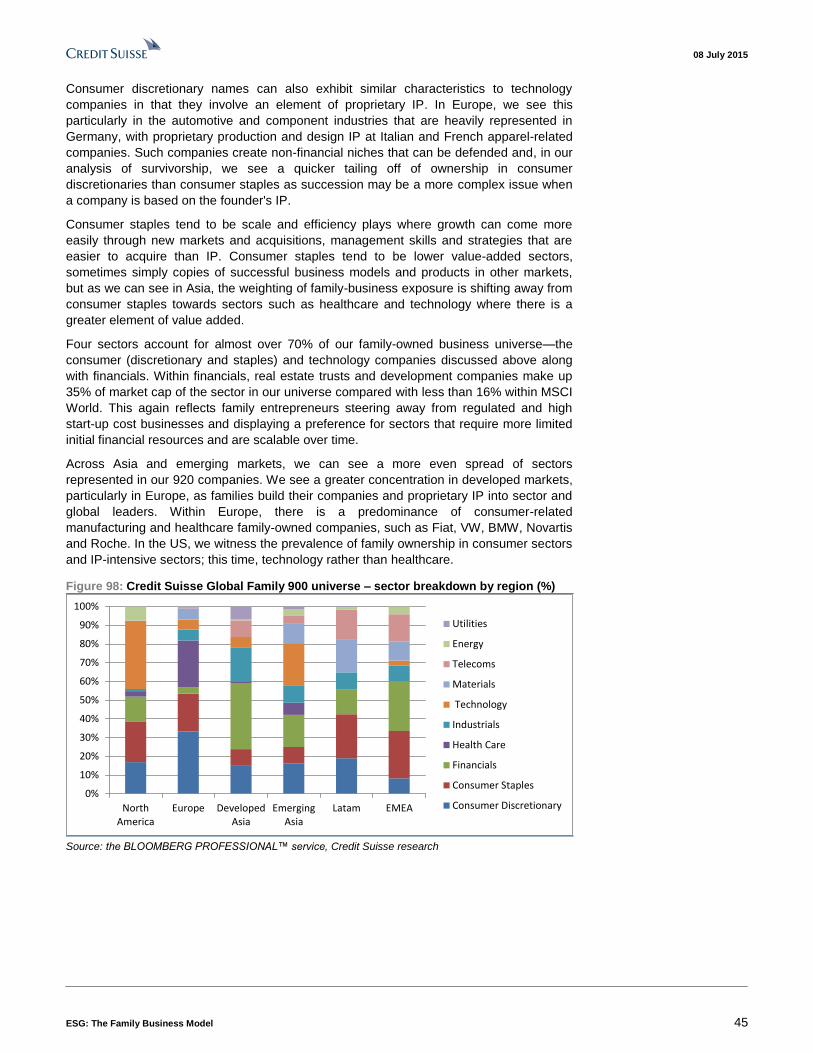

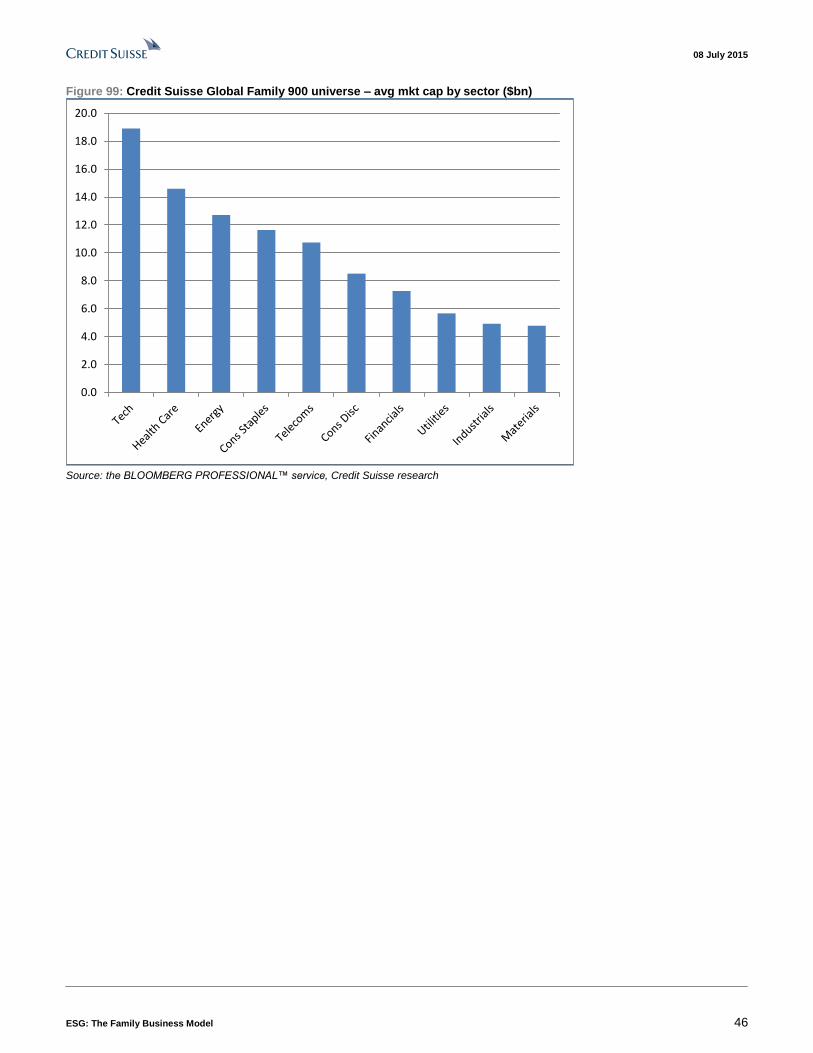

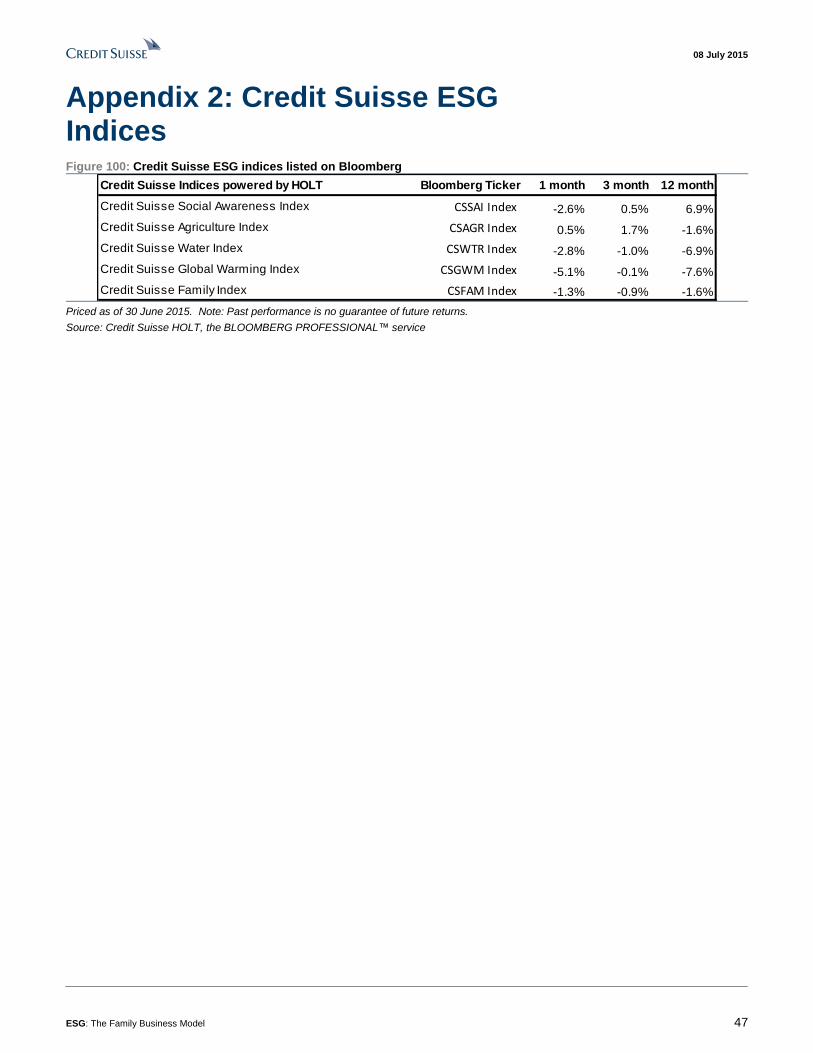

Download - ESG: The Family Business Model

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

08 July 2015

Global

Equity Research

ESG: The Family Business Model Environmental, Social and Governance (ESG) Research

The Credit Suisse Global Family 900 universe

High-profile family-owned corporate collapses and management control

concerns have led minority investors to question whether the returns warrant

the risk. For this report, we have constructed the Credit Suisse Global Family

universe of more than 900 companies with a market cap over $1bn to analyse

the family business model and establish whether the risks of concentrated

ownership and limited control are justified by superior returns.

Key findings:

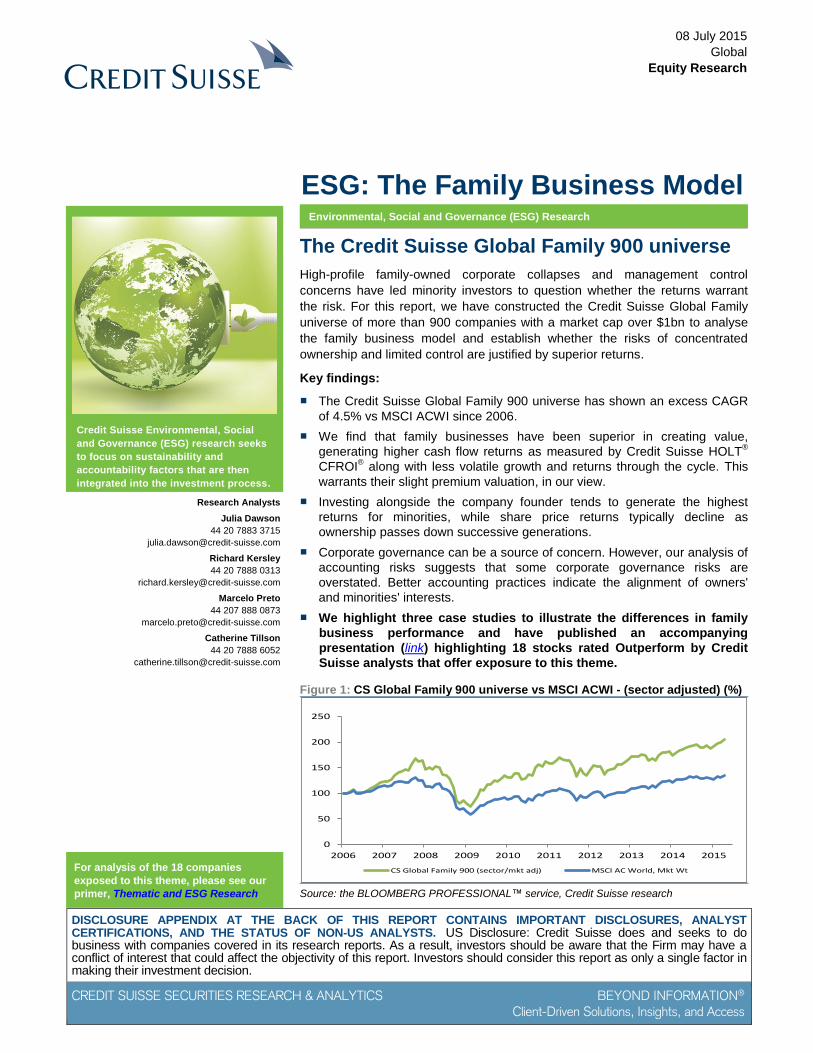

■ The Credit Suisse Global Family 900 universe has shown an excess CAGR

of 4.5% vs MSCI ACWI since 2006.

■ We find that family businesses have been superior in creating value,

generating higher cash flow returns as measured by Credit Suisse HOLT®

CFROI® along with less volatile growth and returns through the cycle. This

warrants their slight premium valuation, in our view.

■ Investing alongside the company founder tends to generate the highest

returns for minorities, while share price returns typically decline as

ownership passes down successive generations.

■ Corporate governance can be a source of concern. However, our analysis of

accounting risks suggests that some corporate governance risks are

overstated. Better accounting practices indicate the alignment of owners'

and minorities' interests.

■ We highlight three case studies to illustrate the differences in family

business performance and have published an accompanying

presentation (link) highlighting 18 stocks rated Outperform by Credit

Suisse analysts that offer exposure to this theme.

Figure 1: CS Global Family 900 universe vs MSCI ACWI - (sector adjusted) (%)

0

50

100

150

200

250

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

CS Global Family 900 (sector/mkt adj) MSCI AC World, Mkt Wt

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse research

Credit Suisse Environmental, Social

and Governance (ESG) research seeks

to focus on sustainability and

accountability factors that are then

integrated into the investment process.

Research Analysts

Julia Dawson

44 20 7883 3715

Richard Kersley

44 20 7888 0313

Marcelo Preto

44 207 888 0873

Catherine Tillson

44 20 7888 6052

For analysis of the 18 companies

exposed to this theme, please see our

primer, Thematic and ESG Research

08 July 2015

ESG: The Family Business Model 2

Table of contents Key highlights 4 Introduction 5 Are family businesses a good investment? 6 Top picks 9 The CS Global Family 900 universe 11 The business case for family-owned companies 12

Superior and more stable growth 12 Return on equity fails to capture value creation 12 Higher cash flow returns – CFROI 14 Economic Profit – the real value creation 15

US case study: Wal-Mart vs Costco and Whole Foods 17 European case study: Alfa Laval vs Hochtief 18 Asian case study: Sino Biopharmaceutical vs CR Sanjiu Pharma 19

Leverage – lower in the US and Europe, as expected 20 R&D intensity 21 Are family-owned companies better at M&A? 22 So what are the negatives to family-owned businesses? 23 The risk of succession and survivorship 24 Accounting quality is in fact superior 26 Diversity 26

The investment case for family-owned companies 28 When should you invest? 31 Dividends 32 Are there 'supergroups' within the family-owned universe? 34

ESG: Do families make good managers? 35 So what to buy? 37 Appendix 1: The Credit Suisse Global Family 900 universe 41 Appendix 2: Credit Suisse ESG Indices 47 Selected reading 48

The authors of this report wish to acknowledge the contribution made by Mahadevan

Subramanian and Akanksha Kharbanda, employees of CRISIL Global Research and

Analytics, a business division of CRISIL Limited, a third-party provider of research services

to Credit Suisse.

08 July 2015

ESG: The Family Business Model 3

Key charts Figure 2: Share price returns by generation Figure 3: Credit Suisse Global Family 900 universe

CFROI® vs MSCI ACWI

60

85

110

135

160

185

210

235

Jan

-06

Jun

-06

No

v-0

6

Ap

r-0

7

Se

p-0

7

Fe

b-0

8

Jul-

08

De

c-0

8

Ma

y-0

9

Oct-

09

Ma

r-1

0

Au

g-1

0

Jan

-11

Jun

-11

No

v-1

1

Ap

r-1

2

Se

p-1

2

Fe

b-1

3

Jul-

13

De

c-1

3

Ma

y-1

4

Oct-

14

Ma

r-1

5

Performance By Generation1 2 3 4 5

4%

5%

6%

7%

8%

9%

10%

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

CFR

OI

CS Global Family 900 universe (ex Fin & Reg Utils) Global Universe (ex Fin & Reg Utils)

Source: Credit Suisse HOLT Source: Credit Suisse HOLT

Figure 4: Economic Profit as % of EV Figure 5: Annual sales growth (%)

(1.0%)

(0.5%)

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Eco

nom

ic P

rofit

as

% o

f E

V

CS Global Family 900universe

CS HOLT Universe

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

CS Global Family 900 universe (ex-financials) Benchmark (ex-financials)

Source: Credit Suisse research, Credit Suisse HOLT Source: Credit Suisse HOLT

Figure 6: CS Global Family 900 universe sector

breakdown

Figure 7: Family business accounting quality

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

MSCI World CS Global Family 900universe

Utilities

Telecoms

Materials

Industrials

Information Technology

Health Care

Financials

Energy

Consumer staples

Consumer discretionary

0%

5%

10%

15%

20%

25%

Good Above Average Average Below Average Poor

CS Family businesses CS HOLT universe

Source: The BLOOMBERG PROFESSIONAL™ service, Credit

Suisse research

Source: Credit Suisse HOLT

08 July 2015

ESG: The Family Business Model 4

Key highlights Here are the key findings from our analysis, which covers 920 companies with a market

cap over $1bn and family ownership of at least 20%:

■ The Credit Suisse Global Family 900 universe has shown an excess return of 4.5%

CAGR vs the MSCI All Countries World Index (ACWI) since 2006.

■ Investing alongside the founder tends to generate the best share-price returns, but we

see the outperformance decreasing over subsequent generations.

■ Family-owned companies are a lower Return on Equity (ROE) business model in the

more developed markets of US and Europe. They demonstrate higher ROEs in Asia

and EMEA. Lower ROEs tend to be indicative of more conservative strategies as well

as broader priorities for family ownership beyond simply financial returns.

■ However, over the longer term, family companies in the CS Global Family 900 have

generated 2x the Economic Profit – earnings in excess of the opportunity cost of

utilising assets or capital – compared to benchmarks. We illustrate this with case

studies of Wal-Mart, Alfa Laval and Sino Biopharmaceuticals.

■ Family-owned companies trade on slightly higher EV/EBITDA and PB multiples

compared to benchmarks. Share-price appreciation is closely correlated to economic

profit generation.

■ Leverage is lower at US and European family businesses in line with previous

academic research. We are able to show the faster de-leveraging post-crisis

compared to benchmarks. Asian family business leverage is higher, on the other hand.

■ The business cycle is smoother and more stable. We show that sales growth is less

volatile through the cycle with lower peaks and less pronounced troughs.

■ Family companies tend to invest less in R&D. In the US, R&D intensity is just 25% of

benchmark levels; in Europe it is 20% below benchmark. Whilst this is indicative of the

more conservative style of management, we also believe that it reflects more efficient

R&D given the relatively limited difference in returns.

■ Family business growth is typically organic. Since 1990, M&A has been just 2.1% of

sales vs 5.8% at non-family businesses. We also find that family businesses generally

make better and cheaper acquisitions as they drive better growth and returns in the

three-year period post-acquisition.

■ Corporate governance risks appear overstated. Whilst there have been high-profile

corporate collapses at family-owned businesses in recent decades, we evaluate

empirical measures of accounting performance as a corporate governance proxy and

find there is a closer alignment between owner and minority interests than is generally

perceived. Based on our HOLT analysis, accounting quality at family-owned

companies is superior, reflecting the owners' focus on preserving wealth over the long

term.

■ We find 'survivorship' and transition to be easier in sectors that are more reliant on

tangible assets. We see a quicker dilution of ownership in companies founded on

intellectual property. This may reflect that successor generations do not share the

founder's vision or interests.

■ We discuss potential risks and weaknesses that include related-party risks, closed

pools of managers, employment of under-qualified family members and different

voting rights.

08 July 2015

ESG: The Family Business Model 5

Introduction There has been considerable research into family-owned businesses to establish whether

or not there is a positive correlation between close corporate ownership and company

performance. To date, there are no definitive findings, although most reports tend to find

positive benefits. However, studies are typically limited to single markets and relate to

different time periods so that an overall, broad conclusion is hard to establish.

With the Credit Suisse Family 900 universe introduced in this report, we look to further the

findings from a number of previous Credit Suisse reports into family businesses,

specifically the Credit Suisse White Paper 01 "Family Businesses in Europe: Growth

Trends and Challenges" (February 2007), The Life-Cycle of UK Family Businesses (July

2008), Credit Suisse Research Institute's Asian Family Businesses Report (2011) and

Family Businesses: Sustaining Performance (2012) and focus on whether there is a

business case for family-owned companies on a global basis and indeed an investment

case for external shareholders.

In the Credit Suisse White Paper 01 "Family Businesses in Europe: Growth Trends and

Challenges" (February 2007), we highlighted six strengths that characterise family

businesses:

■ Long-term commitment of owners

■ Visible and identifiable ownership, in contrast to ownership by numerous institutional

investors

■ Track record of standing by their companies during hard times

■ Trademark names that continue to open doors in the business community

■ Consistency in decision-making and business practice, thereby lowering the business

risks for external providers of capital

■ Better alignment of owner and management interests

To this, we would now add a number of characteristics that help to elucidate why family

businesses stand apart and why the return profile is different to that of the broader

corporate universe:

■ Desire to maintain control leads to more cautious and also more efficient management

and strategies

■ Focus on value-added products and brand development, the corollary of which is the

negatives for family owners from public failure

■ Focus on core activities means they are less acquisitive and growth is organic

■ Investment intensity, be it R&D or broader capex, is lower but the more limited

compression to ROEs suggests that investment and R&D is more efficient

■ Lower volatility in family-owned company returns vs more broadly held companies

■ Value creation through superior cash flow return spreads and asset growth

Entrepreneurship is borne of opportunity and necessity. As the macro-economic backdrop

has moved towards increased deregulation and decreased involvement of the State, we

have seen that family-owned businesses are not just key drivers of economic growth but

are today key employers. It is therefore imperative to understand how and why these

companies perform and how they will impact macroeconomic policies and stock market

performance. With the lessening of the role of the State in the economy across the globe,

entrepreneurs will likely be the innovators and drivers of future growth and development.

08 July 2015

ESG: The Family Business Model 6

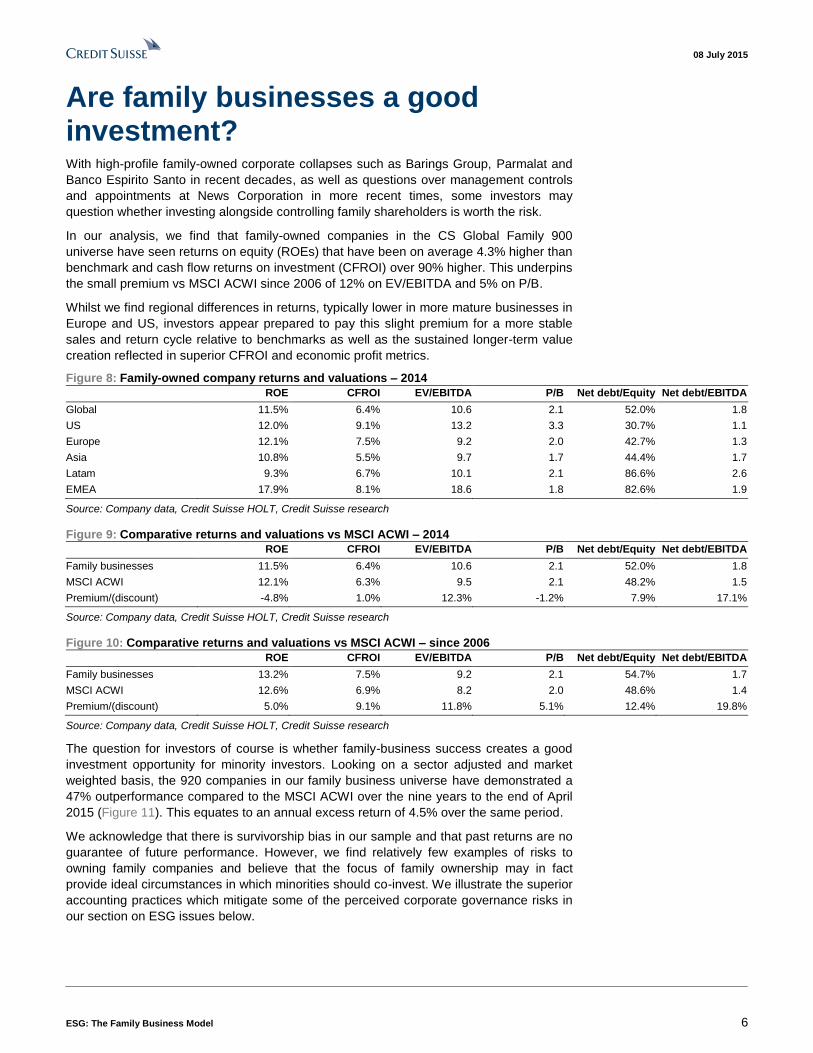

Are family businesses a good investment? With high-profile family-owned corporate collapses such as Barings Group, Parmalat and

Banco Espirito Santo in recent decades, as well as questions over management controls

and appointments at News Corporation in more recent times, some investors may

question whether investing alongside controlling family shareholders is worth the risk.

In our analysis, we find that family-owned companies in the CS Global Family 900

universe have seen returns on equity (ROEs) that have been on average 4.3% higher than

benchmark and cash flow returns on investment (CFROI) over 90% higher. This underpins

the small premium vs MSCI ACWI since 2006 of 12% on EV/EBITDA and 5% on P/B.

Whilst we find regional differences in returns, typically lower in more mature businesses in

Europe and US, investors appear prepared to pay this slight premium for a more stable

sales and return cycle relative to benchmarks as well as the sustained longer-term value

creation reflected in superior CFROI and economic profit metrics.

Figure 8: Family-owned company returns and valuations – 2014

ROE CFROI EV/EBITDA P/B Net debt/Equity Net debt/EBITDA

Global 11.5% 6.4% 10.6 2.1 52.0% 1.8

US 12.0% 9.1% 13.2 3.3 30.7% 1.1

Europe 12.1% 7.5% 9.2 2.0 42.7% 1.3

Asia 10.8% 5.5% 9.7 1.7 44.4% 1.7

Latam 9.3% 6.7% 10.1 2.1 86.6% 2.6

EMEA 17.9% 8.1% 18.6 1.8 82.6% 1.9

Source: Company data, Credit Suisse HOLT, Credit Suisse research

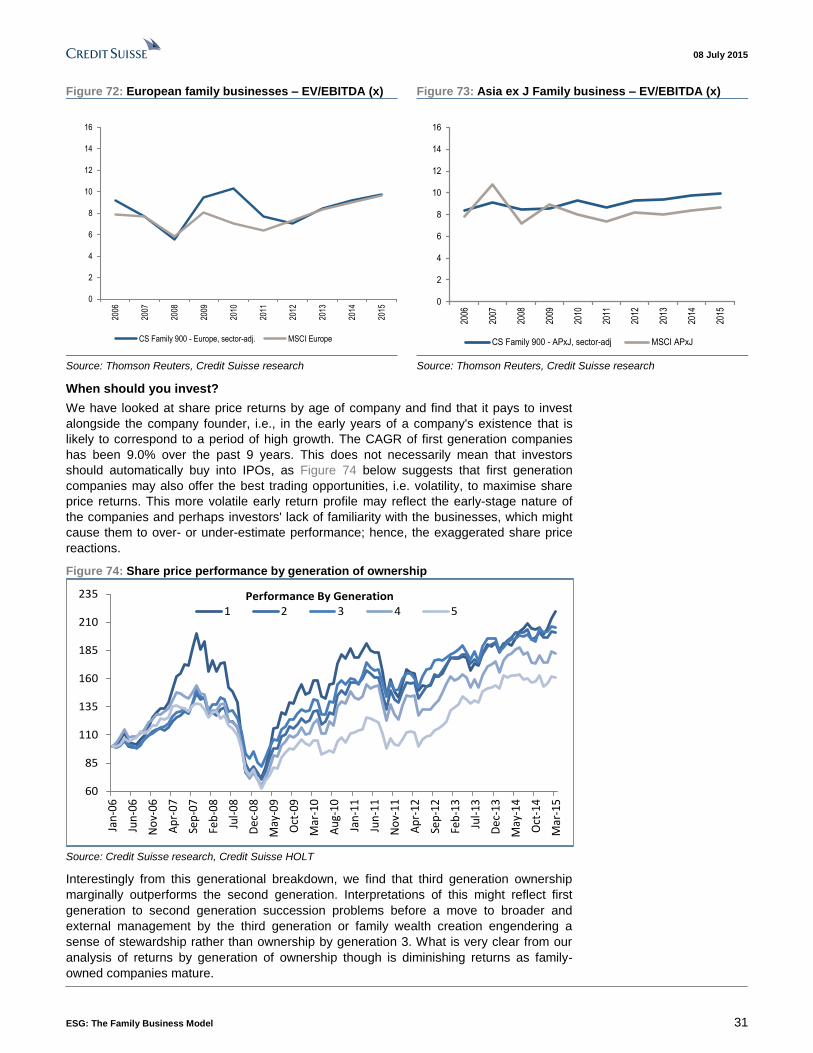

Figure 9: Comparative returns and valuations vs MSCI ACWI – 2014

ROE CFROI EV/EBITDA P/B Net debt/Equity Net debt/EBITDA

Family businesses 11.5% 6.4% 10.6 2.1 52.0% 1.8

MSCI ACWI 12.1% 6.3% 9.5 2.1 48.2% 1.5

Premium/(discount) -4.8% 1.0% 12.3% -1.2% 7.9% 17.1%

Source: Company data, Credit Suisse HOLT, Credit Suisse research

Figure 10: Comparative returns and valuations vs MSCI ACWI – since 2006

ROE CFROI EV/EBITDA P/B Net debt/Equity Net debt/EBITDA

Family businesses 13.2% 7.5% 9.2 2.1 54.7% 1.7

MSCI ACWI 12.6% 6.9% 8.2 2.0 48.6% 1.4

Premium/(discount) 5.0% 9.1% 11.8% 5.1% 12.4% 19.8%

Source: Company data, Credit Suisse HOLT, Credit Suisse research

The question for investors of course is whether family-business success creates a good

investment opportunity for minority investors. Looking on a sector adjusted and market

weighted basis, the 920 companies in our family business universe have demonstrated a

47% outperformance compared to the MSCI ACWI over the nine years to the end of April

2015 (Figure 11). This equates to an annual excess return of 4.5% over the same period.

We acknowledge that there is survivorship bias in our sample and that past returns are no

guarantee of future performance. However, we find relatively few examples of risks to

owning family companies and believe that the focus of family ownership may in fact

provide ideal circumstances in which minorities should co-invest. We illustrate the superior

accounting practices which mitigate some of the perceived corporate governance risks in

our section on ESG issues below.

08 July 2015

ESG: The Family Business Model 7

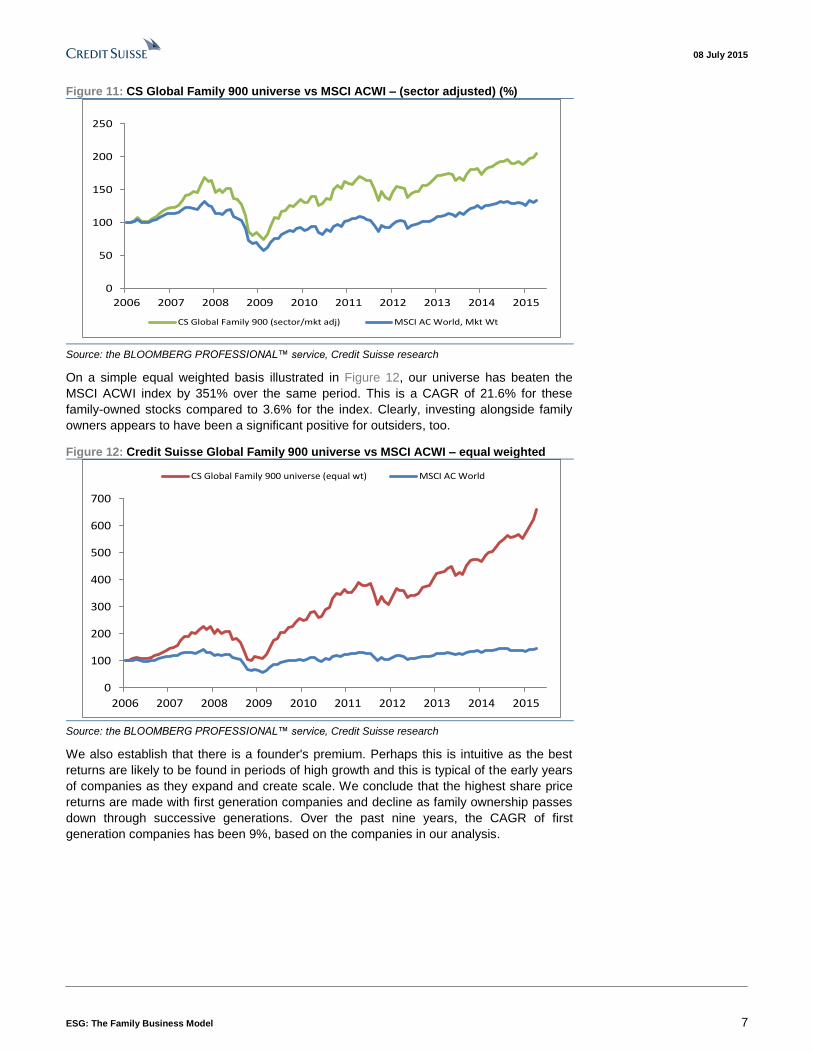

Figure 11: CS Global Family 900 universe vs MSCI ACWI – (sector adjusted) (%)

0

50

100

150

200

250

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

CS Global Family 900 (sector/mkt adj) MSCI AC World, Mkt Wt

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse research

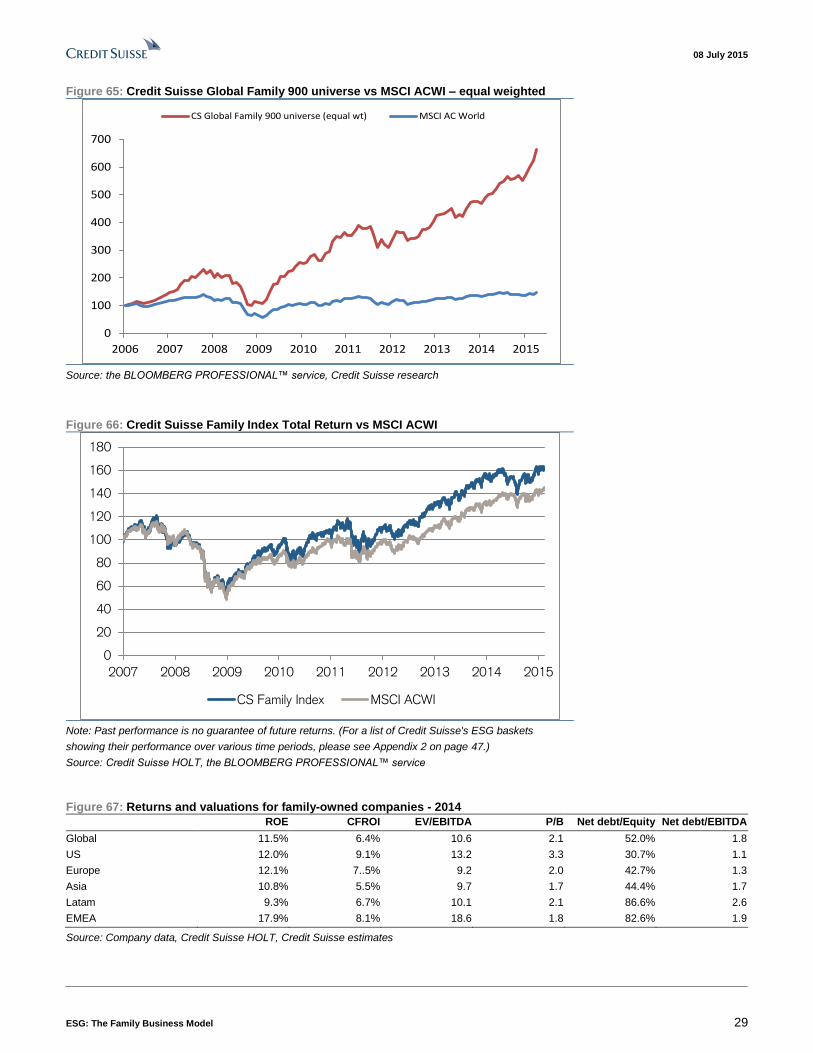

On a simple equal weighted basis illustrated in Figure 12, our universe has beaten the

MSCI ACWI index by 351% over the same period. This is a CAGR of 21.6% for these

family-owned stocks compared to 3.6% for the index. Clearly, investing alongside family

owners appears to have been a significant positive for outsiders, too.

Figure 12: Credit Suisse Global Family 900 universe vs MSCI ACWI – equal weighted

0

100

200

300

400

500

600

700

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

CS Global Family 900 universe (equal wt) MSCI AC World

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse research

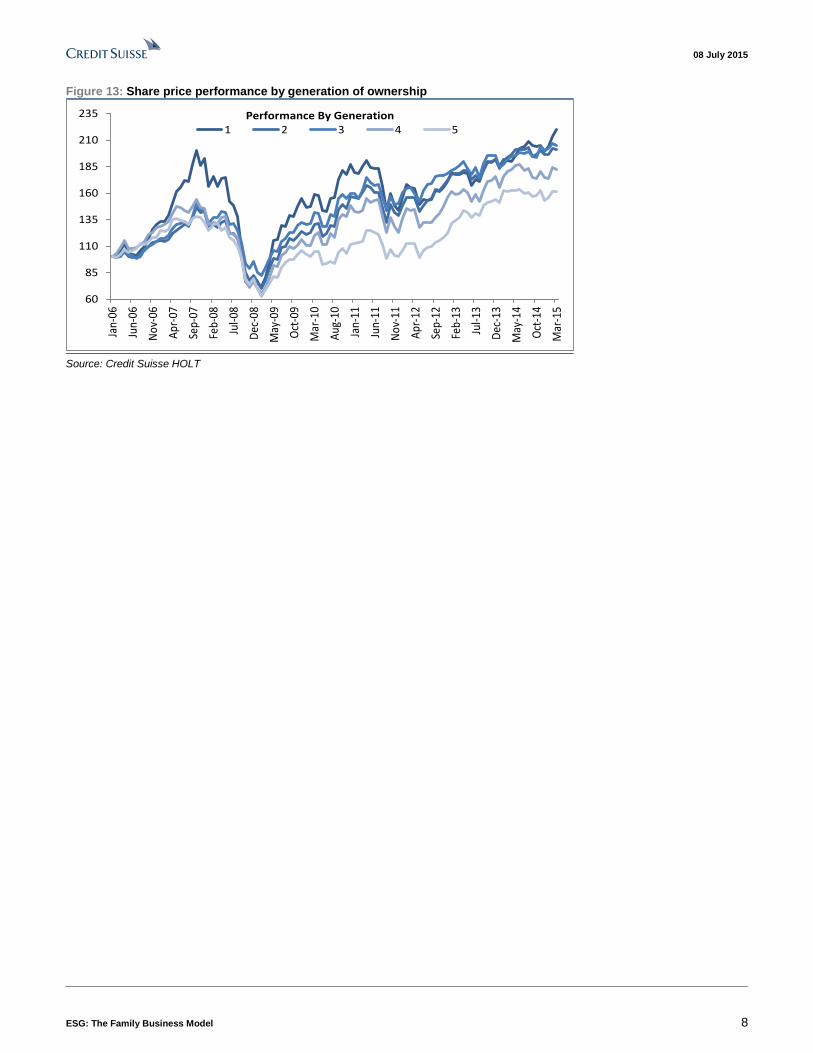

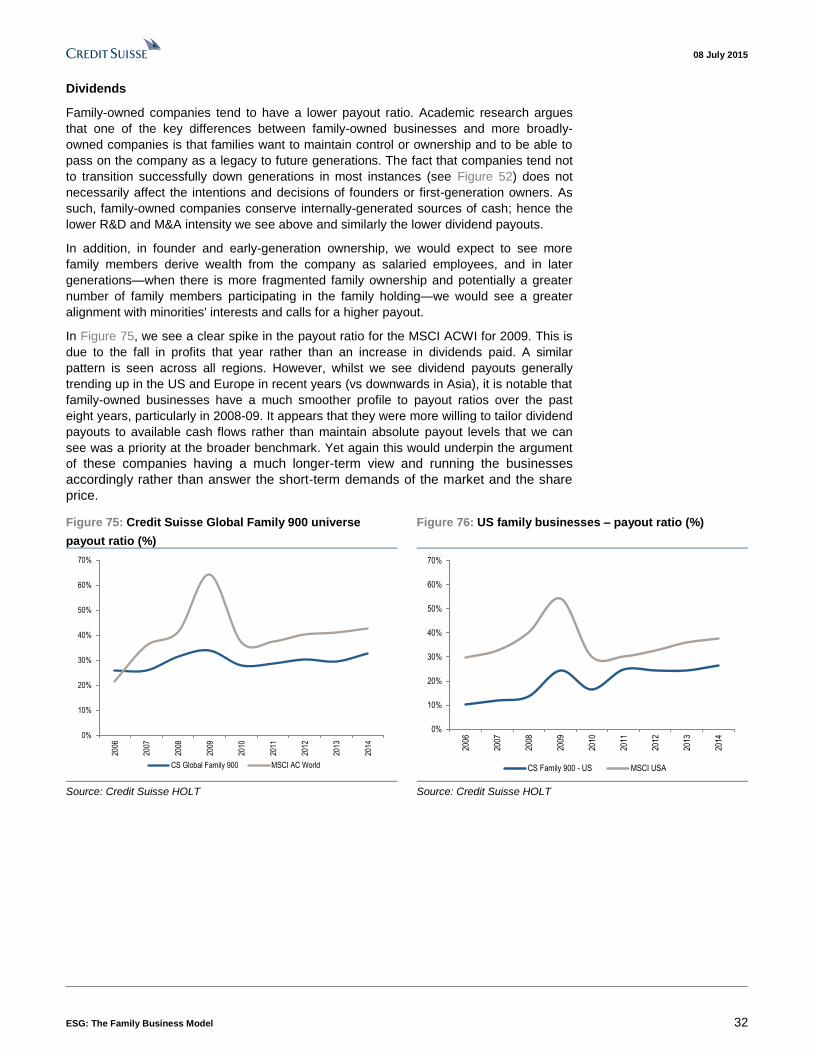

We also establish that there is a founder's premium. Perhaps this is intuitive as the best

returns are likely to be found in periods of high growth and this is typical of the early years

of companies as they expand and create scale. We conclude that the highest share price

returns are made with first generation companies and decline as family ownership passes

down through successive generations. Over the past nine years, the CAGR of first

generation companies has been 9%, based on the companies in our analysis.

08 July 2015

ESG: The Family Business Model 8

Figure 13: Share price performance by generation of ownership

60

85

110

135

160

185

210

235Ja

n-06

Jun-

06

Nov

-06

Apr

-07

Sep-

07

Feb-

08

Jul-0

8

Dec

-08

May

-09

Oct

-09

Mar

-10

Aug

-10

Jan-

11

Jun-

11

Nov

-11

Apr

-12

Sep-

12

Feb-

13

Jul-1

3

Dec

-13

May

-14

Oct

-14

Mar

-15

Performance By Generation1 2 3 4 5

Source: Credit Suisse HOLT

08 July 2015

ESG: The Family Business Model 9

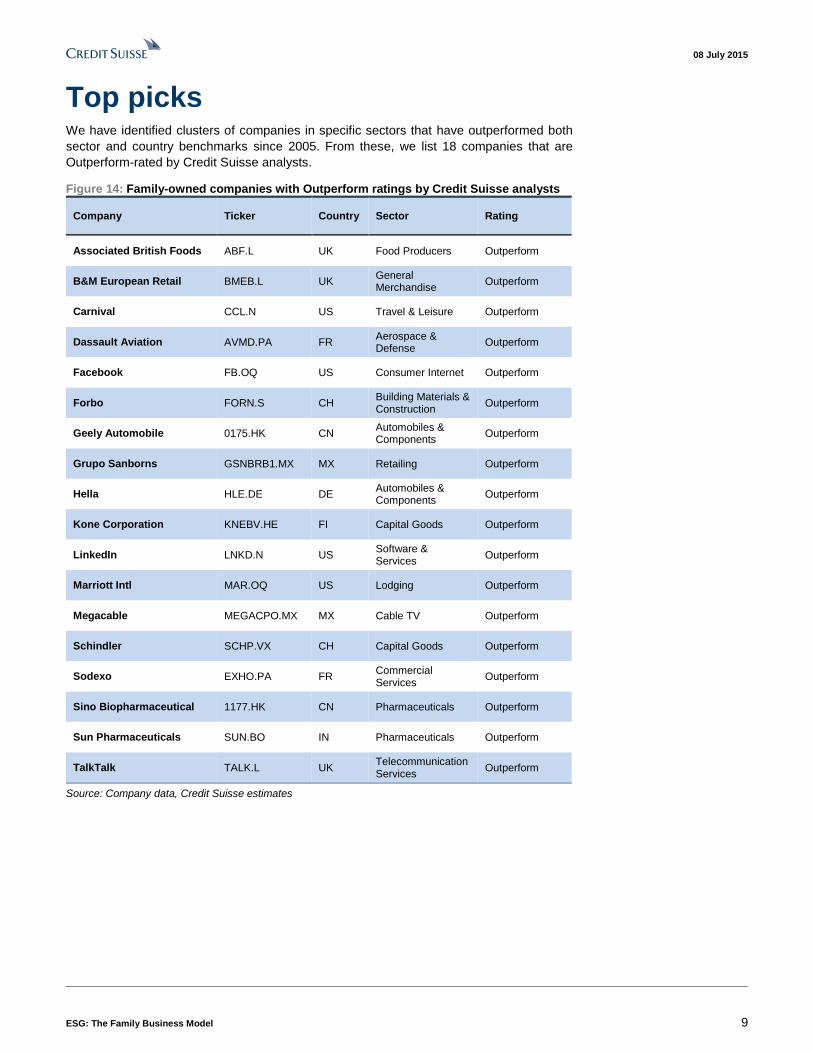

Top picks We have identified clusters of companies in specific sectors that have outperformed both

sector and country benchmarks since 2005. From these, we list 18 companies that are

Outperform-rated by Credit Suisse analysts.

Figure 14: Family-owned companies with Outperform ratings by Credit Suisse analysts

Company Ticker Country Sector Rating

Associated British Foods ABF.L UK Food Producers Outperform

B&M European Retail BMEB.L UK General Merchandise

Outperform

Carnival CCL.N US Travel & Leisure Outperform

Dassault Aviation AVMD.PA FR Aerospace & Defense

Outperform

Facebook FB.OQ US Consumer Internet Outperform

Forbo FORN.S CH Building Materials & Construction

Outperform

Geely Automobile 0175.HK CN Automobiles & Components

Outperform

Grupo Sanborns GSNBRB1.MX MX Retailing Outperform

Hella HLE.DE DE Automobiles & Components

Outperform

Kone Corporation KNEBV.HE FI Capital Goods Outperform

LinkedIn LNKD.N US Software & Services

Outperform

Marriott Intl MAR.OQ US Lodging Outperform

Megacable MEGACPO.MX MX Cable TV Outperform

Schindler SCHP.VX CH Capital Goods Outperform

Sodexo EXHO.PA FR Commercial Services

Outperform

Sino Biopharmaceutical 1177.HK CN Pharmaceuticals Outperform

Sun Pharmaceuticals SUN.BO IN Pharmaceuticals Outperform

TalkTalk TALK.L UK Telecommunication Services

Outperform

Source: Company data, Credit Suisse estimates

08 July 2015

ESG: The Family Business Model 10

We have also used HOLT screens to identify the top 20 family-owned companies for

quality and momentum where our analysts have Outperform ratings. These are listed

below in Figure 15.

Figure 15: Top 20 picks from HOLT with Credit Suisse Outperform ratings

Price Data Price Change (%) Analyst estimates

Valuation 12m

Fwd

Profitability

2015E

H

O

Ctry Company Ticker Sector Price (lc) Mcap ($m) 1m 3m 12m

CS

Rating

% to CS

TP

P/E

(x)

Div.

yield ROE CFROI

CN Jiangsu Hengrui Medicine Co. 600276.SS Health Care 60.8 14,772 10% 51% 92% OP 7% 44.6 0.3% 20% 17%

IN Sun Pharmaceuticals Industries SUN.BO Health Care 974.7 36,722 5% 11% 67% OP 7% 26.8 0.5% 10% 17%

CN Jiangsu Yanghe Brewery Joint-stock Co. 002304.SZ Consumer Staples 93.0 16,153 0% 16% 70% OP 15% 19.5 2.3% 23% 18%

TW CTBC Holding 2891.TW Financials 23.6 11,745 -4% 13% 27% OP 15% 10.8 2.9% 16% 11%

TW Hon Hai Precision 2317.TW Information Technology 98.3 47,248 5% 13% 18% OP 29% 10.2 3.5% 15% 8%

HK Belle International Holdings Ltd 1880.HK Consumer Discretionary 10.3 11,162 -2% 22% 36% OP 27% 14.8 3.1% 19% 10%

KR Samsung Electronics 005930.KS Information Technology 1,309,000 174,653 -4% -4% -9% OP 28% 8.3 1.6% 13% 9%

SG United Overseas Bank UOBH.SI Financials 23.7 28,326 -5% 3% 7% OP 18% 11.2 3.3% 10% 9%

TW Advanced Semicon. Engr. 2311.TW Information Technology 44.2 11,292 -3% 4% 13% OP 6% 12.5 4.8% 17% 9%

FI Kone Corporation KNEBV.HE Industrials 39.2 20,785 -2% -5% 28% OP 15% 21.8 3.6% 42% 39%

GB Schroders SDR.L Financials 34.1 11,838 4% 11% 31% OP -19% 18.1 2.7% 17% 21%

FR Dassault Systemes DAST.PA Information Technology 72.1 20,124 4% 15% 54% OP 4% 31.8 0.7% 16% 17%

FR Sodexo EXHO.PA Consumer Discretionary 95.3 16,380 4% 6% 19% OP -3% 21.2 2.4% 17% 22%

CH Compagnie Financiere Richemont SA CFR.VX Consumer Discretionary 84.3 46,477 -2% 0% -11% OP 19% 20.1 2.0% 9% 12%

CH Roche ROG.VX Health Care 280.7 252,298 3% 8% 6% OP 14% 18.9 3.0% 50% 10%

CH Swatch Group UHR.VX Consumer Discretionary 377.7 21,599 -11% -13% -28% OP 16% 14.5 2.1% 11% 7%

US Facebook Inc. FB.OQ Information Technology 80.6 226,203 0% 2% 27% OP 32% 35.6 0.0% 9% 24%

US McKesson Corporation MCK.N Health Care 239.2 55,388 5% 5% 31% OP 10% 18.4 0.4% 32% 22%

US Marriott International MAR.OQ Consumer Discretionary 79.2 21,776 -3% -5% 33% OP 17% 23.9 1.1% -43% 30%

US L Brands, Inc. LB.N Consumer Discretionary 87.3 25,523 -3% -5% 58% OP 8% 22.4 3.6% nm 14% Prices as of 3 July 2015; Source: Company data, Credit Suisse estimates, Credit Suisse HOLT

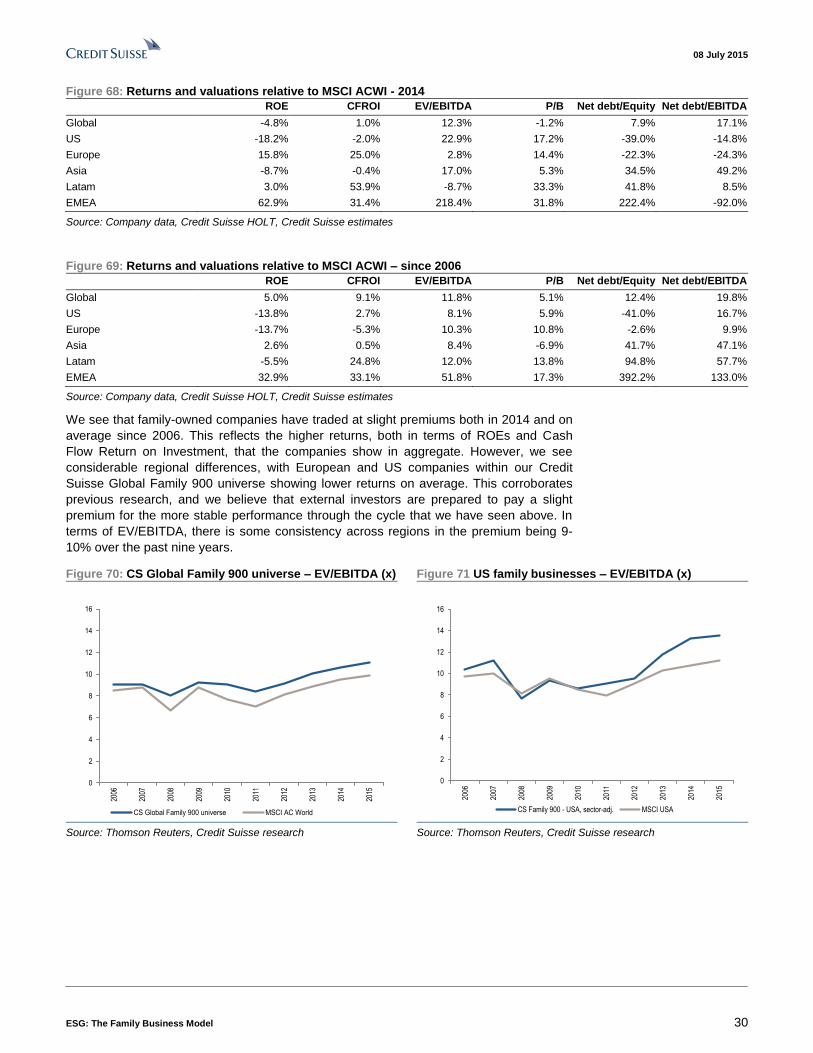

Credit Suisse has previously launched the Credit Suisse Family Business Index

(Bloomberg ticker CSFAM Index), a Delta One index comprising 40 listed US and

European family-owned companies based on HOLT's Best in Class characteristics. Since

the index's launch in March 2007, it has outperformed the MSCI ACWI by a CAGR of

140bps annually. This index is not sector or market adjusted. (For a list of Credit Suisse's

ESG baskets showing their performance over various time periods, please see Appendix 2

on page 47.)

Figure 16: Credit Suisse Family Index performance vs MSCI ACWI

0

20

40

60

80

100

120

140

160

180

2007 2008 2009 2010 2011 2012 2013 2014 2015

CS Family Index MSCI ACWI

Note: Past performance is no guarantee of future returns.

Source: Credit Suisse HOLT, the BLOOMBERG PROFESSIONAL™ service

08 July 2015

ESG: The Family Business Model 11

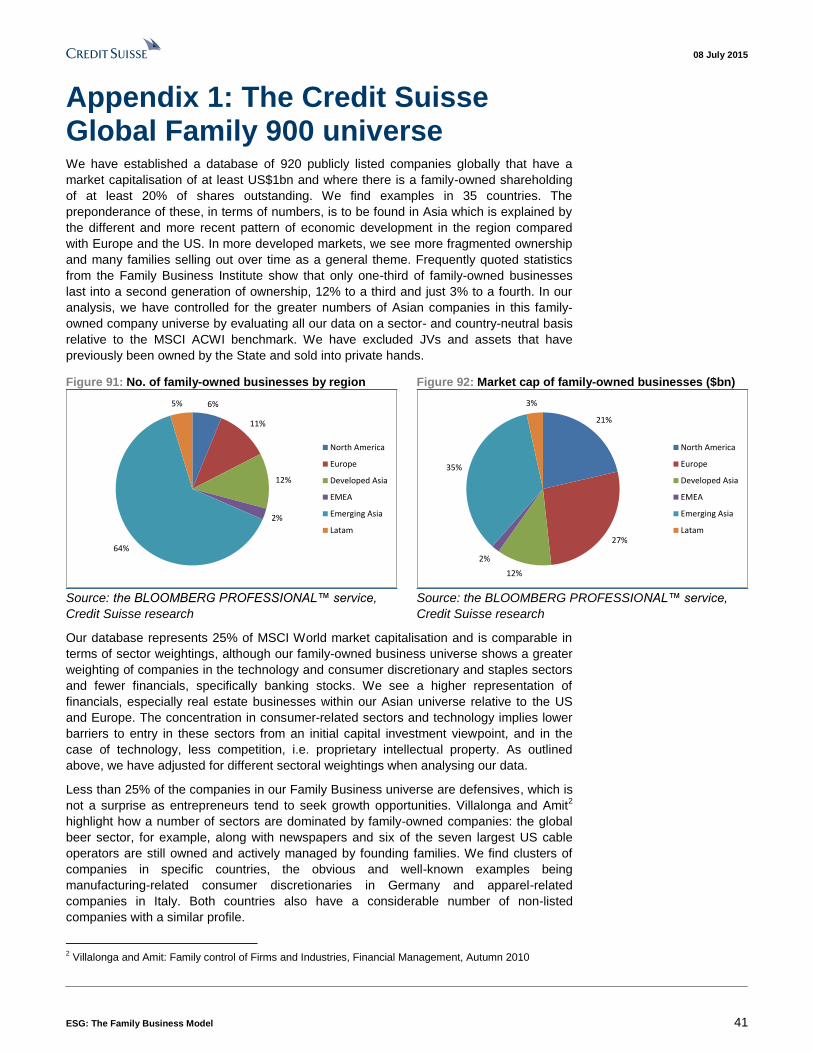

The CS Global Family 900 universe We have established a database of 920 publicly listed companies globally that have a

market capitalisation of at least US$1bn and where there is a family-owned shareholding

of at least 20% of shares outstanding. We find examples in 35 countries. The

preponderance of these, in terms of numbers, is to be found in Asia which is explained by

the different and more recent pattern of economic development in the region compared to

Europe and the US. In more developed markets, we see more fragmented ownership and

many families selling out over time as a general theme. Whilst families often sell down to

diversify their holdings and investments, they may be diluting returns as a result, given the

outperformance we see in our research.

Frequently quoted statistics from the Family Business Institute show that only one third of

family-owned businesses last into a second generation of ownership, 12% to a third and

just 3% to a fourth. In our analysis, we have controlled for the greater numbers of Asian

companies in this family-owned company universe by evaluating all our data on a sector-

and country-neutral basis relative to the MSCI ACWI benchmark. We have excluded joint

ventures and assets which have previously been owned by the State and sold into private

hands.

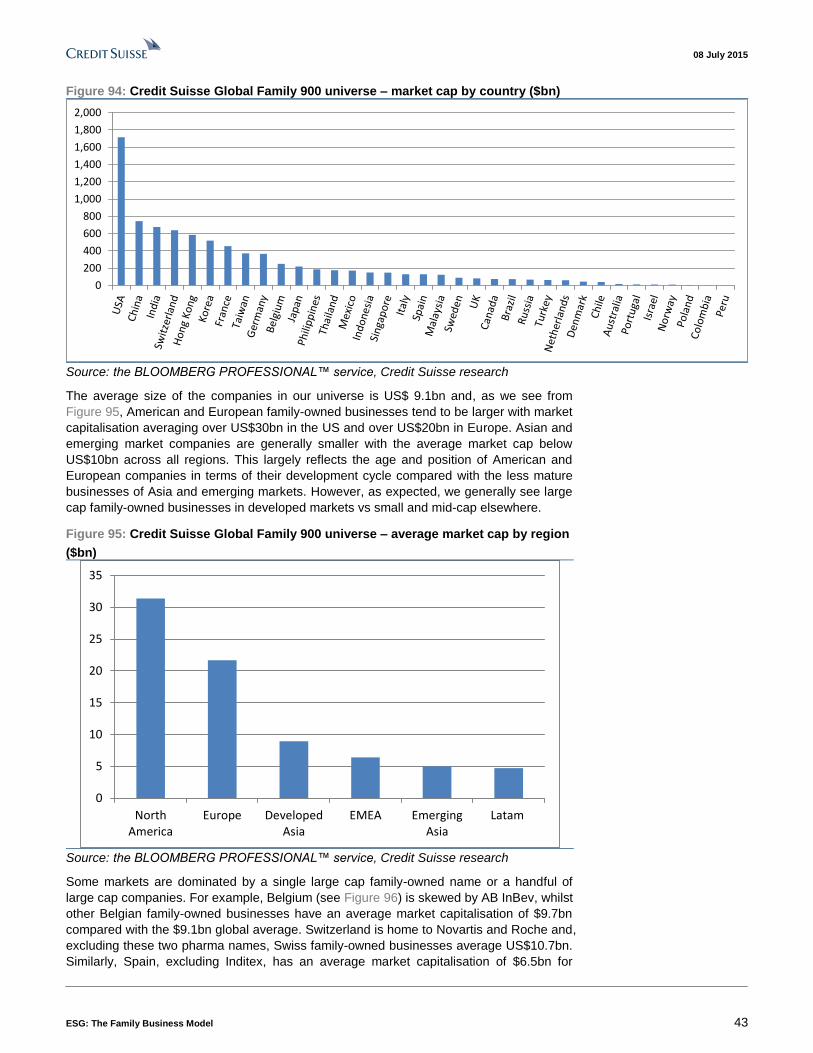

For full details of the country and sector breakdown of the companies in the Credit Suisse

Global Family 900 universe, please see Appendix 1.

Figure 17: Top 10 family-owned companies by region the Credit Suisse Global Family 900 universe Prices as of 30 June 2015

Price Data Price Change (%) Analyst estimates

Valuation 12m

Fwd

Profitability

2015E

Ctry Company Ticker Sector Price (lc) Mcap ($m) 1m 3m 12m

CS

Rating

% to CS

TP

P/E

(x)

Div.

yield ROE CFROI

North America

US Facebook Inc. FB.OQ Information Technology 85.8 240,848 7% 5% 26% OP 24% 36.9 0.0% 9% 24%

US Wal-Mart Stores, Inc. WMT Consumer Staples 70.9 228,434 -5% -12% -6% OP 20% 14.5 2.8% 19% 10%

US Google, Inc. GOOGL.OQ Information Technology 540.0 184,001 -2% 0% -9% OP 28% 17.7 0.0% 15% 16%

US Oracle Corporation ORCL.N Information Technology 40.3 174,744 -8% -5% -1% OP 24% 14.7 1.3% 26% 20%

US Berkshire Hatha BRKb.N Financials 136 167,068 -5% -5% 7% NR NA 17.7 0.0% 8% 7%

US Nike Inc. NKE Consumer Discretionary 108.0 92,870 6% 8% 38% OP 2% 25.7 1.1% 26% 17%

US Kinder Morgan, Inc. KMI Energy 38.4 83,235 -7% -8% 6% OP 35% 42.1 5.5% 5% 5%

US McKesson Corporation MCK Health Care 224.8 52,228 -6% 1% 19% OP 17% 17.6 0.4% 32% 21%

US Phillips 66 PSX Energy 80.6 43,690 2% 3% 0% OP 30% 11.8 2.7% 17% 4%

US Carnival CCL Consumer Discretionary 49.4 38,705 6% 3% 32% OP 17% 16.7 2.2% 8% 6%

Europe

CH Novartis NOVN.VX Health Care 92.2 263,215 -5% -4% 14% OP 19% 18.0 3.2% 14% 8%

CH Roche ROG.VX Health Care 262.0 237,902 -6% -2% -1% OP 22% 17.5 3.3% 50% 10%

BE Anheuser-Busch InBev ABI.BR Consumer Staples 107.5 192,370 -2% -7% 28% OP 17% 21.1 3.4% 17% 25%

ES Inditex ITX.MC Consumer Discretionary 29.2 101,107 -5% -3% 30% UP -31% 29.5 2.1% 32% 13%

FR L'Oreal OREP.PA Consumer Staples 160.0 99,647 -8% -7% 27% NT 9% 24.5 2.0% 17% 20%

FR LVMH LVMH.PA Consumer Discretionary 157.2 88,818 -4% -4% 24% UP -14% 18.8 2.5% 16% 13%

DE SAP SAPG.F Information Technology 62.8 85,900 -7% -6% 11% OP 35% 16.1 1.9% 18% 29%

DE BMW BMWG.DE Consumer Discretionary 98.2 65,765 -3% -15% 5% NR NA 9.9 3.5% 16% 7%

SE Hennes & Mauritz HMb.ST Consumer Discretionary 319.2 56,116 -6% -9% 10% NT 13% 22.9 3.4% 37% 17%

DE Merck KGaA MRCG.DE Health Care 89.4 49,671 -9% -15% 39% OP 29% 16.5 1.3% 18% 4%

Asia

KR Samsung Electronics 005930.KS Information Technology 1,295,000 170,778 0% -10% -1% OP 30% 8.2 1.7% 13% 8%

IN Tata Consultancy Services TCS.BO Information Technology 2,552.2 78,577 -2% 0% 8% OP 21% 20.2 1.8% 34% 26%

JP SoftBank Group Corp. 9984.T Telecommunication Serv ices 7,166.0 70,110 -3% 2% -5% OP 20% 15.9 0.6% 32% 6%

HK CK Hutchison Holdings Limited 0001.HK Industrials 113.9 56,715 -7% 24% 44% OP 26% 8.7 3.1% 8% 4%

IN Reliance Industries RELI.BO Energy 1,000.5 50,894 11% 20% -1% OP 4% 11.8 1.1% 11% 4%

TW Hon Hai Precision 2317.TW Information Technology 98.0 47,838 1% 5% 8% OP 30% 10.1 3.6% 15% 9%

CN JD.com, Inc. JD.OQ Consumer Discretionary 34.1 47,167 -2% 16% 15% OP 17% nm 0.0% -6% 1%

JP Fast Retailing 9983.T Consumer Discretionary 56,610.0 46,980 10% 20% 69% NT -21% 40.1 0.7% 19% 8%

HK Sun Hung Kai Properties 0016.HK Financials 125.6 46,582 -5% 4% 18% OP 21% 14.6 2.8% 5% 4%

SG Jardine Matheson JARD.SI Industrials 57 39,646 -8% -9% -5% NT 7% 12.3 2.7% 8% 5% Priced as of 30 June 2015; Source: Company data, Credit Suisse Research Institute's Asian Family Businesses Report (2011), Credit Suisse

estimates for rated stocks; the BLOOMBERG PROFESSIONAL™ service for Not Rated (NR) stocks

08 July 2015

ESG: The Family Business Model 12

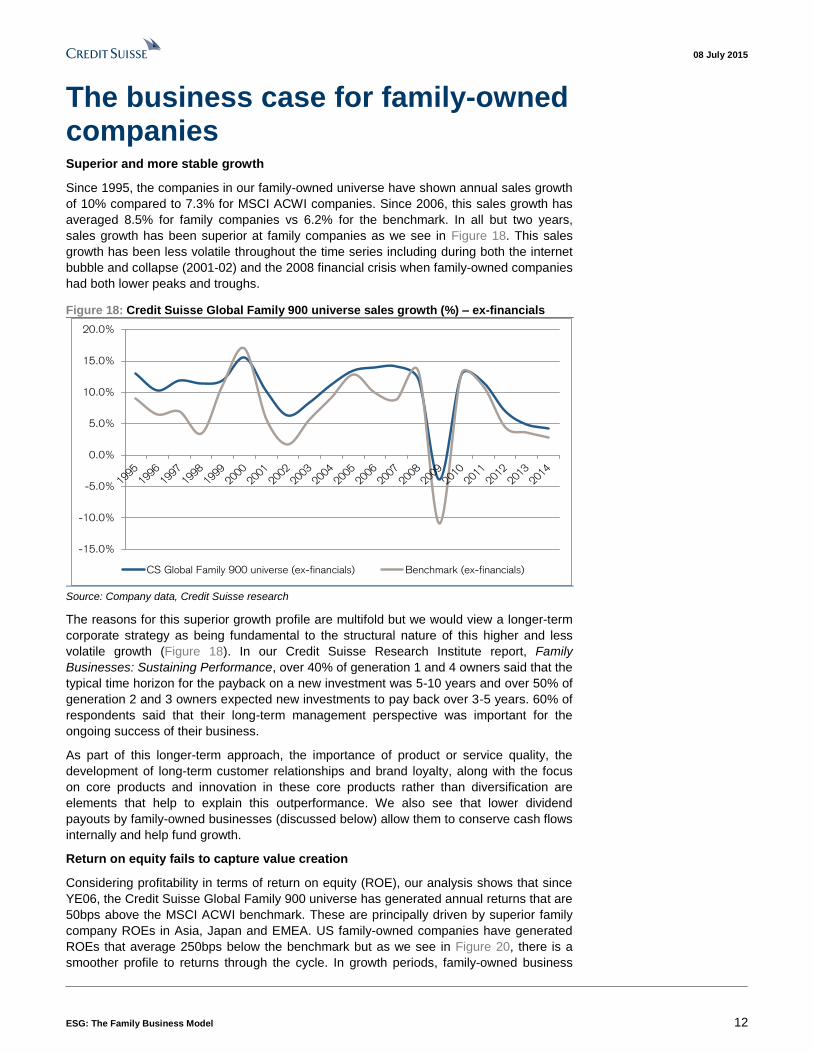

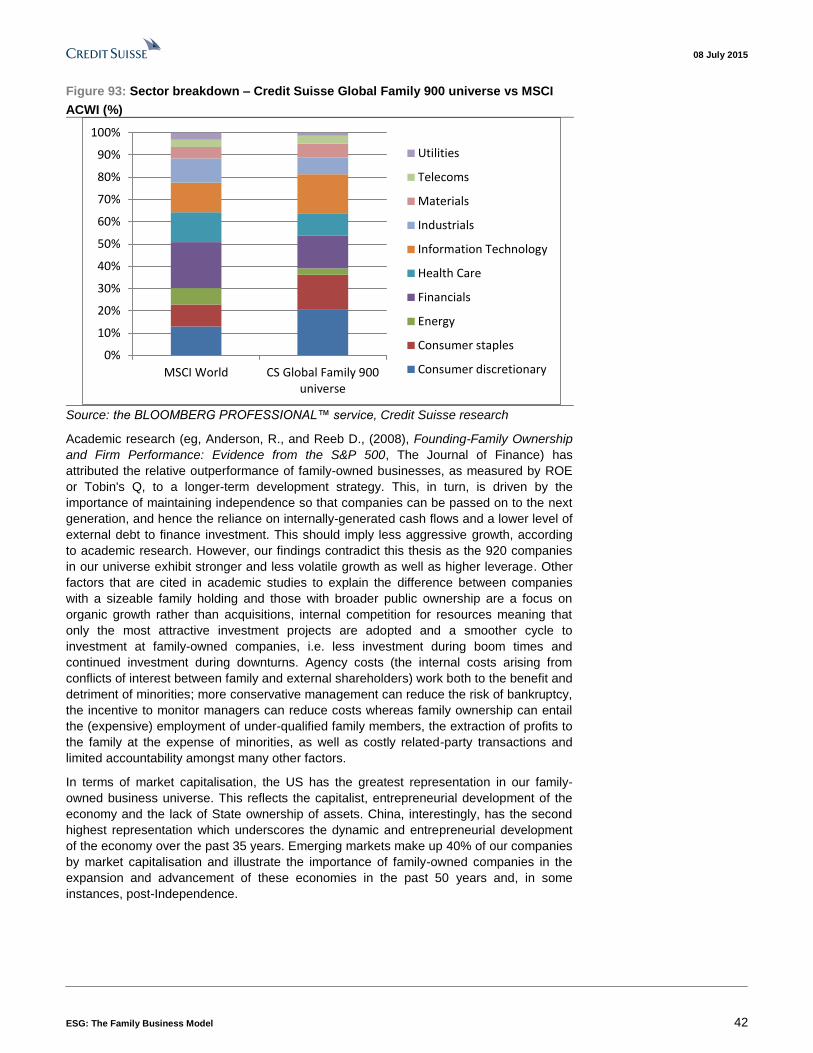

The business case for family-owned companies Superior and more stable growth

Since 1995, the companies in our family-owned universe have shown annual sales growth

of 10% compared to 7.3% for MSCI ACWI companies. Since 2006, this sales growth has

averaged 8.5% for family companies vs 6.2% for the benchmark. In all but two years,

sales growth has been superior at family companies as we see in Figure 18. This sales

growth has been less volatile throughout the time series including during both the internet

bubble and collapse (2001-02) and the 2008 financial crisis when family-owned companies

had both lower peaks and troughs.

Figure 18: Credit Suisse Global Family 900 universe sales growth (%) – ex-financials

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

CS Global Family 900 universe (ex-financials) Benchmark (ex-financials)

Source: Company data, Credit Suisse research

The reasons for this superior growth profile are multifold but we would view a longer-term

corporate strategy as being fundamental to the structural nature of this higher and less

volatile growth (Figure 18). In our Credit Suisse Research Institute report, Family

Businesses: Sustaining Performance, over 40% of generation 1 and 4 owners said that the

typical time horizon for the payback on a new investment was 5-10 years and over 50% of

generation 2 and 3 owners expected new investments to pay back over 3-5 years. 60% of

respondents said that their long-term management perspective was important for the

ongoing success of their business.

As part of this longer-term approach, the importance of product or service quality, the

development of long-term customer relationships and brand loyalty, along with the focus

on core products and innovation in these core products rather than diversification are

elements that help to explain this outperformance. We also see that lower dividend

payouts by family-owned businesses (discussed below) allow them to conserve cash flows

internally and help fund growth.

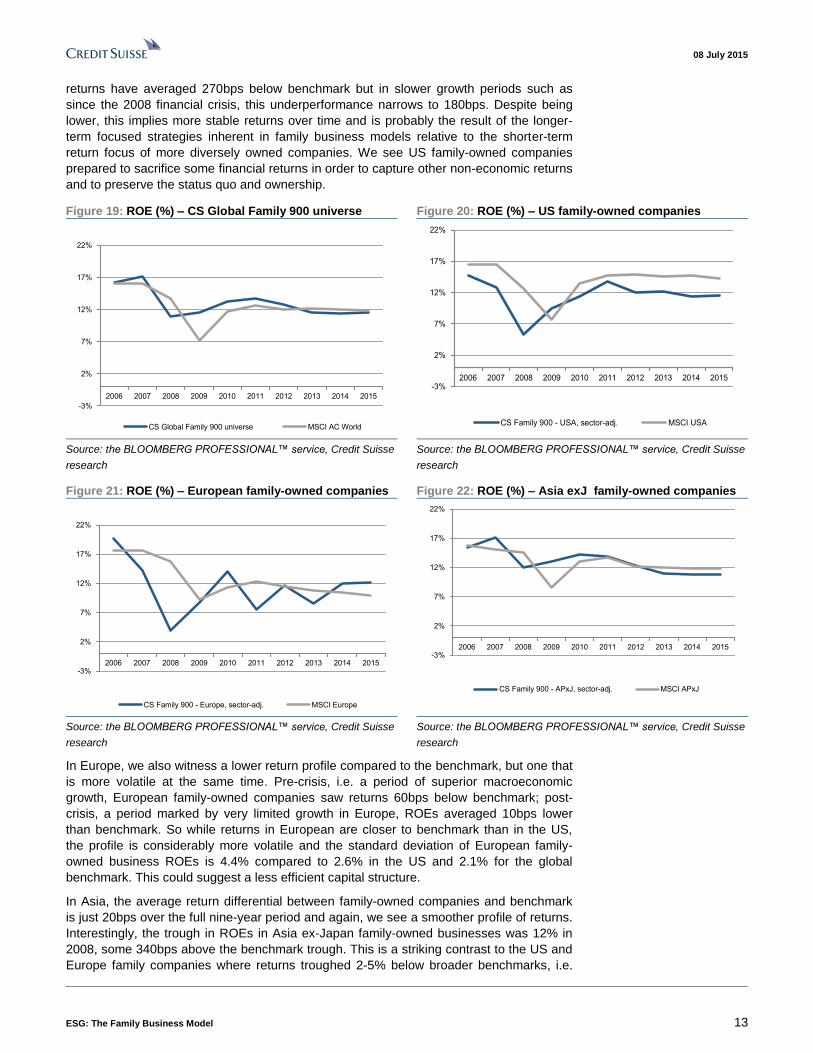

Return on equity fails to capture value creation

Considering profitability in terms of return on equity (ROE), our analysis shows that since

YE06, the Credit Suisse Global Family 900 universe has generated annual returns that are

50bps above the MSCI ACWI benchmark. These are principally driven by superior family

company ROEs in Asia, Japan and EMEA. US family-owned companies have generated

ROEs that average 250bps below the benchmark but as we see in Figure 20, there is a

smoother profile to returns through the cycle. In growth periods, family-owned business

08 July 2015

ESG: The Family Business Model 13

returns have averaged 270bps below benchmark but in slower growth periods such as

since the 2008 financial crisis, this underperformance narrows to 180bps. Despite being

lower, this implies more stable returns over time and is probably the result of the longer-

term focused strategies inherent in family business models relative to the shorter-term

return focus of more diversely owned companies. We see US family-owned companies

prepared to sacrifice some financial returns in order to capture other non-economic returns

and to preserve the status quo and ownership.

Figure 19: ROE (%) – CS Global Family 900 universe Figure 20: ROE (%) – US family-owned companies

-3%

2%

7%

12%

17%

22%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

CS Global Family 900 universe MSCI AC World

-3%

2%

7%

12%

17%

22%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

CS Family 900 - USA, sector-adj. MSCI USA

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse

research

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse

research

Figure 21: ROE (%) – European family-owned companies Figure 22: ROE (%) – Asia exJ family-owned companies

-3%

2%

7%

12%

17%

22%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

CS Family 900 - Europe, sector-adj. MSCI Europe

-3%

2%

7%

12%

17%

22%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

CS Family 900 - APxJ, sector-adj. MSCI APxJ

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse

research

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse

research

In Europe, we also witness a lower return profile compared to the benchmark, but one that

is more volatile at the same time. Pre-crisis, i.e. a period of superior macroeconomic

growth, European family-owned companies saw returns 60bps below benchmark; post-

crisis, a period marked by very limited growth in Europe, ROEs averaged 10bps lower

than benchmark. So while returns in European are closer to benchmark than in the US,

the profile is considerably more volatile and the standard deviation of European family-

owned business ROEs is 4.4% compared to 2.6% in the US and 2.1% for the global

benchmark. This could suggest a less efficient capital structure.

In Asia, the average return differential between family-owned companies and benchmark

is just 20bps over the full nine-year period and again, we see a smoother profile of returns.

Interestingly, the trough in ROEs in Asia ex-Japan family-owned businesses was 12% in

2008, some 340bps above the benchmark trough. This is a striking contrast to the US and

Europe family companies where returns troughed 2-5% below broader benchmarks, i.e.

08 July 2015

ESG: The Family Business Model 14

family-owned businesses bore the brunt of the 2008 hit. So up until 2013, we can see

stronger performance from family-owned companies in years of superior macro growth

and more limited downside during more challenging macro backdrops.

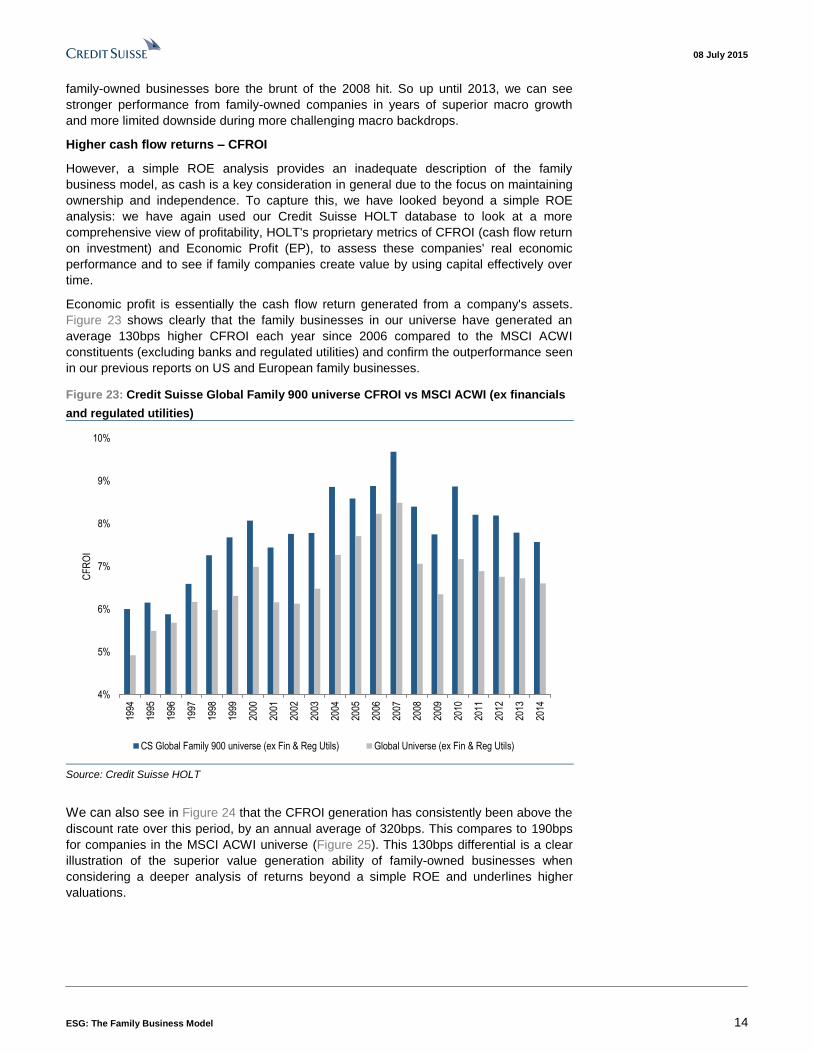

Higher cash flow returns – CFROI

However, a simple ROE analysis provides an inadequate description of the family

business model, as cash is a key consideration in general due to the focus on maintaining

ownership and independence. To capture this, we have looked beyond a simple ROE

analysis: we have again used our Credit Suisse HOLT database to look at a more

comprehensive view of profitability, HOLT's proprietary metrics of CFROI (cash flow return

on investment) and Economic Profit (EP), to assess these companies' real economic

performance and to see if family companies create value by using capital effectively over

time.

Economic profit is essentially the cash flow return generated from a company's assets.

Figure 23 shows clearly that the family businesses in our universe have generated an

average 130bps higher CFROI each year since 2006 compared to the MSCI ACWI

constituents (excluding banks and regulated utilities) and confirm the outperformance seen

in our previous reports on US and European family businesses.

Figure 23: Credit Suisse Global Family 900 universe CFROI vs MSCI ACWI (ex financials

and regulated utilities)

4%

5%

6%

7%

8%

9%

10%

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

CF

RO

I

CS Global Family 900 universe (ex Fin & Reg Utils) Global Universe (ex Fin & Reg Utils)

Source: Credit Suisse HOLT

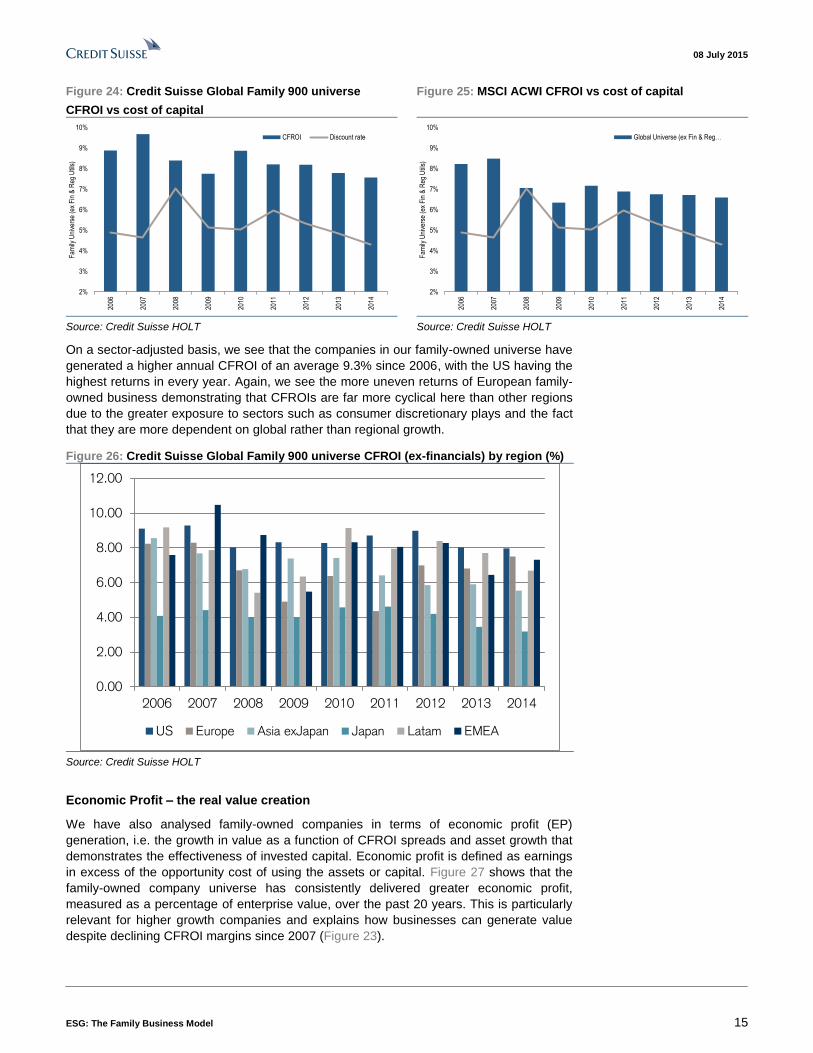

We can also see in Figure 24 that the CFROI generation has consistently been above the

discount rate over this period, by an annual average of 320bps. This compares to 190bps

for companies in the MSCI ACWI universe (Figure 25). This 130bps differential is a clear

illustration of the superior value generation ability of family-owned businesses when

considering a deeper analysis of returns beyond a simple ROE and underlines higher

valuations.

08 July 2015

ESG: The Family Business Model 15

Figure 24: Credit Suisse Global Family 900 universe

CFROI vs cost of capital

Figure 25: MSCI ACWI CFROI vs cost of capital

2%

3%

4%

5%

6%

7%

8%

9%

10%

2006

2007

2008

2009

2010

2011

2012

2013

2014

Fam

ily U

nive

rse

(ex

Fin

& R

eg U

tils)

CFROI Discount rate

2%

3%

4%

5%

6%

7%

8%

9%

10%

2006

2007

2008

2009

2010

2011

2012

2013

2014

Fam

ily U

nive

rse

(ex

Fin

& R

eg U

tils)

Global Universe (ex Fin & Reg…

Source: Credit Suisse HOLT Source: Credit Suisse HOLT

On a sector-adjusted basis, we see that the companies in our family-owned universe have

generated a higher annual CFROI of an average 9.3% since 2006, with the US having the

highest returns in every year. Again, we see the more uneven returns of European family-

owned business demonstrating that CFROIs are far more cyclical here than other regions

due to the greater exposure to sectors such as consumer discretionary plays and the fact

that they are more dependent on global rather than regional growth.

Figure 26: Credit Suisse Global Family 900 universe CFROI (ex-financials) by region (%)

0.00

2.00

4.00

6.00

8.00

10.00

12.00

2006 2007 2008 2009 2010 2011 2012 2013 2014

US Europe Asia exJapan Japan Latam EMEA

Source: Credit Suisse HOLT

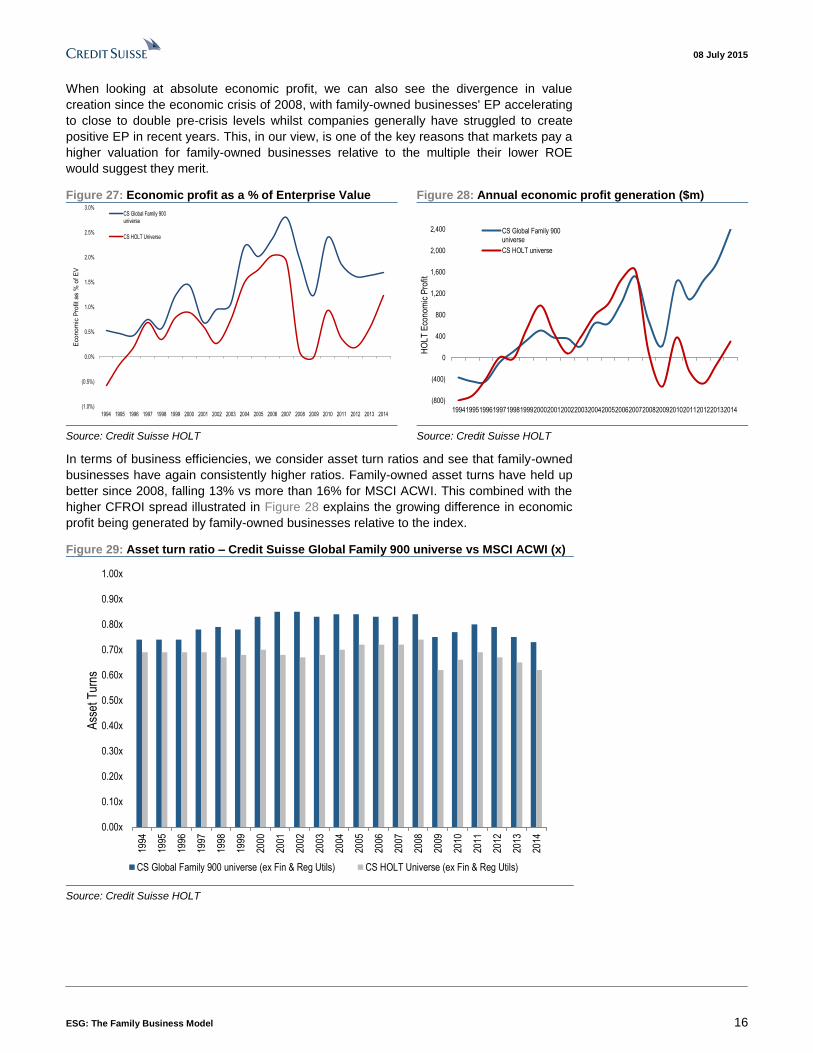

Economic Profit – the real value creation

We have also analysed family-owned companies in terms of economic profit (EP)

generation, i.e. the growth in value as a function of CFROI spreads and asset growth that

demonstrates the effectiveness of invested capital. Economic profit is defined as earnings

in excess of the opportunity cost of using the assets or capital. Figure 27 shows that the

family-owned company universe has consistently delivered greater economic profit,

measured as a percentage of enterprise value, over the past 20 years. This is particularly

relevant for higher growth companies and explains how businesses can generate value

despite declining CFROI margins since 2007 (Figure 23).

08 July 2015

ESG: The Family Business Model 16

When looking at absolute economic profit, we can also see the divergence in value

creation since the economic crisis of 2008, with family-owned businesses' EP accelerating

to close to double pre-crisis levels whilst companies generally have struggled to create

positive EP in recent years. This, in our view, is one of the key reasons that markets pay a

higher valuation for family-owned businesses relative to the multiple their lower ROE

would suggest they merit.

Figure 27: Economic profit as a % of Enterprise Value Figure 28: Annual economic profit generation ($m)

(1.0%)

(0.5%)

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Eco

no

mic

Pro

fit

as %

of

EV

CS Global Family 900universe

CS HOLT Universe

(800)

(400)

0

400

800

1,200

1,600

2,000

2,400

199419951996199719981999200020012002200320042005200620072008200920102011201220132014

HO

LT

Eco

no

mic

Pro

fit

CS Global Family 900universe

CS HOLT universe

Source: Credit Suisse HOLT Source: Credit Suisse HOLT

In terms of business efficiencies, we consider asset turn ratios and see that family-owned

businesses have again consistently higher ratios. Family-owned asset turns have held up

better since 2008, falling 13% vs more than 16% for MSCI ACWI. This combined with the

higher CFROI spread illustrated in Figure 28 explains the growing difference in economic

profit being generated by family-owned businesses relative to the index.

Figure 29: Asset turn ratio – Credit Suisse Global Family 900 universe vs MSCI ACWI (x)

0.00x

0.10x

0.20x

0.30x

0.40x

0.50x

0.60x

0.70x

0.80x

0.90x

1.00x

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Ass

et T

urns

CS Global Family 900 universe (ex Fin & Reg Utils) CS HOLT Universe (ex Fin & Reg Utils)

Source: Credit Suisse HOLT

08 July 2015

ESG: The Family Business Model 17

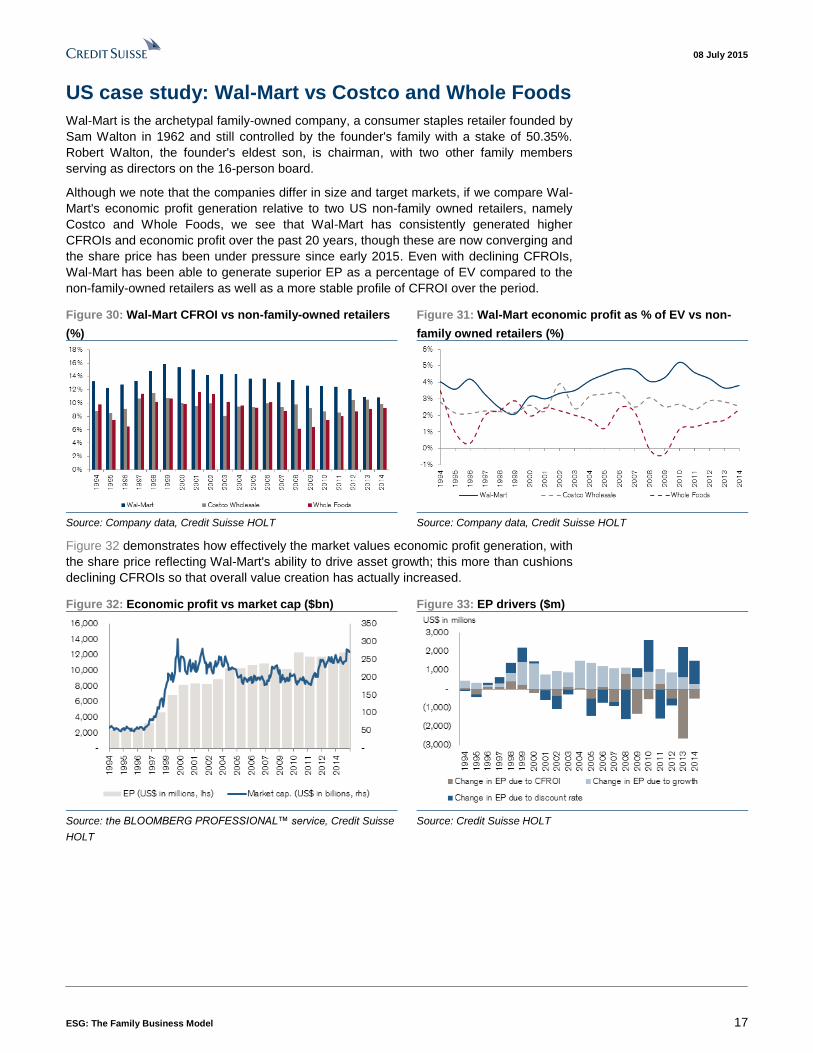

US case study: Wal-Mart vs Costco and Whole Foods

Wal-Mart is the archetypal family-owned company, a consumer staples retailer founded by

Sam Walton in 1962 and still controlled by the founder's family with a stake of 50.35%.

Robert Walton, the founder's eldest son, is chairman, with two other family members

serving as directors on the 16-person board.

Although we note that the companies differ in size and target markets, if we compare Wal-

Mart's economic profit generation relative to two US non-family owned retailers, namely

Costco and Whole Foods, we see that Wal-Mart has consistently generated higher

CFROIs and economic profit over the past 20 years, though these are now converging and

the share price has been under pressure since early 2015. Even with declining CFROIs,

Wal-Mart has been able to generate superior EP as a percentage of EV compared to the

non-family-owned retailers as well as a more stable profile of CFROI over the period.

Figure 30: Wal-Mart CFROI vs non-family-owned retailers

(%)

Figure 31: Wal-Mart economic profit as % of EV vs non-

family owned retailers (%)

Source: Company data, Credit Suisse HOLT Source: Company data, Credit Suisse HOLT

Figure 32 demonstrates how effectively the market values economic profit generation, with

the share price reflecting Wal-Mart's ability to drive asset growth; this more than cushions

declining CFROIs so that overall value creation has actually increased.

Figure 32: Economic profit vs market cap ($bn) Figure 33: EP drivers ($m)

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse

HOLT

Source: Credit Suisse HOLT

08 July 2015

ESG: The Family Business Model 18

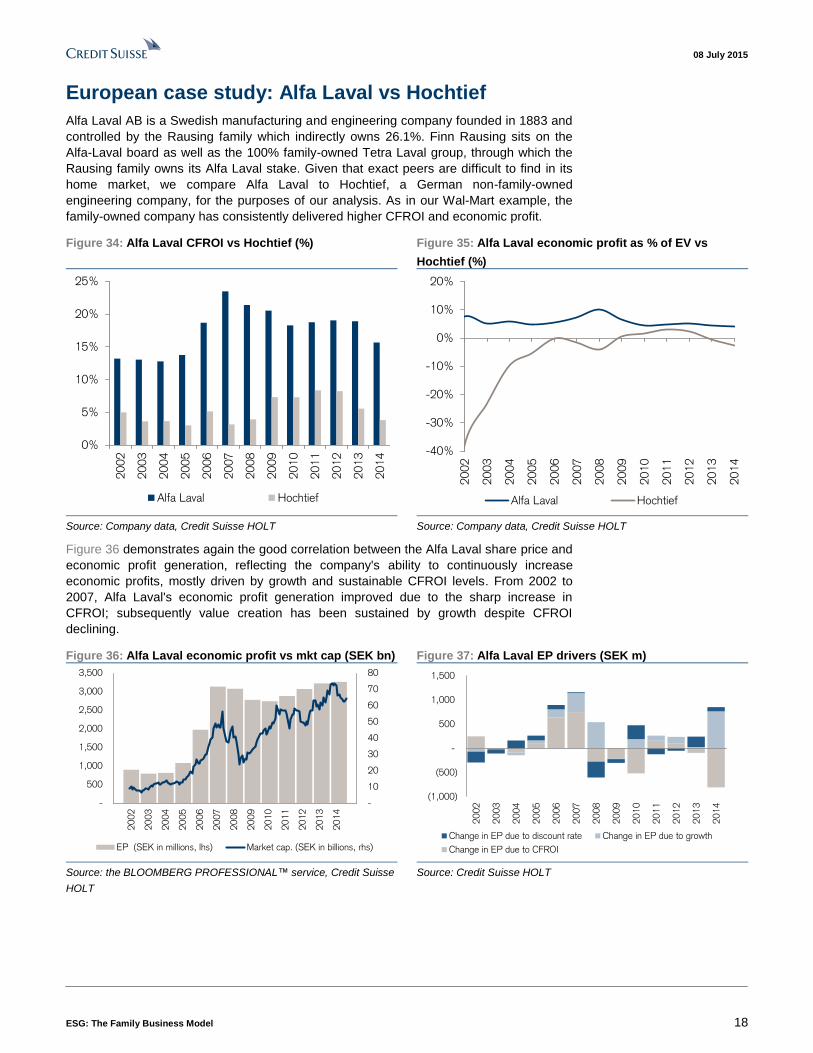

European case study: Alfa Laval vs Hochtief

Alfa Laval AB is a Swedish manufacturing and engineering company founded in 1883 and

controlled by the Rausing family which indirectly owns 26.1%. Finn Rausing sits on the

Alfa-Laval board as well as the 100% family-owned Tetra Laval group, through which the

Rausing family owns its Alfa Laval stake. Given that exact peers are difficult to find in its

home market, we compare Alfa Laval to Hochtief, a German non-family-owned

engineering company, for the purposes of our analysis. As in our Wal-Mart example, the

family-owned company has consistently delivered higher CFROI and economic profit.

Figure 34: Alfa Laval CFROI vs Hochtief (%) Figure 35: Alfa Laval economic profit as % of EV vs

Hochtief (%)

0%

5%

10%

15%

20%

25%

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Alfa Laval Hochtief

-40%

-30%

-20%

-10%

0%

10%

20%

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Alfa Laval Hochtief

Source: Company data, Credit Suisse HOLT Source: Company data, Credit Suisse HOLT

Figure 36 demonstrates again the good correlation between the Alfa Laval share price and

economic profit generation, reflecting the company's ability to continuously increase

economic profits, mostly driven by growth and sustainable CFROI levels. From 2002 to

2007, Alfa Laval's economic profit generation improved due to the sharp increase in

CFROI; subsequently value creation has been sustained by growth despite CFROI

declining.

Figure 36: Alfa Laval economic profit vs mkt cap (SEK bn) Figure 37: Alfa Laval EP drivers (SEK m)

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

-

500

1,000

1,500

2,000

2,500

3,000

3,500

-

10

20

30

40

50

60

70

80

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

EP (SEK in millions, lhs) Market cap. (SEK in billions, rhs)

(1,000)

(500)

-

500

1,000

1,500

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Change in EP due to discount rate Change in EP due to growth

Change in EP due to CFROI

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse

HOLT

Source: Credit Suisse HOLT

08 July 2015

ESG: The Family Business Model 19

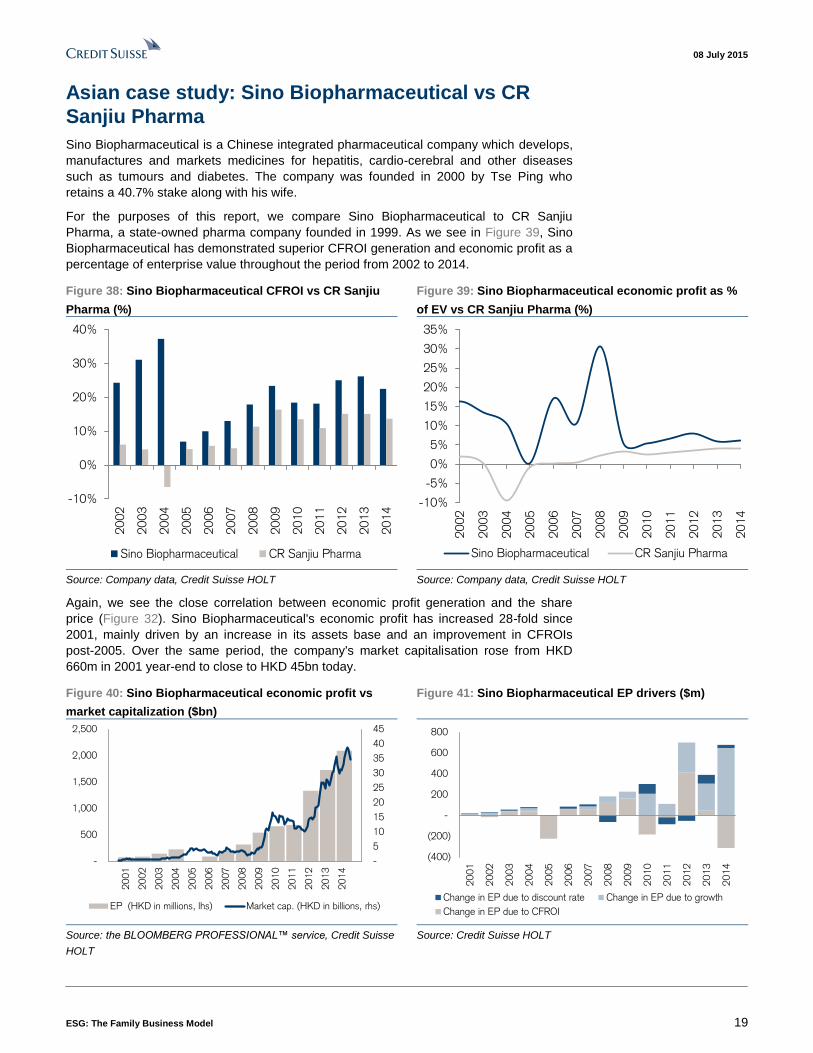

Asian case study: Sino Biopharmaceutical vs CR

Sanjiu Pharma

Sino Biopharmaceutical is a Chinese integrated pharmaceutical company which develops,

manufactures and markets medicines for hepatitis, cardio-cerebral and other diseases

such as tumours and diabetes. The company was founded in 2000 by Tse Ping who

retains a 40.7% stake along with his wife.

For the purposes of this report, we compare Sino Biopharmaceutical to CR Sanjiu

Pharma, a state-owned pharma company founded in 1999. As we see in Figure 39, Sino

Biopharmaceutical has demonstrated superior CFROI generation and economic profit as a

percentage of enterprise value throughout the period from 2002 to 2014.

Figure 38: Sino Biopharmaceutical CFROI vs CR Sanjiu

Pharma (%)

Figure 39: Sino Biopharmaceutical economic profit as %

of EV vs CR Sanjiu Pharma (%)

-10%

0%

10%

20%

30%

40%

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Sino Biopharmaceutical CR Sanjiu Pharma

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Sino Biopharmaceutical CR Sanjiu Pharma

Source: Company data, Credit Suisse HOLT Source: Company data, Credit Suisse HOLT

Again, we see the close correlation between economic profit generation and the share

price (Figure 32). Sino Biopharmaceutical's economic profit has increased 28-fold since

2001, mainly driven by an increase in its assets base and an improvement in CFROIs

post-2005. Over the same period, the company's market capitalisation rose from HKD

660m in 2001 year-end to close to HKD 45bn today.

Figure 40: Sino Biopharmaceutical economic profit vs

market capitalization ($bn)

Figure 41: Sino Biopharmaceutical EP drivers ($m)

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

-

500

1,000

1,500

2,000

2,500

-

5

10

15

20

25

30

35

40

45

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

EP (HKD in millions, lhs) Market cap. (HKD in billions, rhs)

(400)

(200)

-

200

400

600

800

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Change in EP due to discount rate Change in EP due to growth

Change in EP due to CFROI

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse

HOLT

Source: Credit Suisse HOLT

08 July 2015

ESG: The Family Business Model 20

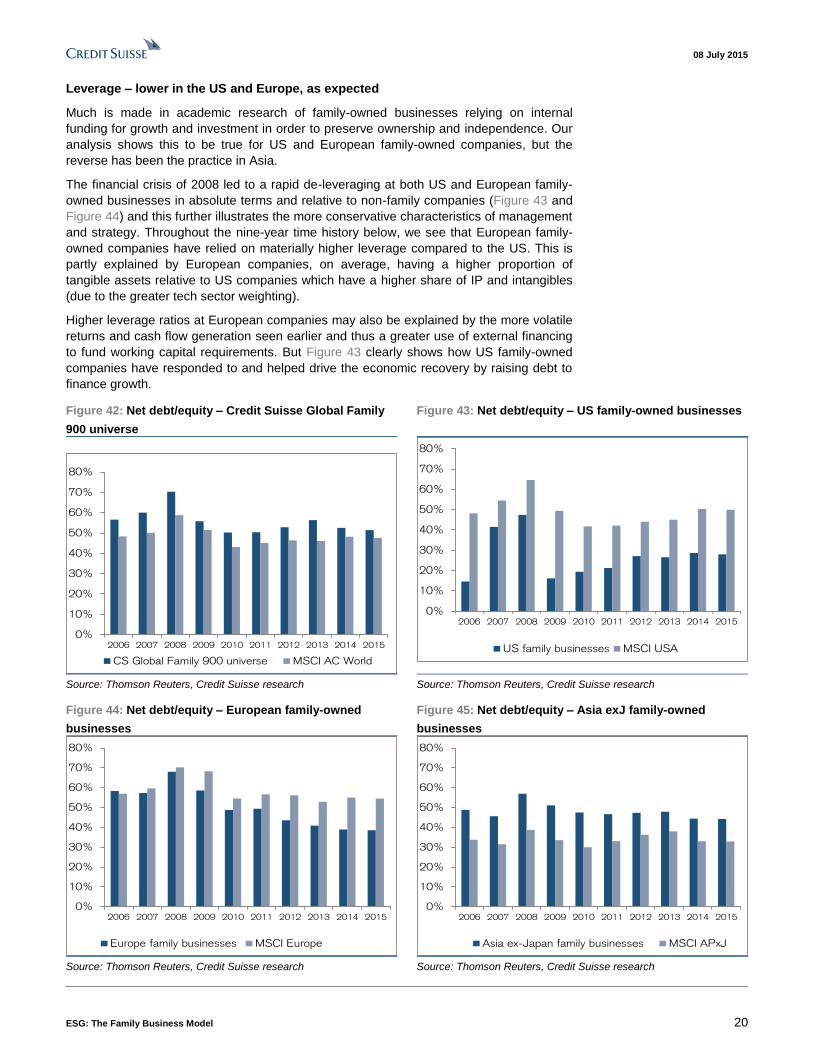

Leverage – lower in the US and Europe, as expected

Much is made in academic research of family-owned businesses relying on internal

funding for growth and investment in order to preserve ownership and independence. Our

analysis shows this to be true for US and European family-owned companies, but the

reverse has been the practice in Asia.

The financial crisis of 2008 led to a rapid de-leveraging at both US and European family-

owned businesses in absolute terms and relative to non-family companies (Figure 43 and

Figure 44) and this further illustrates the more conservative characteristics of management

and strategy. Throughout the nine-year time history below, we see that European family-

owned companies have relied on materially higher leverage compared to the US. This is

partly explained by European companies, on average, having a higher proportion of

tangible assets relative to US companies which have a higher share of IP and intangibles

(due to the greater tech sector weighting).

Higher leverage ratios at European companies may also be explained by the more volatile

returns and cash flow generation seen earlier and thus a greater use of external financing

to fund working capital requirements. But Figure 43 clearly shows how US family-owned

companies have responded to and helped drive the economic recovery by raising debt to

finance growth.

Figure 42: Net debt/equity – Credit Suisse Global Family

900 universe

Figure 43: Net debt/equity – US family-owned businesses

0%

10%

20%

30%

40%

50%

60%

70%

80%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

CS Global Family 900 universe MSCI AC World

0%

10%

20%

30%

40%

50%

60%

70%

80%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

US family businesses MSCI USA

Source: Thomson Reuters, Credit Suisse research Source: Thomson Reuters, Credit Suisse research

Figure 44: Net debt/equity – European family-owned

businesses

Figure 45: Net debt/equity – Asia exJ family-owned

businesses

0%

10%

20%

30%

40%

50%

60%

70%

80%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Europe family businesses MSCI Europe

0%

10%

20%

30%

40%

50%

60%

70%

80%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Asia ex-Japan family businesses MSCI APxJ

Source: Thomson Reuters, Credit Suisse research Source: Thomson Reuters, Credit Suisse research

08 July 2015

ESG: The Family Business Model 21

We see higher leverage in Asia vs benchmark (Figure 45). There are three likely reasons

in our view. Firstly, the companies are relatively young in the region, so founders are still

trying to maintain control and fund growth rather than risk dilution. Secondly, as we see in

Figure 95 above, the companies are smaller in terms of market cap and may not have

required as much funding for growth. And thirdly, founders may not have had access to

savings, capital provided by family networks or other means. We note that many Chinese

companies have resorted to more VC funding as we have mentioned above.

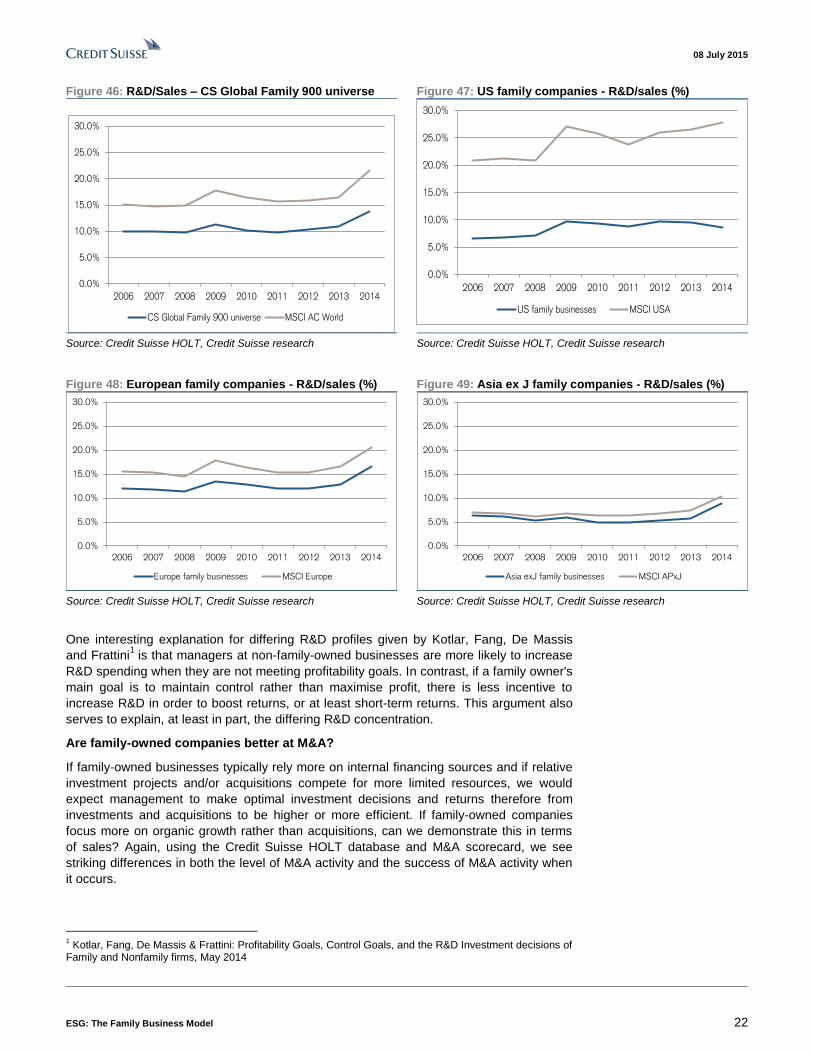

R&D intensity

Academic research findings are equivocal as to whether family businesses show greater

R&D intensity, or whether they are more conservative in their spending on R&D given

more limited access to or use of external financing. The desire to protect independence

and the status quo perhaps exacerbates the trade-off between R&D and investments and

cash flow available for dividends.

Our findings are unequivocal. Using the Credit Suisse HOLT database, we find that family-

owned business investment in R&D, as measured by capitalised R&D/sales, has averaged

5-6% below the R&D intensity of the MSCI ACWI Index, i.e. it is 30% lower in absolute

terms. On a sector adjusted basis, it was 17% below in 2014. Figure 46 shows that this

spread has in fact widened since the 2008 financial crisis, underpinning the argument of a

more conservative style of management with a slower pick-up in R&D commitment by

family businesses in the aftermath of the crisis and mirroring the de-leveraging discussed

above.

Our analysis also shows that this lower R&D intensity at family companies is characteristic

of all regions. Since 2006, we see average R&D/sales running at 5-10% in both the US

and Asia-ex-Japan with Asian levels closely tracking benchmark levels, just 120bps

differential on average since 2006, a reflection of the heavy weighting of family-owned

companies in Asia generally. However, we see a far greater variation in the US which,

although R&D/sales again ranges between 5-10%, is a very significant 16% of sales lower

than benchmark. In other words, R&D intensity at US family companies is effectively just a

quarter of benchmark levels. Figure 20 illustrates that these same companies generate

return on equity that was an average of 250bps lower during the period 2006-2014. The

discrepancy between R&D investment levels and returns would suggest that US family

businesses are far more efficient in their R&D choices and priorities in our view rather than

this differential simply being a reflection of conservative management.

For Europe, we observe much higher levels of R&D by family companies in Figure 48 with

an average of 12.8% of sales over the past 9 years, although this is still close to 4% below

benchmark. As a percentage of sales, however, this is more than double the level of US

family-owned companies. Different sector exposure is at least part of the explanation given

the much higher weighting of healthcare companies amongst our European family-owned

business universe compared to the US. The healthcare sector generally shows double the

capitalised R&D ratio compared to technology and three times that of consumer

discretionaries.

08 July 2015

ESG: The Family Business Model 22

Figure 46: R&D/Sales – CS Global Family 900 universe Figure 47: US family companies - R&D/sales (%)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2006 2007 2008 2009 2010 2011 2012 2013 2014

CS Global Family 900 universe MSCI AC World

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2006 2007 2008 2009 2010 2011 2012 2013 2014

US family businesses MSCI USA

Source: Credit Suisse HOLT, Credit Suisse research Source: Credit Suisse HOLT, Credit Suisse research

Figure 48: European family companies - R&D/sales (%) Figure 49: Asia ex J family companies - R&D/sales (%)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2006 2007 2008 2009 2010 2011 2012 2013 2014

Europe family businesses MSCI Europe

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2006 2007 2008 2009 2010 2011 2012 2013 2014

Asia exJ family businesses MSCI APxJ

Source: Credit Suisse HOLT, Credit Suisse research Source: Credit Suisse HOLT, Credit Suisse research

One interesting explanation for differing R&D profiles given by Kotlar, Fang, De Massis

and Frattini1 is that managers at non-family-owned businesses are more likely to increase

R&D spending when they are not meeting profitability goals. In contrast, if a family owner's

main goal is to maintain control rather than maximise profit, there is less incentive to

increase R&D in order to boost returns, or at least short-term returns. This argument also

serves to explain, at least in part, the differing R&D concentration.

Are family-owned companies better at M&A?

If family-owned businesses typically rely more on internal financing sources and if relative

investment projects and/or acquisitions compete for more limited resources, we would

expect management to make optimal investment decisions and returns therefore from

investments and acquisitions to be higher or more efficient. If family-owned companies

focus more on organic growth rather than acquisitions, can we demonstrate this in terms

of sales? Again, using the Credit Suisse HOLT database and M&A scorecard, we see

striking differences in both the level of M&A activity and the success of M&A activity when

it occurs.

1 Kotlar, Fang, De Massis & Frattini: Profitability Goals, Control Goals, and the R&D Investment decisions of

Family and Nonfamily firms, May 2014

08 July 2015

ESG: The Family Business Model 23

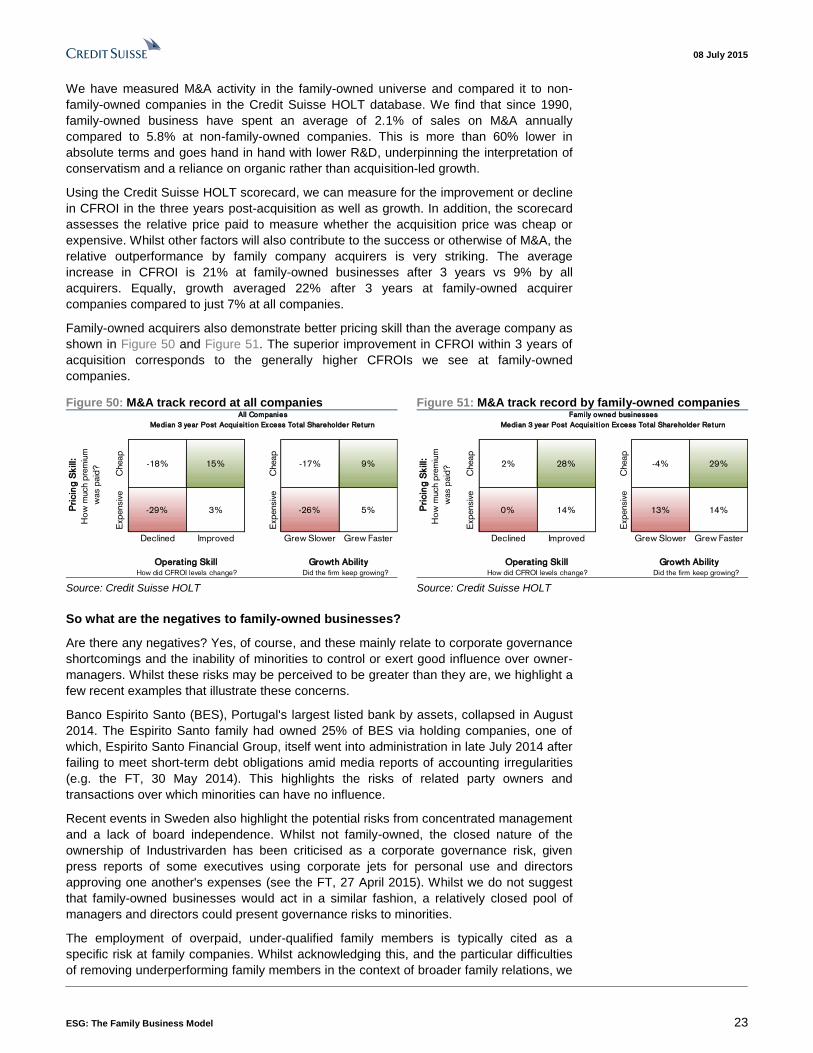

We have measured M&A activity in the family-owned universe and compared it to non-

family-owned companies in the Credit Suisse HOLT database. We find that since 1990,

family-owned business have spent an average of 2.1% of sales on M&A annually

compared to 5.8% at non-family-owned companies. This is more than 60% lower in

absolute terms and goes hand in hand with lower R&D, underpinning the interpretation of

conservatism and a reliance on organic rather than acquisition-led growth.

Using the Credit Suisse HOLT scorecard, we can measure for the improvement or decline

in CFROI in the three years post-acquisition as well as growth. In addition, the scorecard

assesses the relative price paid to measure whether the acquisition price was cheap or

expensive. Whilst other factors will also contribute to the success or otherwise of M&A, the

relative outperformance by family company acquirers is very striking. The average

increase in CFROI is 21% at family-owned businesses after 3 years vs 9% by all

acquirers. Equally, growth averaged 22% after 3 years at family-owned acquirer

companies compared to just 7% at all companies.

Family-owned acquirers also demonstrate better pricing skill than the average company as

shown in Figure 50 and Figure 51. The superior improvement in CFROI within 3 years of

acquisition corresponds to the generally higher CFROIs we see at family-owned

companies.

Figure 50: M&A track record at all companies Figure 51: M&A track record by family-owned companies

Cheap

-18% 15%

Cheap

-17% 9%

Exp

ensiv

e

-29% 3%

Exp

ensiv

e

-26% 5%

Declined Improved Grew Slower Grew Faster

How did CFROI levels change? Did the firm keep growing?

All Companies

Median 3 year Post Acquisi t ion Excess Total Shareholder Return

Pri

cin

g S

kill:

Ho

w m

uch p

rem

ium

was p

aid

?

Operat ing Skill Growth Ability

Cheap

2% 28%

Cheap

-4% 29%E

xpensiv

e

0% 14%

Exp

ensiv

e

13% 14%

Declined Improved Grew Slower Grew Faster

How did CFROI levels change? Did the firm keep growing?

Fami ly owned businesses

Median 3 year Post Acquisi t ion Excess Total Shareholder ReturnP

ric

ing

Sk

ill:

Ho

w m

uch p

rem

ium

was p

aid

?

Operat ing Skill Growth Ability

Source: Credit Suisse HOLT Source: Credit Suisse HOLT

So what are the negatives to family-owned businesses?

Are there any negatives? Yes, of course, and these mainly relate to corporate governance

shortcomings and the inability of minorities to control or exert good influence over owner-

managers. Whilst these risks may be perceived to be greater than they are, we highlight a

few recent examples that illustrate these concerns.

Banco Espirito Santo (BES), Portugal's largest listed bank by assets, collapsed in August

2014. The Espirito Santo family had owned 25% of BES via holding companies, one of

which, Espirito Santo Financial Group, itself went into administration in late July 2014 after

failing to meet short-term debt obligations amid media reports of accounting irregularities

(e.g. the FT, 30 May 2014). This highlights the risks of related party owners and

transactions over which minorities can have no influence.

Recent events in Sweden also highlight the potential risks from concentrated management

and a lack of board independence. Whilst not family-owned, the closed nature of the

ownership of Industrivarden has been criticised as a corporate governance risk, given

press reports of some executives using corporate jets for personal use and directors

approving one another's expenses (see the FT, 27 April 2015). Whilst we do not suggest

that family-owned businesses would act in a similar fashion, a relatively closed pool of

managers and directors could present governance risks to minorities.

The employment of overpaid, under-qualified family members is typically cited as a

specific risk at family companies. Whilst acknowledging this, and the particular difficulties

of removing underperforming family members in the context of broader family relations, we

08 July 2015

ESG: The Family Business Model 24

witness an increasing level of professional education and qualifications amongst later

generations taking over from the founding entrepreneur. These issues are of course more

important when families retain a greater stake in the company.

A number of family-owned companies offer different classes of shares, most typically non-

voting shares to external shareholders. This has been a trend in many tech companies

that have IPOed in recent years enabling founders to sell down whilst securing control

nonetheless. The Renault AGM of April 2015 highlighted the drawbacks of different voting

rights proposals when the French government used the Florange Law to ensure double

voting rights for its 15% stake in the company and secure control. Given that most retail

shares are held in bearer form and it is the larger shareholders and particularly key

shareholders who are named on the register, this law has served to further entrench and

concentrate family control. Most of the family-owned companies in France have double

voting rights now; the most notable exception is L'Oreal, which voted in April 2015 to

maintain one share one vote. The adoption of double voting rights to reward long-term

investors is a clear negative, in our view.

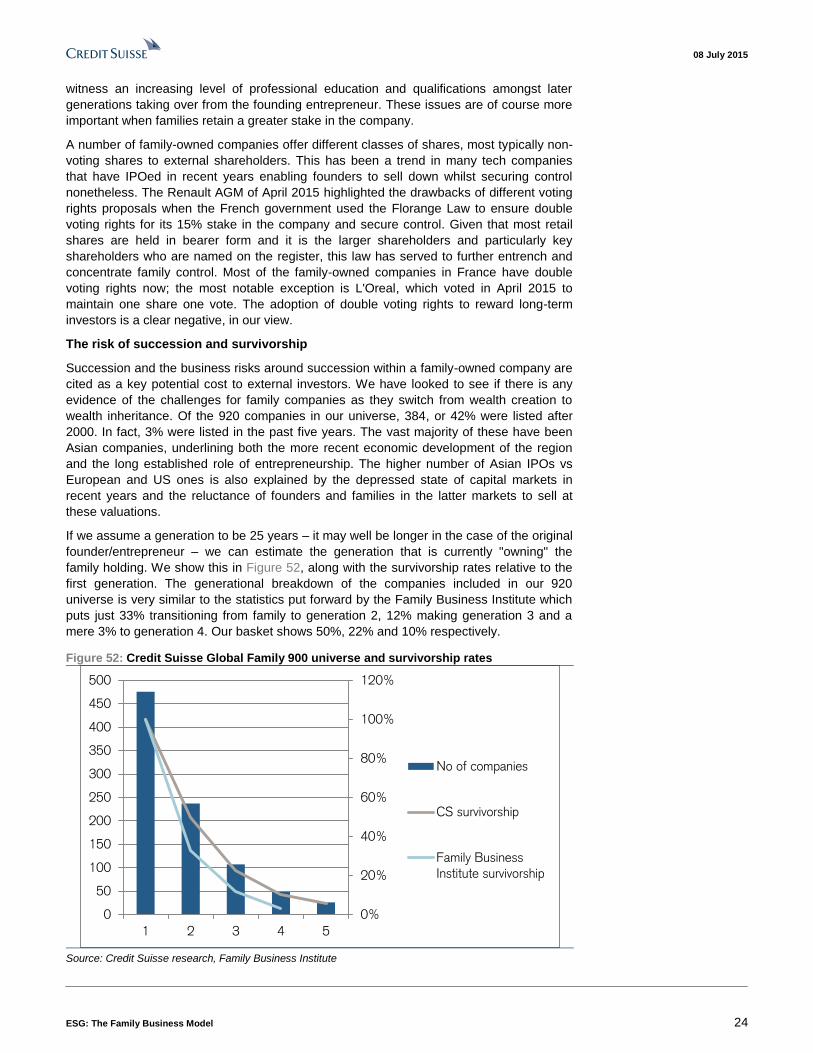

The risk of succession and survivorship

Succession and the business risks around succession within a family-owned company are

cited as a key potential cost to external investors. We have looked to see if there is any

evidence of the challenges for family companies as they switch from wealth creation to

wealth inheritance. Of the 920 companies in our universe, 384, or 42% were listed after

2000. In fact, 3% were listed in the past five years. The vast majority of these have been

Asian companies, underlining both the more recent economic development of the region

and the long established role of entrepreneurship. The higher number of Asian IPOs vs

European and US ones is also explained by the depressed state of capital markets in

recent years and the reluctance of founders and families in the latter markets to sell at

these valuations.

If we assume a generation to be 25 years – it may well be longer in the case of the original

founder/entrepreneur – we can estimate the generation that is currently "owning" the

family holding. We show this in Figure 52, along with the survivorship rates relative to the

first generation. The generational breakdown of the companies included in our 920

universe is very similar to the statistics put forward by the Family Business Institute which

puts just 33% transitioning from family to generation 2, 12% making generation 3 and a

mere 3% to generation 4. Our basket shows 50%, 22% and 10% respectively.

Figure 52: Credit Suisse Global Family 900 universe and survivorship rates

0%

20%

40%

60%

80%

100%

120%

0

50

100

150

200

250

300

350

400

450

500

1 2 3 4 5

No of companies

CS survivorship

Family Business

Institute survivorship

Source: Credit Suisse research, Family Business Institute

08 July 2015

ESG: The Family Business Model 25

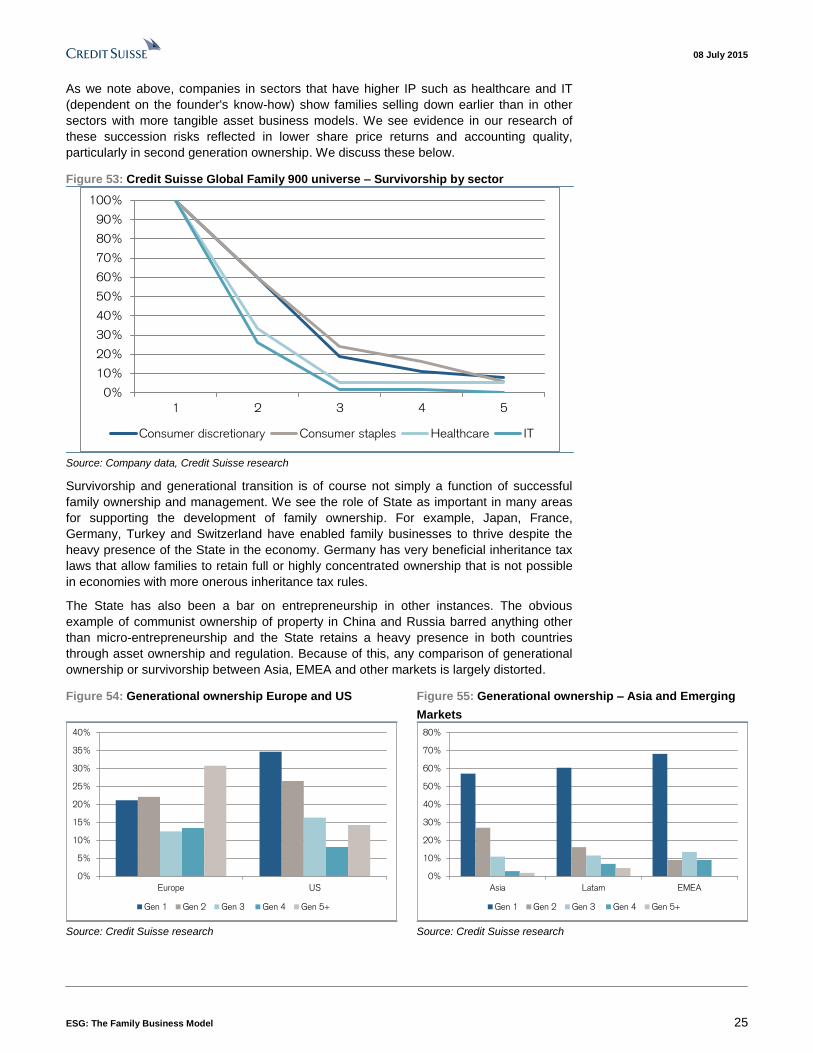

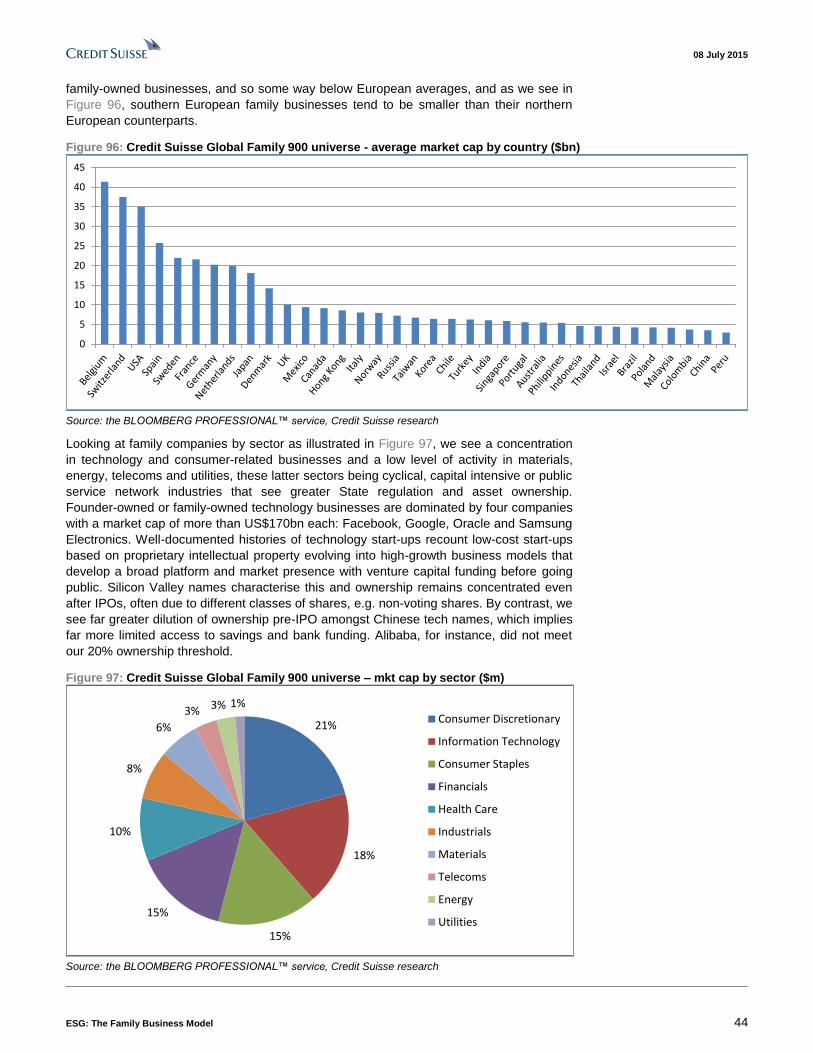

As we note above, companies in sectors that have higher IP such as healthcare and IT

(dependent on the founder's know-how) show families selling down earlier than in other

sectors with more tangible asset business models. We see evidence in our research of

these succession risks reflected in lower share price returns and accounting quality,

particularly in second generation ownership. We discuss these below.

Figure 53: Credit Suisse Global Family 900 universe – Survivorship by sector

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 2 3 4 5

Consumer discretionary Consumer staples Healthcare IT

Source: Company data, Credit Suisse research

Survivorship and generational transition is of course not simply a function of successful

family ownership and management. We see the role of State as important in many areas

for supporting the development of family ownership. For example, Japan, France,

Germany, Turkey and Switzerland have enabled family businesses to thrive despite the

heavy presence of the State in the economy. Germany has very beneficial inheritance tax

laws that allow families to retain full or highly concentrated ownership that is not possible

in economies with more onerous inheritance tax rules.

The State has also been a bar on entrepreneurship in other instances. The obvious

example of communist ownership of property in China and Russia barred anything other

than micro-entrepreneurship and the State retains a heavy presence in both countries

through asset ownership and regulation. Because of this, any comparison of generational

ownership or survivorship between Asia, EMEA and other markets is largely distorted.

Figure 54: Generational ownership Europe and US Figure 55: Generational ownership – Asia and Emerging

Markets

0%

5%

10%

15%

20%

25%

30%

35%

40%

Europe US

Gen 1 Gen 2 Gen 3 Gen 4 Gen 5+

0%

10%

20%

30%

40%

50%

60%

70%

80%

Asia Latam EMEA

Gen 1 Gen 2 Gen 3 Gen 4 Gen 5+

Source: Credit Suisse research Source: Credit Suisse research

08 July 2015

ESG: The Family Business Model 26

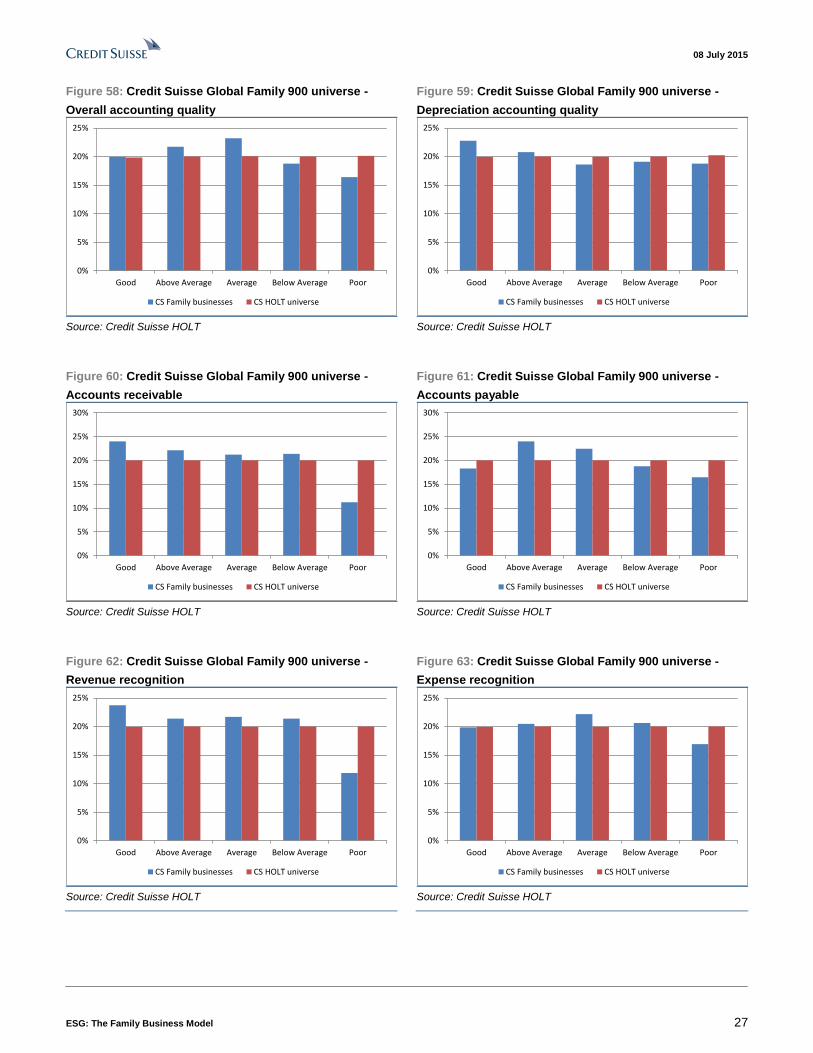

Accounting quality is in fact superior

In addition to MSCI ESG rankings, we are able to look at proprietary indicators using

Credit Suisse HOLT as an alternative proxy for corporate governance and assess the real

risks of family owners' interests vs outside shareholders. Using Credit Suisse HOLT's

accounting analysis, we have found no evidence of potential agency costs or actual

discrepancies in accounting practice that are to the detriment of minorities. In fact,

accounting quality (Figure 58) at family-owned businesses is generally superior to the

overall Credit Suisse HOLT universe with 67% of the companies ranking average or above

compared to the 60% within Credit Suisse HOLT (the companies being ranked into

quintiles).

When we consider more detailed accounting metrics, we also see this superior practice at

family-owned companies. Accounts receivable show 67% of these companies rank

average or above along with 64% on accounts payable. This might also suggest better

working capital management. Similarly, we see 65% of family-owned companies ranked

as average or above on revenue recognition and 62% for expense recognition implying

good transparency and reliability of financial statements. From this accounting point of

view, we believe that some of the perceived corporate governance risks may be

overstated and that there is a better alignment of interests by family and minority owners

than may be generally perceived.

Diversity

Further to our Credit Suisse Gender 3000: Women in Senior Management report of

September 2014, we look to see whether family-owned companies have higher levels of

diversity as academic research suggests. We find very interesting results that demonstrate

clearly higher levels of female representation on boards of directors and in senior

management at family-owned companies in the US and Asia. By contrast, we see fewer

female board directors in Europe which shows both the slower response of family

companies to the mandated quotas and targets in place and perhaps the lack of female

family members available to fill these positions. In Latin America, diversity is worse in

family companies in both the boardroom and management and highlights the cultural

drivers of diversity that we discussed in the Credit Suisse Gender 3000 report.

Figure 56: Diversity at family-owned companies

BOARDS Senior mgmt

2010 2011 2012 2013 2013

North America 15.4% 16.0% 16.8% 18.2% 16.2%

Europe 12.1% 14.0% 16.6% 19.4% 15.0%

Developed Asia 7.4% 7.9% 8.6% 9.0% 13.2%

Emerging Asia 7.6% 8.0% 8.0% 8.8% 15.4%

Latin America 6.0% 6.0% 5.6% 5.0% 5.9%

EMEA 13.1% 12.6% 11.8% 12.6% 10.9%

Total 9.0% 9.7% 10.2% 11.2% 13.8%

Source: Company data, Credit Suisse research

Figure 57: Difference vs Credit Suisse Gender 3000

BOARDS Senior mgmt

2010 2011 2012 2013 2013

North America 2.7% 3.1% 3.3% 4.2% 1.2%

Europe -1.4% -0.9% -1.1% -1.2% 0.3%

Developed Asia 1.9% 1.5% 1.6% 1.2% 0.6%

Emerging Asia 1.4% 1.5% 1.1% 0.8% 5.0%

Latin America 0.2% -0.3% -0.2% -1.2% -3.2%

EMEA 5.8% 5.3% 4.2% 4.4% -0.5%

Total -0.6% -0.6% -1.1% -1.5% 0.9%

Source: Company data, Credit Suisse estimates

08 July 2015

ESG: The Family Business Model 27

Figure 58: Credit Suisse Global Family 900 universe -

Overall accounting quality

Figure 59: Credit Suisse Global Family 900 universe -

Depreciation accounting quality

0%

5%

10%

15%

20%

25%

Good Above Average Average Below Average Poor

CS Family businesses CS HOLT universe

0%

5%

10%

15%

20%

25%

Good Above Average Average Below Average Poor

CS Family businesses CS HOLT universe

Source: Credit Suisse HOLT Source: Credit Suisse HOLT

Figure 60: Credit Suisse Global Family 900 universe -

Accounts receivable

Figure 61: Credit Suisse Global Family 900 universe -

Accounts payable

0%

5%

10%

15%

20%

25%

30%

Good Above Average Average Below Average Poor

CS Family businesses CS HOLT universe

0%

5%

10%

15%

20%

25%

30%

Good Above Average Average Below Average Poor

CS Family businesses CS HOLT universe

Source: Credit Suisse HOLT Source: Credit Suisse HOLT

Figure 62: Credit Suisse Global Family 900 universe -

Revenue recognition

Figure 63: Credit Suisse Global Family 900 universe -

Expense recognition

0%

5%

10%

15%

20%

25%

Good Above Average Average Below Average Poor

CS Family businesses CS HOLT universe

0%

5%

10%

15%

20%

25%

Good Above Average Average Below Average Poor

CS Family businesses CS HOLT universe

Source: Credit Suisse HOLT Source: Credit Suisse HOLT

08 July 2015

ESG: The Family Business Model 28

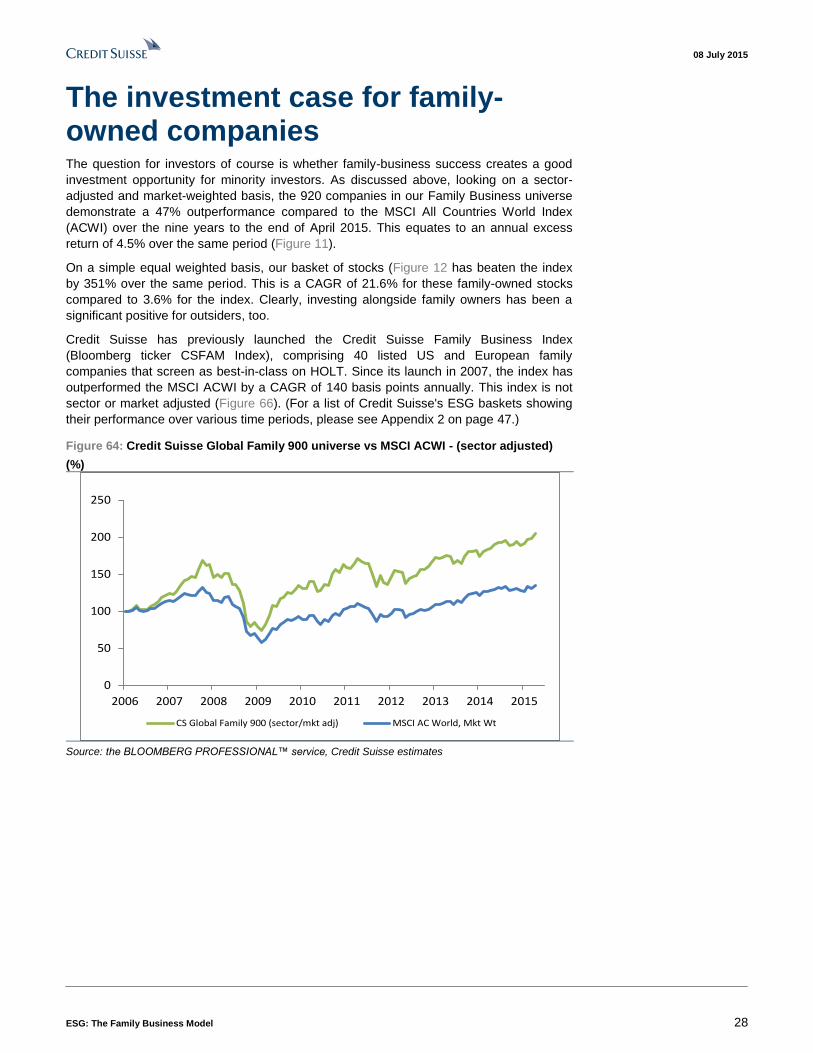

The investment case for family-owned companies The question for investors of course is whether family-business success creates a good

investment opportunity for minority investors. As discussed above, looking on a sector-

adjusted and market-weighted basis, the 920 companies in our Family Business universe

demonstrate a 47% outperformance compared to the MSCI All Countries World Index

(ACWI) over the nine years to the end of April 2015. This equates to an annual excess

return of 4.5% over the same period (Figure 11).

On a simple equal weighted basis, our basket of stocks (Figure 12 has beaten the index

by 351% over the same period. This is a CAGR of 21.6% for these family-owned stocks

compared to 3.6% for the index. Clearly, investing alongside family owners has been a

significant positive for outsiders, too.

Credit Suisse has previously launched the Credit Suisse Family Business Index

(Bloomberg ticker CSFAM Index), comprising 40 listed US and European family

companies that screen as best-in-class on HOLT. Since its launch in 2007, the index has

outperformed the MSCI ACWI by a CAGR of 140 basis points annually. This index is not

sector or market adjusted (Figure 66). (For a list of Credit Suisse's ESG baskets showing

their performance over various time periods, please see Appendix 2 on page 47.)

Figure 64: Credit Suisse Global Family 900 universe vs MSCI ACWI - (sector adjusted)

(%)

0

50

100

150

200

250

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

CS Global Family 900 (sector/mkt adj) MSCI AC World, Mkt Wt

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse estimates

08 July 2015

ESG: The Family Business Model 29