BUSINESS STUDIESGrade 10

TERM 1Business environment

and Business operations

MICRO ENVIRONMENT

THE MICRO ENVIRONMENT AND THE BUSINESS ENVIRONMENT

Businesses operate in the business environment.

The business environment is made up of three components:

* Micro environment

* Market environment

* Macro environment

MICRO ENVIRONMENT…

1. Vision, mission statement, goals and objectives

2. Organisational culture

3. Organisational resources

4. Management and leadership

5. Business organisational structure

6. Eight business functions

MARKET ENVIRONMENT...

7. The market

8. Suppliers

9. Intermediaries

10. Competitors

11. Other organisations:

11.1 CBO’s

11.2 NGO’s

11.3 Regulators

11.4 Strategic allies

11.5 Unions

12. Opportunities and threats

MACRO ENVIRONMENT...

13. Physical/natural environment

14. Economic environment

15. Social, culture and demographic environment

16. Technological environment

17. Legal and political environment

18. Internasional/Global environment

19. Institutional environment

CHARACTERISTICS OF THE MICRO ENVIRONMENT

Is the business itself.

Also known as the internal environment.

Businesses have full control.

COMPONENTS AND FEATURES OF THE MICRO BUSINESS ENVIRONMENT The micro environment is made up of the

following components:

• Vision (describes what a business wants to achieve in the long term)

• Mission (describes the reason for a business’s existence)

• Strategy (describes how a business will achieve its goals)

• Goals (translates the vision and mission into performance target, include deadline for achievement for each goal)

The vision, mission statement, strategy and goals all describe what a business wants to achieve.

Organisational culture:

• Refers to the way in which things are done in an enterprise.

• Includes aspects such as employees’ dress code and the manner in which employees address each other.

• Organisational culture is also influenced by the culture of employees.

Organisational resources:

• Refer to all the resources that a business enterprise uses – make sure that it operates efficiently.

• Enterprises need:

* capital resources Called also:

* human resources factors of

* natural resources production

* entrepreneurial resources

• Each factor of production has its own remuneration (“payment” for that particular factor of production)

Resources

Capital resources

Description

Money that is invested in a business, so that the business can acquire capital goods, for example land, buildings and equipment.

Remuneration

Interest

Resources

Human resources

Description

The work people do to produce products and services – called labour.

Remuneration

Salaries and wages

Resources

Natural resources

Description

All natural assests used to produce products and services – example: water, coal and gold.

Remuneration

Rent

Resources

Entrepreneurial resources

Description

People that combine the above mentioned factors of production in such a way that the business becomes operational and profitable.

Remuneration

Profit

MANAGEMENT AND LEADERSHIP

Managers and leaders are responsible for making sure that a business achieves its goals.

DIFFERENCE BETWEEN MANAGERS AND LEADERS

MANAGERS

Holds a particular position in an enterprise, e.g. Financial manager.

A person can only become a manager if there is a vacant managerial position in a business.

A manager gives instructions to subordinates and checks that these tasks are carried out.

A manager has the authority to tell subordinates what to do.

DEFFERENCE BETWEEN MANAGERS AND LEADERS

LEADERS

A leader does not necessarily hold a managerial position – any employee can be a leader.

A leader emerges when there is a need for leadership in a group – leadership is a characteristic.

A leader is usually part of a team and helps to perform tasks.

A leader usually inspires team members to perform.

8 BUSINESS FUNCTIONS CAN BE IDENTIFIED IN A BUSINESS ENTERPRISE

1. Purchasing function

2. Production function

3. Public relations function

4. General management function

8 BUSINESS FUNCTIONS CAN BE IDENTIFIED IN A BUSINESS ENTERPRISE

5. Marketing function

6. Human resources function

7. Administration function

8. Financial function

(A) GENERAL MANAGEMENT

It is the responsibility of general management to ensure

that all business functions operate efficiently.

LEVELS OF MANAGEMENT

There are three levels of management, each with its own

roles and responsibilities.

LEVELS OF MANAGEMENT

Top level

Middle level

Lower level

TOP LEVEL MANAGEMENT

Top level managers are people like:

• Chief Executive Officers (CEO’s)• Directors of companies• Owners of sole traders or partners in partnerships

Top level managers look at a business and its activities as a whole.

ROLES AND RESPONSIBILITIES

Plans for the future of the enterprise.

Monitors the business’s relationship with the external environment.

Manages change in the business environment.

Determine the vision, mission, strategy and objectives – ensure that the business achieves it.

Makes strategic decisions – long term example: change its packaging.

MIDDLE LEVEL

Managers are the heads of the different departments.

They have specialised knowledge of the activities that must be performed in the department under their management.

ROLES AND RESPONSIBILITIES

Serves a link between top level management and lower level management.

Implements plans made by top level management by making tactical decisions.

Manages each department, example: marketing department.

Achieves the goals and objectives set for a particular department.

Acquires resources needed in a particular department.

LOWER LEVEL MANAGEMENT

Are the lowest level of management.

Known as first line or supervisory management.

Are foremen and team leaders.

They possess technical knowledge and have the ability to guide and motivate workers.

ROLES AND RESPONSIBILITIES

Serves as a link between the heads of the different departments and the workers on ground level.

Carries out tactical decisions made by middle management.

Utilises the resources acquired by middle management to execute daily instructions.

Make routine type decisions.

Responsible for achieving daily objectives..

Executes instructions given by middle management.

MANAGEMENT TASKS

Planning

The process of setting goals and making plans to achieve these goals.

Done by managers on all three levels of management.

Top management plans for the long term future of an enterprise.

Top management plans how an enterpise will achieve its overall goals.

MANAGEMENT TASKS

Middle level management plans for the medium term.

Middle level management plans how each departement will achieve its goals.

Lower level management plans for the short term.

Lower level management plans for the achievement of operational targets on a daily basis.

MANAGEMENT TASKS

Organising

Refer to the way in which employees in an enterprise are arranged in order to carry out plans.

Responsibilities and duties.

Describes what tasks employees are responsible for, who employees must report to and from whom orders must be taken.

Employees in an enterprise can be organised in different organisational structures.

MANAGEMENT TASKS

Activating

To start doing the work that will enable an enterpise to achieve its goals.

MANAGEMENT TASKS

Leading

To guide employees through their duties and responsibilities.

Involves inspiring employees to achieve the business’s goals.

MANAGEMENT TASKS

Directing

Ensuring that a business runs smoothly.

Involves establishment of a productive working climate, supervising and making sure that effective communication

channels are in place.

MANAGEMENT TASKS

Controlling

Making sure that tasks are carried out as planned.

Involves comparing actual results with the goals set by management.

Corrective measures must be taken if there is a difference between actual results and the goals the business set out to achieve.

MANAGEMENT TASKS Risk Management

Although risk management is not classified as a traditional management task, it remains an important management

responsiblility.

Involves identifying risks and finding strategies to deal with risks.

The following steps are involved:

1. Identify threats/risks from all business environment.2. Determine the extent to which the business is exposed to these

threats.3. Evaluate the risk.4. Control the risk by minising losses.5. Finance the risk by working possible losses into the budget.

ORGANISATIONAL STRUCTURES

1. Organisational structure indicates:

• Give instructions• Feedback• Communication between managers and

employees and among employees.

2. There are different organisational structures which are suitable in different types of businesses and different types of situations.

LINE ORGANISATIONAL STRUCTURE

1. Oldest organisational structure.

2. Most suitable for small business enterprises.

3. Allows for fast decision making – managers hold the authority to make decisions without having to consult with other employees.

4. Authority flows from the most senior person in a business in a downward line to employees on the lowest level of an enterprise.

FUNCTIONAL ORGANISATIONAL STRUCTURE

1. Similar to line organsation – provides for larger businesses.

2. The same type of work is grouped together in functional departments.

3. Each department is managed by a manager who is an expert in his/her field.

4. Each department performs its activity for the whole business – marketing department handles the marketing.

LINE STRUCTURE

1. Line organisational structure forms the basis of the line and staff organisational structure.

2. Experts act as advisors for managers.

3. Managers are known as line managers, while the experts or advisors are known as staff officers.

4. Advisors don’t have any authority over employees.

5. Allows for quick decision making and a quick flow of authority.

6. Suitable for large businesses.

PROJECT OR MATRIX ORGANISATIONAL STRUCTURE

1. Team members from different departments come together to complete a project.

2. Project teams are headed by project managers.

3. Once the project is completed, teams dissolve and return to their departments.

4. Therefore, this is a temporary structure.

5. While team members are working on a project, orders are taken from the project manager, as well as the manager from the department that employees are from.

6. Conflict of loyalty can arise between project managers and functional managers.

THE RESPONSIBILITIES OF MANAGEMENT AND THE ALIGNMENT BETWEEN MANAGEMENT LEVELS

Top managemen

t

Middle management

Lower management

Alignment between levels

Management responsibilities

Plans for a business in its entirety, set the direction of a business.

Serves as a link between top management and lower level management, carries out decisions mand by top level management.

Carries out tactical decisions made by middle level.

Long term planning, making strategic decisions, managing change and risk.

Medium term planning, making tactical decisions, managing each department.

Short term planning, making tactical decisions, setting daily performance targets.

(B) ADMINISTRATIONRESPONSIBILITIES OF THE ADMINISTRATION FUNCTION

1. Collecting data and information.

2. Handeling data and information.

3. Managing information.

4. Office practice.

5. Information technology.

COLLECTING DATA AND INFORMATION

The administration function should collect data and

information which can assist management in decision

making, for example:

1. Market trends

2. Inflation rates

3. Interest rates

4. Sale figures

5. Stock levels

6. Information about suppliers

HANDELING DATA AND INFORMATION

Correspondence

All communcation to and from a business enterprise, whether oral or written.

Coping and duplicating

Information must be copied so that it is available to managers.

Some information is confidential and should be handled carefully.

HANDELING DATA AND INFORMATION

Filing and storing

Correspondence and records such as financial statements etc. Must be sorted and filed.

This information must be stored for future reference.

Indexing

File the same type of information together.

Index this information in terms of importance, date or nature.

HANDELING DATA AND INFORMATION

Handling of mail

Deliver mail to managers to ensure a quick response.

Distribution of information to management

Information must be distributed to managers so that they can identify opportunities and respond to threats.

HANDELING OF DATA AND INFORMATION

Accounting records

Must be kept to: keep record of all business transactions and set financial statements.

Statistics

Involves the collection and interpretation of raw data.

Enable managers to identify trends and to make informed decisions about the future of a business enterprise.

HANDELING OF DATA AND INFORMATION

Budgets

Estimates how much money a business will spend and receive during a particular financial year.

Different kinds of budgets include:

1. Marketing budget

2. Human resource budget

3. Production budget

4. Corporate social investment budget

MANAGING INFORMATION

1. Data must be collected and processed into meaningful information which is useful to management.

2. This information must assist management in making management decisions.

3. Information must be used to predict future trends and to transform these trends into strenghts and opportunities.

4. Information should be verified.

5. Information must be up to date and obtaining the information should be cost effective.

OFFICE PRACTICE

Refer to the way in which the administration function

handles activities such as:

1. Telephone etiquette.

2. The delivery of messages to applicable employees.

3. The way in which e-mails and faxes are handled in terms of ugency.

4. The number of copies which can be made by employees.

INFORMATION TECHNOLOGY (IT)

1. Information technology (IT) deals with the use of computers and computer software in order to convert, store, protect, process and retrieve information securely.

2. Include the field of electronic communication.

3. New term, Information and Communication Technology (ICT),

ICT REFER TO...

Telephones

An internal telephone system connects the business departments with the switchboard and each other.

An external telephone system enables a business to make external phone calls to people outside the enterpise and to other business

enterprises.

Fax machines

Enable us to send written documents to other people electronically.

ICT REFER TO...

Cell phones

Cell phones are wireless, cell phones enable us to reach people any time and any place.

Are used to make conference calls, which means that a person can telephonically communcate with several other people at the same

time.

Provide access to the internet.

ICT REFER TO...

Electronic sales terminals

Enable a person to pay for products with a debit or credit card.

The device is connected to the bank and money is transferred electronically from the buyer’s account to the seller’s account.

ICT REFER TO...

Photocopiers

Is used to copy, enlarge and reduce documents.

Copiers can also bind documents, punch or staple documents.

Copiers can be connected to computers instead of printers.

Documents are the printed by die copier – cheaper.

Most copiers, however, are maintenanace intensive.

ICT REFER TO...

Interactive white boards

Is a large, touch sensitive board which is connected to a digital projector and a computer.

The projector displays the image form the computer screen on the white board.

The computer is either controlled by touching the board directly, or with a special pen.

You can use your computer to create presentations on the white board.

Everything you write on the board is saved on your computer.

ICT REFER TO...

Computers

Used as communication medium for e-mailing and skype.

Skype is a programme that allows people to have telephone conversations via the internet.

A person can access the internet via computer.

Use various computer programmes.

(C) FINANCINGRESPONSIBILITIES OF THE FINANCIAL FUNCTION

1. To plan how money will be spent.

2. To get financing if necessary.

3. To make money available so that the business can operate efficiently.

4. To follow up on outstanding money.

5. To pay the business’s account.

IMPORTANT CONCEPTS

Income

Income is all the money that flows into the business.(example: interest)

Expenditure

Refers to money paid for things that a business needs, but won’t last.

(example: water and electricity)

IMPORTANT CONCEPTS

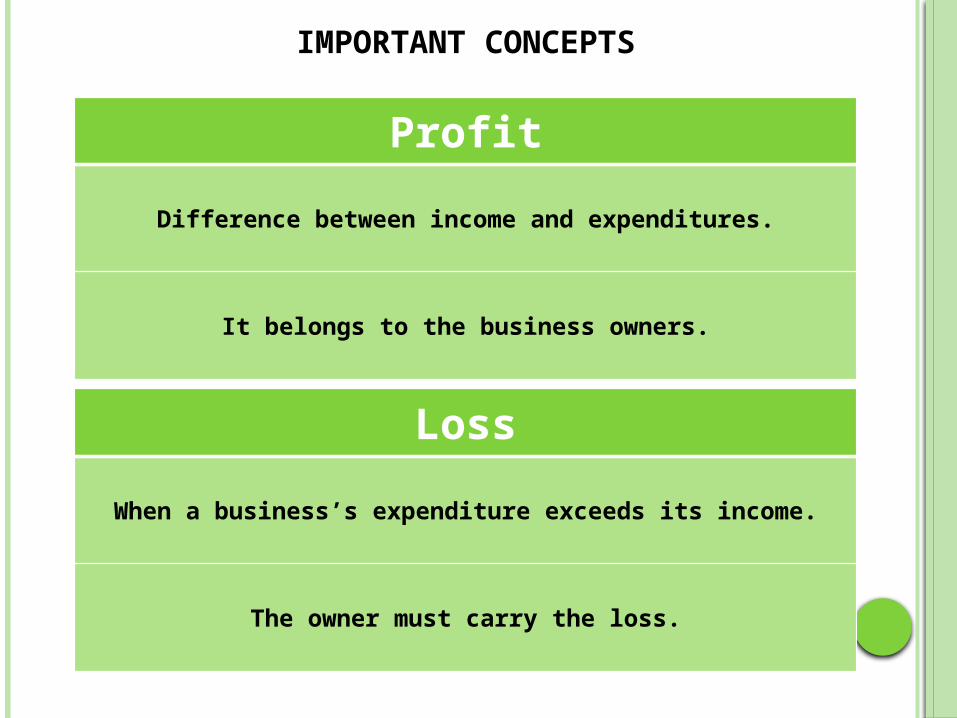

Profit

Difference between income and expenditures.

It belongs to the business owners.

Loss

When a business’s expenditure exceeds its income.

The owner must carry the loss.

IMPORTANT CONCEPTS

Assets

Remain in the business permanently.(example: equipment)

Things that can be turned into money.(example: trading stock)

Liabilities

Refer to all the money that the business owes to its creditors.

IMPORTANT CONCEPTS

Creditors

A business owes money to its creditors. Creditors are therefore liabilities.

Debtors

Owe money to a business. The debtor’s debt can be converted into cash and debtors are therefore classified as assets.

IMPORTANT CONCEPTS

Fixed capital

Portion of a business’s capital that is invested o non-current assets.

Working capital

Portion of a business’s capital that is used to buy trading stock and to pay for expenses.

TYPES OF FINANCING

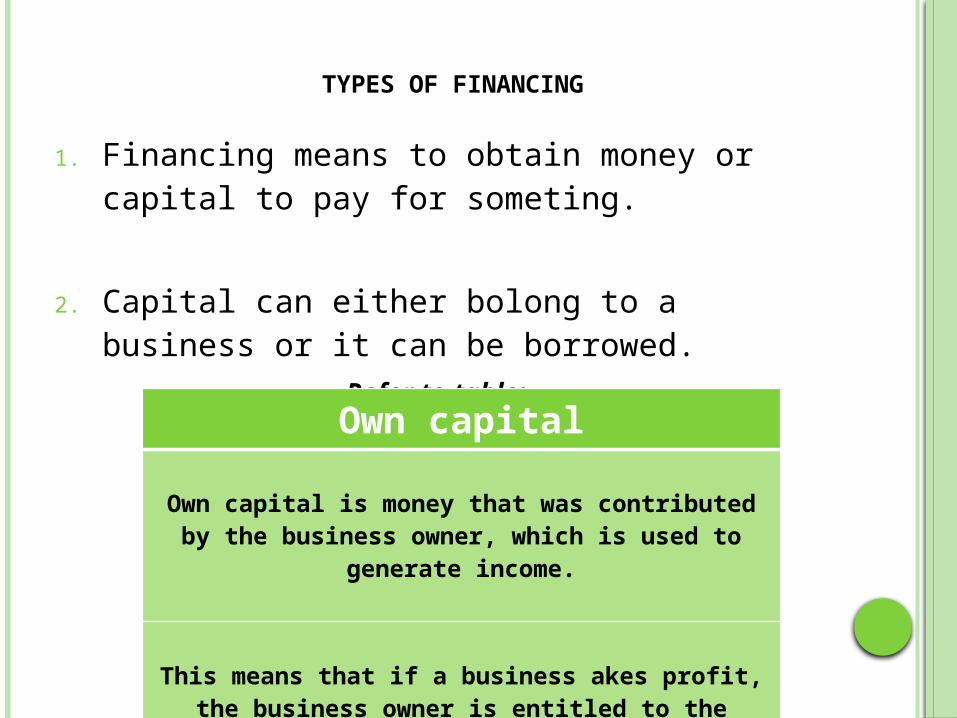

1. Financing means to obtain money or capital to pay for someting.

2. Capital can either bolong to a business or it can be borrowed.

Refer to table:

Own capital

Own capital is money that was contributed by the business owner, which is used to generate income.

This means that if a business akes profit, the business owner is entitled to the profit.

Borrowed capital

Obtained from financial institutions like banks.

Must be repaid with interest.

Long term borrowed capital, e.g. a mortgage bond.

Short term borrowed, e.g. a bank overdraft.

SOURCES OF FINANCING

Short term

Bank overdraftA business arranges with the bank to withdraw more

money than what is available in the business’s account.

Suppliers’ creditThe seleer has agreed that the buyer can take the

products that he/she requires and pay for them at a later stage.

Loan Money must be paid back with interest over a short term (5 years).

Lease account Instead of buying an asset, it can be hired.

SOURCES OF FINANCING

Long term

JSE A business can sell its shares to obtain capital.

LoanMoney must be paid back with interest over a long

term (sometimes up to 30 years).

Reserve funds A business can access money that was not distributed to a business’s owners.

BUDGETING

1. Serve as the business’s financial planning.

2. It is an indication of possible future income and expenditure.

3. There are two types of budgets:

Capital budget Cash budget

Determines a business’s fixed capital requirements.

Determines a business’s working capital requirements.

Focuses on the long term. Focuses on the short terum.

INTODUCTION TO INVESTMENTS

1. Refer to the use of money to generate wealth and income without having to work.

2. Businesses invest surplus funds.

3. Businesses appoint investment managers to look after its investment portfolio.

4. An investment portfolio refers to the different kinds of investments made by a business.

5. Money can be invested in, for example: Property, shares, gold etc.

TYPES OF CAPITAL

1. Fixed capital:

Capital which is invested in non-current assets such as vehicles, equipment, land and buildings.

2. Working capital:

Capital used to grant credit, buy stock and pay for expenses. Working capital is liquid which means that is flows out of the business on a regular basis.

(D) PURCHASINGRESPONSIBILITIES OF THE PURCHASING FUNCTION

1. To purchase everything a business needs to carry out its activities.

2. Managing stock.

3. Find the best suppliers.

4. Following up on orders that were placed with suppliers.

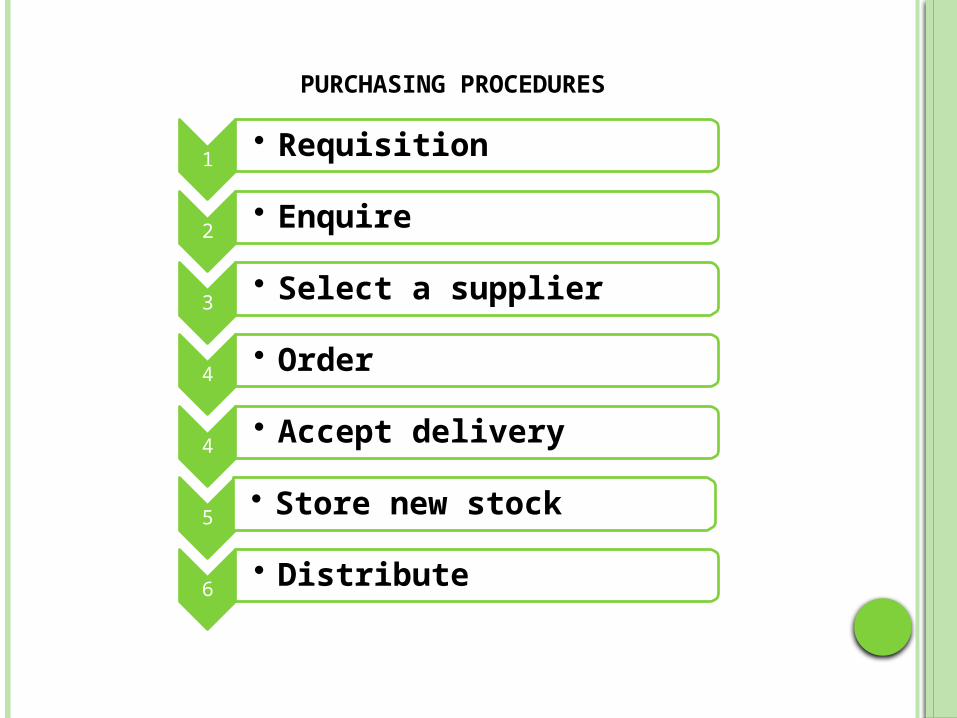

PURCHASING PROCEDURES

1• Requisition

2• Enquire

3• Select a supplier

4• Order

4• Accept delivery

5• Store new stock

6• Distribute

PURCHASING ACTIVITIES

Employees in the purchasing department will engage in the

following activities:

1. Making contact with the other business departments to determine each department’s needs.

2. Continuously looking for the best suppliers.

3. Ensuring that there is enough stock available.

4. Negotiating the best possible terms of payment with suppliers.

5. Placing orders with suppliers and following up.

6. Sending damaged goods back to the supplier.

CASH TRADING

Advantages:

1. Cash traders don’t have problems with unsettled debts.

2. No accounts have to be sent to debtors.

3. The cash seller will have cash available to pay current expenditures like water and electricity.

4. The cash purchaser can qualify for cash discount.

CASH TRADING

Disadvantages:

1. The cash trader can lose the support of customers who don’t have enough money to make cash purchases.

2. Money in a bank account earns interest – if a cash trader makes a payment, there is less money in that business’s bank account that can earn interest.

CREDIT TRADING

1. Takes place when goods that are sold and taken from the store are paid for at a later stage.

2. This means that business owners trust that consumers will pay for the products they have already taken, but not paid for.

3. Because the dredit trader has to wait for payment, he/she charges interest on the outstanding amount.

4. A credit trader usually allows 30, 60 or 90 days for accounts to be settled.

5. Some credit traders only allow 30 days.

CREDIT TRADING

Advantages:

1. Credit trader is entitled to charge more for his/her products to compensate for the time he/she waits for payment.

2. Credit purchasing enables people who can only afford to pay at the end of the month to satisfy urgent needs immediately.

3. Because purchased goods only need to be paid for later, the purchaser can earn interest on the money i his/her acount.

CREDIT TRADING

Disadvantages:

1. The credit trader will have to buy new stock before receiving payment form debtors.

2. There is always a risk of unsettled debts.

3. Accounts must be sent out to debtors.

STOCK CONTROL

Definition:

1. To monitor stock levels to ensure that the business keeps the right amount of stock.

2. If a business keeps too little stock, customers will buy the products they are looking for from another business.

3. However, if a business has too much stock, it will have to be stored.

STOCK CONTROL

Purpose:

1. To determine at any stage, without physical stock taking, the number and value of stock.

2. To ensure sufficient stock to meet normal demand for customers at all times.

3. Compare the stock on the shelves with stock records to detect obsolescence and theft.

STOCK CONTROL

Stockholding costs:

Stockholding costs:

1. Losses owing to dated and perished products

2. Losses owing to theft

3. Losses owing to fire

4. Insurance on stock in the storeroom

5. Costs associated with storage: rent, cold storage, electricity etc.

STOCK CONTROL

Important terms:

Minimum stock levels

The smallest amount of stock that must be kept to satisfy normal demand.

Maximum stock levels

Quantities of stock which should not be exceeded.

Standard orderFixed orders

Example: A café orders 100 bottels of milk per week.

Ordering levelRefers to the level of stock which should be

reached before new stock is ordered.

THE PURCHASING FUNCTION AND THE NATIONAL CREDIT ACT (ACT 34 OF 2005)

Reason:

1. Provide credit providers and consumers with guidelines relating to their rights and responsibilities.

2. A credit provider is a business or person who lends money to another person or business.

3. A credit applicant (consumer) is a business or person who needs to borrow money.

THE PURCHASING FUNCTION AND THE NATIONAL CREDIT ACT (ACT 34 OF 2005)

Nature and purpose:

1. Development of a credit market that is accessible to all South Africans.

2. Encouraging responsible borrowing, avoidance of over-indebtedness and fulfilment of financial obligations by consumers.

3. Promoting equity in the credit market.

4. Addressing and correcting imbalances in negotiating power between consumers and credit providers.

5. Discouraging reckless credit granting by credit providers and contractual default by consumers.

THE PURCHASING FUNCTION AND THE NATIONAL CREDIT ACT (ACT 34 OF 2005)

Rights of credit providers:

1. May issue a summons and apply for judgement against the consumer.

2. Where there is no debt review application the credit provider may take legal action against the consumer, if:

• The consumer has been in default for at least 20 days.

• The credit provider has given the consumer at least 10 days written notice by registered mail.

• The consumer has not responded.

THE PURCHASING FUNCTION AND THE NATIONAL CREDIT ACT (ACT 34 OF 2005)

3. The consumer must inform the credit provider of any change concerning:

• The consumer’s resiential or business address.

• The address where the goods are kept.

• The name and address of any other person to whom possession of the goods have been transferred.

THE PURCHASING FUNCTION AND THE NATIONAL CREDIT ACT (ACT 34 OF 2005)

Rights of credit applicants:

1. The right to receive a copy of the document that records the credit agreement.

2. The right not to be discriminated against unfairly.

3. The right to reasons for credit being refused.

4. The right to information in an official language.

5. The right to information in plain and understandable language.

6. The right to access and challenge credit records and information.

THE PURCHASING FUNCTION AND THE NATIONAL CREDIT ACT (ACT 34 OF 2005)

Remedies:

1. The consumer can rely on the rights afforded by the National Credit Act, for example:

• The credit agreement may not contain unlawful provisions.

• The consumer is entitled to apply for debt review.

• The credit provider cannot pursue his remedies against the consumer while the consumer is under debt review.

2. A credit provider may issue a summons and apply for judgment against the consumer.

THE PURCHASING FUNCTION AND THE NATIONAL CREDIT ACT (ACT 34 OF 2005)

Impact on purchasing function:

1. The strict credit control measures have lead to a reduction in available credit.

2. The purchasing function cannot depend on obtaining credit any more.

3. The purchasing department, together with the financial department will have to make sure that there is enough cash at hand to acquire goods.

THE PURCHASING FUNCTION AND THE NATIONAL CONSUMER PROTECTION ACT (ACT 68 OF 2008)

Reason:

1. Create awareness of consumer rights.

2. Protect consumer rights.

THE PURCHASING FUNCTION AND THE NATIONAL CONSUMER PROTECTION ACT (ACT 68 OF 2008)

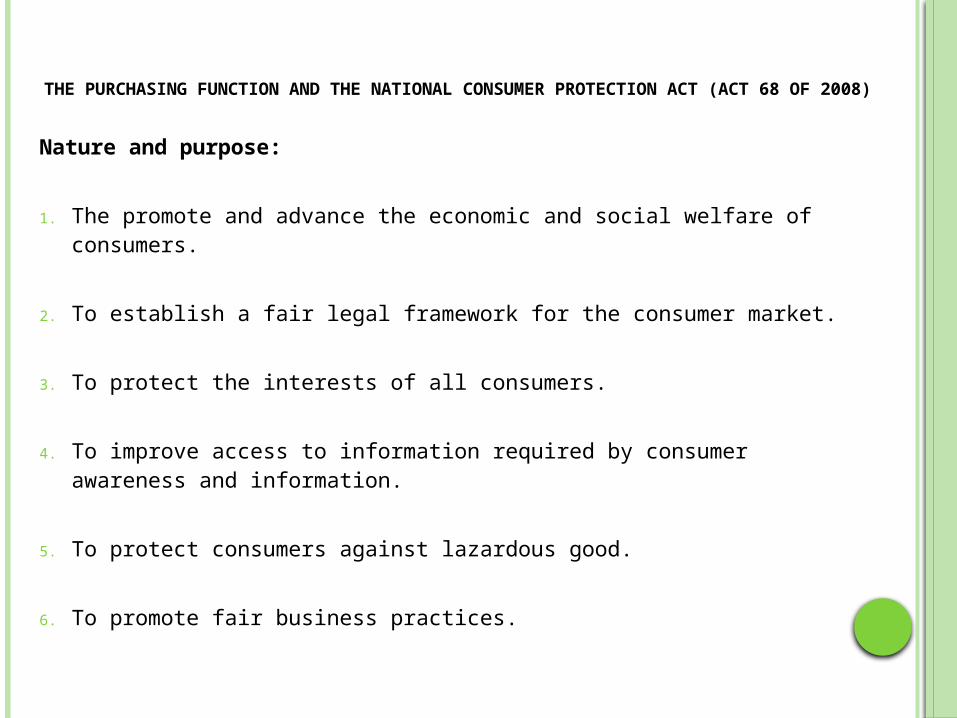

Nature and purpose:

1. The promote and advance the economic and social welfare of consumers.

2. To establish a fair legal framework for the consumer market.

3. To protect the interests of all consumers.

4. To improve access to information required by consumer awareness and information.

5. To protect consumers against lazardous good.

6. To promote fair business practices.

THE PURCHASING FUNCTION AND THE NATIONAL CONSUMER PROTECTION ACT (ACT 68 OF 2008)

Rights of service providers:

1. The supplier may cancel a fixed term agreement 20 days after giving the consumer notice of a material failure by the consumer.

2. Except on public holidays the supplier may approach the consumer for direct marketing purposes between 8:00 and 20:00 on week days and on Saterdays between 9:00 and 13:00.

3. Suppliers can enforce consumer agreements if the agreement was in plain and understandable language.

4. A supplier can enforce consumer agreement that is in writing even if the agreement has not been signed by the consumer.

THE PURCHASING FUNCTION AND THE NATIONAL CONSUMER PROTECTION ACT (ACT 68 OF 2008)

Rights of consumers:

1. The right to privacy.

2. The right to choice.

3. The right to information.

4. The right to accountability from suppliers.

5. The right to fair and responsible marketing.

6. The right to fair and reasonable terms and conditions.

THE PURCHASING FUNCTION AND THE NATIONAL CONSUMER PROTECTION ACT (ACT 68 OF 2008)

Remedies:

1. Consumers can refer a complaint to the National Consumer Commission.

2. Consumers and suppliers have access to alternative dispute resolution mechanisms.

3. Suppliers are subject to administrative fines.

4. The National Consumer Commission can investigate market practices of suppliers.

THE PURCHASING FUNCTION AND THE NATIONAL CONSUMER PROTECTION ACT (ACT 68 OF 2008)

Impact on purchasing function:

1. Suppliers and producers can be held accountable for harm caused by defective products..

2. More paper work and staff training is required of suppliers.

3. It will be more difficult for suppliers to render defective performance or deliver defective goods.

(E) THE PUBLIC RELATIONS FUNCTION

Role:

1. The public relations function aims to create a good image of a business.

Importance:

2. Creating a good business image is important:

• Attract customers.

• Satisfy shareholders.

• Attract good employees.

• Gain the goodwill of the community.

(E) THE PUBLIC RELATIONS FUNCTION

Methods:

1. Methods that support the public relations function:

• Use of the telephone

• Word of mouth

• Publicity

• Exhibitions

• Social responsibility

• Media

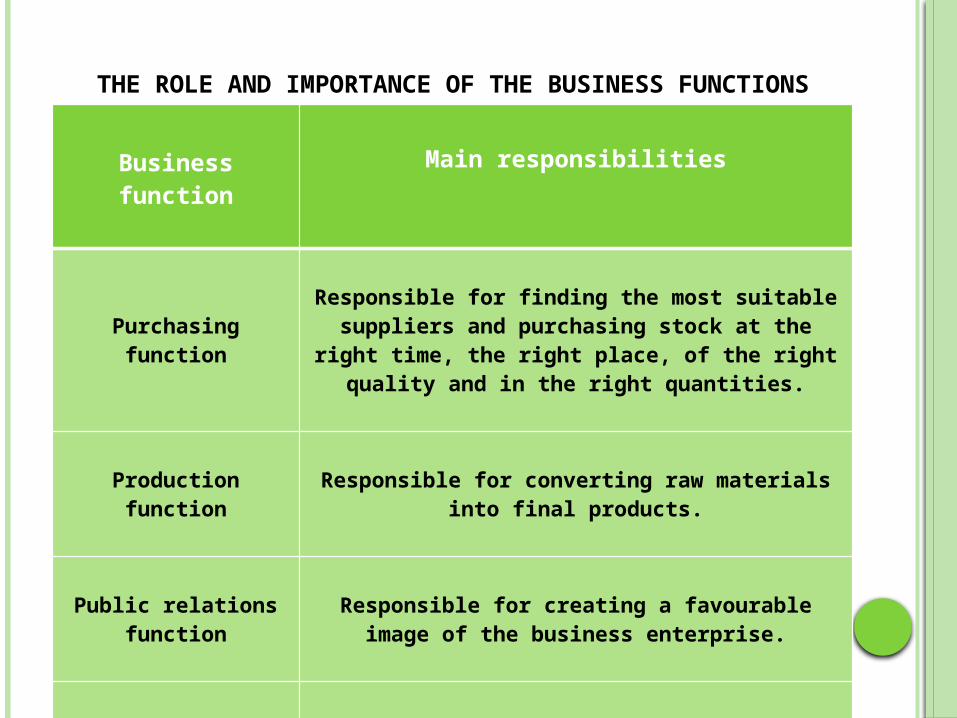

THE ROLE AND IMPORTANCE OF THE BUSINESS FUNCTIONS

Business function

Main responsibilities

Purchasing functionResponsible for finding the most suitable suppliers

and purchasing stock at the right time, the right place, of the right quality and in the right quantities.

Production function Responsible for converting raw materials into final products.

Public relations function

Responsible for creating a favourable image of the business enterprise.

General management function

Responsible for the over all management: planning, organising, leading and control.

THE ROLE AND IMPORTANCE OF THE BUSINESS FUNCTIONS

Business function

Main responsibilities

Marketing function Responsible for distributing and selling the enterprise’s products.

Human resources function

Responsible for recruiting, selecting and appointing new employees.

Administration function

Responsible for collecting, storing and distributing business information.

Financial function Responsible for finacing all business activities.

BUSINESS FUNCTIONS IN SMALL AND LARGE BUSINESS CONTEXTS

1. The 8 business functions will appear on a small scale in small business enterprises.

2. The opposite will be true of large business enterprises – the 8 business functions are clearly distinguished form one another.

3. The way in which resources is applied in a small business will also be different form the way in which resources is applied in larger enterprises.

THE ROLE OF MANAGEMENT IN THE SUCCESS OF A BUSINESS

1. It is management’s responsibility to determine realistic and attainable objectives for a business.

2. The performance of a business is measured against these objectives.

3. Management must allocate tasks to the right employees.

4. Management must choose an organisational stucture that supports productivity and performance.

THE ROLE OF MANAGEMENT IN THE SUCCESS OF A BUSINESS

5. It is management’s responsibility to create an atmosphere.

6. If employees are able to achieve the business’s objectives on a daily basis, the business will be successful in the long term.

7. Managers carry a heavy responsibility, because the decisions that a manager makes can benefit an enterprise, or sink an enterprise.

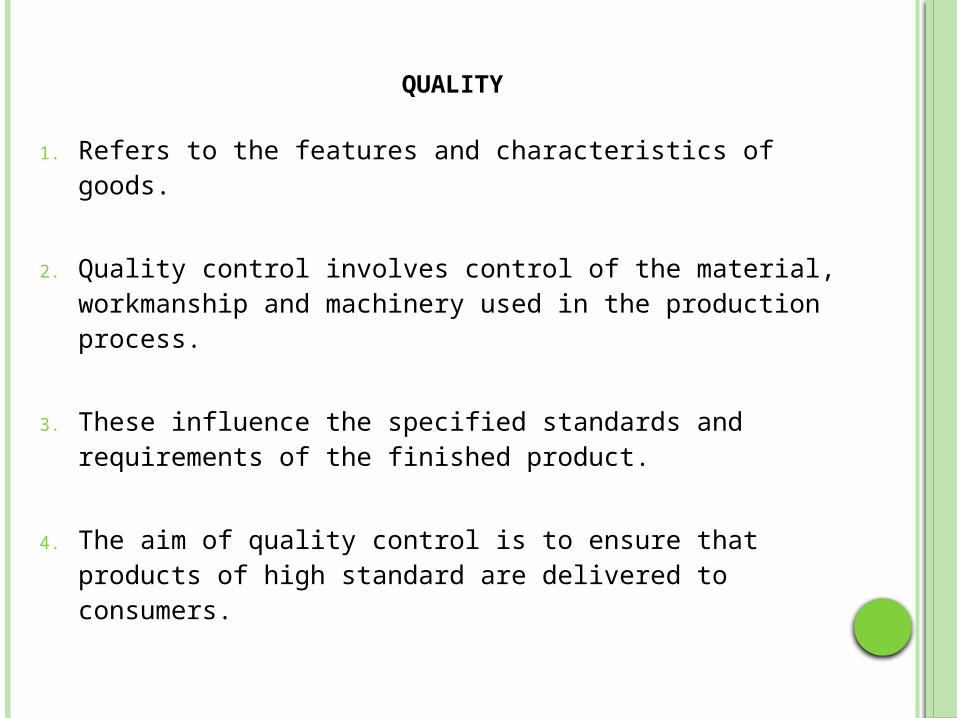

QUALITY

1. Refers to the features and characteristics of goods.

2. Quality control involves control of the material, workmanship and machinery used in the production process.

3. These influence the specified standards and requirements of the finished product.

4. The aim of quality control is to ensure that products of high standard are delivered to consumers.

QUALITY

Advantages:

1. Dealers and consumers are assured that products are of good quality.

2. Quality control encourages workers to continue to produce quality products.

3. Production costs can be reduced through elimination of poor productions.

4. Quality control leads to improved quality and product design.

QUALITY

1. One of a business’s overall goals is to deliver quality goods and services.

2. To achieve this goals, each business function must deliver good quality work, for example:

• Production

• Purchasing

• Public relations

QUALITY

• General management

• Marketing

• Human Resources

• Administration

• Financial

Activitie

s