Economic Value AddedFIN 461: Financial Cases & Modeling

George W. GallingerAssociate Professor of FinanceW. P. Carey School of Business

Arizona State University

W. P. Carey School of Business Slide 2

How Value is Created

Management makes decisions, hopefully, with benefits exceeding costs Benefits may be near or distant future Costs should include direct investment

costs + cost of capital True source of value-enhancing projects

Firm’s comparative or competitive advantage.

W. P. Carey School of Business Slide 3

Comparative Advantage

Advantage one firm has over another in terms of Cost of producing or Distributing goods/services

Example: Wal-Mart invested in regional warehouses and

distribution system Reduces the need for retail inventory Replenish store inventory quickly.

W. P. Carey School of Business Slide 4

Competitive Advantage

Advantage one firm has over another because of structure of the markets in which they operate

Barriers to entry Patents Capital requirements Regulation

Influence over suppliers Influence over buyers

Must besustainable to be a truecompetitiveadvantage

Traditional Measures

W. P. Carey School of Business Slide 6

Fuzzy Finance

W. P. Carey School of Business Slide 7

Return on Investment

Compare benefits (numerator) with resources (denominator) affecting that benefit Basic earning power ratio

EBIT / Total assets Return on assets

Net income / Total assets Return on equity

Net income / Book value of equity

Measuredrelativeto what?

W. P. Carey School of Business Slide 8

Pro’s & Con’s

Benefits of these ratios Ease of calculation & interpretation Decompose to reveal sources of changes

Downside of these ratios Sensitive to choice of accounting method Accumulation of monetary values from

different periods Backward looking Fail to consider risk.

W. P. Carey School of Business Slide 9

EPS: Opiate of theExecutive Suite

EPS is such an unreliable measure of value that managers often make “dumb” decisions to increase it

Prompts managers to misallocate capital Treats retained earnings as a free source

of capital Promotes retaining capital and using it

wastefully.

W. P. Carey School of Business Slide 10

EPS…

Accounting rules discourage EPS-manic managers from spending capital on value enhancing investments in intangibles like brands, research and training

Why? GAAP requires outlays to be written

off immediately against earnings.

W. P. Carey School of Business Slide 11

EPS…

EPS focus may cause management to refrain from issuing equity at times when the company really needs it

Fabricate EPS gains by using more debt than prudent Both on and off the balance sheet

Accept weak projects that happen to be financed with debt.

W. P. Carey School of Business Slide 12

EPS…

Earnings manipulation often used Establish reserves Invest pension funds in equities Extreme cases, make up numbers as

you go Worldcom and HealthSouth.

W. P. Carey School of Business Slide 13

EPS…

Today’s market perception:“Management that aims to boost earnings at the expense of quality will be more certainly penalized then ever before with a lower stock price and a sullied reputation.”

W. P. Carey School of Business Slide 14

Performance vs. Valuation

Performance measurement Relies on actual results

Historical GAAP vs. GAP

Valuation Relies on forecasts Stock price relies on investors’

expectations, not historical performance.

Cash Flows

W. P. Carey School of Business Slide 16

Statement of Cash Flows

SCF combines balance sheet and income info Eliminates the “sins of accrual

accounting” SCF consists of:

Operating cash flows Investing cash flows Financing cash flows.

Free cash flow

W. P. Carey School of Business Slide 17

Cash Flow Not the Answer Cash flow has problems as a valid

performance measure So long as investments in projects earn

a return higher than shareholders could earn by investing on their own, then the more investment a company makes and the more negative its cash flow becomes, the higher its share price will be.

Think Wal-Mart.

W. P. Carey School of Business Slide 18

Better Than Some Alternatives

Accounting profits versus cash operating profits

Cash flow frequently defined as:

Net income + depreciation or as EBITDA

Poor definition

Quality of earnings ...

-500

0

500

1000

1500

2000

2500

3000

'97 '98 '99 '00 '01 '02

NI + depr.

NI

CFFO

W. P. Carey School of Business Slide 19

Free Cash Flows Definition:

After-tax operating earnings + non-cash charges - investments in operating working capital, PP&E and other assets

It doesn’t incorporate financing related cash flows

Represents cash flow available to service debt and equity.

When used in capital budgeting proposals Based on expectations.

W. P. Carey School of Business Slide 20

FCF & Capital Budgeting

FCF is the method of choice of most firms for evaluating capital budgets

Identify incremental Investment in PP&E + working capital Revenues Costs (excluding financing) Depreciation tax shields.

W. P. Carey School of Business Slide 21

Common Techniques

Evaluation techniques: Payback Accounting rate of return DCF analysis

Consists of NPV and IRR DCF analysis is not a problem in theory

Only in practice.

W. P. Carey School of Business Slide 22

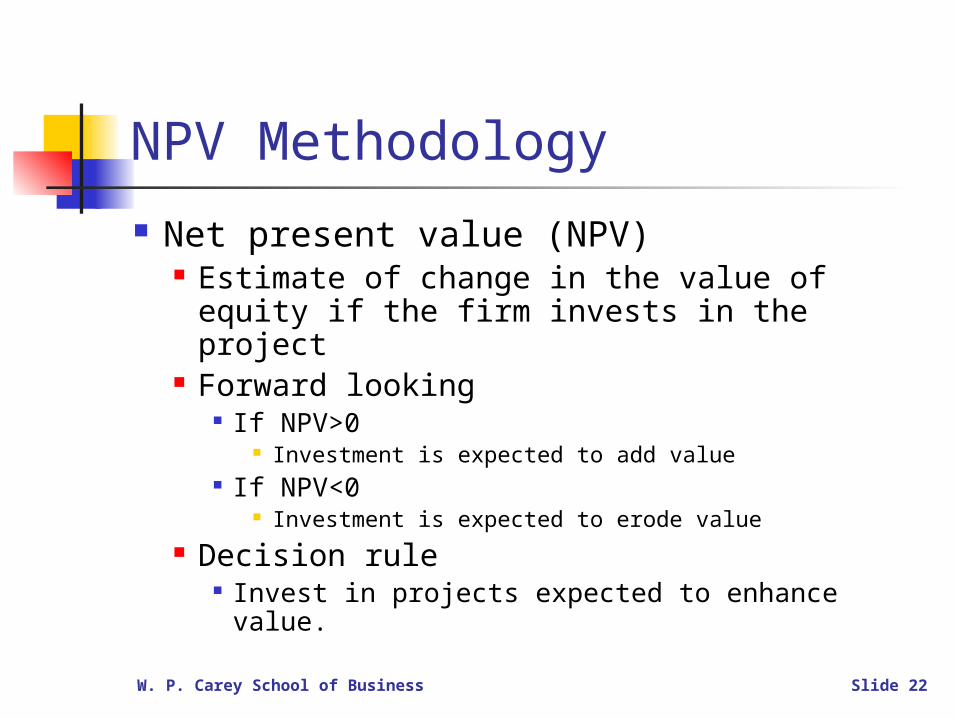

NPV Methodology

Net present value (NPV) Estimate of change in the value of equity

if the firm invests in the project Forward looking

If NPV>0 Investment is expected to add value

If NPV<0 Investment is expected to erode value

Decision rule Invest in projects expected to enhance value.

W. P. Carey School of Business Slide 23

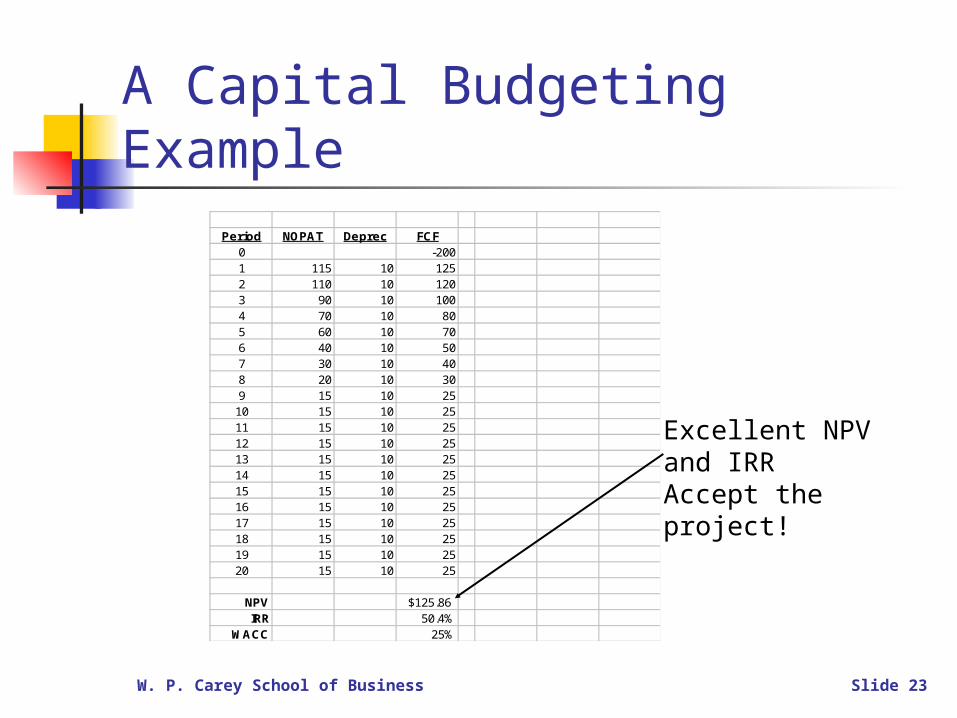

A Capital Budgeting ExamplePeriod NOPAT Deprec FCF

0 -2001 115 10 1252 110 10 1203 90 10 1004 70 10 805 60 10 706 40 10 507 30 10 408 20 10 309 15 10 2510 15 10 2511 15 10 2512 15 10 2513 15 10 2514 15 10 2515 15 10 2516 15 10 2517 15 10 2518 15 10 2519 15 10 2520 15 10 25

NPV $125.86IRR 50.4%

WACC 25%

Excellent NPV and IRRAccept the project!

W. P. Carey School of Business Slide 24

NPV(Using FCF) Profile

Free Cash Flow Profile

-250

-200

-150

-100

-50

0

50

100

150

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

NPV of FCF = $125.86

Significant info revealed?

W. P. Carey School of Business Slide 25

Internal Rate of Return

Practice is to compare IRR with weighted average cost of capital

Problem: IRR fails to measure scale or growth It sees no difference between earning

a 20% return on a $1 million investment or a $1 billion investment

These two projects are very different with distinctly different NPVs.

W. P. Carey School of Business Slide 26

IRR Profiles(New Example)

($700)

($500)

($300)

($100)

$100

$300

$500

$700

$900

$1,100

0% 16% 50%

IRRNE=19.63%

IRRATL =36.53%

•

W. P. Carey School of Business Slide 27

Conflicts: NPV & IRRWhich to Choose?

Discount rate

Marketing CampaignIRR = 16.35%

Product developmentIRR = 13.24%

10.7%10%

NPV

Select project with higher NPV (product development project)

W. P. Carey School of Business Slide 28

Value Enhanced?

Once a project is applied, the investment becomes buried in the balance sheet How is its contribution measured?

No idea whether project generates value Accounting measure relied upon

EBITDA and EPS generally increase Means Bonuses probably will be paid

Motivation: Get your hands on as much capital as

possible.

Focused Finance & EVA

W. P. Carey School of Business Slide 30

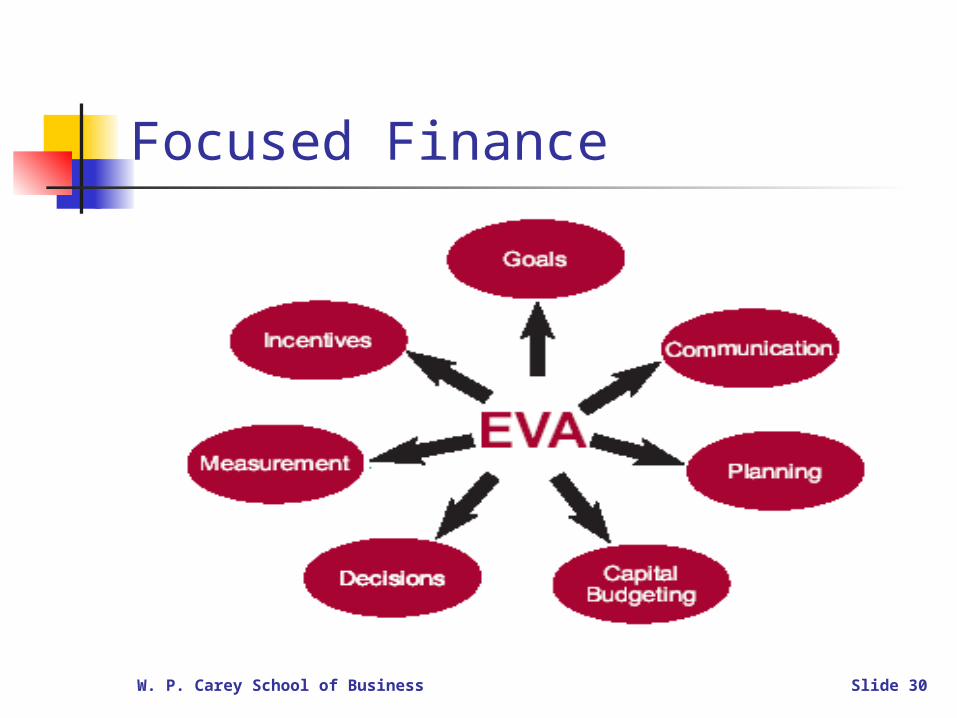

Focused Finance

W. P. Carey School of Business Slide 31

EVA & Wealth Creation

Warren Buffet:We feel noble intentions should be checked periodically against results. We test the wisdom of retaining earnings by assessing whether retention, over time, delivers shareholders at least $1 of market value for each $1 retained.

Translation:Ultimate litmus test of any company’s success lies in increasing its market value by more than it increases its capital.

W. P. Carey School of Business Slide 32

View of the Firm

Value of firm = Value of debt + value of stock

Market value of a company reflects: Earning power of invested assets

Present value of current operations Present value of expected improvement in

operating performance.

Market Valued Balance Sheet

Assets DebtEquity

W. P. Carey School of Business Slide 33

What is Required to Focus? Tie performance methods to capital

budgeting techniques: Economic value added (EVA) Market value added (MVA)

Want to gauge management’s performance Focus on:

Decisions made in the past to help project the future.

Links to NPV

W. P. Carey School of Business Slide 34

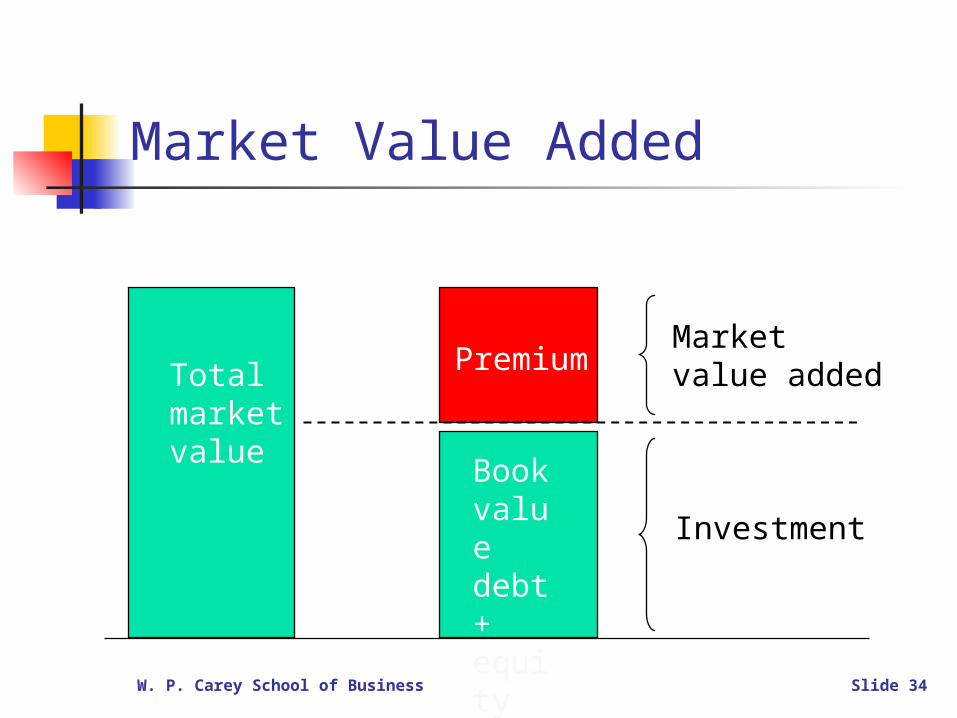

Market Value Added

Total market value

Book valuedebt +equity

Marketvalue added

Investment

Premium

W. P. Carey School of Business Slide 35

Also, Market Value Added

Total market value

Bookvaluedebt +equity

Expectedimprovement in EVA

MVA

Current levelof EVA

MVA = Present value of all future EVA

W. P. Carey School of Business Slide 36

What is EVA?

EVA = Economic profit Not the same as accounting profit

Difference between revenues and costs Costs include not only expenses but also cost of capital

Economic profit adjusts for distortions caused by accounting methods

Doesn’t have to follow GAAP R&D, advertising, restructuring costs, ...

Cost of capital accounted for explicitly Rate of return required by suppliers of a firm’s debt

and equity capital Represents minimum acceptable return.

W. P. Carey School of Business Slide 37

Components of EVA

NOPLAT Net operating profit after tax

Operating capital Net operating working capital, net PP&E,

goodwill, and other operating assets Cost of capital

Weighted average cost of capital % Capital charge

Cost of capital % * operating capital Economic value added

NOPLAT less the capital charge.

W. P. Carey School of Business Slide 38

What is NOPAT?

Net sales 150,000Cost of sales 135,000Depreciation 2,000SG&A 7,000Net Operating profit 6,000Taxes @ 40% 2,400NOPAT 3,600

Excludes financing charges

W. P. Carey School of Business Slide 39

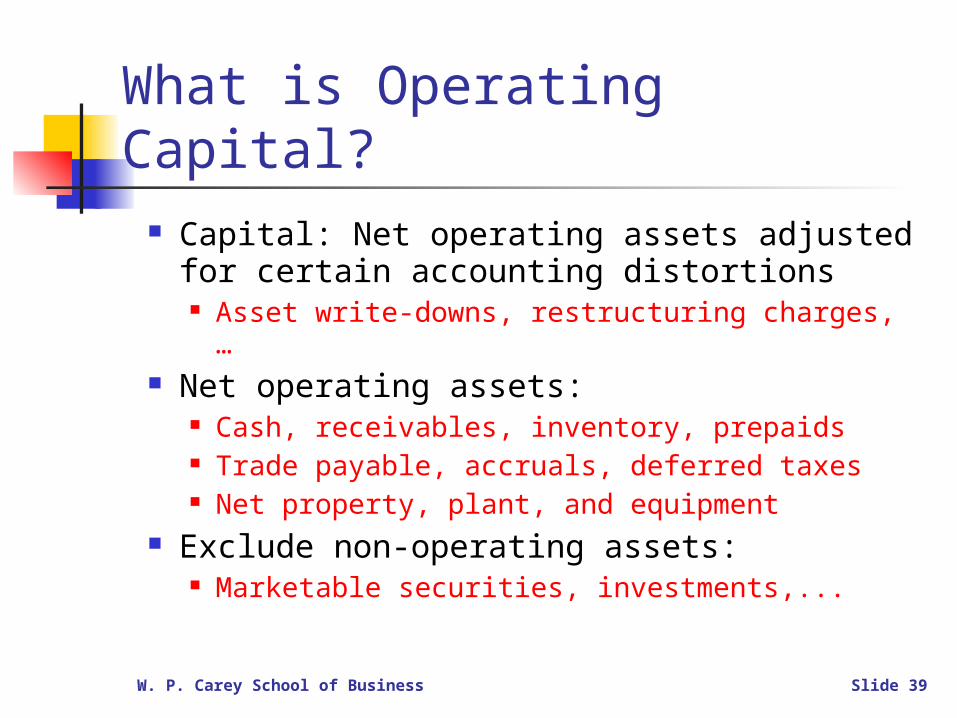

What is Operating Capital? Capital: Net operating assets adjusted

for certain accounting distortions Asset write-downs, restructuring charges, …

Net operating assets: Cash, receivables, inventory, prepaids Trade payable, accruals, deferred taxes Net property, plant, and equipment

Exclude non-operating assets: Marketable securities, investments,...

W. P. Carey School of Business Slide 40

What is Cost of Capital? Weighted average cost of capital consists of:

Cost of debt after taxes= Market interest rate x (1 – tax rate)

Cost of equity= Risk-free rate + beta x (market risk

premium)WACC

= Cost of debt after taxes x % debt + cost of equity x %

equitywhere % debt + % equity = 100%.

W. P. Carey School of Business Slide 41

What is the Capital Charge?

Represents a rental charge for the use of the operating capital

Minimum rate of return the operating capital should earn

Calculated as the firm’s weighted average cost of capital % x invested capital.

W. P. Carey School of Business Slide 42

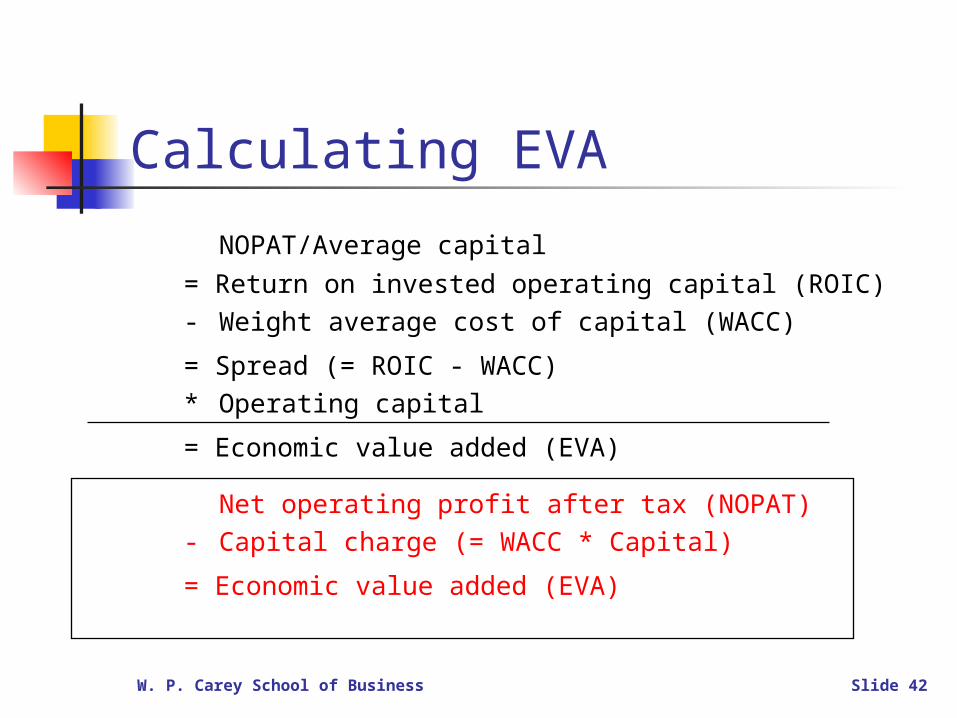

Calculating EVA

NOPAT/Average capital

= Return on invested operating capital (ROIC)- Weight average cost of capital (WACC)

= Spread (= ROIC - WACC)* Operating capital

= Economic value added (EVA)

Net operating profit after tax (NOPAT)- Capital charge (= WACC * Capital)

= Economic value added (EVA)

W. P. Carey School of Business Slide 43

What’s Affecting EVA?

Sales- Operating expenses- Taxes

= NOPAT- Capital charge

= EVA

COGS, SG&A + other

Net working capitalPP&EWACC

Evaluate the many assumptions!

Potential gov’t actions

Market potential

W. P. Carey School of Business Slide 44

Forward Looking Relationship for EVA & MVA

EVA EVA EVA EVAYear 1 Year 2 Year 3 .... Year n

MarketValueMarketvalue

MVA

Bookvaluecapital

=EVA + EVA + EVA + ... + EVA1 + r (1 + r)2 (1 + r)3 (1 + r)n

Market value is based on establishing theeconomic investment made in the company(capital), making a best guess about what economic profits (EVA) will happen in the future, and discounting those EVAs to the present to get market value added.

MVA

W. P. Carey School of Business Slide 45

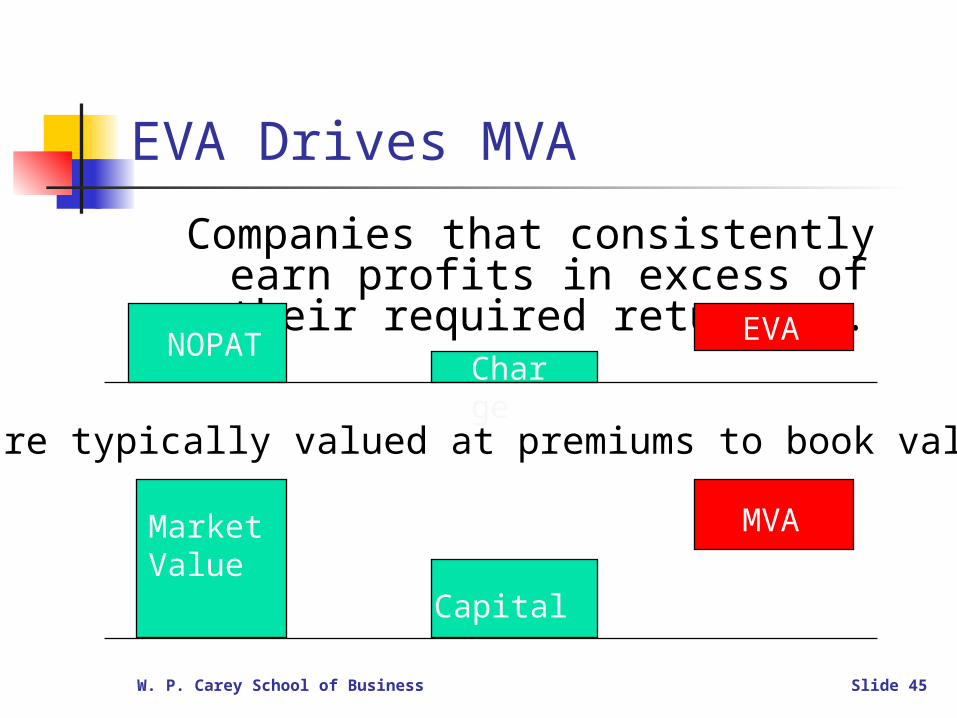

EVA Drives MVA

Companies that consistently earn profits in excess of their required

return ...NOPAT EVA

MarketValue

Capital

MVA

Charge

… are typically valued at premiums to book value.

W. P. Carey School of Business Slide 46

Fundamental Strategies

Capital * capital ofCost Capital

NOPATEVA

Operate: Improve thereturn on existingoperating capital Build: Invest as long as returns

exceed the cost of capital

Harvest: Re-deploy capital when returns fail to achieve the cost of capital.

Decrease: WACC

W. P. Carey School of Business Slide 47

An Example of Drivers

W. P. Carey School of Business Slide 48

Focus on EVA Improvement

A positive change in EVA is better than a positive yet unchanging base level of EVA Why?

Positive changes in EVA are consistent with “shareholder value added” -- whether from a positive or negative base

Positive changes in EVA are consistent with the managerial notion of continuous improvement in performance.

W. P. Carey School of Business Slide 49

Why Use EVA & Not NPV?

Present value of EVA = Present value of NPV

Provides insight into each period Is a direct link to performance More useful for future project

audits.

W. P. Carey School of Business Slide 50

An Example Revisited(See Slides 27 & 28)

Asset'sPeriod NOPAT Deprec FCF CapChg Balance EVA

0 -200 2001 115 10 125 50.0 190 65.02 110 10 120 47.5 180 62.53 90 10 100 45.0 170 45.04 70 10 80 42.5 160 27.55 60 10 70 40.0 150 20.06 40 10 50 37.5 140 2.57 30 10 40 35.0 130 -5.08 20 10 30 32.5 120 -12.59 15 10 25 30.0 110 -15.010 15 10 25 27.5 100 -12.511 15 10 25 25.0 90 -10.012 15 10 25 22.5 80 -7.513 15 10 25 20.0 70 -5.014 15 10 25 17.5 60 -2.515 15 10 25 15.0 50 0.016 15 10 25 12.5 40 2.517 15 10 25 10.0 30 5.018 15 10 25 7.5 20 7.519 15 10 25 5.0 10 10.020 15 10 25 2.5 0 12.5

NPV $125.86 $125.86IRR 50.4%

WACC 25%

EVA =NOPAT – WACC * Beginning Balance= 110 – 25% * 190= 110 = 47.5= 62.5

W. P. Carey School of Business Slide 51

NPV (Using FCF) & EVA Profiles

FCF vs. EVA

-250

-200

-150

-100

-50

0

50

100

150

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

FCF

EVA

NPV of FCF = NPV of EVA = $125.86

Significant info revealed?

W. P. Carey School of Business Slide 52

Real Life EVA The Manitowoc Co. in Manitowoc, Wis., a diversified food service, crane manufacturing

and marine operations company, outsourced a reverse-auction procurement system to a vendor instead of acquiring a software package itself. A comparison using Economic Value Added of buying vs. renting would look like this for the first year (hypothetical numbers):

In-house application $180,000 in net benefits - ($1 million capital investment x 12% cost of capital) = $60,000 EVA

Outsourced application $180,000 in net benefits - ($0 capital investment x 12% cost of capital) - $80,000 in rental fees = $100,000 EVA

Outsourced application requires no capital investment thus, no capital charge. Suppose the operating costs to run the system in-house were $50,000 per year.

Most companies only look at the income statement side of the ledger; they wouldn't outsource this application because it would be exchanging $50,000 of in-house expenses for the $80,000 rental fee, another kind of expense on the income statement. Yet on an EVA basis, the company would outsource the system, because doing so would produce more residual income ($100,000 vs. $60,000) by virtue of the $0 capital charge.

"When you are exposed to the EVA philosophy, you recognize how to better manage your capital," says Jim Pecquex, Manitowoc's CIO.

Source: Computerworld, February 17, 2003.

W. P. Carey School of Business Slide 53

Real Life EVA … Consider a recent EVA analysis that Robert Egan, vice president of IT at Boise

Cascade Corp., and his colleagues conducted for a storage investment. The decision was whether to keep storage assets or replace them with new technology that has lower maintenance charges.

The example is illustrative. Egan declined to provide real cost figures. The new storage technology costs $1 million, with maintenance costs of $100,000

per year. The maintenance expense on the old storage technology is $350,000. For simplicity, we'll assume that the new storage equipment offers no benefits other than

the lower maintenance costs. Boise's cost of capital is about 16%. Thus, the capital charge for investing in the

new storage is 16% x $1 million = $160,000, which EVA says must be added to the $100,000 maintenance costs to get the true cost.

The result: The total cost of the new storage is $260,000, vs. $350,000 for the old storage. "In this case, have you lowered the operating cost enough to make up for spending the

capital?" asks Egan. Yes -- $90,000 worth. Boise is constantly reminded of the obvious point that technology isn't free. The

company is also aware of the less obvious fact: neither is the capital to finance it. Source: Computerworld, February 17, 2003.

W. P. Carey School of Business Slide 54

Real Life: Walgreen’s Performance

W. P. Carey School of Business Slide 55

Real Life: EVA & MVA

3-year changes in MVA explained byregression analysis

W. P. Carey School of Business Slide 56

Measure Earnings with EVA

Simple to explain and understand EPS (and NI) ignore cost of equity capital

EVA doesn’t Retained earnings no longer considered free

Benefits: Reduce cost of capital Improve operational efficiency Better management of assets Profitable growth.

W. P. Carey School of Business Slide 57

Custo m er Satis faction N ew P ro ducts

Vo lume M arketing

P roduct P ricing G row th

S a les

O verhead Co mpensation

Acco unt M anagem ent T ra ining & D evelo pm ent

M anufacturing Co sts

Operating E xpens es

Acqu isitions & D ivestitures W o rking Cap ita l M anagem ent

A lliances Acco unts R eceivab le

R & D D ecisio ns I nventory M anagem ent

C apita l C harge

Improvement in EVA

Manufacturing EVA DriversReduce inventoryReduce cycle time

Improve yieldsReduce scrap/waste

Maximize labor efficienciesImprove vendor efficiencies

Process improvements

Staff EVA DriversWork group/process simplification

Consistency “monitors” – auditCentralizing resources/synergies

Best practices benchmarkingInsourcing/outsourcing decisions

Simplify EVA measurements/reportingEnsure compliance with legislation

Manufacturing EVA DriversReduce inventoryReduce cycle time

Improve yieldsReduce scrap/waste

Maximize labor efficienciesImprove vendor efficiencies

Process improvements

Staff EVA DriversWork group/process simplification

Consistency “monitors” – auditCentralizing resources/synergies

Best practices benchmarkingInsourcing/outsourcing decisions

Simplify EVA measurements/reportingEnsure compliance with legislation

Research & Development EVA DriversImprove “to-market” process

Reduce R&D expenses as % of new product salesStrategic partners for R&D

Stronger links to product marketingNew products via:

- Research- Formulation

- Development-Acquisition

Marketing EVA DriversIncrease market share / revenue

New marketsMore focused channel programs

Voice of customer / consumerLeverage advertising / promotion

Build brand awareness

Research & Development EVA DriversImprove “to-market” process

Reduce R&D expenses as % of new product salesStrategic partners for R&D

Stronger links to product marketingNew products via:

- Research- Formulation

- Development-Acquisition

Marketing EVA DriversIncrease market share / revenue

New marketsMore focused channel programs

Voice of customer / consumerLeverage advertising / promotion

Build brand awareness

W. P. Carey School of Business Slide 58

The End