page

1

briefing paper

The Changing Retailing Environment

David Hurst and Andrew Black

International Economics | October 2011 | IE WIT BP 2011/05

Summary points

zz By 2025, most retail investment will be in the developing world. Consumer spending will be higher than in the developed world and modern retailing formats will expand to meet the demand for branded, added-value and luxury goods and services. Investment in modern retailing capacity will induce consumers to move away from more traditional formats and will increase consumption.

zz In the developed world, relatively less retail space will be devoted to food and grocery and much more to health, beauty, recreation, restaurants and financial services.

zz European and US retailers are becoming increasingly international as their home markets become saturated and as legislation in developing markets is relaxed. But international retailers will have to reflect local needs and a significant core of local retail business will remain.

zz The internet will play an increasingly important part in retailing as producers sell directly to consumers, although food and grocery will be less affected. Multi-channel shopping will become more common, combining both internet and traditional shopping approaches.

zz The rapid global growth in the number of elderly people is likely to lead to a drop in the consumption of some types of retail goods and further changes in shopping formats to adapt to their needs.

www.chathamhouse.org

The World’s Industrial Transformation Series

www.chathamhouse.org

page

2

The Changing Retailing Environment

IntroductionShopping is one of the oldest features of society, devel-oping from exchange of goods, then open markets, to shops as more permanent fixtures that facilitate the exchange of goods.

There are three basic types of retailing: ‘hardline’ goods such as electrical appliances and furniture, ‘softline’ goods such as clothing, soft furnishings and fabrics; and finally food/grocery products. This paper considers all forms of retailing, including services and fast-moving consumer goods (FMCG) and grocery. These include many different retailing formats. ‘Informal trade’ and ‘direct selling’ cover street vendors, door-to-door sales and unregulated street markets. ‘Traditional trade’ covers open market stalls, travelling fairs, bazaars, kiosks and counter service. ‘Modern trade’ includes self-service, large department stores, hyper- and supermarkets, discount stores, ware-houses and speciality ‘category killer’ stores.

Retail locations may be divided into ‘destination’ and ‘convenience’ venues. Destination venues include high streets, shopping malls, smaller specialist shops, street markets and car-boot sales. They offer consumers economies of scale and scope and, when enclosed, air-conditioned comfort. ‘Convenience’ venues offer consumers easier access but a more restricted range and frequently higher-priced goods.

The fundamentals of retailing have changed very little over time: a visit to Pompeii shows many shops there are recognizably similar to small shops today. However, a major difference today is the increased scale and efficiency of operations due to the use of the internet, computerized payments systems and mobile communications which are changing the nature of the retail experience and leading to a further step change in the industry.1 They have even created the completely new form of e-shopping.

Recent trends in retailing Twenty-five years ago many retail experts predicted that the world would follow US retailing trends such as large shopping malls, vast car parks and extensive retail units. Today, many argue that the United States is somewhat atypical. Although retail parks on the edge of towns continue to appear in many regions, the future may reflect the experience of other rich countries, such as Japan, where space is at a premium and the advantage goes to smaller stores and complexes that are nearer their customers. The case for a steady convergence towards ever-larger destination venues, hypermarkets and shop-ping malls is not proven.

The development of large-scale retail formats is strongly linked to the growth in car ownership. A car enables more goods to be purchased on shopping trips and allows customers to shop over a larger area. This trend will continue in emerging markets; increasing levels of car ownership are already facilitating the growth of hyper- and supermarkets in China and India.

In industrialized countries, by contrast, high fuel prices, congestion and parking charges are reducing the relative attractiveness of using cars for shopping but there is a fine balance between the cost of shopping ‘in town’ and ‘out of town’. There are signs that out-of-town shopping centres may be less viable.2 This is being countered by attracting an increased range of retail outlets under one roof. Improved public transport will be a key determinant as to which of these models succeeds.

1 While it is true that postal catalogues existed in the past, ‘distance’ buying through the internet is now much more widespread, and possible for a much

broader range of goods than previously.

2 A trend already observable in the United States, where many out-of-town shopping malls have closed owing to lack of customers.

‘ Today the increased scale and efficiency of operations due to the use of the internet, computerized payments systems and mobile communications are changing the nature of the retail experience and leading to a further step change in the industry ’

www.chathamhouse.org

page

3

The Changing Retailing Environment

Rising incomes and widening income differentials have increased the number of people who can afford conspicuous consumption and led to an explosion of luxury designer and ‘super designer’ brands and retail destinations around the world. This has resulted in some fragmentation of specialist retailing. These smaller retail units have been aided by the internet, which allows individual designers to access a global market at minimal cost.

At the other end of the income scale, the poorest cannot afford cars or even motorbikes, have limited storage facilities at home and spend relatively little. They will continue to be served through ‘informal trade’ and smaller ‘traditional trade’ formats offering a smaller assort-ment of cheaper lines, often at the expense of quality.3 Paradoxically poorer consumers are more likely to buy branded versions of critical items such as baby milk, since they can less afford to make purchasing mistakes than more affluent consumers.

Retailers made their customers ‘work harder’ for their shopping during the second half of the 20th century. Customers were persuaded to opt for lower service levels at self-service stores and supermarkets for prod-ucts sold at more transparent and fixed prices. Elements of personal service, such as door-to-door delivery, packing and selecting goods, were eliminated. This allowed retailers to turn over larger volumes and achieve scale economies while providing consumers with a wider range of products at cheaper prices but at lower service levels.

Today some of these ‘old-fashioned’ retail services are reappearing. For customers who are money rich but time poor, retail delivery and personal shopper services are making a comeback, as retailers scramble to increase market share in static or declining markets. Consumers shop, while the hard work of carrying the goods is taken care of by the retailer. The very perception of ‘shops’ is also changing towards showrooms and ‘experience’ centres, rather than places where the goods are actually bought.

Factors driving retailing trendsThe main factors driving change in the global retail industry are:

zz income and spending power;zz demographics – age cohorts, household size, urbanization;zz raw material, energy and transport costs;zz planning and land use; zz the internet and mobile communication.

Income and spending power – an initial view

Individual and household incomes strongly determine the type and quantity of goods and services consumed, and hence the shape of retailing. The future will be greatly influenced by the contrasting strong growth in retail turnover in emerging markets and stagnating or falling retail turnover in developed markets.

On current estimates, total consumer spending power4 in the developing world will be substantially more by 2025 than in the developed world and the centre of gravity for consumption will move away from the West. By 2025 consumers in Central Asia and China will be spending $15 trillion more, at purchasing power parity (PPP) rates, than in 2010. Although the average spending power per head in developing and emerging markets (henceforth referred to as D&E markets), currently about 25% of that in the West, will remain lower for some time, there will be increasing and significant numbers of people in the devel-oping world able to afford Western lifestyles (see Figure 1).

The world population can be divided into broad income bands, reflecting stages in consumption behaviour combined with an improving quality of retail offering. This is shown in Table 1.

As incomes rise, the types of goods and the retail formats where they are typically purchased change. ‘Modern trade’ can be expected to develop at GDP/head over $5,000 (at PPP rates). At the top of the scale, as the number of rich people has grown, a range of quality positionings beyond prestige – designer, super-designer, couturier – has opened up, boosting the number of luxury retail outlets.

3 Private label is not always equated with low quality. Some retailers’ ‘brands’ replace manufacturers’ brands as an indication of quality.

4 As measured by private consumer expenditure at purchasing power parity exchange (PPP) rates.

www.chathamhouse.org

page

4

The Changing Retailing Environment

Figure 1 shows how the number of people in each group is distributed in the developed and developing worlds. In the foreseeable future there will be at least as many devel-oping-world consumers in the same higher income bands as there currently are in the developed world.

In 2010, 30% of the people in the world (around two billion) bought ‘basic’ or ‘economy’ products, mostly through the ‘traditional trade’. A further one billion people were still living on ‘a dollar a day’ or less, and not participating regularly in the organized market economy. By 2025, demand will have shifted. The majority of

people in the developing world are likely to be shop-ping in ‘modern trade’, and able to afford branded and added-value packaged goods. If economic growth in the D&E markets continues at around 6%, approximately one billion more customers will be shopping in ‘modern trade’ outlets by 2020.

These income bands are also associated with differences in patterns of retail spending shown in Table 2. Rising per capita income is associated with faster increases in the consumption of health, recreation, housing and other services.

Table 1: Consumer incomes, FMCG types and retail formats: indicative view

Income rangeGDP per head at PPP rates ($) Characteristic FMCG product types Characteristic retailing type

0 –1,000 Subsistence: not regularly participating in the organized economy Informal trade, open markets and street hawkers, with some barter

1,000–2,500 Basic goods: hard soap, bouillon cubes Open markets, transition to ‘traditional’ stores

2,500–5,000 Economy and affordable products: packet margarine and toilet soap Counter service in small general and specialist stores

5,000–10,000 Branded ‘commodity’ products: fabric washing powders Developing self-service; emergence of supermarkets and ‘modern trade’

10,000–20,000 Added-value products: fabric conditioners, low-fat margarines Hypermarkets; extensive multiple stores

20,000–40,000 ‘Luxury’ products: dishwashers, expensive ice cream Shopping malls, shared shopping space, growth of hard discount as mass retailers go for quality, ‘branded’ private labels

40,000+ ‘Prestige’ and ‘designer’ products Retail fragmentation, with specialist shops, international luxury retail outlets, shift back to convenience

Figure 1: World population by income, 2010

Source: TLE Strategy Globegro© 2011

1,800

1,600

1,400

1,200

1,000

800

600

400

200

0

Mill

ions

<1,000 2,500 5,000 10,000 20,000 40,000 >40,000

Income US$ PPP

Subsistence

Basic

Economy

Standard

Added valueLuxury

Prestige

Developing

Developed

Source: TLE Characteristic Consumption Steps c2010

www.chathamhouse.org

page

5

The Changing Retailing Environment

Customers spend more absolutely as their incomes rise, but the amount spent tends to fall as a proportion of their incomes. This is particularly true for the consumption of food and groceries. The composition of the High Street in more prosperous regions of both the developed and developing world will change to reflect this, with a smaller proportion of floor space devoted to food, and much more to health, beauty, recreation, restaurants and financial services.

Above incomes of around $25,000 per head, the abso-lute amount spent per head on food and grocery starts to plateau. Grocery retailing competition becomes more intense and focuses primarily on price, and then on quality. Retail ‘branding’ becomes an increasingly important means of emphasizing product differentiation. ‘Zero-sum’

competition leads to further concentration in parts of the retail industry. Retailers’ own brands also prosper, as they appropriate the margin branded manufacturers use for advertising to add to product quality, or ‘give’ the money back to the consumer through lower prices.

Income and spending power – changes in the global

balance

Figure 2 shows that the combined share of North America and Europe in global retailing in 2008 was about 53%. In 2014 this share is expected to fall to just over 43% while Asia-Pacific is expected to account for nearly 40%. This is already influencing investment decisions by local and international retailers.

Table 2: Expenditure breakdown by income level (as % of total expenditure), 2005: Global Averages

GDP/head ($PPP)Food, beverages,

tobaccoClothing and household Health

Transport and communication

Recreation, education and

restaurants

Other (inc. financial

services)

500 64 14 3 10 7 3

1,000 59 14 3 11 9 4

2,500 52 13 4 15 11 5

5,000 38 14 7 18 16 7

10,000 37 11 8 21 17 7

20,000 19 12 11 20 28 11

40,000 13 10 14 19 27 18

Sources: TLE Consumption Curves/ http://data.worldbank.org/data-catalog/international-comparison-program/OECD Family Expenditure 2005

Figure 2: Geographical changes in consumer spending

Source: TNS

Retail sales shares 2008 Retail sales shares 2014

Other, 7.5%

Latin America, 7.6%

AsiaPacific,30.8%

N. America,32.4%

W. Europe,20.6%

Latin America, 7.2%

AsiaPacific,38.6%

N. America,26.6%

W. Europe,16.8%

MENA, 1.1%

Other, 9.4%

MENA, 1.4%

www.chathamhouse.org

page

6

The Changing Retailing Environment

In developed countries, consumption, previously an engine of growth, may rise more slowly than GDP as households rebalance their spending.5 In some developing economies, the opposite can happen. In China, consumption, currently only 40% of GDP, and retailing value added will rise faster than GDP in the short run, but in the longer term retailing’s share of GDP will decline in China as elsewhere. Rural emigration to the cities combined with higher urban consumption will make urban retailing very attractive.6

Changes in the relative size of the retailing industry

The absolute size of the retail industry grows as economies grow, but the relative size of retailing, as measured by its share of value added, falls. Figure 3 shows per capita GDP levels in 1992 and 2008 in three main group-ings: the Organization for Economic Co-operation and Development (OECD), the BRICs (Brazil, Russia, India and China) and the developing world. The solid line shows value added by the retail sector as a percentage of GDP, supporting the thesis that the richer the region, the smaller the relative size of retailing. This is due to the greater scale efficiencies in centralized supply and delivery

chains in richer countries. In the developing world there will be huge efficiency gains as incomes rise.

However, in some countries the transition to more economically efficient retail systems will be held back by concerns about employment. India, Japan and Italy, for example, favour smaller, more labour-intensive, and sometimes ‘traditional’ retail systems, whereas in Brazil much of urban retail system is already very similar to that of most of the West. There will be different patterns of retail development in different parts of the world.

Demographics: age cohorts, household size and

urbanization

A quarter of a century ago, the primary consumer unit was the nuclear family and women did most of the shopping. Today the consumer profile is more diverse, with smaller household sizes, more single-parent, single-person and elderly households. Then, the ‘Baby Boomer’ generation was entering its peak consumption years. In 2025 the Millennial and Generation ‘Y’ groups will determine consumption patterns.7 A quarter of a century ago, only 41% of the world population was urban. By 2035 the figure could reach 61%.8

5 This trend is reinforced by the current difficulties in the market for consumer loans and general levels of consumer debt.

6 Rural developing market retail trends are dealt with below.

7 For the purposes of this report, Baby Boomers are defined as those born between 1945 and 1965; Generation X from 1966 to 1980; Generation Y from 1981

to 1995, and the Millennials from 1996 to the present.

8 See Globegro©2010 and 2011 projections based on FAO Statistical Yearbooks.

Figure 3: Retail industry share of value added

falls as GDP per capita rises

Sources: UN Population Statistics (2009) & UN National Accounts (2010)

Figure 4: Relative levels of consumer income by

age band and education level

Source: Fernández-Villaverde and Krueger (2004)

45,000

40,000

35,000

30,000

25,000

20,000

15,000

10,000

5,000

0OECD BRIC Developing

US$

14

12

10

8

6

4

2

0

%

GDP per cap pa US$ 1992

GDP per cap pa US$ 2008

GDP CAGR 2008/1992

45,000

40,000

35,000

30,000

25,000

20,000

15,000

10,000

5,000

0OECD BRIC Developing

GD

P p

er c

apita

17.0

15.5

15.0

14.5

14.0

13.5

13.0

12.5

GDP per cap pa US$ 1992

GDP per cap pa US$ 2008

Average retail value added %

<0=&=4>&/?8&8?&&@AB&!CC"&

<0=&=4>&/?8&@AB&8?&"((D&

E54>?;4&24F?96&G?6H4&EII&%&

16.0

16.5

17.5

Average retail value added %

1.6

1.5

1.4

1.3

1.2

1.1

1.0

0.9

0.7

0.6

0.8

20 30 40 50 60 70 80 90Age

High educationBenchmarkLow education

Nor

mal

con

sum

ptio

n =

1.0

www.chathamhouse.org

page

7

The Changing Retailing Environment

The rapid rise in the number of elderly households will have a major impact over the next 20 years. As people age, their incomes fall and they spend a smaller share of their income on transport, clothing, furnishings, electronic appliances and restaurants, but much more on healthcare. The elderly require proportionately more convenience shops, small pack sizes, ease of access, and fewer bulk shopping trips.

Age, education and income are closely associated, as can be seen in Figure 4. People with higher levels of education have a much more pronounced rise in income up to age 50 and also a much sharper fall as they age.

The age structures of different parts of the world have a big impact on income (and consumption). Much of the developed world is ageing fast whereas the rest of the world is still facing the growth of middle-aged cohorts. Variations in generational spending patterns in Western countries are shown in Figure 5.

‘Baby Boomers’ spend the most in virtually all the categories shown. Living standards of younger genera-tions are falling owing to significant increases in the costs of housing, travel and education.9 If this trend becomes more generalized, the level of consumption for many retail

goods in West may show secular declines, unless offset by major increases in income, currently seen as unlikely.

Figure 6 shows shifts in different age cohorts of the population in developed countries over time. The situa-tion has changed greatly since the 1950s and 1960s. In the last decade there has been virtually no population growth in the younger age cohorts, and the population in much of the developed world is expected to shrink.

9 See Paulin (2008).

Figure 5: Indexed consumption levels

Sources: Hale (2010), Nielsen & TLE Calculations

350

300

250

200

150

100

50

0

Bab

y B

oom

ers

= 1

00

Generation Y Generation X Baby Boomers War generation

Baby food

Carbonated beverages

Cereal

Detergents

Hair care

Ice cream

Pet food

Vitamins

Wine

Figure 6: Population growth in developed countries,

by age band

Source: UN Population Statistics (2009)

60

50

40

30

20

10

0

%

50/60 60/70 70/80 80/90 90/00 00/10

Time by decade

Under 20s

20–35 yrs

35–50 yrs

50–70 yrs

70 yrs

80+

60

40

30

20

10

-10

-20

%

50/60 60/70 70/80 80/90 90/00 00/10Time by decade

Under 20s

20–35 yrs

35–50 yrs

50–70 yrs

70 yrs

80+ 0

50

www.chathamhouse.org

page

8

The Changing Retailing Environment

Contrast this with the situation in emerging markets, shown in Figure 7. Here population growth in all age cohorts has been rapid, including in the last decade. Two broad trends are observable: first the slackening of growth in the ‘Under 20s’ group, and secondly the rapid growth in the elderly population. In fact, in both developed and emerging markets, the rise of the elderly consumer is one of the most important changes facing retailing.

Closer examination of emerging economies shows there are important differences between rural and urban demo-graphics. Rural areas experience a flow of people in their prime working ages (20s to 50s) to the cities in search of a better standard of living, boosting the size of these age cohorts in cities disproportionately.

Rural areas in emerging markets will see a depletion of the middle-aged, and some increase in the elderly, as well as in the very young, as working parents leave offspring to be looked after by grandparents and other members of extended families.

On current trends, retail outlets in rural areas in both the developed and emerging worlds will be increasingly uneco-nomic. Out-of-town shopping centres offer better value for money and draw away customers who have motor vehicles, and urban migration reduces the population base.

Household sizes are continuing to fall, in terms of both space and numbers per household, with the result that the volume of products sold per shopping trip will also decline. While the nuclear family will remain the most important retail buying ‘unit’, its share of total households, which has fallen in recent years, is likely to stabilize at under 70%.10

As spending power grows, D&E market retailing struc-tures are likely to emulate those of developed countries. The extent of this will depend on the rate of income changes, infrastructure investment, shifts in consumption style, possibly influenced by adoption of Western habits, and car ownership. The higher these are, the more likely it is that D&E market retailing will follow the West; the lower they are, the more they will come to resemble Japan or Singapore.

Raw material, transport and energy costs

Western living standards have been supported since the Second World War by relatively cheap energy, food and industrial raw materials. This period may have ended with the 2008 financial crisis. Figure 8 shows recent develop-ments in global energy and oil prices.

The wide selection of goods on sale in developed-world shops owed much to low energy and transport

10 See PwC (2007), p. 5.

Figure 7: Population growth in emerging markets,

by age band

Source: UN Population Statistics (2009)

60

50

40

30

20

10

0

%

50/60 60/70 70/80 80/90 90/00 00/10

Time by decade

Under 20s

20–35 yrs

35–50 yrs

50–70 yrs

70 yrs

80+

Figure 8: Energy commodity prices recover after

2008 financial crisis

Sources: IMF (2011), primary energy commodity prices

160

140

120

100

80

60

40

20

0

Feb 0

1

Aug 0

1

Feb 0

2

Aug 0

2

Feb 0

3

Aug 0

3

Feb 0

4

Aug 0

4

Feb 0

5

Aug 0

5

Feb 0

6

Aug 0

6

Feb 0

7

Aug 0

7

Feb 0

8

Aug 0

8

Feb 0

9

Aug 0

9

Feb 1

0

Aug 1

0

Other energyOilUS$

www.chathamhouse.org

page

9

The Changing Retailing Environment

costs, which made it economic to transport goods over long distances. Higher energy prices will improve the economics of locally produce over imported goods, and will reduce the advantage of long, complex supply chains, to the possible detriment of Chinese producers.

Under ‘normal’ circumstances, a large decline in commodity demand from the West after 2008 would have been sufficient to lower global commodity prices. However, continuing demand from the developing world, particularly China, has pushed up commodity prices and, competitive conditions notwithstanding, many of these higher costs are being passed on to consumers, resulting in higher inflation.

Nominal personal incomes in Western countries have been fairly stable recently so rising food, materials and energy prices have constrained living standards. Higher food and commodity prices will also reduce, or slow down, the rise in emerging market living standards. Developing countries will be faced with real policy dilemmas about the extent to which they continue to subsidize key food and energy products, and the degree to which they expose their population to world prices.11 This is likely to affect both the structure of retailing as well as the speed of change.

Planning and land use

The supply of retail sites is greatly influenced by the price and availability of land. In less densely populated countries, new retail developments can be extensive and located on the fringes of cities where motorized transport is easier. This can lead to a ‘hollowing out’ of cities as people go out of town to shop. Where land is scarcer and more expensive, this is less feasible.

It is frequently asserted that city shopping areas are becoming increasingly similar, as high local property prices and taxes drive out smaller shopkeepers, leaving space free for larger, better capitalized shopping chains. More affluent neighbourhoods frequently maintain more

varied shopping environments, whereas poorer areas experience local shop closures, forcing local inhabitants to travel further to meet their shopping requirements. This already complex situation is made more difficult through the impact of the internet.

Different types of government have often emphasized particular types of retailing. Centrally planned economies had under-developed retail industries, and a single town might have had just one supermarket acting as a goods collection/distribution point. Other countries, such as India, Italy and Japan, have important vested interests that are keen to maintain a pattern of small shops. Regulations are designed to make it difficult for larger stores and chains to become established, and existing retailers can ‘tweak’ local planning rules to discourage unwelcome low-cost competition.12

As modern retail formats become more wide-spread in emerging markets, so retail markets will become more efficient and some prices could even fall; this will in turn encourage higher consumption. Moreover, just as the development process leads to a shift of employment from agriculture to industry and services, it will also lead to a shift of employment out of retailing as less efficient formats give way to more efficient ones.

11 Energy subsidies, for instance, vary widely across the world. In Iran around one-third of the government budget is spent on energy subsidies. These vary from

6% in Russia, 3.4% in Indonesia (2005), 1.8% in India, and 0.4% of GDP in China. Globally fuel subsidies were estimated at US$557 billion in 2008.

See also IEA (2010), p. 29 and IEA (2006), p. 281.

12 Discounters such as Aldi and Lidl have found it difficult to get good sites in the United Kingdom, since the incumbent grocers buy them up and keep them in

their own large land banks.

‘As modern retail formats become more widespread in emerging markets, so retail markets will become more efficient and some prices could even fall; this will in turn encourage higher consumption ’

www.chathamhouse.org

page

10

The Changing Retailing Environment

The internet and mobile communications

The impact of the internet on retailing is likely to be profound, and in some areas conventional retail activity may be entirely replaced. Manufacturers may find it easier to reach customers directly, use the banking or alternative payment systems and deliver goods directly via postal and parcel delivery services. If this becomes generalized, certain types of retailers could become ‘disintermediated’. This means that purchasing decisions are made either by consumers directly with manufac-turers, or with intermediaries other than retail outlets (e.g. Amazon). In this retailing model, the importance of retail branding and the availability of goods are critical to success.

Figure 9 provides a view on the growth in internet users by region. While there is still healthy growth in North America and Europe, spectacular growth is occurring in the Middle East, Africa and the Asia-Pacific region. These regions will catch up with the West by adopting their best practices, which will leave room for their own local adaptations.

Not all areas of retailing will be equally affected by the internet. There is a clear difference between the food and grocery trade and other forms of retailing. Customers still

prefer to do their food shopping themselves. While great efforts have been made to improve shopping by using ‘pickers’, internet shopping has its own problems – notably in ensuring the products are delivered to the right person at the right time. Bulky materials cannot be put into post boxes, and failed deliveries cause logistical problems, similar to those associated with the loss of airline luggage.

If food and grocery shopping are proving resistant to the internet, the same cannot be said for electrical and electronic goods. Already over one-third of sales of these goods is over the internet.13 Customers can find what they want (assuming they know what they are looking for) and often at prices substantially lower than on the high street.

Many grocers are expanding their product range by selling a higher proportion of non-food and non-grocery products. This brings them into direct competition with internet suppliers.14 While retailers may develop their own internet services, they may struggle to retain as much control of the value chain in the future.

Age-related differences in the use of online purchasing may be overstated. While the young may be more eager internet users generally, Baby Boomers and Generation X’ers buy more online. Customers are

13 See Deloitte (2011) for more details.

14 Profit margins on non-food categories at Tesco are reputedly lower than for food items.

Figure 9: Regional growth in internet users

Sources: Forrester Research and Internetworldstats.com, June 2010

MENA and Africa

Asia-Pacific

South America

Total

Europe

North America

0 5 10 15 20 25 30 35%

www.chathamhouse.org

page

11

The Changing Retailing Environment

becoming increasingly ‘multi-channel’ – they may initially find out about a product through some form of media, investigate further over the internet, go to a shop to see an example, and then revert to the internet to make the purchase. Customers following this kind of pattern tend to buy the most, whereas those who only visit shops tend to buy the least – a conclusion that will worry the retail trade.

We will also see shifts in the way information is organ-ized. A top-down ‘brand’ strategy – information about products and prices – came largely from the suppliers (manufacturers and retailers). Social networking sites, peer group reviews and product comparison sites make it easier for customers to form their own judgments about the merits of products, independently from the claims made by advertisers. They will also be able to buy outside designated sales ‘territories’.

Payment systems too have changed radically. What started out as a cash transaction mutated into a cheque payments system and then to credit, debit and store cards. These systems are owned mainly by banks and financial institutions. PayPal, mobile phones and other handheld devices making inter-bank transfers are becoming more widespread.15

The future of retailing: the shape of things to come?Many factors influence the future shape of retailing, and it may be useful to separate the trends in grocery and food distribution from the rest of the industry since it is less exposed to internet competition.

Figure 10 shows how retail grocery formats evolve as incomes grow. As consumers get richer, and as there is more investment in hyper- and supermarkets, so the share of this retailing format increases and then starts to fall again. As countries get still richer, they support a more varied pattern of retailing.

For example, in urban China, 60% of retail grocery trade is though hyper- and supermarkets, up from 50% in 2005. However, China’s ageing population and high savings rates may slow down this expansion, as an increasing proportion of personal income, following global trends, is spent on health and residential care in the absence of an extended family to care for the elderly.

Figure 10 does not extend back to income groups that characterize the emerging world. $5,000 per household is around the threshold income level above which people can afford cars and supermarkets become viable. Households with incomes below this level do use more sophisticated retail outlets but only occasionally.

15 Interestingly, mobile phone payment systems are used extensively in parts of Africa, leapfrogging a number of older technologies.

Figure 10: Relationship between retail grocery developments and income level

Sources: TLE Strategy Retail Model; Euromonitor International

Others

Specialist stores

Independent food stores

Petrol/gas/service stations

Standard convenience stores

Discounters

Supermarkets/hypermarkets

100

90

80

70

60

50

40

30

20

10

0

%

4,000 7,000 10,000 13,000 16,000 19,000 22,000 25,000 28,000 31,000 34,000

GDP per capita (€)

www.chathamhouse.org

page

12

The Changing Retailing Environment

Outside the food retailing segment the situation is more complicated. Some retailing, such as the audio media industry, is already being annihilated as a result of internet competition, both legal and illegal. In some countries, such as Spain, where piracy is widespread, CD/DVD retailers and distributors have effectively withdrawn from the market.16

Figure 11 provides another view of future retail developments, by plotting growth against the inten-sity of modern retailing. The x-axis divides countries and regions according to whether their retail turnover is growing or shrinking, and the y-axis measures the intensity of modern retailing. The approximate posi-tion of different countries and regions is plotted.

The emerging markets, represented by grey arrows, have different starting levels of modern retail intensity. They are all experiencing fast retail growth, and the general trend is for them to move from the bottom right to the top right quad-rant, becoming more like developed economies. The slope of the arrows reflects the degree of difficulty in obtaining the investment to improve the retail infrastructure.

The developed world, represented by blue arrows, is currently experiencing low or negative retail growth, and hence the arrows are all moving from the top right quadrant to the top left one. It is conceivable that, in

some countries, the intensity of modern retailing may also decline – possibly as a result of increased internet trade, which would result in fewer shops.

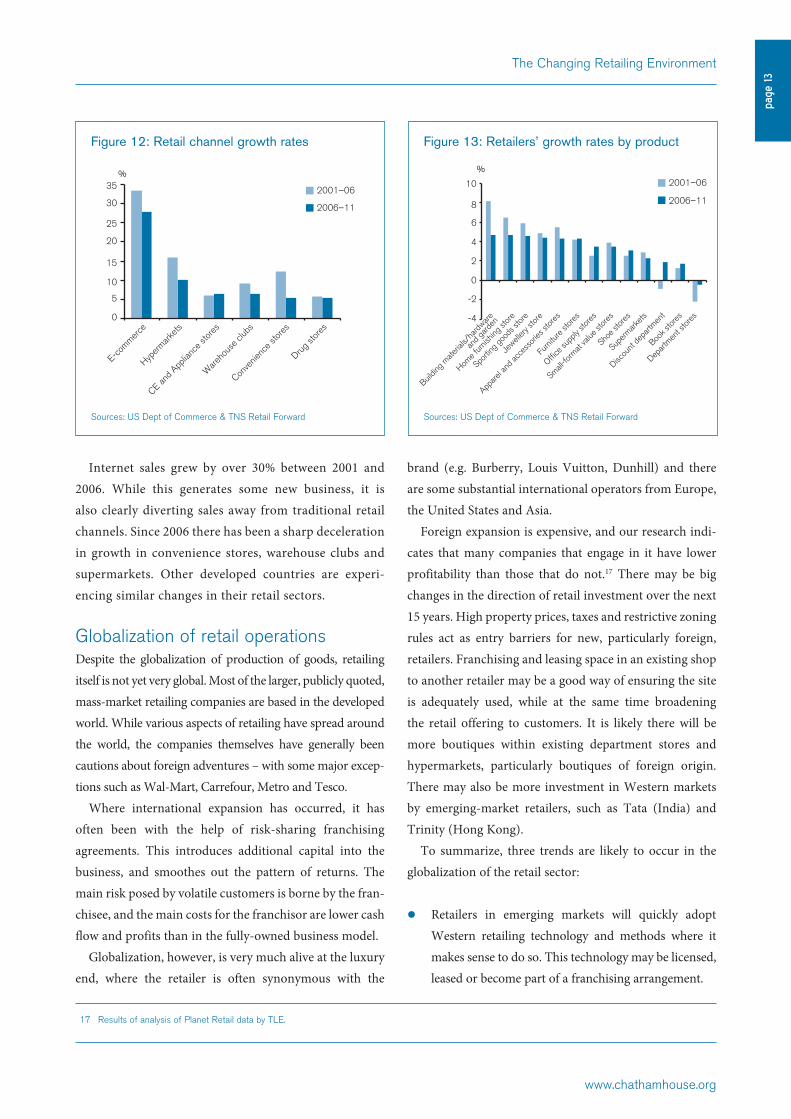

Retailing is a relatively volatile industry, experiencing constant pressure for change. Figures 12 and 13 give an indication of the winds of creative destruction blowing strongly in the US retail sector. As consumer tastes change, so some segments of retailing prosper, while others do not. Milliners, smiths, haberdashers, saddlers have all long since disappeared, to be replaced by other forms of retailing.

16 The Economist, ‘Consumer goods in the recession. The game has changed’, 20 August 2009.

Figure 11: Stylized view of future retail developments

Intensity of modern retailing

Retail turnover growth0%

100%

Brazil

USA

EU

Japan

India

Africa

China

Russia

‘ Some retailing, such as the audio media industry, is already being annihilated as a result of internet competition . . . In Spain, where piracy is widespread, CD/DVD retailers and distributors have effectively withdrawn from the market ’

www.chathamhouse.org

page

13

The Changing Retailing Environment

Internet sales grew by over 30% between 2001 and 2006. While this generates some new business, it is also clearly diverting sales away from traditional retail channels. Since 2006 there has been a sharp deceleration in growth in convenience stores, warehouse clubs and supermarkets. Other developed countries are experi-encing similar changes in their retail sectors.

Globalization of retail operationsDespite the globalization of production of goods, retailing itself is not yet very global. Most of the larger, publicly quoted, mass-market retailing companies are based in the developed world. While various aspects of retailing have spread around the world, the companies themselves have generally been cautions about foreign adventures – with some major excep-tions such as Wal-Mart, Carrefour, Metro and Tesco.

Where international expansion has occurred, it has often been with the help of risk-sharing franchising agreements. This introduces additional capital into the business, and smoothes out the pattern of returns. The main risk posed by volatile customers is borne by the fran-chisee, and the main costs for the franchisor are lower cash flow and profits than in the fully-owned business model.

Globalization, however, is very much alive at the luxury end, where the retailer is often synonymous with the

brand (e.g. Burberry, Louis Vuitton, Dunhill) and there are some substantial international operators from Europe, the United States and Asia.

Foreign expansion is expensive, and our research indi-cates that many companies that engage in it have lower profitability than those that do not.17 There may be big changes in the direction of retail investment over the next 15 years. High property prices, taxes and restrictive zoning rules act as entry barriers for new, particularly foreign, retailers. Franchising and leasing space in an existing shop to another retailer may be a good way of ensuring the site is adequately used, while at the same time broadening the retail offering to customers. It is likely there will be more boutiques within existing department stores and hypermarkets, particularly boutiques of foreign origin. There may also be more investment in Western markets by emerging-market retailers, such as Tata (India) and Trinity (Hong Kong).

To summarize, three trends are likely to occur in the globalization of the retail sector:

zz Retailers in emerging markets will quickly adopt Western retailing technology and methods where it makes sense to do so. This technology may be licensed, leased or become part of a franchising arrangement.

Figure 12: Retail channel growth rates

Sources: US Dept of Commerce & TNS Retail Forward

Figure 13: Retailers’ growth rates by product

Sources: US Dept of Commerce & TNS Retail Forward

2001–06

2006–11

35

30

25

20

15

10

5

0

%

E-com

merce

Hyper

markets

CE and A

pplia

nce s

tores

Ware

hous

e club

s

Conve

nienc

e stor

es

Drug s

tores

Buildin

g mate

rials/

hardw

are

and g

arden

Home f

urnish

ing st

ore

Sportin

g goo

ds st

ore

Jewelr

y stor

e

Appare

l and

acce

ssori

es st

ores

Furni

ture s

tores

Office s

upply

store

s

Small fo

rmat

value

store

s

Shore

stores

Superm

arkets

Discou

nt de

partm

ent

Book s

tores

17 Results of analysis of Planet Retail data by TLE.

-4

-2

0

2

4

6

8

10 2001–06

2006–11

%

Buildin

g mate

rials/

hardw

are

and g

arden

Home f

urnish

ing st

ore

Sportin

g goo

ds st

ore

Jewell

ery st

ore

Appare

l and

acce

ssori

es st

ores

Furni

ture s

tores

Office s

upply

store

s

Small-fo

rmat

value

store

s

Shoe s

tores

Superm

arkets

Discou

nt de

partm

ent

Book s

tores

Depart

ment s

tores

www.chathamhouse.org

page

14

The Changing Retailing Environment

zz Western retailers, particularly those faced with static domestic markets, will try to expand into emerging markets. While some may succeed, many will not.

zz Some emerging-market retailers will also look to expand into developed markets where sales and profit values are higher than in their domestic markets.

ConclusionThere is not likely to be a single global ‘retail future’. What happens will depend on location, local income and demo-graphics. Patterns of change in the developed world may well look different from those in the emerging markets.

Developed-world retailing will face stagnant demand, ageing and shrinking populations, and tough price compe-tition. It will be a zero-sum game in many instances, made more difficult by the gradual diversion of sales away from the high street and toward the internet.

Emerging markets will enjoy faster growth as popula-tions and incomes rise quite rapidly. However, higher global demand is keeping the price of many commodities high, and these crucial inputs will make some goods less affordable for consumers in poorer countries. This suggests that the increase in living standards, and hence shifts to consuming higher-value products, may be slightly delayed in emerging markets.

It is likely that there will be changes in the balance between the different retail channels. Hyper- and super-markets may become less dominant in the higher-income countries, as convenience become relatively more important and hard discounters out-compete them on price.

There may be more ‘disintermediation’ of different types of retailers and retail channels where the internet is an attractive alternative to conventional shopping. There will be a rise in multi-channel shopping, which might suggest a new role for shops – to offer an ‘experience’ rather than being the main location of retail sales.

We could also expect some convergence in retailing forms, climate and zoning laws, permitting more street markets in the West and more supermarkets in emerging markets. There could be some new arrange-ments, with ‘vertical shopping’ reflecting the increased diversity of floor space usage in skyscrapers being but one example.18

Finally, while there will be further advances in internet retailing, shopping is unlikely to be reduced to a TV or computer screen and the local post office. Shopping fulfils a hugely important social and human need. This suggests that inter-personal contact and an ability to examine products before purchasing them will remain powerful reasons to expect the retail industry to persist in its tradi-tionally recognizable forms well into the 21st century.

References and sources

Alch, Mark L. (2000), ‘The echo-boom generation: a growing force in American society’. The Futurist. vol. 34, no. 5, September.

Benson-Armer, Richard, Peter Czerepak and Tim Koller (2010), ‘The Commodity Crunch in Consumer Packaged Goods’, McKinsey Quarterly, December.

Bolton, Steve, ‘Retail Systems Multi Channel Summit’, Retailpragmatist.com.

Branson, W. H. (1972), Macroeconomic Theory and Policy (New York: Harper International).

Deloitte (2011), ‘The Multi-channel Opportunity. Consumer Survey Findings’, February.

18 The ‘high street’ may now be on floors 15 to 20 out of a 40-storey skyscraper; Galerie Lafayette in Frankfurt Zeil is an example. This development also has

echoes of the original concepts for large skyscraper blocks proposed by Le Corbusier in the 1920s.

‘ Inter-personal contact and an ability to examine products before purchasing them will remain powerful reasons to expect the retail industry to persist in its traditionally recognizable forms well into the 21st century ’

www.chathamhouse.org

page

15

The Changing Retailing Environment

Deloitte (2004), ‘Synchronicity: An Emerging Vision of the Retail Future’, A Deloitte Research Consumer Business Brief by Carl Steidtmann (Chief Economist).

Department of Trade and Industry, Retail Strategy Group (2004), The Retail Development Process and Land Assembly: Volume 1 – Report, February.

Dickinson, Helen (2010), ‘Social Networking becomes an Integral Part of Retail’, KPMG briefing notes, August.

The Economist (2009), ‘Consumer goods in the recession. The game has changed’, 20 August.

Economist Intelligence Unit (2009a), ‘World Consumer Goods and Retail Industry Forecast 2009’.

Economist Intelligence Unit (2009b), ‘World Expenditure on Food, Beverages and Tobacco’.

Euromonitor (2009), www.blog.euromonitor.com/2009. Regional focus ageing asia pacific html.

European Commission (2009), ‘Road Freight Transport Vademecum’, DG for Energy & Transport, March.

Eurostat (2009), ‘European Business, Facts and Figures’, Luxembourg.

Fernandez-Villaverde, Jesús and Dirk Krueger (2004), ‘Consumption Over the Life Cycle. Facts from Consumer Expenditure Survey Data’ (University of Frankfurt, CEPR, NBER and University of Pennsylvania, 14 September).

Findlay, Anne and Leigh Sparks (2006), Retail Planning and Food Retailing Competition Issues, Briefing Paper 5, Institute for Retail Studies, University of Stirling, October

Forrester Research and Internetworldstats.com, (2010), JuneForum for the Future (2009), ‘PepsiCo Scenarios and

Strategy 2030’, www.forumforthefuture.org Hale, Todd (2010), ‘Mining the U.S. Generation Gaps’,

Generations, 4 March.IEA (2006), World Energy Outlook 2006 (Paris:

International Energy Agency).IEA/Office of the Chief Economist (2010), ‘Energy

Subsidies: Getting the Prices Right’, 7 June. IEA/OPEC/OECD/World Bank Joint Report (2010),

Analysis of the Scope of Energy Subsidies and Suggestion for the G-20 Initiative, prepared for submission to the G-20 Summit Meeting Toronto (Canada), 26–27 June.

IMAP (2010), Retail Industry Global Report, ‘No Off the Shelf Solutions’.

IMF (2011), Primary Commodity Prices. IMF database, downloaded March 2011.

KPMG & Knight Frank (2010), ‘Retail Property: Investment Trends and Opportunities in China’, May.

KPMG and UK India Council (2011), ‘The India Imperative’, Spring/Summer.

KPMG/Synovate Retail (2010), Think Tank White Paper No. 17: ‘How is the Internet Changing UK Retail?’, July.

Madden, Peter (2007), ‘Scenarios for the Future of UK Retail and Sustainable Development’, Forum for the Future.

Market Wire (2004), ‘Generational Buying Behaviours Examines Shopping Habits of Gen X’ers, Boomers, and Matures’, December.

Morrison, Ewan, ‘Why Y Matters (mapping the coming con sum ption patterns of Generation Y)’, at www.bellacaledonia.org.uk

Overman, Henry (2011), Big Ideas: Economic Geography, Centre for Economic Performance: Paper No. CEPCP331, March.

Paulin, Geoffrey (2008), ‘Expenditure Patterns of Young Single Adults: Two Recent Generations Compared’, Monthly Labour Review, December.

Paulin, Geoffrey and Brian Riordon (1998), ‘Making It On Their Own: The Baby Boom Meets Generation X’, Monthly Labour Review, February.

Planet Retail, Global Input figures.PwC (2008), ‘Global Sourcing: Shifting Strategies’, London.PwC, TNS Retail Forward (2007), ‘Retailing 2015, New

Frontier’, London.TLE, ChannelGro© Model, summary tables.TLE, Globegro© 2010 and 2011.TLE, Retail Curves Model 2007, summary charts.United Nations National Accounts (2010), ‘Share of

GDP by Activity’, 2010 figures, downloaded May 2011 from online database.

United Nations, Department of Economic and Social Affairs, Population Division (2009), World Population Prospects: The 2008 Revision, CD-ROM Edition.

World Bank (2005), http://data.worldbank.org/data-catalog/international-comparison-program.

www.chathamhouse.org

page

16

The Changing Retailing Environment

Chatham House has been the home of the Royal

Institute of International Affairs for ninety years. Our

mission is to be a world-leading source of independent

analysis, informed debate and influential ideas on how

to build a prosperous and secure world for all.

David Hurst is the chairman of TLE Strategy Ltd

and has worked for many years in the fast-moving

consumer goods (FMCG) industry. He has deep

knowledge of how FMCG companies sell to retailers,

and has developed innovative ways of analysing future

trends.

Dr Andrew Black works for TLE, as well as being

the managing director of BVA Ltd, a financial and

management consultancy company. He has extensive

experience of the FMCG, defence and the automotive

industries. He worked for many years as a director at

PwC and has written books on shareholder value.

The authors would like to thank Donald Hepburn, and

their colleagues at TLE, for many useful suggestions

and views. The authors remain responsible for any

errors and omissions.

Chatham House10 St James’s SquareLondon SW1Y 4LEwww.chathamhouse.org

Registered charity no: 208223

Chatham House (the Royal Institute of International Affairs) is an independent body which promotes the rigorous study of international questions and does not express opinions of its own. The opinions expressed in this publication are the responsibility of the authors.

© The Royal Institute of International Affairs, 2011

This material is offered free of charge for personal and non-commercial use, provided the source is acknowledged. For commercial or any other use, prior written permission must be obtained from the Royal Institute of International Affairs. In no case may this material be altered, sold or rented.

Cover image © istockphoto.com

Designed and typeset by Soapbox, www.soapbox.co.uk

The World’s Industrial Transformation Series

This briefing paper forms part of a major Chatham

House project on the changing industrial landscape

and follows a framework paper, Mapping the World’s

Changing Industrial Landscape, by Donald Hepburn

(July 2011).

Other Case Studies

zz The Changing Landscape of the Aircraft Industry

S. McGuire (July 2011)

zz The New Georgraphy of Automotive

Manufacturing M. Ferrazzi and A. Goldstein

(July 2011)

zz Shifting Patterns in the Pharmaceutical Industry

M. Owen (October 2011)

Financial support for this project from the Toshiba

International Foundation (TIFO) is gratefully

acknowledged.

www.chathamhouse.org/industrialtransformation/