0.02

0.01

0.00

7281

Mac

h.to

ols f

or sp

ecia

lized

par

ticul

1240

43.0

130.

6311

.097

0.00

0.11

0.36

0.00

0.00

0.30

5989

Che

mic

al p

rodu

cts a

nd p

repa

ratio

ns12

2346

.626

0.62

5088

.771

0.33

0.23

0.78

0.00

0.07

0.14

5111

acy

clic

hyd

roca

rbon

s10

6006

.10.

5361

91.7

080.

410.

000.

781.

70

2483

Woo

d of

non

-con

ifero

us sp

ecie

s,saw

n10

5749

.306

0.53

1789

.557

0.12

0.02

7.27

0.00

0.02

8720

Med

ical

inst

rum

ents

and

app

lianc

es10

1082

.991

0.51

2739

.939

0.18

0.01

0.49

0.00

0.00

0.00

6418

Pape

r & p

aper

boar

d,im

preg

nat.c

oat.

9801

2.15

10.

4995

85.0

380.

630.

130.

200.

010.

07

7492

taps

,coc

ks,v

alve

s etc

.for p

ipes

,tan

9754

0.29

20.

4929

1.03

80.

020.

000.

210.

000.

000.

00

6997

arti

cles

of i

ron

or st

eel,

n.e.

s.91

868.

674

0.46

488.

743

0.03

0.28

0.52

0.00

0.09

0.66

5839

oth

er p

olym

eriz

atio

n an

d co

polim

eri

8760

8.29

70.

4476

04.2

040.

500.

240.

400.

170.

750.

07

4236

Sunfl

ower

seed

oil

8403

4.06

40.

4232

.534

0.00

0.39

0.62

6.32

0.19

0.16

0342

Fish

,froz

en (e

xclu

ding

fille

ts)

8067

2.74

0.41

82.9

480.

010.

000.

181.

390.

010.

00

5156

het

eroc

yclic

com

poun

ds;n

ucle

ic a

cid

7907

5.05

0.40

442.

661

0.03

0.00

0.01

0.00

0.00

5832

Poly

prop

ylen

e77

244.

594

0.39

2342

8.50

71.

530.

900.

730.

070.

600.

11

tabl

e 3

(Con

t’d)

194

International Journal of Economics and Management

6749

oth

er sh

eets

and

pla

tes,o

f iro

n 77

006.

135

0.39

8179

.244

0.54

0.02

0.32

0.01

0.06

0.00

5833

Poly

styr

ene

and

its c

opol

ymer

s76

989.

008

0.39

6074

.534

0.40

0.48

1.64

0.06

0.33

0.02

0611

Suga

rs,b

eet a

nd c

ane,

raw,

solid

7375

9.66

80.

370.

000.

000.

010.

09

7821

Mot

or v

ehic

les f

or tr

ansp

ort o

f goo

ds73

527.

096

0.37

776.

299

0.05

0.00

0.02

0.01

0.01

0224

Milk

& c

ream

,pre

serv

ed,c

once

ntra

ted

7246

4.82

60.

3710

3.36

80.

017.

120.

564.

510.

430.

30

0612

Refi

ned

suga

rs a

nd o

ther

pro

d.

7133

5.48

90.

3614

9.39

80.

010.

000.

750.

000.

370.

16

6415

Pape

r and

pap

erbo

ard,

in ro

lls o

r sh

eets

7108

6.89

70.

3631

42.9

40.

210.

200.

240.

060.

030.

04

5823

alk

yds a

nd o

ther

pol

yest

ers

6900

6.25

30.

3512

234.

899

0.80

0.55

0.82

0.02

0.10

0.18

0230

But

ter

6867

0.14

10.

350.

000.

000.

020.

310.

390.

17n

o of

pro

duct

s with

IrC

A>1

311

75

3N

ote:

the

shad

ed c

ells

repr

esen

t pro

duct

s with

pot

entia

lly h

ighe

r int

ra-tr

ade

with

thei

r res

pect

ive

IRC

as t

hat h

ave

valu

es o

f gre

ater

than

1.

tabl

e 3

(Con

t’d)

195

are there Prospects for Future Economic Integration among Muslim Countries?

1% each), while the remaining 11 products (i.e., excluding petrol, oils & crude oils) constitute import share of no greater than 4%.

Based on the IRCa of trading partners, it was found that 27 products show potential improvement in intra-oIC trade. these include 6 items each from food & live animals (SITC 0) and manufactured goods (SITC 6), five items from machinery & transport equipment (SItC 7), three items from chemicals & materials (SItC 5), two items each from minerals & fuels (SItC 3) and miscellaneous manufactures (SItC 8), as well as 1 item each from beverages & tobacco (SItC 1), crude materials (SItC 2), and animal & vegetable fat (SItC 4).

as was the case with Egypt, Malaysia seems to demonstrate the highest number of products (13 products) in which it has trade complementarities with Jordan. this is followed by Egypt, Syria, oman and Saudi arabia with 9, 6, 4 and 2 products, respectively. out of the 27 products that show prospects for higher intra-oIC trade, 7 products are found to have more than 1 trading partner possessing comparative advantage. Petrol, oils & crude oils (SItC 3330) again dominates intra-oIC imports with a share of 54.21%.

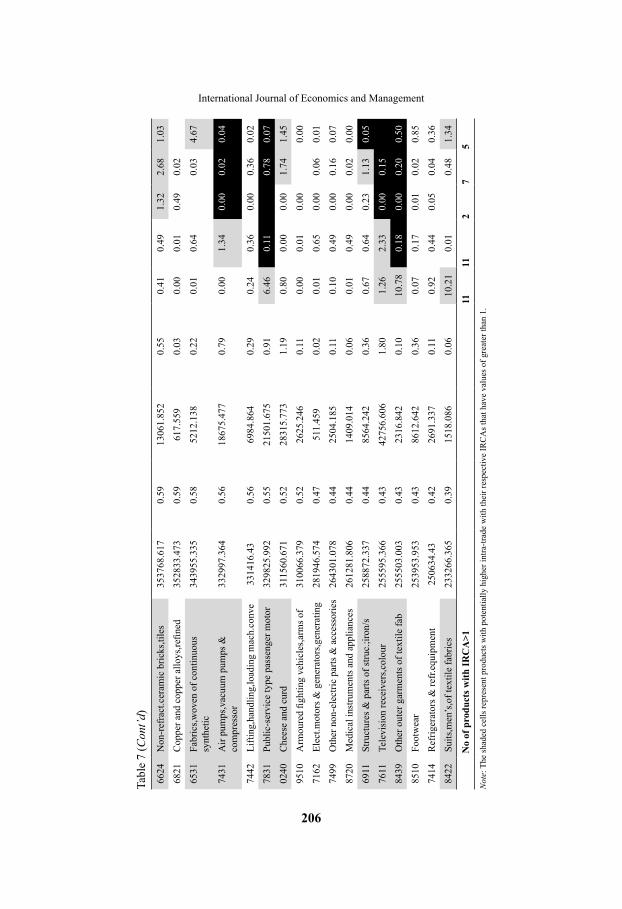

Malaysiatable 5 provides Malaysia’s import structure and her corresponding IRCas of selected oIC partners. Based on the top 50 products imported by Malaysia, electronic microcircuits (SItC 7764) make up the largest share of 12.42% with uS$14.11 billion of total import value. at 1-digit aggregate level the statistics reveals that Malaysia’s import in 2005 are dominated by machinery & transport equipment (SItC 7) which accounts for 48.07% of the total followed by manufactured goods (SItC 6), minerals & fuels (SItC 3) and chemical & materials (SItC 5) with the shares of 4.08%, 3.39% and 2.91% of the total, respectively.

a review of complementarity of Malaysia’s imports and its trading partner’s comparative advantage does not seem to show much prospect for future economic integration among these countries. only 11 of the 50 major products imported by Malaysia are found to have potential for intra-trade with Egypt registering the highest number of items (5 products) followed by Jordan and Saudi arabia (both 3 products) and oman and Syria (both 2 products).

these 11 products have a regional import share of only 7.48% and the extent of the disparity between imports and products with IRCa<1 among these six selected oIC countries is the highest for Malaysia. out of the top 50 major imports which represent 62.44% of Malaysia’s imports, 78% of these products show an IRCa of less than 1, suggesting the extent to which the region is lacking in “efficiency” to meet Malaysia’s import needs.

196

International Journal of Economics and ManagementTa

ble

4 M

ajor

impo

rts o

f Jor

dan

and

inde

x of

reve

aled

com

para

tive

adva

ntag

e (I

RC

a) o

f sel

ecte

d o

IC p

artn

er c

ount

ries

SIT

CPr

oduc

t des

crip

tion

Trad

e va

lue

(uS$

‘000

)

Shar

e in

tota

l im

port

s (%

)

Trad

e va

lue

from

sele

cted

O

IC c

ount

ries

(u

S$ ‘0

00)

Shar

e of

impo

rts

from

sele

cted

OIC

co

untr

ies

(%)

IrC

A

Jord

anM

alay

sia

Om

anSa

udi

Syri

a

3330

Petro

l.oils

& c

rude

oils

1,

711,

157.

086

16.3

71,

710,

972.

699

54.2

10.

810.

873.

260.

510.

00

7810

Pass

enge

r mot

or c

ars,f

or tr

ansp

ort

412,

230.

189

3.94

19.0

540.

000.

000.

020.

000.

06

6552

Kni

tted/

croc

hete

d fa

bric

s of fi

bres

411,

364.

425

3.93

141.

619

0.00

2.25

0.45

0.00

0.04

7643

Rad

iote

legr

aphi

c &

radi

otel

epho

nic

306,

467.

344

2.93

4,22

8.07

20.

130.

021.

550.

060.

010.

09

5417

Med

icam

ents

(incl

udin

g ve

terin

ary

med

.)21

4,66

0.16

12.

057,

384.

979

0.23

0.12

0.02

0.00

0.87

0.42

7821

Mot

or v

ehic

les f

or tr

ansp

ort o

f goo

ds19

1,71

6.73

11.

8324

.629

0.00

0.27

0.02

0.00

0.01

8973

Jew

elle

ry o

f gol

d,si

lver

or p

latin

um15

8,08

5.41

71.

515,

698.

615

0.18

2.15

6724

Pudd

led

bars

and

pili

ngs;

ingo

ts14

8,12

8.32

11.

420.

001.

050.

002.

110.

05

7649

Parts

of a

ppar

atus

of d

ivis

ion

76--

142,

150.

781

1.36

271.

958

0.01

0.03

1.38

0.03

0.32

7929

Parts

of h

eadi

ng 7

92--

,exc

l.tyr

es12

4,50

7.06

61.

190.

000.

160.

590.

00

0411

dur

um w

heat

,unm

illed

119,

857.

843

1.15

10,1

43.0

620.

320.

010.

000.

260.

010.

01

3414

Petro

leum

gas

es a

nd o

ther

gas

eous

10

2,52

7.21

10.

9810

2,52

7.21

13.

250.

340.

180.

000.

000.

09

0430

Bar

ley,

unm

illed

100,

470.

846

0.96

0.00

0.01

0.00

0.00

0.00

0.01

4242

Palm

oil

89,8

67.5

940.

8620

,007

.582

0.63

0.02

30.9

90.

700.

580.

21

3413

Petro

leum

gas

es a

nd o

ther

gas

eous

85

,232

.056

0.82

59,2

04.9

101.

8822

.91

6.29

0.16

0.63

5831

Poly

ethy

lene

83,7

09.5

180.

8049

,353

.284

1.56

0.29

1.29

0.11

0.31

7849

oth

er p

arts

& a

cces

sorie

s of m

otor

83,0

23.4

760.

791,

286.

253

0.04

0.13

0.11

0.00

0612

Refi

ned

suga

rs a

nd o

ther

pro

d.

77,4

13.5

420.

7431

,791

.188

1.01

1.87

0.72

0.00

1.34

6531

Fabr

ics,w

oven

of c

ontin

uous

synt

h.76

,562

.462

0.73

14,2

02.4

030.

450.

020.

640.

460.

040.

08

7284

Mac

h.&

app

lianc

es fo

r spe

cial

ized

76

,140

.245

0.73

1,98

9.53

10.

060.

010.

510.

170.

000.

09

197

are there Prospects for Future Economic Integration among Muslim Countries?

7832

Roa

d tra

ctor

s and

sem

i-tra

ilers

70,8

74.1

700.

680.

000.

210.

020.

00

0980

Edib

le p

rodu

cts a

nd p

repa

ratio

ns

69,8

34.9

580.

6721

,563

.792

0.68

0.32

0.52

0.32

0.18

3.12

9710

Gol

d,no

n-m

onet

ary

68,6

00.0

410.

660.

000.

86

6783

oth

er tu

bes a

nd p

ipes

,of i

ron

or st

eel

67,7

46.7

970.

651,

790.

801

0.06

0.07

1.71

0.01

0.00

0440

Mai

ze (c

orn)

,unm

illed

66,1

85.1

300.

6312

2.88

20.

000.

100.

010.

270.

12

3510

Elec

tric

curr

ent

65,9

11.8

230.

6365

,911

.823

2.09

0.13

0.21

0.10

0.02

0.51

0224

Milk

& c

ream

,pre

serv

ed,c

once

ntra

ted

64,7

23.5

200.

623,

985.

685

0.13

0.09

0.55

4.51

0.43

4.40

0422

Ric

e se

mi-m

illed

or w

holly

mill

ed59

,129

.711

0.57

16,5

50.3

390.

5233

.99

0.01

0.03

1223

toba

cco,

man

ufac

ture

d (in

c.sm

okin

g)58

,003

.112

0.55

693.

994

0.02

0.11

1.57

0.07

0.00

6842

alu

min

ium

and

alu

min

ium

al

loys

,wor

k57

,645

.789

0.55

8,97

3.40

90.

280.

000.

500.

010.

02

6822

Cop

per a

nd c

oppe

r allo

ys,w

orke

d56

,431

.625

0.54

35,6

62.1

761.

132.

201.

360.

180.

00

0813

oil-

cake

& o

ther

resi

dues

55,2

60.6

270.

531,

131.

421

0.04

0.43

0.45

0.69

0.14

1.53

6749

oth

er sh

eets

and

pla

tes,o

f iro

n or

stee

l54

,364

.197

0.52

11,6

65.8

070.

370.

020.

320.

060.

02

8939

Mis

cella

neou

s art.

of m

ater

ials

52

,623

.243

0.50

7,55

4.51

20.

240.

240.

510.

17

1110

Non

alc

ohol

ic b

ever

ages

,n.e

.s.51

,089

.784

0.49

35,5

30.9

471.

130.

400.

500.

000.

00

2483

Woo

d of

non

-con

ifero

us sp

ecie

s,saw

n50

,907

.177

0.49

277.

757

0.01

0.02

7.27

0.00

0.60

7161

Mot

ors &

gen

erat

ors,d

irect

cur

rent

50,8

23.7

780.

4940

.721

0.00

0.28

0.18

1.17

0.00

0.08

5989

Che

mic

al p

rodu

cts a

nd p

repa

ratio

ns50

,435

.189

0.48

7,29

4.56

00.

230.

010.

780.

590.

000.

05

0111

Mea

t of b

ovin

e an

imal

s, fr

esh,

chi

lled

46,1

09.3

710.

4412

9.23

30.

000.

030.

010.

010.

010.

17

7599

Parts

of a

nd a

cces

sorie

s 45

,936

.901

0.44

1,26

3.46

70.

040.

003.

640.

000.

000.

02

7721

Elec

t.app

.such

as s

witc

hes,r

elay

s45

,913

.919

0.44

4,85

7.95

20.

150.

022.

980.

020.

010.

00

6624

Non

-ref

ract

.cer

amic

bric

ks,ti

les

45,8

04.4

580.

4414

,396

.907

0.46

0.22

0.49

1.66

0.17

0.94

5530

Perf

umer

y,co

smet

ics a

nd to

ilet p

rep

45,4

46.3

920.

4313

,661

.024

0.43

4.00

0.21

0.39

0.27

0.39

8720

Med

ical

inst

rum

ents

and

app

lianc

es44

,832

.464

0.43

193.

876

0.01

0.02

0.49

0.04

tabl

e 4

(Con

t’d)

198

International Journal of Economics and Managementta

ble

4 (C

ont’d

)82

19o

ther

furn

iture

and

par

ts43

,388

.261

0.42

7,42

4.22

80.

240.

021.

940.

00

5832

Poly

prop

ylen

e42

,954

.710

0.41

26,7

47.6

800.

850.

720.

730.

020.

050.

01

5169

org

anic

che

mic

als,n

.e.s

42,3

03.8

080.

403,

136.

244

0.10

10.1

20.

020.

220.

841.

49

8459

oth

er o

uter

gar

men

ts &

cl

othi

ng,k

nitw

ear

42,0

56.1

010.

401,

491.

048

0.05

0.55

0.60

0.19

6841

alu

min

ium

and

alu

min

ium

allo

ys41

,222

.156

0.39

0.00

1.55

0.25

0.07

0.01

0.00

0012

Shee

p an

d go

ats,

live

39,8

61.4

250.

380.

000.

270.

000.

551.

0529

7.73

no

of p

rodu

cts w

ith Ir

CA

>19

134

26

Not

e: t

he sh

aded

cel

ls re

pres

ent p

rodu

cts w

ith p

oten

tially

hig

her i

ntra

-trad

e w

ith th

eir r

espe

ctiv

e IR

Ca

s tha

t hav

e va

lues

of g

reat

er th

an 1

.

Tabl

e 5

Maj

or im

ports

of M

alay

sia

and

inde

x of

reve

aled

com

para

tive

adva

ntag

e (I

RC

a) o

f sel

ecte

d o

IC p

artn

er c

ount

ries

SIT

CPr

oduc

t des

crip

tion

Trad

e va

lue

(uS$

‘000

)

Shar

e in

tota

l im

port

s (%

)

Trad

e va

lue

from

sele

cted

O

IC c

ount

ries

(u

S$ ‘0

00)

Shar

e of

impo

rts

from

sele

cted

O

IC c

ount

ries

(%

)

IrC

A

Egy

ptJo

rdan

Om

anSa

udi

Syri

a

7764

Elec

troni

c m

icro

circ

uits

1410

8322

.61

12.4

23.

679

0.00

0.00

0.01

0.00

7768

Piez

o-el

ectri

c cr

ysta

ls,m

ount

ed11

0868

39.7

39.

7623

8.8

0.01

0.03

0.00

0.00

0.00

7599

Parts

of a

nd a

cces

sorie

s sui

tabl

e 64

8293

3.24

85.

7141

.357

0.00

0.00

0.00

0.00

0.00

3330

Petro

l.oils

& c

rude

oils

34

0556

0.53

53.

0015

0913

8.15

971

.11

0.86

11.5

512

.73

9.89

7788

oth

er e

lect

.mac

hine

ry a

nd e

quip

men

t23

3551

9.88

82.

0697

.948

0.00

0.01

0.01

0.00

0.00

0.00

7721

Elec

t.app

.such

as s

witc

hes,r

elay

s,19

7687

8.04

11.

7423

07.7

020.

110.

030.

070.

020.

010.

00

7649

Parts

of a

ppar

atus

of d

ivis

ion

76--

1900

048.

452

1.67

124.

741

0.01

0.03

0.00

0.00

0.00

0.00

7722

Prin

ted

circ

uits

and

par

ts th

ereo

f18

8059

3.84

51.

661.

907

0.00

0.00

0.00

0.00

7763

dio

des,t

rans

isto

rs a

nd si

m.se

mi-

cond

ucto

rs16

4392

8.36

51.

450.

000.

000.

000.

000.

00

199

are there Prospects for Future Economic Integration among Muslim Countries?

7284

Mac

h.&

app

lianc

es fo

r spe

cial

ized

14

6087

2.77

41.

2915

.103

0.00

0.03

0.06

0.00

0.00

0.01

9710

Gol

d,no

n-m

onet

ary

1360

887.

444

1.20

13.4

020.

000.

420.

050.

050.

30

7810

Pass

enge

r mot

or c

ars,f

or tr

ansp

ort

1302

975.

569

1.15

40.6

430.

000.

000.

000.

000.

00

7643

Rad

iote

legr

aphi

c &

radi

otel

epho

nic

1240

973.

754

1.09

0.00

0.00

0.00

0.00

0.00

0.00

7525

Perip

hera

l uni

ts,in

cl.c

ontro

l & a

da11

4105

6.36

51.

002.

987

0.00

0.00

0.00

0.00

0.01

7522

Com

plet

e di

gita

l dat

a pr

oces

sing

10

4710

9.66

60.

920.

000.

000.

000.

000.

00

7849

oth

er p

arts

& a

cces

sorie

s of m

otor

9909

51.5

650.

8713

4.75

90.

010.

020.

020.

000.

03

6822

Cop

per a

nd c

oppe

r allo

ys,w

orke

d76

6725

.588

0.68

48.5

790.

000.

050.

350.

280.

070.

05

6783

oth

er tu

bes a

nd p

ipes

,of i

ron

or st

eel

7287

95.2

870.

640.

000.

030.

191.

570.

140.

13

8742

dra

win

g,m

arki

ng-o

ut,d

isc

calc

ulat

or70

9549

.607

0.62

19.5

70.

000.

000.

000.

000.

00

6821

Cop

per a

nd c

oppe

r allo

ys,re

fined

68

0620

.928

0.60

8550

.665

0.40

0.02

0.00

0.49

0.01

6746

Shee

ts &

pla

tes,r

olle

d;th

ickn

ess

6676

46.5

710.

5913

.426

0.00

0.00

0.00

0.09

0.00

7162

Elec

t.mot

ors &

gen

erat

ors,g

ener

atin

g66

0822

.868

0.58

0.00

0.06

0.01

0.00

0.01

0.01

8939

Mis

cella

neou

s art.

of m

ater

ials

63

3624

.16

0.56

7.31

80.

000.

301.

180.

140.

100.

54

7712

oth

er e

lect

ric p

ower

mac

hine

ry,p

art

6229

43.2

890.

551.

329

0.00

0.00

0.00

0.00

0.00

0.01

7932

Ship

s,boa

ts a

nd o

ther

ves

sels

6003

19.8

930.

530.

000.

070.

000.

000.

000.

00

5112

Cyc

lic h

ydro

carb

ons

5989

71.4

410.

530.

000.

000.

001.

613.

16

2820

Was

te a

nd sc

rap

met

al o

f iro

n or

stee

l56

5992

.383

0.50

0.00

0.15

0.81

0.04

0.00

0.04

7781

Bat

terie

s and

acc

umul

ator

s and

par

t54

6378

.966

0.48

11.3

280.

000.

280.

440.

340.

060.

04

5831

Poly

ethy

lene

5160

49.9

680.

4553

694.

641

2.53

3.83

0.21

0.16

4.31

0.29

7924

airc

raft

exce

edin

g an

unl

aden

wei

gh50

7481

.029

0.45

1.50

60.

00

5417

Med

icam

ents

(incl

udin

g ve

terin

ary

med

.)50

5004

.113

0.44

301.

825

0.01

0.29

3.46

0.00

0.03

0.20

5989

Che

mic

al p

rodu

cts a

nd p

repa

ratio

ns,

4968

49.4

160.

4423

.706

0.00

0.22

0.23

0.00

0.07

0.14

7929

Parts

of h

eadi

ng 7

92--

,exc

l.tyr

es49

1842

.447

0.43

965.

201

0.05

0.00

0.00

0.00

0.07

tabl

e 5

(Con

t’d)

200

International Journal of Economics and Management

7761

tele

visi

on p

ictu

re tu

bes,c

atho

de

4880

78.9

150.

430.

000.

000.

000.

00

6749

oth

er sh

eets

and

pla

tes,o

f iro

n or

stee

l47

8433

.695

0.42

21.1

360.

000.

050.

020.

010.

060.

00

6842

alu

min

ium

and

alu

min

ium

al

loys

,wor

k45

1024

.101

0.40

0.00

1.26

0.81

0.52

0.14

0.30

3222

Oth

er c

oal,w

heth

er/n

ot p

ulve

rized

4496

00.9

290.

400.

000.

000.

000.

000.

15

7149

Parts

of t

he e

ngin

es &

mot

ors o

f 71

4490

53.9

790.

400.

000.

000.

000.

000.

01

6841

alu

min

ium

and

alu

min

ium

allo

ys44

0380

.323

0.39

9812

.073

0.46

2.07

0.52

0.00

0.00

0.02

8749

Parts

,n.e

.s.ac

cess

orie

s for

873

--,8

4293

92.8

160.

383.

510.

000.

000.

000.

000.

000.

00

6727

Iron

or s

teel

coi

ls fo

r re-

rolli

ng42

6271

.649

0.38

0.00

7.06

0.00

0.03

0.01

2320

Nat

ural

rubb

er la

tex;

nat

.rubb

er

4227

13.4

990.

370.

000.

170.

000.

010.

02

5823

alk

yds a

nd o

ther

pol

yest

ers

4214

10.6

950.

3728

.983

0.00

0.00

0.55

0.02

0.10

0.18

7528

off-

line

data

pro

cess

ing

equi

pmen

t.41

9976

.035

0.37

5.91

10.

000.

000.

000.

03

7499

oth

er n

on-e

lect

ric p

arts

& a