Roche Pharma Day 2015

Biosimilar market in context

Fermin Ruiz de Erenchun | Global Head Biologic Strategy Team

Pharmaceuticals Division

2

Biosimilars: Ten years in the making

Regulatory environment

Summary

Biosimilars: Ten years in the making

3

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

EU pioneered the biosimilar

concept

– Six products approved, including the first mAb biosimilar (infliximab)

– Uptake did not achieve

saving expectations

WHO leading global efforts; many emerging countries implemented WHO biosimilar guidelines as a reference

US published final biosimilars guideline

– FDA pathway operating, 3 applications pending, one approval

Biosimilar entry timelines delayed (incl. Herceptin & MabThera)

Differential adoption of WHO biosimilar guidelines led to registration of Non-Comparable Biotherapeutic products (NCBs)*, driven by:

– Capacity issues at National

Regulatory Agencies

– Local economic development policies

*For definition and industry position on NCBs please refer to IFPMA Policy Statement:

http://www.ifpma.org/uploads/media/Non-comparable_Biotherapeutic_Products__English__01.pdfr

0.6 6.3

57.0

80 95

119

219

267

317

254

315

377

0

50

100

150

200

250

300

350

400

MAT Jun 2013 MAT Jun 2014 MAT Jun 2015

Sa

les in

CH

Fm

Infliximab

Somatropin

Filgrastim

Epo

Current biosimilar trends

So far, sales have not achieved initial expectations

4

MAT 870 CHFm (June 2015) (CAGR 25.5%)

*Excludes US as no biosimilars have been approved in the US so far (Omnitrope was approved under the 505(b) pathway)

IMS Health; MAT=moving annual total

Generics vs biosimilars

Clear divide in uptake; complex market drivers

0%

20%

40%

60%

80%

100%

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

5

Market share

Zyprexa (Eli Lilly)

Diovan (Novartis)

Filgrastim

EPO

Somatropin

Small molecule

Virtually disappear

Payer driven: 7 biosimilars

Efficacy visible immediately

High turnover of patients

Driven by price and patient offering

9 innovators, one biosimilar

Efficacy visible only longer term

No switching

Sources: IMS Biosimilar Dashboard, IMS & Roche analysis 1 Volume market share based on EU5 average; 2 Volume market share based on average of France & Germany EPO; 3 Data based on % remaining sales in EU

1

1

2

3

3

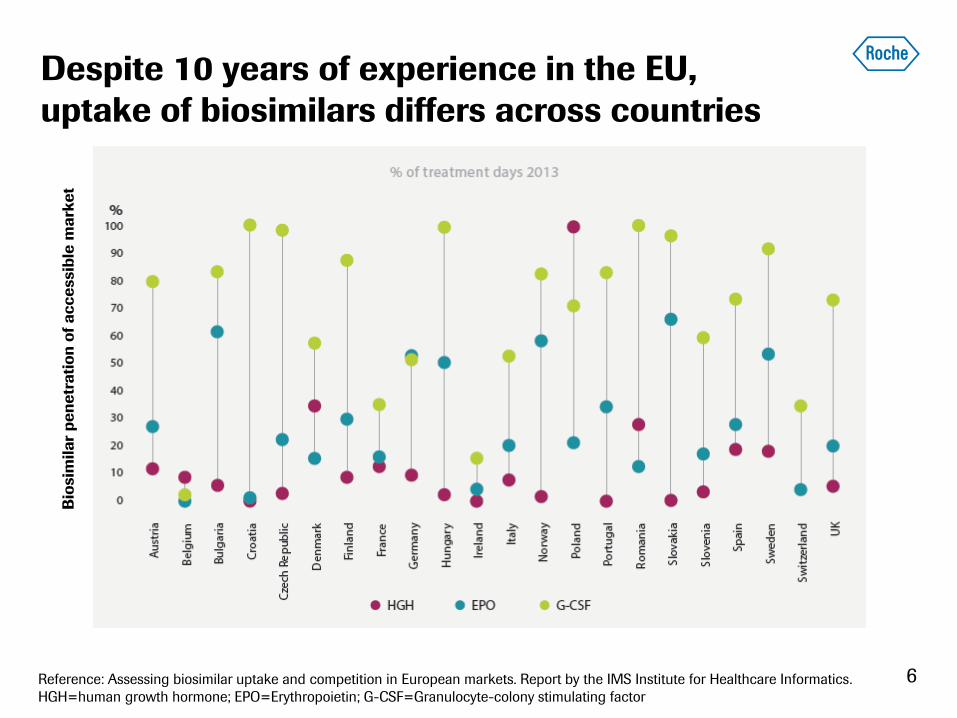

Despite 10 years of experience in the EU,

uptake of biosimilars differs across countries

6

Bio

sim

ila

r p

en

etr

ati

on

of

ac

ce

ssib

le m

ark

et

Reference: Assessing biosimilar uptake and competition in European markets. Report by the IMS Institute for Healthcare Informatics.

HGH=human growth hormone; EPO=Erythropoietin; G-CSF=Granulocyte-colony stimulating factor

Anti-TNF market is not a good analogue for

oncology

7

Anti TNF

Other

biologics

IV Anti-TNF

SC

Anti-TNF

Biological

products used

to treat RA, IDB

& Psoriasis

Infliximab biosimilar could expand beyond it’s accessible market and obtain market

share from Enbrel® and Humira®

Remicade®

Biosimilar accessible market

Small molecules and biologics

Not all the same

• Small molecule policies allow substituting patients only the price counts

• For biologics, European Medicine Agency (EMA) does not provide

guidance on interchangeability and substitution

• Most countries in Europe have specific policies in place to distinguish

between small molecule and biologic medicines

– Biologics must be prescribed by brand name

– Laws against substitution

– Switching remains a physician’s choice

8

Payer environment is one of multiple drivers for

biosimilar uptake

9

Drivers?

Payer environment

Therapeutic area

Innovation and change in

SoC

Physician’s support

10

Biosimilars: Ten years in the making

Regulatory environment

Summary

Biosimilar pathways

in place

Biosimilar pathways

under development

2010 2015

Establishment of biosimilar guidelines has

increased driven by WHO efforts

11

Requirements and study designs are different

for biosimilars vs innovator products

12

Aspects of

development Biosimilar Innovator product

Patient population Sensitive and homogeneous

(patients are models)

Any

Clinical design Comparative versus innovator,

normally equivalence

Superiority vs standard of care

(SoC*)

Study endpoints Sensitive, clinically validated PD

markers

Clinical outcomes data or

accepted/established

surrogates (e.g. OS and PFS)

Safety Similar safety profile to

innovator; no new findings

Acceptable benefit/risk profile

versus SoC*

Immunogenicity Similar immunogenicity profile to

innovator

Acceptable risk/benefit profile

versus SoC*

Extrapolation Possible if justified Not allowed

* In some cases SoC may not exist

How should extrapolation risk be managed?

The regulator’s perspective

13

Analytical

Non-clinical

Clinical

How should extrapolation risk be managed?

The physicians’ perspective

14

Analytical

Non-clinical

Clinical

Analytical

Clinical

Non-clinical

I would like to

see a phase III

trial for each

indication

What is the right patient population to establish

clinical similarity to Herceptin?

15

Topic Metastatic population

(advanced BC)

Neoadjuvant/Adjuvant population

(early BC)

PK Affected by patient`s status & tumor

burden

Homogeneous population can be

selected

PD Clinically validated PD marker not available

Clinical

efficacy/safety • Difficult to select homogeneous group

• Need to control and stratify for multiple

factors (e.g. prior use of chemotherapy,

performance status…)

• Population with heterogeneous

characteristics affecting final clinical

outcome

Populations less likely to be confounded by

baseline characteristics and external

factors

Immunogenicity Immune system affected by performance

status and concomitant chemotherapies

received

Immune system impaired during

chemotherapy cycles, but likely to

recover to normal status thereafter

mBC Phase III Start

Date

Regulatory

Filing

eBC Phase III Start

Date

Celltrion Q2 2010 Q1 2014

Mylan Q4 2012

Pfizer Q4 2013 Q2 2014

Samsung Q2 2014

Amgen Q4 2013

Pfizer

Samsung

2011 2012 2013 2014 2010

mBC

eBC

Initiation of

clinical trial(s)

Celltrion Mylan Pfizer

Celltrion

Amgen

The regulatory thinking is evolving

The Herceptin case

16

17

Biosimilars: Ten years in the making

Regulatory environment

Summary

Generics, biosimilars: Not all the same

18

• Small molecules: Policies allow fast penetration of generics

• Biosimilars: Countries in Europe have specific policies in place to distinguish

between small molecule and biologic medicines

– Biologics must be prescribed by brand name, laws against automatic

substitution, switching remains a physician’s choice, EMA - no guidance

on interchangeability

– After 10 years of experience in the EU, uptake of biosimilars differ heavily

across countries

• Regulatory environment: Still evolving with authorities in the process of finally

establishing frameworks; case by case decisions likely