Download - Diamond Prjct

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 1/48

A DIAMOND PERSPECTIVE «

SUNNY SOLANKI

SCMHRD

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 2/48

CONTENTS OF THE PROJECT « Introduction of Diamond as gem

Properties of Diamond

Global Bird¶s Eye View on Diamond

The Indian perspective

The Status-Quo Diamond in various Indianstates

The Demand forecast Analysis

The Roadmap for the future

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 3/48

Introduction to Diamond as a gem .. Diamond is one of the precious gemstones known to

mankind

Out of all the gemstones available it is the costliest aswell as Hardest

Diamond is highly cherished because of its Rarity,Eternity, and Purity

Diamond is perceived as a Status symbol and usuallyconsidered to be the prerogative of the rich people

Diamond Industry is Huge in terms of the value and

volume The most familiar usage of diamonds today is as

gemstones used for adornment. This usage dates backto ages

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 4/48

Historical Significance of Diamond.. Diamonds are thought to have been first recognized and

mined in India

Major deposits of the stone were found along the riverslike Godavari, Krishna.

Diamonds have been known in India for at least 3000years but most likely 6000 years

Diamonds quickly became associated with divinity, beingused to decorate religious icons

They were believed to bring good fortune to those who

carried them. Ownership was restricted among various castes bycolor, with only kings being allowed to own all colors of diamond

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 5/48

Properties related to diamond.. The characteristics related to the diamond can be

explained in the terms of..

Gemological Properties ( 4C¶)

Material Properties

Diamond is the hardest known natural material

They are found inside the earth in the alluvial deposits

Diamonds are then mined with the help of differentprocesses like kimberley etc..

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 6/48

4 C·s of Diamond 1. Cut :

Diamond cutting is the art and science of creating agem-quality diamond out of mined rough

The cut of a diamond describes the quality of workmanship

Round Brilliant Cut, Tolkowsky, Genesis cut etc.. aredifferent types of cuts

The cut increases polishing and thereby luster of the

stone

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 7/48

4 C·s of Diamond continued « Color :

A chemically pure and structurally perfectdiamond is perfectly transparent with no hue, orcolor

The color of a diamond may be affected bychemical impurities and/or structural defects inthe crystal lattice

The GIA has developed a rating system for color in

white diamonds, from "D" to "Z" (with D being"colorless" and Z having a bright yellow

coloration)

The GIA system uses a benchmark set of naturaldiamonds of known color grade

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 8/48

4 C·s of Diamond continued« Carat :

The carat weight measures the mass of adiamond.

One carat is defined as 200 milligrams (about0.007 ounce).

The point unit²equal to one one-hundredth of acarat (0.01 carat, or 2 mg)²is commonly used fordiamonds of less than one carat

A weekly diamond price list, the RapaportDiamond Report is published by Martin Rapaport,

It is currently considered the de-facto retail price

baseline.

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 9/48

4 C·s of Diamond continued« Clarity :

Clarity is a measure of internal defects of adiamond called inclusions

The number, size, color, relative location,orientation, and visibility of inclusions can allaffect the relative clarity of a diamond

There are various clarity standards as VVS1, VVS,VS1, VS, S1etc..( where VVS1 being the best)

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 10/48

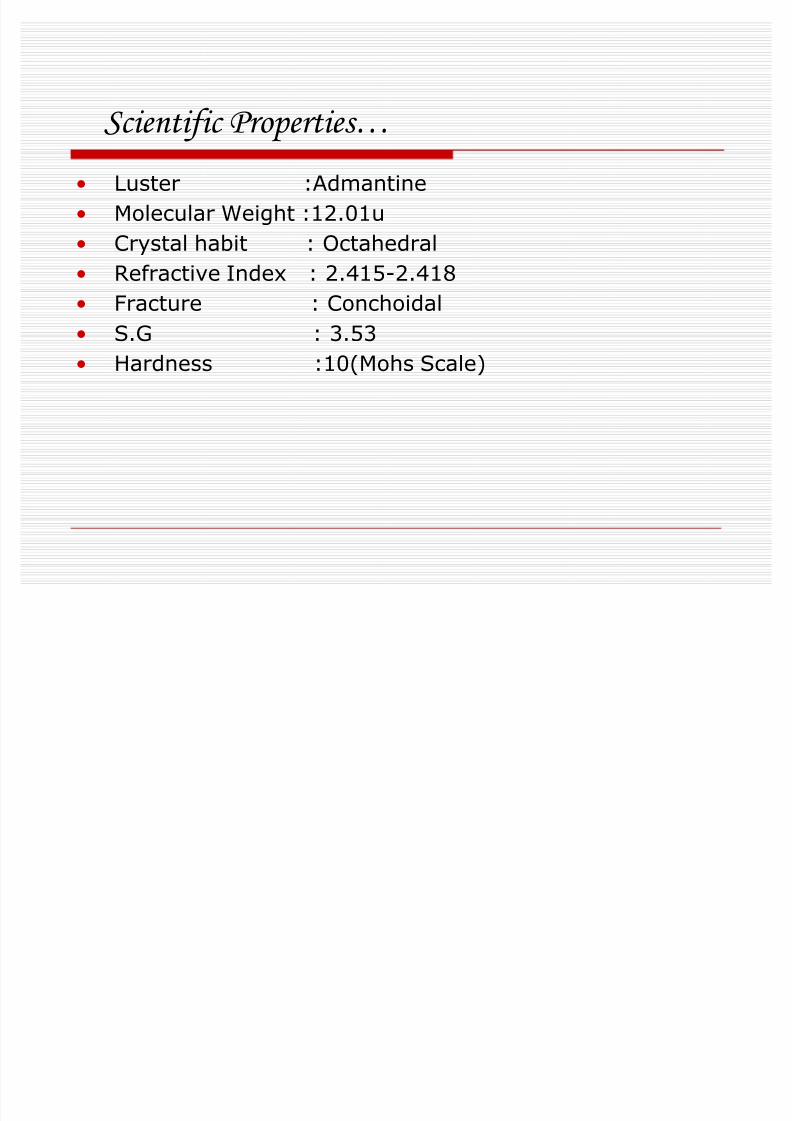

Scientific Properties« Luster :Admantine

Molecular Weight :12.01u

Crystal habit : Octahedral

Refractive Index : 2.415-2.418 Fracture : Conchoidal

S.G : 3.53

Hardness :10(Mohs Scale)

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 11/48

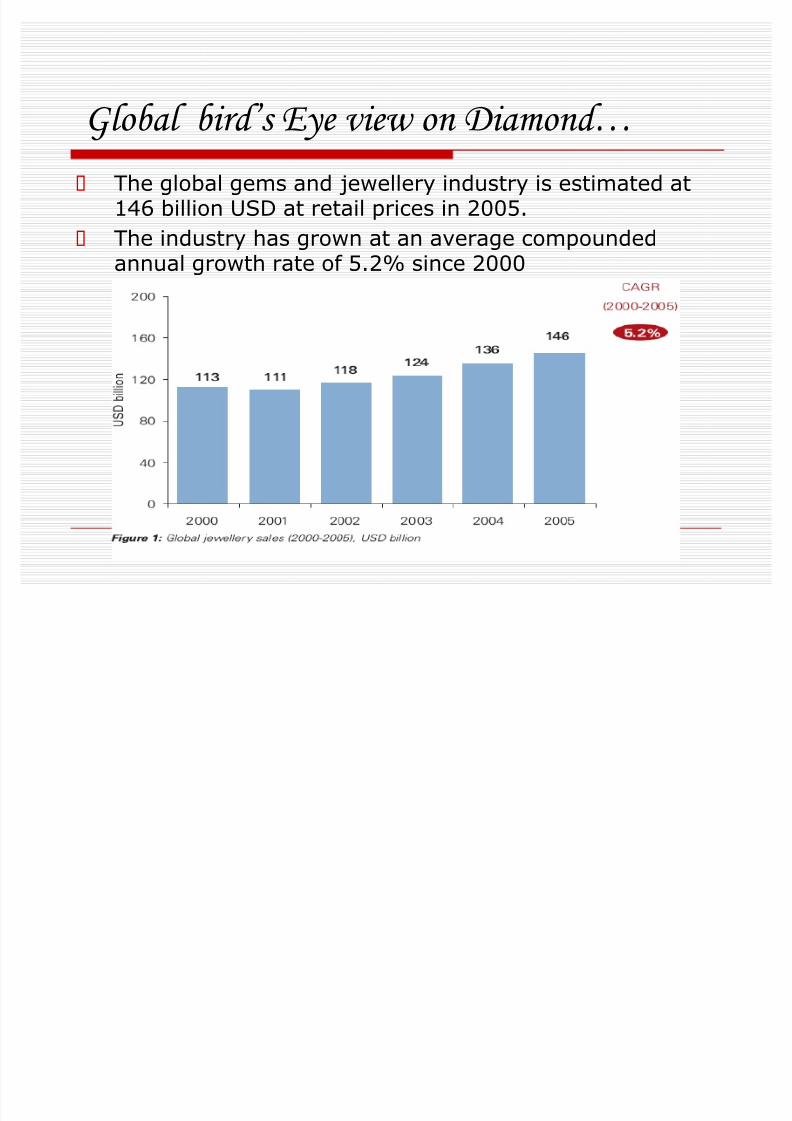

G lobal bird·s Eye view on Diamond« The global gems and jewellery industry is estimated at

146 billion USD at retail prices in 2005.

The industry has grown at an average compoundedannual growth rate of 5.2% since 2000

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 12/48

Continued«

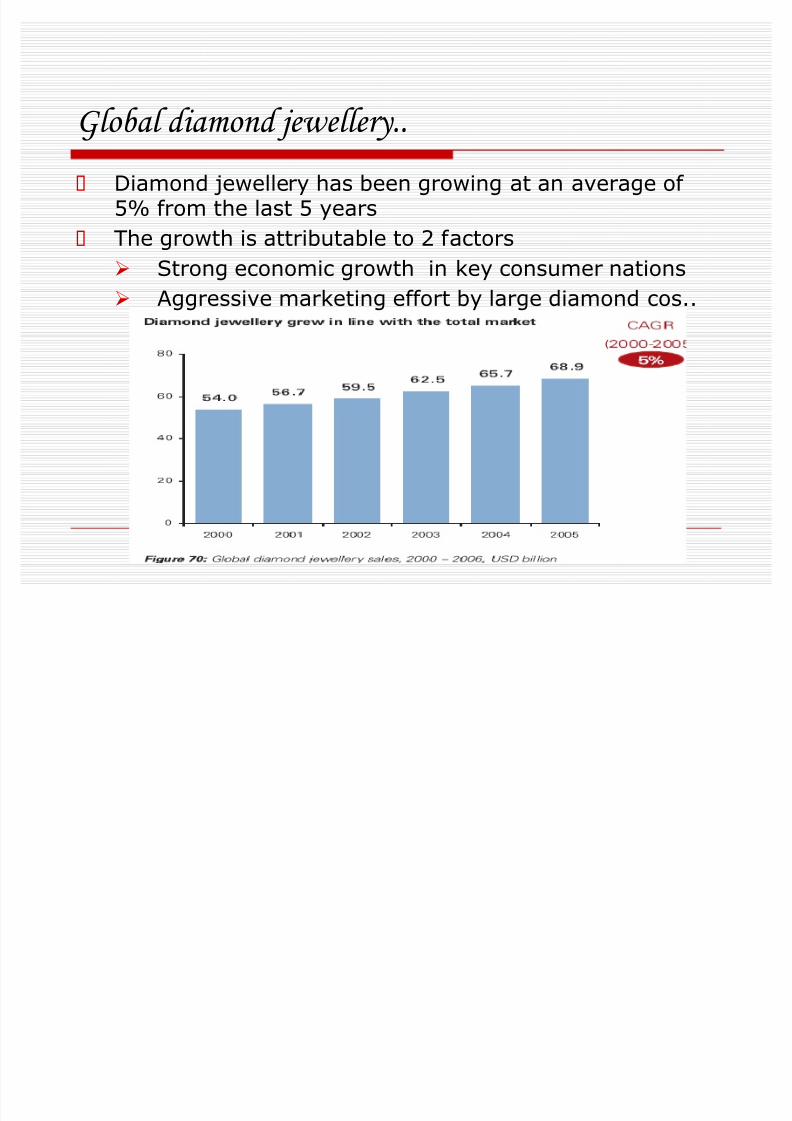

Diamond studded jewellery is the largest segment of thisindustry(2005 sales esimated at USD 69 Billion).

It has grown at CAGR of 5% in the last 5 years

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 13/48

G lobal diamond jewellery.. Diamond jewellery has been growing at an average of

5% from the last 5 years

The growth is attributable to 2 factors

Strong economic growth in key consumer nations

Aggressive marketing effort by large diamond cos..

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 14/48

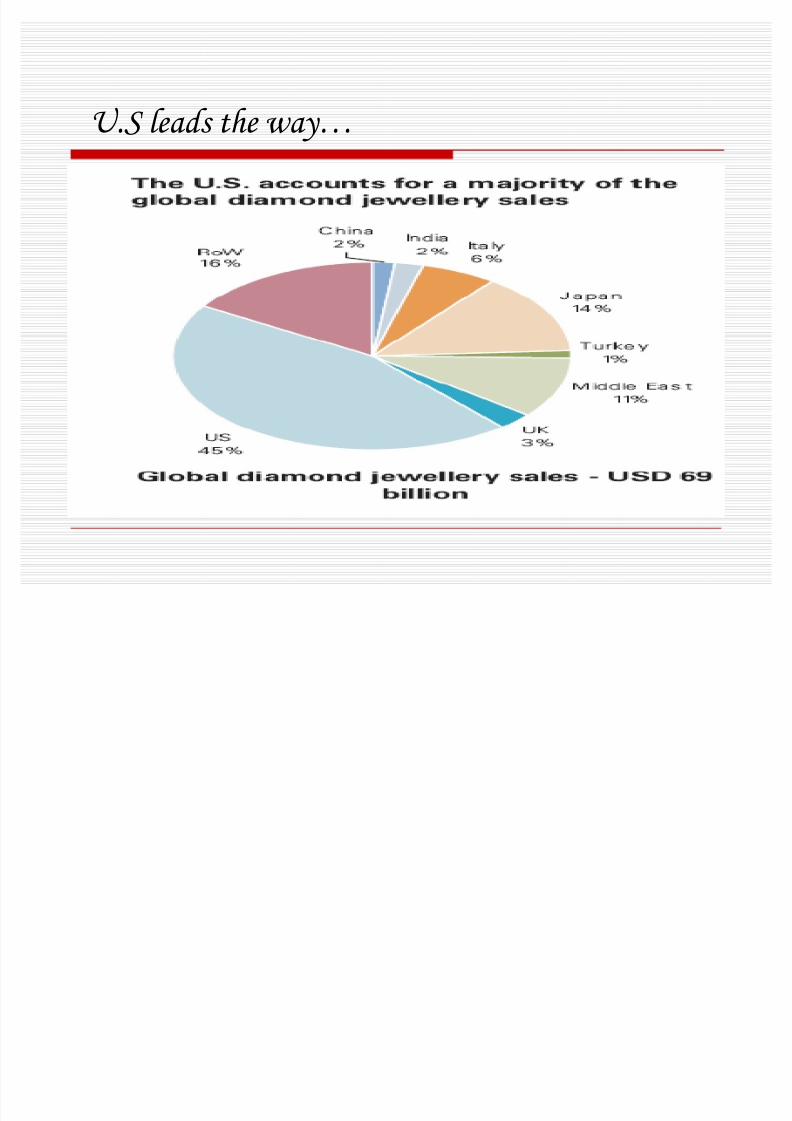

U.S leads the way«

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 15/48

Continued..

Value addition at the two ends of the value chain is thehighest with interim segments adding lower values

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 16/48

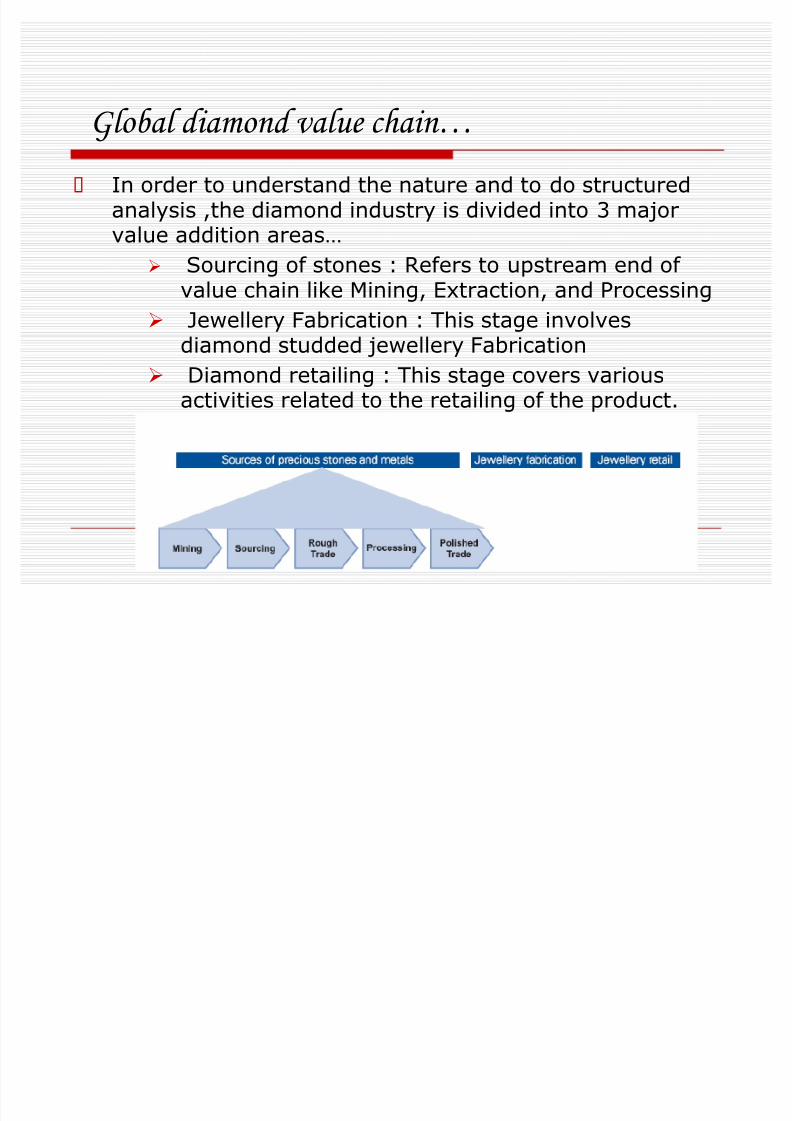

G lobal diamond value chain« In order to understand the nature and to do structured

analysis ,the diamond industry is divided into 3 majorvalue addition areas«

Sourcing of stones : Refers to upstream end of value chain like Mining, Extraction, and Processing

Jewellery Fabrication : This stage involvesdiamond studded jewellery Fabrication

Diamond retailing : This stage covers variousactivities related to the retailing of the product.

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 17/48

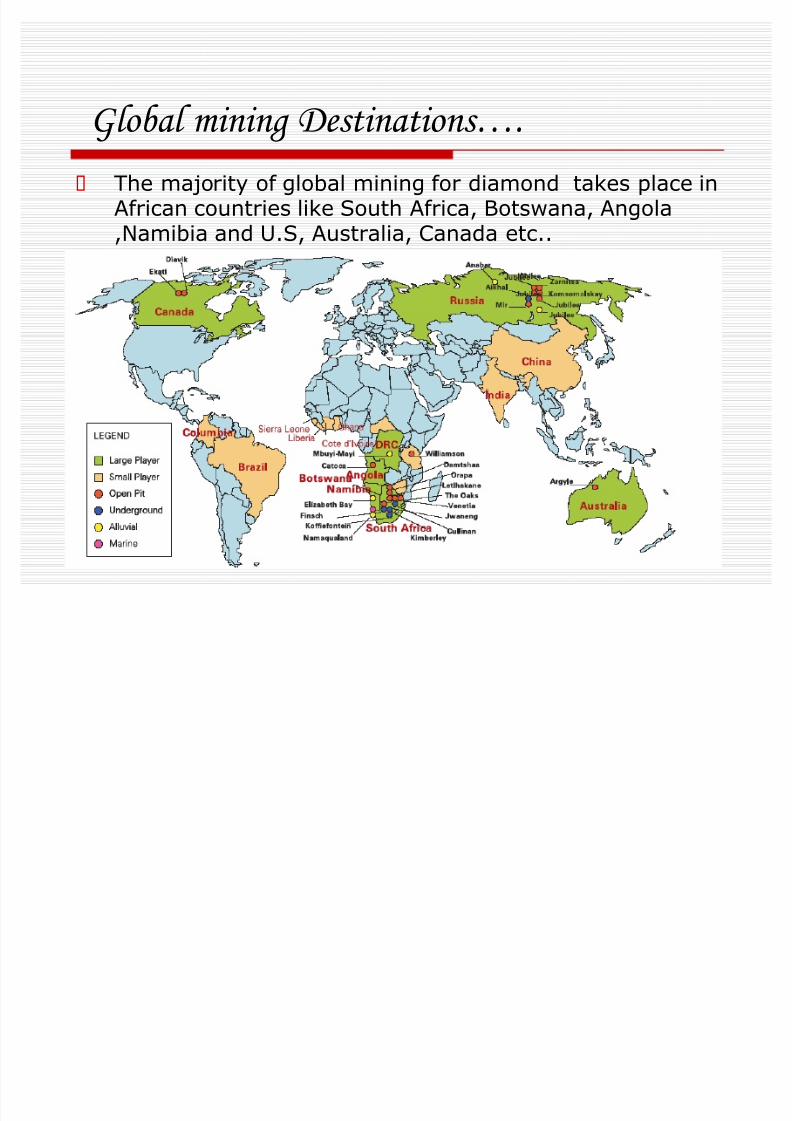

G lobal mining Destinations«. The majority of global mining for diamond takes place in

African countries like South Africa, Botswana, Angola,Namibia and U.S, Australia, Canada etc..

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 18/48

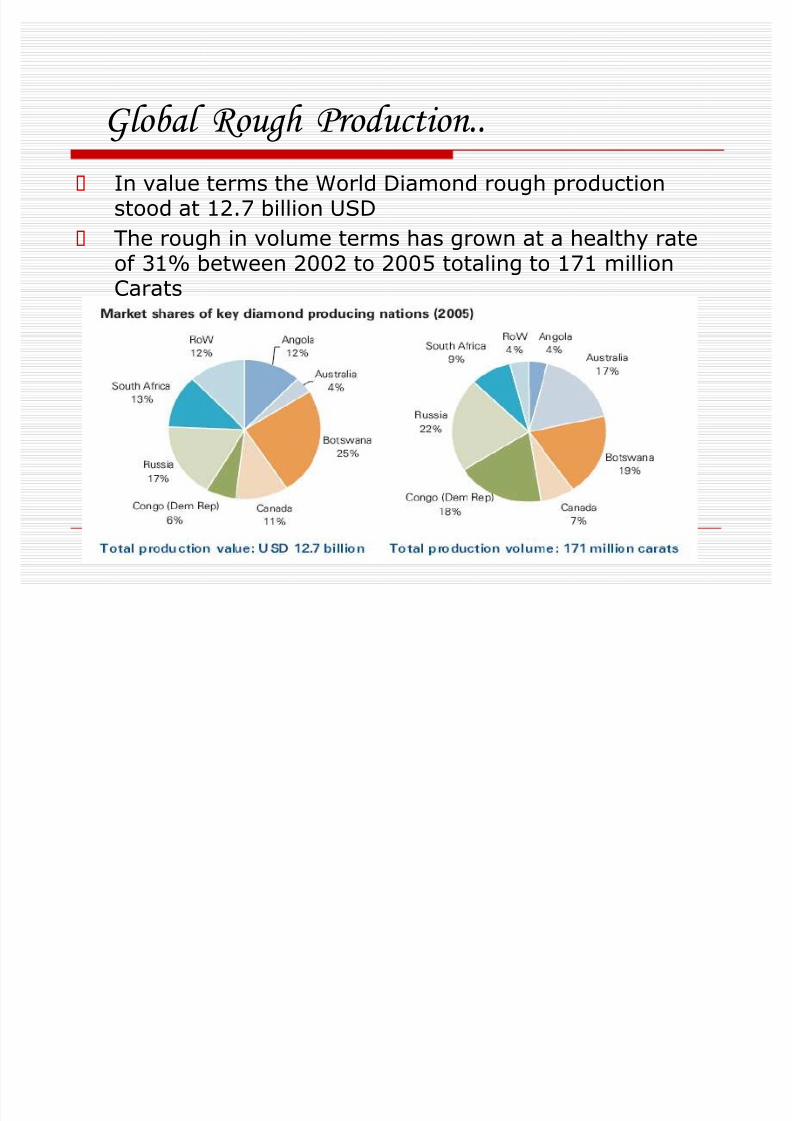

G lobal Rough Production.. In value terms the World Diamond rough production

stood at 12.7 billion USD

The rough in volume terms has grown at a healthy rateof 31% between 2002 to 2005 totaling to 171 millionCarats

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 19/48

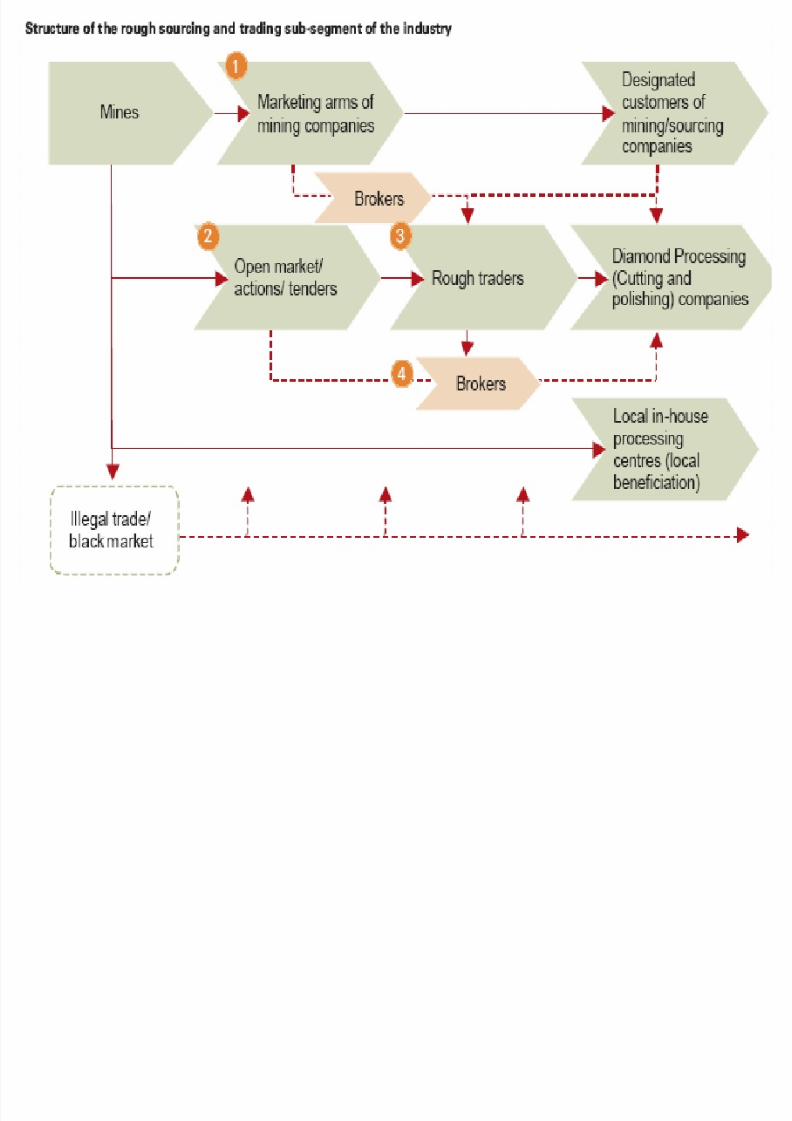

Sourcing and Trading «

This stage in the diamond value chain has been non-transparent and discreet.

But now a days ,due to more professional players,financial reporting , consolidation among the playershas led to change in the manner in which it wasoperated.

The current industry has 4 diffferent channels whereeach player can add value as..

Centralized distribution

Direct Selling

Rough Trading

brokerage

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 20/48

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 21/48

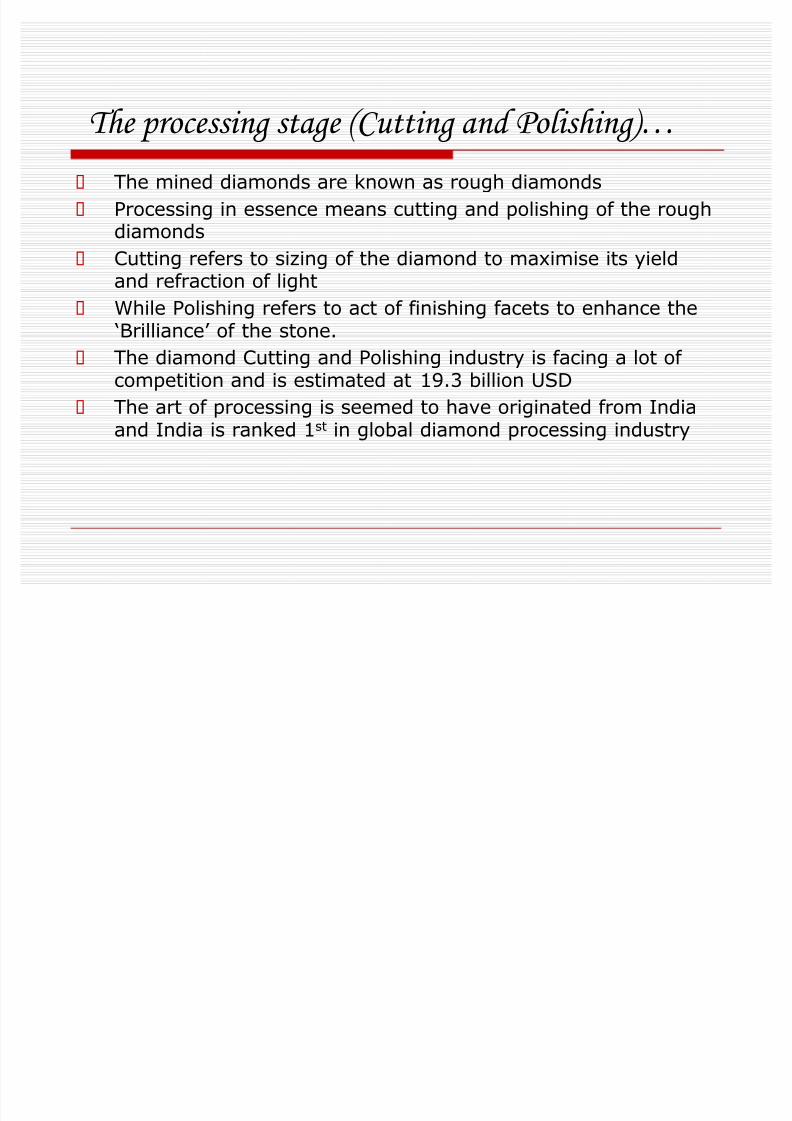

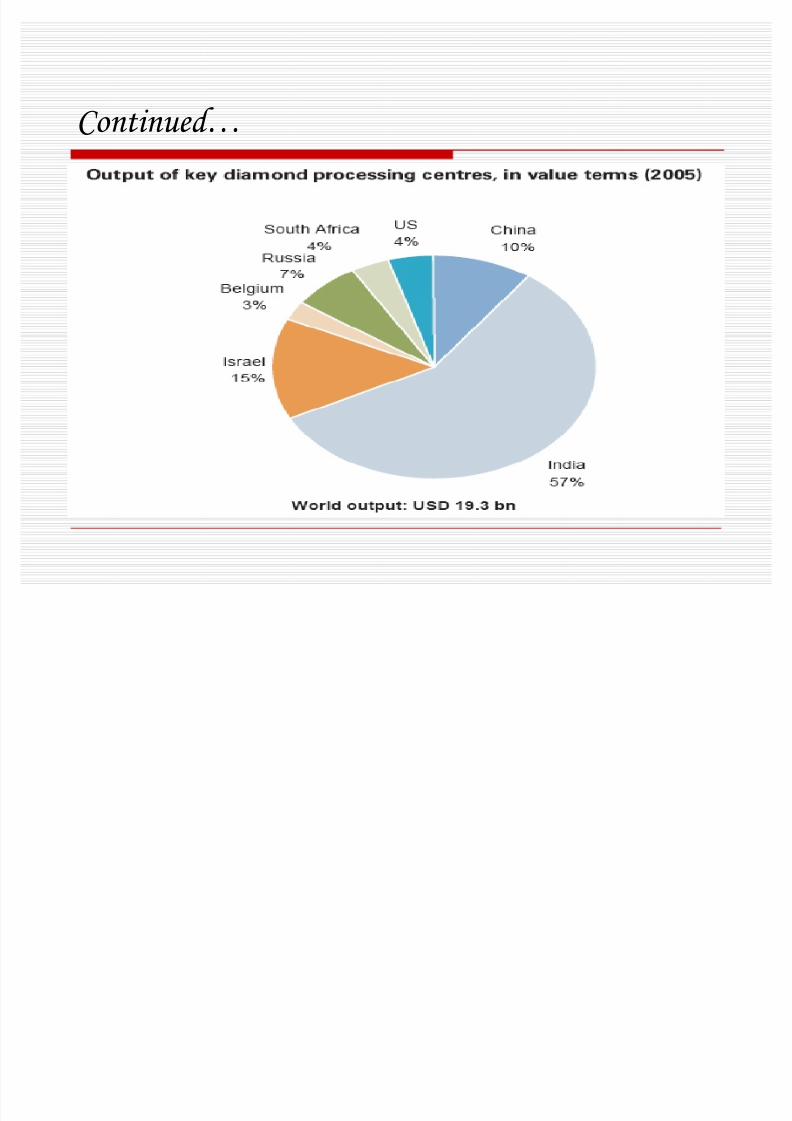

The processing stage (Cutting and Polishing)« The mined diamonds are known as rough diamonds

Processing in essence means cutting and polishing of the roughdiamonds

Cutting refers to sizing of the diamond to maximise its yield

and refraction of light While Polishing refers to act of finishing facets to enhance the

µBrilliance¶ of the stone.

The diamond Cutting and Polishing industry is facing a lot of competition and is estimated at 19.3 billion USD

The art of processing is seemed to have originated from Indiaand India is ranked 1st in global diamond processing industry

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 22/48

Continued«

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 23/48

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 24/48

Role of De Beers

De beers is the largest diamond mining company in theworld

The co was founded in 1988 and is based inJohanasburg, South Africa..

The De Beers currently holds 40% of the worldsDiamond mines by value

The co produces and controls hugh reserves of diamondmines

The Sales and marketing arm of De Beers is a companycalled DTC (Diamond Trading Company)

DTC sells around 45% of the worlds rough by value tothe worlds leading Diamondtaires called as µSightholders¶

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 25/48

DTC continued..

These sightholders are selected on the basis of theirability to add value to diamond, their adherence to DTCrules and Diamond Best Practices Principles..

It operates with a punchline µA Diamond is Forever¶

DTC in India operates with 4 different brands likeNakshtra, Arisia, Asmi, and Sangini..

Its campaigns show diamond as a symbol of commitment, love, regality, mystique ness have beenhighly successful in creating high recall value for the

brand

DTC in last 10 years helped Indian market to getconsolidation

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 26/48

W hat's moving the market..

Growth in the diamond jewellery sales have renownedinterest in diamond mining deposits.

As per µDiamond Facts 2005¶(Diamond industry Report-Northwest Territories Canada) total expenditure ondiamond exploration in 2004 was estimated to be around$300 million

Out of two-thirds were invested by industry majors likeDe beers, Rio tinto, Alrosa and BHP Billiton

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 27/48

INDIAN PERSPECTIVE OF DIAMONDS..

Diamond and jewellery has been part of Indiancivilization from since its recorded history

But the real growth has been from last 2 decades

In 1966 the export turnover of the industry was just 220million which has now grown to 15 billion in 2005-06

It is now contributing to the 18% of the indian exportsand securing healthy foreign exchange

Indian Gems and jewellery is now backed by full fledgedgovt agency called Gems and Jewellery export promotioncouncil (GJEPC)

There are some far reaching changes expected in indiangems and jewellery sector

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 28/48

Indian gems and jewellery Industry

Indian gems and jewellery has grown rapidly inconsumption terms (CAGR of 10% in last 5 years)

As per 2005 figures it is estimated at USD at 12.17Billion

It is estimated to grow at 7.64% to reach to 13.1 USDBillion in 2006-07

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 29/48

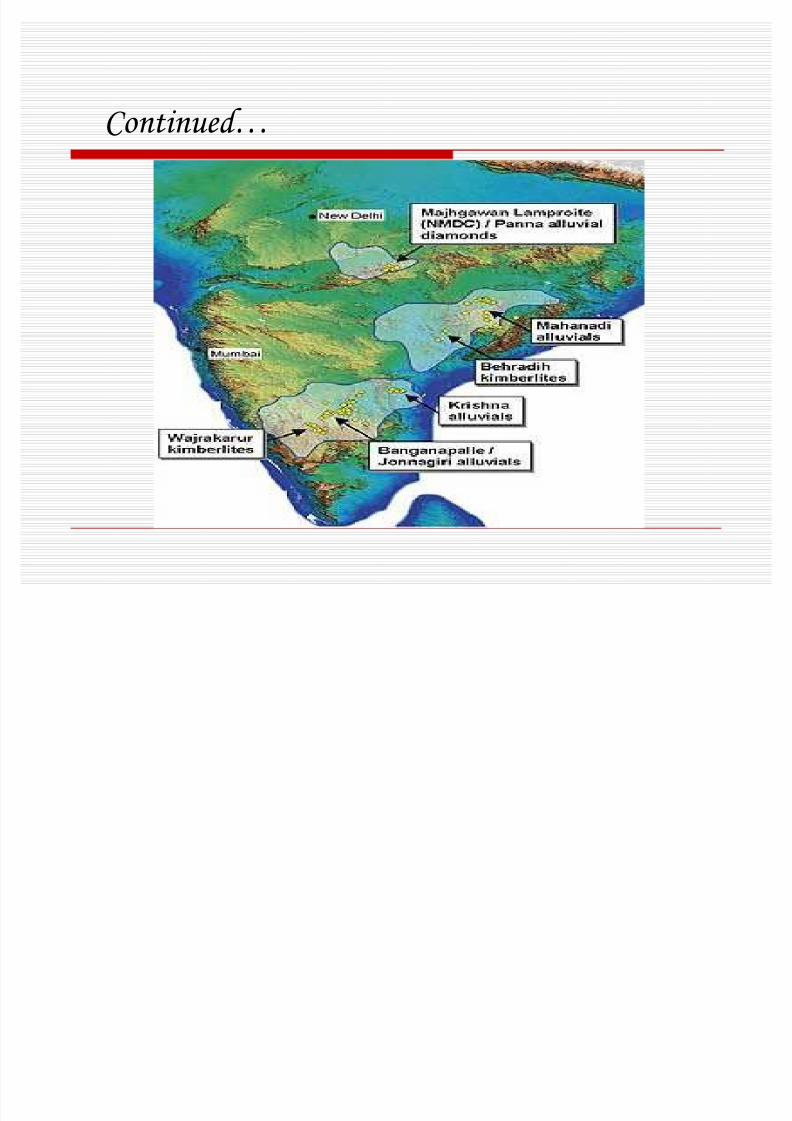

Diamond mining Destinations in India..

Golconda in A.P has the distinction of being the 1st

diamond mining site India

It has large reserves of diamonds even today

In rest of India, diamond mining is done in Orrisa, U.P,Chattisgarh, A.P, Karnataka etc,..

India's known diamond reserves are currently estimatedat 4580336 carats as per country's National MineralSurvey

Some 84000 are to be sold every year

Kimberley Process is followed while exploration is done

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 30/48

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 31/48

Indian Diamond CPD Industry«

India is largest player in the diamond processingindustry ,processing over 57% of worlds rough stock of diamond by value

In volume terms it accounts for almost 92% of worlds

rough cutting and polishing(11 out 12 diamonds in theworld are processed by india)

India¶s exports of cut and polished diamonds are stoodat USD 11.8 Billion in 2005 and around USD 12.5 billionin 2006

The majority of the cutting and polishing in india is done

in Surat, Mumbai and jaipur In the face of severe competition the CPD industry is

likely to consolidate and integrate vertically as well ashorizontally

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 32/48

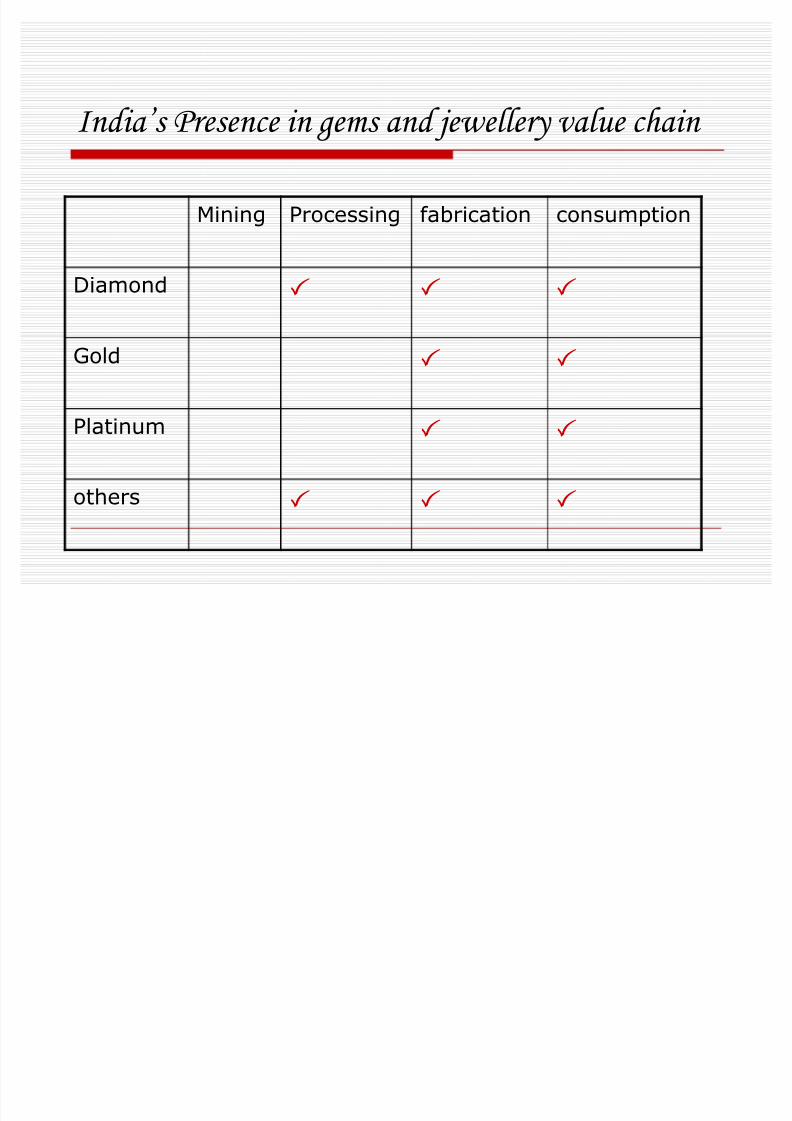

India·s Presence in gems and jewellery value chain

Mining Processing fabrication consumption

Diamond

Gold

Platinum

others

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 33/48

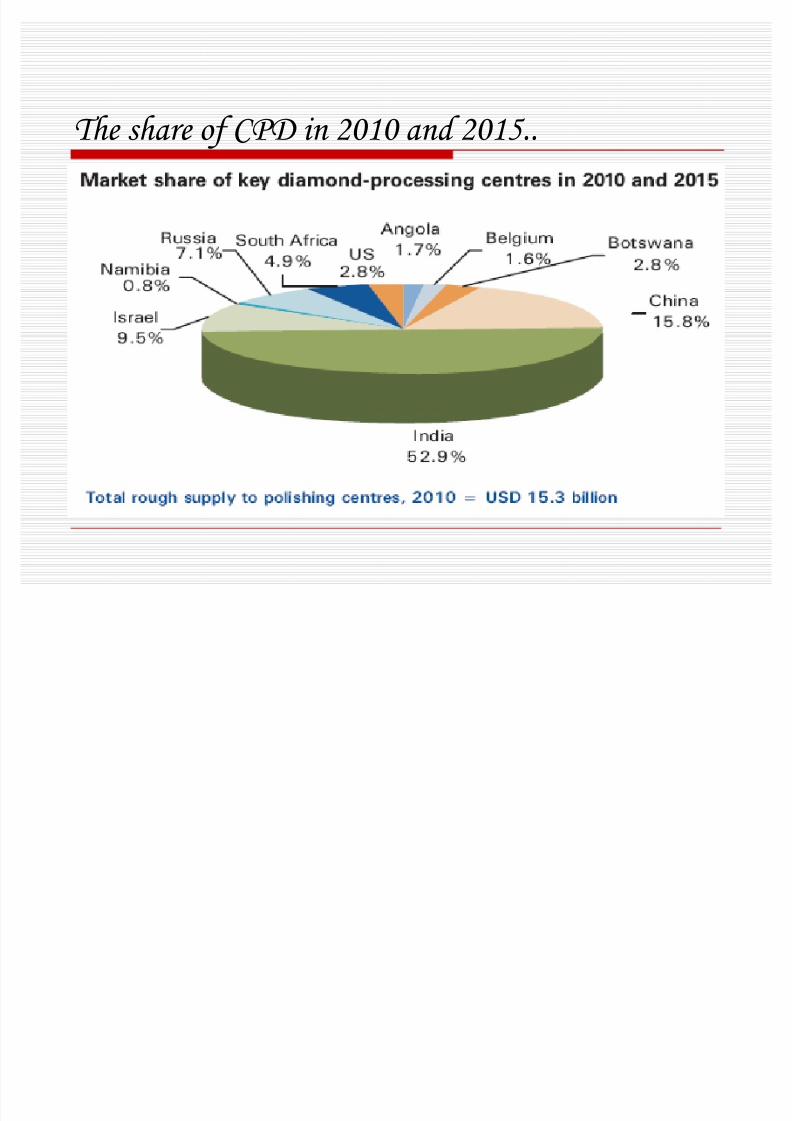

The share of CPD in 2010 and 2015..

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 34/48

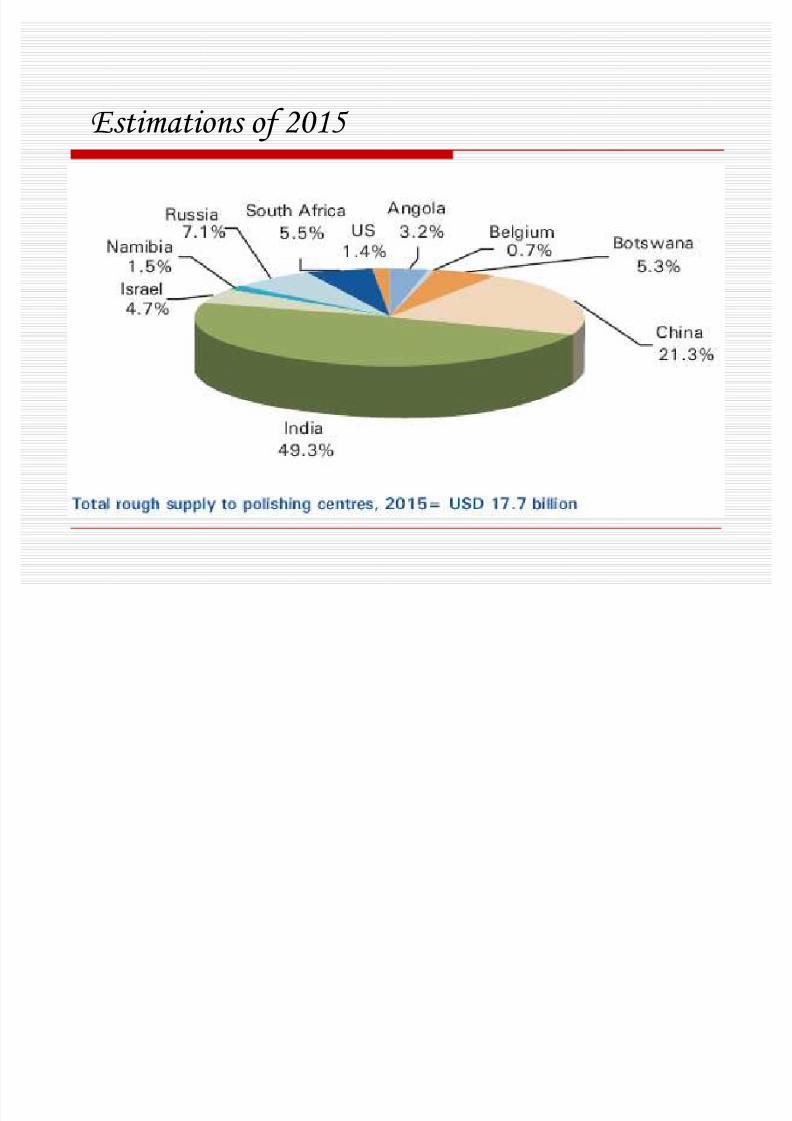

Estimations of 2015

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 35/48

Export destinations for polished diamonds by

value..

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 36/48

Indias diamond jewellery market«

India is one of the worlds fastest growing market fordiamond jewellery

As per DTC, the diamond jewellery market is estimatedat USD 1.5 billion ( Rs. 6600 crores industry)

Demand for diamond jewellery in India is grown at aCAGR of 43.5% in last 5 years

In last 3 years in a row, it is the fastest growing in theworld with average of 20% plus growth..

As per estimates the global diamond jewellery isexpected to be of USD 75 billion and USD 95 billion by2015

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 37/48

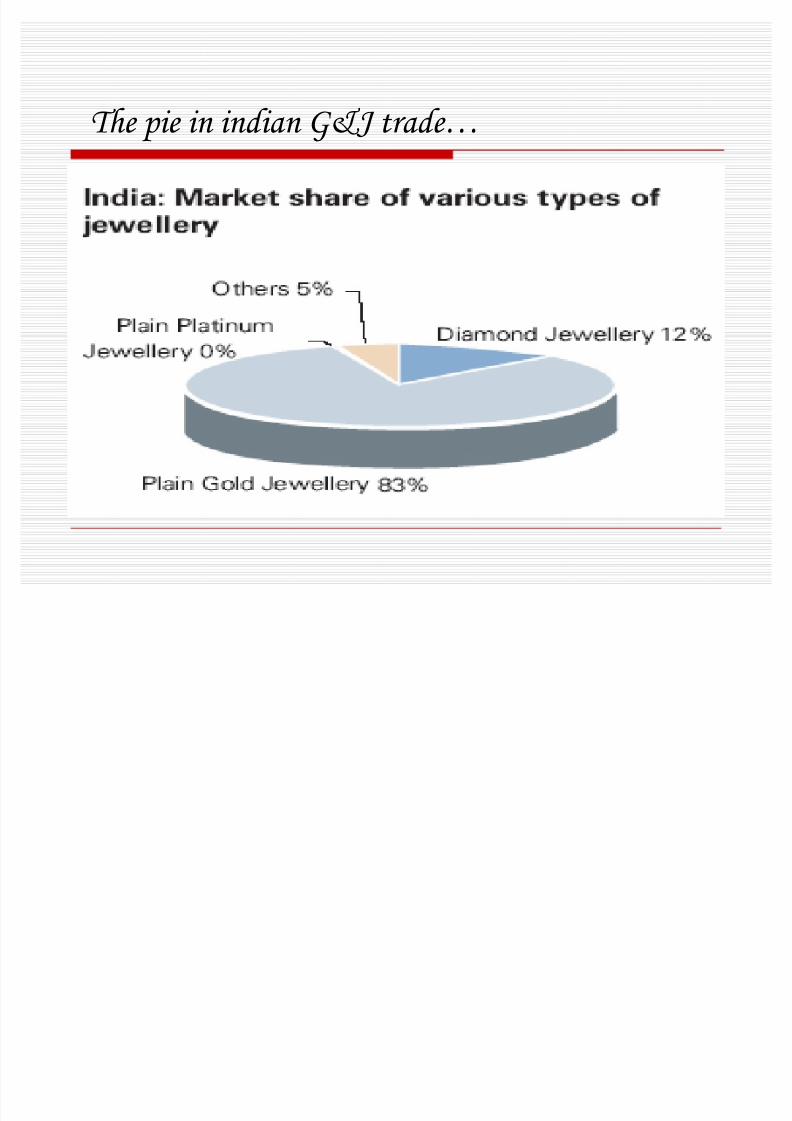

The pie in indian G& J trade«

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 38/48

Major players in the market..

Company Owner Key highlights

Asian Star co Ltd Shah and kothari Profits in the range

$5 million per yr.Highest exporteraward by DTC

Saushish DiamondsLtd.

Ramesh kumarGoenka

Largest Diamond co.T.O around $200million.100% export

oriented unitSui Raj DiamondJewelllery Ltd

Sui Raj group 5TH largest in india.T.O of $200 million.exports of processeddiamonds

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 39/48

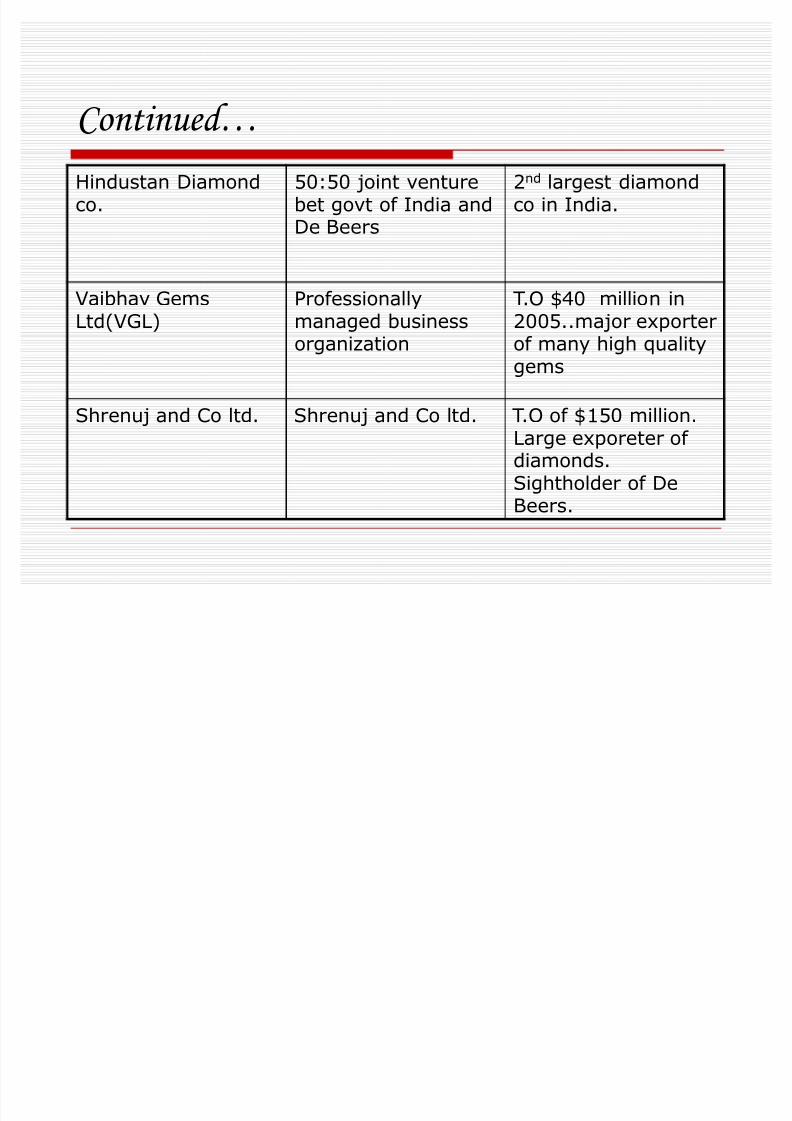

Continued«

Hindustan Diamondco.

50:50 joint venturebet govt of India andDe Beers

2nd largest diamondco in India.

Vaibhav GemsLtd(VGL)

Professionallymanaged businessorganization

T.O $40 million in2005..major exporterof many high qualitygems

Shrenuj and Co ltd. Shrenuj and Co ltd. T.O of $150 million.Large exporeter of diamonds.Sightholder of DeBeers.

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 40/48

Continued..

gili Gitanjali group One of the largestdiamond groups inIndia. Niche player in18 carat brandeddiamond jewellery.Tie ups with severallifestyle stores

Intergold Rosyblue which isworlds largestdiamiond

manufacturing co

Largest diamondretailer in india. 24exclusive showrooms

across various cities.finest designs andquality.

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 41/48

Indian States and Their performance«

Indian states show variable performance when it comesto diamond market.

Among the different Indian states ,Maharashtra, Gujarat,and Andhra Pradesh are leading in total diamond

consumption.

In an Industry of $1.5 billion USD (6600 crores),morethan 50% is accounted for in these states.

Other states like Rajasthan, Karnataka, Delhi are catchinup well to drive the growth seen in last few years.

A lot of the demand is attributed to increasing per capitaincome, changing lifestyles, consumption drivenbehavior.

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 42/48

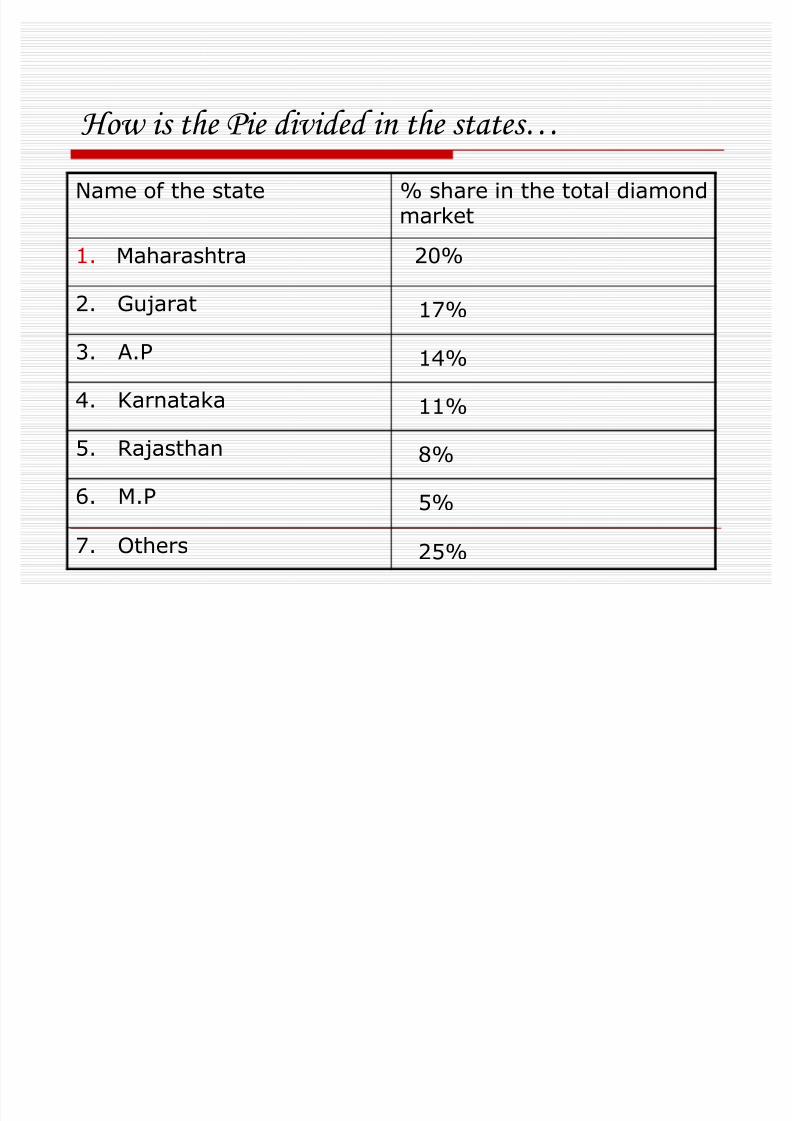

How is the Pie divided in the states«

Name of the state % share in the total diamondmarket

1. Maharashtra 20%

2. Gujarat 17%

3. A.P 14%

4. Karnataka 11%

5. Rajasthan 8%

6. M.P 5%

7. Others25%

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 43/48

How The Pie Looks«

Maharashtra

Gujarat

A.P

Karnataka

Rajasthan

M.P

Others

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 44/48

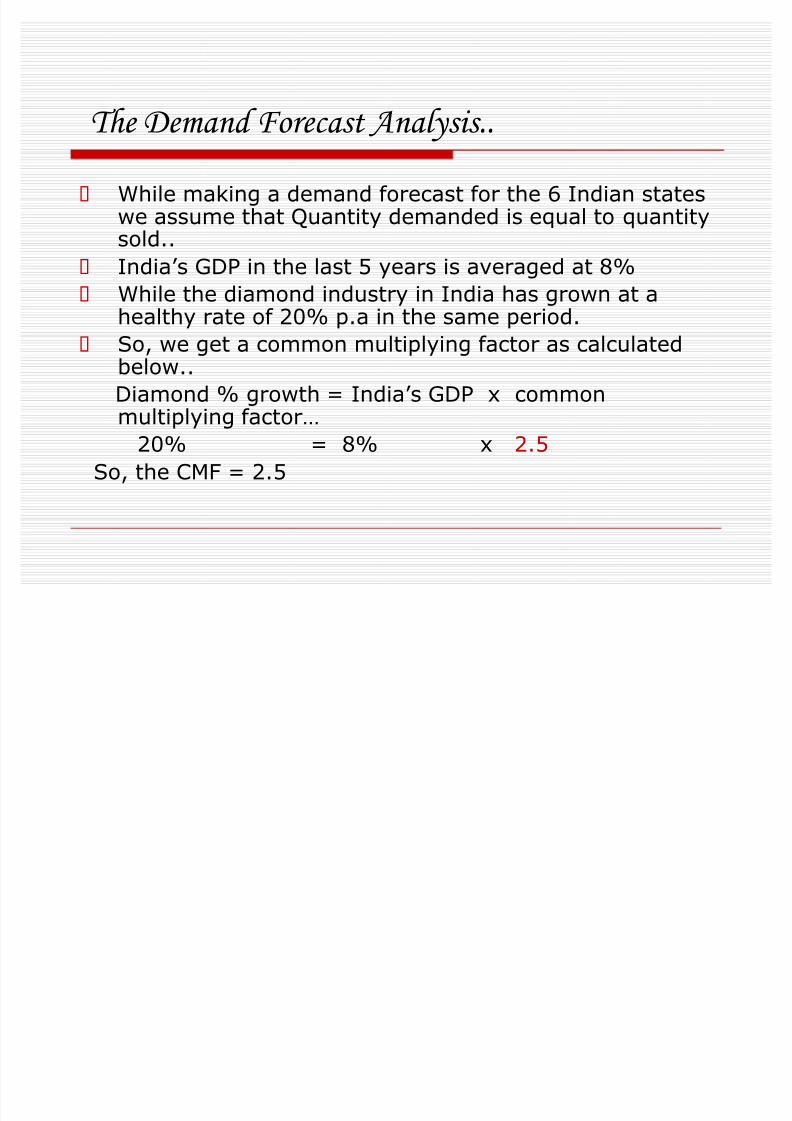

The Demand Forecast Analysis..

While making a demand forecast for the 6 Indian stateswe assume that Quantity demanded is equal to quantitysold..

India¶s GDP in the last 5 years is averaged at 8%

While the diamond industry in India has grown at ahealthy rate of 20% p.a in the same period.

So, we get a common multiplying factor as calculatedbelow..

Diamond % growth = India¶s GDP x common

multiplying factor«20% = 8% x 2.5

So, the CMF = 2.5

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 45/48

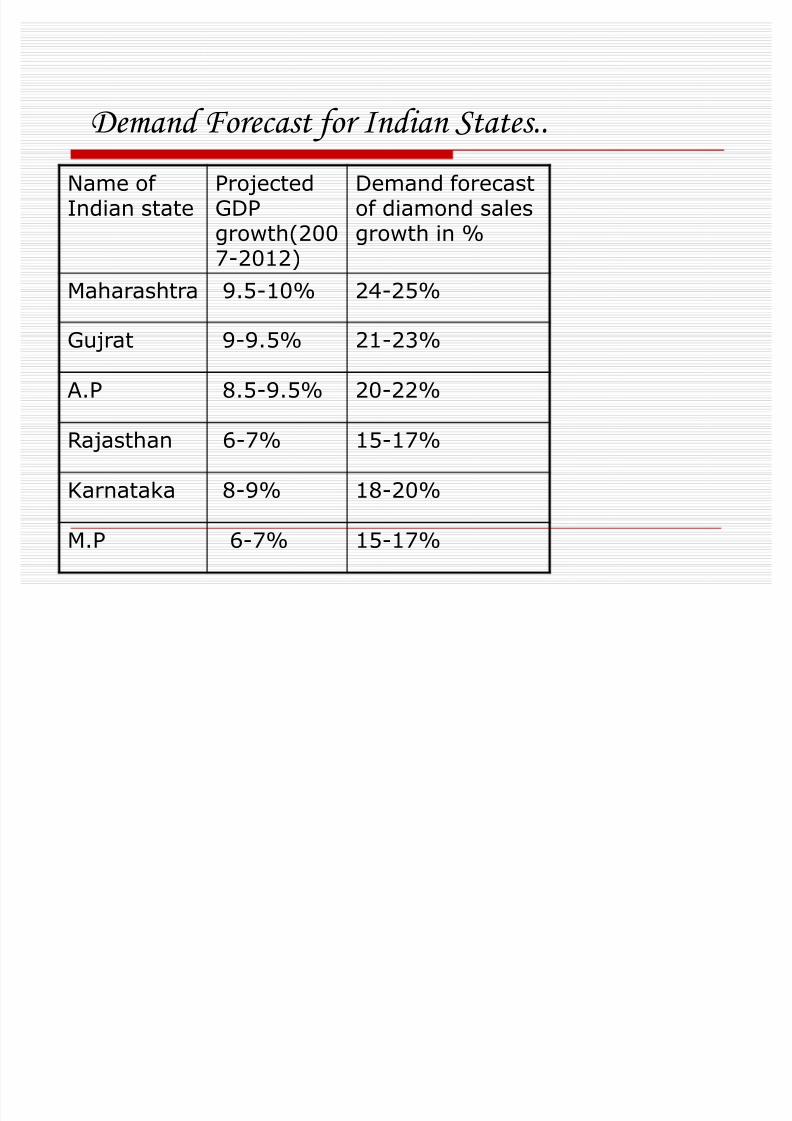

Demand Forecast for Indian States..

Name of Indian state

ProjectedGDPgrowth(2007-2012)

Demand forecastof diamond salesgrowth in %

Maharashtra 9.5-10% 24-25%

Gujrat 9-9.5% 21-23%

A.P 8.5-9.5% 20-22%

Rajasthan 6-7% 15-17%

Karnataka 8-9% 18-20%

M.P 6-7% 15-17%

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 46/48

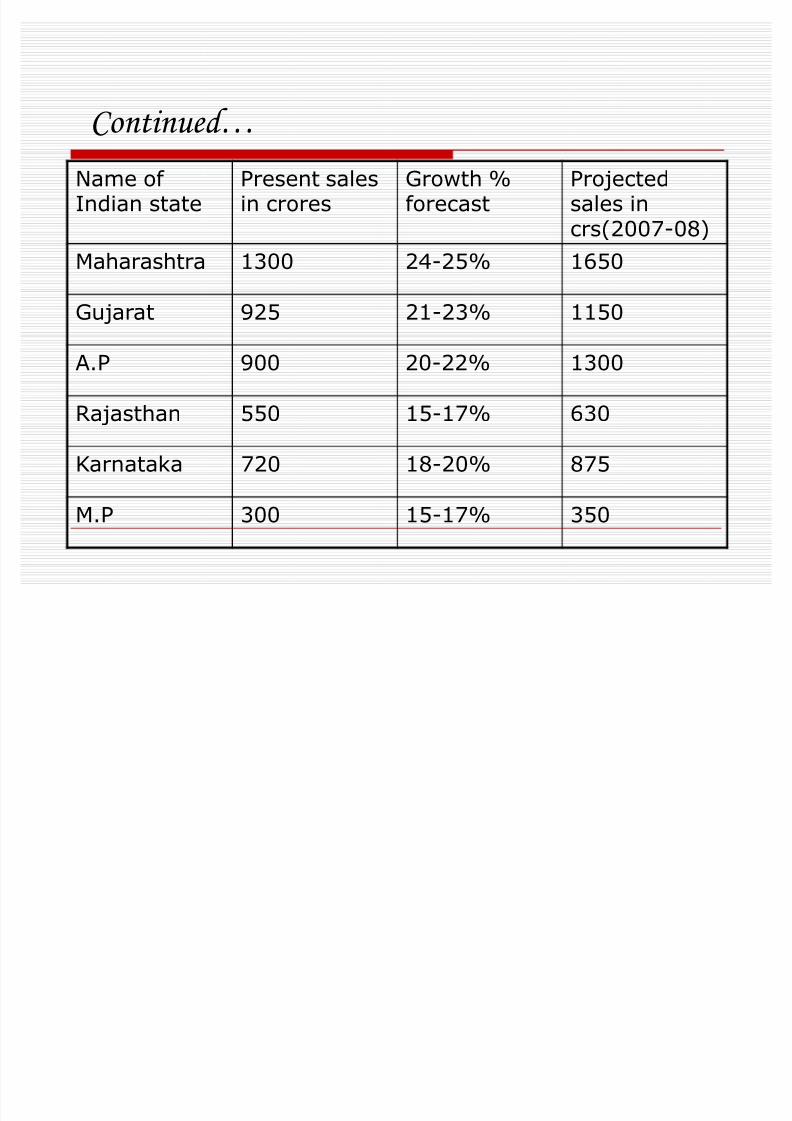

Continued«

Name of Indian state

Present salesin crores

Growth %forecast

Projectedsales incrs(2007-08)

Maharashtra 1300 24-25% 1650

Gujarat 925 21-23% 1150

A.P 900 20-22% 1300

Rajasthan55

015

-17% 630

Karnataka 720 18-20% 875

M.P 300 15-17% 350

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 47/48

8/8/2019 Diamond Prjct

http://slidepdf.com/reader/full/diamond-prjct 48/48

Roadmap for the future..

The future of the industry is quite promising but thesector is facing competition from gradual decrease in theplain jewellery.

Competition from consumer durables has become a

major threat

Shrinking margins and shortened fashion cycles haveadded to the concerns

A way ahead is to tap the latent markets , use of technology, aggressive marketing policies, Anticipation

of fashion cycles and new product offerings will definitelyhelp to boost the demand.