AUSTIN

2016

Credits & ContactPitchBook Data, Inc.

JOHN GABBERT Founder, CEO

ADLEY BOWDEN Vice President,

Market Development & Analysis

ContentGARRETT JAMES BLACK Senior Analyst

BRYAN HANSON Data Analyst

JENNIFER SAM Senior Graphic Designer

Contact PitchBook pitchbook.com

RESEARCH

EDITORIAL

SALES

COPYRIGHT © 2017 by PitchBook Data, Inc. All rights reserved. No part of this publication may be reproduced in any form or by any means—graphic, electronic, or mechanical, including photocopying, recording, taping, and information storage and retrieval systems—without the express written permission of PitchBook Data, Inc. Contents are based on information from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. Nothing herein should be construed as any past, current or future recommendation to buy or sell any security or an offer to sell, or a solicitation of an offer to buy any security. This material does not purport to contain all of the information that a prospective investor may wish to consider and is not to be relied upon as such or used in substitution for the exercise of independent judgment.

Introduction 3

Review: Austin in the US venture

ecosystem4

Economy 5

Investment activity 6-10

Exits & fundraising 11-12

Select league tables 13

The PitchBook PlatformThe data in this report comes from the PitchBook Platform–our data software for

VC, PE and M&A. Contact [email protected] to request a free trial.

Photo courtesy of Eric Hunt, Wikimedia Commons.

Contents

2 PITCHBOOK 2016 VENTURE ECOSYSTEM FACTBOOK: AUSTIN

A promising venture ecosystem facing hurdlesIntroduction

When it comes to analyzing trends in venture investment, thinking in terms

of an ecosystem is one of the more powerful approaches, as much within

venture capital is not quite as quantifiable as one would like. Moreover, framing

an investment ecosystem as an overlapping, interlocking system of cycles is

especially illuminating when it comes to analysis of VC within a specific region,

given the interplay between general business cycles, fund investing lifecycles,

policy mandates and more. For example, the primary narrative for the US venture

industry throughout 2016 has been a decline in activity even as valuations

have remained relatively strong, with certain metropolitan areas enjoying more

resilient numbers than others. But when zeroing in on one of those metropolitan

areas, the location-specific historical trend in the supply of startups jockeying for

and garnering VC investment becomes a more critical component for analysis.

The metro-specific growth over the past several years also matters considerably.

On top of that, it’s important to highlight how metro-specific venture activity

is necessarily limited by the speed of the spread of viable information within a

given network, plus the size of the nodes in a venture network, i.e. the size of

capital sources. Likewise, livability and interconnectivity within a metro matter,

ranging from metrics such as ease of doing business to tax rates to typical rents

to sprawl. The purpose of this PitchBook report series is to place PitchBook

venture data within a broader context on a more geography-specific basis, the

better to illustrate potential use cases for analysis. It’s critical to note that within

that broader context one must take timing into account. The growth percentage

over time is an important indicator of a venture ecosystem’s overall health, as

one of my collaborators remarked during our review, and there is always more to

any existing ecosystem than can be rendered in a dataset.

As this is the inaugural installment of the metro-specific series, we welcome your

feedback and questions—reach out to us at [email protected]. I’d like

to thank S3 Ventures, Sante Ventures, the Austin Chamber of Commerce, PTV

Healthcare Capital, and the National Venture Capital Association, among others

whom assisted in the production of this report.

GARRETT JAMES BLACK

Senior Analyst

Look up a company.

And its cap table.

And its investors.

And its EBITDA

multiples.

And its board

members.

In seconds.

The PitchBook Platform

has the data you need

to close your next deal.

Learn more at

pitchbook.com

3 PITCHBOOK 2016 VENTURE ECOSYSTEM FACTBOOK: AUSTIN

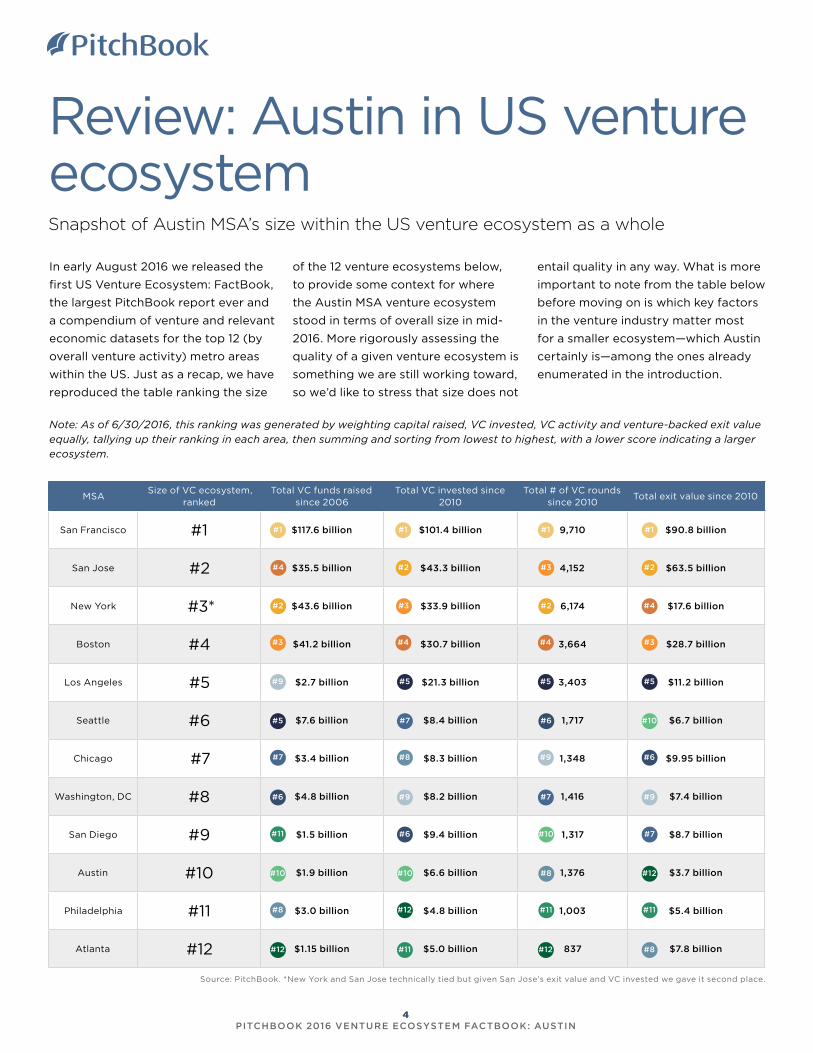

Review: Austin in US venture ecosystemSnapshot of Austin MSA’s size within the US venture ecosystem as a whole

In early August 2016 we released the

first US Venture Ecosystem: FactBook,

the largest PitchBook report ever and

a compendium of venture and relevant

economic datasets for the top 12 (by

overall venture activity) metro areas

within the US. Just as a recap, we have

reproduced the table ranking the size

Source: PitchBook. *New York and San Jose technically tied but given San Jose’s exit value and VC invested we gave it second place.

Note: As of 6/30/2016, this ranking was generated by weighting capital raised, VC invested, VC activity and venture-backed exit value equally, tallying up their ranking in each area, then summing and sorting from lowest to highest, with a lower score indicating a larger ecosystem.

MSASize of VC ecosystem,

rankedTotal VC funds raised

since 2006Total VC invested since

2010Total # of VC rounds

since 2010Total exit value since 2010

San Francisco #1 $117.6 billion $101.4 billion 9,710 $90.8 billion

San Jose #2 $35.5 billion $43.3 billion 4,152 $63.5 billion

New York #3* $43.6 billion $33.9 billion 6,174 $17.6 billion

Boston #4 $41.2 billion $30.7 billion 3,664 $28.7 billion

Los Angeles #5 $2.7 billion $21.3 billion 3,403 $11.2 billion

Seattle #6 $7.6 billion $8.4 billion 1,717 $6.7 billion

Chicago #7 $3.4 billion $8.3 billion 1,348 $9.95 billion

Washington, DC #8 $4.8 billion $8.2 billion 1,416 $7.4 billion

San Diego #9 $1.5 billion $9.4 billion 1,317 $8.7 billion

Austin #10 $1.9 billion $6.6 billion 1,376 $3.7 billion

Philadelphia #11 $3.0 billion $4.8 billion 1,003 $5.4 billion

Atlanta #12 $1.15 billion $5.0 billion 837 $7.8 billion

#1

#2

#1

#3

#4

#5

#6

#7

#8

#9

#10

#11

#12

#1 #1

#2

#2 #2#4

#3

#5

#6

#7

#8

#9

#10

#11

#12

#3

#4

#5

#7

#8

#6

#9

#10

#11

#12

#4

#3

#5

#6

#7

#10

#9

#12

#11

#8

of the 12 venture ecosystems below,

to provide some context for where

the Austin MSA venture ecosystem

stood in terms of overall size in mid-

2016. More rigorously assessing the

quality of a given venture ecosystem is

something we are still working toward,

so we’d like to stress that size does not

entail quality in any way. What is more

important to note from the table below

before moving on is which key factors

in the venture industry matter most

for a smaller ecosystem—which Austin

certainly is—among the ones already

enumerated in the introduction.

4 PITCHBOOK 2016 VENTURE ECOSYSTEM FACTBOOK: AUSTIN

EconomyAustin’s current economic condition & recent trends

When assessing how the health of the

local economy impacts the venture

ecosystem, some primary factors to

look at are tax burdens, relative wages,

rental rates and the supply of talent.

Seasonal temporary hiring contributed

to Austin’s unadjusted employment

rate declining to 3% in December

2016, while Texas on the whole saw

a 4.6% seasonally adjusted jobless

rate in November 2016, per the Texas

Workforce Commission. Austin and

Texas on the whole are still exhibiting

significantly strong numbers, but

by and large it appears the marked

expansion since the financial crisis is

slowing. The Federal Reserve Bank of

Dallas released data in late December

showing the Austin Business-Cycle

Index grew by an annualized rate of

2.9% in October 2016, considerably

below relative to the last decade as a

whole. We emphasize year-over-year

changes—the better to gauge more

recent changes that will have affected

current sentiment—so the impact of

monthly or quarterly influxes of data

do not overly drown out longer-term

trends. Such longer-term perspectives

are crucial to take into account when

considering typical venture investment

cycles. That said, a more recent decline

in economic indicators, however, will

contribute to and may have already

clouded domestic and outside investor

sentiment, at least somewhat. For now,

the state of the Austin economy is still

quite healthy—any negative changes

are distinct mainly due to the fact they

are in proportion to previous, markedly

strong numbers.

A brief note on Austin’s livability: Given

the increasing popularity of events

such as SXSW and Austin’s persisting

Austin metropolitan statistical areaSelect

statistics

Labor force, 2016* 1,101,336

Labor force growth, Oct. ‘15-Oct. ‘16 2.3%

Employment growth, Oct. ‘15-Oct. ‘16 2.4%

Unemployment growth, Oct. ‘15-Oct. ‘16 -0.9%

Average hourly earnings of all employees, August 2016 $27.35

Growth in average hourly earnings of all employees, 2015 YTD-2016 YTD 2.4%

Change in existing building inventory, 2015 YTD-2016 YTD 0.93%

Change in vacancy rate, 2015 YTD-2016 YTD -0.2%

Change in quoted full-service equivalent rental rates 8.2%

Quoted full-service equivalency rental rate $32.7

Change in existing home sales, 2015 YTD-2016 YTD 3.8%

Change in existing home average price, 2015 YTD-2016 YTD 5.3%

Metro Business Cycle Index, August 2016 (Oct. 1980=100) 795.34

Change in Metro Business Cycle Index, 2015 YTD-2016 YTD 6.4%

Austin Business-Cycle Index, October 2016* 2.9%

Monthly change in unemployment rate, September 2016-October 2016* -0.2%

Change in percentage of homes sold that were affordable for median-income families, 2Q 2016-3Q 2016*

2.4%

Sources: US Bureau of Labor Statistics, CoStar Group, Federal Reserve Bank of Dallas, Real Estate Center

at Texas A+M University & National Association of Realtors, & Texas Workforce Commission, data not

seasonally adjusted. YTD as of 11/19/2016 excepting average hourly earnings, which are as of 9/29/2016.

Office rental data is as of 10/6/2016, residential as of 11/1/2016. *As of 12/1/2016.

Texas has no corporate, individual income or state property tax. It also ranks 41st among the 50 US states in taxes paid per $1,000 of personal income, at $88.

cultural reputation, as well as a sizable

transportation bill that passed recently

and input from multiple domestic

parties, it appears the area is still

and will remain quite attractive as a

residence for some time.

5 PITCHBOOK 2016 VENTURE ECOSYSTEM FACTBOOK: AUSTIN

Austin MSA venture activity

Source: PitchBook

Overall, the rate of venture investing in Austin startups has slid

considerably, after a boom period of two years straight

Austin MSA venture activity

Investment activityAn overview of Austin’s venture investment activity

$633

$846

$905

$459

$688

$881

$996

$811

$1,4

24

$1,2

91

$978

78102 98

107134

156

190

251286 296

199

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Deal Value ($M) # of Deals Closed

Investment in Austin-based startups

is on the downswing relative to

elevated activity from 2014 to 2015.

Beginning in the final quarter of 2015,

activity has oscillated in a subdued

fashion on a quarterly basis, although

aggregate capital invested flatlined

in the back half of 2016. There are

multiple challenges that could

contribute to a cyclical downturn

within Austin specifically, relative

to the nationwide decline. As we’ve

already seen, the local economy is

healthy, but among these challenges

are: an insufficient supply of startups

decreasing the probability of VCs

finding worthwhile opportunities; lack

of robust domestic sources of capital;

declining interest on the part of both

local and outside investors due to

increases in perception of risk; and a

sluggish recycling of capital. So which

of these are most relevant for Austin,

right now?

0

10

20

30

40

50

60

70

80

90

$0.0

$100.0

$200.0

$300.0

$400.0

$500.0

$600.0

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2010 2011 2012 2013 2014 2015 2016

Deal Value ($M) # of Deals Closed

Source: PitchBook

6 PITCHBOOK 2016 VENTURE ECOSYSTEM FACTBOOK: AUSTIN

First financings have also declined considerably in number through the

end of 2016 but value has remained stable

First-time financings of Austin MSA-based startups

$150

$148

$167

$105

$103

$119

$249

$103

$197

$189

$144

2539 38

43

55 5765

9687 85

49

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Deal Value ($M) # of Deals Closed

Source: PitchBook

Activity may be declining, but median sums invested

remain resolutely high

Median venture financing size ($M) in Austin MSA

Valuations are either up or at least staying flat

Median venture financing post valuation ($M) in Austin

MSA

$0.7 $1.0

$3.96 $4.0

$5.9

$9.3

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Angel/Seed Early Stage VC Later Stage VC

$5.0 $4.5

$20.8 $21.5

$33.5

$60.0

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

$70.0

$80.0

$90.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Angel/Seed Early Stage VC Later Stage VC

According to the most recent edition

of the Kauffman Index of Startup

Activity, the Austin metro area

ranked first in the US in its rate of

new entrepreneurs and fourth in

terms of startup density (defined as

number of startups per 1,000 firm

population), plus second in growth

entrepreneurship. It should be noted

that the composition of that startup

population is diverse enough that it

may not be exactly representative

of the types of industries that are

likely to attract venture capital—food

vendors such as taco trucks, for

instance. The strong supply of new

business formation makes sense in the

context of economic data—it’s simply

less expensive to build companies in

Austin. Accordingly, the total supply

of startups likely to vie for funding is

not as much of an issue, from both

quantitative and anecdotal angles.

But inflated financings and valuations

are. Coupled with a decline in

financing activity overall plus a

drop-off in the number of first-time

financings (although VC invested in

first-time rounds is quite robust), the

resolutely high median financing size

and post-valuation—particularly at

the late stage—imply that investors’

supply of capital is still ample, yet the

benchmarks for obtaining financings

of such size have shifted upward. Each

venture ecosystem across the US will

experience somewhat insulated rises in

those metrics, interconnected as they

are by information flow but insulated

somewhat by relative costs and

available/willing sources of capital. It’s

easy to ascribe such a shift to a typical

period in any investment cycle where

Source: PitchBook Source: PitchBook

7 PITCHBOOK 2016 VENTURE ECOSYSTEM FACTBOOK: AUSTIN

Aligning with national trends, early-stage numbers

have been hit hard

Austin MSA VC activity (#) by round size

Capital invested in significantly sized rounds has

declined but not as sharply

Austin MSA VC activity ($M) by round size

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Under $500K $500K-$1M $1M-$5M

$5M-$10M $10M-$25M $25M+

0

50

100

150

200

250

300

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Under $500K $500K-$1M $1M-$5M

$5M-$10M $10M-$25M $25M+

Proportionally, later stages are still resilient yet Series

A financings hit a multiyear low in 2016

Austin MSA VC activity (#) by series

Quite coincidentally, Series B financings saw no less

than $211.5M in total value in 2016

Austin MSA VC activity ($M) by series

Source: PitchBook

investors fear of overexuberance

and oversupply of capital leading to

slumping returns on sums invested

and consequently begin to pull back

somewhat. Thus, once reversion to the

mean has completed, Austin is likely

to see venture financing creep up

once more, barring significant macro

shocks.

However, when it comes to metro-level

analysis, the pipeline of previously

financed companies eligible for

follow-on rounds becomes more

crucial. Sufficient levels of funding

across the entire capital stack has a

greater impact when analyzing overall

activity on a metro scale. There was

a significant ramp-up in seed-stage

financings in tandem with a much

more modest increase in Series A

fundings across the past few years,

for example. This increase doubtless

already fed into Series A financings

that are occurring now. Yet any

potential slump in the seed stage such

as that which was observed in 2016

through late November could portend

ill for the width of the startup pipeline

when it comes to Series A funding

down the line. Such a phenomenon

could well have come into effect in

2016 already, happening to any given

series of financing and subsequent

rounds. Accordingly, with overall

supply not being an issue yet the

benchmarks of quality for startups to

garner venture financing having moved

upward in a highly valued climate, the

0

20

40

60

80

100

120

140

160

180

200

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Seed Series A Series B

Series C Series D+

$0.0

$200.0

$400.0

$600.0

$800.0

$1,000.0

$1,200.0

$1,400.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Seed Series A Series B

Series C Series D+

Source: PitchBook

Source: PitchBookSource: PitchBook

8 PITCHBOOK 2016 VENTURE ECOSYSTEM FACTBOOK: AUSTIN

Austin MSA VC activity ($M) by sector

Austin MSA VC activity (#) by sector

0%

20%

40%

60%

80%

100%

2010 2011 2012 2013 2014 2015 2016

CommercialServicesConsumer Goods& RecreationEnergy

HC Devices &SuppliesHC Services &SystemsIT Hardware

Media

Other

Pharma & Biotech

Software

0%

20%

40%

60%

80%

100%

2010 2011 2012 2013 2014 2015 2016

CommercialServicesConsumer Goods& RecreationEnergy

HC Devices &SuppliesHC Services &SystemsIT Hardware

Media

Other

Pharma & Biotech

Software

Source: PitchBook

Austin MSA VC activity in healthcare devices & services

$14

$55

$103

$16

$48

$29

$71

$114

$27

$37

$23

4

5

8 8

10

7

9 9

6

1211

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Deal Value ($M) # of Deals Closed

stutter in the startup pipeline could

lead to repercussions in the years to

come for the Austin area.

However, the timeline of supply is

also regulated by ongoing startup

activity within sectors more primed

to attract venture investors’ interest.

Particularly analyzing within an

ecosystem framework, the formation

of sizable new educational institutions

or headquarters relocations of major

companies plays into such associated

startup formation considerably. The

opening of the new Dell Seton Medical

Center as well as the establishment

of a nonprofit—Capital City

Innovation—that will target connecting

entrepreneurs with the healthcare

research and development efforts at

the new center could help engender

the creation of new healthcare-

related startups. Anecdotally, the

healthcare sector pipeline is still

underrepresented in Austin—if not

the nation—as of late in the gradual

recovery since the financial crisis,

barring a gradual uptick in Austin over

the past few years. Sector diversity

within a venture ecosystem matters

more and more nowadays for long-

term health. Particularly as the lines

between various sectors blur with

advances in enterprise-specific

software programs and advances in

certain hardware segments, a truly

thriving venture/startup ecosystem will

see more startups geared toward such

confluences. Similar interactions are

crucial for sectors apart from general

consumer and enterprise software,

which have benefited more directly

than most from the dramatic decrease

in launching costs over the past 15

years. Examples include startups

targeting medical records systems in

particular with tailored capabilities as

opposed to, say, a general filesharing

service like Dropbox.

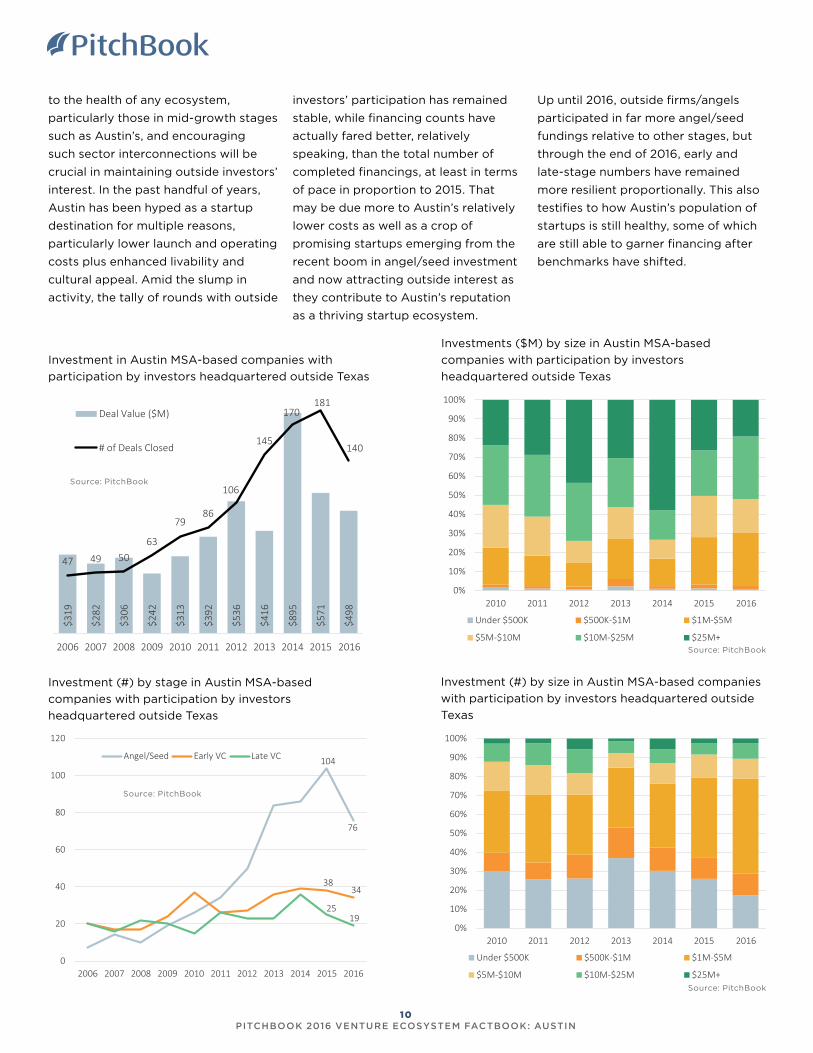

Drawing outside investment is critical

Source: PitchBook

Source: PitchBook

9 PITCHBOOK 2016 VENTURE ECOSYSTEM FACTBOOK: AUSTIN

Investment in Austin MSA-based companies with

participation by investors headquartered outside Texas

Investments ($M) by size in Austin MSA-based

companies with participation by investors

headquartered outside Texas

$319

$282

$306

$242

$313

$392

$536

$416

$895

$571

$498

47 49 5063

7986

106

145

170181

140

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Deal Value ($M)

# of Deals Closed

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016

Under $500K $500K-$1M $1M-$5M

$5M-$10M $10M-$25M $25M+

Investment (#) by size in Austin MSA-based companies

with participation by investors headquartered outside

Texas

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016

Under $500K $500K-$1M $1M-$5M

$5M-$10M $10M-$25M $25M+

Investment (#) by stage in Austin MSA-based

companies with participation by investors

headquartered outside Texas

104

76

3834

2519

0

20

40

60

80

100

120

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Angel/Seed Early VC Late VC

to the health of any ecosystem,

particularly those in mid-growth stages

such as Austin’s, and encouraging

such sector interconnections will be

crucial in maintaining outside investors’

interest. In the past handful of years,

Austin has been hyped as a startup

destination for multiple reasons,

particularly lower launch and operating

costs plus enhanced livability and

cultural appeal. Amid the slump in

activity, the tally of rounds with outside

investors’ participation has remained

stable, while financing counts have

actually fared better, relatively

speaking, than the total number of

completed financings, at least in terms

of pace in proportion to 2015. That

may be due more to Austin’s relatively

lower costs as well as a crop of

promising startups emerging from the

recent boom in angel/seed investment

and now attracting outside interest as

they contribute to Austin’s reputation

as a thriving startup ecosystem.

Up until 2016, outside firms/angels

participated in far more angel/seed

fundings relative to other stages, but

through the end of 2016, early and

late-stage numbers have remained

more resilient proportionally. This also

testifies to how Austin’s population of

startups is still healthy, some of which

are still able to garner financing after

benchmarks have shifted.

Source: PitchBook

Source: PitchBook

Source: PitchBook

Source: PitchBook

10 PITCHBOOK 2016 VENTURE ECOSYSTEM FACTBOOK: AUSTIN

Exits & fundraisingDatasets of venture-backed exits and local venture fundraising in Austin

Given the historical scale of Austin exits, activity in 2016 has been

relatively healthy, although value was toward the lower end

Venture-backed exits of Austin MSA-based companies

$190

$156

$391

$986

$859

$604

$520

$502

$254

$530

$361

12

7

12

14

19 18

23

19

24

1817

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Exit Value ($M) # of Exits

Corporate buyers still shell out the most, however

Venture-backed exits ($M) by type of Austin MSA-

based companies

Interestingly, acquisitions are at a decade low

Venture-backed exits (#) by type of Austin MSA-based

companies

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016Acquisition Buyout IPO

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016Acquisition Buyout IPO

A central component of any venture

ecosystem is the recycling of dollars

invested by both LPs and GPs. In

the overall fundraising and investing

cycle, attrition will occur at certain

periods, yet if long-term fund

economics do not work out, with

fund investors eventually getting

their money back, then any local

ecosystem cannot survive. And, to

reiterate an earlier point, without a

reasonably healthy local ecosystem,

outside investment simply will not be

feasible. Accordingly, the relatively

stable level of venture-backed exits of

Austin-based companies in 2016 bodes

well, although the total value exited

is toward the lower end of historical

tallies. However, considering the

natural lag between investment and

exit periods, 2016 exit value is decent

relative to annual sums invested

between 2006 and 2013.

Source: PitchBook

Source: PitchBook Source: PitchBook

11 PITCHBOOK 2016 VENTURE ECOSYSTEM FACTBOOK: AUSTIN

A clear majority of exit value in several sizable sales

Venture-backed exits of Austin MSA-based companies

($M) by size

A fair number of lucrative exits occurred

Venture-backed exits of Austin MSA-based companies

(#) by size

The peak of domestic fundraising is still carrying forward, given typical

investment lifecycles

Austin MSA venture fundraising

$821

$20

$147

$0 $39

$105

$462

$268

$97

$75

4

1

2 2

3 3

4 4

1 1

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Capital Raised ($B)

# of Funds Closed

Source: PitchBook

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Under $25M $25M-$50M $50M-$100M $100M-$500M

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Under $25M $25M-$50M $50M-$100M $100M-$500M

The timing of fundraising and exit

cycles could be initially presumed

to roughly sync, with a successful

fundraising period overlapping

somewhat with hefty sums exited,

yet the impact of hype cycles and

flourishing local startup scenes should

not be overlooked. Hence the surge in

domestic funds closed between 2013

and 2014. Many of the funds raised

even two to three years ago are likely

still investing, although some are

perhaps nearing the tail end of their

active period. With outside investors

still maintaining a significant presence

in Austin, the role of local firms in

syndicates will still be crucial, yet

not solely responsible for bolstering

investment totals. That said, greater

growth is unlikely to occur without a

ramp-up in domestic fundraising.

Source: PitchBook Source: PitchBook

12 PITCHBOOK 2016 VENTURE ECOSYSTEM FACTBOOK: AUSTIN

Capital Factory 10

Silverton Partners 9

Central Texas Angel Network 9

LiveOak Venture Partners 5

Mercury Fund 5

Wild Basin Investments 5

ATX Seed Ventures 4

Floodgate Fund 4

S3 Ventures 4

Techstars 4

UT Horizon Fund 4

Altos Ventures 3

Founders Fund 3

Frontier Tech Ventures 3

New Science Ventures 3

Noro-Moseley Partners 3

Most active investors in Austin MSA

Venture capitalVenture capital, for the purposes of this report, is defined as institutional investors that have raised a fund structured as a limited

partnership from a group of accredited investors, or a corporate entity making venture capital investments.

ValuationsPre-money valuation: the valuation of a company prior to the round of investment. Post-money valuation: the valuation of a company

following an investment.

Exits

This report includes both full and partial exits via mergers and acquisitions, private equity buyouts and IPOs.

FundraisingThis report includes Austin-based venture capital funds that have held a final close. Funds-of-funds and secondary funds are not

included.

All league tables are compiled using the number of completed VC rounds for Austin MSA or Austin-based companies in 2016 through December 31. To ensure your firm is accurately represented in future PitchBook reports, please contact [email protected].

Source: PitchBook

Company Deal size ($M)Series/stage

Sector Select investors

Pivot3 $55.5 CSystems & info mgmt

Argonaut Private Equity, S3 Ventures

Spredfast $50.1 FMedia & info

servicesRiverwood Capital

Lumos Pharma $34 BDrug

discoveryDeerfield Management

Bigcommerce $30 EBusiness/

productivity software

GGV Capital, American Express Ventures, SoftBank Capital

Silvercar $28 C AutomotiveAudi of America, Austin

Ventures

CognitiveScale $21.8 BSystems & info mgmt

Norwest Venture Partners, Intel Capital

FloSports $21.2 BSocial/

platform software

DCM Ventures, Bertelsmann Digital Media Investments

Twyla $19 ASpecialty

retailGoogle Ventures

OutboundEngine $18 CMedia & info

services

S3 Ventures, Altos Ventures, Silverton

Partners

ESO Solutions $17.7 CMedical records systems

Accel-KKR, Wild Basin Investments

The Zebra $17 AMedia & info

servicesBallast Point Ventures,

Daher Capital

TrendKite $16.3 DBusiness/

productivity software

Adams Street Partners, Mercury Fund

Source: PitchBook

Select league tablesSelect rankings of most active investors and deals in Austin

Select 2016 venture financings of companies headquartered in Austin

13 PITCHBOOK 2016 VENTURE ECOSYSTEM FACTBOOK: AUSTIN

See how the PitchBook Platform can

help your private equity firm close your

next deal.

We do EBITDA multiples,private comps,valuations,market trends,growth metrics.

You build a better portfolio.