Download - for any topic contact sandy @ 9136689849

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-

buying bank’s products: Analysis ofcross-selling activities in HSBC

Dissertation submitted to Birmingham City University in

partial fulfilment of the requirements for the degree of

Master of Business Administration

International Business

Prepared By : LijoChirackalManavalan Varghese

Student ID : S11531298

Submission Date: 31st August 2012

S11531298 Page 1

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

TABLE OF CONTENTS

Title page................................................................................................................................i

Table of contents....................................................................................................................ii

List of Figures........................................................................................................................v

List of Abbreviations............................................................................................................. vi

Acknowledgement.................................................................................................................vii

Abstract.................................................................................................................................. viii

Chapter One – Introduction................................................................................................... 1

1.0 Introduction........................................................................................................... 1

1.1 Background of the study....................................................................................... 1

1.2 Research Objectives.............................................................................................. 2

1.3 Rationale of the research....................................................................................... 2

1.4 Methodology......................................................................................................... 3

1.5 Limitations............................................................................................................ 3

Chapter Two – Literature Review..........................................................................................4

2.0 Introduction...................................................................................................................... 4

2.1 Customer Retention and Cross-Buying............................................................................ 4

2.1.1 Customer Retention...................................................................................... .4

2.1.2 Customer’s perception towards cross-buying............................................... .5

2.1.3 Conceptual Model...........................................................................................5

2.1.3.1 Base models for the research.......................................................................8

2.1.4 Factors influencing customer retention.......................................................................... 9

2.1.4.1 Brand, firm’s reputation and expertise....................................................9

2.1.4.2 Service quality, satisfaction and customer retention...................................................9

S11531298 Page 2

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

2.1.4.3 Location convenience. ..............................................................................................10

2.1.4.4Employee’s cultural similarity and Customer retention.............................................10

2.1.5 Factors influencing cross-buying...............................................................11

2.1.5.1 Product quality and cross-buying...........................................................11

2.1.5.2 Perceived convenience............................................................................11

2.1.5.3 Trust and Confidence..............................................................................11

2.1.5.4 Customer’s loyalty towards banks..........................................................12

2.1.5.5 Switching banks and multi-brand loyalty...............................................12

2.1.5.6 Customer relationship with bank............................................................ 13

2.2 Marketing Activities of banks........................................................................................... 13

2.2.1 Marketing Strategy......................................................................................................... 13

2.2.2 Market segmentation.......................................................................................................14

2.2.3 Focus on ethnic groups and cultures...............................................................................14

2.2.4 Branding and relationship..............................................................................................15

2.2.5 Demographic features.....................................................................................................15

2.2.6 Cross-selling activities of banks.................................................................15

2.3 Conclusion..............................................................................................................16

3. Chapter Three – Research Methodology.............................................................................18

3.0 Introduction............................................................................................................18

3.1 Quantitative and qualitative research methods.......................................................18

3.2 Data collection........................................................................................................19

3.2.1 Primary data.................................................................................................20

3.2.2. Secondary data............................................................................................20

3.3 Questionnaire design...............................................................................................20

3.4 Sample method.......................................................................................................22

3.5 Data validity and reliability....................................................................................22

S11531298 Page 3

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

3.6 Limitations..............................................................................................................23

3.7 Ethics in research....................................................................................................23

4. Chapter Four – Research findings and analysis...................................................................24

4.0 Introduction.............................................................................................................24

4.1 Factors influencing customer retention and cross-buying......................................24

4.1.1 Customer retention........................................................................................33

4.1.2 Cross-buying from banks...............................................................................40

4.2 Analysis of HSBC bank’s cross-selling activities...................................................51

Chapter Five – Conclusions and Recommendations................................................................55

5.1 Conclusion..............................................................................................................55

5.2 Recommendations..................................................................................................58

5.3 Limitations of the study..........................................................................................59

5.4 Future research direction........................................................................................60

List of References.....................................................................................................................62

Appendices................................................................................................................................67

Appendix One – Questionnaire forwarded to Banking Customers (Questionnaire 1)..67

Commentary about the Questionnaire1………………………………………..73

Appendix Two – Questionnaire forwarded to HSBC bank (Questionnaire 2)……….78

Commentary about the Questionnaire1……………………………………….78

Appendix Three – Data gathered through Questionnaire 1…………………………..79

Appendix Four – Data collected From HSBC bank through Questionnaire 2……….82

S11531298 Page 4

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

LISTOF FIGURES

Figure 2.1.....................................................................................................................................7

Figure 2.2.....................................................................................................................................8

Figure 2.3.....................................................................................................................................8

Figure 4.1...................................................................................................................................25

Figure 4.2...................................................................................................................................25

Figure 4.3...................................................................................................................................25

Figure 4.4...................................................................................................................................26

Figure 4.5...................................................................................................................................27

Figure 4.6...................................................................................................................................27

Figure 4.7...................................................................................................................................28

Figure 4.8...................................................................................................................................29

Figure 4.9...................................................................................................................................29

Figure 4.10.................................................................................................................................30

Figure 4.11.................................................................................................................................30

Figure 4.12.................................................................................................................................31

Figure 4.13.................................................................................................................................31

Figure 4.14.................................................................................................................................32

Figure 4.15.................................................................................................................................32

Figure 4.16.................................................................................................................................33

Figure 4.17.................................................................................................................................34

Figure 4.18.................................................................................................................................35

Figure 4.19.................................................................................................................................35

Figure 4.20.................................................................................................................................36

S11531298 Page 5

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

Figure 4.21.................................................................................................................................36

Figure 4.22.................................................................................................................................37

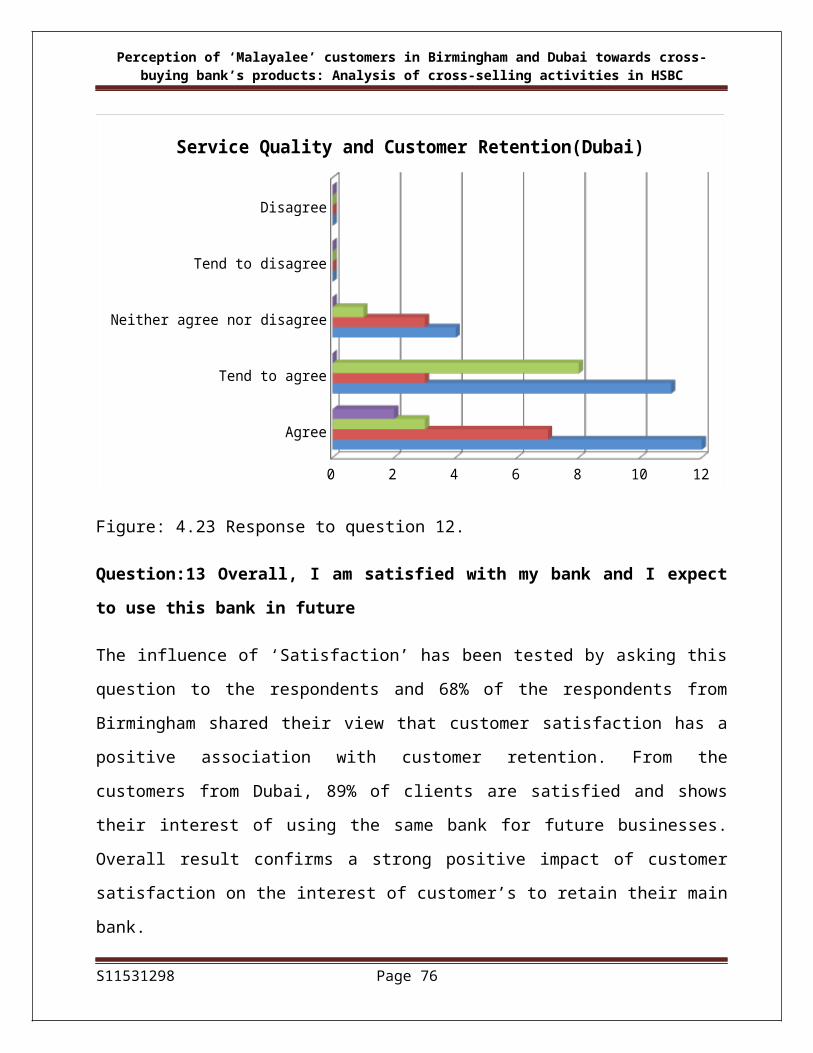

Figure 4.23.................................................................................................................................38

Figure 4.24.................................................................................................................................39

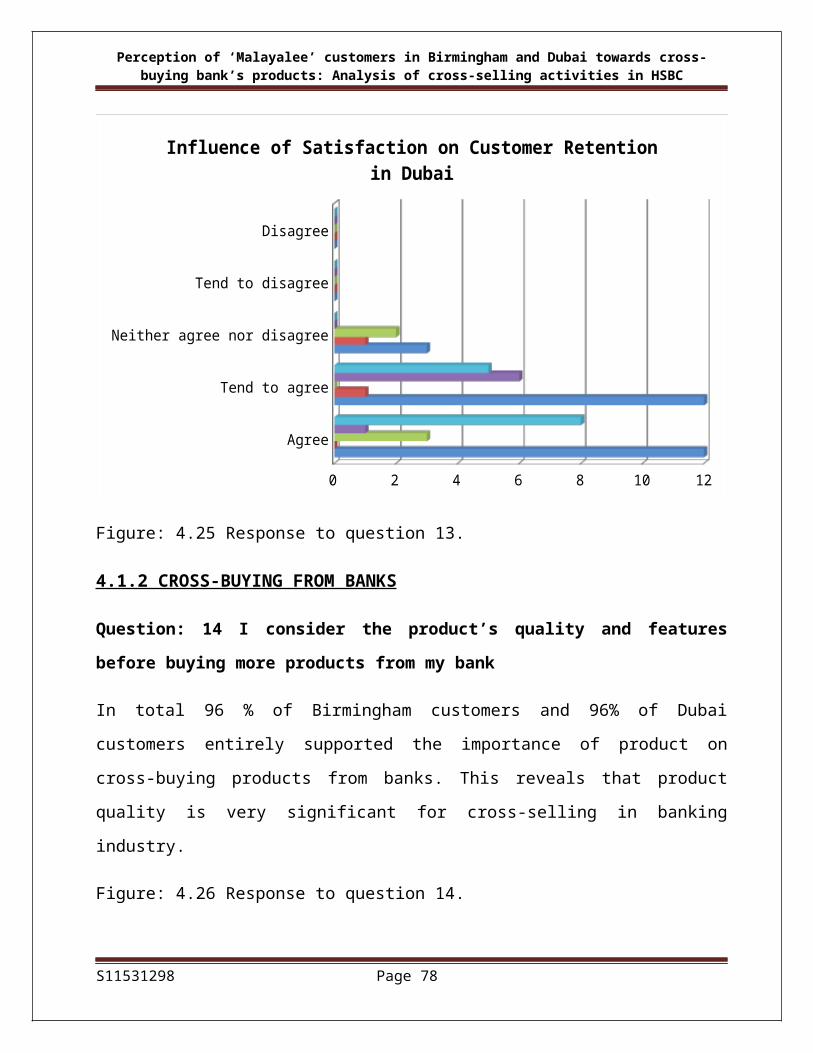

Figure 4.25.................................................................................................................................39

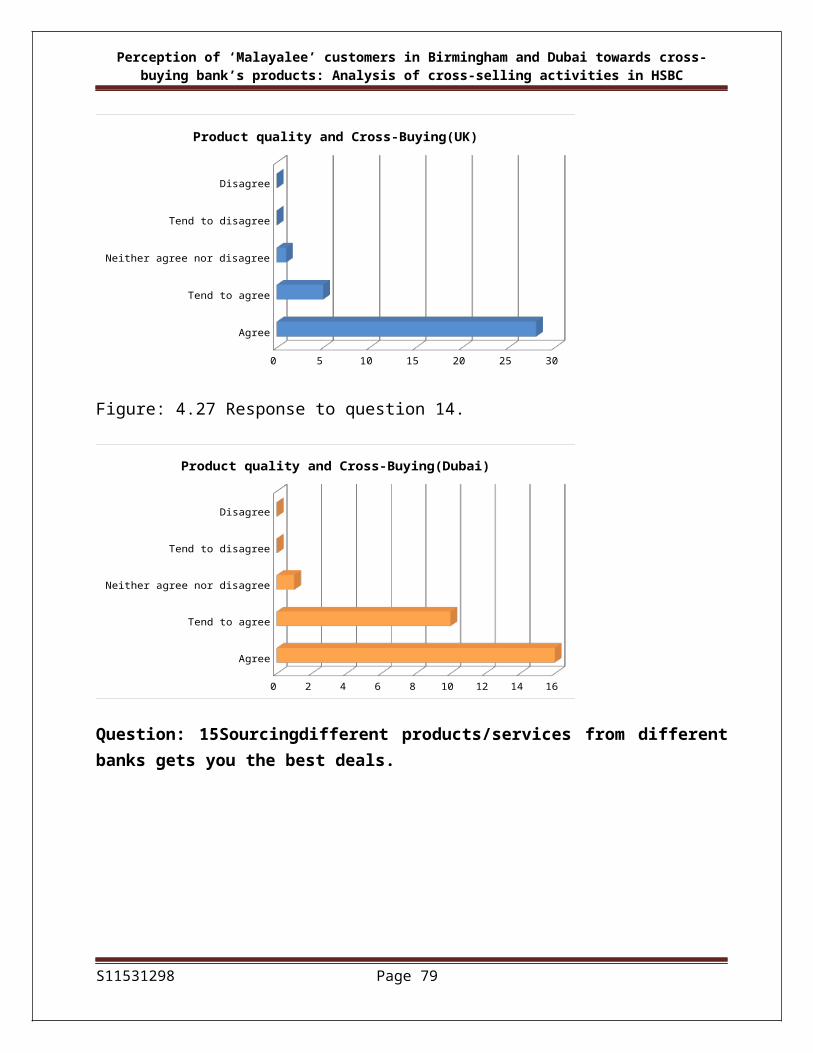

Figure 4.26.................................................................................................................................40

Figure 4.27.................................................................................................................................40

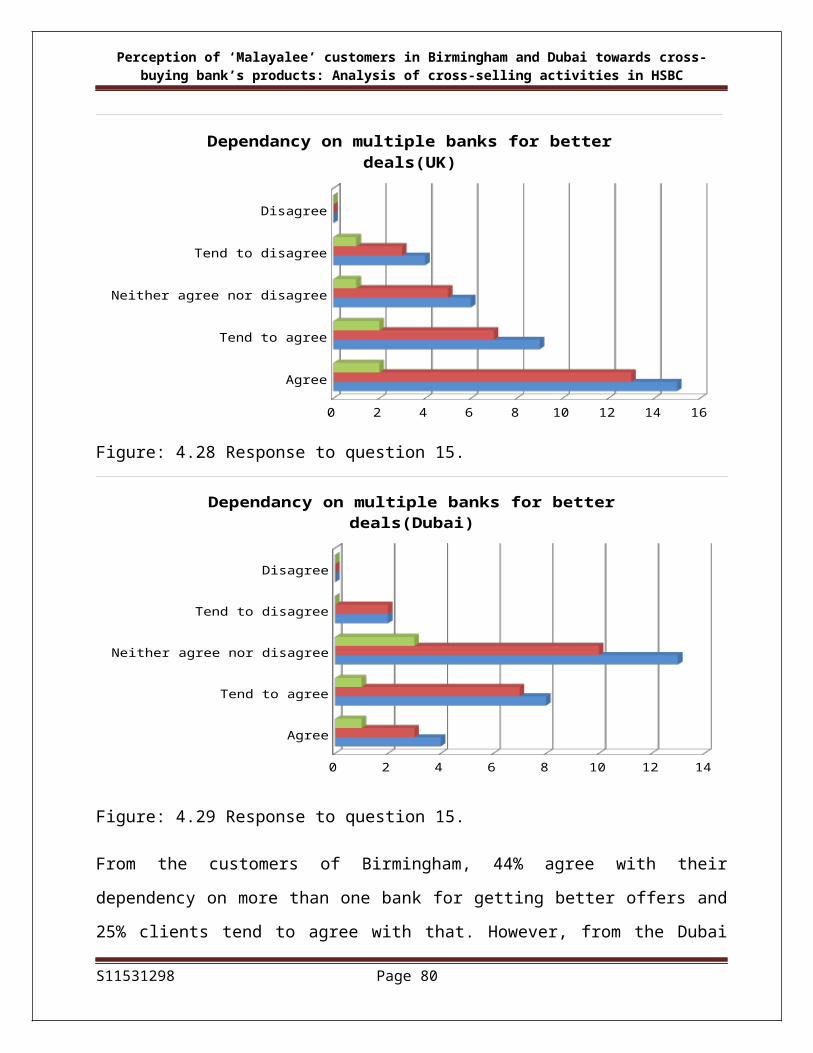

Figure 4.28.................................................................................................................................41

Figure 4.29.................................................................................................................................41

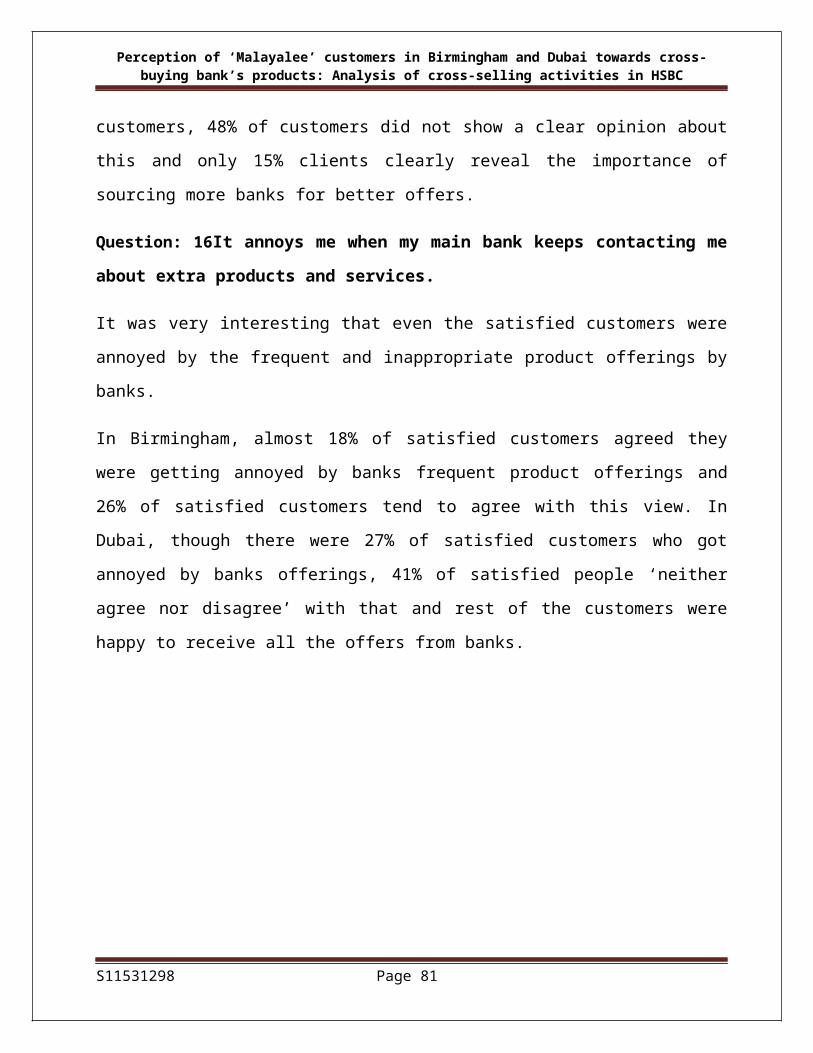

Figure 4.30.................................................................................................................................42

Figure 4.31.................................................................................................................................43

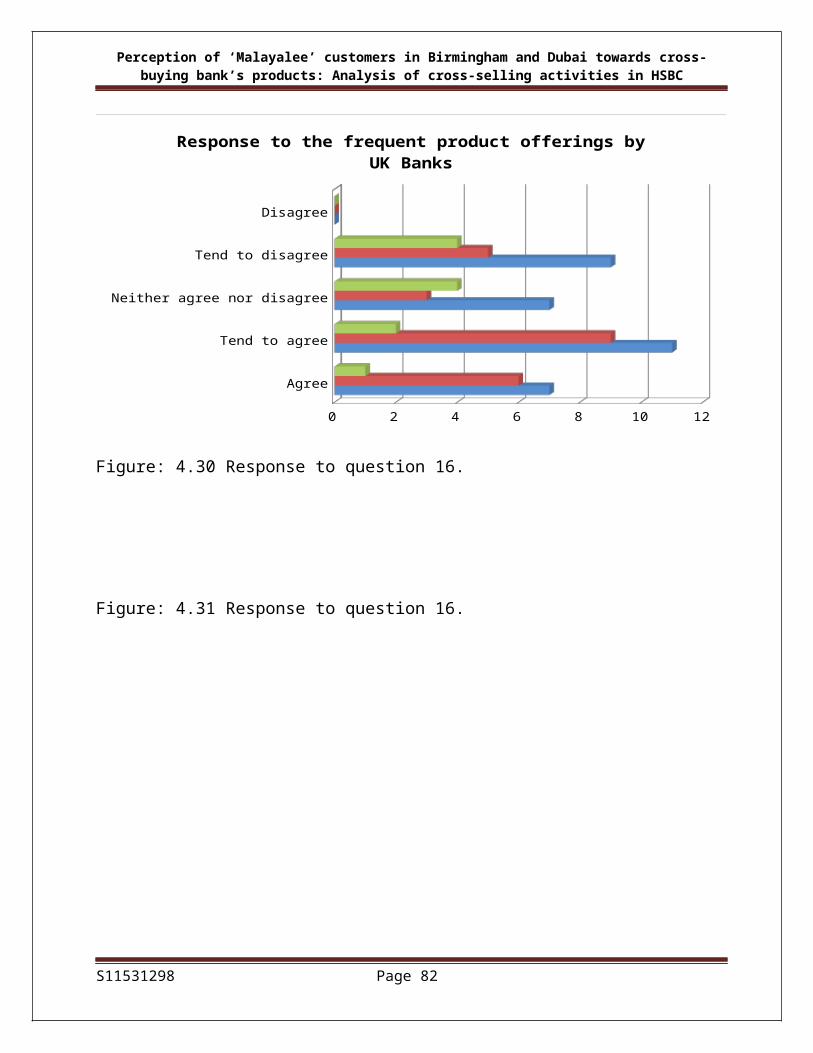

Figure 4.32.................................................................................................................................43

Figure 4.33.................................................................................................................................44

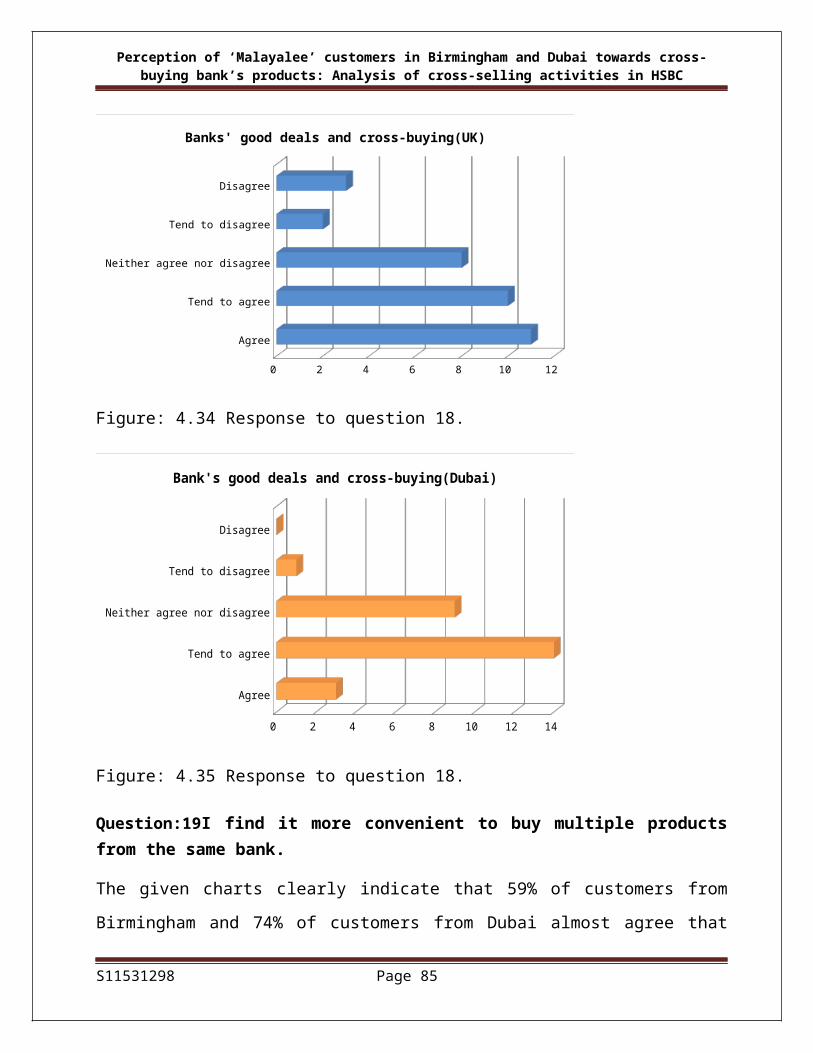

Figure 4.34.................................................................................................................................44

Figure 4.35................................................................................................................................45

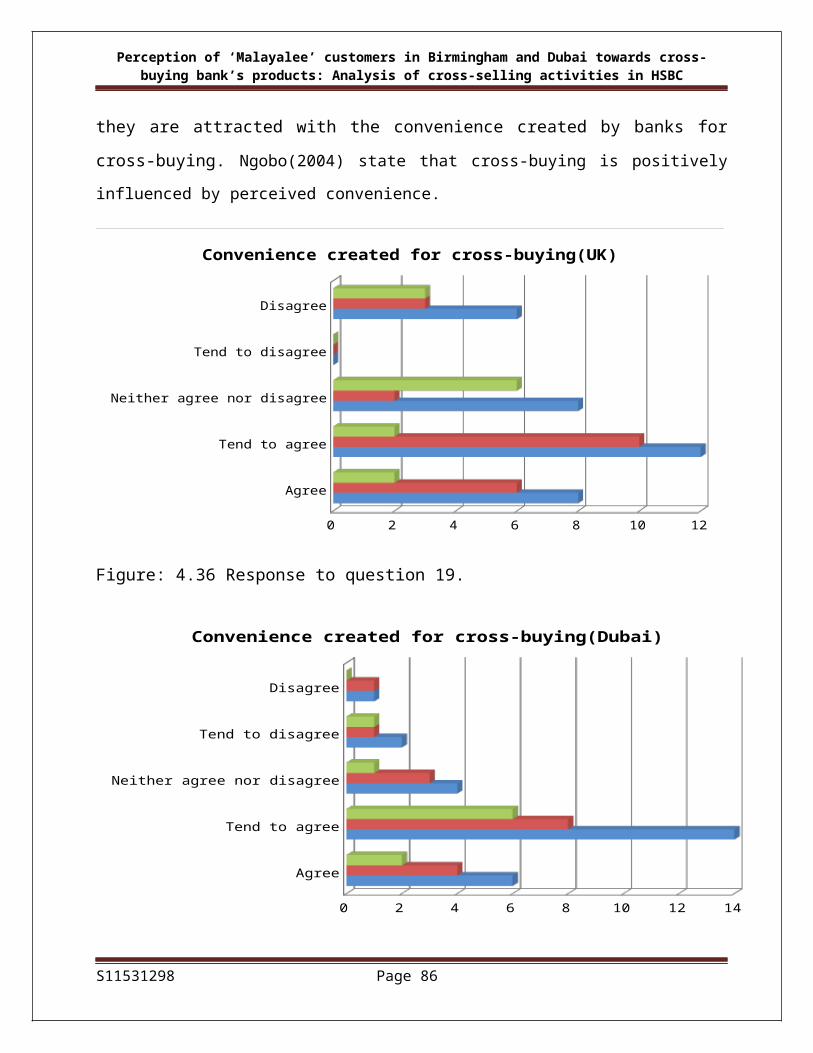

Figure 4.36.................................................................................................................................46

Figure 4.37.................................................................................................................................46

Figure 4.38.................................................................................................................................47

Figure 4.39.................................................................................................................................47

Figure 4.40.................................................................................................................................48

Figure 4.41.................................................................................................................................48

Figure 4.42.................................................................................................................................49

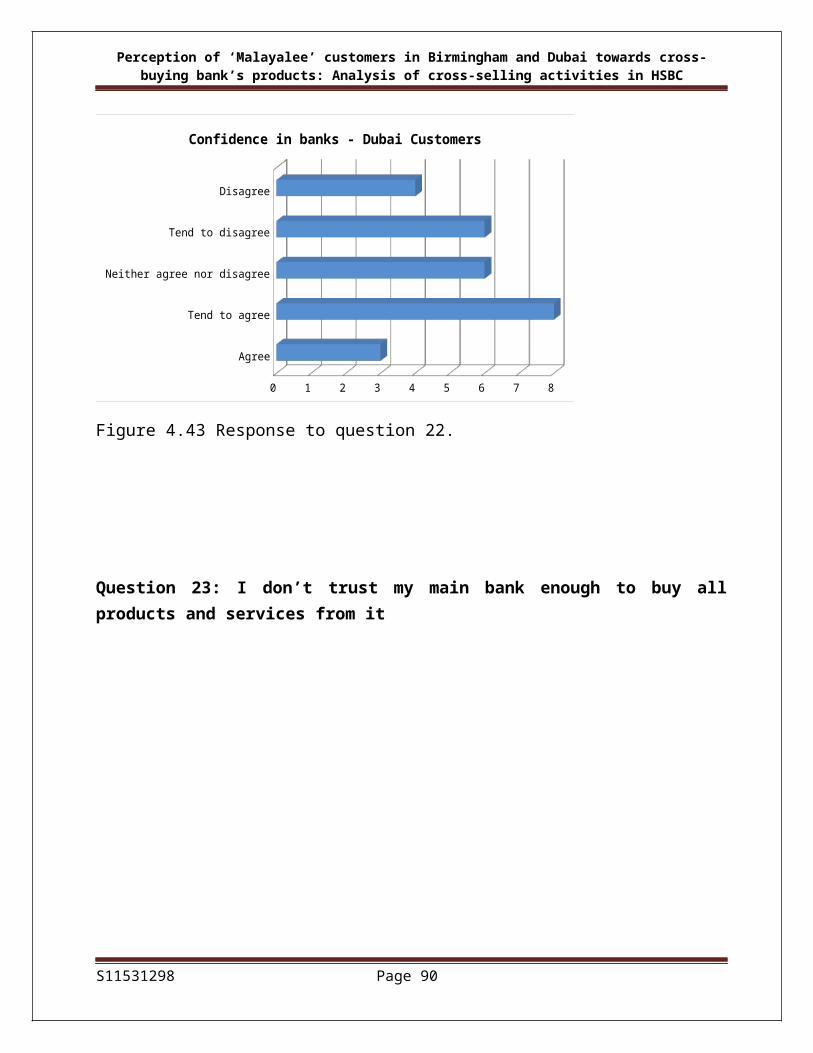

Figure 4.43.................................................................................................................................49

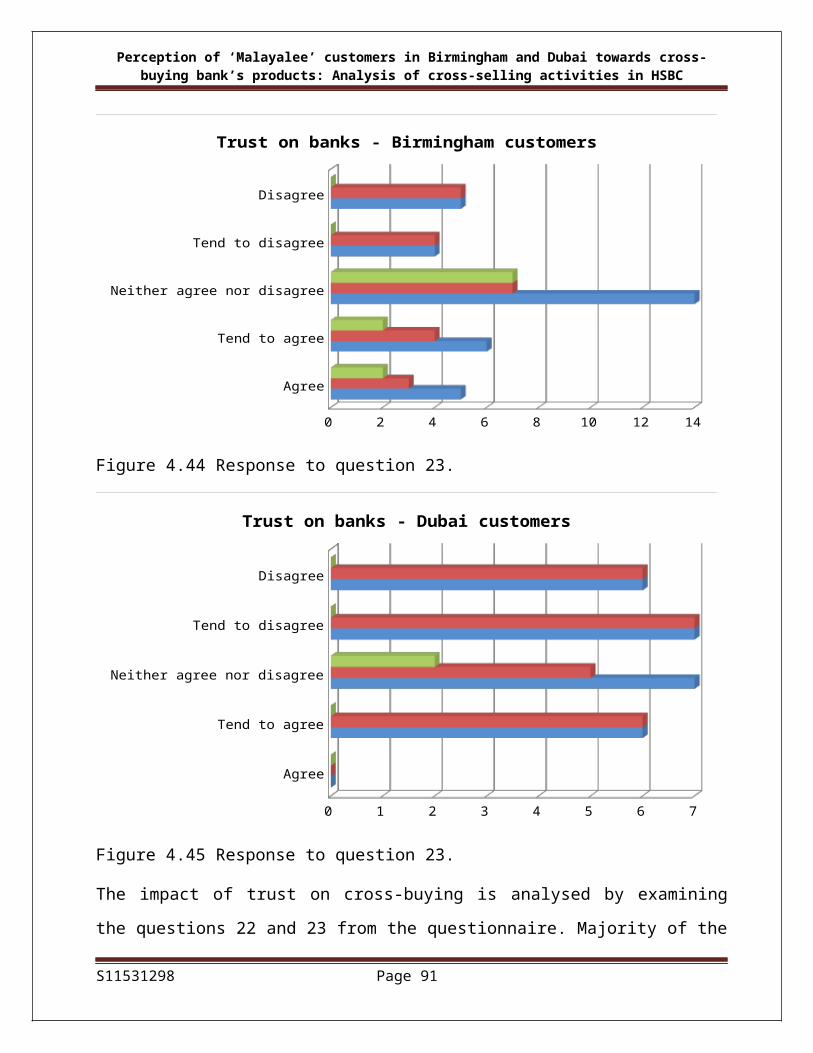

Figure 4.44.................................................................................................................................50

Figure 4.45.................................................................................................................................50

S11531298 Page 6

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

LIST OF ABBREVIATIONS

Malayalee Community- People from the Kerala state in India

UK- United Kingdom

UAE- United Arab Emirates

CRMS- Customer Relationship Management System

INR - Individual Needs Review

S11531298 Page 7

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

ACKNOWLEDGEMENTS

First of all, I give glory to the Almighty God, for granting me the grace, mercy and aptitude to complete this research.

I would like to express my gratitude to my supervisor Dr. Chris Lewis for his quality guidance and encouragement throughout this project.

Finally, I sincerely appreciate all the people participated in the research, for their kind contribution to this research.

S11531298 Page 8

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

EXECUTIVE SUMMARY

Banking customer shold certain perception towards the services of banks and this perception

can influence the banking activities. However, banks have to craft their plans and approaches

in the corporate and national level to become competitive in the industry. The study

investigated the perception of ‘Malyalee’ community in Birmingham and Dubai towards

customer retention and cross-buying from banks. The study also tried to understand the cross-

selling activities of HSBC bank and how they utilise the views of Indian expatriates for

crafting their strategies.

Several literatures of significant studies have reviewed to understand the factors that are

associated with customer retention and cross-buying intentions. The conceptual framework

was created and performed with a critical evaluation of all the models and the factors included

in the conceptual model. This model included bank’s reputation and expertise, service quality,

satisfaction, employee’s cultural similarity and location convenience and tested the impact of

all these factors on customer retention. The association of factors such as bank’s reputation

and expertise, perceived convenience, trust, switching cost and product attributes with cross-

buying are also thoroughly analysed. Bank’s marketing and cross-selling activities, their focus

on ethnic communities, branding and relationship marketing were critically examined through

literature review.

Research administered questionnaires to gather data from banking customers and HSBC bank.

Quantitative data from 61 participants from Birmingham and Dubai were collected and

included the response of a manager in HSBC bank Dubai, which was gathered as qualitative

data through a questionnaire. All these samples selected were self-selection samples and the

questionnaires were forwarded online. Research also made use of some secondary data to

strengthen the research. The views of customers from Birmingham and Dubai are analysed

S11531298 Page 9

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

and compared to know the similarities and differences in their perceptions. The responses

from HSBC bank were also critically examined to generate positive recommendations.

The research revealed that bank’s reputation and expertise, service quality, satisfaction,

employee’s cultural similarity and location convenience have positive association with

customer retention. Cross-buying intentions of customers are positively influenced by bank’s

reputation and expertise, perceived convenience, trust, switching cost and product attributes.

Even many of the satisfied customers are getting annoyed by the improper product offering

methods but most of these satisfied customers trust their banks. The results of this study are

similar to some of the previous studies that tested the same hypothesis and factors in other

countries. This research proposes further research opening in the banking industry to test and

compare the same model in other countries.

S11531298 Page 10

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

1. CHAPTER -ONE 1.0 INTRODUCTION

Globalization has been creating a complete transformation on the world business structure for

the past few decades. In this present scenario, people from different cultures have mixed up in

almost all the regions in the world due to job opportunities in other countries. So in the

banking industry, in order to be very competitive, banks should craft separate business

strategies according to the needs and wants of people from different cultures. Expatriates from

different countries have perceptions towards the banking services; they would be receiving

from foreign banks that are international in nature. The influence of this perception of these

customers has been lifted up by the severe competition between the banks in the international

level. Expatriates have the opportunity to do business with multiple banks, in which they are

satisfied with.

1.1 BACKGROUND OF THE STUDY

Indian expatriates living in UK and UAE, especially ‘Malayalee Community from Kerala state

in India’, are relatively large in number with sufficient income. According to UK labour force

survey 2006, there were 578600 Indian migrants worked in UK (mighealth). It is estimated

that about 1.4 million Indian expatriates residing in UAE and it is over 50% of the total work

force in UAE (Embassy of India), with a high contribution from Kerala people. Banks should

consider these expatriates as long term customers. So it is very significant to perform a

research to investigate about the factors, the ‘Malayalees’ from Birmingham and Dubai

consider for retaining business with a bank and for cross-buying products from the same bank.

Several significant studies have been done to investigate the factors influencing the cross-

buying intentions. Liu & Wu (2007) conducted a research in Taiwan, with the participation of

bank customers who had opened bank accounts. The study by Ngobo (2004) performed in

France analysed the factors, customers consider for retaining relationship with banks and

buying more products from the bank. These researches added value to researcher’s new

investigation to find the perceptions of Malayalee community towards bank’s activities.

S11531298 Page 11

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

Researcher found the importance of analysing the bank’s services for the customers from this

particular group. Banks can improve financial performance by keeping a long term

relationship with these customers. Banks have their own strategies to do business with ethnic

groups. Banks try to cross-sell products that create maximum benefits, and it is significant to

investigate whether banks consider the view of customers for that. Within this context, as an

example the researcher analyses, whether HSBC bank cross-sell their products to the

Malayalee community by considering the expectations of these customers.

The selection of HSBC bank for the research worth, since the excellent performance of HSBC

bank in providing services such as commercial banking, investment banking and wealth

management for its customers enhanced its development in International level (HSBC, 2012).

The motive and interest behind this study is that researcher is a member of ‘Malayalee

community’ and researcher can make use of the work experience in the financial service sector

for the benefits of this community and recommend the best possible ways to HSBC Bank and

other banks, for improving their relationship with customers.

1.2RESEARCH OBJECTIVES

The research has mainly four achievable objectives.

1) To investigate the factors that customers consider as important for retaining banking

with the current bank.

2) To understand the perception of customers towards Cross-Buying bank’s products.

3) Recognize the strategies that has been implemented by HSBC bank, for retaining

customers and for cross-selling its products.

4) To analyse whether HSBC bank make use of the ‘perception of Indian Expatriates

towards bank’s activities’, for retaining them and for cross-selling bank’s products.

1.3RATIONALE FOR THE RESEARCH

Banks are organizations responsible to serve the community, but basically have high power

over their customers (Dash, Bruning&Acharya, 2009). Ethnic minorities living in different

S11531298 Page 12

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

countries have their own views about the banking services. The results of the ample researches

performed in some of the European and Asian countries clearly highlights the important

aspects, customer consider for retaining business with banks and cross-buying. This study

facilitates the banking customers from Malayalee community to express their expectations

about banking services. The perception of these customers towards customer retention and

cross-buying has a great impact on bank’s operations and services. This study is looking

forward to make some theoretical and practical propositions for banks and banking customers.

It is expected that the findings of this research facilitate an opportunity for banks to understand

about the expectations of Malayalee community, to segment this community and craft

marketing strategies specifically for them. Banks can evaluate their existing methods, used for

product offering, customer retention and cross-selling. This would be an opening for banks to

successfully compete in the banking industry and keep these customers loyal, for long term.

1.4METHODOLOGY

This is a concise form of the proposed methodology for this dissertation. To successfully

achieve the objectives of this research, it is intend to collect quantitative data from banking

customers using questionnaire. The research will also gather qualitative data from banks about

their marketing activities and cross-selling strategies, using questionnaire with open ended

questions. The support of relevant secondary data can improve the quality of the research

analysis.

1.5 LIMITATIONS

Researcher is concerned about the anticipated limitations of the study. The first limitation is

expected to be due to usage of self-selection sample, which may lead to biased responses. The

researcher only got the approval for sending questionnaire to HSBC bank, not for an

interview, which will affect the quality of information from the bank.

S11531298 Page 13

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

2. CHAPTER TWO - LITERATURE REVIEW

2.0 INTRODUCTION

This chapter tries to ascertain an understanding of the literature and the major factors that

drive the behaviour of customers for retaining business with banks and cross-buying financial

products from banks. This chapter also performs a critical analysis of the literatures that

describe the marketing and cross-selling strategies of banks.

The important modules covered in the first section of literature review are the influence of

brand on customers, firm’s reputation and expertise, service quality and satisfaction, which are

considered to be the important aspects for customer retention in banks. The literature review

discussed the customer’s trust and confidence on banks, customer’s attractions towards bank’s

innovative products, switching costs, customer’s relationship with banks, loyalty towards

banks and multi-brand loyalty, which are known to be the main factors customers consider for

cross-buying.

The second section of the literature review, basically discussed about the marketing and cross-

selling activities of banks. The literatures that discussed about the branding and marketing

strategies of banks, the segmentation process and relationship banking with the ethnic groups

are extremely integrated in this chapter.

2.1 CUSTOMER RETENTION AND CROSS-BUYING

2.1.1Customer Retention

Customer’s purchase of financial services is based on some important features of customer

behaviour and they consider their own experience and the experience of others in decision

making (Farquhar &Meida, 2010). Customer retention is the measurement of the continuation

of relationship (Liu & Wu, 2007) and appears as the result of recurring decisions by clients.

Kassim&Souiden (2007) discussed the demonstration of customer retention in many ways,

which is to prefer a bank over others and continue business with it or enhancing the deals with

S11531298 Page 14

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

the company in the future with frequent purchasing. The factors influencing the customer

retention are analyzed in details in this literature review.

2.1.2 Customer’s perception towards Cross-Buying

Cross-buying can be explained as the customer’s interest of accepting additional products

from the existing financial service provider (Ngobo, 2004) and cross-buying can be mainly

achieved by extending the firm’s relationship with its customers (Liu & Wu, 2007).Kumar et

al(2008) analysed the drivers for cross-buying with help of the study by Verhoef et al., (2001)

and found the motives as ‘customer’s perception and attitude towards an organization and its

products, socio-demographic characteristics and the marketing effort by the firm’.

Perception of customers on services varies and it can be the perception on a single transaction

as well as the overall perception towards a bank. Zeithaml, Bitner&Gremler(2009). Kumar et

al., (2008) suggests that cross-buying intentions of customers depends on some factors like

customer’s interest on the brand, perceived service quality and the offered value for the

products. Kumar et al., (2008) say that the total cost can be reduced by one-stop shopping,

which influence the customers for cross-buying. Trust and confidence gained by the customers

on the brand and the products are aspects to cross-buy.

2.1.3 Conceptual Model

Many important studies had performed to identify and analyse the factors that influence the

customer retention and cross-buying behaviour of customers. The study conducted by Ngobo

(2004) in France with the participation of 257 clients of major retailing banks in France,

revealed the relation of customer’s cross-buying with the high quality services for different

service actions, customer satisfaction, image conflicts, switching cost and the convenience

received for cross-buying.

Another research conducted by Liu & Wu (2007) in Taiwan, by participating 470 individuals

who had savings accounts with banks, which mainly focused on customer retention and cross-

S11531298 Page 15

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

buying in banking sector. Liu & Wu (2007) found that the aspects such firm’s location,

satisfaction, convenience of single time shopping, firm’s reputation and expertise were significant

for retaining business with the banks. The intentions of cross-buying were based on firm’s

reputation and expertise and customer’s trust on the banks.

Herjanto& Gaur (2011) disclose that customers also consider the cultural similarity of the

banks and the sales person for maintaining the relationship. Since the research is basically

performed with the participation of Indian expatriates living in Birmingham and Dubai, author

is interested to find out the significance of cultural similarity of employees on customer

retention.

Although little has been done to investigate the impact of product attributes and customer’s

cross-buying behaviour, Liang & Wang (2004) states the value of product attributes in

creation of customer satisfaction with the support of research conducted in Taiwan. By

considering this study author is testing the influence of product attributes on cross-buying in

banking industry.

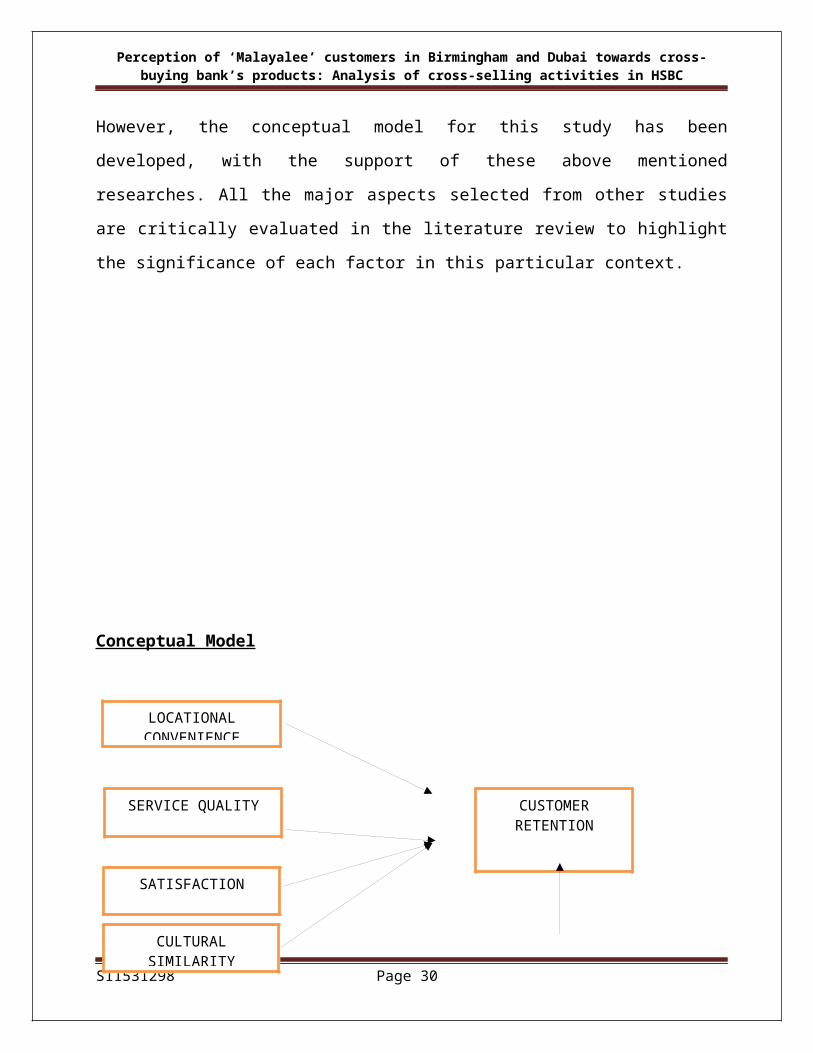

However, the conceptual model for this study has been developed, with the support of these

above mentioned researches. All the major aspects selected from other studies are critically

evaluated in the literature review to highlight the significance of each factor in this particular

context.

S11531298 Page 16

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

Conceptual Model

S11531298 Page 17

LOCATIONAL CONVENIENCE

CUSTOMER RETENTION

SERVICE QUALITY

SATISFACTION

CULTURAL SIMILARITY

FIRM'S REPUTATION AND EXPERTIZE

PRODUCT ATTRIBUTES

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

PERCEIVED CONVENIENCE

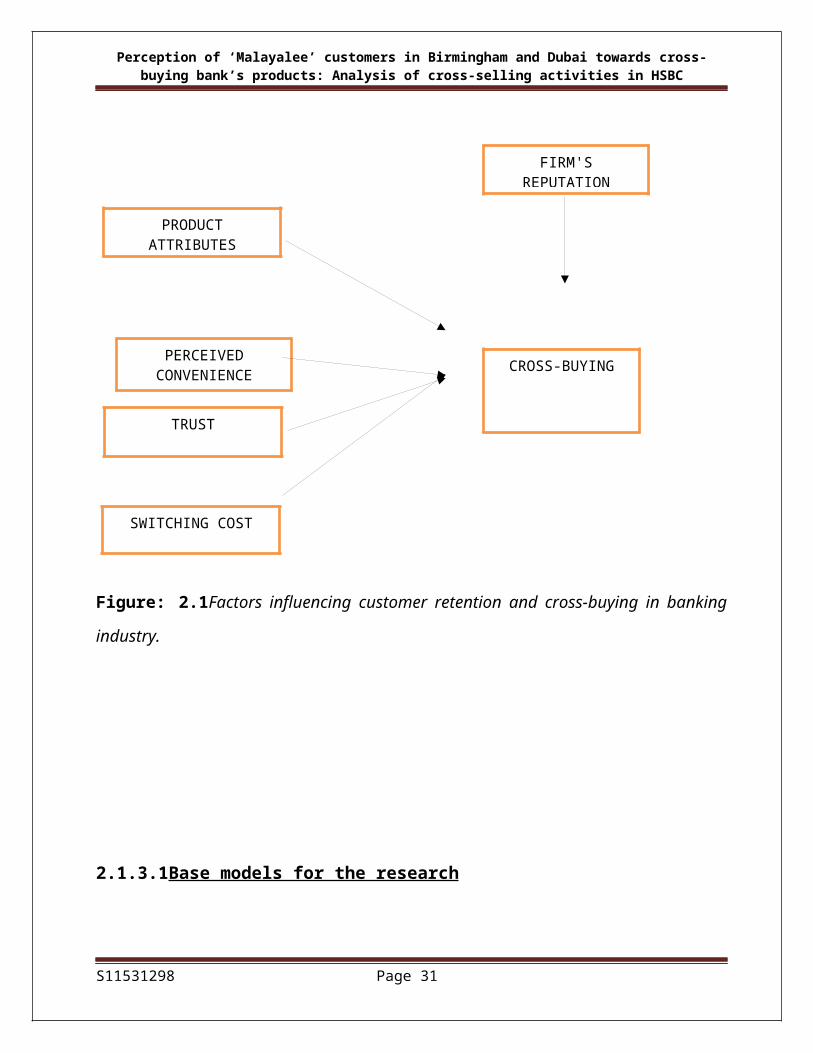

Figure: 2.1Factors influencing customer retention and cross-buying in banking industry.

2.1.3.1Base models for the research

The conceptual model for this research was developed mainly by critically evaluating the

studies by Ngobo (2004) and Liu & Wu (2007).

S11531298 Page 18

CROSS-BUYING

TRUST

SWITCHING COST

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

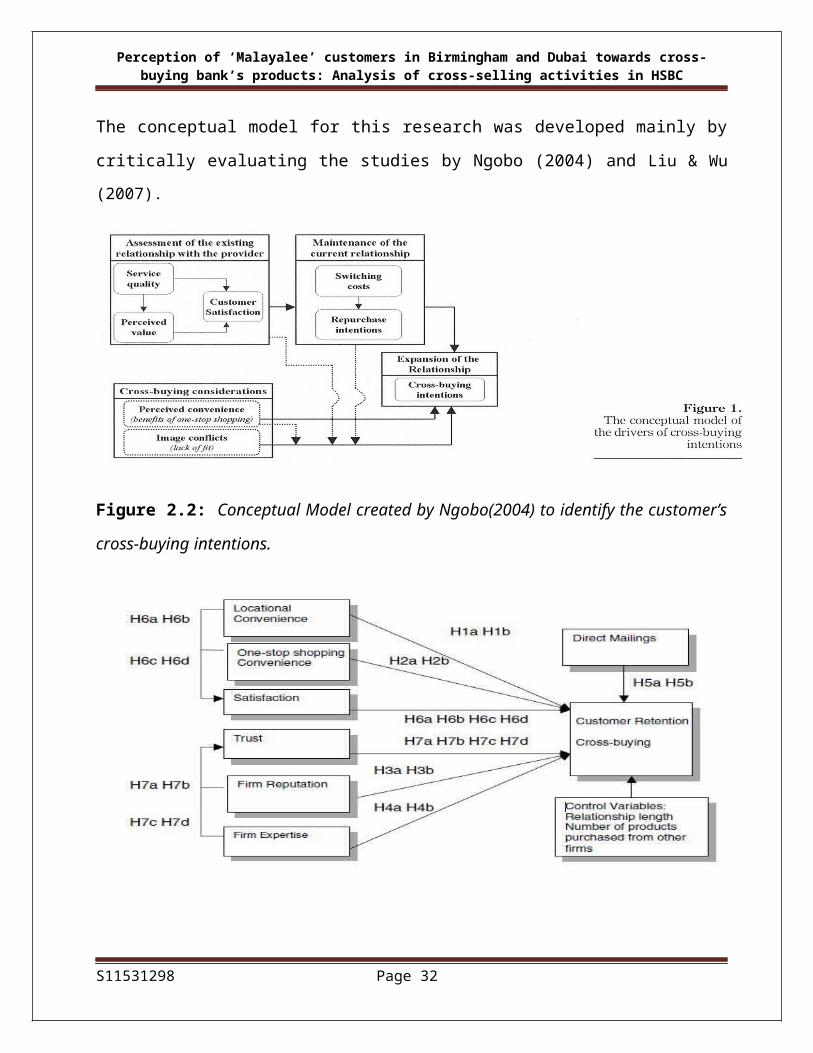

Figure 2.2: Conceptual Model created by Ngobo(2004) to identify the customer’s cross-

buying intentions.

Figure 2.3:Conceptual Model used by Liu & Wu (2007) to investigate about customer

retention and cross-buying.

2.1.4Factors influencing customer retention

2.1.4.1 Brand, Firm’s Reputation and Expertise

S11531298 Page 19

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

Brand is a strong symbol that pushes the customer to purchase goods and services

(Papasolomou&Vrontis, 2006) and the reliance on the same brand will be high for the

customers (Farquhar &Meidan, 2010). This habit of purchase can be assured by keeping

successful brand relationship (Petruzzellis, 2011), which can be achieved through customer

experience and brand knowledge. Tong (2012) states that brand image can be considered as a

switching barrier for the customers.

The reputation of a firm (Liu & Wu, 2007) can be the degree to which a customer feels a

service provider showing the honesty and loyalty towards its customers. Reputation helps

service providers to maintain relationship with customers. Bontis& Booker (2007) reveal the

positive association of customer satisfaction with the corporate reputation.

The level to which a customer recognize sales person to have the required knowledge and

skills to offer products to customers is described as firm expertise (Liu & Wu, 2007). In

contrast to the previous view, Jamal & Anastasiadou (2007) found the result of their study

conducted in Greece that the firm’s expertise is negatively related to customer loyalty . They

realized the customer switching due to the higher expertise level.

2.1.4.2 Service Quality, Satisfaction and Customer Retention

Studies proved that quality perceived by the customer for a product or service and satisfaction

have effect on the repurchase or cross-buying of financial products (Awan et al., 2011). But

there are variations in the views of authors in explaining the relation between service quality

and customer satisfaction. Awan et al., (2011) and Jham& Khan (2009) explained customer

satisfaction is the result of comparison of customer anticipation and the actual attitude after

using the product or service. Awan et al., (2011) cited the concepts of LeBlanc and Nguyen

(1988) to project that the level of customer satisfaction is a factor, which generates the

perceived service quality for a customer. In contrary to the above concept, another view by

Petruzzellis(2011); Yao(2011) that the perceived quality by customer can increase the degree

of satisfaction, and this idea is supported by Ngobo(2004), says that the perceived value

through service quality from firms leads to customer satisfaction.

S11531298 Page 20

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

Kumar et al., (2008) used the study of Verhoef et al., (2001) to state that there is no impact of

differences in satisfaction from multiple firms and the cross-buying intentions of customers.

And analysis of customer satisfaction cannot be done only on the basis of service quality,

since other non-quality dimensions such as needs, equity and self-esteem can create

satisfaction in customers (Awan et al., 2011). These literatures does not make clear that which

aspects mostly lead to customer satisfaction and many of the researches had been performed

by using the most accepted feature “service quality” for analysing customer satisfaction.

2.1.4.3 Location convenience

Location convenience for customers is the perceived level of duration and effort needed to

reach a financial service provider (Liu & Wu, 2007).Liu & Wu (2007) state the direct impact

of location convenience on customer retention. Dusuki and Abdullah (2007) described the

Malasian banking customer’s selection and retention of banks according to the location

convenience. The findings of the research by Jones, Mothersbaugh& Beatty(2003) were against

the previously mentioned view and state that location convenience did not have an impact on the

repurchase intentions of customers in the financial industry

2.1.4.4 Employee’s cultural similarity and customer retention

Customers are interested to do business with banks that hold employees of customer’s own

culture (Herjanto& Gaur, 2011).The similarity of the bank personal in appearance, language,

religion and the social and economic class with the customers make them more relaxed to

amplify the level and number of interaction, which ultimately direct to customer satisfaction.

One of the important studies by Woodside &Devenport (1974) states the impact of similarity in

appearance of sales person and the purchase intentions of customers.

2.1.5Factors influencing cross-buying

S11531298 Page 21

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

2.1.5.1 Product Quality and cross-buying

Customers will purchase new innovative as well as existing products according to the

convenience in purchase, reliability of the product, flexibility, security and easiness of usage

(Marfo-Yiadom, 2012). For instance some customers prefer to cross-buy single as well as

some hybrid insurance products from banks because of the simplicity of products

(Konstantinos, Ioannis&Madalini, 2004). But customers are expected to know about the

product quality, features and availability (Petruzzellis, 2011), banks should define the product

features, differentiation and provide training for using some products to ensure the product

awareness for customers. Papasolomou-Doukakis& Kitchen (2004) say, the chances of

switching the product are high, if the customers are not fully convinced about the quality of

the product.

2.1.5.2 Perceived Convenience

The convenience of one-stop shopping is significant that many clients, who seeks the easy and

cheap method to get the products from the same source (Liu & Wu, 2007). Ngobo(2004) says

the customers are expected to receive the products faster and easier through cross-buying. The

interest of Malasian customers to do business with banks, according to the convenience

created by banks was explained by Dusuki and Abdullah (2007). Customers focused at the

location convenience, convenience and comfort in the office, the product price and overall

cost to retain the bank.Maenpaa&Voutilainen (2011) reveal that the SME customers were not

convinced with the benefits of one-stop shopping convenience offered by banks using their

combined offerings.

2.1.5.3Trust and Confidence

Trust is important in customer relationship and building long term relationship by banks with

its customers minimizes defection levels, reduces cost and maximizes the revenues (Harrison,

2003). Trust can be established and maintained by creating confidence in customers, by

reducing the perceived risk for customers and through communication (Harrison, 2003) with

consistency and integrity (Adamson, Chan &Handford, 2003). Howcroft& Hamilton (2007)

S11531298 Page 22

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

states that customer’s involvement, also the interaction between the bank and customers can

increase confidence in the customers in three different levels. Firstly motivates the person

towards that product, secondly create interest in the differentiable characteristics of that

product and finally increases the significance of product in that particular situation. The

confidence of the customer in their ability can be increased by their participation, which helps

them to purchase the ‘good’ financial products.

Adamson, Chan, &Handford (2003) say that many Hong Kong based banks, including HSBC

have identified the importance of building trust by relationship marketing and diversifying into

personal banking from their conventional style of operations, which was highly corporate and

commercial.

2.1.5.4Customer’s loyalty towards Bank

Insurance is a vital product for the banks and other financial organizations, so in relation to

this literature, Konstantinos et al., (2004) reveal cross-selling insurance products, entirely

depends on the interest and needs of customer’s and banks cannot even change this with their

aggressive style of selling. Tong (2012) insists that loyalty of customers towards banks is

getting reduced due to the chance of maintaining accounts with multiple banks, and customers

seek banks that are service loyal and this notion is supported by Dutta&Dutta (2009). Satisfied

customers are mostly loyal to the banks (Tong, 2012). The loyalty of customers towards a

bank is also determined by the cost to switch (Zeithaml, Bitner&Gremler, 2009) the products

or banks.

2.1.5.5 Switching Banks and Multi-Brand Loyalty

The execution of firm’s strategy may disturb their customers and can move to others, if they

perceive the service quality does not meet their expectations. This concept is been supported

by Sajtos&Kreis (2010) and states that customers shift from single-provider to multi-provider

by considering financial and other relational factors such as satisfaction and switching cost.

S11531298 Page 23

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

Tong (2012) used the concepts of (Beerli et al, 2004) to reveal that customers become more

unwilling to switch to another bank due to the complexity they feel. Switching cost is known

to be one of the reasons to hold dissatisfied customers from switching banks. Colgate & Hedge

(2001) explains the reasons for the switching the firms such as pricing, inconvenience, failures

in core services, service encountering and services recovery and does not explains switching

cost as a motive for switching banks.

2.1.5.6 Customer Relationship by Banks

Banks have to maintain long-term relationship with the customers to increase the satisfaction,

which result in loyalty and repurchases (Martin-Consuegra, Molina & Esteban, 2006). Chantal

Rootman, Tait& Bosch (2008) reveal that bank customers consider the attitude of the

employee in performing the transaction and knowledge of the bank employee in building the

relationship with the banks. Also the customer’s expectation for benefits from the banks will

be high (Martin-Consuegra, Molina & Esteban, 2006) as the result of good relationship.

However Huang & Chia-Yu (2005) cited Kambil and Nunes(2001) to suggests that customers

show doubts and even negative feeling towards the personalization in banking sector. More

over the application of personalization is complex for large number of customers, since it is

difficult to spend much time on single customer and understand their personal needs.

2.2MARKETING ACTIVITIES OF BANKS

2.2.1 Marketing Strategy

There are mainly three competitive marketing strategies used by the banks such as defensive

strategy, offensive strategy and rationalization (Farquhar &Meidan, 2010). Offensive strategy

was commonly used by the banks and experiencing a shift due to the changing economic

conditions. Lymperopoulos (2008) states that bank’s marketing strategy should be proactive

and the price elasticity can be reduced by focusing on quality in service, satisfaction for

customers and customer loyalty. Banks need to analyse their strategic elements such as

technology, bank assurance services and other services that can add value for the customers.

S11531298 Page 24

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

Strategy to increase the quality to these services can improve bank’s overall performance by

cross-selling products, creating employee and thus customer satisfaction (Lymperopoulos,

2008). Papasolomou-Doukakis& Kitchen (2004) reveal that competition between banks

happened through product features, differentiation strategy and also by establishing brand

loyalty.

2.2.2 Market Segmentation

Cameron, Cornish, & Nelson (2006) emphasize the drivers of segmentation in financial

services. They are motives of demand, consumption of financial services and attitudes and

values hold by the customers. The segmentation has to be done individually and in the house

hold level but the performance of the segmentation will be reduced without key data of the

customers. Meadows &Dibb (1998) disclose the claim of many banks that they used

segmentation as a means for discriminating profitable and non-profitable customers. Some

banks even did not attempt to maintain the unbeneficial customers. Meadows &Dibb(1998)

argue that banks can easily collect the necessary information of clients and need to target the

customer’s desires requirements.

2.2.3 Focus on Ethnic Groups and Cultures

Chaudhry& Crick (2004) disclose HSBC banks marketing strategy towards the ethnic Asian

groups. HSBC bank had given the priority to fulfil the needs of Indian and Chinese

communities and the strategy was to target on sub-cultures in those countries. HSBC bank

tried to keep personalized relationship with the customers. Creation of this strong relationship

between employee and customer has been influenced by the national culture of buyer, and the

sub-cultural aspects such as ‘power distance, uncertainty level, individualism/collectivism and

masculinity/feminism (Herjanto& Gaur, 2011). Buyers from these ethnic cultures perform

some assessment on the current experience from the bank and also some enquiry with the

other members. Bankers have to realize this important period of perception building process.

Dash, Bruning&Acharya (2009) states that allocation of service quality factors in banking

sector has been influenced by the customer’s cultural values. At the same time Dash,

S11531298 Page 25

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

Bruning&Acharya (2009) cited Donthoo and Yoo(1998) to say that in most of the cases banks

have high power over their customers. Indian people keep high power distance and banks

should identify the factors such as tangibles time (Dash, Bruning&Acharya ,2009), empathy

and reliability to create satisfaction in Indian customers (Dutta&Dutta, 2009).

2.2.4 Branding and Relationship

Banks have already realized that branding drives the customer’s interest in purchasing

products. UK retail banking performs internal marketing with the help of employees to create

brand awareness and brand differentiation to the employees (Papasolomou&Vrontis, 2006).

The idea of Petruzzellis (2011) agrees this view and suggests that customer’s commitment

and loyalty towards a brand can be achieved by good relationship, rewards and with better

product offers. Lymperopoulos, Chaniotakis&Soureli (2006) highlight the importance of

keeping customer relationship and suggest it as a crucial element of marketing strategy. A

long-term relationship with customers enables bank to get the detailed and valuable

information about the customers to segment and target the customers. A research conducted by

Hanson, Robison & Siles (1996) reveal that the aim of performing advertising and

personalization is to build a perception on the customers that banks care the people of the

community.

2.2.5 Demographic Features

Based on other studies Konstantinos et al., (2004) says that there are aspects such as

customer’s income, education, life cycle; age and gender have impact of customer’s desire of

buying multiple products from financial firms. Even though banks know the importance to

mould their activities based on the views and interests of customers, they have to follow

strategies that creates maximum benefits to them.

2.2.6Cross-selling Activities of Banks

Liang (2008) found the direct relation between the perception of customers and financial

performance of a financial service provider through cross-selling products. This occurs mainly

by retaining the customers who are loyal and encouraged them to cross-buy products by

S11531298 Page 26

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

creating customer’s confidence on the activities of the financial service provider. Ngobo

(2004) support this aspect and says banks should consider the perceptions of customers

towards their products, while offering multiple products. In contrarily to the above concept

Kumar et al.,(2008) suggests that banks generally identify the potential customers from their

existing customer data base for cross-selling, also consider characteristics of products and

customers, firm’s marketing efforts and exchange characteristics. Banks perform these

activities by giving focus to their own strategy to cross-sell the products than giving attention

to the customer interests.

Ngobo (2004) explains that success of the cross-selling is based on the strength of internal

activities and the acceptance of customers for cross-buying from the same financial firm. The

same concept is being explained by Kumar et al.,(2008) says the chances for improving the

effectiveness of cross-selling of products is according to the identification of factors that

motivate the customers to cross-buy the products, also by the efficient marketing activities.

Customers expect valuable and beneficial services from banks (Ngobo, 2004) and it is really

important to make new products and strategic alliances with other financial service providers

to provide the facility of one-stop shopping (Liu & Wu, 2007).

2.3CONCLUSION

Banks judge retaining customers as their strength to improve their overall performance.

Customers are different in nature, characteristics and with their possession; they think and

interpret the activities of these firms in different ways. Customers make use of their

perceptions towards banking activities to select and retain banks and to buy more products

from the same bank.

Several important studies have been done in different countries to identify and analyse the

aspects of customer retention and cross-buying. The research conducted by Liu & Wu (2007)

in Taiwan, by participating 470 individuals, who had savings accounts with banks and the study

conducted by Ngobo (2004) in France with the participation of 257 clients of major retailing

banks in France, tried to investigate the factors that influence the customer retention and cross-

S11531298 Page 27

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

buying behaviour of customers. Soureli& Lewis (2008) study was performed in Greece,

participated 316 real customers to investigate the impact of some factors on customer’s cross-

buying intentions.

The study conducted in UAE by Kassim&Souiden (2007), selected a convenient sample of

600 banking customers to examine the customer retention process. Hong and Lee (2012)

performed the investigation to bring out the main aspects of cross-buying intentions of the

customers from collectivistic cultures.

Even though there were several studies performed related to this research topic, no research

was conducted to understand the interests of Indian Expatriates, mainly Malayalee

community. So it is very significant to fill the existing research gap and to understand the

perception of Malyalee community towards retaining business with their banks and cross-

buying. The research is conducting with the participation of banking customers from

Birmingham and Dubai. This research provides an opportunity for Malayalee community to

express their needs, interests and perception towards banking activities.

Banks are firms which carries high responsibility to serve the community, while achieving the

financial strength. So the effort of Chaudhry& Crick (2004) to identify HSBC bank’s

marketing strategies towards the Asian Ethnic cultures contributed knowledge to the

academics. The attempt to analyse the way in which HSBC bank craft their strategies for

doing business with the Malaylee community in Birmingham and Dubai, add great value to

this research.

S11531298 Page 28

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

3. CHAPTER THREE – RESEARCH METHODOLOGY

3.0 INTRODUCTION

Different forms of research methods are suggested by academics for performing successful

researches. This chapter discusses various approaches that the researcher had used for

conducting the research work and the justification for the application of those methodologies.

This research used a mixed application of both quantitative and qualitative research methods.

Researcher collected primary data using questionnaires, also collected relevant secondary data

to support the research (Saunders et al., 2009).

The main achievable objectives of this research are listed below.

1) To investigate the factors that customers consider as important for retaining banking

with the current bank.

2) To understand the perception of customers towards Cross-Buying bank’s products.

3) Recognize the strategies that has been implemented by HSBC bank, for retaining

customers and for cross-selling its products.

4) To analyse whether HSBC bank make use of the ‘perception of Indian Expatriates

towards bank’s activities’, for retaining them and for cross-selling bank’s products.

Research methodology chapter is developed by consider the best ways to achieve the

objectives.

3.1 QUANTITATIVE AND QULAITATIVE RESEARCH METHODS

Quantitative data are output of research strategies and the application of data varies from

counting some frequencies to multifaceted statistical comparisons (Saunders et al., 2009;

Creswell, 2009). Quantitative data may not always ensure the meaning which is expected but

the quantitative data collected for this research was useful and provided meaning to the

figures.

S11531298 Page 29

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

Saunders et al., (2009) reveal that qualitative data should be used to provide meaning for more

uncertain, flexible concepts. Qualitative data are collected as non-standardised data, which are

classified and analysed later. The analysis part mainly includes summarising, categorising and

structuring the collected data.

The participants of this research are the banking customers from Birmingham, Dubai and one

manager from HSBC bank Dubai. In order to achieve the first and second objectives of this

study, that is to understand the view of customers about retaining the bank and cross-buying

products from the same bank; author used a self-administered questionnaire to collect the

responses quantitatively. Saunders et al., (2009) explained that the application of questionnaire

for collecting opinions or attitudes will facilitate the researcher to identify and explain the

variation in different incidents.

In the second part of the research, for accomplishing the research objectives three and four,

that is to collect a detailed information about the marketing approaches and cross-selling

activities of HSBC bank, qualitative data were gathered from the HSBC bank manager using a

questionnaire that included open ended questions. Even though ‘semi-structured one–one

interview’ with many HSBC bank managers from Birmingham and Dubai was the best option for

data collection from HSBC bank, the inaccessibility to the senior employees for the interview

forced the researcher to forward questionnaire to only one manager in Dubai.

3.2 DATA COLLECTION

Data can be collected for researches from primary and secondary sources in the form of

primary and secondary data. Many valid documents such as Government publications,

previous research or any service records can be used as secondary sources. Primary data can

be collected with different methods such as Observation, Interviewing and Questionnaire

(Kumar, 2005).

S11531298 Page 30

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

3.2.1 Primary Data

Research was based on the customers’ perception towards services of banks and therefore a

primary data collection was necessary to achieve the objectives. Even though, for this study,

researcher was not experienced in primary data collection process, availability of reliable and

valid data from a reasonably strong sample, boosted confidence of the researcher to perform

the primary data collection. Quantitative and qualitative data were collected through

questionnaires.

3.2.2 Secondary Data

Kumar (2005) categorizes the secondary sources of data collection mainly as Government or

semi-government publications, previous research, personal information and Mass media.

Kumar (2005) also reveals the disadvantages of secondary data. There might be problems in

the validity and reliability of secondary data collected.

The merits and demerits of using primary and secondary data for this research had been

analysed and focused mainly on the primary data collection sources. Questionnaires were used

to collect primary data from both banking customers and one bank manager, also made use of

HSBC bank’s website and other relevant information sheet from HSBC as secondary data.

3.3 QUESTIONNAIRE DESIGN

Saunders et al. (2009) suggest that questionnaires can be used for descriptive research which

includes ‘attitude and opinion questionnaires’ and to understand the organizational

approaches.

Research used self-administered questionnaires (Saunders et al., 2009) for understanding the

view of banking customers about cross-buying financial products. Firstly, for analysing the

attitudes of customers on services, researcher used ‘rating questions’ to get the necessary data.

This questionnaire was mainly included with ‘Likert-style rating scale’ questions and some

‘category’ questions (Saunders et al., 2009).

S11531298 Page 31

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

Finally for collecting the response of HSBC bank on their cross-selling activities, researcher

made use of a questionnaire with only ‘open-ended questions’ to get detailed information on

the particular aspect.

An online survey method ‘Google Document’ was utilized for creating questionnaires to gather

data. Two questionnaires were created, the first one for collecting the views of banking customers

and the second questionnaire for gathering information from HSBC bank. The permission to use

the e-mail addresses of the participants was collected through telephony conversation and e-

mails.The web links of the questionnaires were then forwarded through e-mail along with a

covering letter to the focused respondents in Dubai and Birmingham and HSBC bank in

Dubai. This online method facilitated an opportunity to reach more number of respondents.

The proper and regular follow-up through telephone calls and e-mails helped the researcher to

achieve a good response rate for a successful research, within the limited time period.

Some of the most important questionsfrom questionnaire ONEis included in the methodology

chapter. All the details of questionnaire ONE and questionnaire TWO with the supporting

studies are included in the Appendices.

Question 9: My bank’s reputation and expertise create interest to continue with the bank.

Liu & Wu (2007) researched the relationship of location convenience, firm reputation and firm

expertise with customer retention and confirmed that there is a direct relationship between them.

Question 13: Overall, I am satisfied with my bank and I expect to use this bank in future.

Ngobo(2004) studied the relationship of service quality and satisfaction with the repurchase

intentions.Liu& Wu(2007) also states that there is a positive relation between satisfaction and

customer retention.

S11531298 Page 32

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

3.4 SAMPLE METHOD

The self-selection sampling method was used (Saunders et al., 2009) for selecting the

participants for the survey, which gathered customer’s view on cross-buying. Self-selection

sampling is a non-probability sampling technique and researcher had published the needs to

the respondents by e-mails and telephone and requested them to participate in the survey.

From the responded people, 60 customers were selected from Birmingham and included 50

participants from Dubai for the research. The main advantages due to self-selection sampling

are the choice of employed customers, participation of enough male and females and a fixed

sample size for the research.

Researcher targeted the participants as the ‘Malayalee community’ from Indian Expatriates,

who living in Birmingham and Dubai. For completing the second section of the research,

according to the convenience, permission was taken from one manger from HSBC bank to

forward a questionnaire. Main aspects considered for selecting these fixed sample sizes

include the ‘time constraints’, the need of quick results (Saunders et al., 2009), the confidence

to test the research results and to maintain the accuracy level for the research (Kumar, 2005).

The data validity is considered to be high, since the participants from targeted group have

sufficient income, regularly performs banking transactions and had the previous experience of

cross-buying from banks.

The disadvantage of using non-probability sample is that the findings cannot be generalized to

the total sampling population and the accessible individual may not truly represent the total

sample population.

3.5 DATA VALIDITY AND RELIABILITY

There are mainly three types of validity to be considered for a research (Saunders et al., 2009;

Kumar, R., 2005). They are mainly content validity, predictive validity and construct validity.

Saunders et al. (2009) state that internal validity of a research is the capability to appraise the

intended output, which can be achieved either through questionnaires. The predictive validity

of the research is very low since the research does not focussed entirely on the future activities

S11531298 Page 33

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

of customers and banks to predict the real outcome. Research examined the contribution of

different factors that motivates the customers for cross-buying bank products and calculated a

high variance towards the construct.

Kumar (2005) says that the reliability of a research tool is the consistency and the stability in

predicting accurate data for achieving the objectives. Saunders et al. (2009); Kumar (2005)

suggests the main approaches to determine the reliability of data collection tool. They are

‘test-re-test approach, internal consistency approach and alternative form approach.

3.6 LIMITATIONS

The responses from the self-selection sample, which includes the friends and relatives of

researcher, might generate a biased view. The responses might not be true, but exaggerated to

demonstrate their strength on their opinions. HSBC bank responded to the questions related to

their present marketing strategies and researcher doubts the chances of amendments by bank,

in their responses.

The application of questionnaire instead of semi-structured one-one interviews, affected the

coverage and quality of the collected data from HSBC bank that ultimately reflected on the

final objectives. The incapability of the researcher to perform the ‘test re-test and alternative

form’ approaches (Saunders et.al., 2009; Kumar, 2005) for ensuring the reliability of research,

limited its reliability and validity.

3.7 ETHICS IN RESEARCH

Research ethics are related to “the questions about how we formulate and clarify our research

topic, design our research and gain access, collect data, process and store our data, analyse data

and write up our research findings in a moral and responsible way” (Saunders et.al., 2009 : 184).

The personnel information and research data collected from the participants have been highly

private, protected and can be destroyed immediately after the necessary period. The participants

have had the right to withdraw the complete information if necessary. The research survey would

be completed inside the Birmingham City University’s ethical procedures.

S11531298 Page 34

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

4 CHAPTER FOUR–RESEARCH FINDINGS AND DATA ANALYSIS

4.0INTRODUCTION

The primary data collected using the questionnaire and the secondary data gathered are examined

to test the conceptual model created for this research. Author refers to the relevant sections of

literature review to compare its results with the findings of the previous studies.

Two questionnaires were created using the ‘Google Documents’ and the web links were forwarded

to collect the responses. First questionnaire was used to gather the views of bank’s customers

about cross-buying products. This questionnaire included 23 relevant questions to get the answers

to achieve the research objectives. The questionnaire had sent to a convenient group of

respondents, about 110 from Dubai and Birmingham.

A questionnaire with 10 valid questions was used to gather the response from HSBC bank, Dubai.

Even though HSBC bank only answered SIX questions, their responses included answers for all

the 10 questions and the support of relevant secondary data had improved the credibility of the

analysis of HSBC bank’s cross-selling activities. Microsoft office was used to represent and

analyse the collected data.

4.1 FACTORS INFLUENCING CUSTOMER RETENTION AND CROSS-BUYING

The research intensely analyses all the 23 questions from the ‘First questionnaire’ to interpret

the factors customers consider for retaining banks and cross-buying products. From the overall

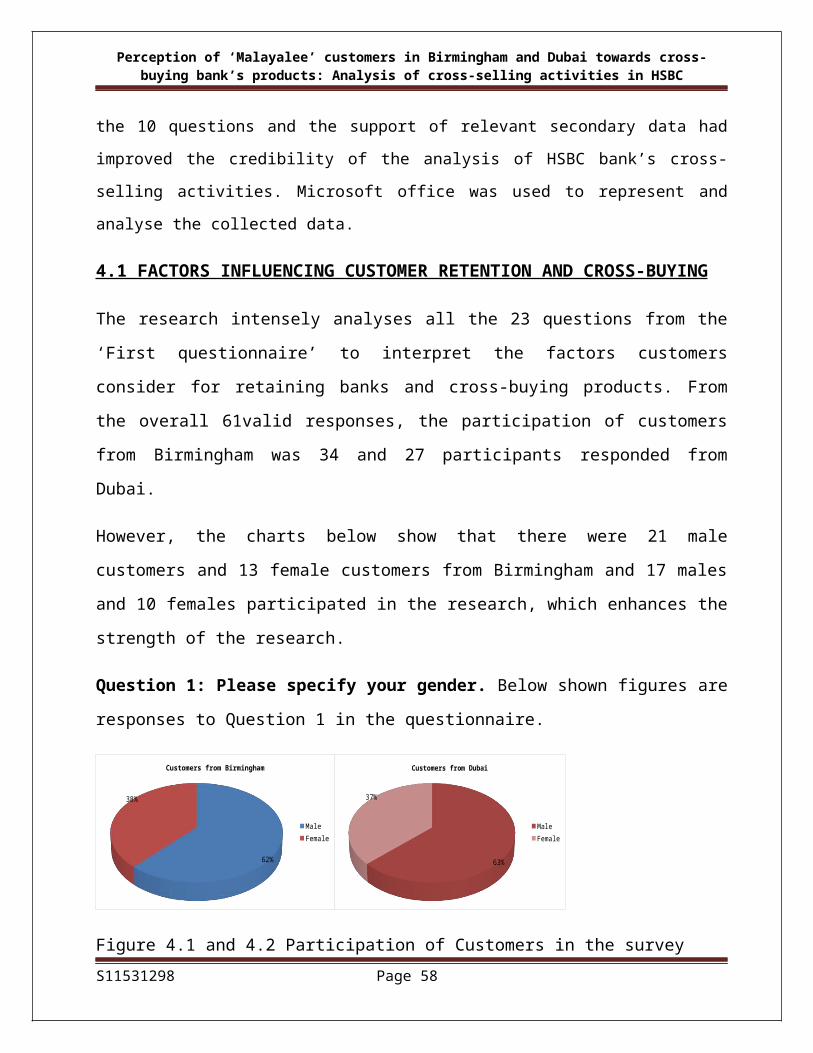

61valid responses, the participation of customers from Birmingham was 34 and 27 participants

responded from Dubai.

However, the charts below show that there were 21 male customers and 13 female customers

from Birmingham and 17 males and 10 females participated in the research, which enhances

the strength of the research.

Question 1: Please specify your gender. Below shown figures are responses to Question 1 in

the questionnaire.

S11531298 Page 35

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

62%

38%

Customers from Birmingham

Male Female

63%

37%

Customers from Dubai

MaleFemale

Figure 4.1 and 4.2 Participation of Customers in the survey

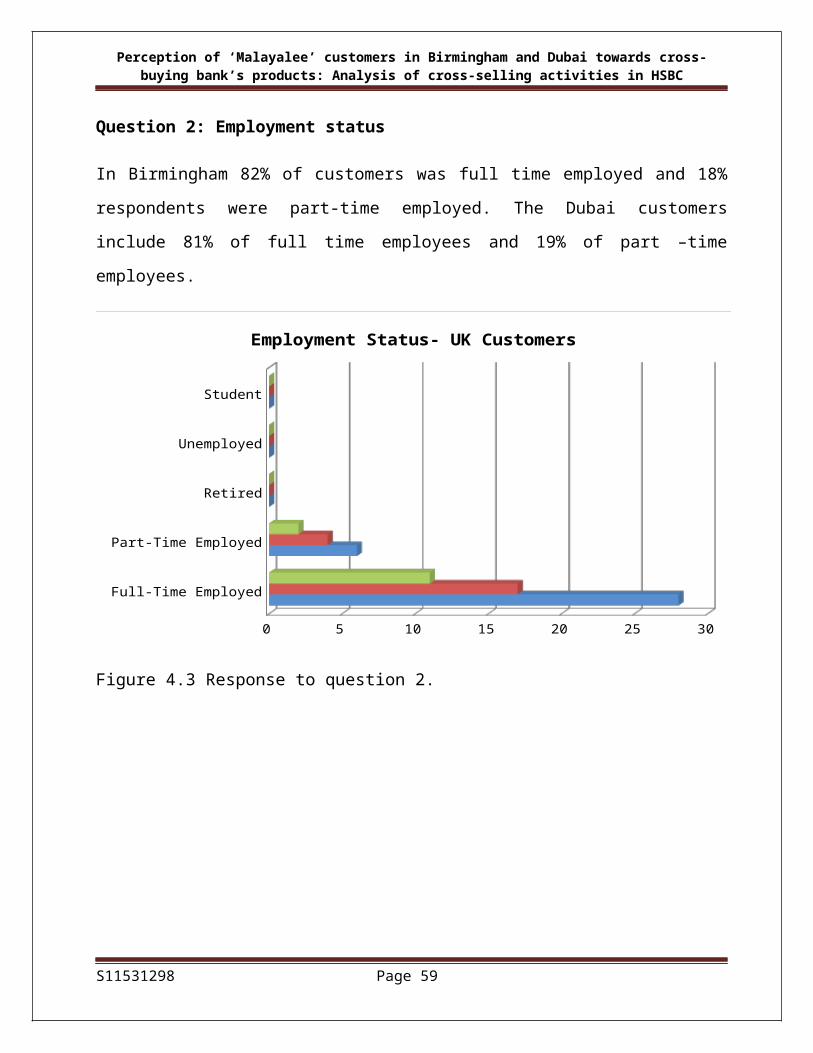

Question 2: Employment status

In Birmingham 82% of customers was full time employed and 18% respondents were part-

time employed. The Dubai customers include 81% of full time employees and 19% of part –

time employees.

Full-Time Employed

Part-Time Employed

Retired

Unemployed

Student

0 5 10 15 20 25 30

Employment Status- UK Customers

Figure 4.3 Response to question 2.

S11531298 Page 36

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

Full-Time Employed

Part-Time Employed

Retired

Unemployed

Student

0 5 10 15 20 25

Employment Status- Dubai Customers

Figure 4.4 Response to question 2.

S11531298 Page 37

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

Question 3: Which country, do you live in?

Birmingham56%

Dubai44%

Participation in the Survey

Figure 4.5 Response to question 3.

Question 4: How many banks, do you currently use?

Total

Less than 6 months

7-12 months

1-3 years

4 or more years

0 2 4 6 8 10 12 14 16

Customer's Loyalty towards Banks(UK)

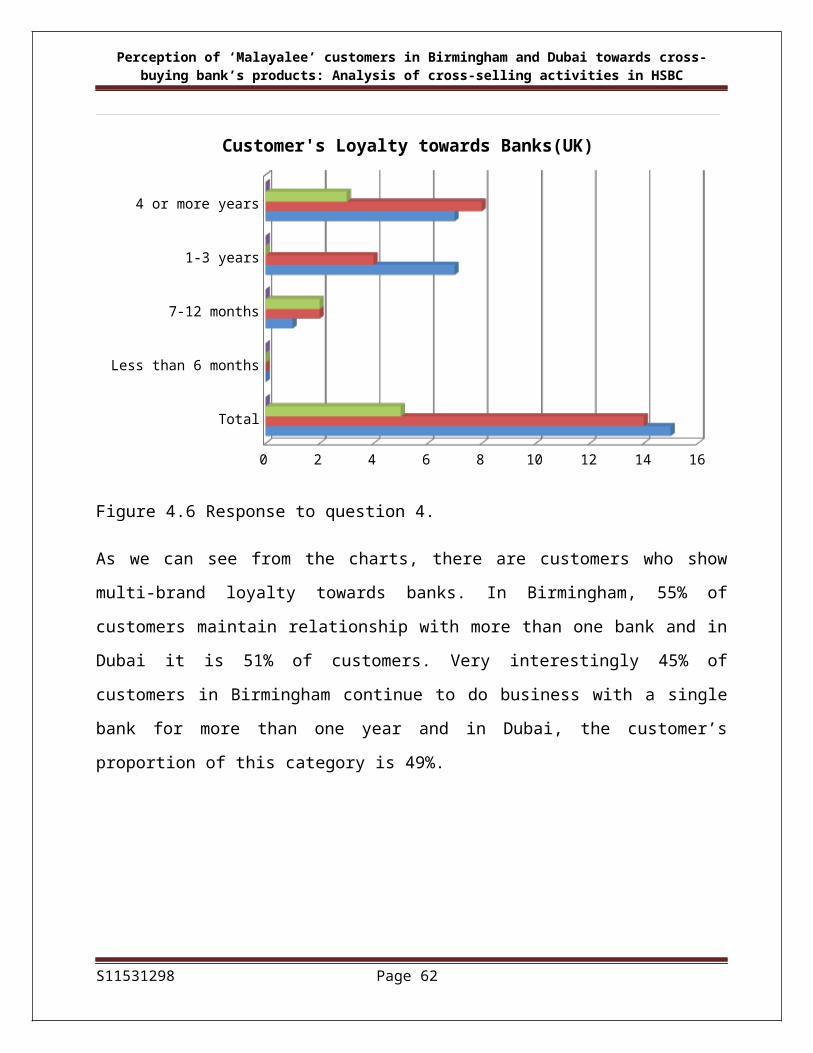

Figure 4.6 Response to question 4.

S11531298 Page 38

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

As we can see from the charts, there are customers who show multi-brand loyalty towards

banks. In Birmingham, 55% of customers maintain relationship with more than one bank and

in Dubai it is 51% of customers. Very interestingly 45% of customers in Birmingham continue

to do business with a single bank for more than one year and in Dubai, the customer’s

proportion of this category is 49%.

Total

Less than 6 months

7-12 months

1-3 years

4 or more years

0 2 4 6 8 10 12 14

Customer's Loyalty towards Banks(Dubai)

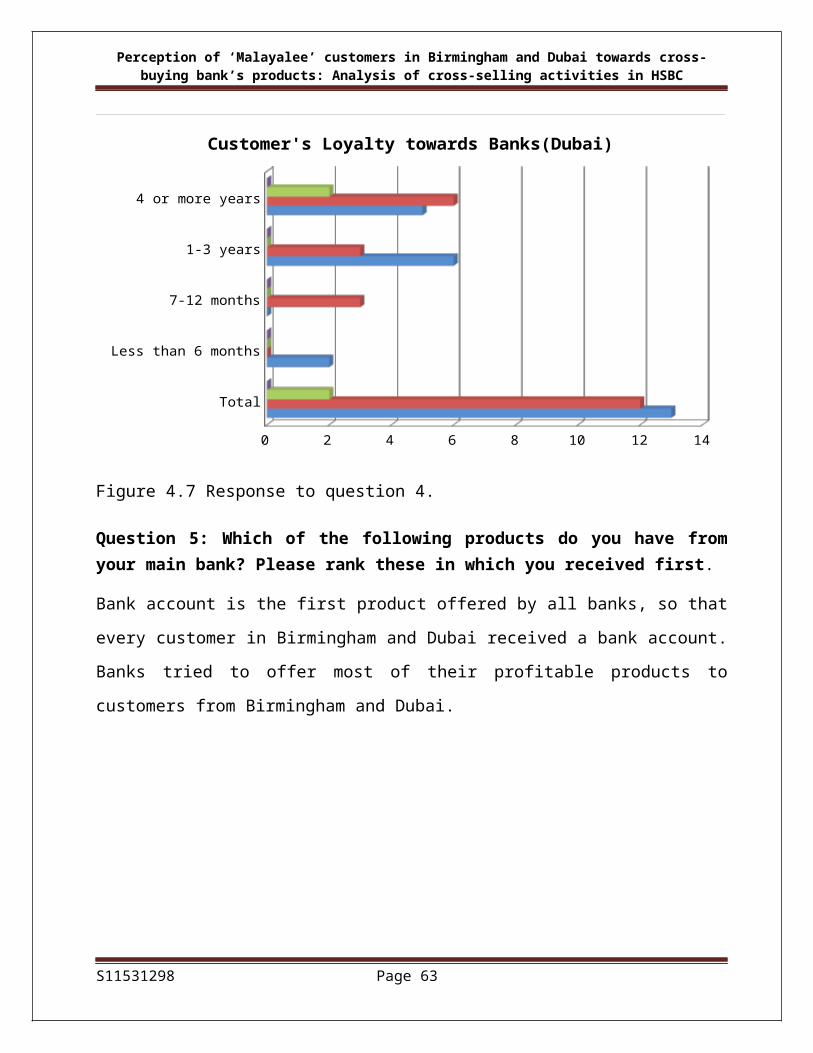

Figure 4.7 Response to question 4.

Question 5: Which of the following products do you have from your main bank? Please rank these in which you received first.

Bank account is the first product offered by all banks, so that every customer in Birmingham

and Dubai received a bank account. Banks tried to offer most of their profitable products to

customers from Birmingham and Dubai.

S11531298 Page 39

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

Bank account

Credit cards

Mortgages & Loans

Insurance

0 5 10 15 20 25 30 35

Product selling by banks in Birmingham

Figure 4.8 Response to question 5.

Bank account

Credit cards

Mortgages & Loans

Insurance

0 5 10 15 20 25 30

Product selling by banks in Dubai

Figure 4.9 Response to question 5.

S11531298 Page 40

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

Question 6: How did your bank offer these products?

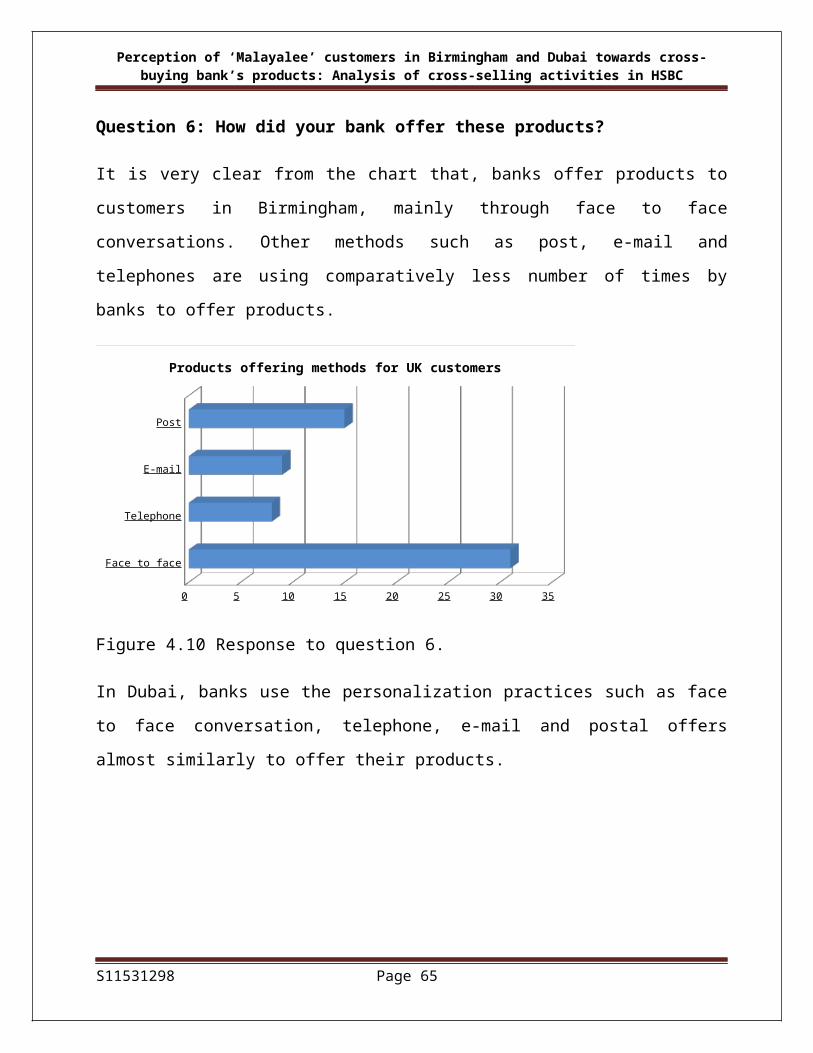

It is very clear from the chart that, banks offer products to customers in Birmingham, mainly

through face to face conversations. Other methods such as post, e-mail and telephones are

using comparatively less number of times by banks to offer products.

Face to face

Telephone

Post

0 5 10 15 20 25 30 35

Products offering methods for UK customers

Figure 4.10 Response to question 6.

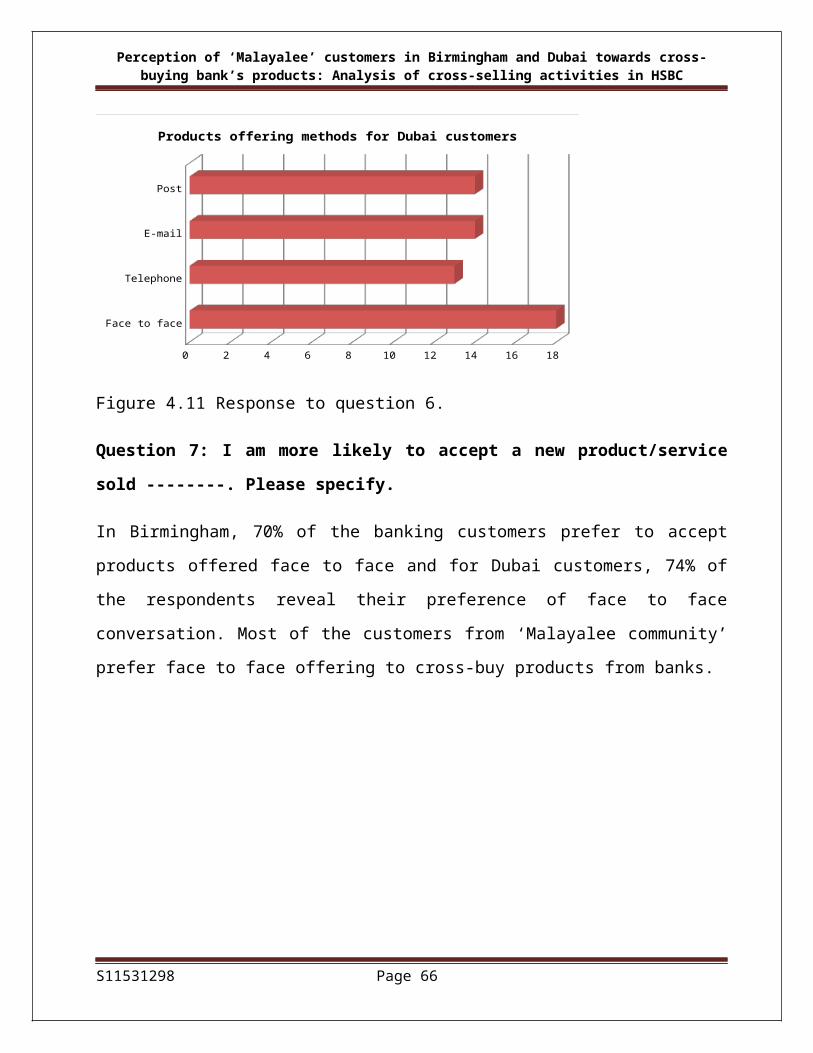

In Dubai, banks use the personalization practices such as face to face conversation, telephone,

e-mail and postal offers almost similarly to offer their products.

Face to face

Telephone

Post

0 2 4 6 8 10 12 14 16 18

Products offering methods for Dubai customers

Figure 4.11 Response to question 6.

S11531298 Page 41

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

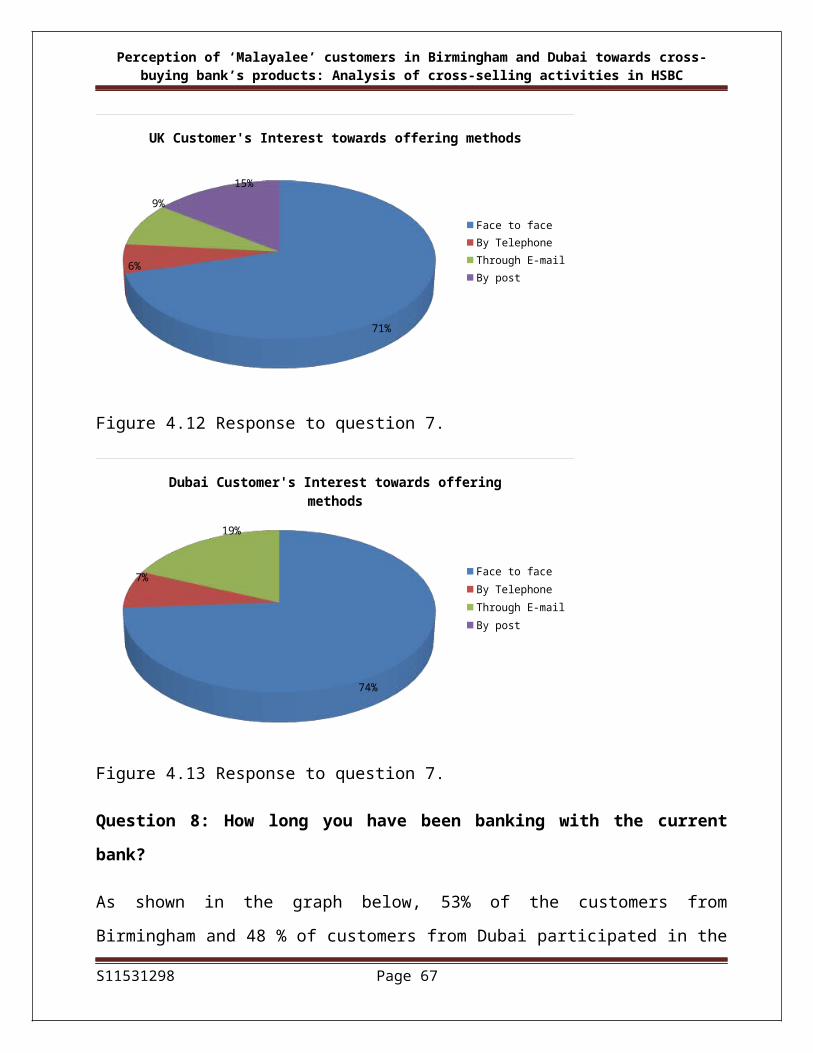

Question 7: I am more likely to accept a new product/service sold --------. Please specify.

In Birmingham, 70% of the banking customers prefer to accept products offered face to face

and for Dubai customers, 74% of the respondents reveal their preference of face to face

conversation. Most of the customers from ‘Malayalee community’ prefer face to face offering

to cross-buy products from banks.

71%

6%

9%

15%

UK Customer's Interest towards offering methods

Face to faceBy TelephoneThrough E-mailBy post

Figure 4.12 Response to question 7.

74%

7%

19%

Dubai Customer's Interest towards offering methods

Face to faceBy TelephoneThrough E-mailBy post

Figure 4.13 Response to question 7.

S11531298 Page 42

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC

Question 8: How long you have been banking with the current bank?

As shown in the graph below, 53% of the customers from Birmingham and 48 % of customers

from Dubai participated in the survey are continuing with their main bank for at least 4 years,

which increase the credibility of research.

15%

32%

53%

UK customer's experience with their main Bank

Less than 6 months7-12 months1-3 years4 or more years

Figure 4.14 Response to question 8.

7% 11%

33%

48%

Dubai customer's experience with their main Bank

Less than 6 months7-12 months1-3 years4 or more years

Figure 4.15 Response to question 8.

S11531298 Page 43

Perception of ‘Malayalee’ customers in Birmingham and Dubai towards cross-buying bank’s products: Analysis of cross-selling activities in HSBC