Caribbean Infrastructure PPP Roadmap

March 2014

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

© 2014 Public-Private Infrastructure Advisory Facility (PPIAF)1818 H Street, NWWashington, DC 20433www.ppiaf.orgE-mail: [email protected] The findings, interpretations, and conclusions expressed in this report are entirely those of the authors and should not be attributed in any manner to the Public-Private Infrastructure Advisory Facility (PPIAF) or to The World Bank Group, to its affiliated organizations, or to members of its Board of Executive Directors or the countries they represent.

Neither PPIAF nor The World Bank Group guarantees the accuracy of the data included in this publication or accepts responsibility for any consequence of their use. The boundaries, colors, denominations, and other information shown on any map in this report do not imply on the part of PPIAF or The World Bank Group any judgment on the legal status of any territory or the endorsement or acceptance of such boundaries. For questions about this publication or information about ordering more copies, please refer to the PPIAF website or contact PPIAF by email at the address above.

Rights and Permissions The material in this work is subject to copyright. Because PPIAF and The World Bank Group encourages dissemination of its knowledge, this work may be reproduced, in whole or in part, for noncommercial purposes, as long as full attribution to this work is given. Any queries on rights and licenses, including subsidiary rights, should be addressed to World Bank Publications, The World Bank Group, 1818 H Street, NW, Washington, DC 20433, USA; fax: 202-522-2625; e-mail: [email protected]. Cover photos: Dominic Chavez / World BankCover design: TM Design, Inc.

i

SECTIONTITLE

TABLE OF CONTENTS

Acknowledgements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ii

Abbreviations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iii

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1 . Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6

2 . Rationale for PPPs in the Caribbean . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7

3 . Caribbean Experience with PPP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10

4 . Emerging PPP Opportunities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13 4.1 TransportSector. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15 4.1.1 Airports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16 4.1.2 Ports. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16 4.1.3 OtherMaritimeTransport . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17 4.1.4 Roads . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18 4.2 ElectricitySector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19 4.3 WaterSector. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22 4.4 TelecommunicationsSector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22 4.5 SocialandGovernmentInfrastructureSectors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .23

5 . Learning from Experience: PPP Constraints . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24 5.1 ImplementationChallenges . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .24 5.2 BarrierstoPPP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25

6 . The Way Forward: PPP Actions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28 6.1 PPPArchitecture:PolicyFrameworks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28 6.2 PPPArchitecture:InstitutionalCapacity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30 6.3 PPPProjectsandPipelines. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .33 6.4 SequencingofActionsandImplementationChallenges. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

AppendicesAppendixA:CaribbeanPPPExperience—ExistingPPPsintheCaribbean . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

TablesTable4.1: ElectricitySector—StructureandPerformance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Table4.2: PotentialElectricityPPPProjects. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

FiguresFigure0.1: CaribbeanPPPPipelinebySector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2Figure0.2: LimitedPPPPolicyandInstitutionalArchitectureintheCaribbean . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3Figure0.3: PPPActions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4Figure3.1: PrivateInfrastructureInvestmentExperienceintheCaribbean. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10Figure3.2: PPPProjectExperienceintheCaribbean . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Figure3.3: PPPPolicyandInstitutionalArchitectureintheCaribbean . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12Figure4.1: NumberofCurrentandPlannedPPPProjectsintheCaribbeanbyCountry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14Figure4.2: CurrentandplannedPPPProjectsintheCaribbeanbySector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15Figure5.1: ConstraintsArisingfromLimitedPPPPolicyandInstitutionalArchitecture . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25Figure5.2: SummaryofBarriersandImplicationsforPPPOutlook . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27Figure6.1: TypicalPPPProgramFunctionsandResponsibilities. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30Figure6.2: TypicalPPPProjectDevelopmentProcess . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .32Figure6.3: SummaryandSequencingofActions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .33

BoxesBox2.1: PPPsand“FiscalSpace” . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9Box3.1: DefiningPPPSuccess . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Box4.1: HowthePPPPipelineProjectswereIdentified. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13Box4.2:TheChallengesofRegionalProjects:OECSRegionalFastFerry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18Box6.1: PPPPoliciesandLaws . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29Box6.2:HowCouldaRegionalPPPUnitWork? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

TABLE OF CONTENTS

ii

ACKNOWLEDGEMENTS

ACKNOWLEDGEMENTS

ThisreporthasbeenpreparedbytheLatinAmericaandCaribbeanSustainableDevelopmentDepartment(LCSSD)oftheWorldBank.TheworkwasledbyHelenMartin,Consultant(LCSSD)—leadauthorofthisreport—undertheoverallguidanceofSophieSirtaine,WorldBankCountryDirectorfortheCaribbean,andCeciliaBriceño-Garmendia,LeadEconomist(LCSSD).TheteamandcontributorsincludedDavidBotBaNjockoftheInternationalFinanceCorporation(IFC)’sC3PAdvisorypractice,andDavidEhrhardt,AlfonsoGuzmán,BrianSamuel,andIkepoOyenugafromCastalia.InitialconclusionsofthereportwerepresentedattheCaribbeanPPPForumheldinBarbadoson19-20November,2013,forvaluablefeedbackfromparticipatinggovernmentofficialsanddevelopmentpartners.

TheteamwishestothankpeerreviewersDanielPulido,PierreNadji,andTomVis;aswellasotherWorldBankGroupcolleagueswhoprovidedcomments,includingRichardCabello,FranciscoGalraoCarneiro,JamesClose,GlenKierse,CristinaMariaLadeiraFerreira,AlessandroLegrottaglie,CliveHarris,RuiMonteiro,GylfiPalsson,GalinaSotirova,MariaAngelicaSotomayor,SatheeshSundararajan,SonaVarma,andJunZhang.Finally,theteamwishestoacknowledgethegeneroussupportforthisactivityfromthePublic-PrivateInfrastructureAdvisoryFacility(PPIAF).

iii

ABBREVIATIONS

ABBREVIATIONS

ESCO EnergyServiceCompany

EU EuropeanUnion

ICT Informationandcommunicationstechnology

IDB Inter-AmericanDevelopmentBank

IFC InternationalFinanceCorporation

IMF InternationalMonetaryFund

IPP Independentpowerproducer

LNG LiquidNaturalGas

MIF MultilateralInvestmentFacility

NRW Non-RevenueWater

OECS OrganizationofEasternCaribbeanStates

PPA Powerpurchaseagreement

PPIAF Public-PrivateInfrastructureAdvisoryFacility

PPP Public-privatepartnership

WB WorldBank

WBG WorldBankGroup

iv LARGER SECTION TITLE

1EXECUTIVE SUMMARY

EXECUTIVE SUMMARY

Executive Summary

There is growing interest in the Caribbean in using public-private partnerships (PPPs) to provide infrastructure. Infrastructureinvestmentneedsaresignificantacrosstheregion,toboosteconomicgrowthandresilience.ManyCaribbeangovernmentsareincreasinglyturningtoPPPstomeetthoseneeds,drivenbyacombinationoftightfiscalconstraints,andgrowingappreciationoftheroleoftheprivatesectorindeliveringpublicservices.Thisinclinationreflectsglobaltrendsandexperience.ManycountrieshavefoundthatPPPs—whenselected,structured,andmanagedwell—canhelpmakethebestuseofthefinancialandtechnicalresourcesofthepublicandprivatesectorstoprovideimprovedinfrastructureassetsandservices.

Experience with PPPs to date in the Caribbean has been mixed. PPPsarenotnewintheregion,havingbeenusedtodeliverneworimprovedroads,ports,airports,bulkwatertreatmentfacilities,andelectricitygenerationplants.ManyPPPprojectshaveoperatedsuccessfullyforyears,deliveringhigh-qualityinfrastructurefacilities.Othershavefacedchallenges.Inmanycases,thecomplexityofthePPPdevelopmentandimplementationprocesshasmeantlongdelaysindeliveringprojects;othersresultedinquestionablevalueorunexpectedcoststogovernmentsorconsumers.AllPPPprojectstodatewereimplementedwithoutoverarchingPPPpolicyframeworks,asdescribedinmoredetailbelow.

This raises a question: How can Caribbean governments navigate the challenges to make the best use of PPPs to deliver improved infrastructure assets and services? This“CaribbeanInfrastructurePPPRoadmap”seekstoanswerthisquestion.ItreviewstheoutlookforPPPsintheregion,by:identifyingPPPprojectopportunitiesinelevenCaribbeancountries1;constraintsorbarrierstosuccessfuldevelopmentofthoseprojectopportunities,basedonpreviousexperience;andpossibleactionstoovercometheseconstraints.TheRoadmapwasdevelopedbytheWorldBankGroup,withinputsfromCaribbeangovernments,privateinvestors,andotherdevelopmentpartners,andsupportfromthePublic-PrivateInfrastructureAdvisoryFacility(PPIAF).

PPP OPPORTUNITIES

This Roadmap identified a potential PPP “pipeline” of 33 projects that are being actively developed as PPPs across 11 Caribbean countries,withatotalestimatedinvestmentvalueofUSD2to3billion.Theseareprojectsthatareactivelyunderdevelopment,albeitinsomecasesatanearlystage,andthatappearpotentiallyviableasPPPsfromaprimafacieassessment—fromtechnical,economic,commercial,legalandregulatory,andpoliticalperspectives—althoughdetailedappraisalisneededinmostcases.Assuch,thispipelineprovidesareasonableestimateofthepotentialforPPPintheCaribbeaninthenexttwotofiveyears.

This pipeline represents a significant planned increase in the use of PPPs in several countries:notablyJamaicaandTrinidadandTobago(whichtogethercontributehalfthepipelineprojects);Suriname;andsomeOrganizationofEasternCaribbeanStates(OECS)memberssuchasSaintLuciaandGrenada.Ontheotherhand,somecountrieswithmorePPPexperiencearemovingawayfromPPPgoingforward.ParticularlyintheDominicanRepublic,challengeswithearlyPPPsinsomesectorshaveledtopoliticalandpublicskepticism.

1TheRoadmapcoversthefollowing11countries:AntiguaandBarbuda,Dominica,theDominicanRepublic,Grenada,Haiti,Jamaica,SaintKittsandNevis,SaintLucia,SaintVincentandtheGrenadines,Suriname,andTrinidadandTobago.ThesewereselectedasWorldBankGroup(WBG)clientcountriesforwhichaninitialdeskreviewprovidedprimafacieevidenceofinterestinPPP.Inpractice,severalnon-WBGclientcountriesintheregionhaveexpressedanintentiontomakegreateruseofPPP.Assuch,theRoadmapdoesnotpresentacomprehensiveoutlookforPPPacrosstheCaribbeanregion,butcouldbeconsideredtoprovidearepresentativepicture.RegionalactionspresentedintheRoadmapcouldinpracticeapplytoawidergroupofcountries.

2

EXECUTIVE SUMMARY

EXECUTIVE SUMMARY

Transport and power opportunities remain significant—although new PPP sectors are also emerging.Figure0.1belowshowsthesectordistributionofthe33pipelineprojects.Transportprojectsincluderoads(bothtollroadsandlong-termrehabilitationandmaintenancecontracts);amajorportconcessionforJamaica’sKingstonContainerTerminals;passengerferryandcruiseshipfacilities;andfiveproposedairportconcessions.Intheenergysector,thefocusinondiversifyingenergysources,withseveralPPPsindevelopmentforrenewableenergygeneration.WhiletelecommunicationsservicesaremostlyprivateintheCaribbean,potentialPPPsintheICTsectorcompriserolloutofhigher-speedbroadbandnetworks,aswellasgovernmentITsystems.ViewsonPPPinthewatersectorremaincircumspect,outsidebulkwaterandwastewatertreatmentprojectsbeingconsideredinJamaica.Finally,severalcountriesareconsideringPPPprojectsforsocialandgovernmentinfrastructuresuchashealthandeducationfacilities—althoughtheaffordabilityofsuchprojectsremainsaquestioninthefaceoftightfiscalconstraints.

Figure 0.1: Caribbean PPP Pipeline by Sector

Source: Authors, based on Castalia and World Bank research, and inputs from relevant governments

Most of these projects are at a very early stage.SubstantialfurtherworkisneededtoassesswhethertheprojectsareviableandrepresentattractivePPPopportunities;andforthosethatdo,totaketheseprojectsthroughtofinancialcloseanddeliverimprovedinfrastructureontheground.Ofthe33projectsidentified,16remainattheconceptstage;13areundergoingmoredetailedfeasibilityanalysisorduediligence;andtransactionsareunderwayforonlyfourprojects.Manyhavebeenreceivingsupportfromdevelopmentpartners,includingtheWorldBankGroup,theInter-AmericanDevelopmentBank(IDB)anditsMultilateralInvestmentFund(MIF),theEuropeanUnion(EU),andtheBill,Hillary&ChelseaClintonFoundation,amongothers.

Policy Law Detailed Guidelines Defined Roles

Dedicated Units(s)

Staff with PPP Experience

Dedicated Project Prep Funding

Jamaica 4(2012)

6 Underway 44

(DBJ&MOF)6

Trinidad & Tobago

4(2012)

6 Underway 44

(MOF)6

Dominican Republic 6 6 6 6 6 6

Haiti 6 6 6 64

(MOF)6

Suriname 6 6 6 6 6 6

OEC States 6 6 6 6 6 6

PPP CONSTRAINTS

Experience in the Caribbean suggests that governments may face some constraints in turning this potential PPP pipeline into successful projects on the ground. CaribbeancountrieshaveimplementedPPPs,andseveralaresuccessfullyprovidingimprovedinfrastructureservices.However,othershaveexperiencedproblemsinimplementation.Theseproblemshaveincludedunexpectedfiscalcosts;questionablevalueformoney;andlongdelaysinclosingdeals.Manyadditionalprojectshavesimplyfailedtolaunch,asevidencedbythelargenumberofpipelineprojectsthathavebeenunderdiscussionforsometime.Inparticular,regionalprojectideashavestruggledtogetoffthegroundinthefaceoflimitedmechanismsforregionalcooperation.

Many of these past problems can be traced back to the lack of “PPP architecture” across most of the Caribbean.Inotherwords,thesearethetypesofproblemsthatcountrieswithsuccessfulPPPprogramshavetypicallysolvedbyintroducingPPP-specificpolicyandinstitutionalframeworks—definingclearprocessesformanagingPPPsthatensurethoroughprojectduediligenceandpreparation;definingresponsibilitiesforcarryingoutthoseprocesses;andbuildingcapacitytodoso(bothinternal,andthroughtheuseofwell-qualifiedadvisors).WhileafewCaribbeancountrieshavemadesignificantrecentprogresstowardsestablishingPPPpoliciesandinstitutions—particularlyJamaicaandTrinidadandTobago,asshowninFigure0.2below—significantgapsremainacrosstheregion.

Figure 0.2: Limited PPP Policy and Institutional Architecture in the Caribbean

4Inplace(date)6 AbsentLowModerateHigh;DevelopmentBankofJamaica(DBJ);MinistryofFinance(MOF)Source: Authors, based on Castalia and World Bank research

3

EXECUTIVE SUMMARY

EXECUTIVE SUMMARY

EXECUTIVE SUMMARY

In addition to these constraints on implementing pipeline projects that appear viable, there are additional barriers to greater use of PPP in the Caribbean—thatis,tofurtherexpansionofthepipeline.Inafewcases,particularlyintheenergysector,completionofon-goingsectorreformprocessesisneededto“unlock”opportunitiesforPPP.Inseveralothers,apparentlyviablePPPopportunitiesappearunlikelytobepursuedintheneartermduetoalackofpoliticalinterestinPPPincertaincountriesandsectors—abarrierthatislikelytobemoreintransigent,althoughitmayerodeovertimeinthefaceoflocalPPP“successstories.”

Ultimately, the small scale of infrastructure needs at the country level—particularly for smaller islands—may limit the extent of “marketable” PPP projects. Flexibleapproacheswillbeneededforcountriestomitigatethisinherentbarrier.Ontheonehand,thiscouldincludegreaterregionalcooperation—whetheronregionalprojectsinsectorssuchasenergyandtransport;oraregionalapproachtodevelopingandmarketingPPPpipelinesthatcouldhelpelicitgreaterinterestfrominternationalinvestors.CaribbeangovernmentscouldalsoconsidertargetingawiderrangeofPPPinvestors—includingeducatingandencouraginglocalentrepreneurstogetintothebusiness,andfindingregionalplayersthatmaybeinterestedinsmaller-scaleprojects.

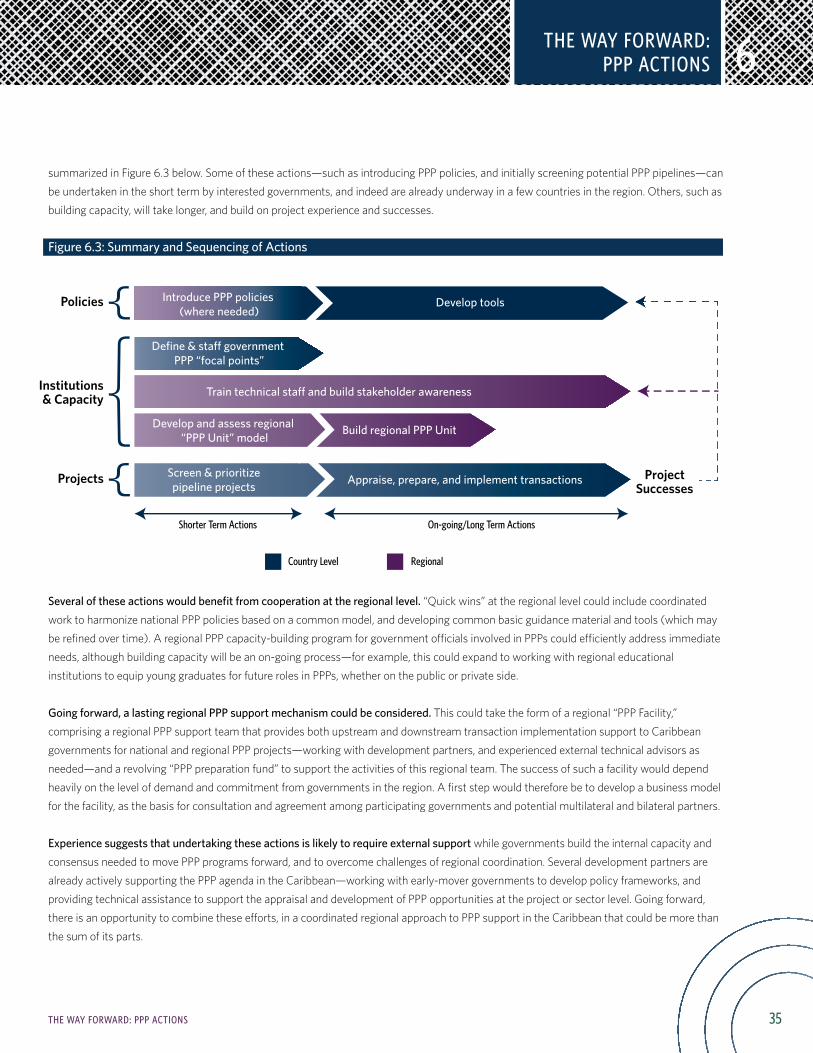

THE WAY FORWARD: PPP ACTIONS

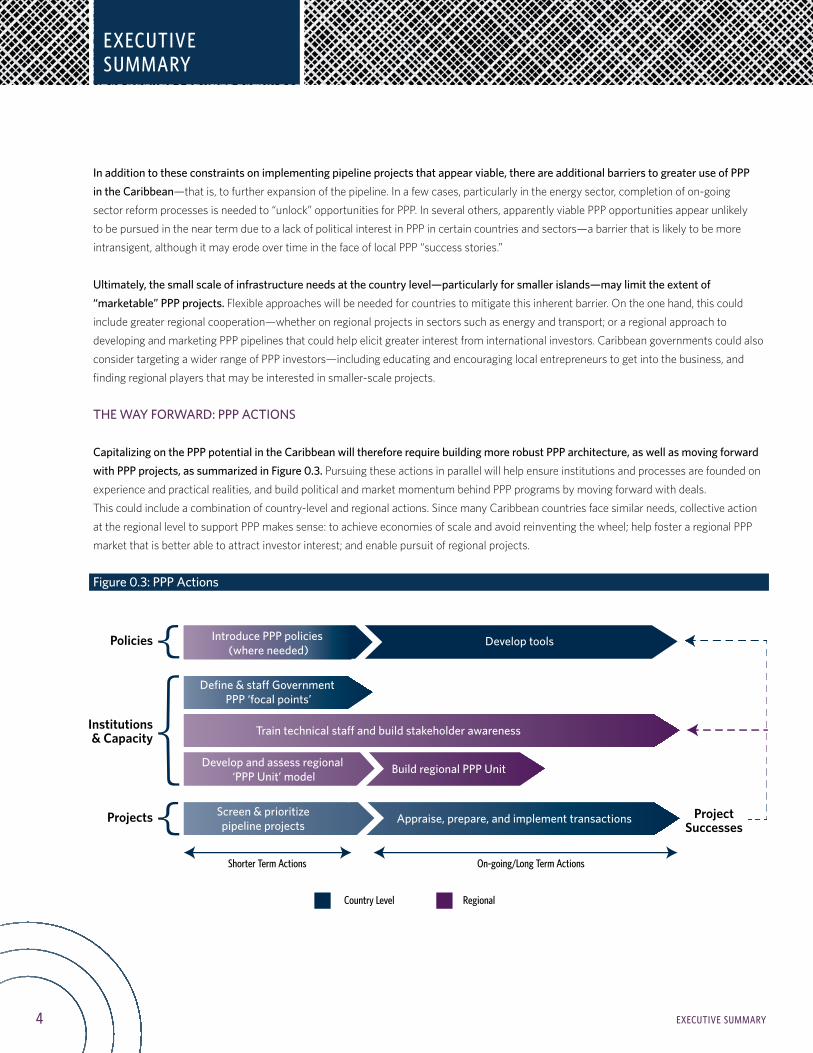

Capitalizing on the PPP potential in the Caribbean will therefore require building more robust PPP architecture, as well as moving forward with PPP projects, as summarized in Figure 0.3.Pursuingtheseactionsinparallelwillhelpensureinstitutionsandprocessesarefoundedonexperienceandpracticalrealities,andbuildpoliticalandmarketmomentumbehindPPPprogramsbymovingforwardwithdeals.Thiscouldincludeacombinationofcountry-levelandregionalactions.SincemanyCaribbeancountriesfacesimilarneeds,collectiveactionattheregionalleveltosupportPPPmakessense:toachieveeconomiesofscaleandavoidreinventingthewheel;helpfosteraregionalPPPmarketthatisbetterabletoattractinvestorinterest;andenablepursuitofregionalprojects.

Figure 0.3: PPP Actions

4 EXECUTIVE SUMMARY

EXECUTIVE SUMMARY

Caribbean countries that intend to make significant use of PPPs going forward would benefit from introducing guiding policy frameworks. Asdescribedabove,ofthecountriescoveredbythisRoadmap,onlyJamaicaandTrinidadandTobagohaverecentlyintroducedPPPpolicies,althoughseveraladditionalgovernmentshaveexpressedinterestindoingso.Whileeachcountrywillneedtodevelopandbuildconsensusarounditsownpolicyorlaw,regionalcooperationonPPPpolicyframeworkscouldinvolvedevelopinga“model”policy,processmanual,andtoolsfromwhichcountriescoulddrawfornationalPPPpolicies.

Building the institutional capacity needed to effectively implement PPP policies and projects could involve actions at both the national and regional level. Theseactionscouldinclude:• Designating “PPP focal points” at the national level byidentifyingteamsorindividualstoplayacoordinatingroleforthePPPpolicyand

projects,andtobearepositoryofexperienceandknowledgeonPPP.JamaicaandTrinidadandTobagohavebothestablishedPPPUnitstothisend,intheDevelopmentBankandMinistryofFinancerespectively.

• Reviewing the case for a regional “PPP Unit,” giventhelimitedscaleofPPPprograms,particularlyonsmallerislands,whichmaymakeitinefficientforeachgovernmenttobuildadedicatedPPPteam.

• Training and capacity building forgovernmentstaffatalllevelswillbeneeded—anotherarearipeforregionalcooperation.AregionalPPPcapacity-buildinginitiativeaimedatgovernmentofficialsinvolvedinPPPscouldaddressimmediateneeds;overtime,thiscouldexpandtoworkingwithregionaleducationalinstitutionstoequipyounggraduatesforfuturerolesinPPPs,whetheronthepublicorprivateside.

At the same time, Caribbean governments can move forward with developing priority PPP projects and pipelines. Intheabsenceofwell-establishedprocessesandinternalcapacity,cautionwillbeneededtoensureearlyPPPprojectsestablishsuccessfulprecedents.Thesupportofexperiencedadvisorswillbecrucial,andgovernmentsneedtobepreparedtoinvestsubstantialresourcesindevelopingPPPswell.GovernmentsmayalsowanttotakeamoresystematicapproachtodevelopingPPPpipelinesbyscreeningprioritypublicinvestmentprojectsforPPPpotential.ThiscanhelpidentifythemostpromisingprojectsforearlyPPPsuccesses,aswellasthelikelyscopeofaPPPprograminthemediumterm.Whileprojectandpipelinedevelopmentintheneartermislikelytofocusatthenationallevel,introducingsuchpipelinestothemarketinacoordinatedway—forexample,througharegionalPPPForum—couldhelpcreatearegional“PPPmarket”andgenerategreaterinvestorinterest.

Experience suggests that undertaking these actions is likely to require external support, whilegovernmentsintheregionbuildtheinternalcapacityandconsensusneededtomovePPPprogramsforward,andtoovercomechallengesofregionalcoordination.TheWorldBankandIFCarealreadysupportingthedevelopmentofPPPprojectsandprogramsinseveralCaribbeancountriesandsectors,asareotherdevelopmentpartnerssuchastheIDBanditsMIF—goingforwardtheseeffortscouldincreasinglybecombinedandcoordinated.“Quickwins”couldincludeworktoharmonizenationalPPPpolicies,buildcommontools,anddeveloparegionalcapacity-buildingprogram.

Going forward, a lasting regional PPP support mechanism could be considered. Thiscouldtaketheformofaregional“PPPFacility,”comprisingaregional“PPPunit”thatprovidesbothupstreamanddownstreamtransactionimplementationsupporttoCaribbeangovernmentsfornationalandregionalPPPprojects—workingwithdevelopmentpartners,andexperiencedexternaltechnicaladvisorsasneeded—andarevolving“PPPpreparationfund”tosupporttheactivitiesofthisregionalteam.Thesuccessofsuchafacilitywoulddependheavilyonthelevelofdemandandcommitmentfromgovernmentsintheregion.Afirststepwouldthereforebetodevelopabusinessmodelforthefacility,asthebasisforconsultationandagreementamongparticipatinggovernmentsandpotentialmultilateralandbilateralpartners.

5EXECUTIVE SUMMARY

6

INTRODUCTION

INTRODUCTION

1

A public-private partnership (PPP) is a long-term contract between a private party and a government agency for providing a public asset or service, in which the private party bears significant risk and management responsibility.2 Thisdiffersfromotherformsofprivate-sectorparticipationininfrastructure,suchasprivatization,wheretheownershipofanassetistransferredtoprivatehands(oftenunderregulation),orajointventure,wheretherelationshipbetweenthepublicandprivatepartiesisdefinedinashareholders’agreement.

There is growing interest in the Caribbean in using PPPs to provide infrastructure. Infrastructure investment needs are significant across the region, to boost economic growth and resilience.ManyCaribbeangovernmentsareincreasinglyturningtoPPPstomeetthoseneeds,drivenbyacombinationoftightfiscalconstraintsandgrowingappreciationoftheroleoftheprivatesectorindeliveringpublicservices.Thisinclinationreflectsglobaltrendsandexperience.ManycountrieshavefoundthatPPPs—whenselected,structured,andmanagedwell—canhelpmakethebestuseofthefinancialandtechnicalresourcesofthepublicandprivatesectorstoprovideimprovedinfrastructureassetsandservices.

Experience with PPPs to date in the Caribbean has been mixed.PPPsarenotnewintheregion,havingbeenusedtodeliverneworimprovedroads,ports,airports,bulkwatertreatmentfacilities,andelectricitygenerationplants.ManyPPPprojectshaveoperatedsuccessfullyforyears,deliveringhigh-qualityinfrastructurefacilities.Othershavefacedchallenges.Inmanycases,thecomplexityofthePPPdevelopmentandimplementationprocesshasmeantlongdelaysindeliveringprojects;othersresultedinquestionablevalueorunexpectedcoststogovernmentsorconsumers.

This raises a question: How can Caribbean governments successfully navigate the challenges to make the best use of PPPs to deliver improved infrastructure assets and services?This“CaribbeanInfrastructurePPPRoadmap”seekstoanswerthisquestion.ItreviewstheoutlookforPPPsintheregion,by:identifyingPPPprojectopportunitiesin11Caribbeancountries3; constraintsorbarrierstosuccessfuldevelopmentofthoseprojects,basedonpreviousexperience;andpossibleactionstoovercometheseconstraints.TheRoadmapwasdevelopedbytheWorldBankGroup,withinputsfromCaribbeangovernments,privateinvestors,andotherdevelopmentpartners,andwithsupportfromthePublic-PrivateInfrastructureAdvisoryFacility(PPIAF).This report presents the “Caribbean Infrastructure PPP Roadmap,”asfollows:• Section2explainstherationaleforPPPsintheCaribbean—itdescribeswhyandhowPPPscanaddvaluebydeliveringneeded

infrastructureeffectivelyandefficiently;• Section3presentsexperiencewithprivate-sectorparticipationininfrastructureandPPPinthe11countriescoveredbytheRoadmap;• Section4reviewsemergingPPPopportunities:apotentialPPPpipelineof33projectsthatarebeingactivelydevelopedasPPPsacross

these11countries;• Section5drawsonexperiencewithPPPintheregiontoidentifypossibleconstraintsonsuccessfuldevelopmentoftheseprojects,and

barrierstogreateruseofPPP;and• Finally,Section6setsoutconcreteactionsthatCaribbeangovernmentscantake—individually,andcollectively—tobuildsuccessfulPPP

projectsandprograms.

2Thereisnosingle,internationallyaccepteddefinitionofPPP,andthetermisoftenusedtodescribearangeofcontracttypes.Thisreportadoptsabroaddefinition,asusedintheWorldBankInstitute’s“PPPReferenceGuide,”availableonlineat:http://wbi.worldbank.org/wbi/news/2012/04/10/now-available-public-private-partnerships-reference-guide-version-10.3TheRoadmapcoversthefollowing11countries:AntiguaandBarbuda,Dominica,theDominicanRepublic,Grenada,Haiti,Jamaica,SaintKittsandNevis,SaintLucia,SaintVincentandtheGrenadines,Suriname,andTrinidadandTobago.ThesewereselectedasWorldBankGroup(WBG)clientcountriesforwhichaninitialdeskreviewprovidedprimafacieevidenceofinterestinPPP.Inpractice,severalnon-WBGclientcountriesintheregionhaveexpressedanintentiontomakegreateruseofPPP.Assuch,theRoadmapdoesnotpresentacomprehensiveoutlookforPPPacrosstheCaribbeanregion,butcouldbeconsideredtoprovidearepresentativepicture.RegionalactionspresentedintheRoadmapcouldinpracticeapplytoawidergroupofcountries.

7

RATIONALE FOR PPPS IN THE

CARIBBEAN

RATIONALE FOR PPPS IN THE CARIBBEAN

2

Rationale for PPPs in the Caribbean

Many Caribbean governments face common challenges in delivering the quality, efficient, accessible infrastructure needed to support sustainable and inclusive growth.EnergycostsinmanyCaribbeancountriesareamongthehighestintheworld,andvulnerabletooilpriceshocks.Transportservices,crucialforcompetitivenessofsmallislandnations,aretypicallyexpensive—oftenreflectingdiseconomiesofscale,butalsounder-investmentandinadequatemaintenance(exacerbatedbyexposuretonaturaldisasters),andoperatinginefficiencies.Whiletelecommunicationsmarketsarecompetitive,gapsinservicessuchashigh-speedbroadbandconstraindevelopmentofnewindustries.Mostgovernmentsareaimingtoovercomethesechallengesinthefaceoftightresourceconstraints.

Caribbean governments are increasingly turning towards partnerships with the private sector to meet these infrastructure challenges. There are two main motivations for this.First,cash-strappedCaribbeangovernmentsseePPPsasameanstocreatemore“fiscalspace”formuch-neededinfrastructureinvestment.Second,thisexigencyisaccompaniedinsomecasesbyashiftinperceptionoftheroleofgovernment—fromhistoricallystate-leddevelopmentmodelstowardsgreateremphasisonprivate-sector-ledgrowth.Inthiscontext,governmentsareinterestedingreaterprivate-sectorinvolvementinprovidinginfrastructurethroughPPPswithaviewtoachievingimprovedperformanceandefficiency,particularlyinthecontextoflimitedmanagerialresourcesinthepublicsector.BoththesemotivationsforPPPintheCaribbeanareborneouttosomeextentbyinternationalexperience.

In some cases, PPPs can mobilize additional resources for infrastructure—although certainly not always, as described further in Box 2.1 on page 9.CareisneededtoensurePPPsdonotsimplymaskthefuturecostofinfrastructureinvestments.PPPstypicallyreplaceupfrontcapitalexpenditureswithlong-termcommitmentsorcontingentliabilities,oracombinationofthetwo.Thecostofthesefiscalcommitmentsneedstobecarefullyassessedandmanaged,particularlyinthecontextoftightfiscalconstraints.WhileinternationalnormsforcapturingPPPsingovernmentaccountsarestillevolving,thereisageneraltrendtowardsrecognizingsomeorallPPPprojectsasconstitutingpublicassetsandliabilities—suchthattheimpactondebtmeasures,forexample,canbethesameunderbothaPPPandadebt-financedtraditionalpublicprocurement.

PPPs can help governments get more value out of resources spent on infrastructure.PPPscanbringprivate-sectorexperienceandinnovationtobearindeliveringinfrastructure,andprovidetherightincentivestoimproveperformance.PotentialadvantagesofPPPcaninclude:• On-time, on-budget completion of investment projects.ManypublicinfrastructureprojectsintheCaribbeangooverbudgetandare

deliveredlate.SomecountrieshavefoundPPPscanreducetheseproblems,becausetheprivatecompanyisonlypaidoncetheassetisoperational—creatingastrongincentivetodeliverontime.41

• Accountability for improved service delivery. Well-structuredPPPstypicallysetclearstandardsforserviceperformance,andfinancialpenaltiesforfailuretodelivertothesestandards.Thiscreatesclearaccountabilityandincentivesforperformancethatcanbehardtoreplicateinthepublicsector,particularlywheremanagerialresourcesareconstrained.

• Reducing whole-of-life costs.PPPstypicallyintegrateup-frontdesignandconstructionwithon-goingoperationsandmaintenanceundertheresponsibilityofoneprivatecompany(ratherthanaseriesofcontracts),creatinganincentivetodobothinawaythatminimizestotalprojectcost.IntheCaribbeantherearesignificantopportunitiestominimizewhole-of-lifecosts—suchasbydesigningmoreenergy-efficientschools,governmentofficesandwaterutilities,andbyreducingroadmaintenancecoststhroughhigher-qualityinitialconstruction.

4IntheUnitedKingdom,forexample,theNationalAuditOfficefoundin2003thatwhereas73percentoftraditionalprojectsranoverbudget,theproportionwasjust22percentforPPPprojects.Seventypercentoftraditionalprojectswerelate,whereasonly23percentofPPPswerelate.(SeeFinlay,Browne,Cham-bers,andRatcliffe,underthedirectionofRichardEales,NationalAuditOffice,2003,“PDI:ConstructionPerformanceReportbytheComptrollerandAuditorGeneral.”)SimilarresultshavebeenfoundinAustralia—seeforexample,InfrastructurePartnershipsAustralia,2007,“PerformanceofPPPsandTraditionalProcurementinAustralia.”

8

RATIONALE FOR PPPS IN THE CARIBBEAN

RATIONALE FOR PPPS IN THE CARIBBEAN

2

• Sustained maintenance and service delivery. PublicinfrastructureacrosstheCaribbeanisplaguedbyinadequatemaintenance,creatingabuild-neglect-rebuildcyclethatgreatlyincreasesthetotalcostofinfrastructureserviceprovision.PPPscanhelpcurtailthiscycle.Becausetheprivatepartneronlygetspaidiftheservicecontinuestobeprovidedatthecontractuallyspecifiedlevel,operatorsseektoensurethecontractprovidessufficientfundsformaintenanceovertheprojectlife,andthatthismaintenanceiscarriedoutinpractice.

• Increased resilience.InfrastructureprojectsintheCaribbeanareparticularlyexposedtothehighwindsandheavyrainfalloftropicalstorms—risksthatwilllikelyintensifyincomingyearsduetotheeffectsofclimatechange.Asaresult,assetsoftendeterioraterapidly.PPPscanbringinnovation,incentivesandexperienceneededtobuildresilientinfrastructureprojects.Becausetheircapitalwilltypicallyonlyberecoverediftheassetisoperating,privateinvestorswillcarefullyassessclimate-relatedrisks,andidentifyinnovativeandprovenapproachestomanagerisks.Forinstance,highwaysaremorelikelytobebuiltwithproperdrainage,andrenewableenergyinstallationswillberesistanttohurricanes.

To achieve these performance and efficiency benefits in practice, PPPs must be carefully chosen and developed.MostbenefitsofPPPrelyonprovidingtherightincentivesfortheprivatepartytobringtobearexperienceandinnovationindeliveringinfrastructurebetteroratlowercost.Theseincentivesdependonawell-structuredcontract,withclearly-identifiedperformancerequirementsandriskallocation.PPPsthereforeworklesswellwheretheoutputsrequiredaredifficulttospecifycontractuallyandmonitor—forexample,insectorswhereneedscanchangerapidly.Thepotentialadvantagesofon-timedeliveryandincreasedresilienceonlyapplyiftheprivatesectorbearstherisksassociatedwithcostoverrunsandclimate-relatedevents,respectively.

Moreover, PPPs can create their own risks.Theirrelativecomplexityraisestheriskofproblemsinthecontractingprocess—suchasfailuretoattractqualifiedbiddersifaprojectisnotwell-structured,orlegalchallengestotheprocess.Governmentscanalsobetemptedtoeschewcompetitiveprocessesandnegotiatedirectlywithpotentialinvestors—makingitdifficulttobesureaprojectisprovidinggoodvalue.Furthermore,asdescribedabove,thefiscalcostsofPPPsaretypicallylessclearthanthoseoftraditionallyprocuredprojects(beinglongterm,andoftencontingent).Governmentscanunderestimatethesecosts—leadingtounexpectedfiscalcosts,oratworst,over-specifiedprojectsthatdonotprovidegoodvalueformoney.Section5belowon“PPPconstraints”describesexamplesofsomeofthesechallengesexperiencedintheCaribbean.

Developing and managing PPP contracts successfully is therefore demanding and resource-intensive.AchievingthebenefitsandavoidingtherisksofPPPscomeatthecostofmorecomplexcontractpreparation,procurement,andmanagement—bothforthegovernmentandforbidders.Thesecostsaresomewhatfixedirrespectiveofprojectsize—meaningtheymaysimplynotbejustifiedforsmall-scaleprojects,aconstraintthatmaybiteformanypotentialCaribbeanPPPs.Governmentswillalsoneedtothinkcarefullyaboutwhetherandhowtheycanensurecapacitytodesign,procure,andmanageaPPPisinplacebeforeembarkingonaproject,asdescribedfurtherinthesectionsthatfollow.

9

RATIONALE FOR PPPS IN THE

CARIBBEAN

RATIONALE FOR PPPS IN THE CARIBBEAN

2

Forsomeprojectsandundersomecircumstances,PPPscanexpandtheresourcesavailableforinfrastructureinvestment.Specifically,PPPscanhelpmobilize:• Additional revenues. SomePPPs—suchastollroads—introducefeesthatreflectthevalueofservicesprovided;otherscan

helpreduceleakageincollectionofexistingcharges.Inprinciple,governmententitiescouldchargefeesandcollectrevenuesefficiently—inpractice,incentivestodosotendtobeweakerinthepublicsector.Privateoperatorscanalsobecreativeinfindingadditionalwaystouseafacilitytogeneraterevenue.Forexample,in2003theVancouverAirportServicesConsortiumtookoveroperationsofSangsterInternationalAirportinMontegoBay,Jamaica,undera30-yearconcession.Theconcessionairedoubledairportcapacityandcreated43newretailspacesatnocosttothepublicpurse.Retailrevenuespartiallyoffsetthecostofexpansion—increasingtherevenuestothegovernmentfromconcessionfees

• Additional capital. Sometimesgovernmentswanttofundprojects,butdonothavethecashorborrowingcapacitytofinancethecapitalexpenditure,evenwhentherevenuegeneratedfromtheinvestmentwouldexceedthecostofdebtservice.Inthesecircumstances,aPPPcanunlocktheinherentcapital-raisingabilityoftheassetinquestionbytakingitoutoftheconstrainedsphereofgovernmentfinance.Asanexample,intheearly90s,theGovernmentofGrenadawasnotabletoinvestinexpandingandimprovingelectricityassetsbecauseoffiscalconstraints.ItsoldacontrollingstakeinGRENLEC—thepowerutilityinGrenada—toaprivatecompany,whichputcapitalintothecompany,allowingittomakeneededinvestmentsinimprovingthesystem.

However,while“mobilizingresources”iscommonlygivenasakeyadvantageofPPPs,therealityishighlycase-specific.Forexample,socialinfrastructureprojectsinvolvingavailabilitypaymentsfromthegovernment(oftencalled“government-pays”projects)donotcreateanyadditionalfundingtopayforinfrastructure.Suchprojectsmaytakeupless“fiscalspace”intheshorttermbyturninganupfrontcapitalexpenditureintoalong-termpaymentcommitment,butultimatelythecostoftheinvestmentisbeingmetfromthepublicpurseeitherway.

Moreover,suchprojectsmaynotreallymobilizemorecapitalthanthegovernmentcouldsimplybyborrowing—inbothcases,financiersarelookingtothefiscalcapacityofthegovernment,toservicedebt,ormakeavailabilitypaymentsovertime.SuchPPPsmaymakesense,iftheyreducecostsorincreaseassetutilizationcomparedtoconventionalprocurement;carefulassessmentisneededofaffordabilityandtherationaleforPPP.

WhereaPPPhasitsownrevenuestream(“user-pays”projects),thereisagreaterlikelihoodthataPPPapproachmaytrulymobilizeadditionalcapitalbeyondwhatthepublicsectorwouldbeabletoprovide,particularlyintheborrowing-constrainedcontextoftheCaribbean.Nonetheless,suchprojectsoftencreatecontingentliabilities,intheformofguaranteesorcontractualclausesunderwhichthegovernmentbearssomerisk.Particularlyinthecontextofhighindebtedness,thepossiblecostsandsustainabilityofacceptingtheseliabilitiesneedstobeassessedandmonitored.

WhileinternationalnormsforcapturingPPPsinpublicaccountsandnationalstatisticsarestillevolving,thereisageneraltrendtowardsrecognizingPPPprojectsascreatingpublicassetsandliabilities—particularlyfor“government-pays,”butalsoinsomecasesfor“user-pays”PPPs.Thismeanstheimpactonnationaldebt,forexample,maybethesameunderaPPPandadebt-financedtraditionalprocurement.ForCaribbeancountriesunderInternationalMonetaryFund(IMF)programs,thetreatmentofPPPliabilitiesunderprogramtargets—todatedefinedonacountry-by-countrybasis,butincreasinglyrequiringrecognitionofsomeorallPPPproject-relatedliabilities—willbeimportantindelineatingthefiscalspaceavailableforinvestmentthroughPPPs.

Box 2.1: PPPs and “Fiscal Space”

10

CARIBBEAN EXPERIENCE WITH PPP

CARIBBEAN EXPERIENCE WITH PPP

3

Caribbean Experience with PPP

Private investment in infrastructure is not new in the Caribbean.Inthelast20years,privateinfrastructurecompaniesandlendershaveinvestedmorethanUSD8.5billionininfrastructureassetsinthe11countriesincludedinthisstudy,withtheDominicanRepublicandJamaicatheleadingdestinationsforinvestment.Thiscomprisesanannualaverageofabout0.7percentofGDPforthese11countriesoverthepast20years,comparedtoanannualaverageof1.2percentofGDPfortheLatinAmericaandCaribbeanregionasawholeoverthesameperiod.AsshowninFigure3.1,thisinvestmenthasbeenconcentratedinthetelecommunicationsandelectricitysectors;attheotherendofthespectrum,therehasbeenrelativelylimitedinterestinattractingprivateinvestmentinthewatersector.

Figure 3.1: Private Infrastructure Investment Experience in the Caribbean

Source: Authors, drawing from Castalia research and World Bank PPI Database

All the countries included in the Roadmap have attracted private infrastructure investment, although most commonly through structures other than PPPs.Thesehaveincludedprivatizationsofpublicutilities,regulatedgreen-fieldprivateinvestments—particularlyinthetelecommunicationssector,whichhasbeenliberalizedinmostCaribbeancountries—andafewjointventures.Thissuggeststhatfortherightprojects,theCaribbeanisanattractiveinvestmentdestination.However,PPPexperienceisrelativelylimited—ofthe95infrastructureinvestmentprojectsrecordedinthese11countries,fewerthanhalfwerethroughsomeformofPPP.

The use of PPPs has been more concentrated by both country and sector, as shown in Figure 3.2 below.MorethanhalfofcurrentPPPprojectsinthecountriesandsectorscoveredbythisRoadmapareintheDominicanRepublic,andonlysevenofthe11countrieshavemadeuseofthePPPmodalityforcoreinfrastructure.51Electricityandtransportsectorprojectsdominate,primarilycomprisinginvestmentsinelectricitygenerationbyindependentpowerproducers(IPPs),andPPPsforrehabilitation,upgrade,orafewnewinvestmentsinroads,ports,andairports.AhandfulofwatercontractsincludeexperimentswithtechnicalassistanceandleasecontractsinHaiti,aswellasfourbulkwatertreatmentplantselsewhere.Noneoftheprivateinvestmentininformationandcommunicationstechnology(ICT)hastodatebeenunderaPPPstructure.AppendixAprovidesalistofthesepreviousPPPs;CaribbeanPPPexperiencebysectorisalsodescribedfurtherinSection4.

5AfewadditionalexamplesinothersectorsincludegovernmentbuildingsinSaintLuciaandTrinidadandTobago.

11

CARIBBEAN EXPERIENCE WITH PPP

CARIBBEAN EXPERIENCE WITH PPP

3

Figure 3.2: PPP Project Experience in the Caribbean

Source: Authors, drawing from Castalia research and World Bank PPI Database

The results of previous PPP experience in the Caribbean have been mixed.WhiledefiningsuccessforaPPPisnotstraightforward—seeBox3.1below—thereareseveralPPPprojectsintheCaribbeanthatcouldreasonablybeconsideredsuccessful.ThesePPPprojectshaveoperatedforyears,providingquality,reliableinfrastructureassetsandservicesatareasonablecost,andoftenwithoutattractingmuchattention.Theseinclude,forexample,Suralco,theCaribbean’soldestPPP—a185MWhydroplantbuiltbyAlcoaAluminumin1958,whichcontinuestosupplyupto60percentofSuriname’selectricityundera75-yearpowerpurchaseagreement(PPA).Atamuchsmallerscale,WindWattNevis,amicro-generatorwithaninstalledcapacityof2.2MW(equivalentto20percentofNevis’demandforelectricity),commencedoperationsin2010undera25-yearPPAandhasoperatedreliablysince.

Box 3.1: Defining PPP Success

WhatdoesitmeantosaythataPPPissuccessful?Inpractice,thismaydependonthenatureoftheproject,andwhatwastherationaleorexpectedbenefitsfromdeliveringtheprojectasaPPP.Ingeneral,asuccessfulPPPcouldbedefinedasoneinwhichtheassetand/orserviceprovidedbytheprivatepartymeetsitsobjectivesovertheprojectlifetime,anddoessoinawaythatprovidesbettervalueformoneytothegovernmentandserviceusersthanthealternatives.

AssessingthesuccessofaPPPinmeetingitsobjectivesisrelativelystraightforward—albeitonlyultimatelypossibleoncethecontractisconcluded.Forexample,thiscouldincludeconsideringwhether:constructionorrehabilitationwascompletedontime;thePPPassetorassetsarecontinuouslyavailableattherequiredstandards;anticipatedserviceperformancelevelsorimprovements(forconcessionsofexistingassets)materializeandaresustained;andtheassetorservicecontinuestocontributetomeetinggovernmentobjectivesinthesectorinquestionoverthecontractlifetime.

AssessingthesuccessofaPPPinprovidingvalueformoneyisharder,becausedirectcomparatorsarerarelyavailable.Nonethelessitispossibletoassesssomeindicatorsofsuccess.Forexample,aPPPthatendsupcostingthegovernmentmorethanexpected(thatis,wherecontingentliabilitiesrealize)maybeconsideredunsuccessfulindeliveringvalueformoney.Itisalsopossibletoassesswhetherconditionsconducivetoachievingvalueformoneywereinplace—forexample,whetherthetransactionprocesswastransparentandcompetitive.

12

CARIBBEAN EXPERIENCE WITH PPP

CARIBBEAN EXPERIENCE WITH PPP

3

Not all Caribbean PPPs have achieved sustained success.Problemshaveincludedunexpectedfiscalcosts,questionablevalueformoney,andsignificantimplementationdelays—whilemanyadditionalpotentialPPPprojectshavesimplyfailedtolaunch.ThesechallengesaredescribedinmoredetailinSection5below,whichlooksattheconstraintsonthesuccessfuluseofPPPintheregion.

None of the existing Caribbean PPPs was implemented under an overarching PPP policy or legal framework.AsshowninFigure3.3,afewgovernmentshavesincebeguntodevelopspecificpolicyandinstitutional“architecture”toguidetheuseofPPPs.JamaicaandTrinidadandTobagobothintroducedPPPpoliciesin2012,establishingguidingprinciples,criteria,processes,androlesformanagingtheirPPPprograms.BothhavealsocreateddedicatedPPPteams—inJamaicathesecompriseaPPPUnitintheDevelopmentBankofJamaica(DBJ)andaPPPNodeintheMinistryofFinanceandPlanning;inTrinidadandTobago,aPPPUnitintheMinistryofFinance.APPPUnitwasalsoestablishedinHaiti’sFinanceMinistryin2012,althoughwithoutaguidingpolicy,theroleandmandateofthisunitremainssomewhatunclear.

Caribbean countries still lack institutional capacity to develop and implement PPPs. GiventhelimitedPPPprojectexperienceoutsidetheDominicanRepublic,relativelyfewgovernmentshavestaffwithexperienceimplementingPPPs.Moreover,wheresuchexperiencedoesexist,itisforthemostpartdistributedamongresponsiblegovernmententities.InJamaica,TrinidadandTobago,andHaiti,effortsareunderwaytoconsolidateandbuildexpertiseindedicatedPPPteams—inthecaseofJamaica,withthebenefitofbuildingonanexistingprivatizationteamatDBJ.DespitethelackofinternalPPPcapacity,governmentshavealsoprovedreluctanttoconsistentlyallocatesufficientfundingtocoverthecosts(whichcanbesignificant)ofexperiencedexternaladvisorysupportneededtopreparehigh-qualityPPPprojects.

Figure 3.3: PPP Policy and Institutional Architecture in the Caribbean

4Inplace(date)6 AbsentLowModerateHigh;DevelopmentBankofJamaica(DBJ);MinistryofFinance(MOF)Source: Authors, based on Castalia and World Bank research

Policy Law Detailed Guidelines Defined Roles

Dedicated Units(s)

Staff with PPP Experience

Dedicated Project Prep Funding

Jamaica 4(2012)

6 Underway 44

(DBJ&MOF)6

Trinidad & Tobago

4(2012)

6 Underway 44

(MOF)6

Dominican Republic 6 6 6 6 6 6

Haiti 6 6 6 64

(MOF)6

Suriname 6 6 6 6 6 6

OEC States 6 6 6 6 6 6

13

EMERGING PPP OPPORTUNITIES

EMERGING PPP OPPORTUNITIES

4

Emerging PPP Opportunities

A ramp-up of PPP activity in infrastructure is planned across much of the Caribbean. Asdescribedinsection2,thedriversofinterestinPPPsvary.Insomecasesthistrendreflectsashiftintheperceivedroleofgovernment,andthepotentialefficiencyandperformancebenefitsofengagingtheprivatesectorininfrastructuredelivery.However,aprimarydrivingconcerninalmostallcasesisthepressingneedforinvestmentinthecontextoftightfiscalconstraints.SincetheabilityofPPPstogenuinelyincreasetheresourcesavailableforinfrastructurevariesbyproject—asdescribedinBox2.1above—thisfiscalimperativeisreflectedinthetypesofPPPsthatarelikelytobesuccessfulacrossmuchoftheCaribbeanintheshorttomediumterm.

The PPP Roadmap identified a potential PPP pipeline of 33 projects being considered or developed as PPPs across 11 Caribbean countries, with a total investment value of more than USD 2 billion.TheprocessandcriteriaforidentifyingthispipelinearedescribedinBox4.1.Broadlyspeaking,theseareprojectsthatareactivelyunderdevelopment—albeitinmanycasesatanearlystage—and,frominitialassessmentbasedonexperienceandavailableinformation,appearviableandimplementableasPPPsinthenearterm.Assuch,thispipelineprovidesareasonableestimateofthepotentialforPPPintheCaribbeaninthenexttwotofiveyears.

Box 4.1: How the PPP Pipeline Projects were Identified

This pipeline represents a significant planned increase in the use of PPP in several countries,asshowninFigure4.1:notably,Jamaica,TrinidadandTobago,Suriname,andsomeOrganizationofEasternCaribbeanStates(OECS)membercountriessuchasSaintLuciaandGrenada.JamaicaandTrinidadandTobagotogethercomprisealmosthalfofthePPPpipelinebynumberofprojects.Theapproximatetotalinvestmentvaluerepresentedbythispipeline,ofmorethanUSD2billion,wouldcomprisearoundtwopercentofGDPinthese11countries;orfourpercentofGDPexcludingtheDominicanRepublic,wherenosufficientlyfirmpipelineprojectswerefound.

FewgovernmentsintheCaribbeanhavewhatcouldbecalleda“PPPpipeline.”BothJamaicaandTrinidadandTobagoareestablishingaprogrammaticapproachtoPPP,whichhasinvolvedsystematicallyscreeningpotentialPPPprojects.Inthesecases,thepipelinepresentedinthisreportisbasedonconsultationwiththeresponsibleofficials,andcapturesthepipelineprojectsthatareinactivepreparation.Intheremainingninecountries,thepipelinepresentedherewasdevelopedforthisroadmap.AwidersetofpotentialPPPswasidentifiedthroughacombinationofdeskresearch,meetingswithgovernmentofficials,privateinvestorsanddevelopmentpartners;andreviewofanyavailableprojectdocumentation.Thesewerescreenedagainstthefollowingcriteria,basedonexperienceand(limited)availabledata:• Prima facie assessment of technical and economic viability of the project—theprojectwoulduseproventechnologytoaddressa

clearly-identifiedserviceneedthatisinlinewithdevelopmentandpublicinvestmentpriorities.• Prima facie assessment of viability as a PPP—thePPPwouldfollowestablishedcontractualmodels,andislikelytogeneratea

revenuestreamthatwouldmaketheprojectfinanciallyviableandattractivetoinvestors.WherethePPPwouldinvolvegovernmentpayments,theseappearaffordablegivenfiscalconstraints.

• Political supportforimplementingtheprojectasaPPP.• Project readinessandfeasibilityofimplementationwithinareasonabletimeframe.Forexample,projectstudiesarealreadyunder-

wayorcompleted;andnomajorsectororotherreformsareneededaspre-requisitesforpursuingaPPP.

Theresultantpipelineisfarfromexhaustive,sinceithasnotarisenfromasystematicreviewofgovernmentinvestmentprioritiestoidentifyprojectsthatcouldoffermorevalueasPPP.Ontheotherhand,giventheearlystageofdevelopmentofmanyoftheprojects,thereislikelytobeattritionfromthispipelinewherefurtheranalysisrevealsthatsomeprojectsorPPPsarenotviableinpractice.

14

EMERGING PPP OPPORTUNITIES

EMERGING PPP OPPORTUNITIES

4

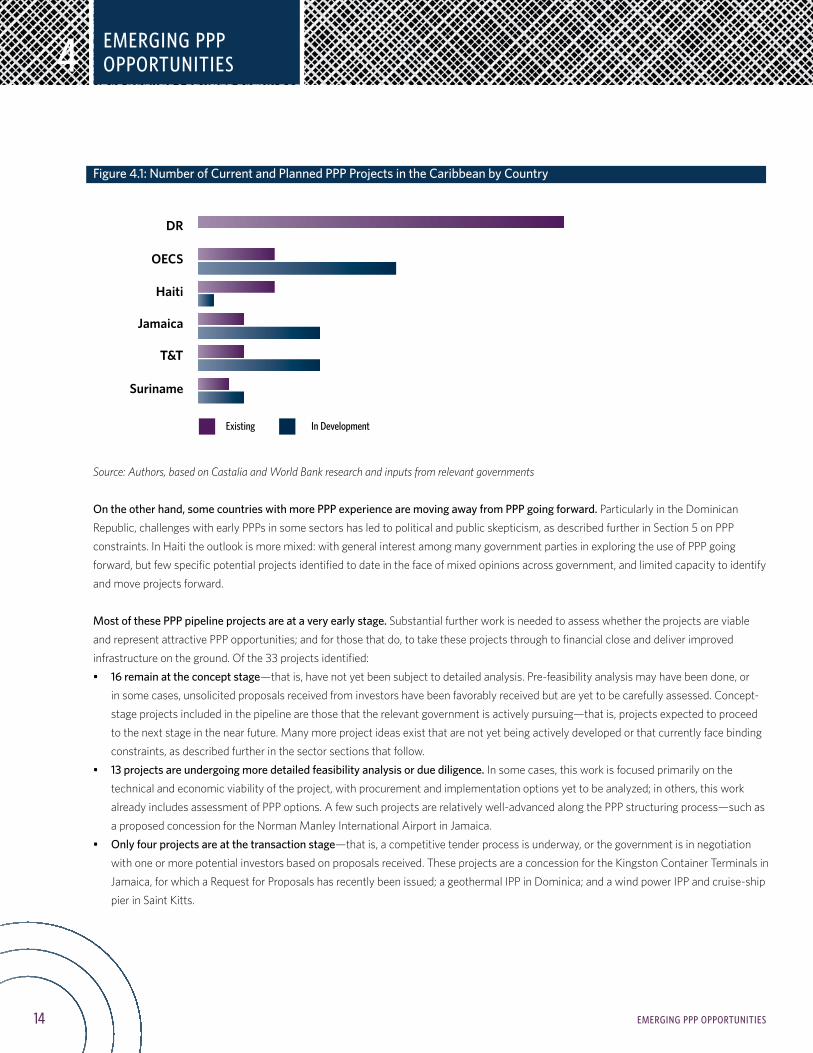

Figure 4.1: Number of Current and Planned PPP Projects in the Caribbean by Country

Source: Authors, based on Castalia and World Bank research and inputs from relevant governments

On the other hand, some countries with more PPP experience are moving away from PPP going forward.ParticularlyintheDominicanRepublic,challengeswithearlyPPPsinsomesectorshasledtopoliticalandpublicskepticism,asdescribedfurtherinSection5onPPPconstraints.InHaititheoutlookismoremixed:withgeneralinterestamongmanygovernmentpartiesinexploringtheuseofPPPgoingforward,butfewspecificpotentialprojectsidentifiedtodateinthefaceofmixedopinionsacrossgovernment,andlimitedcapacitytoidentifyandmoveprojectsforward.

Most of these PPP pipeline projects are at a very early stage. SubstantialfurtherworkisneededtoassesswhethertheprojectsareviableandrepresentattractivePPPopportunities;andforthosethatdo,totaketheseprojectsthroughtofinancialcloseanddeliverimprovedinfrastructureontheground.Ofthe33projectsidentified:• 16 remain at the concept stage—thatis,havenotyetbeensubjecttodetailedanalysis.Pre-feasibilityanalysismayhavebeendone,or

insomecases,unsolicitedproposalsreceivedfrominvestorshavebeenfavorablyreceivedbutareyettobecarefullyassessed.Concept-stageprojectsincludedinthepipelinearethosethattherelevantgovernmentisactivelypursuing—thatis,projectsexpectedtoproceedtothenextstageinthenearfuture.Manymoreprojectideasexistthatarenotyetbeingactivelydevelopedorthatcurrentlyfacebindingconstraints,asdescribedfurtherinthesectorsectionsthatfollow.

• 13 projects are undergoing more detailed feasibility analysis or due diligence.Insomecases,thisworkisfocusedprimarilyonthetechnicalandeconomicviabilityoftheproject,withprocurementandimplementationoptionsyettobeanalyzed;inothers,thisworkalreadyincludesassessmentofPPPoptions.Afewsuchprojectsarerelativelywell-advancedalongthePPPstructuringprocess—suchasaproposedconcessionfortheNormanManleyInternationalAirportinJamaica.

• Only four projects are at the transaction stage—thatis,acompetitivetenderprocessisunderway,orthegovernmentisinnegotiationwithoneormorepotentialinvestorsbasedonproposalsreceived.TheseprojectsareaconcessionfortheKingstonContainerTerminalsinJamaica,forwhichaRequestforProposalshasrecentlybeenissued;ageothermalIPPinDominica;andawindpowerIPPandcruise-shippierinSaintKitts.

15

EMERGING PPP OPPORTUNITIES

EMERGING PPP OPPORTUNITIES

4

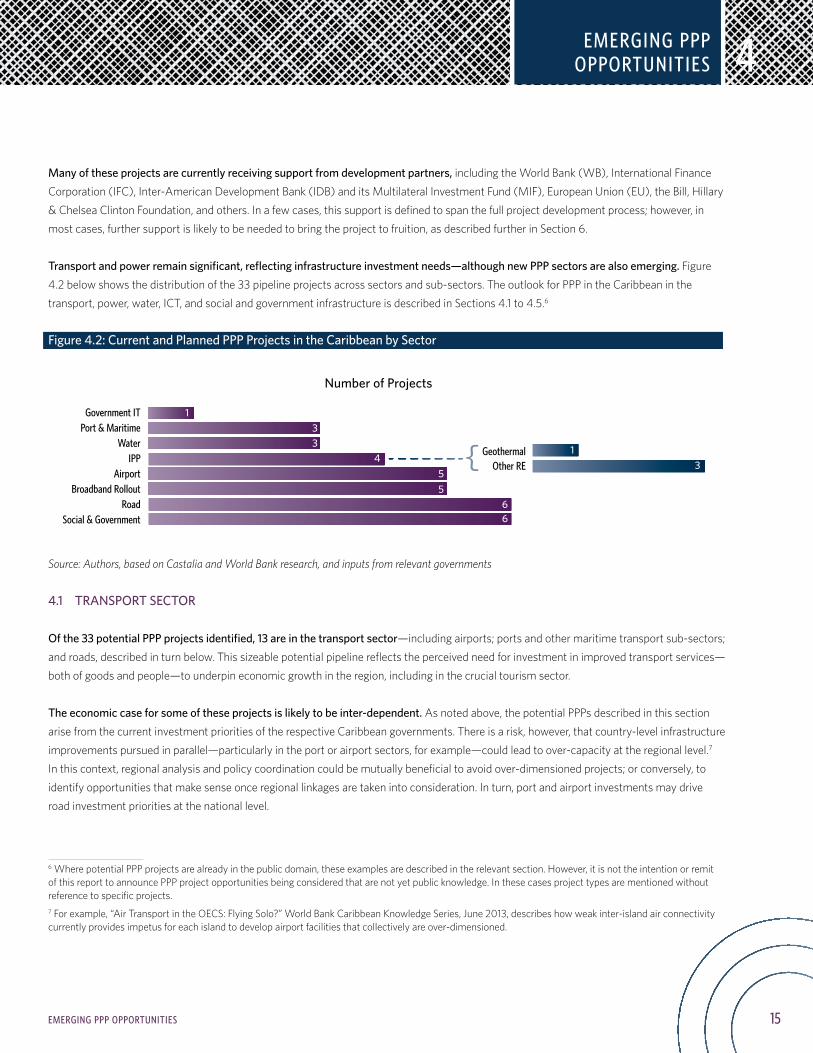

Many of these projects are currently receiving support from development partners,includingtheWorldBank(WB),InternationalFinanceCorporation(IFC),Inter-AmericanDevelopmentBank(IDB)anditsMultilateralInvestmentFund(MIF),EuropeanUnion(EU),theBill,Hillary&ChelseaClintonFoundation,andothers.Inafewcases,thissupportisdefinedtospanthefullprojectdevelopmentprocess;however,inmostcases,furthersupportislikelytobeneededtobringtheprojecttofruition,asdescribedfurtherinSection6.

Transport and power remain significant, reflecting infrastructure investment needs—although new PPP sectors are also emerging.Figure4.2belowshowsthedistributionofthe33pipelineprojectsacrosssectorsandsub-sectors.TheoutlookforPPPintheCaribbeaninthetransport,power,water,ICT,andsocialandgovernmentinfrastructureisdescribedinSections4.1to4.5.6

Figure 4.2: Current and Planned PPP Projects in the Caribbean by Sector

Source: Authors, based on Castalia and World Bank research, and inputs from relevant governments

4.1 TRANSPORT SECTOR

Of the 33 potential PPP projects identified, 13 are in the transport sector—includingairports;portsandothermaritimetransportsub-sectors;androads,describedinturnbelow.Thissizeablepotentialpipelinereflectstheperceivedneedforinvestmentinimprovedtransportservices—bothofgoodsandpeople—tounderpineconomicgrowthintheregion,includinginthecrucialtourismsector.

The economic case for some of these projects is likely to be inter-dependent.Asnotedabove,thepotentialPPPsdescribedinthissectionarisefromthecurrentinvestmentprioritiesoftherespectiveCaribbeangovernments.Thereisarisk,however,thatcountry-levelinfrastructureimprovementspursuedinparallel—particularlyintheportorairportsectors,forexample—couldleadtoover-capacityattheregionallevel.7 Inthiscontext,regionalanalysisandpolicycoordinationcouldbemutuallybeneficialtoavoidover-dimensionedprojects;orconversely,toidentifyopportunitiesthatmakesenseonceregionallinkagesaretakenintoconsideration.Inturn,portandairportinvestmentsmaydriveroadinvestmentprioritiesatthenationallevel.

6WherepotentialPPPprojectsarealreadyinthepublicdomain,theseexamplesaredescribedintherelevantsection.However,itisnottheintentionorremitofthisreporttoannouncePPPprojectopportunitiesbeingconsideredthatarenotyetpublicknowledge.Inthesecasesprojecttypesarementionedwithoutreferencetospecificprojects.7Forexample,“AirTransportintheOECS:FlyingSolo?”WorldBankCaribbeanKnowledgeSeries,June2013,describeshowweakinter-islandairconnectivitycurrentlyprovidesimpetusforeachislandtodevelopairportfacilitiesthatcollectivelyareover-dimensioned.

16

EMERGING PPP OPPORTUNITIES

EMERGING PPP OPPORTUNITIES

4

4.1.1 AIRPORTS

Virtually all governments in the region want to develop first-class airport facilities—toimproveconnectivityandsupporteconomicgrowth,inparticularpromotingtourism,aswellasforreasonsofnationalprestige.AirportrehabilitationorexpansionprojectscanbegoodcandidatesforPPPs—asstand-aloneassetswithserviceobligationsthatcanbeclearlydefined;withrevenuestreamsthataretypicallysufficienttocoveroperatingandcapitalcosts;theopportunitytocreatevaluethroughbetterconsumerservices,suchasincreasedretailfacilities;andwithawell-establishedPPPmarket,particularlyinEuropeandLatinAmerica.The Caribbean has already seen several successful airport PPPs, reflecting international experiences. JamaicasetaprecedentforprivateparticipationintheairportsectorintheCaribbean,withasuccessfulPPPforitslargestairport,SangsterInternationalatMontegoBay.Underthisconcessionsince2003,airportcapacityhasdoubled,and43newretailspaceshavebeenadded,amongothersystemimprovements.TheDominicanRepublichasaconcessionagreementwithaprivateoperatorinplacesforsixairports—alargelysuccessfulPPPinacountrywherePPPexperienceoverallhasbeenmixed.PuertoRicoalsorecentlyintroducedaconcessionforitsmainairportatSanJuan.

Building on this experience, there is strong interest in additional airport PPPs in the region going forward, with five such projects included in the pipeline of 33 potential PPPs.TheGovernmentofJamaicaiscurrentlypreparingaconcessionforitssecondinternationalairport,theNormanManleyInternationalAirportinKingston.FouradditionalairportconcessionsareunderconsiderationinthecountriescoveredbythisRoadmap.AllappeartoholdthepotentialtobeviableasPPPs,althoughallareatarelativelyearlystage,withfurtherassessmentneededofeconomicandfinancialviability.Asnotedabove,analysisofneedsattheregionallevelcouldhelpavoidcreatingexcesscapacitythatcouldunderminethesuccessofindividualprojects.

Scale limitations may limit the potential for substantial further PPP development in the sector beyond these near-term opportunities.Thesmallsizeofmanyairportsintheregionmeanstheysufferfromdiseconomiesofscale—suchthatexpansionsorupgradesmaynotbefinanciallyviable,evenifeconomicallybeneficial—andmaybetoosmalltoattractinterestfromexperiencedinvestorswithoutprovidingsubstantialincentives(whichmaynotresultinvalueformoneyforthegovernment).Thischallengecaninsomecasesbeovercomebybundling—forexample,thesixairportsintheDominicanRepublicareunderprivateoperationunderonemasterconcessioncontract—butsuchopportunitieswithinCaribbeancountriesarelimited.

Moreover, in some countries, political and public opposition to private operation of airports persists.Airportsaresometimesseenasstrategicassetsthatgovernmentsprefertoretainunderpubliccontrol,particularlyinsmallcountrieswithonlyonesignificantairportfacility.ProjectsthatcouldmakeattractivePPPs—suchasaconcessionforthePortauPrinceairportinHaiti,whereinvestmentneedsarecombinedwithsignificantpassengerflows—areunlikelytoprogressinthefaceoflimitedpoliticalinterest.ThisdynamicmaychangeovertimeastheregionbuildsexperiencewithairportPPPs.

4.1.2 PORTS

The Caribbean port sector consists of facilities of vastly differing sizes and traffic levels, from1.9millionTEUs(standardcontainers)peryearinJamaicatojust19,000TEUsperyearinDominica.Theseportsfaceconcomitantlydifferingchallenges.Largerportswithsignificantglobaltrans-shipmentbusinessarepreparingfortheforthcomingexpansionofthePanamaCanal—whichinmostcaseswillrequireinvestmenttoenableportstohandlelargerships.Formid-sizeandsmallerportsservingprimarilyintra-regionalanddomestictraffic,theprimarychallengeislowefficiency,whichresultsinhighportchargesandimport/exportcosts.Whilediseconomiesofscaleareinevitableinmanycases,thesearetypicallyexacerbatedbyahistoryofunder-investmentandoperatinginefficiencies—particularly,ofhighstaffinglevels.

17

EMERGING PPP OPPORTUNITIES

EMERGING PPP OPPORTUNITIES

4

Most Caribbean ports remain publicly owned and controlled—in contrast with global trends.Globally,manygovernmentshaveturnedtotheprivatesectortoundertakeportinvestmentandimproveoperationalperformance.Amajorityofportsworldwidearenowunderprivateownershiporcontrol—whetherasfullyprivateentities,orundersometypeofPPP.Incontrast,onlyafewCaribbeancountrieshaveadoptedportPPPstructuresthatinvolvesignificantinvestmentorriskforaprivateoperator—althoughmosthavesomelevelofprivateprovisionofportservices(suchascargohandlingorstevedoring)withinportsthatarepubliclyownedandrun.IntheDominicanRepublic,severalportsareoperatedunderconcessioncontracts,whileonesuchconcessionisinplaceinSurinameforthePortofNieuweHaven.

Going forward, a handful of the Caribbean governments included in this Roadmap are considering port PPPs.PrincipalamongtheseistheGovernmentofJamaica,whichiscurrentlyseekingaprivateportoperatorunderaconcessionarrangementfortheKingstonContainerTerminals(thelargestportintheregion);severalfullyprivateportinvestmentsarealsounderconsiderationaspartofthegovernment’s“LogisticsHub”initiative.Thepipelineof33potentialPPPsincludesonlyoneotherpotentialportprojectthatisunderactiveconsiderationbytherelevantgovernment.

Elsewhere the port sector remains largely in public hands for a combination of reasons, which appear unlikely to change in the immediate future.Primarily,thereappearstobelimitedpoliticalwillinsomecasestocedeportoperationstoprivateinterests,givenwidespreadpoliticalandpublicperceptionthatportsarestrategicassets.TheseviewsmaychangeovertimeasmorePPPportsintheregionareintroducedandaresuccessful.Portreformcanbeespeciallypoliticallychallengingincaseswhereover-staffingisamajorcauseofinefficiencythataprivateoperatorwouldlikelyseektoresolve,particularlygivenastrongunionpresenceinseveralcountries.Finally,asfortheairportsectorasdescribedabove,someofthesmallerportsintheregionaresimplyofaverysmallscale,makingattractingprivateoperatorsdifficult.

4.1.3 OTHER MARITIME TRANSPORT

The outlook for the cruise ship industry in the Caribbean appears bright.AccordingtotheCruiseLinesInternationalAssociation,moderategrowthinglobalcruisepassengernumbersisexpectedin2014,whiletheCaribbeanisexpectedtoextenditsleadasthedominantcruisedestination,witha12percentincreaseincruiseshipdeploymentstotheregion.8 However,thetrendintheindustryistowardslargercruiseships,withthenewgenerationofshipscapableofaccommodatingupwardsof5,000passengers.ManyCaribbeandestinations,althoughpopularwithcruiselines,donothaveadequateberthingandancillaryfacilitiesfortheexpectedincreasesinpassengerarrivals.

Several Caribbean countries have turned to PPPs to develop new cruise ship pier facilities—withsuccessfulprojectsinJamaica,Grenada,andHaiti.CruiseshippierscanmakeattractivePPPs—asstand-aloneassets,withreliablerevenuestreamswithplentyofroomtoaddvaluebyimprovingcustomerservices.Insomecasesinvestorsarecruiseshiplinesseekingtocapitalizeonsynergiesbetweencruiseandpieroperations—suchastheHaitiLabadiePier,andJamaica’snewFalmouthcruiseshippier,bothoperatedbyRoyalCaribbeanCruises.

Several more countries are considering private investment in cruise ship piers under PPPs or similar structures.Onesuchpipelineprojectiswelladvanced:asecondcruiseshippierinSaintKittsandNevis,expectedtoaccommodateupto200,000passengersinitsfirstyear.InSeptember2013,thegovernmentsigneda30-yearconcessionagreementwithmarineconstructioncompanyJayCashman,followingaMemorandumofUnderstandingsignedinMay.Undertheagreement,alocalsubsidiarywillbeestablishedtodesign,finance,build,andmaintainthepier.ThepierwillthenbeleasedbacktotheAirandSeaportsAuthority(SCASPA),whichwillberesponsibleforoperations.Theprojectisnowpursuingfinancialclose,withthefirstcruiseshipexpectedtodockinOctober2014.Basedontheroadmapdiscussions,severalmorecountriesareconsideringenteringintoPPPorsimilararrangementsforcruiseshippiers,butareattooearlyastageforthesetobeconsideredaspipelineprojects.

8CruiseLinesInternationalAssociation“StateoftheCruiseIndustryin2014,”www.cruising.org.

18

EMERGING PPP OPPORTUNITIES

EMERGING PPP OPPORTUNITIES

4

Another possible area of interest for PPP is in the ferry sector. FerrytransportiscommonbetweenislandsintheCaribbean,andistypicallyfullyprivatelyoperated,underregulationbymaritimeauthorities(thatis,notunderPPPstructures).However,PPPscanberelevantwhereferryprojectsinvolveasignificantinvestmentinland-sideinfrastructure—potentiallyrequiringgovernmentsupport,orrequiringalong-terminvestmentforwhichspecificationofrightsandobligationsofpublicandprivatepartiesisbeneficial.ThiswouldbethecasefortheonepotentialferryPPPprojectincludedinthepipeline,albeitatanearlystageofdevelopment—aproposedfootandvehiclepassengerferryinHaiti,forwhichwharfandterminalfacilitieswouldalsobeneeded.

Given the high cost of intra-regional travel—with air travel the only option on many routes—further development of the ferry sector appears attractive,whetherthroughPPPsorfully-privateregulatedstructures.Forseveralyears,therehavebeendiscussionsandplanstolauncharegionalfastferry,asdescribedinBox4.2.However,theseplanshavenotcometofruition.Thisisanexampleofthechallengesinachievingtheregionalcooperationrequiredtomoveforwardwithprojectsthatcouldbemutuallybeneficial,butlackanobviousprojectchampion.

Box 4.2: The Challenges of Regional Projects: OECS Regional Fast Ferry

4.1.4 ROADS

The vast majority of roads in the Caribbean are publicly run, and free to users.Theonlycountrieswithprivately-runtollroads,operatedunderconcessioncontracts,areJamaicaandtheDominicanRepublic.ThesePPPshavebeenamongthemostdifficult,intermsofriskallocationandunforeseenfiscalcosts.Forexample,theDominicanRepublichasfourexistingroadPPPs,allofwhichhavecreatedunexpectedfiscalcoststothegovernment—inthefaceofthisexperience,thegovernmentdoesnotcurrentlyintendtopursuefurthertoll-roadPPPs.Nonetheless,twogovernmentsareactivelyconsideringintroducingtoll-roadPPPprojects,andtwosuchprojectsarethereforeincludedinthepipeline.Theseprojectswillneedtobecarefullyassessedanddevelopedtoavoidthesamepitfalls.GiventhelowleveloftrafficinmostCaribbeancountries,andlimitedpoliticalinterestinchargingroadtolls,therearelikelytobeverylimitedopportunitiesfor“self-financing”toll-roadPPPs—thatis,tollroadsthatarefinanciallyviablebasedontollrevenue,withoutgovernmentsubsidies.

Road sector PPPs do not have to be fully “self-financing” toll roads.Otheroptionsincludecontractsbasedon“shadowtolls”oravailabilitypayments,underwhichprivatecontractorsbuildorrehabilitatearoad,andmaintainittoaspecifiedqualityoverthecontractlifetime.Suchcontractscanhelpgetthemostvalueoutofpublicinvestmentintheroadsector—forexample,overcomingproblemswithunder-maintenancethatarecommontheCaribbean,bypre-committingtoadequatemaintenanceoverthecontractlifetime.ThesePPPscanalsoincentivizeandprovideroomforinnovationinconstructionthatimprovesresilience,includingtoclimate-relatedrisks(providedthecontractisstructuredsuchthatthecostofsuchrisksisbornebytheconcessionaire)—suchasroaddrainagesystemsthatreducetheimpactofstormrainfall.

FastferryservicesarecommoninmanyarchipelagosofsimilarsizetotheOECS,suchasregionsintheMediterraneanandnorthernEurope.Aregionalfastferryservicecouldpotentiallyprovidecheapertravelthanairservice.Whilesuchaprojectcouldbelargelyprivatelyimplemented,regionalgovernmentswouldberequiredtograntlicenses,regulatesafety,andpossiblyregulatethetariffsoftheprivateoperator(s).

Aprivately-operatedregionalferryservicehasbeendiscussedamongregionalgovernmentsformanyyears,buthasyettocometofruition.Themostrecentinitiativefounderedin2008-09,whenoneoftheseveralgovernmentsinvolveddeclinedtocertifytheproposedvesselsasseaworthy.Thisillustratestheinherentdifficultiesofnegotiatingprojectsamongmultiplegovernments,whichmayhaveconflictinginterestsandfiscalobjectives.NoneoftheninegovernmentsinterviewedforthisstudymentionedthefastferryasapotentialPPPproject.

19

EMERGING PPP OPPORTUNITIES

EMERGING PPP OPPORTUNITIES

4

A few Caribbean governments have started to transition towards performance-based PPP road contracts.Forexample,theGovernmentsofSurinameandSaintLuciahavebothusedaformofthisarrangementinwhichtheroadisguaranteedoverathree-yearperiod.Goingforward,afewgovernmentsarenowlookingatlonger-termperformance-basedroadPPPcontracts,whereintheprivateoperatorwouldtakeonagreaterdegreeofrisk—foursuchprojectsareincludedinthe33pipelineprojects;allatanearlystage.Aspublicly-fundedprojects,thescopeforsignificantadditionalPPPsinthisareanaturallydependsonthepriorityaffordedtoroadinvestmentbygovernmentsoperatingundersignificantfiscalconstraints.

4.2 ELECTRICITY SECTOR

Electricity prices in many Caribbean countries are among the highest in the world,andasignificantconstraintoncompetitivenessandgrowth9 WhilemanyofthecountriescoveredbythisRoadmaphavehighlevelsofenergyaccessandrelativelyreliablesupply,asshowninTable4.1below,loweringthecostofpowerbydiversifyinggenerationsourcesawayfromexpensivedieselpowerisapriority.HaitiandtheDominicanRepublicareexceptions,inthatexpandingaccess(intheformer)andachievingsufficientgenerationcapacitytoensurereliablesupplyremainchallenges.

Table 4.1: Electricity Sector—Structure and Performance

Source: Authors, drawing on Castalia research using Annual Reports of each Utility; access estimates for 2010 from World Bank Sustainable Energy for All database

9Forexample,theWorldBankGroup’sEnterpriseSurveysidentifyelectricityasoneofthemostseriousconstraintstobusinesssuccessinseveralCaribbeancountries;formoredetailsseewww.enterprisesurveys.org.

Country Private Utility IPPs Independent Regulator Access (%) Peak Demand/

Capacity (%)% from Diesel

Average Retail Tariff (US$/kWh)

A&B 4 88% 60% 100% N/a

Dominica 4 91% 63% 75% 0.43

DR 4 4 98% N/a 53% 0.20

Grenada 4 88% 59% 100% 0.40

Jamaica 4 4 4 92% 76% 95% 0.36

Haiti 4 34% N/a 80% 0.38

Nevis 4 88% 60% 85% N/a

Saint Kitts 88% 56% 85% N/a

Saint Lucia Mixed 88% 67% 100% 0.38

SVG 73% 49% 89% 0.36

Suriname 100% 74% 49% N/a

T&T 4 4 99% 48% 1% N/a

20

EMERGING PPP OPPORTUNITIES

EMERGING PPP OPPORTUNITIES

4

The Caribbean electricity sector has seen significant PPP activity, as well as other forms of private investment—reflectingabroaderpoliticalacceptanceofprivate-sectorparticipationinenergy,comparedtootherinfrastructuresectorssuchastransportorwater.Of12electricityutilitiesinthecountriescoveredbythisreport,fourareprivatelyowned,asshowninTable4.1.Inthesmallerislands,mostelectricityutilitiesareverticallyintegrated,withjustacoupleofIPPsoperatinginAntiguaandSaintKitts.InthelargermarketsofJamaica,TrinidadandTobago,theDominicanRepublic,andHaiti,governmentshaveliberalizedgeneration,introducingIPPs,and(exceptinHaiti)establishedindependentregulators—althoughtheeffectivenessoftheseregulatorsvaries.AregionalregulatorisintheprocessofbeingestablishedintheOECS,withtwoprospectivemembercountriessofar.10

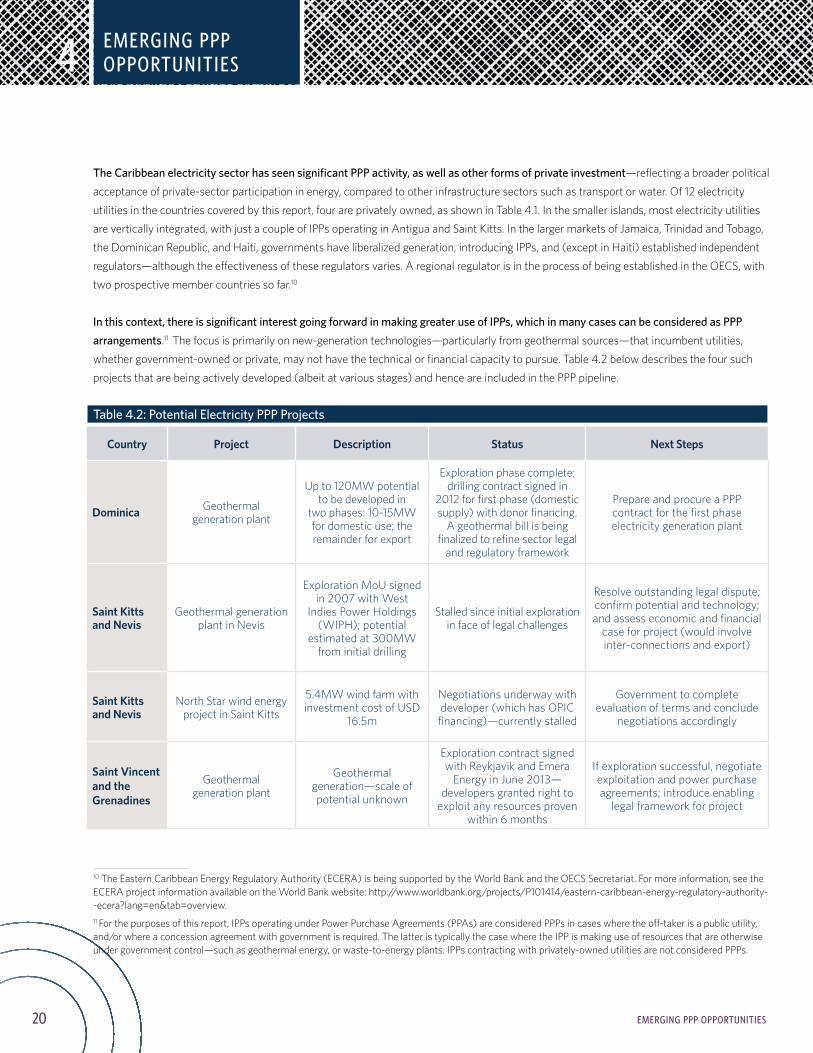

In this context, there is significant interest going forward in making greater use of IPPs, which in many cases can be considered as PPP arrangements.11 Thefocusisprimarilyonnew-generationtechnologies—particularlyfromgeothermalsources—thatincumbentutilities,whethergovernment-ownedorprivate,maynothavethetechnicalorfinancialcapacitytopursue.Table4.2belowdescribesthefoursuchprojectsthatarebeingactivelydeveloped(albeitatvariousstages)andhenceareincludedinthePPPpipeline.

Table 4.2: Potential Electricity PPP Projects

10TheEasternCaribbeanEnergyRegulatoryAuthority(ECERA)isbeingsupportedbytheWorldBankandtheOECSSecretariat.Formoreinformation,seetheECERAprojectinformationavailableontheWorldBankwebsite:http://www.worldbank.org/projects/P101414/eastern-caribbean-energy-regulatory-authority--ecera?lang=en&tab=overview.11Forthepurposesofthisreport,IPPsoperatingunderPowerPurchaseAgreements(PPAs)areconsideredPPPsincaseswheretheoff-takerisapublicutility,and/orwhereaconcessionagreementwithgovernmentisrequired.ThelatteristypicallythecasewheretheIPPismakinguseofresourcesthatareotherwiseundergovernmentcontrol—suchasgeothermalenergy,orwaste-to-energyplants.IPPscontractingwithprivately-ownedutilitiesarenotconsideredPPPs.

Country Project Description Status Next Steps

Dominica Geothermalgenerationplant

Upto120MWpotentialtobedevelopedin

twophases:10-15MWfordomesticuse;theremainderforexport

Explorationphasecomplete;drillingcontractsignedin

2012forfirstphase(domesticsupply)withdonorfinancing.

Ageothermalbillisbeingfinalizedtorefinesectorlegal

andregulatoryframework

PrepareandprocureaPPPcontractforthefirstphaseelectricitygenerationplant

Saint Kitts and Nevis

GeothermalgenerationplantinNevis

ExplorationMoUsignedin2007withWest

IndiesPowerHoldings(WIPH);potential

estimatedat300MWfrominitialdrilling

Stalledsinceinitialexplorationinfaceoflegalchallenges

Resolveoutstandinglegaldispute;confirmpotentialandtechnology;andassesseconomicandfinancial

caseforproject(wouldinvolveinter-connectionsandexport)

Saint Kitts and Nevis

NorthStarwindenergyprojectinSaintKitts

5.4MWwindfarmwithinvestmentcostofUSD

16.5m

Negotiationsunderwaywithdeveloper(whichhasOPIC

financing)—currentlystalled

Governmenttocompleteevaluationoftermsandconclude

negotiationsaccordingly

Saint Vincent and the Grenadines

Geothermalgenerationplant

Geothermalgeneration—scaleofpotentialunknown

ExplorationcontractsignedwithReykjavikandEmera

EnergyinJune2013—developersgrantedrightto

exploitanyresourcesprovenwithin6months

Ifexplorationsuccessful,negotiateexploitationandpowerpurchaseagreements;introduceenabling

legalframeworkforproject

21

EMERGING PPP OPPORTUNITIES

EMERGING PPP OPPORTUNITIES

4

While these projects are being actively developed and so are included in the pipeline, they remain for the most part at a relatively early stage,andinthecaseofgeothermal,facesignificantuncertaintyandcomplexity.Oftheproposedgeothermalprojects,Dominica’sismostadvanced,andhasbeenreceivingsubstantialsupportfromdevelopmentpartners,includingtheEuropeanUnionandtheWorldBank.Likewise,theGovernmentofSaintVincentandtheGrenadinesisworkingcloselywiththeClintonInitiativetodevelopitsgeothermalexploration(withpotentialasyetunproven).ThecomplexitiesandcapacitychallengesfacingtheseprojectsarehighlightedbytheexperienceofSaintKittsandNevis,wherebothpotentialenergyprojectsarecurrentlystalled(andinthecaseofthegeothermalproject,havebeenstalledforsometime),givenprocesschallenges.

Several other governments expressed interest in greater use of PPPs in the energy sector, in addition to the projects listed above.Additionalprojectsbeingconsideredarealsolargelyinrenewableenergygeneration,whereunlikesomeothersectors,privateinvestmentappearspoliticallypalatablethroughoutmostoftheregion.However,theseprojectshavenotyetbeenincludedaspipelineprojectsbecauseofthebarriersthatwouldneedtobeovercomeforthemtomoveforward.Theseconsistof:

• Sector-wide barriers—somegovernmentsarestillintheprocessofdevelopingsector-widestrategiesormajorreformprocessesthatwouldneedtoprecedeanyprivateinvestment.Forexample,theGovernmentsofSurinameandGrenadabothexpressedstronginterestinIPPsforelectricitygeneration,butwouldfirstneedtocompleteon-goingorproposedsectorreformprocesses.TheGovernmentofHaitiisalsoconsideringsectorreformoptionsthatcouldinvolvetheprivatesectormorewidelyacrosstheelectricitysub-sectors,asawaytoimproveperformanceandenableinvestment,butthisprocessisatanearlystage.

• Technology barriers—somerenewableenergytechnologiesthatareattractinginterestarenewtotheregion.Inparticular,fourcountriesexpressedinterestinwaste-to-energyprojects,butacknowledgethatthistechnologyisasyetunprovenatscalesthatwouldpertainintheCaribbean.

Furthermore, energy generation and supply is a sector in which there may be significant value from regional solutions, which have yet to be fully explored.Allofthegeothermalprojectsdescribedabove,ifdevelopedtotheirfullpotential,wouldhaveregionalimplications,astheywouldinvolvecross-borderpowersupply(althoughtheviabilityofcableinter-connectionshasyettobeestablished).Otherregionalsolutionshavebeenmooted,inparticulararegionalapproachtosupplyofLiquidNaturalGas(LNG)andconversionofgenerationfacilitiestorunonLNG.Thisideaisatanearlystage,andhasyettogaintractionintheabsenceofaclearchampionoreffectiveregionalcoordinationmechanism.TheIDBissupportingafeasibilitystudyforaregionalapproachtoLNGsupply,comparedtoalternativessuchasgreaterinvestmentinrenewableenergygeneration,withaviewtobuildingconsensusandacoalitionaroundsuchaproject.