Code of Conduct Assessment Report

UNACCO FINANCIAL SERVICES PRIVATE LIMITED

November 2015

________________________________________________________________________

Conducted by:

ACCESS ASSIST28A Hauz Khas VillageNew Delhi, 110 016Tel: +91 11 2651 0915, 2685 0821Mobile: +91 9748623494; +91 8794341531www.accessdev.org

For:

UNACCO FINANCIAL SERVICES PRIVATELIMITEDBuilding no-12, SB Complex, Radha Path,Bhetapara Chariali, Ward no-58Guwahati-781028Tel: +91 [email protected];[email protected]

UNACCO_________________________________________________________________________________________

____________________________________________________________________________________________Code of Conduct Assessment Report

Disclaimer

This Code of Conduct Assessment Report is meant for use by UNACCO Financial Services Pvt. Ltd. only.

This is a one-time assessment based on the information provided by UNACCO Financial Services Pvt.

Ltd. (UFSL) to ACCESS-ASSIST. ACCESS-ASSIST especially states that it has no financial liability

whatsoever to the subscribers/ users/ transmitters/ distributors of this report. ACCESS-ASSIST

reserves the right to suspend, withdraw or revise the MFI assessment at any point of time based on

any new information or unavailability of information or any other circumstances brought to ACCESS-

ASSIST’s notice which ACCESS-ASSIST may believe that it has impacted the assessment.

ACCESS-ASSIST's Code of Conduct Assessment reflects ACCESS-ASSIST’s current opinion on the ability

of a MFI to adhere to a Code of Conduct while delegating operation. The MFI assessment does not

constitute an audit of the assessed MFI by ACCESS-ASSIST. MFI assessment applies only to their

microfinance programmes. ACCESS-ASSIST’s MFI assessment is based on information provided by the

assessed MFI, or obtained from sources which ACCESS-ASSIST considers reliable. This assessment does

not opine on the MFI’s ability for timely payment of interest and principal. Nor it is a recommendation

to purchase, sell, or hold any financial instrument issued by the assessed MFI. The MFI grading

assigned by ACCESS-ASSIST cannot be used by the MFI in any form for mobilizing

deposits/savings/thrift from its members or general public.

© ACCESS-ASSIST – 2015

UNACCO_________________________________________________________________________________________

____________________________________________________________________________________________Code of Conduct Assessment Report

UNACCO Financial Services Pvt. Ltd.

Legal Form Private Ltd Co(NBFC) About UNACCO Financial Services Pvt Ltd

Date EstablishedInitiation of Operations

July 2008 UNACCO Financial Services Private Limited (UFSPL),the erstwhile Shavi Trexim & Holdings Private Limited(STHPL), is a non-banking financial company nondeposit (NBFC-ND). STHPL registered with RBI in1992, was engaged in the business of share trading andhire purchase financing. The present owners took overthe company in 2008 to use it as microfinance servicesdelivery channel and hence was changed from STHPLto UFSPL in 2009. The UFSPL has designed a loanproduct named as Income generating loan and alsoprovides insurance services to its group clients.

UFSPL entered the microfinance business in July 2008.As on March 31’ 2015, the promoters, Mr. N IrabantaSingh and associates, owned 53.72 percent stake inUFSPL, while Employee’s Trust and an NBFC held theremaining 46.28 percent.

As on March 31’ 2015, UFSPL has 27 branches across10 districts of Assam, 2 districts of Manipur, and 1district each of Tripura, West Bengal & Mizoram, withloans outstanding of Rs 360.28 million to 41,105borrowers. UFSPL follows the Joint Liability Group(JLG) model as on the above date, and lends to womengroup for income generating business purpose,

Operational Area• Covering through 27 branches in North-

Eastern region – Assam, Manipur, WestBengal, Tripura and Mizoram

Services and Products offered• Income generating Loan of amount

ranging from Rs 5,000 to Rs 25,000.• Insurance product in tie-up with Bajaj

Allianz Life Insurance through GroupTerm Life Insurance.

Lending Model• Follows the JLG model of lending

Average Score Rating Grade

3.34

3.50-4.00 AA

3.00-3.49 A

2.50-2.99 BB

2.00-2.49 B

1.50-1.99 CC

1.00-1.49 C

UNACCO_________________________________________________________________________________________

____________________________________________________________________________________________Code of Conduct Assessment Report

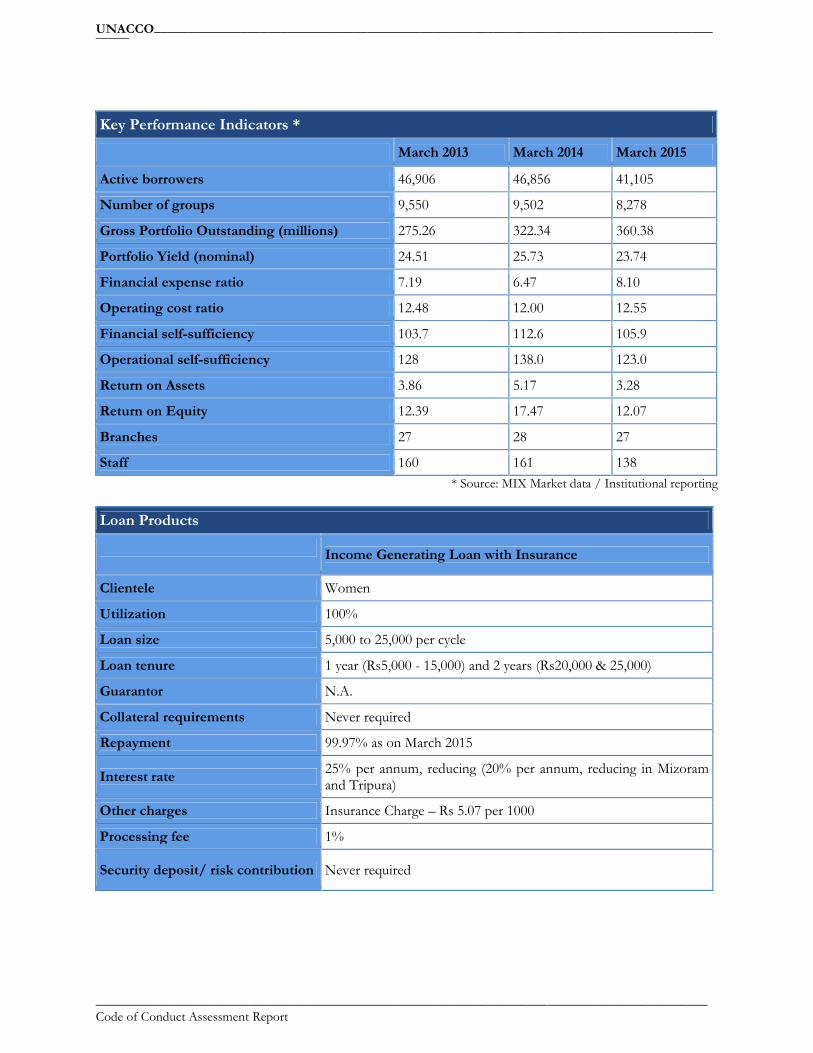

Key Performance Indicators *

March 2013 March 2014 March 2015

Active borrowers 46,906 46,856 41,105

Number of groups 9,550 9,502 8,278

Gross Portfolio Outstanding (millions) 275.26 322.34 360.38

Portfolio Yield (nominal) 24.51 25.73 23.74

Financial expense ratio 7.19 6.47 8.10

Operating cost ratio 12.48 12.00 12.55

Financial self-sufficiency 103.7 112.6 105.9

Operational self-sufficiency 128 138.0 123.0

Return on Assets 3.86 5.17 3.28

Return on Equity 12.39 17.47 12.07

Branches 27 28 27

Staff 160 161 138* Source: MIX Market data / Institutional reporting

Loan Products

Income Generating Loan with Insurance

Clientele Women

Utilization 100%

Loan size 5,000 to 25,000 per cycle

Loan tenure 1 year (Rs5,000 - 15,000) and 2 years (Rs20,000 & 25,000)

Guarantor N.A.

Collateral requirements Never required

Repayment 99.97% as on March 2015

Interest rate 25% per annum, reducing (20% per annum, reducing in Mizoramand Tripura)

Other charges Insurance Charge – Rs 5.07 per 1000

Processing fee 1%

Security deposit/ risk contribution Never required

UNACCO_________________________________________________________________________________________

____________________________________________________________________________________________Code of Conduct Assessment Report

HighlightsStrengths:

1. Board / Governance found to be robust and have a wide exposure and reputation in the microfinance andfinancial sector, giving an opportunity to the organisation to expand at a larger scale.

2. Training of Staff is found to be of utmost importance for both Field level and HQ level staffs. Inductionfound to be extensive covering 3 to 4 weeks for each staff (5 day office training and 20 to 21 days OJT).More the staff is aligned to the mission and vision of the organisation, better would be the effectiveness andefficiency of the staff

3. UFSPL’s employees maintain very high standards of conduct during their interactions with clients and couldbe validated during the client interaction.

4. The clients of the UFSPL are more than satisfied with the conduct of the staff and the operationaltimeliness, allowing them to emotionally connect with the organisation. Regardless of less amount of loangiven at initial stages compared to other MFIs, the clients seem to be well connected with the organisation.

5. Staffs have average experience of 3 to 5 years in similar industry and are emotionally connected to theorganisation. The trust factor has thus grown among them and are helping organisation to increase itsoperational sufficiency.

6. There is a proper system of storing documents collected from clients in a secure manner at UFSPL’sregistered office and is strictly followed.

7. UFSPL charges interest rates on reducing balance basis and makes efforts to communicate this to its clients.The clients interaction revealed that they were aware of the interest rates and other terms & conditions ofthe products & services offered.

8. Being a home grown MFI, the organisation can emotionally connect to the clients of north eastern areas dueto their indigenous characteristics and can develop healthy relation in the future.

Areas for Improvement:

1. The Code of Conduct found to be generic and could be modified further to personalise and align with themission and vision of the organisation.

2. Head office role found to be limited in appraisal process, hence can be improved through presence ofofficials from Head office in loan appraisal committee in random selection process to gauge the discussionsand see if any changes are required.

3. Very minimal use of written materials found for the clients awareness process. The mode of communicationalso found to be generic that is, majorly verbal. Hence the use of other modes and pamphlets and pagerscan be used to increase the branding of the organisation.

4. There is a need to conduct frequent review of products and services through client satisfaction surveys andother methods like market research of competitor’s product to be able to create a niche in the market anddistinct the organisation itself.

5. Feedback from the clients should be sought for at regular intervals to gauge the efficiency of the functionsof the organisation

6. Diversity of loan products. Specific activity loan products with required gestation periods could be launchedkeeping in view the target groups.

7. Incentive structure should be inculcated into the business function to increase the effectiveness of the staffwith respect to organisational growth.

8. Other services can also be provided to the client such as enterprise development products, healthprogramme / children’s education services, asset insurance, etc. to widen its market scope.

UNACCO_________________________________________________________________________________________

____________________________________________________________________________________________Code of Conduct Assessment Report

Code of Conduct Assessment Report for UNACCO Financial Services Pvt. Ltd.Summary of the studyThe overall grade obtained by UFSPL is 3.34, falling in the category of “A”, which indicates that the organization hasgood systems and adequate policies to ensure alignment and adherence to a developed Code of Conduct. UFSPLexcels in Governance, Code of Conduct, Human Resources and Loan Appraisal process, with defined practices thatare followed throughout. More could be done to improve the quality of newer products and services, Feedbackmechanisms and staff conduct.

The results of the nine broad assessment categories are summarized in the following table. Detailed analysis isprovided in the body of the report.

Baseline Results for UNACCO Financial Services Pvt. Ltd.Assessment Area Score (out of 4.00) Key Elements to be evaluated

Code of Conduct 3.64 Design, Visibility, Training (Staff), Refresher, Awareness(Staff), Awareness (Client),

Market Entry 3.50 Criteria for Identification, Procedure, Saturation, DueDiligence

Appraisal Process 3.33Client Data Collection, Repayment Capacity, DebtThresholds, Loan History, Processing Time, Approval,Verification

Client Comprehension 3.46Client Review Time, Explanatory Channels, Awareness,Disclosure of Price and Terms, Rights and Obligations,Training (Staff),

Products and Services 2.65 Design and Appropriateness, Review, Diversity,Convenience, Linkages

Pricing 3.55 Competition, Transparency, Fees, Security Deposit,Prepayment, Default

Feedback Mechanisms 3.20 Existence, Staff Training, Client Awareness, Usage,Checking, Staff Resources

Staff Conduct 3.20 Rule Book, General Training, Induction, Evaluation, Reviewof Conduct, Incentive/ Disincentive, Recovery/ Default

Governance 3.67 Responsibility, Role, Meeting Frequency, Attendance,Microfinance Experience, Composition

Human Resource 3.44 Field Staff experience/exposure in MF, Recruitment, StaffExit, Complaint Redressal

UNACCO_________________________________________________________________________________________

____________________________________________________________________________________________Code of Conduct Assessment Report

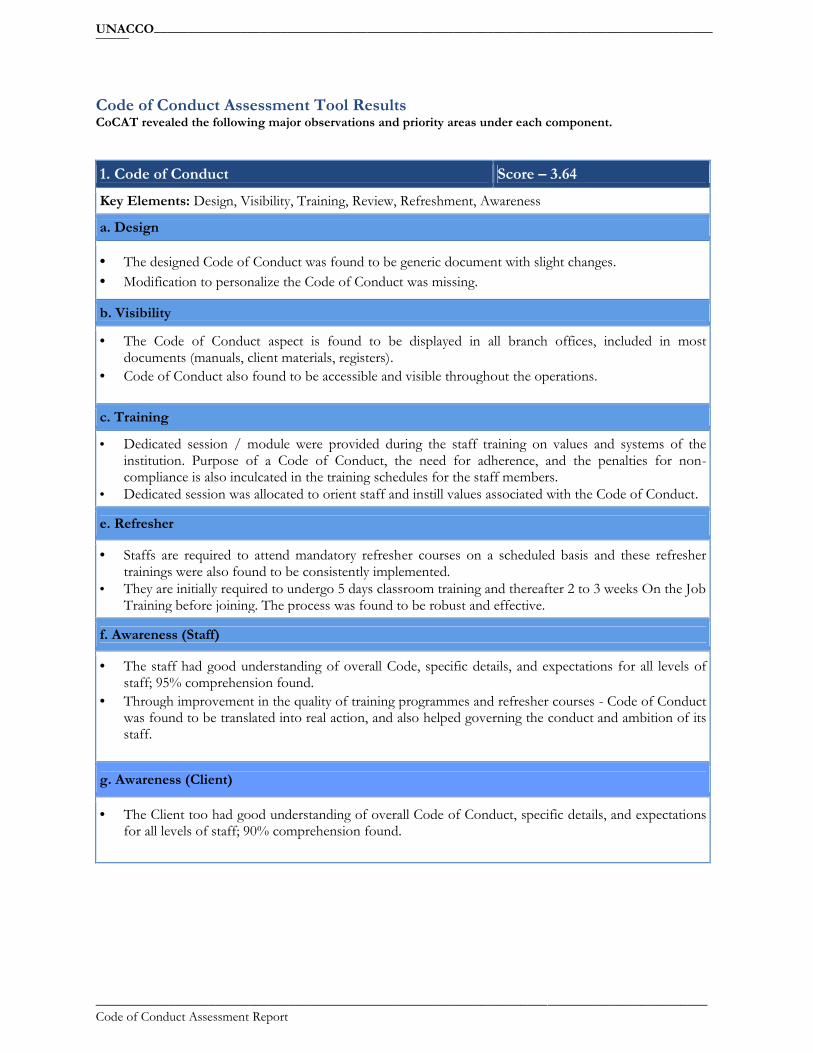

Code of Conduct Assessment Tool ResultsCoCAT revealed the following major observations and priority areas under each component.

1. Code of Conduct Score – 3.64Key Elements: Design, Visibility, Training, Review, Refreshment, Awareness

a. Design

The designed Code of Conduct was found to be generic document with slight changes. Modification to personalize the Code of Conduct was missing.

b. Visibility

The Code of Conduct aspect is found to be displayed in all branch offices, included in mostdocuments (manuals, client materials, registers).

Code of Conduct also found to be accessible and visible throughout the operations.

c. Training

Dedicated session / module were provided during the staff training on values and systems of theinstitution. Purpose of a Code of Conduct, the need for adherence, and the penalties for non-compliance is also inculcated in the training schedules for the staff members.

Dedicated session was allocated to orient staff and instill values associated with the Code of Conduct.

e. Refresher

Staffs are required to attend mandatory refresher courses on a scheduled basis and these refreshertrainings were also found to be consistently implemented.

They are initially required to undergo 5 days classroom training and thereafter 2 to 3 weeks On the JobTraining before joining. The process was found to be robust and effective.

f. Awareness (Staff)

The staff had good understanding of overall Code, specific details, and expectations for all levels ofstaff; 95% comprehension found.

Through improvement in the quality of training programmes and refresher courses - Code of Conductwas found to be translated into real action, and also helped governing the conduct and ambition of itsstaff.

g. Awareness (Client)

The Client too had good understanding of overall Code of Conduct, specific details, and expectationsfor all levels of staff; 90% comprehension found.

UNACCO_________________________________________________________________________________________

____________________________________________________________________________________________Code of Conduct Assessment Report

2. Market Entry Score – 3.50Key Elements: Identification, Procedure, Saturation, Due Diligence

a. Identification

Rules clearly specify quantitative parameters that qualify the target population (income level, assets,opportunities)

Parameters for Identification of new location is found to be well defined Systems were put in place with specific parameters that help identify the intended population to be

served

b. Procedure

The practice includes general community survey along with random household visits; communicationwith other MFIs in the locality, as well as village panchayat or local government.

Also had an established written protocol for market entry; generate surveys and questionnaires thatfacilitate the process and allow for an inclusive perspective

c. Saturation

Serving a market with 2 existing MFIs Identify areas with a very underdeveloped credit market, where the impact of microfinance is much

larger and the risks of multiple lending are tempered Found to be doing business majorly with less MFI operating areas and hence is an opportunity to

explore into the deep pockets.

d. Due Diligence

Extensive and intensive research conducted by all departments to ensure that every aspect of thecommunity is satisfactory, and that expansion is aligned with the institution’s vision

All the major departments like Operations, Administrations and Finance found to be mutuallyinvolved in the validation process.

Established procedures found for market entry that require the entire organization to be involved,from the field staff who conduct the same to the board who reviews and approves.

UNACCO_________________________________________________________________________________________

____________________________________________________________________________________________Code of Conduct Assessment Report

3. Appraisal Process Score – 3.33Key Elements: Client Data Collection, Repayment Capacity, Debt Thresholds, Loan History, ProcessingTime, Approval, Verification

a. Client Data Collection

Found to be well structured through usage of verbal collection, most information is in documentationform according to the guidelines and are closely followed.

Focus more closely on written documentation, regardless of literacy problems; create an appraisaltemplate with space for all information to be written, in addition to notes.

b. Repayment Capacity

Loan appraisals are critically evaluated, also household incomes, expenditures, assets and liabilities arecollected and maintained at both Branch and Head Office.

Standard time is allocated to the measure repayment capacity using few channels as possible to gaugethe financial status of an individual or household as a whole, which includes home visits and cross-verification from other group members.

Repayment capacity is also mapped through other channels like– exchange of information from otherMFIs informally, Highmark database, personal visits, etc.

c. Debt Thresholds

Threshold is conditional on at least 2 parameters, including income, expenditure, assets, outstanding,etc.

Maintained a system for capturing explicitly limits and monitors indebtedness of the clients.

d. Loan History

Found to be fully reviewed and considered throughout the appraisal process Aggregate materials, whether paper or MIS, to ensure that the client’s entire profile is available for

review; also beneficial for staff to prepare themselves for client meetings or appraisal.

e. Processing Time

1-2 weeks Processing time is found to be acceptable among the clients, in case of first loans. However, for

subsequent loans, they felt the time taken is more and hence need to enhance the delivery.

f. Approval

Different levels of field operations through a credit committee. Head office role in approval is limited.

g. Verification

Verification by Internal audit found to be done once in 2 months and are regular in nature. Internal audits conducts reviews of the appraisal process, the level of detail and accuracy in the

application process, and all other details; entire sample is selected from each branch office on amonthly basis.

UNACCO_________________________________________________________________________________________

____________________________________________________________________________________________Code of Conduct Assessment Report

4. Client Comprehension Score – 3.46Key Elements: Client Review Time, Explanatory Channels, Verification, Disclosure of Price and Terms,Rights and Obligations, Staff Training

a. Client Review Time

Enough review time given to Clients, normally found 3 to 7 days given. Ample time given tounderstand and review the loan terms, pricing, format, and other details of the product

Clients are also allowed additional time to review products, ask questions, and consider their options.

b. Explanatory Channels

Numerous channels and sessions found to be used to educate and explain information; includingverbal explanation, written documentation (both personal and public), along with other materials

4-5, average meetings found to be organised for explanation session and are majorly verbalcommunications.

Clients found to be well versed with the process.

c. Awareness

Oral and limited written (within literacy limitations); attempts made to informally test each person’soral understanding.

Thorough disclosure of price & terms found in the field. However, the awareness of mechanisms forgrievance redressal mechanisms was limited.

d. Disclosure of Price and Terms

Disclosure of conditions were found to be full and thorough, both verbal and written materials; allpricing information is broken into fees/interest/principal for a standard amount (per Rs1,000)

Pricing found to be clear, and expresses in an easy-to-understand format; schedules also found to beprovided, with either numbered weeks or specific dates.

e. Rights and Obligations

Rights and Obligations were fully explained and reviewed with each client of each group came intodisplay during the discussion with the clients.

Clients had a clear understanding of the terms of their relationship with the financial institution;(expectations for conduct, right to express grievances and other actions)

f. Staff Training

Dedicated modules were provided to the staff as an examples and guidance for how to interact withclients.

Field staff were given communications training to deal with problems of education or literacy, but alsoto make sure that terms, rights, and other vital information is expressed in a clear and coherentmanner and are found to be general.

UNACCO_________________________________________________________________________________________

____________________________________________________________________________________________Code of Conduct Assessment Report

5. Products and Services Score – 2.65Key Elements: Design and Appropriateness, Review, Diversity, Convenience, Linkages

a. Design and Appropriateness

Modifications could be seen to suit specific needs of the community requirement and also designedand tweaked on the basis of demand of target clients.

Microfinance aims to provide appropriate and prudent financial services to the poor; this requiresproduct design that directly accounts for the specific needs and demands of clients, which was foundto be available in terms of designing

b. Review

Annual review of products with track record of modifications found, based on which changes havebeen made by increasing the loan size to Rs 25,000.

Product review found to be done at regular intervals which can also serve as something of a clientreview, observing how well the products can match the client needs, and whether there are problemsat either end that require resolution.

c. Diversity

Less diversity found in the product portfolio - actual products are very similar with hardly anynoticeable difference.

Less consideration found among the differentiation of existing income generating loan products tobetter serve current and future clients.

d. Convenience

Found to be Moderate as meeting requires weekly / fortnightly center meetings of all group membersbut doorstep delivery and collection are done from group leaders (not members)

Required efforts to reduce the burdens of time and energy of the clients is also being considered andfound to be delivering credit and taking repayments in a less intrusive, less intensive manner.

More than 90% of the clients found to be satisfied with operational process of UFSPL.

e. Linkages

Only 1 linked product with added value found i.e., Life Insurance in tie-up with Bajaj Allianz LifeInsurance

Plan to add new products that cater to client needs.

UNACCO_________________________________________________________________________________________

____________________________________________________________________________________________Code of Conduct Assessment Report

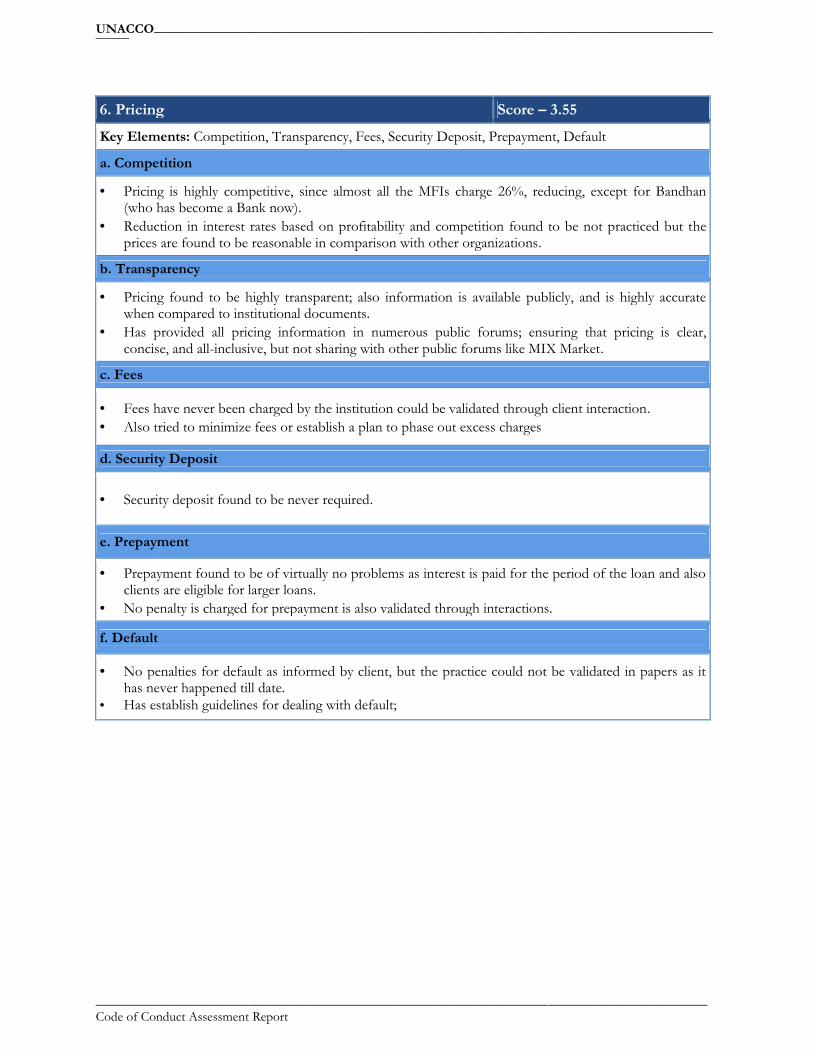

6. Pricing Score – 3.55Key Elements: Competition, Transparency, Fees, Security Deposit, Prepayment, Default

a. Competition

Pricing is highly competitive, since almost all the MFIs charge 26%, reducing, except for Bandhan(who has become a Bank now).

Reduction in interest rates based on profitability and competition found to be not practiced but theprices are found to be reasonable in comparison with other organizations.

b. Transparency

Pricing found to be highly transparent; also information is available publicly, and is highly accuratewhen compared to institutional documents.

Has provided all pricing information in numerous public forums; ensuring that pricing is clear,concise, and all-inclusive, but not sharing with other public forums like MIX Market.

c. Fees

Fees have never been charged by the institution could be validated through client interaction. Also tried to minimize fees or establish a plan to phase out excess charges

d. Security Deposit

Security deposit found to be never required.

e. Prepayment

Prepayment found to be of virtually no problems as interest is paid for the period of the loan and alsoclients are eligible for larger loans.

No penalty is charged for prepayment is also validated through interactions.

f. Default

No penalties for default as informed by client, but the practice could not be validated in papers as ithas never happened till date.

Has establish guidelines for dealing with default;

UNACCO_________________________________________________________________________________________

____________________________________________________________________________________________Code of Conduct Assessment Report

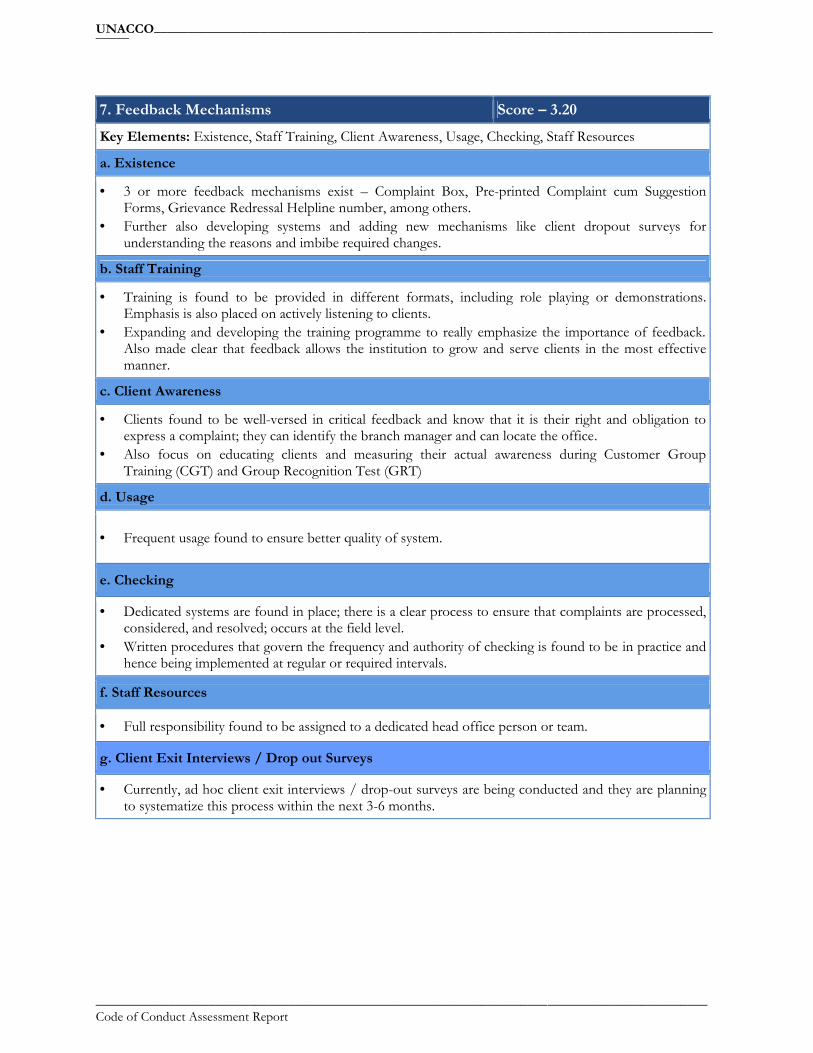

7. Feedback Mechanisms Score – 3.20Key Elements: Existence, Staff Training, Client Awareness, Usage, Checking, Staff Resources

a. Existence

3 or more feedback mechanisms exist – Complaint Box, Pre-printed Complaint cum SuggestionForms, Grievance Redressal Helpline number, among others.

Further also developing systems and adding new mechanisms like client dropout surveys forunderstanding the reasons and imbibe required changes.

b. Staff Training

Training is found to be provided in different formats, including role playing or demonstrations.Emphasis is also placed on actively listening to clients.

Expanding and developing the training programme to really emphasize the importance of feedback.Also made clear that feedback allows the institution to grow and serve clients in the most effectivemanner.

c. Client Awareness

Clients found to be well-versed in critical feedback and know that it is their right and obligation toexpress a complaint; they can identify the branch manager and can locate the office.

Also focus on educating clients and measuring their actual awareness during Customer GroupTraining (CGT) and Group Recognition Test (GRT)

d. Usage

Frequent usage found to ensure better quality of system.

e. Checking

Dedicated systems are found in place; there is a clear process to ensure that complaints are processed,considered, and resolved; occurs at the field level.

Written procedures that govern the frequency and authority of checking is found to be in practice andhence being implemented at regular or required intervals.

f. Staff Resources

Full responsibility found to be assigned to a dedicated head office person or team.

g. Client Exit Interviews / Drop out Surveys

Currently, ad hoc client exit interviews / drop-out surveys are being conducted and they are planningto systematize this process within the next 3-6 months.

UNACCO_________________________________________________________________________________________

____________________________________________________________________________________________Code of Conduct Assessment Report

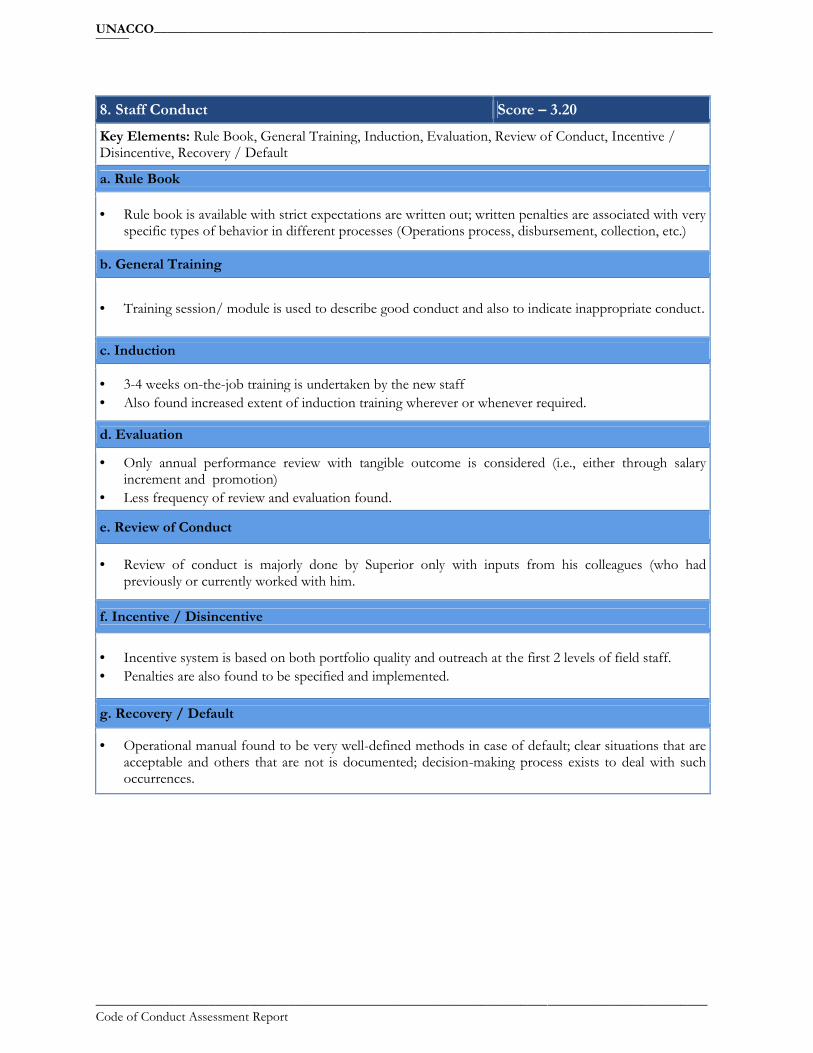

8. Staff Conduct Score – 3.20Key Elements: Rule Book, General Training, Induction, Evaluation, Review of Conduct, Incentive /Disincentive, Recovery / Default

a. Rule Book

Rule book is available with strict expectations are written out; written penalties are associated with veryspecific types of behavior in different processes (Operations process, disbursement, collection, etc.)

b. General Training

Training session/ module is used to describe good conduct and also to indicate inappropriate conduct.

c. Induction

3-4 weeks on-the-job training is undertaken by the new staff Also found increased extent of induction training wherever or whenever required.

d. Evaluation

Only annual performance review with tangible outcome is considered (i.e., either through salaryincrement and promotion)

Less frequency of review and evaluation found.

e. Review of Conduct

Review of conduct is majorly done by Superior only with inputs from his colleagues (who hadpreviously or currently worked with him.

f. Incentive / Disincentive

Incentive system is based on both portfolio quality and outreach at the first 2 levels of field staff. Penalties are also found to be specified and implemented.

g. Recovery / Default

Operational manual found to be very well-defined methods in case of default; clear situations that areacceptable and others that are not is documented; decision-making process exists to deal with suchoccurrences.

UNACCO_________________________________________________________________________________________

____________________________________________________________________________________________Code of Conduct Assessment Report

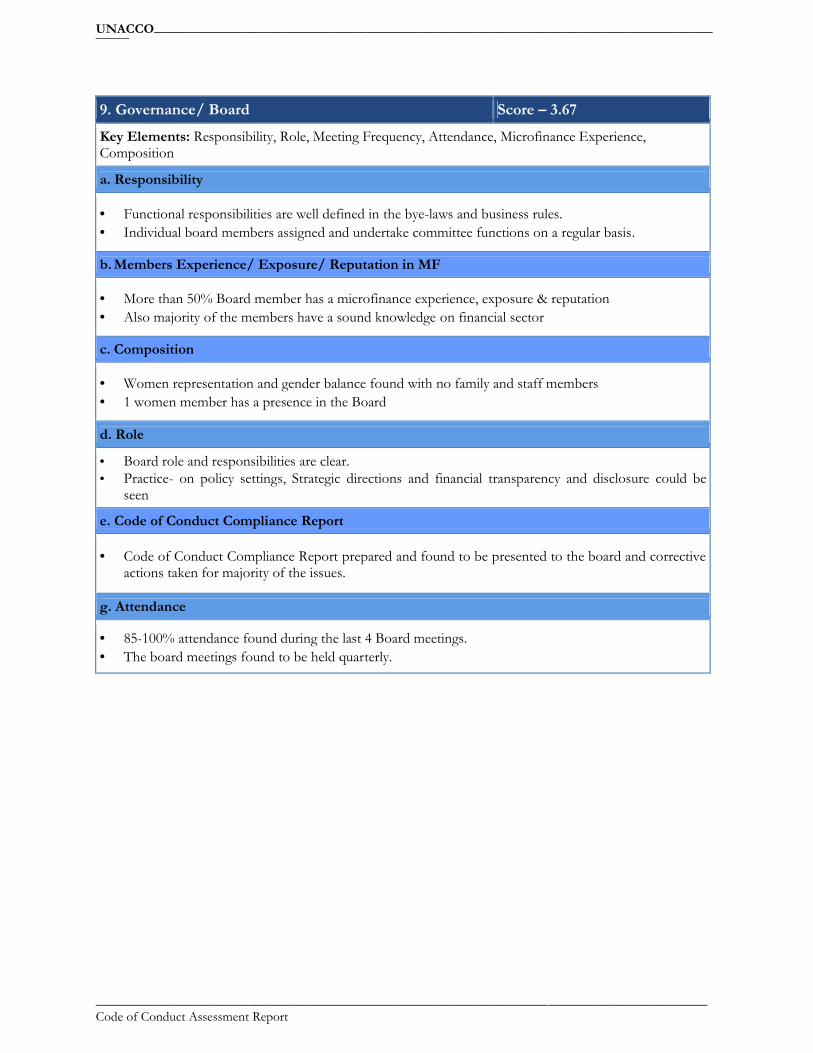

9. Governance/ Board Score – 3.67Key Elements: Responsibility, Role, Meeting Frequency, Attendance, Microfinance Experience,Composition

a. Responsibility

Functional responsibilities are well defined in the bye-laws and business rules. Individual board members assigned and undertake committee functions on a regular basis.

b. Members Experience/ Exposure/ Reputation in MF

More than 50% Board member has a microfinance experience, exposure & reputation Also majority of the members have a sound knowledge on financial sector

c. Composition

Women representation and gender balance found with no family and staff members 1 women member has a presence in the Board

d. Role

Board role and responsibilities are clear. Practice- on policy settings, Strategic directions and financial transparency and disclosure could be

seen

e. Code of Conduct Compliance Report

Code of Conduct Compliance Report prepared and found to be presented to the board and correctiveactions taken for majority of the issues.

g. Attendance

85-100% attendance found during the last 4 Board meetings. The board meetings found to be held quarterly.

UNACCO_________________________________________________________________________________________

____________________________________________________________________________________________Code of Conduct Assessment Report

10. Human Resources Score - 3.44

Key Elements: Field Staff experience/exposure in MF, Recruitment, Staff Exit, Complaint Redressal

a. Field Staff experience/exposure in MF

Field staff found to have average experience of 3-5 year in micro finance or relevant sector

b. Recruitment

Recruitments are conducted with reference checks from previous employer (MFI or any otherinstitution)

The HR policy has a structured system w.r.t the Recruitment and is strictly adhered.

c. Staff Exit

Staff exit interviews conducted for all staff quitting and action taken to resolve the issues.

d. Complaint Redressal

Dedicated systems are put in place. There is a clear process to ensure that complaints are processed,considered, and resolved.

The grievance redressal committee is endorsed with the process implementation. As on date verylimited usage could be noticed.

UNACCO_________________________________________________________________________________________

____________________________________________________________________________________________Code of Conduct Assessment Report

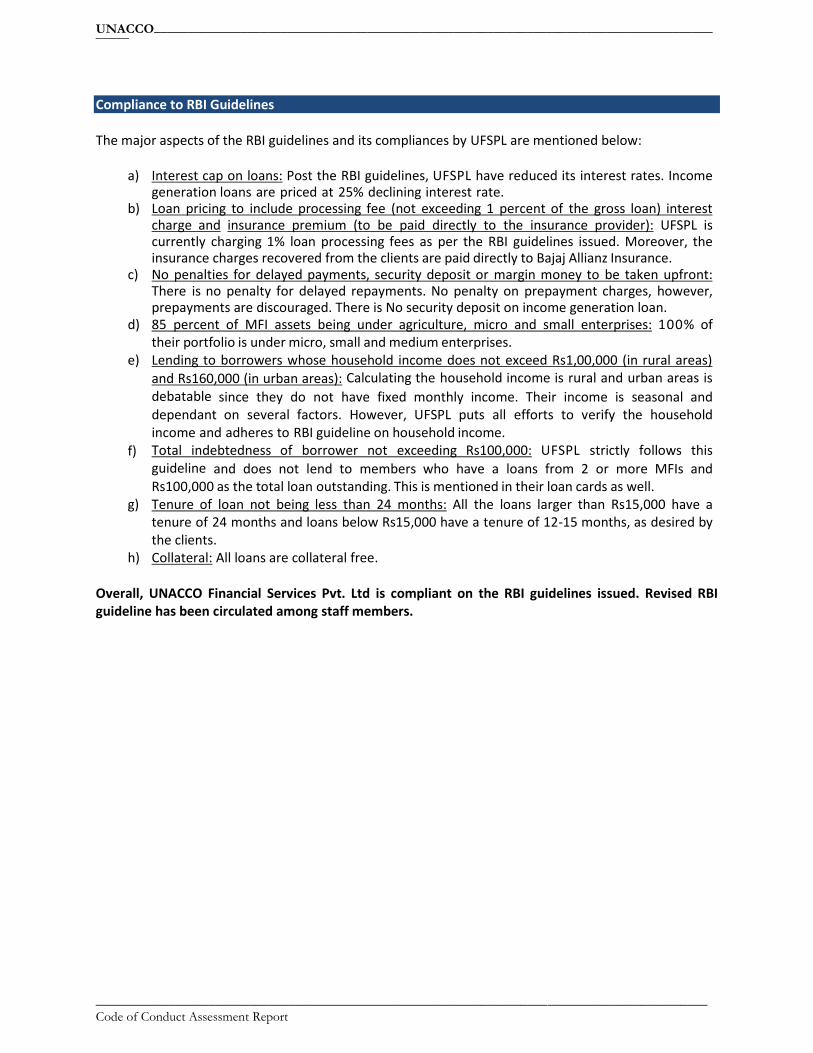

Compliance to RBI Guidelines

The major aspects of the RBI guidelines and its compliances by UFSPL are mentioned below:

a) Interest cap on loans: Post the RBI guidelines, UFSPL have reduced its interest rates. Incomegeneration loans are priced at 25% declining interest rate.

b) Loan pricing to include processing fee (not exceeding 1 percent of the gross loan) interestcharge and insurance premium (to be paid directly to the insurance provider): UFSPL iscurrently charging 1% loan processing fees as per the RBI guidelines issued. Moreover, theinsurance charges recovered from the clients are paid directly to Bajaj Allianz Insurance.

c) No penalties for delayed payments, security deposit or margin money to be taken upfront:There is no penalty for delayed repayments. No penalty on prepayment charges, however,prepayments are discouraged. There is No security deposit on income generation loan.

d) 85 percent of MFI assets being under agriculture, micro and small enterprises: 100% oftheir portfolio is under micro, small and medium enterprises.

e) Lending to borrowers whose household income does not exceed Rs1,00,000 (in rural areas)and Rs160,000 (in urban areas): Calculating the household income is rural and urban areas isdebatable since they do not have fixed monthly income. Their income is seasonal anddependant on several factors. However, UFSPL puts all efforts to verify the householdincome and adheres to RBI guideline on household income.

f) Total indebtedness of borrower not exceeding Rs100,000: UFSPL strictly follows thisguideline and does not lend to members who have a loans from 2 or more MFIs andRs100,000 as the total loan outstanding. This is mentioned in their loan cards as well.

g) Tenure of loan not being less than 24 months: All the loans larger than Rs15,000 have atenure of 24 months and loans below Rs15,000 have a tenure of 12-15 months, as desired bythe clients.

h) Collateral: All loans are collateral free.

Overall, UNACCO Financial Services Pvt. Ltd is compliant on the RBI guidelines issued. Revised RBIguideline has been circulated among staff members.

UNACCO_________________________________________________________________________________________

____________________________________________________________________________________________Code of Conduct Assessment Report

Conclusion

UNACCO Financial Services Pvt. Ltd has achieved a composite CoCAT score of 3.34 with an overall gradeof “A”, indicating that the organisation is growing and matured. Although there is strong institutionalperformance in some areas, there is room to provide technical assistance with a view of strengtheningsystems.

Highlights and best practices:

1. Board / Governance found to be robust and have a wide exposure and reputation in the microfinance andfinancial sector, giving an opportunity to the organisation to expand at a larger scale.

2. Training of Staff is found to be of utmost importance for both Field level and HQ level staffs. Induction foundto be extensive covering 3 to 4 weeks for each staff (5 day office training and 20 to 21 days OJT). More thestaff is aligned to the mission and vision of the organisation, better would be the effectiveness and efficiency ofthe staff

3. UFSPL’s employees maintain very high standards of conduct during their interactions with clients and could bevalidated during the client interaction.

4. The clients of the UFSPL are more than satisfied with the conduct of the staff and the operational timeliness,allowing them to emotionally connect with the organisation. Regardless of less amount of loan given at initialstages compared to other MFIs, the clients seem to be well connected with the organisation.

5. Staffs have average experience of 3 to 5 years in similar industry and are emotionally connected to theorganisation. The trust factor has thus grown among them and are helping organisation to increase itsoperational sufficiency.

6. There is a proper system of storing documents collected from clients in a secure manner at UFSPL’s registeredoffice and is strictly followed.

7. UFSPL charges interest rates on reducing balance basis and makes efforts to communicate this to its clients.The clients interaction revealed that they were aware of the interest rates and other terms & conditions of theproducts & services offered.

8. Being a home grown MFI, the organisation can emotionally connect to the clients of north eastern areas due totheir indigenous characteristics and can develop healthy relation in the future.

Areas for Improvement:

1. The Code of Conduct found to be generic and could be modified further to personalise and align with themission and vision of the organisation.

2. Head office role found to be limited in appraisal process, hence can be improved through presence of officialsfrom Head office in loan appraisal committee in random selection process to gauge the discussions and see ifany changes are required.

3. Very minimal use of written materials found for the clients awareness process. The mode of communicationalso found to be generic that is, majorly verbal. Hence the use of other modes and pamphlets and pagers can beused to increase the branding of the organisation.

4. There is a need to conduct frequent review of products and services through client satisfaction surveys andother methods like market research of competitor’s product to be able to create a niche in the market anddistinct the organisation itself.

5. Feedback from the clients should be sought for at regular intervals to gauge the efficiency of the functions ofthe organisation

6. Diversity of loan products. Specific activity loan products with required gestation periods could be launchedkeeping in view the target groups.

7. Incentive structure should be inculcated into the business function to increase the effectiveness of the staffwith respect to organisational growth.

8. Other services can also be provided to the client such as enterprise development products, health programme /children’s education services, asset insurance, etc. to widen its market scope.

UNACCO_________________________________________________________________________________________

____________________________________________________________________________________________Code of Conduct Assessment Report

Average Score Rating Grade

3.34

3.50-4.00 AA

3.00-3.49 A

2.50-2.99 BB

2.00-2.49 B

1.50-1.99 CC

1.00-1.49 C

UNACCO_________________________________________________________________________________________

____________________________________________________________________________________________Code of Conduct Assessment Report

Annexure 1: Code of Conduct Assessment Tool (CoCAT)

IntroductionThe Code of Conduct Assessment Tool (CoCAT) is a comprehensive instrument used to measure thedevelopment and implementation of policies that best serve the client. Starting with the Code of Conduct,CoCAT determines whether written procedures have been generated in accordance with the mission andvision of the institution. Through a careful analysis of internal documents and conversations with staffmembers, CoCAT seeks to analyse the alignment between theory and reality, checking at all levels to see howwell policies align with practice. Where possible, CoCAT tries to quantify the parameters to removesubjectivity.

CoCAT has been developed to address some of the ideas that are implicit in Social Performance and ClientProtection, but to do so in a structured manner with set parameters that have to be fulfilled. One of the majortenets of this tool is analysing the quality of service provided by the staff, and the quality of delivery offeredto the client. Ultimately, the tool is used to identify important policies that could strengthen practices,enhancing the relationship between customer and institution.

CoCAT has 9 broad assessment components which are further disaggregated into 53 elements. The 9 broadcomponents are: Code of Conduct, Market Entry, Appraisal Process, Client Comprehension, Products and Services, Pricing,Feedback Mechanisms, Staff Conduct, and Governance.

Each component is made up of between 4 and 7 elements. Each element has been allocated a Weight thatranges from 1% to 3% of the total score. The components are weighted according to the sum of theirconstituent elements. These elements are given a Score from “1” (Lacking) to “4” (Excellent). In case anelement is not applicable, it is removed from the overall rating and the weights are adjusted accordingly.

CoCAT helps to:

• Generate baseline information on institutional conduct and the relationship between staff and clients• Build a practical, experiential profile of the institution’s methodology• Understand the formal institutional processes that govern client interactions• Analyse the institutional mentality and correspondence between social and financial missions• Provide detailed information on best practices being followed by the institution

Methodology

CoCAT is administered in a participatory manner and is a multi-stage process:

1. Collection of primary and secondary data: Website, Annual reports, Audited financial statements;Institutional manuals (HR, Operations, IA), Training materials; 3rd party ratings, etc.

2. Structured discussions: Board, Senior Management, Head office staff, Field personnel

3. Field visit: Branch office discussions with field personnel, meetings with clients, observation of differentstages of the operational process

CoCAT is largely based on observation of behaviour, conduct, and practices. Although the premise is theexistence of a Code of Conduct, the tool is really meant to monitor compliance with the principles laid out bythe organization. If broad principles are missing from the institution’s consideration, these will be identified.Other standards may be written, but may not be turned into any meaningful practice. CoCAT differentiatesbetween each of these, and provides a comprehensive portrait of the institution’s ability to focus on itsclients, serving them ethically and responsibly.

UNACCO_________________________________________________________________________________________

____________________________________________________________________________________________Code of Conduct Assessment Report

Annexure 2: List of Branch Offices visited and number of clients visited

S.No Name of Branch Office Number of Clients Visited1 Morigaon 122 Sonarpur 143 Mirza 124 Chhayagaon 275 Beltola 166 Mangaldoi 47

Total 128