Download - Fortum Q3 2015 presentation

Interim report January-September 2015 Fortum Corporation

22 October 2015

2

Disclaimer

This presentation does not constitute an invitation to underwrite, subscribe for,

or otherwise acquire or dispose of any Fortum shares

Past performance is no guide to future performance, and persons needing

advice should consult an independent financial adviser

IFRS restatement relating to discontinued operations

Distribution segment has been reclassified as discontinued operations in Q1/2015.

As a result, continuing operations and discontinued operations are presented

separately for Fortum Group. Comparative period information for 2014 has been

restated accordingly

Restated information for the interim periods of 2014 can be found in a stock

exchange release published 15 April 2015

3

Global megatrends have great impact on the energy sector globally

Climate change

and CO2 emissions price

Shifts in macro economy

New technologies;

digitalisation

Changes in

consumer behaviour

4

Resource efficiency

Urbanisation and

electrification

VISION – STRATEGY – STRUCTURE

More concrete actions communicated at the full year release

Focus currently in strategic planning in order to decide our future direction

5

Future direction

• Decide the best way to increase investments in renewables

• Look for ways to grow faster in modern energy services for consumers, communities and businesses

• Keep our eyes open for opportunities as the restructuring of the energy industry proceeds

Operational excellence

• Further increase the productivity of our existing fleet in order to keep it competitive in the current low-

price environment

Q3 2015 Results

6

Key figures (MEUR) III/2015 III/2014 I-III/2015 I-III/2014 2014 LTM

Sales, continuing operations 661 861 2,495 2,955 4,088 3,628

Comparable EBITDA, continuing operations 163 242 787 1,000 1,457 1,244

Operating profit:

Continuing operations -682 113 -188 712 1,296 396

Discontinued operations 0 36 4,395 2,066 2,132 4,461

Fortum total -682 149 4,207 2,778 3,428 4,857

Comparable operating profit:

Continuing operations 79 147 565 715 1,085 935

Discontinued operations 0 36 113 200 266 179

Fortum total 79 183 678 915 1,351 1,114

Profit before taxes:

Continuing operations -818 61 -325 658 1,232 249

Discontinued operations 0 34 4,393 2,063 2,128 4,458

Fortum total -819 95 4,068 2,721 3,360 4,707

Earnings per share:

Continuing operations -0.74 0.06 -0.28 0.63 1.22 0.31

Discontinued operations 0.00 0.04 4.92 2.28 2.33 4.97

Fortum total -0.74 0.10 4.64 2.91 3.55 5.28

Net cash from operating activities, continuing operations 151 212 896 1,011 1,406 1,291

Summary of the third quarter 2015

• Fortum’s results burdened by

– The decision of early closure of nuclear units 1 and 2 in Oskarshamn, Sweden

– Continued pressure on electricity prices

• Exceptionally high inflow due to late snow melt created pressure on electricity prices particurlarily in Sweden

and Norway. The price in Finland decreased less, as the price area is exposed to a much lesser extent, to

hydrological pressure

• Record high hydroproduction

• Decision to participate in the Fennovoima nuclear plant project in Finland with a 6.6%

share

• The targeted operating profit level (EBIT) for the Russia segment, RUB 18.2 billion is

delayed by 2 to 3 years. Previously this level was targeted to be reached during 2015

after finalising the investment programme

7

Market conditions in the third quarter of 2015

Nordic countries

• Power consumption in the Nordic countries at the same level as in Q3 2014

• Nordic system spot prices approximately EUR 19 per MWh lower than in Q3

2014, while area prices were in Finland EUR 8 per MWh lower and in Sweden

EUR 18 per MWh lower

European business environment and carbon market

• The EU Council formally adopted the European Commission’s proposal to

create a reserve to hold surplus CO2 permits under the EU Emissions Trading

System

• The proposed Market Stability Reserve will become operational in January

2019

Russia

• Power consumption in Fortum’s operating areas was on the same level as in

Q3 2014

• Electricity spot price (in RUB) in the Urals hub declined 10% compared to Q3

2014

8

Nordic water reservoirs

9

Source: Nord Pool Spot

Q1 Q2 Q3 Q4

20

40

60

80

100

120

rese

rvo

ir c

on

ten

t (T

Wh)

0

2000 2003 2014 2013 reference level 2015

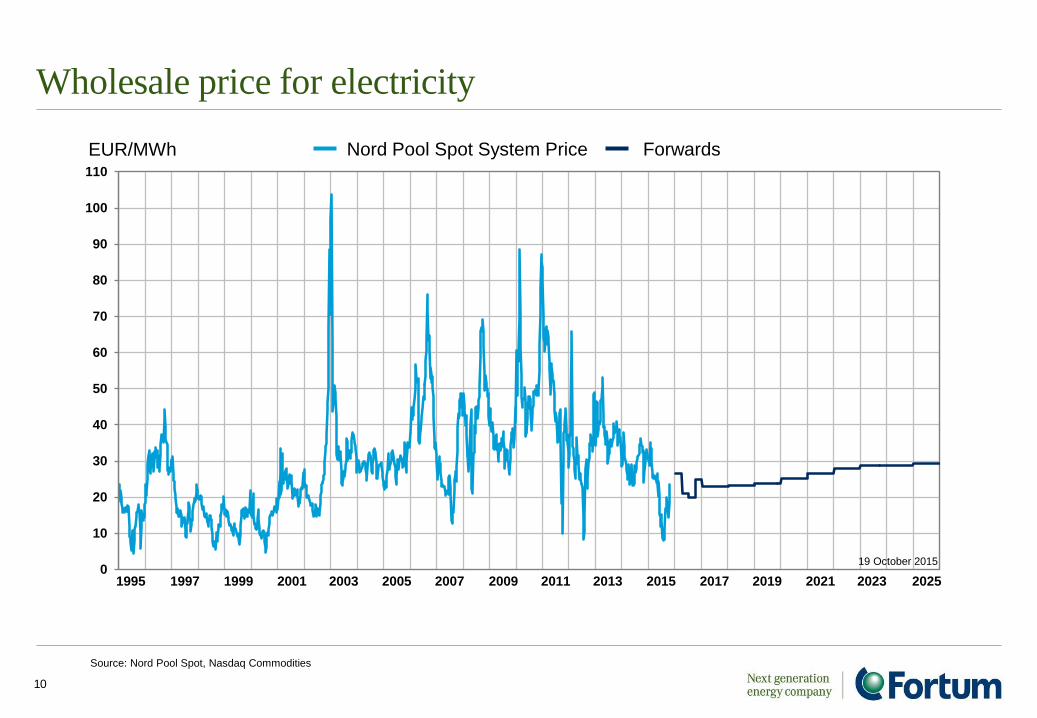

Wholesale price for electricity

10

Source: Nord Pool Spot, Nasdaq Commodities

0

10

20

30

40

50

60

70

80

90

100

110

EUR/MWh Nord Pool Spot System Price Forwards

19 October 2015

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021 2023 2025

0

30

60

90

120

150

US

D /

bb

l

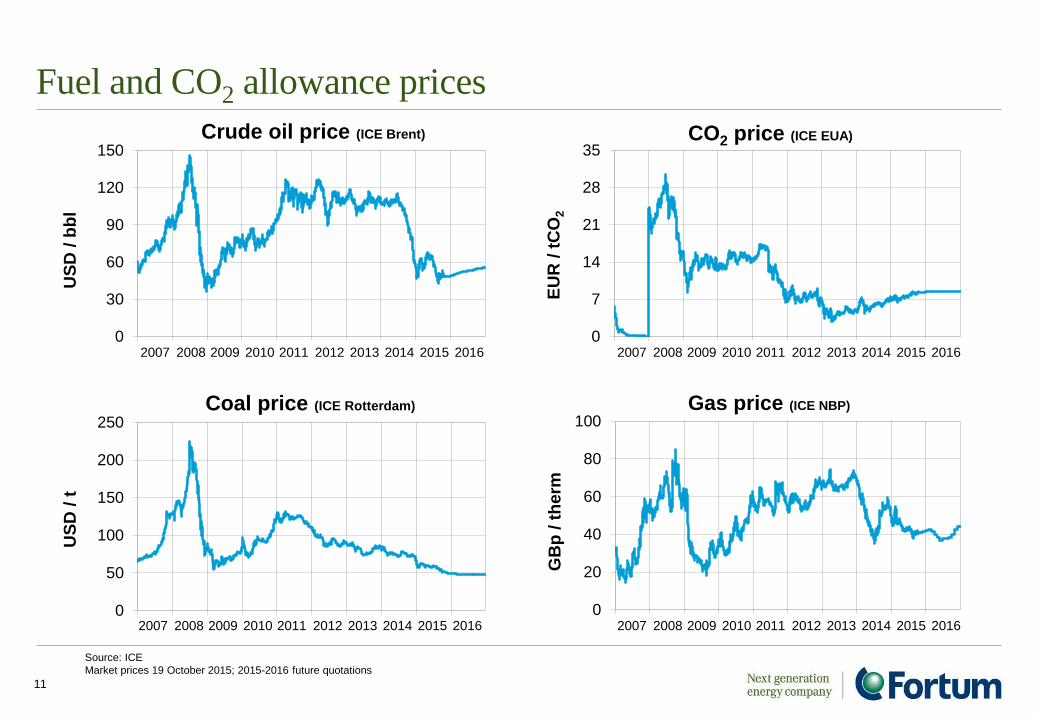

Crude oil price (ICE Brent)

2007 2008 20112009 2010 20132012 2014 2015 20160

7

14

21

28

35

EU

R /

tC

O2

CO2 price (ICE EUA)

2007 2008 20112009 2010 20132012 2014 2015 2016

0

50

100

150

200

250

US

D /

t

Coal price (ICE Rotterdam)

2007 2008 20112009 2010 20132012 2014 2015 20160

20

40

60

80

100

GB

p /

th

erm

Gas price (ICE NBP)

2007 2008 20112009 2010 20132012 2014 2015 2016

11

Source: ICE

Market prices 19 October 2015; 2015-2016 future quotations

Fuel and CO2 allowance prices

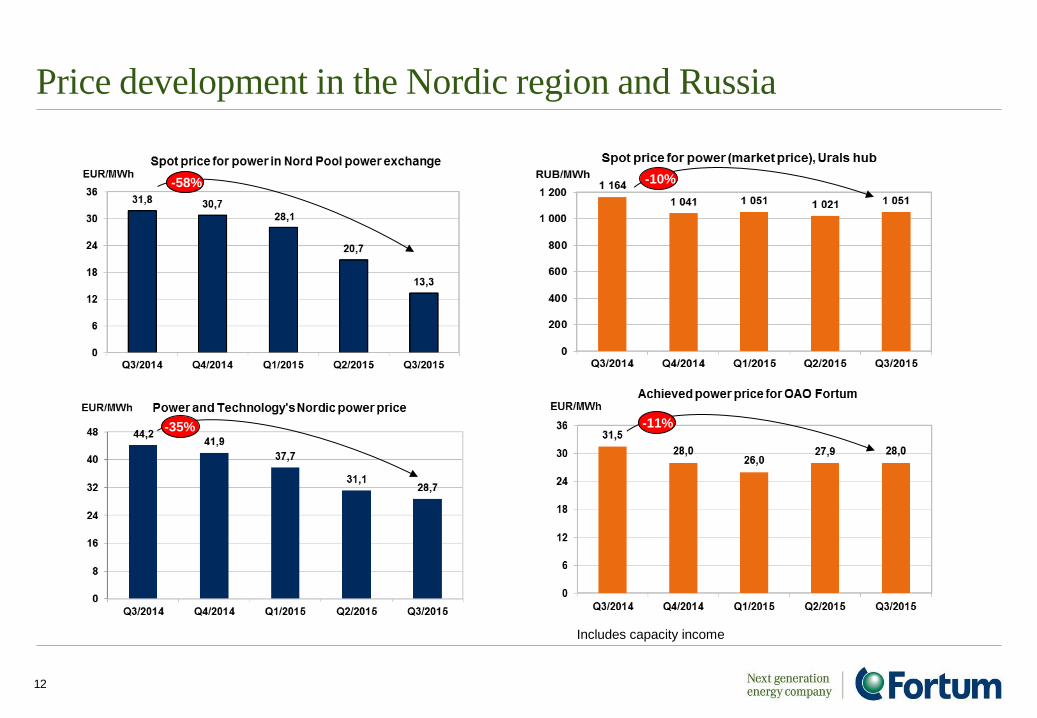

Price development in the Nordic region and Russia

12

Includes capacity income

-58%

-35% -11%

-10%

Q3: Low electricity prices continued to impact results negatively – somewhat compensated by hydro volumes

13

Comparable operating profit, EUR million

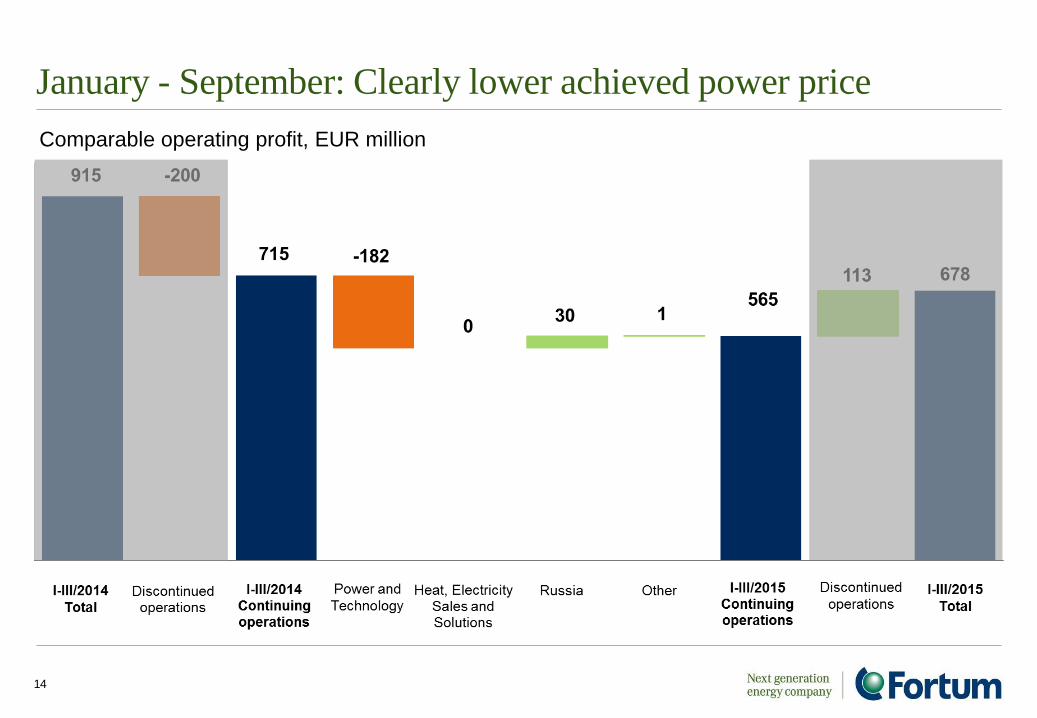

January - September: Clearly lower achieved power price

14

Comparable operating profit, EUR million

Financials

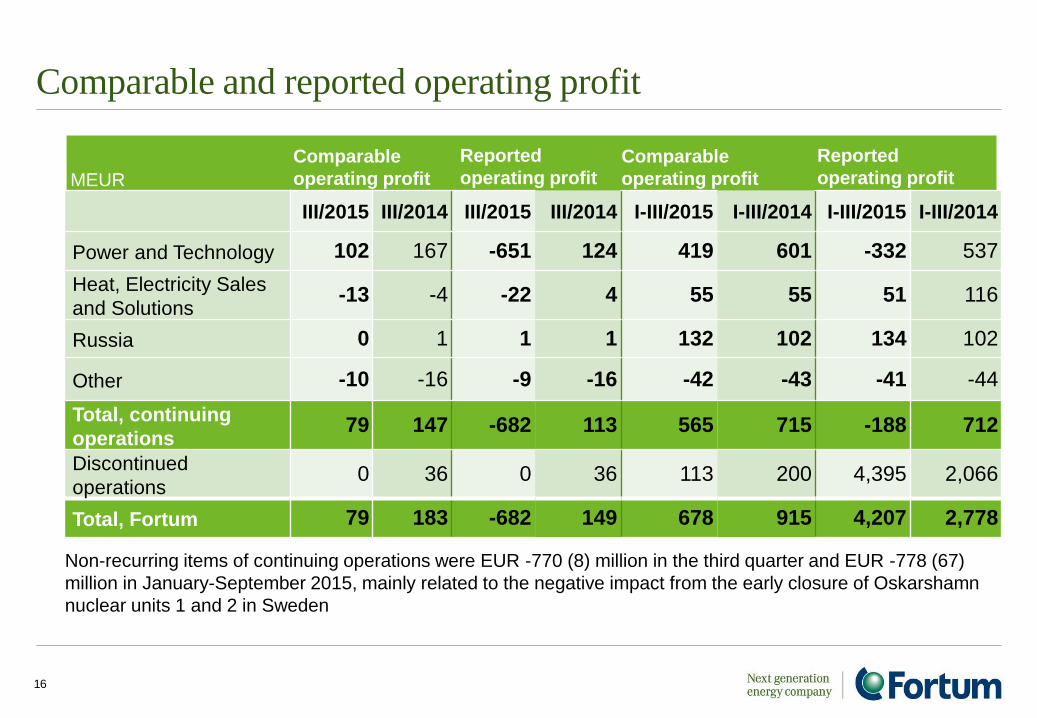

Comparable and reported operating profit

III/2015 III/2014 III/2015 III/2014 I-III/2015 I-III/2014 I-III/2015 I-III/2014

Power and Technology 102 167 -651 124 419 601 -332 537

Heat, Electricity Sales

and Solutions -13 -4 -22 4 55 55 51 116

Russia 0 1 1 1 132 102 134 102

Other -10 -16 -9 -16 -42 -43 -41 -44

Total, continuing

operations 79 147 -682 113 565 715 -188 712

Discontinued

operations 0 36 0 36 113 200 4,395 2,066

Total, Fortum 79 183 -682 149 678 915 4,207 2,778

16

Comparable

operating profit

Reported

operating profit MEUR

Non-recurring items of continuing operations were EUR -770 (8) million in the third quarter and EUR -778 (67)

million in January-September 2015, mainly related to the negative impact from the early closure of Oskarshamn

nuclear units 1 and 2 in Sweden

Reported

operating profit Comparable

operating profit

Impact of early closure of nuclear units 1 and 2 in Oskarshamn

17

• Mainly write-down of asset values in OKG AB for unit 1 and 2

• Provision for future investments and costs

EUR -784 million in operating profit

• Write-down of Fortum IFRS adjustments for OKG AB, i.e. capitalised borrowing cost and asset retirement obligation

EUR -104 million in share of profits from

associates (net of tax)

• Positive income tax effect due to impact of write-downs and provisions in operating profit

EUR +173 million in Income tax expenses

• EPS effect EUR -0.80 EUR -710 million net profit

Power and Technology

MEUR III/2015 III/2014 I-III/2015 I-III/2014 2014 LTM

Sales 377 495 1,282 1,568 2,156 1,870

Comparable EBITDA 131 197 506 692 998 812

Comparable operating profit 102 167 419 601 877 695

Net assets 5,944 6,083 6,001

Comparable RONA % 14.2 11.6

Gross investments 52 66 122 138 198 182

18

Q3 2015

• Clearly lower achieved power price

• Nordic system spot

• Sweden

• Record high hydro volumes

January-September 2015

• Clearly lower achieved power price

• First quarter unusually mild, second

quarter characterised by among the

highest precipitation in recent history, and

during the third quarter exceptionally high

inflow that increased water reservoirs

rapidly

Heat, Electricity Sales and Solutions

MEUR III/2015 III/2014 I-III/2015 I-III/2014 2014 LTM

Sales 185 224 835 939 1,332 1,228

Comparable EBITDA 12 20 129 130 204 203

Comparable operating profit -13 -4 55 55 104 104

Net assets 2,049 2,188 2,112

Comparable RONA % 8.7 7.7

Gross investments 33 59 67 85 124 106

19

Q3 2015

• The comparable operating profit was

negatively affected mainly by lower achieved

power price for power sales from CHP

production

January- September 2015

• Comparable operating on last year’s level

• Lower power price compensated by

lower fuel price

• In retail electricity sales, the customer base

continued to grow and the sales margin

improved

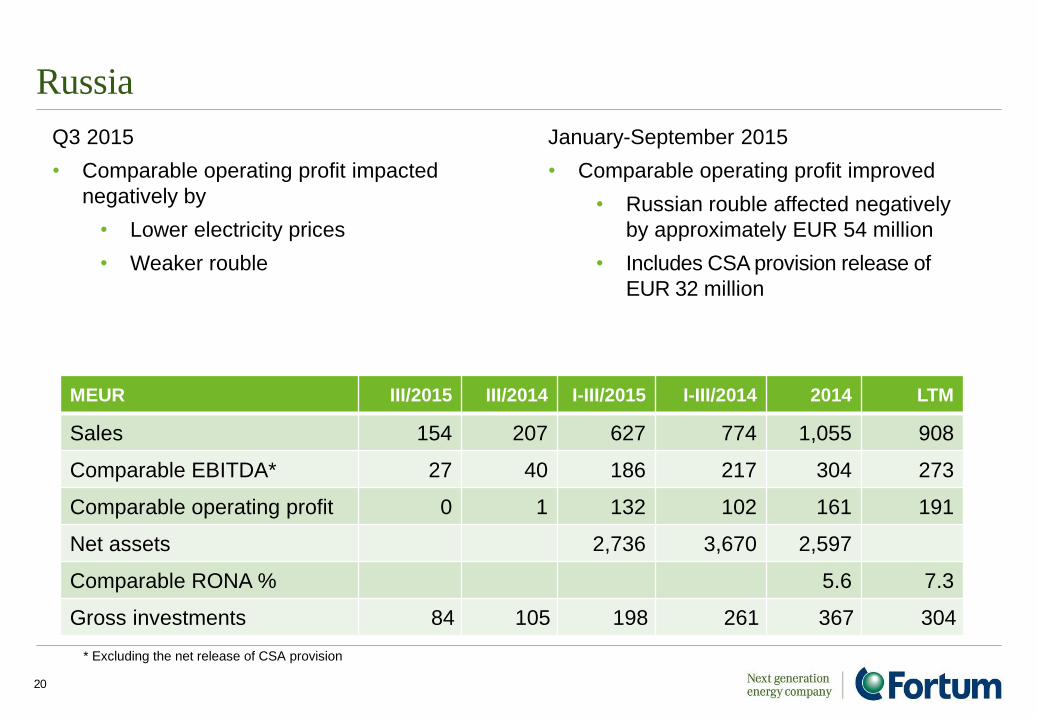

Russia

Q3 2015

• Comparable operating profit impacted

negatively by

• Lower electricity prices

• Weaker rouble

20

MEUR III/2015 III/2014 I-III/2015 I-III/2014 2014 LTM

Sales 154 207 627 774 1,055 908

Comparable EBITDA* 27 40 186 217 304 273

Comparable operating profit 0 1 132 102 161 191

Net assets 2,736 3,670 2,597

Comparable RONA % 5.6 7.3

Gross investments 84 105 198 261 367 304

January-September 2015

• Comparable operating profit improved

• Russian rouble affected negatively

by approximately EUR 54 million

• Includes CSA provision release of

EUR 32 million

* Excluding the net release of CSA provision

Discontinued operations (Distribution)

21

Q3 and January-September 2015

• On 1 June 2015, Fortum completed the divestment of its Swedish electricity distribution

business. Fortum booked a one-time sales gain of approximately EUR 4.3 billion,

corresponding to EUR 4.82 per share

Table below includes January-March 2014 results for the Finnish, January-May 2014 results for the Norwegian and full year 2014

results as well as January-May 2015 for the Swedish distribution business

MEUR III/2015 III/2014 I-III/2015 I-III/2014 2014 LTM

Sales 0 130 274 578 751 447

Comparable EBITDA 0 67 163 318 416 261

Comparable operating profit 0 36 113 200 266 179

Net assets 0 2,634 2,615

Gross investments 0 29 44 89 147 102

Income statement MEUR III/2015 III/2014 I-III/2015 I-III/2014 2014 LTM

Sales 661 861 2,495 2,955 4,088 3,628

Other income and expenses -582 -714 -1,930 -2,240 -3,003 -2,693

Comparable operating profit 79 147 565 715 1,085 935

Items affecting comparability -761 -34 -752 -3 211 -538

Operating profit -682 113 -188 712 1,296 396

Share of profit of associates and jv’s -95 1 -15 108 146 23

Financial expenses, net -42 -54 -123 -163 -210 -170

Profit before taxes -818 61 -325 658 1,232 249

Income tax expense 160 -3 80 -92 -143 29

Net profit, continuing operations -659 58 -246 566 1,089 277

Net profit, discontinued operations 0 27 4,369 2,021 2,073 4,421

Net profit, Fortum total -659 84 4,123 2,587 3,161 4,697

EPS, basic (EUR), continuing operations -0.74 0.06 -0.28 0.63 1.22 0.31

EPS, basic (EUR), discontinued operations 0.00 0.04 4.92 2.28 2.33 4.97

EPS, basic (EUR), Fortum Total -0.74 0.10 4.64 2.91 3.55 5.28

22

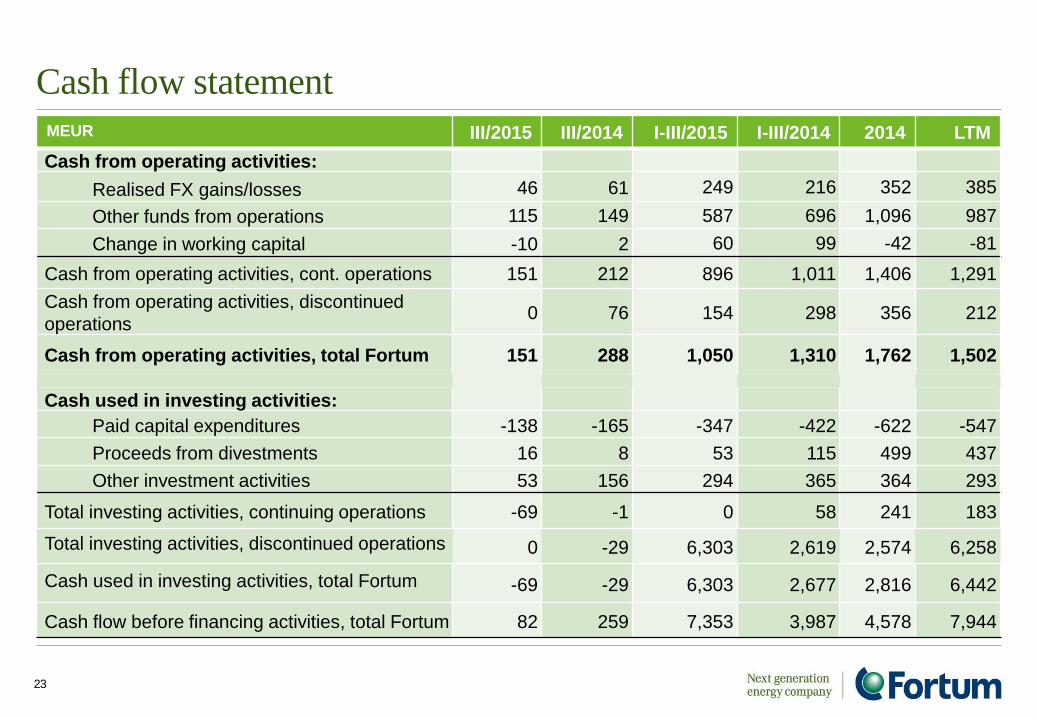

Cash flow statement

MEUR III/2015 III/2014 I-III/2015 I-III/2014 2014 LTM

Cash from operating activities:

Realised FX gains/losses 46 61 249 216 352 385

Other funds from operations 115 149 587 696 1,096 987

Change in working capital -10 2 60 99 -42 -81

Cash from operating activities, cont. operations 151 212 896 1,011 1,406 1,291

Cash from operating activities, discontinued

operations 0 76 154 298 356 212

Cash from operating activities, total Fortum 151 288 1,050 1,310 1,762 1,502

Cash used in investing activities:

Paid capital expenditures -138 -165 -347 -422 -622 -547

Proceeds from divestments 16 8 53 115 499 437

Other investment activities 53 156 294 365 364 293

Total investing activities, continuing operations -69 -1 0 58 241 183

Total investing activities, discontinued operations

0 -29 6,303 2,619 2,574 6,258

Cash used in investing activities, total Fortum

-69 -29 6,303 2,677 2,816 6,442

Cash flow before financing activities, total Fortum 82 259 7,353 3,987 4,578 7,944

23

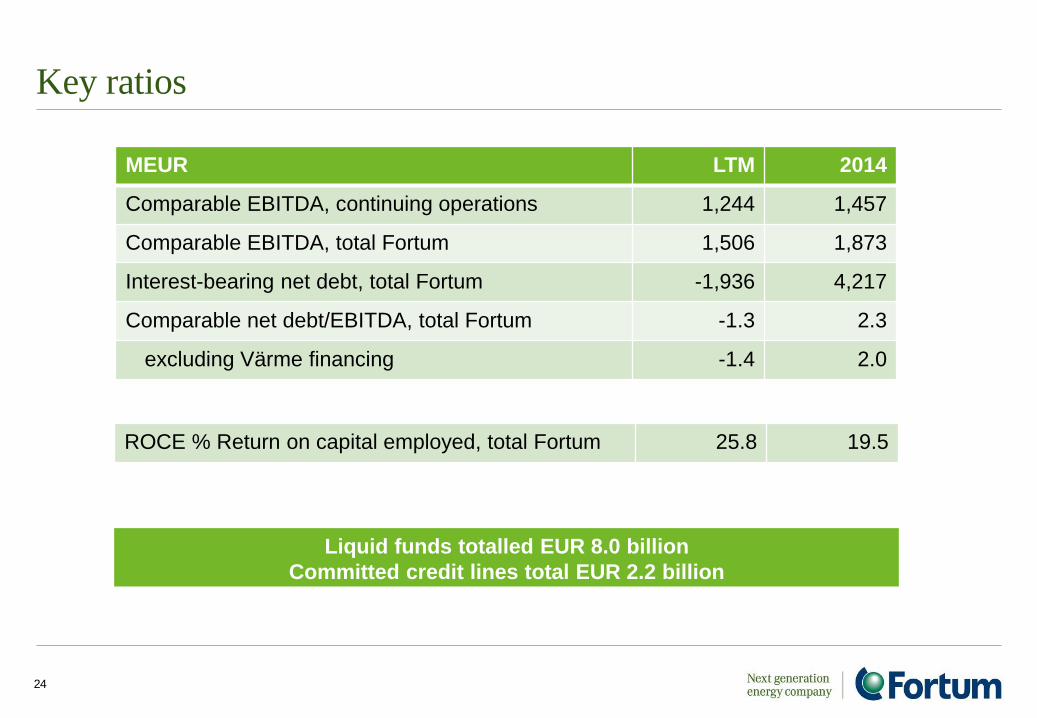

Key ratios

MEUR LTM 2014

Comparable EBITDA, continuing operations 1,244 1,457

Comparable EBITDA, total Fortum 1,506 1,873

Interest-bearing net debt, total Fortum -1,936 4,217

Comparable net debt/EBITDA, total Fortum -1.3 2.3

excluding Värme financing -1.4 2.0

24

ROCE % Return on capital employed, total Fortum 25.8 19.5

Liquid funds totalled EUR 8.0 billion

Committed credit lines total EUR 2.2 billion

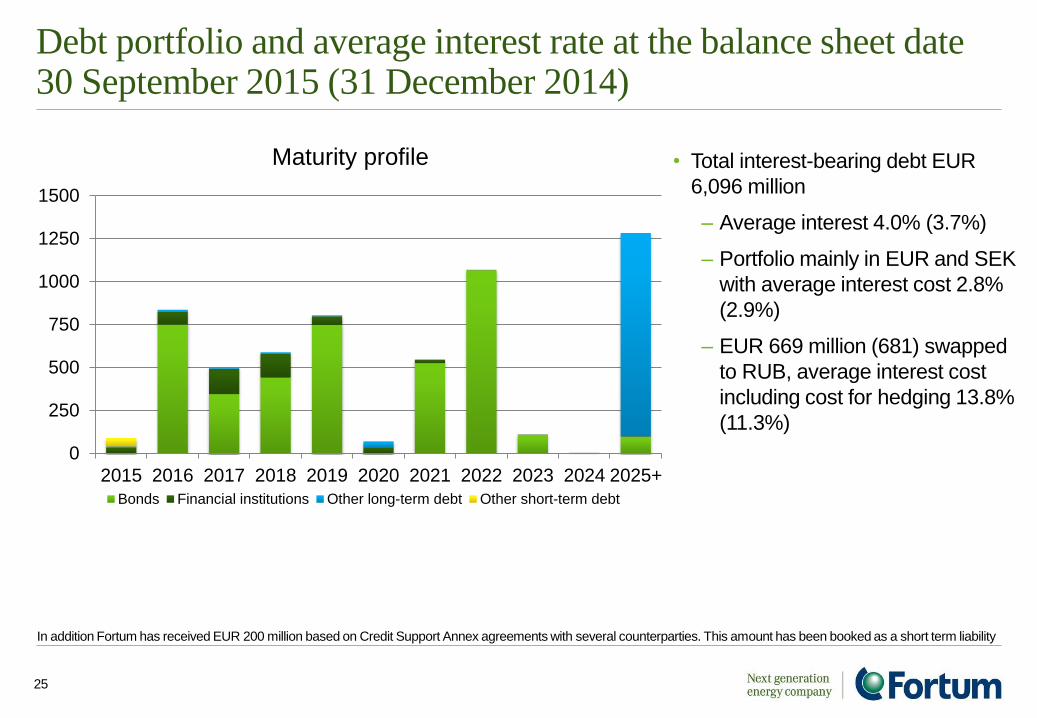

Debt portfolio and average interest rate at the balance sheet date 30 September 2015 (31 December 2014)

25

In addition Fortum has received EUR 200 million based on Credit Support Annex agreements with several counterparties. This amount has been booked as a short term liability

• Total interest-bearing debt EUR

6,096 million

– Average interest 4.0% (3.7%)

– Portfolio mainly in EUR and SEK

with average interest cost 2.8%

(2.9%)

– EUR 669 million (681) swapped

to RUB, average interest cost

including cost for hedging 13.8%

(11.3%)

0

250

500

750

1000

1250

1500

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025+

Bonds Financial institutions Other long-term debt Other short-term debt

Maturity profile

Outlook

Outlook

Nordic markets

• Fortum continues to expect that the average annual electricity demand

growth will be on average approximately 0.5% in the coming years

• Electricity is expected to continue to gain share of total energy consumption

Russia

• The targeted operating profit (EBIT) level of RUB 18.2 billion in the Russia

segment is delayed by 2 to 3 years. Previously the run-rate operating profit level

(EBIT) was targeted to be reached during 2015 after finalising the investment

programme.

Key drivers and risks

• Economic

• Political

• Currency

• Wholesale price of electricity and volumes

• demand and supply • fuels

• hydrological situation • power plant availability

• CO2 emissions allowance prices

27

Outlook

Annual capex estimate, excluding potential acquisitions

• 2015 approximately EUR 0.6 billion

Hedging

• Rest of 2015 approx. 65% hedge ratio at approx. EUR 36/MWh

• 2016 approx. 35% hedge ratio at approx. EUR 34/MWh

• 2017 approx. 15% hedge ratio at approx. EUR 33/MWh

Taxation

• Effective tax rate for 2015 for the Group 19-21%

• The Swedish Parliament decided to approve the proposed tax increase of 17% on

installed nuclear capacity. The tax was implemented as of 1 August 2015. The

estimated impact on Fortum is approximately EUR 15 million annually, albeit

corporate tax-deductible

28

For more information www.fortum.com/investors