- 1 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Estates Content of Business Cases

This document is intended to update NHS Trusts and Local Health Boards in Wales on the requirements of the Welsh Assembly Government for supporting documentation outlining the estates content of Capital schemes in Strategic Outline, Outline and Full Business Cases. This information is complementary to the Five Case Model and would be required to produce any robust Business Case. Some of the documentation has been produced to line up the requirements of the Business Case process with the Designed for Life: Building for Wales construction procurement initiative. These documents must be used for all major Capital Projects where the total Capital Cost exceeds £5 million. Estates Component Annex Many Business Cases in recent years have failed to provide sufficient information on the current estate and the proposed scheme. In future it is a requirement that all Business Cases contain an Annex which provides the fundamental estates information to inform and assist the Business Case scrutiny process. Annexure A to this document includes three outlines of the minimum information required to be included in Strategic Outline, Outline and Full Business Cases. Provision of this information will assist a speedy scrutiny of the Business Case. Revised Cost Forms Revised Cost Forms for Strategic Outline, Outline and Full Business Cases have been produced and are attached as Annexure B. Quantified Risk DoH guidance states that ‘Quantified risk analysis’ refers to the work undertaken in business cases to obtain the expected value of risks in monetary terms. This is through the development of a risk register and for each individual risk the estimation of impact values and probabilities of occurrence. “Quantified risk” can be separated into two elements:

Quantified Trust managed risk Quantified Supply Chain Partner (SCP) managed risk.

Quantified risks should be recorded in a project specific Risk Register. A typical example is attached as Annexure C. The register has been populated with a starting list of risks that have been identified on previous major projects and may be applicable on other schemes. NHS Trusts and SCPs should use the list as a checklist only and develop a project specific register for the intended scheme. Once a specific risk has been identified it should be recorded in the Risk Register. Only one Risk Register should exist for the project but the data should be sorted into various configurations to suit specific purposes, e.g. by Risk Owner, by Risk Type, etc.

- 2 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

The potential impact of each risk and the likelihood of occurrence should be determined and the effect on these of putting in mitigating elements should follow. If the impact or chance of occurrence can be influenced by mitigation, then if it is agreed to put in place the mitigation, the cost consequence of the mitigation should be taken into account in the Risk Register and the cost of mitigation added to the project base cost. The Risk Register therefore covers the chance that the risk will still occur with either a reduced likelihood or potential impact or both. The Quantified Supply Chain Partner’s managed risk identified in the Target Cost will be used in the eventual calculation of the Pain/Gain share. Risks should be fairly borne and NHS Trusts should give due consideration to their risk exposure balanced against the financial consequences of passing unfair or unreasonable risks onto the SCP. No risks should be shared. NHS Trusts in Wales shall confirm in writing at the commencement of FBC the cost figure they expect the SCP to progress the design and construction of the scheme. It will normally be the approved OBC Works Cost (line 5 on Cost Form OBC1) with the addition of the SCPs Fees and the SCPs Quantified Risk. Inflation Fixed Price Contracts (less than 24 months) Strategic Outline (SOC) and Outline Business Case (OBC) costs are compiled on the basis of Departmental Cost Allowances and On-costs and are related to a MIPS index level (currently 455). For Fixed Price Contracts, projected inflation costs to project completion will need to be calculated and provided to and agreed with Welsh Health Estates. These costs should be compiled by Trust Cost Advisors (TCAs) at SOC stage and by Supply Chain Partners (SCPs) in collaboration with the TCA at OBC and FBC stages and shall be agreed with Welsh Health Estates prior to submission of the Business Case. After OBC the method of cost compilation changes to an elemental cost plan arrangement which ultimately becomes the Target Cost. This cost plan should contain an item to cover inflation through the construction period to completion. This should be based on the figure agreed with Welsh Health Estates. Once the Target Cost is agreed no further adjustment will be made for inflation. The Target Cost would be based on costs to completion. Valuations are subsequently based on actual costs with reconciliation between Target Cost and Actual Cost at the end determining the gain/pain share. Variation of Price Contracts (greater than 24 months) Strategic Outline (SOC) and Outline Business Case (OBC) costs are compiled on the basis of Departmental Cost Allowances and On-costs and are related to a MIPS index level (currently 445). For Variation of Price Contracts, projected inflation costs to project completion will need to be calculated and and provided to and agreed with Welsh Health Estates. These costs should be compiled by Trust Cost Advisors (TCAs) at SOC stage and by Supply Chain Partners (SCPs) in

- 3 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

collaboration with the TCA at OBC and FBC stages and shall be agreed with Welsh Health Estates prior to submission of the Business Case. After OBC the method of cost compilation changes to an elemental cost plan arrangement which ultimately becomes the Target Cost. The Target Cost allows for inflation up to the submission of the Full Business Case and will be adjusted monthly during the construction phase in accordance with the contract requirements for construction inflation to “keep pace” with actual cost and allow the calculation of “the preliminary assessment of the Contractor’s share” at project completion. The Target Cost inflation assessment would then be adjusted when the published firm indices have been issued and “the final assessment of the Contractor’s share” made. During the project valuations are based on actual costs. Rules for payment of project sponsorship costs Project sponsorship costs are internal NHS Trust costs that are necessary to initiate, develop and complete a capital project. One of the key success factors for a capital project is the management and resources input by the NHS Trust to identify their requirements and respond to the needs of the Supply Chain in progressing the project to programme. These costs would not exist if there were no capital project. Project sponsorship costs must be capital costs. The NHS Capital Accounting manual states: “The costs of an NHS body’s capital projects department may only be allocated to individual capital schemes where it can be demonstrated that these costs relate to the production of a capital asset (and not its management or maintenance), and that the basis of apportionment is reasonable” The WAG accepts the need to fund the internal resources necessary to enable the NHS Trust to progress and support the capital project with the following conditions:

There is no scheme until the Strategic Outline Case has been approved by the Capital Investment Board. Trusts should therefore be aware that if a project does not progress after SOC any costs attributable to the capital project must be written off as a revenue item.

Project sponsorship funding can only be drawn down after approval of the SOC.

The Project sponsorship team must be a distinct unit. Staff can be specifically recruited or be

transferred or seconded into the unit from other departments. Only the costs associated with staff who are not currently employed by the NHS Trust or whose post will require “backfilling” during their transfer or secondment period will be allowed. Once the capital project is completed funding will cease and these staff will either be redeployed or return to their original departments or come to the end of their contractual employment and move on to other projects either within the NHS Trust or elsewhere.

Pre-OBC an organisational structure chart identifying the proposed internal project structure

must be provided by the Trust to the Capital, Estates and Facilities Branch together with a costed resource schedule spanning the whole project duration. This chart and schedule should be refreshed and updated at OBC and FBC submission stages.

- 4 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Programme guidance The Business Case Cost Forms all include a section at the end for NHS Trusts and LHBs to identify their key programme dates. These will be used by the Welsh Assembly Government to inform the ongoing Capital Programme planning process and identify future funding requirements and priorities. It is vital that realistic programmes are submitted and kept to as failure to meet a submission date may result in projects missing their funding slot and others taking up that funding. To assist NHS Trusts and LHBs in planning major Capital Projects tables of typical project durations for new build and refurbishment schemes is attached as Annexure D. These durations allow reasonable periods for the delivery of each phase. However refurbishment projects need to be adjusted to take account of the number of phases, the extent and sequencing of works and the presence of materials such as asbestos which can significantly affect programme. Value Added Tax The Outline and Full Business Cases should include a statement indicating the status of the project with HM Revenue and Customs (HMRC), the identity of the Trust VAT advisor and an outline of the proposed VAT Recovery Strategy. The VAT costs identified on the Capital Cost forms should reflect the implications of the proposed VAT Recovery Strategy. Whole Life Costing Annexure E includes for use at FBC stage a suggested process for the application of Whole Life Costing on major Capital Projects as well as typical proforma that would assist the process. Further work will be done over the next twelve months or so to rationalise the process within the NHS in Wales. Queries Any queries on the contents of this guidance should be directed to Patrick Riordan, Welsh Health Estates, telephone 02920 315545; e-mail: [email protected] Electronic copies of the forms, in Excel format, are available on the Welsh Health Estates website www.wales.nhs.uk/whe and Designed for Life : Building for Wales extranet.

- 5 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

ANNEXURE A

Content of a SOC Estate Component Annex

Executive Summary Estates Investment Objectives Summary of Trust Estates Strategy

The Existing Estate

o Existing Estate Site Plans

Current Estate Performance

o Functional Suitability o Space Utilisation o Statutory Compliance o Physical Condition o Energy Performance o Backlog Maintenance Liability

Estate Performance Improvement Targets

Schedule of Proposed Functional Content Proposed Project Estate Options Capital Costs and projected cashflows (See SOC1- 4 forms) Inflation calculations Initial Assessments of Estate and Facilities Revenue Implications

- 6 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Content of an OBC Estate Component Annex Executive Summary of the Estate implications of the Business Case Estates Investment Objectives Summary of Trust Estates Strategy

The Existing Estate

o Existing Estate Site Plans

Current Estate Performance (identifying data collection date)

Estate Performance Improvement Targets

Proposes Changes to the Estate

Capital Investment Programme

Land and Property Disposal and Acquisition Programme Proposed Project Estate Options (minimum 1:500 scale) Preferred Option Development Control Plan (minimum 1:200 scale) Project Design Principles Project Details Site ownership status Planning Permission Status Quality Assurance and Standards Compliance

AEDET NEAT

Statement of Sustainable Development Commitment Capital Costs and projected cashflows (See OBC1- 8 forms) Inflation calculations Whole Life Cycle Cost Assessments VAT Recovery Strategy

- 7 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Assessments of Estate and Facilities Revenue Implications compared with the base option

Capital Charges Energy Rates Rent Water and sewage Maintenance Security Cleaning Linen and laundry Car Parking Waste disposal Photocopying Telecommunications Portering Postal Services Commissioning De-commissioning

Comparison and reconciliation of functional content and capital costs with SOC

- 8 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Content of an FBC Estate Component Annex Executive Summary of the Estate implications of the Business Case Estates Investment Objectives Summary of Trust Estates Strategy

The Existing Estate

o Existing Estate Site Plans

Current Estate Performance

Estate Performance Improvement Targets

Proposes Changes to the Estate

Capital Investment Programme

Land and Property Disposal and Acquisition Programme Proposed Project Estate Options (minimum 1:500 scale) Preferred Option Development Control Plan (minimum 1:200 scale) Project Design Principles Preferred Option Project Details

Gross floor area analysis Site Plan Floor Plans (minimum 1:200 scale) Elevations Outline Specification Fire Strategy M&E Design Intent

Site acquisition status Planning Permission Status Statement of Sustainable Development Commitment Quality Assurance and Standards Compliance

AEDET NEAT

Capital Costs and projected cashflows (See FBC1- 8 forms)

- 9 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Inflation calculations Whole Life Cycle Cost Assessments VAT Recovery Strategy Assessments of Estate and Facilities Revenue Implications compared with the base option

Capital Charges Energy Rates Rent Water and sewage Maintenance Security Cleaning Linen and laundry Car Parking Waste disposal Photocopying Telecommunications Portering Postal Services Commissioning De-commissioning

Comparison and reconciliation of functional content and capital costs with OBC

- 10 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

ANNEXURE B Notes on completion of Strategic Outline Case Cost Forms 1. Department Costs should be based on Departmental Cost Allowances (DCAs) where

appropriate and include allowances for essential complimentary accommodation and optional

accommodation and services where details are not available.

2. If Departmental Cost Allowances are not available state the area and rate per m2 used.

3. On-costs must be based on a project specific assessment.

4. The provisional location adjustment alters the average DCA price levels and on-costs for

local market conditions. Refer to the Department of Health: Estates and Facilities Division:

Quarterly Briefing for the latest factor.

5. Fees should include all resource costs associated with the scheme e.g. project sponsorship,

supervisors etc.

6. Note the VAT figures included on Cost Form SOC1 should be those after adjustment for any

reclaimable VAT e.g. VAT on professional fees is normally 100% reclaimable.

7. Non-works costs should include such items as contributions to statutory and local

authorities; building regulations and planning fees; land costs and associated legal fees.

8. If Equipment Costs are to include transferred equipment an assessed abatement

percentage should be identified.

9. Inflation forecasts should be made by the NHS Trust submitting the Business Case and be

agreed with Welsh Health Estates prior to submission of the Business Case.

10. Firm and Variation of Price contracts should allow for projected inflation adjustments up to

and including the date of submission of the Full Business Case together with an assessment of

inflation during the construction period to completion. Equipment cost inflation should also

be included.

- 11 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Insert in Cost Form SOC2 the following categories against each Department:

a. N for new build,

b. A for adaptations for alternative use or

c. C for upgrading existing building retaining current use.

- 12 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Notes on completion of Outline Business Case Cost Forms 1. Department Costs should be based on Departmental Cost Allowances where appropriate

and include allowances for essential complimentary accommodation and optional

accommodation and services where details are not available.

2. Identify separately any proposed adjustment (over or under cost allowances) justifiable in

value for money terms (details to be provided).

3. If Departmental Cost Allowances are not available state the area and rate per m2 used.

4. The provisional location adjustment alters the average DCA price levels and on-costs for

local market conditions. Refer to the Department of Health: Estates and Facilities Division:

Quarterly Briefing for the latest factor.

5. On-costs must be based on project specific assessments/measurements with sufficient

information provided to define the scope of works.

6. In Cost Form OB3 the term “External” refers to the elements external to the department(s)

not just external to the building.

7. Any enabling or preliminary works to prepare the site in advance, for example demolitions;

service diversions; site investigation and other exploratory works, should be identified on

Cost Form OB3 item 5c. Any proposed additional capital expenditure justifiable in terms of

value for money terms should also be identified under this item.

8. Fees should include all resource costs associated with the scheme e.g. project sponsorship,

supervisors etc.

9. Note the VAT figures included on Cost Form OB1 should be those after adjustment for any

reclaimable VAT e.g. VAT on professional fees is normally 100% reclaimable.

10. Non-works costs should be supported by a breakdown and include such items as

contributions to statutory and local authorities; building regulations and planning fees; land

costs and associated legal fees.

11. If Equipment Costs are abated for transferred equipment details should be provided.

12. Inflation forecasts should be made by the NHS Trust submitting the Business Case and be

agreed with Welsh Health Estates prior to submission of the Business Case.

13. Firm and Variation of Price contracts should allow for projected inflation adjustments up to

and including the date of submission of the Full Business Case together with an assessment of

inflation during the construction period to completion. Equipment cost inflation should also

be included.

- 13 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

14. Insert in Cost Form OB2 the following categories against each Department:

a. N for new build,

b. A for adaptations for alternative use or

c. C for upgrading existing building retaining current use.

- 14 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Notes on completion of Full Business Case Cost Forms 1. Cost Form FBC 1 should be completed by the NHS Trust in collaboration with the Trust

Cost Advisor.

2. Cost Form FBC 2 should be completed by the NHS Trust in collaboration with the Trust

Cost Advisor

3. Cost Forms FBC 3, 4/*and 5 should be completed by the Supply Chain Partner.

4. Cost Forms FBC 6,7,8 and 9 should be completed by the NHS Trust in collaboration with

the Trust Cost Advisor and Supply Chain Partner.

5. Fees should include all resource costs associated with the scheme including expenditure to

date.

6. Note the VAT figures should be those after adjustment for any reclaimable VAT e.g. VAT on

professional fees is normally 100% reclaimable.

7. Non-works costs should be supported by a detailed breakdown of sub-elements.

8. Equipment Costs should be based on costed schedules and take account of any transferred

equipment.

9. Inflation forecasts should be made by the NHS Trust submitting the Business Case and be

agreed with Welsh Health Estates prior to submitting the Business Case.

10. Firm and Variation of Price contracts should allow for projected inflation adjustments up to

and including the date of submission of the Full Business Case together with an assessment of

inflation during the construction period to completion. Equipment cost inflation should also

be included.

- 15 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

ANNEXURE C

Designed for Life: Building for Wales

Notes on completion of Project Risk Register

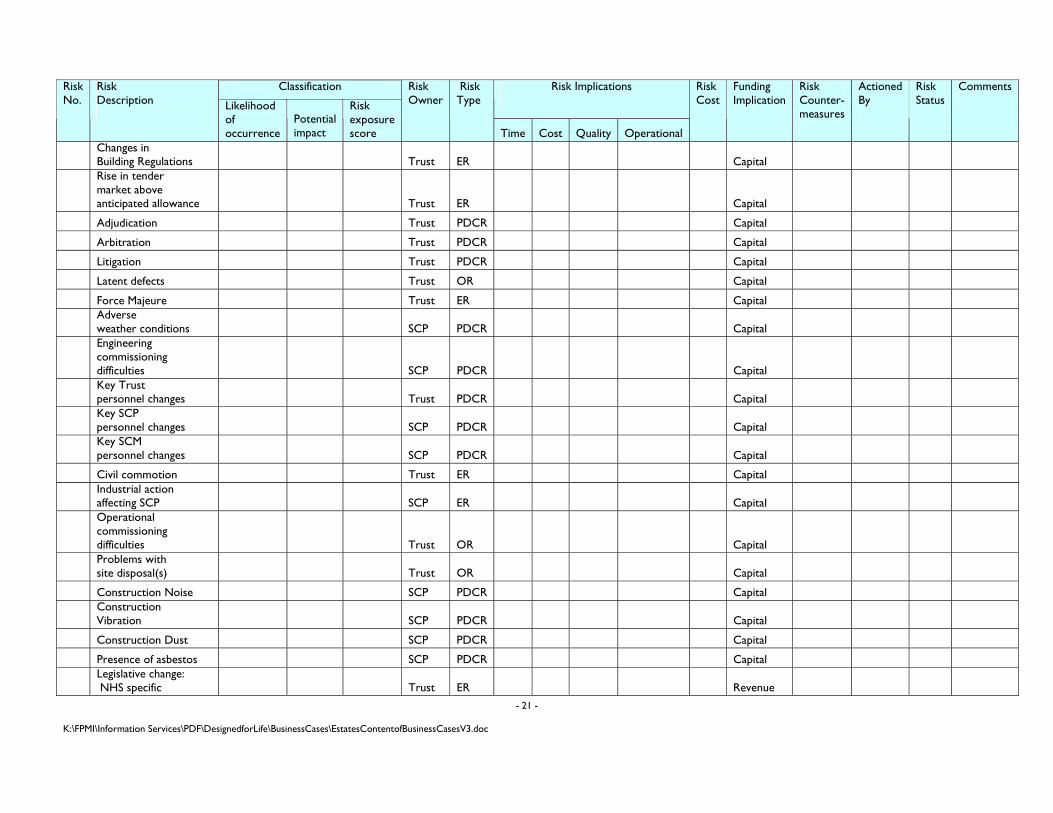

The standard format for the project risk register is attached as Annex A. The owner of the overall project risk register is the Trust appointed Project Manager who will collate and co-ordinate inputs from both the NHS Trust and the Supply Chain Partner (SCP). This format has been agreed with IPAG and is to be used on all projects within the Designed for Life: Building for Wales framework. The project risk register should be reviewed and updated regularly by the whole project team. It should be regarded as a key project control document and should be an agenda item at every project team meeting. The register has been populated with a starting list of risks that have been identified on previous major projects and may be applicable on other schemes. NHS Trusts and SCPs should use the list as a checklist only and develop a project specific register for the intended scheme. Each version of the Risk Register should be given a version number, identify when it was last reviewed and identify the author/collator of the document. Notes are included below to assist in the completion of the Register. The headings match the column headings of the standard format. Risk Number Each risk should be given a unique number which must not be changed during the life of the project. Even if a risk is cleared the number should be retained on the Register. This will allow the history of each risk to be traced by comparison of various versions of the Risk register. Risk Description Each risk should be described briefly. Classification There are two variables of risk – likelihood and impact(consequence). The product of both identifies the seriousness of the risk exposure.

- 16 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Likelihood of occurrence There are 5 categories of likelihood of exposure:

Rare Will occur only in exceptional circumstances

Unlikely Unlikely to occur Possible Reasonable chance of occurring/

may occur occasionally. Likely Likely to occur Almost certain More likely to occur than not

Potential impact There are 5 categories of impact of exposure:

Insignificant No risk to the project. No impact on services. No impact on the environment

Minor Minimal risk to the project. Slight impact on services. Slight impact on the environment

Moderate Some impact on project Some service disruption Moderate impact on the environment

Major Significant impact on the project Cost implications in excess of £250k Major impact on the environment

Catastrophic Stops or delays project. Cost implications in excess of £1m

Risk exposure score The product of likelihood x impact identifies the seriousness of the risk exposure. There are three categories: Low risk 1-5 Medium risk 6-14 High risk 15-25 Risk Owner This will either be the Trust or the SCP. There should be no shared risks. NHS Trusts should consider the extent of their risk exposure and decide whether some risks are retained by them rather than passed over to the SCP.

- 17 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Risk Type Three groupings of risk have been identified: Planning, Design and Construction Operational External Risk Implications Risks can have an impact on generally four areas: Time Cost Quality Operations Some risks may impact on more than one area and may even affect all four areas. Risk Costs Text to be agreed. Funding Implications Identify whether the funding to remedy the risk is either Capital or Revenue. Risk Countermeasures Identify the mitigation measures that need to be put in place and other actions that could be taken if the risk occurs. Actioned By Identify the organisation tasked with implementing the countermeasures and mitigation proposals. Risk Status Cleared Current Future Comments Add any comments to remind, action or explain any special circumstances relating to the risk. Identify any links or interdependencies between risks.

- 18 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Designed for Life: Building for Wales

Project Risk Register

Trust _________________________________ Project ___________________________________________________

Version: Date last reviewed:

Produced by: A.N.Other, Project Management Ltd. Contact telephone : 02920 123456 Classification Risk

No. Risk Description

Likelihood of occurrence

Potential impact

Risk exposure score

Risk Owner

Risk Type

Risk Implications

Risk Cost

Funding Implication

Risk Counter- measures

Actioned By

Risk Status

Comments

Legend:

Capital

Revenue

Trust

SCP (Supply Chain Partners)

Likelihood

Rare 1 PDCR (Planning, Design and Construction Risk) Cleared

Unlikely 2 OR (Operational Risk) Current

Possible 3 ER (External Risks) Future

Likely 4

Almost certain 5

Impact

Insignificant 1 Time

Minor 2 Cost

Moderate 3 Quality

Major 4 Operational

Catastrophic 5

Score

Low risk 1-5

Medium risk 6-14

High risk 15-25

- 19 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Designed for Life: Building for Wales

Project Risk Register

Trust __________________________________ Project ___________________________________________________

Version: Date last reviewed:

Produced by: A.N.Other, Project Management Ltd. Contact telephone : 02920 123456

Classification Risk Implications

Risk No.

Risk Description

Likelihood of occurrence

Potential impact

Risk exposure score

Risk Owner

Risk Type

Time Cost Quality Operational

Risk Cost

Funding Implication

Risk Counter- measures

Actioned By

Risk Status

Comments

Inability to purchase suitable site Trust PDCR Capital

Site access issues Trust PDCR Capital

Site boundary issues Trust PDCR Capital

Inadequate off site service infrastructure difficulties Trust PDCR Capital

Poor ground conditions SCP PDCR Capital

Contaminated land SCP PDCR Capital

Site service infrastructure difficulties SCP PDCR Capital

Flora and fauna issues Trust PDCR Capital

Archeological issues Trust PDCR Capital

Environmental Impact Assessment difficulties Trust PDCR Capital

Traffic Impact Assessment difficulties Trust PDCR Capital

Failure to achieve Outline Planning Permission Trust PDCR Capital

Delay in achieving Outline Planning Permission Trust PDCR Capital

Poor Trust organisational Trust PDCR Capital

- 20 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Classification Risk Implications

Risk No.

Risk Description

Likelihood of occurrence

Potential impact

Risk exposure score

Risk Owner

Risk Type

Time Cost Quality Operational

Risk Cost

Funding Implication

Risk Counter- measures

Actioned By

Risk Status

Comments

structure

Limited Trust project resources Trust PDCR Capital

Poor Trust brief Trust PDCR Capital

Trust changing service requirements Trust PDCR Capital

Trust design changes Trust PDCR Capital

Failure to achieve Full Planning Permission Trust PDCR Capital

Onerous Planning Conditions Trust PDCR Capital

Failure to achieve Building Control approval SCP PDCR Capital

Breach of CDM Regulations SCP PDCR Capital

SCP bankruptcy Trust PDCR Capital

Availability of materials SCP PDCR Capital

Availability of labour SCP PDCR Capital

Poor SCP co-ordination SCP PDCR Capital

Poor SCP site supervision SCP PDCR Capital

Poor workmanship SCP PDCR Capital

SCP design changes SCP PDCR Capital

SCM bankruptcy SCP PDCR Capital

Poor SCM performance SCP PDCR Capital

Fire prior to completion SCP PDCR Capital

Changes in VAT rate Trust ER Capital

Failure to achieve anticipated VAT recovery Trust PDCR Capital

- 21 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Classification Risk Implications

Risk No.

Risk Description

Likelihood of occurrence

Potential impact

Risk exposure score

Risk Owner

Risk Type

Time Cost Quality Operational

Risk Cost

Funding Implication

Risk Counter- measures

Actioned By

Risk Status

Comments

Changes in Building Regulations Trust ER Capital

Rise in tender market above anticipated allowance Trust ER Capital

Adjudication Trust PDCR Capital

Arbitration Trust PDCR Capital

Litigation Trust PDCR Capital

Latent defects Trust OR Capital

Force Majeure Trust ER Capital

Adverse weather conditions SCP PDCR Capital

Engineering commissioning difficulties SCP PDCR Capital

Key Trust personnel changes Trust PDCR Capital

Key SCP personnel changes SCP PDCR Capital

Key SCM personnel changes SCP PDCR Capital

Civil commotion Trust ER Capital

Industrial action affecting SCP SCP ER Capital

Operational commissioning difficulties Trust OR Capital

Problems with site disposal(s) Trust OR Capital

Construction Noise SCP PDCR Capital

Construction Vibration SCP PDCR Capital

Construction Dust SCP PDCR Capital

Presence of asbestos SCP PDCR Capital

Legislative change: NHS specific Trust ER Revenue

- 22 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Classification Risk Implications

Risk No.

Risk Description

Likelihood of occurrence

Potential impact

Risk exposure score

Risk Owner

Risk Type

Time Cost Quality Operational

Risk Cost

Funding Implication

Risk Counter- measures

Actioned By

Risk Status

Comments

Legislative change: Non-NHS specific Trust ER Capital

Poor Trust Project Management Trust PDCR Capital

Poor Trust Cost Control Trust PDCR Capital

Accidental loss of engineering services to existing facilities SCP PDCR Capital

Delayed support from commissioners Trust PDCR Capital

Delayed approval by WAG Trust PDCR Capital

Failure to agree Target Cost Trust PDCR Capital

Construction buildability issues SCP PDCR Capital

Serious accident on site SCP PDCR Capital

Phasing interface difficulties SCP PDCR Capital

Programme over-run Trust PDCR Capital

Capital Cost over-run Trust PDCR Capital

Incorrect assessment of maintenance costs Trust OR Revenue

Incorrect assessment of projected energy use Trust OR Revenue

Capital Charge calculations inadequate Trust OR Revenue

Revenue cost assumptions underestimated Trust OR Revenue

Site sale receipts not realised Trust OR Capital

Technological change resulting in asset obsolescence Trust OR Revenue

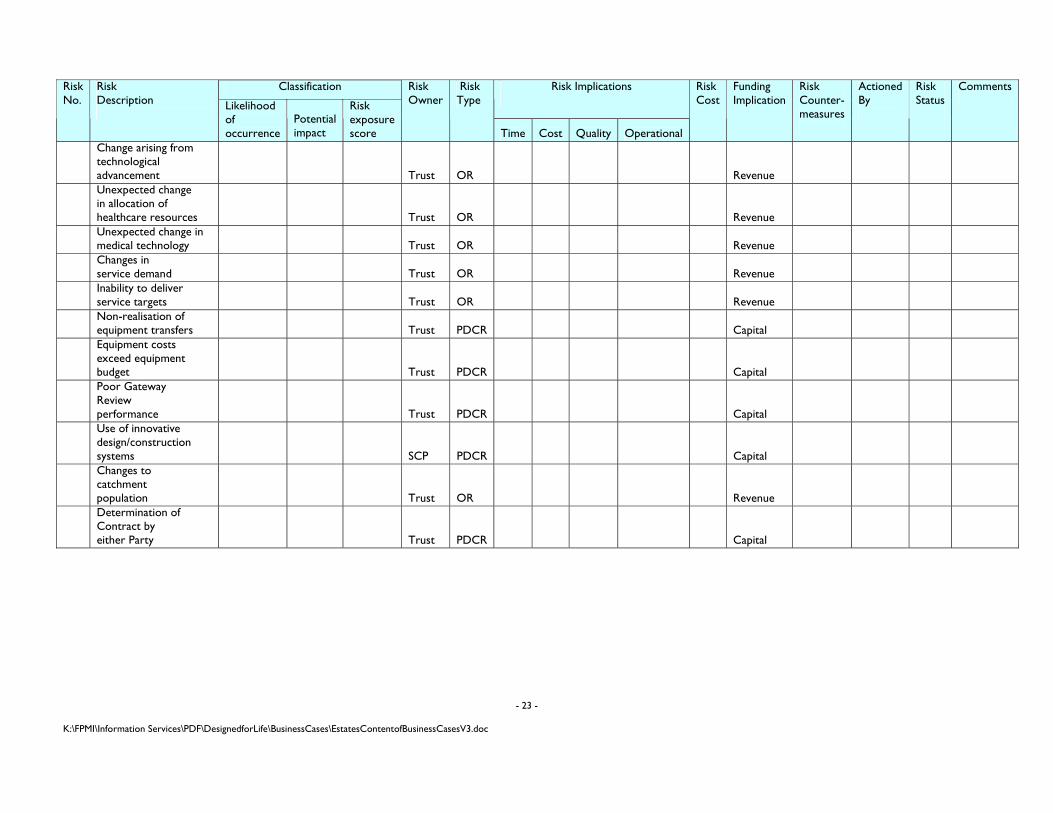

- 23 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Classification Risk Implications

Risk No.

Risk Description

Likelihood of occurrence

Potential impact

Risk exposure score

Risk Owner

Risk Type

Time Cost Quality Operational

Risk Cost

Funding Implication

Risk Counter- measures

Actioned By

Risk Status

Comments

Change arising from technological advancement Trust OR Revenue

Unexpected change in allocation of healthcare resources Trust OR Revenue

Unexpected change in medical technology Trust OR Revenue

Changes in service demand Trust OR Revenue

Inability to deliver service targets Trust OR Revenue

Non-realisation of equipment transfers Trust PDCR Capital

Equipment costs exceed equipment budget Trust PDCR Capital

Poor Gateway Review performance Trust PDCR Capital

Use of innovative design/construction systems SCP PDCR Capital

Changes to catchment population Trust OR Revenue

Determination of Contract by either Party Trust PDCR Capital

- 24 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

ANNEXURE D Designed for Life: Building for Wales

Typical Project Durations (months) - New Build

Construction Value (£m)

Appoint SCs

SOC

RO Approval

Appoint SCs + SCP

OBC

WAG Approval

FBC

WAG Approval

DC & C

Sub- total

OC

Duration to Opening

Project Closure

Total Duration

5 -10 1 3 2 1.5 4 2 9 2 24 48.5 1 49.5 9 58.5

10-15 1 3 2 1.5 4 2 9 2 24 48.5 1 49.5 9 58.5

15-20 1 3 2 1.5 4 2 9 2 27 51.5 2 53.5 9 62.5

20-25 1 3 2 1.5 4 2 9 2 27 51.5 2 53.5 9 62.5

25-30 1 3 2 1.5 5 2 12 2 27 55.5 3 58.5 9 67.5

30-35 1 3 2 1.5 5 2 12 2 30 58.5 3 61.5 9 70.5

35-40 1 3 2 1.5 5 2 12 2 30 58.5 4 62.5 9 71.5

40-45 1 3 2 1.5 6 2 12 2 33 62.5 4 66.5 9 75.5

45-50 1 3 2 1.5 6 2 14 2 33 64.5 5 69.5 9 78.5

50-55 1 3 2 1.5 6 2 14 2 36 67.5 5 72.5 9 81.5

55-60 1 3 2 1.5 6 2 14 2 36 67.5 6 73.5 9 82.5

Schemes over £60m to be separately assessed.

Legend: SOC Strategic Outline Case OBC Outline Business Case FBC Full Business Case DC & C Design Completion and Construction OC Operational Commissioning Assumptions: SCs Support Consultants SOC, OBC and FBC periods include Trust obtaining commissioner support. RO Regional Office FBC assumes 70-80% of design completed and market tested. SCP Supply Chain Partner Trust has prepared appropriate briefs prior to commencement of SOC, OBC and FBC stage. WAG Welsh Assembly Government

- 25 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Designed for Life: Building for Wales Typical Project Durations (months) - Refurbishment

Construction Assumed No. Appoint SOC RO Appoint OBC WAG FBC WAG Demolitions/ Fit- out

Sub- total OC Duration to Project Total

Value (£m) of phases SCs Approval SCs + SCP Approval Approval gutting Opening Closure Duration

5 -10 1 1 3 2 1.5 4 2 9 2 2 10 36.5 1.5 38 9 47 10-15 1 1 3 2 1.5 4 2 9 2 2 13 39.5 1.5 41 9 50 15-20 2 1 3 2 1.5 4 2 9 2 4 16 44.5 3 47.5 9 56.5 20-25 2 1 3 2 1.5 4 2 9 2 4 20 48.5 3 51.5 9 60.5 25-30 2 1 3 2 1.5 5 2 12 2 4 24 56.5 3 59.5 9 68.5 30-35 3 1 3 2 1.5 5 2 12 2 6 27 61.5 4.5 66 9 75 35-40 3 1 3 2 1.5 5 2 12 2 6 30 64.5 4.5 69 9 78 40-45 3 1 3 2 1.5 6 2 12 2 6 34 69.5 4.5 74 9 83 45-50 4 1 3 2 1.5 6 2 14 2 8 38 77.5 6 83.5 9 92.5 50-55 4 1 3 2 1.5 6 2 14 2 8 40 79.5 6 85.5 9 94.5 55-60 4 1 3 2 1.5 6 2 14 2 8 42 81.5 6 87.5 9 96.5

Schemes over £60m to be separately assessed.

Legend: SOC Strategic Outline Case OBC Outline Business Case FBC Full Business Case DC & C Design Completion and Construction OC Operational Commissioning

Assumptions: SCs Support Consutants SOC, OBC and FBC periods include Trust obtaining commissioner support. RO Regional Office FBC assumes 70-80% of design completed and market tested. SCP Supply Chain Partner Trust has prepared appropriate briefs prior to commencement of SOC, OBC and FBC stage. WAG Welsh Assembly Government Excludes asbestos removal

- 26 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

ANNEXURE E

Suggested Whole Life Cost Process at FBC stage

1. Approval to Outline Business Case.

2. Determine Project Base Construction Cost

3. Confirm buildable area

4. Prepare Notional Cost Plan

5. Carry out Whole Life Cost elemental specification selection

6. Agree Target Cost Plan

7. Cost checking/value engineering

8. Utilise Whole Life Cost principles in component selection

9. Complete Full Business Case

10. Finalise Target Cost

- 27 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Designed for Life: Building for Wales

Life Costing Exercise

Project :

Element:

Summary of Options

Option Option Capital Costs Revenue Costs Discounted cashflow calculations Comments:

No. Description Maintenance Operational Energy Present Equivalent

Initial Replacement Disposal Costs Costs Costs Value Annual Cost

Cost Cost Cost Annual Recurring Annual Annual

1

2

3

4

5

Notes:

- 28 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

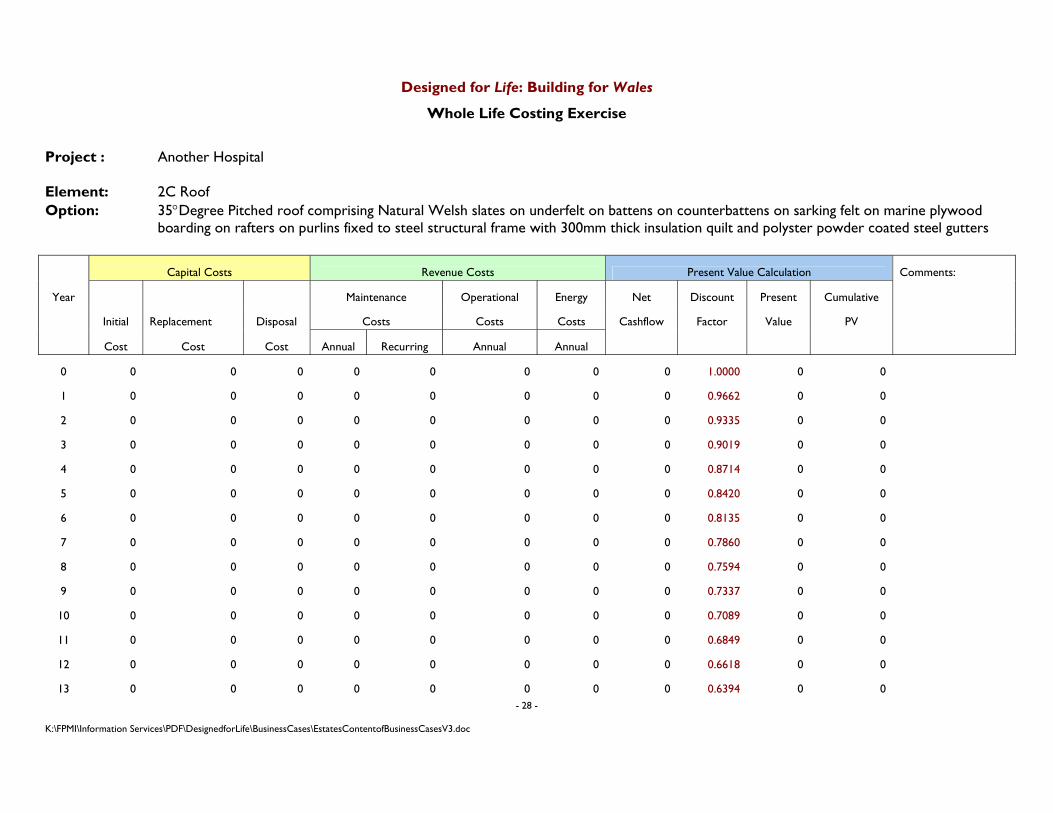

Designed for Life: Building for Wales

Whole Life Costing Exercise

Project : Another Hospital Element: 2C Roof Option: 35°Degree Pitched roof comprising Natural Welsh slates on underfelt on battens on counterbattens on sarking felt on marine plywood

boarding on rafters on purlins fixed to steel structural frame with 300mm thick insulation quilt and polyster powder coated steel gutters

Capital Costs Revenue Costs Present Value Calculation Comments:

Year Maintenance Operational Energy Net Discount Present Cumulative

Initial Replacement Disposal Costs Costs Costs Cashflow Factor Value PV

Cost Cost Cost Annual Recurring Annual Annual

0 0 0 0 0 0 0 0 0 1.0000 0 0

1 0 0 0 0 0 0 0 0 0.9662 0 0

2 0 0 0 0 0 0 0 0 0.9335 0 0

3 0 0 0 0 0 0 0 0 0.9019 0 0

4 0 0 0 0 0 0 0 0 0.8714 0 0

5 0 0 0 0 0 0 0 0 0.8420 0 0

6 0 0 0 0 0 0 0 0 0.8135 0 0

7 0 0 0 0 0 0 0 0 0.7860 0 0

8 0 0 0 0 0 0 0 0 0.7594 0 0

9 0 0 0 0 0 0 0 0 0.7337 0 0

10 0 0 0 0 0 0 0 0 0.7089 0 0

11 0 0 0 0 0 0 0 0 0.6849 0 0

12 0 0 0 0 0 0 0 0 0.6618 0 0

13 0 0 0 0 0 0 0 0 0.6394 0 0

- 29 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Capital Costs Revenue Costs Present Value Calculation Comments:

Year Maintenance Operational Energy Net Discount Present Cumulative

Initial Replacement Disposal Costs Costs Costs Cashflow Factor Value PV

Cost Cost Cost Annual Recurring Annual Annual

14 0 0 0 0 0 0 0 0 0.6178 0 0

15 0 0 0 0 0 0 0 0 0.5969 0 0

16 0 0 0 0 0 0 0 0 0.5767 0 0

17 0 0 0 0 0 0 0 0 0.5572 0 0

18 0 0 0 0 0 0 0 0 0.5384 0 0

19 0 0 0 0 0 0 0 0 0.5202 0 0

20 0 0 0 0 0 0 0 0 0.5026 0 0

21 0 0 0 0 0 0 0 0 0.4856 0 0

22 0 0 0 0 0 0 0 0 0.4692 0 0

23 0 0 0 0 0 0 0 0 0.4533 0 0

24 0 0 0 0 0 0 0 0 0.4380 0 0

25 0 0 0 0 0 0 0 0 0.4231 0 0

26 0 0 0 0 0 0 0 0 0.4088 0 0

27 0 0 0 0 0 0 0 0 0.3950 0 0

28 0 0 0 0 0 0 0 0 0.3817 0 0

29 0 0 0 0 0 0 0 0 0.3687 0 0

30 0 0 0 0 0 0 0 0 0.3563 0 0

31 0 0 0 0 0 0 0 0 0.4000 0 0

32 0 0 0 0 0 0 0 0 0.3883 0 0

33 0 0 0 0 0 0 0 0 0.3770 0 0

34 0 0 0 0 0 0 0 0 0.3660 0 0

- 30 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Capital Costs Revenue Costs Present Value Calculation Comments:

Year Maintenance Operational Energy Net Discount Present Cumulative

Initial Replacement Disposal Costs Costs Costs Cashflow Factor Value PV

Cost Cost Cost Annual Recurring Annual Annual

35 0 0 0 0 0 0 0 0 0.3554 0 0

36 0 0 0 0 0 0 0 0 0.3450 0 0

37 0 0 0 0 0 0 0 0 0.3350 0 0

38 0 0 0 0 0 0 0 0 0.3252 0 0

39 0 0 0 0 0 0 0 0 0.3158 0 0

40 0 0 0 0 0 0 0 0 0.3066 0 0

41 0 0 0 0 0 0 0 0 0.2976 0 0

42 0 0 0 0 0 0 0 0 0.2890 0 0

43 0 0 0 0 0 0 0 0 0.2805 0 0

44 0 0 0 0 0 0 0 0 0.2724 0 0

45 0 0 0 0 0 0 0 0 0.2644 0 0

46 0 0 0 0 0 0 0 0 0.2567 0 0

47 0 0 0 0 0 0 0 0 0.2493 0 0

48 0 0 0 0 0 0 0 0 0.2420 0 0

49 0 0 0 0 0 0 0 0 0.2350 0 0

50 0 0 0 0 0 0 0 0 0.2281 0 0

51 0 0 0 0 0 0 0 0 0.2215 0 0

52 0 0 0 0 0 0 0 0 0.2150 0 0

53 0 0 0 0 0 0 0 0 0.2088 0 0

54 0 0 0 0 0 0 0 0 0.2027 0 0

55 0 0 0 0 0 0 0 0 0.1968 0 0

- 31 - K:\FPMI\Information Services\PDF\DesignedforLife\BusinessCases\EstatesContentofBusinessCasesV3.doc

Capital Costs Revenue Costs Present Value Calculation Comments:

Year Maintenance Operational Energy Net Discount Present Cumulative

Initial Replacement Disposal Costs Costs Costs Cashflow Factor Value PV

Cost Cost Cost Annual Recurring Annual Annual

56 0 0 0 0 0 0 0 0 0.1910 0 0

57 0 0 0 0 0 0 0 0 0.1855 0 0

58 0 0 0 0 0 0 0 0 0.1801 0 0

59 0 0 0 0 0 0 0 0 0.1748 0 0

0 0 0 0 0 0 0 0 0

EAC factor (60 years) 27.2975

Equivalent Annual Cost 0

Note: Costs exclude inflation and VAT Red=3.5% Blue=3%

Notes: