1Confidential

The Changing Canadian M&A MarketFEI Canada Breakfast Seminar

TRANSACTION ADVISORY SERVICES

March/April 2006

2Confidential

M&A Market Participants

DatePrivate and Confidential

3Confidential

M&A Market Participants

Market participants and their roles are changing in today’s transaction environment: Strategic Acquirers

Private Equity Groups

Public Markets

4Confidential

strategic acquirers

5Confidential

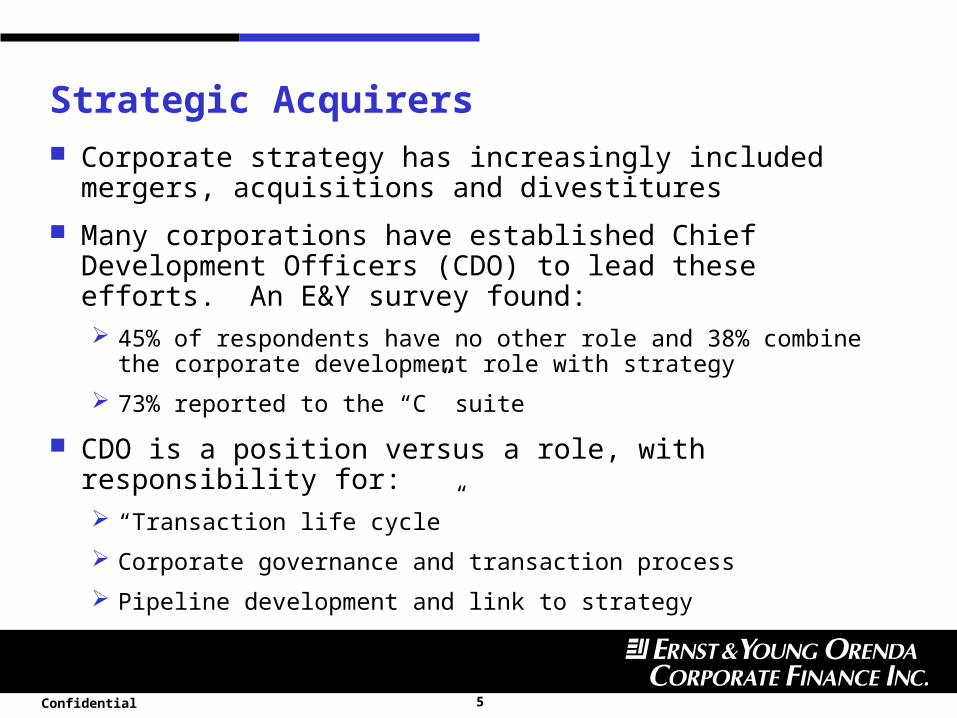

Strategic Acquirers Corporate strategy has increasingly included mergers, acquisitions and

divestitures Many corporations have established Chief Development Officers

(CDO) to lead these efforts. An E&Y survey found: 45% of respondents have no other role and 38% combine the corporate

development role with strategy

73% reported to the “C” suite

CDO is a position versus a role, with responsibility for: “Transaction life cycle”

Corporate governance and transaction process

Pipeline development and link to strategy

6Confidential

Strategic Acquirers (cont’d)

77%

70%

38%

31%

21%

18%

11%

10%

9%

6%

0 20 40 60 80 100

Human Resources

Risk Management

Information Technology

Tax

Sales and Marketing

Treasury

Legal

Operations

Strategic Planning

Finance/Accounting

Note: Percentage is of total population – 175 all Companies

CDO – Functional Skills

7Confidential

private equity groups (PEGs)

8Confidential

Private Equity Groups

PEGs represent a large and growing source of capital (funds raised 2001-2004):

1.51.8

2.4

3.6

0.6 0.7 0.71

0

0.5

1

1.5

2

2.5

3

3.5

4

2001 2002 2003 2004

Buyout

Mezzanine

Source: Thomson Macdonald

9Confidential

Private Equity Groups (cont’d)

PEG funds were invested in a diverse set of transaction types:

MBO 29%

Acquisitions 22%Refinancing 16%Other 1%

Restructuring16%

Expansion 17%

Source: Thomson Macdonald

10Confidential

Private Equity Groups (cont’d)

The growth in private equity groups also masks some important underlying changes: Buy out pools now represent nearly half of the private equity universe

Private-independent fund managers gain importance:— Account for close to 40% of capital under management— Gaining share as they draw commitments from institutional investors and reorganize

from corporate funds

11Confidential

Private Equity Groups (cont’d)

These fund managers generally have a diverse background (investment banking, legal and operational) and have a strong understanding of return/risk

Vendors may prefer to deal with PEGs:—Not a competitor and therefore less concerns with confidentiality—Clear financial metrics—May have greater structuring flexibility (e.g., vendor retains a minority stake)

12Confidential

income trusts

13Confidential

Income Trusts

57 64

98

134

165

233 240

$0

$50

$100

$150

$200

$250

$300

2000 2001 2002 2003 2004 2005 2006

0

50

100

150

200

250

300Market Capitalization

Number of Trusts

Ma

rke

t Ca

pita

liza

tion

(C$

bill

ion

s)

Nu

mb

er o

f Tru

sts

Source: Scotia Capital

14Confidential

Income Trusts (cont’d) – Total Issuance

Source: Scotia Capital

15Confidential

Income Trusts (cont’d) – IPO Size Distribution (2001-2006 YTD)

10

32

23

18

12

57

0

5

10

15

20

25

30

35

<$50 $50-$100 $100-$150 $150-$200 $200-$250 $250-$300 >$300

Nu

mb

er

of D

ea

ls

Average: $148.6

Offering Size (C$ Millions)

16Confidential

Income Trusts (cont’d) – Leverage and Yield

2325

36

6

16

0

5

10

15

20

25

30

35

40

<1.0x 1.0x - 1.5x 1.5x - 2.0x 2.0x - 2.5x >2.5x

Num

ber

of IP

O's

Average: $1.6x

IPO Leverage Income Trust IPO Yield

1

1013

22

28

21

75

0

5

10

15

20

25

30

35

40

<8.00% 8.00% -9.00%

9.00% -10.00%

10.00% -11.00%

11.00% -12.00%

12.00%-13.00%

13.00%-14.00%

> 14.00%N

um

be

r o

f IP

O's

Average: 11.00%

Source: Scotia Capital

17Confidential

Income Trusts (cont’d) – Retained Interest (2001-2006 YTD)

23

10

22

1113

10

17

0

5

10

15

20

25

<10% 10% - 20% 20% - 30% 30% - 40% 40% - 50% 50% - 60% >60%

Num

ber

of D

eals

Average: 32%

Source: Scotia Capital

18Confidential

implications for transactions

19Confidential

Implications for transactions

There is a robust market for Canadian companies: Significant interest from strategic purchasers, both within Canada and

internationally

Broad availability of capital:— Private market through PEGs— Public market, where Income Trusts provide attractive valuations

20Confidential

Implications for transactions (cont’d)

A recent Ernst & Young survey on mid-market companies revealed some interesting insight:

—Of companies which used an advisor, 37% were sold to purchasers outside Canada

—21% of vendors were acquired by a financial buyer.

21Confidential

Financing in Today’s M&A Market

22Confidential

Overview: State of the Capital Markets

As the economy firms and absolute interest rates remain relatively low, lenders and investors are becoming increasingly more comfortable with higher leverage levels

23Confidential

Overview: Leverage Has Increased in the Market

Source: S&P/Loan Pricing Corporation

5.3x 4.5

x 4.1x 3.7

x3.8x

4.0x

4.4x

24Confidential

Overview: Leverage Has Increased in the Market (cont’d)

Source: Bank of America/S&P/Loan Pricing Corporation

Includes 2nd lien debt which pushes up senior leverage

25Confidential

3.5

4

4.5

5

5.5

6

6.5M

ax. d

ebt t

o EBI

TDA

1997 1998 1999 2000 2001 2002 2003 2004 2005

Sponsored LBO

Overview: Leverage Has Increased in the Market (cont’d)

Source: Reuters Loan Pricing Corporation/Deal Scan

The oversupply of funds also resulted in lenders relaxing covenant levels

In particular, average debt to EBITDA covenants for LBO financings increased dramatically in 2005

26Confidential

Availability of Non-Traditional Financing

Target Return% p.a.

Risk

5 10 15 20 25 30 35

EQUITY

SUB DEBT

SCLs / High yield

notes

ABLs

Bank / Senior Notes

There has been an ongoing shift away from traditional bank structures to multi-tiered structures

27Confidential

Availability of Non-Traditional Financing (cont’d)

COMPANY SIZE:

Very Small Small Mid-Size Large

Typically has limited resources and no track record.

Possibly has high growth potential, but often with limited track record.

Typically has proven track record and continued growth potential. Substantial assets/stock available for collateral.

Known track record and risk. Strong financial flexibility.

LOW

HIGH

Ris

k

Commercial Paper

Private Placement Senior Notes and Senior Unsecured Debt

Asset Monetization

Senior Secured Debt

Subordinated Debt

High Yield Notes

Private Equity Public Equity

Second Lien Notes

28Confidential

Second Lien Loans Second lien and high yield markets continue to gain momentum

Second liens loans require on average 300 to 400 bps spread premium over traditional senior debt

Source: S&P/Loan Pricing Corporation

29Confidential

Second Lien Loans (cont’d) Often called “Secured Senior Notes” or “Second Lien Secured Notes,” they are similar to

other high yield bonds – except they are secured Second Lien Debt or Second Collateral Loans (SCL) are often viewed as a substitution for

more expensive private or public mezzanine debt Second lien lenders generally offer terms and pricing that are more flexible than an unsecured

mezzanine provider

Second lien loans carry less onerous prepayment penalties

Terms on the second lien loans are shorter than traditional mezzanine debt at 3 to 5 years, however the loans can be structured with a longer tenor

In a cash-flow based second lien loan, the amount of the loan is determined by using an EBITDA multiple, whereas the amount of asset based second lien loans are based on appraisal valuations

The second lien loan is behind the senior debt for repayment priority with respect to collateral proceeds, but ranks ahead of other unsecured senior debt such as trade payables

30Confidential

Second Lien Loans (cont’d)

Second lien loans can be more attractive than subordinated or mezzanine debt because often pricing does not require warrants thus the issuer may avoid giving up equity

Prepayments are also more flexible than mezzanine or high yield debt

Second lien debt can often achieve similar leverage to that of mezzanine debt

In general, pricing for subordinated debt has decreased significantly as a result of increased competition and as second lien debt gains greater market acceptance Second lien loans require a return of approximately 10% to 15%

31Confidential

M&Aimplications

32Confidential

Average Debt/EBITDA Ratio for Transactions with Second Lien Loans

Source: S&P/Leveraged Commentary & Data

4.2x

4.2x

5.1x

33Confidential

…and an Increase in Purchase Price Multiples

Source: S&P/Loan Pricing Corporation

7.8x

8.0x 7.4

x 6.1x

6.0x

6.4x

7.0x

7.4x

7.3x

7.1x

7.2x

6.8x

6.9x 5.4

x

6.4x

6.9x

7.2x

8.0x

34Confidential

summary

35Confidential

Financing Summary

Capital market conditions have improved dramatically over the last year and there is substantial liquidity in the market

There is a great deal of institutional money chasing very few quality opportunities

Accordingly, debt leverage has increased in all markets and pricing has declined

Mezzanine providers are being squeezed by both the Second Lien Loan (Junior Secured) and High Yield Debt markets

Second lien loans have provided access to high ratio/leveraged finance without typical equity dilution, filling the gap between senior and mezzanine debt and allowing purchase multiples to increase

36Confidential

© 2005 Ernst & Young Orenda Corporate Finance Inc.

A Member of Ernst & Young Global

ERNST & YOUNG ORENDA CORPORATE FINANCE INC.

eyorenda.com

Tickets now on sale for the CFO of the Year Gala

May 4th, 2006 (Fairmont Royal York)

Presented by