Bank crisis, reforms and opportunities in Moldova

Sergiu Cioclea National Bank of Moldova EBRD Annual Meeting Cyprus – May 9-11, 2017

CRISIS

Bank crisis, reforms and opportunities in Moldova

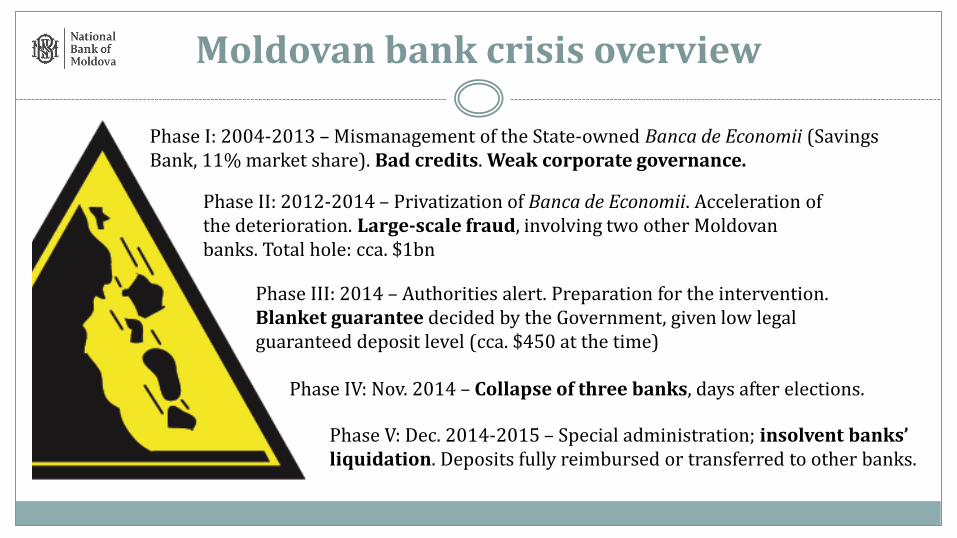

Moldovan bank crisis overview

Phase I: 2004-2013 – Mismanagement of the State-owned Banca de Economii (Savings Bank, 11% market share). Bad credits. Weak corporate governance.

Phase II: 2012-2014 – Privatization of Banca de Economii. Acceleration of the deterioration. Large-scale fraud, involving two other Moldovan banks. Total hole: cca. $1bn

Phase III: 2014 – Authorities alert. Preparation for the intervention. Blanket guarantee decided by the Government, given low legal guaranteed deposit level (cca. $450 at the time)

Phase IV: Nov. 2014 – Collapse of three banks, days after elections.

Phase V: Dec. 2014-2015 – Special administration; insolvent banks’ liquidation. Deposits fully reimbursed or transferred to other banks.

Moldovan ‘‘theft of the century’’

3 banks, incl. Banca de Economii (27% of market share in total) owned by the same group

The 3 banks coordinated to increase liquidity and facilitate massive increase in lending

Complex network of firms receiving loans acting in concert

Use of collateral from foreign banks to facilitate lending

Funds passed to UK firms with Latvian accounts (cca. $3bn flows)

Loan portfolio sold to a UK partnership – Fortuna United LP

Total funds dissipated – USD600mn

The 3 banks collapsed with loan exposure of $1bn (12% of GDP)ee

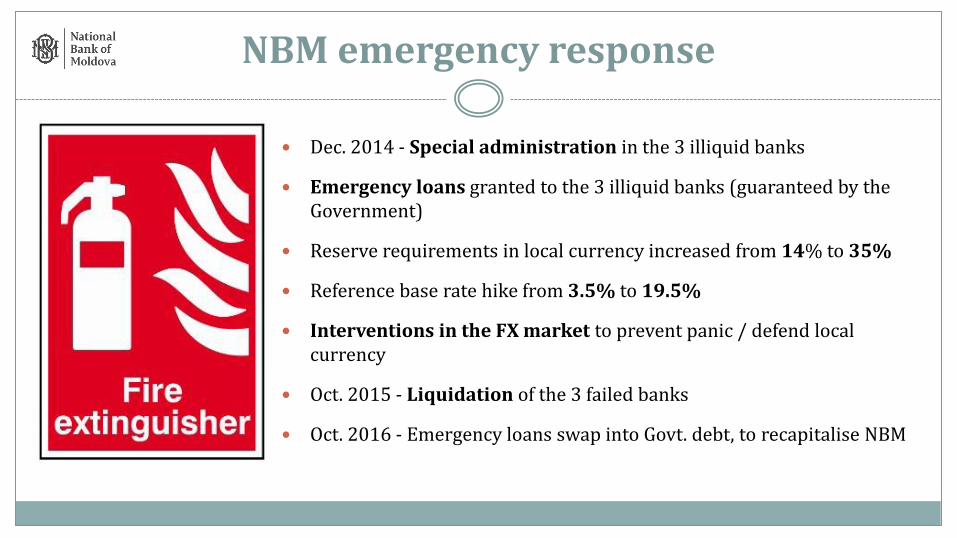

NBM emergency response

Dec. 2014 - Special administration in the 3 illiquid banks

Emergency loans granted to the 3 illiquid banks (guaranteed by the Government)

Reserve requirements in local currency increased from 14% to 35%

Reference base rate hike from 3.5% to 19.5%

Interventions in the FX market to prevent panic / defend local currency

Oct. 2015 - Liquidation of the 3 failed banks

Oct. 2016 - Emergency loans swap into Govt. debt, to recapitalise NBM

REFORMS

Bank crisis, reforms and opportunities in Moldova

Reasons behind the bank crisis

Lack of shareholding transparency / Incapable or fraud shareholders

Non-performing loans / Related-party lending / Deficient risk management

Shortfalls in cooperation between State agencies and regulators

Weak corporate governance / lack of managers’ independency vis-à-vis shareholders

Imperfect legal and regulatory framework / prudential supervisory

Weak sanctioning and enforcement regime

Political interference / complicity (?) – On-going investigation

Special supervision measures by NBM

Mid-2015 - the 3 largest banks (cca. 64% assets) put under special supervision by NBM

Full diagnostic reviews by external auditors (UBO, AML, related-parties, etc.)

Management reshuffles / corporate governance bodies reinforced

Remedy plans prepared and being implemented (risk management, internal control)

Loan portfolio reclassification and additional reserves/provisions created

NBM supervision of all material decisions / NBM observers participation in Boards

Special supervision to be lifted only after completion of remedy plans (planned by the end of 2017)

Full reviews of the 3 largest banks being finalised by H1, 2017. In other banks - by the end of 2017.

Removal of non-transparent UBOs

Actions vis-à-vis MAIB – the largest bank (27% market share)

43% of shares blocked in March 2016 and put for sale on stock exchange

On-going due-diligence by financial investors

Actions vis-à-vis MICB –2nd largest bank (20% market share)

64% of shares blocked in October 2016 and forced for sale (on-going)

NBM imposed temporary administrators on the basis of new Bank Recovery & Resolution Law

Independent asset-quality review and share valuation by KPMG

Discussions with reputable strategic investors. Due-diligence to start.

Victoriabank (3rd largest bank) – on-going review / UBOs sanctioned

UBO review and controls in all licensed banks by end-2017.

New laws and regulation

Changes to the Banking Law (approved in Apr. 2016 and Oct. 2016)

Sanctions for shareholders (up to 100% of their shares) and beyond

Sanctions for managers (up to 100 monthly revenues / 10-year professional ban)

Tougher rules re: related-parties lending (presumption, deduction from capital)

New Bank Recovery & Resolution Law (approved in Oct. 2016)

Provides for a regime of early intervention (by imposing temporary administrators)

Provides for new resolution tools (bridge-bank, P&A, bail-in)

Favours private solutions vs. Government last-resort intervention and early measures

Creation of a Single Central Depository (approved in April 2017) to protect against raider attacks

New Banking Law (Basel III principles) – drafted, planned to be approved by end-2017

New laws being prepared re: AML & CTF, non-banking financial institutions, etc.

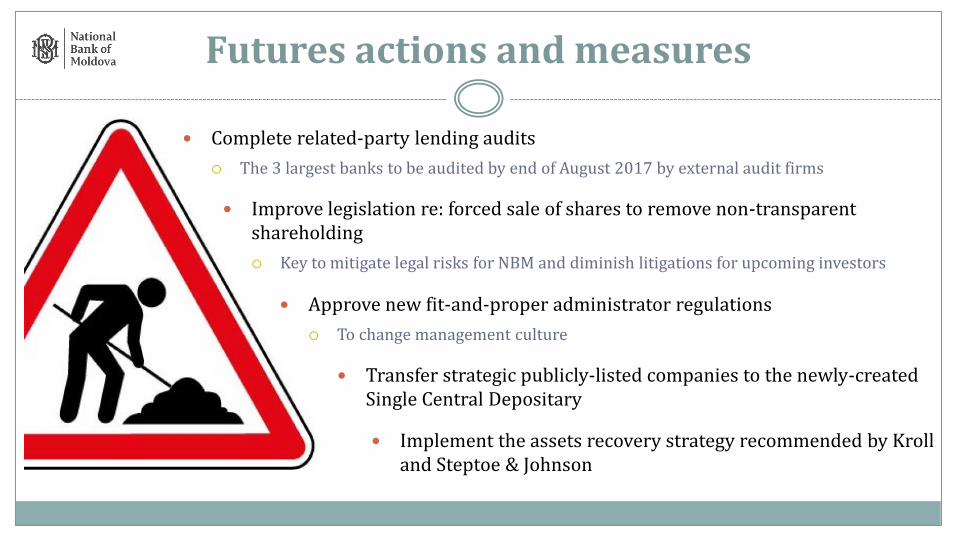

Futures actions and measures

Complete related-party lending audits

The 3 largest banks to be audited by end of August 2017 by external audit firms

Improve legislation re: forced sale of shares to remove non-transparent shareholding

Key to mitigate legal risks for NBM and diminish litigations for upcoming investors

Approve new fit-and-proper administrator regulations

To change management culture

Transfer strategic publicly-listed companies to the newly-created Single Central Depositary

Implement the assets recovery strategy recommended by Kroll and Steptoe & Johnson

ENVIRONMENT & OPPORTUNITIES

Bank crisis, reforms and opportunities in Moldova

MDL exchange rate stabilisation

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

EURMDL

USDMDL

FX interventions

Bank crisis

-34% vs. USD -18% vs. EUR

Consumer Price Inflation (%)

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Ja

nF

eb

Ma

rA

pr

Ma

yJ

un

Ju

lA

ug

Sep

Oct

No

vD

ecJ

an

Fe

bM

ar

Ap

rM

ay

Ju

nJ

ul

Au

gS

epO

ctN

ov

Dec

Ja

nF

eb

Ma

rA

pr

Ma

yJ

un

Ju

lA

ug

Sep

Oct

No

vD

ecJ

an

Fe

bM

ar

Ap

rM

ay

Ju

nJ

ul

Au

gS

epO

ctN

ov

Dec

Ja

nF

eb

Ma

r

2013 2014 2015 2016 2017

13.4%

2.5%

5.1%

Target: 5%+ 1.5 p.p.

Bank crisis

Monetary conditions normalisation

0123456789

10111213141516171819202122232425 Cca. 25%

9%

7.5%

19.5%

3.5%

Bank crisis 3-M T-bills

Base rate

Low banking penetration (2015 data)

Banking sector metrics (1/2)

Banking sector metrics (2/2)

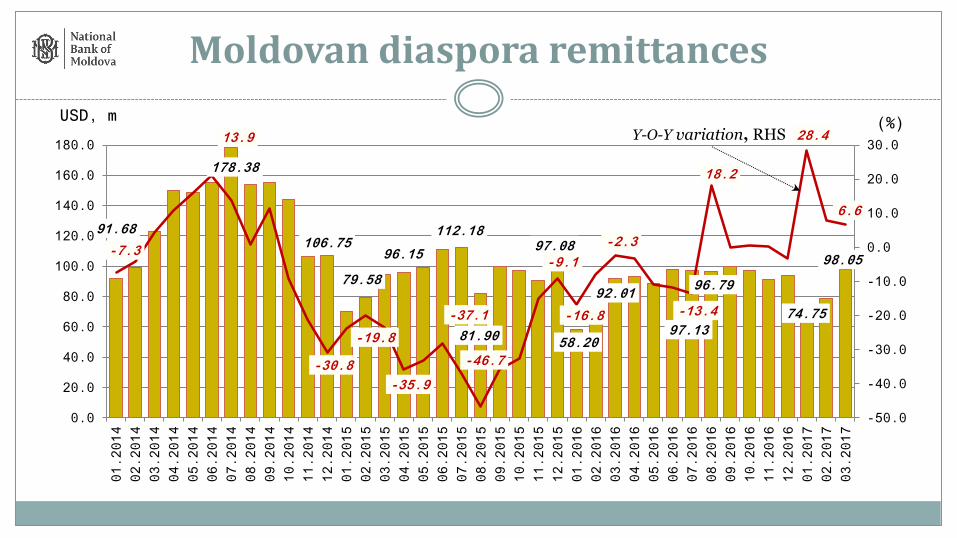

Moldovan diaspora remittances

91.68

178.38

106.75

79.58

96.15

112.18

81.90

97.08

58.20

92.01

97.13

96.79

74.75

98.05 -7.3

13.9

-30.8

-19.8

-35.9

-37.1

-46.7

-9.1

-16.8

-2.3

-13.4

18.2

28.4

6.6

-50.0

-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

01.2014

02.2014

03.2014

04.2014

05.2014

06.2014

07.2014

08.2014

09.2014

10.2014

11.2014

12.2014

01.2015

02.2015

03.2015

04.2015

05.2015

06.2015

07.2015

08.2015

09.2015

10.2015

11.2015

12.2015

01.2016

02.2016

03.2016

04.2016

05.2016

06.2016

07.2016

08.2016

09.2016

10.2016

11.2016

12.2016

01.2017

02.2017

03.2017

(%) USD, m

Y-O-Y variation, RHS

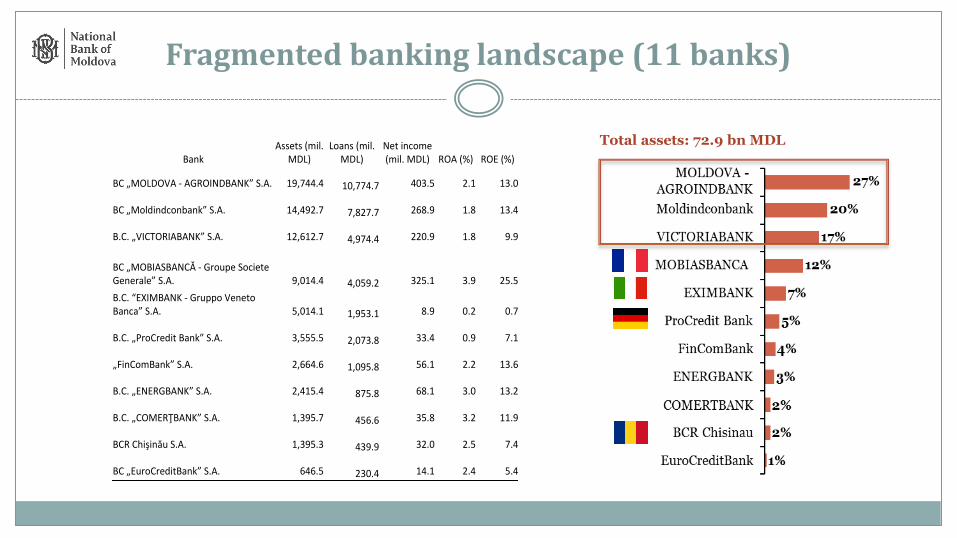

Fragmented banking landscape (11 banks)

Bank

Assets(mil.MDL)

Loans(mil.MDL)

Netincome(mil.MDL) ROA(%) ROE(%)

BC„MOLDOVA-AGROINDBANK”S.A. 19,744.4 10,774.7 403.5 2.1 13.0

BC„Moldindconbank”S.A. 14,492.7 7,827.7 268.9 1.8 13.4

B.C.„VICTORIABANK”S.A. 12,612.7 4,974.4 220.9 1.8 9.9

BC„MOBIASBANCĂ-GroupeSocieteGenerale”S.A. 9,014.4 4,059.2 325.1 3.9 25.5

B.C.“EXIMBANK-GruppoVenetoBanca”S.A. 5,014.1 1,953.1 8.9 0.2 0.7

B.C.„ProCreditBank”S.A. 3,555.5 2,073.8 33.4 0.9 7.1

„FinComBank”S.A. 2,664.6 1,095.8 56.1 2.2 13.6

B.C.„ENERGBANK”S.A. 2,415.4 875.8 68.1 3.0 13.2

B.C.„COMERŢBANK”S.A. 1,395.7 456.6 35.8 3.2 11.9

BCRChişinăuS.A. 1,395.3 439.9 32.0 2.5 7.4

BC„EuroCreditBank”S.A. 646.5 230.4 14.1 2.4 5.4

Bank Assets Loans Net

income ROA ROE

BC„MOLDOVA-AGROINDBANK”S.A. 1 1 1 7 5

BC„Moldindconbank”S.A. 2 2 3 9 3

B.C.„VICTORIABANK”S.A. 3 3 4 8 7

BC„MOBIASBANCĂ-GroupeSocieteGenerale”S.A. 4 4 2 1 1

B.C.“EXIMBANK-GruppoVenetoBanca”S.A. 5 6 11 11 11

B.C.„ProCreditBank”S.A. 6 5 8 10 9

„FinComBank”S.A. 7 7 6 6 2

B.C.„ENERGBANK”S.A. 8 8 5 3 4

B.C.„COMERŢBANK”S.A. 9 9 7 2 6

BCRChişinăuS.A. 10 10 9 4 8

BC„EuroCreditBank”S.A. 11 11 10 5 10

Mainindicators Banksrankings

Total assets: 72.9 bn MDL

Sergiu Cioclea Governor of National Bank of Moldova 1 Grigore Vieru Avenue, MD-2005 Chisinau, Republic of Moldova www.bnm.md Phone: +373 22 822 606 Email: [email protected]