BANK NEGARA MALAYSIACENTRAL BANK OF MALAYSIA

Jordan Loan Guarantee Corporation – SME Financing and Loan Guarantee Conference 2014

Central Bank’s Programmes Supporting SME Financing

Marina KaharDirector of Development Finance and Enterprise DepartmentBank Negara Malaysia25 November 2014

BANK NEGARA MALAYSIACENTRAL BANK OF MALAYSIA

Coverage of presentation

• Strategic importance of SMEs to the economy

• Building the SME financing eco-system: A Malaysian perspective

• Malaysia’s holistic approach towards SME policy interventions

• Promoting and supporting innovation and new growth areas

• Development of a supportive payment system to drive innovative businesses

• Proportionate regulation to drive SME development

• Conclusion

BANK NEGARA MALAYSIACENTRAL BANK OF MALAYSIA

SMEs are an important contributor to the Malaysian GDP

GDP Growth: SMEs and Overall Economy

p: preliminary f: forecast

Source: Department of Statistics, SME Corporation Malaysia, Bank Negara Malaysia

• SME GDP growth outpaced the overall economy (cumulative growth of 6.3% for 2006-2013)

• Contribution to GDP increased by 3.7 ppt since 2005

• Services sectors remain as the largest contributor to SME growth

• Banking system remains supportive of SMEs, in all key economic sectors

Lending to SMEs by Banking System (RM b)

3

BANK NEGARA MALAYSIACENTRAL BANK OF MALAYSIA

Micro75%

Small19%

Medium3%

Large3%

% of Total Establishments

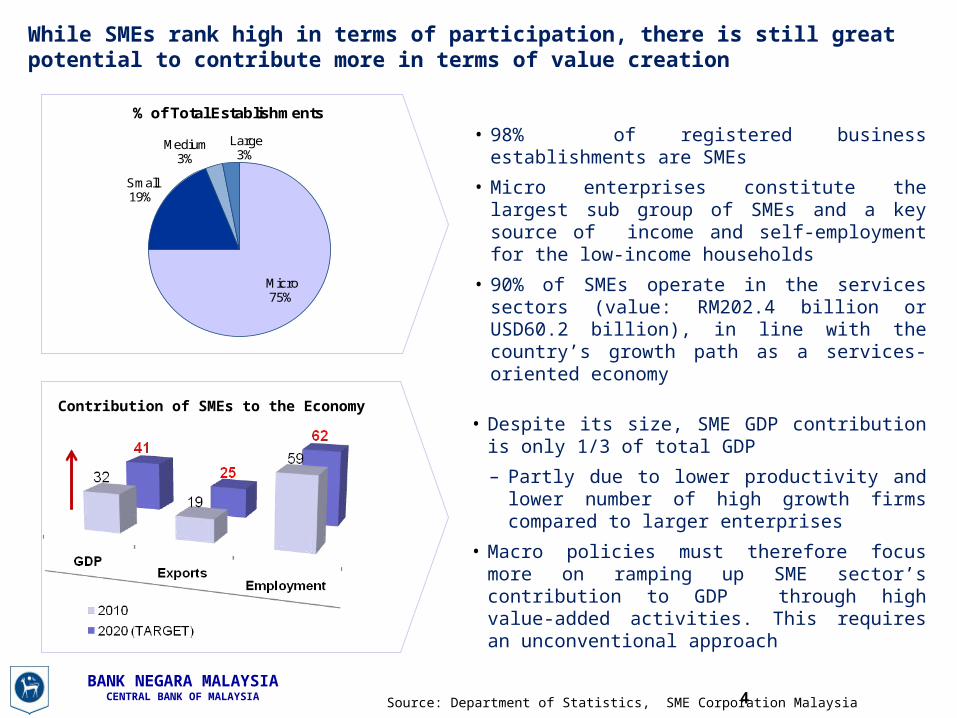

While SMEs rank high in terms of participation, there is still great potential to contribute more in terms of value creation

Contribution of SMEs to the Economy

• 98% of registered business establishments are SMEs

• Micro enterprises constitute the largest sub group of SMEs and a key source of income and self-employment for the low-income households

• 90% of SMEs operate in the services sectors (value: RM202.4 billion or USD60.2 billion), in line with the country’s growth path as a services-oriented economy

• Despite its size, SME GDP contribution is only 1/3 of total GDP

– Partly due to lower productivity and lower number of high growth firms compared to larger enterprises

• Macro policies must therefore focus more on ramping up SME sector’s contribution to GDP through high value-added activities. This requires an unconventional approach

Source: Department of Statistics, SME Corporation Malaysia4

BANK NEGARA MALAYSIACENTRAL BANK OF MALAYSIA

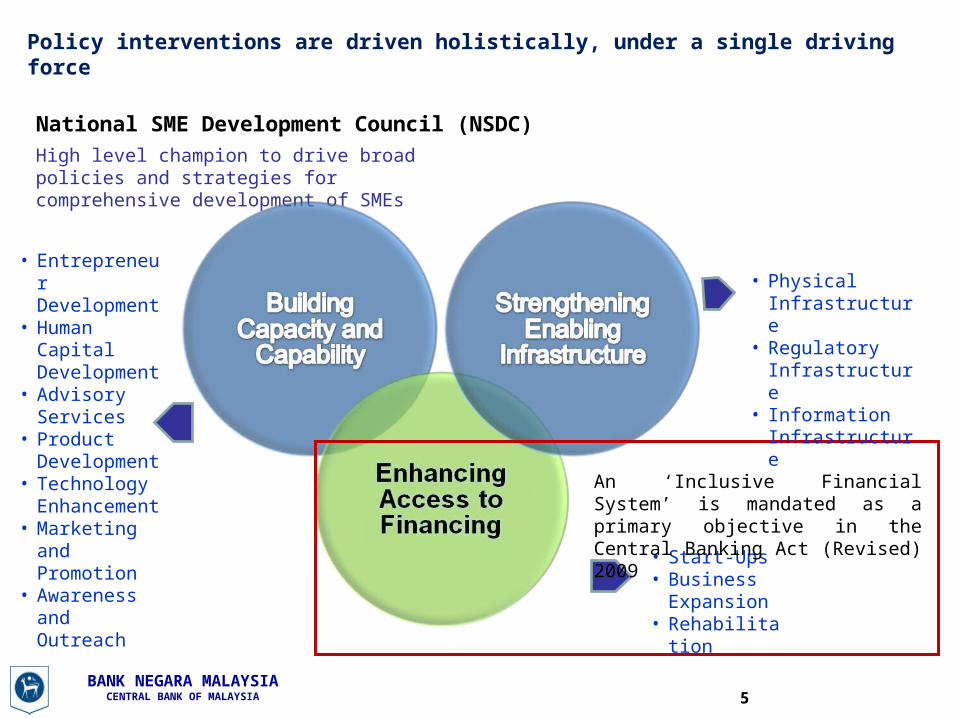

National SME Development Council (NSDC)

• Entrepreneur Development

• Human Capital Development

• Advisory Services

• Product Development

• Technology Enhancement

• Marketing and Promotion

• Awareness and Outreach • Start-Ups

• Business Expansion

• Rehabilitation

High level champion to drive broad policies and strategies for comprehensive development of SMEs

Policy interventions are driven holistically, under a single driving force

5

An ‘Inclusive Financial System’ is mandated as a primary objective in the Central Banking Act (Revised) 2009

• Physical Infrastructure

• Regulatory Infrastructure

• Information Infrastructure

BANK NEGARA MALAYSIACENTRAL BANK OF MALAYSIA

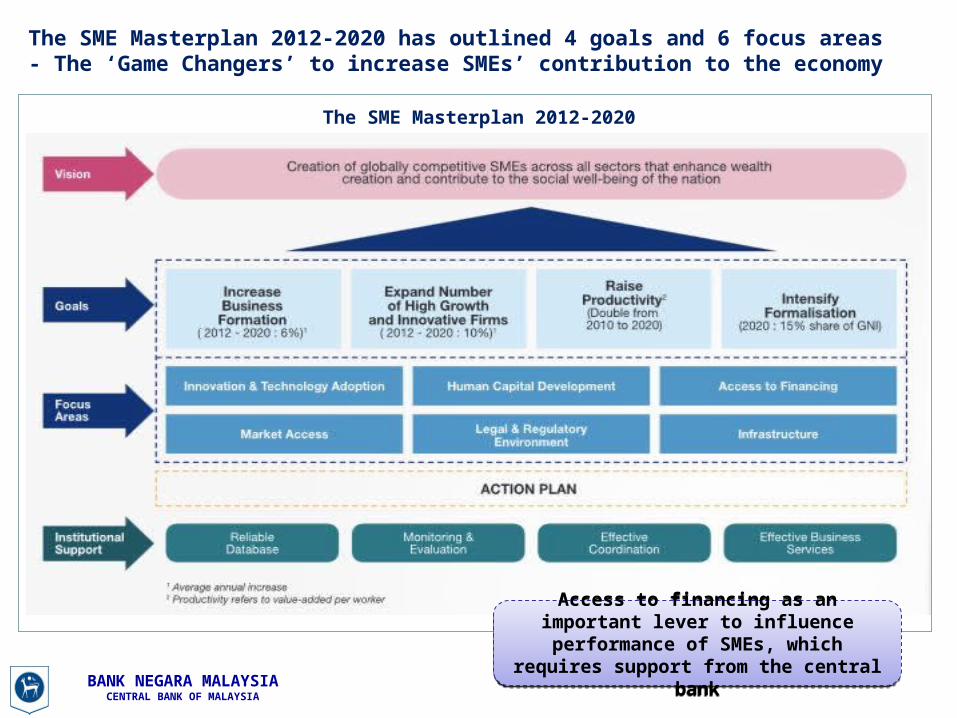

The SME Masterplan 2012-2020 has outlined 4 goals and 6 focus areas - The ‘Game Changers’ to increase SMEs’ contribution to the economy

The SME Masterplan 2012-2020

Access to financing as an important lever to influence performance of SMEs, which

requires support from the central bank

Access to financing as an important lever to influence performance of SMEs, which

requires support from the central bank

7

7

BNM’s commitment in financial inclusion embedded in legislation and financial sector blueprint

Revised Central Bank Act 2009

• Formulate and conduct monetary policy• Promote exchange rate regime consistent with

fundamentals • Regulate and supervise financial institutions• Promote sound, progressive and inclusive

financial system

• Provide oversight over the money and foreign exchange market

• Hold and manage foreign reserves of Malaysia

• Issue currency • Exercise oversight over payment system

Principal Functions

Promote monetary stability and financial stability conducive to the sustainable growth of the Malaysian economy

Principal Objective

Financial Sector Blueprint (FSBP)

1

2

Enhance capability to support high

value-added activities

Increase supply of a broad range of

private risk capital funding

Improve access to information

Enhance access to financing for

micro enterprises

BANK NEGARA MALAYSIACENTRAL BANK OF MALAYSIA

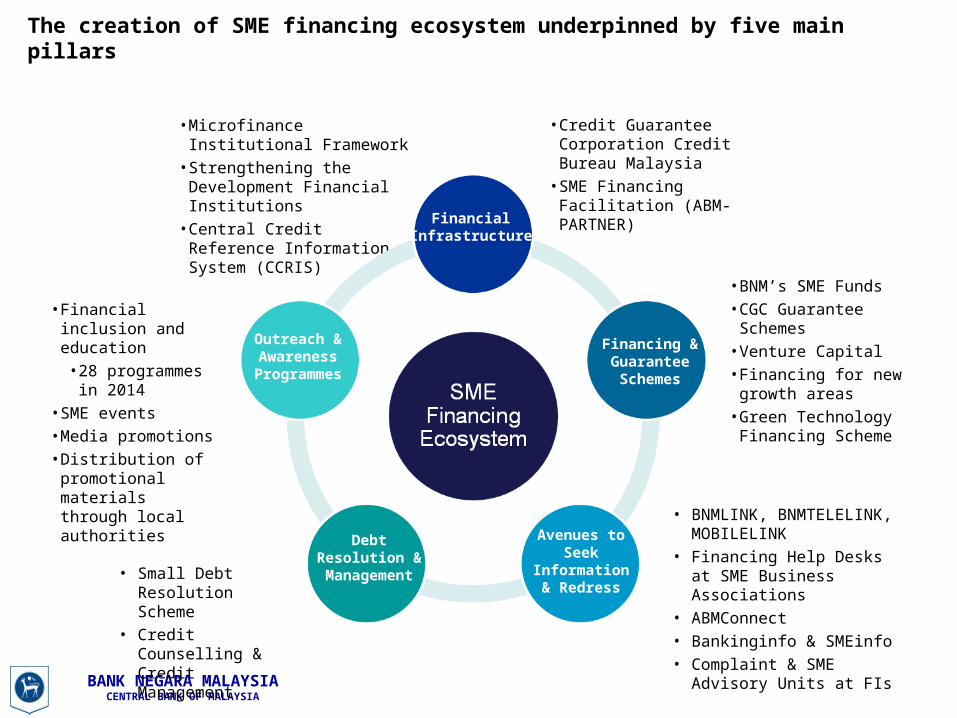

The creation of SME financing ecosystem underpinned by five main pillars

• Microfinance Institutional Framework

• Strengthening the Development Financial Institutions

• Central Credit Reference Information System (CCRIS)

• BNM’s SME Funds • CGC Guarantee

Schemes• Venture Capital • Financing for new

growth areas• Green Technology

Financing Scheme

• BNMLINK, BNMTELELINK, MOBILELINK

• Financing Help Desks at SME Business Associations

• ABMConnect• Bankinginfo & SMEinfo• Complaint & SME Advisory

Units at FIs

• Small Debt Resolution Scheme

• Credit Counselling & Credit Management

• Financial inclusion and education • 28 programmes in

2014• SME events• Media promotions• Distribution of

promotional materials through local authorities

• Credit Guarantee Corporation Credit Bureau Malaysia

• SME Financing Facilitation (ABM-PARTNER)Financial

Infrastructure

Financing & Guarantee Schemes

Avenues to Seek

Information & Redress

Debt Resolution & Management

Outreach & Awareness

Programmes

BANK NEGARA MALAYSIACENTRAL BANK OF MALAYSIA

• Green Technology Financing Facility (USD1.06 bil) comprising of 30 actively participating FIs

• Assessment tools by experts to complement credit assessment by FIs

• Green Tech certification

• Business matching with financial institutions

• Green Tech Business Review by Malaysia Green Tech Corporation

• Technical briefings by MDeC and Biotech Corp

• Conference on Green Technology Financing and IP Financing

• Seminar on Intellectual Property Awareness by the Intellectual Property Corp of Malaysia

• GT Financing Programmes by Asian Institute of Chartered Bankers

• IP Financing Scheme by MDV and CGC

Collaborative approach between BNM and Government agencies to support innovative and new growth areasCreating a stable environment to spur innovation and growth

1

4

3

Products and Services

Technical Assessment by Experts

Business Facilitation/ Market Platform

Capacity Building

2

More than USD1.8 bil in financing assistance provided

9

• IP Marketplace by Malaysia Intellectual Property Corporation (MyIPO)

• Technology Commercialisation Platform to assist in end-to-end R&D&C by Agensi Inovasi Malaysia

• Commercialisation Innovation Fund (USD0.15 bil)

Examples:

BANK NEGARA MALAYSIACENTRAL BANK OF MALAYSIA

The evolution of Credit Guarantee Corporation’s role

Role of BNM in ensuring sustainable performance

• Provides guarantee for loans without collateral / with inadequate collateral and track record

• Provides advisory services such as financial management .

• Provides direct financing for specific segments such as start-ups

• Implements Government-funded schemes targeting specific sectors such as innovative and new growth areas.

Key roles of CGC

SMEs benefitted from CGC schemes 422,585

Total value of loans guaranteed

RM52.9 billion

• As a major shareholder, BNM initiated transformation plan for CGC to undertake more effective role in assisting viable SMEs

– Greater emphasis on enhancing outreach, while maintaining financial sustainability

• Close engagement with CGC’s Board to ensure effective performance and achievement of mandate

• Close monitoring through regular reports submitted by CGC

• Provide guarantees to banks, to increase receptiveness of SME customers

• Concessionary guarantee fee to keep borrowing cost low

• Expanded branch network nationwide

• Implemented Direct Access Guarantee Scheme

• Enhanced advisory services to SMEs

• Achieve financial sustainability

• Expand products and services to meet evolving needs of SMEs

• Balance financial sustainability with developmental role

BANK NEGARA MALAYSIACENTRAL BANK OF MALAYSIA

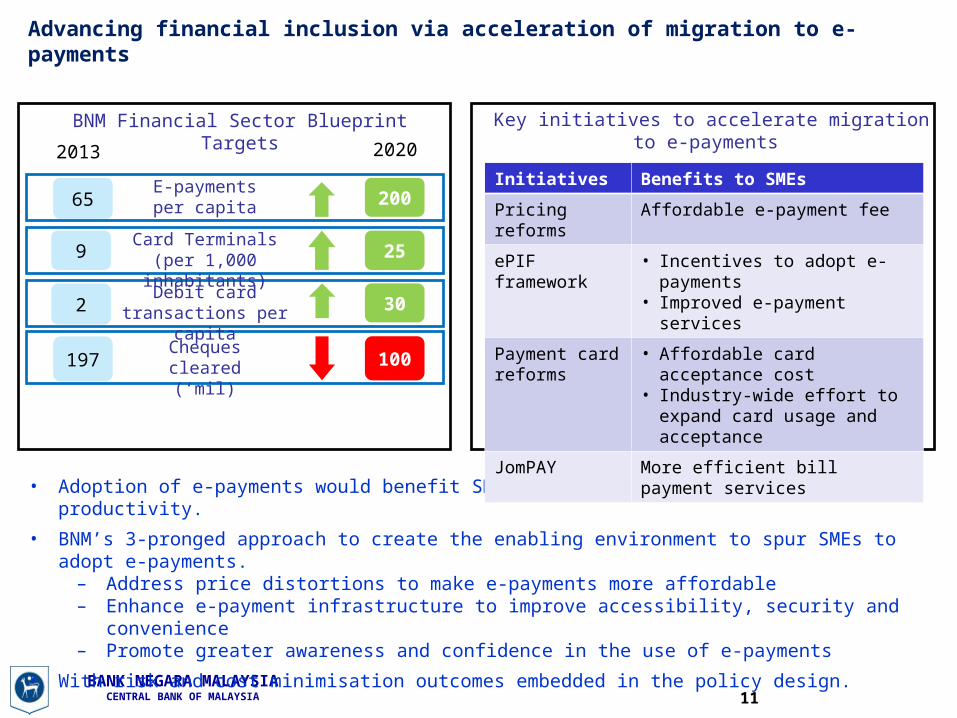

Advancing financial inclusion via acceleration of migration to e-payments

• Adoption of e-payments would benefit SMEs by enhancing efficiency and productivity.

• BNM’s 3-pronged approach to create the enabling environment to spur SMEs to adopt e-payments.– Address price distortions to make e-payments more affordable– Enhance e-payment infrastructure to improve accessibility, security and convenience – Promote greater awareness and confidence in the use of e-payments

• With risk and cost minimisation outcomes embedded in the policy design.

2

65

197

9

E-payments per capita

Cheques cleared (‘mil)

Card Terminals(per 1,000 inhabitants)

200

100

2013 2020

25

Debit card transactions per capita 30

BNM Financial Sector Blueprint Targets Key initiatives to accelerate migration to e-payments

Initiatives Benefits to SMEs

Pricing reforms Affordable e-payment fee

ePIF framework • Incentives to adopt e-payments• Improved e-payment services

Payment card reforms

• Affordable card acceptance cost• Industry-wide effort to expand card

usage and acceptance

JomPAY More efficient bill payment services

11

BANK NEGARA MALAYSIACENTRAL BANK OF MALAYSIA

• High cost of doing business

• Uncompetitive / low productivity

• Lower profits

• Difficulty obtaining funding

• Low expansion opportunity

Continuous efforts undertaken to address challenges in SME development

Barriers for SME growth

Source: Bank Negara Malaysia; SME Corporation Malaysia12

Business / Entrepreneurial impediments

Low innovation and technology adoption

Market access – lack marketing and branding knowledge

Human capital – skill mismatch of workforce

High Transaction Costs

Information Asymmetry

Lack Collateral / Track Records

Financing issues

BANK NEGARA MALAYSIACENTRAL BANK OF MALAYSIA

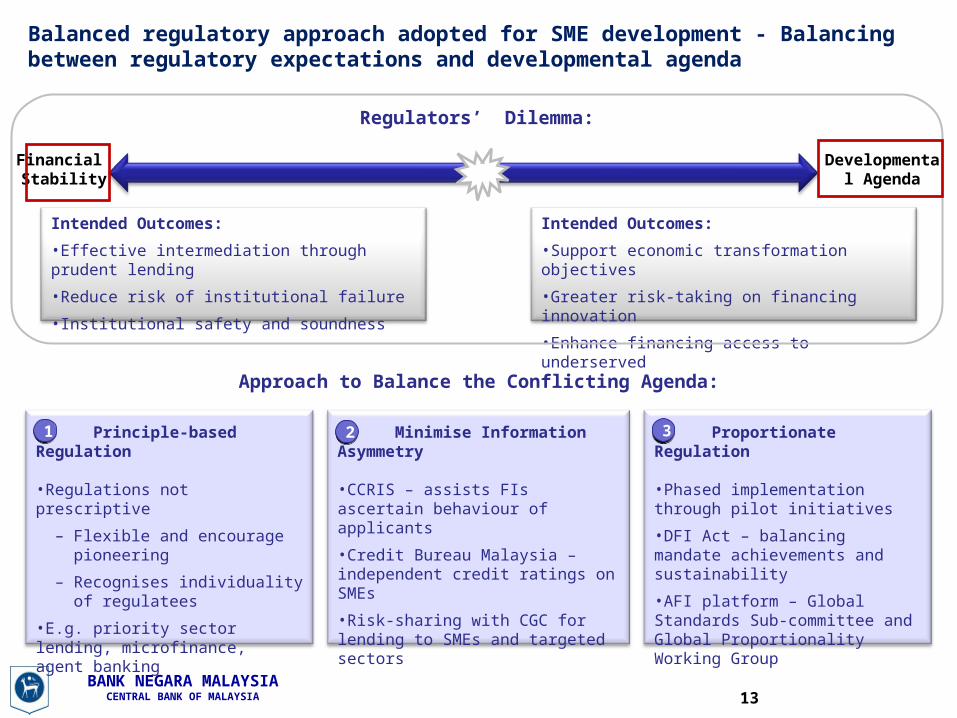

Balanced regulatory approach adopted for SME development - Balancing between regulatory expectations and developmental agenda

Financial Stability

Developmental Agenda

Intended Outcomes:

•Effective intermediation through prudent lending

•Reduce risk of institutional failure

•Institutional safety and soundness

Intended Outcomes:

•Support economic transformation objectives

•Greater risk-taking on financing innovation

•Enhance financing access to underserved

Principle-based Regulation

•Regulations not prescriptive

– Flexible and encourage pioneering

– Recognises individuality of regulatees

•E.g. priority sector lending, microfinance, agent banking

Minimise Information Asymmetry

•CCRIS – assists FIs ascertain behaviour of applicants

•Credit Bureau Malaysia – independent credit ratings on SMEs

•Risk-sharing with CGC for lending to SMEs and targeted sectors

Proportionate Regulation

•Phased implementation through pilot initiatives

•DFI Act – balancing mandate achievements and sustainability

•AFI platform – Global Standards Sub-committee and Global Proportionality Working Group

11 22 33

Approach to Balance the Conflicting Agenda:

Regulators’ Dilemma:

13

BANK NEGARA MALAYSIACENTRAL BANK OF MALAYSIA

Continuous surveillance and oversight over SMEs’ performance and access to financing

Pro-active measures taken by BNM for effective surveillance to ensure continued access to financing

•Robust surveillance and oversight over market practices and new products offered by financial institutions.

•Keep abreast of new emerging risks and vulnerabilities for timely identification and mitigation of risks.

•Ensure compliance by FIs with regulatory requirements on the offering of new financial products and services particularly management and control of risks.

•Continuous engagements with FIs, SMEs, Government agencies and business associations on challenges faced by SMEs to address their concerns.

•Perform assessment through demand side survey on SMEs to facilitate formulation of policies to support the growth of SMEs.

BANK NEGARA MALAYSIACENTRAL BANK OF MALAYSIA

In conclusion

• Collaborative efforts among stakeholders must be championed by a higher voice to harmonise conflicting objectives – ecosystems need all parts to work cohesively.

• The Central Bank needs to strengthen SME market surveillance and promote a market-driven approach to encourage industry players in enhancing SMEs’ access to financing.

• The awareness level of financiers needs to be accelerated in order to increase understanding of the new growth areas and the associated risks.

• Innovation leads to growth and ultimately prosperity but financial stability must not be compromised.

• All stakeholders including the Government and the Central Bank must continuously enhance the eco-system to support SME growth.

15