Credit Reporting - Three Pillars

Agenda

• Data Standard

• Reciprocity

• Trust and Confidence

Background

In March 2014 the Privacy Act 1988 was amended to allow for the exchange of comprehensive credit information.

• Defaults

• Payment Information

• New Arrangement

Information

• Judgements

• Court proceedings

• Personal insolvency

information

• Serious credit

infringements

Negative

Negative

Partial

Consumer Credit Liability

Information • type of consumer credit

• credit limit

• credit start and end dates

• credit provider details

• credit terms & conditions

Negative

Comprehensive*

Consumer Credit Liability

Information

Repayment History

Information*• if a payment is due

• payment due date

• payment date if late payment

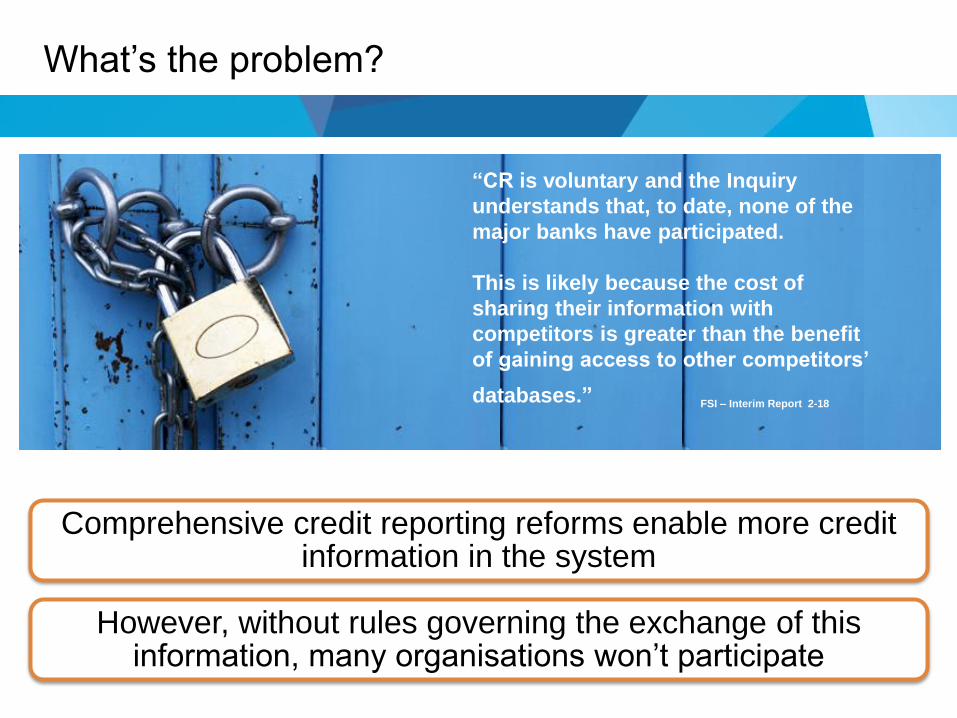

What’s the problem?

Comprehensive credit reporting reforms enable more credit information in the system

However, without rules governing the exchange of this information, many organisations won’t participate

“CR is voluntary and the Inquiry

understands that, to date, none of the

major banks have participated.

This is likely because the cost of

sharing their information with

competitors is greater than the benefit

of gaining access to other competitors’

databases.” FSI – Interim Report 2-18

More information is valuable: it enables better risk management and better

credit decisions

What’s the problem?

There is a risk in allowing a competitor access to more information about

an organisation’s customers, and could therefore threaten this customer

base

What’s the solution?

What’s the solution?

What’s the solution?

Reciprocity is one

of the human rocks

on which societies

are built.

Marcel Mauss

What’s the solution?What’s the solution?

The most efficient teams, firms, and societies are often those where reciprocities are the most developed.

What’s the solution?What’s the solution?

• Society has developed various

types of reciprocities among

communities, organisations and,

industries, and

• social anthropologists have

identified that reciprocities in

society are pervasive and

necessary, having regard to the

overall quality of a society, of

relations in it, and of its members

themselves.

What’s the solution?What’s the solution?

Reciprocity is the only alternative to

oppressive command, regulation and

selfish exchange.

RECIPROCITY:

ITS SCOPE, RATIONALES, AND CONSEQUENCES

Serge-Christophe KOLM

What’s the solution?

• Data will be shared on the

principle that subscribers

receive the same credit

performance level data that

they contribute, and should

contribute all such data

available.

What’s the solution?

• Reciprocity is a key principle for credit

data sharing.

• A creditor could accept sharing its

information and break its information

monopoly if it gains access to the

information of other creditors and, thus, be

able to perform a better credit risk assessment and

thus use his resources more efficiently.

• The reciprocity principle is enforced in credit

registers through provisions that ensure that

access to credit data is granted only to

those who contribute with their

information.

What’s the solution?

• Reciprocity is the fundamental

guideline and should be embedded

in all credit reporting systems to

ensure that data is accessed only

by those creditors that report the

same type of data to the credit

register, save a few exceptions.

What’s the solution?

To the extent that the National

Credit Act requires all credit

providers to do an affordability

assessment and an assessment of

past debt repayment history prior

to entering into credit agreements,

it implies compulsory consumer

credit information sharing among

all lenders.

Rules of reciprocity mean you only get back what you put in

Data standards improve the exchange and reduce the cost of business

Reciprocity is about providing a guarantee to organisations exchanging

comprehensive credit information: they get back what they put in.

This means that everyone shares the benefit of more information, yet

everyone contributing data creates a level playing field.

Implementing a data standard enhances the exchange: the same types

of information look the same, regardless of their source. This means

organisations can readily use data, and there are no added costs of

data interpretation

What’s the solution?What’s the solution?

Build trust and confidence in the credit reporting system for all users

• Strengthen and support the reciprocity arrangements that currently exist in bilateral contracts between credit providers and credit reporting bodies

• Introduce a new data exchange standard for the credit reporting system that will help improve accuracy and completeness

• Create a tiered system of exchange – negative, partial and full comprehensive

Create a clear industry standard for the management, treatment and

acceptance of credit related information

What’s the solution?

PRDE Principles

Principle 1:

PRDE to be binding & enforceable for signatories

Principle 2:

To exchange CCLI and RHI, must be a signatory

Principle 3:

Service agreements will require reciprocity and

use of the data standard

PRDE Principles

Principle 4:

Transition rules will encourage early adoption of

comprehensive reporting

Principle 5:

Monitoring, reporting & compliance

Principle 6:

Review of the PRDE

Principle 1: Binding & Effective

• All negative data is available to non signatories

• Use of deed poll as a means to bind signatories

• Bound to only exchange information at the

nominated Tier Level (negative, partial or

comprehensive)

• CP able to nominate a Designated Entity

• Specific exceptions will be set out in PRDE

Principle 2: CCLI and RHI

• Must be a PRDE signatory to be supplied or

contribute CCLI and/or RHI

• Means by which exchange of ‘new data’ is

governed

• A CP is restricted from on-supplying CCLI and

RHI to a non-signatory

• Exception for Securitisation Entities

Principle 3: Data standards

• Both CPs and CRBs are required to adhere to

the data standards

• CRBs can provide a conversion service

• A CP is not restricted from contributing

information to multiple CRBs

Principle 4: Transition rules

• CP must provide 50% of Tier Level, before

obtaining first supply

• Remaining 50% of information at Tier Level to

be provided within 12 months

• RHI contribution requires 3 months of data as a

show of goodwill

• Tier Level contribution can be concurrent

Principle 5: Monitoring, reporting & compliance

• Compliance outcomes are reached through a

process that encourages

– Negotiation

– Mediation

– Conciliation

• PRDE Administrator Entity facilitates process –

maintains register & signatory website

Principle 6: Review

• Independent review of PRDE initially at 3 years,

afterwards 5 years, process managed by PRDE

Administrator Entity

• CPs and CRBs required to assist review in good

faith

Next Steps

ACCC authorisation

As the new arrangements will impose particular

obligations on the way PRDE signatories

exchange data with others, ARCA will approach

the ACCC to make sure the new arrangements

are appropriately authorised….

Next Steps

“the likely public benefits flowing from the

proposed conduct for which authorisation is

sought outweigh the likely public detriments

flowing from that conduct”

More information

www.creditsmart.org.au

www.arca.asn.au