Cost Engineering’s Added Value —Making Better Capital Investment

Decisions

John K. Hollmann PE CCE CEPValidation Estimating LLC

Introduction

• John K. Hollmann PE CCE CEP– Owner – Validation Estimating LLC

• Active in AACE International– Fellow, Award of Merit– Co-Chair: Decision and Risk Management

Professional (DRMP) Certification Task Force– Technical Board– Former Regional Director of ICEC

• Editor/Lead Author of AACE’s Total CostManagement Framework

Cost EngineeringBack to Adding Value

• Investments, Profitability and Cost Engineering• Cost Engineering’s Value Proposition• Total Cost Management (TCM) Process• Decision and Risk Management

Profitability and Cost Engineering• AACE defined Cost Engineering at its founding in

1956 as the application of scientific methods toproblems of “…profitability”; emphasizing cost

• The founders’ main interest was in making bettercapex investment decisions based on better dataand methods centering on engineering economicsand conceptual cost estimating methods

• They recognized that “cost is king” and “time iscost” (in decision analysis, inputs are estimated inmonetary equivalents) with profitability being themain objective

• Today, AACE’s TCM process revolves aroundInvestment Decision Making– i.e., where Cost Engineering adds its value!

*by 1990, profitability was gone from AACE’s CE definition (more on that later)

Profitability and Cost Engineering• AACE defined Cost Engineering at its founding in

1956 as the application of scientific methods toproblems of “…profitability”; emphasizing cost

• The founders’ main interest was in making bettercapex investment decisions based on better dataand methods centering on engineering economicsand conceptual cost estimating methods

• They recognized that “cost is king” and “time iscost” (in decision analysis, inputs are estimated inmonetary equivalents) with profitability being themain objective

• Today, AACE’s TCM process revolves aroundInvestment Decision Making– i.e., where Cost Engineering adds its value!

*by 1990, profitability was gone from AACE’s CE definition (more on that later)

Estimator, Cost Engineering or Decision Maker?

Most of us have heard of Hans Joachim Lang, inventor of the“Lang Factor”

(AACE Award of Merit, 1983)

Did you know he became a CEO and that when he retired toteach he authored “Cost Analysis for Capital Investment

Decisions” and co-authored “The Selection Process for CapitalProjects”: a leading global textbook on engineering economics

and capital investment decision making?

Capital Investmentand Profitability

• “For Profit” companies (most of our employers)have a profitability measure that incorporates theidea of return-on-investments. For example…– Return on assets, return on average capital employed,

return on net assets, etc., etc.

• For discussion, we can simplify this to:Profitability =

This means, minimizing CAPEX is as important asincreasing Revenue and decreasing OPEX

• However, CAPEX “competitiveness” is likely notamong your company’s KPIs (go check)– Why is this?

*CAPEX = Capital Expenditure, OPEX = Operating Expenditure,KPI = Key Performance Indicator in Balance Scorecard (strategy deployment scheme)

Owner Capital Cost Knowledge HasBeen Outsourced

• Started in 1980s; by 1990 signs become clear– Business Process Reengineering (BPR) by Hammer– AACE drops “Profitability” from its definition of Cost

Engineering (puts “manage” and projects” in its place)

• 1993: Outsourcing on a roll– “Today, the (chemical) industry has no dynamic strategy

and constantly shifting structures.... it has adopted thedubious tactic of personnel reduction” 2

• 1997: Mission Accomplished?– “almost half of all projects have substantial contractor

involvement in project definition… Of particular concernis the technical competence to assist the businesses inarriving at the most appropriate project to meet thebusiness need has been lost” 3

1 Wikipedia article on BRP2 “The End of the Chemical Century…?”, JK Smith, 19943 The Business Stake in Effective Project Systems, Business Roundtable , 1997

Cost Engineering’sFocus on Capex and Profitability?• Late 1990s: “Did we go too far?”

– BRT, CII, IPA and other forums and research on “CoreCompetency” all concluded that Owner’s had outsourcedtheir capital cost knowledge and had to reverse this

• 1996: Regaining Cost Engineering at AACE/ICEC– TCM Framework which is Investment Decision-Centric is

outlined (life cycle process for applying Cost Engineering)– Resistance: outsourcing’s beneficiaries succeeded in

equating Cost Engineering with “project control”• 2006: TCM Framework released• We are not back yet

– A generation of lost focus and skills– Cost Engineering vs. Project Control debate rages on– “Management Accounting” takes Capex Decision lead– Finance does not understand Capital Effectiveness (not in KPIs)– Cost Engineers are not key players in the “business case”

• Decision and Risk Management initiatives at AACE

Cost EngineeringBack to Adding Value

• Investments, Profitability and Cost Engineering• Cost Engineering’s Value Proposition• Total Cost Management (TCM) Process• Decision and Risk Management

Selected Terminology

• Profitability – Return on Investment (or similar measures)• Business Case – Analysis justifying a capital investment alternative• Phase-Gate Process – Planned, incremental development of scope

and approval of investment funds (e.g., FEL or Front-End Loading)• Decision Analysis – Quantitative method for analyzing and rating

alternatives (often based on monetary equivalents or “costs”)– Discounted Cash Flow: deals with the time value of monetary streams

• Engineering Economics – The “hard” side of investment analysis(e.g., NPVs, IRR, etc.) looking at the life cycle of the asset

• Behavioral Economics – the “soft” side of investment analysislooking at human factors in decision making under uncertainty

• Capital Effectiveness vs. Predictability – Lower absolute costs vs. atighter range (difficult to have both)

• Balanced Scorecard, KPIs, etc. – Methods to deploy businessstrategy; keep all in alignment with corporate objectives

Value Proposition: Why Investment DecisionMaking is a Key Cost Engineering Focus

• Research by IPA, Inc. shows that the business success of aventure (measured by achievement of NPV) is determinedBEFORE the project is authorized*– “Business FEL” explained 85% of the variation between planned and

actual NPV outcomes

• Further, project control is about “capital conservation”(i.e., predictability)..”not basic venture success”.*

• Therefore, if you are working for an owner, and want toadd value to the business (not just conserve it), onemust focus on Making Better Investment Decisions– At your workplace, are you actively involved in (or just feeding

estimates to) business case development?

*F. Biery:“Improving Construction Project Outcomes and Project Returns”, Northwest ConstructionConsumer Council, May 2002

Value Proposition: Lower Capex Drives ROIfor Commodity Projects

12

-7%

-5%

-3%

-1%

1%

3%

5%

7%

From: Hollmann, John K., Best Owner Practices For ProjectControl, 2002 AACE Transactions

Cha

nge

inIR

R

20% 10% -10% -20%

Cost

ScheduleChange in Performance Metric

10% less cost = 2%greater IRR

Corporate Objectives andStrategy Deployment

• Most companies have a strategy deployment method– e.g., Balanced Scorecard: measures are established at each level of

the organization that should align with the higher level objectivesuch as Profitability

• Lets look at a strategy deployment example:

Corporate Goal of Better Profitability =Marketing Goal and KPI: Increase price & revenue 5% (same capacity)Operations Goal and KPI: Decrease opex 5%Capital Goal and KPI: Decrease capex 5%

Capital Goal and KPI: Capex within +/-2% of annual budget(or all projects within +10/-10%, etc.)

This yields Predictability, not Competitiveness or Profitability!

What you want in a strategy:

What you see in strategies:

Competitiveness vs. Predictability

• It is a paradox that the more accurate a company’s projectcost are, the less competitive their capital costs tend to be

• The easiest way to under-run estimates, to hit budgettargets and get tight accuracy is to over-estimate, over-fundand spend all the money approved

• Unfortunately, when companies create “scorecard” metricsfor their processes, they look at accuracy– Why? Because range is easy to measure, cultures are punitive and,

lacking cost engineering knowledge, they have no means tomeasure “should cost”

• Does your company measure capital effectiveness?

Capital ConfusionVery Few Companies Measure Capital Effectiveness

CompanyCategory

Top Level CorporateObjective

Capital Strategy Implied Capital Focus

Major Global Oil “competitive shareholderreturn”

“capital and cost discipline” Predictability

Major EuroChem

“premium on our cost ofcapital” (return)

“disciplined with regard to costs andexpenditures”

Predictability

Major Global Oil “pre-tax profitability” “enhance capital efficiency”(“In particular a Centralised DevelopmentsOrganisation is being established”… rival hasbeen operating under a similar model and isconsidered an industry leader in profitability)

Competitiveness!

Major GlobalPharms

growth and innovation(could not find profit?)

“free up working capital” Get More Capital

Major Euro NGOUtility

“competitive return overtime.”

“organic expansion….combined withacquisitions”

Ambiguous

Major GlobalMining

“best returns” “project delivery” (also low cost overlife of properties; opex focus)

Predictability /Ambiguous

These were all taken from current company website Investor pages or annual report summarizingcorporate “strategy” (i.e., try it yourself; just enter “[company name]” + ”strategy” in Google)

Which is the Path to CapitalCost Competitiveness?

16

Cost

The Wrong Path:Predictable Mediocrity

with Masked Risks•Fat, padded baseestimates (hard to detect)•No measures of absolutecost competitiveness (noidea of “should costs”)•Punish overruns (anddeemphasize control)•“Cresting Wave”distribution of outcomes

The Right Path:Excellence withManaged RiskPredictable +Competitive

•Set Challenging target(will miss some of them)•Measure absolute costcompetitiveness (identify“should cost”)•Only punish “notknowing” cost statusand/or failure to taketimely corrective action

Stat

usQ

uo

Cost EngineeringBack to Adding Value

• Investments, Profitability and Cost Engineering• Cost Engineering’s Value Proposition• Total Cost Management (TCM) Process• Decision and Risk Management

Total Cost Management (TCM) Centers onInvestment Decision Making

Project Control is a Recursive Process Within the Strategic Asset Management Process

If there is no project-there is no Project Control, But Cost Engineering Goes On!

*From the TCM Framework, Chapter 2.2

The Heart of TCM

AssetPerformanceAssessment

(6.1)

AssetPlanning

(3.2)

InvestmentDecision Making

(3.3)

Analysis Basis & Feedback

ProjectImplementation

(4.1)

Decision(ResourceAllocation

forProjects)

Asset CostAccounting

(5.1

AssetPerformanceMeasurement

(5.2)

ProjectControl

(2.4)

Improvement Opportunities(variance from baseline plans)

Require-ments

RequirementsElicitation and

Analysis(3.1)

Asset Performance andValuation Measures

BaselineAsset Management Plans

EnterpriseManagement

BusinessStrategies,

Goals,Objectives

ProjectImplement-

ationBasis

ProjectPerformance

AssetOperation or Use

AssetPerformance

Stakeholdersand Customers

Planning Processes:Scope and Execution Strategy Development

(7.1)Schedule Planning and Development (7.2)

Cost Estimating and Budgeting (7.3)Resource Planning (7.4)

Value Analysis and Engineering (7.5)Risk Management (7.6)

Needsand

Desires

AssetChange

Management(6.2)

Requirements Changes

Asset Historical Database Management(6.3)

All Strategic AssetManagementProcesses(3.1 to 6.4)

ActualData

HistoricalData

ActualData

HistoricalData

OtherEnterprises

Benchmarking Information

Decision(ResourceAllocation

forOperations)

ForensicPerformanceAssessment

(6.4)PerformanceInformation

Strategic Asset Management ProcessDeploys Business Strategy

*From the TCMFramework, Chapter 2.3

AssetPlanning

(3.2)

InvestmentDecision Making

(3.3)

Investment Decision Making ProcessIn TCM (3.3)

Decisions can never be reduced to an equation, butsuccessful decisions must be “informed”

*From the TCM Framework, Chapter 3.3

Key CE Practices That Add Value To andSupport Investment Decision Making

• Engineering Economics *• Cost Models (stochastic at early phases) *• Time Models (stochastic at early phases)• Decision Models• Decision Analysis• Integrated Risk Analysis (incl. Revenue, Opex and Capex)• Value Improving Practices (VIPs: capitalize on opportunities)• Strategic Metrics Analysis: KPIs related to Capex• Historical Data/Knowledge Base (supports all of above)• Soft Skills (e.g., understand Behavioral Economics)

*At AACE’s creation in 1956, these were the primary focuses of Cost Engineering

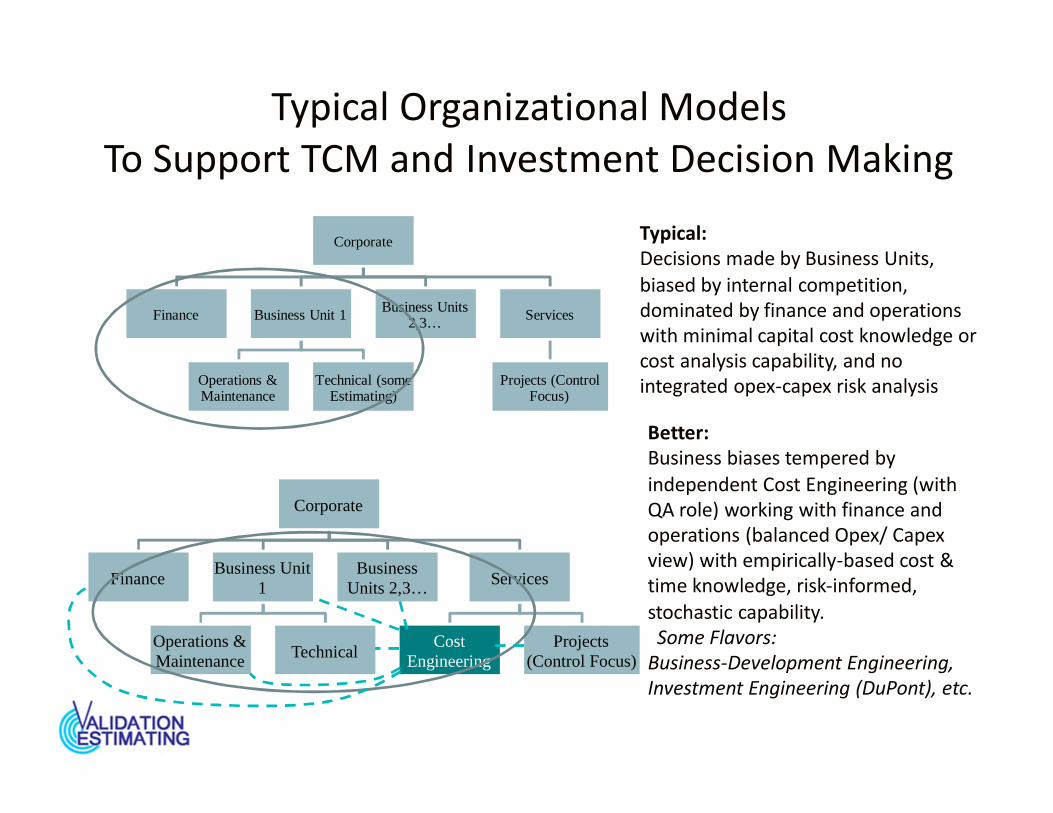

Typical Organizational ModelsTo Support TCM and Investment Decision Making

Corporate

Finance Business Unit 1

Operations &Maintenance

Technical (someEstimating)

Business Units2,3… Services

Projects (ControlFocus)

Typical:Decisions made by Business Units,biased by internal competition,dominated by finance and operationswith minimal capital cost knowledge orcost analysis capability, and nointegrated opex-capex risk analysis

Corporate

FinanceBusiness Unit

1

Operations &Maintenance Technical

BusinessUnits 2,3… Services

CostEngineering

Projects(Control Focus)

Better:Business biases tempered byindependent Cost Engineering (withQA role) working with finance andoperations (balanced Opex/ Capexview) with empirically-based cost &time knowledge, risk-informed,stochastic capability.Some Flavors:

Business-Development Engineering,Investment Engineering (DuPont), etc.

Cost EngineeringBack to Adding Value

• Investments, Profitability and Cost Engineering• Cost Engineering’s Value Proposition• Total Cost Management (TCM) Process• Decision and Risk Management

Decision Making Under Uncertainty

• Understanding the “base” cost of our capitalasset investments is not enough; we must alsounderstand risk *

• Cost Engineering adds value to Decision Makingunder Uncertainty or Risk.

• AACE effort is being focused on enhancing the“Risk” area of the CE body of knowledge:– Processes: (TCM Chapter 7.6, “Risk Management”)– Methods: e.g., Risk Analysis, Contingency and

Escalation Estimating Recommended Practices– Tools: working Hackney and RAND Excel models– Skills and Knowledge: Decision and Risk Management

Professional Certification (DRMP-beta: 2012) and itsproposed Study Guide

*In TCM (and ISO 31000) risk is uncertainty that could potentially effect objectives. Inother words risk is synonymous with uncertainty (or risk is “uncertainty that matters”)

Some AACE Risk QuantificationRecommended Practices

• 17R-97: Cost Estimate Classification System (Systemic risk driver)• 27R-03: Schedule Classification System (Systemic risk driver)• 40R-08: Contingency Estimating: General Principles• 41R-08: Risk Analysis and Contingency Determination Using Range Estimating• 42R-08: Risk Analysis and Contingency Determination Using Parametric Estimating

– RM-12: Extension of 42R-08 to Schedule Risk (in progress)– 43R-08: Risk Analysis and Contingency Determination Using Parametric Estimating – Example

Models as Applied for the Process Industries (i.e., Hackney and RAND Excel® models)• 44R-08: Risk Analysis and Contingency Determination Using Expected Value• 57R-09: Integrated Cost and Schedule Risk Analysis Using CPM and Monte Carlo

Simulation (exposure draft)• RM-14: Integrated Cost and Schedule Risk Analysis Using Expected Value and

Monte Carlo Simulation (in progress)• 15R-10: Selecting Probability Distribution Functions for Use in Cost and Schedule

Risk Simulation Models (committee draft)• 58R-10: Escalation Estimating Principles and Methods Using Indices• 58R-10 Extension: Escalation Estimating Using Indices and Monte Carlo Simulation

(in progress)• And more on the way…

Value Proposition: Why Risk Management isa Key Cost Engineering Focus

• To repeat, to add value to your business (not justconserve value), one must focus on Making BetterInvestment Decisions; however, to make the rightdecisions, and avoid lost value during execution, onemust also address risk

• Evidence of industry’s failure to address riskadequately is in the news every day

• Cost Engineering adds particular value in terms ofquantification of risks and impacts– Most company “Risk” departments (and books on the topic)

are limited to “qualitative” risk screening because truequantification is difficult (one must understand the asset,project and environment) and controversial (some argue thatmost risk cannot be quantified)

TCM: Risk Management Process

*From the TCM Framework, Chapter 7.6

TCM is the only industry process that explicitly quantifies therisk in a way that supports decisions and control (i.e., recycles

residual risks through Assessment)

How Does Business Management AddressRisk in Investment Decision Making

• First Pass: run DCF on business case model applying a target“hurdle rate” (e.g., 12-15% needed to exceed typical stock return)

• Bounds Testing using Sensitivities/Scenarios: Rerun the modelwith different key “market and financial” driver values (e.g., firstsale date, sale price, interest and tax rates) and run the modelwith rough estimates of impact on return of each driver

• Go/No Go: If scenarios exceed hurdle rate, likely to make the cut

• Analysis is typically led by finance: capital contingency andreserve analysis by the team is largely ignored (engineering noise)and most teams provide little useful schedule risk information

– More sophisticated owners may consider p90 capex or highlighted reserveitems as scenario variables; a Cost Engineering value add!

– Escalation of capex is treated superficially (e.g., CPI on capex and opex) withlittle recognition that rates now vary markedly with each model element

*DCF = Discounted Cash Flow

Quantification Gone Wrong(Traditional “Ranging” Does Not Work)

• Even if business uses “P90” capex and startup date values…They are Wrong

(if you are doing “line-item or activity ranging”)• Findings from empirical research…

– “…contingency estimates are, on average, getting further from theactual contingency required.”… When project scope was poorlydefined, the more sophisticated techniques were “a disaster”

• Why does ranging fail?– Monte Carlo is not the problem, it is the underlying models– Traditional “ranging” models have no direct risk-to-impact link or

consideration of systemic risks (even if one gets the Monte Carlorequirements such as dependencies correct)

* Burroughs Scott E. and Gob Juntima, “ExploringTechniques for Contingency Setting” , 2004

Risk Analysis Must Address Systemic Risks

• Systemic Risks (empirically based methods)– Project or process system attributes such as how well you define the

scope, estimating biases, use of technology, complexity, etc.– Predominate risk in early scope development– Best estimated using Parametric Modeling (models directly link risks

with cost and schedule impacts)

• Project-Specific Risks– Result from attributes, conditions, events, activities, and so on in a

specific project– These risks are generally not readily identifiable until later in project

definition– Best estimated using Expected Value Modeling

• These issues/methods are well covered in AACE literature

Risk Analysis Must Address Systemic Risks

• Systemic Risks (entirely empirical)– Project or process system attributes such as how well you define the

scope, estimating biases, use of technology, complexity, etc.– Predominate risk in early scope development– Best estimated using Parametric Modeling (models directly link risks

with cost and schedule impacts)

• Project-Specific Risks– Result from attributes, conditions, events, activities, and so on in a

specific project– These risks are generally not readily identifiable until later in project

definition– Best estimated using Expected Value Modeling

• These issues/methods are well covered in AACE literature

Estimator, Cost Engineer or Decision Maker?

Many of us have heard of John W. Hackney, the “godfather” ofCost Engineering

(an AACE Founder, Award of Merit 1961)

Before becoming Manager of Cost Engineering at Mobil (and“profitability analysis” with Diamond Shamrock before that), didyou know he conducted research and published the world’s first

parametric risk model linking the level of project scopedevelopment to cost growth? This is a foundation to the phase-

gate (FEL) decision making processes we all use today.

A Big Systemic Risk for Decision Making(Behavioral Economics)

Cost Engineers must move beyond Engineering Economics….Behavioral Economics (part of DRMP body of knowledge)

– 2002 Nobel to Daniel Kahneman for having "integrated insights frompsychological research into…decision-making under uncertainty”

Example derived from above: “Strategic Representation”(i.e., Optimism Bias-or better known as Lying)– American Planning Association endorses Bent Flyvbjerg’s

“Reference Class Forecasting” for public works projects becausecosts overrun >100% and demand underrun >50% not uncommon

– A cynical (but realistic?) approach: just use history for your mostlikely outcome and probability distribution (forget VIPs)

• Less cynically, AACE uses Benchmarking/Validation as a bounds test of models

– He recommends better “Management Accounting” (Unfortunately,he does not recognize Cost Engineering)

Get in the Scenario Game

• In addition to addressing systemic risks (and hence real p90values) realize that business decision makers are looking atsensitivities and scenarios using DCF and EMV (“expectedmonetary value from decision trees)

• Cost Engineers must support these approaches Stochastic cost models that examine multiple options Identify “reserve” risks that cost contingency cannot fund (e.g., low

probability, high impact); considered these in DCF sensitivity runs Identify and highlight schedule completion risks because the “first

sale” date is always a key variable in DCF (finance folks get this) Identify and offer “contingency risk response plans” for the above If you can include portfolio considerations (interaction of projects) in

all of the above, so much the better

Cost EngineeringBack to Adding Value

• Investments, Profitability and Cost Engineering• Cost Engineering’s Value Proposition• Total Cost Management (TCM) Process• Decision and Risk Management

– and Value Management (& VIPs)

35

Value and Risk ManagementProcesses Should Work In Alignment

PlannedValue

AddedValue

ReducedValue

The Risk and Value ManagementShield Protects Investment Value

36

Apply VIPs Early and Often Enough toInfluence Design, Planning and Decisions

Pote

ntia

lto

Influ

ence

Val

ue

Asset Planning Asset Implementation Project Control

Asset OptionSelected

AssetOpportunityIdentified

Project Fully Authorized

Asset Planning and Implementation Phase

37

Example: IPA VIPs

From: The Use and Impact of Value Improving Practices and Best PracticesJim Lozon, P.Eng. and Dr. George Jergeas, P.Eng.AACE Cost Engineering Journal, Vol. 50/No. 6 JUNE 2008

Cost Engineering is CriticalAll VIPs end in Decisions, and most Decisions hinge on Costs

In Conclusion: Cost Engineering HelpsAvoid the Capex Drain

Over Funded Capital/Poor Profitability

Overrun

BecomeRisk Averse

Low RiskPredictable

Projects

Loss ofCredibility

Business Pads Plans

Fails to MeetRequirements

Rework, Debottleneck, Modification Projects

Optimism bias goesuncheckedUnder Funded Capital

GiveRewards

Underdesign

Underrunor Alwayson Budget

GiveRewards

Punish

Weak CostEngineering

PROPOSAL

Overdesign

Value of alternatives not assessed

In Conclusion: Cost EngineeringAdds Value

• Cost Engineering’s added value is in MakingBetter Capital Investment Decision– Profitability is determined before the project– Project Control only conserves value

• AACE’s Total Cost Management FrameworkProcess is centered on the Investment DecisionMaking in consideration of Risk– A current AACE focus is building on Decision and Risk

Management technology, education and certification• Many Cost Engineers need to update their skills

and knowledge so that they are valued by theBusiness Leaders who make decision– Start by being the gurus of Capital Effectiveness and

capital cost and schedule risk– Play in/feed the financial scenario game

40

Questions?

• Contact:– John K. Hollmann PE CCE CEP (…and future DRMP)– [email protected]– www.validest.com– 1-703-945-5483

• Key References:– TCM and RPs

• Free (.pdf format) from AACE at www.aacei.org/technical