*Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/qualified pursuant to FINRA regulations.

Au

gu

st 2

010

Becalm

ed

?

By James Magness and Robert Clover

We have cut our five year wind industry global demand CAGR estimate to

7.0% from 7.5% previously and our 10-year CAGR estimate to 5.5% from 6.7%

We remain cautious on the wind OEMs, and see few near term catalysts for share

price performance. Our favourite part of the value chain is still the wind

farm developers, and Acciona and EDP R, both rated OW(V),

are our highest conviction investment ideas

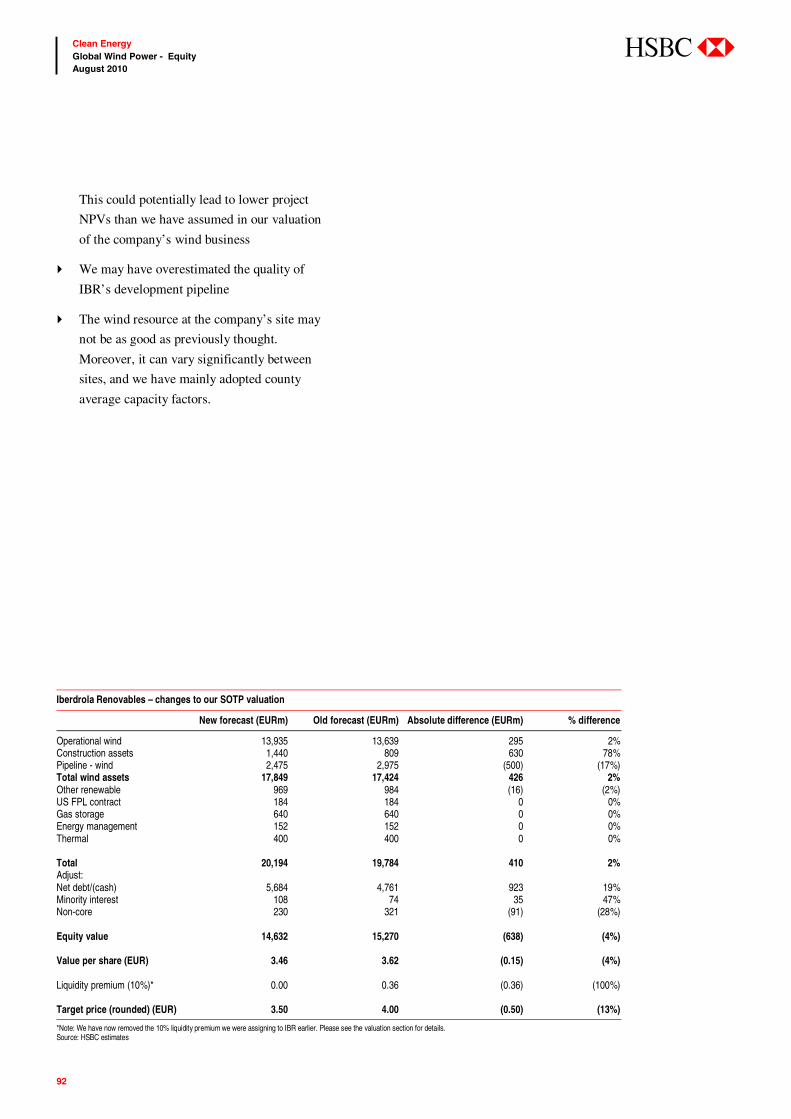

We cut target prices on Acciona, Hansen Tranmissions, Iberdrola Renovables, EDP Renovaveis,

EDF Energies Nouvelles, Vestas, Gamesa, Repower, and Suzlon, and increase our target

price on Clipper. We have downgraded Gamesa and Repower to N(V) from OW(V)

and upgraded Clipper from N(V) to OW(V)

Becalmed?Is it all over for the global wind markets?

Disclosures and Disclaimer This report must be read with the disclosures and analyst

certifications in the Disclosure appendix, and with the Disclaimer, which forms part of it

Global Clean Energy – Equity

August 2010

Glo

bal C

lean

En

erg

y –

Eq

uity

James Magness*

Analyst

HSBC Bank Plc

+44 20 7991 3464

James is an analyst in the Alternative Energy team based in London. He joined HSBC in August 2005 from a large accounting firm

where he qualified as a chartered accountant and worked in the Valuation and Strategy team. Prior to that he graduated from

Oxford University with a first class degree in Physics.

Robert Clover*

Analyst

HSBC Bank Plc

+44 20 7991 6741

Robert Clover is the Global Head of Alternative and Renewable Energy Equity Research and he joined HSBC in 2004.

Throughout his career he has been ranked in Extel, II and Greenwich. He has an MA (Hons) from Oxford in

Classics and Modern languages, is ACCA-qualified and has worked as an investment analyst since 1995.

100827_28253 Wind Industry thematic_F2:Layout 1 8/31/2010 1:02 AM Page 1

1

Clean Energy Global Wind Power - Equity August 2010

abc

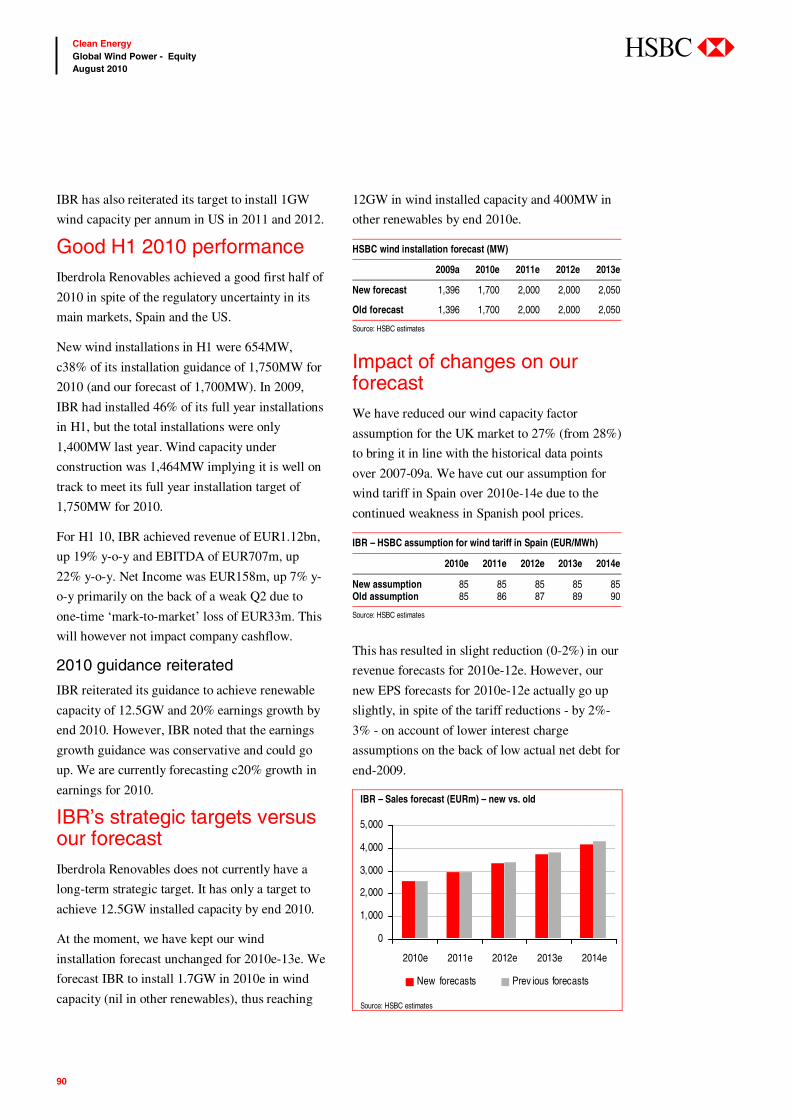

What’s going on with the markets? Why has the wind sector been so weak?

The wind sector has been weak since the start of the credit crisis in September 2008. Until this point it

had held up pretty well, when most other sectors had already been selling off. However, in the two

months following the collapse of Lehman Brothers, the sector more than halved in value; the wind farm

developers lost 50-60% and the wind turbine manufacturers lost 60-70%. The focus at this time was lack

of availability of project finance.

The sector then recovered some of its share price losses during the March 2009 bear market rally, but

subsequently spent a year in the doldrums, with share prices moving sideways. The main reason for this

was lack of order flow during 2009 due to US regulatory uncertainty and only a modest improvement in

project finance markets throughout the course of 2009. Order flow has finally started to pick up in H1

2010, double the H12009 level, but importantly it remains around 70% below H12008, and the recovery

is less strong than we had hoped for due to the Sovereign debt concerns in Southern Europe, increasing

the possibility of tariff reductions (see our note dated 21 June 2010, entitled ‘Carbon default – real of

imagined?’), and at the same time the Clean Energy regulatory rollercoaster in the US Senate started

heading for derailment. From mid-April onwards, the sector sold off along with the wider Southern

European markets, but whereas the Southern European markets have recovered some 20% since early

June, the wind sector has not; some stocks have recovered slightly but most have not. This, we believe, is

due to continued uncertainty over clean energy legislation in the US, which is now unlikely to pass the

Senate before mid-term elections in November.

Summary

Weak electricity demand resulting from energy efficiency measures and recessionary forces have made national wind installation targets easier to achieve. We have therefore cut our five year wind industry global demand CAGR to 7.0% from 7.5% previously and our 10-year CAGR to 5.5% from 6.7%. We remain cautious on the wind OEMs, and see few near term catalysts for share price performance. Our favourite part of the value chain remains the wind farm developers as we feel that that the developers offer a more compelling combination of earnings visibility and valuation and our preference for this part of the value chain has now increased. Acciona and EDP R, both rated OW(V), are our highest conviction investment ideas

2

Clean Energy Global Wind Power - Equity August 2010

abc

In our view, the sector weakness gives rise to some attractive long-term investment opportunities, but on

a selective basis. We continue to favour the wind farm developers, with our preference for this part of the

value chain increasing. In this note, we reiterate our cautious stance on the OEMs due to regulatory risk

and the impact of energy efficiency measures weighing on our longer-term growth assumptions for the

wind turbine market.

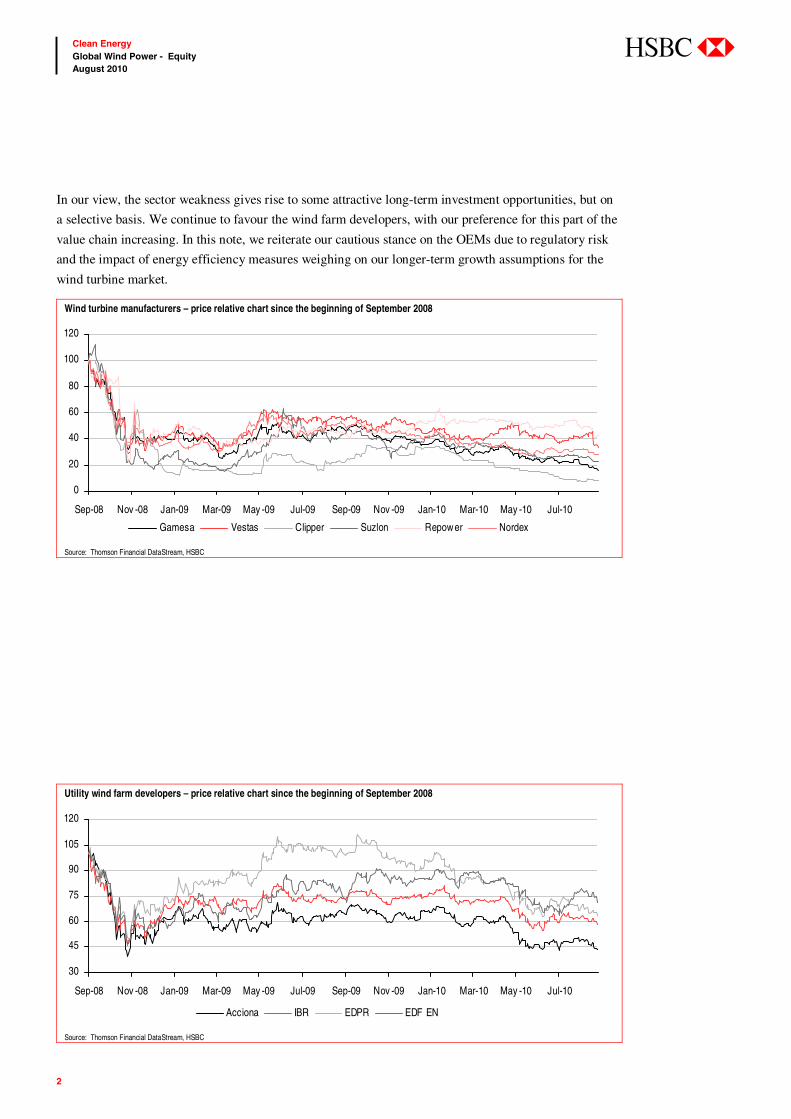

Wind turbine manufacturers – price relative chart since the beginning of September 2008

0

20

40

60

80

100

120

Sep-08 Nov -08 Jan-09 Mar-09 May -09 Jul-09 Sep-09 Nov -09 Jan-10 Mar-10 May -10 Jul-10

Gamesa Vestas Clipper Suzlon Repower Nordex

Source: Thomson Financial DataStream, HSBC

Utility wind farm developers – price relative chart since the beginning of September 2008

30

45

60

75

90

105

120

Sep-08 Nov -08 Jan-09 Mar-09 May -09 Jul-09 Sep-09 Nov -09 Jan-10 Mar-10 May -10 Jul-10

Acciona IBR EDPR EDF EN

Source: Thomson Financial DataStream, HSBC

3

Clean Energy Global Wind Power - Equity August 2010

abc

Wind turbine manufacturers – price relative chart of each stock relative to its local market since mid-April 2010

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

Apr-10 May -10 Jun-10 Jul-10 Aug-10

GAM/MADRIDI VWS/DKKFXXIN CWP/FTAIM10 SZE/IBOMSENRPW/SDAXIDZ NDX1/MDAXIDX

Source: Thomson Financial DataStream, HSBC

Utility wind farm developers – price relative chart of each stock relative to its local market since mid-April 2010

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

Apr-10 May -10 Jun-10 Jul-10 Aug-10

ANA/IBEX35 IBR/IBEX35 EDPR/DJPORTL EEN/EN1FRU1

Source: Thomson Financial DataStream, HSBC

4

Clean Energy Global Wind Power - Equity August 2010

abc

We see selective opportunities with the Developers…

The impact of regulatory uncertainty on the wind farm developers is more muted, in our view; they all have

large existing operating portfolios of wind farms, which are unlikely to be affected by potential regulatory

change (e.g. in the US, a majority of wind farms owned by the companies we cover are operating under

long-term power purchase agreements with pre-determined electricity off-take prices). We maintain our

positive stance on the wind farm developers and we highlight the valuation opportunities in the table below.

Our highest conviction investment ideas are Acciona and EDP Renovaveis.

Utility wind farm developers – comparison of valuation of renewable assets (EUR/share)

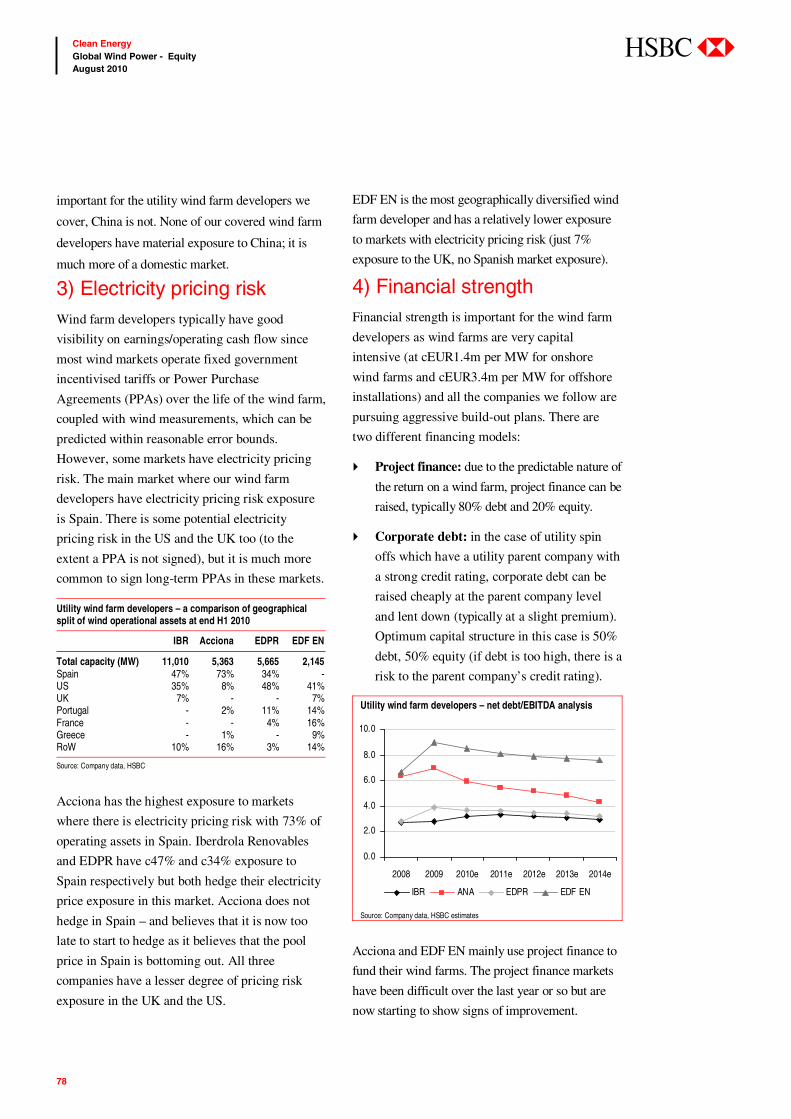

Valuation (EUR/share) Acciona EDPR IBR*

Operating assets 116.68 8.73 3.30 Construction assets 7.00 1.41 0.34 Other renewables 36.84 0.00 0.23 Less: Net Debt 91.14 4.33 1.35 Equity value per share (renewables) 69.38 5.80 2.52 Current share price (as of close of 25 August 2010) 60.70 4.33 2.52 % (discount)/premium to equity value of operating/construction assets (13%) (25%) 0% Pipeline valuation 19.34 1.38 0.59 Total equity value (renewables) 88.72 7.18 3.11 % (discount)/premium to current share price 46% 66% 23%

*Note: we have possibly underestimated the equity value of IBR’s operating/construction assets since we have not excluded the component of net debt relating to non-renewable assets (as the company does not provide a split). Source: HSBC estimates

Thematic summary Lower electricity demand due to the recession in Europe and the US is bad news for renewable electricity targets and hence for wind turbine demand

Due to the impact of the deep global recession, Europe and the US have both experienced reduced

electricity demand growth over the last couple of years. This, coupled with energy efficiency savings, has

caused us to lower our long-term electricity demand assumptions out to 2020, thus making the renewable

electricity targets in Europe and the US easier to achieve. This is bad news for wind turbine demand. In

the US, reduced electricity demand is compounded by a weak regulatory environment.

US regulation is weak – a potential federal LCES would still only provide a flat market out to 2020, with considerable downside in the absence of this

Even under our relatively optimistic regulatory scenario, i.e. that we get some form of LCES (Low

Carbon Electricity Standard) in the US in 2011, we calculate that a potential federal LCES (assuming

13% renewable electricity) would support a wind market of under 10GW pa (average) over the period

2010e-20e. This would imply flat/no growth in the US market, which delivered record new installations

of 10 GW in 2009. We note that these provisions are not law yet and indeed there is considerable

uncertainty over the final form of a potential federal LCES, with no fewer than 12 draft pieces of

legislation before Congress with quite different proposals. In our analysis, we adopt the Lugar version of

the bill as the most likely version to be passed into law. This version gives ‘clean’ energy targets which

include CCS (Carbon Capture and Storage) and nuclear installations, rather than just renewable energy

targets (as per the House of Representatives’ version of the bill), which we believe are necessary to

appease the coal and nuclear lobby and therefore eventually see the bill passed in the Senate; it is a good

general representation of most Senate versions of the bill. However, we consider it highly unlikely that

5

Clean Energy Global Wind Power - Equity August 2010

abc

this will be passed before the mid-term elections in November. Furthermore, note that any provisions

coming out of the Senate still need to be reconciled with the House of Representatives’ version of the bill

(the Waxman-Markey bill) before eventually moving for President Obama’s sign-off. The Waxman-

Markey bill gives renewable energy targets rather than ‘clean’ energy targets and is therefore more

favourable for renewables and wind, in our view.

In the absence of federal legislation, the main support mechanism for the US market would be the State

level legislation. Currently, some 31 states have their own targets for renewable electricity, known as

state level RPSs (Renewable Portfolio Standards), and a further 6 states have some sort of informal target

(ie not formally a state RPS). Based on states with an RPS or informal target alone, the US market would

be only a 5GW pa (average) wind market until 2020. If we consider only states with penalty schemes to

support their state level RPS targets (just 16 states), we calculate wind demand in the US of just 3.6GW

pa (average) up to 2020. This eventuality is unlikely, but nevertheless would be disastrous for the wind

companies, in our view.

In our view, GE, Mitsubishi and Clipper will suffer more than most players since these companies all

have more than 85% sales exposure to the US market. Vestas, Gamesa and Suzlon all have around 25%

of their sales from the US.

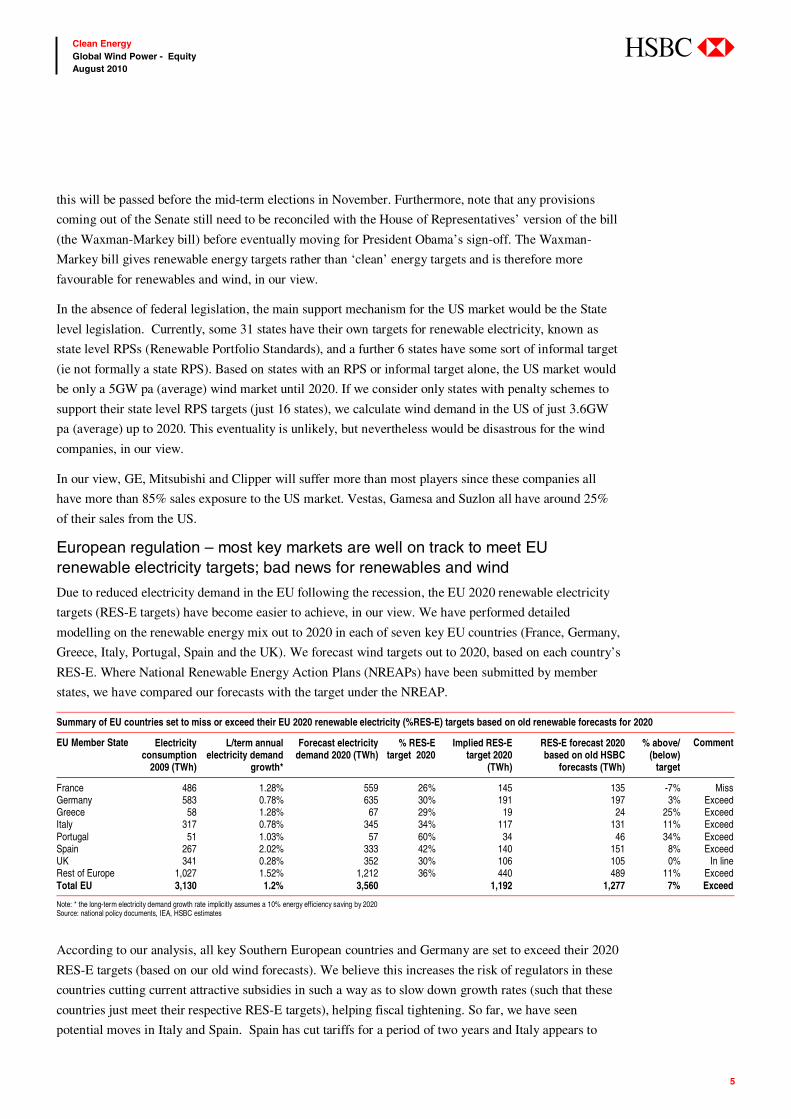

European regulation – most key markets are well on track to meet EU renewable electricity targets; bad news for renewables and wind

Due to reduced electricity demand in the EU following the recession, the EU 2020 renewable electricity

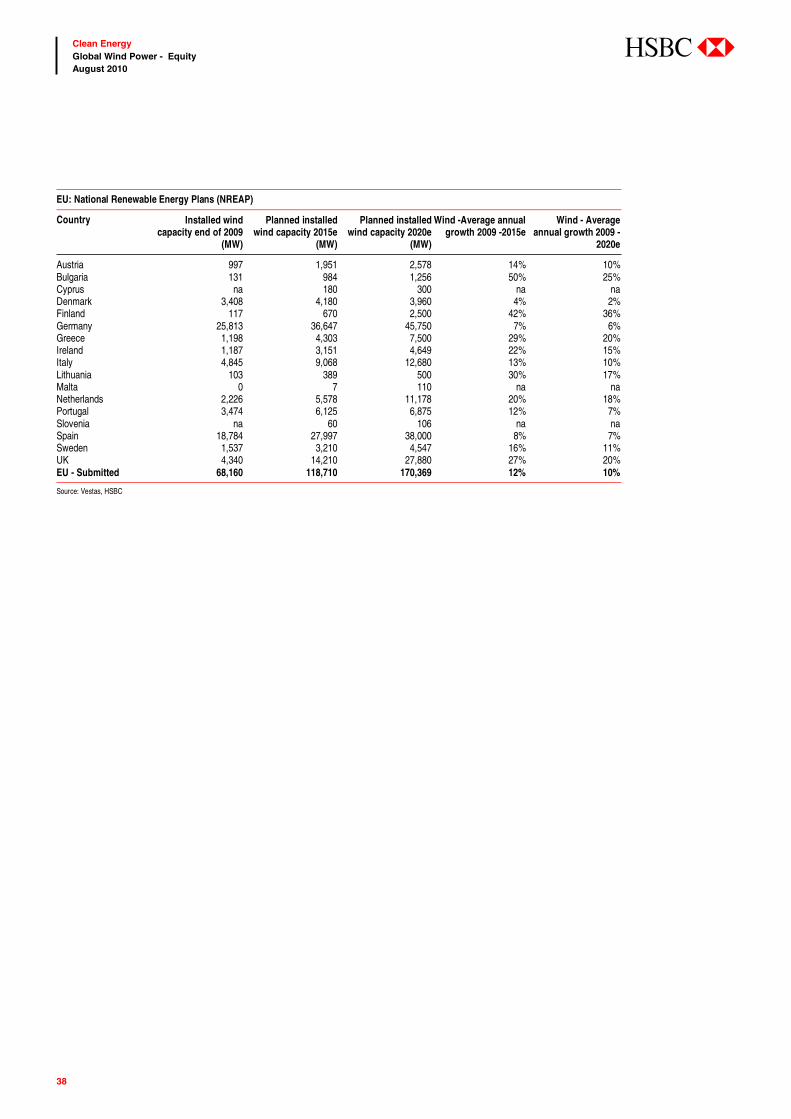

targets (RES-E targets) have become easier to achieve, in our view. We have performed detailed

modelling on the renewable energy mix out to 2020 in each of seven key EU countries (France, Germany,

Greece, Italy, Portugal, Spain and the UK). We forecast wind targets out to 2020, based on each country’s

RES-E. Where National Renewable Energy Action Plans (NREAPs) have been submitted by member

states, we have compared our forecasts with the target under the NREAP.

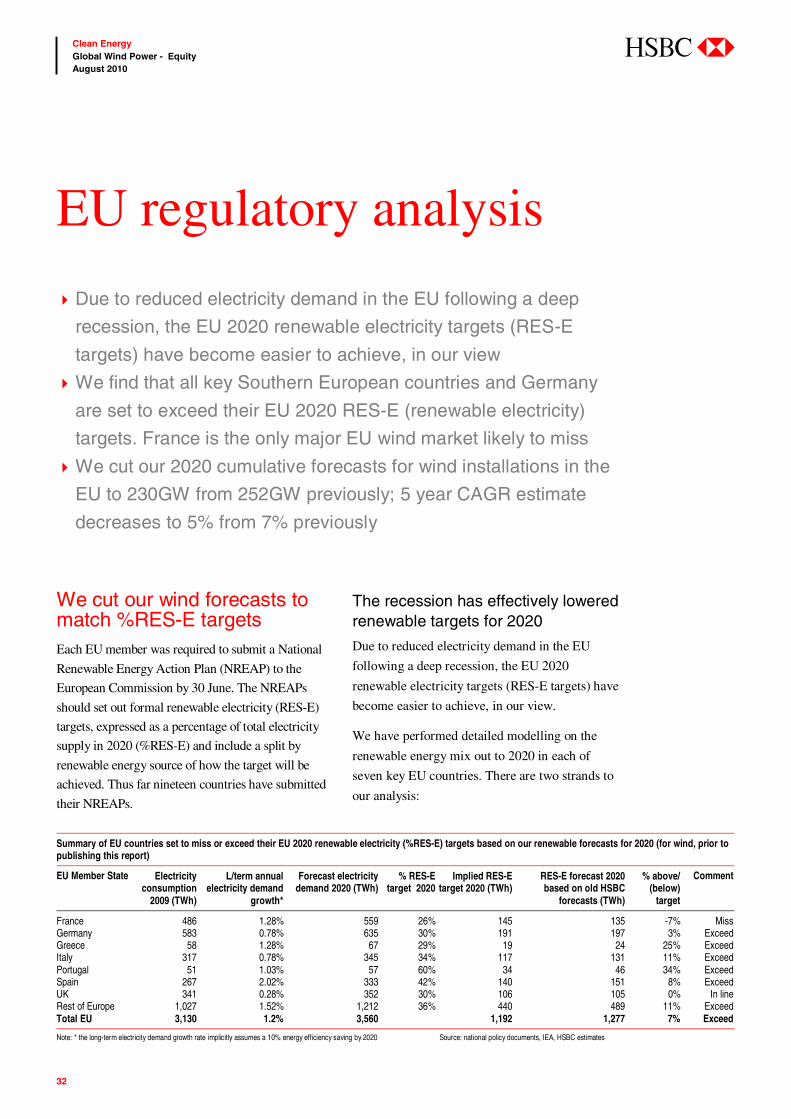

Summary of EU countries set to miss or exceed their EU 2020 renewable electricity (%RES-E) targets based on old renewable forecasts for 2020

EU Member State Electricity consumption

2009 (TWh)

L/term annual electricity demand

growth*

Forecast electricity demand 2020 (TWh)

% RES-E target 2020

Implied RES-E target 2020

(TWh)

RES-E forecast 2020 based on old HSBC

forecasts (TWh)

% above/ (below)

target

Comment

France 486 1.28% 559 26% 145 135 -7% MissGermany 583 0.78% 635 30% 191 197 3% ExceedGreece 58 1.28% 67 29% 19 24 25% ExceedItaly 317 0.78% 345 34% 117 131 11% ExceedPortugal 51 1.03% 57 60% 34 46 34% ExceedSpain 267 2.02% 333 42% 140 151 8% ExceedUK 341 0.28% 352 30% 106 105 0% In lineRest of Europe 1,027 1.52% 1,212 36% 440 489 11% ExceedTotal EU 3,130 1.2% 3,560 1,192 1,277 7% Exceed

Note: * the long-term electricity demand growth rate implicitly assumes a 10% energy efficiency saving by 2020 Source: national policy documents, IEA, HSBC estimates

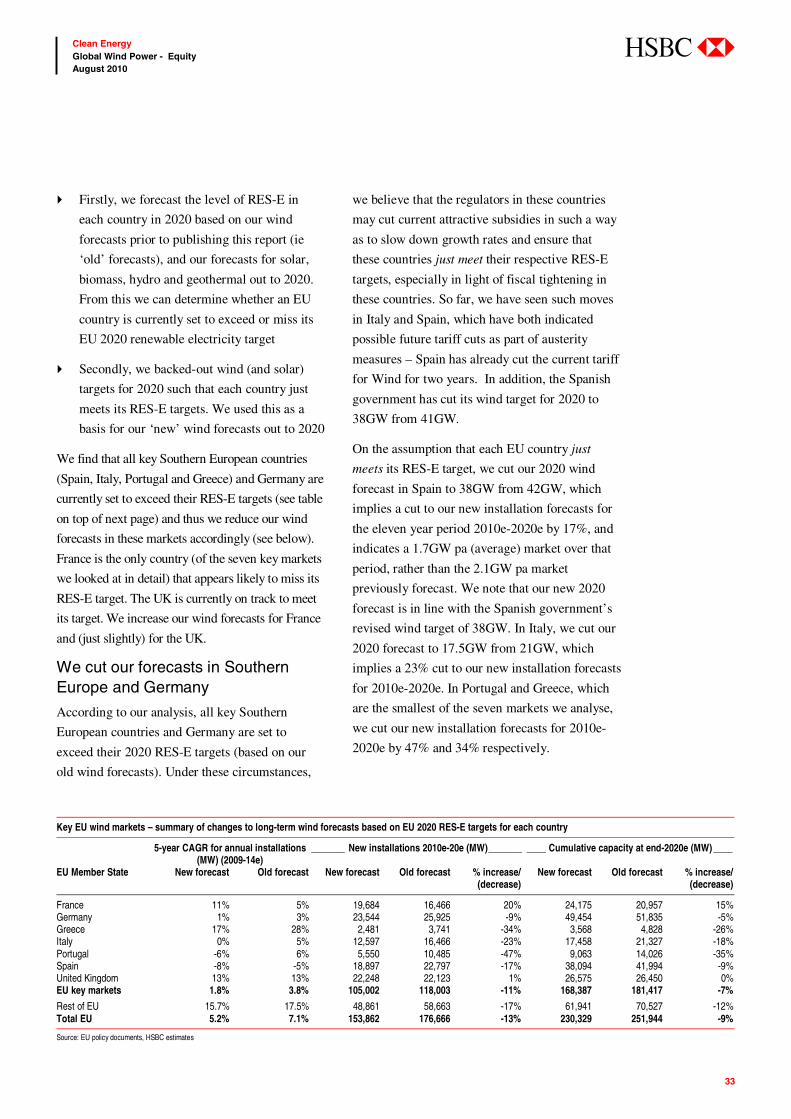

According to our analysis, all key Southern European countries and Germany are set to exceed their 2020

RES-E targets (based on our old wind forecasts). We believe this increases the risk of regulators in these

countries cutting current attractive subsidies in such a way as to slow down growth rates (such that these

countries just meet their respective RES-E targets), helping fiscal tightening. So far, we have seen

potential moves in Italy and Spain. Spain has cut tariffs for a period of two years and Italy appears to

6

Clean Energy Global Wind Power - Equity August 2010

abc

have shied away from making cuts, at least for now. In addition, the Spanish government has cut its wind

target for 2020 to 38GW from 41GW. We find that the France is the only country that is set to miss its

2020 RES-E target (relative to our old forecasts). The UK is more or less on track to meet its target.

Enercon and Gamesa have the highest exposure to these markets, from which they both derive around

50% of their sales. Vestas, Nordex and REpower derive around a third of their sales from these markets.

Wind industry demand forecasts – we cut our forecasts in the US and Europe but increase forecasts in China

Due to lower electricity demand following the deep recession in Europe and the US, and weak regulation

in the US, we cut our wind forecasts in these regions. In the US, we now forecast flat new installation

growth over the next five years (from 7% pa previously) and in Europe, we forecast 5% pa growth (from

7% pa previously), although we see pockets of stronger growth in the UK (13% pa) and France (11% pa).

Global wind demand forecasts – summary of changes (MW)

2010e 2011e 2012e 2013e 2014e Total 2010e-14e

Old forecast 36,963 41,896 45,920 50,094 53,810 228,683 New forecast 36,325 40,275 45950 49,275 52,450 225,275 Difference -638 -621 30 -819 -1,360 -3,408 % increase/(decrease) -1.7% -1.5% 0.1% -1.6% -2.5% -1.5% Due to: Decrease in US -1,693 -2,496 -2,995 -3,969 -4,460 -15,613 Decrease in Europe -895 -550 -400 -800 -1,275 -3,920 Increase in China 1,000 1,000 1,500 2,000 2,500 8,000 Increase in RoW 950 1,425 1,925 1,950 1,875 8,125 Total change in forecasts -638 -621 30 -819 -1,360 -3,408

Source: HSBC estimates

We cut our five year global demand CAGR to 7.0% from 7.5% previously and our 10-year industry demand

CAGR forecast to 5.5% from 6.7% previously. We would have cut our global wind market forecasts by

more but for support from a strong Chinese market and also pockets of growth in emerging markets in areas

such as South America, Eastern Europe, Turkey and Canada. China will be the most significant driver of

global growth, in our view. We forecast that it will account for 38% of the global market over the next five

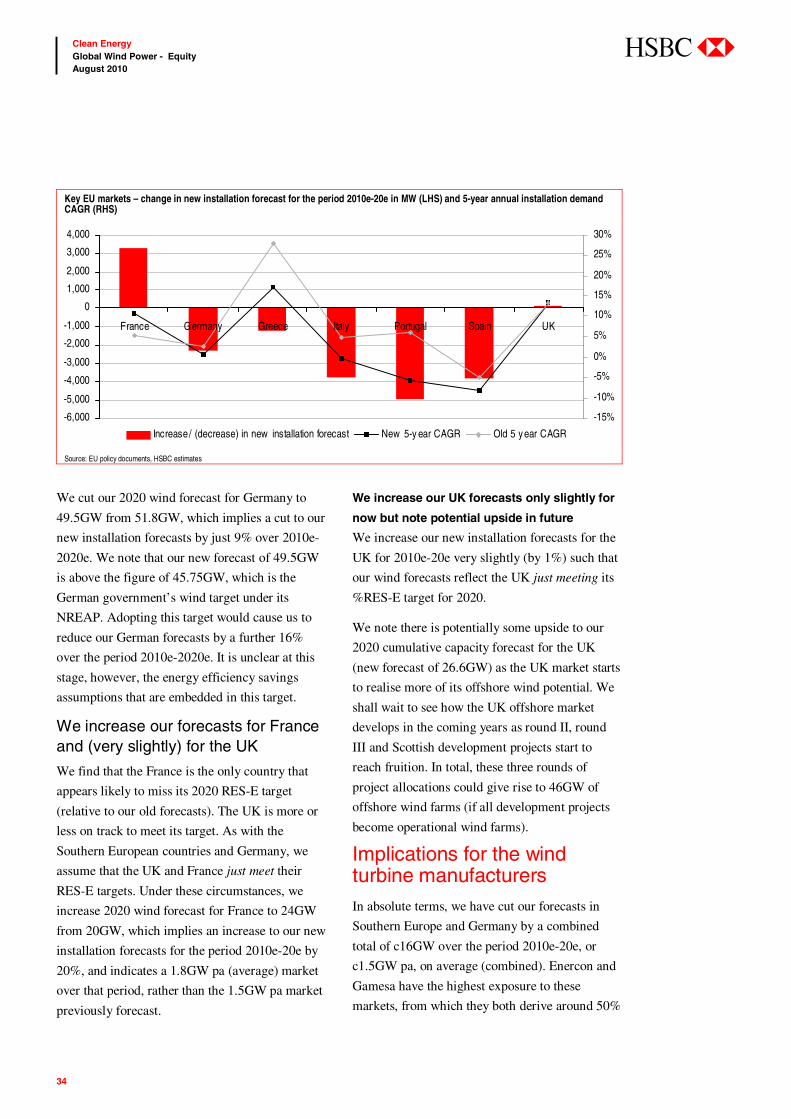

Key EU markets – change in new installation forecast for the period 2010e-20e (LHS) and 5-year annual installation demand CAGR (RHS)

-6,000

-5,000

-4,000

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

France Germany Greece Italy Portugal Spain UK

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Increase/ (decrease) in new installation forecast New 5-y ear CAGR Old 5 y ear CAGR

Source: EU policy documents, HSBC estimates

7

Clean Energy Global Wind Power - Equity August 2010

abc

years (2010e-14e) and will grow at 8% pa. The current National Development and Reform Commission

(NDRC) target for wind in China is 150GW by 2020, but the goal post keeps moving (the target has been

upgraded three times in the last five years). We forecast cumulative capacity of 241GW by 2020.

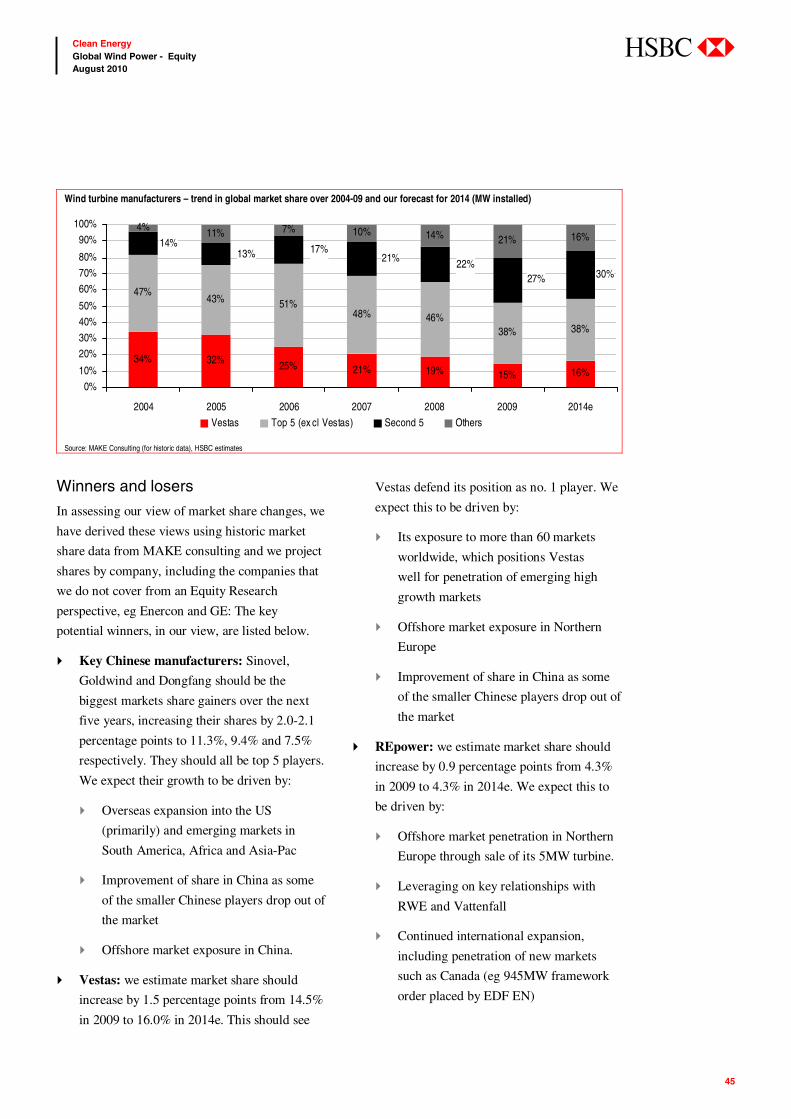

We analyse the exposure of key wind OEMs to three market groupings that we define as “high growth”,

“growth” and “ex-growth”. The Chinese manufactures, Sinovel, Goldwind and Dongfang, currently have the

best growth prospects in our view, on the back of domestic Chinese market growth. Furthermore they are all

looking to internationalise, particularly into the US; any new market penetration will add to their growth

profile. Clipper, GE and Gamesa are the least exposed to growth markets (roughly 0-25% of sales exposed to

such markets). Vestas, Suzlon, REpower and Nordex all have good exposure to growth markets (roughly 40-

60% of sales exposed to such markets). These are the best positioned of the non-Chinese players, in our view.

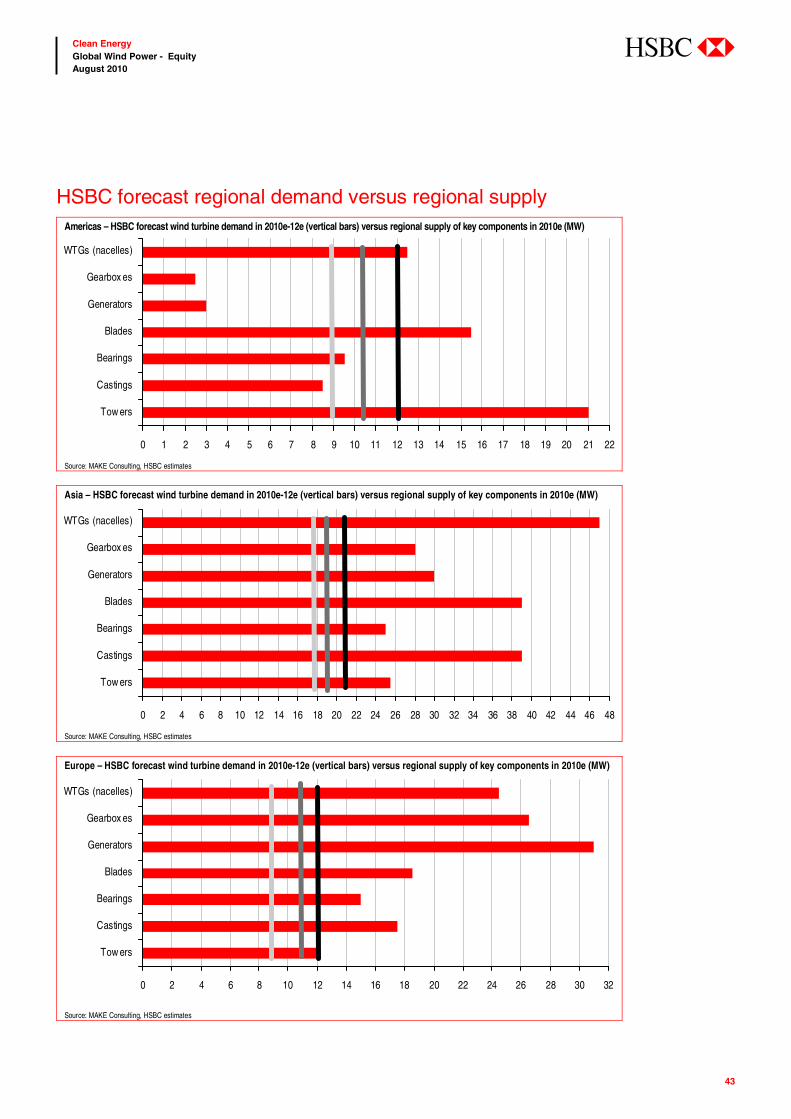

We expect no supply bottlenecks in the coming years, in fact we think the market is oversupplied

The wind industry dynamic has changed considerably since early 2008. In early 2008, due to strong

growth in the industry over the period 2005-08 (4-year CAGR of 34%), there were bottlenecks in some

parts of the supply chain. However, the credit crisis (from September 2008) led to a dry up in project

finance for renewable projects and order flow slowed to a trickle. Due to this, today, wind turbine

manufacturers and their sub-suppliers have found themselves with under utilised factory space, following

a period of heavy investment in the run up to the credit crisis.

HSBC forecast global wind turbine demand (grey line) versus global supply of key components in 2012e (MW)

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95

Tow ers

Castings

Bearings

Blades

Generators

Gearbox es

WTGs (nacelles)

Source: EU policy documents, HSBC estimates

We do not see any bottlenecks of any key components in the coming years (2010e-12e), based on our global

demand forecasts and MAKE Consulting’s supply forecasts. We see bearings as the tightest part of the value

chain but still with 11% overcapacity by 2012e. We also note that increasing demand for larger turbines could

create bottlenecks in some other large-sized (2MW or higher) components. There are, however, important

differences between regional supply chains: Asia is in short supply of larger turbines, these will likely need to

be exported from overseas (which is more expensive than sourcing from within Asia); the Americas are in

short supply of gearboxes and generators, again these will likely need to be imported, probably from Europe.

8

Clean Energy Global Wind Power - Equity August 2010

abc

It is not as important to be vertically integrated as it was pre-2008, when there were shortages in a number

of key components. That said, we still believe it is beneficial for a global wind turbine manufacturer to

have in-house capacity in most key components and ideally with a global spread. This will help quality

control and also reduce transportation costs due to proximity to regional markets, in our view. In the case

of Vestas and Gamesa (and other Western wind turbine manufactures), which have integrated facilities in

China, in-house capacity should also give access to cheaper manufacturing costs. Vestas, Gamesa and

Suzlon all have a good level of in-house manufacturing capacity, although Vestas and Suzlon both have

no in-house gearbox capacity. Vestas has the mostly globally spread manufacturing capacity with

factories in six European countries, the US, India and China.

We expect M&A to return to the sector

Following a period of industry consolidation in the early 2000s, globally, the competitive landscape for

the wind sector is becoming more fragmented once again. This is driven by the emergence of a large

number of domestic, Chinese players, of which a small number (Sinovel, Goldwind and DongFang) are

taking significant global market share on the back of a strong Chinese market. We see further

fragmentation in the coming years due to the emergence of Korean players such as Daewoo, Hyundai,

and Samsung. This increased fragmentation, coupled with anaemic growth (relative to previous years) in

the US and Europe increases the chances of M&A in the coming years.

We see the Chinese and Korean players as potential acquirers as they internationalise. In particular,

acquisition of a European player to penetrate Europe, where the grid codes are more stringent and thus

require higher-tech turbines (with power control electronics), would make sense, in our view.

Long-term (ie ten years out), we see the top 10 players comprising Vestas, one other European player,

GE, and Siemens, with the remainder split between Chinese and Korean players.

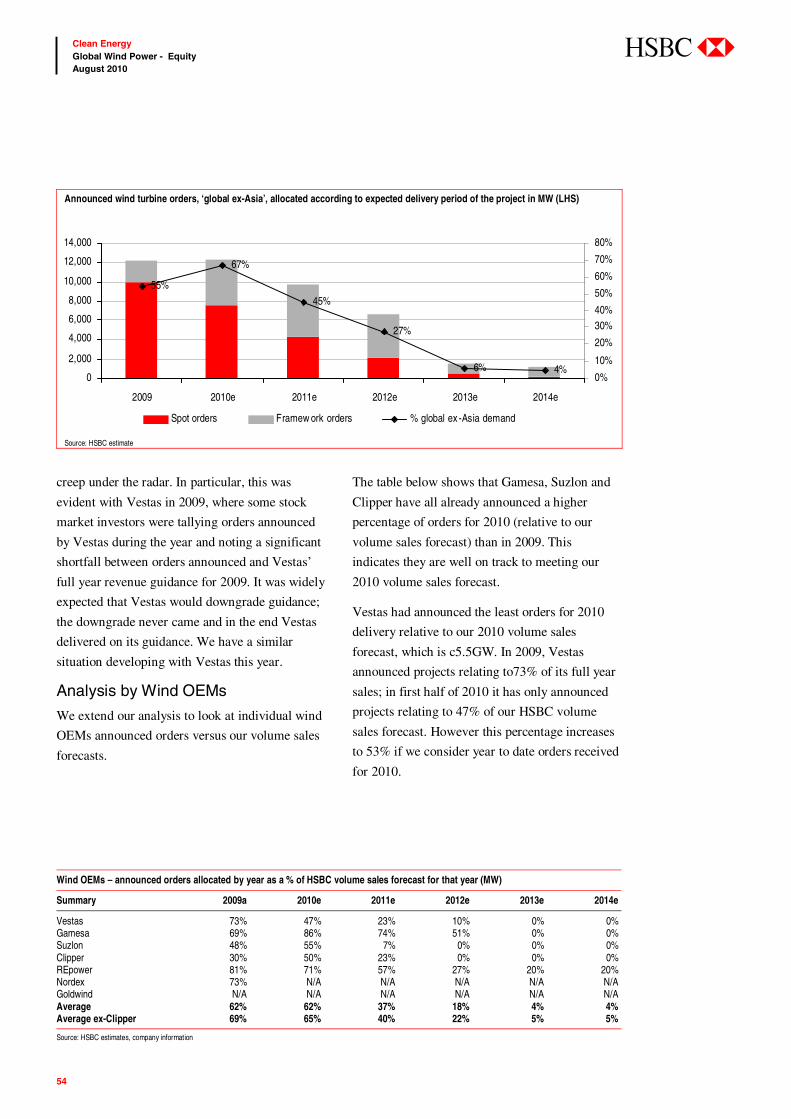

Order flow data supports our industry forecasts (near term) and suggests most manufacturers are on track to meet our 2010 volume sales forecasts

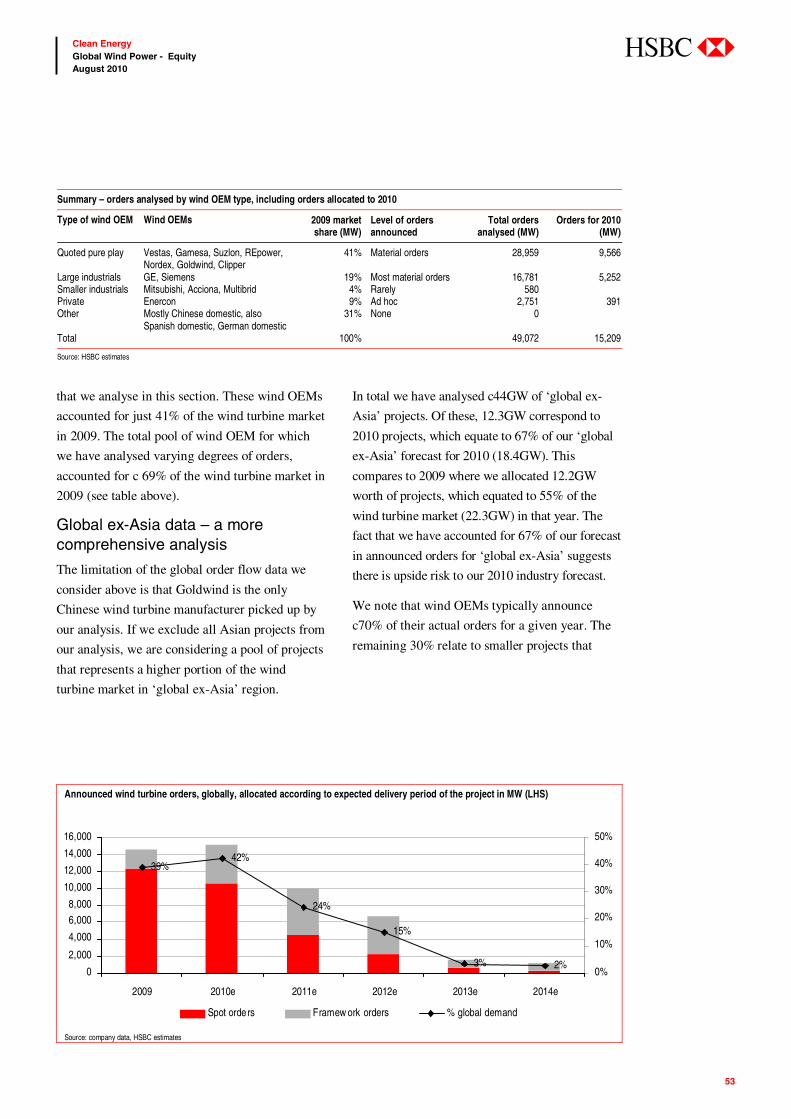

We have analysed order data since the start of 2007 for a selection of leading wind OEMs, which publicly

announce their orders (albeit only material ones). We have analysed a total of 49GW worth of orders,

which correspond mostly to ‘global ex-Asia’ orders (44GW). Of the ‘global ex-Asia’ orders, 12.3GW

correspond to 2010 projects, which equate to 67% of our ‘global ex-Asia’ forecast for 2010 (18.4GW).

This compares to 2009 announced orders, which represented just 55% of the wind turbine market

(22.3GW) in that year. Thus, bottom-up data suggests the wind industry is well on track to meet our 2010

market forecast. We note that wind OEMs typically announce c70% of their actual orders for a given

year. The remaining 30% relate to smaller projects that creep under the radar.

We extend our analysis to look at individual wind OEMs’ announced orders versus our volume sales

forecasts. Gamesa, Suzlon and Clipper are all on track to meet our 2010 volume sales forecasts. Vestas is

off track: in 2009, Vestas announced projects relating to 73% of its full year sales; thus far in 2010 it has

only announced projects relating to 53% of our HSBC volume sales forecast (and this is with our cut

2010 forecasts to match the company’s revised EUR6bn revenue target).

9

Clean Energy Global Wind Power - Equity August 2010

abc

Investment ideas Our sector stance

Our preference is for the wind developers and we are cautious on the OEMs. Our highest conviction

investment ideas among wind farm developers remain Acciona and EDP R (both Overweight (V)).

However, in this note we have lowered our lower tariff expectations going forward and this has resulted

in reductions in price targets for the developers. We have cut our target price for Acciona to EUR94

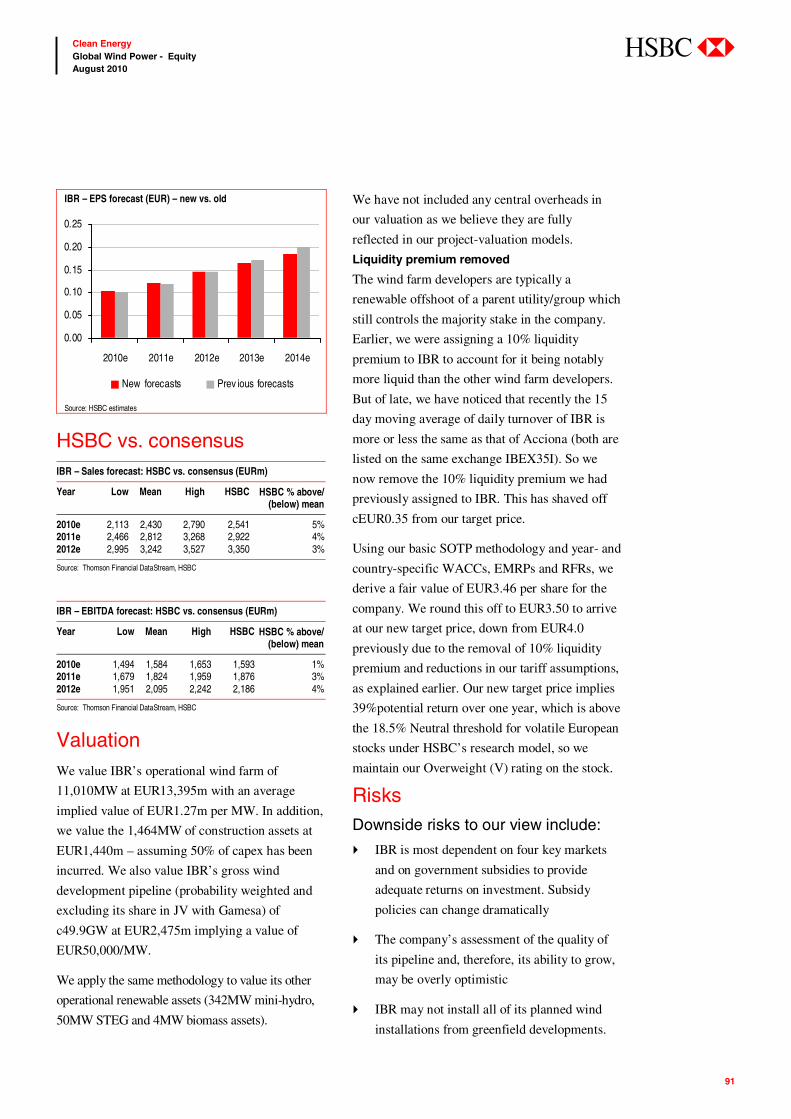

(previously EUR120) and for Iberdrola Renovables to EUR3.50 (previously EUR4.00). We have also cut

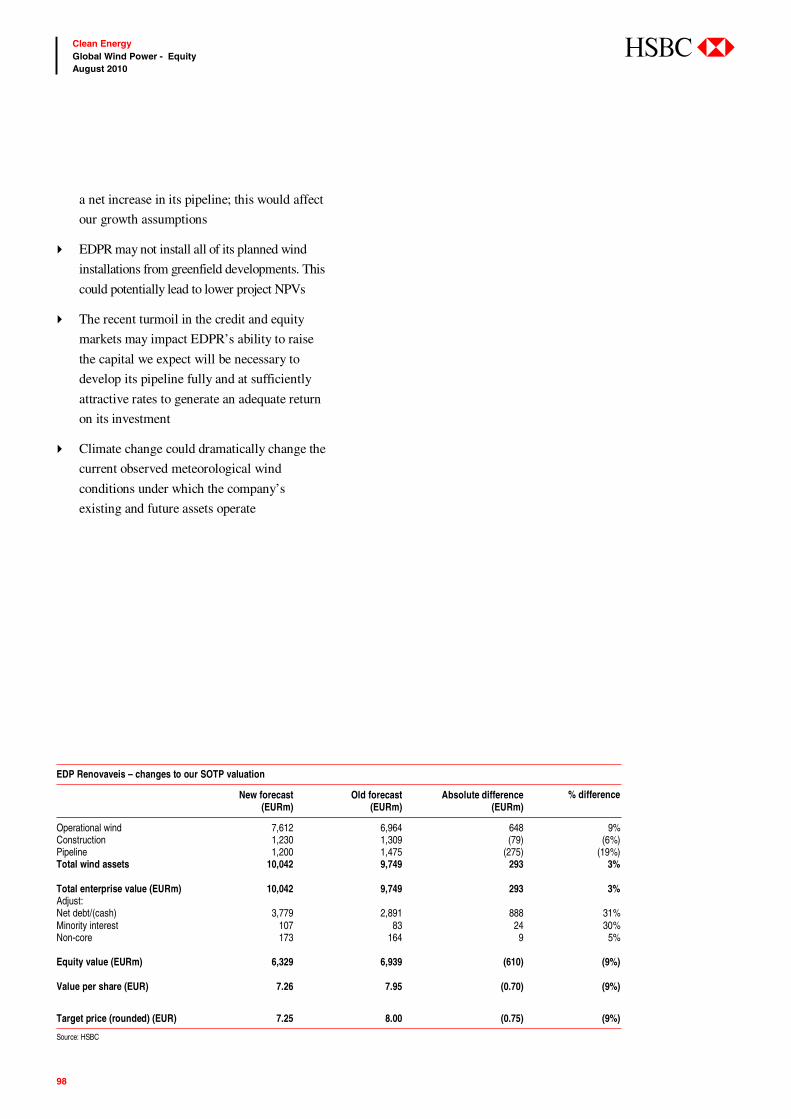

our target price on EDP Renovaveis (OW(V)) to EUR7.25 from EUR8.00 and on EDF Energies

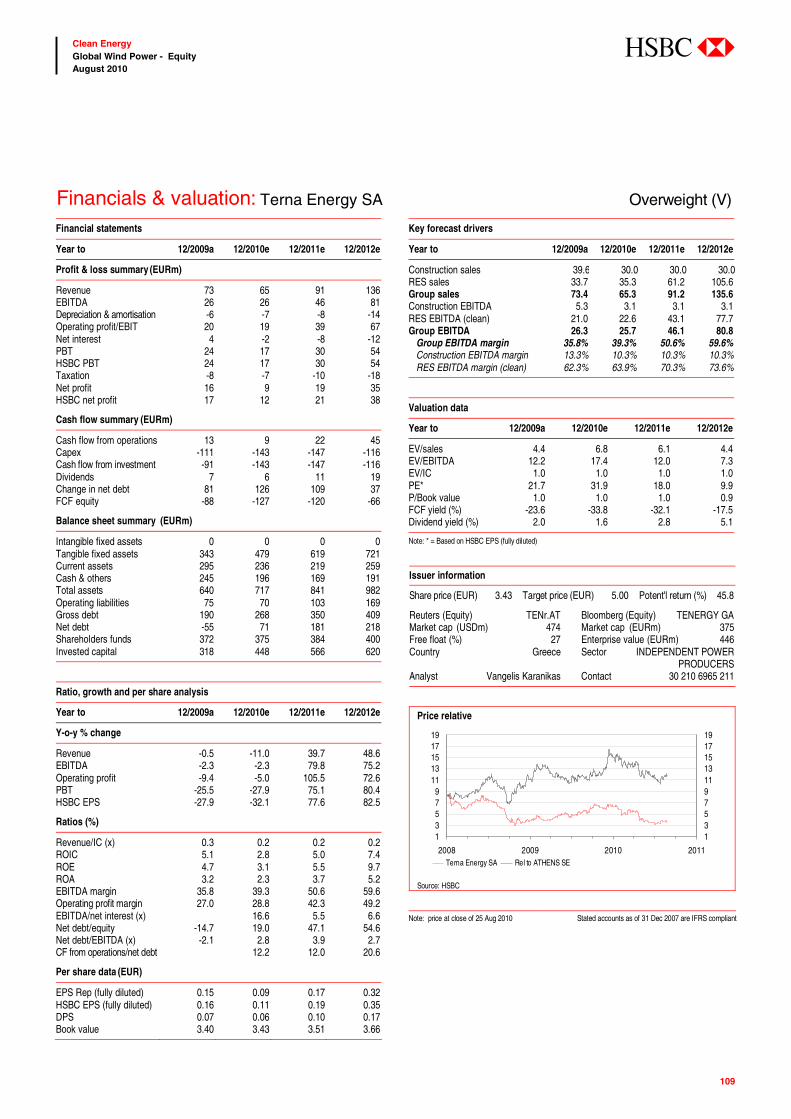

Nouvelles (N(V)) to EUR34.00 from EUR40.00. We maintain our rating and target price on Terna

Energy (Overweight (V), TP EUR5.00).

We have developed a qualitative scorecard to rank the wind developers on a number of criteria.

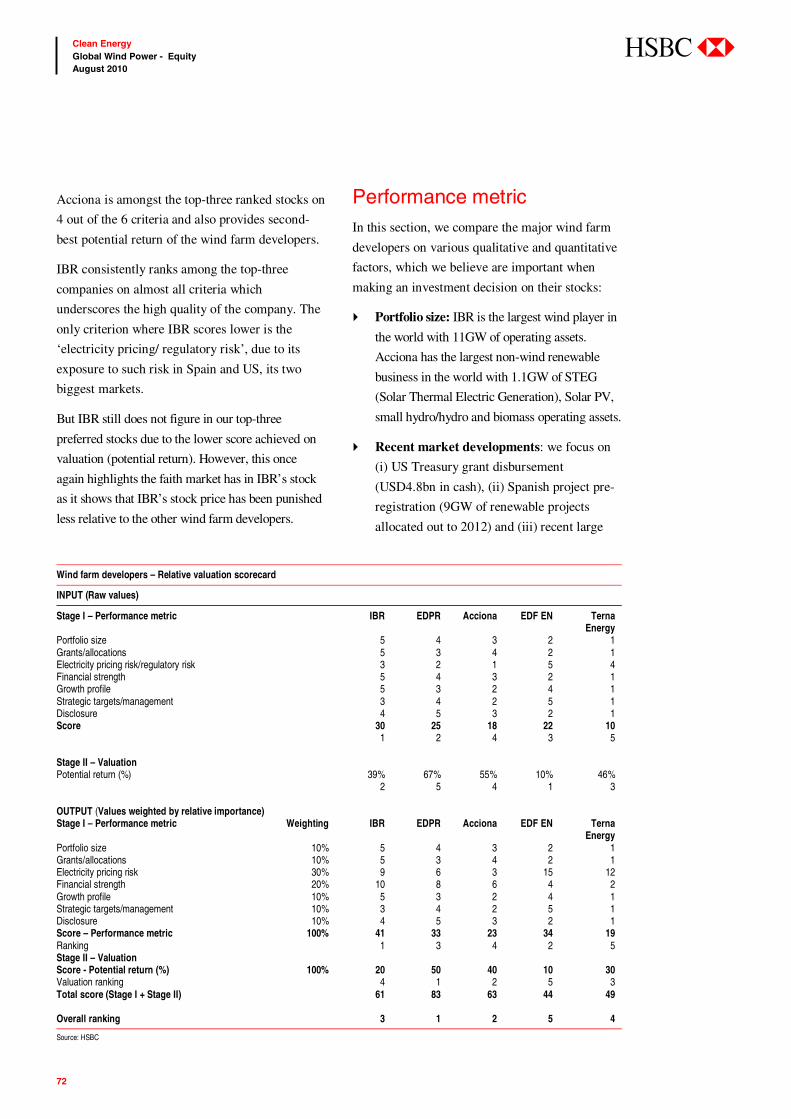

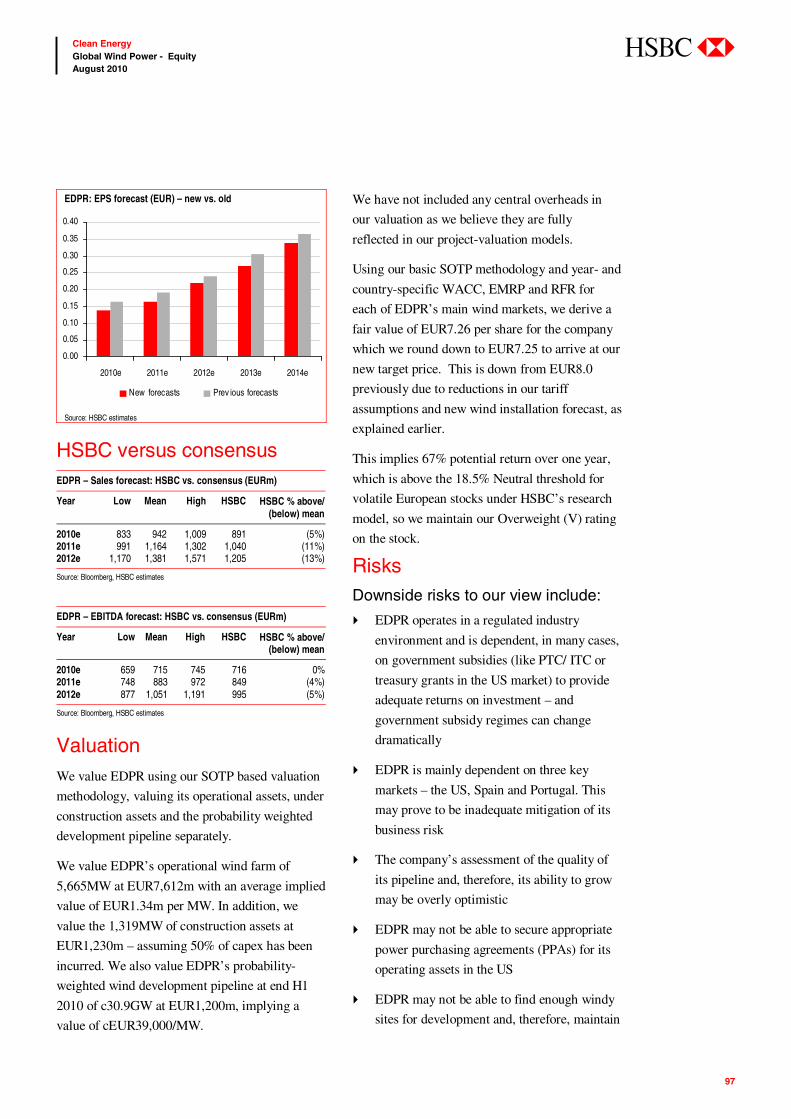

Qualitative scorecard We have developed a performance scorecard for the wind farm developers. EDPR is our highest

conviction idea and Acciona is second as per this scorecard (see table on page 12).

EDPR and Acciona are our highest conviction ideas EDPR provides the best disclosure and is second best (after IBR) in terms of portfolio size, financial

strength and quality of management. EDPR currently provides the most potential return out of the wind

farm developers.

Acciona is amongst the top-three ranked stocks on 4 out of the 6 criteria, and provides second-best

potential return out of the wind farm developers.

We note that based on the first-stage score, IBR is the strongest company but in our view its share price

does not offer as high return potential as EDPR and Acciona, thus overall it is ranked number 3 behind

EDPR and Acciona.

Methodology

Our two-stage scorecard takes into account a) a performance metric (comprising of various qualitative

and quantitative criteria) and b) potential return on the stock.

At the first stage, the quantitative criteria include the portfolio size, grants/allocations received, electricity

pricing risk/ regulatory risk, financial strength, and the future growth profile. For the qualitative criteria, we

include strategic targets/ quality of management and the level of disclosure provided by a particular company.

To the ranks of each company on every criterion, we then apply different weights (which we assign based

on our view of their relative importance to the company’s performance) and arrive at first-stage score.

The second-stage ranks the stocks on the potential return offered by a stock and multiply the rank with a

multiple (10x) to arrive at the second-stage score.

We apply equal weights to the two scores from the end of each stage and the sum total of the two

weighted score gives us our overall ranking.

10

Clean Energy Global Wind Power - Equity August 2010

abc

The scores are given in descending order (from 5 to 1), meaning better a company is on a particular

criterion, the higher the score it gets. For example, the level of disclosure is best for EDPR so it gets a score

of 5 on that criterion while Terna Energy is weakest in disclosures and hence it gets the lowest score of 1.

Stage I – Performance metric In stage I, we compare the major wind farm developers on various qualitative and quantitative factors,

which we believe are important when making an investment decision on their stocks:

Portfolio size: IBR is the largest wind player in the world with 11GW of operating assets. Acciona

has the largest non-wind renewable business in the world with 1.1GW of STEG, Solar PV, small

hydro/hydro and biomass operating assets.

Recent market developments: we focus on (i) US Treasury grant disbursement (USD4.8bn in cash),

(ii) Spanish project pre-registration (9GW of renewable projects allocated out to 2012) and (iii)

recent large offshore development right allocations in the UK totalling 32GW (enough to power a

quarter of the UK’s electricity). IBR was a winner in all three markets.

Electricity pricing risk: how secure are the wind farm developers’ cash flows? Acciona is most

exposed to electricity prices, with 73% exposure to Spain (unhedged). IBR and EDPR are both

hedged. EDF EN has no exposure to Spain.

Financial strength: IBR and EDPR have strong financial support from their parent groups, which

provide credit for the financing of nearly all of their wind farms. EDF EN and Acciona raise project

finance, which has made financing difficult over the last year or so; however, the project finance

markets are now starting to improve.

Growth profile: EDPR offers the most attractive earnings (EPS) growth with a three year EPS

CAGR of 24% over 2010e-13e. EDF EN has the best three year EBITDA CAGR of 20%.

Strategic targets and detailed disclosure: Information disclosure is good at EDPR and IBR at all levels.

Acciona and EDF EN give their long-term new installations (wind and other renewables) as well as their

financial targets but limited or no information on capacity factors and wind tariffs across geographies.

11

Clean Energy Global Wind Power - Equity August 2010

abc

Stage II – Valuation The stage II ranks the stocks on the basis of the potential return currently provided by it. The more

potential return a stock has, the higher score it gets. Out of the wind farm developers, EDPR currently has

the most potential upside while Acciona is the second best.

Wind farm developers – Relative valuation scorecard

INPUT

Stage I – Performance Metric IBR EDPR Acciona EDF EN Terna Energy Portfolio size 5 4 3 2 1 Grants/allocations 5 3 4 2 1 Electricity pricing risk/regulatory risk 3 2 1 5 4 Financial strength 5 4 3 2 1 Growth profile 5 3 2 4 1 Strategic targets/management 3 4 2 5 1 Disclosure 4 5 3 2 1 Score 30 25 18 22 10 1 2 4 3 5 Stage II – Valuation Potential return (%) 39% 67% 55% 10% 46% 2 5 4 1 3 OUTPUT Stage I – Performance Metric Weighting IBR EDPR Acciona EDF EN Terna Energy Portfolio size 10% 5 4 3 2 1 Grants/allocations 10% 5 3 4 2 1 Electricity pricing risk 30% 9 6 3 15 12 Financial strength 20% 10 8 6 4 2 Growth profile 10% 5 3 2 4 1 Strategic targets/management 10% 3 4 2 5 1 Disclosure 10% 4 5 3 2 1 Score – Performance metric 100% 41 33 23 34 19 Stage I ranking 1 3 4 2 5 Stage II – Valuation Score – Potential return (%) 100% 20 50 40 10 30 Valuation ranking 4 1 2 5 3 Total score 61 83 63 44 49

Overall ranking 3 1 2 5 4

Source: HSBC

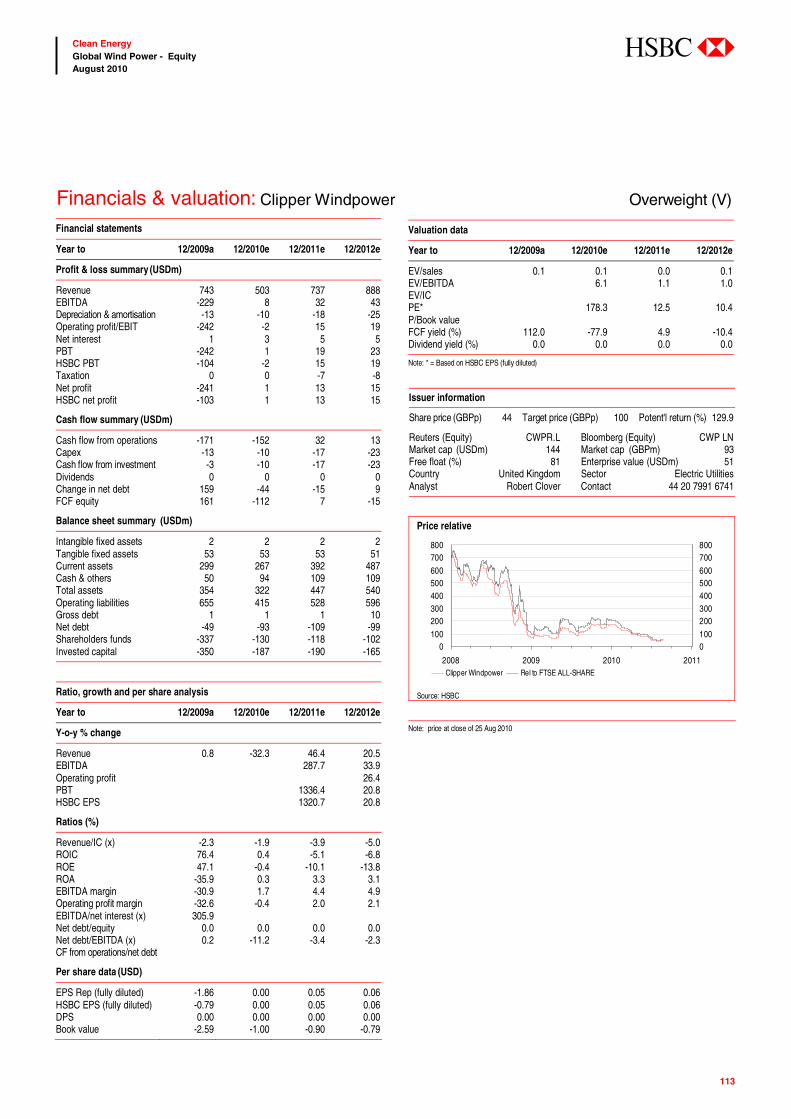

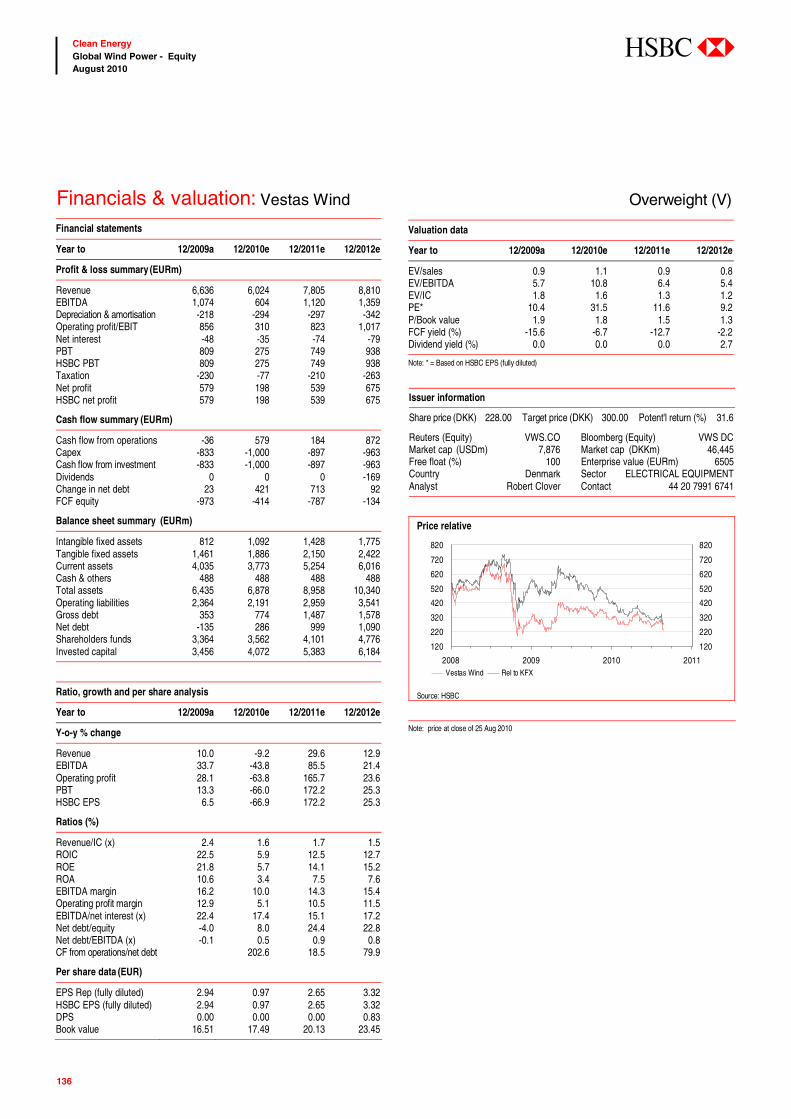

Among wind turbine manufacturers we downgrade Gamesa from OW(V) to N(V) due to the cuts in our

industry growth expectations. We decrease our target price for Gamesa to EUR5.50 from EUR14.00.

We also cut our target price for REpower to EUR115 from EUR150 and rating from Overweight (V)

rating to Neutral (V). For Vestas, the 27% share price reduction in its value after the August 18th profit

warning has meant that we still see value in Vestas, although short term catalysts for re-rating are harder

to see. We decrease our target price for Vestas to DKK300 from DKK425. We maintain our target price

for Nordex of EUR10, and our Overweight (V) rating. We have increased our target price for Clipper to

GBP1.00 (from GBP0.9) and upgrade our Neutral (V) rating on the stock to OW(V), based on our

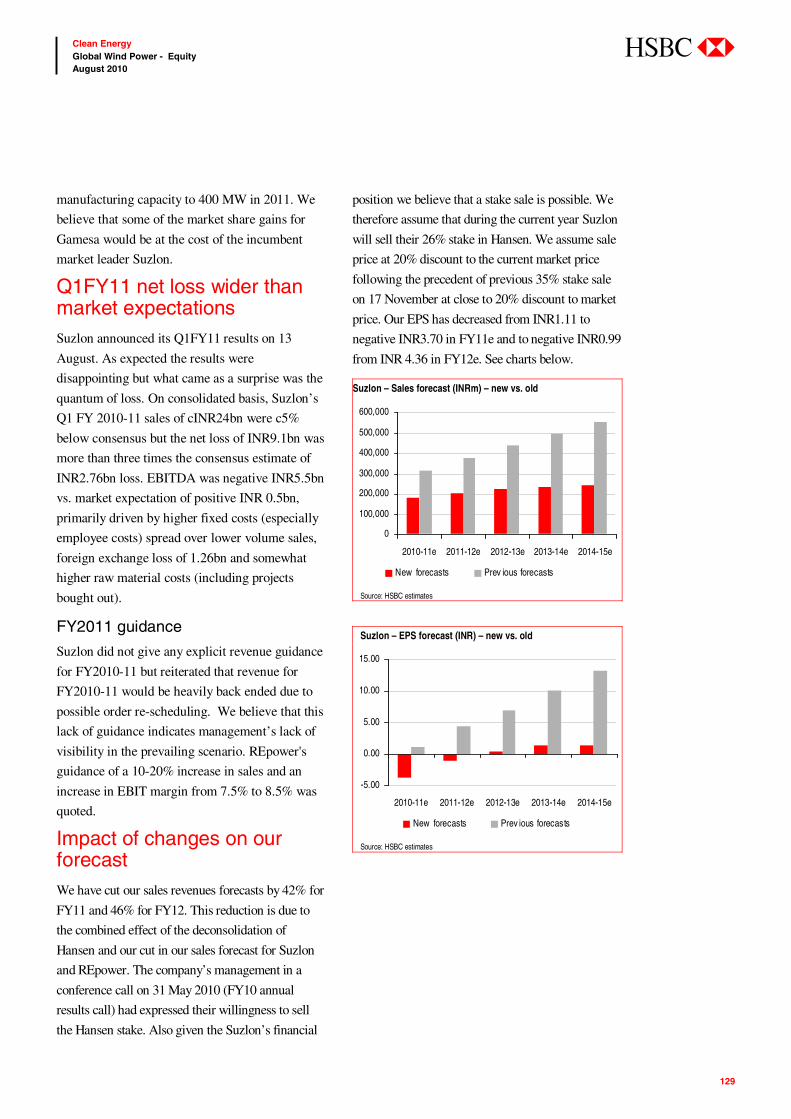

expectation of potential new orders. We cut our target price for Suzlon to INR42 from INR50, but

maintain our Underweight (V) rating on the stock.

12

Clean Energy Global Wind Power - Equity August 2010

abc

Valuation summary Wind coverage – summary target prices and ratings (Price as close of 25 August 2010)

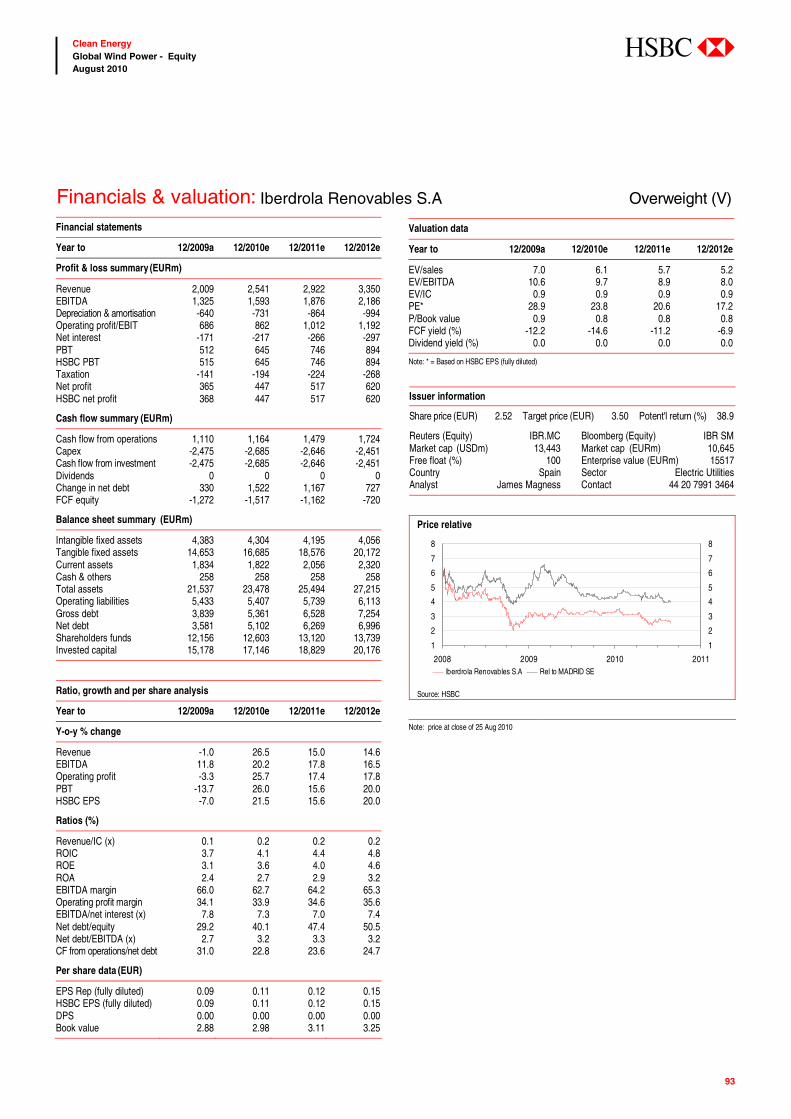

Stock Bloomberg Currency New TP Previous TP % potential return New rating Previous rating

Wind farm developers Acciona ANA SM EUR 94.00 120.00 55% Overweight (V) Overweight (V) Iberdrola Renovables IBR SM EUR 3.50 4.00 39% Overweight (V) Overweight (V) Terna Energy TENERGY GA EUR 5.00 5.00 45% Overweight (V) Overweight (V) EDP Renovaveis EDPR PL EUR 7.25 8.00 67% Overweight (V) Overweight (V) EDF Energies Nouvelles EEN FP EUR 34.00 40.00 10% Neutral (V) Neutral (V) Wind OEMs Vestas VWS DC DKK 300.00 425.00 32% Overweight (V) Overweight (V) Clipper CWP LN GBP 1.00 0.90 130% Overweight (V) Neutral (V) Nordex NDX1 GR EUR 10.00 10.00 47% Overweight (V) Overweight (V) Gamesa GAM SM EUR 5.50 14.00 8% Neutral (V) Overweight (V) REpower RPW GR EUR 115.00 150.00 17% Neutral (V) Overweight (V) Suzlon SUEL IN INR 42.00 50.00 -15% Underweight (V) Underweight (V)

Hansen Transmissions HSN LN GBP 0.95 1.35 76% Overweight (V) Overweight (V)

Source: Bloomberg, HSBC

Valuation data (price as of close of 25th Aug. 2010)

New Previous C’cy New Previous Current Potential ____EV/sales _____ ____EV/EBITDA _____ __ HSBC PE ____ ________ PEG _________ P/BV rating rating TP TP Price Return 2010e 2011e 2012e 2010e 2011e 2012e 2010e 2011e 2012e 2010e 2011e 2012e 2010e

Wind farm developers Acciona OW(V) OW(V) EUR 94.00 120.00 60.70 55% 1.6 1.6 1.6 9.0 8.1 7.4 18.4 14.5 12.1 1.0 1.0 1.1 0.7IBR OW(V) OW(V) EUR 3.50 4.00 2.52 39% 6.2 5.8 5.3 10.0 9.1 8.1 23.8 20.6 17.2 1.4 1.4 1.2 0.8Terna Energy

OW(V) OW(V) EUR 5.00 5.00 3.43 46% 6.8 6.1 4.4 17.4 12.0 7.3 31.9 18.0 9.9 N/A N/A n.m. 1.0

EDPR OW(V) OW(V) EUR 7.25 8.00 4.33 67% 6.8 6.3 5.8 8.4 7.7 7.0 30.8 26.1 19.7 1.3 1.0 0.8 0.7EDF EN N(V) N(V) EUR 34.00 40.00 30.89 10% 4.7 4.6 4.4 14.5 12.8 11.8 21.9 16.8 13.5 0.9 1.0 1.1 1.7 Mean 5.2 4.9 4.3 11.9 9.9 8.3 25.4 19.2 14.5 1.2 1.1 1.1 1.0 Median 6.2 5.8 4.4 10.0 9.1 7.4 23.8 18.0 13.5 1.2 1.0 1.1 0.8Wind OEMs Vestas OW(V) OW(V) DKK 300.00 425.00 228.00 32% 1.1 0.9 0.8 10.8 6.5 5.4 31.5 11.6 9.2 0.6 0.8 0.9 1.8Clipper OW(V) N(V) GBP 1.00 0.90 0.44 130% 0.1 0.0 0.0 6.2 1.1 0.7 n.m. 12.6 9.2 0.8 0.3 0.2 naNordex OW(V) OW(V) EUR 10.00 10.00 6.82 47% 0.2 0.2 0.1 4.1 2.9 1.9 18.5 11.4 7.1 na n.m. n.m. 1.2Gamesa N(V) OW(V) EUR 5.50 14.00 5.10 8% 0.7 0.6 0.6 7.8 6.7 6.1 21.4 16.4 12.4 0.7 0.7 0.7 0.8REpower N(V) OW(V) EUR 115.00 150.00 98.48 17% 0.5 0.4 0.3 6.0 5.3 4.2 15.8 14.8 12.4 na na n.m. 1.9Suzlon UW(V) UW(V) INR 42.00 50.00 49.60 -15% 1.0 0.9 0.8 17.8 12.5 9.3 n.m. n.m. 41.2 0.2 n.m. 0.7 1.2

Hansen OW(V) OW(V) GBP 0.95 1.35 0.54 76% 1.0 0.8 0.7 10.4 7.2 5.1 n.m. 30.6 10.6 na 0.7 0.2 0.7

Mean 0.6 0.6 0.5 9.0 6.0 4.7 21.8 16.2 10.2 0.6 0.6 0.5 1.3 Median 0.7 0.6 0.6 7.8 6.5 5.1 19.9 13.7 9.9 0.7 0.7 0.7 1.2

Source: Bloomberg, HSBC estimates

13

Clean Energy Global Wind Power - Equity August 2010

abc

Summary of changes to EPS estimates HSBC wind stock coverage – Summary of changes in our EPS forecast for 2010e-12e

Currency _____________2010e ____________ _____________ 2011e ____________ _____________ 2012e ____________ New Old % change New Old % change New Old % change

Windfarm developers Acciona EUR 3.30 5.60 (41%) 4.19 7.03 (40%) 5.00 8.44 (43%) IBR EUR 0.11 0.10 3% 0.12 0.12 2% 0.15 0.15 0% EDPR EUR 0.14 0.17 (15%) 0.17 0.19 (13%) 0.22 0.24 (9%) EDF EN EUR 1.41 1.23 15% 1.84 1.65 11% 2.29 1.67 37% Wind OEMs Vestas EUR 0.97 2.52 -61% 2.65 3.01 -12% 3.32 3.56 -7% Gamesa EUR 0.24 0.42 -43% 0.31 0.64 -52% 0.41 0.81 -49% Clipper USD 0.00 0.00 nm 0.06 0.06 0% 0.07 0.08 -14% REpower EUR 7.05 6.22 -12% 8.29 6.66 -20% 7.96 na na Nordex EUR 0.37 0.37 0% 0.60 0.60 0% 0.96 0.96 0% Suzlon INR -3.70 1.11 nm -0.99 4.36 nm 0.42 6.99 -94% Hansen EUR 0.00 0.00 nm 0.029 0.031 -6% 0.07 0.08 -14%

Source: HSBC estimates. For Suzlon, REpower and Hansen above, 2010-12e refer to FY1-FY13e

Why change forecasts and valuations?

We have made changes to target prices for our coverage universe of wind OEMs and wind farm

developers. The main catalysts are:

Weaker electricity demand in the EU. We have undertaken a detail review of the renewable

electricity (RES-E) targets for 2020 in the EU, including our own proprietary analysis of a possible

renewable energy mix in seven key EU wind markets that will allow these markets to hit their RES-E

targets for 2020. This has caused us to revise down our European market forecasts

Weaker electricity demand and a weak regulatory environment in the US. We have undertaken a

detailed review of the complex US regulatory environment, including an analysis of the state-level

Renewable Portfolio Standards (“RPSs”) and a potential federal Low Carbon Electricity Standard

(“LCES”). This has caused us to revise down our US market forecasts

Detailed analysis of global market data for 2009. This has caused us to revisit our global market

forecasts and market share model. In particular we consider the impact of the Chinese market and

Chinese wind turbine manufacturers (now three top 10 players, albeit on the strength of their

domestic market) on the global wind industry

Detailed analysis of trends in wind order flow over the last three and half years. We have looked at

spot project and framework projects pending in the coming years in order to match our top-down

regulatory analysis to the bottom up data in the coming years. This has caused us to revise down our

near term forecasts globally (in conjunction with our European and US regulatory analysis)

Although not the primary driver of this report, we have also updated our forecasts to reflect recent results

released by a number of our companies.

So what has changed?

Downgrading our global market forecasts

We downgrade our forecasts for the global wind power market, due to cuts to our US and European

forecasts out to 2020, which more than offset the increase we made to our Chinese market forecast. Our

14

Clean Energy Global Wind Power - Equity August 2010

abc

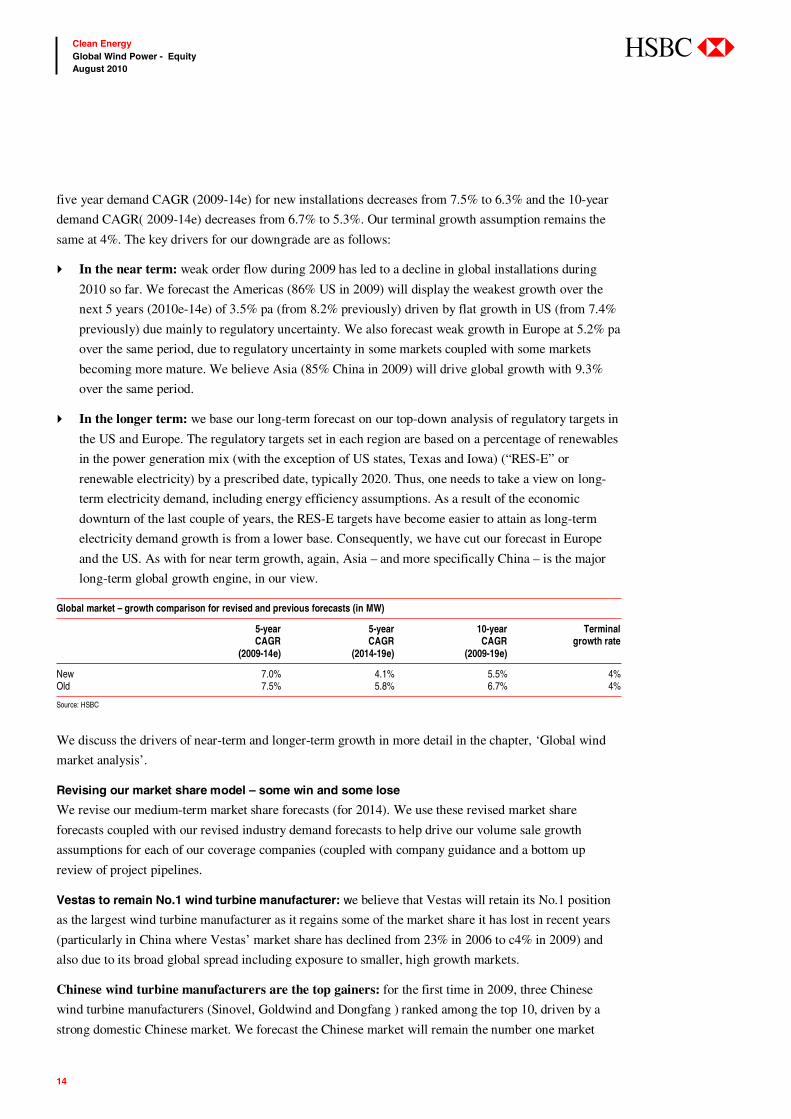

five year demand CAGR (2009-14e) for new installations decreases from 7.5% to 6.3% and the 10-year

demand CAGR( 2009-14e) decreases from 6.7% to 5.3%. Our terminal growth assumption remains the

same at 4%. The key drivers for our downgrade are as follows:

In the near term: weak order flow during 2009 has led to a decline in global installations during

2010 so far. We forecast the Americas (86% US in 2009) will display the weakest growth over the

next 5 years (2010e-14e) of 3.5% pa (from 8.2% previously) driven by flat growth in US (from 7.4%

previously) due mainly to regulatory uncertainty. We also forecast weak growth in Europe at 5.2% pa

over the same period, due to regulatory uncertainty in some markets coupled with some markets

becoming more mature. We believe Asia (85% China in 2009) will drive global growth with 9.3%

over the same period.

In the longer term: we base our long-term forecast on our top-down analysis of regulatory targets in

the US and Europe. The regulatory targets set in each region are based on a percentage of renewables

in the power generation mix (with the exception of US states, Texas and Iowa) (“RES-E” or

renewable electricity) by a prescribed date, typically 2020. Thus, one needs to take a view on long-

term electricity demand, including energy efficiency assumptions. As a result of the economic

downturn of the last couple of years, the RES-E targets have become easier to attain as long-term

electricity demand growth is from a lower base. Consequently, we have cut our forecast in Europe

and the US. As with for near term growth, again, Asia – and more specifically China – is the major

long-term global growth engine, in our view.

Global market – growth comparison for revised and previous forecasts (in MW)

5-year 5-year 10-year Terminal CAGR CAGR CAGR growth rate (2009-14e) (2014-19e) (2009-19e)

New 7.0% 4.1% 5.5% 4% Old 7.5% 5.8% 6.7% 4%

Source: HSBC

We discuss the drivers of near-term and longer-term growth in more detail in the chapter, ‘Global wind

market analysis’.

Revising our market share model – some win and some lose

We revise our medium-term market share forecasts (for 2014). We use these revised market share

forecasts coupled with our revised industry demand forecasts to help drive our volume sale growth

assumptions for each of our coverage companies (coupled with company guidance and a bottom up

review of project pipelines.

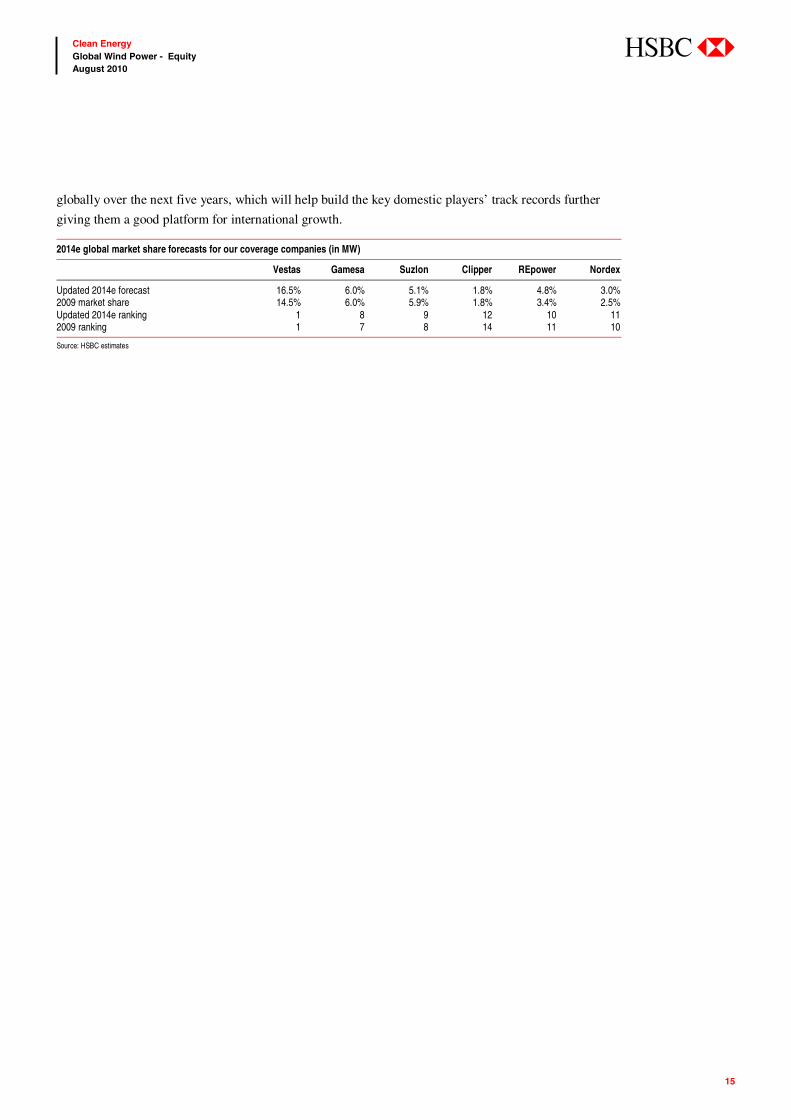

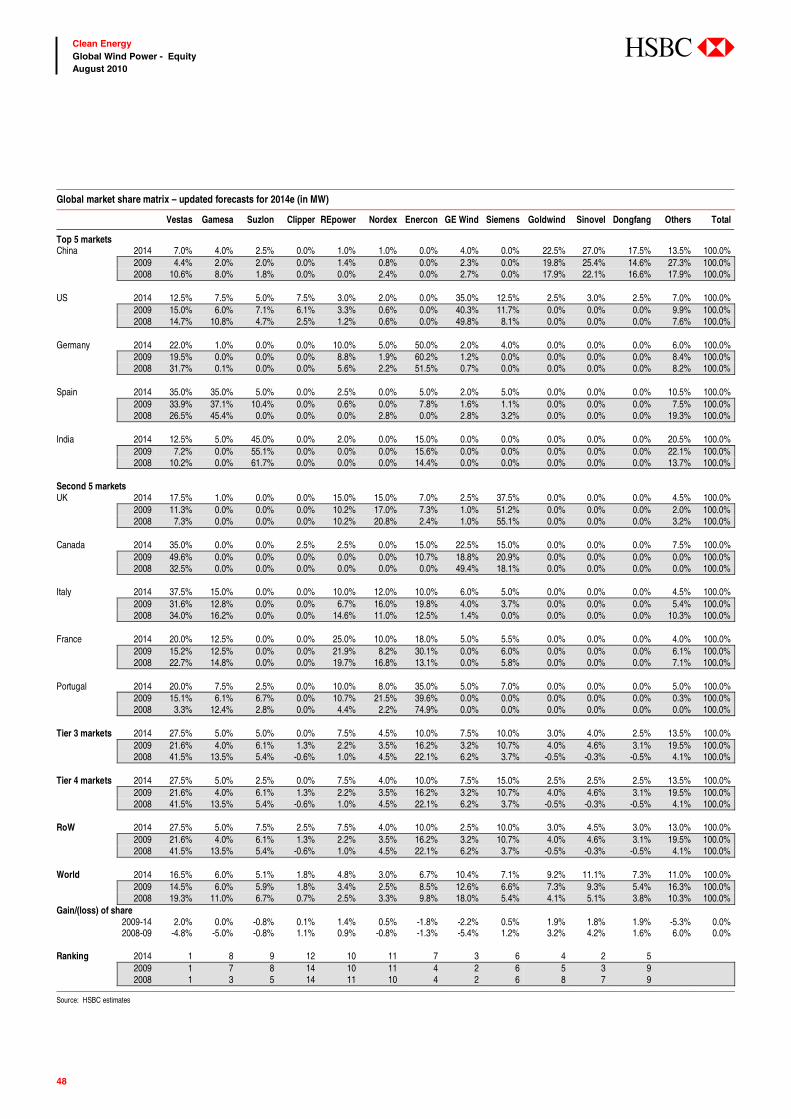

Vestas to remain No.1 wind turbine manufacturer: we believe that Vestas will retain its No.1 position

as the largest wind turbine manufacturer as it regains some of the market share it has lost in recent years

(particularly in China where Vestas’ market share has declined from 23% in 2006 to c4% in 2009) and

also due to its broad global spread including exposure to smaller, high growth markets.

Chinese wind turbine manufacturers are the top gainers: for the first time in 2009, three Chinese

wind turbine manufacturers (Sinovel, Goldwind and Dongfang ) ranked among the top 10, driven by a

strong domestic Chinese market. We forecast the Chinese market will remain the number one market

15

Clean Energy Global Wind Power - Equity August 2010

abc

globally over the next five years, which will help build the key domestic players’ track records further

giving them a good platform for international growth.

2014e global market share forecasts for our coverage companies (in MW)

Vestas Gamesa Suzlon Clipper REpower Nordex

Updated 2014e forecast 16.5% 6.0% 5.1% 1.8% 4.8% 3.0% 2009 market share 14.5% 6.0% 5.9% 1.8% 3.4% 2.5% Updated 2014e ranking 1 8 9 12 10 11 2009 ranking 1 7 8 14 11 10

Source: HSBC estimates

16

Clean Energy Global Wind Power - Equity August 2010

abc

Global wind market analysis 17

US regulatory analysis 25

EU regulatory analysis 32

Supply-side 39

Changing competitive landscape 44

Wind OEMs – order flow 52

Valuation 60

Comparing the wind farm developers 71

Companies section 81

Acciona (ANA SM) 82

Iberdrola Renovables (IBR SM) 89

EDP Renovaveis (EDPR PL) 94

EDF Energies Nouvelles (EEN FP)100

Terna Energy (TENERGY GA) 106

Clipper (CWP LN) 110

Gamesa (GAM SM) 114

Hansen Transmissions (HSN LN) 118

Nordex (NDX1 GR) 122

REpower (RPW GR) 125

Suzlon (SUEL IN) 128

Vestas (VWS DC) 132

Disclosure appendix 137

Disclaimer 140

“We would like to acknowledge the contributions of Ankit

Sharma and Deepak Singhal to this report.”

Contents

17

Clean Energy Global Wind Power - Equity August 2010

abc

Industry forecasts: China the main driver We cut our five year global demand CAGR

estimate to 7.0% from 7.5% previously and our 10-

year industry demand CAGR forecast to 5.5% from

6.7% previously, primarily driven by the following:

Europe: reduced electricity demand resulting in

reduced renewable targets in most key European

markets. We cut our five year demand CAGR

estimate to 5% from 7% previously.

US: reduced electricity demand resulting in

reduced renewable targets, exacerbated by a

weak longer-term regulatory environment.

We cut our five year demand CAGR estimate

to 0% from 7% previously.

Order flow: order flow is picking up but

continues to point towards a weak year in

2010. We cut our 2010 demand growth

forecast to -3.0% from -1.3% previously.

Partially offset by: continued strong growth

in the Chinese markets driven by high

demand for electricity and a willingness on

the part of the Chinese government to be

considered more green, and also pockets of

growth from new emerging markets in areas

such as South America, Eastern Europe,

Canada and Turkey.

In this report, we have undertaken a detailed

analysis of the regulatory environment in the US

and Europe (see “US regulatory analysis” and

“EU regulatory analysis” chapter). We have

performed a top down review of these markets

and derived long-term forecasts out to 2020 based

on renewable targets in each region. We find that

both regions are currently set to exceed their

respective targets (draft target in the US) and thus

we cut our wind forecasts in each region.

China will be the most significant driver of global

growth, in our view. We forecast that it will

Global wind market analysis

We cut our five-year industry demand CAGR forecast to 7.0%

globally from 7.5%

We cut our new installations forecast for the US market by 27%

(15.6GW) over the next five years due reduced electricity demand

and a weak regulatory environment

We cut our forecasts for Europe by 6% (3.9GW) over the next five

years due to reduced electricity demand resulting in reduced

renewable targets

18

Clean Energy Global Wind Power - Equity August 2010

abc

account for 38% of the global market over the

next five years (2010e-14e) and will grow at 8%

pa. The current NDRC target for wind is 150GW

by 2020, but the goal post keeps moving (the

target has been upgraded three times in the last

five years). We forecast cumulative capacity of

241GW by 2020.

We cut our 2010 new installation forecasts to

36.3GW

Following a detailed review of order book data for

the wind turbines manufacturers (see “wind

OEMs – order books” chapter), we cut our global

new installations forecasts for 2010 to 36.3GW,

implying a negative growth rate of 3% (versus

negative1.4% previously), although off of a

record base year in 2009 of 37.5GW. In fact,

excluding China we are now forecasting negative

growth of 13% in 2010, driven by negative

growth of 29% in the US and 14% in Europe.

No growth expected in the US – even with new legislation

We have undertaken a detailed analysis of the

existing state level Renewable Portfolio Standards

(RPSs) available in the US and a potential federal

Renewable Electricity Standards (RESs) (see

chapter on “US regulatory analysis”). Under the

current proposed federal RES, we forecast

average new wind installations of 10GW pa over

the eleven year period to 2020. This is c33%

lower than the 15GW pa (average) we were

previously forecasting over the same period.

US market – new versus old forecasts (MW)

0

2,000

4,000

6,0008,000

10,000

12,00014,000

16,000

2009 2010e 2011e 2012e 2013e 2014eUS - new US - old

Source: MAKE Consulting (for historic data), HSBC estimates

Under these circumstances, we reduce our five

year demand CAGR estimate for the US market to

0% from 7% previously. In terms of new

installations over the five year period 2010-14, we

cut our forecast by 27% from 57.6GW to

42.0GW. This gives the US market a 20% share

of global installations.

The state level RPSs alone are notably worse,

with average demand of just 6GW pa over the

eleven year period to 2020.

Europe – we cut our forecasts in Southern Europe and Germany

We have undertaken a detailed review of EU

20:20:20 targets for seven key EU markets and

their implication for renewable electricity and

wind markets. These seven markets accounted for

more than 80% of wind turbine demand in Europe

in 2009. Based on our analysis, we find that all

Global wind demand forecasts – summary of changes

2010e 2011e 2012e 2013e 2014e Total 2010e-14e

Old forecast 36,963 41,896 45,920 50,094 53,810 228,683 New forecast 36,325 40,275 45950 49,275 52,450 225,275 Difference -638 -621 30 -819 -1,360 -3,408 % increase/(decrease) -1.7% -1.5% 0.1% -1.6% -2.5% -1.5% Explained by: Decrease in US -1,693 -2,496 -2,995 -3,969 -4,460 -15,613 Decrease in Europe -895 -550 -400 -800 -1,275 -3,920 Increase in China 1,000 1,000 1,500 2,000 2,500 8,000 Increase in RoW 950 1,425 1,925 1,950 1,875 8,125 Total -638 -621 30 -819 -1,360 -3,408

Source: HSBC estimates

19

Clean Energy Global Wind Power - Equity August 2010

abc

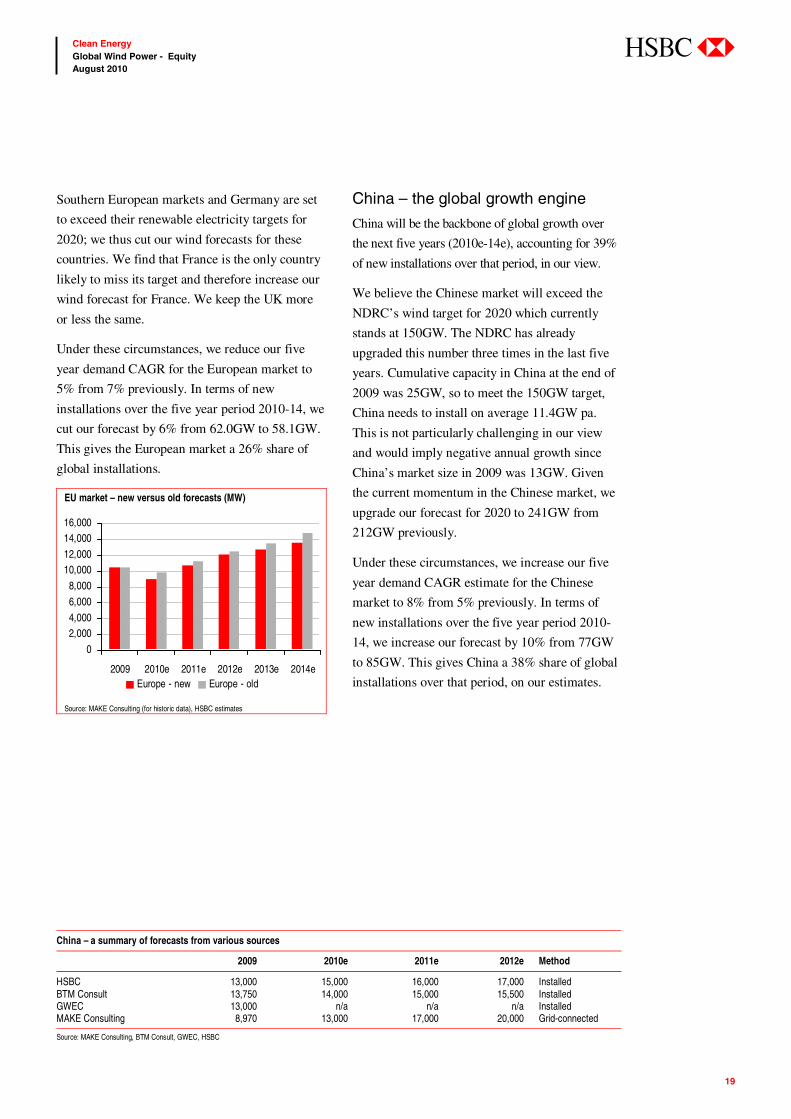

Southern European markets and Germany are set

to exceed their renewable electricity targets for

2020; we thus cut our wind forecasts for these

countries. We find that France is the only country

likely to miss its target and therefore increase our

wind forecast for France. We keep the UK more

or less the same.

Under these circumstances, we reduce our five

year demand CAGR for the European market to

5% from 7% previously. In terms of new

installations over the five year period 2010-14, we

cut our forecast by 6% from 62.0GW to 58.1GW.

This gives the European market a 26% share of

global installations.

EU market – new versus old forecasts (MW)

0

2,0004,000

6,000

8,000

10,00012,000

14,00016,000

2009 2010e 2011e 2012e 2013e 2014eEurope - new Europe - old

Source: MAKE Consulting (for historic data), HSBC estimates

China – the global growth engine

China will be the backbone of global growth over

the next five years (2010e-14e), accounting for 39%

of new installations over that period, in our view.

We believe the Chinese market will exceed the

NDRC’s wind target for 2020 which currently

stands at 150GW. The NDRC has already

upgraded this number three times in the last five

years. Cumulative capacity in China at the end of

2009 was 25GW, so to meet the 150GW target,

China needs to install on average 11.4GW pa.

This is not particularly challenging in our view

and would imply negative annual growth since

China’s market size in 2009 was 13GW. Given

the current momentum in the Chinese market, we

upgrade our forecast for 2020 to 241GW from

212GW previously.

Under these circumstances, we increase our five

year demand CAGR estimate for the Chinese

market to 8% from 5% previously. In terms of

new installations over the five year period 2010-

14, we increase our forecast by 10% from 77GW

to 85GW. This gives China a 38% share of global

installations over that period, on our estimates.

China – a summary of forecasts from various sources

2009 2010e 2011e 2012e Method

HSBC 13,000 15,000 16,000 17,000 Installed BTM Consult 13,750 14,000 15,000 15,500 Installed GWEC 13,000 n/a n/a n/a Installed MAKE Consulting 8,970 13,000 17,000 20,000 Grid-connected

Source: MAKE Consulting, BTM Consult, GWEC, HSBC

20

Clean Energy Global Wind Power - Equity August 2010

abc

Chinese market – new versus old forecasts (MW)

02,0004,0006,0008,000

10,00012,00014,00016,00018,00020,000

2009 2010e 2011e 2012e 2013e 2014eChina - new China - old

Source: MAKE Consulting (for historic data), HSBC estimates

Grid-connection is one of the biggest challenges

One of the biggest challenges in China at the

moment is connecting installed turbines to the

grid; this issue is particularly pronounced in Inner

Mongolia. This has caused a large mismatch

between installed and grid-connected turbines;

depending on whose numbers one looks at, up to a

third of installed turbines in China are not grid-

connected (ie running idle). MAKE Consulting

bases its Chinese market forecasts on grid-

connected turbines, whereas BTM Consult,

GWEC (the Global Wind Energy Council) base

their forecasts on installed turbines. We fall in the

latter camp.

We believe turbines installed (rather than grid-

connected) best represents the market for wind

turbines (ie a turbine sales contract is typically

complete when the turbines are installed, not

necessarily grid-connected), although tallying

turbines installed is more subjective.

We believe that ensuring existing installed

capacity becomes grid-connected will become

more of a focus for wind farm developers in the

coming years, which is one of the reasons for

growth in the Chinese market slowing to a five

year CAGR of 8%, on our forecasts (based on

installed, not grid-connected capacity) compared

to triple digit growth over the last five years. We

note that grid-connected capacity will grow at a

five-year CAGR of 20%, on our forecasts, due to

the closing of the gap between installed and grid-

connected capacity. The other reason being the

fact China is now the world’s largest wind turbine

market thus the base year of 2009 is at a record

high (for any wind market, ever) of 13GW.

Note that our Chinese market assumptions herein

assume considerable investment in grid

infrastructure to enable nearly all wind farms to

become grid-connected by 2014e. This is

particularly an issue in Inner Mongolia.

China – installed versus grid-connected capacity over the period 2010e-14e

2009 2010e 2011e 2012e 2013e 2014e 2015e 5-year CAGR (2009-14e)

Grid-connected capacity

Cumulative 19,223 32,424 47,695 65,158 84,935 107,146 126,412 41% Annual (or new) 8,970 13,201 15,271 17,463 19,776 22,211 19,266 20% % increase/(decrease) 92% 47% 16% 14% 13% 12% -13%

Installed capacity

Cumulative 24,893 39,893 55,893 72,893 90,893 109,893 129,653 35% Annual (or new) 13,000 15,000 16,000 17,000 18,000 19,000 19,760 8% % increase/(decrease) 106% 15% 7% 6% 6% 6% 4%

Grid-connected as % installed capacity

Cumulative 77% 81% 85% 89% 93% 98% 98% Annual (or new) 69% 88% 95% 103% 110% 117% 98%

Source: MAKE Consulting (for historic data), HSBC estimates

21

Clean Energy Global Wind Power - Equity August 2010

abc

Market analysis: where’s the growth coming from? We have ranked 22 wind markets, worldwide,

based on our forecast new installations over the

next five years (2010e-14e) and also forecast

“other Americas”, “other Europe”, “other

Asia/Pacific and RoW. From this pool of markets,

we form three groups:

Growth markets (out of top 10 markets)

Ex-growth markets (out of top 10 markets)

High growth markets (remaining markets).

Top 10 markets: five growth and five ex-growth

We forecast that the top 10 markets will account

for 85% of all new installations over the period.

We identify two distinct groupings within the top

10 markets, five markets with zero or negative

growth over the next five years and five markets,

which are all growing faster than the global

average of 7.0% pa over the same period:

Growing faster than the global market:

India (five year CAGR estimate of 12%), the

UK (five year CAGR estimate of 13%) and

Canada (five year CAGR estimate of 19%),

France (five year CAGR estimate of 11%)

and China (five year CAGR estimate of 8%)

Negative or zero growth: US (five-year

CAGR estimate of 0%), Germany (five year

CAGR estimate of 1%), Spain (five year

CAGR estimate of minus 8%), Italy (five year

CAGR estimate of 0%) and Portugal (five

year CAGR estimate of minus 6%)

Remaining markets: high growth

The remaining 12 markets plus “other Americas”,

“other Europe” and “other Asia/Pacific” and

RoW, we forecast will in aggregate account for

just 19% of new installations over the period

2010e-20e. However, we believe these smaller

markets will provide the strongest growth

opportunity, mainly due to a low base effect due

to their relative immaturity. We forecast a five

year CAGR for these markets combined of 21%.

Top 10 wind markets by forecast installations over 2010-14 in MW (LHS) and forecast five year demand CAGR for each market (RHS)

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

China US Canada Germany India Spain UK France Italy Portugal

-10%

-5%

0%

5%

10%

15%

20%

5 -year global CAGR of 7.0%

Source: HSBC estimates

22

Clean Energy Global Wind Power - Equity August 2010

abc

Implications for the wind turbine manufacturers We have analysed the exposure of the top 10 wind

turbine manufacturers plus Nordex and Clipper to

the three grouping defined above, namely “high

growth”, “growth” and “ex-growth”.

The Chinese manufactures, Sinovel, Goldwind

and Dongfang, currently have the best growth

prospects in our view, on the back of domestic

Chinese market growth. Furthermore they are all

looking to internationalise, particularly into the

US; any new market penetration should add to

their growth profile.

Clipper, GE and Gamesa are the least exposed to

growth markets with 0%, 13% and 25% sales

exposure to growth markets in 2009 respectively.

In the case of Clipper and GE this is due to their

very high exposure to the US market (100% and

85% of sales respectively), and in the case of

Gamesa is due to its high exposure to Spain and

the US (two-thirds of sales). We note that in the

coming years Clipper is looking to expand outside

of the US into growth markets such as Latin

America and Canada.

The remaining manufacturers, including Vestas,

Suzlon, REpower and Nordex, all have exposure

to growth markets in the range of 40-60% of

sales. These are the best positioned of the non-

Chinese players.

Implications for the wind farm developers Exposure to high growth markets not essential…

It is not a prerequisite that the wind farm

developers are exposed to the highest growth

markets. Based on our forecasts, the wind farm

developers will barely grow their annual

installations over the next five years, with the

exception of Iberdrola Renovables, which we

forecast will growth annual installations at 7% pa

over 2010e-14e). Iberdrola Renovables’ higher

growth is due to a suppressed base in 2009 (just

1.4GW versus the 2GW pa targeted by the

company previously). In fact, we forecast that all

wind farm developers except Iberdrola

Renovables will deliver a lower number of

installations in 2010 than in 2009.

Top 10 wind turbine manufacturers plus Nordex and Clipper – sales exposure to growth, ex-growth and high growth (RoW) markets in MW (LHS) and % sales exposure to growth/high growth markets (RHS) in 2009

42%

13%

100%

42%

100%

50%

25%

55%

100%

48%55%

0%0

1,000

2,000

3,000

4,000

5,000

6,000

Vestas GE Wind Sinovel Enercon Goldw ind Siemens Gamesa Suzlon Dongfang REpow er Nordex Clipper

0%

20%

40%

60%

80%

100%

120%

Growth High growth Ex -grow th % exposure to grow th markets

Source: MAKE Consulting, HSBC estimates

23

Clean Energy Global Wind Power - Equity August 2010

abc

Wind farm developers – HSBC new installations forecasts over the period 2009-2014e

0

500

1,000

1,500

2,000

2009a 2010e 2011e 2012e 2013e 2014e

ANA IBR EDPR EDF EN

Source: HSBC estimates

…quality of pipeline much more important

What is more important for the wind farm

developers is the quality of their pipeline, in terms

of project viability, return, and geographical

spread, and also their access to finance. The focus

at the moment is on which developers are exposed

to markets with high regulatory risk such as

Spain, Italy and the US.

From April, investors have been discounting heavily

developers exposed to Spain due to uncertainty over

the tariff system, including the possibility of a

retroactive cut to tariffs. In early July some visibility

was given on the tariff cuts to wind in the form of a

draft Royal Decree, which looks for temporary tariff

(premium) cuts in 2011 and 2012; this is not

particularly unfavourable and importantly adds some

visibility to an unclear situation. Iberdrola

Renovables, EDPR and Acciona all have operating

asset and pipeline exposure to Spain.

2009: wind power a mainstream technology The wind industry had another record year in 2009

with new wind installations of 37.5GW worldwide.

In Europe, wind was the power generation source

of choice in terms of new installations for the

second year running, accounting for 39% (2008:

36%) of all new installations with gas in second

place accounting for 26% of new installations.

Similarly in the US, wind energy accounted for

39% of new installations in 2009, marginally

beaten by gas with 43%.

Who’s number 1, US or China?

According to the Global Wind Energy Council

(GWEC), in 2009, global wind turbine

installations reached 37.5GW, an increase of 38%

y-o-y (2008: 35%). GWEC’s analysis suggests

that China is the leading market with 13GW of

new installations globally accounting for 35% of

new installations globally (13GW). The global

market for wind turbine installations in 2009 was

worth about EUR45bn (~USD60bn) (source:

GWEC). Cumulative total installations globally

reached 157.9GW.

New power capacity installations in the EU in 2009 (Total 26GW) – by technology

New power capacity installations in the US in 2009 (Total c26GW) – by technology

Wind39%

Solar17%

Coal9%

Otherrenewables

5%

Other2%

Nuclear2%

Gas26%

Wind39%

Solar17%

Coal9%

Otherrenewables

5%

Other2%

Nuclear2%

Gas26%

Wind39%

Gas43%

Other5%

Coal13%

Wind39%

Gas43%

Other5%

Coal13%

Source: EWEA, HSBC Source: AWEA, SEIA, SNL, Lawrence Berkeley Laboratory, HSBC

24

Clean Energy Global Wind Power - Equity August 2010

abc

However, according to MAKE consulting, a

leading wind industry consultant, global wind

turbine installations reached c33GW in 2009, up

27% y-o-y. The main growth drivers were China

(up 92% y-o-y) and US (up 16% y-o-y), which

installed c9GW and 10GW of grid-connected

wind turbines in 2009 respectively.

The difference between MAKE and GWEC

numbers can be explained by the difference in

their methodology. MAKE calculates installation

numbers based on completed projects i.e.

mechanically installed and fully commissioned

wind turbines, grid available and connected, either

operating or fully ready to operate, whereas, we

believe GWEC numbers are based on installed

capacity, irrespective of its grid connection status.

The MAKE number thus understates the size of

the wind turbine market, in our view, since we

believe installed capacity is more relevant when

talking about the market for size for wind turbine

manufacturers as a completed wind farm (albeit

not grid connected) represents a completed

contract for a wind turbine manufacturer.

US: a positive surprise

In the US, new installations increased by 19% y-

o-y to c10GW (2008: 8.4GW), bringing the total

installed capacity to 35GW. At the beginning of

2009, it was widely expected that the US market

will be weak due to a lack of adequate project

financing (in particular tax equity in order to fully

utilise the Production Tax Credit (PTC), the

federal level incentive). However, the swift

implementation of ARRA incentives and the

disbursal of treasury grants in the second half of

2009 had a positive impact on the new

installations with c4GW of new installations

achieved in the fourth quarter.

China: stronger than expected

In China, new installations reached 13GW, more

than double their level in 2008 (6.3GW). This

brings total installed capacity to 25GW at the end

of 2009 (2008: 12GW). Wind energy

development was largely unaffected by the lack of

financing which negatively impacted the rest of

the world. It also overtook US as the world’s

largest market for wind turbines in 2009 (on an

installed, not grid-connected, basis).

EU: robust growth

In the EU, new installations increased by 18% y-

o-y to c10.5GW (2008: 8.9GW), driven by robust

new installations in the UK, France and Italy, and

better than expected new installations in the more

mature markets of Spain and Germany. This

brings the total installed capacity in the EU to

76.5GW and makes the EU by far the largest

region from a total installed base perspective, with

48% of the global total installed base.

Electricity generation goes green in the EU

In the EU, wind energy was the no.1 electricity-

generating technology, in terms of new

installations, for the second year in running, with

39% of new installations in 2009 (2008: 36%). In

fact, 61% of new installations during 2009 were

from renewable sources (2008: more than 50%).

Gas was the next most popular electricity

generation source, with 26% of new installations.

25

Clean Energy Global Wind Power - Equity August 2010

abc

Current US regulation is weak The US wind industry recorded a record year of

10 GW in 2009 but was knocked off its top spot

as the world’s largest market (having been no.1

since 2005 – with c25% of the global wind turbine

market over the period 2005-09) for the first time

by China (13GW). The good news stops there.

Compared to this level of new installations, the

current potential regulatory scenarios in the US do

not bode well for wind turbine demand growth

over the next decade or so. We calculate that the

state RPSs alone would support just a 5.7GW pa

(average) wind market until 2020.

A potential federal LCES (assuming 13%

renewable electricity by 2020) would support a

wind market over the same period of nearly 10GW

pa, we calculate. This is the best possibility, in our

view, and implies only flat demand growth over the

period to 2020. We note that there is considerable

uncertainty over the final form of a potential

federal LCES, and there are a number of draft

pieces of legislation before Congress with quite

different proposals. The House of Representatives

have passed a bill (the Waxman-Markey bill) with

federal RES provisions but this still needs to be

reconciled with any such provisions coming out of

the Senate. Our federal LCES scenario adopts the

Lugar version of the federal LCES (see

assumptions below for detail). The Lugar bill is one

of many versions of the legislation in the Senate

right now. The Lugar bill gives ‘clean’ energy

targets which include CCS (Carbon Capture and

Storage) and nuclear installations, rather than just

renewable energy targets (as per the House of

Representatives’ version of the bill), which we

believe are necessary to appease the coal and

nuclear lobby and therefore eventually see the bill

passed in the Senate; it is a good general

representation of most Senate versions of the bill.

The worst case scenario is unlikely to materialise

In what we consider the worst case regulatory

scenario, which would entail no federal LCES,

and a US market based only on those states with

penalty schemes to support their state level RPS

targets, we calculate wind demand in the US of

just 3.8GW pa (average) up to 2020. We believe

this scenario is unlikely, but nevertheless would

be very negative for the Wind OEMs.

US regulatory analysis

We calculate that the state RPSs alone would support only a 5GW

pa (on average) wind market until 2020

We calculate that a federal LCES (assuming 13% renewable

electricity) could support a 10GW pa wind market until 2020

Based on a federal LCES (assuming 13% renewable electricity by

2020), we cut our new installations forecast for the US market by

27% over the next five years (combined)

26

Clean Energy Global Wind Power - Equity August 2010

abc

Implications for the wind turbine manufacturers Flat demand in the US up to 2020 (and that is the

best case of our three regulatory scenarios) will

have a negative impact for most wind turbine

manufacturers in, perhaps, the most competitive

market globally. In our view, GE, Mitsubishi and

Clipper will suffer more than most players since

these companies all have more than 85% sales

exposure to the US market. Vestas, Gamesa and

Suzlon all have around 25% of their sales exposed

to the US.

The US – the most exposed wind turbine manufacturers

__ Sales exposure (MW) _ __ Market share (MW) _ Average

2007-092009 Average

2007-09 2009

GE 84% 85% 45% 40% Siemens 53% 47% 12% 12% Clipper 100% 92% 3% 6% Mitsubishi 93% 100% 7% 8% Vestas 25% 27% 16% 15% Gamesa 24% 26% 9% 6% Suzlon 23% 32% 5% 7%

Source: MAKE Consulting, HSBC estimates

REpower and Nordex both have under 15% sales

exposure to the US market.

Competition fierce – Asian players trying to penetrate

In our view, the US market is already the most

competitive market globally (China is the second

most competitive). Many European turbine

manufacturers have already set up manufacturing

US regulation - summary of current regulatory scenarios and implications for the wind market

Federal RES (potential) State RPS (all states with an RPS) (ii)

State RPS (penalty scheme only)

No of states 50 37 16

Renewable electricity as % total electricity in 2020 (un-diluted) 20.0% 11.3% 5.7% Dilution to base due to exemptions for large hydro and MSW (ii) 1.5% 15% 10% Clean electricity as % total electricity in 2020 (diluted) 18.5% 9.7% 5.4% Energy efficiency saving (smart grid etc) 3.7% Clean electricity as % total electricity in 2020 (diluted) 14.8% 9.7% 5.4% Dilution due non-renewable but ‘clean’ energy sources 1.9% Renewable electricity as % total electricity in 2020 (diluted) 12.9% 9.7% 5.4% Wind as % renewable electricity 65% 54% 57% Wind as % total electricity in 2020 8.4% 5.4% 3.1% 2020e wind produced electricity (TWh) (i) 370 232 136 2020e wind capacity (GW) (i) 141 88 52 2009 wind capacity (GW) (i) 35 25 10 New wind installations 2010-2020 (GW)* 106 63 42 Average wind installations pa (GW) 9.6 5.7 3.8 2020e cumulative installations (all states) 141 98 87

Note: (i) Summed over states in question only; (ii) Includes states with an informal target as well as a formal RPS; (iii) dilution is due to an exemption for small power producers for RPS schemes Source: DoE website, IEA, EIA, HSBC estimates

27

Clean Energy Global Wind Power - Equity August 2010

abc

facilities in the US. Despite the flat demand

growth we forecast for the US market, we believe

key Chinese players, such as Goldwind, Sinovel,

A1 Power, and Ming Yang, will continue to

penetrate the US market. We have already seen an

Indian manufacturer, Suzlon, enjoy some success

in penetrating the US market over the last couple

of years, with 704MW of US sales in 2010e (c7%

market share).

In addition, we expect a further wave of penetration

from Korean manufacturers such as Samsung,

Hyundai and Daewoo. Furthermore, these are all

already trusted brands in the Western world and

therefore could cause more of a threat to Western

turbine manufacturers than the Chinese

manufacturers, which are less well known.

The emergence of Asian players trying to

penetrate the US market is likely to put

downwards pressure on pricing as they under cut

on price in order to win market share.

Investment in US manufacturing capacity

Many European wind turbine manufacturers,

including Vestas, Gamesa, and Nordex, and also

Suzlon, have invested in the US in recent years as

improved regulatory visibility (ie a more stable

Production Tax Credit (“PTC”)) allowed them to

commit capital to the region. However, Gamesa

and Suzlon have had to make redundancies at

their US plants, which are currently significantly

under-utilised. Vestas has made no redundancies

at its US plants.

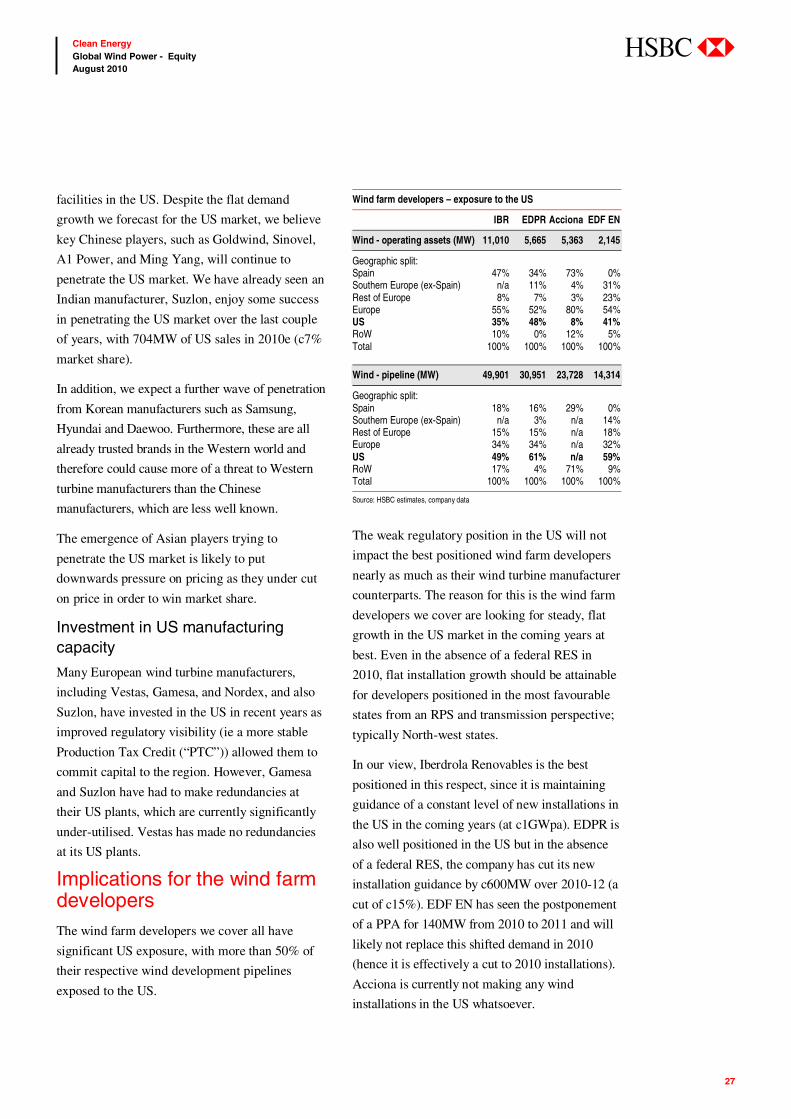

Implications for the wind farm developers The wind farm developers we cover all have

significant US exposure, with more than 50% of

their respective wind development pipelines

exposed to the US.

Wind farm developers – exposure to the US

IBR EDPR Acciona EDF EN

Wind - operating assets (MW) 11,010 5,665 5,363 2,145

Geographic split: Spain 47% 34% 73% 0% Southern Europe (ex-Spain) n/a 11% 4% 31% Rest of Europe 8% 7% 3% 23% Europe 55% 52% 80% 54% US 35% 48% 8% 41% RoW 10% 0% 12% 5% Total 100% 100% 100% 100%

Wind - pipeline (MW) 49,901 30,951 23,728 14,314

Geographic split: Spain 18% 16% 29% 0% Southern Europe (ex-Spain) n/a 3% n/a 14% Rest of Europe 15% 15% n/a 18% Europe 34% 34% n/a 32% US 49% 61% n/a 59% RoW 17% 4% 71% 9% Total 100% 100% 100% 100%

Source: HSBC estimates, company data

The weak regulatory position in the US will not

impact the best positioned wind farm developers

nearly as much as their wind turbine manufacturer

counterparts. The reason for this is the wind farm

developers we cover are looking for steady, flat

growth in the US market in the coming years at

best. Even in the absence of a federal RES in

2010, flat installation growth should be attainable

for developers positioned in the most favourable

states from an RPS and transmission perspective;

typically North-west states.

In our view, Iberdrola Renovables is the best

positioned in this respect, since it is maintaining

guidance of a constant level of new installations in

the US in the coming years (at c1GWpa). EDPR is

also well positioned in the US but in the absence

of a federal RES, the company has cut its new

installation guidance by c600MW over 2010-12 (a

cut of c15%). EDF EN has seen the postponement

of a PPA for 140MW from 2010 to 2011 and will

likely not replace this shifted demand in 2010

(hence it is effectively a cut to 2010 installations).

Acciona is currently not making any wind

installations in the US whatsoever.

28

Clean Energy Global Wind Power - Equity August 2010

abc

Modelling assumptions State RPS scenario

In the US, there are 31 states with a formal

Renewable Portfolio Standard (“RPS”) and a

further 6 states with an informal target. Of these

states, only 16 have a formal penalty system to

deal with non-compliance. The level of renewable

electricity targeted under each RPS varies by

state, typically ranging from 15% of total

electricity generated to 25% (although there are

some RPSs outside of this range), as does the

timeframe for compliance, which typically ranges

from 2015-2025. However, in order to perform a

consistent analysis, we have derived effective

RPS targets for each state as at 2020. For states

with an RPS target with a timeframe longer than

2020, we have used linear interpolation between

the level of renewable in that state and the RPS

target, and for states with a timeframe shorter than

2020, we have simply adopted the target at the

earlier date and assumed that this level is

maintained. The table below sets out the states

which have an RPS, the RPS target, timeframe,

and some other assumptions we have adopted.

Summary of assumptions and outputs for US states with an RPS

____________2020 RES-E target ____________ State REN

target (%) Achieved by end of

Penalty system

2020 target (adjusted)

Exemption USED

2020 target (adjusted)

2009 % RES-E

*Electricity demand in 2020

All states

Penalty only

After dilution (all states)

After dilution (penalty only)