AUDITED FINANCIAL STATEMENTS

AND

SUPPLEMENTARY INFORMATION

PUTNAM SPECIAL SERVICES DISTRICT

YEAR ENDED JUNE 30, 2016

PUTNAM SPECIAL SERVICES DISTRICT

Table of Contents

Page

Independent Auditors’ Report ......................................................................................................................... 3

Management’s Discussion and Analysis .......................................................................................................... 5

Basic Financial Statements:

Government-Wide Financial Statements:

Statement of Net Position ........................................................................................................................... 11

Statement of Activities ................................................................................................................................ 12

Fund Financial Statements:

Balance Sheet–Governmental Fund ............................................................................................................ 13

Reconciliation of the Statement of Net Position to the

Balance Sheet-Governmental Fund ..................................................................................................... 14

Statement of Revenues, Expenditures and Changes in

Fund Balance–Governmental Fund ...................................................................................................... 15

Reconciliation of the Statement of Activities to the

Statement of Revenues, Expenditures and Changes in Fund

Balance-Governmental Fund ................................................................................................................ 16

Notes to Financial Statements ..................................................................................................................... 17

Required Supplementary Information:

General Fund Budgetary Comparison Schedule ............................................................................................... 36

Town of Putnam Retirement Plan Schedule of Employer Contributions .......................................................... 40

Town of Putnam Retirement Plan Schedule of Changes in the Net Pension Liability and Related Ratio’s ..... 41

Schedule of the Districts Municipal Employees Retirement System Pension Contributions ............................ 42

Members of the American Institute of Certified Public Accountants Members of the Connecticut Society of Certified Public Accountants

Ansonia

158 Main Street, Suite 301

Ansonia, Connecticut 06401

P: 203-732-2311

Killingworth

166 Route 81

Killingworth, Connecticut 06419

P: 860-663-0110

New Haven

900 Chapel Street, Suite 620

New Haven, Connecticut 06510

P: 203-773-0384

Westport

611 Riverside Avenue

Westport, Connecticut 06880

P: 877-839-7423

Guiding Successful People

Principals

Francis H. Michaud Jr. CPA

John A. Accavallo CPA

Sandra M. Woodbridge CPA

Dominic L. Cusano MBA CPA

Darin L. Offerdahl MBA CPA

INDEPENDENT AUDITORS’ REPORT

Putnam Special Services District

189 Church Street

Putnam, Connecticut

We have audited the accompanying financial statements of the governmental activities, each major fund and the

aggregate remaining fund information of Putnam Special Services District, as of and for the year ended June 30,

2016, and the related notes to the financial statements, which collectively comprise the District’s basic financial

statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance

with accounting principles generally accepted in the United States of America; this includes the design,

implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial

statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We conducted our

audit in accordance with auditing standards generally accepted in the United States of America. Those standards

require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements

are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the

financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the

risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk

assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the

financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the

purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no

such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the

reasonableness of significant accounting estimates made by management, as well as evaluating the overall

presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit

opinions.

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective

financial position of the governmental activities, each major fund, and the aggregate remaining fund information

of the Putnam Special Services District, as of June 30, 2016, and the respective changes in financial position for

the year then ended in accordance with accounting principles generally accepted in the United States of America.

- 4 -

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management’s

discussion and analysis, budgetary comparison information and schedules of districts pension contributions on

pages 5-10 and 36-42 be presented to supplement the basic financial statements. Such information, although not a

part of the basic financial statements, is required by the Governmental Accounting Standards Board, who

considers it to be an essential part of financial reporting for placing the basic financial statements in an

appropriate operational, economic or historical context. We have applied certain limited procedures to the

required supplementary information in accordance with auditing standards generally accepted in the United States

of America, which consisted of inquiries of management about the methods of preparing the information and

comparing the information for consistency with management’s responses to our inquiries, the basic financial

statements, and other knowledge we obtained during our audit of the basic financial statements. We do not

express an opinion or provide any assurance on the information because the limited procedures do not provide us

with sufficient evidence to express an opinion or provide any assurance.

Michaud Accavallo Woodbridge & Cusano, LLC

Killingworth, Connecticut

December 22, 2016

PUTNUM SPECIAL SERVICES DISTRICT

MANAGEMENT’S DISCUSSION AND ANALYSIS

- 5 -

As management of the Putnam Special Services District, we offer the readers of the District’s financial statements

this narrative overview and analysis of the financial activities of the District for the fiscal year ended June 30,

2016.

Financial Highlights

The assets of the Putnam Special Services District exceeded its liabilities at June 30, 2016 by $1,406,036

(net position).

The District’s total net position increased by $171,957 due to general revenues exceeding net expense.

As of the close of the current fiscal year, the District’s general fund reported an ending fund balance of

$784,634, an increase of $325,182 as a result of expenditures in excess of revenues (page 14).

Overview of the Financial Statements

This discussion and analysis is intended to serve as an introduction to the District’s basic financial statements.

The District’s basic financial statements comprise three components: 1) government-wide financial statements, 2)

fund financial statements, and 3) notes to the financial statements. This report also contains required

supplementary information in addition to the basic financial statements themselves.

Government-wide Financial Statements — The government-wide financial statements are designed to provide

readers with a broad overview of the District’s finances, in a manner similar to a private-sector business.

The statement of net position presents information on all of the District’s assets and liabilities, with the difference

between the two reported as net position. Over time, increases or decreases in net position may serve as a useful

indicator of whether the financial position of the District is improving or deteriorating.

The statement of activities presents information showing how the District’s net position changed during the most

recent fiscal year. All changes in net position are reported as soon as the underlying event giving rise to the

change occurs, regardless of the timing of related cash flows. Thus, revenues and expenses are reported in this

statement for some items that will only result in cash flows in future fiscal periods (e.g., uncollected taxes and

earned but unused sick leave).

Both of the government-wide financial statements distinguish functions of the District that are principally

supported by taxes and intergovernmental revenues. The governmental activity of the District is public safety.

The government-wide financial statements can be found on pages 11-12 of this report.

Fund Financial Statements — a fund is a grouping of related accounts that is used to maintain control over

resources that have been segregated for specific activities or objectives. The District, like other state and local

governments, uses fund accounting to ensure and demonstrate compliance with finance-related legal

requirements. The only fund of the District is the governmental fund (General Fund).

Governmental Funds — Governmental funds are used to account for essentially the same functions reported as

governmental activities in the government-wide financial statements. However, unlike the government-wide

financial statements, governmental fund financial statements focus on near-term inflows and outflows of

spendable resources, as well as on balances of spendable resources available at the end of the fiscal year. Such

information may be useful in evaluating a government’s near-term financing requirements.

Because the focus of the governmental fund is narrower than that of the government-wide financial statements, it

is useful to compare the information presented for governmental funds with similar information presented for

governmental activities in the government-wide financial statements. By doing so, readers may better understand

the long-term impact of the government’s near-term financing decisions. Both the governmental fund balance

- 6 -

sheet and the governmental fund statement of revenues, expenditures and changes in fund balance provide a

reconciliation to facilitate this comparison between governmental funds and governmental activities.

The District has one governmental fund. Information is presented separately in the governmental fund balance

sheet and in the governmental fund statement of revenues, expenditures and changes in fund balance for the

general fund, which is considered to be a major fund.

The District adopts an annual appropriated budget for its general fund. A budgetary comparison statement has

been provided for the general fund to demonstrate compliance with this budget.

The basic governmental fund financial statements can be found on pages 13 to 16 of this report.

Notes to the Financial Statements — The notes provide additional information that is essential to a full

understanding of the data provided in the government-wide and fund financial statements. The notes to the

financial statements can be found starting on page 16 of this report.

Required Supplementary and Supplementary Information — In addition to the basic financial statements and

accompanying notes, this report also presents certain required supplementary information. Supplementary

information can be found starting on page 36 of this report.

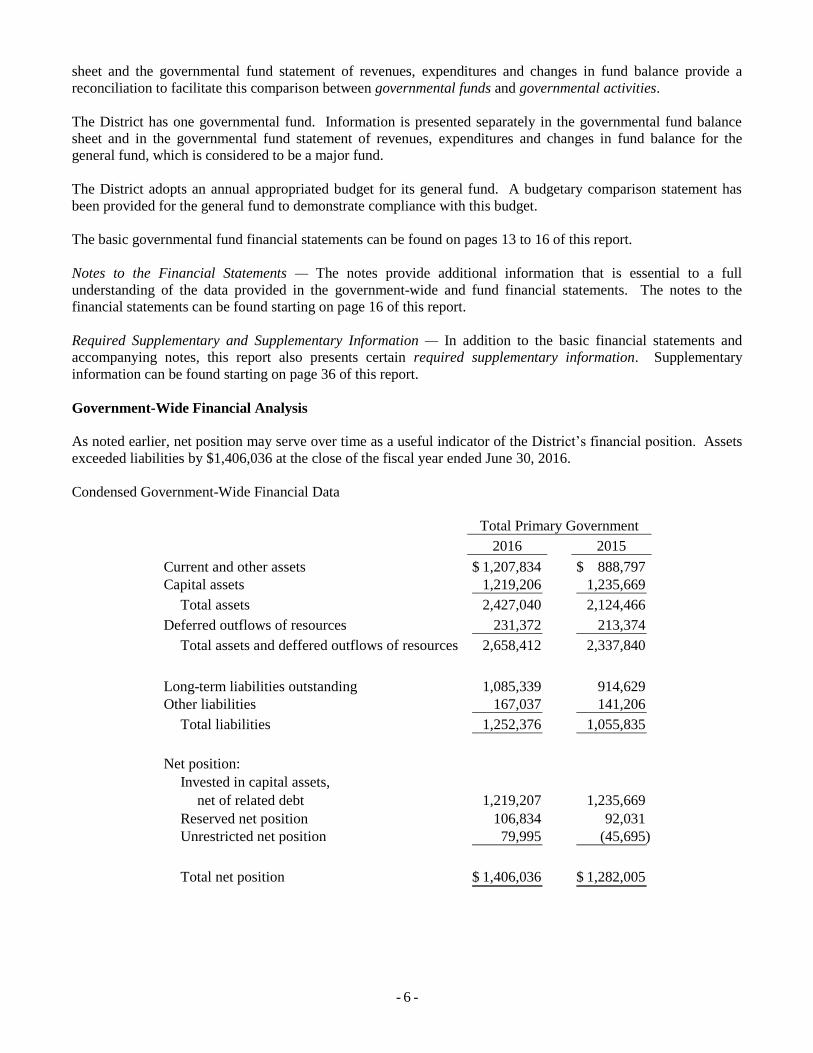

Government-Wide Financial Analysis

As noted earlier, net position may serve over time as a useful indicator of the District’s financial position. Assets

exceeded liabilities by $1,406,036 at the close of the fiscal year ended June 30, 2016.

Condensed Government-Wide Financial Data

2016 2015

Current and other assets 1,207,834$ 888,797$

Capital assets 1,219,206 1,235,669

Total assets 2,427,040 2,124,466

Deferred outflows of resources 231,372 213,374

Total assets and deffered outflows of resources 2,658,412 2,337,840

Long-term liabilities outstanding 1,085,339 914,629

Other liabilities 167,037 141,206

Total liabilities 1,252,376 1,055,835

Net position:

Invested in capital assets,

net of related debt 1,219,207 1,235,669

Reserved net position 106,834 92,031

Unrestricted net position 79,995 (45,695)

Total net position 1,406,036$ 1,282,005$

Total Primary Government

- 7 -

By far the largest portion of the District’s net position reflects its investment in capital assets net of related debt of

$1,219,207. The District uses these capital assets to provide fire services to citizens; consequently, these assets

are not available for future spending.

At the end of the current fiscal year, the District reported a positive balance in its investment in capital assets net

of related debt $1,219,207, reserved net position of $106,834 and unrestricted net position of $79,995.

The District’s governmental net position decreased by $171,957 during the current fiscal year. The District

brought in general revenues of $3,559,788 that were exceeded by its operating expenses of $3,957,903. These

expenses were offset by $570,072 in charges for services and grant revenue. The District’s general revenue was

comprised of $3,412,525 in tax collections, $136,959 in grants, $2,701 in unrestricted investment income, and

$7,603 in contributions and other revenues.

Governmental Activities – Governmental activities decreased the District’s net position by $171,957. Key

elements of this decrease are as follows:

2016 2015

Charges for services 554,072$ 267,589$

Program grants 16,000 66,000

Property taxes 3,412,525 3,272,678

Grants and contributions not

restricted to specific purpose 136,959 146,278

Unrestricted investment earnings 2,701 1,149

Other revenues 7,603 3,001

TOTAL REVENUES 4,129,860 3,756,695

Administrative 159,784 162,037

Personnel and Operations 3,798,119 3,228,508

TOTAL EXPENSES 3,957,903 3,390,545

INCREASE (DECREASE) IN NET POSITION 171,957 366,150

Net position at beginning of year 1,282,005 1,661,836

Adjustment to beginning net position (see Note 13) (47,926) (745,981)

Net position at beginning of year, as restated 1,234,079 915,855

1,406,036$ 1,282,005$

Total Primary Government

REVENUES

General revenues:

NET POSITION AT END OF YEAR

Program revenues:

EXPENSES

The costs of each of the District’s programs as well as each program’s net cost (total cost less revenues generated

by the activities) includes Personnel and Operations of $3,798,119 and General Government of $159,784. The

net expense reflects the financial burden that was placed on the District’s taxpayers by each of these functions.

Financial Analysis of the District’s Funds

As noted earlier, the Putnam Special Services District uses fund accounting to ensure and demonstrate compliance

with finance-related legal requirements.

- 8 -

Governmental funds – The focus of the District’s governmental funds is to provide information on near-term

inflows, outflows and balances of spendable resources. Such information is useful in assessing the District’s

financing requirements. In particular, unreserved fund balance may serve as a useful measure of a government’s

net resources available for spending at the end of the fiscal year.

As of the end of the current fiscal year, the District’s general fund reported an ending fund balance of $784,634,

an increase of $325,182 in comparison with the prior year.

General Fund Budgetary Highlights

Actual revenues were favorable when compared to the final budget by $508,978 due to a greater that expected

fees for services of $430,595 and property tax revenues of $75,086 off set by less than expected state grants of

$12,637. Actual expenditures were $133,140 higher than budgeted due to greater than anticipated personnel and

operating costs primarily related to police personal. For the year, results of operations generated a net favorable

budget variance of $375,838.

Capital Asset and Debt Administration

Capital assets – The District’s investment in capital assets for its governmental activities includes buildings,

grounds and improvements, vehicles, equipment, and furniture and fixtures. The total increase in the District’s

investment in capital assets (before depreciation) for the current fiscal year was $186,145 for the purchase of

equipment necessary in the District. A summary of the capital assets, net of depreciation, on a comparative basis

is as follows:

2016 2015

Buildings and grounds 186,693$ 205,163$

Vehicles 629,035 651,998

Equipment 403,478 378,508

1,219,206$ 1,235,669$

Total Primary Government

Additional information on the District’s capital assets can be found in Note 6 of this report.

Long-term debt – At the end of the current fiscal year, the Fire District has $1,085,339 of debt outstanding

comprised of CMERS pension obligations of $944,011 and compensated absences of $141,328.

The District’s total debt increased by $218,636 (25%) during the current fiscal year, mainly the result of increased

pension obligations related to CMERS.

State statutes limit the amount of general obligation debt a governmental entity may issue to 7 times its tax

collections plus interest and lien fees. For June 30, 2016, the maximum and net amount of borrowing permitted

under the formula would be $21,583,506. As of June 30, 2016, there was no bonded debt (see “Statement of Debt

Limitation” included in this report). Additional information on the District’s long-term debt can be found in Note

7 of this report.

- 9 -

Economic Factors and Next Year’s Budget

On June 22, 2015, a special meeting of the Putnam Special Services District voters was held and they approved a

resolution authorizing payment of $66,653to Ricky Hayes in settlement of a 13% permanent partial disability for

a heart and hypertension claim. There were no other heart and hypertension payouts during the years ended June

30, 2016 and 2015.

The overall result of all these factors did not result in an increase in the mill rate for the fiscal year ending June

31, 2016.

All of these factors were considered in preparing the District’s budget for the 2015-2016 fiscal years.

Requests for Information

This financial report is designed to provide a general overview of the Putnam Special Services District’s finances

for all those with an interest in the District’s operations. Questions concerning any of the information provided in

this report or requests for additional financial information should be addressed to the Putnam Special Services

District, 189 Church Street, Putnam, Connecticut 06260.

BASIC FINANCIAL STATEMENTS

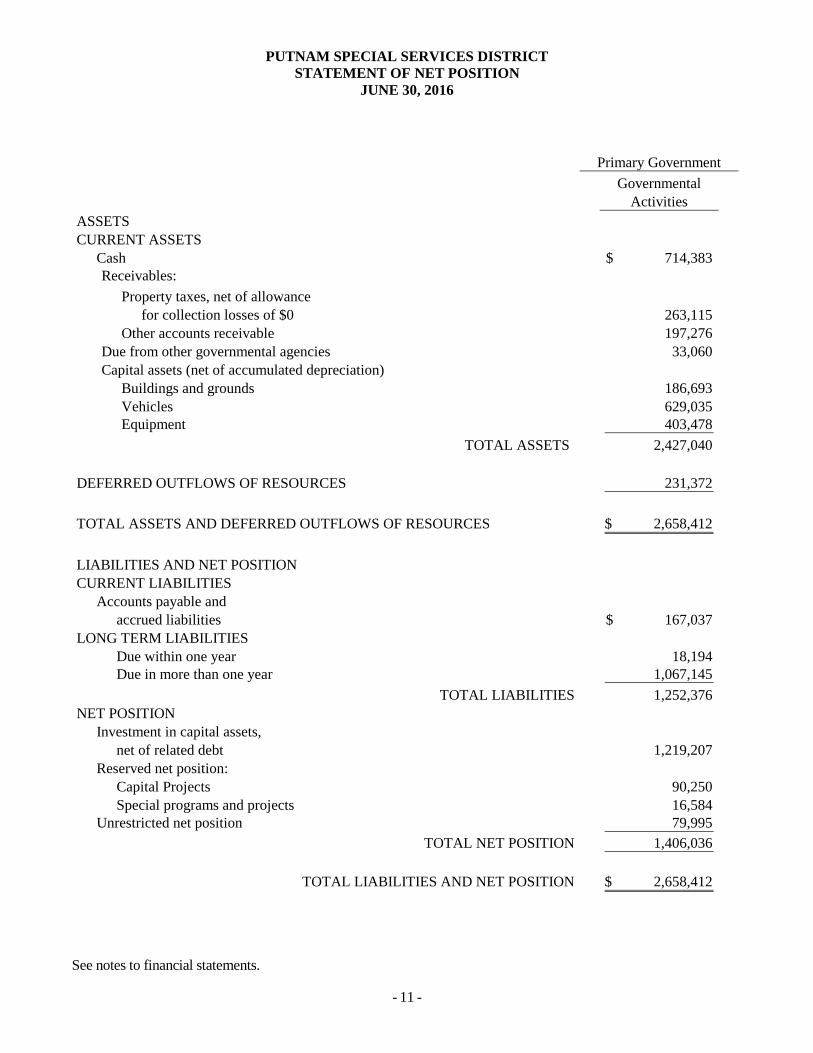

PUTNAM SPECIAL SERVICES DISTRICT

STATEMENT OF NET POSITION

JUNE 30, 2016

See notes to financial statements.

- 11 -

Governmental

Activities

ASSETS

CURRENT ASSETS

Cash 714,383$

Receivables:

Property taxes, net of allowance

for collection losses of $0 263,115

Other accounts receivable 197,276

Due from other governmental agencies 33,060

Capital assets (net of accumulated depreciation)

Buildings and grounds 186,693

Vehicles 629,035

Equipment 403,478

TOTAL ASSETS 2,427,040

DEFERRED OUTFLOWS OF RESOURCES 231,372

TOTAL ASSETS AND DEFERRED OUTFLOWS OF RESOURCES 2,658,412$

LIABILITIES AND NET POSITION

CURRENT LIABILITIES

Accounts payable and

accrued liabilities 167,037$

LONG TERM LIABILITIES

Due within one year 18,194

Due in more than one year 1,067,145

TOTAL LIABILITIES 1,252,376

NET POSITION

Investment in capital assets,

net of related debt 1,219,207

Reserved net position:

Capital Projects 90,250

Special programs and projects 16,584

Unrestricted net position 79,995

TOTAL NET POSITION 1,406,036

TOTAL LIABILITIES AND NET POSITION 2,658,412$

Primary Government

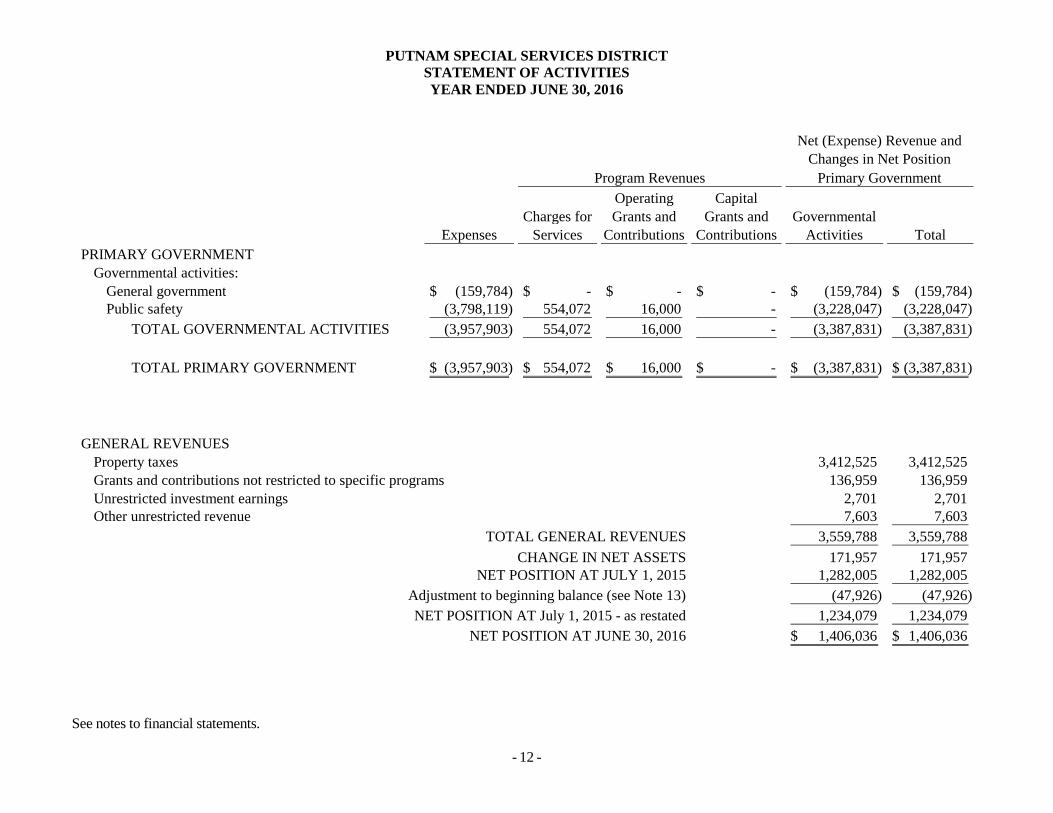

PUTNAM SPECIAL SERVICES DISTRICT

STATEMENT OF ACTIVITIES

YEAR ENDED JUNE 30, 2016

See notes to financial statements.

- 12 -

Program Revenues Primary Government

Operating Capital

Charges for Grants and Grants and Governmental

Expenses Services Contributions Contributions Activities Total

PRIMARY GOVERNMENT

Governmental activities:

General government (159,784)$ -$ -$ -$ (159,784)$ (159,784)$

Public safety (3,798,119) 554,072 16,000 - (3,228,047) (3,228,047)

TOTAL GOVERNMENTAL ACTIVITIES (3,957,903) 554,072 16,000 - (3,387,831) (3,387,831)

TOTAL PRIMARY GOVERNMENT (3,957,903)$ 554,072$ 16,000$ -$ (3,387,831)$ (3,387,831)$

GENERAL REVENUES

Property taxes 3,412,525 3,412,525

Grants and contributions not restricted to specific programs 136,959 136,959

Unrestricted investment earnings 2,701 2,701

Other unrestricted revenue 7,603 7,603

TOTAL GENERAL REVENUES 3,559,788 3,559,788

CHANGE IN NET ASSETS 171,957 171,957

NET POSITION AT JULY 1, 2015 1,282,005 1,282,005

Adjustment to beginning balance (see Note 13) (47,926) (47,926)

NET POSITION AT July 1, 2015 - as restated 1,234,079 1,234,079

NET POSITION AT JUNE 30, 2016 1,406,036$ 1,406,036$

Net (Expense) Revenue and

Changes in Net Position

PUTNAM SPECIAL SERVICES DISTRICT

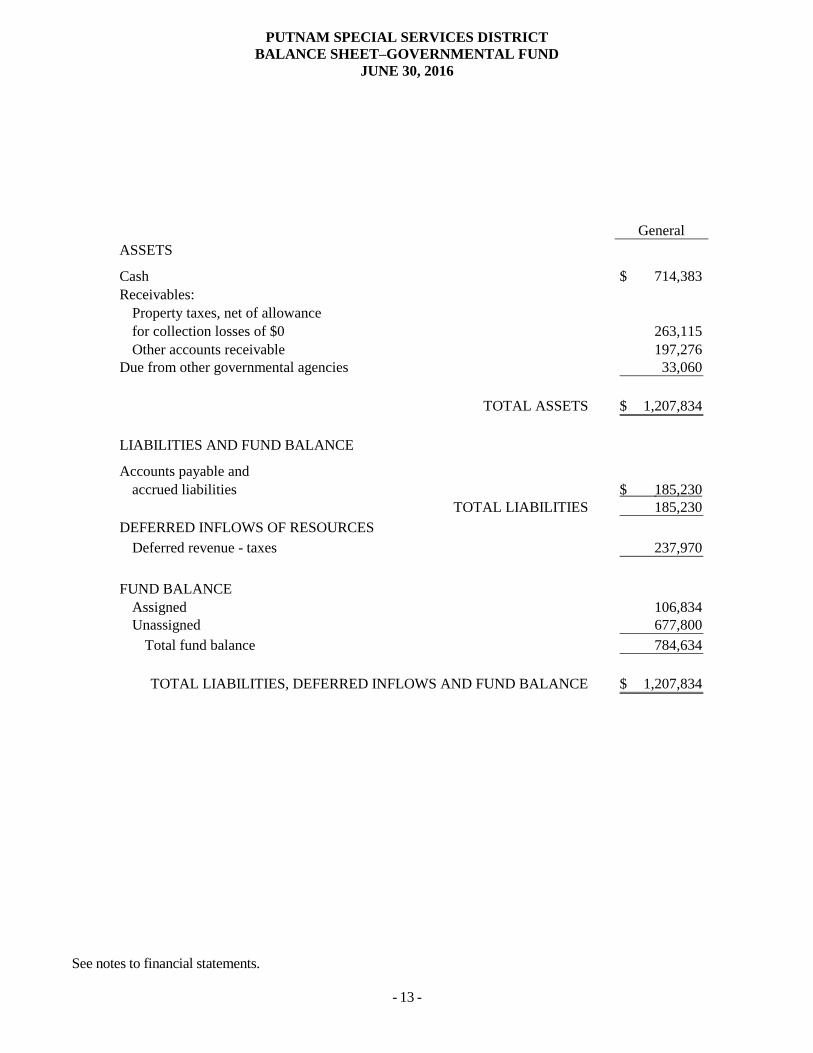

BALANCE SHEET–GOVERNMENTAL FUND

JUNE 30, 2016

See notes to financial statements.

- 13 -

General

Cash 714,383$

Receivables:

Property taxes, net of allowance

for collection losses of $0 263,115

Other accounts receivable 197,276

Due from other governmental agencies 33,060

TOTAL ASSETS 1,207,834$

Accounts payable and

accrued liabilities 185,230$

TOTAL LIABILITIES 185,230

DEFERRED INFLOWS OF RESOURCES

Deferred revenue - taxes 237,970

FUND BALANCE

Assigned 106,834

Unassigned 677,800

Total fund balance 784,634

TOTAL LIABILITIES, DEFERRED INFLOWS AND FUND BALANCE 1,207,834$

ASSETS

LIABILITIES AND FUND BALANCE

PUTNAM SPECIAL SERVICES DISTRICT

RECONCILIATION OF THE STATEMENT OF STATEMENT

OF NET POSITION TO THE BALANCE SHEET

-GOVERNMENTAL FUND

JUNE 30, 2016

See notes to financial statements.

- 14 -

Fund Balance 784,634$

Amounts reported for governmental activities in the

statement of net assets are different because:

Capital assets used in governmental activities are

not financial resources and, therefore, are not

reported in the funds. 1,219,206

Deferred outflows for future MERS pension obligation 231,372

Long-term assets are not available to pay for

current-period expenditures and, therefore, are

not reported in the funds. 237,969

Long-term liabilities, including compensated absenses,

are not due and payable in the current period and,

therefore, are not reported in the funds. (1,067,145)

Net position of governmental activities 1,406,036$

PUTNAM SPECIAL SERVICES DISTRICT

STATEMENT OF REVENUES, EXPENDITURES

AND CHANGES IN FUND BALANCE–GOVERNMENTAL FUND

JUNE 30, 2016

See notes to financial statements.

- 15 -

General

REVENUES

Property taxes 3,145,747$

Federal and state grants 152,959

Charges for services 554,073

Interest income 2,701

Miscellaneous 7,603

TOTAL REVENUES 3,863,083

EXPENDITURES

Current:

General government 159,785

Public safety 3,222,694

Capital outlays 155,422

TOTAL EXPENDITURES 3,537,901

EXCESS OF EXPENDITURES OVER REVENUES 325,182

FUND BALANCE AT JULY 1, 2015 459,452

FUND BALANCE AT JUNE 30, 2016 784,634$

PUTNAM SPECIAL SERVICES DISTRICT

RECONCILIATION OF THE STATEMENT OF ACTIVITIES

TO THE STATEMENT OF REVENUES, EXPENDITURES

AND CHANGES IN FUND BALANCE-GOVERNMENTAL FUND

YEAR ENDED JUNE 30, 2016

See notes to financial statements.

- 16 -

Amounts reported for governmental activities in the statement of

activities are different because:

Net change in fund balances - total governmental funds 325,182$

Governmental funds report capital outlays as expenditures.

However, in the statement of activities, the cost of those

assets is allocated over their estimated useful lives and

reported as depreciation expense. This is the amount by

which capital outlays exceeded depreciation expense in the

current period. 16,463

Revenues from taxes and assessments are reported as income

in the year revenues provide current financial resources to 266,778

governmental funds.

Some expenses (compensated absences) reported in the

statement of activities do not require the use of

current financial resources and , therefore, are not

reported as expenditures in governmental funds. (436,466)

Change in net position of governmental activities 171,957$

PUTNUM SPECIAL SERVICES DISTRICT

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2016

- 17 -

NOTE 1 — REPORTING ENTITY, DESCRIPTION OF FUNDS, AND SUMMARY OF SIGNIFICANT

ACCOUNTING POLICIES

Reporting Entity

The District is the basic level of government, which has oversight responsibility and control over all activities related

to police, fire and emergency dispatch protection in the Putnam Special Services District of the District of Putnam,

Connecticut. The District receives funding through the levy of property taxes from the residents it serves. The

District is not included in any other governmental “reporting entity” as defined by Governmental Accounting

Standards Board (GASB) pronouncement, since its District Authority Board are elected by the public and have

decision-making authority, the authority to levy taxes, the power to designate management, the ability to significantly

influence operations and primary accountability for fiscal matters.

The accounting policies of the Putnam Special Services District conform to generally accepted accounting

principles as applicable to governmental units. Proprietary funds and similar component units apply Financial

Accounting Standards Board (FASB) pronouncements and Accounting Principles Board (APB) opinions issued

on or before November 30, 1989, unless those pronouncements conflict with or contradict Governmental

Accounting Standards Board (GASB) pronouncements, in which case, GASB prevails. A summary of the more

significant policies are stated herein.

Accounting Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United

States of America requires management to make estimates and assumptions that affect the reported amounts of assets

and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported

amounts of revenues, expenses and expenditures during the reporting period. Actual results could differ from those

estimates.

Implementation of New Accounting Standards

For the year ended June 30, 2015, the District implemented the provisions of GASB Statement No. 68, Accounting

and Financial Reporting for Pensions, as amended by GASB Statement No. 71, Pension Transition for Contributions

Made Subsequent to the Measurement Date, and GASB Statement No. 69, Government Combinations and Disposals

of Governmental Operations. GASB Statement Nos. 68 and 71 establish standards for measuring and recognizing net

pension (assets and) liabilities, deferred outflows of resources, deferred inflows of resources, and

expenses/expenditures related to pension benefits provided through defined benefit pension plans. In addition,

Statement No. 68 requires disclosure of information related to pension benefits. GASB Statement No. 69 establishes

accounting and financial reporting standards related to government combinations and disposals of government

operations.

Government-wide and Fund Financial Statements

The government-wide financial statements (i.e., the Statement of Net Position and the Statement of Activities)

report information on all non-fiduciary activities of the primary government as a whole. Governmental activities,

which normally are supported by taxes and intergovernmental revenues, are reported separately from business-

type activities (if any), which rely to a significant extent on fees and charges for support.

PUTNUM SPECIAL SERVICES DISTRICT

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2016

- 18 -

The Statement of Net Position presents the financial position of the District at the end of its fiscal year. The

Statement of Activities demonstrates the degree to which direct expenses of a given function or segment is offset

by program revenues. Direct expenses are those that are clearly identifiable with a specific function or segment.

Program revenues include a) charges to customers or applicants who purchase, use or directly benefit from goods

or services, or privileges provided by a given function or segment, b) grants and contributions that are restricted to

meeting the operational or capital requirements of a particular function or segment and c) interest earned on grants

that is required to be used to support a particular program. Taxes and other items not identified as program

revenues are reported as general revenues. The District does not allocate indirect expenses to functions in the

Statement of Activities.

Measurement Focus, Basis of Accounting, and Financial Statement Presentation

The government-wide financial statements are reported using the economic resources measurement focus and the

accrual basis of accounting. Revenues are recorded when earned and expenses are recorded when a liability is

incurred, regardless of the timing of related cash flows. Grants and similar items are recognized as revenues as soon

as all eligibility requirements imposed by the provider have been met.

Governmental fund financial statements are reported using the current financial resources measurement focus and the

modified accrual basis of accounting. Revenues are recognized as soon as they are both measurable and available.

Revenues are considered to be available when they are collectible within the current period or soon enough thereafter

to pay liabilities of the current period. Expenditures are recorded when the related liability is incurred, as under

accrual accounting.

The government reports the following major governmental fund:

General Fund

The General Fund is the general operating fund of the District government. All unrestricted resources except those

required to be accounted for in another fund are accounted for in this fund. From this fund are paid general operating

expenditures, fixed charges, principal and interest on long-term debt, and capital improvement costs of the District,

which are not paid through a special fund.

Amounts reported as program revenues include 1) charges to customers or applicants for goods, services or privileges

provided, 2) operating grants and contributions, and 3) capital grants and contributions, including special assessments.

When both restricted and unrestricted resources are available for use, it is the District’s policy to use restricted

resources first, then unrestricted resources as they are needed.

Cash Equivalents

The District considers all highly liquid investments and those with original maturities of three months or less to be

cash equivalents.

Investments

Investments are stated at fair value. Fair value is determined based on quoted market prices.

PUTNUM SPECIAL SERVICES DISTRICT

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2016

- 19 -

Capital Assets

Capital assets, which include property and equipment, are reported in the governmental activities column in

government-wide financial statements. Capital assets are defined by the government as assets with an initial,

individual cost of more than $1,000 and an estimated useful life in excess of one year. Such assets are recorded at

historical cost or estimated historical cost if purchased or constructed. Donated capital assets are recorded at

estimated fair value at the date of donation.

The costs of normal maintenance and repairs that do not add to the value of the net asset or materially extend assets

lives are not capitalized.

Major outlays for capital assets and improvements are capitalized as projects are constructed.

Property and equipment of the District are depreciated using the straight-line method over the following estimated

useful lives:

Buildings and improvements 20 – 50 years

Equipment 5 – 25 years

Motor vehicles 5 – 10 years

Deferred Revenue

Deferred revenue arises when potential revenue does not meet both the “measurable” and “available” criteria for

recognition in the current period. Deferred revenue also arises when resources are received by the District before it

has a legal claim to them, as when grant monies are received prior to the incurrence of qualifying expenditures. In

subsequent periods, when both revenue recognition criteria are met, or when the District has a legal claim to the

resources, the liability for deferred revenue is removed and revenue is recognized.

Deferred Outflows/Inflows of Resources

In addition to assets, the statement of financial position will sometimes report a separate section for deferred

outflows of resources. This separate financial statement element represents a consumption of net position that

applies to a future period and so will not be recognized as an outflow of resources (expense/expenditure) until

then. In addition to liabilities, the statement of financial position will sometimes report a separate section for

deferred inflows of resources. This separate financial statement element represents an acquisition of net position

that applies to a future period and so will not be recognized as an inflow of resources (revenue) until that time. As

of June 30, 2014, the governmental funds report unavailable revenues from one source, property taxes. These

amounts are deferred and recognized as an inflow of resources in the period that the amounts become available.

Compensated Absences

Sick leave for employees of the District prior to July 1, 2007 will be based on ten (10) days per year, accumulation to

ninety days. Payment for each day of unused sick leave up to a maximum of ninety days (90) days shall be paid at the

time of retirement, or at the employee’s option, applied to early retirement. An employee’s unused sick leave at the

time of death will be paid to his estate. Each day of unused sick leave, for which payment is made, shall be computed

by multiplying his regular hourly rate by normal daily hours. Effective July 1, 2007 all new employees will have

fourteen (14) days per year sick time, which cannot be accumulated or carried over. Any sick time remaining at the

end of the year will be forfeited. Employees hired before July 1, 2007 will continue to accrue sick leave based on

their original agreement.

PUTNUM SPECIAL SERVICES DISTRICT

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2016

- 20 -

Net Position

Net position represents the difference between assets, deferred outflows of resources, liabilities and deferred

inflows of resources. Net position is reported as restricted when there are limitations imposed on its use either

through the enabling legislation adopted by the District or through external restrictions imposed by creditors,

grantors, or laws or regulations of other governments. Net position on the Statement of Net Position includes, net

investment in capital assets, restricted for debt service and special revenue funds. The balance is classified as

unrestricted.

Fund Balance

Generally, fund balance represents the difference between current assets and current liabilities. In the fund

financial statements, governmental funds report fund classifications that comprise a hierarchy based primarily on

the extent to which the District is bound to honor constraints on the specific purposes for which amounts in those

funds can be spent. Under this standard, the fund balance classifications are as follows:

Nonspendable fund balance includes amounts that cannot be spent because they are either not in

spendable form (inventories, prepaid amounts, long-term receivables) or they are legally or contractually

required to be maintained intact (the corpus of a permanent fund).

Restricted fund balance is to be reported when constraints placed on the use of the resources are imposed

by grantors, contributors, laws or regulations of other governments or imposed by law through enabling

legislation. Enabling legislation includes a legally enforceable requirement that these resources be used

only for the specific purposes as provided in the legislation. This fund balance classification will be used

to report funds that are restricted for debt service obligations and for other items contained in the

Connecticut statutes.

Committed fund balance will be reported for amounts that can only be used for specific purposes pursuant

to formal action of the District’s highest level of decision-making authority, a motion at a District

Meeting. These funds may only be used for the purpose specified unless the entity removes or changes

the purpose by taking the same action that was used to establish the commitment. This classification

includes certain designations established and approved by the entity’s governing boards.

Assigned fund balance, in the General Fund, will represent amounts constrained by either the entity’s

highest level of decision-making authority or a person with delegated authority from the governing board

to assign amounts for a specific intended purpose. Currently, this is done by the District Council. An

assignment cannot result in a deficit in the unassigned fund balance in the General Fund. This

classification will include amounts designated for balancing the subsequent year’s budget and

encumbrances. Assigned fund balance in all other governmental funds represents any positive remaining

amount after classifying nonspendable, restricted or committed fund balance amounts.

Unassigned fund balance, in the General Fund, represents amounts not classified as nonspendable,

restricted, committed or assigned. The General Fund is the only fund that would report a positive amount

in unassigned fund balance. For all governmental funds other than the General Fund, unassigned fund

balance would necessarily be negative, since the fund’s liabilities, together with amounts already

classified as nonspendable, restricted and committed would exceed the fund’s assets.

PUTNUM SPECIAL SERVICES DISTRICT

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2016

- 21 -

When both restricted and unrestricted amounts of fund balance are available for use for expenditures incurred, it is

the District’s policy to use restricted amounts first and then unrestricted amounts, as they are needed. For

unrestricted amounts of fund balance, the District considers that committed amounts would be reduced first,

followed by assigned amounts, and then unassigned amounts when expenditures are incurred for purposes for

which amounts in any of these unrestricted fund balance classifications could be used.

NOTE 2 — GOVERNMENT-WIDE FINANCIAL STATEMENTS

Beginning net position for governmental activities was determined as follows:

Fund balances of the general fund as of July 1, 2015 459,452$

Add: governmental capital assets, including

general fixed assets and infrastructure as

as of July 1, 2015 3,861,502

Add: tax revenue receivable as July 1, 2015 245,630

Add: Deferred outflows of resourses related to pension 160,031

Deduct: Net pension liability as of July 1, 2015 (see Note 13) (698,055)

Deduct: accumulated depreciation as of July 1, 2015

on above governmental capital assets (2,625,833)

Deduct: compensated absences payable and other

long-term liabilities as of July 1, 2015 (168,648)

NET POSITION AS OF JULY 1, 2015 (AS RESTATED) 1,234,079$

NOTE 3 — RECONCILIATION OF GOVERNMENT-WIDE AND FUND FINANCIAL STATEMENTS

Explanation of Certain Differences between the Governmental Fund Balance Sheet and the Government-Wide

Statement of Activities:

The governmental fund balance sheet includes reconciliation between fund balance – total governmental funds and

net position – governmental activities as reported in the government-wide statement of net position. One element of

that reconciliation explains, “Long-term liabilities are not due and payable in the current period and therefore are not

reported in the funds”. The details of this difference are as follows:

Compensated absences 123,134$

Net adjustment to reduce fund balance -

total governmental funds to arrive

at net position - governmental activities 123,134$

Explanation of Certain Differences between the Governmental Fund Statement of Revenues, Expenditures and

Changes in Fund Balance and the Government-Wide Statement of Activities:

The governmental fund statement of revenues, expenditures and changes in fund balance includes reconciliation

between net changes in fund balances – total governmental funds and changes in net position of governmental

activities as reported in the government-wide statement of activities. One element of that reconciliation explains that

PUTNUM SPECIAL SERVICES DISTRICT

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2016

- 22 -

“Governmental funds report capital outlays as expenditures. However, in the statement of activities the cost of those

assets is allocated over their estimated useful lives and reported as depreciation expense.” The details of this $16,463

difference are as follows:

Capital outlay 157,647$

Depreciation expense (174,110)

(16,463)$

Net adjustment to increase net changes in fund balance total governmental funds,

to arrive at changes in net assets of governmental activities

Another element of that reconciliation states that “Long-term debt (e.g., compensated absences)” provides current

financial resources to governmental funds, while the repayment of the principal of long-term debt consumes the

current financial resources of governmental funds. Neither transaction, however, has any effect on net position”. The

details of this $27,320 difference are as follows:

Contractual adjustment to compensated absences 33,655$

Compensated absences (6,335)

27,320$

Net adjustment to decrease net assets in fund balance total governmental funds to

arrive at changes in net assets of governmental activities

NOTE 4 — BUDGETS AND BUDGETARY ACCOUNTING

General Fund

The District’s annual budget is a management tool that assists its users in analyzing financial activity for its fiscal

year ending June 30, 2016. The District’s general budget policies are as follows:

1. Annually, at such a time as is designed by the District Authority, but prior to the annual meeting, the

District Authority presents to the District’s taxpayers an itemized estimate of revenues and expenditures for

the ensuing fiscal year.

2. The annual meeting is held on the second Monday in May. A majority vote is required to approve the

budget.

3. The District Authority may transfer amounts between the budgets line items provided the total budget is not

exceeded. For the year ended June 30, 2016, the District’s net under expended budget totaled $375,838,

which included any favorable charges for services of $430,595.

4. The District Authority may borrow money as needed, in anticipation of future taxes, to continue the safe

and efficient operation of the District.

5. Appropriations lapse at the end of the year.

As of June 30, 2016, there were no outstanding encumbrances.

PUTNUM SPECIAL SERVICES DISTRICT

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2016

- 23 -

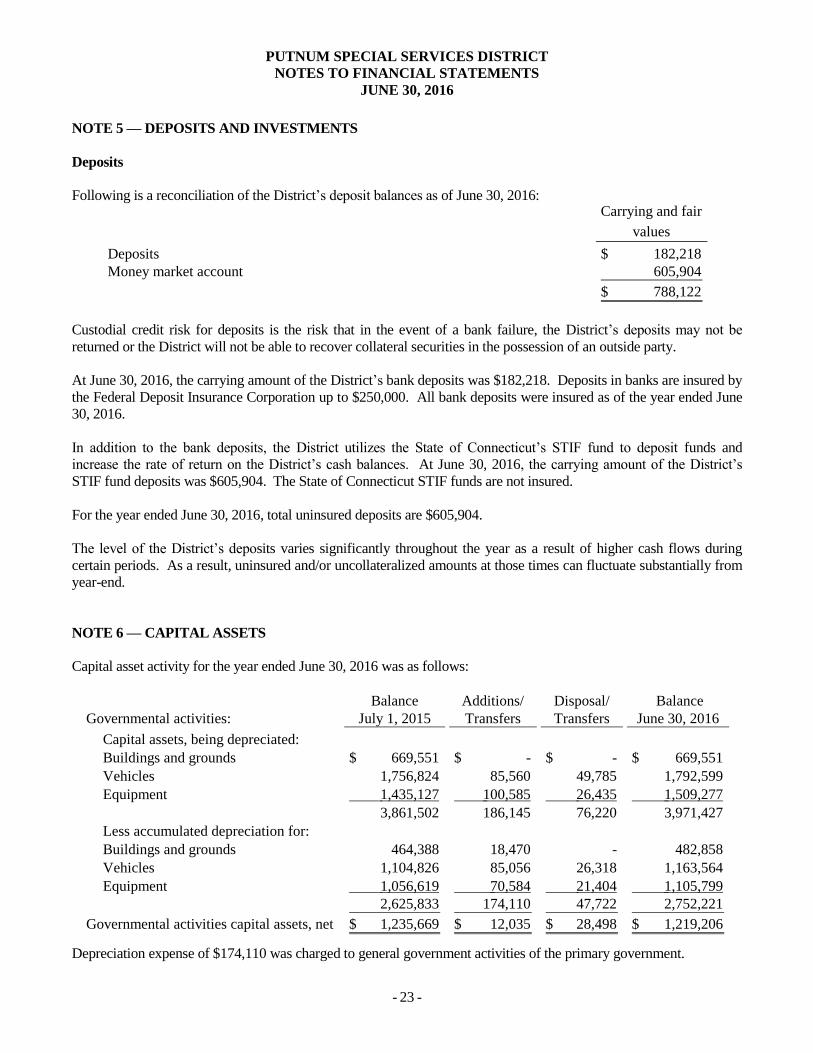

NOTE 5 — DEPOSITS AND INVESTMENTS

Deposits

Following is a reconciliation of the District’s deposit balances as of June 30, 2016: Carrying and fair

values

Deposits 182,218$

Money market account 605,904

788,122$

Custodial credit risk for deposits is the risk that in the event of a bank failure, the District’s deposits may not be

returned or the District will not be able to recover collateral securities in the possession of an outside party.

At June 30, 2016, the carrying amount of the District’s bank deposits was $182,218. Deposits in banks are insured by

the Federal Deposit Insurance Corporation up to $250,000. All bank deposits were insured as of the year ended June

30, 2016.

In addition to the bank deposits, the District utilizes the State of Connecticut’s STIF fund to deposit funds and

increase the rate of return on the District’s cash balances. At June 30, 2016, the carrying amount of the District’s

STIF fund deposits was $605,904. The State of Connecticut STIF funds are not insured.

For the year ended June 30, 2016, total uninsured deposits are $605,904.

The level of the District’s deposits varies significantly throughout the year as a result of higher cash flows during

certain periods. As a result, uninsured and/or uncollateralized amounts at those times can fluctuate substantially from

year-end.

NOTE 6 — CAPITAL ASSETS

Capital asset activity for the year ended June 30, 2016 was as follows:

Balance Additions/ Disposal/ Balance

Governmental activities: July 1, 2015 Transfers Transfers June 30, 2016

Capital assets, being depreciated:

Buildings and grounds 669,551$ -$ -$ 669,551$

Vehicles 1,756,824 85,560 49,785 1,792,599

Equipment 1,435,127 100,585 26,435 1,509,277

3,861,502 186,145 76,220 3,971,427

Less accumulated depreciation for:

Buildings and grounds 464,388 18,470 - 482,858

Vehicles 1,104,826 85,056 26,318 1,163,564

Equipment 1,056,619 70,584 21,404 1,105,799

2,625,833 174,110 47,722 2,752,221

Governmental activities capital assets, net 1,235,669$ 12,035$ 28,498$ 1,219,206$

Depreciation expense of $174,110 was charged to general government activities of the primary government.

PUTNUM SPECIAL SERVICES DISTRICT

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2016

- 24 -

NOTE 7 – DEBT

Changes in debt for the year ended June 30, 2016 was as follows:

July 1, 2015 Balance at Due Within

(as restated) Increases Decreases June 30, 2016 One Year

Governmental activities:

Net pension liability, CMERS 698,055$ 245,956$ -$ 944,011$ -$

Compensated absences 168,648 6,335 33,655 141,328 18,194

866,703$ 252,291$ 33,655$ 1,085,339$ 18,194$

All the long-term debt is liquidated by the General Fund of the District.

Debt Limitation

The Connecticut General Statutes provide that the District’s total outstanding and authorized debt shall not exceed

certain limitations. The following schedule details these limitations and the debt issued to date:

The Connecticut General Statutes provide that the total authorized debt of the District shall not exceed seven

times the base, or $21,583,506, nor shall the total authorized particular purpose debt exceed the individual debt

limitations reflected in the table below. As of June 30, 2016, the District had no authorized debt approved or

outstanding.

Total tax collections (including interest and lien

fees) for the year ended June 30, 2016 3,083,358$

General Urban Unfunded

Purpose Schools Sewers Renewal Pension

Debt Limitation:

2 ¼ times base 6,937,556$ - - - -

4 ½ times base - 13,875,111$ - - -

3 ¾ times base - - 11,562,593$ - -

3 ¼ times base - - - 10,020,914$ -

3 times base - - - - 9,250,074$

Total debt limitation 6,937,556$ 13,875,111$ 11,562,593$ 10,020,914$ 9,250,074$

Indebtedness:

Bonds payable - - - - -

Debt Limitation in

excess of outstanding

and authorized debt 6,937,556$ 13,875,111$ 11,562,593$ 10,020,914$ 9,250,074$

PUTNUM SPECIAL SERVICES DISTRICT

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2016

- 25 -

NOTE 8 — COMMITMENTS AND CONTINGENCIES

There are several claims pending against the District. The outcome and eventual liability of the District, if any, in

these cases are not known at this time. The District’s legal counsel estimates that potential claims against the

District not covered by insurance, resulting from such litigation would not materially affect the financial position

of the District.

NOTE 9 - RISK MANAGEMENT

The District is exposed to various risks of loss related to torts; theft of, damage to and destruction of assets; errors

and omissions; medical; workers’ compensation claims and natural disasters for which the District carries

commercial insurance. There were no significant reductions in insurance coverage from the prior year and the

amount of claim settlements have not exceeded insurance coverage for the current year or the three prior years.

The District currently is a member of the Connecticut Interlocal Risk Management Agency ("CIRMA"), a public

entity risk pool established for the purpose of administering an interlocal risk management program pursuant to

the provisions of Section 7-479a of the Connecticut General Statutes, for workers' compensation and employer

liability coverage. CIRMA is to be self-sustaining through members' premiums, but reinsurers in excess of

$1,000,000 for each insured occurrence. Members may be subject to supplemental assessment in the event of

deficiencies; however, potential assessments are limited by the by-laws.

As of June 30, 2016, there are no claims pending against the District.

NOTE 10 — EMPLOYEE RETIREMENT PLANS

Employees Other Than Police Personnel

Plan Description

The District contributes to the Town of Putnam's Retirement Plan (the Plan), a single-employer, defined benefit

pension plan that is reported as a Pension Trust Fund in the Town of Putnam's financial statements. The Plan is

accounted for using the accrual basis of accounting. Plan member contributions are recognized in the period in which

the contributions are due. Employer contributions to the Plans are recognized when due and the employer has made a

formal commitment to provide contributions. Benefits and refunds are recognized when due and payable in

accordance with the terms of the Plan.

Plan Membership

Membership in the Plan consisted of the following at July 1, 2015, the date of the most recent actuarial valuation:

Inactive plan members or beneficiaries

receiving benefits

47

Inactive plan members entitled to but not yet

receiving benefits

68

Active plan members 109

224

PUTNUM SPECIAL SERVICES DISTRICT

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2016

- 26 -

Employees of the Putnam Special Services District, other than police personnel, are eligible to participate in the

Town's Plan. Included in Plan membership above are three active plan members employed by the Putnam Special

Services District and four terminated employees of the Putnam Special Services District entitled to benefits, but not

yet receiving them.

Benefit Provisions

Employees who work more than 30 hours per week are eligible to participate in the Plan. Benefits fully vest after 5

years of service. Normal retirement date is the later of the participant's 65th birthday or the 5th anniversary of joining

the Plan.

Pension benefits for normal retirement under the Plan are based on the average monthly compensation during the five

consecutive years of service, at which the participants' earnings were at their highest level. The participant's monthly

benefit shall be equal to 1.3% of the average monthly compensation multiplied by the total number of years of

employment with the Town (limited to 40 years). The Plan permits early retirement for participants at age 55 with 15

years of service. Benefits for early retirement shall be equal to the present value of the participants' accrued benefit.

Participants are required to contribute 3% of their annual earnings.

Other Plan Provisions

The Plan does not provide for disability benefits. If an employee becomes disabled and must cease employment, he

will be entitled to the same benefits as a participant who has terminated employment. In the event of death, a

beneficiary shall receive benefits payable upon death, which is subject to certain limitations imposed by law. Death

benefits will be equal to the present value of the accrued benefits.

Fire Personnel are participants in the Towns plan but do not contribute to the pension plan under arrangements

that were established with the Town of Putnam, and became effective January 1, 1975. Firefighters who have

completed 20 years of continuous service with the Fire Department and attain the age of 62, are qualified to

receive benefits upon their retirement from service with the Putnam Special Services District's Fire Department.

Benefits are based on 40% of the annual compensation of a participant for the year preceding his/her retirement

plus $1.00 for every year of credited service with the Fire Dept. Benefits are paid every December 1st, in a lump

sum, and cease upon the death of the participant.

Benefit provisions of the Town of Putnam’s Pension Plan are established and can be amended by the District Council

of the Town of Putnam.

Funding Policy

Plan members are required to contribute 3% of their covered compensation to the Plan. The District is required to

contribute an actuarially determined amount each year. The total contribution to the Plan in relation to the actuarially

determined employer contribution (ADEC) was $185,420. The District's contributions to the Plan for the year ended

June 30, 2016 was $17,062.

Other financial information regarding the Town of Putnam’s Employee Pension Plan is included in the Town of

Putnam’s annual financial statements.

PUTNUM SPECIAL SERVICES DISTRICT

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2016

- 27 -

Investments

Investments are recorded at fair value based on quoted market prices. Short-term investments are reported at cost,

which approximates fair value. Fair value of other securities is determined by the mean of the most recent bid and

asked prices as obtained from dealers that make markets in such securities. Investments for which market quotations

are not readily available are valued at their fair values as determined by the custodian under the direction of the Town,

with the assistance of a valuation service. Securities traded on national exchanges are valued at the last reported sales

price. Investment income is recognized when earned and gains and losses on sales or exchanges are recognized on

the transaction date.

The following was the Town of Putnam’s adopted asset allocation policy as of June 30, 2016:

Asset Class

Target

Allocation

Large Cap 32%

Mid/Small Cap 12%

International 11%

Intermediate Bond 44%

Short Term Bond/Cash 1%

100%

Rate of Return

The annual money-weighted rate of return on pension plan investments, net of pension plan investment expenses was

-.8322%at June 30, 2016. The money-weighted rate of return expresses investment performance, net of investment

expense, adjusted for the changing amounts actually invested.

Administrative costs of the Plan are funded by the Town. The District's current year covered payroll for this Plan was

approximately $190,787.

Net Pension Liability

The components of the Town of Putnam’s net pension liability at June 30, 2016 were as follows:

Total pension liability 10,724,584$

Plan fiduciary net position 11,810,617

Net pension liability (1,086,033)$

Plan fiduciary net position as percentage 110.13%

of the total pension liability

PUTNUM SPECIAL SERVICES DISTRICT

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2016

- 28 -

Actuarial Assumptions

The total pension liability was determined by an actuarial valuation as of July 1, 2015, using the following actuarial

assumptions, applied to all periods included in the measurement:

Inflation 3.0%

Salary 5.0%, including inflation

Investment rate of return 7.0%

Actuarial cost method Entry Age Actuarial (level percentage of salary)

Mortality rates were based on the RP-2014 adjusted to 2006 total dataset mortality table projected to valuation dated

with scale MP-2015.

Discount Rate

The discount rate used to measure the total pension liability was 7%. The projection of cash flows used to determine

the discount rate assumed the plan members contributions will be made at the current contribution rate and that Town

contributions will be made at rates equal to the difference between actuarially determined contribution rate and the

member rate. Based on those assumptions, the pension plan’s fiduciary net position was projected to be available to

make all projected future benefit payments of current plan members. Therefore, the long-term expected rate of return

on pension plan investments was applied to all periods of projected benefit payments to determine the total pension

liability.

Sensitivity of the net pension liability to changes in the discount rate

The following presents the net pension liability, calculated using the discount rate of 7% as well as what the Town’s

net pension liability would be if it were calculated using a discount rate that is 1 percentage point lower (6%) or 1

percentage point higher (8%) than the current rate:

1%

Decrease

(6%)

Current

Discount

(7%)

1%

Increase

(8%)

(1,086,033)$ 252,884$ (2,224,247)$

Pension expense and deferred outflows of resources and deferred inflows of resources related to pensions

For the year ended June 30, 2016, the Town of Putnam recognized pension expense of $358,572. The Town reported

deferred outflows of resources related to pensions from the following sources:

Deferred Deferred

Outflows of Inflows ofResources Resources

Differences between expected and actual experience -$ (361,855)$

Changes of assumptions 154,230 (124,501)

Net difference between projected and actual

earnings on pension plan investements 1,025,668 -

1,179,898$ (486,356)$

PUTNUM SPECIAL SERVICES DISTRICT

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2016

- 29 -

Amounts reported as deferred outflows (inflows) of resources related to pension expense from the recognition of

difference between expected and actual experience will be recognized in pension expense as follows:

2017 218,929$

2018 218,929

2019 218,931

2020 124,699

2021 (65,954)

Thereafter (21,992)

693,542$

Connecticut Municipal Employees’ Retirement Plan (CMERS)

Connecticut's Municipal Employees Retirement System (CMERS) is the public pension plan offered by the State of

Connecticut for municipal employees in participating municipalities. The plan was established in 1947 and is

governed by Connecticut Statute Title 7, Chapter 113. CMERS is a multiemployer pension plan administered by the

Connecticut State Retirement Commission. The State Retirement Commission is responsible for the administration of

the Connecticut Municipal Employees Retirement System (CMERS). The State Treasurer is responsible for investing

CMERS funds for the exclusive benefit of CMERS members. The District has one participating group of employees

with in this plan, Police Employees, who are covered under the Policemen and firemen with social security section of

the plan.

Plan description

Municipalities may designate which departments (including elective officers if so specified) are to be covered under

the Municipal Employees Retirement System. This designation may be the result of collective bargaining. Only

employees covered under the State Teachers Retirement System may not be included. There is no minimum age or

service requirements. Membership is mandatory for all regular full time employees of participating departments

except Police and Fire hired after age 60.

The plan has 4 sub plans as follows:

General employees with social security

General employees without social security

Policemen and firemen with social security

Policemen and firemen without social security

Benefit provisions

The plan provides retirement, disability and death benefits.

General Employees-Employees are eligible to retire at age 55 with 5 years of continuous service, or 15 years of active

aggregate service, or 25 years of aggregate service.

Policemen and Firemen-Compulsory retirement age for police and fire members is age 65. Normal Retirement: For

members not covered by social security, the benefit is 2% of average final compensation times years of service.

PUTNUM SPECIAL SERVICES DISTRICT

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2016

- 30 -

For members covered by social security, the benefit is 1 %% of the average final compensation not in excess of the

year's breakpoint plus 2% of average final compensation in excess of the year's breakpoint, times years of service.

The maximum benefit is 100% of average final compensation and the minimum benefit is $1,000 annually. Both the

minimum and the maximum include workers' compensation and social security benefits. If any member covered by

social security retires before age 62, the benefit until age 62 is reached or a social security disability award is received,

is computed as if the member is not under social security.

Early Retirement: Employees are eligible after 5 years of continuous or 15 years of active aggregate service. The

benefit is calculated on the basis of average final compensation and service to date of termination. Deferred to normal

retirement age, or an actuarially reduced allowance may begin at the time of separation.

Disability Retirement: Employees are eligible for service-related disability benefits from being permanently or totally

disabled from engaging in the service of the municipality provided such disability has arisen out of and in the course

of employment with the municipality. Disability due to hypertension or heart disease, in the case of firemen and

policemen, is presumed to have been suffered in the line of duty. Disability benefits are calculated based on

compensation and service to the date of the disability with a minimum benefit (including workers' compensation

benefits) of 50% of compensation at the time of disability.

Employees are eligible for non-service-related disability benefits with 10 years of service and being permanently or

totally disabled from engaging in gainful employment in the service of the municipality. Disability benefits are

calculated based on compensation and service to the date of the disability.

Pre-Retirement Death Benefit: The plan also offers a lump sum return of contributions with interest or surviving

spouse benefit depending on length of service.

Contributions

Employer:

Participating municipalities make annual contributions consisting of a normal cost contribution, a contribution for the

amortization of the net unfunded accrued liability and a prior service amortization payment which covers the

liabilities of the system not met by member contributions.

Employees:

For employees not covered by social security, each person is required to contribute 5% of compensation.

For employees covered by social security, each person is required to contribute 2 %% of compensation up to the

social security taxable wage base plus 5% of compensation, if any, in excess of such base.

PUTNUM SPECIAL SERVICES DISTRICT

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2016

- 31 -

Allocation methodology for Pension Liability, Pension Expense and Deferred outflows/inflows of resources

The schedules of employer allocations were calculated based upon the 2014 actuarial (expected) payroll amounts

reported by participating employers. Expected payroll adjusts actual payroll for known changes in the status of

employees, annualized salaries for partial year employees and anticipated salary increases. The employer allocations

were then applied to the net pension liability, pension expense, deferred inflows, sensitivity analysis and the deferred

inflow amounts to be recognized in fiscal years subsequent to the reporting date to determine the amount applicable to

each employer. The schedules of employer allocations reflect actuarial employer payroll for the fiscal year ended

June 30, 2014. Based upon the employer's payroll as compared to the total, an employer allocation percentage is

calculated to six decimal places and is used to allocate the elements noted above.

Pension Liability

At June 30, 2015, the District reported a liability of $944,011 for its proportionate share of the CMERS’ net pension

liability. The net pension liability was measured as of June 30, 2015. The total pension liability used to calculate the

net pension liability was determined using update procedures to roll forward the total pension liability from an

actuarial valuation as of June 30, 2014, to the measurement date of June 30, 2015.

Net Pension Liability of the District

The components of the net pension liability of the District at June 30, 2016 was as follows:

Total pension liability 12,969,230$

Plan fiduciary net assets 12,025,219

Net Pension Liability 944,011$

Plan fiduciary net position as a percentage

of the total pension liability 92.72%

Percentage of the total 3.085286%

PUTNUM SPECIAL SERVICES DISTRICT

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2016

- 32 -

Pension expense and deferred outflows/inflows of resources

For the year ended June 30, 2015, the District recognized pension expense for their portion of the CMERS of

$156,942. At June 30, 2015, the District reported deferred outflows of resources related to pensions from the

following sources:

Deferred

Outflows of

Resources

Differences between expected

and actual experience -$

Changes in assumptions -

Net difference between projected and

actual earnings on investments 71,341

Total 71,341$

Percentage of total 3.085286%

Pension Expense 198,018$

Deferred outflows of resources related to CMERS pensions will be recognized in pension expense as follows:

2017 4,499$

2018 4,499

2019 4,499

2020 57,844

Total 71,341$

Year Ending June 30,

Actuarial Assumptions

The total pension liability was determined by an actuarial valuation as of June 30, 2014, using the following

actuarial assumptions, applied to all periods included in the measurement:

Inflation 3.25%

Salary

Investment rate of return

4.25-11.00%, including inflation

8% net of pension plan investment expense, including

inflation

PUTNUM SPECIAL SERVICES DISTRICT

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2016

- 33 -

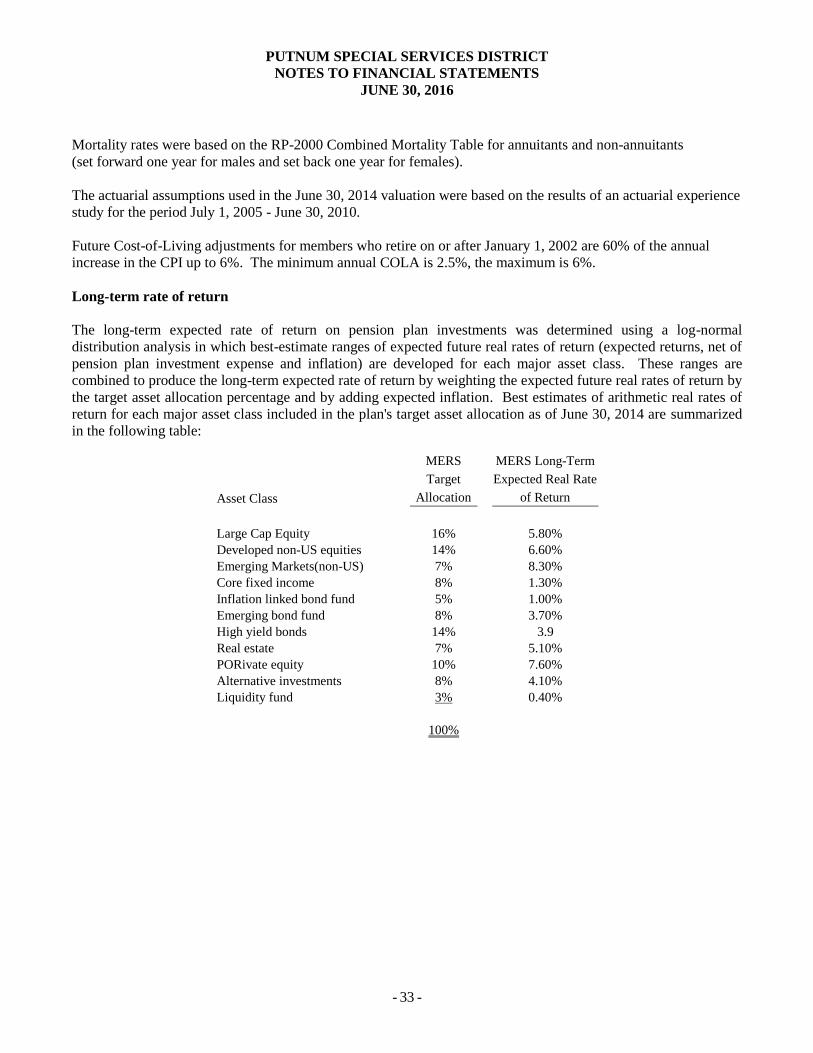

Mortality rates were based on the RP-2000 Combined Mortality Table for annuitants and non-annuitants

(set forward one year for males and set back one year for females).

The actuarial assumptions used in the June 30, 2014 valuation were based on the results of an actuarial experience

study for the period July 1, 2005 - June 30, 2010.

Future Cost-of-Living adjustments for members who retire on or after January 1, 2002 are 60% of the annual

increase in the CPI up to 6%. The minimum annual COLA is 2.5%, the maximum is 6%.

Long-term rate of return

The long-term expected rate of return on pension plan investments was determined using a log-normal

distribution analysis in which best-estimate ranges of expected future real rates of return (expected returns, net of

pension plan investment expense and inflation) are developed for each major asset class. These ranges are

combined to produce the long-term expected rate of return by weighting the expected future real rates of return by

the target asset allocation percentage and by adding expected inflation. Best estimates of arithmetic real rates of

return for each major asset class included in the plan's target asset allocation as of June 30, 2014 are summarized

in the following table:

Asset Class

MERS

Target

Allocation

MERS Long-Term

Expected Real Rate

of Return

Large Cap Equity 16% 5.80%

Developed non-US equities 14% 6.60%

Emerging Markets(non-US) 7% 8.30%

Core fixed income 8% 1.30%

Inflation linked bond fund 5% 1.00%

Emerging bond fund 8% 3.70%

High yield bonds 14% 3.9

Real estate 7% 5.10%

PORivate equity 10% 7.60%

Alternative investments 8% 4.10%

Liquidity fund 3% 0.40%

100%

PUTNUM SPECIAL SERVICES DISTRICT

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2016

- 34 -

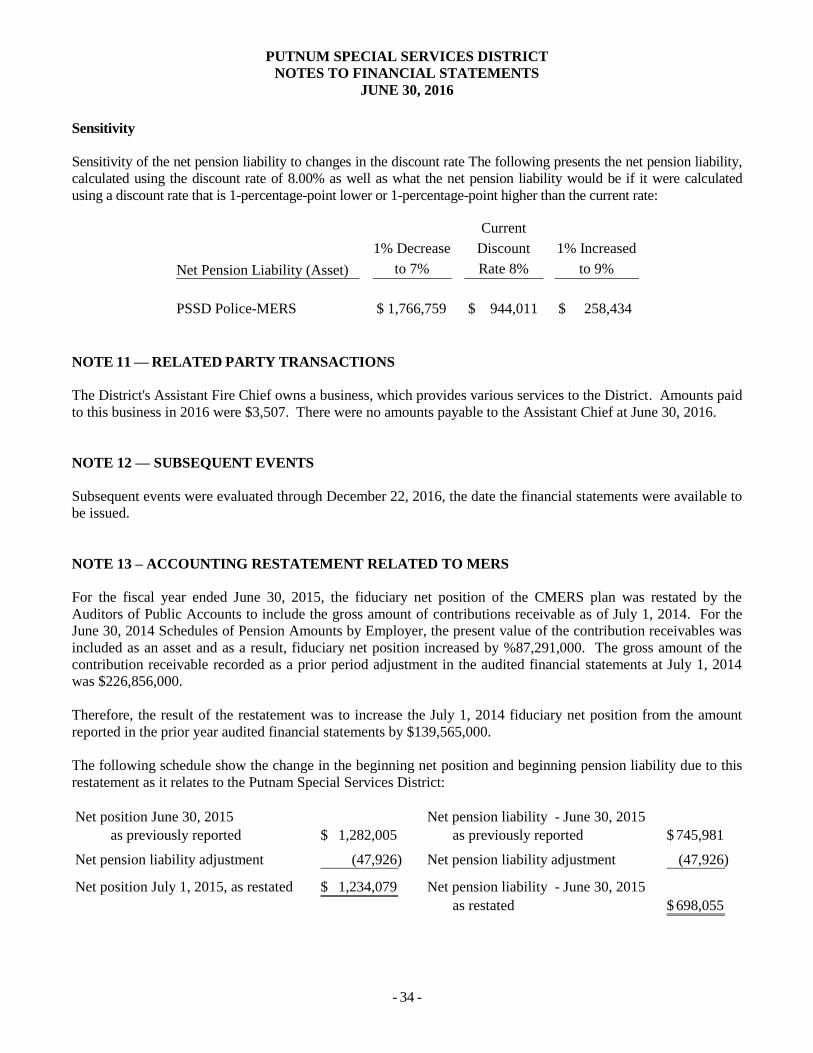

Sensitivity

Sensitivity of the net pension liability to changes in the discount rate The following presents the net pension liability,

calculated using the discount rate of 8.00% as well as what the net pension liability would be if it were calculated

using a discount rate that is 1-percentage-point lower or 1-percentage-point higher than the current rate:

Net Pension Liability (Asset)

1% Decrease

to 7%

Current

Discount

Rate 8%

1% Increased

to 9%

PSSD Police-MERS $ 1,766,759 $ 944,011 $ 258,434

NOTE 11 — RELATED PARTY TRANSACTIONS

The District's Assistant Fire Chief owns a business, which provides various services to the District. Amounts paid

to this business in 2016 were $3,507. There were no amounts payable to the Assistant Chief at June 30, 2016.

NOTE 12 — SUBSEQUENT EVENTS

Subsequent events were evaluated through December 22, 2016, the date the financial statements were available to

be issued.

NOTE 13 – ACCOUNTING RESTATEMENT RELATED TO MERS

For the fiscal year ended June 30, 2015, the fiduciary net position of the CMERS plan was restated by the

Auditors of Public Accounts to include the gross amount of contributions receivable as of July 1, 2014. For the

June 30, 2014 Schedules of Pension Amounts by Employer, the present value of the contribution receivables was

included as an asset and as a result, fiduciary net position increased by %87,291,000. The gross amount of the

contribution receivable recorded as a prior period adjustment in the audited financial statements at July 1, 2014

was $226,856,000.

Therefore, the result of the restatement was to increase the July 1, 2014 fiduciary net position from the amount

reported in the prior year audited financial statements by $139,565,000.

The following schedule show the change in the beginning net position and beginning pension liability due to this

restatement as it relates to the Putnam Special Services District:

Net position June 30, 2015 Net pension liability - June 30, 2015

as previously reported 1,282,005$ as previously reported 745,981$

Net pension liability adjustment (47,926) Net pension liability adjustment (47,926)

Net position July 1, 2015, as restated 1,234,079$ Net pension liability - June 30, 2015

as restated 698,055$

REQUIRED SUPPLEMENTARY INFORMATION

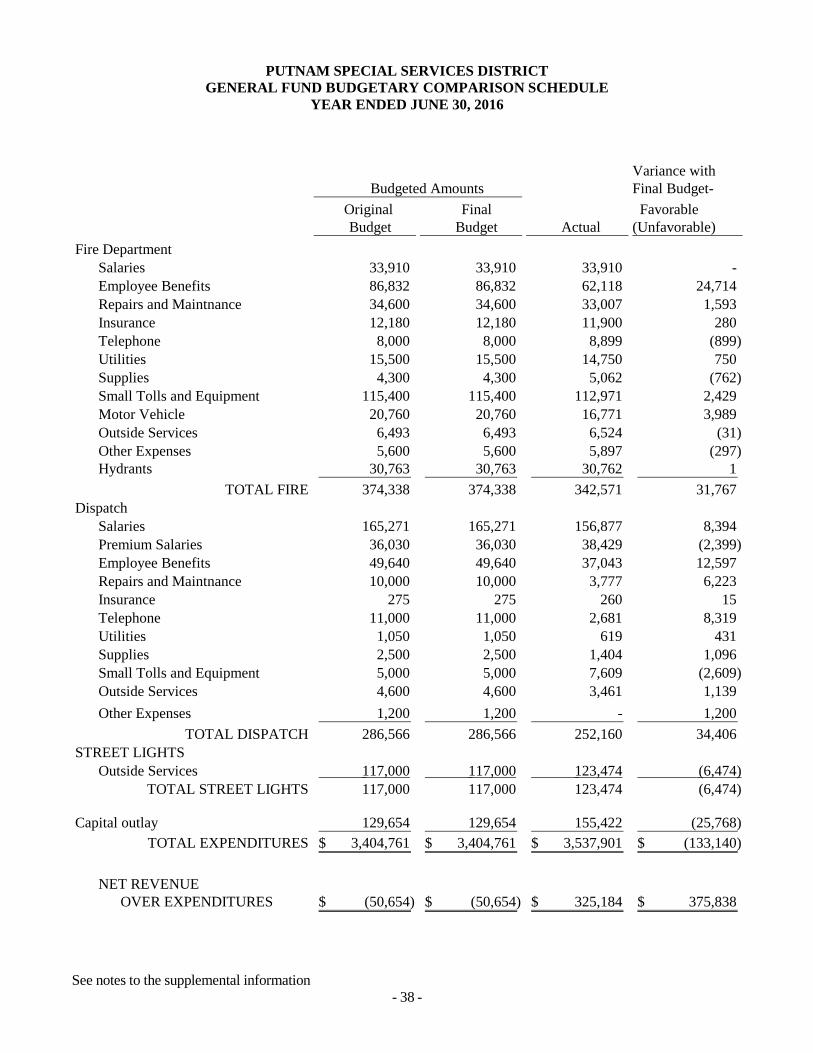

PUTNAM SPECIAL SERVICES DISTRICT

GENERAL FUND BUDGETARY COMPARISON SCHEDULE

YEAR ENDED JUNE 30, 2016

See notes to the supplemental information

- 36 -

Variance with

Final Budget-

Original Final Favorable

Budget Budget Actual (Unfavorable)

Property taxes

Property taxes 3,070,661$ 3,070,661$ 3,145,747$ 75,086$

Other Income

Federal grants 16,000 16,000 16,000 -

State grants - Housing

Authority in lieu 18,500 18,500 18,821 321

State Grants - Pilot 20,680 20,680 20,332 (348)

State grants -

Property tax releif 92,270 92,270 79,522 (12,748)

State grants - other 18,147 18,147 18,285 138

165,597 165,597 152,960 (12,637)

Charges for services

Licenses and permits 3,500 3,500 5,430 1,930

Charges for services 101,849 101,849 532,444 430,595

Fines 10,000 10,000 16,200 6,200

115,349 115,349 554,074 438,725

Investment income 2,000 2,000 2,701 701

Other income 500 500 7,603 7,103

2,500 2,500 10,304 7,804

TOTAL REVENUES 3,354,107$ 3,354,107$ 3,863,085$ 508,978$

Budgeted Amounts

PUTNAM SPECIAL SERVICES DISTRICT

GENERAL FUND BUDGETARY COMPARISON SCHEDULE

YEAR ENDED JUNE 30, 2016

See notes to the supplemental information

- 37 -

Variance with

Final Budget-

Original Final Favorable

Budget Budget Actual (Unfavorable)

Administrative

Salaries 46,196$ 46,196$ 47,100$ (904)$

Employee Benefits 12,768 12,768 12,936 (168)

Repairs and Maintnance 1,000 1,000 1,000 -

Rent 2,300 2,300 1,987 313

Insurance 260 260 148 112

Telephone 800 800 502 298

Supplies 1,500 1,500 1,122 378

Postage 750 750 640 110

Small tools and equipment 500 500 85 415

Outside Services 97,600 97,600 94,264 3,336

Other Expenses 200 200 - 200

TOTAL ADMINISTRATIVE 163,874 163,874 159,784 4,090

Police Department

Salaries 1,130,827 1,130,827 1,110,585 20,242

Premium Salaries 203,189 203,189 434,954 (231,765)

Employee Benefits 716,972 716,972 676,042 40,930

Repairs and Maintnance 21,200 21,200 25,421 (4,221)

Rent 1 1 1 -

Insurance 35,290 35,290 45,340 (10,050)

Telephone 18,100 18,100 24,246 (6,146)

Utilities 17,500 17,500 15,862 1,638

Supplies 14,000 14,000 11,147 2,853

Postage 1,500 1,500 638 862

Small Tolls and Equipment 10,250 10,250 6,999 3,251

Narcotics Canine Expense 6,500 6,500 3,381 3,119

Motor Vehicle 61,500 61,500 50,318 11,182

Outside Services 68,500 68,500 69,746 (1,246)

Other Expenses 28,000 28,000 29,810 (1,810)

TOTAL POLICE 2,333,329 2,333,329 2,504,490 (171,161)

Budgeted Amounts

PUTNAM SPECIAL SERVICES DISTRICT

GENERAL FUND BUDGETARY COMPARISON SCHEDULE

YEAR ENDED JUNE 30, 2016

See notes to the supplemental information

- 38 -

Variance with

Final Budget-

Original Final Favorable

Budget Budget Actual (Unfavorable)

Budgeted Amounts

Fire Department

Salaries 33,910 33,910 33,910 -

Employee Benefits 86,832 86,832 62,118 24,714

Repairs and Maintnance 34,600 34,600 33,007 1,593

Insurance 12,180 12,180 11,900 280

Telephone 8,000 8,000 8,899 (899)

Utilities 15,500 15,500 14,750 750

Supplies 4,300 4,300 5,062 (762)

Small Tolls and Equipment 115,400 115,400 112,971 2,429