Changes in the economic well-being following the death of a spouse :

Are public survivor pensions sufficient ?

Some evidence for France

Carole Bonnet (INED)

Jean-Michel Hourriez (Crest, INSEE)

CERP, 18-19 September 2008

Background (1)

The loss of a spouse is a shock that could jeopardize financial security during retirement

High poverty rates of widows during the 60’s and 70’s, in a context of high poverty rates of the elderly

increase in the rate of the survivor pension (a part of the pension of the (married) deceased spouse provided to the surviving one) :

From 50 % to 52 % in 1982 and to 54 % in 1995 It has been decided this year to increase this rate to 60 % in 2011

Background (2)

And yet, poverty has sharply decreased among the elderly including widows.

Even if their living standard is still lower than those of married couples (by 16 %)

So, some questions are raised : Does this less well-off situation of widows result from a not

generous enough survivor pension? Or from structural effects ? In a general context of budgetary pressures, do we need to

increase the generosity of survivor benefit ? Survivor pensions represent 14 % of the total pension expenditures

in 2006 (ie 30 billions €)

Outline

In spite of these questions and the financial importance of survivor pensions, no work has been made on this topic, at least in France

Two approaches to study the changes in the economic well-being following the death of the spouse

A theoretical perpective : some calculation on simple representative individuals

An empirical analysis : data used and results

Survivor pension rules (French pension system)

Scheme of the deceased spouse

Survivor pension rate

Means-testing

Civil servant

50% No

Private sector

Basic scheme 54% Yes (own pension + survivor pension <

1392 € / month)

Complementary schemes

60% No

Changes in the living standard : a theoretical perspective (1)

Situation : Married retired couple. Pensions are the only ressources

Living standard before the spouse’s death :

• Living standard after the spouse’s death :

Change in the living standard (N2/ N1) :

and x=Ps/Pd

cu

PPN SD

11

1

1

x

ratexcu

SD PPrateN 2

Pd : pension of the deceased spousePs : pension of the surviving spouse Cu : consumption unit (OECD-modified scale)N : living standards

Rate : survivor pension rate

0,6

0,7

0,8

0,9

1,0

1,1

1,2

1,3

0 0,5 1 1,5Ratio Ps/Pd

N2/

N1

rate=50 %rate=60 %rate=54 %

Changes in the living standard : a theoretical perspective (2)

No means-test – (Civil servant pension scheme – rate = 50%)

Changes in the living standard : a theoretical perspective (3)

0,7

0,8

0,8

0,9

0,9

1,0

1,0

1,1

1,1

0 500 1000 1500 2000 2500 3000

Survivor's own pension (€ per month)

N2

/ N

1

Deceased spouse - Mean PensionDeceased spouse - High Pension

Introduction of a means-test – Private worker scheme

Threshold of the means-test : 1392 € / month

Changes in the living standard : a theoretical perspective (4)

0,7

0,8

0,9

1,0

1,1

0 500 1000 1500 2000 2500 3000

Survivor's own pension (€ per month)

N2

/ N

1

Deceased spouse - Mean Pension

Deceased spouse - High Pension

Changes in the living standard : an empirical analysis (1)

Data used Perfect data : panel data on income with reliable income

dynamics

Income Tax Surveys, 1996-2001

Result of the matching of the Labour Force Surveys and Income tax :

The Labour Force Survey is a rotating panel survey (one third of the sample is replaced each year) two waves of three years panel data

Two different approaches : longitudinal and cross-sectional

Changes in the living standard : an empirical analysis (2)

Marital status

Average living standard Median living standard

€/cu per year Index €/cu per year Index

Women and men, aged 65 and over

15 848 100 (ref) 13 783 100 (ref)

Women, aged 65 and over, living alone

Widowed 13 333 84 11 963 87

Divorced 13 074 82 11 859 86

Single 14 419 91 13 076 95

Men aged 65 and over, living alone

Widowed 17 726 109 14 530 105

Divorced 15 820 100 13 615 99

Single 11 949 75 10 696 78

Source : Income Tax Surveys 1999-2001

Changes in the living standard : an empirical analysis - longitudinal (3)

t : date of spouse’s death Men Women

Disposable Income(t+1) /

Disposable Income(t-1)

Q1 0,69 0,61

Q2 0,79 0,65

Q3 0,87 0,71

Mean 0,77 (0,04) 0,65 (0,02)

Living standard(t+1) /

Living standard(t-1)

Q1 1,04 0,92

Q2 1,18 0,98

Q3 1,31 1,06

Mean 1,17 (0,05) 0,97 (0,03)

Sample 45 102

Source : Income Tax Surveys 1998-2001

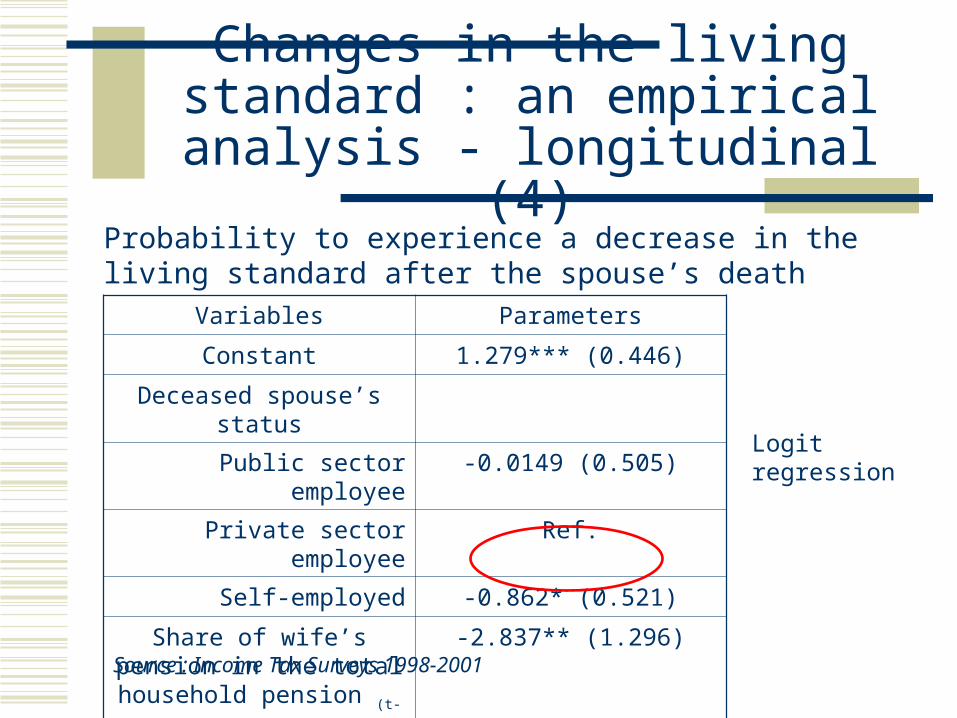

Changes in the living standard : an empirical analysis - longitudinal (4)

Variables Parameters

Constant 1.279*** (0.446)

Deceased spouse’s status

Public sector employee -0.0149 (0.505)

Private sector employee Ref.

Self-employed -0.862* (0.521)

Share of wife’s pension in the total household pension (t-1)

-2.837** (1.296)

Sample size 102

Probability to experience a decrease in the living standard after the spouse’s death

Logit regression

Source : Income Tax Surveys 1998-2001

WomenAv. : 0,84 =Med : 0,86 =

MenAv. : 1,06 =Med : 1,05 =

0,92 0,91

1,15 1,23

0,97 0,94 1,00 0,95

0,90 1,02 0,87 0,98

Changes in the living standard : an empirical analysis– cross-sectional (5)

nerwidowandcouple

coupleinerwidown

ncouple

nerwidowandcouple

ncoupleinerwidow

nerwidow

ncouple

nerwidow

nMnM

nMnD

nM

nMnM

nMnD

nD

nM

nD

N

N

N

N

N

N

N

N

)2()1(

)1()1(

)1(

)2()1(

)1()1(

)1(

)1(

)1(

)(

)()(

)(

)()(

WomenAv. : 0,84 =Med : 0,86 =

MenAv. : 1,06 =Med : 1,05 =

0,92 0,91

1,15 1,23

0,97 0,94 1,00 0,95

0,90 1,02 0,87 0,98

Changes in the living standard following a spouse’s death : Decrease for women : between – 8 and –2 % (on av. and median) Increase for men : between + 15 and + 23 % (on av. and median)

French survivor pension system nearly succeed in maintaining the living standard of women following the spouse’s death.

Only on average. Some women experience a drop in their living standard, especially those without an own pension.

For men, the living standard is almost always higher after the spouse’s death.

Different rules for civil servants and private workers achieve the same results on the maintain of living standard

Discussion and conclusion (1)

One element not discussed today but in the paper (and important)Does OECD-modified equivalence scale fits to widows ?

Consumption structure of elderly people is different In general, widows do not adjust their housing consumption after the

death of a spouse The income needed by the surviving spouse to maintain her living standard could be higher

Increased needs of the surviving spouse : deteriorated health status for example

It could take some time to the surviving spouse to adapt to the new situation

Discussion and conclusion (2)

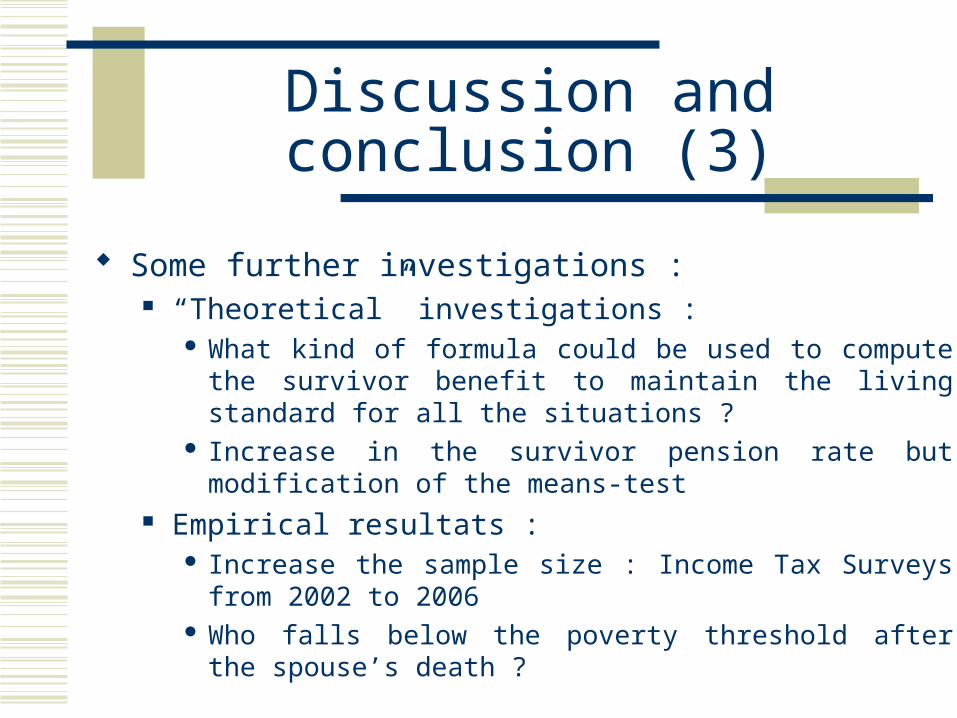

Some further investigations : “Theoretical” investigations :

What kind of formula could be used to compute the survivor benefit to maintain the living standard for all the situations ?

Increase in the survivor pension rate but modification of the means-test

Empirical resultats : Increase the sample size : Income Tax Surveys from 2002 to 2006 Who falls below the poverty threshold after the spouse’s death ?

Discussion and conclusion (3)

Role of wealth : do households for whom the death of a spouse means a decrease in the living standard of the surviving spouse hold more wealth or different type of assets than the others ?

Financial wealth in Income Tax Surveys is not well reported : only taxable wealth. For example, not life insurance.

Use Wealth survey

Discussion and conclusion (4)

Thank you for your attention