Disclaimer

2

This presentation does not constitute an offer of securities for sale in the United States of America or any other jurisdiction.

Certain information contained in this document may include projections and forecasts. They express objectives based on current assessments and estimates of the Group’s executive management which are subject to numerous factors, risks and uncertainties. Consequently, reported figures and assessments may differ significantly from projected figures. The following factors among others set out in the Reference Document (Document de Référence) filed with the French Financial Markets Authority (Autorité des Marchés Financiers - AMF) on April 9, 2014 which is available on Kering’s website at www.kering.com may cause actual figures to differ materially from projected figures: any unfavourable development affecting consumer spending in the activities of the Group in France and abroad, notably for products and services sold by the Luxury Goods and Sport & Lifestyle brands, the events, crises, fears, and resulting costs of complying with environmental, health and safety regulations and all other regulations with which Group companies are required to comply; the competitive situation on each of our markets; exchange rate and other risks related to international activities; risks arising from current or future litigation. Kering gives no commitment to updating and/or revising and/or commenting any projections and forecasts, or their impact on the results and perspectives of the Group, which may be contained in this presentation.

The information contained in this document has been selected by the Group’s executive management to present Kering’s Full-year 2014 results. This document has not been independently verified. Kering makes no representation or undertaking as to the accuracy or completeness of such information. None of the Kering or any of its affiliates representatives shall bear any liability (in negligence or otherwise) for any loss arising from any use of this presentation or its contents or otherwise arising in connection with this presentation.

IN NO WAY DOES KERING ASSUME ANY RESPONSIBILITY FOR ANY INVESTMENT OR OTHER DECISIONS MADE BASED UPON THE INFORMATION PROVIDED IN THIS PRESENTATION. READERS ARE ADVISED TO REVIEW THE COMPANY'S REFERENCE DOCUMENT AND THE COMPANY'S APPLICABLE AMF FILINGS BEFORE MAKING ANY INVESTMENT OR OTHER DECISION.

3

François-Henri Pinault Chairman & CEO

4

2 0 1 4 , b u i l d i n g u p

Jean-François Palus

2014 annual results

Group Managing Director

Our multi-brand model – virtuous and distinctive

5

Group revenue dynamic (comparable growth, in %)

Group revenue breakdown (by region, and comparable growth in %)

Group EBITDA (in €m and change in %)

Free cash flow from operations (reported change, in €m)

Steady revenue growth quarter after quarter, higher comparable consolidated EBIT

Western

Europe

31% (+2%)

North America

21% (+6%) Japan

10% (+7%)

Asia Pacific

26% (+5%)

RoW

12% (+6%)

2014 Comparable

FX change

Net impact of

currencies*

2013

1,991

-7.1%

2,043

+4.5%

1,078

+26%

2013 2014

857

(*) Combined currency and hedging impact

FY 14:

+4.5% FY 13:

+4.0% 2014 €10bn

4.2% 4.1%

4.6%

4.9%

Q1 14 Q2 14 Q3 14 Q4 14

2 0 1 4 , b u i l d i n g u p

Growth by segment (comparable revenue growth, in %)

Breakdown of Luxury revenues (by region, and comparable growth, in %)

Western

Europe

32% (+2%)

North America

19% (+6%) Japan

10% (+13%)

Asia Pacific

31% (+5%)

RoW

8% (+6%)

2014 €6.8bn

6.4%

5.5%

3.8% 4.3%

-0.2%

1.1%

6.1% 6.4%

Q1 14 Q2 14 Q3 14 Q4 14

Luxury Sport & Lifestyle

Well-balanced, resilient profile; multiple opportunities

Luxury: plentiful growth opportunities

Geographic expansion

∞ Huge growth drivers in key markets

Complementary stages of maturity

∞ Significant potential

APAC: 22% of Saint Laurent revenues

North America: 13% of Bottega Veneta

revenues

Distribution channels

∞ Confirmed growth momentum

Luxury retail sales: +8% comparable

Luxury e-commerce: +20% comparable

∞ Opportunities from directly operated

stores

61% of Saint Laurent revenues

39% of Other Luxury Brands revenues

Product offer

∞ Clear positioning of each brand

Complementary brand portfolio

∞ Significant potential

Ready-to-wear and shoes: 11% of

Bottega Veneta revenues

Build strength in watches

6

Analysis of opportunities guiding capital allocation, ensuring sustainable performances

2 0 1 4 , b u i l d i n g u p

Integrated, pragmatic, responsive operational model

7

∞ Increasingly relevant value proposition for our customers

∞ Ongoing adaptation of the structure and effectiveness of our collections

∞ Constant search for product categories whose potential remains underexploited

∞ An innovative model: Kering Eyewear

∞ Adapted expansion of our geographic footprint

∞ Priority given to directly operated stores

∞ Flexible, down-to-earth approach to Wholesale

∞ Focus on consolidating Group digital leadership

∞ Gradual expansion of shared services model

∞ Development of Supply Chain across all entities

∞ Broad-based project to modernize and optimize our information systems

Distribution

Creation and products

Operating processes

Th

ree

actio

n a

rea

s

2 0 1 4 , b u i l d i n g u p

Kering Eyewear, a strategic initiative

8

∞ A major market, with high-end segment experiencing double-digit growth

∞ A strategic aspirational category

∞ Revenue and distribution synergies:

Gradual but systematic implementation across our entire brand portfolio

Internalization of design, product development and marketing; complete oversight over

outsourced manufacturing

Optimized distribution

∞ Progressive ramp-up (2015-2016) and positive earnings contribution in 2017

2 0 1 4 , b u i l d i n g u p

Integrated, pragmatic, responsive operational model

9

∞ Increasingly relevant value proposition for our customers

∞ Ongoing adaptation of the structure and effectiveness of our collections

∞ Constant search for product categories whose potential remains underexploited

∞ An innovative model: Kering Eyewear

∞ Adapted expansion of our geographic footprint

∞ Priority given to directly operated stores

∞ Flexible, down-to-earth approach to Wholesale

∞ Focus on consolidating Group digital leadership

∞ Gradual expansion of shared services model

∞ Development of Supply Chain across all entities

∞ Broad-based project to modernize and optimize our information systems

Distribution

Creation and products

Operating processes

Th

ree

actio

n a

rea

s

2 0 1 4 , b u i l d i n g u p

∞ Brand-by-brand customization according to client requirements: in-store product availability, exchanges, store pickup...

∞ Gradual launch of new functions

∞ New site functionalities to improve client experience, traffic and conversion

∞ Boost digital marketing and social media presence

∞ Optimized tablet and smartphone applications

Reinforce the Group’s digital leadership

10

Build online presence for

the Group’s brands 1

3

Enhance the Group

brands’ online presence 2

Omni-channel and

CRM 4

Our clients

are

increasingly

…

Develop cross-channel

platforms

∞ All Group brands (apart from Boucheron, Sowind and Ulysse Nardin) run an e-commerce site

∞ Broad product, language and country coverage

∞ e-commerce now accounts for 2% of Group Luxury revenues

∞ Redefinition and uniformization of POS solutions

∞ Investment in systems and CRM favoring convergence of online and offline databases

∞ Impact on logistics

global … and seamless connected asking for

customization

2 0 1 4 , b u i l d i n g u p

Integrated, pragmatic, responsive operational model

11

∞ Increasingly relevant value proposition for our customers

∞ Ongoing adaptation of the structure and effectiveness of our collections

∞ Constant search for product categories whose potential remains underexploited

∞ An innovative model: Kering Eyewear

∞ Adapted expansion of our geographic footprint

∞ Priority given to directly operated stores

∞ Flexible, down-to-earth approach to Wholesale

∞ Focus on consolidating Group digital leadership

∞ Gradual expansion of shared services model

∞ Development of Supply Chain across all entities

∞ Broad-based project to modernize and optimize our information systems

Distribution

Creation and products

Operating processes

Th

ree

actio

n a

rea

s

2 0 1 4 , b u i l d i n g u p

12

Jean-Marc Duplaix Group Chief Financial Officer

A n a l y s i s o f r e s u l t s

2014 annual results

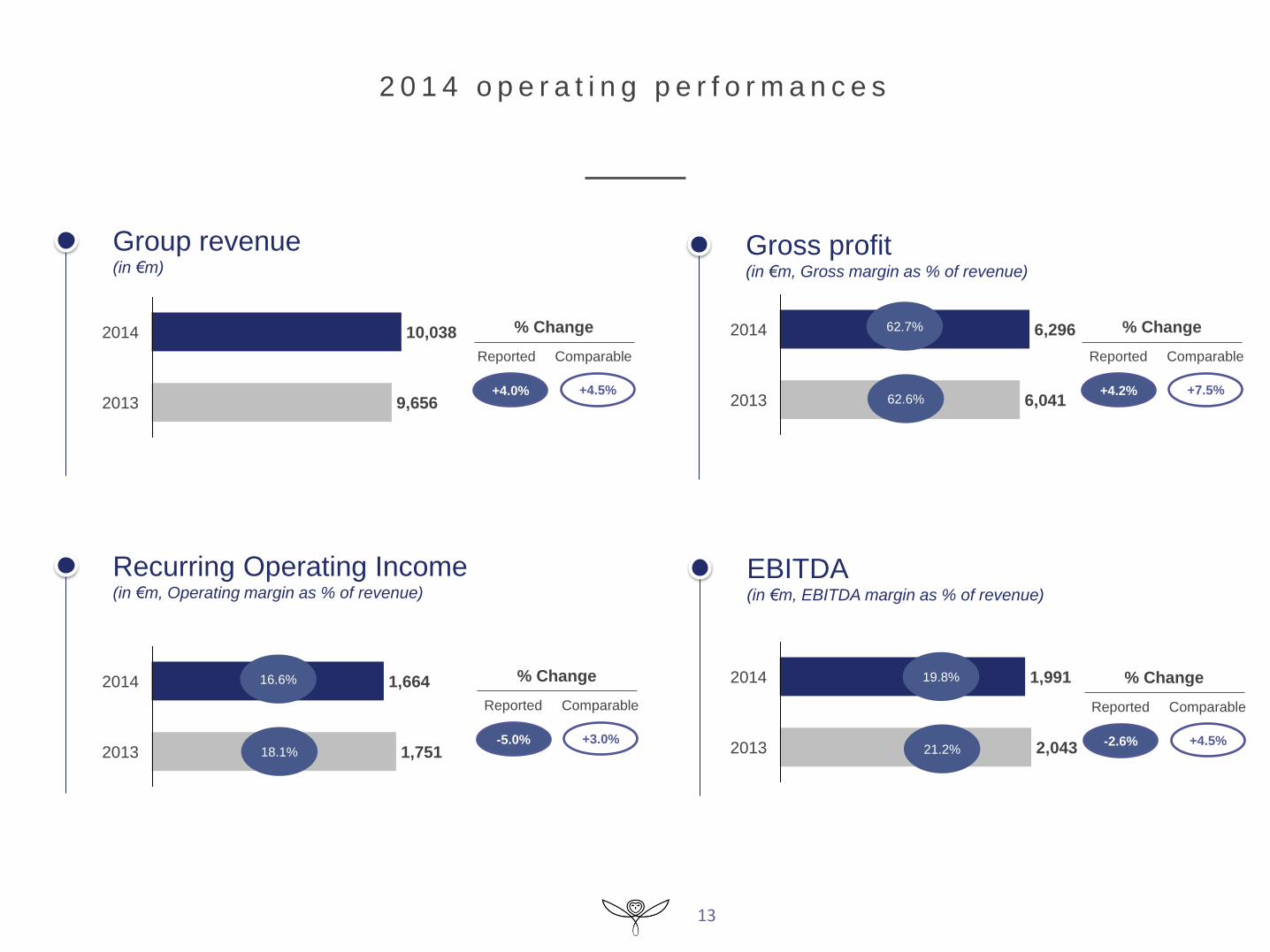

2 0 1 4 o p e r a t i n g p e r f o r m a n c e s

13

Group revenue (in €m)

Gross profit (in €m, Gross margin as % of revenue)

Recurring Operating Income (in €m, Operating margin as % of revenue)

EBITDA (in €m, EBITDA margin as % of revenue)

2014 10,038

9,656 2013

2014 6,296

6,041 2013

62.7%

62.6%

2014 1,664

1,751 2013

16.6%

18.1%

2014 1,991

2,043 2013

19.8%

21.2%

+4.5%

% Change

Reported Comparable

+4.0%

+3.0%

% Change

Reported Comparable

-5.0%

+7.5%

% Change

Reported Comparable

+4.2%

+4.5%

% Change

Reported Comparable

-2.6%

In €m 2014

Reported

change

Revenue 6,759 +6.0%

Recurring operating income Recurring operating income margin

1,666 24.6%

-1.1% -1.8pt

EBITDA EBITDA margin

1,919 28.4%

+0.4%

Gross CAPEX 372 -14.0%

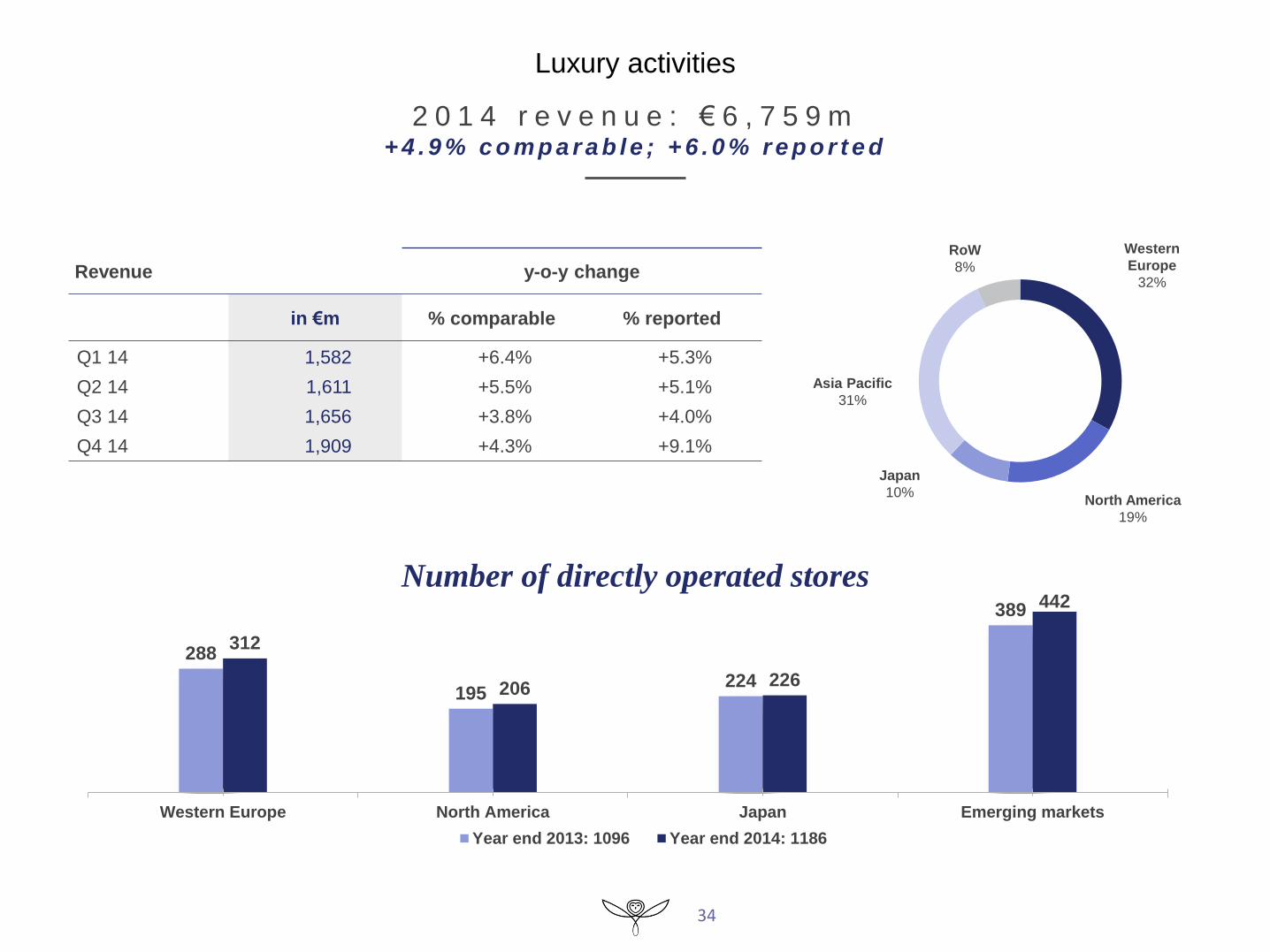

2 0 1 4 r e v e n u e : + 4 . 9 % c o m p a r a b l e

Robust revenue growth and EBIT performance

∞ Sales growth fueled by directly operated stores (+8%), with more sustained growth in mature countries

∞ Pertinence of multibrand strategy resulting in healthy …

– Sales growth, consistent throughout the year

– EBITDA performance, unchanged from 2013

– Recurring operating income

∞ Lower CAPEX, reflecting adaptation of capital allocation to

– Sector cycle

– Maturity and development priorities of each brand

Luxury activities

14

X%: comparable growth

Royalties

-3%

Wholesale

0%

Retail

+8%

Scope

+2%

FX impact

-1%

2013

6,378

2014

6,759

15

P r o g r e s s i o n o f L u x u r y c o m p a r a b l e r e c u r r i n g o p e r a t i n g i n c o m e S i g n i f i c a n t c u r r e n c y i m p a c t i n 2 0 1 4

Recurring operating income – Luxury activities (in €m and change in %)

Stable EBIT margin at Gucci (-0.1pt) and 1.2pt improvement at Bottega Veneta at comparable FX

2014

1,666

Net impact of currencies*

-6%

Comparable FX change

+5%

2013

1,684

Of which Gucci (in €m and change in %)

Of which Bottega Veneta (in €m and change in %)

2014

1,056

Net impact of

currencies*

-6%

Comparable

FX change

-1%

2013

1,132

2014

357

Net impact of

currencies*

-9%

Comparable

FX change

+17%

2013

331

(*) Combined currency and hedging impact

16

2 0 1 4 r e v e n u e : - 1 . 1 % c o m p a r a b l e

Sturdy EBIT margin in mixed environment

In €m 2014

Reported

change

Revenue 3,497 -1.8%

Recurring operating income Recurring operating income margin

1,056 30.2%

-6.7% -1.6pt

EBITDA EBITDA margin

1,199 34.3%

-6.0%

Gross CAPEX 186 -13.1%

3,497

Retail (79% of sales): +2%

2014 Royalties

-9%

Wholesale

-11%

RoW

+18%

Asia

Pacific

2013

3,561

Western

Europe

+5%

North

America

+10%

Japan

-3% +1%

X%: comparable growth

∞ Contrasted sales momentum

– Good performance from directly operated stores (+2%), notably in mature markets (+4.4%, 55% of revenue), driven

by handbags, ready-to-wear and shoes

– Tougher environment in Asia Pacific, steady deterioration of the economic climate in H2

– Gradual improvement in wholesale: exclusivity strategy and increased control over distribution

∞ Resilient EBIT margin in constant FX

– Positive gross margin momentum

– Tight OPEX control despite rising rents

∞ Adapted CAPEX

– Slower pace of store openings, further optimization of store network

17

2 0 1 4 r e v e n u e : + 1 2 . 6 % c o m p a r a b l e

Growth plan on track

In €m 2014

Reported

change

Revenue 1,131 +11.3%

Recurring operating income Recurring operating income margin

357 31.6%

+8.0% -0.9pt

EBITDA EBITDA margin

389 34.4%

+9.6%

Gross CAPEX 41 -34.2%

X%: comparable growth

2014

Retail (80% of sales): +11%

1,131

Royalties

+14%

Wholesale

+20%

RoW

+14%

Asia

Pacific

+10%

Japan

+17%

North

America

+9%

Western

Europe

+10%

2013

1,016

∞ Another year of significant revenue growth

– Double-digit growth in directly operated stores, reflecting systematic implementation of operating excellence strategy

– Outstanding wholesale momentum while maintaining exacting selectivity

– Slowdown in Asia Pacific toward year end

∞ EBIT margin maintained at very high level and increase in recurring operating income in line with medium-

term growth roadmap

∞ Tight CAPEX control

– Slower DOS opening pace (+15 net store openings, well balanced between mature and emerging markets) following

heavy investments in stores and operations in 2013

18

2 0 1 4 r e v e n u e : + 2 7 . 2 % c o m p a r a b l e

Contribution to Group growth and profitability now significant

In €m 2014

Reported

change

Revenue 707 +27.0%

Recurring operating income Recurring operating income margin

105 14.9%

+37.2% +1.1pt

EBITDA EBITDA margin

131 18.5%

+40.8%

Gross CAPEX 54 -17.0%

X%: comparable growth

2014

707

Royalties

+8%

Wholesale

+11%

RoW

+86%

Asia

Pacific

+44%

Japan

+43%

North

America

+46%

Western

Europe

+28%

2013

557

Retail (61% of sales): +40%

∞ Sales doubled over 3 years, reflecting Saint Laurent’s successful brand positioning

– Growth fueled by retail sales across all regions and all product categories (leather goods +40%, ready-to-wear +34%)

∞ Recurring operating income up 37%, EBIT margin up 110bp

– Strong gross margin momentum

– Operating leverage driven by same-store sales growth and scale effect

∞ CAPEX remaining at high level (7.7% of revenue)

– Continued selective network expansion (13 net store openings)

– Renovations in line with new concept

Other luxury brands

19

2 0 1 4 r e v e n u e : + 6 . 0 % c o m p a r a b l e

Solid performance of Couture and Leather Goods

In €m 2014

Reported

change

Revenue 1,424 +14.4%

Recurring operating income Recurring operating income margin

147 10.3%

+1.8% -1.3pt

EBITDA EBITDA margin

200 14.1%

+7.1%

Gross CAPEX 91 +0.1%

X%: comparable growth

1,424

2014 Royalties

+6%

Wholesale

+2%

Retail

+13%

Scope

+8%

FX impact

0%

2013

1,244

∞ Couture and Leather Goods: solid revenue growth (+9%)

– Double-digit increases at Balenciaga, Alexander McQueen, Stella McCartney and Christopher Kane

– Satisfactory growth of retail at Brioni, penalized by drop in Russian tourism

∞ Watches and Jewelry: volatile market conditions

– Positive performances in Jewelry:

• Improving year-end trends at Boucheron

• Solid reception of new collections at Pomellato Group

– Watches: pressure on Sowind, in environment marked by caution from distributors

∞ Slight drop in EBIT margin, primarily due to Sowind

Sport & Lifestyle

20

Puma €1,474m

Puma €1,386m

2 0 1 4 r e v e n u e : + 3 . 5 % c o m p a r a b l e

Activity turnaround confirmed in second half

In €m 2014

Reported

change

Revenue 3,245 -0.1%

Recurring operating income Recurring operating income margin

138 4.2%

-31.4% -2.0pts

EBITDA EBITDA margin

191 5.9%

-26.0%

Gross CAPEX 86 +14.3%

2014

3,245

RoW

+7%

Asia Pacific

+7%

Japan

-4%

North

America

+5%

Western

Europe

+1%

2013

3,247

X%: comparable growth

∞ Puma: momentum regained, marketing efforts strengthened in second half

– Fueled by 6.3% growth in H2, comparable full-year sales up 3.4%. Confirmed rebound in wholesale (+3.3%) and solid performances

in DOS

– Growth in all key regions, notably Americas and Asia Pacific

– Footwear sales back in positive territory in H2

– Sustained growth in sales of accessories and apparel: successful partnership with Arsenal football club

∞ Other brands: promising repositioning

∞ Recurring operating income impacted by Puma relaunch and adverse currency impact

∞ Return to higher CAPEX: modernization of IT systems

% change

% comparable % reported

Puma

Other brands

+3.4%

+4.7%

-0.4%

+4.0%

F i n a n c i a l p e r f o r m a n c e

In €m 2014 2013

Recurring operating income 1,664 1,751

Other non-recurring operating income and expenses

Net financial charges

Corporate income tax

Share in earnings of associates

Net loss from discontinued operations

(112)

(197)

(326)

(1)

(479)

(441)

(210)

(237)

2

(825)

Consolidated net income

Of which: net income, Group share

549

529

40

50

Net income, Group share, from continuing operations

excluding non-recurring items 1,177 1,231

Net income, Group share, per share (in euro)

Net income per share from continuing operations, Group share,

excluding non-recurring items (in euro)

4.20

9.35

0.39

9.77

21

F r e e c a s h f l o w f r o m o p e r a t i o n s

In €m 2014 2013

Cash flow before taxes, dividends and interest

Change in working capital requirement (excluding taxes)

Corporate income tax paid

1,844

(160)

(423)

1,983

(75)

(387)

Net cash flow from operating activities 1,261 1,521

Acquisition of fixed operating assets

Sale of fixed operating assets

(551)

368

(675)

10

Free cash flow from operations 1,078 857

22

C h a n g e i n n e t f i n a n c i a l d e b t

23

Acquisitions

and disposals

Net debt at

December

31, 2014

4,391 1,198

Net debt before

acquisitions

and disposals

3,193

Other

movements

94

Purchases of

Kering shares

9

Dividends paid

498

Net interest paid

and dividend

received

228

Free cash flow

from operations

-1,078

Net debt at

December

31, 2013

3,443

1.7x

2.2x Net debt /

EBITDA

2013-2014 net financial debt bridge, before and after acquisitions and disposals impact (change in €m, and net debt / EBITDA ratio)

1.6x

€5.5bn

€1bn

€3.5bn

€4bn

€3bn

€18bn

€11bn

Assets Liabilities

€23bn

∞ Equity: 48% of balance sheet

∞ Debt to equity ratio of 39%

∞ Average maturity lengthened

∞ Further reduction in cost of financing in 2014

Non current

assets

Current assets

Cash

Equity

Non current

liabilities

Current

liabilities

Gross debt

1,198

184

443

541 536

1,489

2015* 2016** 2017** 2018** 2019** Beyond**

Condensed balance sheet - 2014 Liquidity overview – Net debt (net financial debt, in €m)

24

* Gross debt minus cash & cash equivalents

** Gross debt

2 0 1 4 b a l a n c e s h e e t

H e a l t h y f i n a n c i a l s t r u c t u r e

47.6% 41.8%

37.3% 38.5% 42.9%

52.9% 59.8% 61.6% 64.0%

59.4%

2010** 2011** 2012** 2013** 2014*

% of recurring net income, Group share, from continuing ops. % of available cash flow

* Subject to April 23, 2015 AGM approval. Interim payment of €1.50

paid on January 26, 2015

** Published not restated

3.50 3.50

3.75 3.75

4.00

2010 2011 2012 2013 2014*

+ 7.1%

25

P r o p o s e d d i v i d e n d u p 7 %

+ 6.7%

Dividend per share (in €)

Dividend payout (in %)

François-Henri Pinault Chairman & CEO

26

Strategy and Out look

2014 annual results

27

S t r a t e g y a n d o u t l o o k

High-potential Group in fast-growing sector

Luxury is a sector expected to enjoy long-

term structural growth

∞ Driven by favorable economic and demographic factors, tourism

∞ New consumer trends

∞ New growth levers

1

3

2 Group brands have huge organic growth

potential

∞ An ensemble of brands with complementary maturity cycles and

positionings

∞ Significant growth potential

∞ Enhanced steering structures to better support the growth of our

brands: business expertise and synergies, renewed teams

With a strong entrepreneurial culture, Kering

is integrating to create more value

∞ Short-term responsiveness, long-term investments

∞ Disciplined oversight, brand managers fully accountable

S t r a t e g y a n d O u t l o o k

Gucci, new momentum

Two key directions

Revitalize Accelerate

28

1. Identity and Creativity

Rejuvenate the brand and

revitalize our product offer

Appealing, modern identity

Radical contemporary vision fully

embracing our heritage

2. Communications

Express a consistent brand image

Clear brand narrative, conveyed globally

and meticulously

3. Store network

Adapt and consolidate

Ad hoc expansion and fine-tuning,

adaptation of store concept taking into

account the specific needs of each

location

1. Store excellence Intensify existing programs

Client service culture to drive our

new momentum

2. Organization

Simplify to boost efficiency

Accelerated redefinition of functions

to enable regional directions to focus

on operations

29

S t r a t e g y a n d O u t l o o k

Puma, five clear priorities

1. Consolidate relaunch

∞ Focus on Sport Performance and women’s fitness…

∞ … notably in footwear

2. Accelerate product innovation

∞ Boost pipeline of products with highly innovative content

3. Pursue distribution upgrading

∞ Enhance sales quality to support virtuous gross margin momentum

4. Optimize organization

∞ Update information and management systems; redesign supply

chain

5. Minimize negative impact of currency fluctuation

30

S t r a t e g y a n d o u t l o o k

2015 outlook

∞ Environment

– Macroeconomic environment still unsettled, but new growth drivers

∞ Currency fluctuations

– Weaker Euro supporting sales, but mixed impact on Group results

∞ Beyond cycles, a sector experiencing sharp underlying growth

∞ Integrated, pragmatic, responsive Group

– Action plans focusing on organic growth

– Short-term responsiveness and long-term investments

– Disciplined management and allocation of resources

– No acquisition plans in the short term

∞ Steady, profitable growth trajectory, focus on cash flow generation to gradually reduce debt and support

attractive dividend payout

31

2014 annual results

A p p e n d i c e s

2 0 1 4 r e v e n u e

Change

In €m, continuing operations 2014 2013 €m %

Gucci

Bottega Veneta

Saint Laurent

Other brands

3,497.2

1,130.5

707.3

1,423.6

3,560.8

1,015.8

556.9

1,244.0

(63.6)

114.7

150.4

179.6

-1.8%

+11.3%

+27.0%

+14.4%

Luxury 6,758.6 6,377.5 381.1 +6.0%

Puma

Other brands

2,990.2

254.9

3,001.9

245.1

(11.7)

9.8

-0.4%

+4.0%

Sport & Lifestyle 3,245.1 3,247.0 (1.9) -0.1%

Corporate & Others 33.8 31.2 2.6 +8.3%

Kering 10,037.5 9,655.7 381.8 +4.0%

32

Leather Goods Ready to Wear Footwear Other categories*

56% 12% 14% 18%

87% 5% 6% 2%

47% 23% 19% 11%

22% 34% 6% 38%

37% 43% 20%

76% 5% 19%

Lu

xu

ry

33

2 0 1 4 r e v e n u e

b y p r o d u c t c a t e g o r y

Other brands

Other brands

* Watches, Jewellery and licensing revenue (for Luxury); Licensing

revenue and accessories (for Sport & Lifestyle)

Sport

&

Lif

esty

le

33

2 0 1 4 r e v e n u e : € 6 , 7 5 9 m + 4 . 9 % c o m p a r a b l e ; + 6 . 0 % r e p o r t e d

Western

Europe

32%

North America

19%

Japan

10%

Asia Pacific

31%

RoW

8%

Number of directly operated stores

288

195 224

389

312

206 226

442

Western Europe North America Japan Emerging markets

Year end 2013: 1096 Year end 2014: 1186

34

Revenue y-o-y change

in €m % comparable % reported

Q1 14

Q2 14

Q3 14

Q4 14

1,582

1,611

1,656

1,909

+6.4%

+5.5%

+3.8%

+4.3%

+5.3%

+5.1%

+4.0%

+9.1%

Luxury activities

+14% € 838m

Western

Europe

27%

North America

20%

Japan

10%

Asia Pacific

36%

RoW

7%

Number of directly operated stores

35

Revenue y-o-y change

in €m % comparable % reported

Q1 14

Q2 14

Q3 14

Q4 14

838

838

851

970

+0.3%

(2.4%)

(1.9%)

(0.5%)

(3.2%)

(5.7%)

(1.6%)

+3.0%

2 0 1 4 r e v e n u e : € 3 , 4 9 7 m - 1 . 1 % c o m p a r a b l e ; - 1 . 8 % r e p o r t e d

109 116

66

183

116 117

65

207

Western Europe North America Japan Emerging markets

Year end 2013: 474 Year end 2014: 505

Western

Europe

29%

North America

13%

Japan

14%

Asia Pacific

40%

RoW

4%

Number of directly operated stores

36

Revenue y-o-y change

in €m % comparable % reported

Q1 14

Q2 14

Q3 14

Q4 14

251

275

286

319

+14.6%

+20.2%

+10.8%

+6.8%

+9.5%

+16.1%

+10.4%

+9.6%

46

27

58

90

52

29

58

97

Western Europe North America Japan Emerging markets

Year end 2013: 221 Year end 2014: 236

2 0 1 4 r e v e n u e : € 1 , 1 3 1 m + 1 2 . 6 % c o m p a r a b l e ; + 11 . 3 % r e p o r t e d

Western

Europe

41%

North America

22%

Japan

7%

Asia Pacific

22%

RoW

8%

Number of directly operated stores

37

Revenue y-o-y change

in €m % comparable % reported

Q1 14

Q2 14

Q3 14

Q4 14

158

163

178

209

+27.1%

+29.4%

+27.5%

+25.3%

+24.2%

+26.9%

+27.6%

+28.7%

31

17 21

46

33

22 21

52

Western Europe North America Japan Emerging markets

Year end 2013: 115 Year end 2014: 128

2 0 1 4 r e v e n u e : € 7 0 7 m + 2 7 . 2 % c o m p a r a b l e ; + 2 7 . 0 % r e p o r t e d

Other Luxury brands

Western

Europe

45%

North America

19%

Japan

8%

Asia Pacific

17%

RoW

11%

Number of directly operated stores

38

Revenue y-o-y change

in €m % comparable % reported

Q1 14

Q2 14

Q3 14

Q4 14

335

336

341

412

+8.9%

+6.9%

+3.3%

+5.4%

+19.4%

+20.2%

+3.8%

+15.9%

102

35

79 70

111

38

82 86

Western Europe North America Japan Emerging markets

Year end 2013: 286 Year end 2014: 317

2 0 1 4 r e v e n u e : € 1 , 4 2 4 m + 6 . 0 % c o m p a r a b l e ; + 1 4 . 4 % r e p o r t e d

Western

Europe

30%

North America

26%

Japan

9%

Asia Pacific

14%

RoW

21%

39

Revenue y-o-y change

in €m % comparable % reported

Q1 14

Q2 14

Q3 14

Q4 14

790

709

922

824

(0.2%)

+1.1%

+6.1%

+6.4%

(6.3%)

(4.7%)

+2.9%

+7.9%

Sport & Lifestyle

2 0 1 4 r e v e n u e : € 3 , 2 4 5 m + 3 . 5 % c o m p a r a b l e ; - 0 . 1 % r e p o r t e d

2 0 1 4 r e c u r r i n g o p e r a t i n g i n c o m e

Change

In €m, continuing operations 2014 2013 €m %

Gucci

Bottega Veneta

Saint Laurent

Other brands

1,056.0

357.2

105.1

147.3

1,131.8

330.6

76.6

144.7

(75.8)

26.6

28.5

2.6

-6.7%

+8.0%

+37.2%

+1.8%

Luxury 1,665.6 1,683.7 (18.1) -1.1%

Puma

Other brands

128.0

9.5

191.9

8.5

(63.9)

1.0

-33.3%

+11.8%

Sport & Lifestyle 137.5 200.4 (62.9) -31.4%

Corporate & Others (139.1) (132.9) (6.2) -4.7%

Kering 1,664.0 1,751.2 (87.2) -5.0%

40

Change

In €m, continuing operations 2014 2013 €m %

Gucci

Bottega Veneta

Saint Laurent

Other brands

1,199.2

388.8

130.9

200.3

1,275.8

354.8

93.0

187.1

(76.6)

34.0

37.9

13.2

-6.0%

+9.6%

+40.8%

+7.1%

Luxury 1,919.2 1,910.7 8.5 +0.4%

Puma

Other brands

178.6

12.6

246.4

11.9

(67.8)

0.7

-27.5%

+5.9%

Sport & Lifestyle 191.2 258.3 (67.1) -26.0%

Corporate & Others (119.7) (125.7) 6.0 -4.8%

Kering 1,990.7 2,043.3 (52.6) -2.6%

41

2 0 1 4 E B I T D A

2 0 1 4 n e t f i n a n c i a l c o s t s

a n d i n c o m e t a x

In €m 2014 2013

Cost of net debt

Other financial income and expenses

(151)

(46)

(174)

(36)

Financial costs (net) (197) (210)

In €m 2014 2013

Tax on recurring income

Tax on non-recurring items

(268)

(58)

(268)

31

Total tax charge (326) (237)

Effective tax rate 24.0% 21.5%

Recurring tax rate 18.3% 17.4%

42

2 0 1 4 c o n d e n s e d c o n s o l i d a t e d b a l a n c e s h e e t

In €m 2014 2013

Goodwill, brands & other intangible assets - Net

Other net non-current assets

Net current assets

Provisions

14,788

310

924

(394)

14,473

(120)

836

(366)

CAPITAL EMPLOYED 15,628 14,823

Net assets held for sale 25 (184)

SHAREHOLDERS’ EQUITY 11,262 11,196

NET DEBT 4,391 3,443

43