Download - Broadband for All through Universal Service?

Broadband for All through Universal Service?

17 June 2010, Lisbon

The Impact of Broadbandon Growth and Productivity (MICUS)

Widespread take-up triggers economic impact

New objectives in European Digital Agenda

Basic broadband access for all by 2013 Access for all to 30 Mbps and beyond

by 2020 Subscription by 50% of households to

100 Mbps by 2020

The Role of Effective Competition

Competition, based on ex-ante regulation, has led to over 90% market coverage:

At the end of 2008, fixed broadband networks covered almost 93% of the EU population (98% urban; 77% rural)

As a result of effective wholesale access and increasing level of competition significant decrease in end user prices

A pro-competitive legal framework is needed to move forward (see later)

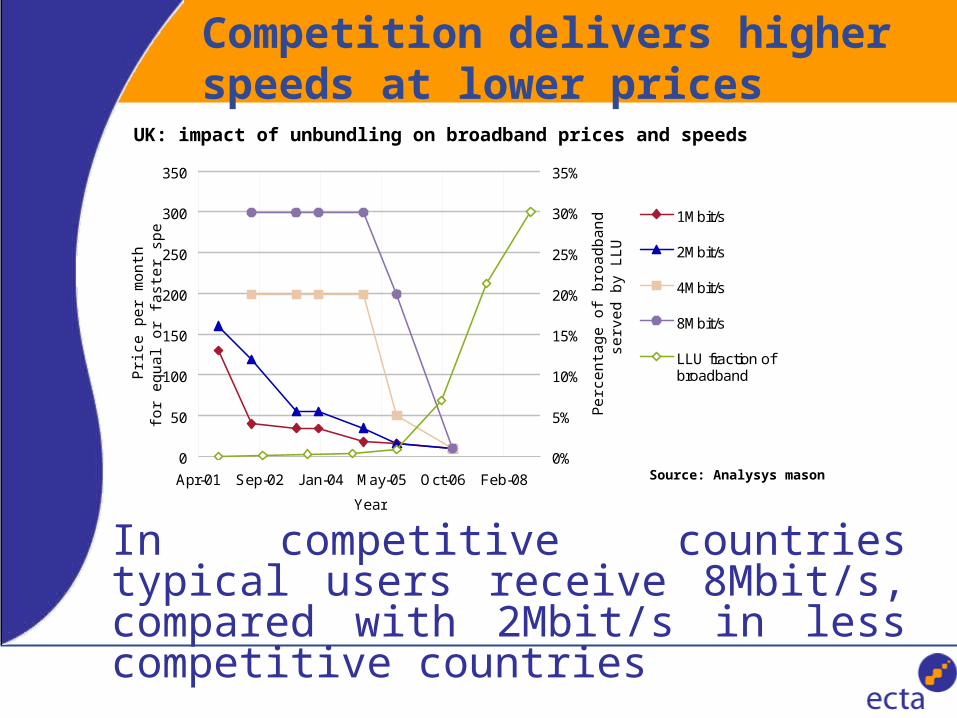

Competition delivers higher speeds at lower prices

0

50

100

150

200

250

300

350

Apr-01 Sep-02 Jan-04 May-05 Oct-06 Feb-08

Year

Pric

e pe

r m

onth

fo

r eq

ual o

r fa

ster

spe

ed, G

BP

0%

5%

10%

15%

20%

25%

30%

35%

Per

cent

age

of b

road

band

line

s s

erve

d by

LLU

1Mbit/s

2Mbit/s

4Mbit/s

8Mbit/s

LLU fraction ofbroadband

Source: Analysys mason

UK: impact of unbundling on broadband prices and speeds

In competitive countries typical users receive 8Mbit/s, compared with 2Mbit/s in less competitive countries

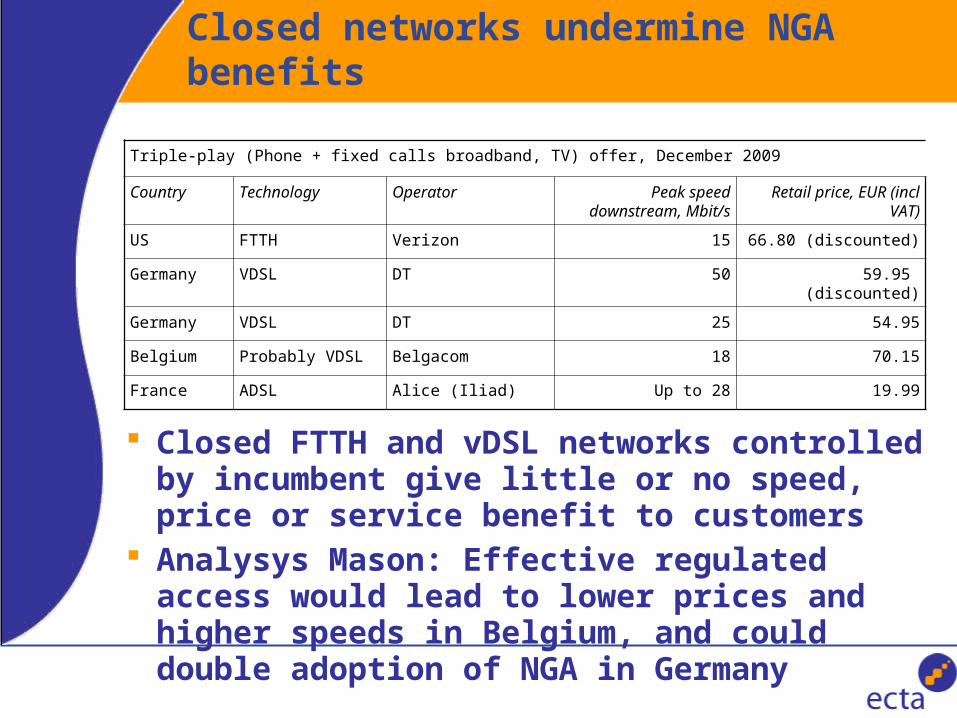

Closed networks undermine NGA benefits

Triple-play (Phone + fixed calls broadband, TV) offer, December 2009

Country Technology Operator Peak speed downstream, Mbit/s

Retail price, EUR (incl VAT)

US FTTH Verizon 15 66.80 (discounted)

Germany VDSL DT 50 59.95 (discounted)

Germany VDSL DT 25 54.95

Belgium Probably VDSL Belgacom 18 70.15

France ADSL Alice (Iliad) Up to 28 19.99

Closed FTTH and vDSL networks controlled by incumbent give little or no speed, price or service benefit to customers

Analysys Mason: Effective regulated access would lead to lower prices and higher speeds in Belgium, and could double adoption of NGA in Germany

High broadband take-up in competitive markets

0

5

10

15

20

25

30

35

40

Nethe

rland

s

Denm

ark

Norway

Switzer

land

Korea

Icela

nd

Sweden

Luxe

mbo

urg

Finlan

d

Canad

a

Ger

man

y

Franc

e

Unite

d Kin

gdom

Belgiu

m

Unite

d Sta

tes

Austra

lia

Japa

n

New Z

eala

nd

Austri

a

Irelan

d

Spain

Italy

Czech

Rep

ublic

Portu

gal

Gre

ece

Hunga

ry

Slova

k Rep

ublic

Polan

d

Turke

y

Mex

ico

Source: OECD

DSL Cable Fibre/LAN Other

OECD Broadband subscribers per 100 inhabitants, by technology, June 2009

OECD

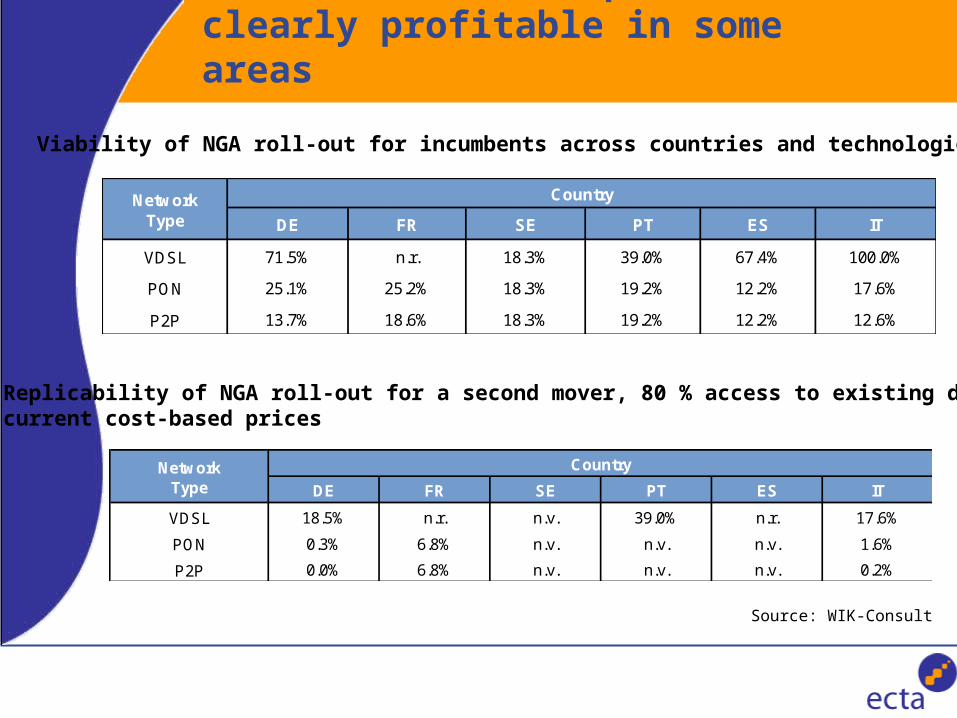

NGAN rollout is expensive but clearly profitable in some areas

VDSL

PON

P2P

SE PT ES IT

71.5% n.r. 18.3% 39.0% 67.4% 100.0%

DE FR

25.1% 25.2% 18.3% 19.2%

13.7% 18.6% 18.3% 19.2%

12.2% 17.6%

12.2% 12.6%

CountryNetwork Type

VDSL

PON

P2P

n.v. 1.6%

0.0% 6.8% n.v. n.v. n.v. 0.2%

0.3% 6.8% n.v. n.v.

Network Type

Country

DE FR SE PT ES IT

18.5% n.r. n.v. 39.0% n.r. 17.6%

Viability of NGA roll-out for incumbents across countries and technologies

Replicability of NGA roll-out for a second mover, 80 % access to existing ducts at current cost-based prices

Source: WIK-Consult

Effective regulation and strong enforcement result in higher levels of investment

Relationship between Regualtion and Investment

0

50

100

150

200

250

300

350

100.0 120.0 140.0 160.0 180.0 200.0 220.0 240.0 260.0 280.0

Institutions and Regualtory Score 2007

Inve

stm

ent

per

Cap

ita

2007

DK

NL

UK

NOIE

IT

FR

ESSE

HU

PT

FIDE

ATEL

CZPL

BE

Achieving Broadband for All

Universal service is not the best tool to

deliver broadband for all: Designed for traditional voice-based services

(market is already delivering) Payphones and printed directories are much less

relevant Inefficient funding mechanisms Dynamically developing markets

Other instruments already in place

The Role of Targeted State Aid

Where private investment in NGA networks is not commercially viable, for example in sparsely- populated, rural or remote areas, targeted state aid can play an important role in providing access to broadband:

Community Guidelines for the application of State aid rules in relation to rapid deployment of broadband networks

Public funding, not a sector-specific levy

The Role of Wireless Broadband

Where the deployment of high-speed fibre infrastructure is entirely unreasonable, even with public funding, wireless broadband can contribute to bridging the digital divide:

• Important, complementary, role for wireless broadband (not substitutable for fixed)

• Non-discriminatory, pro-competitive allocation of spectrum by Member States

• RSPP should recommend a catalogue of solutions to the competitive challenge

• Opening up the Digital Dividend to wireless broadband services by 2015, at the latest

• More spectrum allocated for the rollout of mobile broadband services