202 Global Securitisation and Structured Finance 2007

29

T his chapter updates Deutsche Bank research published in 2004 entitled

“Credit Resiliency of European Residential Mortgage-Backed Securities”.

At that time, there was no shortage of headlines in the press and other

publications about the residential housing bubble in many European

markets, with commentators speculating on whether a correction in house

prices was pending. Since 2004, residential house prices have continued to

climb across most European jurisdictions, the only exception being Germany.

The recent US subprime meltdown has brought into light similar deflation

risks in Europe, with the United Kingdom, Spain and Ireland particularly cited

as markets most exposed to risks of a property slump.

This chapter looks at the resiliency of European mortgage-backed

securities to a decline in house prices. Losses experienced by residential

mortgage-backed securities (RMBS) are a simultaneous function of default

rates and recoveries (the latter in turn determined primarily by house prices).

The chapter isolates the stresses on house prices in order to test for break-

even default rates for each hypothetical country RMBS. It observes that

default rates and house-price trends are often not independent, in that

higher mortgage default rates would in all likelihood depress house prices

and sometimes vice versa. House-price declines alone may not necessarily

result in higher defaults, particularly in countries where borrowers remain

willing to pay despite negative equity.

The chapter formulates hypothetical benchmark RMBS pools that most

closely resemble RMBS portfolios outstanding in selected European

mortgage-backed markets. It then calculates the default rates that each

tranche in typical European RMBS capital structures can withstand under a

Credit resiliency of European residentialmortgage-backed securities in 2007

Carole Bernard

Deutsche Bank

© Deutsche Bank 2007

Credit resiliency of European residential mortgage-backed securities in 2007 I Global Securitisation and Structured Finance 2007

Global Securitisation and Structured Finance 2007 203Deutsche Bank

severe house-price shock, which is assumed as a mean

reversion of house prices back to their average levels

since 1995 in each European country.

Defining the hypothetical European RMBS

Deutsche Bank has created 10 hypothetical RMBS deals

representative of mortgage-backed securitisations in

the most developed RMBS markets in Europe.

For each hypothetical RMBS portfolio, loan-to-value

distributions have been formulated using pools

information from benchmark deals outstanding. Loan-to-

value distributions are an important consideration, as two

mortgage pools with the same weighted average loan-to-

value but different loan-to-value distributions will behave

differently from house-price stresses. This study includes

for the first time high loan-to-value Spanish RMBS,

reflecting the recent proliferation of such deals.

For each country-specific RMBS benchmark portfolio,

a geographic distribution of borrower/property domiciles

has been assumed, reflecting the typical RMBS deal from

that jurisdiction. The house-price stress applied in the

study uses an average house-price trend weighted by the

regional significance of the hypothetical RMBS pool,

rather than the national average house-price trend. In

effect, the house-price decline assumptions are made

more meaningful by taking into account RMBS-pool

regional concentrations.

The seasoning assumed in this study is consistent

with the various RMBS markets (all mortgage loans are

assumed to share the same pool average seasoning). The

analysis gives credit to seasoned collateral by taking into

account house-price changes (if any) over the age of the

mortgage, thus reflecting current loan-to-value figures

rather than original loan-to-value figures. As no principal

repayment in seasoned mortgages is taken into account,

the bias is conservative.

For each jurisdiction, different recovery periods and

legal costs associated with repossessions are assumed.

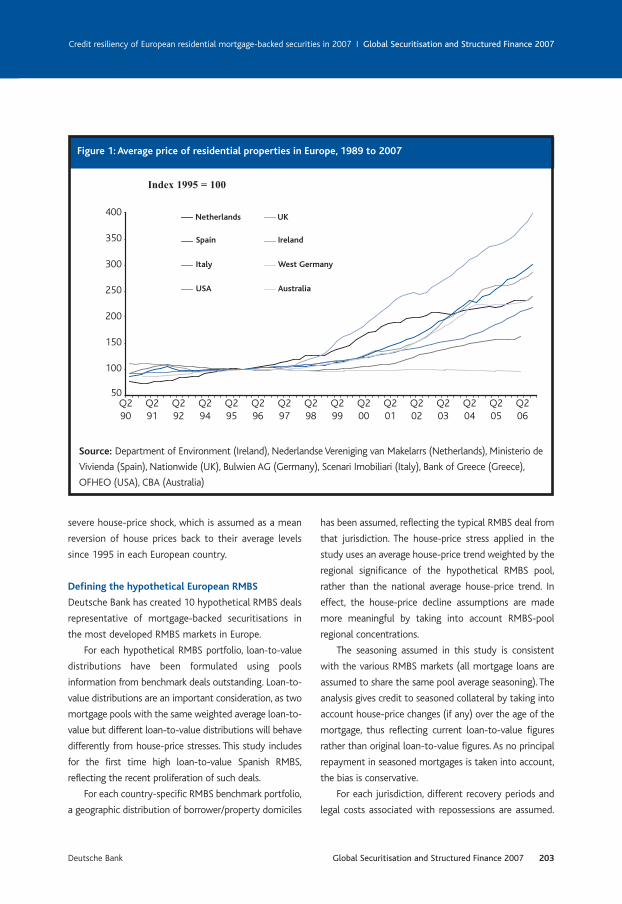

Figure 1: Average price of residential properties in Europe, 1989 to 2007

Source: Department of Environment (Ireland), Nederlandse Vereniging van Makelarrs (Netherlands), Ministerio de

Vivienda (Spain), Nationwide (UK), Bulwien AG (Germany), Scenari Imobiliari (Italy), Bank of Greece (Greece),

OFHEO (USA), CBA (Australia)

400

300

200

150

Netherlands

250

Q291

USA

Italy

Spain

Index 1995 = 100

50

100

350

UK

Australia

West Germany

Ireland

Q292

Q294

Q295

Q296

Q297

Q298

Q299

Q200

Q201

Q202

Q203

Q204

Q205

Q206

Q290

Global Securitisation and Structured Finance 2007 I Credit resiliency of European residential mortgage-backed securities in 2007

204 Global Securitisation and Structured Finance 2007 Deutsche Bank

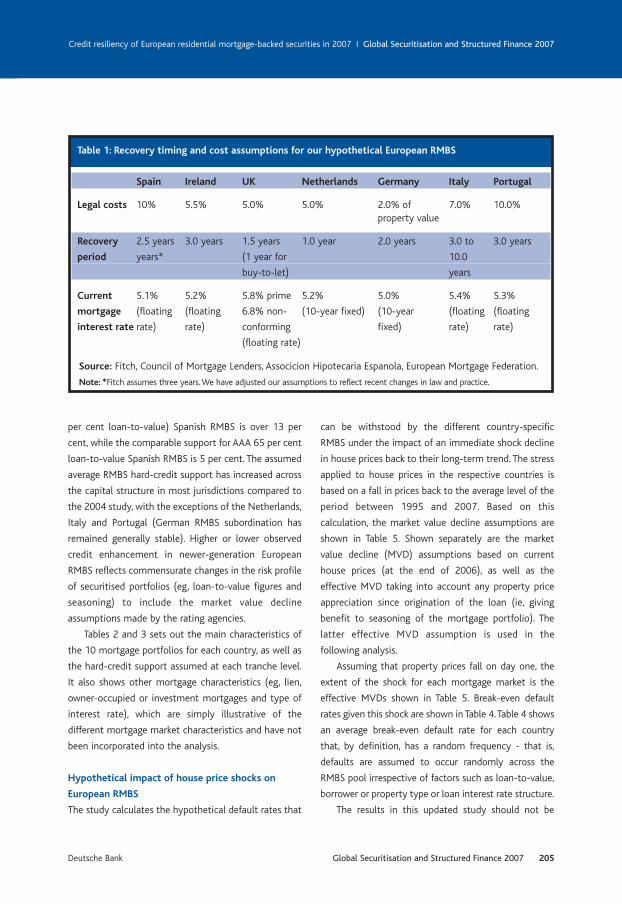

Such assumptions are based on information taken from

Fitch’s rating methodology reports (see Fitch’s RMBS

criteria reports for the relevant jurisdictions). The

recovery period represents the time lag between the first

day of the delinquency and the forced sale of the

repossessed property, and all legal costs associated with

the legal process include lawyer fees, taxes, eviction of

residents if necessary, refurbishment, valuation and

brokerage. Legal and accrued carry costs (current interest

rates have been assumed during the foreclosure period)

are deducted from gross proceeds for property

repossessions. Table 1 summarises the assumptions

made in costing the recovery process in each country.

All 10 hypothetical RMBS deals assume a static,

pass-through structure (with the exception of UK prime

RMBS). Hard-credit enhancement (ie, subordination

only or ignoring excess spread) at each rating or tranche

level is based on averages for benchmark deals in each

of the mortgage markets under study. For example, the

subordination level for AAA high loan-to-value (ie, 97

Figure 2: Impact of house price shocks on European RMBS – outline of study

Source: DB Global Markets Research

Assumptions Stress runs

ash Reserve 0

50

100

150 200 250 300 350

‘89

‘90 ‘91

‘92 ‘93

‘94 ‘95

‘96 ‘97

‘98 ‘99

‘00 ‘01

HypotheticalRMBS

credit structures

Hypothetical RMBS portfolio

Apply house price ‘shocks’

AAA94%

A4%

BBB2%

Cash reserve2%

weighted average LTV,

distribution of LTV

seasoning

geographic distribution

repayment type and

prepayments

LTV distribution

recovery timing and costs

Tranche loss = f (default rate, loss severity, credit enhancement)

Quantify the hypothetical default rate that the RMBS portfolio can withstand before the rated notes experience the first unit of

principal loss

Long termtrend line

Marketvalue

decline

Credit resiliency of European residential mortgage-backed securities in 2007 I Global Securitisation and Structured Finance 2007

Global Securitisation and Structured Finance 2007 205Deutsche Bank

per cent loan-to-value) Spanish RMBS is over 13 per

cent, while the comparable support for AAA 65 per cent

loan-to-value Spanish RMBS is 5 per cent. The assumed

average RMBS hard-credit support has increased across

the capital structure in most jurisdictions compared to

the 2004 study, with the exceptions of the Netherlands,

Italy and Portugal (German RMBS subordination has

remained generally stable). Higher or lower observed

credit enhancement in newer-generation European

RMBS reflects commensurate changes in the risk profile

of securitised portfolios (eg, loan-to-value figures and

seasoning) to include the market value decline

assumptions made by the rating agencies.

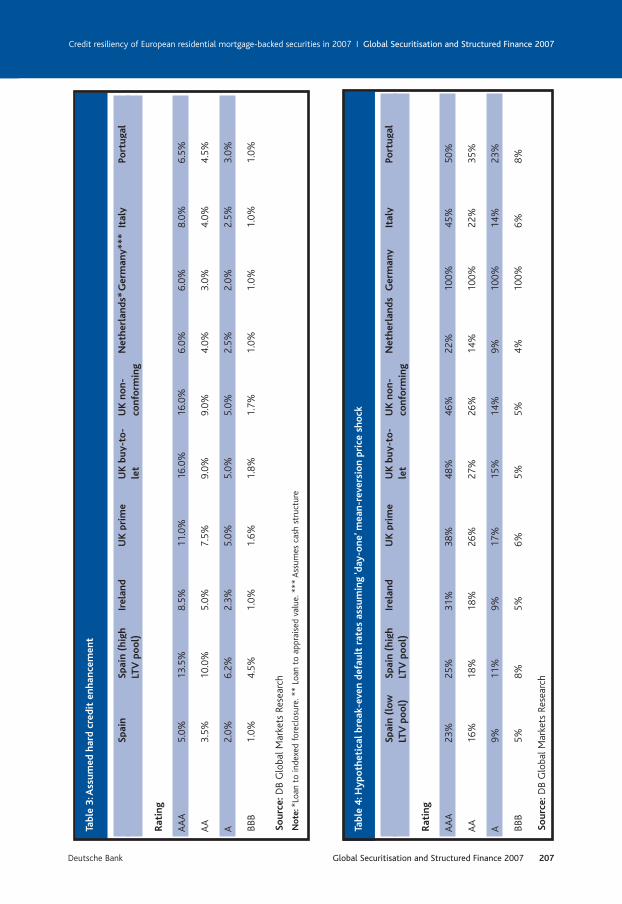

Tables 2 and 3 sets out the main characteristics of

the 10 mortgage portfolios for each country, as well as

the hard-credit support assumed at each tranche level.

It also shows other mortgage characteristics (eg, lien,

owner-occupied or investment mortgages and type of

interest rate), which are simply illustrative of the

different mortgage market characteristics and have not

been incorporated into the analysis.

Hypothetical impact of house price shocks on

European RMBS

The study calculates the hypothetical default rates that

can be withstood by the different country-specific

RMBS under the impact of an immediate shock decline

in house prices back to their long-term trend. The stress

applied to house prices in the respective countries is

based on a fall in prices back to the average level of the

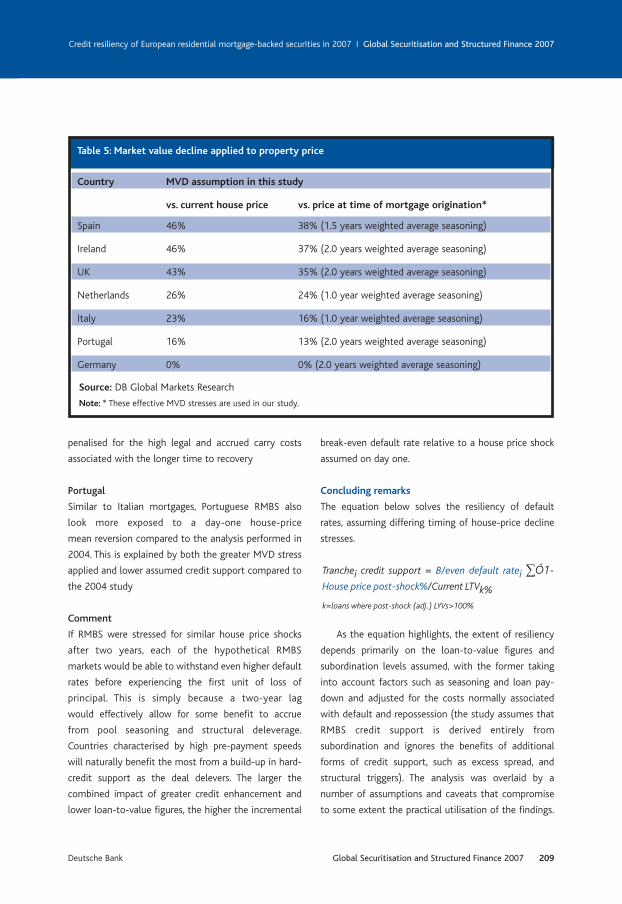

period between 1995 and 2007. Based on this

calculation, the market value decline assumptions are

shown in Table 5. Shown separately are the market

value decline (MVD) assumptions based on current

house prices (at the end of 2006), as well as the

effective MVD taking into account any property price

appreciation since origination of the loan (ie, giving

benefit to seasoning of the mortgage portfolio). The

latter effective MVD assumption is used in the

following analysis.

Assuming that property prices fall on day one, the

extent of the shock for each mortgage market is the

effective MVDs shown in Table 5. Break-even default

rates given this shock are shown in Table 4.Table 4 shows

an average break-even default rate for each country

that, by definition, has a random frequency - that is,

defaults are assumed to occur randomly across the

RMBS pool irrespective of factors such as loan-to-value,

borrower or property type or loan interest rate structure.

The results in this updated study should not be

Spain Ireland UK Netherlands Germany Italy Portugal

Legal costs 10% 5.5% 5.0% 5.0% 2.0% of 7.0% 10.0%property value

Recovery 2.5 years 3.0 years 1.5 years 1.0 year 2.0 years 3.0 to 3.0 years

period years* (1 year for 10.0

buy-to-let) years

Current 5.1% 5.2% 5.8% prime 5.2% 5.0% 5.4% 5.3%

mortgage (floating (floating 6.8% non- (10-year fixed) (10-year (floating (floating

interest rate rate) rate) conforming fixed) rate) rate)

(floating rate)

Table 1: Recovery timing and cost assumptions for our hypothetical European RMBS

Source: Fitch, Council of Mortgage Lenders, Associcion Hipotecaria Espanola, European Mortgage Federation.

Note: *Fitch assumes three years.We have adjusted our assumptions to reflect recent changes in law and practice.

Global Securitisation and Structured Finance 2007 I Credit resiliency of European residential mortgage-backed securities in 2007

206 Global Securitisation and Structured Finance 2007 Deutsche Bank

SpainSpain (high

IrelandU

K prim

eU

K buy-to

-U

K no

n-N

etherlands*G

ermany***

ItalyPo

rtugal

LTV po

ol)

letco

nform

ing

Poo

ls characteristics

Original w

eighted65%

97%74%

75%79%

78%85%

55%**

65%72%

average LTV

Seasoning 1.5 years

1.7 years2.0 years

2.0 years6 m

onths6 m

onths1.0 year

3.0 years1.0 year

2.0 years

Mortgage typ

esA

ll floatingA

ll floating30%

fixed55%

fixed60%

fixed25%

fixed100%

fixed100%

fixedA

ll floatingA

ll floating

First lien100%

100%100%

100%100%

100%100%

50%100%

100%

Ow

ner-100%

100%100%

100%0%

95%100%

70%100%

100%

occupied

Repayment type

Annuity

100%100%

100%60%

10%

50%0%

30%100%

100%

Interest only0%

0%0%

10%90%

50%50%

5%0%

0%

Endowm

ent/life/0%

0%0%

30%0%

0%50%

65%0%

0%

savings

Geograp

hic Valencia 15%

,C

atalunya 12%,D

ublin40%

London &London &

London &Z

.Holland

Berlin 10%,

North 60%

Lisboa 35%

concentrationC

atalunyaM

adrid 65%SE 30%

SE 50%SE 30%

20%,

East Germ

anyCentral 20%

20%,M

adrid N

.Holland

15%South 20%

30%15%

,

N.Brabant

15%

Average p

ortfolio25

2827

2025

2530

2520

25

maturity (years)

Table 2:Euro

pean RM

BS hypothetical po

ols and capital structures

Source: D

B Global M

arkets Research

Note:*Loan to indexed foreclosure.**

Loan to appraised value.***A

ssumes cash structure

Credit resiliency of European residential mortgage-backed securities in 2007 I Global Securitisation and Structured Finance 2007

Global Securitisation and Structured Finance 2007 207Deutsche Bank

Spai

nSp

ain

(hig

hIr

elan

dU

K p

rim

eU

K b

uy-t

o-

UK

no

n-N

ethe

rlan

ds*

Ger

man

y***

Ital

yPo

rtug

alLT

V p

oo

l)le

tco

nfo

rmin

g

Rat

ing

AA

A5.

0%13

.5%

8.5%

11.0

%16

.0%

16.0

%6.

0%6.

0%8.

0%6.

5%

AA

3.5%

10.0

%5.

0%7.

5%9.

0%9.

0%4.

0%3.

0%4.

0%4.

5%

A

2.0%

6.2%

2.3%

5.0%

5.0%

5.0%

2.5%

2.0%

2.5%

3.0%

BBB

1.0%

4.5%

1.0%

1.6%

1.8%

1.7%

1.0%

1.0%

1.0%

1.0%

Sour

ce:D

B G

loba

l Mar

kets

Res

earc

h

Not

e:*L

oan

to in

dexe

d fo

recl

osur

e.**

Loan

to

appr

aise

d va

lue.

***

Ass

umes

cas

h st

ruct

ure

Tabl

e 3

:Ass

umed

har

d cr

edit

enh

ance

men

t

Spai

n (l

owSp

ain

(hig

hIr

elan

dU

K p

rim

eU

K b

uy-t

o-

UK

no

n-N

ethe

rlan

dsG

erm

any

Ital

yPo

rtug

alLT

Vpo

ol)

LTV

po

ol)

let

conf

orm

ing

Rat

ing

AA

A23

%25

%31

%38

%48

%46

%22

%10

0%45

%50

%

AA

16%

18%

18%

26%

27%

26%

14%

100%

22%

35%

A

9%11

%9%

17%

15%

14%

9%10

0%14

%23

%

BBB

5%8%

5%6%

5%5%

4%10

0%6%

8%

Sour

ce:D

B G

loba

l Mar

kets

Res

earc

h

Tabl

e 4

:Hyp

oth

etic

al b

reak

-eve

n de

faul

t ra

tes

assu

min

g ‘d

ay-o

ne’m

ean-

reve

rsio

n pr

ice

sho

ck

Global Securitisation and Structured Finance 2007 I Credit resiliency of European residential mortgage-backed securities in 2007

208 Global Securitisation and Structured Finance 2007 Deutsche Bank

surprising and are consistent with the findings in the

original study. The thrust of the analysis and the

assumptions used accentuate the influence of loan-to-

value coverage and historical house-price trends on

RMBS credit resiliency, taking into account the benefits

provided by hard-credit support. High loan-to-value

RMBS in a country that has experienced strong house-

price growth will, by definition of the analysis, have

lower break-even default rates compared to low loan-

to-value RMBS or RMBS from jurisdictions experiencing

more moderate house price inflation. The conclusions

are again intuitively defensible, but do not take into

account household default behaviour or affordability

factors. With the exception of Germany, all other RMBS

markets in this updated study look incrementally more

exposed to a day-one mean reversion in house prices

compared to the original study in 2004. Further

observations are set out below by country.

The Netherlands

Dutch RMBS exhibit a lower break-even default rate in the

updated study compared to the original analysis, despite

lower effective MVD assumptions. This is explained by

lower credit enhancement levels in recent benchmark

Dutch RMBS relative to the observations in 2004

Spain

Spanish RMBS pools are particularly penalised under this

scenario given the significantly greater market-value

stresses used today, without commensurate increases in

credit enhancement. However, Spanish high loan-to-

value pools exhibit incrementally higher break-even

default rates across the capital structure compared to

Spanish low loan-to-value pools in the study, suggesting

- academically at least - that the risks associated with

higher loan-to-value loans appear adequately covered by

higher credit support.

United Kingdom

Similar to Spain, UK prime RMBS look less resilient in

the updated study given the greater potential degree of

house-price correction today without corresponding

increases in credit support. A significant additional

factor for the UK prime market is that the 2004 study

gave some benefit to mortgage indemnity guarantees,

whereas the updated study does not take into account

any mortgage insurance, reflecting current market

practice. For example, in 2004 Deutsche Bank calculated

that a BBB prime UK RMBS tranche would have had a

break-even default rate of 30 per cent, compared to 6

per cent today. By contrast, senior UK non-conforming

RMBS look incrementally more resilient in the updated

study, although junior tranches are more exposed

compared to the 2004 study. This default break-even

outcome reflects greater observed credit enhancement

at the senior part of non-conforming RMBS capital

structures, which acts to more than offset the more

severe house-price decline stresses used in the updated

study. It is no coincidence that higher credit support

among senior bonds in certain UK non-conforming

RMBS stems from recent adjustments to rating agency

methodology in order to take into account pool loan-

to-value distributions.

Ireland

Irish RMBS also exhibit lower break-even default rates

compared to the results in the 2004 study, owing

mostly to the fact that mortgages securitised are no

longer covered by mortgage indemnity guarantees,

which used to benefit loans with a loan-to-value

greater than 75 per cent.

Germany

According to the analysis, German RMBS remain equally

well positioned to withstand this scenario three years

on, in that the entire pool could hypothetically default

under the assumptions without loss of principal to

investors. This resiliency is largely thanks to historically

stable house prices.

Italy

Italian RMBS are shown to have a lower break-even

default rate compared to the original study, given the

greater stresses used in the model coupled with lower

observable hard-credit support across recent capital

structures. Italian mortgage securitisations are also

Credit resiliency of European residential mortgage-backed securities in 2007 I Global Securitisation and Structured Finance 2007

Global Securitisation and Structured Finance 2007 209Deutsche Bank

penalised for the high legal and accrued carry costs

associated with the longer time to recovery

Portugal

Similar to Italian mortgages, Portuguese RMBS also

look more exposed to a day-one house-price

mean reversion compared to the analysis performed in

2004. This is explained by both the greater MVD stress

applied and lower assumed credit support compared to

the 2004 study

Comment

If RMBS were stressed for similar house price shocks

after two years, each of the hypothetical RMBS

markets would be able to withstand even higher default

rates before experiencing the first unit of loss of

principal. This is simply because a two-year lag

would effectively allow for some benefit to accrue

from pool seasoning and structural deleverage.

Countries characterised by high pre-payment speeds

will naturally benefit the most from a build-up in hard-

credit support as the deal delevers. The larger the

combined impact of greater credit enhancement and

lower loan-to-value figures, the higher the incremental

break-even default rate relative to a house price shock

assumed on day one.

Concluding remarks

The equation below solves the resiliency of default

rates, assuming differing timing of house-price decline

stresses.

As the equation highlights, the extent of resiliency

depends primarily on the loan-to-value figures and

subordination levels assumed, with the former taking

into account factors such as seasoning and loan pay-

down and adjusted for the costs normally associated

with default and repossession (the study assumes that

RMBS credit support is derived entirely from

subordination and ignores the benefits of additional

forms of credit support, such as excess spread, and

structural triggers). The analysis was overlaid by a

number of assumptions and caveats that compromise

to some extent the practical utilisation of the findings.

Country MVD assumption in this study

vs. current house price vs. price at time of mortgage origination*

Spain 46% 38% (1.5 years weighted average seasoning)

Ireland 46% 37% (2.0 years weighted average seasoning)

UK 43% 35% (2.0 years weighted average seasoning)

Netherlands 26% 24% (1.0 year weighted average seasoning)

Italy 23% 16% (1.0 year weighted average seasoning)

Portugal 16% 13% (2.0 years weighted average seasoning)

Germany 0% 0% (2.0 years weighted average seasoning)

Source: DB Global Markets Research

Note: * These effective MVD stresses are used in our study.

Table 5: Market value decline applied to property price

Tranchei credit support = B/even default ratei ∑Ó1-

House price post-shock%/Current LTVk%

k=loans where post-shock (adj.) LYVs>100%

Global Securitisation and Structured Finance 2007 I Credit resiliency of European residential mortgage-backed securities in 2007

210 Global Securitisation and Structured Finance 2007 Deutsche Bank

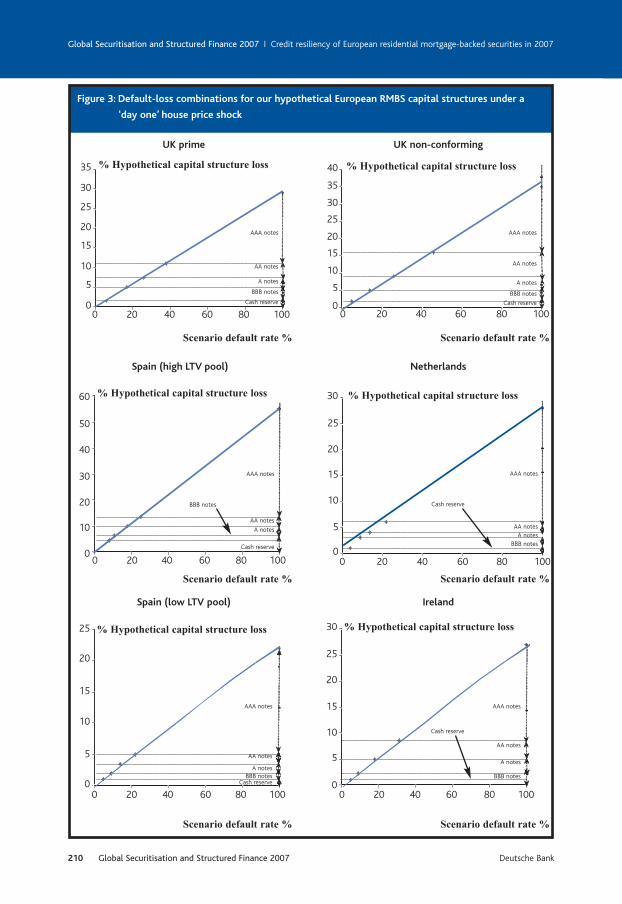

Figure 3: Default-loss combinations for our hypothetical European RMBS capital structures under a

‘day one’ house price shock

35

0

5

10

15

20

25

30

0 10080604020

UK prime

% Hypothetical capital structure loss

Scenario default rate %

Cash reserve

AA notes

AAA notes

35

0

5

10

15

20

25

30

0 80604020

UK non-conforming

% Hypothetical capital structure loss

Scenario default rate %

AA notes

AAA notes

100Cash reserve

A notes

BBB notes

0 10080604020

Spain (high LTV pool)

% Hypothetical capital structure loss

Cash reserve

AA notes

AAA notes

BBB notes

0 10080604020

Netherlands

AAA notes

0 10080604020

Spain (low LTV pool)

0 10080604020

Ireland

Cash reserve

A notes

AA notes

BBB notes

AAA notes

A notes

BBB notes

40

60

0

10

20

30

40

50

A notes

30

0

5

10

15

20

25

% Hypothetical capital structure loss

Scenario default rate % Scenario default rate %

AA notesA notes

BBB notes

Cash reserve

% Hypothetical capital structure loss25

0

5

10

15

20

Scenario default rate %

Cash reserve

AA notes

AAA notes

A notesBBB notes

% Hypothetical capital structure loss30

0

10

15

20

25

5

Scenario default rate %

Credit resiliency of European residential mortgage-backed securities in 2007 I Global Securitisation and Structured Finance 2007

Global Securitisation and Structured Finance 2007 211Deutsche Bank

This has been an academic exercise (for a full list of

other assumptions, please see the report published on

April 18 2007). However, Deutsche Bank believes that

the study will nonetheless serve as a useful litmus test

of European RMBS resiliency to any housing market

shocks. The break-even default rates, although

hypothetical, can also provide greater academic clarity

as to comparative strengths of different RMBS under

extreme scenarios.

Based on these findings, AAA RMBS tranches among

European RMBS continue to appear to be well insulated

against any house-price shock, although hypothetically

less so compared to the 2004 study. However, the risk of

principal loss on the hypothetical senior RMBS tranches

continues to appear very remote. Subordinated

mortgages look noticeably more vulnerable compared to

the 2004 results (Germany being the only exception), yet

the cushion to BBB default thresholds remains

appreciable considering current pool performance and

historical default trends.Take the example of Spanish and

Dutch BBB RMBS, which are among the weakest of the

RMBS tranches under study. However, assuming house

prices mean revert on day one, the risk of loss is limited

unless default rates reach 40 and 16 times the existing

late-stage arrears experienced by both markets

respectively. In the case of Spain, the likelihood of house

prices falling by 46 per cent looks remote, considering

historical house-price performance and housing market

fundamentals. Defaults in UK prime BBB RMBS could

hypothetically reach 75 times the current mortgage

market repossession rate before tranches experience the

first unit of principal loss. Although UK non-conforming

BBB RMBS appear to be the most vulnerable when

comparing hypothetical break-even defaults to current

late-stage arrears, the analysis ignores the benefit of

excess spread which provides material protection in

such deals.

In short, the findings of the analysis suggest that

any bursting of house-price bubbles, if taken in

isolation, appears unlikely to pose material credit risks

to European RMBS.

This chapter is taken from previously published Deutsche

Bank research.