D.U. Journal of Marketing, Vol. 16, No. 1, June 2013 (Published in December, 2015)

FACTORS CONSIDERED IN BUSINESS BUYING ACROSS

DIFFERENT LEVELS OF DISTRIBUTION CHANNELS: A

STUDY ON CEMENT INDUSTRY OF BANGLADESH

Abu Naser Ahmed Ishtiaque1

Moutushi Tanha2

Arifur Rahman3

Abstract: The significance of business buying of distribution channel

members in cement industry is multifaceted. Cement industry itself has a

great strategic value in economy. It is the major component in construction

sector. In Bangladesh, some local cement companies are dominating the

market with their quality products, adoption of state-of-the-art technologies

and effective marketing strategy including countrywide distribution channel

whereas some multinational companies also are operating with financial

power and technological acumen backed by global reputation. Distribution

channel members of cement in the country sometimes face unfavorable

circumstances and fail to reap the multifarious benefits from such lucrative

industry. The current study aims at identifying and analyzing the factors

that distribution channel members of cement consider while buying cement.

The study found high demand, high quality, high commission rate, rational,

competitive and reasonable price, good Brand-Image, delivery as per

scheduled time, quick delivery, transportation facility and credit time,

availability, good and effective communication are important economic and

non-economic factors considered while buying cement in the context of

Bangladesh.

Keywords: Cement, SCM, Distributor, Dealer, Retailer, Channel Conflict,

Brand

INTRODUCTION

In recent years supply chain management (SCM) has become a highly discussed

topic in economics and business throughout the world (Arntzen et al., 1995).

There has been much interest amongst managers and academics regarding SCM

and supply chain integration. The term SCM is used frequently in today‟s

materials management environment and is generally associated with advanced

information technologies, rapid and responsive logistics services, effective

physical distribution, supplier management, and customer relationship

management (Lee and Billington, 1995). According to Lee and Billington (1995)

most managers are familiar with the supply chain slogan– “suppliers‟ supplier to

customers‟ customer.” Physical distribution system backed by the necessary

1 Professor, Department of Marketing, University of Dhaka, Bangladesh.

2 Associate Professor, Department of Marketing, University of Dhaka, Bangladesh. 3 Associate Professor, Department of Marketing, University of Dhaka, Bangladesh.

82 D.U. Journal of Marketing, Vol. 16, No. 1, June 2013

flows (Bovet and Martha, 2003) is one of the key function of managing a supply

chain apart from material sourcing, production scheduling. Successful

management of the distribution channel is required for competitive advantage.

Cement industry is considered as one of the most energy-intensive manufacturing

industries around the world as it is the basic component of making concrete.

Therefore, this industry is a priority one requiring a careful planning and

controlling of its manufacturing and managerial activities and operations (The

Daily Star, 2010). Cement industry, a relatively fast growing industry in

Bangladesh, is developing in keeping pace with increasing building and

construction activities. Cement, being the major component in construction

sector, the industry itself has a great strategic value. Though there are some

multinational cement companies with financial power and technological acumen

backed by global reputation; certain local companies are dominating the market

with their quality products, adoption of state-of-the-art technologies and effective

marketing strategy including countrywide distribution channel (The Daily Star,

2010).

From the above discussion it is evident that proper utilization of an effective and

efficient distribution network is a perquisite for sustaining in this fiercely

competitive industry of cement in Bangladesh. And distribution channel

members are the role players of such network. Dynamics of their behavior across

distribution channel are very influential for smooth flows of distribution of

cement. This study is therefore worthy to research.

LITERATURE REVIEW

The management of supply chain is gaining increased attention due to the

expansion and complexity of the distribution networks. Yuva (2002) identified

that managing an efficient distribution system in a supply chain is one of the

important factors required to reduce the costs and thereby increasing profit. The

supply chain consists of many stages including fulfilling a customer request.

Fawcett and Magan (2002) argued that the supply chain not only includes the

manufacturer and suppliers, but also transporters, warehouses and all other

related operations and processes. Past research on supply chain management

mainly focused on some of its implementation issues (Handfield and Nichols Jr.,

1999) which includes all functions involved in filling the customer request. Such

functions include, but are not limited to, new product development, marketing,

operations, distribution, and finance and customer services. The primary purpose

for the existence of any supply chain is to satisfy customer needs. Distribution

activities begin with the customer orders and end after delivering the required

items to the right customer at the right place (Mentzer et al., 2001). A company‟s

supply chain encompasses all of the facilities, functions and activities involved in

producing a product or schedule, facility location, transportation and distribution.

All these are affected by product demand in the short run and by utilizing new

technology in addition to market demand in the long run (Davis and Drumm,

Factors Considered In Business Buying Across Different Levels Of Distribution Channels 83

2001). Distribution of cement is not beyond an exception. In Bangladesh, there is

an expanded and complicated distribution activity in cement industry.

The purchase of components and services has direct effects on the business.

According to prior studies of Chisnall (1985), Brands (1994), Gadde and

Hakansson (1994), Hurt and Speh (1998) and Cavinato (1999), industrial

purchasing involves many activities: identifying the supplier base, establishing

bidding competition, creating tools for managing the purchasing activity,

minimizing supplier related risk, evaluating and comparing the potential supply

partners, and forming supply contracts. Despite the complexity of purchasing

process the essential choices are manifested in companies‟ purchasing strategies

in different contextual buying settings (Faces et al., 2001; Hurt and Speh, 1998).

Key dilemmas in strategy formulation relate to the nature of exchange and to the

selection of suppliers among the excess of potential actors (Cavinato, 1999; Faes

et al., 2001).

Business buying is something different form consumer buying in terms of the use

of the product. According to Kotler and Armstrong (2012) business buyers do not

use products for their consumption rather for reselling or further processing

purpose whereas consumer buyers use for their own consumption. Distribution

channel members are business buyers and therefore, their buying is much more

rational and responsible buying unlike consumer buyer.

Distribution channel consists of different levels including supplier, manufacturer,

distributor and consumer and is a network of companies that influences each

other from raw materials to finished goods (Christopher et al., 2002; chain,

2003). For formulating effective distribution strategy it is important to identify

different levels of distribution network of any industry. Lamming et al. (2001)

suggested that there are varying degrees of supply chain visibility or sharing of

information between partners in a supply chain and refers to it as transparency.

According to Lamming‟s et al. (2001) categorization of the varying degrees of

transparency is Opaque, Translucent and Transparent. An increasing in available

supply chain data gives the illusion of visibility, however, it can add to a firm‟s

challenge of matching insights from the analyses to strategy.

According to Chan (2003), visibility for a distribution network is important for

accurate and fast delivery of information. Therefore, which actors are playing in

a particular distribution channel and the existing network is significant.

Identifying distribution channel members of cement and the information flow

among them is therefore justified to a large extent. In connection with this

argument, Lee et al. (1997) stated that lack of accurate information can cause

certain negative consequences such as the bullwhip-effect in supply chains.

According to Svensson (2004) the two main influences on the perception of

corporate vulnerability in supply chains are the degree of transparency and the

degree of obscurity. He stated that the more accurate the information, the higher

the transparency, but the more accurate the information deteriorates, the higher

84 D.U. Journal of Marketing, Vol. 16, No. 1, June 2013

becomes the obscurity. He believed that, together, these two influences create a

conceptual framework and contribute to the dilemma of corporate vulnerability.

Therefore, effective communication between channel members is prerequisite for

successful distribution. Trust and dependence are elementary qualities in

customer-supplier relationships of networked organizations. Some level of trust

is a necessary condition for all repeated inter organizational transactional (Das

and Teng, 1998; Ring and Van de Ven, 1992) and as a relationship develops

further, the interdependence between the partners is likely to increase (Pfeffer

and Salancik, 1978). However, the increasing dependence may contribute to the

fear of partner‟s opportunistic behavior, the magnitude of expected coordination

costs, and the difficulties of the relationship coordination (Gulati and Singh,

1998; Krishnan et al., 2006).

Sterling and Lambert (1989) studied the office systems and furniture industry and

the plastic industry in some depth. From a large number of variables (99 and 112,

respectively) representing product, price, promotion and physical distribution,

they were able to determine those that were most important to the buyers,

customers and influencers of purchases from these industries. Based on mean

scores of importance, as indicated by respondents on a one to seven point scale,

they rank ordered the service (physical distribution) elements in each of these

industries. They ranked customer service variables by order of importance for 2

industries: office systems and furniture industry and plastic industry. For office

systems and furniture industry, they considered ability of manufacturer to meet

promised delivery date, accuracy in filling orders, overall manufacturing and

design quality relative to price, competitiveness of price, advance notice on

shipping delays, timely response to requests for assistance from manufacturer‟s

representatives, action on customer service complaints, order cycle consistency

(small variability), accuracy of manufacturer in forecasting estimated ship dates,

overall aesthetics and finish, continuity (nonobsolescence of products),

manufacturer‟s willingness to accept returns of damaged products, length of

promised lead time for quick-ship orders, completeness of contract orders,

completeness of quick-ship orders and realistic and consistent pricing policy.

And for plastic industry they considered supplier‟s resins are of consistent

quality, accuracy in filling orders (correct product is shipped), competitiveness of

price, processability of resin (main ingredients of plastic), consistent lead times

(vendor consistently meets expected delivery date), consistent melt flow, ability

to expedite emergency orders in a fast responsive manner, information provided

when order is placed– projected shipping date, advance notice of shipping delays,

adequate quality of resin relative to price, overall quality of resin relative to

price, actions on complaints (e.g., order servicing, shipping, product etc.), length

of promised lead times (from order submission to delivery-in-stock products) and

inventory availability.

Factors Considered In Business Buying Across Different Levels Of Distribution Channels 85

Their research showed that physical distribution is an integral and necessary

component of the marketing mix, and that it offers a significant opportunity for

firms to gain differential advantage in the marketplace. Evaluation of the 16

variables rated as most important by dealers, end users and architectural and

design firms disclosed that at least one-half were physical distribution variables

(Sterling and Lambert, 1989).

In another study conducted by Lambert and Harrington (1989), 9 of the 18

variables rated as most important were related to logistics in case of plastic

industry. Of the remaining variables, 5 related to product quality, 2 to price and 2

to the sales force. The Sterling-Lambert research certainly suggested that

logistics customer service is dominant in the minds of customers in the office

systems and furniture industry and the plastics industry. Although such a small

sample of industries may not be overly convincing, others have observed the

same phenomenon. In a similar study of the auto glass after market, Innis and

LaLonde (1994) found that 6out of the top 10 customer service attributes were

logistical in nature.

Notably, high fill rates, frequency of delivery and information on inventory

availability, projected shipping date and projected delivery date at the time of

order placement received high ratings among the retail customer base. Further,

LaLonde and Zinszer (1994) found that product availability (order completeness,

order accuracy and stocking levels) and order-cycle time (order-transit time and

time for assembly and shipping) were dominant in the minds of users, being most

important to 63% of the respondents in their study.

Marr (1994) also surveyed a number of firms with the following conclusions:

only one respondent mentioned cost of service, of the top seven elements, only

one was outside the control of distribution management, the most important

service element was speed of delivery.

Shycon Associates surveyed purchasing and distribution executives across a

large cross section of American industry, asking them to rate their suppliers

(Baritz and Zissman, 1983). Their study showed the most common service

complaints from customer part. Late delivery, a logistics customer service

variable, accounted for nearly half of the mentioned service infractions, while

product or quality mistakes represented about a third. Besides, damaged goods,

frequently cut items are also important. Jackson et al. (1986) were able to show

how service elements take on different degrees of importance, depending on the

product type being purchased. They surveyed 254 purchasing agents in 25

companies about the importance of 6 physical distribution service elements: in-

stock performance, lead time, consistency of delivery time, order progress

information, protective packaging, cooperation in handling, shipping problems.

Their results showed ranking of six physical distribution service elements by

product type. In summary, the following are considered the most important

86 D.U. Journal of Marketing, Vol. 16, No. 1, June 2013

logistics customer service elements: on-time delivery, order fill rate, product

condition and accurate documentation.

According to Kotler and Armstrong (2010), during supplier selection, the buyers

often draw up a list of the desired supplier attributes and their relative

importance. Such attributes include product and service quality, reputation, on-

time delivery, ethical corporate behavior, honest communication and competitive

prices. The buyers rate suppliers against these attributes and identify the best

supplier(s).

Finally, dynamism of channel relationships consist of degree of collaboration,

commitment and trust among channel members, power and dependence (Cravens

and Piercy, 2009). They argued that the extent of collaboration is influenced by

the complexity of the product, the potential benefits of collaboration, and the

willingness of channel members to work together as partners. Distribution

channel model encourages collaboration and information-sharing between

suppliers and producers. Like any distribution channel network, cement also

demands largely a fair amount of collaboration, commitment and trust among its

channel members. Absence of such factors results in obvious conflict of interest.

According to Cravens and Piercy (2009), highly collaborative relationships

among channel members call for a considerable degree of commitment and trust

between the partners. In every business, the cooperating organizations provide

access to confidential product plans, market data and other trade secrets. Bovet

and Martha (2003) argued that trust normally develops as the partners learn to

work with each other and find the relationship to be favorable to each partner‟s

objectives. Conventional channel relationships may, nevertheless, result in some

channel members possessing more bargaining power than others. In many

sectors, suppliers face unprecedented pressure from powerful channel members.

Responses may include suppliers reclaiming important value-added services from

distributors to build stronger relationships with end-users, eliminating layers in

the conventional channel; or creating new channels.

Lastly, conflict of interest is another dimension of channel behavioral dynamism.

According to Cravens and Piercy (2009), conflicts are certain to occur between

the channel members and in multi-channeling between channels, because of

differences in objectives, priorities and corporate cultures. Looking at a proposed

channel relationship by each participating organization may identify areas (e.g.,

incompatible objectives) that are likely to lead to major conflicts. In such

situations, management may decide to seek another channel partner. Accurate

and timely flow of information is necessary to reduce conflict among channel

members that is also justified by Cravens and Piercy (2009) that effective

communications before and after establishing the channel relationships can also

help to eliminate or reduce conflicts.

Factors Considered In Business Buying Across Different Levels Of Distribution Channels 87

OBJECTIVES

The foremost thrust of the study is to explore the factors that are considered in

business buying of distribution channel members (manufacturers, dealers,

distributors and retailers) of cement industry across different levels of the

distribution channel. In the light of this main objective, specific objectives

(Malhotra, 2007) of the study are:

1. to identify the distribution channel members across different levels of the

distribution channel of cement,

2. to explore the reasons behind preference of selling a particular brand of

cement by distributors, dealers and retailers,

3. to discover the reasons behind distributors‟ discouragement as perceived by

dealers and retailers,

4. to explore the reasons behind dealers‟ discouragement stated by retailers,

5. to know the dealers‟ efforts to induce retailers to sell specific brands,

6. to know dealers‟ motive to push specific brands to retailers,

7. to identify conflict among distribution channel members of cement, and

8. to draw some recommendations.

METHODOLOGY

An exploratory followed by descriptive study on the channel members

(manufacturers, dealers, distributors, retailers) was conducted in the context of

Bangladeshi cement industry. At first, qualitative approach was used. In-depth

interviews with distributors, dealers, retailers, institutional buyers and individual

buyers were conducted. Survey was conducted for addressing descriptive aspect

of the study.

Both primary and secondary data have been collected to conduct this study. The

survey was conducted in 10 districts of Bangladesh. The primary data were

collected from 5 respondent bases that included distributors, dealers, retailers,

institutional buyers and individual buyers. The sample size was 555. The quota

sampling technique was used in this research. At the first, researchers developed

the quotas of population elements i.e., respondent bases and in the second stage,

respondents were selected on the basis of judgment. Structured questionnaire

were used in tapping the information which was designed in the light of the

objectives of the study according to the level of channel members.

The secondary data sourced from various published materials especially from

books, journals, Internet, and seminar proceedings as well as some working

papers. An extensive review of literatures helped to make coherent picture on the

topic of the study.

Data have been processed and tabulated by using sophisticated statistical package

used in social science then an effort has been taken to summarize the data in the

88 D.U. Journal of Marketing, Vol. 16, No. 1, June 2013

table by calculating simple percentage. Final analysis has been made on the

relevant statistic like rank order.

At present Holcim, Shah, Heidelberg, Premier, Crown, 7 Rings, King Brand,

Lafarge Surma, Akiz, Cemex, Fresh, Mir, Tiger, Anwar, Metrocem, Elephant,

and Seven Horse are the brands of cement mostly operating in Bangladesh.

Manufacturers taken for this study have almost similar distribution network of

channel members. Due to the privacy policy of the study, the name of the brands

has not been disclosed. Different brands are denoted here as Brand A, B, C and

the like.

MAJOR FINDINGS

Findings of the conducted interviews are presented in accordance with the

sequence followed in questionnaire i.e. identification of the distribution channel

members across different levels of the distribution channel of cement in

Bangladesh; of the reasons behind preference of selling a particular brand of

cement by distributors, dealers and retailers; of the reasons behind distributors‟

discouragement as perceived by dealers and retailers; of the perceived reasons

behind dealers‟ discouragement stated by retailers; of the dealers‟ efforts to

induce retailers to sell specific brands; of the dealers‟ motive to push specific

brands to retailers and of the conflict among distribution channel members of

cement.

Cement’s Channel of Distribution

In Bangladesh, distribution channel of cement is mostly indirect and in some

cases direct. In case of indirect distribution channel, manufacturers use appointed

distributors. Distributors buy from manufacturers and sell to dealers and retailers.

Dealers generally buy from distributors but also buy from manufacturers directly.

Retailers buy generally from dealers. They also buy from distributors. Retailers

generally don‟t have any direct contact with manufacturers. On the other hand, in

case of direct distribution channel, institutional buyers buy directly from

manufacturers. Finally, individual house builders buy, in small scale, from

retailers.

The current distribution channel of cement is presented in Figure 1 which is

followed by the modes of operation of the channel as shown in Table 1 (See the

appendix).

Factors Considered In Business Buying Across Different Levels Of Distribution Channels 89

Figure 1: Distribution System of Cement

Source: Researchers Contribution

Channel Members’ Preferences for Different Brands of Cement

Unlike consumer buying, buying of channel members considers several rational

factors. As their prime buying motive is reselling, therefore, their buying

consideration is much more cost-benefit analysis oriented and less emotion

oriented. In this study, we identified preference of dealers and retailers.

Preference of dealers: Dealers usually go for dealership of cements on the basis

of their individual preference based on local demand. Several brands of cement

that are mostly preferred by dealers are shown in Table: 2 (See the appendix). In

terms of the 1st preference of most dealers, Brand-B Cement is found to take the

first position preferred by 9 dealers (20.4 %). It was followed by Brand-A 7

(16%) and Brand-D Cement 6 (13.6%). However, when all the brands are ranked

based on the first three preferences, Brand-A tops the list having been followed

by Brand-B, Brand-C, Brand-D and Brand-E, in order of performance. The

„Others‟ category includes Brand-M, Brand-N, Brand-O, Brand-P, Brand-Q, etc.

The study shows that the most preferred reason behind dealership of a specific

brand of cement is its high sales (high demand) as stated by 21 (60%) of the

dealers followed by high quality reported by 23% of the dealers. However, when

all the reasons are ranked based on the first three recalls the same order persists

among the reasons behind selling cement; i.e., high sales, high quality, high

commission rate, good brand image, etc. ( See the appendix: Table: 3)

In response to the question as to which brand brings about the most profit (per

bag) from selling to retailers, 9 (21.4%) dealers stated that Brand-B Cement is in

the first position which is followed by Brand-E Cement (12%), Brand-D (9.5%),

Brand-A (9.5%) and Brand-F (9.5%) follow suit . However, when all the

90 D.U. Journal of Marketing, Vol. 16, No. 1, June 2013

companies are ranked based on the first three profit yielding levels, Brand-B

Cement still tops the list having been succeeded by Brand-E, Brand-D, Brand-A,

and Brand-F (See the appendix: Table: 4).

Table 5 (See the appendix) presents a dismal picture which should not be ignored

to set things on the right track. This may be a worthwhile cause of concern for

many cement companies.

Preference of retailers. Retailers usually deal in cements of some 3 to 8 brands

of their individual preference. Several brands of cement that are mostly preferred

by retailers (See the appendix: Table: 6). In terms of the 1st preference of the

most retailers, Brand-B Cement is found to take the first position preferred by 36

retailers (17.4 %). It was followed by Brand-C 29 (14%) and Brand-A Cement 25

(12.1%). However, when all the brands are ranked based on the first three

preferences, Brand-B Cement tops the list having been succeeded by Brand-C,

Brand-A and Brand-H. In this respect the position of Brand-E is only 9th. The

„Others‟ category includes Brand-M, Brand-N, Brand-O, Brand-Q, Brand-P

brands, etc.

The first preferred reason behind retailing a specific brand of cement is its high

sales (high demand) as stated by 124 (70.9%) of the retailers followed by high

quality reported by 20.0% of the retailers shown in the Table 7 (See the

appendix). However, when all the reasons are ranked based on the first three

recalls the same order is maintained among the reasons behind selling cement;

i.e., high sales, high quality, quick delivery, good brand image, etc.

In response to the question as to which brand brings about the most profit (per

bag) from retailing, 28 (14.6%) retailers stated that Brand-B Cement is in the first

position which is followed by Brand-K Cement (12.5%) and Brand-A (7.8%) and

Brand-D (7.8%). However, when all the companies are ranked based on the first

three profit yielding levels, Brand-B Cement still tops the list having been

followed by Brand-K, Brand-A, Brand-C, Brand-F and Brand-D. In this respect

Brand-E is in the 9th position (See the appendix: Table 8).

The study shows that the dealers of which company are more aggressive (i.e., put

more effort) in pushing the products of their companies to the retailers shown in

Table: 9 (See the appendix). In terms of the top (1st) level effort, Brand-B, Brand-

A, Brand-I and Brand-K are more enthusiastic than Brand-E, Brand-C, King and

Brand-F. In this respect Brand-E is in the 5th position. The dealers of the

remaining competitors are much more lagging behind them. However, when all

three levels of effort are put together, the order remains almost same.

The driving forces are shown in the Table 10 (See the appendix) behind such

enthusiasm of dealers. In this matter „high profit‟ is found to be more effective

than all other factors. However, high quality of cement also plays a prominent

role.

Factors Considered In Business Buying Across Different Levels Of Distribution Channels 91

Table 11 (See the appendix) presents a dismal picture which should not be

ignored to set things on the right track. This may be a worthwhile cause of

concern for the management of cement companies.

The key reason as perceived by retailers is low availability of Brand-E cement to

the concerned distributor(s). Table 12 (See the appendix) presents a dismal

picture which should not be ignored to set things on the right track. This may be

worthwhile causes of concern for the management of cement companies.

Channel Conflict

Distribution channel members of cement very often engage in conflicting

situations due to their conflict of interest. The identified areas of conflicts among

them are worthy to mention.

Conflict of retailers with companies: The areas of conflict between the retailers

on the one side and companies on the other are demonstrated in the table: 13 (See

the appendix). It is observed that the most common complaint is about delay in

delivery. Direct selling to corporate clients and low commission rate are also

important areas of complaint.

The Table 14 (See the appendix) also resonate the same complaint about which

the companies need to pay heed. Timely supply of cement to retailers and prompt

payment of retailer commission are important areas for improvement. Direct

selling should be as less as possible.

Conflict of retailers with dealers: The areas of dealer-retailer conflict are

shown in the Table: 15 (See the appendix). The common complaints are non-

availability of dealers at the time of need, charging of uneven prices and

application of force for making payment.

Conflict of retailers with distributors: The complaints of retailers against the

distributors which are more or less the same as with dealers are demonstrated in

the Table: 16 (See the appendix).

Conflict among retailers: The main reason behind the conflicts among retailers

is the variation of price of cement from retailer to retailer, which should be

another area needing company‟s attention. Such price variation should be as less

as possible (See the appendix: Table: 17).

Conflict of dealers with companies: The areas of conflict between the dealers

on the one side and companies on the other are shown in the Table: 18 (See the

appendix). It is observed that the most common complaint is about delay in

delivery. Direct selling to corporate clients and low commission rate are also

important areas of complaint.

The study also resonate the same complaints about which the companies need to

pay heed. Timely supply of cement to dealers, prompt payment of dealer

commission and informing the qualities of cement are important areas for

92 D.U. Journal of Marketing, Vol. 16, No. 1, June 2013

improvement. Direct selling should be as less as possible. (See the appendix:

Table: 19)

The complaints of dealers against the distributors are shown in the table: 20 (See

the appendix) in which the major reason is stated as direct selling to retailers

followed by unavailability and higher price charged.

The main reason behind the conflicts among the dealers is the variation of price

of cement from dealer to dealer, which should be another area needing

company‟s attention. Such price variation should be as less as possible (See the

appendix: Table: 21).

Business Buying of Institutional Buyers (IBs) and Individual House Builders

(IHBs)

According to the study, institutional buyers and individual buyers also are

channel members of cement apart from distributors, dealers and retailers. The

study identified that IBs e.g. government, defense, real estates, developers,

commercial organizations, contractors and so on buy generally directly from

manufacturers due to their large volume of buying. On the other hand, IHBs

generally do not buy directly from manufacturers due to their small scale buying.

Buying of individual house builders (IHBs): In case of selection of retailers by

IHBs, proximity is observed to be in the first position as cited by 77 of the 152

IHBs among whom 72 (59%) cited it to be the „first‟ consideration (recall),

which is followed by quick delivery (11.5%) and large stock (5.7%) (See the

appendix: Table: 22). However, when all the factors are ranked based on the first

two recalls, proximity is observed to be on top of the list succeeded by quick

delivery. The „Others‟ category includes mainly familiar retailers, good

relationship, quick delivery and large stock.

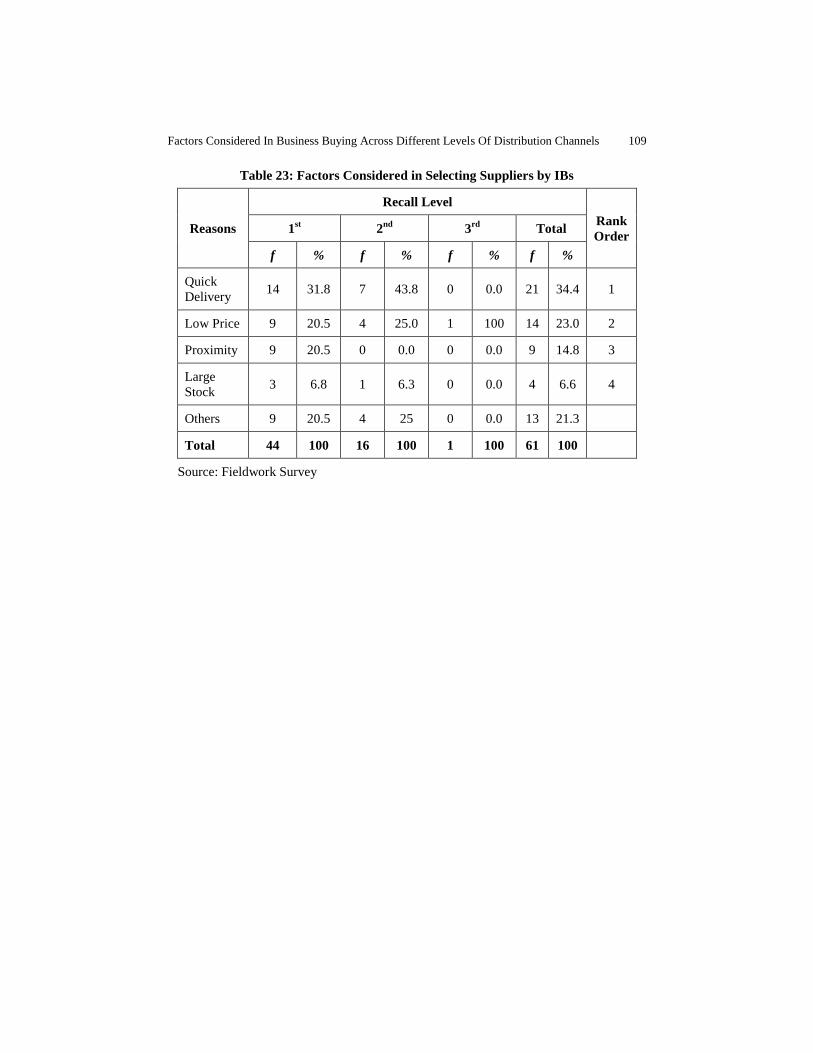

Buying of individual buyers (IBs): In case of selection of suppliers by IBs,

quick delivery is observed to be in the first position as cited by 31.8% of IBs,

which is followed by low price (20.5%), proximity (20.5%), large stock (6.8%)

(See the appendix: Table: 23). However, when all the factors are ranked based on

the first three recalls, quick delivery still is observed to be on top of the list

followed by low price and proximity.

RECOMMENDATIONS

The identification of different channel members and different factors considered

in business buying of channel members in cement industry is helpful for

distribution professionals and practitioners in a number of ways.

First, it helps to identify economic and noneconomic factors of business buying

of distribution channel members under different circumstances in case of cement

industry particularly in Bangladesh. As mentioned by the findings of the study,

some factors in terms of high demand, high quality, high commission rate,

Factors Considered In Business Buying Across Different Levels Of Distribution Channels 93

rational, competitive and reasonable price, good brand-Image, delivery as per

scheduled time, quick delivery, transportation facility and credit time,

availability, good and effective communication are important economic and non-

economic factors considered while buying cement in the context of Bangladesh.

Second, it can aid practitioners in looking for underlying reasons behind their

business buying.

Third, it can help them to design strategies to check and balance the feasibility of

their purchase by determining the optimum level.

Effective distribution depends on how channel members are organized across the

particular channel and play their expected role. Organized performance of

distribution channel members is prerequisite for distribution success. In this

study existing distribution routes of cement can be effectively used if the channel

members (manufacturers, wholesalers, retailers, dealers and distributors) play

their due and expected roles and each distribution partner considers the buying

factors of his buyers. As found from the study, dealers prefer high sales, high

quality, high commission rate, good brand image etc. As dealers directly buy

from distributors and sometimes from manufacturers, distribution arrangement

should be based on agreed upon terms and conditions so that conflicts between

manufacturers, distributors and dealers would not arise. Distributors and

manufacturers should pay attention to these factors. Again, retailers prefer high

sales, high quality, quick delivery, good brand image etc. that are almost similar

with factors preferred by dealers.

As retailers‟ most common complaints found from the study are delayed

delivery, direct selling to corporate clients and low commission rate. Therefore,

dealers and distributors who deal with retailers should pay attention to these

factors. Again, common conflicts of dealers with distributors are charging of

unequal prices and application of force for making payment that should be dealt

with proper action.

Manufacturers, their appointed distributors and dealers should strictly handle

these issues for the sake of overall effectiveness of the distribution network of

cement.

CONCLUSION

This study addresses the factors that business buyers consider while buying

cement and in order to address factors, objectives have been set to identify the

distribution channel members across different levels of the distribution channel

of cement, to explore the reasons behind preference of selling a particular brand

of cement by distributors, dealers and retailers, to discover the reasons behind

distributors‟ discouragement as perceived by dealers and retailers, to explore the

reasons behind dealers‟ discouragement stated by retailers, to know the dealers‟

efforts to induce retailers to sell specific brands, to know dealers‟ motive to push

94 D.U. Journal of Marketing, Vol. 16, No. 1, June 2013

specific brands to retailers, to identify conflict among distribution channel

members of cement and to draw some recommendations.

All these objectives have been achieved in the context of cement industry of

Bangladesh. By following a systematic literature review and conducting survey

on operating companies and their distribution channel members, this study

attempts to achieve these objectives.

This study is, to our knowledge, the first comprehensive review of the factors

bringing together evidence from the fields of purchasing and supply management

and marketing management. The findings of this study may be useful for

marketers as well as distribution and supply chain specialists for formulating

strategies.

Further research on distribution channel members operating across vertical and

horizontal level can be pursued as an extension of this study.

REFERENCES

Arntzen, B. C., Brown, G. G., Harrison, T. P. and Trafton, L. (1995). “Global Supply

Chain Management at Digital Equipment Corporation”, Interfaces, Vol. 25, No. 1

pp.69-93.

Austin, R. D. and Nolan, R. L. (1999). “How to Manage ERP Initiatives”, Harvard

Business School, Cambridge, MA.

Ballaou, H. R. and Srivastava, K. S. (2007). “Business Logistics/Supply Chain

Management”, 5th

edition, Pearson, USA.

Baritz, G. S. and Zissman, L. (1983). “Researching Customer Service: The Right Way”,

Proceedings of the National Council of Physical Distribution Management, Vol. 2

(New Orleans), LA, pp.608-619.

Bovet, D. and Martha, J. (2003). “Supply Chain Hidden Profits”, Mercer Management

consulting, Visit <www.valuenets.com/bookAnSf Preint.pdf>, Retrieved on

August 8, 2013).

Brandes, H. (1994). “Strategic Changes in Purchasing: Two Main Tracks”, European

Journal of ________________

Cavinato, J. L. (1999). “Fitting Purchasing to the Five Stages of Strategic Management”,

European Journal of Purchasing and Supply Management, Vol. 5, pp.75-83.

Chan, F. T. S. (2003). “Performance Measurement in a Supply Chain”, International

Journal of Advanced Manufacturing Technology, Vol. 21, pp.534-48.

Chisnall, P. M. (1985). “Strategic Industrial Marketing”, Prentice- Hall International,

London.

Chopra, S. and Meindl, P. (2007). “Supply Chain Management: Strategy, Planning and

Operation”, Social Sciences Literature Publishing House, Beijing, p.26.

Christopher, M. G., Mckinnin, A., Sharp, J., Wilding, R., Prck, H., Chapman, P., Juttner,

U. and Bolumole, V. (2002). “Supply Chain Vulnerability”, Report for the

Department of Transport, Local Government and the Regions, Cranfield

University, Cranfield.

Das, T. and Teng, B. S. (1998). “Between Trust and Control: Developing Confidence in

Partner Cooperation in Alliances”. The Academy of Management Review, Vol. 23,

No. 3, pp.491-512.

Factors Considered In Business Buying Across Different Levels Of Distribution Channels 95

Das, T. and Teng, B. S. (2003). “Partner Analysis and Alliance Performance”,

Scandinavian Journal of Management, Vol. 19, No. 3, pp.279-308.

Davis, W. H. and Drumm, H. W. (2001). “Logistics Costs and Service 2001”, Annual

Conference Proceedings, (Kansas City, MO: Council of Logistics Management)

Faces, W., Knight, L. and Matthyssens, P. (2001). “Buyer Profiles: An Empirical

Investigation of Changing Organizational Requirements”, European Journal of

Purchasing and Supply Management, Vol. 7, No. 3, pp.197-208.

Fawcett, E. S. and Magan M. G. (2002). “The Rhetoric and Reality of Supply Chain

Integration”, International Journal of Physical Distribution & Logistics

Management, Vol. 32, No. 5, pp. 339-361

Ferguson, B. (2000). “Implementing Supply Chain Management”, Production &

Inventory Management Journal, Vol. 41, pp.64-67.

Gadde, L. E. and Hakansson, H. (1994). “The Changing Role of Purchasing:

Reconsidering Three Strategic Issues”, European Journal of Purchasing and

Supply Management, Vol. 1, No. 1, pp.27-35.

Gulati, R. and Singh, H. (1998). “The Architecture of Cooperation: Managing

Coordination Costs and Appropriation Concerns in Strategic Alliance”,

Administrative Science Quarterly, Vol. 43, No. 4, pp.718-814.

Hakansson, H. and Snehota, I. (1995). “Developing Relationships in Business Networks”,

Routledge, London.

Hakansson, H. and Ford, D. (2002). “How Should Companies Interact in Business

Environments”, Journal of Business Research, Vol. 55, pp.133-139.

Handfield B. R. and Nichols Jr. L. E. (1999). “Introduction to Supply Chain

Management”, Upper Saddle River, NJ: Prentice-Hall, p.2

Holcim (2009). Cement Industry of Bangladesh, Retrieved on November 20, 2009 from

<http:/www.Brand-A.com.bd/>

Hurt, M. D. and Speh, T. W. (1998). “Business Marketing Management: A Strategic

View of Industrial and Organizational Markets”, 6th

edition, The Dryden Press,

Orlando, FL.

Innis, E. D. and LaLonde, J. B. (1994). “Customer Service: The Key to Customer

Satisfaction, Customer Loyalty, and Market Share”, Journal of Business Logistics,

Vol. 15, No. 1, pp.1-27.

Jackson, W. D., Keith, E. J. and Burdick, K. R. (1986). “Examining the Relative

Importance of Physical Distribution Service Elements”, Journal of Business

Logistics, Vol. 7, No. 2, pp.14-32.

Kotler, P. and Armstrong, G. (2010). “Principles of Marketing”, 13th

edition, Prentice

Hall, NY.

LaLonde and Zinszer (1994). “Customer Service: Meaning and Measurement”, Prentice

Hall.

Lambert, M. D. and Harrington, C. T. (1989). “Establishing Customer Service Strategies

within the Marketing Mix: More Empirical Evidence,” Journal of Business

Logistics, Vol. 10, No. 2, p.50.

Lamming, R. C., Caldwell, N. D., Harrison, D. A. and Phillips, W. (2001). “Transparency

in Supply Relationship: Concept and Practice”, Journal of Supply Chain

Management, Vol. 37, No. 4, p.4.

Lee, H. L. and Billington, C. (1995). “The Evolution of Supply Chain Management

Models and Practice at Hewlett Packard”, Interfaces, Vol. 25, No. 1, pp.42-63.

96 D.U. Journal of Marketing, Vol. 16, No. 1, June 2013

Lee, H. L., Padmanabhan, V. and Whang, S. (1997). “The Bullship Effect in Supply

Chains”, Sloan Management Review, Vol. 38 No. 3, pp.93-102.

Malhotra, K. N. (2007), “Marketing Research– An Applied Orientation”, 5th

edition,

Prentice-Hall Inc., NJ.

Marr, E. N., (1994). “Do Managers Really Know What Service Their Customers

Require?” International Journal of Physical Distribution & Logistics

Management’, Vol. 24 No. 4, pp.24 -31.

McAfee, A. P. (1998). “The Impact of Information Technology on Operational

Effectiveness: An Empirical Investigation”, Working paper, Harvard Business

School, Cambridge, MA.

Mentzer, T. J., DeWitt, W., Keebler,S. J., Min, N., Nix, W. N., Smith, D. C. and

Zacharia, G. Z. (2001). “Defining Supply Chain Management”, Journal of

Business Logistics, Volume. 22, No. 2, pp.1-25

Pfeffer, J. and Salancik, G. R. (1978). “The External Control of Organizations: A

Resource Dependence Perspective”, New York: Harper and Row, Purchasing and

Supply Management, Vol. 1 No. 2, pp.77-78.

Ring, P. and Ven de Ven, A. (1992). “Structuring Cooperative Relationships between

Organizations”, Strategic Management Journal, Vol. 13 No. 7, pp.483-498.

Sterling, U. J. and Lambert, M. D. (1989). “Customer Service Research: Past, Present,

and Future”, International Journal of Physical Distribution & Materials

Management, Vol. 19 No. 2, p.17.

Svensson, G. (2004). “Key Areas, Causes and Contingency Planning of Corporate

Vulnerability in Supply Chains. A Qualitative Approach”, International Journal of

Physical Distribution & Logistics Management, Vol. 34 No. 9, pp.728-48.

The Daily Star (2010). “Distribution Channels of the Cement Companies”, Dhaka,

Bangladesh.

Yuva, J. (2002). “Collaborative Logistics: Building a United Network”, Inside Supply

Management, Volume. 13, No. 5, p.50

Zacharia, G. Z. (2001). “Defining Supply Chain Management”, Journal of Business

Logistics, Volume. 22, No. 2, pp.1-25

Factors Considered In Business Buying Across Different Levels Of Distribution Channels 97

APPENDIX

Table 1: Modes of Operation of the Cement’s Distribution channel

Sl. Channel Flow Specification of

Expenses Expense Bearing Entity

1. Cement

manufacturer

to Institutional

Buyers

Transportation Cost Cement manufacturer

Loading and

unloading cost

Cement manufacturer

2. Cement

manufacturer to

Distributors

Transportation Cost Distributors/ Hired transportation

agency

Loading Cement manufacturer

Unloading Distributors/ Transporter

3. Distributors to

Dealer

Transportation Cost Distributors/ Dealers/ Hired

transportation agency

Loading cost Cement manufacturer

Unloading cost Distributors/ Dealers/Hired

transportation agency

4. Distributors to

Retailers

Transportation Cost Distributors

Loading cost Cement manufacturer/ Distributors

Unloading cost Distributors

5. Cement

manufacturer

to Dealers

Transportation Dealers/ Hired transportation agency

Loading cost Cement manufacturer

Unloading cost Dealers/ Transporter

6. Dealers to

Retailers

Transportation Dealers/ Hired transportation agency

Loading cost Cement manufacturer

Unloading cost Dealers/ Hired transportation agency

7. Dealers to End-

user

Transportation Dealers

Loading cost Cement manufacturer

Unloading cost Dealers

Source: Fieldwork Survey

98 D.U. Journal of Marketing, Vol. 16, No. 1, June 2013

Table 2: Highly Preferred Brands by Dealers

Brands

Preference

Rank

Order 1st 2nd 3rd Total

f % f % f % f %

Brand-A 7 16.3 4 13.8 2 9.1 13 13.7 1

Brand-B 9 20.9 1 3.4 1 4.5 11 11.6 2

Brand-C 4 9.3 5 17.2 1 4.5 10 10.5 3

Brand-D 6 14.0 1 3.4 2 9.1 9 9.5 4

Brand-E 5 11.6 2 6.9 1 4.5 8 8.4 5

Brand-F 3 7.0 3 10.3 2 9.1 8 8.4 5

Brand-G 2 4.7 3 10.3 1 4.5 6 6.3 7

Brand-H 2 4.7 0 0.0 3 13.6 5 5.3 8

Brand-I 1 2.3 2 6.9 2 9.1 5 5.3 8

Brand-J 1 2.3 2 6.9 0 0.0 3 3.2 10

Others 3 7.0 6 20.7 7 31.8 17 17.9

Total 43 100 29 100 22 100 95 100

Source: Fieldwork Survey

Table 3: Reasons behind Selling Particular Cement Brands by Dealers

Reasons

Recall Level Rank

Order 1st 2nd 3rd Total

f % f % f % f %

High Sales 21 60.0 4 26.7 0 0.0 25 48.1 1

High Quality 8 22.9 7 46.7 0 0.0 15 28.8 2

High Commission

Rate

2 5.7 1 6.7 1 50.0 4 7.7 3

Good Brand-Image 2 5.7 1 6.7 1 50.0 4 7.7 3

Quick Delivery 2 5.7 0 0.0 0 0.0 2 3.8 5

Transportation

Facility

0 0.0 1 6.7 0 0.0 1 1.9 6

Credit Time 0 0.0 1 6.7 0 0.0 1 1.9 6

Total 35 100 15 100 2 100 52 100

Source: Fieldwork Survey

Factors Considered In Business Buying Across Different Levels Of Distribution Channels 99

Table 4: Most Profit Yielding Brands to Dealers

Brand

Name

Profit Yielding Levels

Rank

Order 1st 2nd 3rd Total

f % f % f % f %

Brand-B 9 21.4 1 6.7 1 20.0 11 17.7 1

Brand-E 5 12.0 2 13.3 1 20.0 8 12.9 2

Brand-D 4 9.5 3 20.0 0 0.0 7 11.3 3

Brand-A 4 9.5 1 6.7 1 20.0 6 9.7 4

Brand-F 4 9.5 0 0.0 1 20.0 5 8.1 5

Brand-H 3 7.1 2 13.3 0 0.0 5 8.1 5

Brand-K 3 7.1 0 0.0 0 0.0 3 4.8 7

Brand-C 1 2.4 1 6.7 0 0.0 2 3.2 8

Brand-I 0 0.0 2 13.3 0 0.0 2 3.2 8

Brand-G 2 4.8 0 0.0 0 0.0 2 3.2 8

Others 7 16.7 3 20.0 1 20.0 11 17.7

Total 42 100 15 100 5 100 62 100

Source: Fieldwork Survey

Table 5: Reasons behind Distributors' Discouragement as perceived by Dealers

Reasons

Recall Level

Rank

Order 1st 2nd Total

f % f % f %

Low Profit 2 25.0 0 0.0 2 22.0 1

Poor Transportation

Facility 1 12.5 0 0.0 1 11.0 2

Low Availability 0 0.0 1 100 1 11.0 2

Others 5 62.5 0 0.0 5 56.0

Total 8 100 1 100 9 100

Source: Fieldwork Survey

100 D.U. Journal of Marketing, Vol. 16, No. 1, June 2013

Table 6: Preference for Various Cement Brands by Retailers

Brands

Preference

Rank

Order 1

st 2

nd 3

rd Total

f % f % f % f %

Brand-B 36 17.4 32 16.1 21 12.2 89 15.3 1

Brand-C 29 14.0 37 18.6 16 9.3 82 14.0 2

Brand-A 25 12.1 24 12.1 14 8.1 63 10.8 3

Brand-H 14 6.8 19 9.5 19 11.0 52 9.1 4

Brand-K 21 10.1 16 8.0 12 7.0 49 8.4 5

Brand-I 12 5.8 7 3.5 13 7.6 32 5.6 6

Brand-F 9 4.3 11 5.5 12 7.0 32 5.6 6

Brand-G 15 7.2 7 3.5 7 4.1 29 4.9 8

Brand-E 12 5.8 6 3.0 8 4.7 26 4.5 9

Brand-J 4 1.9 11 5.5 9 5.2 24 4.2 10

Brand-D 8 3.9 5 2.5 7 4.1 20 3.5 11

Others 22 10.6 24 12.1 34 14.7 80 14.1

Total 207 100 199 100 172 100 578 100

Source: Fieldwork Survey

Table 7: Reasons behind Selling Particular Brands by Retailers

Reasons

Recall Level

Rank

Order 1

st 2

nd 3

rd Total

f % f % f % f %

High Sales 124 70.9 30 29.4 1 5.0 155 52.2 1

High Quality 35 20.0 35 34.3 8 40.0 78 26.3 2

Quick Delivery 4 2.3 11 10.8 2 10.0 17 5.7 3

Good Brand-

Image 5 2.9 7 6.9 4 20.0 16 5.4 4

High

Commission 3 1.7 9 8.8 2 10.0 14 4.7 5

Factors Considered In Business Buying Across Different Levels Of Distribution Channels 101

Reasons

Recall Level

Rank

Order 1

st 2

nd 3

rd Total

f % f % f % f %

Rate

Credit Time 4 2.3 5 4.9 1 5.0 10 3.3 6

Transportation

Facility 0 0.0 5 4.9 2 10.0 7 2.4 7

Total 175 100 102 100 20 100 297 100

Source: Fieldwork Survey

Table 8: Most Profit Yielding Brands to Retailers

Brands

Profit Yielding Levels

Rank

Order 1

st 2

nd 3

rd Total

F % f % f % f %

Brand-B 28 14.6 21 22.3 10 24.4 59 18.0 1

Brand-K 24 12.5 5 5.3 2 4.9 31 9.5 2

Brand-A 15 7.8 5 5.3 5 12.2 25 7.6 3

Brand-C 9 4.7 11 11.7 4 9.8 24 7.3 4

Brand-F 12 6.3 10 10.6 1 2.4 23 7.0 5

Brand-D 15 7.8 3 3.2 4 9.8 22 6.7 6

Brand-G 11 5.7 4 4.3 5 12.2 20 6.1 7

Brand-I 10 5.2 7 7.4 2 4.9 19 5.8 8

Brand-E 9 4.7 6 6.4 3 7.3 18 5.5 9

Brand-H 7 3.6 8 8.5 2 4.9 17 5.2 10

Brand-J 3 1.6 4 4.3 0 0.0 7 2.1 11

Others 49 25.5 10 10.6 3 7.3 62 19.0

Total 192 100 94 100 41 100 327 100

Source: Fieldwork Survey

102 D.U. Journal of Marketing, Vol. 16, No. 1, June 2013

Table 9: Dealers’ Efforts to Induce Retailers to Sell Specific Brands

Brands

Recall Level

Rank

Order 1

st 2

nd 3

rd Total

f % f % f % f %

Brand-B 31 18.1 28 22.8 11 12.8 70 18.4 1

Brand-I 18 10.5 13 10.6 13 15.1 44 11.6 2

Brand-A 24 14.0 8 6.5 8 9.3 40 10.5 3

Brand-C 10 5.9 15 12.2 12 14.0 37 9.7 4

Brand-H 7 4.1 14 11.4 10 11.5 31 8.2 5

Brand-F 9 5.3 8 6.5 7 8.1 24 6.3 6

Brand-K 15 8.8 7 5.6 1 1.2 23 6.0 7

Brand-E 11 6.4 4 3.3 5 5.8 20 5.3 8

Brand-G 10 5.9 5 4.1 3 3.5 18 4.7 9

Brand-D 7 4.1 9 7.3 1 1.2 17 4.5 10

Brand-J 3 1.8 5 4.1 3 3.5 11 3.0 11

Brand-L 2 1.1 0 0.0 1 1.2 3 1.0 12

Others 24 14.0 7 5.6 11 12.8 42 11.0

Total 171 100 123 100 86 100 380 100

Source: Fieldwork Survey

Factors Considered In Business Buying Across Different Levels Of Distribution Channels 103

Table 10: Dealers' Motive to Push Specific Brands to Retailers

Reasons

Motivation Level

Rank

Order 1

st 2

nd 3

rd Total

f % f % f % f %

High Profit 64 46.4 5 10.4 1 11.1 70 35.9 1

High Quality 49 35.5 7 14.6 1 11.1 57 29.2 2

Available 5 3.6 22 45.8 5 55.5 32 16.4 3

High

Commission

Rate

7 5.1 6 12.5 1 11.1 14 7.2 4

Transportation

Facility 4 2.9 5 10.4 0 0.0 9 4.6 5

Others 9 6.5 3 6.3 1 11.1 13 6.7

Total 138 100 48 100 9 100 195 100

Source: Fieldwork Survey

Table 11: Perceived Reasons behind Dealers' Discouragement Stated by Retailers

Reasons

Recall Level

Rank

Order 1

st 2

nd 3

rd Total

f % f % f % f %

low

Availability 34 59.6 1 12.5 1 100.0

36 54.5 1

low Profit 6 10.5 0 0.0 0 0.0 6 9.1 2

Others 17 29.9 7 87.5 0 0.0 24 35.3

Total 57 100 8 100 1 100 66 100

Source: Fieldwork Survey

104 D.U. Journal of Marketing, Vol. 16, No. 1, June 2013

Table 12: Perceived Reasons behind Distributors' Discouragement Stated by

Retailers

Reasons

Recall Level

Rank

Order 1

st 2

nd 3

rd Total

f % f % f % f %

Unavailability 19 44.2 1 33.3 1 100.0 21 44.7 1

Low Profit 10 23.3 0 0.0 0 0.0 10 21.3 2

Low Transportation

Facility 0 0.0 2 66.7 0 0.0

2 4.3 3

Low Commission

Rate 1 2.3 0 0.0 0 0.0

1 2.1 4

Others 13 30.2 0 0.0 0 0.0 13 27.6

Total 43 100 3 100 1 100 47 100

Source: Fieldwork Survey

Table 13: Conflict of Retailers with Cement Companies

Reasons

Recall Level Rank

Order 1

st 2

nd 3

rd Total

f % f % f % f %

Delay in Delivery 31 39.7 13 54.

2 0 0.0 44 41.5 1

Direct Selling to

Corporate Clients 18 23.1 0 0.0 0 0.0 18 17.0 2

Low Commission Rate 10 12.8 2 8.3 0 0.0 12 11.3 3

Delay Payment of

Commission 3 3.8 3

12.

5 1 25.0 7 6.6 4

Forced Decision 5 6.4 0 0.0 0 0.0 5 4.7 5

Others 11 14.1 6 25.

0 3 75.0 20 18.9

Total 78 100 24 100 4 100 106 100

Source: Fieldwork Survey

Factors Considered In Business Buying Across Different Levels Of Distribution Channels 105

Table 14: Retailers’ Expected Service from Cement Companies

Services

Recall Level

Rank

Order 1

st 2

nd 3

rd Total

f % f % f % f %

Timely Cement

Supply 61 46.9 15 34.1 1 11.1 77 42.1 1

Not to Sell Directly

to Other Customers

(Corporate Clients)

23 17.7 9 20.5 1 11.1 33 18.0 2

Timely Payment of

Commission 21 16.2 3 6.8 3 33.3 27 14.7 3

Inform the Qualities

of Cement 6 4.6 2 4.5 2 22.2 10 5.5 4

Not to Force 2 1.5 2 4.5 0 0.0 4 2.2 5

Others 17 13.1 13 29.5 2 22.2 32 17.5

Total 130 100 44 100 9 100 183 100

Source: Fieldwork Survey

Table15: Conflict of Retailers with Dealers

Reasons

Recall Level

Rank

Order 1

st 2

nd 3

rd Total

f % f % f % f %

Unavailable When

Required 24 40.0 3 37.5 0 0.0 27 37.5 1

Force For Payment 8 13.3 1 12.5 2 50.0 11 15.3 2

Higher Price

Charged than Other

Dealers

10 16.7 1 12.5 0 0.0 11 15.3 2

Poor Transportation

Facility 0 0.0 1 12.5 0 0.0 1 1.4 4

Others 18 30.0 2 25.0 2 50.0 22 30.5

Total 60 100 8 100 4 100 72 100

Source: Fieldwork Survey

106 D.U. Journal of Marketing, Vol. 16, No. 1, June 2013

Table 16: Conflict of Retailers with Distributors

Reasons

Recall Level

Rank

Order 1

st 2

nd Total

f % f % f %

Higher Price Charged 8 42.1 1 20.0 9 37.5 1

Unavailable when Required 7 36.8 1 20.0 8 33.3 2

Force for Payment 1 5.3 3 60.0 4 16.7 3

Others 3 15.8 0 0.0 3 12.5

Total 19 100 5 100 24 100

Source: Fieldwork Survey

Table17: Conflict among Retailers

Causes f %

Price Variation 74 81.3

Others 17 18.7

Total 91 100.0

Source: Fieldwork Survey

Table18: Reasons behind Problem with Companies

Reasons

Recall Level

Rank

Order 1

st 2

nd Total

f % f % f %

Delay in Delivery 13 43.3 1 9.0 14 34.1 1

Direct Selling to

Corporate Clients 5 16.7 1 9.0 6 14.6 2

Low Commission Rate 0 0.0 4 36.0 4 9.8 3

Forced Decision 3 10.0 0 0.0 3 7.3 4

Presence of More than

One Dealer or Retailer 3 10.0 0 0.0 3 7.3 4

Factors Considered In Business Buying Across Different Levels Of Distribution Channels 107

Reasons

Recall Level

Rank

Order 1

st 2

nd Total

f % f % f %

Delay Payment of

Commission 1 3.0 0 0.0 1 2.4 6

Others 5 16.7 5 46.0 10 24.4

Total 30 100 11 100 41 100

Source: Fieldwork Survey

Table 19: Stated by Dealers Expected Service from Cement Companies

Services

Recall Level Rank

Orde

r

1st 2

nd 3

rd Total

f % f % f % f %

Timely Cement Supply 9 26.5 12 71.0 0 0.0 21 37.5 1

Timely Payment of

Commission 8 23.5 1 6.0 0 0.0 9 16.1 2

To Inform the Qualities

of Cement 5 14.7 2 12.0 2 40.0 9 16.1 2

Not to Sell Directly to

Other Customers

(Corporate Clients) in

Your Locality

7 20.6 0 0.0 0 0.0 7 12.5 4

Others 5 14.7 2 12.0 3 60.0 10 17.9

Total 34 100 17 100 5 100 56 100

Source: Fieldwork Survey

108 D.U. Journal of Marketing, Vol. 16, No. 1, June 2013

Table 20: Reasons behind Conflict with Distributors Stated by Dealers

Reasons

Recall Level

Rank

Order 1

st 2

nd Total

f % f % f %

Direct Sell to Retailers 3 30.0

3 25.0 1

Unavailable When

Required 2 20.0

2 16.7 2

Higher Price Charged

1 50.0 1 8.3 3

Others 5 50.0 1 50.0 6 50.0

Total 10 100 2 100 12 100

Source: Fieldwork Survey

Table 21: Conflict among Dealers Stated by Dealers

Reasons f %

Price Variation 16 36.4

System 28 63.6

Total 44 100

Source: Fieldwork Survey

Table 22: Factors behind Selection of Retailers by Individual House Builders

Reasons

Recall Level

Rank

Order 1

st 2

nd Total

f % f % f %

Proximity 72 59.0 5 12.0 77 46.7 1

Quick Delivery 14 11.5 16 37.0 30 18.2 2

Large Stock 7 5.7 4 9.0 11 6.7 3

Others 29 23.8 18 42.0 47 28.4

Total 122 100 43 100 165 100

Source: Fieldwork Survey

Factors Considered In Business Buying Across Different Levels Of Distribution Channels 109

Table 23: Factors Considered in Selecting Suppliers by IBs

Reasons

Recall Level

Rank

Order 1

st 2

nd 3

rd Total

f % f % f % f %

Quick

Delivery 14 31.8 7 43.8 0 0.0 21 34.4 1

Low Price 9 20.5 4 25.0 1 100 14 23.0 2

Proximity 9 20.5 0 0.0 0 0.0 9 14.8 3

Large

Stock 3 6.8 1 6.3 0 0.0 4 6.6 4

Others 9 20.5 4 25 0 0.0 13 21.3

Total 44 100 16 100 1 100 61 100

Source: Fieldwork Survey