CLOSING THE PROSPERITY GAP

KEY POLICY AREAS

THE REGIONAL DIVIDEGreater London GVA- 171% of UK

West Wales and Valleys- 72.6% of UK

41000 jobs to be created in the Square Mile by 2023

40000 jobs needed in Valleys to reach average employment rate

Most geographically unequal nation in the EU

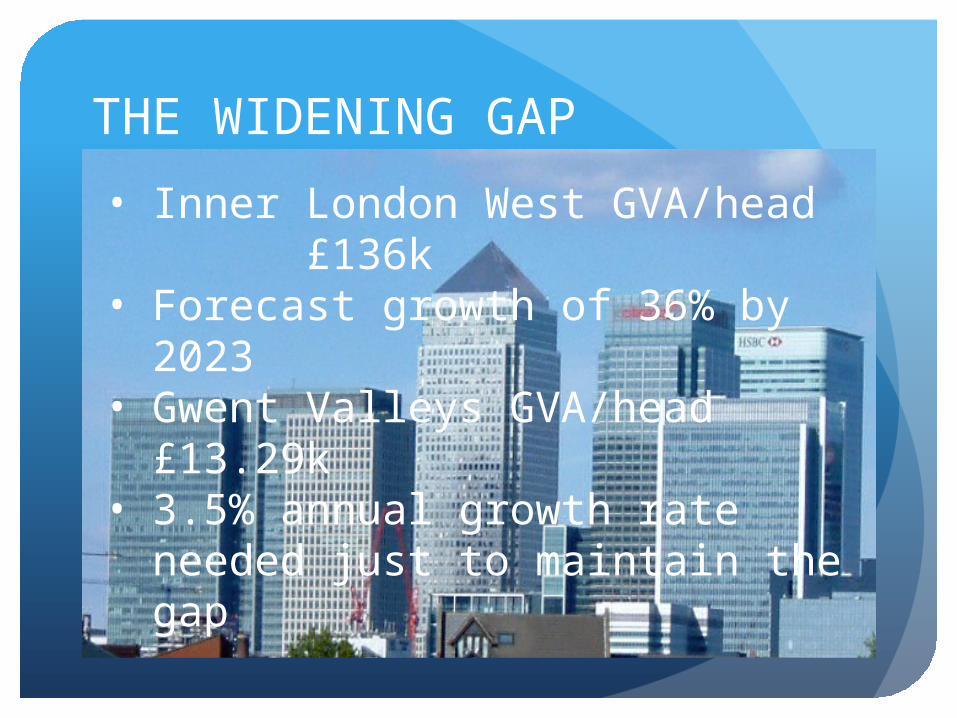

THE WIDENING GAP

• Inner London West GVA/head £136k

• Forecast growth of 36% by 2023• Gwent Valleys GVA/head

£13.29k• 3.5% annual growth rate

needed just to maintain the gap

OUTPUT PER HEAD

• UK £23394• England £24091• Scotland £21982• Northern Ireland £17948• Wales £16893• West Wales & Valleys £14763

LABOUR PRODUCTIVITY

Nominal GVA/hour worked – UK =100

England 101.5

Scotland 97.4

Wales 85.2

Northern Ireland 82.8

Complex reasons – low business investment, infrastructure, low rates of innovation and relatively low skills etc.

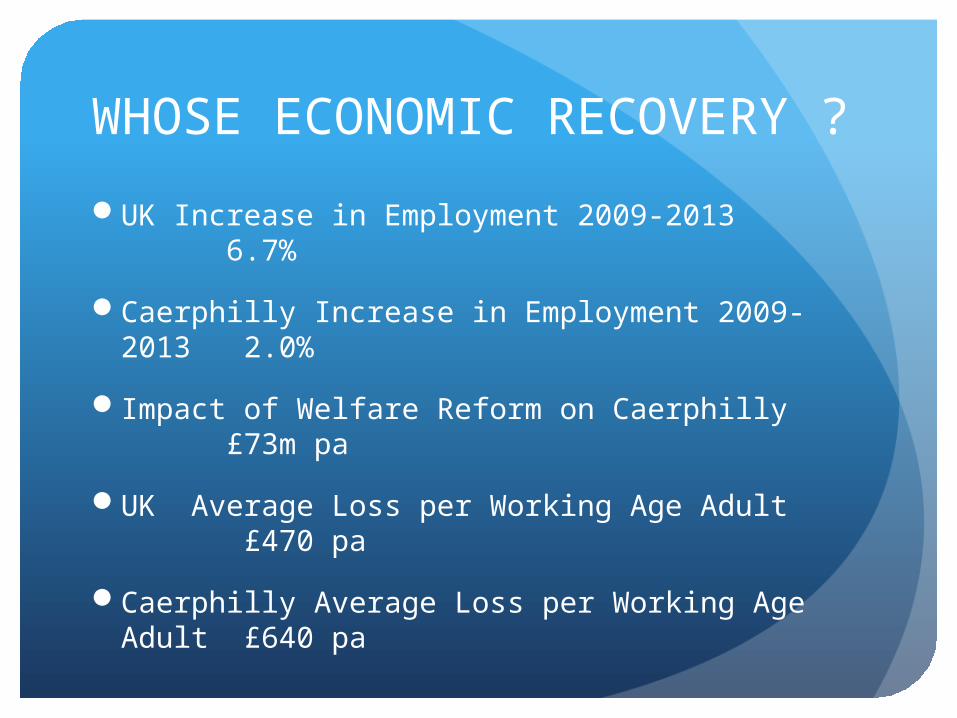

WHOSE ECONOMIC RECOVERY ?

UK Increase in Employment 2009-2013 6.7%

Caerphilly Increase in Employment 2009-2013 2.0%

Impact of Welfare Reform on Caerphilly £73m pa

UK Average Loss per Working Age Adult £470 pa

Caerphilly Average Loss per Working Age Adult £640 pa

RE-BALNCING THE ECONOMY

Growth will not close the gap – need redistribution of economic activity

Developing regional dimension to economic policy

Maximizing the impact of City Regions/City Deal

Devolving powers to local authorities

Reviving industrial investment and production

Targeting places and creating resilient economies

A PROACTIVE REGIONAL POLICY

Move Away from unsustainable South East - centric mentality

Target Investment on under-utilized assets in the regions such as land, labour, property and infrastructure

Include Regional Benefits Test in Government decision making

Build on the manufacturing base in the regions

Improve inter and intra regional connectivity

CARDIFF CAPITAL REGION

Need for labour market realism

Develop poly-centric approach

Role of infrastructure – Valleys Metro & M4 Relief Road

City Deal – opportunity to re-balance infrastructure spending?

Need to address governance & accountability issues

Needs versus opportunities

DEVOLVING POWER TO LOCAL AUTHORITIES

Combined Working

Fiscal devolution – flexibility over spending and borrowing

Building economic resilience through investment in skills, infrastructure and business support

Remove uncertainty

Promote strong leadership

REVIVNG THE MANUFACTURING SECTOR

Caerphilly – 22.5% jobs are in Manufacturing – almost 3x GB average

Maximize potential of Tier 1 Assisted Area Status with the balance in favour of grants rather than loans

Target business support finance on projects that improve productivity

Support successful companies as well as target sectors

Address skills mismatch and under-employment

Develop Anchor Companies

CREATING BETTER JOBS

UK has a higher proportion of lower skilled jobs than any other OECD country, except Spain

Low skilled jobs contributing to productivity gap & increasing in-work poverty

21 % of workers over-qualified for their jobs, up from 13% in 2011

40% of Welsh companies failing to invest in workforce

Need to build on WAG’s Employer Pledge

Enhanced role for anchor companies WAG’s apprenticeship programme & UK Futures programme

ROLE OF ANCHOR COMPANIES

Global companies have a significant presence in Wales

38 Anchor companies identified by WAG

Less than 1% of all companies but provide 40% of private sector employment

Tend to invest more in R&D and training

Generate more GVA that can be shared through the supply chain

Potential across all sectors to support diverse economy

Targeting Places and Creating Economic Resilience

Geography and decision making

Using procurement as a development tool – supply chains and SMEs

EU Funds – need for balance between large projects and local needs

Target Jobs Growth Wales on weaker labour markets

Re-focus Work Programme on skills , health, intermediate labour markets and local delivery

Some Final Thoughts

Move beyond simple employment numbers Commuting can widen job choice – but needs to be

accompanied by raising skills and earning potential Understand that where money is spent rather than

where it is earned is just as important to local economies

Avoid over-dependence on particular sectors Be better informed on local labour markets and the local

business environment Plan for all eventualities in a fast moving world No quick solutions – 1923 Special Development Areas!