Audit partner and audit firm rotation and the assessment of internal control deficiencies

Brian C. Fitzgerald

Texas A&M University

Anne M. Thompson*

University of Illinois at Urbana-Champaign

Thomas C. Omer

Texas A&M University

April 26, 2012

Acknowledgments: We appreciate helpful comments and suggestions from Tim Bauer,

Kathleen Bentley, Colleen Boland, Tony Bucaro, Keith Czerny, Brad Lawson, Mark Peecher,

Brad Pomeroy, and Jaime Schmidt. We also thank Ryan Larkin, Will Lauer, and Wenyi Ying for

assistance with data collection.

*corresponding author ([email protected])

Audit partner and audit firm rotation and the assessment of internal control deficiencies

ABSTRACT: This study examines the effects of audit partner and audit firm rotation on the

reporting of internal control deficiencies. Auditor assessment of internal control deficiencies has

potential implications for planned audit test procedures. Further, auditor choices about whether

and how to report these deficiencies have the potential to revise the decision making of their

clients’ stakeholders. Thus, the empirical relation among the reporting of control deficiencies

and attributes of the auditor-client relationship may shed some light on the likely costs and

benefits of audit partner and audit firm rotation. Using a sample of audit reports issued for large

U.S. not-for-profit organizations between 2001 and 2007, we find a significant increase in

material weaknesses, reportable conditions, and audit findings reported in the first year of audit

firm tenure. While we find no significant association between audit partner changes and the

reporting of internal control deficiencies, we do find that partners are more likely to report audit

findings if their tenure exceeds five years. These results are consistent with an audit firm’s

investment in understanding and testing internal controls in their initial year of an engagement

leading to greater reporting of control deficiencies and with longer audit partner tenure leading to

an improvement in audit quality.

Keywords: Audit firm rotation, audit partner rotation, internal control, nonprofit organizations

Data Availability: All data used in this study is publicly available.

1

Audit partner and audit firm rotation and the assessment of internal control deficiencies

I. INTRODUCTION

This study examines the effects of audit partner and audit firm rotation on the reporting

of internal control deficiencies among large U.S. not-for-profit (NFP) organizations. Regulators

and standard setters in the U.S. and other financial markets frequently assert that auditor

independence and audit quality may decline over long auditor-client relationships (AICPA 1978,

GAO 2003, PCAOB 2011, House of Lords 2011, European Commission 2010) and many

countries (including the U.S.) now mandate audit partner rotation for public companies. Prior

research finds mixed evidence on the value of audit partner rotation in improving audit quality in

countries such as Australia and Taiwan (e.g. Carey and Simnett 2006; Chen et al. 2008; Carson

et al. 2012) and research on audit partner tenure and rotation in the U.S. is limited because audit

partner-level data is not generally available for public companies. Research on U.S. and

international public companies suggests lower audit quality in the early versus later years of

audit firm tenure due to less client-specific knowledge and greater reliance on management

representations (e.g. Gul et al. 2007; Myers et al. 2003; Johnson et al. 2002).

Understanding the effects of audit firm and audit partner rotation on the reporting of

internal control deficiencies is important because internal control assessment is an integral

component of the audit risk model, guiding the nature, timing, and extent of planned audit

procedures (SAS No. 47, AICPA 1983). For example, if the lack of client-specific knowledge

leads to over-reliance on a relatively weak control environment, the auditor may fail to detect a

material misstatement early in the tenure of the auditor-client relationship. Alternately, under-

reliance on controls by a new partner or new audit firm may lead to an inefficient audit program

and potentially increase the cost of audit firm and audit partner changes. In addition, the internal

2

control opinion included in the audit report may influence stakeholder decision making about

auditee organizations. Thus, understanding whether or how the detection and reporting of control

deficiencies varies with the auditor-client relationship is fundamental to understanding the costs

and benefits of audit partner and audit firm rotation.

Ex-ante, it is unclear whether or how either audit firm or audit partner rotation will affect

the detection and reporting of internal control deficiencies. Audit firm rotation introduces a

different audit methodology to the client and the additional planning effort in the initial year may

increase the likelihood of detecting internal control deficiencies. Audit firm rotation also brings a

“fresh look” to the client and may result in an increase in reported internal control deficiencies if

differences in professional judgment lead to different characterizations of control exceptions

detected by the predecessor auditor that were not reported in prior years. However, lack of client

familiarity may inhibit a new audit firm from obtaining the same depth of understanding of the

client’s control environment as the predecessor audit firm, which may offset the benefits of audit

firm rotation.

With respect to audit partner rotation, audit partners increase the extent of planned audit

procedures in their initial year on an engagement (Bedard and Johnstone 2010), suggesting that

audit partner rotation may result in improved detection and reporting of internal control

deficiencies. However, these incremental procedures may or may not exceed the benefits of

client-specific knowledge held by veteran audit partners. Also, audit firm methodology,

documentation, and other engagement personnel often are held constant surrounding audit

partner rotations (Bamber and Bamber 2009; Chi et al. 2009). Thus, whether audit firm and audit

partner rotation are associated with added detection and reporting of internal control deficiencies

is an empirical question.

3

We conduct our tests using audit reports issued for large not-for-profit organizations

(NFPs) between 2001 and 2007. In order to support compliance with applicable laws and

regulations and to ensure appropriate administration of federal funds, the federal government

imposes internal control attestation requirements under OMB Section A-133 for audits of federal

award recipients.1 A-133 audit reports issued for NFPs provide an advantageous setting to

examine our research questions for two reasons. First, the identity of both the audit firm and

engagement partner are observable, allowing us to separate the effects of audit firm change and

audit partner rotation. Second, A-133 audit reports disclose not just material weaknesses, but also

less severe internal control deficiencies that typically are not observable for public companies,

including reportable conditions (i.e. significant deficiencies) and audit findings (i.e. exceptions

identified in the controls and substantive testing over major program compliance).

We document a substantial increase in the reporting of material weaknesses, significant

deficiencies, and audit findings in the first year of the audit firm-client relationship. Specifically,

the rates of financial statement reportable conditions and material weaknesses nearly double in

the first year of audit firm tenure when compared to other years. We find little evidence that

audit partners rotating on to a client report internal control deficiencies with greater frequency

than in other years. However, audit partners with more than five years of experience on the same

client are significantly more likely to report audit findings and questioned costs, suggesting that

client-specific knowledge does improve the detection of less severe deficiencies and exceptions

in substantive testing. Finally, we find no decline in reported internal control deficiencies in the

last year of audit firm tenure, suggesting that our results are not attributable to a decline in the

predecessor auditor’ objectivity.

1 Office of Management and Budget (OMB) Circular A-133: Audits of States, Local Governments, and Nonprofit

Organizations (A-133), requires that all charitable organizations expending federal awards over a certain threshold,

currently $500 thousand, must be audited annually. See Section II for additional detail on the A-133 audit process.

4

Our study makes three main contributions. Our results suggest that an audit firm’s

investment in understanding the client’s control environment in the initial year of the

engagement leads to an increase in the reporting of internal control deficiencies. We

acknowledge that our results may be interpreted as suggesting that audit quality is higher in the

initial year of an engagement than in later years, in contrast to studies that document lower audit

quality in the initial year of audit firm tenure (e.g. Johnson et al. 2002; Myers et al. 2003; Gul et

al. 2007; Carcello and Nagy 2004). However, prior literature commonly relies on the auditee’s

accruals quality to assess audit quality over the term of the auditor-client relationship. This study

looks at a directly-observable output of the audit process and thus provides a more direct test of

how the audit process evolves over audit partner and audit firm tenure. Furthermore, because

recent studies link internal control quality to financial reporting quality (Doyle et al. 2007,

Ashbaugh-Skaife et al. 2008), our findings suggest that auditors’ additional investment in

internal control procedures during the initial year of the audit engagement may add value to

clients if the early remediation of detected internal control deficiencies improves financial

reporting quality in later years.

Second, we find no evidence in this setting suggesting that audit partner rotation provides

a “fresh look” resulting in an increase in reported internal control deficiencies similar to increase

documented for audit firm change discussed above. However, the results do support the notion,

at least in our context, that client-specific knowledge appears to improve audit quality.

Specifically, we provide initial evidence from the United States that audit partner tenure in

excess of five years, the limit imposed by the Sarbanes-Oxley Act for public company audits

(U.S. Congress 2002), is associated with greater reporting of audit findings. In addition, we find

5

that Big N audit partners with tenure exceeding five years are more likely to report material

weaknesses.

Finally, we contribute to the longstanding debate in the United States and other countries

concerning policies on audit firm rotation. Currently, no state or federal regulation requires NFP

entities to rotate audit firms, but many U.S. state and local governments require audit firm

rotation (Zeff 2003). However, because many states regulate the governance of NFP

organizations similarly to the regulation of public companies (Iyer and Watkins 2008; Petrovits

et al. 2011), actions taken by the PCAOB concerning auditor rotation may affect the NFP sector.

It is unclear how closely our findings in the NFP sector would generalize to SEC registered

companies or to enterprises in other countries due to differences in the reporting objectives and

client risk. But, similarities in the audit methodology and training of engagement personnel

across public company and NFP engagements suggest that these findings may be useful to

standard setters in evaluating the costs and benefits of audit firm and audit partner rotation in

other sectors of the U.S. and global economies.

This paper proceeds as follows: Section II provides background information and develops

our hypotheses. Section III outlines our research design. Section IV presents the results of our

empirical tests and Section V concludes.

II. BACKGROUND INFORMATION AND HYPOTHESIS DEVELOPMENT

Background Information on the NFP Sector and A-133 Audit Reports

The NFP sector comprises a significant portion of the U.S. economy. NFP organizations

contribute 5% of GDP and employ 10% of the U.S. workforce (IRS 2010; NCCS 2011). The

GAO estimates that at least $235 billion in federal funds reached the NFP sector in 2006 and

NFPs benefitted from $50 billion in foregone federal income tax payments due to the tax

6

advantaged status of the NFP sector (GAO 2009). The growth in the NFP sector has attracted

scrutiny from both the GAO and U.S. Congress because NFPs face fewer regulations than

taxable organizations and there are documented cases of some NFPs exploiting their tax-exempt

status to earn economic rents at the expense of their for-profit counterparts (GAO 2002; GAO

2008b; Grassley 2006; Grassley 2010; Carreyrou and Martinez 2008).

Under the guidelines of the Office of Management and Budget (OMB) Circular A-133:

Audits of States, Local Governments, and Nonprofit Organizations (A-133), all charitable

organizations expending federal awards over a $500 thousand threshold, must be audited

annually. The auditor’s report includes a financial statement audit, an evaluation of the entity’s

internal controls, and an assessment of the organization’s use of federal funds in compliance with

applicable laws and regulations. 2, 3

Donors, granting agencies, and other stakeholders use A-133

audit reports to assess whether the NFP’s funds were used in accordance with the NFP’s stated

mission and donors’ intentions. NFPs face negative financial consequences to non-compliance

(Keating et al. 2005) and donations and government grants decrease after the disclosure of an

internal control problem (Petrovits et al. 2011) or the receipt of a going-concern opinion (Feng

2010).

Although A-133 audit reports provide information to various stakeholders, the quality of

the auditors’ testing to support these opinions has repeatedly been called into question (GAO

2 During an A-133 audit, the auditor must evaluate the nonprofit’s internal controls separately for financial reporting

and for major programs. Section .520 of A-133 provides quantitative and qualitative guidance on which federal

programs are to be classified as major programs for the NFP. The auditor must designate as major programs at least

50 percent of the total federal awards received by the auditee; 25 percent for nonprofits designated as ‘low risk’

(OMB 2007). Refer to the definition of the LOWRISK variable in Appendix A for additional information on the

‘low risk’ designation.

3 A deficiency identified during internal control testing can be a ‘reportable conditions’ or ‘material weaknesses.’

Effective June, 26, 2007, A-133 was revised to redefine a ‘reportable condition’ finding as a ‘significant deficiency.’

A-133 refers to generally accepted auditing standards for the definition of ‘significant deficiency’ and ‘material

weakness’ (OMB 2007). SAS No. 115 aligns the definitions of ‘significant deficiency’ and ‘material weaknesses’

with the definitions included in Auditing Standard No. 5 issued by the PCAOB.

7

2008a; GAO 2002; Ramen and Wilson 1992). In June 2007, the President’s Council on Integrity

and Efficiency (PCIE) issued a report summarizing the findings of the National Single Audit

Sampling Project (PCIE 2007). The study concluded that 35 percent of A-133 audits are of

unacceptable quality. The most commonly identified problems included failure to sufficiently

document or test the NFP’s internal controls, suggesting that internal control deficiencies are

likely under-reported in NFP sector. The federal government places significant reliance on

entities’ internal controls to support compliance and appropriate administration of federal

awards, thus the failure to document and test controls raises concerns about the overall quality of

audits of among NFP entities.

Hypothesis Development

Prior research commonly defines audit quality as the joint probability that the auditor

detects and reports a material misstatement in the client’s financial reporting (DeAngelo 1981).

The auditor’s ability to detect misstatements is influenced by the auditor’s assessment of inherent

risk and the client’s control risk because these factors guide the nature, timing, and extent of

planned audit procedures in the audit risk model (AICPA 1983). Conceptually, a material

misstatement implies a weakness in the control environment (Kinney and McDaniel 1989; López

and Peters 2010; Rice and Weber 2012). This link is supported by audit work paper studies

connecting weaknesses in the control environment to financial reporting misstatements. (See

Eilifsen and Messier 2000 for a review.) In addition, recent evidence from public companies

suggests a negative relationship between financial reporting quality and the likelihood of

disclosing a weakness in internal controls (Doyle et al. 2007; Ashbaugh-Skaife et al. 2008).

Taken together, these studies suggest that the detection and reporting of internal control

deficiencies is an important dimension of audit quality.

8

Our first hypothesis examines the association between audit firm changes and reported

internal control deficiencies. Professional standards require auditors to obtain an understanding

of the client’s internal control environment sufficient to plan the audit (AU 319). The procedures

employed by auditors to obtain this understanding vary with factors including previous

experience with the entity (AU 319 .26). Further, standards governing initial audit engagements

state that “the auditor may need to expand the planning activities because the auditor does not

ordinarily have the previous experience with the entity that is considered when planning

recurring engagements” (AU 311 .26).

Prior research suggests that audit hours are significantly higher in the initial year of the

audit firm-client relationship (Caramanis and Lennox 2008; Deis and Giroux 1996).

Furthermore, Johnstone and Bedard (2001) find no difference in initial-year audit effort for

governmental/NFP audit clients and for other clients. If a new audit firm makes a substantial

audit effort investment to understand a new client’s internal control environment, the audit firm

may identify previously unreported internal control deficiencies in the initial year of the audit

engagement. In this case, we would expect an increase in reported internal control deficiencies

immediately following an audit firm change.

We may also observe an increase in reported internal control deficiencies immediately

following an audit firm change if the predecessor audit team is less likely to report internal

control deficiencies as tenure increases due to the potential loss of auditor objectivity over time.

Experimental research suggests that escalation of commitment is common to situations where the

decision maker has responsibility for prior decisions that are perceived to be irrevocable. During

evidence acquisition, auditors tend pay more attention to information that is consistent with

previous assessments, which may cause auditors to be less likely to detect potential audit issues

9

(Tan 1995). During evidence evaluation, auditors tend to remain committed to their initial

decisions, despite subsequent evidence contrary to their original assessments, which may cause

auditors to be less likely to report potential audit issues (Jeffrey 1992; Brody and Kaplan 1996).

In internal controls testing, a setting that exhibits substantial variation in judgment,4 this bias

may be particularly problematic if the auditor identifies a new deficiency in a process unchanged

from the prior year because the identification of the new deficiency calls into question the quality

of the prior-year’s internal control testing. For these reasons, escalation of commitment by the

predecessor auditors also suggests that audit firms may be more likely to report internal control

deficiencies in the initial year of audit firm tenure.

However, the new audit firm may be at an informational disadvantage due to less client-

specific knowledge, forcing auditors to place greater reliance on estimates and representations

made by the client.5 Prior research examining U.S. for-profit companies document lower audit

quality in the initial years of audit firm tenure, followed by an improvement in audit quality in

later years (Johnson et al. 2002; Geiger and Raghunandan 2002; Myers et al. 2003; Carcello and

Nagy 2004). These studies suggest that audit teams gain client-specific knowledge that enables

them to better identify their clients’ unique financial reporting risks and objectively evaluate

their clients’ accounting choices. Consistent with this explanation, Gul et al. (2007) document

that accruals quality is lower in the early years of audit firm tenure among clients of non-industry

specialists, when compared to accruals quality among clients of industry specialists. In addition,

Srinidhi et al. (2010) report that accruals quality increases with long audit firm tenure only for

4 Trotman and Wood’s (1991) meta-analysis of internal control judgments reports a mean correlation of 0.629

between internal control judgments and the studies’ independent variables of interest, which suggests that substantial

variation remains unexplained by the studies’ proposed moderating relationships. 5 Palmrose (1991) concludes that audit firms have a higher chance of litigation for negligent audits during the early

years of the professional engagement period.

10

clients that require a high degree of client-specific knowledge. If an NFP’s auditor requires a

high degree of client-specific knowledge to effectively evaluate the NFP’s internal control

environment, we expect audit teams to be better able to identify internal control deficiencies as

audit tenure increases. In this case, we would expect lower likelihoods of reported internal

control deficiencies in the initial years of the audit firm-client relationship.

Because it is unclear whether the additional procedures performed in the initial year of

the audit engagement will offset the lack of client-specific knowledge and whether escalation of

commitment effects the predecessor audit team members’ evaluation of internal controls, we

state our first hypothesis in the null form:

H1: Audit firms are no more likely to report internal control deficiencies in the initial

year of audit firm tenure.

Our second and third hypotheses examine whether audit partner rotation and tenure are

associated with reported internal control deficiencies. Regulators in the U.S. and other countries

argue that audit partners develop relationships with their clients over time that may compromise

auditor independence and impair audit quality. Thus, audit partner rotation should bring a “fresh

look” to the engagement. Using proprietary data from a large accounting firm, Bedard and

Johnstone (2010) report that planned audit effort increases following audit partner rotation,

suggesting that new audit partners invest in gaining client-specific knowledge in their first year

on engagements. If the expanded procedures performed by new audit partners provide a new

assessment of the client, we expect that the likelihood of an internal control deficiency disclosure

to increase in the year of audit partner rotation.

However, audit partner rotation may not increase the likelihood of reporting internal

control deficiencies. U.S. audit partners report that at least two years of client-specific experience

is necessary to gain familiarity with a client (Daughtery et al. 2012), suggesting that rotation may

11

not immediately improve audit quality. In addition, much of the client-specific knowledge is

retained through reference to the prior-year work papers and in the established audit

methodology. Further, many members of the audit team are not required to rotate periodically.

Thus the new audit partner may not bring a truly “fresh look” to the engagement, which may

limit the improvement in independence and audit quality related to audit partner rotation

because, although new audit partners are potentially more independent than rotated partners, they

may rely heavily on existing staff and work papers, which may keep the likelihood of reporting

internal control deficiencies unchanged (Bamber and Bamber 2009; Chi et al. 2009). Finally,

Carson et al. (2012) find that, although audit quality is higher in the two years following both

audit partner and audit firm changes in Australia, the effect of audit firm change dominates the

effect of audit partner rotation. Because the evidence on the effectiveness of audit partner

rotation is inconclusive, we state our second hypothesis in the null form:

H2: Audit partners are no more likely to report internal control deficiencies in the initial

year of audit partner tenure on a continuing client.

Our third hypothesis examines the association between audit partner tenure and the

reporting of internal control deficiencies. As discussed previously, regulators argue that audit

partner objectivity may decline over time. However, because independence is critical to the value

of attest services, audit partners have strong incentives to maintain their professional skepticism

(POB 2000). As such, any potential benefit to the audit partner derived from an impairment of

judgment may be negated by the potential cost to one’s professional reputation (DeAngelo

1981). Because audit partners with longer client relationships amass greater reputational capital

through successive audits, opponents of auditor rotation suggest that reputation protection likely

mitigates any reduction in independence that might occur over time. However, as discussed in

12

the motivation of H1, cognitive biases may limit the audit partner’s ability to detect and report an

internal control weakness as audit partner tenure increases. Prior research in non-U.S.

jurisdictions yields mixed evidence on the association between audit partner tenure and audit

quality. Although evidence from Australia suggests that audit quality declines with audit partner

tenure (Carey and Simnett 2006; Ye et al. 2011; Carson et al. 2012), studies from other countries

suggest either no association between audit partner tenure and audit quality (e.g. Knechel and

Vanstraelen 2007) or an improvement in audit quality as audit partner tenure increases (e.g. Chen

et al. 2010). For U.S. for-profit companies, Gul et al. (2009) and Lim and Tan (2010) suggest

that longer audit firm tenure is associated with higher accruals quality for companies audited by

specialist audit firms, who also have higher levels of reputational capital to protect. Because it is

unclear whether reputation protection concerns, as evidenced by U.S. research at the audit firm

level, sufficiently mitigates the potential loss of independence over time, we state our third

hypothesis in the null form:

H3: Audit partners are no more likely to report internal control deficiencies on clients

with longer partner tenure.

III. RESEARCH DESIGN

Sample Selection

To construct our sample, we begin by identifying NFP entities with available data in both

the Federal Audit Clearinghouse database of OMB Section A-133 audit reports and the IRS

Statement of Income (SOI) files maintained by the National Center for Charitable Statistics

(NCCS). The SOI files include financial statement and organizational data on nonprofit entities

from IRS Form 990 informational tax returns. The SOI files are compiled annually and include

data from large NFPs (total assets exceeding $30 million) and a stratified random sample of

13

smaller NFP organizations.6 The A-133 database includes financial statement auditor and audit

opinion information for nonprofits expending a minimum threshold of federal awards during the

year.7

Our sample period spans the 2000 through 2007 tax years. The IRS made significant

changes to the Form 990 for the 2000 and 2008 filing years, thus the information reported on the

Form 990 is more comparable between 2000 and 2007 than in the years prior to 2000 or in 2008

(Feng et al. 2011).8 In addition, 1997 is the earliest year in the A-133 database, therefore

beginning the sample earlier than 2000 would limit our ability to measure audit partner tenure for

observations in our sample. We exclude NFP entities missing three or more years of data in both

files during our sample period because we cannot reliably measure audit firm and partner

changes for observations missing multiple years of data in the A-133 database. In addition,

entities missing multiple years may not consistently expend the minimum threshold of federal

funds to require an A-133 audit, or they may have severe difficulties meeting these compliance

requirements. Finally, the control and compliance environments may differ systematically

6 Our sample size is smaller than studies that use the IRS Core files (e.g. Petrovits et al. 2011; Tate 2007). The IRS

Core files contain a limited number of financial statement variables (approximately 150 data items total) for a large

number of organizations. In contrast, the SOI files include more than 400 data items during our sample years for

large NFPs and a stratified random sample of smaller NFP organizations. Accordingly, the differences in sample

composition between our study and other studies are in the proportion of smaller NFP organizations. Our interest

lies in the larger organizations because we expect greater complexity and stronger internal control environments

among these organizations. Consistent with this expectation, 98.6% of A-133 audits in the SOI files received

unqualified financial statement audit opinions compared to 90.1% of other audits. For financial statement reportable

conditions (material weaknesses), the differences are 15.6% (5.1%) for observations with SOI file data versus 24.4%

(10.9%) for other observations. The proportion of going concern report modifications is the same in both samples

(0.08%).

7 During our sample period, the minimum threshold was $300,000 in annual federal expenditures prior to 2004 and

$500,000 in annual federal expenditures in 2004 onward.

8 2008 was the last available year at the time we collected our data in September 2011 because SOI files are

released, on average, three years after the filing year has ended. Our inferences are unchanged when including 2008

in the sample.

14

between NFPs with and without annual A-133 audits due to differences in federal expenditures

and inconsistency in applying the Single Audit Act compliance requirements.

The SOI files contain 192,241 NFP observations from 2000-2007. Of these, 22,936

observations include auditor and audit opinion information in the A-133 database. We eliminate

3,809 observations for entities missing three or more years of data in both files, and exclude 236

observations due to missing or incorrect audit partner information. Our selection model requires

two consecutive years of data; therefore we exclude year 2000 observations from our main

analysis, and eliminate 1,140 observations due to missing consecutive years of data during the

sample period. Our final sample consists of 15,664 observations with tax return filing years

2001-2007. These sample selection procedures are outlined in Table 1.

[INSERT TABLE 1 HERE]

Measuring Audit Firm and Audit Partner Changes

We identify audit firm and audit partner changes by examining consecutive years of audit

reports in the A-133 database. We classify a NFP organization as changing audit firms if the

financial statement auditor in year t is not the same as the auditor in year t-1 (CHANGEFIRM).

We review all audit firm changes by hand and reclassify CHANGEFIRM to equal zero if the

change in auditor name is due to a firm name change or merger of two public accounting firms.

We identify the audit partner as the individual listed in the field CPACONTACT. As

discussed previously, we exclude observations if the field CPATTITLE indicates that the contact

holds a position other than partner or equivalent position in their firm.9 We classify an NFP as

changing audit partners in year t when CHANGEFIRM equals zero and the audit partner in year t

9 We consider positions such as “owner,” “shareholder,” “managing director,” “principal,” “vice-president,”

“proprietor,” or any position that includes the word partner as a partner-equivalent position. We exclude

observations where the CPATITLE field indicates senior manager, senior associate, audit manager, or staff. We also

exclude A-133 audit reports issued by the Defense Contract Audit Agency because the financial statement audit firm

and partner information is not observable for these NFPs.

15

is not the same as in year t-1 (CHANGEPARTNER).10

We calculate audit partner tenure as the

number of years the partner has been listed as the signing partner in the A-133 database as of

year t and classify partners as having short (1-2 years), medium (3-5 years), or long (6 or more

years, LONGTENURE) of tenure on the client as of year t.11

Multivariate Model

We estimate the following model of the joint detection and reporting of internal control

deficiencies in the auditor’s report:

Control Deficiency is a variable equal to one if the auditor reports one of the following

conditions: financial statement reportable condition (FS_RC) or material weakness (FS_MW), a

major program reportable condition (MP_RC) or material weakness (MP_MC), or an audit

finding or questioned cost (FINDORQ), and equal to zero otherwise.12

Our primary independent variables are CHANGEFIRM, CHANGEPARTNER, and

LONGTENURE as defined previously. We follow Petrovits et al. (2011) in controlling for

10

We observe 57 cases of clients following an audit partner to a new public accounting firm. 24 of these cases are

due to Andersen clients following a partner to a new audit firm between 2001 and 2002. We treat these observations

as firm changes because of differences in the audit methodology and quality control procedures between the

predecessor and successor firm. Excluding these observations from our sample has no effect on our inferences.

11

The earliest year of data in the A-133 database is 1997. Therefore, we cannot observe or measure audit firm

tenure prior to an audit firm change. Per discussion with practitioners, many firms maintain policies of audit partner

rotation after 7 years for non-SEC clients, therefore examining observations in 2003 onward may provide clearer

inferences concerning the role of longer partner tenure on internal control deficiency identification and reporting.

Our inferences are the same examining only 2003 onward.

12

We cannot determine the number or nature of control deficiencies reported from the A-133 database because the

Data Collection Form submitted to the Census department does not include these fields.

16

determinants of internal control weaknesses in NFP organizations:13

COMPLEXITY equals the

number of revenue sources listed on Form 990 (public support, government contributions,

program revenue). SURPLUS equals one if the client reported revenues in excess of expenses

during year t and equals zero otherwise. GCAR equals one if the prior-year audit report included

a going concern modification and equals zero otherwise. ASSETSIZE equals the natural log of

total assets reported at the end of year t and GROWTH equals the growth rate in total assets over

the prior year (Line 59 Column B divided by Line 59 Column A). LOWRISK equals one if the

client qualifies as low risk under Section .530 of the Single Audit Act. NFPs do not qualify for

low risk status if the auditor reported a material weakness or a finding or questioned cost in the

prior year.14

We control for audit firm size with indicator variables equal to one if the audit firm is a

Big N firm (BIGN), a second tier firm, or a NFP industry specialist. We define a second tier firm

(SECTIER) as one of the largest 30 public accounting firms other than the Big 4 per the Public

Accounting Report in 2007, the last year of our sample. We define a NFP industry specialist as a

public accounting firm other than a BIGN or SECTIER firm that performed at least 50 audits in

our sample (SPECIALIST). Finally, we determine whether the audit firms in our sample are

registered with the PCAOB per Audit Analytics and review of the PCAOB website listing of

registered firms as of September 2011. We include an indicator variable OTHERPCAOB equal to

one if the public accounting firm is registered with the PCAOB but not otherwise categorized as

a BIGN, SECTIER, or SPECIALIST firm.

13

We exclude one variable from the Petrovits et al. (2011) model. Their model includes NEWGRANTEE, an

indicator variable equal to one in the first year an organization expends federal funds. We exclude all first-time A-

133 audits from our sample because we cannot observe changes in audit firms or audit partners for new grantees

Therefore, NEWGRANTEE equals zero for all observations in our sample by construction.

14

Refer to Appendix A for further criteria on the LOWRISK designation.

17

We augment the Petrovits et al. (2011) model for audit-specific factors that may influence

the audit firm’s detection and reporting of internal control deficiencies. Because audit resources

expended (audit hours and staffing mix) may affect the detection and reporting of internal control

deficiencies, we include fees paid for outside accounting services as a proxy for audit fees.15

LNACCTFEES equals the natural log of total accounting fees paid in year t (line 31, column A).

We include LAGPROBLEM because the prior-year audit report is available to the audit firm and

the existence of internal control deficiencies or a modified opinion in the prior year may

influence planned audit procedures in the current year. LAGPROBLEM is equal to the sum of the

number of problems reported in the prior year including financial statement or major program

reportable conditions or material weaknesses, going concern audit reports, audit opinion

qualifications, material non-compliance findings, and questioned costs (Tate 2007).

NFPs issuing tax-exempt debt may pose greater litigation risk to the audit firm, and these

NFPs may be subject to greater monitoring or compliance requirements from bondholders and

external financing authorities. Therefore, we control for leverage at the end of year t

(LEVERAGE, Line 64a, Column B divided by Line 59, Column B). Next, we control for the

number of employees because low headcount may constrain NFPs’ abilities to effectively

segregate duties and implement manual control procedures. LNEMPLOYEES equals the natural

log of the number of employees paid greater than $30,000 during the year that are not among the

five highest paid employees (Schedule A, Part 1). Finally, we include an indicator variable equal

to one if the NFP engaged in lobbying activities during the year (LOBBY, Schedule A line 37b).

We include indicator variables for year and industry and cluster standard errors by entity

15

Auditor litigation risk for NFP organizations is low. Accordingly, we expect that the risk premium component of

audit fees for NFPs is low.

18

identifier (EIN). Finally, we winsorize all continuous variables at 1 and 99 percent to reduce the

influence of outliers.

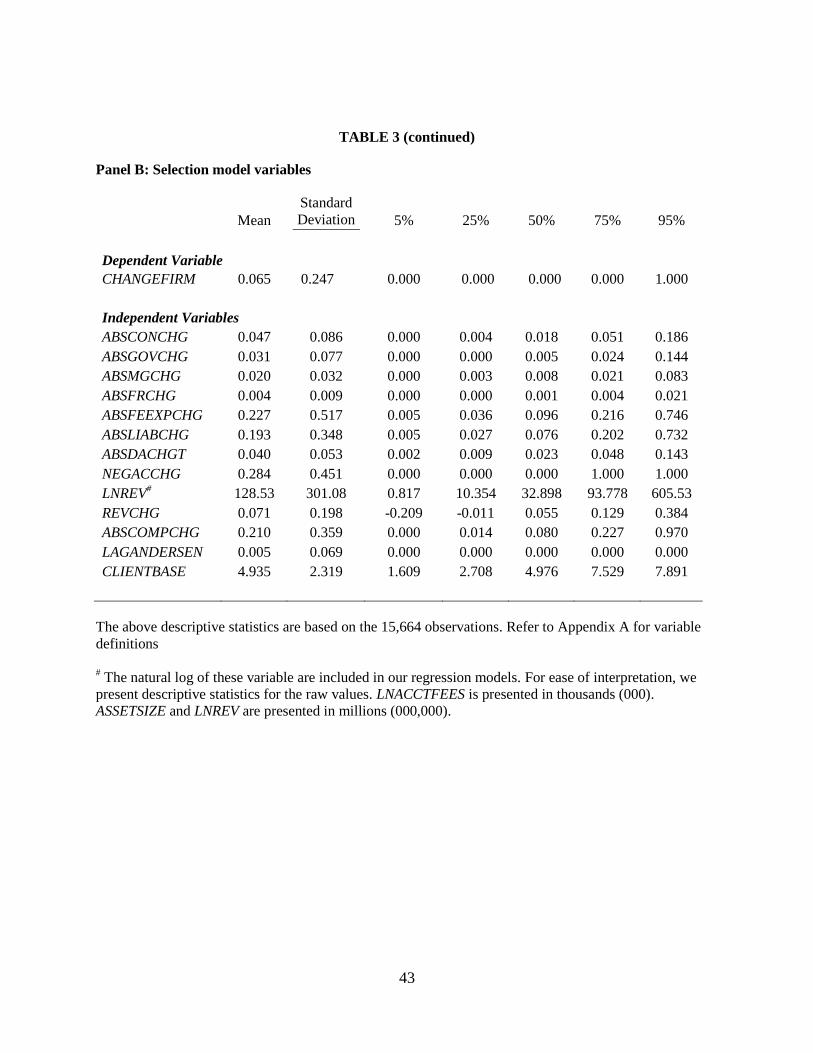

Selection Bias

Because prior research suggests that public companies are more likely to change auditors

following an adverse internal control opinion (Zhang et al. 2007; Ettredge et al. 2011), the

decision to terminate the auditor-client relationship likely does not arise randomly in our sample.

We control for possible selection bias arising from auditor changes using the Heckman

maximum likelihood estimation method (Heckman 1979). We follow Tate (2007) and estimate

the following model:

Where auditor changes among NFP organizations (CHANGEFIRM) is modeled as a function of

the absolute value change from year t-1 to year t in total contributions (ABSCONCHG),

government funding (ABSGOVCHG), management and general expenses (ABSMGCHG),

fundraising expenses (ABSFRCHG), federal expenditures (ABSFEEXPCHG), total liabilities

(ABSLIABCHG), leverage (ABSDACHG), and executive compensation (ABSCOMPCHG). In

addition, the Tate (2007) model includes the natural log of total revenues in year t (LNREV), the

change in revenue from year t-1 to year t (REVCHG), and an indicator variable equal to one if

total accounting fees declined from year t-1 to year t (NEGACCHG).

We also include an indicator variable equal to one if the predecessor auditor was a Big N

auditor (LAGBIGN) an indicator variable equal to one if the predecessor auditor was Arthur

19

Andersen (LAGANDERSEN), and the auditor’s client base, calculated as the natural log of the

number of audit opinions issued during the year by the audit firm (CLIENTBASE). We include

all control variables from the second stage model discussed previously, as well as indicator

variables for year, state, and industry. The discriminatory power of the model is acceptable

(ROC = 0.786). Finally, we perform multi-collinearity diagnostics for all second stage models

and confirm the stability of the coefficient estimates (Belsley et al. 1980).

IV. EMPIRICAL RESULTS

Descriptive statistics

Table 2 presents descriptive and univariate statistics for internal control deficiencies and

for audit finding and questioned costs (collectively referred to as audit findings). Table 2, Panel

A presents reported internal control deficiencies and audit findings for clients in the year of an

audit firm change, an audit partner change, and no change of firm or partner. We identify no

differences in either reportable conditions or material weaknesses between NFPs changing audit

partners since the prior year and NFPs with no changes during the year. NFPs changing audit

firms report internal control deficiencies at significantly higher rates than NFPs changing only

audit partners. Twenty five percent of NFPs changing audit firms report a financial statement

reportable condition as compared to 14 percent of NFPs with an audit partner rotation (p<0.01).

The rates of financial statement and major program material weaknesses among NFPs changing

audit firms (9 and 6 percent respectively) are double the rates of material weaknesses among

NFPs with a new audit partner (4 and 3percent respectively, both p<0.01).

We find higher rates of findings or questioned costs when NFP clients experience a

partner change (28 versus 24 percent, p<0.01) and higher rates of findings and questioned costs

among NFP clients with a new audit firm than a new audit partner (33 versus 28 percent,

20

p<0.01). The increase in reported audit findings and questioned costs following an audit partner

change are consistent with audit partners increasing planned audit procedures in their first year

on a continuing client (Bedard and Johnstone 2010). However, our findings suggest that this

increase in planned audit procedures does not result in an increase in detection and reporting of

more severe internal control deficiencies.

[INSERT TABLE 2 HERE]

Table 2, Panel B presents reported internal control deficiencies and audit findings by

audit partner tenure and audit firm size. Generally, the percentage of audit reports with internal

control deficiencies and audit findings is higher among audits with short firm or partner tenure,

consistent with the findings in Panel A. Among Big N NFP clients, the rates of internal control

deficiencies are similar across short, medium, and long audit partner tenure, although Big N

auditors report findings and questioned costs more frequently among NFPs with long partner

tenure (40 percent of long partner tenure NFPs, 35 percent of short and medium partner tenure

NFPs). In addition, Big N auditors report financial statement reportable conditions and material

weaknesses less frequently than other auditors, consistent with these NFPs maintaining stronger

internal control over financial reporting. PCAOB registered audit firms report internal control

deficiencies and audit findings more frequently than non-PCAOB registered firms, however the

rate of material weakness disclosures are comparable between PCAOB and non-PCAOB

registered audit firms. We expect that clients of non-PCAOB registered audit firms are smaller

and maintain weaker internal control environments; therefore the results suggest lower audit

quality among non-PCAOB registered auditors.

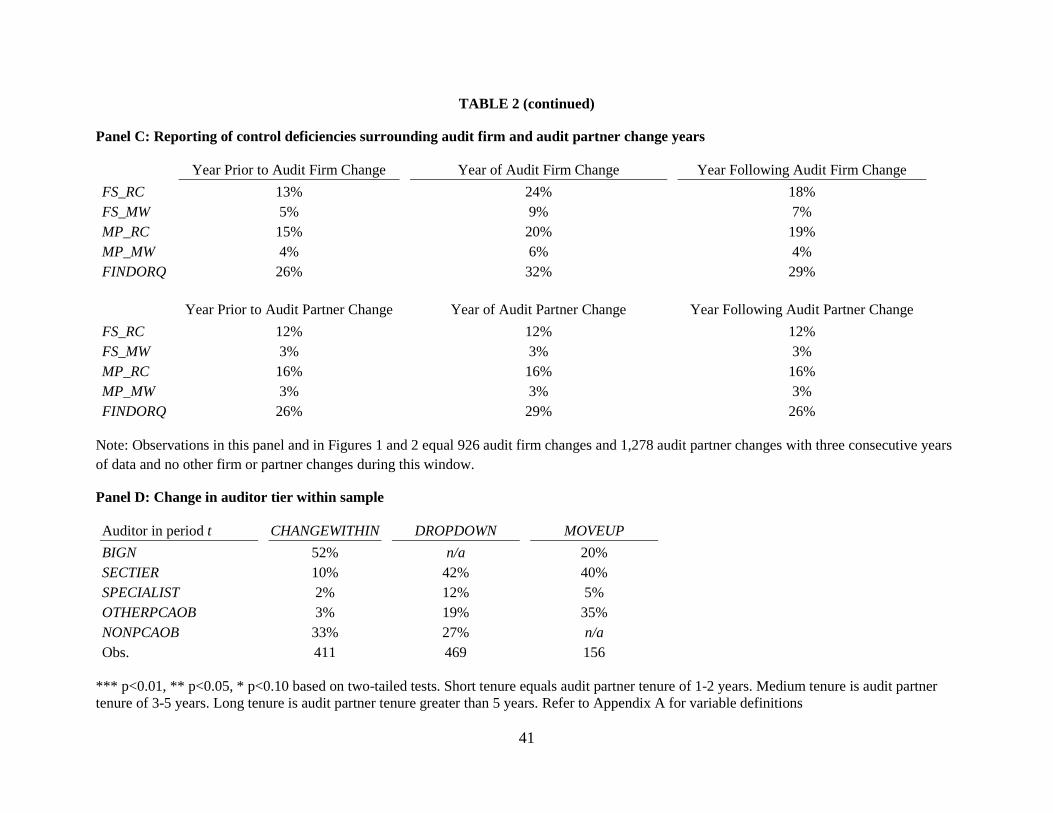

Table 2, Panel C presents the rates of internal control deficiencies in the three years

surrounding audit firm and audit partner changes. Figures 1 and 2 present these findings

21

graphically. The percentage of audit reports disclosing reportable conditions and material

weaknesses is higher in the year of an audit firm change than in the prior year or subsequent

year. Twenty four percent of audit reports disclose a financial statement reportable condition in

the year of an audit firm change, compared to 13 percent in the year prior to the change and 18

percent in the year following the change. We identify a similar pattern for financial statement

material weaknesses, for major program reportable conditions and material weaknesses, and for

audit findings. We identify no changes in reportable conditions or material weaknesses

surrounding audit partner changes, although reported findings and questioned costs are more

frequent in the year of an audit partner change than the surrounding years (29 percent in the year

of change versus 26 percent in the prior and subsequent years). These descriptive statistics

suggest that the increase in reported internal control deficiencies surrounding audit firm changes

observed in Table 2, Panel A reflects a one-time reporting difference, as the rates of reported

internal control deficiencies are comparable in years t-1 and t+1. Finally, Table 2, Panel D

tabulates the observed frequency of audit firm changes within the same audit firm size tier versus

dropping down or moving up in the audit firm tier.

Table 3 presents descriptive statistics for the variables used in the multivariate regression

analysis. Table 3, Panel A presents descriptive statistics for the main regression model. The

primary variables of interest are consistent with those reported in Table 2, Panel A. Six percent

of observations changed audit firms since the prior year, 12.7 percent changed audit partners

since the prior year, and 27 percent of observations are characterized by long audit partner tenure

(greater than five years). The mean (median) client in our sample reports $246 ($59.9) million in

total assets and employs 1,166 (333) employees earning greater than $30,000 per year. Table 3,

Panel B presents descriptive statistics for the selection model.

22

[INSERT TABLE 3 HERE]

Multivariate Results

Table 4 presents probit regression coefficient estimates for the audit firm change

selection model. The discriminatory ability of the model is adequate (ROC=0.786, Pseudo R-

Square=0.243). The inferences for this model are generally consistent with Tate (2007) even

though our sample is estimated using a different time period (2001-2007 versus 1997-2003) and

excluding smaller entities because of the differences in the SOI versus CORE files.

[INSERT TABLE 4 HERE]

Table 5 presents coefficient estimates for our logistic regression models examining the

association between audit firm and audit partner changes on reported control deficiencies and

audit findings. Across all five dependent variables, the coefficient for CHANGEFIRM is positive

and significant at p<0.05, indicating that changing audit firms is associated with higher odds of

reported internal control deficiencies and audit findings. The coefficients for

CHANGEPARTNER are not significant in any of these models. The coefficient for

LONGTENURE is positive and significant when the dependent variable equals FINDORQ

(p<0.01), suggesting that greater familiarity with the NFP increases the likelihood of reporting

audit findings and questioned costs. The discriminatory power of these models range from

adequate (ROC between 0.70 and 0.80) to excellent (ROC between 0.80 and 0.90) and confirm

model fit using goodness of fit test statistics.

[INSERT TABLE 5 HERE]

Table 6 presents coefficient estimates by audit firm size. Table 6, Panel A, presents

coefficient estimates for CHANGEFIRM, CHANGEPARTNER, and LONGTENURE when the

dependent variable equals FS_RC. The coefficient for CHANGEFIRM is positive and significant

for Big N, second tier, and specialist audit firms at p<0.01 and for other PCAOB registered firms

23

at p<0.10. The coefficients for CHANGEFIRM are not significant for other non-PCAOB

registered audit firms. Table 6, Panel B presents similar findings with FS_MW as the dependent

variable. In addition, the coefficient on LONGTENURE is positive and significant for Big N

clients, suggesting that longer relationships between the client and engagement partner are

associated with higher odds of reporting a material weakness. Because NFP client familiarity

may be low in the initial year of the engagement, these findings suggest that larger audit firms

are better able to overcome the lack of client-specific knowledge in evaluating their clients’

internal control environments.

[INSERT TABLE 6 HERE]

Table 7 presents our analysis partitioning CHANGEFIRM by changes in audit firm size

tier. This analysis provides evidence on the role of changes in audit firm size on internal control

deficiency detection and reporting.16

We separate audit firm changes into changes within audit

firm size tier (CHANGEWITHIN), changes from a larger to smaller audit firm size tier

(DROPDOWN) and changes from a smaller to larger audit firm size tier (MOVEUP). For

purposes of this analysis, audit firm size is ranked from largest to smallest as BIGN, SECTIER,

SPECIALIST, OTHERPCAOB, and other audit firms not registered with the PCAOB.17

We find

positive and significant coefficients on CHANGEWITHIN and MOVEUP for all 5 models,

however these results are driven by Big N and second tier audit firms and generally we do not

find significant coefficients for SPECIALIST and other audit firms (untabulated). Next, we find

16

Our selection model includes controls for auditor selectivity in terminating the auditor-client relationship. We

note that, although auditor selectivity for publicly traded companies was high during some years of our sample (due

to audit demand constraints imposed by implementation of the internal controls attestation requirements of the

Sarbanes-Oxley Act of 2002), NFP clients pose significantly lower litigation risk to an audit firm. Also, these clients

generally do not report as of December 31 and, therefore, are useful to the auditor for increasing utilization during

periods characterized by lower billable hours. Our conversations with practitioners confirm these expectations

regarding the frequency of audit firm changes due to selectivity among NFP clients during our sample period.

17

We recognize that many specialist audit firms are not PCOAB registrants.

24

that, among SPECIALIST audit firms, the coefficient on DROPDOWN is negative and significant

(p<0.05) for FS_MW, MP_RC, and MP_MW, indicating that these audit firms are significantly

less likely to detect and report these types of severe internal control deficiencies for new NFP

clients that were previously audited by larger audit firms. Finally, the inferences for

CHANGEPARTNER and LONGTENURE are consistent with our prior analysis.

[INSERT TABLE 7 HERE]

Overall, these findings consistently indicate that audit firms are significantly more likely

to detect and report severe internal control deficiencies for new NFP clients, and that this result

is strongest among Big N and second tier audit firms. We also observe that audit firms are more

likely to report audit findings and questioned costs when audit partner tenure is greater than five

years, suggesting that, among NFP clients, the acquisition of client-specific knowledge may

improve the detection and reporting of audit findings.

Supplemental Analysis

As discussed previously, new audit firms may be more likely to report internal control

deficiencies in the initial year if the predecessor auditor either did not detect existing internal

control deficiencies or assessed known internal control deficiencies to be less severe than the

successor auditor. In addition, it is possible new audit partners may not provide a “fresh look” if

the practitioner has previous experience with the client. Table 8 presents additional analysis to

examine these two possibilities. First, we determine whether the audit partner has prior client

knowledge by examining whether a partner rotating onto the client signed an audit opinion for

the same NFP client in the eight previous years.18

We separate CHANGEPARTNER into two

variables – CHANGEPARTER_EXP to denote prior experience with the client and

18

We do not identity any audit partners rotating back onto a client with a lag greater than eight years although our

ability to observe audit partner identity is limited to the years since 1997.

25

CHANGEPARTNER_NOEXP to denote no prior experience with the client. We then examine the

effect of prior client knowledge on the joint detection and reporting of FS_RC, FS_MW, and

FINDORQ. In Table 8, Panel A, the coefficient for CHANGEPARTNER_EXP is positive and

significant (p<0.05) when the dependent variable is FS_RC, indicating that audit partners

rotating back onto a client are significantly more likely to report a reportable condition.

However, audit partners rotating back onto a client are no more likely to report financial

statement material weaknesses, findings or questioned cost, or major program control

deficiencies. Finally, the coefficient on CHANGEPARTNER_NOEXP is not significant in any of

these models.

[INSERT TABLE 8 HERE]

To examine whether the increase in reported internal control deficiencies in the year of an

auditor change is due to under-reporting of internal control deficiencies by the predecessor

auditor, we include indicator variables equal to one for the last year of an audit firm engagement

(LAST FIRM YEAR), the audit partner’s last year where the audit firm is continuing as the

auditor (LAST PARTNER YEAR), and indicator variables equal to one for the audit partner’s

second and third years following an audit partner change on a continuing client

(PARTNERTENURE=2 and PARTNERTENURE=3).

Table 8, Panel B presents these results for all firms in the sample and Table 8, Panel C

presents results only for Big N and second tier audit firms. We find positive and significant

coefficients on LAST FIRM YEAR for both FS_RC and FS_MW as dependent variables (p<0.01

in both panels). Consistent with our prior results, the coefficient on CHANGEFIRM remains

positive and significant (p<0.01) in all models. These results indicate that audit firms are

26

significantly more likely to report reportable conditions and material weaknesses in both the last

year of an engagement and first year of a new engagement.

When we examine the likelihood of internal control deficiency disclosure in the year

preceding audit partner change, the coefficient on LAST PARTNER YEAR is also positive and

significant for FS_RC in both panels (p<0.05) and the coefficient on FS_MW is positive and

significant among Big N and second tier audit firms (p<0.10). These results suggest that audit

partners are more likely to report internal control deficiencies in the last year on an engagement.

We also find a positive and significant coefficient on PARTNERTENURE=2 (p<0.05) for

reportable conditions, indicating that audit partners in their second year on an engagement are

more likely to report reportable conditions. Finally, consistent with Table 6, we find that

LONGTENURE is positively associated with reporting a financial statement material weakness

among Big N clients. Overall, these results suggest that both audit firms and audit partners in

their last year on the engagement are significantly more likely to report internal control

deficiencies, consistent with audit arguments that auditors protect their reputations in the later

years of an engagement. These results also suggest that the increase in reported internal control

deficiencies following an audit firm change is more likely due to the application of new audit

methodology and planning procedures than due to under-reporting of internal control

deficiencies by the predecessor auditor.

Robustness Tests

In untabulated analysis, we examine the role of audit partner tenure in the detection and

reporting of internal control deficiencies only among clients that did not change auditors since

the prior year. Again, the coefficients on CHANGEPARTNER and LONGTENURE are not

significant for internal control deficiencies and the coefficient for LONGTENURE is positive and

significant for FINDORQ. In addition, we control for prior-year audit partner tenure surrounding

27

audit firm or partner changes and alternatively interact lagged partner tenure with

CHANGEFIRM and CHANGEPARTNER. We find no association between prior period audit

partner tenure and the detection and reporting of internal control deficiencies in the year of an

audit firm or audit partner change. We control for former Andersen partners and re-perform our

analysis excluding former Andersen partners and Andersen NFP clients and find no changes in

inferences.

We estimate our regressions on an annual cross-sectional basis to determine if our results

are driven by specific years and to examine whether passage of the Sarbanes-Oxley Act and

implementation of Auditing Standard 2 influenced internal control detection and reporting

among NFP clients. The coefficient for CHANGEFIRM is positive and significant in every year

when material weaknesses are the dependent variable (FS_MW and MP_MW) and is positive and

significant when reportable conditions are the dependent variable (FS_RC and MP_RC) in every

year except 2002. CHANGEPARTNER is not significant in any of the four models in any year.

These results suggest that our findings are not driven by specific years, or regulatory changes to

public accounting firms and SEC registered firms during our sample period.

Finally, we re-estimate our models using “first time” internal control deficiencies to rule

out the influence of internal control deficiencies reported in prior years. We define a “first time”

internal control deficiency as a reportable condition, material weakness or finding reported in

year t only if no internal control deficiencies or modified audit opinions were reported the prior

two years. Our inferences from Tables 5-8 are consistent when we substitute “first time” internal

control deficiencies as our dependent variables. These results support our conclusions that the

increase in internal control deficiencies surrounding audit firm changes are due to the application

28

of new audit methodology and enhanced audit planning procedures in the initial year of the audit

engagement.

V. CONCLUSION

This study examines the effects of audit firm and audit partner rotation on the reporting

of internal control deficiencies. Auditor assessment of internal control deficiencies has potential

implications for planned audit test procedures and auditor choices about whether and how to

report these deficiencies can influence the decision making of the clients stakeholders. Thus, the

empirical relation among the reporting of internal control deficiencies and attributes of the

auditor-client relationship may shed some light on the likely costs and benefits of audit partner

and audit firm rotation.

Using a sample of audit reports issued for large U.S. not-for-profit organizations between

2001 and 2007, we find a significant increase in material weaknesses, reportable conditions, and

audit findings reported in the first year following an audit firm change. We find no association

between audit partner changes and the detection and reporting of internal control deficiencies.

However, partners with tenure exceeding five years are more likely to report audit findings.

These results suggest that an audit firm’s investment in understanding and testing internal

controls in the initial year of the engagement leads to greater reporting of internal control

deficiencies. We also find that longer audit partner tenure may improve audit quality. We

provide initial evidence from the United States on the association between audit partner tenure

and rotation on the reporting of internal control deficiencies, a measure of auditor independence

and a dimension of audit quality. In addition, our results may be useful to regulators in

evaluating the costs and benefits of audit firm and audit partner rotation. Finally, our results

29

should interest state and federal agencies when evaluating policies to improve audit quality in

NFP sector.

Our study is subject to two primary limitations. First, as discussed earlier, it is unclear

how closely findings from NFP sector clients generalize to SEC registered clients or clients

located in other countries. Therefore, further research is needed before drawing policy

conclusions from this study. Second, we cannot observe the nature of the internal control

deficiencies as is possible with public companies. For this reason, we cannot examine the

remediation of control weaknesses, nor can we perform tests distinguishing between account

level versus entity level internal control deficiencies or internal control deficiencies detected by

management versus the auditor. These and other questions provide opportunities for future

research.

30

REFERENCES

American Institute of Certified Public Accountants (AICPA). 1978. The Commission on

Auditors’ Responsibilities: Report, Conclusions, and Recommendations. New York:

AICPA.

American Institute of Certified Public Accountants (AIPCA). 1983. Statement on Auditing

Standards No. 47: Audit risk and materiality in conducting an audit. New York: AIPCA.

Ashbaugh-Skaife, H., D. Collins, and W. Kinney. and R. LaFond. 2008. The effect of SOX

internal control deficiencies and their remediation on accrual quality. The Accounting

Review 83 (1): 217–250.

Bamber, E. M., and L. S. Bamber. 2009. Discussion of "Mandatory audit partner rotation, audit

quality, and market perception: Evidence from Taiwan". Contemporary Accounting

Research 26 (2): 393-402.

Bedard, J. C., and K. M. Johnstone. 2010. Audit partner tenure and audit planning and pricing.

Auditing: A Journal of Practice & Theory 29 (2): 45-70.

Belsley, D.A., E. Kuh, and R.E. Welsch, 1980. Regression Diagnostics: Identifying Influential

Data and Sources of Collinearity. New York: John Wiley and Sons Inc.

Brody, R. G., and S. E. Kaplan. 1996. Escalation of commitment among internal auditors.

Auditing: A Journal of Practice & Theory 15 (1): 1–15.

Caramanis, C., and C. Lennox. 2008 Audit effort and earnings management. Journal of

Accounting and Economics 45(1): 116-138.

Carcello, J. V., and A. L. Nagy. 2004. Audit firm tenure and fraudulent financial reporting.

Auditing: A Journal of Practice & Theory 23 (2): 55-60.

Carey, P., and R. Simnett. 2006. Audit partner tenure and audit quality. The Accounting Review

81 (3): 653-676.

Carreyrou, J. and B. Martinez. 2008. Grassley targets nonprofit hospitals on charity care. The

Wall Street Journal (December 18).

Carson, E., A. Luc, and L. Wong. 2012. Disentangling the effects of audit partner tenure and

audit firm tenure on audit quality. Working paper, University of New South Wales.

Chen, C-Y., C-J. Lin, and Y-C. Lin. 2008. Auditor partner tenure, audit firm tenure, and

discretionary accruals: Does long auditor tenure impair earnings quality? Contemporary

Accounting Research 25 (2): 415-446.

Chen, S., S. Sun, and D. Wu. 2010. Client importance, institutional improvements, and audit

quality in China: An office and individual auditor level analysis. The Accounting Review

85 (1): 127-158.

31

Chi, W., H. Huang, Y. Liao, and H. Xie. 2009. Mandatory audit partner rotation, audit quality,

and market perception: Evidence from Taiwan. Contemporary Accounting Research 26

(2): 329-358.

Daugherty, B., D. Dickens, R. Hatfield, and J. Higgs. 2012. An examination of partner

perceptions of partner rotation: Direct and indirect consequences to audit quality.

Auditing: A Journal of Practice & Theory 31(1): 97-114.

DeAngelo, L. 1981. Auditor size and audit quality. Journal of Accounting and Economics 3 (3):

183-199.

Deis, D., and G. Giroux. 1996. The effect of auditor changes on audit fees, audit hours, and audit

quality. Journal of Accounting and Public Policy 15(1): 55-76.

Doyle, J., W. Ge, and S. McVay. 2007. Accruals quality and internal control over financial

reporting. The Accounting Review 82 (5): 1141–1170.

Eilifsen, A., and W. F. Messier. 2000. Auditor detection of misstatements: A review and

integration of empirical research. Journal of Accounting Literature 19: 1-43.

Ettredge, M., J. Heintz, C. Li, and S. Scholz. 2011. Auditor realignments accompanying

implementation of SOX 404 ICFR reporting requirements. Accounting Horizons 25(1):

17-39.

European Commission. 2010. Audit Policy: Lessons from the Crisis. Green Paper. Brussels:

European Commission.

Feng, N. C., Q. Ling, D. Neely, and A. A. Roberts. 2011. Using archival data sources to conduct

nonprofit accounting research. Working paper, Providence College, Marquette

University, University of Wisconsin – Milwaukee and University of Virginia.

Feng, N. C. 2010. Determinants and Ecomonic Consequenes of Going Concern Audit Opinions

in Nonprofit Organizations. DBA dissertation, Boston University.

Geiger, M. A., and K. Raghunandan. 2002. Auditor tenure and audit reporting failures. Auditing:

A Journal of Practice & Theory 21 (1): 67-78.

Grassley, C. 2006. Strengthening the nonprofit sector. The Hill. (July 12).

———. 2010. Memorandum to Reporters and Editors: Illinois Supreme Court ruling on

hospital’s state tax exemption. Dated March 18, 2010. Available at:

http://grassley.senate.gov/news/Article.cfm?RenderForPrint=1&customel_dataPageID_1

502=25826.

Gul, F. A., S. Y. K. Fung, and B. L. Jaggi. 2009. Earnings quality: Some evidence on the role of

auditor tenure and auditors’ industry expertise. Journal of Accounting and Economics 47

(3): 265-287.

32

Gul, F. A., B. L. Jaggi, and G. V. Krishnan. 2007. Auditor independence: Evidence on the joint

effect of auditor tenure and nonaudit fees. Auditing: A Journal of Practice & Theory 26

(2): 117-142.

Heckman, J. 1979. Sample selection bias as a specification error. Econometrica 47 (1): 153-161.

House of Lords Select Committee on Economic Affairs (House of Lords). 2011. Auditors:

Market Concentration and Their Role. Volume I: Report. London: House of Lords.

Internal Revenue Service (IRS). 2010. IRS Business Master File with a limited selection of

variables for all 501(c)(3) and other 501(c) exempt organizations combined, Jan 2010.

Available at: http://nccsdataweb.urban.org/PubApps/showDD.php#Business Master

Files.

Iyer, V., and A. Watkins. 2008. Adoption of Sarbanes-Oxley measures by nonprofit

organizations: An empirical study. Accounting Horizons 22 (3): 255-277.

Jeffrey, C. 1992. The relation of judgment, personal involvement, and experience in the audit of

bank loans. The Accounting Review 67 (4): 802–819.

Johnson, E., I. K. Khurana, and J. K. Reynolds. 2002. Audit-firm tenure and the quality of

financial reports. Contemporary Accounting Research 19 (4): 637-660.

Johnstone, K., and J. Bedard. 2001. Engagement planning, bid pricing, and client response in the

market for initial attest engagements. The Accounting Review 76 (2): 199-220.

Keating, E., M. Fischer, T. Gordon, and J. Greenlee. 2005. The Single Audit Act: How

compliant are nonprofit organizations? Journal of Public Budgeting, Accounting and

Financial Management 17 (3): 285-309.

Kinney, W., and L. McDaniel. 1989. Characteristics of firms correcting previously reported

quarterly earnings. Journal of Accounting and Economics 11 (1):71-93.

Knechel, W. R. & Vanstraelen, A. 2007. The relationship between auditor tenure and audit

quality implied by going concern opinions. Auditing: A Journal of Practice & Theory: 26

(1): 113–31.

Lim, C.-Y., and H.-T. Tan. 2010. Does auditor tenure improve audit quality? Moderating effects

of industry specialization and fee dependence. Contemporary Accounting Research 27

(3): 923-957.

López, D. M., and G. F. Peters. 2010. Internal control reporting differences among public and

governmental auditors: The case of city and county Circular A-133 audits. Journal of

Accounting and Public Policy 29 (5): 510–524.

Myers, J. N., L. A. Myers, and T. C. Omer. 2003. Exploring the term of the auditor-client

relationship and the quality of earnings: A case for mandatory auditor rotation? The

Accounting Review 78 (July): 779-801.

33

National Center for Charitable Statistics (NCCS). 2011. Number of nonprofit organizations in

the United States, 1999 – 2009. Available at:

http://nccsdataweb.urban.org/PubApps/profile1.php?state=US.

Office of Management and Budget (OMB). 2007. Circular No. A-133: Audits of States, Local

Governments, and Non-Profit Organizations. Revised to show changes published in the

Federal Register June 27, 2003 and June 26, 2007. Washington, D.C.: OMB.

Palmrose, Z. V. 1991. Trials of legal disputes involving independent auditors: Some empirical

evidence. Journal of Accounting Research 29 (Supplement): 149-185.

Petovits, C., C. Shakespeare, and A. Shih. 2011. The causes and consequences of internal control

problems in nonprofit organizations. The Accounting Review 86 (1): 325-357.

President’s Council on Integrity and Efficiency (PCIE). 2007. Report on National Single Audit

Sampling Project. Washington, D.C.: Government Printing Office.

Public Company Accounting Oversight Board (PCAOB). 2011. Concept Release on Auditor

Independence and Audit Firm Rotation. Release No. 2011-006, Washington, D.C.:

PCAOB.

Public Oversight Board (POB). 2000. Panel on Audit Effectiveness: Public Oversight Board

Report and Recommendations. Stamford, CT: POB.

Ramen, K., and E. Wilson. 1992. An empirical investigation of the market for ‘single audit’

services. Journal of Accounting and Public Policy 11(4): 271-295.

Rice, S., and D. Weber. 2012. How effective is internal control reporting under SOX 404?

Determinants of the (non-)disclosure of existing material weaknesses. Journal of

Accounting Research, forthcoming.

Srinidhi, B., S. Leung, and F. A. Gul. 2010. Auditor tenure and audit quality: The role of the

demand for unique client specific knowledge. Working paper, City University of Hong

Kong and The Hong Kong Polytechnic University.

Tan, H. T. 1995. Effects of expectations, prior involvement, and review awareness on memory

for audit evidence and judgment. Journal of Accounting Research 33 (1): 113–136.

Trotman, K. T., and R. Wood. 1991. A meta-analysis of studies on internal control judgments.

Journal of Accounting Research 29 (1): 180-192.

Tate, S. 2007. Auditor change and auditor choice in nonprofit organizations. Auditing: A Journal

of Practice & Theory 26 (1): 47-70.

U.S. Congress. 2002. The Sarbanes–Oxley Act of 2002. 107th Congress of the United States of

America. H.R. 3763. Washington, D.C.: Government Printing Office.

34

U.S. General Accountability Office (GAO). 2002. Improvements possible in public, IRS, and

state oversight of charities. GAO-02-526 (April). Washington, D.C.: Government

Printing Office.

———. 2003. Public Accounting Firms: Required Study on the Potential Effects of Mandatory

Audit Firm Rotation. Washington, D.C.: Government Printing Office.

———. 2008a. Single Audit Quality. Actions needed to address persistent audit quality

problems. GAO 08-213T. Washington, D.C.: Government Printing Office

———. 2008b. Variation in standards and guidance limit comparison of how hospitals meet the

community benefit requirement. GAO-08-880 (September). Washington, D.C.:

Government Printing Office.

———. 2009. Significant federal funds reach the sector through various mechanisms, but more

complete and reliable funding data are needed. GAO report 09-193. Washington D.C.:

Government Printing Office.

Ye, P. E. Carson, and R. Simnett. 2011. Threats to auditor independence: The impact of

relationship and economic bonds. Auditing: A Journal of Practice & Theory 30 (1): 121-

148.

Zeff, S. 2003. Du Pont’s early policy on the rotation of audit firms. Journal of Accounting and

Public Policy 22 (1): 1-18.

Zhang, Y., J. Zhou, and N. Zhou. 2007. Audit committee quality, auditor independence, and

internal control weaknesses. Journal of Accounting and Public Policy 26 (3): 300-327.

35

APPENDIX A

Variable Definitions

Dependent Variables

FS_RC Equals one if the audit report in year t discloses a financial

statement control deficiency classified as a reportable condition

during the year, and equals zero otherwise

FS_MW Equals one if the audit report in year t discloses a financial

statement control deficiency classified as a material weakness

during the year, and equals zero otherwise

FINDORQ Equals one if the audit report in year t discloses a major program

audit finding or questioned cost during the year, and equals zero

otherwise

MP_RC Equals one if the audit report in year t discloses a major program

control deficiency classified as a reportable condition during the

year, and equals zero otherwise

MP_MW Equals one if the audit report in year t discloses a major program

control deficiency classified as a material weakness during the year,

and equals zero otherwise

Independent Variables

CHANGEFIRM Equals one if the client changed auditors between year t-1 and year

t, and equals zero otherwise

CHANGEPARTNER Equals one if the auditor is the same in year t-1 and year t but the

audit partner has changed between year t-1 and year t, and equals

zero otherwise

LONGTENURE Equals one if audit partner tenure in year t is greater than or equal to

six years, and equals zero otherwise

LNACCTFEES Equals the natural log of total accounting fees paid in year t

LAGPROBLEM Equals the number of problems reported in year t-1 (i.e.: the sum of

going concern opinion, qualified/adverse/disclaimer opinion,

reportable condition, material weakness, audit finding, and

questioned cost)

COMPLEXITY Equals the number of revenue sources in year t listed on Form 990

(public support, government contributions, and program revenue)