Download - FPA_LinkedIn_Evolution_121115_R7

Communication Evolution:

Financial Professionals and the Future of Thought Leadership and Social Media

2 | © 2015 LinkedIn® and Financial Planning Association (FPA)

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 3

About LinkedIn Marketing Solutions: Financial ServicesLinkedIn Marketing Solutions: Financial Services is a business unit within LinkedIn, delivering a comprehensive platform to connect financial services brands with the audiences and issues that matter most. Our targeted full-funnel business development platform provides financial services marketers with unique insights into the preferences, interests and challenges of more than 400 million members. These insights make it possible to build trust with customers and prospects through personal and relevant communication. As the world’s most powerful publisher of meaningful content, we have partnered with 380 of the top financial services brands worldwide to help them build mind share and claim a winning position in the marketplace.

About LinkedInLinkedIn connects the world’s professionals to make them more productive and successful and transforms the ways companies hire, market and sell. Our vision is to create economic opportunity for every member of the global workforce through the ongoing development of the world’s first Economic Graph. LinkedIn has more than 400 million members and has offices around the world.

About the Financial Planning Association® (FPA®)Since 2000, FPA has been the principal professional organization for CERTIFIED FINANCIAL PLANNERTM (CFP®) professionals, educators, financial services professionals and students who seek advancement in a growing, dynamic profession. Nearly 25,000 FPA members adhere to the highest standards of professional competence, ethical conduct and clear, complete disclosure to those they serve. Through a collaborative effort to provide members with One ConnectionTM to tools and resources for professional development, business success, advocacy and community, FPA has become an indispensable force in the advancement of today’s CFP® professional. Learn more about FPA at OneFPA.org and follow on Twitter at twitter.com/fpassociation.

4 | © 2015 LinkedIn® and Financial Planning Association (FPA)

Table of Contents

Welcome 3

Methodology 4

Executive Summary 7

Existing Clients and the Role of Education 10

Prospective Clients and the Role of Social Media 13

Social Media and the Next Generation 15

The Strategic Response: The Role Of Thought Leadership 17

Winning Strategies from High Growth Advisers 19

The Tactical Response: Using Social Media 21

The Impact of Social Media 32

Conclusion 35

Your Action Plan 36

Appendix 1 – Participant Profile 38

Appendix 2 – Profile of Investor Respondents 41

Appendix 3 – Profile of Growth Segment 43

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 5

Welcome

How are financial advisers using social media today to engage clients and prospects?

Are advisers using thought leadership as a way to engage prospects while providing

a means to educate consumers? How are consumers using social media and thought

leadership to connect with advisers?

These and other issues are the focus of Communication Evolution: Financial Professionals and

the Future of Thought Leadership and Social Media, a joint research initiative of LinkedIn and

the Financial Planning Association® (FPA®).

This report aims to help financial advisers of all business models understand how their peers

are engaging in social media and thought leadership, the connection between business growth

and these communication tactics, and what advisers are planning to do moving forward.

With 67 percent of high growth firms saying they added new clients directly as a result

of social media activity, there is much to learn on how all advisers can realize that same

level of growth.

LAUREN M. SCHADLE, CAE

CEO/Executive Director

Financial Planning Association

6 | © 2015 LinkedIn® and Financial Planning Association (FPA)

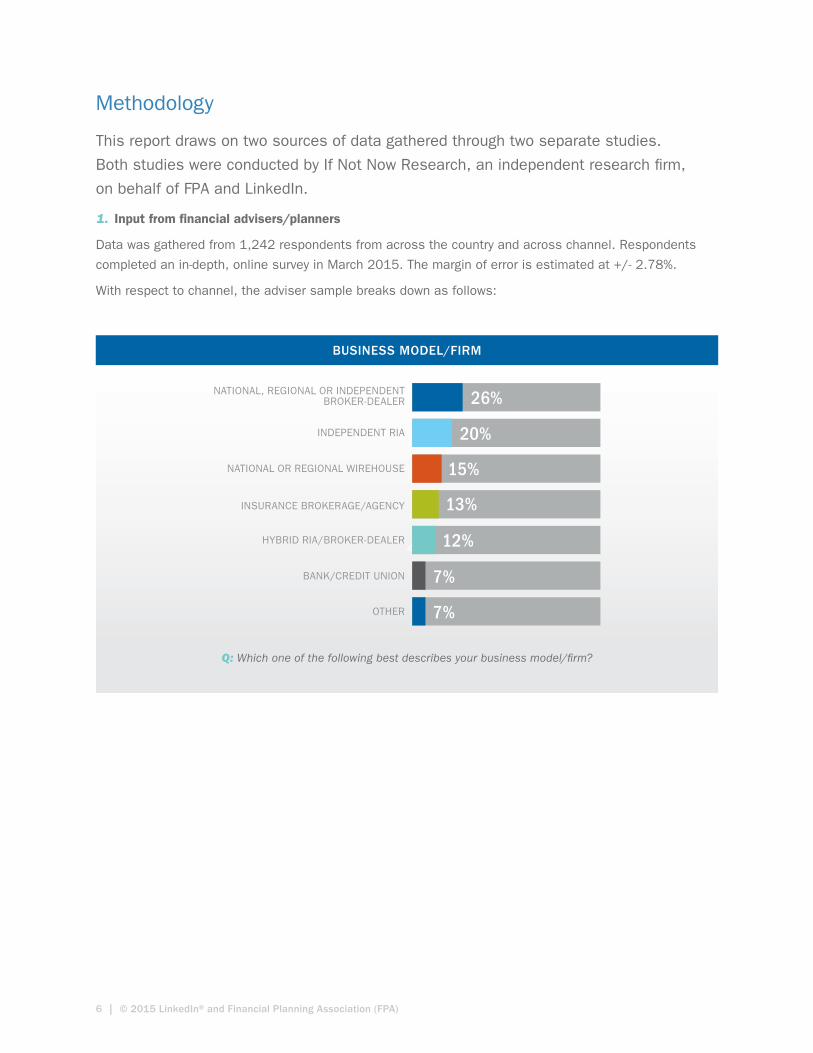

Methodology

This report draws on two sources of data gathered through two separate studies.

Both studies were conducted by If Not Now Research, an independent research fi rm,

on behalf of FPA and LinkedIn.

1. Input from fi nancial advisers/planners

Data was gathered from 1,242 respondents from across the country and across channel. Respondents

completed an in-depth, online survey in March 2015. The margin of error is estimated at +/- 2.78%.

With respect to channel, the adviser sample breaks down as follows:

46%

15%

26%

20%

BUSINESS MODEL/FIRM

NATIONAL, REGIONAL OR INDEPENDENTBROKER-DEALER

INDEPENDENT RIA

NATIONAL OR REGIONAL WIREHOUSE

13%INSURANCE BROKERAGE/AGENCY

12%HYBRID RIA/BROKER-DEALER

7%BANK/CREDIT UNION

OTHER 7%

CHART 1

Q: Which one of the following best describes your business model/fi rm?

BUSINESS MODEL/FIRM

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 7

CLIENT AGE

To gain insight into the drivers of growth, respondents were segmented based on annual revenue growth

in the previous year. A summary of the low, moderate and high growth segments highlighted throughout

the report is below.

The overall sample breaks down as follows:

2. Input from clients of fi nancial advisers/planners

Data was gathered from 1,041 respondents from across the country using multiple, established investor

panels. Respondents completed an in-depth, online survey in May 2015. All respondents work with a

fi nancial adviser/planner, make or contribute to the fi nancial decisions in the household and meet specifi c

criteria on investable assets. The margin of error is estimated at +/- 3.04%.

A summary of the age and wealth profi le of the investor respondents is shown below; however, a full

profi le can be found in Appendix 2.

PERCENTAGE OF RESPONDENTS

MEDIAN NUMBER OF NEW CLIENTS ADDED

IN 2014

PERCENTAGE ACHIEVING 20%+

GROWTH IN REVENUE IN 2014

LOW GROWTH 29% 9 5%

MODERATE GROWTH 39% 14 14%

HIGH GROWTH 32% 19 57%

For a full profi le of the adviser/planner respondents see Appendix 1.

Q: What is your age?

46%

9%

1%

7%

18–24

25–34

35–44

11%45–54

33%55–64

38%65+

8 | © 2015 LinkedIn® and Financial Planning Association (FPA)

Q: Please tell us which best describes your current total investable assets, including all mutual funds, stocks, bonds, 401(k), IRA and other retirement accounts, but excluding real estate?

Q: Which of the following best describes your annual household income before taxes?

10%

29%27%

CURRENT TOTAL INVESTABLE ASSETS

$50,000 –$99,999

$100,000 –$499,999

$500,000 –$999,999

24%

$1,000,000 –$4,999,999

9%

$5,000,000OR MORE

11%

39%35%

ANNUAL HOUSEHOLD INCOME BEFORE TAXES

LESS THAN$50,000

$50,000 –$99,999

$100,000 –$199,999

14%

$200,000AND OVER

2%

PREFER NOTTO SAY

CLIENT INVESTABLE ASSETS

HOUSEHOLD INCOME

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 9

Executive Summary

By examining the behaviors of clients we can predict the strategies that will be used

by some of the most successful advisers. Two distinct, but related, changes in client

behavior and expectations are driving the fastest growing advisers to invest in thought

leadership strategies, executed via professional and social networks. In this study,

we examine how client behavior is influencing the way in which the most successful

advisers communicate and the tools they are using to take action.

Client and Prospect Behavior

1. The Client

While it is accepted wisdom that many clients choose to work with a financial adviser in order to delegate

decision making, the data shows that they look to their advisers to provide ongoing education. Three-quarters

of clients say they look to their adviser to provide some form of education, suggesting they not only look

to their adviser for expertise, but to also help them make informed decisions. Client engagement is not

only about the adviser’s expertise but the extent to which he or she helps clients make informed decisions

through meaningful education.

2. The Prospect

Advisers report that client referrals continue to be the most important source of new business. While there is

no sign that this is changing, the referral process is being increasingly influenced by professional and social

networks. A third of clients, across all age ranges, say they searched online or via a professional or social

network to learn more about a prospective adviser. This number will increase going forward as an increasing

number of clients (across all age groups) say that the ability to go online as part of how they validate a

decision to meet with an adviser will be important, even when referred. Social media is becoming a key part

of the new business development process, including adviser’s ability to attract referrals.

10 | © 2015 LinkedIn® and Financial Planning Association (FPA)

The Strategic Response to Client Behaviors

The fastest growing advisers and firms are implementing thought leadership strategies in response to the

demand for education among existing clients. They leverage that activity via social media to build

credibility and attract prospective clients.

High growth firms recognize that they can respond to both client and prospect needs and behaviors

by focusing on three key communications strategies. Compared to low growth firms, they are more

likely to:

• Offer educational events

• Leverage professional networks on LinkedIn

• Focus on thought leadership activities

The impact of those activities may contribute to the success those firms have achieved. Forty-one percent

of the high growth firms—identified in the study—experienced asset growth in excess of 30 percent.

Just 11 percent of all respondents achieved that level of growth. A full profile of this group is available

in Appendix 3.

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 11

The Tactical Response

If thought leadership is the strategic response, social media is the tactical response, providing the

fastest growing advisers with a way to efficiently execute on that strategy. And while social media

is acknowledged—by respondents—as an important way to communicate with younger clients,

it is further seen as a way to build deeper relationships with existing clients and build credibility.

The data shows that:

1. High growth firms are more likely to execute thought leadership strategies via social media.

2. Advisers use different professional and social networks to meet different objectives. LinkedIn is seen primarily as a way to find new relationships, Facebook to maintain and deepen relationships and Twitter to listen and learn from others.

3. While many advisers cite compliance restrictions as the reason they do not use social media, almost as many say they are unsure how to use the networks effectively, or they do not feel they are appropriate for business.

4. Going forward, advisers will de-emphasize passive uses of social media (e.g. listening and learning from others) and focus more on using social media to actively build credibility.

The Impact

While 30 percent of advisers do not see any connection between social media activity and new business,

the majority of advisers see a direct or indirect link to growth. Only nine percent see social media as leading

directly to new business. Sixty-one percent say it supports business development activities, particularly

referrals. Forty-two percent of high growth advisers say social media has a positive impact on client

referrals. Despite the view that social media is more a support than driver of new business, 67 percent

of high growth firms say they added new clients directly as a result of social media activity.

12 | © 2015 LinkedIn® and Financial Planning Association (FPA)

Existing Clients and the Role of Education

Clients are looking to advisers for meaningful educational content and activities,

building confi dence and driving engagement. That engagement is a core driver

of growth in an advisory business.

The study of client engagement is critical for advisers. Clients are not only the most satisfi ed; they drive

all referral growth. And while client engagement is a complex topic, we do know that education is an

important driver. Three-quarters of clients say they look to their adviser to provide some form of education,

suggesting they not only look to their adviser for expertise but also to help them make informed decisions.

PERCENTAGE OF INVESTORS

NOT AT ALL IMPORTANT 2%

NOT VERY IMPORTANT 4%

NEUTRAL 18%

SOMEWHAT IMPORTANT 50%

CRITICAL 26%

Q: How important is it that your adviser provides you with education related to the market, investments or other fi nancial topics?

Client engagement is not only

about the adviser’s expertise but

the extent to which he or she helps

clients make informed decisions

through meaningful education.

IMPORTANCE OF EDUCATION

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 13

Q: To what extent do you agree or disagree that your adviser provides you with education related to the market, investments or other fi nancial topics?

Q: To what extent do you agree or disagree that your adviser provides you with education related to the market, investments or other fi nancial topics?

* Engaged clients are defi ned as those who are very satisfi ed (5 out of 5 on overall satisfaction) and indicate they provided a referral in the last 12 months.

33%

25%

38%

38%

36%

37%

<25%

100%

80%

60%

40%

20%

0%25–49% 50–74%

30%

55%

75%+

SOMEWHAT AGREE

PER

CEN

TAG

E O

F R

ESPO

ND

ENTS

COMPLETELY AGREE

37%

35%

23%

69%

NOT ENGAGED

100%

80%

60%

40%

20%

0%ENGAGED*

SOMEWHAT AGREE

PER

CEN

TAG

E O

F R

ESPO

ND

ENTS

COMPLETELY AGREE

SATISFYING DEMAND FOR EDUCATION

CONNECTING EDUCATION AND SHARE OF WALLET

More importantly, we can see that the extent to which advisers are satisfying the demand for education

is tied directly to key engagement and growth metrics such as engagement, referrals and share of wallet.

14 | © 2015 LinkedIn® and Financial Planning Association (FPA)

Q: How would you rate the value of receiving information from your adviser via the following methods? Shows percentage rating ‘somewhat or very valuable’.

How educational content is delivered varies by adviser; however, clients generally agree that in-person

workshops and seminars have the highest value. Clients who are over the age of 55 tend to value receiving

relevant articles, whereas those who are between 45–54 are more likely to respond to information shared

via blogs or professional networks.

Financial planning topics are the most popular type of content to share, dropping signifi cantly down

to investment-related topics. Forty-three percent of advisers say they create or curate content

on non-fi nancial topics.

CLIENT AGE

AGES18–44

AGES45–54

AGES55–64

AGES65+

RELEVANT ARTICLES 33% 56% 55% 36%

ADVISER BLOG 23% 44% 16% 13%

INFORMATION SHARED VIA PROFESSIONAL NETWORKS (e.g. LinkedIn) 23% 40% 10% 5%

IN-PERSON WORKSHOPS/SEMINARS 54% 56% 48% 43%

ONLINE WORKSHOPS/SEMINARS 40% 56% 37% 8%

COMMUNICATION PREFERENCES BY AGE

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 15

Q: Which, if any, of the following did you do to learn more about your adviser prior to contacting or meeting with him or her?

Prospective Clients and the Role of Social Media

While client referrals are still the primary source of new business for advisers, prospects

are turning to social media to research an adviser before meeting or to validate the

decision afterwards. This trend spans generations.

Today, there is a clear connection between age and the way in which prospective clients seek out

information on an adviser with whom they may want to meet. Younger prospective clients (under age 44)

were about four times as likely to use online searches or professional or social networks to learn about

their adviser prior to contacting or meeting with him or her than those who are 65 or older.

It is only when we look forward that we uncover the real trend. At the time many clients started working

with their current adviser, the use of online searches or professional networks may not have been an

option. When we look forward, an increasing number of investors say that access to information via

social/professional networks would be important if they were looking for an adviser today. That trend is

clear across all age groups. While fewer than fi ve percent used professional or social networks when they

found their current adviser, 21 percent responded that this would be important going forward. That number

doubles for those clients under the age of 45.

CLIENT AGE

AGES18–44

AGES45–54

AGES55–64

AGES65+

ONLINE SEARCH (e.g. Google) 35% 17% 15% 10%

CHECKED FOR INFORMATION ON PROFESSIONAL NETWORKS (e.g. LinkedIn) 24% 10% 6% 4%

CHECKED FOR INFORMATION ON SOCIAL NETWORKS (e.g. Facebook) 18% 4% 2% 1%

SEARCH PREFERENCES AND AGE

16 | © 2015 LinkedIn® and Financial Planning Association (FPA)

Age also impacts when prospective clients go online to research an adviser. Younger clients are more

likely to search prior to making any contact with an adviser, while older clients are more likely to use these

networks as a way to validate their thinking after meeting with the adviser.

Q: If you were looking for a new fi nancial adviser today, how important would access to information via social/professional networks be in researching a prospective adviser?

Q: When did you seek out information on your adviser using professional or social networks?N= those who sought information using professional or social networks

AGES18–44

AGES45–54

AGES55–64

AGES65+

NOT AT ALL/NOT VERY IMPORTANT 27% 47% 50% 51%

NEUTRAL 31% 25% 30% 27%

IMPORTANT/CRITICAL 43% 28% 20% 21%

AGES18–44

AGES45–54

AGES55–64

AGES65+

PRIOR TO MAKING ANY CONTACT 51% 46% 50% 29%

AFTER CONTACTING BUT PRIOR TO MEETING 39% 46% 38% 41%

AFTER MEETING BUT PRIOR TO MAKING A DECISION 10% 8% 8% 29%

IMPORTANCE OF ONLINE PROFILES BY AGE

TIMING OF ONLINE SEARCHES BY AGE

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 17

Social Media and the Next Generation

The age differentials—that the data highlights—are not lost on advisers; most see

social media as an important way to target younger clients. Three-quarters of advisers

see the use of social media as an important way to target younger clients and younger

clients agree.

In order to understand the impact of age, we turn back to the client and examine if and how they are using

different networks for both personal and business use. Perhaps not surprisingly, younger clients report

using social networks more extensively, supporting the industry’s view that this is an important medium.

Usage is signifi cantly different across age groups; however, it is important to note that signifi cant numbers

of older clients are also using social media.

Q: Which, if any, of the following do you use in your personal or professional life today? Shows percentage responding ‘yes’

AGES18–44

AGES45–54

AGES55–64

AGES65+

LINKEDIN 62% 55% 42% 33%

FACEBOOK 86% 74% 66% 59%

TWITTER 55% 30% 16% 13%

PINTEREST 51% 42% 20% 14%

INSTAGRAM 46% 19% 10% 4%

SOCIAL AND PROFESSIONAL NETWORK USAGE BY AGE

18 | © 2015 LinkedIn® and Financial Planning Association (FPA)

For younger clients, higher usage translated into an expectation that their adviser should have a presence

on social media, particularly LinkedIn.

Q: How important do you think it is for your adviser to have a presence on the following networks? Shows percentage rating somewhat/very important.

AGES18–44

AGES45–54

AGES55–64

AGES65+

LINKEDIN 42% 25% 18% 11%

FACEBOOK 25% 11% 5% 6%

TWITTER 22% 5% 4% 4%

EXPECTATIONS FOR ONLINE PRESENCE BY AGE

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 19

The Strategic Response: The Role of Thought Leadership

The fastest growing advisers are focusing on thought leadership strategies in response

to the demand for education among existing clients. They leverage that activity using social

media to build credibility and attract prospective clients.

Two key implications emerge from the assessment of client behavior.

1. Educational activities are a critical part of client engagement. While it is easy to assume that clients do not value education because they have opted to work with an expert to help them make informed decisions, this is not the case. Clients choose to work with an adviser but still want or demand meaningful education to increase confi dence in their own decision making.

2. Having a robust online presence is no longer a “nice to have.” If you are targeting younger clients, the information they fi nd online is your calling card; it may be the determinant of whether they reach out or not. For older clients, the information they fi nd online will help validate their decision or move them toward a decision.

Thought leadership is, in part, characterized by sharing meaningful

content with clients and prospects. Today, about 70 percent of

advisers share content with clients or prospects in order to build

credibility, raise awareness and deepen relationships with existing

clients; however, they rely primarily on traditional methods of

distributing that information, such as email.

While many advisers are

providing clients with meaningful

content, they rely on email to

distribute the content.

Q: Do you author or share content (e.g. articles) with clients or prospects?

20%

52%

31%

YES, BY SOME OTHER METHOD(e.g. Email, Mail)

YES, VIA PROFESSIONAL NETWORKS(e.g. LinkedIn)

YES, VIA SOCIAL NETWORKS(e.g. Facebook, Twitter)

9%YES, MY OWN BLOG

AGES18–44

AGES45–54

AGES55–64

AGES65+

LINKEDIN 42% 25% 18% 11%

FACEBOOK 25% 11% 5% 6%

TWITTER 22% 5% 4% 4%

METHODS OF CONTENT DISTRIBUTION

20 | © 2015 LinkedIn® and Financial Planning Association (FPA)

The objectives for sharing content include building credibility, raising awareness of the fi rm or building

deeper relationships with existing clients.

Q: What impact do you believe that sharing and/or authoring relevant content has on your business, clients or prospects?

46%

70%

83%

76%

BUILDS CREDIBILITY

RAISES AWARENESS OF MY BUSINESS

DEEPENS RELATIONSHIPSWITH EXISTING CLIENTS

57%HELPS CLIENT RETENTION

52%DIFFERENTIATES ME/MY FIRM

33%MOVES PROSPECTS ALONG THE PIPELINE

IMPACT OF SHARING RELEVANT CONTENT

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 21

Winning Strategies from High Growth Advisers

By examining advisory fi rms that have experienced higher growth, we are able to identify

strategies and tactics that may be more effective.

In order to understand the drivers of growth, the study isolated the third of respondents who were

experiencing the most signifi cant growth. Growth rates varied dramatically across advisory businesses

in 2014; 23 percent of respondents reported revenue growth rates of 20 percent or higher and a third less

than 10 percent. On the basis of the data provided, we created three segments, using asset growth as a proxy

for overall growth. Forty-one percent of high growth fi rms experienced asset growth in excess of 30 percent.

Just 11 percent of all respondents achieved that level of growth.

The overall sample breaks down as follows:

The Winning Strategies

High growth fi rms differed in two substantial ways:

1. They were more likely to use almost every form of communication with clients and prospects;

they simply communicate more frequently.

2. They were more likely to focus on education and thought leadership leveraged via

professional networks.

Today, advisers use a range of activities as part of their overall communications plans. The top

three forms of communication and the percentage of advisers using them are:

• Client appreciation/social events 57%

• Direct mail/email 49%

• Educational events 41%

PERCENTAGE OF RESPONDENTS

MEDIAN NUMBER OF NEW CLIENTS ADDED

IN 2014

LOW GROWTH ADVISERS 29% 9

MODERATE GROWTH ADVISERS 39% 14

HIGH GROWTH ADVISERS 32% 19

22 | © 2015 LinkedIn® and Financial Planning Association (FPA)

However, the communications and activities that characterized the past will look different in the future.

Looking forward, few high growth fi rms see an increase in the use of advertising and direct mail/

email, opting for more engaging activities. Specifi cally, high growth fi rms see increased emphasis

being placed on:

• Leveraging professional networks on LinkedIn

• Thought leadership/content strategy (e.g. blogs, sharing curated content)

• Leveraging social networks

While high growth fi rms may be early adopters when it comes to thought leadership and social media,

there is evidence that this refl ects a more generalized trend among advisers. Sixty-six percent of all

advisers say thought leadership will play a more important role going forward.

ALL RESPONDENTSHIGH GROWTH

ADVISER

LEVERAGING MY PROFESSIONAL NETWORK ON LINKEDIN 72% 71%

THOUGHT LEADERSHIP/CONTENT STRATEGY (e.g. blogs, sharing curated content) 66% 70%

LEVERAGING SOCIAL NETWORKS (e.g. Facebook, Twitter) 72% 68%

SOCIAL EVENTS/CLIENT APPRECIATION 59% 66%

PUBLIC RELATIONS 51% 63%

EDUCATIONAL EVENTS (live or webinars) 55% 54%

SPEAKING ENGAGEMENTS 47% 46%

ADVERTISING 24% 29%

DIRECT MAIL/EMAIL 18% 20%

Q: Looking forward in the next three years, how do you think about the relative importance of the strategies you are using today? Shows percentage selecting

‘Will become more important’ for high growth fi rms.

RELATIVE IMPORTANCE OF MARKETING STRATEGIES

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 23

The Tactical Response: Using Social Media

If thought leadership is the strategic response, social media is the tactical response,

providing the fastest growing advisers with a way to effi ciently execute on thought

leadership strategies. And while social media is acknowledged as an important way

to communicate with younger clients, it is further seen as a way to deepen existing

relationships and build credibility. In this section, we examine both the use of social

media generally and the key differences for high growth advisers.

Perhaps not surprisingly, LinkedIn is the dominant network being used by fi nancial advisers. While lower in

terms of current usage, advisers expect to increase use of both Facebook and Twitter.

Q: Which, if any, of the following do you use in your personal or professional life today?

76%

9%LINKEDIN

43%

11%FACEBOOK

23%

15%TWITTER

USE NOWNOT NOW BUT WILL USE IN THE FUTURE

SOCIAL AND PROFESSIONAL NETWORK USAGE: ADVISERS

24 | © 2015 LinkedIn® and Financial Planning Association (FPA)

When asked why they don’t use specifi c networks, many respondents indicated they were restricted by

their company; however, this result was infl uenced by channel. Registered Investment Advisers (RIAs) are

less likely to be restricted; full-service brokerage fi rms and broker-dealers are much more likely to restrict

Facebook and Twitter than LinkedIn.

Q: Please indicate the reason or reasons for not using <network> for business purposes. Shows percentage responding ‘My company restricts use of this network for business.’

49%35%

RESTRICTED NETWORK USE

LINKEDIN FACEBOOK

45%

RESTRICTIONS ON SOCIAL AND PROFESSIONAL NETWORKS

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 25

Often we refer to ‘social media’ usage as if it is a single strategy with cohesive objectives. The reality is

that advisers use different networks to meet different objectives. They range from more passive goals,

such as listening and learning from others, to more active, such as fi nding new relationships. LinkedIn

is seen primarily as a way to fi nd new relationships, Facebook to maintain and deepen relationships

and Twitter to listen and learn from others. They are seen as being equally effective in building brand/

credibility; however, based on the objectives identifi ed for each network, advisers consider LinkedIn and

Facebook more effective than Twitter.

Q: Which, if any, of the following do you use in your personal or professional life today? Shows percentage responding ‘yes’

LINKEDIN FACEBOOK TWITTER

FIND NEW RELATIONSHIPS 48% 14% 9%

MAINTAIN/DEEPEN EXISTING RELATIONSHIPS 12% 48% 8%

LISTEN AND LEARNFROM OTHERS 9% 7% 45%

BUILD BRAND/CREDIBILITY 28% 25% 25%

REASONS FOR USING SOCIAL AND PROFESSIONAL NETWORKS

26 | © 2015 LinkedIn® and Financial Planning Association (FPA)

Looking forward, there are clear changes in how social media will be used more actively not just more

frequently. Advisers acknowledge the increased role of social media in building credibility, building deeper

relationships and fi nding new relationships, whereas they don’t see as big a change on “listening and

learning,” which is a more passive activity.

Executing a Social Media Plan

Exactly how professional and social networks are being used varies; however, we can learn from high

growth advisers.

1. High growth advisers are more likely to use multiple professional/social networks.

Q: Which, if any, of the following do you use in your personal or professional life today? Shows percentage responding ‘yes’

LOW GROWTH

MODERATE GROWTH

HIGH GROWTH

NUMBER OF SOCIAL MEDIA NETWORKS CURRENTLY

USE 3+31% 36% 42%

Q: Thinking about your plans to use social networks/social media going forward, how will the importance of each objective change relative to today? Shows percentage rating ‘more important’.

35%

57%

52%

BUILD BRAND/CREDIBILITY

FIND NEW RELATIONSHIPS

LISTEN AND LEARN FROM OTHERS

57%MAINTAIN/DEEPENEXISTING RELATIONSHIPS

CHANGES IN OBJECTIVES FOR SOCIAL AND PROFESSIONAL NETWORKS

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 27

2. High growth advisers actively engaged with clients and prospects

In general, advisers use social media to research people, connect with clients and follow clients. They

typically rely on their fi rms to provide that information or curate publicly available information. High growth

fi rms are more likely to:

• Connect/engage with clients

• Follow clients and prospects

• Consume content posted by peers or others

REASONS TO USE NETWORKS BASED ON GROWTH PROFILE

LOWGROWTH ADVISERS

MODERATE GROWTH ADVISERS

HIGH GROWTH ADVISERS

SHARE BUSINESS INFORMATION/UPDATES 29% 32% 31%

SHARE ORIGINAL OR CURATED CONTENT 22% 27% 31%

FOLLOW CLIENTS 35% 39% 45%

FOLLOW PROSPECTS 31% 29% 40%

CONNECT/ENGAGE WITH CLIENTS 38% 39% 47%

CONSUME CONTENT FROM ASSET MANAGERS AND OTHER SERVICE

PROVIDERS (e.g. Whitepapers)24% 21% 28%

CONSUME CONTENT POSTED BY PEERS AND OTHER MEMBERS 30% 31% 40%

PARTICIPATE IN DISCUSSION GROUPS 15% 14% 11%

LOOK FOR NEW PROSPECTS 38% 36% 46%

ADVERTISE JOBS 5% 9% 14%

RESEARCH PEOPLE OR COMPANIES 52% 50% 57%

CONDUCT DUE DILIGENCE ON PRODUCT PROVIDERS (e.g. Asset Management,

Insurance Companies)8% 8% 10%

STAY ON TOP OF BREAKING NEWS AND/OR MARKET PERSPECTIVES 33% 31% 43%

IDENTIFY POTENTIAL BUSINESS PARTNERS (e.g. Centers of Infl uence) 36% 31% 40%

Q: Which of the following specifi c activities do you do on social networks for business purposes?

28 | © 2015 LinkedIn® and Financial Planning Association (FPA)

Advisers who say they share original or curated content often use content provided by their fi rm or that is

publicly available; however, a relatively signifi cant proportion is created by the team.

Peer to Peer

In addition to sharing content, advisers shared examples of how they engage with clients and prospects to

increase followers or connections on professional or social networks.

Q: What is the source of the content you share?

46%

45%

58%

48%

IT IS PROVIDED BY MY COMPANY

I REPURPOSE PUBLICLY AVAILABLE CONTENT

I WRITE IT MYSELF

24%IT IS CREATED BY SOMEONE ON MY TEAM

3%OTHER

SOURCE OF CONTENT SHARED

ADVISERS SPEAK OUT: BEST PRACTICES FOR USING PROFESSIONAL NETWORKS

Active engagement. Take social media off autopilot. Be authentic.

Actively look for new contacts using existing network.

Be a resource.

Blogs written by team members.

Change the content as much as possible.

Commit time to building a larger network.

Content on Twitter, leading back to our website/LinkedIn/Facebook and increasing the use of mobile apps which have additional information on the Twitter content.

Daily interaction.

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 29

ADVISERS SPEAK OUT: BEST PRACTICES FOR USING PROFESSIONAL NETWORKS – CONTINUED

Q: What have you found to be the most effective ways to increase followers/connections?

Direct invitations to follow me.

Engage in discussions.

Great headlines.

I join professional networks on the social media sites to add to my credibility and increase search exposure.

I request connections almost immediately after meeting business or personal connections.

Joining groups, writing comments.

Looking at others’ profi les a day or two before inviting them to connect.

Name searches both by industry and my niche companies.

Offer valuable content that helps the follower/connection increase their profi tability.

Post consistently and follow up in a timely manner.

Posting really good/interesting content with photos. People love photos!

Posting social and family activities.

Proprietary content has increased the number of followers signifi cantly.

Providing reliable, non-biased fi nancial education and counseling.

Reaching out to centers of infl uence.

Share others posts and comment on those posts. Do not always send industry content, but personal content to show you are a person.

Strategic alliances who share a common goal to help each other grow their business.

Writing about a subject and asking for feedback/interaction.

30 | © 2015 LinkedIn® and Financial Planning Association (FPA)

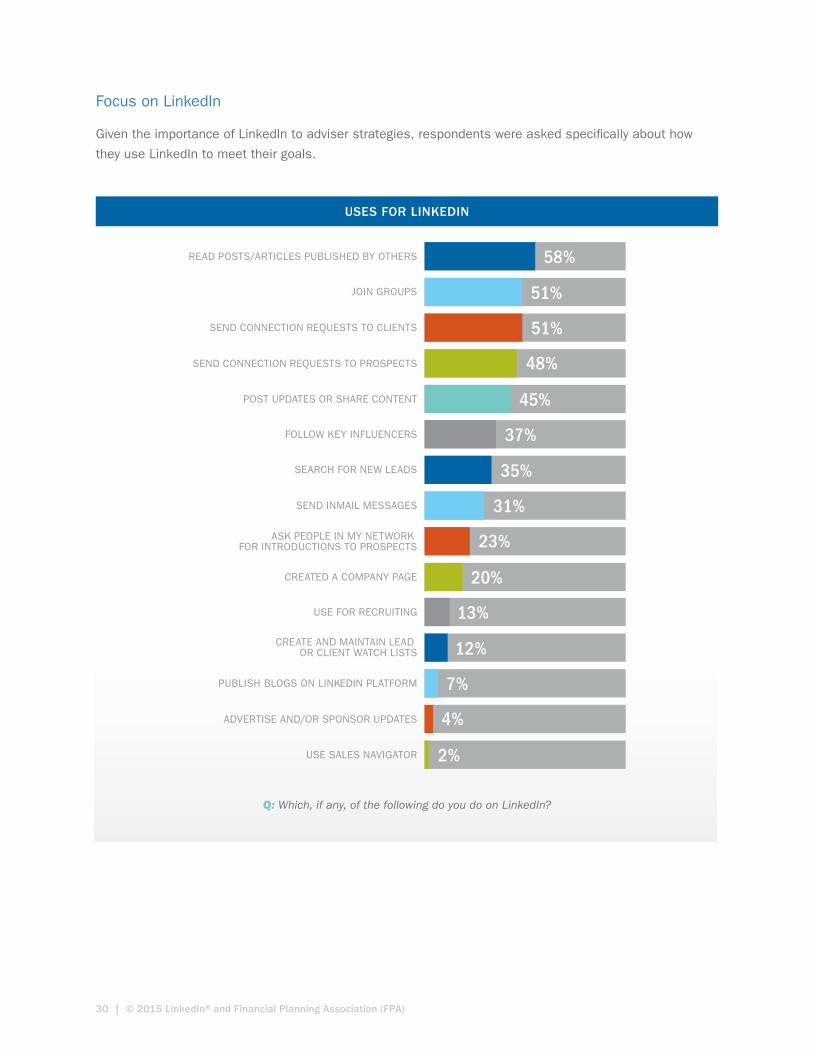

Focus on LinkedIn

Given the importance of LinkedIn to adviser strategies, respondents were asked specifi cally about how

they use LinkedIn to meet their goals.

Q: Which, if any, of the following do you do on LinkedIn?

51%

58%

51%

READ POSTS/ARTICLES PUBLISHED BY OTHERS

JOIN GROUPS

SEND CONNECTION REQUESTS TO CLIENTS

48%SEND CONNECTION REQUESTS TO PROSPECTS

45%POST UPDATES OR SHARE CONTENT

31%

37%

35%

FOLLOW KEY INFLUENCERS

SEARCH FOR NEW LEADS

SEND INMAIL MESSAGES

23%ASK PEOPLE IN MY NETWORK FOR INTRODUCTIONS TO PROSPECTS

20%CREATED A COMPANY PAGE

7%

13%

12%

USE FOR RECRUITING

CREATE AND MAINTAIN LEAD OR CLIENT WATCH LISTS

PUBLISH BLOGS ON LINKEDIN PLATFORM

4%ADVERTISE AND/OR SPONSOR UPDATES

2%USE SALES NAVIGATOR

USES FOR LINKEDIN

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 31

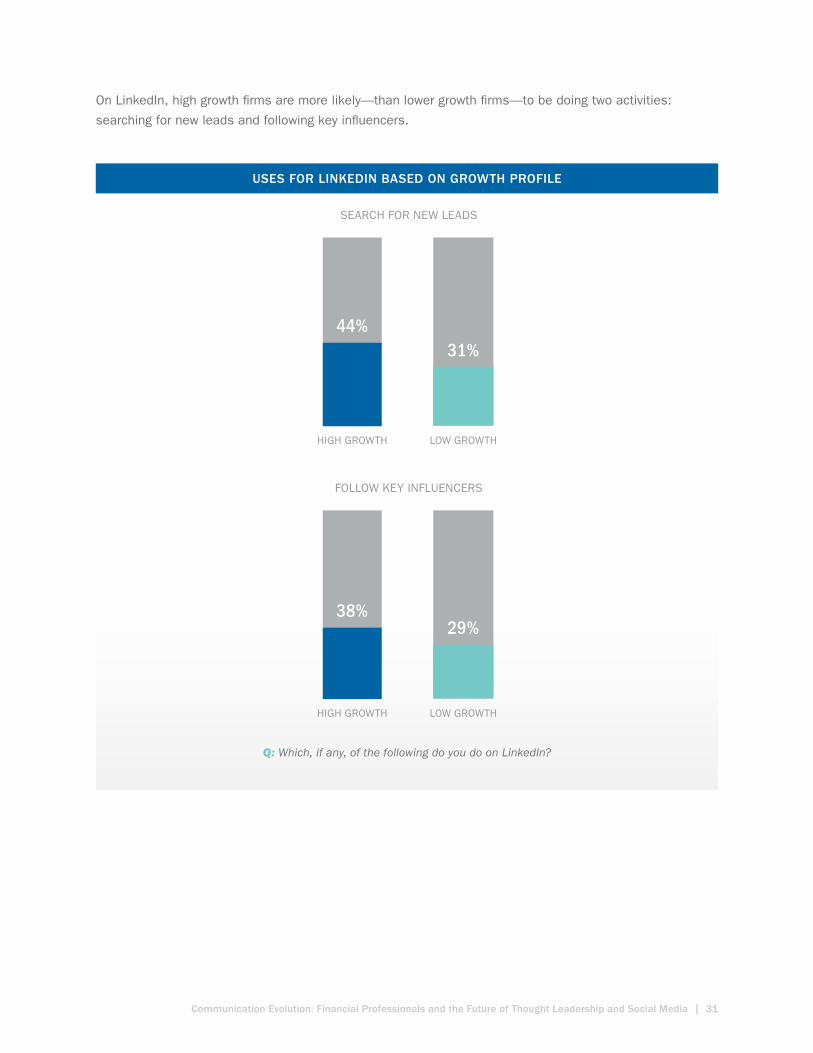

On LinkedIn, high growth fi rms are more likely—than lower growth fi rms—to be doing two activities:

searching for new leads and following key infl uencers.

Q: Which, if any, of the following do you do on LinkedIn?

31%44%

SEARCH FOR NEW LEADS

HIGH GROWTH LOW GROWTH

29%38%

FOLLOW KEY INFLUENCERS

HIGH GROWTH LOW GROWTH

USES FOR LINKEDIN BASED ON GROWTH PROFILE

32 | © 2015 LinkedIn® and Financial Planning Association (FPA)

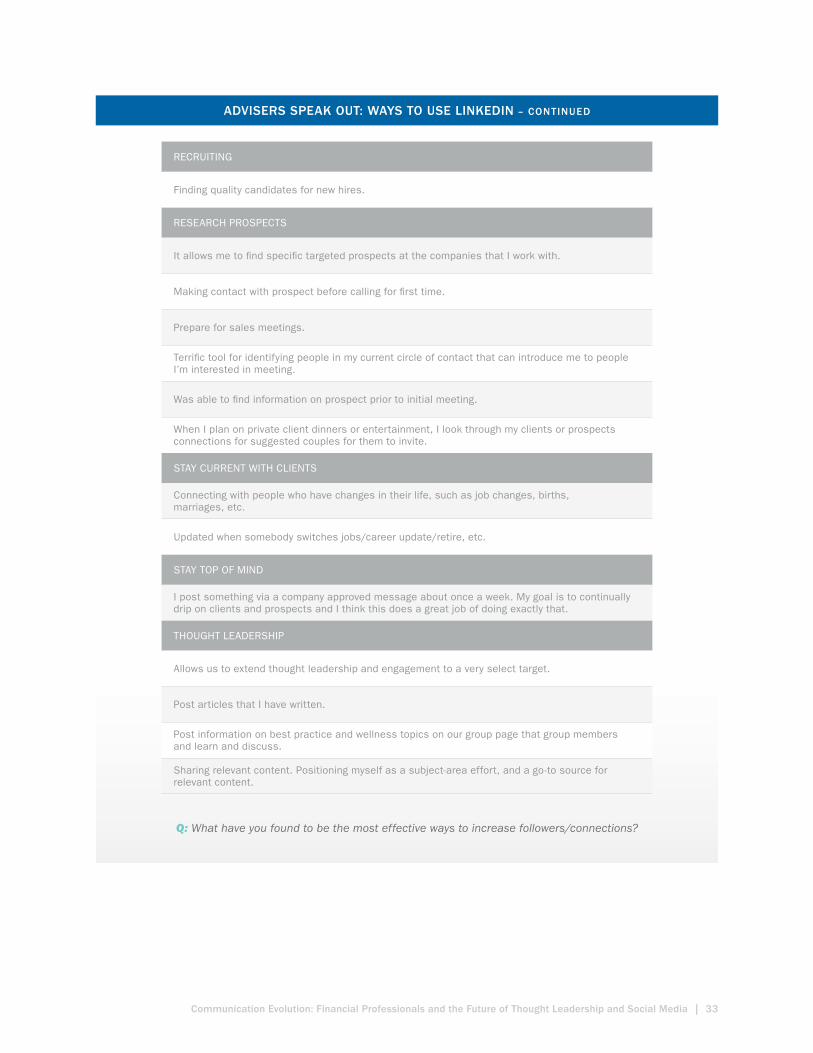

Going deeper, respondents provided specifi c examples of how they are using LinkedIn to reach specifi c

goals and objectives.

ADVISERS SPEAK OUT: WAYS TO USE LINKEDIN

CONNECT TO PROSPECTS

Connecting to new clients through referrals generated from current professional network members.

Former clients have found me using LinkedIn and have become new clients.

Getting a message out to a large audience of people I am not connected with through targeted groups.

Great tool to see someone else’s network and a sk for introductions.

I made appointments after connecting on LinkedIn.

Maintain contact with individuals I meet in the community.

Make contact with individuals I do not know. I use it to identify key-decision makers within an organization.

ENHANCE KNOWLEDGE

Participation in peer discussion allows me to remain confi dent in my knowledge and abilities.

Staying aware of changes in the industry.

PROFESSIONAL REFERRALS

I have used LinkedIn to set up meeting with potential referral sources.

Identifi ed centers of infl uence who can help me break into the workplace seminar circuit, and engaged them to assist me in providing introductions to people on their LinkedIn contacts list.

Strengthened relationships I have with power partners and helps them make referrals.

Promote the business.

Creates a solid place for people to understand what my business can provide and my credentials.

Described myself in ways that have allowed organizations and individuals to solicit me as a speaker.

Helping me build my brand and increase awareness of what I do with casual contacts.

Set up networking events.

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 33

ADVISERS SPEAK OUT: WAYS TO USE LINKEDIN – CONTINUED

Q: What have you found to be the most effective ways to increase followers/connections?

RECRUITING

Finding quality candidates for new hires.

RESEARCH PROSPECTS

It allows me to fi nd specifi c targeted prospects at the companies that I work with.

Making contact with prospect before calling for fi rst time.

Prepare for sales meetings.

Terrifi c tool for identifying people in my current circle of contact that can introduce me to people I’m interested in meeting.

Was able to fi nd information on prospect prior to initial meeting.

When I plan on private client dinners or entertainment, I look through my clients or prospects connections for suggested couples for them to invite.

STAY CURRENT WITH CLIENTS

Connecting with people who have changes in their life, such as job changes, births, marriages, etc.

Updated when somebody switches jobs/career update/retire, etc.

STAY TOP OF MIND

I post something via a company approved message about once a week. My goal is to continually drip on clients and prospects and I think this does a great job of doing exactly that.

THOUGHT LEADERSHIP

Allows us to extend thought leadership and engagement to a very select target.

Post articles that I have written.

Post information on best practice and wellness topics on our group page that group members and learn and discuss.

Sharing relevant content. Positioning myself as a subject-area effort, and a go-to source for relevant content.

34 | © 2015 LinkedIn® and Financial Planning Association (FPA)

The Impact of Social Media

The issue of the return on investment on social media has been debated across the

industry; many have questioned whether the use of social media has a measurable

impact on growth or client engagement. What is clear from the data is that while

advisers may not believe that social media leads directly to new clients, they do see it

as a critical part of the business development process.

Just over half of advisers who use social media said they had added new clients directly as a result of the

use, averaging five new clients and $3.5m in new assets in the last year. Despite that, a small minority

of advisers see the use of social media as leading directly to new business; rather, they see it supporting

new business development. This is true across all growth segments.

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 35

In particular, high growth advisers see social media as a support for client referrals.

Q: Which of the following best describes your experience in using social media, specifi cally as it relates to business development?

Q: To what extent do you think your business development activity was positively impacted by social networking? Show percentage rating some or signifi cant impact.

Shows percentage rating ‘some’ or ‘signifi cant’ impact.

LOWGROWTH ADVISERS

MODERATE GROWTH ADVISERS

HIGH GROWTH ADVISERS

IT LEADS DIRECTLY TO NEW CLIENTS 10% 9% 9%

IT ACTIVELY SUPPORTS OVERALL NEW BUSINESS DEVELOPMENT ACTIVITIES, BUT DOES NOT

NECESSARILY LEAD TO NEW CLIENTS59% 59% 68%

NEITHER, IT’S NOT ABOUT NEW BUSINESS 30% 32% 24%

LOWGROWTH ADVISERS

MODERATE GROWTH ADVISERS

HIGH GROWTH ADVISERS

CLIENT REFERRALS 29% 33% 42%

CENTER OF INFLUENCE REFERRALS 22% 31% 34%

OTHER PROSPECTING ACTIVITY (NOT REFERRALS) 29% 32% 40%

LEADS THAT CONTACT YOU DIRECTLY (NOT RELATED TO THE ABOVE ACTIVITY) 22% 26% 30%

IMPACT OF SOCIAL MEDIA

SOCIAL MEDIA AND REFERRAL ACTIVITY

36 | © 2015 LinkedIn® and Financial Planning Association (FPA)

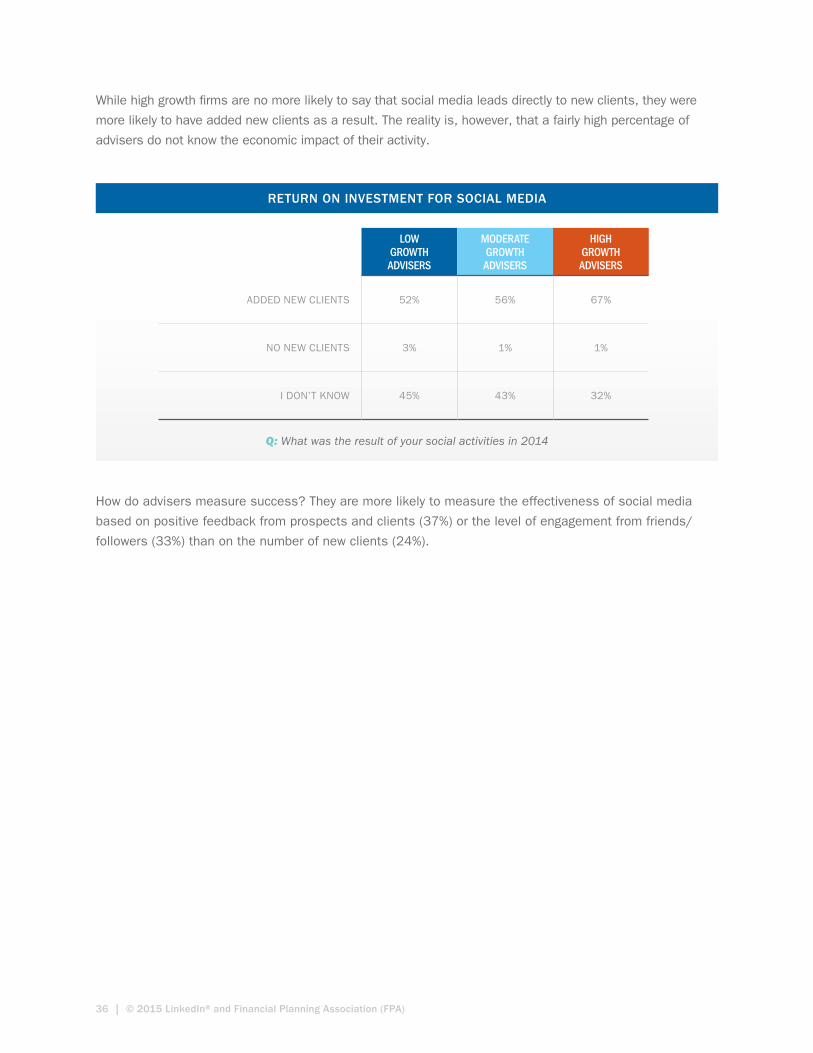

While high growth fi rms are no more likely to say that social media leads directly to new clients, they were

more likely to have added new clients as a result. The reality is, however, that a fairly high percentage of

advisers do not know the economic impact of their activity.

How do advisers measure success? They are more likely to measure the effectiveness of social media

based on positive feedback from prospects and clients (37%) or the level of engagement from friends/

followers (33%) than on the number of new clients (24%).

Q: What was the result of your social activities in 2014

LOWGROWTH ADVISERS

MODERATE GROWTH ADVISERS

HIGH GROWTH ADVISERS

ADDED NEW CLIENTS 52% 56% 67%

NO NEW CLIENTS 3% 1% 1%

I DON’T KNOW 45% 43% 32%

RETURN ON INVESTMENT FOR SOCIAL MEDIA

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 37

Conclusion

Too often, research that incorporates data on social media starts and ends with the

tools being used. While important, that data is not the end of the story. To understand

if and how advisers need to think about engagement, we need to start with the client

and create strategies that respond to his or her core needs.

We know from examining client behavior that clients demand education and that prospective clients

are going online to research advisers. The highest growth advisers have responded to those distinct

but related trends and are increasingly focused on thought leadership strategies—executed via social

media. In so doing, they respond both to the demand for education and the need to have a robust

online presence.

For advisers who are looking to stay ahead of the trends, the focus on how high growth advisers are

executing on their thought leadership strategies becomes most important. Across the board, we see

that advisers are using different social networks to meet different objectives and those who, have seen

the highest growth are more actively engaging with both clients and prospects.

Change does not happen overnight. The analysis of both client behavior and adviser activities suggest

small but important changes in current behavior and clear changes in the perceptions of advisers going

forward. Today we have a choice; to watch how the change plays out or to take action and be part of the

change. The data suggests that the leaders are the high growth firms that are reaping the rewards

of driving the change.

38 | © 2015 LinkedIn® and Financial Planning Association (FPA)

Your Action Plan

The study highlights a range of activities as it relates to thought leadership and the use

of social media. Consider the following to lay the foundation for a more active strategy

in the future or to enhance what you are doing today.

1. Gather input from clients to help you tailor your education and thought leadership activities on the issues that will have the greatest impact. Specifically assess:

a. Interest in gaining access to educational activities or information

b. Specific topics of interest

c. Key concerns

d. Preferences regarding how information is consumed (e.g. live events versus articles)

e. Current social media activity (e.g. what networks are they using and for what purpose)

You can gather input formally (e.g. a survey) or informally (ask during review meetings)

and assess the results based on the age of the respondent to identify important trends.

2. Map out a simple educational plan based on the information gathered in Step 1. Choose one or two ways to tackle client concerns, focusing on how they consume content today. You might choose from:

a. Live events (in person or webinars)

b. On-demand events (webinars)

c. Curating content (articles, blog posts)

d. Writing original content (articles, blog posts)

3. Alert clients to content that you share socially so they are aware of what you are creating and can easily share with friends and family.

4. Audit your online presence to ensure:

a. You have a presence on social and professional networks used by your clients

b. Your messaging is consistent across all networks

c. You messaging is focused on the issues that matter most to your clients

d. Content is easily shareable

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 39

5. Actively engage with clients and prospects on professional and social networks

a. Follow/connect with key clients and prospects

b. Engage with key clients and prospects by commenting or sharing their content

c. Join relevant groups

6. Make a start. If you are not active on professional and social networks, take a few small steps forward. You may choose to start by “listening and learning” and then move to more engaging activities.

40 | © 2015 LinkedIn® and Financial Planning Association (FPA)

Appendix 1

Participant Profi le

Q: Which of the following best describes your role?

Q: Which of the following describes your age?

CEO/PRESIDENT 17%

SENIOR FINANCIAL ADVISER 57%

JUNIOR/ASSOCIATE FINANCIAL ADVISER 55%

NON-ADVISER MANAGEMENT 4%

SUPPORT STAFF (INCLUDING TECHNICAL) 2%

OTHER 4%

UNDER 30 8%

30–39 16%

40–49 24%

50–59 29%

60–64 12%

65 OR OVER 9%

I PREFER NOT TO ANSWER 1%

ADVISER ROLE

ADVISER AGE

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 41

Q: Which is your gender?

Q: How long have you worked in the fi nancial services industry?

MALE 76%

FEMALE 22%

I PREFER NOT TO ANSWER 2%

LESS THAN 2 YEARS 6%

2–4 YEARS 8%

5–9 YEARS 14%

10–14 YEARS 14%

15–19 YEARS 16%

20 YEARS OR MORE 40%

I PREFER NOT TO ANSWER 1%

ADVISER GENDER

ADVISER TENURE

Q: What was your gross revenue in 2014?

UNDER $250K 43%

$250K–$499.9K 22%

$500K–$999.9K 15%

$1M–$2.49M 12%

$2.5M–$4.9M 4%

$5M+ 4%

ADVISER REVENUE

42 | © 2015 LinkedIn® and Financial Planning Association (FPA)

Q: What were your individual assets under management on December 31, 2014?

Q: Which of the following best describes your business model/fi rm?

UNDER $50M 48%

$50M–$99M 19%

$100M–$249.9M 17%

$250M–$499.9M 7%

$500M–$999.9M 4%

$1B+ 5%

NATIONAL, REGIONAL OR INDEPENDENT 26%

INDEPENDENT RIA 20%NATIONAL OR REGIONAL

WIREHOUSE 15%INSURANCE BROKERAGE/

AGENCY 13%

HYBRID RIA/BROKER-DEALER 12%

BANK/CREDIT UNION 7%

OTHER 7%

ADVISER ASSETS UNDER MANAGEMENT

BUSINESS MODEL/FIRM

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 43

Appendix 2

Profi le of Investor RespondentsProfi le of Investor RespondentsProfi le of Investor Respondents

Q: Are you...?

Q: Are you...?

Q: Please tell us which best describes your current total investable assets, including all mutual funds, stocks, bonds, 401(k), IRA and other retirement accounts, but excluding real estate?

Q: Which of the following best describes your annual household income before taxes?

CLIENT GENDER

CLIENT AGE

CLIENT WEALTH AND INCOME

MALE FEMALE

56% 44%

18–24 25–34 35–44 45–54 55–64 65+

1% 7% 9% 11% 33% 38%

$50,000 – $99,999

$100,000 – $499,999

$500,000 – $999,999

$1,000,000 – $4,999,999

$5,000,000 OR MORE

10% 27% 29% 24% 9%

LESS THAN $50,000

$50,000 – $99,999

$100,000 – $199,999

$200,000AND OVER

PREFER NOT TO SAY

11% 35% 39% 14% 2%

44 | © 2015 LinkedIn® and Financial Planning Association (FPA)

Q: Where do you live?

CLIENT REGION

EAST MIDWEST SOUTH WEST

27% 25% 26% 22%

GRADE SCHOOL OR SOME

HIGH SCHOOL

COMPLETED HIGH

SCHOOL

SOME TECHNICAL/ COMMUNITY

COLLEGE

COMPLETED TECHNICAL/ COMMUNITY

COLLEGE

SOME COLLEGE DEGREE/PROGRAM

COMPLETED COLLEGE DEGREE/PROGRAM

ADVANCED GRADUATE DEGREE/

POST GRADUATE DEGREE

0% 6% 3% 5% 10% 40% 36%

GRADE SCHOOL OR SOME

HIGH SCHOOL

COMPLETED HIGH

SCHOOL

SOME TECHNICAL/ COMMUNITY

COLLEGE

COMPLETED TECHNICAL/ COMMUNITY

COLLEGE

SOME COLLEGE DEGREE/PROGRAM

COMPLETED COLLEGE DEGREE/PROGRAM

ADVANCED GRADUATE DEGREE/

POST GRADUATE DEGREE

0%0% 6%6% 3%3% 5%5% 10%10% 40% 36%36%

Q: What is the highest level of formal education that you have completed?

CLIENT EDUCATION

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 45

Appendix 3

Profi le of Growth Segment

The profi le of those fi rms is below:

Q: What were your individual assets under management on December 31, 2014?

Q: What was your gross revenue in 2014?

ADVISER ASSETS UNDER MANAGEMENT

ADVISER REVENUE

LOWGROWTH ADVISERS

MODERATE GROWTH ADVISERS

HIGH GROWTH ADVISERS

UNDER $50M 54% 40% 45%

$50M–$99M 24% 22% 14%

$100M–$249.9M 21% 24% 9%

$250M–$499.9M 0% 6% 14%

$500M–$999.9M 0% 5% 7%

$1B+ 0% 3% 11%

LOWGROWTH ADVISERS

MODERATE GROWTH ADVISERS

HIGH GROWTH ADVISERS

UNDER $250K 46% 32% 40%

$250K–$499.9K 27% 25% 16%

$500K–$999.9K 18% 18% 12%

$1M–$2.49M 7% 16% 12%

$2.5M–$4.9M 1% 5% 8%

$5M+ 0% 3% 9%

NOT APPLICABLE/I DON’T KNOW 2% 2% 3%

46 | © 2015 LinkedIn® and Financial Planning Association (FPA)

Q: In 2014, what was the net percentage growth rate of each of the following?

Q: In 2014, what was the net percentage growth rate of each of the following - Assets?

ADVISER REVENUE GROWTH RATE

ADVISER ASSET GROWTH RATE

LOW GROWTH

MODERATE GROWTH

HIGH GROWTH

NEGATIVE GROWTH 8% 2% 0%

NO GROWTH 13% 2% 0%

1–4% 22% 8% 1%

5–9% 33% 20% 6%

10–14% 14% 35% 17%

15–19% 6% 17% 16%

20–29% 3% 10% 23%

30%+ 2% 4% 34%

LOW GROWTH

MODERATE GROWTH

HIGH GROWTH

NEGATIVE GROWTH 5% 0% 0%

NO GROWTH 11% 2% 0%

1–4% 30% 3% 0%

5–9% 55% 9% 0%

10–14% 0% 51% 11%

15–19% 0% 34% 11%

20–29% 0% 0% 37%

30%+ 0% 0% 41%

Communication Evolution: Financial Professionals and the Future of Thought Leadership and Social Media | 47

Q: How many clients did you add in 2014?

ADVISER NUMBER OF CLIENTS

LOW GROWTH

MODERATE GROWTH

HIGH GROWTH

NONE 4% 1% 0%

1–4 28% 13% 7%

5–9 30% 26% 18%

10–14 14% 24% 21%

15–19 7% 13% 11%

20–29 8% 9% 16%

30+ 8% 14% 27%