www.icaigurgaon.org

NOVEMBER 2016 | VOLUME 1

e-NEWSLETTER Chartered Accountant

04 | GST Impact on Procurement P lanning/ Vendor Management 06 | GST Payment Rules - Made S imple 08 | Workshop on Goods and Serv ices Tax 09 | Const i tut ional Prov is ions for GST 15 | Va luat ions under GST 17 | Offences and penalt ies under GST 19 | ERP Readiness for GST 21 | Yoga - a way to hea lthy l iv ing 22 | Deduct ions do not go l ibera l wi th Courts 24 | Assessment in GST- a repet i t ion avoided 26 | Gl impses 29 | Corporate t ie -up

Index

"The right combination is between a free economy and social policy that addresses the needs of

society and creates equal opportunity." - Benjamin Netanyahu

www.icaigurgaon.org

Managing Committee Editorial Board

CA. Naveen Garg - Chairman

CA. Rakesh K. Agarwal - Vice Chairman

CA. Arun Aggarwal - Secretary

CA. Manish Goyal - Treasurer

CA. Amit Gupta - Executive Member

CA. Lalit Aggarwal - Executive Member

CA. Sandeep Garg - Executive Member

CA. Vipul Jain - Executive Member

CA. Naveen Garg - Chief Editor

Members:

CA. Rakesh K. Agarwal

CA. Arun Aggarwal

CA. Manish Goyal

CA. Amit Gupta

CA. Lalit Aggarwal

CA. Sandeep Garg

CA. Vipul Jain

Chairman’s Message

CA. Naveen Garg (Chairman)

Gurgaon Branch of NIRC of ICAI

Dear Professional Colleagues and Students,

November is an important month for the students, the month of ICAI exams. It is the

time when they have to make the best of their efforts as great future awaits them. The

very old and simple saying that “there is no substitute for hard work” has been proven

right time and again. By the time, this newsletter will reach you, our CA students must

be writing their examinations and my fellow members must have come out of their

festive spirits. October was yet another hectic month with all due dates of tax audits,

service tax returns and TDS returns falling one another. But this all exhaustion and

fatigue got over with the zeal of festival celebrations.

The activities at the institute are continuing at high spirits with support from all of you.

Continuing from September month, the workshop on ‘GST - Place of Supply under

MGL’ were also organized in the month of October on Friday, 7th October 2016. A

seminar on ‘Audit and GST Features in Tally and Diwali Milan’ were organized on

Saturday, 22ndOctober 2016.

To give short snap of the ongoing month, Gurgaon branch has started with ‘Certificate

Course on IFRS’ from 5th of Nov onwards. Also there is a big reason for cheers as our

Gurgaon CA members Cricket team brought laurels by winning an ‘Inter Branch Cricket

Tournament’ held on 5th& 6th Nov hosted by our Gurgaon branch only.

We have two more major events awaiting in December month. Gurgaon Branch is going

to host ‘CA Students National Convention’ on 10th and 11thDecember, 2016. All the

members are requested to please encourage their articles to participate in every activity

of this mega programme. This is not only an academic event but a platform for skill

enhancement and public speaking. A Post Qualification Course on International

Taxation will be starting from 17th December in Gurgaon.

Gurgaon branch, once again requests all its members to bring sponsorships for the

events and the seminars. Any advertisement for e- newsletter is also welcome. Also it’s

open for any type of corporate tie ups for the benefit of CA fraternity.

Gurgaon branch is open to new ideas and programmes, members are requested to give

suggestions and contribute their thoughts.

‘A journey of a thousand miles must begin with a single step.’

--- lao Tsu

Thank You!

02

www.icaigurgaon.org

CA. Arun Agarwal (Secretary)

Gurgaon Branch of NIRC of ICAI

03

Dear Professional Colleagues,

We indeed are living in interesting times that will make path breaking impact on this

country’s history!

The month of October was a lighter one at the branch with one seminars and

one Group Discussion. Inter branch cricket tournament held on 5-6 November 2016

was a huge success with participation of eight teams from across north India. There

was a great display of sportsman ship shown by the players. We are happy to inform

that your Own Gurgaon Team won the series defeating mighty Faridabad team in the

nail biting finals!

The group discussions on GST started earlier were halted for a few weeks on account

of Diwali celebrations and the ITR fillings deadline on 17th October 2017. We shall

start the same in this month and continue through next few months.

We started the First ever Certificate Course on IFRS in Gurgaon Branch from 5th

November 2016 with 46 participants. Following this and in line with the intent of

members received in the survey conducted earlier, we have planned a Diploma

Course on International Taxation from 17th December 2016. Interested members may

contact the branch for more information.

Further, the countdown has begun for the National Convention for CA students in

Gurgaon to be hosted on 10-11th December 2016. We request you to educate CA

students around you and to take active participations in this event which is “By the

CA Students, For the CA Students”

Friends, the step of demonetization of High Denomination currency by our

Honorable Prime Minister is a strong step to address the grave issues of fake currency

and unaccounted money in the economy. On the part of Branch, we shall be holding

a special seminar on “Government’s crusade on Black Money (incl Overview and

Impact analysis of Demonetization of High Denomination Currency Notes)” early

next week. The details of this seminar shall be out soon.

Each one of the committee member is getting regular suggestions from you with

respect to the branch’s working. We are grateful of your participation and request to

please keep them coming!

Thank You!

Managing Committee Editorial Board

CA. Naveen Garg - Chairman

CA. Rakesh K. Agarwal - Vice Chairman

CA. Arun Aggarwal - Secretary

CA. Manish Goyal - Treasurer

CA. Amit Gupta - Executive Member

CA. Lalit Aggarwal - Executive Member

CA. Sandeep Garg - Executive Member

CA. Vipul Jain - Executive Member

CA. Naveen Garg - Chief Editor

Members:

CA. Rakesh K. Agarwal

CA. Arun Aggarwal

CA. Manish Goyal

CA. Amit Gupta

CA. Lalit Aggarwal

CA. Sandeep Garg

CA. Vipul Jain

Secretary’s Message

www.icaigurgaon.org

GST Impact on Procurement Planning/ Vendor Management

CA. Ashish Chaudhary

Proper procurement planning and vendor management is going to be key during GST regime especially during transition phase and upto sometimes post migration. There after there may be need to have continuous relook at professionalism of vendor base and the need to reconsider alternative source of procurement so that the overall cost of procurement is optimized.

Few important aspects in procurement planning and vendor management could be as follows:

1. Procurement from registered vendors: The cascading effect of taxes is going to come down significantly in GST owing to cross sectional credit admissibility. This requires that the vendor must be registered so that the tax paid by him on his procurement is not added to the cost of goods/services and passed on to the company resulting in reduction of cost to that extent.

2. Purchase from unregistered vendor- likelihood of tax on purchases: It is learnt that purchase of goods/services from unregistered dealers could attract the levy of GST in the hand of recipient resulting in increased compliance burden.

3. Purchase from taxable person under composition scheme: There could be a situation where the vendor is registered under composition scheme and not charging GST. On the face of invoice, it could appear that the prices are lower but it may not be necessary considering the fact that tax paid on his procurement become integral part of the cost of his product/service and not passed on the company. Hence, all B2B purchase should be made from vendor registered under normal scheme.

4. Timely registration of vendor during migration to GST: There is provision that all existing registered assessee under VAT, CST, Excise, Service Tax or other taxes being subsumed in GST would be allowed automatic registration under GST on provisional basis valid for 6 months. Final registration would be granted on furnishing necessary details. But it is always preferable to insist the vendor to migrate/obtain registration under GST in advance to avoid the follow-ing problems:

a. The vendor master of ERP could be updated timely. b. In case the vendor is not allowed to registration owing

to deficiency in documentations/any other reasons, the credit taken during the period tax charged by him

under provisional registration could be questioned. (though provision is not clear till date as to what would happen under this circumstances)

c. There is no need of having reconciliation/updation of records on vendor obtaining normal registration post provisional number.

5. Realignment of source of vendor: The factors determining selection of vendors, in past, were largely driven based on indirect tax impact due to many restriction/non-allowability of credits. However, these considerations may not be determining factors in GST while making vendor selection. Important criteria under GST for vendor selection could be as follows:

a. The cost of product/service being offered b. The quality of product/services being offered c. The professionalism of vendor in doing the business d. Compliance level (registration, timely raising of

invoices, timely payment of taxes and filing of returns etc.) followed by vendors under GST

e. Proximity of source of procurement to the place of its usage in case the product/service is critical to the product/services being supplied by company.

f. Cost of transportation This indicates that the tax consideration may not be domi-nant after GST. Hence, existing vendors selected based on the tax consideration may require relook in GST. 6. Change in procurement/inventory policy: The policy

followed by company may require relook in GST especially the policy followed as to inventory holding viz a viz Just in Time (JIT) Purchase considering the fact that accumulation of stock in large quantity could entail blockages of huge working capital. Most of the businesses would prefer to go for JIT purchase in GST with minimum stock in hand.

7. Centralized vs decentralized contract: The decision to go for centralized or decentralized contract for procurement especially in case of service contracts is going to be very critical considering that the services provided by vendor to multiple offices located in different states of the same company under single contract could involve the complexities of deemed supply among various offices of the recipient. i.e. A company awards contract for advertisement to a media

Email: [email protected]

04

www.icaigurgaon.org

GST Impact on Procurement Planning/ Vendor Management

agency for undertaking advertisement of multiple products/services of the company across the country for lump sum consideration. The invoice is required to be issued to contracting office of the service recipient which is not registered as ISD. As the service is enjoyed by various offices of the recipient located across different states, it could be considered as deemed supply by contracting office to all other offices and liable to GST within multiple offices of the same company.

8. Amendment of existing contracts with vendors: There may be need to amend existing contracts with vendors in light of GST.

9. Evaluation of cost of goods/services procured with existing vendors: It is commonly understood that the cost of goods/services are likely to come down in medium term post GST implementation though there could be some rise in the initial period. This depends on various factors i.e. existing rate of tax viz a viz tax rate under GST, exemptions, availability of higher credits, interest cost on differential cash flow etc. This requires in-depth assessment of the cost of procurement from different sources/vendors. Following could be broad guiding factors:

a. Wherever the cost of goods/services is likely to come down, the negotiation should be made with vendors to pass on the benefit. There may be clause in the agreement to re-evaluate cost at periodical interval.

b. If the impact of GST is likely to be negative on some of the products/services, long term contract should be entered into with vendor with specific condition of not allowing price variation during the tenure of the contract.

10. Timely payment of taxes by vendor under GST: Credit would be allowed under GST provided the vendor has paid full tax to government. If the credit is availed by recipient but supplier has not paid tax to the government, it would be added to the tax liability of recipient who needs to pay it along with interest. This requires proper monitoring as to whether vendor has paid tax to the government. If the vendor base is from unorganized sector, this could pose significant challenge for recipient resulting in negative impact on working capital and frequent instances requiring reversal of credit/payment of interest. This necessitates proper monitoring system to be put in place for vendors especially unorganized vendors.

11. Filing of timely returns by vendors: Similar to payment of tax, filing of return by vendor is mandatory for allowing credit to the recipient. Hence, proper control/ monitoring mechanism must be established to ensure that returns are filed timely by vendors.

12. Practice of making advance to vendors: GST is payable at

the time of supply of goods/services. Receiving advance is

also one of the criterion for determining time of supply. Hence, the vendor needs to pay GST at the time of advance. Credit is admissible to recipient at the time of receipt of goods/services. This could result in situations where GST is payable at the time of making payment to vendor but credit is admissible at the time of receipt of goods/services. This could result in timing differences between cash outflow (of taxes) and taking credits. Hence, practice of making advances to vendors may require to be looked into.

13. Identification of place of supply of procurement: Place of supply of goods/service needs to be ascertained to determine applicable taxes (IGST or CGST & SGST). Wrong determination of place of supply could lead to charging and payment of wrong taxes. The Model GST Law, in such cases, provides for paying correct taxes and claiming the refund of tax paid wrongly. Such cases could result in blockage of credits at the end of recipient also. Hence, the recipient is required to determine the place of supply of all procurements properly so that the tax charged by vendor is correct and there is no blockage of credits in their hand.

14. Discounting policy: There could be need to redesign the discounting policy as the Model GST Law requires the discount/incentive to be linked to original invoice. If not linked, the deduction from transaction value may not be allowed and liability to pay tax arises.

15. Vendor Compliance Rating Score- an important criterion for vendor selection: One of the important criterion for vendor selection could be their compliance rating score in GST.

16. E-Procurement: There may need to explore the alternative ways of selection of vendors and one of such ways could be to make e-procurement so that the cost competitiveness could be ensured.

17. GST ready of vendors: It is equally important that all the vendors of the company get the impact of GST assessment done on their business and proper processes and procedures put in place so that all negative consequences, as discussed above at many places, could be avoided.

Conclusion: Above highlights critical points in vendor selection and procurement planning under GST so that the entity is able to take all possible benefits and safeguarded against any unwarranted outcomes. There could be few other important aspects similar to such based on nature of actual composition of vendor base of the company. Author could be reached at [email protected]

05

www.icaigurgaon.org

GST Payment Rules - Made Simple

CA Raman Gopal Jamdagni

Section 35 of the Model GST Law provides provisions

for payment of tax, interest, penalty and other amounts.

As per which, every deposit made towards tax, interest,

penalty, fee or any other amount by a taxable person

shall be credited to the electronic cash ledger of such

person. Further, it also provides that the input tax credit

as self-assessed in the return of a taxable person shall be

credited to his electronic credit ledger.

The Government has prescribed the manner of

maintaining electronic cash and credit ledgers through

the draft GST Payment Rules. These electronic ledgers

function similarly to a bank account where in deposits

and withdrawals are credited and debited respectively.

As per rule 3 of the said rules, the electronic cash

ledger shall be maintained in FORM GST PMT-3 for

each registered taxable person on the Common

Portal (GSTN server). All the cash deposits made

by the assessee towards payment of tax, interest,

penalty, fee or any other amount would be credited

in the cash ledger and such cash ledger would be

debited as and when the amount is utilized to

discharge respective liabilities.

Further, any amount deducted at source on account

of a taxable person shall also get credited to this

electronic cash ledger. Similarly, the amount of cash

refund claimed by the assessee shall also get debited

from the said ledger. However, when the refund

application is rejected, Electronic Cash Ledger shall

be credited back to the extent of rejection.

The registered taxable person or any other person

on his behalf making payment shall generate a

challan in Form GST PMT-4 with the respective

payment details on the said GST common portal.

The said challan shall be valid for a period of 15

days.

The payment shall be made through any of the

following modes:

i. Internet Banking through authorized banks;

ii. Credit card or Debit card after registering the same

with the Common Portal;

iii. National Electronic Fund Transfer (NEFT) or Real

Time Gross Settlement (RTGS) from any bank;

iv. Over the Counter payment (OTC) through

authorized banks for deposits up to ten thousand

rupees per challan per tax period, by cash, cheque

or demand draft – Restriction of Rs.10,000/- is not

applicable to Government department/ recovery

agents/officer authorized in this regard.

Person who is not registered under GST required to

make payment shall obtain a temporary

identification number from the authorized officer

and deposit using Form GST PMT-5 details of which

will be maintained at common portal.

In case of payment made by way of NEFT or RTGS

mode, the mandate form shall be generated along

with the challan & shall be submitted to the bank

from where the payment is to be made. Such

mandate form would be valid up to 15 days from

the challan date.

A Challan Identification Number (CIN) will be

generated on successful credit of the amount to the

concerned government account and such CIN shall

Email: [email protected]

Electronic Cash Ledger

06

www.icaigurgaon.org

GST Payment Rules - Made Simple

be indicated in the challan. When due to any

technical fault, CIN is not generated, then the

assessee may represent electronically in FORM GST

PMT-6.

On receipt of CIN from the authorized Bank, the

said amount shall be credited to the electronic cash

ledger.

Section 2(41) of Model GST Law defines electronic

credit ledger as “Input tax credit ledger in electronic

form maintained at the common portal (GSTN

Server) for each registered taxable person in the

manner prescribed in GST payment rules.

Any claim of input tax credit (CSGT, SGST & IGST)

on supply of goods and or services shall be credited

to the electronic credit ledger maintained in Form

GST PMT-2. Such electronic credit ledger shall be

debited on utilization for making tax payment under

the provisions of the GST Act.

Unutilized balance in Cenvat credit ledger can be

claimed as refund by a registered taxable person at

the end of any tax period at the option of assessee.

The amount to the extent of the refund claim shall

be debited in the said ledger. Then, to the extent of

refund claim rejected if any, shall be re-credited to

the electronic credit ledger by the proper officer by

an order made in Form GST PMT -2A.

All liabilities of a taxable person under GST Act

shall be recorded and maintained in an electronic

register called Electronic Tax Liability Register

(ETLR). Rule 1 of the proposed GST payment rules

provides that the ETLR shall be maintained in Form

GST PMT-1 on the Common Portal.

The electronic tax liability register of a registered

taxable person shall be debited by:

The amount payable towards tax, interest, late fee

or any other amount payable as per the return filed.

The amount of tax, interest, penalty or any other

amount payable as determined by a proper officer

in pursuance of any proceeding under the Act.

The amount of tax and interest payable as a result

of mismatch of input tax credit.

Any amount of interest that may accrue from time

to time.

Electronic tax liability ledger shall be credited as and

when the taxable person discharges his liability

either through Electronic Credit Ledger or

Electronic Cash Ledger.

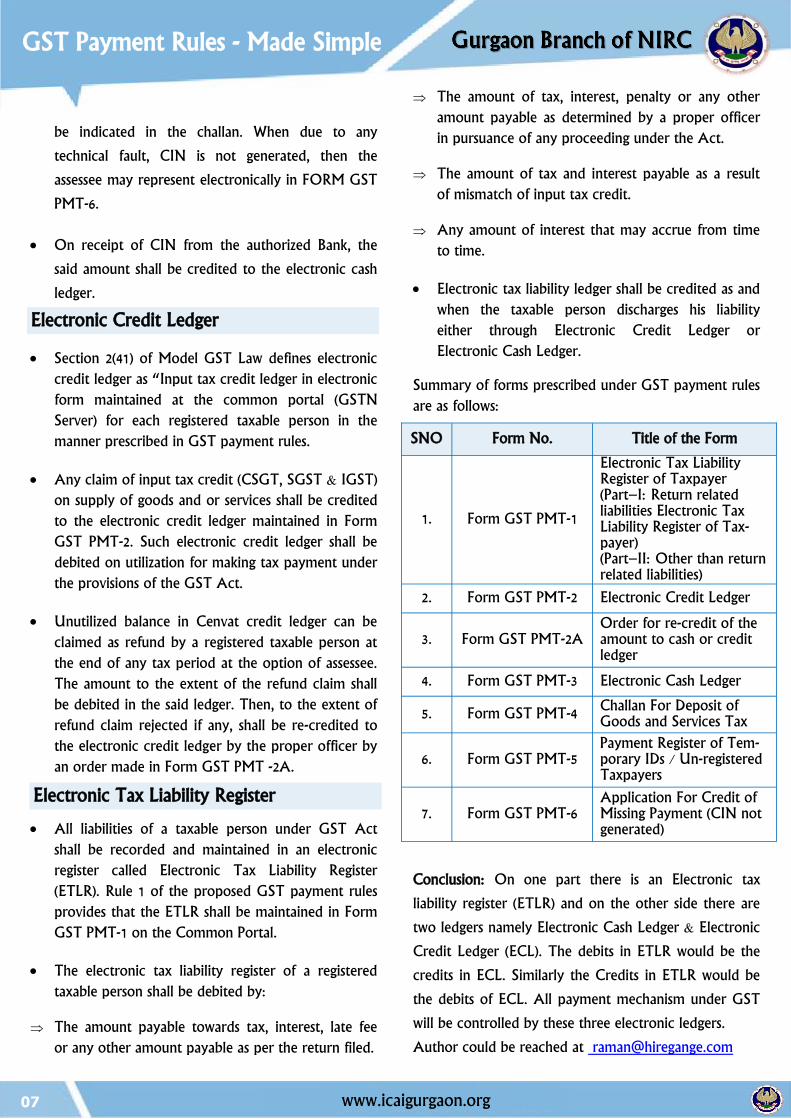

Summary of forms prescribed under GST payment rules

are as follows:

Conclusion: On one part there is an Electronic tax

liability register (ETLR) and on the other side there are

two ledgers namely Electronic Cash Ledger & Electronic

Credit Ledger (ECL). The debits in ETLR would be the

credits in ECL. Similarly the Credits in ETLR would be

the debits of ECL. All payment mechanism under GST

will be controlled by these three electronic ledgers.

Author could be reached at [email protected]

07

Electronic Credit Ledger

Electronic Tax Liability Register

SNO Form No. Title of the Form

1. Form GST PMT-1

Electronic Tax Liability Register of Taxpayer (Part–I: Return related liabilities Electronic Tax Liability Register of Tax-payer) (Part–II: Other than return related liabilities)

2. Form GST PMT-2 Electronic Credit Ledger

3. Form GST PMT-2A Order for re-credit of the amount to cash or credit ledger

4. Form GST PMT-3 Electronic Cash Ledger

5. Form GST PMT-4 Challan For Deposit of Goods and Services Tax

6. Form GST PMT-5 Payment Register of Tem-porary IDs / Un-registered Taxpayers

7. Form GST PMT-6 Application For Credit of Missing Payment (CIN not generated)

www.icaigurgaon.org

Workshop

Gurgaon Branch of NIRC of ICAI is hosting weekly Group Discussion on

Goods and Services Tax

Tentative Topics

Principles of Supply under Model GST Law

Principles of Place of Supply under Model GST Law

Principles of Time of Supply under Model GST Law

Principles of Value of Supply under Model GST Law

GST from CEO/ CFO/ Owners point of view

Input tax Credit under Model GST Law

Impact of GST for IT/ITES/ BPO sector / Technology

Matching reversal under Model GST Law

Impact of GST for Logistics sector

Impact of GST for Automotive sector

Registrations, returns and payment processes in GST

Transitional provisions

Impact of GST for Hospitality sector

Weekly Discussion on Every Friday/Saturday 02(Two) CPE credit hours for each session. Led by Industry/Topic Experts No fee applicable

08

www.icaigurgaon.org

Constitutional Provisions for GST

CA Raman Singla

As you are aware that for nearly thirteen years, India

has been on the verge of implementing a GST (Goods

& Services Tax). But now, with political consensus

secured, the nation is on the cusp of executing one of

the most ambitious and remarkable tax reforms in its

independent history. As per Article 265 of Constitution

of India, no tax can be collected without the authority

of law. Thus, there needs to know the Constitutional

amendments made for GST to have a complete grip

over the subject.

The GST Constitutional (122nd Amendment) Bill’ 2014

became the GST Constitutional (101st Amendment)

Act’ 2016 when the president assented the provisions of

bill on 8th Sept’ 2016.

GST Constitutional (101st Amendment) Act’ 2016

contains the provisions which are necessary for the

implementation of GST Regime. The present

amendments would subsume a number of indirect taxes

presently being levied by Central and State

Governments into GST thereby doing away the

cascading of taxes and providing a common national

market for Goods and Services. The aim to bring about

these amendments in the Constitution is to confer

simultaneous power on Parliament and State

legislatures to make laws for levying GST

simultaneously on every transaction of supply and

Goods and Services.

The amendment Act contains 20 amendments. As per

Sub Section (2) of Section 1, the constitutional

amendments are to be enforced with effect from such

date as the Central Government may, by notification in

the Official Gazette, appoint. The central government,

in exercise of this power has appointed the 16th day of

September, 2016 as the date on which the provisions of

Sections 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 13, 14, 15, 16, 17,

18, 19 and 20 of the said Constitutional amendment

Act, shall come into force. This notification has been

issued to carry out the provisions of Constitutional

amendments. Prior to this notification, the presidential

order dated 12th September 2016, has also confirmed the

constitution of GST Council.

Thus, all the amendments of Constitution (One Hundred

and First Amendment) Act, 2016 is now active. The

amendments are tabled below for ready reference of the

readers:-

Email: [email protected]

09

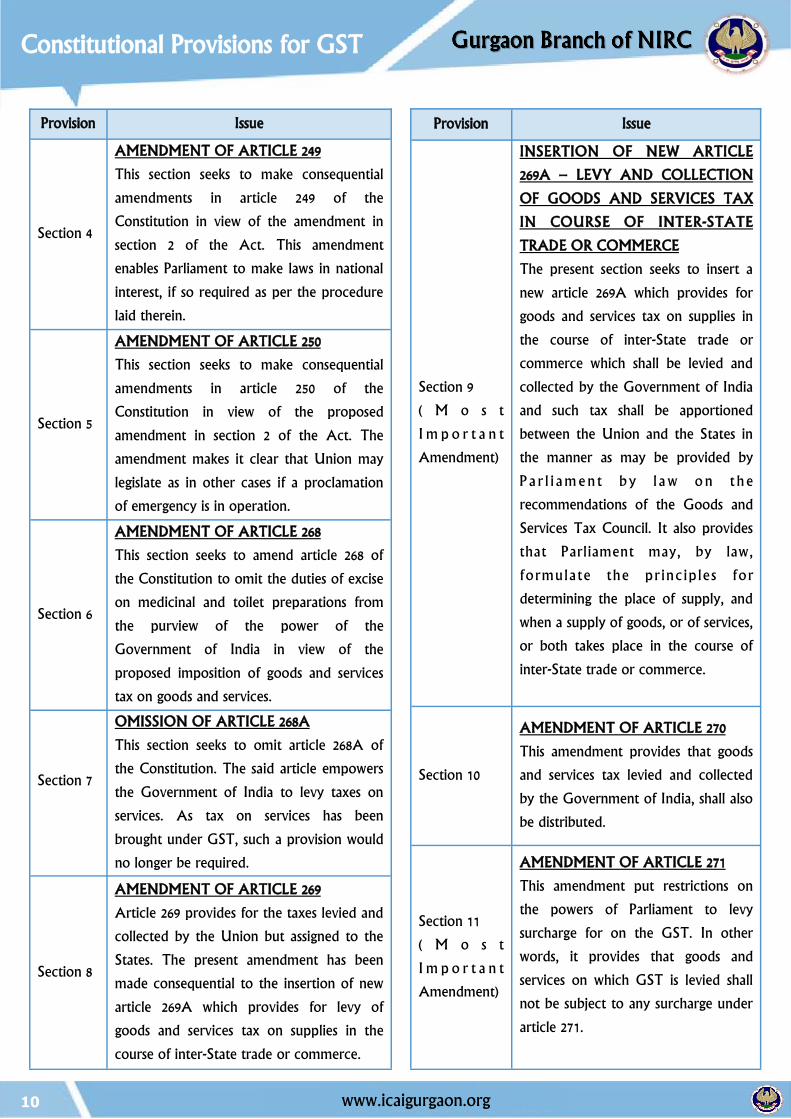

Provision Issue

Section 1

This section provides for short title and commencement o f the Constitution (Amendment) Act. As per Sub Sect ion (2 ) , these amendments are to be applicable from the date to be notified by the Central Government.

Section 2 (Most Important Amendment)

N E W A R T I C L E 2 4 6 A INSERTED – SPECIAL PROVISION WITH RESPECT TO GOODS AND SERVICES TAX This section makes enabling provisions for the Union and States with respect to the GST legislation. It further specifies that Parliament has exclusive power to make laws with respect to GST on interstate transactions. Thus, as per these provisions, the CGST and SGST Act shall be made by Central Government and State Governments respectively, while the IGST Act shall be made by Central Government only.

Section 3

AMENDMENT OF ARTICLE 248 This section seeks to make consequential amendments in article 248 of the Constitution in view of the amendment in section 2 of the Bill.

www.icaigurgaon.org 10

Provision Issue

Section 4

AMENDMENT OF ARTICLE 249

This section seeks to make consequential

amendments in article 249 of the

Constitution in view of the amendment in

section 2 of the Act. This amendment

enables Parliament to make laws in national

interest, if so required as per the procedure

laid therein.

Section 5

AMENDMENT OF ARTICLE 250

This section seeks to make consequential

amendments in article 250 of the

Constitution in view of the proposed

amendment in section 2 of the Act. The

amendment makes it clear that Union may

legislate as in other cases if a proclamation

of emergency is in operation.

Section 6

AMENDMENT OF ARTICLE 268

This section seeks to amend article 268 of

the Constitution to omit the duties of excise

on medicinal and toilet preparations from

the purview of the power of the

Government of India in view of the

proposed imposition of goods and services

tax on goods and services.

Section 7

OMISSION OF ARTICLE 268A

This section seeks to omit article 268A of

the Constitution. The said article empowers

the Government of India to levy taxes on

services. As tax on services has been

brought under GST, such a provision would

no longer be required.

Section 8

AMENDMENT OF ARTICLE 269

Article 269 provides for the taxes levied and

collected by the Union but assigned to the

States. The present amendment has been

made consequential to the insertion of new

article 269A which provides for levy of

goods and services tax on supplies in the

course of inter-State trade or commerce.

Provision Issue

Section 9

( M o s t

I m p o r t a n t

Amendment)

INSERTION OF NEW ARTICLE

269A – LEVY AND COLLECTION

OF GOODS AND SERVICES TAX

IN COURSE OF INTER-STATE

TRADE OR COMMERCE

The present section seeks to insert a

new article 269A which provides for

goods and services tax on supplies in

the course of inter-State trade or

commerce which shall be levied and

collected by the Government of India

and such tax shall be apportioned

between the Union and the States in

the manner as may be provided by

P a r l i am e n t b y l a w o n t h e

recommendations of the Goods and

Services Tax Council. It also provides

that Parliament may, by law,

formula te the pr inc ip les for

determining the place of supply, and

when a supply of goods, or of services,

or both takes place in the course of

inter-State trade or commerce.

Section 10

AMENDMENT OF ARTICLE 270

This amendment provides that goods

and services tax levied and collected

by the Government of India, shall also

be distributed.

Section 11

( M o s t

I m p o r t a n t

Amendment)

AMENDMENT OF ARTICLE 271

This amendment put restrictions on

the powers of Parliament to levy

surcharge for on the GST. In other

words, it provides that goods and

services on which GST is levied shall

not be subject to any surcharge under

article 271.

Constitutional Provisions for GST

www.icaigurgaon.org 11

Constitutional Provisions for GST

Provision Issue

Section 12 ( M o s t I m p o r t a n t Amendment)

INSERTION OF NEW ARTICLE 279A – GOODS AND SERVICES TAX COUNCIL The present section has inserted the provisions for GST Council. The Goods and Services Tax Council shall consist of the following members, namely:- The Union Finance Minister........................ Chairperson; The Union Minister of State in charge of Revenue or Finance................. Member; The Minister in charge of Finance or Taxation or any other Minister nominated by each State Government....................Members. Further the Goods and Services Tax Council shall make recommendations to the Union and the States on- The taxes, cesses and surcharges levied by the Union, the States and the local bodies which may be subsumed in the goods and services tax; The goods and services that may be subjected to, or exempted from the goods and services tax; Model Goods and Services Tax Laws, principles of levy, apportionment of Integrated Goods and Services Tax and the principles that govern the place of supply; The threshold limit of turnover below which goods and services may be exempted from goods and services tax; The rates including floor rates with bands of goods and services tax; Any special rate or rates for a specified period, to raise additional resources during any natural calamity or disaster; Special provision with respect to the States of Arunachal Pradesh, Assam, Jammu and Kashmir, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, Himachal Pradesh and Uttarakhand; and Any other matter relating to the goods and services tax, as the Council may decide.

Section 13 AMENDMENT OF ARTICLE 286 This is a consequential amendment

Section 14 ( I m p o r t a n t Amendment)

AMENDMENT OF ARTICLE 366 The present section specifies the definition of 'Goods and Services Tax’, ‘Services’ and ‘State’. As per the definitions, only alcoholic liquor for human consumption has been excluded from the ambit of GST Constitutionally. All other forms of alcohol like alcohol for industrial use and medicinal and toilet preparation containing alcohol which falls in the taxing domain of the Central Government have been included in GST. This exclusion has been done to address the strong concern of the states regarding loss of revenue if potable alcohol was to be subsumed under GST.

Section 15

AMENDMENT OF ARTICLE 368 This clause seeks to amend article 368 of the Constitution in view of the amendments referred to in Section 12 of the said Act (GST Council) so as to apply the special procedure which requires the ratification of the Bill by the Legislatures of not less than one half of the States in addition to the method of voting provided for amendment of the Constitution. Thus, any modification in GST Council shall also require the ratification by the legislatures of one half of the states.

Section 16

AMENDMENT OF SIXTH SCHEDULE This section seeks to amend the sub-paragraph (3) of paragraph 8 of the Sixth Schedule to the Constitution with a view to empower the District Council for an autonomous district to have the power to levy and collect taxes on entertainment and amusements within such district.

Section 17 ( I m p o r t a n t Amendment)

AMENDMENT OF SEVENTH SCHEDULE This section seeks to make the consequential amendments in Union List and State List Entries

Section 18

The present section provides for the Mandatory Compensation to States for 5 years for loss of revenue on account of introduction of goods and services tax. The present Constitutional amendment Act has deleted the provisions for the applicability of 1% additional tax on interstate transactions.

Section 19 This section seeks to provide for transitional provisions. This section prescribe a timeframe of 1 year within which the subsuming of different indirect taxes into GST would take place and enable the competent Legislature to amend or repeal their existing laws to pave the way for imposition of SGST in the States.

Section 20 This section provides the power to president to remove difficulties within a period of 3 years.

www.icaigurgaon.org

Key Differences between Ind AS and IFRS under Asset Group

CA. Pankaj Sharma

MCA has notified 40 Indian Accounting Standards

(Ind ASs) vide its notification dated February 16, 2015

and March 30, 2016. Indian Accounting Standards are

the set of converged accounting standards notified by

the MCA which are in line with IFRS as issued by the

IASB but subject to certain carve outs (differences) as

notified by the MCA. Ind AS are almost similar to

the IFRS but with few carve outs so as to make them

suitable for Indian Economic Environment. A carve

out essentially means that certain requirements of an

accounting standard under IFRS will not be adopted.

In this article a summary of significant differences

between Ind AS and IFRS under Asset Group is

provided.

1. Elimination of option on recognition of inventories

as an expense based on function-wise classification

Paragraph 38 of IAS 2 dealing with recognition of

inventories as an expense based on function-wise

classification, has been deleted keeping in view the

fact that option provided in IAS 1 to present an

analysis of expenses recognized in profit or loss using

a classification based on their function within the

entity has been removed.

In Ind AS 2 this option has been deleted since Ind AS

1 permits only nature-wise classification of expenses.

1. Elimination of option to reduce the government

grant in arriving at the carrying amount of property,

plant and equipment.

IAS 16 provides in relation to the measurement of

cost, the carrying amount of an item of property,

plant and equipment may be reduced by government

grants in accordance with IAS 20 Accounting for

Government Grants and Disclosure of Government

Assistance.

In Ind AS 16, Paragraph 28 has been deleted since Ind

AS 20, Accounting for Government Grants and

Disclosure of Government Assistance, does not

permit the option of reducing the carrying amount of

an item of property, plant and equipment by the

amount of government grant received in respect of

such an item, which is permitted in IAS 20.

1. Measurement of land and building classified as

investment property and valued at fair value model.

As per paragraph 18-19 of IAS 17, Separate

measurement of the land and buildings elements is

not required when the lessee’s interest in both land

and buildings is classified as an investment property in

accordance with IAS 40 and the fair value model is

adopted.

Not Applicable since Ind AS 40, Investment Property,

prohibits the use of fair value model. Accordingly,

paragraph 18-19 of Ind AS 17 has been deleted.

2. Treatment of escalation of lease rentals due to the

general inflation

No guidance under IFRS

Paragraphs 33 and 50 of Ind AS 17 have been

modified to provide that where the escalation of lease

rentals is in line with the expected general inflation so

as to compensate the lessor for expected inflationary

cost, the increases in the rentals shall not be straight

lined.

Email: [email protected]

INTERNATIONAL ACCOUNTING STANDARD 2 INVENTORIES

12

INTERNATIONAL ACCOUNTING STANDARD 17 LEASES

INTERNATIONAL ACCOUNTING STANDARD 16 PROPERTY, PLANT AND EQUIPMENT

www.icaigurgaon.org

Key Differences between Ind AS and IFRS under Asset Group

1. Elimination of option to measure the

non-monetary government grants at nominal value

IAS 20 gives an option to measure non-monetary

government grants either at their fair value or at

nominal value.

Ind AS 20 requires measurement of such grants only

at their fair value. Thus, the option to measure these

grants at nominal value is not available under Ind AS

20.

2. Elimination of option to present grants as

deduction in arriving at the carrying amount of the

asset.

IAS 20 gives an option to present the grants related

to assets, including non-monetary grants at fair value

in the balance sheet either by setting up the grant as

deferred income or by deducting the grant in arriving

at the carrying amount of the asset.

Ind AS 20 requires presentation of such grants in

balance sheet only by setting up the grant as deferred

income. Thus, the option to present such grants by

deduction of the grant in arriving at the carrying

amount of the asset is not available under Ind AS 20.

1. Guidance on exchange difference arising from

foreign currency eligible for capitalization

IAS 23 provides no guidance as to how the

adjustment prescribed in paragraph 6(e) is to be

determined.

However in Ind AS 23, paragraph 6A is added to

provide the guidance on the exchange difference

arising from foreign currency eligible for

capitalization.

“Para 6A. With regard to exchange difference

required to be treated as borrowing costs in

accordance with paragraph 6(e), the manner of

arriving at the adjustments stated therein shall be as

follows:

(i)the adjustment should be of an amount which is

equivalent to the extent to which the exchange loss

does not exceed the difference between the cost of

borrowing in functional currency when compared to

the cost of borrowing in a foreign currency.

(ii)where there is an unrealized exchange loss which is

treated as an adjustment to interest and subsequently

there is a realized or unrealized gain in respect of the

settlement or translation of the same borrowing, the

gain to the extent of the loss previously recognized as

an adjustment should also be recognized as an

adjustment to interest.”

1. Impairment of the Investment Property measured

at fair value

IAS 36 is not applicable regarding impairment of

Investment Property that is measured at fair value.

Under Ind AS 36 it’s not applicable since the fair

value measurement option is not available under Ind

AS 40. Therefore paragraph 2(f) is deleted in Ind AS

36 as Ind AS 40 requires cost model.

1. Acquisition of an Intangible asset by way of a gov-

ernment grant

IAS 38, Intangible Assets, provides the option to an

entity to recognize both asset and grant initially at fair

value or at a nominal amount plus any expenditure

that is directly attributable to preparing the asset for

its intended use.

13

INTERNATIONAL ACCOUNTING STANDARD 20 ACCOUNTING FOR GOVERNMENT GRANTS AND DISCLOSURE OF GOVERNMENT ASSISTANCE

INTERNATIONAL ACCOUNTING STANDARD 23 BORROWING COSTS

INTERNATIONAL ACCOUNTING STANDARD 36 IMPAIRMENT OF ASSETS

INTERNATIONAL ACCOUNTING STANDARD 38 INTANGIBLE ASSETS

www.icaigurgaon.org

Key Differences between Ind AS and IFRS under Asset Group

Ind AS 38 allows only fair value for recognizing the

intangible asset and grant in accordance with Ind AS

20.

2. Amortization of intangible asset arising from

service concession arrangement in respect of toll road

Not applicable under IFRS

Intangible assets recognized for service concession

arrangements in respect of toll road under IGAAP

up to the period ending immediately before the

beginning of the first Ind AS reporting period can be

amortized as per the policy adopted under IGAAP.

“Paragraph 7AA has been inserted to scope out the

entity that opts to amortize the intangible assets

arising from service concession arrangements in

respect of toll roads recognized in the financial

statements for the period ending immediately before

the beginning of the first Ind AS reporting period as

per the exception given in paragraph D22 of

Appendix D to Ind AS 101.”

1. Elimination of option to recognize investment

properties at fair value.

IAS 40 permits both cost model and fair value model

(except in some situations) for measurement of

investment properties after initial recognition.

Ind AS 40 permits only the cost model.

2. Prohibition on the treatment of property interest

held in an operating lease as investment property

IAS 40 permits treatment of property interest held in

an operating lease as investment property, if the

definition of investment property is otherwise met

and fair value model is applied. In such cases, the

operating lease would be accounted as if it were a

finance lease.

Ind AS 40 prohibits the use of fair value model hence

this treatment is prohibited in Ind AS 40.

Ind AS 41 is similar to IAS 41 apart from different

terminology used in Ind AS.

1. Presentation of discontinued operations in the

separate income statement

IFRS 5 has options to present the items of profit or

loss of discontinued operations in a separate income

statement and other comprehensive income or in one

single statement containing both as IAS 1 permits

both methods of presentation.

However, in IND AS 105 the requirements regarding

presentation of discontinued operations in the

separate income statement, where separate income

statement is presented under paragraph 33A have

been deleted.

This change is consequential to the removal of option

regarding two statement approach in Ind AS 1. Ind

AS 1 requires that the components of profit or loss

and components of other comprehensive income

shall be presented as a part of the statement of profit

and loss.

2. Clarification inserted on conditions for classification

of a non-current asset (or disposal group) as held for

sale.

IFRS 5 does not provide any such clarification.

Paragraph 7 of Ind AS 105 prescribes the conditions

for classification of a non-current asset (or disposal

group) as held for sale. A clarification has been added

in Paragraph 7 that the non-current asset (or disposal

group) cannot be classified as held for sale, if the

entity intends to sell it in a distant future.

14

INTERNATIONAL ACCOUNTING STANDARD 40 INVESTMENT PROPERTY

INTERNATIONAL FINANCIAL REPORTING STANDARD 5 NON-CURRENT ASSETS HELD FOR SALE AND DISCONTINUED OPERATIONS

INTERNATIONAL ACCOUNTING STANDARD 41 AGRICULTURE

www.icaigurgaon.org

CA. Saurabh Gupta

GST stands for "Goods and Services Tax", and is

proposed to be a comprehensive indirect tax levy on

manufacture, sale and consumption of goods as well

as services at the national level. It will replace all

indirect taxes levied on goods and services by the

Indian Central and State governments. Second draft

of GST law is supposed to be tabled in Parliament for

approval shortly. The first model law has already

been shared with public and the comments were in-

vited.

So, on which value, GST will be levied?

There seems to be very obvious answer to this i.e.

price on which the exchange of goods and services

will take place. But, is it that simple, let’s check the

GST valuation Rules, 2016. Rule 3 of GST Valuation

rules conveys the same answer and affirms that

transaction value shall even be accepted where the

supplier and recipient of supply are related parties

provided their relationship has not influenced the

price. But this is subject to Rule 7.

Rule 7 empowers the GST officer with draconian

provision to reject transaction value, if he has reasons

to doubt the truth or accuracy of the value declared.

He has been given powers to ask further information

and evidences to cross check the price. If the officer

still has reasonable doubt as to the value of transac-

tion, after evaluation as per Rule 7, the price will be

determined by Rule 4.

Rule 4 is the spinal cord of valuation rules, it

introduces transfer pricing concept in the Model

GST law. As per Rule 4, the transaction value of

goods or services will be value of like kind and

quality supplied at or about the same time to other

customers with the adjustments to relevant factors

like difference in date of supply, commercial and

quantity levels, composition, quality and design.

However, adjustment would also be made for freight

and insurance charges depending upon place of

supply. Rule 5 further strengthens the spinal cord

above and provides that if the value cannot be

determined by method as stated in Rule 4, it will be

computed on the basis of cost of production or cost

of services, charges for the design or brand with the

addition of usual profit and general expenses. The

point to note here is, that these rules are applicable

to all transactions irrespective of related party status.

A cursory reading of above rules may look very

normal and simple to one but as you give a deep

thought to it, you will start feeling the butterflies in

stomach and it will leave you with bundle of nerves.

Basically, the Model GST Law has introduced transfer

pricing concept in the law. Was it required, it is just

copies from earlier laws? It won’t be wrong to say,

the way it has been introduced

“Kahin ki eent, kahin ka roda; bhanumati ne kunba

joda”

Let’s understand more about transfer pricing and it’s

applicability in existing laws. Transfer pricing is the

setting of the price for goods and services sold

between controlled (or related) legal entities within

an enterprise. In principle, a transfer price should

match either what the seller would charge an

independent, arm's length customer, or what the

buyer would pay an independent, arm's length

supplier. Transfer pricing is perceived as major tool

for corporate tax avoidance and is also referred as

base erosion and profit sharing (BEPS). Transfer

pricing adjustments have been a feature of many tax

laws across the globe since the 1930s. All the cross

border transactions made with related parties abroad

are subject to pass the litmus tests of transfer pricing

laws in order to prove that the transaction has been

made on Arm’s length price. The rules in this regard

have been adopted by most of the countries to

safeguard their tax revenue. India’s transfer pricing

regulations also broadly adopts the OECD principles

currently.

Income Tax Act specifically lays out procedure for

transfer pricing audits for transactions entered with

international related parties. Domestic related party

transactions are also required to be reported

Email: [email protected]

Valuations under GST

15

www.icaigurgaon.org

separately with audit requirements for higher

amounts.

The proposed valuation rules in Model GST law are

on the lines of India’s Customs Valuation

(Determination of Value of Imported Goods) Rules,

2007. In fact, it won’t be wrong to say that language of

the proposed law has been copied from existing

custom valuation rules. The custom law also requires

related parties to refer to Special Valuation Branch

(SVB) for evaluation of arms length price. Further,

with the use of technology, customs have developed

the dynamic data bank of historical rates reported by

various importers using tariff codes to identify

abnormally priced transactions. On the top of it,

customs have also fixed duty price in case of various

items to do away with valuation issues. According to

study done by a sample set of importers, among the

various roadblocks in the domain of trade facilitation,

valuation related issues account for 19% of the

grievances, followed by tariff classification grievances

(16%).

The question arises, can customs law be replicated in

GST? The objectives behind transfer provisions are

quite different, in customs law government also needs

to protect interest of domestic players, ensure inferior

goods are not dumped in the country despite

protecting country’s revenue. Here under GST

regime, there is no incentive for tax planning even by

related parties at one stage as it would get taxed in

subsequent stage.

Central excise law in India is the oldest surviving

indirect tax levy in India, but the valuation principles

are still far from being settled. Safe harbor provisions

(likewise Income tax) have been provided to reduce

the litigation in the past. E.g. Rule 8 of excise valuation

rules prescribes, that where the excisable goods are

used by the manufacturer wholly or partly for

in-house consumption in the manufacturing of other

goods, the valuation of goods meant for in‑house

consumption must be completed at 110% of the cost

of production. Compounded levy schemes based upon

installed capacity of production have also been

provided to eliminate the need for transaction

valuations.

Under GST, it would have been made some sense if

lawmaker’s intent would have to double check the

transaction price between related parties; but how

fruitful this exercise is – to question transaction price

between unrelated parties. The draft law questions the

reasonability of price transacted even between

unrelated parties. Unless the tax officer has got the

evidence of receipt of unreported consideration,

keeping of such provisions of rejection of value are

drastic provisions for business. Imagine a situation,

where you supply goods or services at a negotiated

price and pay GST on such price and a day after

completion of your transaction, GST officer negates

this price. There is remotest probability that buyer

will bear the additional tax on price valued by GST

officer. So, the risk lies with seller / dealer only.

“May god save the ease of doing business campaign in

our country. “

Can one imagine a world where any computer

software or any laid out rules are able to arrive at real

transaction prices? This could have been possible in

case of homogeneous goods to some extent but it is

quite an uphill task in case of today’s innovative

product and services. Business is not a science in 21st

century, business is symptomatic of our failure to

efficiently harvest, distribute and replenish resources.

It’s a progression from mystery to heuristic. Let the

service provider be free to decide the price of his

offerings, it’s not an algorithm or a software code.

Model GST law has opened up can of worms of

bureaucracy and litigation by questioning the

transaction between unrelated parties. Will

administrators be ever able to derive an amicable

approach to judge prices of goods or services?

Likewise, present customs and excise laws, we seem to

be entering back to the era of long list of disputed

valuation litigations. Let’s hope the second draft and

further rules on the subject addresses the concern.

Valuations under GST

16

www.icaigurgaon.org

Offences and penalties under GST

CA. Sanjeev Singhal

Offences are most important part of any ACT which

provide stick to the Act for it smooth functioning

and implementation

66. Offences and penalties

1. Where a taxable person who -

i) supplies any goods and/or services without issue

of any invoice or issues an incorrect or false

invoice with regard to any such supply;

ii) issues any invoice or bill without supply of goods

and/or services in violation of the provisions of

this Act, or the rules made there under;

iii) collects any amount as tax but fails to pay the

same to the credit of the appropriate

Government beyond a period of three months

from the date on which such payment becomes

due;

iv) collects any tax in contravention of the provisions

of this Act but fails to pay the same to the credit

of the appropriate Government beyond a period

of three months from the date on which such

payment becomes due;

v) fails to deduct the tax in terms of sub-section (1)

of section 37, or deducts an amount which is less

than the amount required to be deducted under

the said sub-section, or where he fails to pay to

the credit of the appropriate Government under

sub-section (2) thereof, the amount deducted as

tax;

Section -37(1) Tax Deducted at Source

[to deduct tax at the rate of one percent from the

payment made or credited to the supplier

[hereinafter referred to in this section as “the

deductee”] of taxable goods and/or services, notified

by the Central or a State Government on the

Email: [email protected]

17

recommendations of the Council, where the total

value of such supply, under a contract, exceeds

rupees ten lakh]

va) fails to collect tax in terms of sub-section (1) of

section 43C, or collects an amount which is less than

the amount required to be collected under the said

sub-section, or where he fails to pay to the credit of

the appropriate Government under sub-section (4)

thereof, the amount collected as tax;

43C. Collection of tax at source

(1) Notwithstanding anything to the contrary

contained in the Act or in any contract,

arrangement or memorandum of understanding,

every electronic commerce operator

(hereinafter referred to in this section as the

“operator”) shall, at the time of credit of any

amount to the account of the supplier of goods

and/or services or at the time of payment of

any amount in cash or by any other mode,

whichever is earlier, collect an amount, out of

the amount payable or paid to the supplier,

representing consideration towards the supply

of goods and /or services made through it,

calculated at such rate as may be notified in this

behalf by the Central/State Government on the

recommendation of the Council.

(vi) takes and/or utilizes input tax credit without

actual receipt of goods and/or services either

fully or partially, in violation of the provisions

of this Act, or the rules made there under;

(vii) fraudulently obtains refund of any CGST/SGST

under this Act;

(viii) takes or distributes input tax credit in violation

of section 17, or the rules made There under;

www.icaigurgaon.org

(ix) falsifies or substitutes financial records or produces

fake accounts and/or documents or furnishes any

false information or return with an intention to

evade payment of tax due under this Act;

(x) is liable to be registered under this Act but fails to

obtain registration;

(xi) furnishes any false information with regard to

particulars specified as mandatory, either at the time

of applying for registration, or subsequently;

(xii) obstructs or prevents any officer in discharge of his

duties under the Act;

(xiii) transports any taxable goods without the cover of

documents as may be specified in this behalf;

(xiv) suppresses his turnover leading to evasion of tax

under this Act;

(xv) fails to keep, maintain or retain books of account

and other documents in accordance with the

provisions of this Act or the rules made there

under;

(xvi) fails to furnish information and/or documents

called for by a CGST/SGST officer in accordance

with the provisions of this Act or rules made there

under or furnishes false information and/or

documents during any proceedings under this Act;

(xvii) supplies, transports or stores any goods which he

has reason to believe are liable to confiscation under

this Act;

(xviii) issues any invoice or document by using the

identification number of another taxable person;

(xix) tampers with, or destroys any material evidence;

(xx) disposes off or tampers with any goods that have

been detained, seized, or attached under this Act;

There shall be penalty of rupees ten thousand or an

amount equivalent to the tax evaded or the tax not

deducted or short deducted or deducted but not paid

to the Government or input tax credit availed of or

passed on or distributed irregularly, or the refund

claimed fraudulently, as the case may be, whichever is

higher.

(2) Any registered taxable person who repeatedly

makes short payment of tax shall be liable to a

penalty of rupees ten thousand or ten percent of

the tax short paid, whichever is higher.

Explanation.- For the purposes of this

sub-section, a taxable person shall be deemed to

have made short payments ‘repeatedly’, if there

were short payments in three returns during any

six consecutive tax periods.

(3) Any person who

(a) aids or abets any of the offences specified in

clauses (i) to (xx) of sub-section (1) above;

(b) acquires possession of, or in any way concerns

himself in transporting, removing, depositing,

keeping, concealing, supplying, or purchasing or

in any other manner deals with any goods which

he knows or has reason to believe are liable to

confiscation under this Act or the rules made

there under;

(c) receives or is in any way concerned with the

supply of, or in any other manner deals with any

supply of services which he knows or has reason

to believe are in contravention of any provisions

of this Act or the rules made there under;

(d) fails to appear before the CGST/SGST officer,

when issued with a summon for appearance to

give evidence or produce a document in an

enquiry;

(e) fails to issue invoice in accordance with the

provisions of this Act or rules made There

under, or fails to account for an invoice in his

books of account; shall be liable to a penalty

which may extend to rupees twenty five

thousand.

67. General penalty

Any person, who contravenes any of the provisions

of this Act or any rules made There under for which

no penalty is separately provided for in this Act,

shall be liable to a penalty which may extend to

rupees twenty five thousand.

18

Offences and penalties under GST

www.icaigurgaon.org

ERP Readiness for GST

CA. Rohit Chopra

Being Government looks focused in getting GST

implemented by 01st April 2016, IT department/

companies also have to get themselves ready for the

changes they have to carry out in the system

mappings. Processes which is being mapped before

GST has to be revisited and new processes has to be

implemented to cover the statutory requirements of

GST.

All the major players in the market are preparing

themselves in parallel to Government and have already

initiated necessary developments to be carried out in

their respective ERPs based on the Draft Model of

GST released by the Government. JIT technique is

being used in such a way that by the time complete

rules related to GST are laid down, they should be

ready with the base so that delta can be configured

within the shortest duration of time.

In Sync with this, SAP (the market player of ERP) has

already released various basic notes which talks about

GST in the era of SAP. On a broader level, on the

basis of model received, following changes seems to be

carried out by the companies in there ERP software’s:-

1. System Upgrade: - Stack update has to carry out

to make the system compatible with GST. This will

help companies in easy adaptation of the new

changes in there system which will be released by

SAP in form of patches. Further condition based

tax procedures (TAXINN) is suggested by SAP to

its customers & if they are working with formula

based tax procedures (TAXINJ), they have to do

the necessary migration to change the procedure

from TAXINJ to TAXINN. Migration in itself is a

mini project & will take around 10-12 weeks to

implement.

2. Master Data: - As per the model released every

company has to get himself registered in each

state of operation. These numbers has to be

maintained in the system for each legal entity

against each state (business place). This number

than has to be printed on the various invoices as

well. Further for each vendor & customer

operating with the company, his GST

registration number has to be maintained in the

master data record. Further each material has to

be updated with its HSN number and every

service master has to be updated with SAC

(Service Account Code) number. SAP has

already specified fields where these numbers has

to be maintained. Even separate master data

should be created for every region (state) of

supply.

3. Configuration Changes: - There will be lots of

configuration changes which has to be carried

out in the system to make it compatible with

GST ACT. Various existing configuration has to

be deleted/blocked prospectively. All Print out

form need to changes as per GST compliance.

As most of applicable Indirect taxes would be

subsumed under GST, tax master (including

input and output rates as well as input and

output tax condition types) would have to be

fully revised. Every customer need to Identify as

B2B or B2C customer that will be configured in

Customer group field, to comply with GST

return filing.

4. Process Mapping: - Changes by mean of

introduction to new process/BPR of existing

processes has to be carried out in the system.

Even some new processes has to be introduced

in the system which were not exist previously

e.g. on payment of advance against Purchase

Email: [email protected]

19

www.icaigurgaon.org

Orders, tax impacts has to be considered as

well as tax invoice has to be generated in the

system. Stock transfer which so far is making

no accounting impact, now has to be valuated

& tax impacts has to be considered on the

value. In GST Regime Job Work may be

treated as Sales & Purchase. To claim tax

adjustments for debit note/credit note,

reference to original invoice is mandatory and

has to be mapped in the system.

5. Tax Accounting: - Being reporting has to be at

State level, necessary accounting of taxes has

to be done at State Level. This will impact the

Chart of Accounts for the company as it will

lead to increase in the number of GL accounts

of their Trial Balance. A company which is

being operated in 24 States of India now has

to create 6 GL accounts for each state (2 each

for CGST/SGST/IGST, one for receivable &

one for payable), resulting into approx. 144

new GL accounts.

6. Returns/Registers : - Existing market players

20

ERP Readiness for GST

which supports companies in extracting returns/

supporting data for return filling are also making

necessary changes to come out with the output of

necessary returns from the system i.e. GSTR1,

GSTR2, GSTR3…..GSTR8. Along with that

business is expected auto extraction of ITC

Ledger, Cash Ledger & Tax Ledger from the

system to ease there compliance work as well as

necessary reconciliation they have to carry out.

Focus is to make system communicate with GSTN

Portal for necessary data verification and

reconciliation.

7. Migration: - Open Sales return/ Purchase Return/

Credit Note/ Discounts etc. needs to be deal for

transition period. Cut over Strategy will be

devised as per SAP proposed Solution. SAP is

working on designing a Solution on cutover

strategy for transferring the old credit to GST Tax

Components (Clarity on credit transfer awaited)

and for transition period.

8. Still there are bundle of things needs further

clarity from Government, which will be cleared

on the release of detailed rules which may further

lead to other changes as well in the system.

Gurgaon Chartered Accountants, a newsletter owned by Gurgaon Branch of NIRC of ICAI is normally published in the first week of every month. Non Receipt of any issue should be notified within one month. Articles in interest of profession and management skills are welcome. Views expressed by contributors are their own and may not be in concurrence with Gurgaon Branch of NIRC of ICAI and the branch does not take any responsibility of views expressed by contributors. Gurgaon Branch is not responsible in any manner of any result of the action taken on the basis of advertisements published in the newsletter. Rights & copying of articles or write ups is not allowed without permission of Editorial Committee.

www.icaigurgaon.org

YOGA

- A WAY TO HEALTHY LIVING

21

www.icaigurgaon.org

Deductions do not go liberal with Courts

CA. Gopal Nathani

In the computation of income the assessee’s claim

various deductions and exemption under the Act.

Such benefits are however available subject to

fulfillment of conditions provided in the relevant

section. It may so happen that the assessee may not

technically meet such conditions in the relevant year

for uncontrollable factors by reasons of which the

claims for deductions/exemptions may come under

question. For instance in the context of grant of

relief u/s 54/54F an assessee may reinvest into

property in joint names or that he may fail to

reinvest all the amounts within the prescribed period

or that he may fail to deposit the unutilized amount

into deposit account with a scheduled bank. The AO

in such instances may not accept the claim ex facie

and it is only that the Tribunal or the Courts may

have to be approached by an assessee.

For instance the Delhi High Court in CIT v. Ravinder

Kumar Arora (2012) 342ITR38 held that section 54F of

the Income-tax Act, 1961, is a beneficial provision

which should be interpreted liberally in favour of the

exemption/deduction to the taxpayer and deduction

should not be denied on a hyper technical ground so

that in this case it is held that the conditions

stipulated in section 54F stood fulfilled even when

house is given to have been purchased in joint names

of the assessee and his wife. Not to mention that in

another instance in D Devadass v ITO ( 2016) 48ITR

(Trib) 613 the Chennai bench held that the exemption

u/s 54F is exclusive to be claimed by the assessee

which could not be clubbed or applied to the blood

relation or family members so that the assessee is

held deprived of exemption u/s 54F for having made

reinvestment into house in the name of his daughter.

The bench went by the Bombay High Court ruling in

the decision of Prakash v. ITO [2009] 312 ITR 40 than

by any beneficial interpretation to assessee’s

advantage.

The Bombay High Court in their recent ruling in

Humayun Suleman Merchant v. Chief Commissioner

of Income tax and another however stressed on the

point that the decision of one High Court is not a

binding precedent upon another High Court and at

best can only have persuasive value so that the

assessee in this case was declined exemption u/s 54F

for his failing to bank the unutilized amount of capital

gains in specified bank deposit before due date

notwithstanding the Karnataka High Court decision

favouring the assessee. On the very question

whether an assessee could be denied exemption

under section 54F on the ground that he did not

deposit the said amount in capital gains account

scheme before the due date prescribed under section

139(1) the Karnataka High Court held therein that:

"As is clear from Sub-section (4) in the event of the

assessee not investing the capital gains either in

purchasing the residential house or in constructing a

residential house within the period stipulated in

Section 54F(1), if the assessee wants the benefit of

Section 54F, then he should deposit the said capital

gains in an account which is duly notified by the

Central Government. In other words if he want of

claim exemption from payment of income tax by

retaining the cash, then the said amount is to be in-

vested in the said account. If the intention is not to

retain cash but to invest in construction or any pur-

chase of the property and if such investment is made

Email: [email protected]

22

EXEMPTION PROVISIONS DO NOT GO LIBERAL WITH COURTS ALWAYS- HOUSING RELIEFS

BOMBAY HIGH COURT ON STRICTER INTERPRETATION

www.icaigurgaon.org

Deductions do not go liberal with Courts

within the period stipulated therein, then Section 54F

(4) is not at all attracted and therefore the contention

that the assessee has not deposited the amount in the

Bank account as stipulated and therefore, he is not

entitled to the benefit even though he has invested

the money in construction is also not correct."

In distinguishing the Karnataka High Court decision

the Bombay High Court held that the entire basis for

their decision was the intent of the parties and that in

interpreting a fiscal statute one must have regard to

the strict letter of law and intent can never override

the plain and unambiguous letter of the law.

Moreover according to the Bombay High Court

the decision in K Ramachandra Rao (supra) was

rendered sub-silentio, i.e., no argument was made

with regard to the requirement of deposit in notified

bank account in terms of section 54F (4) of the Act

before the due date as provided in section 139(1) of

the Act.

The Bombay High Court also distinguished Delhi

High Court decision in Ravinder Kumar Arora which

went by the analogy that liberal /beneficial

construction should be given to the provisions of

section 54F of the Act as its object was to encourage

the housing sector which would result in the benefit

being extended to the assessee.

The High Court also referred to Gauhati High Court

decision in CIT v Rajesh Kumar Jalan (2006)

286ITR274 which proceeded on beneficial

interpretation over the stricter interpretation to hold

a view that due date for assessee to invest amount of

capital gains in purchase/construction of new

residential asset or investment in capital gains scheme

under section 54F refers to 'extended due date'

under section 139(4). No so long ago the Bombay

High Court in Vodafone India Services P Ltd. v.

Union of India and others (2014) 368ITR1 also held

that while interpreting a fiscal or taxing statute, the

intent or purpose is irrelevant and the words of the

taxing statute have to be interpreted strictly. In the

case of taxing statutes, in the absence of the

provision by itself being susceptible to two or more

meanings, it is not permissible to forgo the strict

rules of interpretation while construing it.

Thus, it is almost certain that in taking benefit of

exemption the assessee must meet the conditions of

the given section and not just make a claim

simplicitor by mere reference to beneficial interpre-

tation of the provision by any Court other than juris-

dictional High Court as he may lend in difficulty at

later stage.

23

Gurgaon Chartered Accountants, a newsletter owned by Gurgaon Branch of NIRC of ICAI is normally published in the first week of every month. Non Receipt of any issue should be notified within one month. Articles in interest of profession and management skills are welcome. Views expressed by contributors are their own and may not be in concurrence with Gurgaon Branch of NIRC of ICAI and the branch does not take any responsibility of views expressed by contributors. Gurgaon Branch is not responsible in any manner of any result of the action taken on the basis of advertisements published in the newsletter. Rights & copying of articles or write ups is not allowed without permission of Editorial Committee.

www.icaigurgaon.org

Assessment in GST- a repetition avoided

CA. Ram Akshya Rout

Goods & Service tax (GST) is one of the biggest and

historical indirect tax reform in India. It is going to

replace the existing cumbersome indirect tax

structures. We know that many indirect taxes,

almost 17 types of taxes are going to be merged into

one tax i.e. GST. The summary of taxes merged are

given below for ready references:

Central Excise duty, Duties of Excise (Medicinal and

Toilet Preparations), Additional Duties of Excise

(Goods of Special Importance), Additional Duties

of Excise (Textiles and Textile Products), Additional

Duties of Customs (commonly known as CVD),

Special Additional Duty of Customs (SAD), Service

Tax, Central Sales Tax, Cesses and surcharges

insofar as far as they relate to supply of goods or

services.

State VAT, Purchase Tax, Luxury Tax, Entry Tax

(All forms), Entertainment Tax (not levied by the

local bodies), Taxes on advertisements, Taxes on

lotteries, betting and gambling, State cesses and

surcharges insofar as far as they relate to supply of

goods or services.

It is to be noted that apart from above, any other

taxes, cess and surcharge as recommended by the

GST Council will be subsumed into GST.

Assessment is defined separately in different indirect