PwC | AWM Asia Pacific Market Research CentreIssue 4 | 2019

Asset and WealthManagement Research Digest

When talking about cross-border fund passporting, the European-originating Undertakings for Collective Investments in Transferable Securities (“UCITS”) framework is widely-regarded as the global gold standard. The UCITS fund passporting regime, which encompasses 28 countries in Europe, has 33,359 funds and EUR 9.28tr of AUM falling under the regime as of December 2018.1 It has facilitated the rise of European fund centres like Luxembourg and Dublin, and has provided a framework for emerging passporting schemes the world over. An additional benefit is to investors who, through the ability to purchase such a massive range of funds, are able to leverage the investment expertise of a myriad of asset managers who distribute qualifying UCITS funds.

By comparison, and perhaps in reflection of the general level of maturity among APAC economies, APAC lacks a developed and comprehensive fund passporting or cross-border scheme as found in Europe with the UCITS framework.

There are green-shoots of progress though, with three unique approaches to fund passporting arrangements emerging across the region, sometimes in overlapping capacities.

Asian Fund Passports – Is it 1988 in APAC?

While the future of fund passporting across APAC may take longer than anticipated and the final scheme may not be directly related to any of the existing programmes, we believe the development of such arrangements is to be encouraged and nurtured by industry players across the region.

1 European Fund and Asset Management Association (EFAMA)

2 Asset and Wealth Management Research Digest

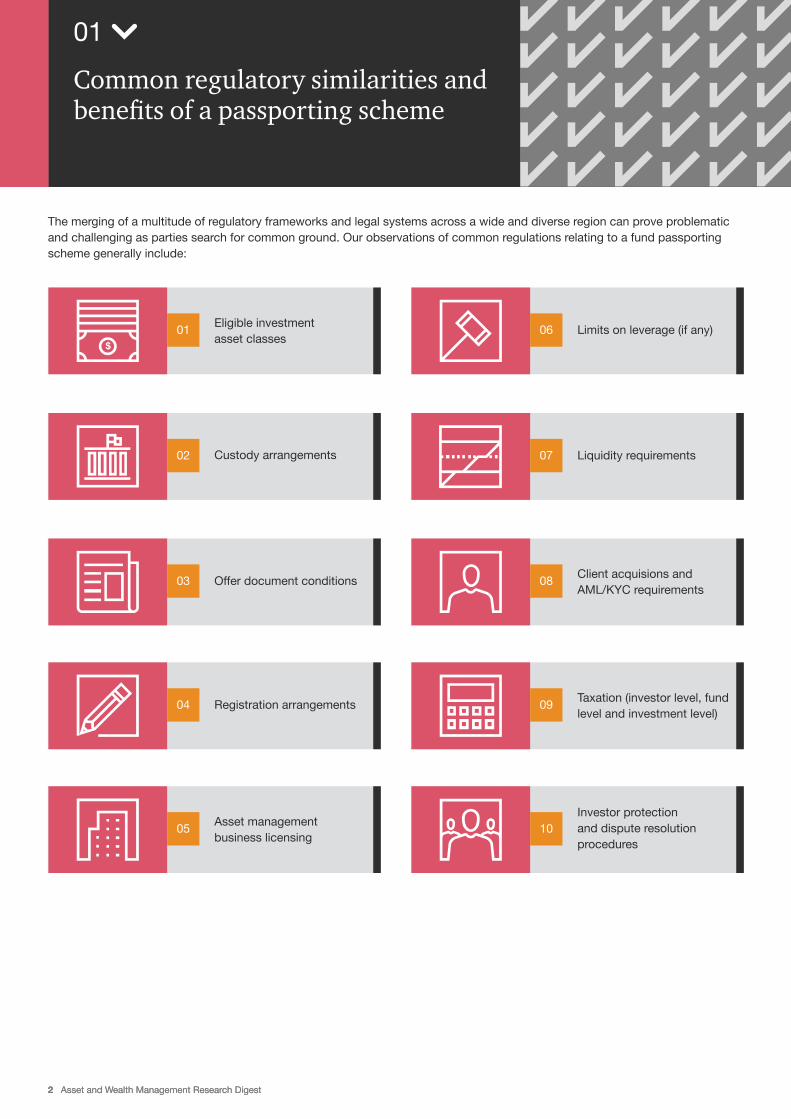

The merging of a multitude of regulatory frameworks and legal systems across a wide and diverse region can prove problematic and challenging as parties search for common ground. Our observations of common regulations relating to a fund passporting scheme generally include:

2 Asset and Wealth Management Research Digest

Eligible investment asset classes

Limits on leverage (if any)

Offer document conditionsClient acquisions and AML/KYC requirements

Custody arrangements Liquidity requirements

Registration arrangementsTaxation (investor level, fund level and investment level)

Asset management business licensing

Investor protection and dispute resolution procedures

01 06

03 08

02 07

04 09

05 10

Common regulatory similarities and benefits of a passporting scheme

01

Asset and Wealth Management Research Digest 3

Where such regulatory challenges, which typically were prescribed to protect the local industry products and market place can be overcome, substantial benefits can be derived for asset managers and investors alike. Specifically, these benefits can include:

Improved efficiency and reduced fees/costs

With fund passporting opening up the possibility of new economies and products for investors to invest into, the potential size of funds swells and, if they can attract new investors, this can result in larger funds. This in turn leads to greater use of economies of scale and efficiency across the fund industry. With a larger pool of investors to target, and more funds and fund managers targeting the same investors, competition within the industry increases which results in greater results for investors and better outcomes for the industry at large. An example of this would be the direct access to offshore funds that passporting brings which in turn eliminates the need for additional distribution layers and thus reduces fees and commissions paid.

Increased investor choice

Fund passporting allows for foreign fund managers to sell their products directly to investors outside their home economies. In addition to the cost savings this model brings, mentioned above, this provides investors with a vastly expanded array of products that were earlier either inaccessible to them or priced higher due to the afore mentioned additional distribution layers. Being able to access an increased range of funds for lower cost will provide investors access to otherwise inaccessible markets and enable greater diversification.

Improved services

As more fund managers are now in the market offering their products to investors, there is greater competition among the fund managers and greater incentives to reap the rewards on offer that innovation, performance, and client servicing brings. This aspect is not limited to fund managers servicing investors, custodian and other fund service providers will have an increased pool of asset managers to target as clients and their levels of performance should rise as well through the increased competition.

Improved consumer protection

Economies across geographic regions are rarely homogenous, some will be more mature, others less so. By entering into a fund passporting scheme, economies can share best-practice among their fund managers and investors have the option of investing with fund managers that provide them with the greatest protection. Thus, fund managers not engaging in industry best practice or not looking out for the interests of investors can adopt practices from other mangers which do practice these matters in order to compete better in the expanded market.

Benefits to the wider economy

The range of economies on offer within a fund passporting scheme means that investors have an impressive selection of economic development levels and growth opportunities to invest in which aids in diversification as covered earlier. It also means that local capital markets can receive inflows from other economies which deepens liquidity across the region the fund passporting scheme relates to. With a unified framework, there is increased visibility and interest in regional funds, and this can translate to increased support for the regional fund management industry.

Despite these benefits, significant challenges to implementing a regional fund passporting regime exist, especially in regards to reconciling differing taxation requirements across the jurisdictions within the passporting scheme.

4 Asset and Wealth Management Research Digest

In spite of the strong integration of APAC countries into the world economy, the asset management industry remains largely fragmented, with each market providing a different level of access, mode of entry for foreign players, and distribution dynamics.

As these markets develop, there is a clear trend towards regionalisation. Efforts to promote cross-border fund distribution aim to provide significant benefits to participating economies, allowing them to strengthen the capacity and expertise of their funds industry while improving international competitiveness of their financial markets.

While APAC currently lacks a regional fund passporting framework at the level of the UCITS regime, there are several green shoots emerging across the region as fund centres and fund passporting schemes which show promise in developing into a comprehensive framework:

Asia Region Fund Passport ASEAN CIS Mutual Recognition of Funds

Status:

MOC signed in April 2016, - commenced 1 February 2019

Status:

Live 25 August 2014

Status:

Live 1 July 2015

Jurisdictions in scope:

Australia, South Korea, New Zealand, Japan, Thailand

Jurisdictions in scope:

Malaysia, Singapore and Thailand

Jurisdictions in scope:

China, Hong Kong

Other MRFs:

Switzerland & Hong KongFrance & Hong KongUK & Hong Kong Luxembourg & Hong Kong

Current APAC fund passporting and cross-border scheme landscape

02

Source: PwC AWM Research Centre analysis

Asset and Wealth Management Research Digest 5

The ARFP is a common framework of coordinated regulatory oversight to facilitate cross border marketing of managed funds across participating economies the APAC. The Memorandum of Cooperation (“MOC”), signed in 2016, sets out the internationally agreed rules and cooperation mechanisms for the ARFP, and is the basis for its implementation into domestic law. Signatories to the MOC, namely: Australia, Japan, Republic of Korea, New Zealand, and Thailand are deemed ‘participating economies’ which entitles them to have representatives on the Joint Committee (“JC”), the body which oversees implementation of the ARFP.

The stated goals of the ARFP are:

• Deepening APACs capital markets to attract finance for economic growth in the region.

• Strengthening the efficiency, expertise, and international competitiveness of the funds management industry in the region.

• Recycling savings and growing the pool of funds available for investment in the region.

• Providing investors in participating economies with a more diverse and competitive range of investment opportunities.

• Maintaining the legal and regulatory frameworks which promote investor protection, and fair, efficient, and transparent markets for financial services.

Engagement with non-ARFP jurisdictions is maintained through their participation as observers on the JC, as Singapore, Philippines, and Hong Kong are. In addition, JC members continue to engage in regional and wider international events to ensure ARFP is represented by its members in international setting and can track industry best-practice and market itself to potential members for future enlargement of the scheme.

Non-members have, in some instances, undertaken targeted capacity building activities in the region, such as technical and policy workshops, to improve the understanding of regulators’ and industry of the ARFP and pave the way for potential future membership.

The potential membership of APAC asset managers is substantial and dispersed across the whole of the APAC region as the chart below shows (numbers denote potential fund managers):

India34

Japan60

Korea56Hong Kong

94

Philippines 4

New Zealand18

Australia109

Taipei34

Thailand18

Indonesia14

Singapore73

The Asia Region Fund Passport (“ARFP”) scheme

03

Country

Australia

Korea

Singapore

Taipei

Indonesia

Hong Kong

India

New Zealand

Japan

Thailand

Philippines

109

56

73

34

14

94

34

18

60

18

4

Sources: Morningstar direct, IMAS Directory, and PwC Analysis

6 Asset and Wealth Management Research Digest

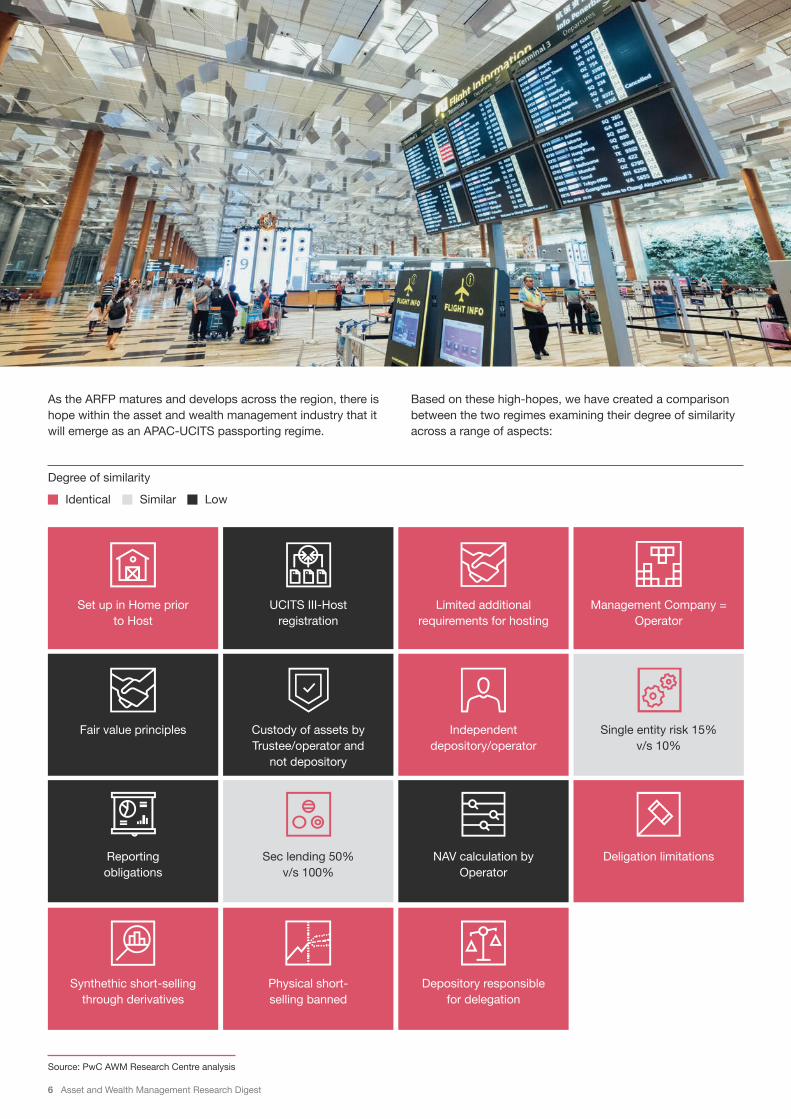

As the ARFP matures and develops across the region, there is hope within the asset and wealth management industry that it will emerge as an APAC-UCITS passporting regime.

Degree of similarity

Identical Similar Low

Based on these high-hopes, we have created a comparison between the two regimes examining their degree of similarity across a range of aspects:

Set up in Home prior to Host

Reporting obligations

Synthethic short-selling through derivatives

Fair value principles

UCITS III-Host registration

Sec lending 50% v/s 100%

Physical short-selling banned

Custody of assets by Trustee/operator and

not depository

Limited additional requirements for hosting

NAV calculation by Operator

Depository responsible for delegation

Independent depository/operator

Management Company = Operator

Deligation limitations

Single entity risk 15% v/s 10%

Source: PwC AWM Research Centre analysis

Asset and Wealth Management Research Digest 7

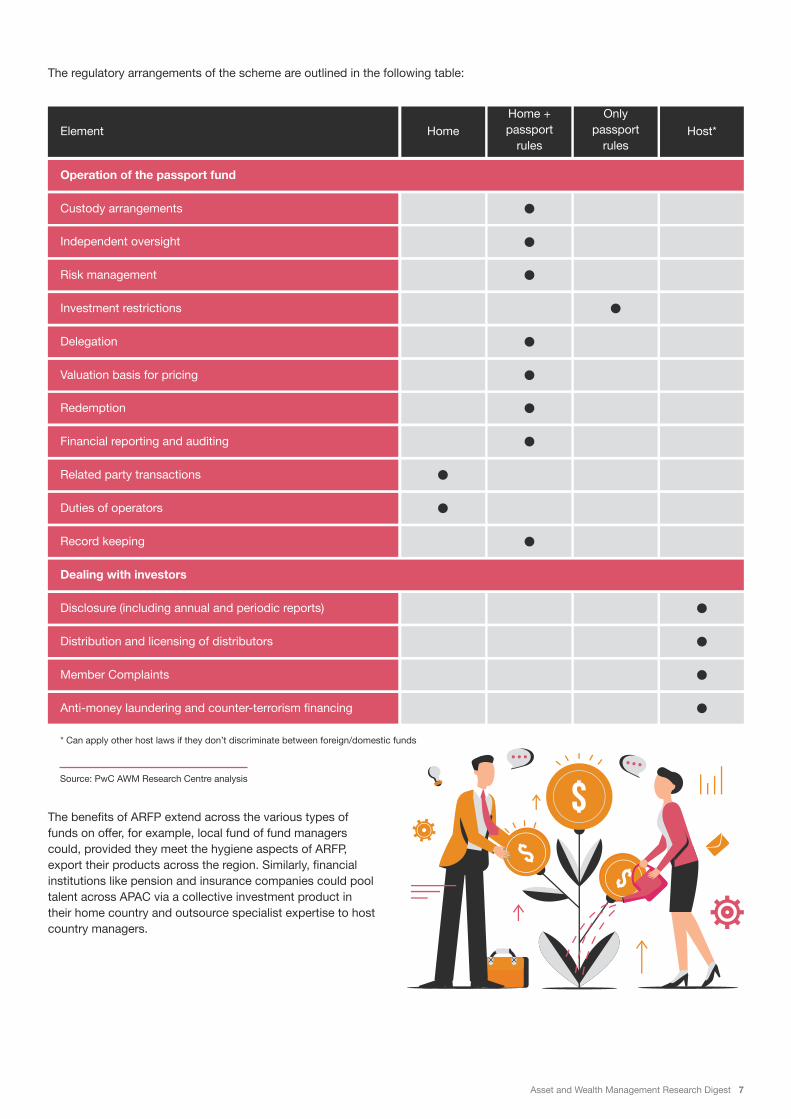

The regulatory arrangements of the scheme are outlined in the following table:

* Can apply other host laws if they don’t discriminate between foreign/domestic funds

Element

Operation of the passport fund

Custody arrangements

Independent oversight

Risk management

Investment restrictions

Delegation

Valuation basis for pricing

Redemption

Financial reporting and auditing

Related party transactions

Disclosure (including annual and periodic reports)

Duties of operators

Distribution and licensing of distributors

Record keeping

Member Complaints

Dealing with investors

Anti-money laundering and counter-terrorism financing

Home

Home + passport

rules

Only passport

rulesHost*

The benefits of ARFP extend across the various types of funds on offer, for example, local fund of fund managers could, provided they meet the hygiene aspects of ARFP, export their products across the region. Similarly, financial institutions like pension and insurance companies could pool talent across APAC via a collective investment product in their home country and outsource specialist expertise to host country managers.

Source: PwC AWM Research Centre analysis

8 Asset and Wealth Management Research Digest

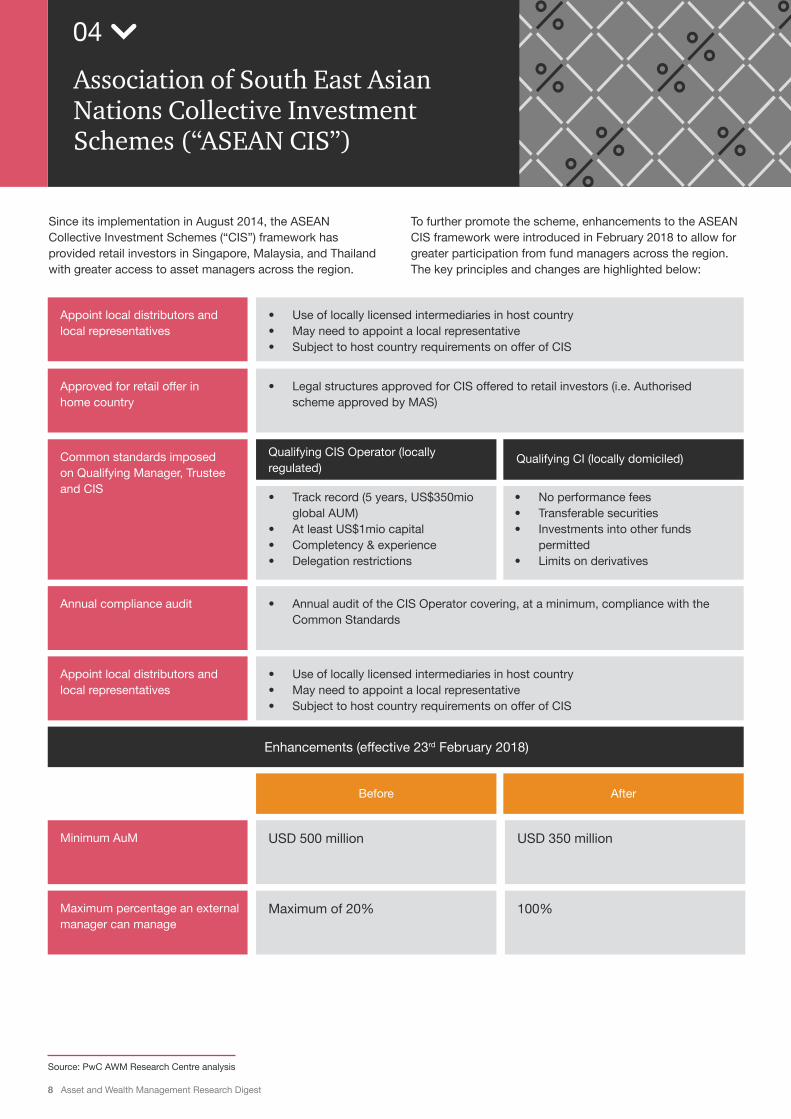

Appoint local distributors and local representatives

Minimum AuM

Maximum percentage an external manager can manage

Annual compliance audit

Appoint local distributors and local representatives

• Use of locally licensed intermediaries in host country• May need to appoint a local representative• Subject to host country requirements on offer of CIS

USD 500 million

Maximum of 20%

USD 350 million

100%

• Annual audit of the CIS Operator covering, at a minimum, compliance with theCommon Standards

• Use of locally licensed intermediaries in host country• May need to appoint a local representative• Subject to host country requirements on offer of CIS

• Track record (5 years, US$350mioglobal AUM)

• At least US$1mio capital• Completency & experience• Delegation restrictions

• No performance fees• Transferable securities• Investments into other funds

permitted• Limits on derivatives

• Legal structures approved for CIS offered to retail investors (i.e. Authorisedscheme approved by MAS)

Qualifying CIS Operator (locally regulated)

Before

Qualifying CI (locally domiciled)

After

Enhancements (effective 23rd February 2018)

Approved for retail offer in home country

Common standards imposed on Qualifying Manager, Trustee and CIS

Since its implementation in August 2014, the ASEAN Collective Investment Schemes (“CIS”) framework has provided retail investors in Singapore, Malaysia, and Thailand with greater access to asset managers across the region.

To further promote the scheme, enhancements to the ASEAN CIS framework were introduced in February 2018 to allow for greater participation from fund managers across the region. The key principles and changes are highlighted below:

Source: PwC AWM Research Centre analysis

Association of South East Asian Nations Collective Investment Schemes (“ASEAN CIS”)

04

Asset and Wealth Management Research Digest 9

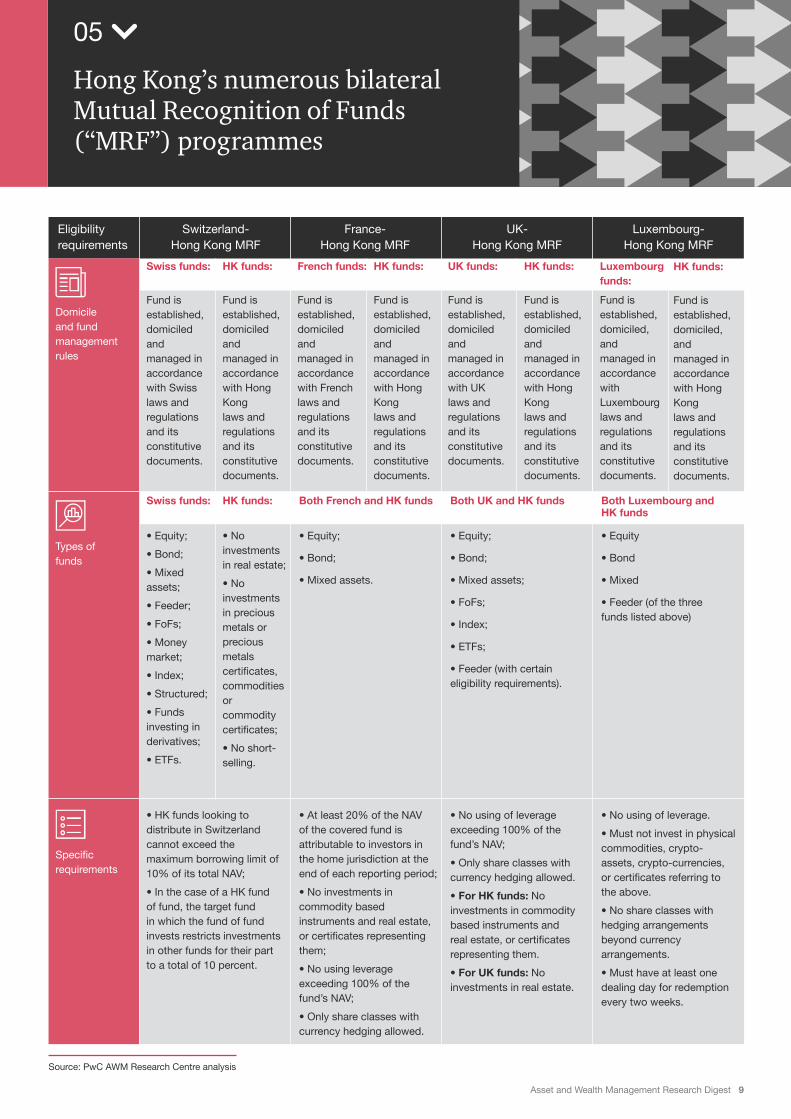

Eligibility requirements

Switzerland- Hong Kong MRF

France- Hong Kong MRF

UK- Hong Kong MRF

Luxembourg- Hong Kong MRF

Fund is established, domiciled and managed in accordance with Swiss laws and regulations and its constitutive documents.

Swiss funds:

• Equity;

• Bond;

• Mixed assets;

• Feeder;

• FoFs;

• Money market;

• Index;

• Structured;

• Funds investing in derivatives;

• ETFs.

Swiss funds:

• HK funds looking to distribute in Switzerland cannot exceed the maximum borrowing limit of 10% of its total NAV;

• In the case of a HK fund of fund, the target fund in which the fund of fund invests restricts investments in other funds for their part to a total of 10 percent.

Domicile and fund management rules

Types of funds

Specific requirements

Fund is established, domiciled and managed in accordance with French laws and regulations and its constitutive documents.

French funds:

Fund is established, domiciled and managed in accordance with UK laws and regulations and its constitutive documents.

UK funds:

Fund is established, domiciled, and managed in accordance with Luxembourg laws and regulations and its constitutive documents.

Luxembourg funds:

Fund is established, domiciled and managed in accordance with Hong Kong laws and regulations and its constitutive documents.

HK funds:

• No investments in real estate;

• No investments in precious metals or precious metals certificates, commodities or commodity certificates;

• No short-selling.

HK funds:

Fund is established, domiciled and managed in accordance with Hong Kong laws and regulations and its constitutive documents.

HK funds:

Fund is established, domiciled and managed in accordance with Hong Kong laws and regulations and its constitutive documents.

HK funds:

Fund is established, domiciled, and managed in accordance with Hong Kong laws and regulations and its constitutive documents.

HK funds:

Both French and HK funds

• At least 20% of the NAV of the covered fund is attributable to investors in the home jurisdiction at the end of each reporting period;

• No investments in commodity based instruments and real estate, or certificates representing them;

• No using leverage exceeding 100% of the fund’s NAV;

• Only share classes with currency hedging allowed.

• Equity;

• Bond;

• Mixed assets.

Both UK and HK funds

• No using of leverage exceeding 100% of the fund’s NAV;

• Only share classes with currency hedging allowed.

• For HK funds: No investments in commodity based instruments and real estate, or certificates representing them.

• For UK funds: No investments in real estate.

• Equity;

• Bond;

• Mixed assets;

• FoFs;

• Index;

• ETFs;

• Feeder (with certain eligibility requirements).

Both Luxembourg and HK funds

• No using of leverage.

• Must not invest in physical commodities, crypto-assets, crypto-currencies, or certificates referring to the above.

• No share classes with hedging arrangements beyond currency arrangements.

• Must have at least one dealing day for redemption every two weeks.

• Equity

• Bond

• Mixed

• Feeder (of the three funds listed above)

Source: PwC AWM Research Centre analysis

Hong Kong’s numerous bilateral Mutual Recognition of Funds (“MRF”) programmes

05

10 Asset and Wealth Management Research Digest

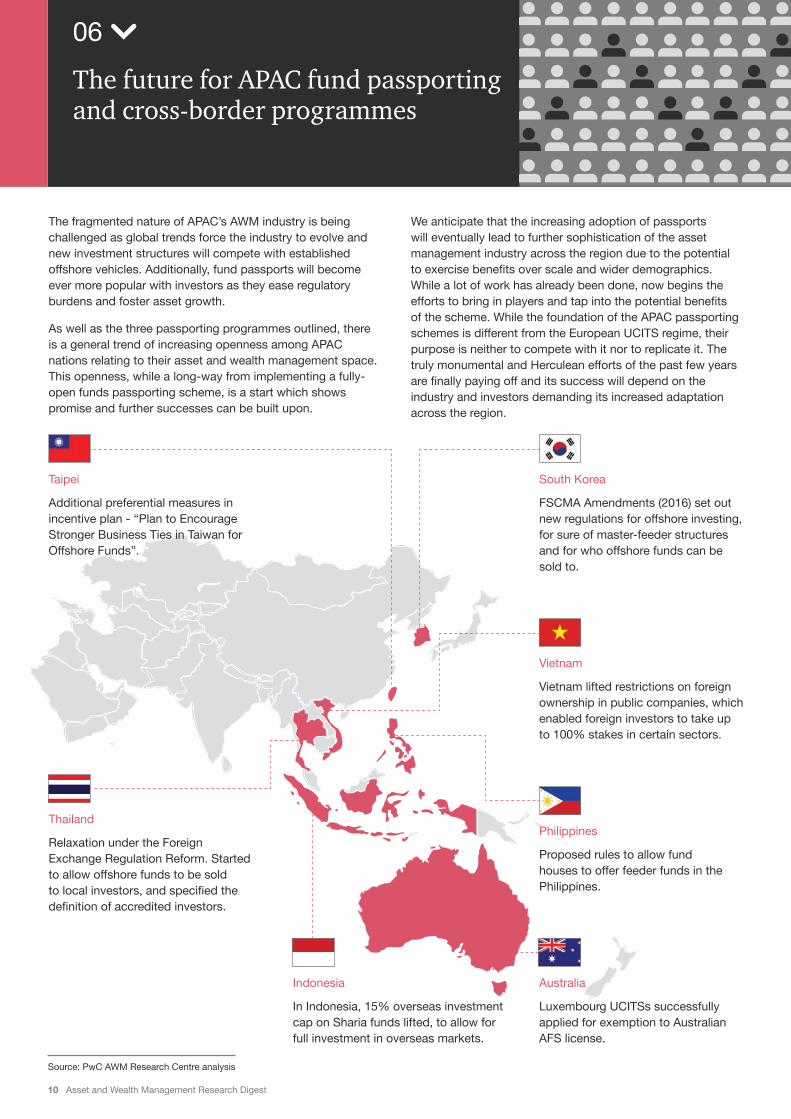

The fragmented nature of APAC’s AWM industry is being challenged as global trends force the industry to evolve and new investment structures will compete with established offshore vehicles. Additionally, fund passports will become ever more popular with investors as they ease regulatory burdens and foster asset growth.

As well as the three passporting programmes outlined, there is a general trend of increasing openness among APAC nations relating to their asset and wealth management space. This openness, while a long-way from implementing a fully-open funds passporting scheme, is a start which shows promise and further successes can be built upon.

We anticipate that the increasing adoption of passports will eventually lead to further sophistication of the asset management industry across the region due to the potential to exercise benefits over scale and wider demographics. While a lot of work has already been done, now begins the efforts to bring in players and tap into the potential benefits of the scheme. While the foundation of the APAC passporting schemes is different from the European UCITS regime, their purpose is neither to compete with it nor to replicate it. The truly monumental and Herculean efforts of the past few years are finally paying off and its success will depend on the industry and investors demanding its increased adaptation across the region.

South Korea

FSCMA Amendments (2016) set out new regulations for offshore investing, for sure of master-feeder structures and for who offshore funds can be sold to.

Taipei

Additional preferential measures in incentive plan - “Plan to Encourage Stronger Business Ties in Taiwan for Offshore Funds”.

Vietnam

Vietnam lifted restrictions on foreign ownership in public companies, which enabled foreign investors to take up to 100% stakes in certain sectors.

Philippines

Proposed rules to allow fund houses to offer feeder funds in the Philippines.

Thailand

Relaxation under the Foreign Exchange Regulation Reform. Started to allow offshore funds to be sold to local investors, and specified the definition of accredited investors.

Australia

Luxembourg UCITSs successfully applied for exemption to Australian AFS license.

Indonesia

In Indonesia, 15% overseas investment cap on Sharia funds lifted, to allow for full investment in overseas markets.

Source: PwC AWM Research Centre analysis

The future for APAC fund passporting and cross-border programmes

06

Asset and Wealth Management Research Digest 11

Our structured, research-based analysis sheds light on the multiple factors affecting your asset management business.

Each market intelligence country digest provides you with:

• The state of the asset & wealth management industry

• The key trends shaping the future of the industry

• Products that are in demand

• Your competitors

• Various types of investors and their asset allocations

• Fund selectors and the asset classes that interest them

• The distribution channels and how they are evolving

• High level regulatory information to get you started

• Prevailing market strategies

Poor operational infrastructure can be a drag on performance and service level. Since interdependencies exist between operational risk and other risk categories, operational failures tend to result in large losses. This is especially important since we are in an environment with increased regulatory requirements for operational risk. Our Investment Fund Centre has experience in performing ODD assessments for investors and has helped prepare asset managers for ODD requests in the APAC region.

A robust and well-designed distribution strategy should identify the specific requirements and best practices of each local target market for the funds you wish to institute. Our analysis of local markets and key distribution channels (whether direct or via partnerships), along with current best practices, will help you develop a distribution strategy that will maximise your opportunities for success.

Benchmarking studies in the fund industry act as an important tool for establishing, evaluating, and justifying inter-company transactions. In achieving these objectives, the Market Research team provides support in developing such benchmarking studies – as part of the tax documentation and fund structuring process, or to help build revenue models – while also performing sensitivity analysis to help assess the impact of your funds’ fee structure on your profitability. In ensuring the reliability and accuracy of our studies, we work with data from specialized databases provided by credited and established vendors within the industry.

Fund Flows

Customised benchmarking

comparison

What fund buyers are looking at

House Views

PwC’s monthly Market Research Digest aims to keep you up to date with not only the ongoings and happenings in the Asset and Wealth Management space in Asia Pacific, but also provide interesting and thought provoking views and analysis of trends in the industry.

Subscribe to get monthly updates through this QR code https://bit.ly/2s4hijH

Market Intelligence Country Digest

Operational Due Diligence (ODD) & Operational Due Diligence Readiness

Distribution Strategy

Benchmarking

Asset and Wealth Management Research Digest

Australia

Philippines

India

Taiwan

Malaysia

New Zealand

Hong Kong

South Korea

Japan

China

Singapore

Indonesia

Asian Investment Fund Centre

Market Mapping

Regulatory Rules

Budgeting

Distribution Models

Armin ChokseyPartner, Asian Investment Fund Centre & Market Research Centre LeaderPwC Singapore+65 6236 4648 [email protected]

© 2019 PricewaterhouseCoopers LLP. All rights reserved. “PricewaterhouseCoopers” and “PwC” refer to the network of member firms of PricewaterhouseCoopers International Limited (PwCIL), or, as the context requires, individual member firms of the PwC network. Each member firm is a separate legal entity and does not act as an agent of PwCIL or any other member firm.

Look out for our next issue of the AWM Market Research digest. Subscribe to receive future research digests at our website here: https://bit.ly/2s4hijH

Conal McMahonSenior Manager, Market Research CentrePwC Singapore+65 9678 [email protected]

Contacts